Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - IHS Inc. | Financial_Report.xls |

| EX-21 - SUBSIDIARIES OF REGISTRANT - IHS Inc. | ex21q414.htm |

| EX-32 - CEO/CFO CERTIFICATION - IHS Inc. | ex32q414.htm |

| EX-23 - CONSENT OF ERNST & YOUNG LLP - IHS Inc. | ex23q414.htm |

| EX-10.1 - LONG-TERM INCENTIVE PLAN - IHS Inc. | ex101q414.htm |

| EX-31.2 - CFO CERTIFICATION - IHS Inc. | ex312q414.htm |

| EX-31.1 - CEO CERTIFICATION - IHS Inc. | ex311q414.htm |

| EX-10.35 - CREDIT AGREEMENT - IHS Inc. | ex1035q414.htm |

| EX-10.38 - AMENDED AND RESTATED CREDIT AGREEMENT - IHS Inc. | ex1038q414.htm |

| EX-10.15 - DEFERRED COMPENSATION PLAN - IHS Inc. | ex1015q414.htm |

| EX-10.16 - DEFERRED COMPENSATION PLAN ADOPTION AGREEMENT - IHS Inc. | ex1016q414.htm |

| EX-10.14 - RECOUPMENT OF INCENTIVE COMPENSATION POLICY - IHS Inc. | ex1014q414.htm |

| EX-24 - POWER OF ATTORNEY - IHS Inc. | ex24powerofattorney2014.htm |

| EX-10.13 - HEDGING AND PLEDGING POLICY - IHS Inc. | ex1013q414.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________________________________

FORM 10-K

___________________________________________________

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended November 30, 2014

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-32511

___________________________________________________

IHS INC.

(Exact name of registrant as specified in its charter)

___________________________________________________

Delaware | 13-3769440 | |

(State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) | |

15 Inverness Way East

Englewood, CO 80112

(Address of Principal Executive Offices)

(303) 790-0600

(Registrant’s telephone number, including area code)

___________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Class A Common Stock, $0.01 par value per share | New York Stock Exchange | |

Series A junior participating preferred stock purchase rights (attached to the Class A Common Stock) | ||

Securities registered pursuant to Section 12(g) of the Act:

None.

___________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes o No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter)

during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | o | ||

Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller Reporting Company | o | ||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates, based upon the closing price for the Class A Common Stock as reported on the New York Stock Exchange composite tape on the last business day of the registrant's most recently completed second fiscal quarter, was approximately $6.3 billion. All executive officers, directors, and holders of five percent or more of the outstanding Class A Common Stock of the registrant have been deemed, solely for purposes of the foregoing calculation, to be "affiliates" of the registrant.

As of December 31, 2014, there were 68,381,329 shares of our Class A Common Stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of the Form 10-K, to the extent not set forth herein, is incorporated herein by reference from the registrant's definitive proxy statement on Schedule 14A for the Annual Meeting of Stockholders to be held on April 8, 2014, to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the close of the registrant's fiscal year.

TABLE OF CONTENTS

Page | |||

Item 1. | |||

Item 1A. | |||

Item 1B. | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 5. | |||

Item 6. | |||

Item 7. | |||

Item 7A. | |||

Item 8. | |||

Item 9. | |||

Item 9A. | |||

Item 9B. | |||

Item 10. | |||

Item 11. | |||

Item 12. | |||

Item 13. | |||

Item 14. | |||

Item 15. | |||

2

Cautionary Note Regarding Forward-Looking Statements

This annual report on Form 10-K contains “forward-looking statements” within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as: “anticipate,” “intend,” “plan,” “goal,” “seek,” “aim,” “strive,” “believe,” “project,” “predict,” “estimate,” “expect,” “continue,” “strategy,” “future,” “likely,” “may,” “might,” “should,” “will,” the negative of these terms, and similar references to future periods. Examples of forward-looking statements include, among others, statements we make regarding: guidance and predictions relating to expected operating results, such as revenue growth and earnings; strategic actions, including acquisitions and dispositions, anticipated benefits from strategic actions, and our success in integrating acquired businesses; anticipated levels of capital expenditures in future periods; our belief that we have sufficient liquidity to fund our ongoing business operations; expectations of the effect on our financial condition of claims, litigation, environmental costs, contingent liabilities and governmental and regulatory investigations and proceedings; and our strategy for customer retention, growth, product development, market position, financial results, and reserves.

Forward-looking statements are neither historical facts nor assurances of future performance. Instead, they are based only on our current beliefs, expectations, and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy, and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others, the following: economic and financial conditions, including volatility in interest and exchange rates; our ability to manage system failures, capacity constraints, and cyber risks; our ability to successfully manage risks associated with changes in demand for our products and services as well as changes in our targeted industries; our ability to develop new platforms to deliver our products and services, pricing, and other competitive pressures, and changes in laws and regulations governing our business; the extent to which we are successful in gaining new long-term relationships with customers or retaining existing ones and the level of service failures that could lead customers to use competitors' services; our ability to successfully identify and integrate acquisitions into our existing businesses and manage risks associated therewith; our ability to satisfy our debt obligations and our other ongoing business obligations; and the other factors described under the caption “Risk Factors” in this annual report on Form 10-K, along with our other filings with the U.S. Securities and Exchange Commission (SEC).

Any forward-looking statement made by us in this annual report on Form 10-K is based only on information currently available to us and speaks only as of the date on which it is made. We undertake no obligation to publicly update any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future developments or otherwise.

Website and Social Media Disclosure

We use our website (www.ihs.com) and corporate Twitter account (@IHS) as channels of distribution of company information. The information we post through these channels may be deemed material; therefore, investors should monitor these channels in addition to our press releases, SEC filings, and public conference calls and webcasts. None of the information provided on our website, in our press releases, public conference calls and webcasts, or through social media channels is incorporated into, or deemed to be a part of, this annual report on Form 10-K.

Fiscal Year End

Our fiscal year ends on November 30 of each year. Unless otherwise indicated, references in this Annual Report to an individual year means the fiscal year ended November 30. For example, “2014” refers to the fiscal year ended November 30, 2014.

3

PART I

Item 1. Business

Our Vision

Our vision is to be the Source for Critical Information and Insight that powers growth and value for our customers. We intend to be the source that customers trust, rely upon and come to first when they need to better understand the present and anticipate the future.

Our Business

We are a leading source of information, insight, and analytics in critical areas that shape today’s business landscape. Businesses and governments around the globe rely on our comprehensive content, expert independent analysis, and flexible delivery methods. Our aim is to embed our solutions within the entire spectrum of our customers’ organizations, enabling executive level capital deployment strategies and following decision-making activities throughout their organizations to front-line employees tasked with managing complex core daily operations. We serve customers across global interconnected capital-intensive industries, including energy and natural resources, chemicals, technology, automotive, aerospace and defense, and maritime and trade.

As further described below, our core competency is sourcing data and transforming it into critical information and insight that businesses, governments, and others use to make high-impact decisions with confidence. We are a sought-after resource for those who require and demand the most accurate and expertly analyzed information available. We are dedicated to providing the information and expert analysis our customers need to make critical decisions that drive growth and value for their operations.

