Attached files

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

TABLE OF CONTENTS1

TABLE OF CONTENTS2

TABLE OF CONTENTS3

TABLE OF CONTENTS4

TABLE OF CONTENTS5

TABLE OF CONTENTS6

TABLE OF CONTENTS7

TABLE OF CONTENTS8

TABLE OF CONTENTS9

TABLE OF CONTENTS10

TABLE OF CONTENTS11

TABLE OF CONTENTS12

TABLE OF CONTENTS13

TABLE OF CONTENTS14

TABLE OF CONTENTS15

TABLE OF CONTENTS16

TABLE OF CONTENTS17

TABLE OF CONTENTS18

TABLE OF CONTENTS19

TABLE OF CONTENTS20

TABLE OF CONTENTS21

TABLE OF CONTENTS22

TABLE OF CONTENTS23

TABLE OF CONTENTS24

TABLE OF CONTENTS25

TABLE OF CONTENTS26

Contents

TABLE OF CONTENTS27

TABLE OF CONTENTS28

TABLE OF CONTENTS29

TABLE OF CONTENTS30

TABLE OF CONTENTS31

TABLE OF CONTENTS32

TABLE OF CONTENTS33

TABLE OF CONTENTS34

TABLE OF CONTENTS35

As filed with the Securities and Exchange Commission on December 23, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Sol-Wind Renewable Power, LP

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

4911 (Primary Standard Industrial Classification Code Number) |

47-1539702 (I.R.S. Employer Identification Number) |

405 Lexington Avenue

Suite 732

New York, New York 10174

(212) 235-0421

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

Scott L. Tonn

Chief Executive Officer

405 Lexington Avenue, Suite 732

New York, New York 10174

(212) 235-0421

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||||

Rod D. Miller, Esq. Brett D. Nadritch, Esq. Milbank, Tweed, Hadley & McCloy LLP One Chase Manhattan Plaza New York, New York 10005 (212) 530-5000 |

Sharon Mauer, Esq. General Counsel 405 Lexington Avenue, Suite 732 New York, New York 10174 (212) 235-0322 |

Mike Rosenwasser E. Ramey Layne Vinson & Elkins L.L.P. 666 Fifth Avenue, 26th Floor New York, New York 10103 (212) 237-0000 |

||

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee |

||

|---|---|---|---|---|

Common units representing limited partner interests |

$100,000,000 | $11,620 | ||

|

||||

- (1)

- Estimated

solely for the purpose of calculating the registration fee pursuant to Rule 457(o).

- (2)

- Includes common units issuable upon exercise of the underwriters' option to purchase additional common units.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

SUBJECT TO COMPLETION, DATED DECEMBER 23, 2014

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

Common Units

Representing Limited Partner Interests

Sol-Wind Renewable Power, LP

This is the initial public offering of our common units representing limited partner interests. No public market currently exists for our common units. We anticipate that the initial public offering price will be between $ and $ per common unit. We have applied to list our common units on the New York Stock Exchange under the symbol "SLWD."

We have granted the underwriters a 30-day option to purchase up to an additional common units at the public offering price less the underwriting discount. We refer to these additional common units as the "option units."

We are an "emerging growth company" as defined under the federal securities laws and, as such, intend to comply with certain reduced public company reporting requirements for future filings. See "Prospectus Summary—Implications of Being an Emerging Growth Company."

Investing in our common units involves risks. See "Risk Factors" beginning on page 27.

These risks include the following:

- •

- We may not have sufficient cash following the establishment of cash reserves and payment of fees and expenses, including

cost reimbursements to our general partner, to enable us to pay the minimum quarterly distribution to holders of our common and subordinated units.

- •

- The assumptions underlying the forecast of cash available for distribution that we include in "Cash Distribution Policy

and Restrictions on Distributions" are inherently uncertain and subject to significant business, economic, financial, regulatory and competitive uncertainties that could cause actual results to differ

materially from those forecasted.

- •

- The historical and unaudited pro forma combined financial information included in this prospectus does not reflect the

financial condition, results of operations or cash flows that we would have achieved as a stand-alone company during the periods presented or that we will achieve in the future and, therefore, may not

be a reliable indicator of our future performance.

- •

- Counterparties to the power purchase agreements for the assets in our Initial Portfolio and counterparties to our debt

investments may not fulfill their obligations, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

- •

- Affiliates of our general partner, including its members, have no duty to sell us or our general partner any renewable

energy assets that they may own or acquire in the future.

- •

- Initially, we will depend on the limited number of assets in our Initial Portfolio for almost all of our anticipated cash

flows.

- •

- The assets in our Initial Portfolio may not perform as we expect.

- •

- We operate in a highly competitive market for renewable energy assets. Future growth of our portfolio depends on our

general partner locating and acquiring additional operating solar and wind power generation assets at an attractive price.

- •

- We are highly dependent on our general partner, particularly for the provision of management and administration services

to our operations and assets.

- •

- Our U.S. federal income tax treatment depends on our status as a partnership for U.S. federal income tax purposes. If the

Internal Revenue Service were to treat us as a corporation for U.S. federal income tax purposes, subject to U.S. corporate income tax, our cash available for distribution to our unitholders may be

substantially reduced.

- •

- Our unitholders' share of our income is taxable to them for U.S. federal income tax purposes even if they do not receive

any cash distributions from us.

- •

- Common unitholders have very limited voting rights and, even if they are dissatisfied, they cannot remove our general partner without the consent of holders of the subordinated units.

|

||||

| |

Per Common Unit |

Total |

||

|---|---|---|---|---|

Public Offering Price |

$ | $ | ||

Underwriting Discounts and Commissions(1) |

$ | $ | ||

Proceeds to Sol-Wind Renewable Power, LP (before expenses) |

$ | $ | ||

|

||||

- (1)

- Excludes an aggregate structuring fee that is equal to % of the gross proceeds of this offering, or approximately $ . See "Underwriting." The structuring fee will be paid to UBS Securities LLC and Citigroup Global Markets Inc. from the proceeds of this offering. See "Use of Proceeds."

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the common units to purchasers on , 2015 through the book-entry facility of The Depository Trust Company.

| UBS Investment Bank | Citigroup |

The date of this prospectus is , 2015.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or in any free writing prospectus we may authorize to be delivered to you. Neither we nor the underwriters have authorized anyone to provide you with additional or different information. We are offering to sell, and seeking offers to buy, our common units only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of our common units.

This prospectus includes industry data and forecasts that we obtained from industry publications and surveys, public filings and internal company sources. Industry publications, surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy or completeness of the included information. While we are not aware of any misstatements regarding the market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings "Forward-Looking Statements" and "Risk Factors" in this prospectus.

i

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the historical and pro forma combined financial statements and the notes to those financial statements, before investing in our common units. Unless otherwise indicated, the information in this prospectus assumes (1) an initial public offering price of $ per common unit (the midpoint of the price range set forth on the cover page of this prospectus) and (2) that the underwriters do not exercise their right to purchase option units. You should read "Risk Factors" for information about important risks that you should consider before buying our common units.

References in this prospectus to "we," "us," "our", "the Partnership" or similar terms refer to Sol-Wind Renewable Power, LP and its subsidiaries and references to "our general partner" refer to Sol-Wind, LLC, the general partner of Sol-Wind Renewable Power, LP. We do not have any officers, directors or employees and we are managed by our general partner and its officers, directors and employees. Unless the context otherwise requires, references in this prospectus to "our directors," "our board," "our officers," "our management" or "our employees" refer to the directors, officers or employees, as applicable, of our general partner.

