Attached files

Table of Contents

As filed with the Securities and Exchange Commission on December 30, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Spark Therapeutics, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 2836 | 46-2654405 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

3737 Market Street

Suite 1300

Philadelphia, PA 19104

(888) 772-7560

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jeffrey D. Marrazzo

Chief Executive Officer

Spark Therapeutics, Inc.

3737 Market Street

Suite 1300

Philadelphia, PA 19104

(888) 772-7560

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Steven D. Singer, Esq. Lia Der Marderosian, Esq. Wilmer Cutler Pickering Hale and Dorr LLP 7 World Trade Center, 250 Greenwich Street New York, NY 10007 Telephone: (212) 230-8800 |

Joseph W. La Barge, Esq. General Counsel Spark Therapeutics, Inc. 3737 Market Street Suite 1300 Philadelphia, PA 19104 Telephone: (888) 772-7560 |

Richard D. Truesdell, Jr., Esq. Sophia Hudson, Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Telephone: (212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |||

| Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities to be registered | Proposed maximum aggregate offering price(1) | Amount of registration fee(2) | ||

| Common Stock, $0.001 par value per share |

$86,250,000 | $10,023 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated December 30, 2014

shares

Common stock

This is an initial public offering of common stock by Spark Therapeutics, Inc. We are selling shares of common stock. The estimated initial public offering price is between $ and $ per share.

Prior to this offering, there has been no public market for our common stock. We have applied to have our common stock listed on the NASDAQ Global Market under the symbol “ONCE.”

We are an emerging growth company as that term is used in the Jumpstart Our Business Startups Act of 2012, and, as such, have elected to comply with certain reduced public reporting requirements.

| Per share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions (1) |

$ | $ | ||||||

| Proceeds to Spark, before expenses |

$ | $ | ||||||

| (1) | We have agreed to reimburse the underwriters for certain FINRA-related expenses. See “Underwriting” beginning on page 165 of this prospectus. |

We have granted the underwriters an option for a period of 30 days to purchase up to an additional shares of common stock.

Investing in our common stock involves risks. See “Risk factors” beginning on page 12 of this prospectus.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to investors on or about , 2015.

| J.P. Morgan | Credit Suisse | |

Cowen and Company

Sanford C. Bernstein

The date of this prospectus is , 2015.

Table of Contents

| Page | ||||

| 1 | ||||

| 12 | ||||

| 61 | ||||

| 63 | ||||

| 64 | ||||

| 64 | ||||

| 65 | ||||

| 67 | ||||

| 70 | ||||

| Management’s discussion and analysis of financial condition and results of operations |

72 | |||

| 84 | ||||

| 128 | ||||

| 137 | ||||

| 149 | ||||

| 152 | ||||

| 154 | ||||

| 158 | ||||

| Material U.S. federal income and estate tax considerations for non-U.S. holders of common stock |

161 | |||

| 165 | ||||

| 171 | ||||

| 171 | ||||

| 171 | ||||

| F-1 | ||||

Neither we nor the underwriters have authorized anyone to provide you with any information other than that contained in this prospectus, any amendment or supplement to this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. The underwriters and we take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until (25 days after the commencement of this offering), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscription.

For investors outside the United States: We have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, especially the “Risk factors” section beginning on page 12 and our financial statements and the related notes appearing at the end of this prospectus, before making an investment decision.

Overview

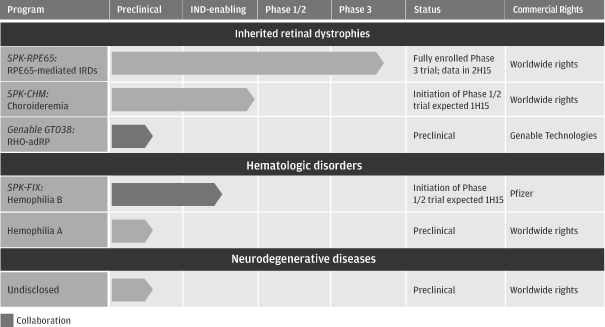

We are a leader in the field of gene therapy, seeking to transform the lives of patients suffering from debilitating genetic diseases by developing one-time, life-altering treatments. Our product candidates have the potential to provide long-lasting effects, dramatically and positively changing the lives of patients with conditions where no, or only palliative, therapies exist. Our initial focus is on treating orphan diseases, and we have demonstrated promising clinical outcomes with our first product candidate targeting rare blinding conditions, which has received both breakthrough therapy and orphan product designation and is in a fully enrolled, pivotal Phase 3 clinical trial with data expected in the second half of 2015. We also have built a pipeline of product candidates targeting additional blinding conditions, hematologic disorders and neurodegenerative diseases, including a second product candidate targeting another rare blinding condition, for which we expect to initiate a clinical trial in the first half of 2015, and a collaboration with Pfizer Inc., or Pfizer, for the development and commercialization of a gene therapy for the treatment of hemophilia B. Our platform technology is based on more than two decades of gene therapy research, development, manufacturing and clinical trials conducted at The Children’s Hospital of Philadelphia, or CHOP.

Product candidates

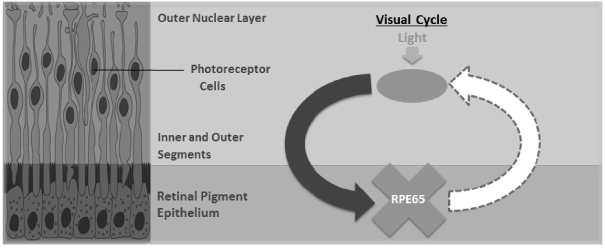

Our most advanced product candidate, SPK-RPE65, which is in a pivotal Phase 3 clinical trial, targets a group of rare blinding conditions known as inherited retinal dystrophies, or IRDs, caused by non sex-linked, or autosomal recessive, mutations in the RPE65 gene. Patients suffering from RPE65-mediated IRDs are affected by a range of severe visual impairments, which ultimately lead to blindness, that make independent activities of daily living challenging. For example, affected children often depend on visual aids to carry out classroom activities while adults with these diseases may face diminished employment opportunities and may be stripped of some of the rewards of parenting, such as watching a child play his or her favorite sport. We estimate that there are approximately 3,500 individuals with RPE65-mediated IRDs in the United States and the five major European markets.

SPK-RPE65 is engineered using a vector derived from an adeno-associated virus, or AAV, which is a small, non-pathogenic cold virus. To create the vector, DNA encoding the AAV viral genes is removed, disarming the virus, and is replaced with the therapeutic gene sequence for the RPE65 protein, which is then delivered via injection to the retina. Production of RPE65 protein in the retina helps convert light into an electrical signal, and is necessary for vision.

To date, the results of our two Phase 1 clinical trials, along with reports from our clinical study team and other feedback regarding the subjects in the trials, suggest that SPK-RPE65 enables subjects to perform activities of daily living with greater independence than prior to treatment and has long-lasting effects in restoring functional vision, with subjects having been followed for a period of at least five years. Notably, as reported by our clinical study team, following a single injection of SPK-RPE65 in one eye, the children from our initial Phase 1 trial no longer depended on visual aids to carry out classroom activities and were able to walk and play more like normally sighted kids. Furthermore, inclusive of the subjects in our ongoing Phase 3 clinical trial, we have not observed any drug-related serious adverse events to date.