By integrating and connecting our information, analytics, and research and analysis with proprietary and widely used decision-support technology on scalable platforms, we produce critical information and analytical solutions designed to meet our customers’ needs. Our product development teams have also created proprietary Web services and application interfaces that enhance access to our information. These services allow our customers to integrate our information with other data, business processes, and applications (such as computer-aided design, enterprise resource planning (ERP), supply chain management, and product data/lifecycle management).

We have been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, we are committed to sustainable, profitable growth and employ approximately 8,800 people in 32 countries around the world.

Our Objectives

To achieve our vision of being the Source for Critical Information and Insight, we have established five inter-dependent objectives upon which we focus our efforts, as described below. We externally benchmark our progress annually against these five objectives. To measure customer satisfaction (which we refer to as Customer Delight) and colleague success, we use third-party surveys and develop goals based on those metrics. For 2015, our corporate objectives are:

• | Improve Customer Delight; |

•Foster a culture that enables colleague success;

•Deliver profitable top- and bottom-line growth;

•Provide an opportunity for stockholder success relative to our peer group; and

•Improve corporate sustainability and responsibility.

Our Strategy

Our strategy is comprised of the following priorities:

Commercial expansion. We intend to continue our business expansion through new product development and customer development and market penetration, as described in the following actions:

4

• | Continue developing new products and analytics. We believe we have a distinctive ability to develop decision-support tools and related services based on our critical information in the industries we serve. We plan to continue to leverage our information and insight expertise to develop new and integrated product platforms and offerings for our customers. |

• | Expand customer relationships. We believe there is significant opportunity to grow within our Target 1000 customer accounts (which consists of high-growth, high-opportunity accounts), and we intend to expand those relationships by cross-selling and up-selling additional information, tools, and analytics that will support customers in their operating, capital, and strategic decision processes. |

• | Leverage our global footprint. Our global sales and marketing organizations have broad geographic reach, which makes it easier for our customers to do business with us. We plan to continue to expand our global reach by investing in key geographical markets to drive continued revenue growth. |

Operational excellence. We have made significant infrastructure investments to scale our internal applications, including implementation of a common ERP and sales management system. Our operational excellence initiative is focused on continuing to refine, enhance, and leverage our systems and processes to drive further operational simplicity and efficiency, and accommodate future revenue growth without having to incur proportional cost increases to support that growth.

Strategic acquisitions. Acquisitions are a key part of our growth strategy. We focus on acquisitions that have long-term growth potential, target high-growth markets, and fill a strategic need in our business portfolio as we seek to provide comprehensive solutions to our customers. We have deployed approximately $4.0 billion in capital on more than 60 acquisitions since 2005, and we plan to continue to selectively acquire strategic assets in our target industries in order to further enhance our product offerings and market position.

Our Global Sales and Operating Model

To best serve our customers and be as close to them as possible, we are organized by geographies into three business segments:

•Americas, which includes the United States, Canada, and Latin America;

•EMEA, which includes Europe, the Middle East, and Africa; and

•APAC, or Asia Pacific.

Our integrated global organization is designed to make it easier for our customers to do business with us by providing a cohesive, consistent, and effective sales-and-marketing approach in each local region. By structuring our business around customers and the regions in which they reside, we are better able to serve the specific needs of our customers both in their local markets and globally. We believe a regional structure provides a solid foundation for profitable growth as it provides an efficient platform to bring new products and services to customers and supports growth in existing accounts and with new customers and markets.

Our Core Competency: Transforming Data into Critical Information and Insight

Our customers benefit from a concentration of intellectual wealth and thought leadership throughout a variety of industries. We believe that our global team of information and industry experts, research analysts, and economists provide our customers with leading strategic information and research.

We convert raw data into critical information through a series of transformational steps that reduce the uncertainty that is inherent in unrefined data. At each step along the way, we work to ensure quality of the data transformation across four dimensions, which we call the "4 Cs":

Correctness | Validate data accuracy through comparison to external reference points. | |

Currency | Deliver new and updated content in a timely manner. | |

Completeness | Provide the right data attributes and analysis to ensure that customers have all of the necessary information to make critical decisions. | |

Consistency | Standardize identifiers and content across databases and products to be sure customers receive consistent information regardless of product platform. | |

5

We have standardized the data transformation process into seven steps. The order of the steps and the need to perform quality checks throughout the process is important because the quality of each step is dependent on the quality of all of the preceding steps. The seven-step process we follow in transforming data into critical information and insight involves the following:

Source data | We locate hundreds of possible data sources and then evaluate them for correctness, currency, and completeness. | |

Capture | We collect documents and digital feeds, harvest content from publicly available sources, visit sites for updates, etc. Once the data is aggregated, we validate and normalize the data before loading it into our proprietary databases. | |

Match | We link disparate instances of the same attribute. This knowledge-based activity ensures consistency over time and across sources, eliminating unlinked information about a single well, a single part, a single chemical, etc. | |

Identify | We attach an IHS identifier to matched information to ensure that the matched information stays linked. We also confirm that industry standard identifiers, which often vary over time, are accurate and appropriately matched to the IHS identifier. | |

Relate | We identify logical relationships and associations between entities and link those relationships through identification numbers. Examples include corporate parent and subsidiary relationships, leases and associated wells, international standards, and national standards. This step supplies the context for analysis. | |

Analyze | We use our industry experts to review, analyze, and add context and editorial commentary to the data to transform it into critical information and expert analysis for our customers. | |

Model and Forecast | We use our critical information and expert analysis to produce additional insight by providing unbiased research and intelligence with proprietary models and forecasting tools. Our experts use their extensive experience to build models and forecasting tools for our customers' use. | |

Using this seven-step process and the "4 Cs" of quality, we seek to transform data into critical information and insight that is both useful to our customers and available where and when they need it. This process also provides the foundation for our integrated solutions that combine our products and services to create differentiated solutions for the customers in our target industries.

Our Customers

We have a diverse customer base, ranging from large entities such as multinational companies and governments to small companies and technical professionals that span many industries, geographies, and end markets. Our customer base includes approximately 75 percent of the Fortune Global 500. Our largest 1,000 customers account for almost two-thirds of our revenue, yet no single customer represents more than 10 percent of our total revenue.

Our customers participate in global interconnected capital-intensive industries, and we are continuing to build on our existing scale to integrate our comprehensive content, expertise, tools, technology, and research and analysis to produce a differentiated solution set that places us at the heart of many of our customers’ core workflows. The result is a primarily subscription-based business, which tends to generate recurring revenue and cash flow for us. Subscription agreements generally represent approximately 75 percent of our total revenue, and are typically annual and non-cancellable for the term of the subscription and may contain provisions for minimum monthly payments. As evidenced by our organic revenue growth rates over the years, our subscription revenue is generally stable and predictable, and we have long-term relationships with many of our customers.