References in this prospectus to "$," "U.S. $" and "U.S. dollars" are to the lawful currency of the United States and references to "CAD$" and "Canadian dollars" are to the lawful currency of Canada. All dollar amounts herein are in U.S. dollars unless otherwise stated.

Unless otherwise noted, references to information being "pro forma" or "on a pro forma basis" mean such information is presented after giving effect to the Formation Transactions (as defined herein), this offering, the sale of the subordinated units and the anticipated use of proceeds therefrom, including the acquisition of our Initial Portfolio (as defined below). See "Selected Historical Financial Information," "Unaudited Pro Forma Combined Financial Information" and "—Formation Transactions and Partnership Structure."

Overview

We are a growth-oriented limited partnership formed to own, acquire, invest in and manage operating solar and wind power generation assets. These assets generate power for retail, municipal, utility and commercial customers under long-term power purchase agreements or similar contracts ("PPAs") that generate stable, long-term contracted cash flows. Our objective is to pay a consistent and growing cash distribution to our unitholders on a long-term basis. Upon completion of this offering, we will acquire from our general partner equity and debt interests in a diversified portfolio of 184.6 megawatts ("MW") of nameplate capacity, or maximum generating capacity, solar and wind power generation assets in the United States, Puerto Rico and Canada (the "Initial Portfolio"). We expect that our cash available for distribution for the twelve-month period ending December 31, 2015 will be approximately $ million, or $ per common unit, based on the midpoint of the price range set forth on the cover page of this prospectus.

We intend to take advantage of favorable trends in the energy industry, including the continued construction of renewable energy assets to supplement existing and aging energy infrastructure; demand for renewable energy required to meet U.S. state renewable portfolio standards ("RPS"); availability of U.S. and overseas government incentives and programs to support development of clean energy; the rapid growth in non-utility customer demand for attractively priced renewable energy generation at a commercial or residential customer's point of delivery, commonly known as "distributed generation;" improvements in solar and wind technological and operational efficiencies; and environmental concerns regarding conventional energy generation. We believe these favorable trends will contribute to significant growth in the renewable energy industry, particularly from regional and local developers of renewable energy projects that are not associated with large utilities or energy firms.

1

We are focused on acquiring assets from middle-market developers, which is an area where we see particularly compelling opportunities. We define "middle-market developers" as those developers who typically, in the case of solar assets, develop projects of between 100 kW and 5 MW in nameplate capacity and, in the case of wind assets, between 1 MW and 10 MW in nameplate capacity.

We have established and continue to grow and form new relationships with middle-market developers of high-quality, long-life assets with long-term contracts serving creditworthy counterparties, but whose ability to construct new generation facilities has historically been constrained by the inability to consistently raise capital. In contrast to some of our competitors, we are not a subsidiary of a large developer and therefore we believe we have greater flexibility in sourcing potential assets from a variety of developers and in choosing the right assets for our portfolio. In addition, we believe we will have a competitive advantage in sourcing acquisition and investment opportunities because of our master limited partnership ("MLP") structure. We believe our structure allows us to utilize low-cost capital in the form of tax equity without affecting our ability to maintain an attractive level of distributions. We intend to leverage these advantages in executing on acquisition and investment opportunities, which will ultimately enable us to grow our distributions.

At the closing of this offering, we will acquire the debt and equity interests in the Initial Portfolio from our general partner. Our partnership agreement (the "Partnership Agreement") requires our general partner to offer to sell us any other renewable energy assets that it may acquire in the future and thereafter seek to sell. In each case, the acquisition of the assets must comply with investment guidelines to be established by our general partner's board of directors or our decision whether to accept such offer will be subject to the approval of an independent committee of the board of directors. However, our general partner is not obligated to identify, acquire or sell us any assets in the future. At the time of this offering, our general partner has entered into multi-year agreements and other arrangements, including right of first refusal agreements, option agreements, memoranda of understanding and term sheets, with several experienced developers to acquire a diversified portfolio of solar power generation assets in construction or scheduled to commence construction, which we refer to as the "Identified Pipeline." Many of these arrangements provide our general partner with a period of exclusivity after completion of development to purchase the asset. In addition, for certain of the assets, tax equity investors have agreed to provide tax equity financing for the asset upon completion of development. Our general partner is targeting the acquisition of these assets over a period of three to 36 months after the completion of this offering. Our general partner has indicated its intent to sell us these assets in accordance with the Partnership Agreement. As a result of these acquisition opportunities and others we intend to pursue or expect to become available in the future, we believe we will be able to grow our business in a manner that will allow us to increase our cash distributions per unit over time.

Our Initial Portfolio

Our general partner has executed agreements to make equity and debt investments in operating solar and wind renewable energy assets owned by unaffiliated third parties. We refer to these assets as our "Initial Portfolio." Our general partner has agreed to sell us the equity investments in the Initial Portfolio pursuant to an initial portfolio purchase agreement (the "IPPA"), and each debt investment pursuant to an assignment and assumption agreement (collectively, the "A&As"). We refer to the IPPA and the A&As together as the "Acquisition Agreements."

In all cases where we have acquired an equity interest in an asset, we will own 100% of, or a managing or controlling interest in, the asset in the Initial Portfolio. The assets in our Initial Portfolio serve retail, municipal, utility and commercial customers under long-term PPAs, which, in the aggregate, had a weighted average remaining term of 18.8 years (based on nameplate capacity of 184.6 MW) as of December 19, 2014. The PPAs are long-term energy sale agreements or leases designed to provide a stable and predictable revenue stream. Generally, pursuant to the PPAs, the counterparty is required to pay a fixed price for energy produced, based on kilowatt hours ("kWh"), and is required to purchase

2

all energy produced by the asset. The PPAs also provide for transmission of electricity into the grid by the asset or net metering, a regulatory policy which allows owners of residential solar energy systems to interconnect their systems to the utility grid and receive credit for power their systems export to the grid, in the event that the counterparty under the PPAs is unable to accept delivery. The counterparties to the PPAs to which the assets are subject have a weighted average credit rating (based on nameplate capacity and calculated and derived by our management) of A3, as described in the table below.

We believe our Initial Portfolio will generate stable cash flows to fund long-term distributions to our unitholders. Our Initial Portfolio will include 130 individual solar assets, which includes one mobile solar generating asset that is expected to consist of 619 units, and 16 individual wind assets. These assets are located in several U.S. states and territories, including California, Massachusetts, Montana, New Jersey, Texas, Colorado and Puerto Rico, as well as Canada. The ongoing oversight of the assets in the Initial Portfolio and any other assets we acquire will be conducted by third-party asset managers pursuant to asset management agreements (each, an "Asset Management Agreement") and the ongoing operations and maintenance of the assets in the Initial Portfolio will continue to be conducted by the seller of the asset pursuant to operations and maintenance agreements (each, an "O&M Agreement"). The ongoing asset management and operations and maintenance of any assets in which we make exclusively a debt investment will be conducted by the owner of that asset.

3

The following table provides summary information for each of the assets in our Initial Portfolio as of December 19, 2014. All of the assets in our Initial Portfolio were constructed and have commenced operations within the past five years.