- 1 -

Table of Contents

We are conducting a fully enrolled, pivotal Phase 3 clinical trial of SPK-RPE65 in which we have dosed all subjects in the treatment group and currently are collecting data. We anticipate reporting final results during the second half of 2015. If successful, we plan to submit a biologics license application, or BLA, to the U.S. Food and Drug Administration, or FDA, in 2016. SPK-RPE65 has the potential to be the first gene therapy approved in the United States for the treatment of a genetic disease and the first approved pharmacologic treatment for any IRD.

RPE65-mediated IRDs historically have been characterized most frequently as Leber’s congenital amaurosis, or LCA, and retinitis pigmentosa, or RP. LCA is a rare, inherited eye disease that results in severe visual impairment and, ultimately, blindness that typically is diagnosed in childhood. RP also is a rare, inherited eye disease that results in severe visual impairment and, ultimately, blindness but that typically is diagnosed in the teenage years or later. According to key opinion leaders, over the past decade, the diagnosis of IRDs has begun to shift from clinical classifications to a diagnosis of disease based on the specific underlying causal gene. To date, across all of our clinical trials, SPK-RPE65 has been studied in subjects with LCA due to RPE65 mutations, as confirmed by genetic testing. However, with the broad availability of genetic testing and this corresponding shift from clinical to genetic diagnosis, we believe SPK-RPE65 will have broad application to all IRDs caused by autosomal recessive RPE65 gene mutations.

We have received both breakthrough therapy and orphan product designation for SPK-RPE65. Breakthrough therapy designation is granted by FDA with the intention of expediting the development and regulatory review of a product candidate intended to treat a serious or life-threatening condition when preliminary clinical evidence, which in our case were the data from our two Phase 1 clinical trials of SPK-RPE65, indicates the potential for substantial improvement over existing therapies. SPK-RPE65 also has received orphan product designation in both the United States and the European Union for the treatment of patients with a diagnosis of LCA due to RPE65 mutations. FDA may designate a biologic product as an orphan product if it is intended to treat a rare disease or condition, which generally is defined as having a patient population of fewer than 200,000 individuals in the United States. Orphan product designation, subject to limited exceptions, can provide a period of market exclusivity for a product that is the first to receive marketing approval for the designated indication. We are seeking expansion of our orphan product designation for SPK-RPE65 to other IRDs caused by RPE65 mutations, in addition to LCA. We believe that the potential one-time nature of a gene therapy treatment could enable a company that receives the first FDA approval for a disease or condition, and which also has obtained orphan product exclusivity for such disease or condition, to treat a substantial portion of the addressable patient population during the period of orphan product exclusivity.

The RPE65 gene is one of more than 220 genes that have been identified to cause IRDs. We are expanding our portfolio of product candidates to target additional IRDs caused by gene mutations for which we believe we will be able to leverage our experience with SPK-RPE65. Our first such follow-on product candidate is SPK-CHM for the treatment of choroideremia, or CHM.

CHM is an IRD linked to the X-chromosome, or X-linked, which manifests in affected males in childhood as night blindness and a reduction of visual field, followed by progressive constriction of visual fields. For CHM patients, it is often in middle age, when people typically are at or near their greatest income-earning potential, that visual impairment begins to limit independent activities of daily living leading to a severe decrease in vision and, eventually, blindness. We estimate that CHM affects approximately 12,500 males in the United States and the five major European markets.

We use the same vector design, administration method and manufacturing process for SPK-CHM that we use for SPK-RPE65. We intend to initiate a dose-escalating, Phase 1/2 clinical trial of SPK-CHM during the first half of 2015, in which we currently expect to enroll up to 10 subjects. We have received orphan product designation for SPK-CHM for the treatment of choroideremia in both the United States and the European Union.

- 2 -

Table of Contents

We have established human proof-of-concept in using gene therapy to deliver and express a therapeutic gene in the liver as part of our SPK-FIX program for the treatment of hemophilia B. Hemophilia B is a serious and rare inherited hematologic disorder, characterized by a mutation in the Factor IX, or FIX, gene which leads to deficient blood coagulation and an increased risk of bleeding or hemorrhaging. According to the 2012 World Federation of Hemophilia Annual Global Survey, approximately 28,000 people worldwide suffer from hemophilia B.

In December 2014, we entered into a global collaboration agreement with Pfizer for the development and commercialization of product candidates in our SPK-FIX program for the treatment of hemophilia B. Under the terms of the agreement, we received a $20.0 million upfront payment and are eligible to receive up to $260.0 million in aggregate milestone payments, as well as royalties calculated as a low-teen percentage of net product sales. Pfizer and we are developing proprietary, bio-engineered AAV vectors utilizing a high-activity transgene and a treatment protocol designed to mitigate immune responses seen in other hemophilia B gene therapy trials, including our own, that have limited the duration of efficacy. We intend to initiate a Phase 1/2 trial in the first half of 2015.

We have preclinical programs in development for the treatment of hemophilia A and neurodegenerative diseases. We have exclusively in-licensed a broad range of rights for these preclinical programs.

From time to time, we may evaluate collaboration opportunities for our product candidates, as we have with Pfizer. We also expect to work opportunistically with pharmaceutical and biotechnology companies, as we are with Genable Technologies Limited, or Genable, seeking to utilize our technology and know-how for developing additional gene therapy products.

The following table summarizes information regarding our product candidates and development programs.

- 3 -

Table of Contents

Technology

We are building a fully integrated gene therapy platform to accelerate the development of product candidates across multiple therapeutic areas. Our platform technology, which leverages two decades of gene therapy research, development, manufacturing and clinical trials conducted at CHOP, enables us to pursue multiple therapeutic targets. Our scientists and scientific advisors have accumulated over 150 years of collective experience in the field of gene therapy, contributing key insights and significant developments that have coincided with a resurgence of interest in gene-based medicines.

Our proprietary manufacturing processes produce consistent yields of highly pure and stable gene therapy product candidates. Gene therapies made using our platform technology, including AAV vectors and vectors derived from the lentivirus family of viruses, or lentiviral vectors, have been, or are being, used by several biopharmaceutical companies in clinical trials of their own gene therapy product candidates, as well as in multiple clinical trials sponsored by the U.S. National Institutes of Health.

Our strategy

Our goal is to transform the lives of patients by being the leading, fully-integrated gene therapy company. We are seeking to develop, manufacture and commercialize multiple product candidates targeting orphan genetic diseases across multiple tissue types and therapeutic areas. To achieve our goal, we are pursuing the following strategies:

| • | Successfully complete clinical development and obtain marketing approval for SPK-RPE65 in the United States and the European Union. |

| • | Establish a global commercial infrastructure for SPK-RPE65. |

| • | Establish a franchise of gene therapies for additional IRDs, focusing next on the treatment of choroideremia with SPK-CHM. |

| • | Continue to build a liver-directed gene therapy platform, with an initial focus on our SPK-FIX program for the treatment of hemophilia B in collaboration with Pfizer. |

| • | Advance preclinical neurodegenerative programs into clinical development. |

| • | Leverage our proprietary manufacturing platform to partner selectively with other pharmaceutical and biotechnology companies. |

Recent financing

In May 2014, we completed a $72.7 million private placement of shares of Series B convertible preferred stock, or our Series B financing. Investors in our Series B financing include investment funds managed by, or affiliated with, Sofinnova Ventures, Brookside Capital, Deerfield Management Company, Rock Springs Capital, T. Rowe Price Associates, Wellington Management Company and two other healthcare investment funds. CHOP also participated in our Series B financing.