We develop our products and services based on customer needs in the target industries we serve and in the workflows that our customers use. By connecting our comprehensive content and expertise to our customers' workflows across our target industries, we strive to create value for our customers by uniquely addressing capital and operating decisions across our customers' entire supply chains and each of their target markets globally.

6

Within each of our geographic segments, our sales force is organized based on the size of our customers, our expertise in key vertical industries, and our horizontal workflows, as described below.

Vertical Industries

Our target industry sectors have many attributes in common. They are large, complex, global industries that have significant annual capital and operating outlays measured in the trillions of dollars. These industries rely on information and make critical decisions based on the comprehensive content, expert analysis, and workflow tools and technologies that we provide.

We have developed substantial breadth and depth of information and expertise in six main vertical industries within two product categories:

Resources

• | Energy and Natural Resources. This industry sector includes specific industries such as Oil & Gas, Coal, and Power & Utilities. All of our other target industries incur significant expense in this industry sector. Our content and analysis provides worldwide information on millions of wells, pipeline miles, and regulatory and mineral rights documents, as well as global information on oil and gas fields, basins, and operating assets and thousands of power and industrial plants. |

• | Chemicals. Our Chemicals content and analysis includes data for manufacturing processes, as well as capital expenditure, cost, price, production, trade, demand, and capacity industry analysis and forecasts for more than 250 chemicals in more than 50 countries. We also have an extensive library of detailed techno-economic analyses of chemicals and refining process technologies. We provide a number of consulting services including training, strategy development, and project development offerings to the chemical and related industries. Our business information services track current events, supply high-velocity information, and hold conferences related to the chemical industry. |

Industrials

• | Automotive. With the addition of R. L. Polk (which includes CARFAX, a leading provider of vehicle history information) in 2013, we substantially increased our value creation proposition by providing a comprehensive global view of the automotive value chain to our customers. We provide original equipment manufacturers (OEMs) and the automotive supply chain with authoritative analysis and forecasts of sales and production for light vehicles, medium and heavy commercial vehicles, powertrain, components, and technology systems across all major markets. We also provide a wide range of performance measurement tools and marketing solutions for car makers, dealers, and agencies. |

• | Technology. This industry sector includes the electronics, telecommunications, and media industries. We deliver comprehensive insight and tools for managing second source and component lifecycles, leveraging our component database of 400 million parts. We also perform teardown analysis to benchmark costs and design practices. Our Technology solutions enable customers to optimize their supplier and customer engagement strategy and differentiate their product portfolio from the competition through market share, supply chain, and technology adoption analyses and forecasts on a geographic, industry, and company level. |

• | Aerospace, Defense & Security. Our Aerospace, Defense & Security data and analysis provides specifications for thousands of military vehicles, naval vessels, and aircraft types. Our budget forecasts cover more than 95 percent of global defense spending, and we have analyzed more than 150,000 terrorism-related events, with more analyzed and added each day. |

• | Maritime & Trade. Our Maritime & Trade content and analysis provides comprehensive data on close to 200,000 ships operating in international waters, as well as monthly import and export statistics on more than 80 countries and tracking more than 90 percent of international trade by value. |

We support significant capital and operating decisions in these large global markets with the information, expertise, knowledge, specialized tools, and technologies that we provide. Many of these vertical industries are significantly interconnected, and our multi-disciplinary industry capabilities allow us to support them and the needs of a broad range of additional end markets that depend on these six industry sectors as critical elements of their supply chains, cost structures, and

7

investment decisions. Such additional end markets include Financials, Retail, Governments, Construction, and Consumer Products.

Horizontal Workflows

We focus on how customers within our target industry sectors and end markets make daily operating and capital investment decisions. We identify specific customer functions and the use of information, insight, analysis, tools, and technology in their daily workflows, and then develop the information, expertise, software tools, and technologies that integrate with their decision processes to enhance their success. We focus on four customer workflows that cover the spectrum from executive and strategic decisions to daily operations:

• | Strategy, Planning, and Analysis |

•Energy Technical

•Product Design

•Operational Excellence & Risk Management

Our targeted workflows and sample roles are outlined below:

Workflow | Sample Roles |

Strategy, Planning, and Analysis | Strategic Planning, Corporate Development, M&A, Investment Analysis, Risk Assessment, Business Development, and Trading |

Energy Technical | Geo-science, Petroleum Engineering |

Product Design | Engineering, Design, Research and Development |

Operational Excellence & Risk Management | Sustainability, Regulatory, Environment, Health and Safety, Procurement, Logistics, Operations, and Manufacturing |

• | Strategy, Planning, and Analysis. We provide strategic and commercial professionals with information, research, and tools that support a wide range of commercial decisions and processes, including capital investments, country-entry strategies, acquisitions, annual strategic planning processes, and monthly/quarterly production and sales forecasts. An example of the value we provide in this workflow is in Energy Insight, where we provide oil and gas producers with strategic analysis on upstream opportunities, provide downstream operators with forecasts of supply and demand for all petroleum products, and provide the gas and power utility sector with research on energy policy and its impact on power supply and demand. We underpin our solutions in this workflow with our economic and country risk capabilities, which translate high-level macroeconomic, political, and security drivers into industry-level demand forecasts and risk factors. We support customers primarily in heavy-asset industries where there is significant capital expenditure, long investment cycles, and important external macroeconomic and policy drivers. These industries require independent, authoritative, and rigorous third-party market information and analysis as critical inputs into strategic decisions. |

• | Energy Technical. Access to cost-effective, reliable, and safe energy sources is one of the most critical issues our society faces. We believe that increased competition for global hydrocarbon energy sources and the increased capital and operational costs required for their exploration, production, transportation, refining, and delivery of the final product to end customers drives demand for connected solutions consisting of raw data, information, insight, and relevant answer products. Supported by a robust service capability, we offer our customers a differentiated solution set that enables accurate, informed, and timely critical decisions. Our Energy Technical offerings include information, software, and advisory services addressing areas such as oil and gas production, geological information, energy activity, strategic planning, reconnaissance, geophysics, production engineering, production optimization, and information and research on unconventional hydrocarbon resources (e.g., shale gas, coal bed methane, and heavy oil). |

• | Product Design. Our Product Design solutions provide technical professionals with the information and insight required to more effectively design products, complete engineering projects, solve technical problems, and address the complex supply chain challenges of today's rapidly changing global economy. Our goal is to provide engineers, scientists, technical professionals, supply chain management, procurement executives, risk managers, and materials management professionals with the technical information and expertise necessary to help them make better decisions, solve complex problems more quickly, and execute their strategies to minimize risk and maximize operational efficiency and profitability. Our Product Design offerings include content and analysis on millions of engineering and technical standards, codes, specifications, handbooks, reference books, journals, and other scientific and technical documents, as well as software-based engineering decision engines for innovation, productivity, and quality. |

8

• | Operational Excellence & Risk Management. Our Operational Excellence & Risk Management solutions advance critical decisions associated with environmental, health, and safety operational risk, product stewardship, greenhouse gas, and corporate social responsibility, as well as advisory services that enable our customers to address the complex supply chain challenges of today's rapidly changing global economy. We deliver information management capabilities that enable the convergence of Operational Excellence & Risk Management information and processes to provide metrics and analytics that promote operational excellence and cost reduction, as well as compliance assurance and non-financial performance management. Our Operational Excellence & Risk Management offerings include solutions that cover air, water, and waste emissions management and reporting, regulatory compliance, sustainability, energy management, trade flows, commodity and component pricing and availability, supply chain market opportunity and risk, and supplier performance and viability metrics, among others. |

Sales and Marketing

Our sales teams are organized to support our customers across our three geographic segments; thus, our customer-facing efforts are designed to be aligned with our customers by industry and workflow within their local market. We also conduct regular customer surveys to understand both current customer satisfaction levels and potential opportunities for improvement, which we then use to provide additional direction to sales and marketing about key areas of focus.