Project

|

Location | Number of Individual Assets |

Capacity MW(1) |

Counterparty to PPA |

Weighted Average Counterparty to PPA Credit Rating(2)(3) |

Weighted Average Remaining Length of PPAs(3) |

Interest(8)(9) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Solar |

||||||||||||||||||

Greenleaf TNX |

California | 20 | 13.3 | California Department of Corrections | A2 | 17.8 | 100% of all equity | |||||||||||

Greenleaf TNX |

California | 1 | 1.7 | Pacific Gas & Electric | Baa1 | 19.5 | 100% Class B | |||||||||||

Alamo I |

Texas | 1 | 49.5 | City of San Antonio Public Services | Aa1 | 24.0 | $52.5M credit facility | |||||||||||

Alamo II |

Texas | 1 | 5.4 | City of San Antonio Public Services | Aa1 | 24.2 | 100% Class B | |||||||||||

PRCC |

Puerto Rico | 1 | 5.6 | The Puerto Rico Convention Center District Authority | Caa2 | (4) | 19.2 | 100% Class B | ||||||||||

DC Solar |

California | 1 | (5) | 15.8 | KMH Systems, Ahern Rentals | B1 | (6) | 9.6 | 100% Class B | |||||||||

SunRay Power |

Massachusetts, New Jersey | 83 | 34.0 | Extra Space Storage, Siemens, Washington Township (NJ) | A3 | (7) | 17.4 | 100% of all equity | ||||||||||

Leicester |

Massachusetts | 2 | 6.0 | Town of Westborough MA | Aa2 | 19.9 | 100% of all equity | |||||||||||

Palmer |

Massachusetts | 3 | 4.2 | Wyman-Gordon Forging | B1 | (6) | 9.3 | 100% Class B | ||||||||||

Cleave Energy Holdings |

Ontario, Canada | 13 | 2.9 | Ontario Power Authority | Aa2 | 19.0 | CAD$23.0M credit facility | |||||||||||

Ecoplexus |

California, Colorado | 4 | 6.4 | Pacific Gas & Electric, Mesa County Housing Authority, Colorado Department of Corrections | A1 | 19.4 | 100% Class B | |||||||||||

Wind |

||||||||||||||||||

Foundation Windpower |

California, Montana | 16 | 39.8 | (10) | Anheuser Busch, Walmart, City of Soledad (CA) | Baa1 | 17.7 | 100% Class B | ||||||||||

| | | | | | | | | | | | | | | | | | | |

|

146 | 184.6 | ||||||||||||||||

- (1)

- Capacity

represents the nameplate capacity of an asset. Upon completion of this offering, we will acquire controlling interests in 132.2 MW of

nameplate capacity, and third-party debt investments with respect to 52.4 MW of nameplate capacity.

- (2)

- Credit

rating was derived by our management and calculated on a weighted average basis (weighted by nameplate capacity) by using the rating assigned to the

counterparty of the PPA for each asset by Moody's Investors Service, Inc. ("Moody's"), Standard & Poor's Financial Services LLC ("S&P") or Fitch Ratings Inc. ("Fitch"), if one was available. If no

rating was available for a counterparty, a below investment grade rating of B1 (Moody's format) was assumed unless the counterparty was deemed investment grade by our management based on the

experience of management and the credit metrics of the counterparties to the PPAs and their tenants, in which case a low investment grade rating of Baa3 (Moody's format) was used for the counterparty.

Approximately 30% of the counterparty credit ratings in the portfolio (based on weighted average nameplate capacity) were derived using internal management estimates where public ratings were not

available.

- (3)

- Weighted

average is calculated based on nameplate capacity of the assets.

- (4)

- Credit

rating is for the general obligation bonds of Puerto Rico. The convention center is owned by a government agency of Puerto Rico.

- (5)

- Upon

completion of this offering, we expect this asset to consist of 619 mobile solar generation units consisting of truck-towable trailer-mounted

solar photovoltaic panels, batteries and inverters. KMH Systems is expected to lease 300 mobile solar generation units. Ahern Rentals currently leases 319 mobile solar generation units.

- (6)

- Counterparty

assumed to have a credit rating of B1.

- (7)

- Investment

grade counterparties are parties to PPAs for approximately 25.21% of the generation capacity of these assets (including 12.91% of which is from

counterparties that are not rated but for which an investment grade rating is assumed). The remainder of the counterparties are assumed to have a B1 credit rating.

- (8)

- For

projects in which we will acquire Class B membership interests, the Class A membership interests will be owned by a tax equity investor.

See "Business—Our Initial Portfolio" for a description of the rights of and allocation to the Class A and Class B members and other tax equity investors in respect of cash

distributions.

- (9)

- For

a description of our debt investments in Alamo I and Cleave Energy Holdings, see "Business—Our Initial

Portfolio."

- (10)

- Reflects contracted capacity. Nameplate capacity is 2 MW higher.

4

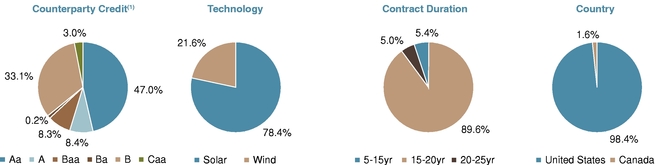

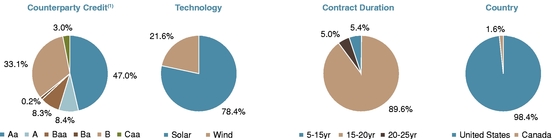

The following charts provide an overview of characteristics of our Initial Portfolio by counterparty credit rating, contract duration, technology and region, in each case based on nameplate capacity:

- (1)

- Approximately 30% of the counterparty credit ratings in the portfolio (based on weighted average nameplate capacity) were derived using internal management estimates where public ratings were not available.

Identified Pipeline

Following completion of this offering, we will continue to focus on investing in and acquiring assets with attributes similar to those in our Initial Portfolio: high-quality, long-life assets that have commenced or are nearly ready to commence commercial operations and which are subject to long-term PPAs with creditworthy counterparties. We also intend to expand and diversify our investment base into other geographic areas, within the U.S. and outside the U.S. in countries with low political risk and well-established legal systems, including Canada, Japan, Mexico and the United Kingdom. The terms of the Partnership Agreement require our general partner to offer to sell us any other renewable energy assets that it may acquire in the future and thereafter seek to sell. In each case, the acquisition of the assets must comply with investment guidelines to be established by our general partner's board of directors or our decision whether to accept such offer will be subject to the approval of an independent committee of the board of directors.

At the time of this offering, our general partner has entered into agreements and other arrangements, including term sheets, memoranda of understanding, rights of first refusal agreements and option agreements, to acquire the Identified Pipeline. In addition, tax equity investors have agreed to provide tax equity financing for certain of the assets in the Identified Pipeline upon completion of development. Our general partner is targeting the acquisition of these assets over a period of three to 36 months after the completion of this offering. The acquisition of the Identified Pipeline by our general partner is subject to negotiation of definitive agreements, due diligence, internal credit committee approval, other closing conditions and our general partner's ability to secure the funds necessary to consummate the acquisitions. The agreements and arrangements are for assets that are expected to represent approximately 1,098.6 MW of solar power generation assets located in the United States, Japan, Mexico, Puerto Rico and the United Kingdom. Our general partner has indicated its intent to offer to sell us these assets in accordance with the Partnership Agreement, subject to negotiations with us and certain time limits.

The following table provides summary information for each of the assets contemplated to be included in the Identified Pipeline as of December 19, 2014, all of which are solar assets. While the Identified Pipeline currently comprises solar assets only, we will continue to selectively review and

5

pursue wind projects in relevant geographies, where the combination of high-quality, long-life assets with long-term contracts serving creditworthy counterparties is present.