Risks associated with our business

Our business is subject to a number of risks of which you should be aware before making an investment decision. These risks are discussed more fully in the “Risk factors” section of this prospectus immediately following this prospectus summary. These risks include the following:

| • | We have incurred net losses since inception. As of September 30, 2014, we had an accumulated deficit of $72.6 million. We expect to incur losses for the foreseeable future and may never achieve or maintain profitability. |

- 4 -

Table of Contents

| • | Our gene therapy product candidates are based on a novel technology, which makes it difficult to predict the time and cost of development and of subsequently obtaining regulatory approval. At the moment, no gene therapy product has been approved in the United States and only one such product has been approved in the European Union. |

| • | Because we are developing product candidates for the treatment of diseases in which there is little clinical experience and, in some cases, using new endpoints or analytical methodologies, there is increased risk that FDA or other regulatory authorities may not consider the endpoints of our pivotal Phase 3 clinical trial to provide clinically meaningful results and that these results may be difficult to analyze. |

| • | While we believe SPK-RPE65 should be applicable for the treatment of patients with any IRD mediated by an RPE65 mutation, the results from our pivotal Phase 3 clinical trial for SPK-RPE65, which included only subjects diagnosed with LCA due to RPE65 mutations, may not support as broad a marketing approval as we seek, and FDA and the European Medicines Agency, or EMA, may require us to conduct additional clinical trials or evaluate subjects for an additional follow-up period. |

| • | Gene therapies are novel, complex and difficult to manufacture. We could experience production problems that result in delays in the development of our product candidates or otherwise adversely affect our business. To date, no current Good Manufacturing Practices, or cGMP, gene therapy manufacturing facility in the United States has received approval from FDA for the manufacture of an approved gene therapy product. |

| • | We have entered into, and may in the future enter into additional, collaborations with third parties to develop product candidates. If these collaborations are not successful, our business could be adversely affected. |

| • | We face significant competition in an environment of rapid technological change. We are aware of at least 12 other companies and academic institutions that currently are developing AAV-based gene therapies. There is a possibility that one or more of our competitors may develop therapies that are more effective than ours or may obtain regulatory approval prior to us. |

| • | To the extent we rely on CHOP’s manufacturing facility for commercial supply, CHOP will be subject to significant regulatory oversight with respect to manufacturing our products. CHOP’s manufacturing facilities may not meet regulatory requirements. |

| • | If we are unable to establish sales and marketing capabilities or enter into agreements with third parties to market and sell any approved product candidates, we may be unable to generate any product revenue. |

| • | If the market opportunities for our product candidates are smaller than we believe they are, or if we do not maintain orphan product designation or receive market exclusivity, our product revenues may be adversely affected and our business may suffer. |

| • | The insurance coverage and reimbursement status of newly approved products is uncertain. Failure to obtain or maintain adequate coverage and reimbursement for our products, if approved, could limit our ability to market those products and decrease our ability to generate product revenue. |

| • | Our gene therapy approach utilizes vectors derived from viruses, which may be perceived as unsafe or may result in unforeseen adverse events. Negative public opinion and increased regulatory scrutiny of gene therapy may damage public perception of the safety of our product candidates and adversely affect our ability to conduct clinical trials or obtain regulatory approvals for our product candidates. |

- 5 -

Table of Contents

| • | We may not be successful in our efforts to identify or discover additional product candidates and may fail to capitalize on programs or product candidates that may be a greater commercial opportunity or for which there is a greater likelihood of success. |

| • | If we are not able to obtain or maintain adequate intellectual property protection covering our product candidates and manufacturing technologies, our competitors could develop and commercialize products and manufacturing technologies similar or identical to ours, and our ability to successfully commercialize our product candidates and manufacturing technologies may be impaired. |

| • | Our rights to develop and commercialize our product candidates are subject, in part, to the terms and conditions of licenses granted to us by others. For example, we have a co-exclusive license to patent rights that relate to methods for treating patients with LCA due to RPE65 mutations, under which one licensor, on behalf of the other co-licensors, has the right to license the same patent rights to one additional party. |

| • | After this offering, our executive officers, directors and principal stockholders will maintain the ability to control all matters submitted to stockholders for approval. |

Our corporate information

Our company was formed as AAVenue Therapeutics, LLC, a Delaware limited liability company, on March 13, 2013. On October 14, 2013, we acquired or exclusively in-licensed the commercial and development rights to certain clinical and preclinical programs and intellectual property from CHOP and the University of Iowa Research Foundation, or UIRF, and in-licensed additional intellectual property from the University of Pennsylvania, or Penn. On October 15, 2013, we changed our name to Spark Therapeutics, LLC. On May 2, 2014, we converted from a Delaware limited liability company into a Delaware corporation, at which time we changed our name to Spark Therapeutics, Inc.

Our executive offices are located at 3737 Market Street, Suite 1300, Philadelphia, PA 19104 and our telephone number is (888) 772-7560. Our website address is http://www.sparktx.com. The information contained in, or accessible through, our website does not constitute part of this prospectus, and the inclusion of our website address in this prospectus is an inactive textual reference only.

In this prospectus, unless otherwise stated or the context otherwise requires:

| • | references to “Spark LLC” refer to Spark Therapeutics, LLC only (which was previously known as AAVenue Therapeutics, LLC); |

| • | references to “Spark Inc.” refer to Spark Therapeutics, Inc. only; |

| • | references to “Spark,” “we,” “us,” “our” and similar references refer to Spark Inc., together with Spark LLC; |

| • | references to the “corporate conversion” refer to all of the transactions related to the conversion of Spark LLC into Spark Inc., including the conversion of all of the outstanding membership interests of Spark LLC into shares of capital stock of Spark Inc.; |

| • | references to (i) common stock refer to the common stock of Spark Inc. or, as applicable, to the common units of Spark LLC and (ii) preferred stock refer to the preferred stock of Spark Inc. or, as applicable, to the preferred units of Spark LLC; |

| • | references to “Spark’s clinical trials” and similar references regarding clinical trials relating to our product candidates and the associated data (including the use of “we,” “us” and “our”) include the applicable rights to clinical and preclinical programs assigned or licensed to us by CHOP or the University of Iowa Research Foundation; |

- 6 -

Table of Contents

| • | references to “Spark’s intellectual property” and similar references regarding intellectual property relating to our product candidates (including the use of “we,” “us” and “our”) include the applicable rights to intellectual property assigned or licensed to us by CHOP, UIRF or Penn; and |

| • | references to “Spark’s manufacturing platform” and similar references regarding manufacturing of gene therapy product candidates (including the use of “we,” “us” and “our”) include the applicable know-how assigned or licensed to us by CHOP. |

“SPARK” and the Spark logo are trademarks of Spark Therapeutics, Inc. The other trademarks, trade names and service marks appearing in this prospectus are the property of their respective owners.