Our strategic account management teams address the needs of our largest customers. Our account managers support the customer renewal process. New customer acquisition is largely conducted by our account managers and new business teams. These sales organizations identify potential new customer opportunities and develop the sales approach for larger new business opportunities. Our inside sales team pursues smaller new-customer opportunities. We enhance our sales model with e-commerce platforms that provide our customers and prospects with the ability to buy ad hoc reports. We also use a network of channel partners to reach customers in locations where it is not cost-effective to use our sales teams or maintain a sales office. Our channel partner network represents less than 5 percent of our total revenue.

Our marketing organization defines our marketing strategy and drives operational execution. A primary focus for marketing strategy is to empower IHS brand awareness, revenue acceleration, and market leadership across our key industries and workflows for all products and services globally. Functionally, this includes corporate marketing, product marketing, field marketing, and e-commerce.

Competition

We believe the principal competitive factors in our business include the following:

• | Depth, breadth, timeliness, and accuracy of information provided; |

•Quality of decision-support tools and services;

•Quality and relevance of our analysis and insight;

•Ease of use;

•Customer support; and

•Value for price.

We believe that we compete favorably on each of these factors. Although we face competition in specific industries and with respect to specific offerings, we do not believe that we have a direct competitor across all of our workflows and industry solutions due to the depth and breadth of our offerings. Competitors within specific industries or with respect to specific offerings are described below.

9

Strategy, Planning, and Analysis | Our Strategy, Planning, and Analysis offerings compete generally by customer market. Among others, we compete in Energy markets with offerings from Wood Mackenzie, Ltd., and PIRA Energy Group; in Aerospace & Defense markets with offerings from Forecast International and Defense News; in Maritime markets with offerings from Informa plc; in Automotive markets with offerings from LMC Automotive, Urban Science, and Experian and, with respect to vehicle history reports, principally with Experian and various other providers approved by the National Motor Vehicle Title Information System of the United States Department of Justice; in Technology markets with offerings from Gartner; and in Chemicals markets with offerings from Reed Elsevier and Nexant. Our economic and country risk and forecasting offerings compete with offerings from the Economist Intelligence Unit and Oxford Economics, among others. | |

Energy Technical | Our Energy Technical critical information offerings compete with offerings from Drilling Info, Inc., TGS-Nopec Geophysical Company, Wood Mackenzie Ltd., and Deloitte Touche Tohmatsu Limited, among others. Our geo-sciences software competes with products from Schlumberger Limited, Halliburton Company, and LMKR, among others. | |

Product Design | Our Product Design offerings compete with offerings of SAI Global, Techstreet, Thomas Publishing, and the standards developing organizations, among others. Our electronics design offerings compete with offerings from Arrow Electronics and parts manufacturers and distributors, among others. | |

Operational Excellence & Risk Management | Our Operational Excellence & Risk Management offerings compete with offerings from SAP and Enablon, among others. | |

Government Contracts

We sell our products to various government agencies and entities. No individual contract is significant to our business. Although some of our government contracts are subject to terms that would allow renegotiation of profits or termination at the election of the government, we believe that no renegotiation or termination of any individual contract or subcontract at the election of the government would have a material adverse effect on our financial results.

Intellectual Property

We rely heavily on intellectual property, including the intellectual property we own and license. We regard our trademarks, copyrights, licenses, and other intellectual property as valuable assets and use intellectual property laws, as well as license and confidentiality agreements with our employees, customers, channel partners, and others, to protect our rights. In addition, we exercise reasonable measures to protect our intellectual property rights and enforce these rights when we become aware of any potential or actual violation or misuse.

Intellectual property licensed from third parties, including standards development organizations (SDOs), government agencies, and manufacturers, is a component of our offerings and, in many cases, cannot be independently replaced or recreated by us or others. We have longstanding relationships with most of the third parties from whom we license information. Almost all of the licenses that we rely upon are nonexclusive and expire within one to two years, unless renewed.

We maintain registered trademarks in jurisdictions around the world. In addition, we have obtained patents and applied for patents in the United States, primarily related to our software portfolio, including our IHS Kingdom and IHS Goldfire products. For more information relating to our intellectual property rights, see "Risk Factors - We may not be able to protect intellectual property rights."

Employees

As of November 30, 2014, we had approximately 8,800 employees located in 32 countries around the world.

Seasonality

Our business has seasonal aspects. Our fourth quarter typically generates our highest quarterly levels of revenue and profit. Conversely, our first quarter generally has our lowest quarterly levels of revenue and profit. We also experience event-driven seasonality in our business; for instance, IHS Energy CERAWeek, an annual energy executive gathering, is held during

10

our second quarter. Another example is the biennial release of the Boiler Pressure Vessel Code (BPVC) engineering standard, which generates revenue for us predominantly in the third quarter of every other year. We most recently recognized a benefit in connection with the BPVC release in the third quarter of 2013.

Financial Information about Segments and Geographic Area

See "Item 8 - Financial Statements and Supplementary Data - Notes to Consolidated Financial Statements - Note 19" in Part II of this Form 10-K for information with respect to each segment's revenues, operating income, and total assets and for information with respect to our revenues and long-lived assets for the U.S., individual material foreign countries, and the rest of the world in aggregate. See also "Risk Factors - Our international operations are subject to exchange rate fluctuations and other risks relating to worldwide operations."

Available Information

Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are available, without charge, on our website, www.ihs.com, as soon as reasonably practicable after they are electronically filed with or furnished to the SEC. We have also posted our code of ethics, which we refer to as our Business Code of Conduct, on our website. Copies of each of these documents are also available, without charge, from IHS Investor Relations and Corporate Communications, 15 Inverness Way East, Englewood, CO 80112.

Item 1A. Risk Factors

In addition to the other information provided in this Form 10-K, you should carefully consider the risks described in this section. The risks described below are not the only risks that could adversely affect our business; other risks currently deemed immaterial or additional risks not currently known to us could also adversely affect us. These and other factors could have a material adverse effect on the value of your investment in our securities, meaning that you could lose all or part of your investment.

Note that this section includes forward-looking statements and future expectations as of the date of this Form 10-K. This discussion of Risk Factors should be read in conjunction with “Management's Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes in Part II of this Form 10-K.