Developer

|

Type | Tax Equity Investor |

Location | Size (MW)(1) |

Number of Projects |

Weighted Average Credit Rating |

Completion of Development/Expected Completion of Development |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Developer #1 |

Term Sheet | Yes | United States | 41.0 | 13 | A2 | Q1/2015—Q1/2016 | ||||||||

Developer #2(2) |

Term Sheet | Yes | United States | 1.9 | 1 | Baa1 | Q1/2015 | ||||||||

Developer #2(2) |

ROFR | No | Japan | 300.6 | 9 | Baa1 | Q2/2015—Q4/2017 | ||||||||

Developer #3 |

MOU | Yes | United States | 26.7 | 1 | Aaa | Q2/2015—Q3/2015 | ||||||||

Developer #3 |

MOU | No | United Kingdom | 19.0 | 1 | Baa1 | Q2/2015 | ||||||||

Developer #3 |

MOU | No | Mexico | 30.0 | 1 | Baa1 | Q3/2015 | ||||||||

Developer #4(2) |

Term Sheet | Yes | United States | 14.0 | 1 | No Rating | Q4/2015 | ||||||||

Developer #4(2) |

ROFR | No | United Kingdom | 76.5 | 20 | Baa1 | Q1/2015 | ||||||||

Developer #4(2) |

ROFR | No | United Kingdom | 194.0 | 26 | Baa1 | Q4/2015 | ||||||||

Developer #4(2) |

ROFR | Yes | United States | 350.0 | 8 | Baa1 | Q4/2015 | ||||||||

Developer #5 |

Option Agreement | Yes | United States | 11.6 | Residential | No Rating | Q3/2015 | ||||||||

Developer #6 |

Term Sheet | Yes | United States | 2.1 | 8 | No Rating | Q2/2015 | ||||||||

Developer #7 |

Option Agreement | Yes | Puerto Rico | 27.0 | 1 | Caa1 | Completed | ||||||||

Developer #8 |

Option Agreement | Yes | United States | 4.2 | 1 | Aa3 | Q1/2015 | ||||||||

|

1,098.6 |

91(3) |

|||||||||||||

- (1)

- Capacity represents the nameplate capacity of an asset.

- (2)

- Developer is also a developer of assets in our Initial Portfolio.

- (3)

- Excludes residential projects.

Industry Overview

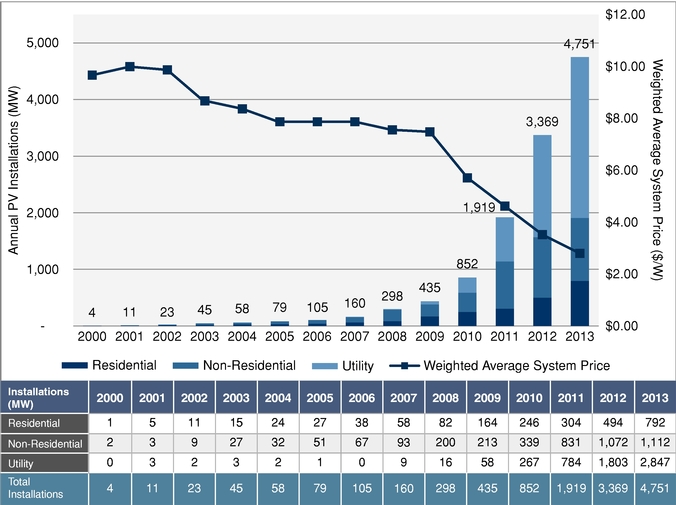

The electrical power generation and transmission industry is one of the largest sectors of the U.S. economy. According to the U.S. Energy Information Administration Annual Energy Outlook of 2014, the U.S. had a total operating power generating capacity of approximately 1,031 gigawatts ("GW") (including combined heat and power) as of December 2013, which was comprised of a diverse mix of fuel types, including 166 GW of renewable capacity (including 88 GW of non-hydroelectric renewable capacity), 95 GW of nuclear capacity, 298 GW of coal-fired capacity, 92 GW of oil and natural gas (steam) capacity and 218 GW of combined cycle capacity. U.S. renewable capacity continues to grow, and according to an early estimate by the American Council on Renewable Energy, is currently estimated to exceed 190 GW by the end of 2014. Renewable energy now provides a significant and increasing percentage of U.S. electricity generation capacity, accounting for nearly 40% of all new domestic power capacity installed in 2013.

The increase in scale, efficiency and technological innovation has resulted in renewable energy becoming increasingly cost competitive with conventional energy sources, and costs continue to fall. This dynamic of growth and innovation has attracted investment capital to the renewable energy sector. According to Bloomberg New Energy Finance, new investment in the renewable energy sector surpassed $250 billion in 2012 and 2013.

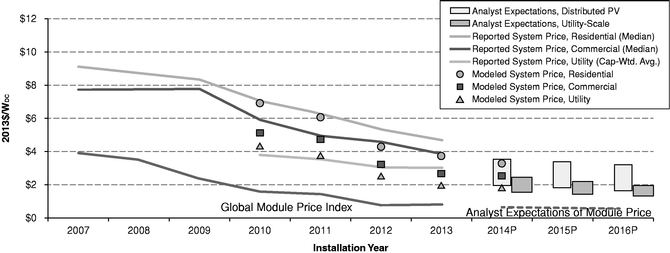

Due to the combination of rapidly decreasing costs and government incentives and regulations, there has been a significant increase in consumer preference for renewable energy. For instance, the price of solar energy has decreased significantly and we believe it will continue to decline, making it increasingly cost-competitive with other sources. On a global basis, from 2010 to 2020, the International Energy Agency ("IEA") expects the average total installation cost of solar photovoltaic ("PV") projects to decline by more than 50%. In 2010, the average installation cost per watt of capacity was $4.01 and fell to $2.01 by 2013.

U.S. federal, state and local governments and utilities have established various incentives to support the development of a cost competitive and self-sustaining renewable energy industry. These incentives include accelerated tax depreciation, production tax credits ("PTCs"), investment tax credits ("ITCs"), solar renewable energy credits and other renewable energy credits, (collectively "RECs") and RPS programs. The availability of these incentives provides the developers and owners of renewable

6

energy assets with the opportunity to raise capital through the sale of tax equity. "Tax equity" is a term that is used to describe a cash investment in exchange for the tax benefits, including ITCs and depreciation, generated by a U.S. solar and wind power generation asset and generally a small amount of cash flows from the asset.

In addition to the United States, the renewable energy sector continues to grow globally. For example, Canada, Japan and the United Kingdom are all experiencing growth and we believe provide investment opportunities for us. In 2012, total electricity generation capacity in Canada reached 134 GW and is expected to grow to 164 GW in 2035, according to the National Energy Board of Canada. Driven by government support for renewable energy at both federal and provincial levels, cumulative installed solar PV capacity in Canada grew 58% from 2012 to 2013 alone, with nearly 930 MW of capacity added since 2010. The Canadian Solar Industries Association estimates that total installed PV capacity could reach from 9 GW to 16 GW by 2025. In Canada, 2013 saw a record 1.6 GW of newly installed wind generation capacity, an increase of more than 70% from 2012, for a total of 7.8 GW. This represented the fifth-highest amount of new installed capacity in the world for 2013. In 2013, Japan ranked second in the world in new solar PV installation with 7 GW built, nearly double the new PV built in the U.S. that year. The IEA Medium-Term Renewable Energy Market Report estimates that Japan will reach 50 GW of solar PV installed capacity by 2020, on par with Germany and larger than the United States, which is expected to build out 40 GW of solar PV installed capacity by 2020. See "Industry Overview" for a discussion on these and other international markets which we are targeting.

We believe that the factors discussed above, including increasing demand, decreasing equipment costs and various government incentives, suggest the renewable energy sector will continue to grow at a rate faster than traditional fossil fuel and nuclear generation creating investment opportunities for us.