Implications of being an emerging growth company

As a company with less than $1 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and we may remain an emerging growth company until the end of the 2020 fiscal year. For so long as we remain an emerging growth company, we are permitted, and intend, to rely on exemptions from certain disclosure and other requirements that are applicable to other public companies that are not emerging growth companies. In particular, in this prospectus, we have not included all of the executive compensation-related information that would be required if we were not an emerging growth company. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold stock.

- 7 -

Table of Contents

The offering

| Common stock offered by |

shares. |

| Common stock to be outstanding after this offering |

shares. |

| Option to purchase additional shares |

The underwriters have an option for a period of 30 days to purchase up to additional shares of our common stock. |

| Use of proceeds |

We intend to use the net proceeds from this offering as follows: approximately $ to fund clinical development of and regulatory submissions and pre-commercial activities for SPK-RPE65; approximately $ to fund clinical development of SPK-CHM; approximately $ to fund research and clinical development of our SPK-FIX program; approximately $ to fund research to advance our pipeline of preclinical product candidates; and the remainder for working capital and other general corporate purposes, including in-licenses or potential acquisitions. See “Use of proceeds” for more information. |

| Risk factors |

You should read the “Risk factors” section of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

| Directed shares |

At our request, the underwriters have reserved for sale, at the initial public offering price, up to % of the shares offered hereby for employees, directors and other persons associated with us who have expressed an interest in purchasing common stock in the offering. See “Underwriting” for more information. |

| Proposed NASDAQ Global Market symbol |

“ONCE.” |

The number of shares of our common stock to be outstanding after this offering is based on the 31,451,610 shares of our common stock outstanding as of December 30, 2014, and the 50,604,324 shares of our common stock issuable upon the automatic conversion, upon the closing of this offering, of all outstanding shares of our preferred stock, including shares of preferred stock that are issuable as accrued dividends, assuming the closing of this offering occurred on December 30, 2014. The number of shares of common stock issuable upon the automatic conversion of the outstanding shares of our preferred stock will continue to increase after December 30, 2014 as a result of the issuance of additional shares of preferred stock accrued as stock dividends at a rate of 8% per annum. For each day occurring between December 30, 2014 and the closing of this offering, the number of shares of common stock issuable upon the automatic conversion of the outstanding shares of our preferred stock will increase by 11,000 shares.

The number of shares of our common stock to be outstanding after this offering excludes:

| • | 11,322,562 shares of common stock issuable upon exercise of stock options outstanding as of December 30, 2014 at a weighted-average exercise price of $0.90 per share; |

| • | 1,047,502 shares of common stock reserved as of December 30, 2014 for future issuance under our 2014 equity incentive plan; |

- 8 -

Table of Contents

| • | additional shares of common stock that will be available for future issuance, as of the closing of this offering, under our 2015 stock incentive plan; and |

| • | additional shares of common stock that will be available for future issuance, as of the closing of this offering, under our 2015 employee stock purchase plan. |

Unless otherwise indicated, this prospectus reflects and assumes the following:

| • | the conversion of all outstanding shares of our preferred stock into 50,604,324 shares of our common stock, which will occur automatically upon the closing of this offering, assuming the closing occurred on December 30, 2014; |

| • | no exercise of outstanding stock options described above; |

| • | the filing of our restated certificate of incorporation and the adoption of our amended and restated by-laws upon the closing of this offering; and |

| • | no exercise by the underwriters of their option to purchase additional shares. |

- 9 -

Table of Contents

Summary financial data

The following tables set forth, for the periods and at the dates indicated, our summary financial data. Historical results are not indicative of the results to be expected in the future and results of interim periods are not necessarily indicative of results for the entire year. You should read the following information together with the more detailed information contained in “Selected financial data,” “Management’s discussion and analysis of financial condition and results of operations” and our financial statements and the accompanying notes thereto appearing elsewhere in this prospectus.

| |

Period from March 13, 2013 (inception) to December 31, 2013 |

|

|

Period from March 13, 2013 (inception) to September 30, 2013 |

|

|

Nine months ended 2014 |

| ||||

| (unaudited) | ||||||||||||

| (in thousands, except share and per share amounts) | ||||||||||||

| Statements of Operations Data: |

||||||||||||

| Revenues |

$ | — | $ | — | $ | 20 | ||||||

| Operating expenses: |

||||||||||||

| Research and development |

4,897 | 2,968 | 10,169 | |||||||||

| Acquired in-process research and development |

50,000 | — | — | |||||||||

| General and administrative |

2,381 | 661 | 5,162 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total operating expenses |

57,278 | 3,629 | 15,331 | |||||||||

|

|

|

|

|

|

|

|||||||

| Loss from operations |

(57,278 | ) | (3,629 | ) | (15,311 | ) | ||||||

| Interest income |

— | — | 2 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net loss |

$ | (57,278 | ) | $ | (3,629 | ) | $ | (15,309 | ) | |||

|

|

|

|

|

|

|

|||||||

| Basic and diluted net loss per common share |

$ | (8.44 | ) | $ | (0.57 | ) | ||||||

|

|

|

|

|

|||||||||

| Weighted average basic and diluted common shares outstanding |

6,788,396 | 26,673,047 | ||||||||||

|

|

|

|

|

|||||||||

| Unaudited pro forma net loss |

$ | (57,278 | ) | $ | (15,309 | ) | ||||||

|

|

|

|

|

|||||||||

| Unaudited pro forma basic and diluted net loss per common share(1) |

$ | (7.05 | ) | $ | (0.29 | ) | ||||||

|

|

|

|

|

|||||||||

| Unaudited pro forma weighted average basic and diluted common shares outstanding(1) |

8,119,454 | 53,190,349 | ||||||||||

|

|

|

|

|

|||||||||

|

|

||||||||||||

| (1) | See Note 3(f) to our audited financial statements and Note 3(i) to our unaudited financial statements included elsewhere in this prospectus for an explanation of the method used to calculate unaudited pro forma net loss per common share and the unaudited pro forma weighted average basic and diluted common shares outstanding used to calculate the pro forma per common share amounts. |

- 10 -

Table of Contents

| As of September 30, 2014 | ||||||||||||

| Actual | Pro forma(1) | Pro forma as adjusted(2) |

||||||||||

| (unaudited) | ||||||||||||

| (in thousands) | ||||||||||||

| Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

$ | 67,273 | $ | 67,273 | $ | |||||||

| Working capital |

$ | 62,281 | $ | 62,281 | $ | |||||||

| Total assets |

$ | 80,914 | $ | 80,914 | $ | |||||||

| Total preferred stock |

$ | 82,437 | $ | — | $ | — | ||||||

| Total stockholders’ equity |

$ | 62,725 | $ | 62,725 | $ | |||||||

|

|

||||||||||||

| (1) | The pro forma balance sheet data give effect to the automatic conversion of all outstanding shares of our preferred stock into an aggregate of 50,604,324 shares of common stock upon the closing of this offering assuming the closing of this offering occurred on December 30, 2014. |

| (2) | The pro forma as adjusted balance sheet data give effect to our issuance and sale of shares of common stock in this offering (assuming no exercise by the underwriters of their option to purchase additional shares) at an assumed initial public offering price of $ per share, the midpoint of the price range listed on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

A $1.00 increase (decrease) in the assumed initial public offering price of $ per share, which is the midpoint of the range listed on the cover page of this prospectus, would increase (decrease) the pro forma as adjusted amount of each of cash and cash equivalents and working capital, total assets and total stockholders’ equity by approximately $ , assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us.