Achieving our growth objectives may prove unsuccessful.

We seek to achieve our growth objectives by enhancing our offerings to meet the needs of our customers through organic development, including by delivering integrated workflow platforms, cross-selling our products across our existing customer base and acquiring new customers, entering into strategic partnerships, and acquisitions. If we are unable to successfully execute on our strategies to achieve our growth objectives, our growth rates could be adversely affected. An additional factor that may adversely affect our growth rates is continued global economic uncertainty. Our non-subscription business in particular may be adversely affected by decisions on the part of our customers to defer spending in uncertain economic environments.

If we are unable to consistently renew and enter into new subscriptions for our offerings, our results could weaken.

The majority of our revenue is based on subscriptions to our offerings. In 2014, we derived approximately 77 percent of our revenues from subscriptions, which revenue we recognize ratably over the subscription terms. Our operating results depend on our ability to achieve and sustain high renewal rates on our existing subscription base and to enter into new subscription arrangements at acceptable prices and other commercially acceptable terms. Failure to meet one or more of these subscription objectives could have a material adverse effect on our business, financial condition, and operating results.

The loss of, or the inability to attract and retain, key personnel could impair our future success.

Our future success depends to a large extent on the continued service of our employees, including our experts in research and analysis and other areas, as well as colleagues in sales, marketing, product development, critical operational roles, and management, including our executive officers. We must maintain our ability to attract, motivate, and retain highly qualified colleagues in order to support our customers and achieve business results. The loss of the services of key personnel and our inability to recruit effective replacements or to otherwise attract, motivate, or retain highly qualified personnel could have a material adverse effect on our business, financial condition, and operating results.

11

We could experience system failures or capacity constraints that could negatively impact our business.

Our ability to provide reliable service largely depends on the efficient and uninterrupted operation of complex systems, relying on people, processes, and technology to function effectively. Some elements of these systems have been outsourced to third-party providers. Some of our systems have been consolidated for the purpose of enhancing scalability and efficiency, which increases our dependency on a smaller number of systems. Any significant interruption to, failure of, or security breaches affecting, our systems could result in significant expense to repair, replace or remediate systems, equipment or facilities, a loss of customers, and harm to our business and reputation. Interruption, system failures or security breaches could result from a wide variety of causes, including the possibility of failures at third-party data centers, disruptions to the Internet, malicious attacks or cyber incidents such as unauthorized access, loss or destruction of data (including confidential and/or personal customer information), account takeovers, computer viruses or other malicious code, and the loss or failure of systems over which we have no control. The failure of our systems, or the loss of data, could result in legal claims or proceedings, disruption to our operations, damage to our reputation and remediation costs, which could individually or in the aggregate adversely affect our business and our insurance may not be adequate to compensate us for all losses, failures, or breaches.

Fraudulent or unpermitted data access and other security or privacy breaches may negatively impact our business and harm our reputation.

Security breaches in our facilities, computer networks, and databases may cause harm to our business and reputation and result in a loss of customers. Our systems may be vulnerable to physical break-ins, computer viruses, attacks by hackers and similar disruptive problems. Third-party contractors also may experience security breaches involving the storage and transmission of proprietary information. If users gain improper access to our databases, they may be able to steal, publish, delete or modify information included in our products or confidential or sensitive customer information that is stored or transmitted on our networks. Any misappropriation and/or misuse of our information could result in us, among other things, being in breach of certain data protection and related legislation, including regulations relating to the privacy of personal or payment card information.

A security or privacy breach may affect us in the following ways:

• | deterring customers from using our solutions; |

• | deterring data suppliers from supplying data to us; |

• | harming our reputation; |

• | exposing us to liability; |

• | increasing expenses to correct problems caused by the breach; |

• | affecting our ability to meet customers’ expectations; or |

• | causing inquiry from governmental authorities. |

Incidents in which customer data has been fraudulently or improperly acquired or viewed, or any other security or privacy breaches, may occur and could go undetected. We have experienced cybersecurity attacks, as have many of our customers and suppliers. While prior cybersecurity attacks have not had a material adverse effect on our financial results, we have taken and are taking reasonable steps to prevent future events, including implementation of system security measures, information back-up and disaster recovery processes. However, these steps may not be effective and there can be no assurance that any such steps can be effective against all possible risks.

If we are unable to successfully identify acquisitions or we experience integration or other risks resulting from our acquisitions, our financial results may be adversely affected.

As we continue pursuing selective acquisitions to support our business and growth strategy, we seek to be a disciplined acquirer, and there can be no assurance that we will be able to identify suitable candidates for successful acquisition at acceptable prices. In addition, our ability to achieve the expected returns and synergies from our past and future acquisitions and alliances depends in part upon our ability to effectively integrate the offerings, technology, sales, administrative functions, and personnel of these businesses into our business. We cannot assure you that we will be successful in integrating acquired businesses or that our acquired businesses will perform at the levels we anticipate. In addition, our past and future acquisitions may subject us to unanticipated risks or liabilities or disrupt our operations.

We depend on content obtained externally to support certain of our offerings, and the inability to continue to obtain access could prove harmful to our business.

12

We obtain data from a wide variety of external sources that we transform into critical information and insight and use to create integrated solutions for our customers. Certain of our offerings include content that is either purchased or licensed from third parties. In particular, our industry standards offerings that are part of our Product Design workflow rely on information licensed from SDOs. Offerings that rely upon SDO information accounted for less than 15 percent of our total revenue in 2014. We believe that the content licensed from many of these third parties, including the SDOs, cannot be obtained from alternate sources on favorable terms, if at all. Our license agreements with these third parties are generally nonexclusive and many are terminable on less than one year's notice. In addition, many of these third parties, including the SDOs, compete with one another and with us. If we lose access to a significant number of data sources and cannot replace the data through alternative sources or we are unable to obtain information licensed to us at cost-effective prices, specific customer solutions may be impacted and it could adversely affect the quality of our offerings and our business, financial condition, and operating results.

Our strategic investments and cost reduction initiatives may not result in anticipated savings or more efficient operations.

Over the past several years, including in 2014, we implemented significant strategic initiatives to reduce our cost structure, standardize our operations, and improve our ability to grow. We are deploying new processes and many of our colleagues across the business are changing the way they perform certain roles to capture efficiencies. We must also continue to invest in enhancing our existing products, including the development of new platforms to deliver our products, to meet the needs of our customers and differentiate our offerings from those of our competitors. There is risk that we may not realize the full potential benefit of our investments.

We may not be able to protect intellectual property rights.

We rely on copyright laws and nondisclosure, license, and confidentiality arrangements to protect our proprietary rights as well as the intellectual property rights of third parties whose content we license. However, we cannot assure you that the steps we have taken to protect our intellectual property rights, and the rights of those from whom we license intellectual property, are adequate to prevent unauthorized use, misappropriation, or theft of our intellectual property. We may also not be able to detect unauthorized uses or take timely and effective steps to remedy unauthorized conduct. In particular, a portion of our revenues are derived from jurisdictions where adequately protecting intellectual property rights may prove more challenging or impossible. To prevent or respond to unauthorized uses of our intellectual property, we might be required to engage in costly and time-consuming litigation and we may not ultimately prevail.