Our Business Strategy

Our primary business objective is to pay a consistent and growing cash distribution to our common unitholders on a long-term basis by owning, acquiring, investing in and managing operating solar and wind power generation assets. We intend to execute this objective with the following business strategy:

Focus on acquiring and investing in long-term contracted renewable energy assets. We intend to focus on acquiring and investing in operating solar and wind power generation assets that are subject to long-term PPAs with creditworthy counterparties that utilize proven technologies, exhibit low operating costs and deliver stable cash flows consistent with our Initial Portfolio. The weighted average remaining term of the PPAs for the assets in our Initial Portfolio is 18.8 years based on nameplate capacity as of December 19, 2014. In addition, we believe that newly constructed renewable energy assets generally have a useful life longer than the term of their initial PPAs and therefore will continue to generate cash flows after the expiration of these agreements. All of the assets in our Initial Portfolio were constructed and have commenced operations within the past five years.

Focus on acquiring and investing in operating assets from experienced middle-market developers. We believe our ability to provide middle-market developers access to a consistent source of capital which was previously unavailable to them will enable us to strategically source renewable energy assets. We are able to provide these developers with the ability to monetize operating assets and execute on development initiatives in their local markets. We have established relationships with a growing number of middle-market developers who develop high-quality, long-life assets with long-term contracts serving creditworthy counterparties, but whose growth has historically been constrained by the inability to consistently raise capital. We believe that our relationships with middle-market developers will enable us to source newly-constructed, long-life and low operating cost assets for our pipeline, which will ultimately enable us to grow our distributions. We intend to strengthen and form new relationships with these developers. Our goal is to enter into additional long-term agreements with these developers, as we believe they view us as a strategic partner and source of liquidity, rather than a competitor.

7

Leverage strategic relationships with tax equity investors. U.S. federal, state and local governments and utilities have established various tax incentives to support the development of renewable energy assets, which permits for the sale of tax equity. The incentives include PTCs, ITCs, accelerated tax depreciation and certain state tax credits (collectively, "Tax Benefits"). Investors in tax equity typically receive all or virtually all of the Tax Benefits, including PTCs, ITCs and depreciation, from U.S. solar and wind power generation assets and a small amount of cash flows from each asset. Traditionally, this form of financing provides in excess of one-third of the capital necessary to acquire such asset. We intend to leverage relationships with providers of tax equity to obtain low-cost financing and thereby lower our cost of acquisitions. For example, we have a commercial relationship with G-I Energy Investments LLC ("G-I"), which has board members in common with 40 North and has provided tax equity financing for a number of the projects in our Initial Portfolio and has also provided or agreed to provide tax equity financing for certain projects in the Identified Pipeline. We regularly consult with G-I with respect to financial and tax structuring of potential acquisitions and G-I consults with us with respect to operational and technical matters relating to projects for which G-I may provide tax equity financing. We believe this commercial experience and relationship will continue to facilitate our ability to identify, assess and finance future acquisitions. Moreover, our ability to leverage relationships with tax equity investors, like G-I, to utilize this form of financing enables us to reduce our cost of capital on U.S. assets we intend to acquire.

Focus on pursuing opportunities in other high-value geographic markets. In addition to maintaining a core focus on the U.S. renewable energy market, we intend to expand and diversify our current portfolio into other countries with low political risk and well-established legal systems that are supportive of renewable energy growth, including Canada, Japan, the United Kingdom, Puerto Rico and Mexico. For acquisitions in high-value geographic markets outside of the United States, we will continue to focus on investing in and acquiring assets with attributes similar to those in our Initial Portfolio: high-quality, long-life operating assets which are subject to long-term PPAs with creditworthy counterparties.

Maintain sound financial practices and flexibility. Upon consummation of this offering, we will have no third-party project-level debt financings on the energy assets in our Initial Portfolio. We believe this lack of project-level indebtedness both eliminates the risks associated with highly-levered assets, such as risks of default or foreclosure, increases our financial flexibility for growth investments and increases the cash available for distribution to unitholders because there is no debt service associated with such assets. We believe our stable cash flow profile, the long-term nature of the PPAs for the assets in our Initial Portfolio, the availability of $ million under the revolving credit facility that will enter into in connection with this offering (the "New Revolver") and our ability to raise equity and debt capital to finance growth, provide us with flexibility to optimize our capital structure and distributions to our unitholders. Although in the future we may incur debt at the project or holding company level, we intend to maintain a commitment to disciplined financial analysis and a balanced capital structure while evaluating opportunities to finance current assets in our Initial Portfolio and future acquisitions, with the goal of increasing cash distributions to unitholders over the long-term.

Our Competitive Strengths

We believe our solar and wind power generation assets and investments will generate high-quality, stable cash flows derived from long-term PPAs with creditworthy counterparties. Upon completion of this offering, we believe we will be well positioned to execute our business strategy successfully due to the following competitive strengths:

Stable, high-quality cash flows. Upon completion of this offering, the revenues generated by investments in our Initial Portfolio will be derived from a diversified portfolio of projects comprising 146 assets that sell their power pursuant to long-term PPAs. These PPAs, in the aggregate, had a weighted average remaining term of 18.8 years based on nameplate capacity as of December 19, 2014.

8

The counterparties under these PPAs have a weighted average credit rating (based on nameplate capacity and calculated and derived by our management) of A3, as described in "Business—Our Initial Portfolio." Generally, the counterparties to the PPAs have agreed to purchase all energy produced by the asset, subject to certain exceptions. We believe that the average life of the PPAs, coupled with the requirement of the counterparties to these PPAs to purchase all of the output of each asset, is a significant indicator of our ability to support our forecasted cash available for distribution. Additionally, our Identified Pipeline includes assets that are expected to represent approximately 1,098.6 MW of solar power generation assets located in the United States, Puerto Rico, Japan, Mexico and the United Kingdom.

Growing independent developer network in the renewable energy industry, unencumbered by legacy assets. We have established strong relationships with developers of renewable energy assets, which exposes us to a broad and diversified pool of primarily middle-market solar and wind power generation assets for our Initial Portfolio and for future acquisitions. In contrast to some of our competitors, we are not a subsidiary of a large developer and therefore we believe we have greater flexibility in sourcing potential assets from a variety of developers and in choosing the right assets for our portfolio. In addition, we will not undertake development activities which can put us into competition with the developers with whom we seek to form and grow relationships.

Access to low cost of capital. We believe we have a competitive advantage in sourcing acquisition and investment opportunities in the renewable energy space as a result of our structure and our general partner's relationship with tax equity investors, which provides access to financing in the form of tax equity. G-I has provided tax equity financing for a portion of the assets in our Initial Portfolio. G-I has also provided or agreed to provide tax equity financing for certain assets in the Identified Pipeline. Our access to tax equity financing, including from G-I and other tax equity investors, provides us with a source of comparatively low-cost capital to fund a portion of the purchase price of acquisitions. In addition, like other master limited partnerships ("MLPs"), we believe the fact that we will generally have little or no income tax liability will allow us to distribute to our unitholders a substantial portion of the cash generated from our operations and issue equity on a cost-effective basis to finance our growth.

High-quality, long-lived solar and wind power generation assets with low operating and capital requirements. Our Initial Portfolio will consist of assets that were constructed and have commenced operations within the past five years. These assets are comprised of proven and reliable technologies with warranties provided by original equipment manufacturers ("OEMs"), including Yingli, Trina and Hanwha, in the case of the solar assets, and General Electric and Mitsubishi, in the case of the wind assets. As a result, we expect to achieve high levels of operating performance with low maintenance-related capital expenditures.