- 11 -

Table of Contents

Investing in our common stock involves a high degree of risk. Before investing in our common stock, you should consider carefully the risks described below, together with the other information contained in this prospectus, including our financial statements and the related notes appearing at the end of this prospectus. If any of the following risks occur, our business, financial condition, results of operations and prospects could be materially and adversely affected. In these circumstances, the market price of our common stock could decline, and you may lose all or part of your investment.

Risks related to our financial position

We have incurred net losses since inception. We expect to incur losses for the foreseeable future and may never achieve or maintain profitability.

Since inception, we have incurred net losses. Our net loss was $15.3 million for the nine months ended September 30, 2014. As of September 30, 2014, we had an accumulated deficit of $72.6 million. We historically have financed our operations primarily through private placements of our preferred stock. We have devoted substantially all of our efforts to research and development, including clinical and preclinical development of our product candidates, as well as to building out our team. We expect that it could be several years, if ever, before we have a commercialized product candidate. We expect to continue to incur significant expenses and increasing operating losses for the foreseeable future. The net losses we incur may fluctuate significantly from quarter to quarter. We anticipate that our expenses will increase substantially if, and as, we:

| • | continue our research and the preclinical and clinical development of our product candidates, including our ongoing pivotal Phase 3 clinical trial for SPK-RPE65 and our other planned clinical trials; |

| • | initiate additional clinical trials and preclinical studies for our other product candidates; |

| • | seek to identify additional product candidates; |

| • | prepare our BLA and marketing authorization application, or MAA, for SPK-RPE65 and seek marketing approvals for any of our other product candidates that successfully complete clinical trials; |

| • | validate a commercial-scale cGMP manufacturing facility; |

| • | further develop our gene therapy platform; |

| • | establish a sales, marketing and distribution infrastructure to commercialize any product candidates for which we may obtain marketing approval; |

| • | maintain, expand and protect our intellectual property portfolio; and |

| • | acquire or in-license other product candidates and technologies. |

To become and remain profitable, we must develop and eventually commercialize product candidates with significant market potential. This will require us to be successful in a range of challenging activities, including completing preclinical testing and clinical trials of our product candidates, obtaining marketing approval for these product candidates, manufacturing, marketing and selling those products for which we may obtain marketing approval and satisfying any post-marketing requirements. We may never succeed in any or all of these activities and, even if we do, we may never generate revenues that are significant or large enough to achieve profitability. If we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis. Our failure to become and remain profitable would decrease the value of our

- 12 -

Table of Contents

company and could impair our ability to raise capital, maintain our research and development efforts, expand our business or continue our operations. A decline in the value of our company also could cause you to lose all or part of your investment.

We have never generated revenue from product sales and may never be profitable.

Our ability to generate revenue from product sales and achieve profitability depends on our ability, alone or with collaborative partners, to successfully complete the development of, and obtain the regulatory approvals necessary to commercialize, our product candidates. We do not anticipate generating revenues from product sales for the next several years, if ever. Our ability to generate future revenues from product sales depends heavily on our, or our collaborators’, success in:

| • | completing research and preclinical and clinical development of our product candidates and identifying new gene therapy product candidates; |

| • | seeking and obtaining regulatory and marketing approvals for product candidates for which we complete clinical trials; |

| • | launching and commercializing product candidates for which we obtain regulatory and marketing approval by establishing a sales force, marketing and distribution infrastructure or, alternatively, collaborating with a commercialization partner; |

| • | qualifying for adequate coverage and reimbursement by government and third-party payors for our product candidates; |

| • | maintaining and enhancing a sustainable, scalable, reproducible and transferable manufacturing process for our vectors and product candidates; |

| • | establishing and maintaining supply and manufacturing relationships with third parties that can provide adequate, in both amount and quality, products and services to support clinical development and the market demand for our product candidates, if approved; |

| • | obtaining market acceptance of our product candidates as a viable treatment option; |

| • | addressing any competing technological and market developments; |

| • | implementing additional internal systems and infrastructure, as needed; |

| • | negotiating favorable terms in any collaboration, licensing or other arrangements into which we may enter and performing our obligations in such collaborations; |

| • | maintaining, protecting and expanding our portfolio of intellectual property rights, including patents, trade secrets and know-how; |

| • | avoiding and defending against third-party interference or infringement claims; and |

| • | attracting, hiring and retaining qualified personnel. |

Even if one or more of the product candidates that we develop is approved for commercial sale, we anticipate incurring significant costs associated with commercializing any approved product candidate. Our expenses could increase beyond expectations if we are required by FDA, EMA or other regulatory authorities to perform clinical and other studies in addition to those that we currently anticipate. Even if we are able to generate revenues from the sale of any approved products, we may not become profitable and may need to obtain additional funding to continue operations.

- 13 -

Table of Contents

Our limited operating history may make it difficult for you to evaluate the success of our business to date and to assess our future viability.

We are a development-stage company founded in March 2013. Our operations to date have been limited to organizing and staffing our company, business planning, raising capital, acquiring our technology, identifying potential product candidates and undertaking preclinical studies and clinical trials of our most advanced product candidates and establishing collaborations. We have not yet demonstrated the ability to complete Phase 3 trials of our product candidates, obtain marketing approvals, manufacture a commercial-scale product or conduct sales and marketing activities necessary for successful commercialization. Consequently, any predictions you make about our future success or viability may not be as accurate as they could be if we had a longer operating history.

In addition, as a new business, we may encounter unforeseen expenses, difficulties, complications, delays and other known and unknown factors. We will need to transition from a company with a research focus to a company that is also capable of supporting commercial activities. We may not be successful in such a transition.

Even if this offering is successful, we will need to raise additional funding, which may not be available on acceptable terms, or at all. Failure to obtain this necessary capital when needed may force us to delay, limit or terminate certain of our product development efforts or other operations.

We expect our expenses to increase in connection with our ongoing activities, particularly as we continue the research and development of, initiate further clinical trials of and seek marketing approval for, our product candidates. In addition, if we obtain marketing approval for any of our product candidates, we expect to incur significant expenses related to product sales, medical affairs, marketing, manufacturing and distribution. Furthermore, upon the closing of this offering, we expect to incur additional costs associated with operating as a public company. Accordingly, we will need to obtain substantial additional funding in connection with our continuing operations. If we are unable to raise capital when needed or on attractive terms, we would be forced to delay, reduce or eliminate certain of our research and development programs.

Our operations have consumed significant amounts of cash since inception. As of September 30, 2014, our cash and cash equivalents were $67.3 million. Our research and development expenses increased from $4.9 million for the period from March 31, 2013 (inception) to December 31, 2013 to $10.2 million for the nine months ended September 30, 2014. We estimate that the net proceeds from this offering will be approximately $ , based on the assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We expect that the net proceeds from this offering, together with our existing cash and cash equivalents, along with the $20.0 million upfront payment received under the Pfizer collaboration, will enable us to fund our operating expenses and capital expenditure requirements at least through . See “Use of proceeds.”