We may be exposed to litigation related to content we make available to customers and we may face legal liability or damage to our reputation if our customers are not satisfied with our offerings or if our offerings are misused.

Our business relies on licensing and delivering intellectual property to our customers and obtaining intellectual property from our suppliers. Accordingly, we may face potential liability for, among other things, breach of contract, negligence, and copyright and trademark infringement. Even litigation or infringement claims that lack merit may expose us to material expense or reputational damage. Damage to our reputation for any reason could adversely affect our ability to attract and retain customers, employees, and information suppliers. In addition, if the information in our offerings is incorrect for any reason, or if it is misused or used inappropriately, we could be subject to reputational damage or litigation that could exceed the value of any insurance coverage and adversely affect our business.

We rely on independent contractors and third parties whose actions could have a material adverse effect on our business.

We use independent contractors to help us obtain certain information. In addition, we rely on third-party dealers to sell our offerings in locations where we do not maintain a sales office or sales teams. We are limited in our ability to monitor and direct the activities of our independent contractors, but if any actions or business practices of these individuals or entities violate our policies or procedures or are otherwise deemed inappropriate or illegal, we could be subject to litigation, regulatory sanctions, or reputational damage, any of which could have a material adverse effect on our business.

As part of our strategic business model, we outsource certain operations and engage independent contractors to perform work in various locations around the world. For example, we outsource certain data hosting functions, as well as certain functions involving our data transformation process, to business partners who we believe offer us deep expertise in these areas, as well as scalability and cost effective services. By entering into these independent contractor arrangements and relying on them for critical business functions, we face risks that one or more independent contractors may unexpectedly cease operations, that they may perform work that deviates from our standards, that events in a given region may disrupt the independent contractor's operations, or that we may not be able to adequately protect our intellectual property. If these or other unforeseen risks were to occur, they could adversely affect our business.

13

We operate in competitive markets, which may adversely affect our market share and financial results.

While we do not believe that we have a direct competitor across all of our workflows and industry solutions, we face competition in specific industries and with respect to specific offerings. We may also face competition from organizations and businesses that have not traditionally competed with us but that could adapt their products and services or utilize significant financial and information-gathering resources, recognized brands, or technological expertise to begin competing with us. We believe that competitors are continuously enhancing their products and services, developing new products and services, and investing in technology to better serve the needs of their existing customers and to attract new customers. Increased competition could require us to make additional capital investments. Some of our competitors may also choose to sell products competitive with ours at lower prices, which may require us to reduce the prices of our offerings. An increase in our capital investments or price reductions by our competitors could negatively impact our margins and results of operations.

Some of the critical information we use in our offerings is publicly available in raw form at little or no cost.

The Internet, widespread availability of sophisticated search engines, and pervasive wireless data delivery have simplified the process of locating, gathering, and disseminating data, potentially diminishing the perceived value of our offerings. While we believe our offerings are distinguished by such factors as currency, accuracy and completeness, and our analysis and other added value, if users choose to obtain the information they need from public or other sources, our business, financial condition, and results of operations could be adversely affected.

Our brand and reputation are key assets and competitive advantages of our company and our business may be affected by how we are perceived in the marketplace.

Our ability to attract and retain customers is affected by external perceptions of our brand and reputation. Reputational damage from negative perceptions or publicity could damage our reputation with customers, prospects, and the public generally. Although we monitor developments for areas of potential risk to our reputation and brand, negative perceptions or publicity could have a material adverse effect on our business and financial results.

Changes in the legislative, regulatory, and commercial environments in which we operate may adversely impact our ability to collect, compile, use, and publish data and may impact our financial results.

Certain types of information we collect, compile, use, and publish, including offerings in our IHS Automotive and CARFAX businesses, are subject to regulation by governmental authorities in jurisdictions in which we operate. In addition, there is increasing concern among certain privacy advocates and government regulators regarding marketing and privacy matters, particularly as they relate to individual privacy interests. These concerns may result in new or amended laws and regulations. Future laws and regulations with respect to the collection, compilation, use, and publication of information and consumer privacy could result in limitations on our operations, increased compliance or litigation expense, adverse publicity, or loss of revenue, which could have a material adverse effect on our business, financial condition, and operating results. It is also possible that we could be prohibited from collecting or disseminating certain types of data, which could affect our ability to meet our customers’ needs.

Our international operations are subject to exchange rate fluctuations and other risks relating to worldwide operations.

We operate in many countries around the world and a significant part of our revenue comes from international sales. In 2014, we generated approximately 40 percent of our revenues from sales outside the United States. Approximately 20 percent of our revenue is transacted in currencies other than the U.S. dollar. We earn revenues, pay expenses, own assets, and incur liabilities in countries using currencies other than the U.S. dollar, including the British Pound, the Canadian Dollar, and the Euro. Because our consolidated financial statements are presented in U.S. dollars, we must translate revenues, income, expenses, and the value of assets and liabilities into U.S. dollars at exchange rates in effect during or at the end of each reporting period. We may use derivative financial instruments to reduce our net exposure to currency exchange rate fluctuations. Nevertheless, increases or decreases in the value of the U.S. dollar against other major currencies can materially affect our net operating revenues, operating income, and the value of balance sheet items denominated in foreign currencies.

Operating in many jurisdictions around the world, we may be affected by: changes in tax rates and tax laws or their interpretation, including changes related to tax holidays or tax incentives; trade protection laws, policies and measures, and other regulatory requirements affecting trade and investment; unexpected changes in regulatory requirements; social, political, labor, or economic conditions in a specific country or region; and difficulties in staffing and managing local operations. We must also manage the uncertainties of obtaining data and creating solutions that are relevant to particular geographic markets; differing

14

levels of intellectual property protection in various jurisdictions; and potential adverse tax consequences on the repatriation of funds. In addition, as we operate our business around the world, we must manage the potential conflicts between locally accepted business practices in any given jurisdiction and our obligations to comply with laws and regulations, including anti-corruption regulations applicable to us, such as the U.S. Foreign Corrupt Practices Act and the UK Bribery Act. We have developed and instituted a corporate compliance program which includes, among other things, employee training and the creation of appropriate policies defining employee behavior that mandate adherence to laws. While we implement policies and procedures intended to promote and facilitate compliance with all applicable laws, our employees, contractors, and agents, as well as those independent companies to which we outsource certain business operations, may take actions in violation of our policies. Any such violation, even if prohibited by our policies, could have an adverse effect on our business and reputation.

Our inability to manage some or all of these risks of operating a global business could have a material adverse effect on our business, financial condition, and operating results.

Our business performance might not be sufficient for us to meet the full-year financial guidance that we provide publicly.