Tax-efficient structure. We believe that our structure as an MLP provides us with greater financial flexibility over other organizational structures and investment platforms. In order to qualify as an MLP, at least 90% of the partnership's income must be "qualified income," which is defined in the Internal Revenue Code. In our structure, we convert income from solar and wind projects which does not constitute qualified income into dividend and interest income which is qualified income and thus we are taxed as a partnership. As an MLP, we can monetize a substantial amount of the Tax Benefits generated by our assets through the sale of tax equity, while at the same time substantially maintaining a single level of taxation because we do not expect our corporate subsidiaries to generate a significant amount of taxable income for at least the next 30 years. This allows us to utilize low-cost capital on a pre-tax basis provided by tax equity without affecting our ability to maintain an attractive level of distributions. Moreover, our MLP structure provides us additional benefits with respect to the acquisition of non-U.S. assets where non-U.S tax rates are often lower than U.S. income tax rates.

9

Asset and geographic diversification. We believe that our Initial Portfolio consists of diversified assets using proven technologies across different geographies. For example, the solar assets in our Initial Portfolio comprise both utility grid-connected and distributed generation assets, including mobile and stationary distributed generation assets. We believe that this diversification in asset type combined with an Initial Portfolio and Identified Pipeline which do not place excessive reliance on any single project or counterparty serves to minimize concentration risk associated with a disruption to a particular asset. As of December 19, 2014, excluding our debt investments, no single project accounts for more than approximately 5.3% of our estimated cash available for distribution. Additionally, the assets in our Initial Portfolio and Identified Pipeline are located across North America and mature renewable energy markets including Europe and Asia. We believe that a geographically diverse portfolio tends to reduce the magnitude of individual project or regional deviations from historical resource conditions, providing a more stable stream of cash flows over the long term than a less diversified portfolio.

An investment in our common units involves risks associated with our business, regulatory and legal matters, limited partnership structure and the tax characteristics of our common units. This is not a comprehensive list of risks to which we are subject, and you should carefully consider the risks described in "Risk Factors" and the other information in this prospectus before deciding whether to invest in our common units.

- •

- We may not have sufficient cash following the establishment of cash reserves and payment of fees and expenses, including

cost reimbursements to our general partner, to enable us to pay the minimum quarterly distribution to holders of our common and subordinated units.

- •

- The assumptions underlying the forecast of cash available for distribution that we include in "Cash Distribution Policy

and Restrictions on Distributions" are inherently uncertain and subject to significant business, economic, financial, regulatory and competitive uncertainties that could cause actual results to differ

materially from those forecasted.

- •

- The historical and unaudited pro forma combined financial information included in this prospectus does not reflect the

financial condition, results of operations or cash flows that we would have achieved as a stand-alone company during the periods presented or that we will achieve in the future and, therefore, may not

be a reliable indicator of our future performance.

- •

- Counterparties to the PPAs for the assets in our Initial Portfolio and counterparties to our debt investments may not

fulfill their obligations, which could have a material adverse effect on our business, financial condition, results of operations and cash flows.

- •

- Affiliates of our general partner, including its members, have no duty to sell us or our general partner any renewable

energy assets that they may own or acquire in the future.

- •

- Initially, we will depend on the limited number of assets in our Initial Portfolio for almost all of our anticipated cash

flows.

- •

- The assets in our Initial Portfolio may not perform as we expect.

- •

- We operate in a highly competitive market for renewable energy assets. Future growth of our portfolio depends on our

general partner locating and acquiring additional operating solar and wind power generation assets at an attractive price.

- •

- We are highly dependent on our general partner, particularly for the provision of management and administration services

to our operations and assets.

- •

- We expect to be dependent on tax equity financing arrangements.

10

- •

- The share of cash distributions we receive from projects with tax equity investors will fluctuate over time, and

accordingly, we will need to continue to acquire new projects in order to maintain and grow distributions to our unitholders.

- •

- Our U.S. federal income tax treatment depends on our status as a partnership for U.S. federal income tax purposes. If the

Internal Revenue Service (the "IRS") were to treat us as a corporation for U.S. federal income tax purposes, subject to U.S. corporate income tax, our cash available for distribution to our

unitholders may be substantially reduced. See "Material U.S. Federal Income Tax Consequences" for further information on our tax status.

- •

- Our unitholders' share of our income is taxable to them for U.S. federal income tax purposes even if they do not receive

any cash distributions from us.

- •

- Common unitholders have very limited voting rights and, even if they are dissatisfied, they cannot remove our general partner without the consent of holders of the subordinated units.

Formation Transactions and Partnership Structure

General

We were formed by Sol-Wind, LLC as a Delaware limited partnership in August 2014. Prior to the closing of this offering, we will not own any solar or wind power generation assets, but our general partner will own or have the right to purchase equity or debt interests in the entities that own the assets in our Initial Portfolio. Our general partner has agreed to sell us all of its interests in the Initial Portfolio. At or prior to the closing of this offering, the following transactions will occur:

- •

- we will issue to 40 North Investments LP, a member of our general partner ("40 North"), or one of its

affiliates all of our subordinated units in exchange for cash at a price per unit equal to the price of common units in this offering, representing a combined % of the limited partner

interests in us;

- •

- we will issue our general partner or

40 North common units at a price per common unit equal to the

price of the common units in this offering;

- •

- we will issue to our general partner the incentive distribution rights, which entitle our general partner to an

increasing percentage, up to 50%, of cash we distribute in excess of $ per unit per quarter;

- •

- we will issue common units to the public, representing % of

the limited partner interests

in us;

- •

- we will enter into (a) the Acquisition Agreements with our general partner, pursuant to which we will acquire the

equity and debt interests in the Initial Portfolio described under "—The Initial Portfolio" from our general partner and (b) the Partnership Agreement with our general partner that

will, among other things, govern the (i) management and administrative services to be provided by our general partner and its affiliates to us and the corresponding fees and expense

reimbursements we will pay to our general partner and its affiliates for and in connection with those services and (ii) indemnification obligations between our general partner and us for

liabilities and the operation of our assets;

- •

- we will use the net proceeds from this offering and the sale of the subordinated units for the purposes set forth in "Use

of Proceeds," including to pay for the acquisition of the interests in our Initial Portfolio from our general partner; and

- •

- one of our subsidiaries will enter into the New Revolver.

To the extent the underwriters exercise their right to purchase the option units, we will use the proceeds to repurchase an equal number of units from our general partner or 40 North. As a result, the number of common units outstanding after this offering will not change whether or not the underwriters exercise this right.

We refer to the foregoing transactions, including the acquisition of interests in our Initial Portfolio, as the "Formation Transactions."

11

Holding Company Structure

We are a holding entity and will conduct our operations and business through subsidiaries to maximize operational flexibility, as is common with publicly traded limited partnerships.

Ownership of Sol-Wind Renewable Power, LP

The following table illustrates our anticipated ownership based on total common units outstanding after giving effect to the Formation Transactions and assumes that the underwriters' right to purchase option units is not exercised.

Common units owned by public |

% | (1) | ||

Common units owned by our general partner or 40 North |

% | |||

Subordinated units |

% | (2) | ||

General partner interest |

—% | (3) | ||

| | | | | |

Total |

100.0 | % | ||

| | | | | |

| | | | | |

- *

- Less

than 1%.

- (1)

- In

connection with this offering, we expect to issue to our general partner's directors and officers an aggregate of restricted common units

(based on the midpoint of the price range set forth on the cover page of this prospectus) as awards under the LTIP (as defined below). These awards will not be issued in exchange for cash. See

"Management's Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies—Equity-Based Compensation" for a discussion of the

accounting for this issuance.

- (2)

- Our

subordinated units will be held by 40 North, a member of our general partner, or one of its affiliates, subject to a limited exception. See "Security

Ownership of Certain Beneficial Owners and Management."