Our future capital requirements will depend on many factors, including:

| • | the results of our Phase 3 trial for SPK-RPE65, and whether additional clinical testing is required to secure regulatory approvals for all intended or desired indications; |

| • | the scope, progress, results and costs of drug discovery, laboratory testing, preclinical development and clinical trials for our other product candidates; |

| • | the costs, timing and outcome of regulatory review of our product candidates; |

| • | the costs of future activities, including product sales, medical affairs, marketing, manufacturing and distribution, for any of our product candidates for which we receive marketing approval; |

- 14 -

Table of Contents

| • | revenue, if any, received from commercial sale of our products, should any of our product candidates receive marketing approval; |

| • | the costs of preparing, filing and prosecuting patent applications, maintaining and enforcing our intellectual property rights and defending intellectual property-related claims; |

| • | our current collaboration agreements remaining in effect and our achievement of milestones under those agreements; |

| • | our ability to establish and maintain additional collaborations on favorable terms, if at all; and |

| • | the extent to which we acquire or in-license other product candidates and technologies. |

Identifying potential product candidates and conducting preclinical testing and clinical trials is a time-consuming, expensive and uncertain process that takes years to complete, and we may never generate the necessary data or results required to obtain marketing approval and achieve product sales. In addition, our product candidates, if approved, may not achieve commercial success. Our product revenues, if any, and any commercial milestones or royalty payments under our collaboration agreements, will be derived from or based on sales of products that may not be commercially available for many years, if at all. Accordingly, we will need to continue to rely on additional financing to achieve our business objectives. To the extent that additional capital is raised through the sale of equity or equity-linked securities, the issuance of those securities could result in substantial dilution for our current stockholders and the terms may include liquidation or other preferences that adversely affect the rights of our current stockholders. Furthermore, the issuance of additional securities, whether equity or debt, by us, or the possibility of such issuance, may cause the market price of our common stock to decline and existing stockholders may not agree with our financing plans or the terms of such financings. Adequate additional financing may not be available to us on acceptable terms, or at all.

Risks related to the development of our product candidates

Our gene therapy product candidates are based on a novel technology, which makes it difficult to predict the time and cost of development and of subsequently obtaining regulatory approval. At the moment, no gene therapy product has been approved in the United States and only one such product has been approved in the European Union.

We have concentrated our research and development efforts on our gene therapy platform, and our future success depends on our successful development of viable gene therapy product candidates. There can be no assurance that we will not experience problems or delays in developing new product candidates and that such problems or delays will not cause unanticipated costs, or that any such development problems can be solved. Although we intend to leverage our experience with SPK-RPE65, we may be unable to reduce development timelines and costs for our other IRD gene therapy development programs. We also may experience unanticipated problems or delays in expanding our manufacturing capacity, which may prevent us from completing our clinical trials, meeting the obligations of our collaborations or commercializing our products on a timely or profitable basis, if at all. For example, we, a collaborator or another group may uncover a previously unknown risk associated with AAV, and this may prolong the period of observation required for obtaining regulatory approval or may necessitate additional clinical testing.

In addition, the clinical trial requirements of FDA, EMA and other regulatory authorities and the criteria these regulators use to determine the safety and efficacy of a product candidate vary substantially according to the type, complexity, novelty and intended use and market of such product candidates. The regulatory approval process for novel product candidates such as ours can be more expensive and take longer than for other, better known or more extensively studied product candidates. Only one gene therapy product, uniQure N.V.’s Glybera,

- 15 -

Table of Contents

has received marketing authorization from the European Commission. It is difficult to determine how long it will take or how much it will cost to obtain regulatory approvals for our product candidates in either the United States or the European Union or how long it will take to commercialize our product candidates. Approvals by European Commission may not be indicative of what FDA may require for approval.

Regulatory requirements governing gene and cell therapy products have changed frequently and may continue to change in the future. FDA has established the Office of Cellular, Tissue and Gene Therapies within its Center for Biologics Evaluation and Research, or CBER, to consolidate the review of gene therapy and related products, and has established the Cellular, Tissue and Gene Therapies Advisory Committee to advise CBER in its review. Gene therapy clinical trials conducted at institutions that receive funding for recombinant DNA research from the United States National Institutes of Health, or NIH, also are potentially subject to review by the NIH Office of Biotechnology Activities’ Recombinant DNA Advisory Committee, or the RAC; however, NIH recently announced that the RAC will soon only publicly review clinical trials if the trials cannot be evaluated by standard oversight bodies and pose unusual risks. Although FDA decides whether individual gene therapy protocols may proceed, the RAC public review process, if undertaken, can delay the initiation of a clinical trial, even if FDA has reviewed the trial design and details and approved its initiation. Conversely, FDA can put an IND on a clinical hold even if the RAC has provided a favorable review or an exemption from in-depth, public review. If we were to engage an NIH-funded institution, such as CHOP, to conduct a clinical trial, that institution’s institutional biosafety committee as well as its institutional review board, or IRB, would need to review the proposed clinical trial to assess the safety of the trial. In addition, adverse developments in clinical trials of gene therapy products conducted by others may cause FDA or other oversight bodies to change the requirements for approval of any of our product candidates. Similarly, EMA may issue new guidelines concerning the development and marketing authorization for gene therapy medicinal products and require that we comply with these new guidelines.

These regulatory review committees and advisory groups and the new guidelines they promulgate may lengthen the regulatory review process, require us to perform additional studies, increase our development costs, lead to changes in regulatory positions and interpretations, delay or prevent approval and commercialization of these product candidates or lead to significant post-approval limitations or restrictions. As we advance our product candidates, we will be required to consult with these regulatory and advisory groups, and comply with applicable guidelines. If we fail to do so, we may be required to delay or discontinue development of certain of our product candidates. These additional processes may result in a review and approval process that is longer than we otherwise would have expected. Delay or failure to obtain, or unexpected costs in obtaining, the regulatory approval necessary to bring a potential product to market could decrease our ability to generate sufficient product revenue, and our business, financial condition, results of operations and prospects would be materially and adversely affected.

Because we are developing product candidates for the treatment of diseases in which there is little clinical experience and, in some cases, using new endpoints or methodologies, there is increased risk that FDA or other regulatory authorities may not consider the endpoints of our pivotal Phase 3 clinical trial to provide clinically meaningful results and that these results may be hard to analyze.

There are no pharmacologic therapies approved to treat the underlying causes of any IRD, including those caused by autosomal recessive mutations to the RPE65 gene or mutations to the CHM gene. In addition, there has been limited clinical trial experience for the development of pharmaceuticals to treat IRDs. Certain aspects of IRDs render efficacy endpoints historically used for vision clinical trials less applicable as clinical endpoints. As a result, the design and conduct of clinical trials for these disorders is subject to increased risk.

FDA described, in general terms, the criteria by which it will judge the validity of the primary efficacy endpoint we chose for our pivotal Phase 3 clinical trial of SPK-RPE65. FDA has communicated that guidance through comments on our request for a Special Protocol Assessment, or SPA, which was submitted in 2009, and during

- 16 -

Table of Contents

subsequent regulatory meetings. FDA stated that the primary endpoint should be clinically meaningful, reflecting a tangible benefit to patients. Further, FDA stated that, preferably, the benefit would improve quality of life, a standard that can be difficult to validate. We voluntarily withdrew our SPA submission at FDA’s request to allow FDA more time for a comprehensive assessment of the Phase 3 trial design. A subsequent Advisory Committee in June 2011 addressed a number of these elements. Although EMA’s only comment on the validity of the primary endpoint for our pivotal Phase 3 clinical trial was to use only the binocular testing condition, there can be no assurances that it may not have additional questions or comments on the primary endpoint in the future.