We provide full-year financial guidance to the public based upon our assumptions regarding our expected financial performance. For example, we provide assumptions regarding our ability to grow revenue and to achieve our profitability targets. While we believe that our annual financial guidance provides investors and analysts with insight to our view of the company's future performance, such financial guidance is based on assumptions that may not always prove to be accurate and may vary from actual results. If we fail to meet the full-year financial guidance that we provide, or if we find it necessary to revise such guidance during the year, the market value of our common stock could be adversely affected.

The price of our common stock may be volatile and may be affected by market conditions beyond our control.

Our share price is likely to fluctuate in the future because of the volatility of the stock market in general and a variety of factors, many of which are beyond our control. Market fluctuations could result in volatility in the price of shares of our common stock, one possible outcome of which could be a decline in the value of your investment. In addition, if our operating results fail to meet the expectations of stock analysts or investors, or if we are perceived by the market to suffer material business or reputational damage, we may experience a significant decline in the trading price of our common stock.

Our indebtedness could adversely affect our business, financial condition, and results of operations.

Our indebtedness could have significant consequences on our future operations, including:

• | making it more difficult for us to satisfy our debt obligations and our other ongoing business obligations, which may result in defaults; |

• | events of default if we fail to comply with the financial and other covenants contained in the agreements governing our debt instruments, which could result in all of our debt becoming immediately due and payable or require us to negotiate an amendment to financial or other covenants that could cause us to incur additional fees and expenses; |

• | sensitivity to interest rate increases on our variable rate outstanding indebtedness, which could cause our debt service obligations to increase significantly; |

• | reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions and other general corporate purposes, and limiting our ability to obtain additional financing for these purposes; |

• | limiting our flexibility in planning for, or reacting to, and increasing our vulnerability to, changes in our business, the industries in which we operate, and the overall economy; |

• | placing us at a competitive disadvantage compared to any of our competitors that have less debt or are less leveraged; and |

• | increasing our vulnerability to the impact of adverse economic and industry conditions. |

Our ability to meet our payment and other obligations under our debt instruments depends on our ability to generate significant cash flow in the future. This, to some extent, is subject to general economic, financial, competitive, legislative and regulatory factors as well as other factors that are beyond our control. We cannot assure you that our business will generate cash flow from operations, or that future borrowings will be available to us under our existing or any future credit facilities or otherwise, in an amount sufficient to enable us to meet our debt obligations and to fund other liquidity needs. We may incur substantial additional indebtedness, including secured indebtedness, for many reasons, including to fund acquisitions. If we add additional debt or other liabilities, the related risks that we face could intensify.

Item 1B. Unresolved Staff Comments

15

None.

Item 2. Properties

Our Facilities

Our colleagues work in offices at 129 locations around the world, comprised of 67 offices in the Americas (54 in the United States), 38 offices in EMEA, and 24 offices in APAC. We own the buildings at three of our facilities, including our headquarters in Englewood, Colorado, and two other office locations. All of our other facilities are leased with terms ranging from month-to-month at several locations to an expiration date in 2027 for one of our facilities. We believe that our properties, taken as a whole, are in good operating condition, are suitable and adequate for our current business operations, and that additional or alternative space will be available on commercially reasonable terms for future use and expansion.

Item 3. Legal Proceedings

See "Item 8 - Financial Statements and Supplementary Data - Notes to Consolidated Financial Statements - Note 15" in Part II of this Form 10-K for information about legal proceedings.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our Class A common stock is quoted on the New York Stock Exchange under the symbol “IHS.” The following table sets forth for the indicated periods the high and low sales prices per share for our Class A common stock on the New York Stock Exchange:

Fiscal Year 2014 Quarters Ended: | High | Low | ||||||

February 28, 2014 | $ | 123.95 | $ | 110.44 | ||||

May 31, 2014 | 126.83 | 116.76 | ||||||

August 31, 2014 | 143.49 | 124.62 | ||||||

November 30, 2014 | 143.92 | 118.41 | ||||||

Fiscal Year 2013 Quarters Ended: | High | Low | ||||||

February 28, 2013 | $ | 109.69 | $ | 89.58 | ||||

May 31, 2013 | 115.64 | 95.43 | ||||||

August 31, 2013 | 117.12 | 95.03 | ||||||

November 30, 2013 | 117.65 | 107.31 | ||||||

We have been advised by our transfer agent, American Stock Transfer, that we had 58 holders of record of our Class A Common Stock as of December 31, 2014. Based on reports of security position listings and the number of proxies requested by brokers in conjunction with the prior year’s annual meeting of stockholders, we believe we have approximately 41,000 beneficial holders of our Class A Common Stock.

Our authorized capital stock consists of 160,000,000 shares of Class A common stock. The holders of our Class A common stock are entitled to one vote per share.

Dividend Policy

We have not previously paid a dividend, and we do not anticipate paying any dividends in the foreseeable future.

16

Securities Authorized for Issuance Under Equity Compensation Plans

The following table sets forth information as of the end of fiscal year 2014 with respect to compensation plans under which equity securities are authorized for issuance.

Equity Compensation Plan Information | |||||||||

Plan Category | Number of securities to be issued upon exercise of outstanding options, warrants and rights ( a ) | Weighted-average exercise price of outstanding options, warrants, and rights ( b ) | Number of securities remaining available for issuance under equity compensation plans (excluding securities reflected in column (a)) ( c ) | ||||||

Equity compensation plans approved by security holders | 3,379,506 | (1) | N/A | (2) | 2,177,440 | (3) | |||

Equity compensation plans not approved by security holders | N/A | N/A | N/A | ||||||

Total | 3,379,506 | N/A | 2,177,440 | ||||||

(1) Includes (a) 2,304,974 restricted stock units and performance stock units at target performance levels that were issued with no exercise price or other consideration, (b) 938,531 shares reserved for issuance if above target performance levels on performance-based stock units are met, (c) 121,848 deferred stock units payable to non-employee directors upon their termination of service, and (d) 14,153 restricted stock units that are payable in cash. | |||||||||

(2) There are no outstanding stock options, warrants, or rights. | |||||||||

(3) Includes shares surrendered to the Company upon vesting of time- and performance-based restricted stock units for a value equal to their minimum statutory tax liability. | |||||||||

Issuer Purchases of Equity Securities

The following table provides detail about our share repurchases during the three months ended November 30, 2014. See "Item 8 - Financial Statements and Supplementary Data - Notes to Consolidated Financial Statements - Note 16" in Part II of this Form 10-K for information regarding our stock repurchase programs.

Total Number of Shares Purchased (1) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Dollar Value of Shares That May Yet Be Purchased Under the Plans or Programs (in thousands) (3) | ||||||||||

September 1 - September 30, 2014: | |||||||||||||

Share repurchase programs (1) | — | $ | — | — | $ | 4,021 | |||||||

Employee transactions (2) | — | $ | — | N/A | N/A | ||||||||

October 1 - October 31, 2014: | |||||||||||||

Share repurchase programs (1) | — | $ | — | — | $ | 4,021 | |||||||

Employee transactions (2) | 8,668 | $ | 123.92 | N/A | N/A | ||||||||

November 1 - November 30, 2014: | |||||||||||||

Share repurchase programs (1) | — | $ | — | — | $ | 4,021 | |||||||

Employee transactions (2) | 77,749 | $ | 129.94 | N/A | N/A | ||||||||

Total share repurchases | 86,417 | $ | 129.33 | — | |||||||||

(1) In March 2011, our board of directors authorized the repurchase of up to one million shares of Class A common stock per fiscal year in the open market (the March 2011 Program). We may execute on this program at our discretion, balancing dilution offset with other investment opportunities of the business, including acquisitions. The March 2011 Program does not have an expiration date.