- (3)

- Our general partner owns a non-economic general partner interest in us. Please read "Provisions Of Our Partnership Agreement Relating to Cash Distributions."

Initially, our general partner will own all of our incentive distribution rights and 40 North or one of its affiliates will own all of our subordinated units.

12

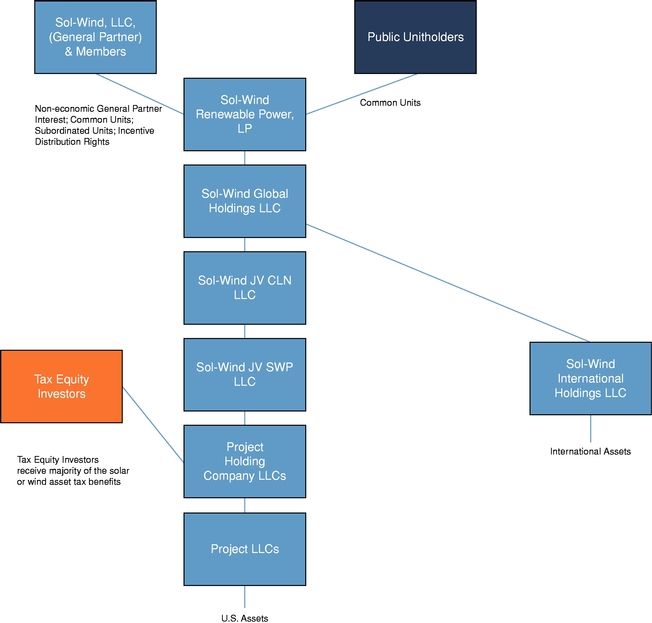

Organizational Structure

The following diagram illustrates our organizational structure immediately following the completion of this offering.

Note: Each of Sol-Wind JV CLN LLC and Sol-Wind International Holdings LLC is treated as an association taxable as a corporation for U.S. federal income tax purposes. All other direct and indirect subsidiaries of Sol-Wind Renewable Power, LP will be treated as either partnerships or entities disregarded as separate from their owners for U.S. federal income tax purposes.

Tax Structure

In order to be treated as a partnership for U.S. federal income taxes, over 90% of the income generated by Sol-Wind Renewable Power, LP must be "qualifying income" as that term is defined in Section 7704 of the U.S. Internal Revenue Code of 1986, as amended (the "Code"). Code Section 7704 specifically provides that income from dividends and interest is qualifying income, except in the case of interest income earned in the conduct of financial or insurance business. As described in more detail in "Risk Factors—Risks Related to Taxation," almost all of Sol-Wind Renewable Power, LP's income will

13

constitute dividend or interest income, and except in the case of a tax-exempt investor that owns more than 50% of the voting power or value of the common units, Sol-Wind Renewable Power, LP will not generate unrelated business taxable income.

Sol-Wind Renewable Power, LP's equity investments in renewable energy assets will be made through wholly-owned subsidiaries that are treated as associations taxable as corporations for U.S. federal income tax purposes. Therefore, all income received from these investments will be distributions on equity that are treated for tax purposes as a return of basis or a dividend. In addition, Sol-Wind Renewable Power, LP's intercompany loans and debt investments in its affiliates will be made either directly or indirectly by Sol-Wind Global Holdings LLC, Sol-Wind JV SWP LLC or Sol-Wind International Holdings LLC pursuant to lending guidelines established under the Partnership Agreement, and therefore we expect interest on these investments will be qualifying income. See "Risk Factors—Risks Related to Taxation—Our U.S. federal income tax treatment depends on our status as a partnership for U.S. federal income tax purposes. If the IRS were to treat us as a corporation for U.S. federal income tax purposes, subject to U.S. corporate income tax, our cash available for distribution to our unitholders may be substantially reduced" and "Material U.S. Federal Income Tax Consequences."

Because we finance our acquisition of renewable energy projects with a combination of intercompany loans and loans to affiliates and equity contributions to subsidiaries, the cash flow distributed to investors will constitute taxable income and a return of principal. Over time, as the intercompany loans and loans to affiliates are repaid, the amount of cash that is treated as a return of principal will increase, and after the loans are repaid, most of the income will be taxable.

U.S. federal, state and local governments and utilities have established various tax incentives to support the development of renewable energy. The incentives include PTCs, ITCs, accelerated tax depreciation and certain state tax credits. The ITC is a U.S. federal tax incentive that provides an income tax credit of 30% of eligible installed costs through 2016 and thereafter it drops to 10% from January 1, 2017. The PTC is a U.S. federal tax incentive alternative that provides a U.S. federal income tax credit to the owners of wind power generation assets based on the amount of energy produced by an asset during the first ten years after it commences commercial operation. These tax credits directly offset U.S. tax liabilities, including alternative minimum tax.

The availability of these Tax Benefits provides the developers and owners of renewable energy assets with the opportunity to raise capital through the sale of tax equity. Tax equity financing has become a driver of the expansion of the U.S. renewable energy market over the past decade. Traditionally, investors in tax equity have been large financial institutions and corporations that invest, in part, to offset their current tax liabilities.

We will seek commercial relationships with tax equity investors to help provide developers with a comprehensive tax equity financing and exit strategy for their qualifying projects. For example, G-I provided tax equity financing for a portion of the assets in our Initial Portfolio. G-I has also provided or agreed to provide tax equity financing for certain assets in the Identified Pipeline. Historically, G-I has invested at the project level for a portion (generally 31%-43%) of the total purchase price our general partner has agreed to pay for the applicable assets. If tax equity financing were to become unavailable from G-I or others (including because of the expiration, elimination or reduction of the Tax Benefits driving tax equity financing structures) our business and growth strategy would be adversely affected. See "Risk Factors—Risks Related to Taxation—Our business currently depends on the availability of tax credits and other financial incentives. The expiration, elimination or reduction of these tax credits and incentives would adversely impact our business."

14

We are managed and operated by our general partner, Sol-Wind, LLC, through its board of directors and executive officers. Our general partner's members will have the right to appoint all of the members of the board of directors of our general partner and, unlike shareholders in a publicly traded corporation, our common unitholders will have no right to elect our general partner or its directors on an annual or other continuing basis. At the closing of this offering, we will not have any employees. Although all of the employees that conduct our business will be employed by our general partner, we sometimes refer to these individuals in this prospectus as our employees.

Under the listing requirements of the New York Stock Exchange ("NYSE"), the board of directors of our general partner will be required to have an audit committee comprised of at least three directors that meet applicable independence standards of the NYSE, subject to certain grace periods. The board of directors of our general partner will initially be comprised of directors, including independent directors, at the completion of this offering.

Following the closing of this offering, 40 North or one of its affiliates will own all of our subordinated units and our general partner will own all of our incentive distribution rights, which will entitle it to increasing percentages, up to a maximum of 50%, of the cash we distribute in excess of $ per unit per quarter, after the closing of this offering. Upon the closing of this offering, assuming we distribute the minimum quarterly distribution only, our general partner will be entitled to receive approximately % of all cash distributed (assuming we grant restricted common units to our general partner's directors and officers at the closing of this offering (based on the midpoint of the price range set forth on the cover page of this prospectus)). See "Certain Relationships and Related Party Transactions."

Prior to the closing of this offering, we will enter into a number of agreements with our general partner, including the Partnership Agreement and the Acquisition Agreements.

Our General Partner's Equityholders

Our general partner's equityholders are BKM, LLC, an entity owned by members of its management team, and 40 North, which is a pooled investment vehicle managed by 40 North Management. 40 North Management is an SEC-registered investment firm founded by Managing Principals David S. Winter and David J. Millstone in 2009. 40 North or one of its affiliates will purchase all of the subordinated units to be issued in the Formation Transactions at a price equal to the offering price of the common units.