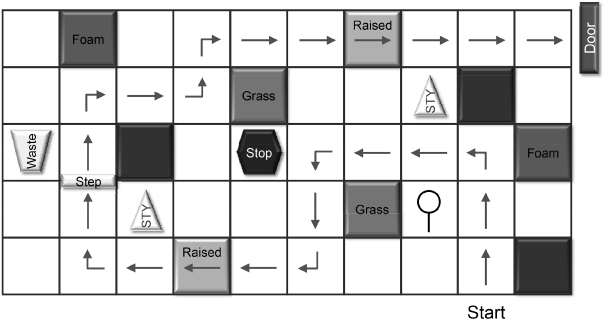

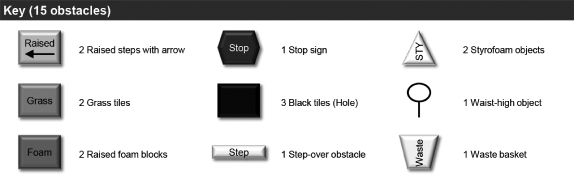

We developed a mobility test that measures subjects’ ability to navigate a specially designed course at incrementally reduced lighting conditions. The subjects follow black arrows on white tiles on the floor around the course, while avoiding common obstacles such as waste baskets. This mobility test is designed to measure improvements in peripheral vision and improvements in night blindness. These are two predominant visual deficits in patients with RPE65-mediated IRDs. The mobility test for our pivotal Phase 3 clinical trial of SPK-RPE65 uses seven decreasing increments of light designed to correspond to light conditions encountered during daily activities and in common environments, such as the interior of a shopping mall, the inside of a stairwell and an outdoor parking lot at night. We defined our primary efficacy endpoint as the ability to navigate the course accurately within a given timeframe, at one or more lighting levels lower than the level at which a subject previously had been able to complete the course.

At an FDA advisory committee meeting on gene therapy products for the treatment of retinal disorders convened by CBER in June 2011, we presented a summary of our clinical data to date, as well as our then-proposed Phase 3 trial design. In May 2012, reviewers from FDA, CBER and several ophthalmologists from FDA provided feedback on our proposed mobility test stating that improvement in the ability to navigate at a lower lighting condition may represent an improvement in visual function. FDA requested that we justify a change score on the endpoint that would reliably confer clinical benefit and power our trial accordingly. In the protocol for the Phase 3 trial submitted to FDA, we described in detail our primary endpoint based on a change score of positive one or more light levels. FDA allowed our clinical trial to proceed using that endpoint, even though FDA has authority to place a clinical trial on hold if the protocol for an investigation is “clearly deficient” in design to meet its stated objectives. FDA has discretion, however, to reserve judgment on whether the endpoint and the change scores seen in our trial sufficiently demonstrate clinical meaningfulness until FDA reviews our BLA. FDA has not communicated further with us its views about the clinical meaningfulness of the proposed change score. Consequently, FDA may decide that achieving a change score of positive one, as we have defined that score, is not clinically meaningful and, therefore, that meeting our primary endpoint does not demonstrate that SPK-RPE65 is effective.

Moreover, even if FDA does find our success criteria to be sufficiently validated and clinically meaningful, we may not achieve the pre-specified endpoint to a degree of statistical significance. Further, even if we do achieve the pre-specified criteria, we may produce results that are unpredictable or inconsistent with the results of the secondary efficacy endpoints in the trial. FDA also could give overriding weight to other efficacy endpoints over the mobility test endpoint, even if we achieve statistically significant results on the mobility test, if we do not achieve statistically significant or clinically meaningful results on any of our secondary efficacy endpoints. FDA also weighs the benefits of a product against its risks and FDA may view the efficacy results in the context of safety as not being supportive of regulatory approval. Other regulatory authorities in the European Union and other countries may make similar comments with respect to these endpoints.

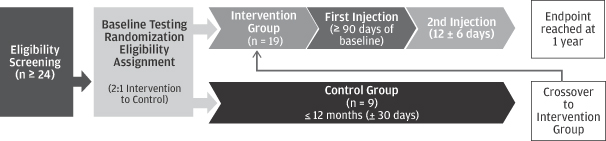

Additionally, for the Phase 3 trial, we enrolled subjects as young as four years of age (compared to subjects as young as eight years of age in our earlier Phase 1 trials). Even though both arms of the Phase 3 trial are balanced as to age, there is a risk that regulators may question whether subjects at this age could demonstrate

- 17 -

Table of Contents

improvement in the mobility trial as a result of their cognitive development, and not due to SPK-RPE65. The mobility test is not designed to detect the extent to which improvement is a result of cognitive development versus the impact of SPK-RPE65, therefore potentially calling into question efficacy results for younger age subjects.

Further, while certain of our secondary endpoints, such as measuring visual acuity, traditionally have been used in clinical settings, due to the unique deficits faced by subjects with IRDs, these traditional tests may not adequately assess patients’ ability to independently carry out activities of daily living. Moreover, quantifying pupillary responses to light, a traditionally qualitative evaluation, in patients with IRDs may be difficult or may yield unreliable quantitative results which could delay or prevent approval of SPK-RPE65, and could result in FDA or other regulatory authorities requiring us to conduct additional clinical trials.

In addition, the treatment of certain IRDs, such as CHM, may require assessment of clinical endpoints that reflect a stabilization, as opposed to an improvement, of functional vision. Assessing these endpoints may require longer periods of observation and may delay the completion of any trials we may undertake.

The results from our pivotal Phase 3 clinical trial for SPK-RPE65 may not support as broad a marketing approval as we seek and FDA and EMA may require us to conduct additional clinical trials, or evaluate subjects for an additional follow-up period.

While we believe SPK-RPE65 should be applicable for the treatment of patients with any IRD mediated by an RPE65 mutation, the results from our pivotal phase 3 clinical trial for SPK-RPE65, which included only subjects diagnosed with LCA due to RPE65 mutations, may not support as broad a marketing approval as we seek. Even if we obtain regulatory approval for SPK-RPE65, we might obtain marketing approval only to treat patients diagnosed with LCA due to RPE65 mutations, based on the inclusion criteria of the Phase 3 trial and the absence of data for patients diagnosed with RPE65-mediated IRDs other than LCA. If SPK-RPE65 is not approved for RPE65-mediated IRDs other than LCA, we may be required by FDA and EMA to conduct additional clinical trials to support approval of SPK-RPE65 for patients with patients diagnosed with RP due to RPE65 mutations or other RPE65-mediated IRDs. This could result in our experiencing substantial delays in obtaining, or never obtaining, marketing approval for SPK-RPE65 to treat patients diagnosed with RP due to RPE65 mutations or other RPE65-mediated IRDs. The inability to market SPK-RPE65 to treat patients with these other clinical classifications would have a material adverse effect on our projected revenues from SPK-RPE65 and our business, financial condition, results of operations and prospects.

Success in preclinical studies or early clinical trials may not be indicative of results obtained in later trials.