In October 2012, our board of directors authorized the repurchase of shares of Class A common stock with a maximum aggregate value of $100 million (the October 2012 Program). We may repurchase shares of Class A common stock in open market purchases or through privately negotiated transactions in compliance with Rule 10b-18 under the Securities Exchange Act of 1934, as amended (Exchange Act), subject to market conditions, applicable legal requirements, and other relevant factors. The October 2012 Program does not obligate us to repurchase any dollar amount or number of shares of Class A common stock, and it may be suspended at any time at our discretion.

17

(2) Amounts represent shares of Class A common stock surrendered by employees in an amount equal to the statutory tax liability associated with the vesting of their equity awards. We then pay the statutory tax on behalf of the employee. Our board of directors approved this program in 2006 in an effort to reduce the dilutive effects of employee equity grants.

(3) Amounts represent remaining dollar value of shares of Class A common stock that may yet be purchased under the October 2012 Program. In addition, the March 2011 Program allows us to repurchase up to one million additional shares of Class A common stock per fiscal year. Since no common shares were repurchased under the March 2011 Program in fiscal 2014, at the end of each of September 2014, October 2014, and November 2014, there were one million shares of Class A common stock that may yet have been purchased at the end of each of those months under the March 2011 Program.

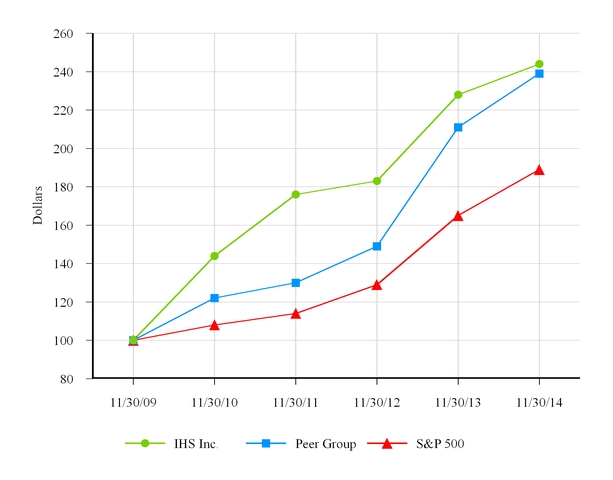

Performance Graph

The following graph compares our total cumulative stockholder return with the Standard & Poor's Composite Stock Index (S&P 500) and a peer index representing the total price change of The Corporate Executive Board Company; The Dun & Bradstreet Corporation; Equifax Inc.; FactSet Research Systems Inc.; Gartner, Inc.; McGraw Hill Financial, Inc.; Moody’s Corporation; MSCI Inc.; Nielsen Holdings N.V.; Solera Holdings, Inc.; Thomson Reuters Corporation; and Verisk Analytics, Inc.

The graph assumes a $100 cash investment on November 30, 2009 and the reinvestment of all dividends (which we did not pay). This graph is not indicative of future financial performance.

Comparison of Cumulative Total Return Among IHS Inc., S&P 500 Index, and Peer Group

18

Item 6. Selected Financial Data

You should read the following selected consolidated financial data in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and the related notes appearing in Part II of this Form 10-K.

Years Ended November 30, | |||||||||||||||

2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||

(in thousands, except for per share amounts) | |||||||||||||||

Statement of Operations Data: | |||||||||||||||

Revenue | $ | 2,230,794 | $ | 1,840,631 | $ | 1,529,869 | $ | 1,325,638 | $ | 1,057,742 | |||||

Income from continuing operations | 194,549 | 131,834 | 158,149 | 135,289 | 133,517 | ||||||||||

Income (loss) from discontinued operations | — | (101 | ) | 19 | 126 | 4,223 | |||||||||

Net income | 194,549 | 131,733 | 158,168 | 135,415 | 137,740 | ||||||||||

Basic earnings per share: | |||||||||||||||

Income from continuing operations | $ | 2.85 | $ | 1.98 | $ | 2.40 | $ | 2.08 | $ | 2.09 | |||||

Income from discontinued operations | — | — | — | — | 0.07 | ||||||||||

Net income | $ | 2.85 | $ | 1.98 | $ | 2.40 | $ | 2.09 | $ | 2.15 | |||||

Diluted earnings per share: | |||||||||||||||

Income from continuing operations | $ | 2.81 | $ | 1.95 | $ | 2.37 | $ | 2.06 | $ | 2.06 | |||||

Income from discontinued operations | — | — | — | — | 0.07 | ||||||||||

Net income | $ | 2.81 | $ | 1.95 | $ | 2.37 | $ | 2.06 | $ | 2.13 | |||||

Balance Sheet Data (as of period end): | |||||||||||||||

Cash and cash equivalents | $ | 153,156 | $ | 258,367 | $ | 345,008 | $ | 234,685 | $ | 200,735 | |||||

Total assets | 5,348,430 | 5,359,613 | 3,549,211 | 3,073,037 | 2,155,702 | ||||||||||

Total long-term debt and capital leases | 1,806,098 | 1,779,065 | 890,922 | 658,911 | 275,095 | ||||||||||

Total stockholders' equity | 2,159,546 | 1,906,963 | 1,584,358 | 1,384,729 | 1,176,081 | ||||||||||

19

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The following discussion of our financial condition and operating results should be read in conjunction with other information and disclosures elsewhere in this Form 10-K, including “Selected Financial Data,” our consolidated financial statements and accompanying notes, and "Website and Social Media Disclosure." The following discussion includes forward-looking statements as described in “Cautionary Note Regarding Forward-Looking Statements” in this Form 10-K. A detailed discussion of risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is outlined under “Risk Factors” in this Form 10-K.

Executive Summary

Business Overview

We are a leading source of information, insight, and analytics in critical areas that shape today's business landscape. Businesses and governments in more than 150 countries around the globe rely on our comprehensive content, expert independent analysis, and flexible delivery methods. Our aim is to embed our solutions within the entire spectrum of our customers’ organization, enabling executive level capital deployment strategies and following decision-making activities throughout their organizations to front-line employees tasked with managing their company’s complex core daily operations. We have been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, we are committed to sustainable, profitable growth and employ approximately 8,800 people in 32 countries around the world.

Inherent in all of our strategies is a firm commitment to put our customers first in everything that we do. To best serve our customers and be as close to them as possible, we are organized by geographies into three business segments: Americas, EMEA, and APAC. Our integrated global organization is designed to make it easier for our customers to do business with us by providing a cohesive, consistent, and effective sales-and-marketing approach in each local region.