Summary of Conflicts of Interest and Fiduciary Duties

General

The officers and directors of our general partner have a contractual duty to manage the Partnership in a manner they believe is in our best interests. At the same time, the officers and directors of our general partner also have fiduciary or other duties to manage our general partner in a manner beneficial to its owners. The board of directors of our general partner may refer any conflicts of interest that may arise in the future between us and our limited partners, on the one hand, and us and our general partner, on the other hand to the conflicts committee of the board of directors of our general partner (the "Conflicts Committee") under our Partnership Agreement, whose determination will be conclusively presumed to not be a breach of any fiduciary or other duties owed to us or our limited partners. The resolution of these conflicts may not be in the best interest of us or our limited partners.

15

Partnership Agreement Modifications to Fiduciary Duties

Delaware law provides that Delaware limited partnerships may, in their partnership agreements, expand, restrict or eliminate the fiduciary or other duties owed by the general partner to limited partners and the partnership. Our Partnership Agreement restricts the remedies available to our common unitholders for actions taken by our general partner that might otherwise constitute breaches of fiduciary duty. By purchasing a common unit, the purchaser agrees to be bound by the terms of our Partnership Agreement, and each common unitholder is treated as having consented to various actions and potential conflicts of interest contemplated in the Partnership Agreement that might otherwise be considered a breach of fiduciary or other duties under applicable state law.

Our Partnership Agreement permits our general partner to make a number of decisions in its individual capacity, as opposed to in its capacity as our general partner, which entitles our general partner to consider only the interests and factors that it desires, and it has no duty or obligation to give any consideration to any interest of or factors affecting us, our affiliates or any common unitholder. When acting in its individual capacity, our general partner may act without any fiduciary or other obligation to us or our common unitholders whatsoever.

Any agreement between us, on the one hand, and our general partner and its affiliates, on the other, will not grant to our common unitholders, separate and apart from us, the right to enforce the obligations of our general partner and its affiliates in our favor. In addition, in the performance of its obligations under the Partnership Agreement, our general partner and its affiliates will not be held to a fiduciary duty standard of care to us, our general partner or our limited partners, but rather will be held to the standard of care specified in the Partnership Agreement.

Our General Partner and its Affiliates May Engage in Competition with Us

Our general partner and its affiliates may compete with us, subject to the requirements of the Partnership Agreement, and may own, acquire, invest in and manage other solar and wind power generation assets. However, to the extent our general partner seeks to sell such assets, it must first offer to sell such assets to us, and in each case our decision whether to accept such offer will be subject to investment guidelines established by the board of directors of our general partner or the approval of an independent committee of the board of directors of our general partner. This requirement does not apply to affiliates of our general partner, including its members. Our general partner and its affiliates are not obligated to identify, acquire, or sell us any assets in the future.

Borrowings. Borrowings by us or by our subsidiaries do not constitute a breach of any duty owed by our general partner or its directors to our common unitholders, including borrowings that have the purpose or effect of (i) enabling our general partner or its affiliates to receive distributions on any units held by them or our incentive distribution rights or (ii) hastening the expiration of the subordination period.

Incentive distribution rights. Our general partner, as the holder of our incentive distribution rights, has the right to reset, at a higher level, the minimum quarterly distribution and the cash target distribution levels upon which the incentive distributions payable to our general partner are based without the approval of our common unitholders at any time when there are no subordinated units outstanding and we have made cash distributions to the holders of our incentive distribution rights at the highest level of incentive distribution for each of the prior four consecutive fiscal quarters.

For a more detailed description of the conflicts of interest and fiduciary or other duties of our general partner, please read "Conflicts of Interest and Fiduciary Duties."

16

Implications of Being an Emerging Growth Company

We are an "emerging growth company" as defined in the Jumpstart Our Business Startups Act (the "JOBS Act"). An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

- •

- the ability to present only two years of audited financial statements and only two years of related Management's

Discussion and Analysis of Financial Condition and Results of Operations;

- •

- exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting;

- •

- reduced disclosure about executive compensation arrangements; and

- •

- exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to our auditor's report in which the auditor would be required to provide additional information about the audit and financial statements.

In addition, Section 107 of the JOBS Act provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the "Securities Act") for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected not to take advantage of this extended transition period for complying with new or revised accounting standards. This election is irrevocable.

We may take advantage of these provisions until the end of the fiscal year following the fifth anniversary of our initial public offering or such earlier time that we are no longer an emerging growth company. We will cease to be an emerging growth company as of the earliest to occur of: (i) the last day of the fiscal year during which we had $1.0 billion or more in annual gross revenues; (ii) the date of our issuance, in a three-year period, of more than $1.0 billion in non-convertible debt; or (iii) the date on which we are deemed to be a "large accelerated filer" as defined for purposes of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), which will occur if the market value of our common units held by non-affiliates exceeds $700.0 million on the last business day of our second fiscal quarter. We may choose to take advantage of some, but not all, of these reduced burdens. For as long as we take advantage of the reduced reporting obligations, the information that we provide to unitholders may be different than information provided by other public companies.

Our principal executive offices are located at 405 Lexington Avenue, Suite 732, New York, New York 10174, and our telephone number is (212) 235-0421. Our website address will be . We intend to make our periodic reports and other information filed with or furnished to the Securities and Exchange Commission (the "SEC") available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

17

Common units offered to the public |

common units. | |

|

common units, if the underwriters exercise in full their right to purchase the option units. |

|

Common and subordinated units outstanding after this offering |

common units and subordinated units, for a total of units. |

|

|

To the extent the underwriters exercise their right to purchase the option units, we will use the proceeds to repurchase an equal number of common units from our general partner or 40 North, as applicable. As a result, the exercise by the underwriters of their right to purchased option units will not affect the number of common units outstanding after this offering or the amount of cash needed to pay the minimum quarterly distribution on all units. |

|

|

In addition, these limited partnership unit numbers exclude up to restricted common units that we may grant to directors and officers of our general partner in connection with this offering (based on the midpoint of the price range set forth on the cover page of this prospectus) and other common units reserved for issuance under the LTIP. See "Executive Compensation—Long-Term Incentive Plan." |

|

Use of proceeds |

We expect to receive approximately $ million from this offering, the sale of common units to our general partner or 40 North and the sale of the subordinated units, after deducting the estimated underwriting discounts, structuring fee and offering expenses payable by us. We intend to use approximately $ million of the net proceeds from this offering, the sale of common units to our general partner or 40 North and the sale of the subordinated units for working capital and general partnership purposes and intend to use the remainder of the proceeds to pay approximately $ in fees and expenses associated with our formation, this offering and the other Formation Transactions, and approximately $ as consideration to our general partner for our acquisition of its interests in our Initial Portfolio. |

|

|

To the extent the underwriters exercise their right to purchase option units, we will use the proceeds to purchase an equal number of common units from 40 North or our general partner. |

18

Cash distributions |

We intend to pay a minimum quarterly distribution of $ per common unit ($ per common unit on an annualized basis) to the extent we have sufficient cash after establishment of cash reserves and payment of fees and expenses. Before we pay any distributions on our common units, we will establish reserves and pay fees and expenses, including reimbursements to our general partner and its affiliates for expenses they incur and payments they make on our behalf, as more fully described under "The Partnership Agreement—Reimbursement of Expenses." We refer to the cash available after establishment of cash reserves and payment of fees and expenses as "available cash." Our ability to pay the minimum quarterly distribution is subject to various restrictions and other factors described in more detail under "Cash Distribution Policy and Restrictions on Distributions." |

|

|