Results from preclinical studies or previous clinical trials are not necessarily predictive of future clinical trial results, and interim results of a clinical trial are not necessarily indicative of final results. Our product candidates may fail to show the desired safety and efficacy in clinical development despite demonstrating positive results in preclinical studies or having successfully advanced through initial clinical trials. For example, after multiple successful preclinical studies using gene therapy to treat hemophilia B, several hemophilia B product candidates, including product candidates we previously evaluated, have produced sub-optimal durability in Phase 1 trials.

We have no clinical data demonstrating either the safety or efficacy of SPK-CHM in humans. In addition, we have no clinical data demonstrating either the safety or efficacy of our current SPK-FIX product candidates in humans, as our current SPK-FIX product candidates are different than what was utilized in our prior Phase 1 hemophilia B trials. There can be no assurance that the success we achieved in the preclinical studies for SPK-CHM or for our current SPK-FIX product candidates ultimately will result in success in our planned clinical trials. In addition, we cannot assure you that we will be able to achieve the same or similar success in our preclinical studies and clinical trials of our other product candidates.

- 18 -

Table of Contents

There is a high failure rate for drugs and biologic products proceeding through clinical trials. Many companies in the pharmaceutical and biotechnology industries have suffered significant setbacks in late-stage clinical trials even after achieving promising results in preclinical testing and earlier-stage clinical trials. Data obtained from preclinical and clinical activities are subject to varying interpretations, which may delay, limit or prevent regulatory approval. In addition, we may experience regulatory delays or rejections as a result of many factors, including due to changes in regulatory policy during the period of our product candidate development. Any such delays could materially and adversely affect our business, financial condition, results of operations and prospects.

We may find it difficult to enroll patients in our clinical trials, which could delay or prevent us from proceeding with clinical trials of our product candidates.

Identifying and qualifying patients to participate in clinical trials of our product candidates is critical to our success. The timing of our clinical trials depends on our ability to recruit patients to participate as well as completion of required follow-up periods. For example, hemophilia trials often take longer to enroll than trials for other indications due to the availability of existing treatments. We have experienced slow enrollment in some of our hemophilia trials, and we may experience similar delays in any of our future clinical trials. If patients are unwilling to participate in our gene therapy studies because of negative publicity from adverse events related to the biotechnology or gene therapy fields, competitive clinical trials for similar patient populations, clinical trials in products employing our vectors or our platform or for other reasons, the timeline for recruiting patients, conducting studies and obtaining regulatory approval of our product candidates may be delayed. These delays could result in increased costs, delays in advancing our product candidates, delays in testing the effectiveness of our product candidates or termination of the clinical trials altogether.

We may not be able to identify, recruit and enroll a sufficient number of patients, or those with required or desired characteristics, to complete our clinical trials in a timely manner. Patient enrollment and trial completion is affected by factors including:

| • | size of the patient population and process for identifying subjects; |

| • | design of the trial protocol; |

| • | eligibility and exclusion criteria; |

| • | perceived risks and benefits of the product candidate under study; |

| • | perceived risks and benefits of gene therapy-based approaches to treatment of diseases; |

| • | availability of competing therapies and clinical trials; |

| • | severity of the disease under investigation; |

| • | availability of genetic testing for potential patients; |

| • | proximity and availability of clinical trial sites for prospective subjects; |

| • | ability to obtain and maintain subject consent; |

| • | risk that enrolled subjects will drop out before completion of the trial; |

| • | patient referral practices of physicians; and |

| • | ability to monitor subjects adequately during and after treatment. |

- 19 -

Table of Contents

Our current product candidates are being developed to treat rare conditions. We plan to seek initial marketing approval in the United States and the European Union. We may not be able to initiate or continue clinical trials if we cannot enroll a sufficient number of eligible patients to participate in the clinical trials required by FDA or EMA or other regulatory authorities. Our ability to successfully initiate, enroll and complete a clinical trial in any foreign country is subject to numerous risks unique to conducting business in foreign countries, including:

| • | difficulty in establishing or managing relationships with contract research organizations, or CROs, and physicians; |

| • | different standards for the conduct of clinical trials; |

| • | absence in some countries of established groups with sufficient regulatory expertise for review of gene therapy protocols; |

| • | our inability to locate qualified local consultants, physicians and partners; and |

| • | the potential burden of complying with a variety of foreign laws, medical standards and regulatory requirements, including the regulation of pharmaceutical and biotechnology products and treatment. |

If we have difficulty enrolling a sufficient number of patients to conduct our clinical trials as planned, we may need to delay, limit or terminate ongoing or planned clinical trials, any of which would have an adverse effect on our business, financial condition, results of operations and prospects.

We may encounter substantial delays in our clinical trials or we may fail to demonstrate safety and efficacy to the satisfaction of applicable regulatory authorities.

Before obtaining marketing approval from regulatory authorities for the sale of our product candidates, we must conduct extensive clinical trials to demonstrate the safety and efficacy of the product candidates. Clinical testing is expensive, time-consuming and uncertain as to outcome. We cannot guarantee that any clinical trials will be conducted as planned or completed on schedule, if at all. A failure of one or more clinical trials can occur at any stage of testing. Events that may prevent successful or timely completion of clinical development include:

| • | delays in reaching a consensus with regulatory authorities on trial design; |

| • | delays in reaching agreement on acceptable terms with prospective CROs and clinical trial sites; |

| • | delays in opening clinical trial sites or obtaining required IRB or independent Ethics Committee approval at each clinical trial site; |

| • | delays in recruiting suitable subjects to participate in our clinical trials; |

| • | imposition of a clinical hold by regulatory authorities as a result of a serious adverse event or after an inspection of our clinical trial operations or trial sites; |

| • | failure by us, any CROs we engage or any other third parties to adhere to clinical trial requirements; |

| • | failure to perform in accordance with FDA good clinical practices, or GCP, or applicable regulatory guidelines in the European Union and other countries; |

| • | delays in the testing, validation, manufacturing and delivery of our product candidates to the clinical sites, including delays by third parties with whom we have contracted to perform certain of those functions; |

| • | delays in having subjects complete participation in a trial or return for post-treatment follow-up; |

- 20 -

Table of Contents

| • | clinical trial sites or subjects dropping out of a trial; |

| • | selection of clinical endpoints that require prolonged periods of clinical observation or analysis of the resulting data; |

| • | occurrence of serious adverse events associated with the product candidate that are viewed to outweigh its potential benefits; |

| • | occurrence of serious adverse events in trials of the same class of agents conducted by other sponsors; or |

| • | changes in regulatory requirements and guidance that require amending or submitting new clinical protocols. |

Any inability to successfully complete preclinical and clinical development could result in additional costs to us or impair our ability to generate revenues from product sales, regulatory and commercialization milestones and royalties. In addition, if we make manufacturing or formulation changes to our product candidates, we may need to conduct additional studies to bridge our modified product candidates to earlier versions. Clinical trial delays also could shorten any periods during which we may have the exclusive right to commercialize our product candidates or allow our competitors to bring products to market before we do, which could impair our ability to successfully commercialize our product candidates and may harm our business, financial condition, results of operations and prospects.

Additionally, if the results of our clinical trials are inconclusive or if there are safety concerns or serious adverse events associated with our product candidates, we may:

| • | be delayed in obtaining marketing approval for our product candidates, if at all; |