Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - KEY TECHNOLOGY INC | exhibit23093014q4.htm |

| EX-31.2 - EXHIBIT 31.2 - KEY TECHNOLOGY INC | exhibit312093014q4.htm |

| EX-31.1 - EXHIBIT 31.1 - KEY TECHNOLOGY INC | exhibit311093014q4.htm |

| EX-21 - EXHIBIT 21 - KEY TECHNOLOGY INC | exhibit21093014q4.htm |

| EX-32.1 - EXHIBIT 32.1 - KEY TECHNOLOGY INC | exhibit321093014q4.htm |

| EXCEL - IDEA: XBRL DOCUMENT - KEY TECHNOLOGY INC | Financial_Report.xls |

| EX-32.2 - EXHIBIT 32.2 - KEY TECHNOLOGY INC | exhibit322093014q4.htm |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

____________________________________________

FORM 10-K

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED SEPTEMBER 30, 2014 |

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM ____ TO ____. |

Commission File No. 0-21820

_________________________________________

KEY TECHNOLOGY, INC.

(Exact name of registrant as specified in its charter)

Oregon (State or jurisdiction of incorporation or organization) | 93-0822509 (I.R.S. Employer Identification No.) |

150 Avery Street Walla Walla, Washington (Address of Principal Executive Offices) | 99362 (Zip Code) |

Registrant’s telephone number, including area code: (509) 529-2161

__________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Common Stock, no par value Preferred Stock Purchase Right | Name of each exchange on which registered The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer ý |

Non-accelerated filer o (Do not check if a smaller reporting company.) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No ý

The aggregate market value of the Registrant's common stock held by non-affiliates on March 31, 2014 (based on the last sale price of such shares) was approximately $74,700,161.

There were 6,296,839 shares of the Registrant's common stock outstanding on December 5, 2014.

DOCUMENTS INCORPORATED BY REFERENCE

Parts of Registrant's Proxy Statement, dated on or about January 2, 2015, prepared in connection with the Annual Meeting of Shareholders to be held on February 4, 2015, are incorporated by reference into Part III of this Report.

KEY TECHNOLOGY, INC.

2014 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

PAGE | ||

INFORMATION CONCERNING FORWARD-LOOKING STATEMENTS

From time to time, Key Technology, Inc. (“we," "us" or "our"), through its management, may make forward-looking public statements with respect to the Company regarding, among other things, expected future revenues or earnings, projections, plans, future performance, product development and commercialization, and other estimates relating to our future operations. Forward-looking statements may be included in reports filed under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), in press releases, in our president's letter to shareholders, or in oral statements made with the approval of an authorized executive officer of the Company. The words or phrases “will likely result,” “are expected to,” “intends,” “is anticipated,” “estimates,” “believes,” “projects” or similar expressions are intended to identify “forward-looking statements” within the meaning of Section 21E of the Exchange Act and Section 27A of the Securities Act of 1933, as amended, as enacted by the Private Securities Litigation Reform Act of 1995.

Forward-looking statements are subject to a number of risks and uncertainties, the occurrence of any of which could cause the price of our common stock to fluctuate significantly, making it difficult for shareholders to resell common stock at a time or price they find attractive. We caution investors not to place undue reliance on our forward-looking statements, which speak only as of the date on which they are made. Our actual results may differ materially from those described in the forward-looking statements as a result of various factors, including those listed below:

• | adverse changes in general economic conditions and disruption in financial markets may adversely affect the business of our customers and our business and results of operations; |

• | ongoing uncertainty and volatility in the global economy may adversely affect our operating results; |

• | adverse economic conditions in the food processing industry, either globally or regionally, may adversely affect our revenues; |

• | the loss of any of our significant customers could reduce our revenues and profitability; |

• | significant investments in unsuccessful research and development efforts could materially adversely affect our business; |

• | industry consolidation could increase competition in the food processing equipment industry; |

• | we are subject to price competition that may reduce our profitability; |

• | the timing and significance of major orders could result in significant fluctuation in quarterly and annual operating results; |

• | the failure of our independent sales representatives to perform as expected would harm our net sales; |

• | we have made, or may make, acquisitions or enter into distribution agreements or similar business relationships that could disrupt our operations and harm our operating results; |

• | our international operations subject us to a number of risks that could adversely affect our revenues, operating results and growth; |

• | fluctuations in foreign currency exchange rates could result in unanticipated losses that could adversely affect our liquidity and results of operations; |

• | our existing and new products may not compete successfully in either current or new markets, which would adversely affect our sales and operating results; |

• | advances in technology by competitors may adversely affect our sales and profitability; |

• | our expansion into new markets, increasingly complex projects and applications, and integrated product offerings could increase our cost of operations and reduce gross margins and profitability; |

• | our inability to obtain products and components from suppliers would adversely affect our ability to manufacture and market our products; |

• | our information systems, computer equipment and information databases are critical to our business operations and any damage or disruptions could adversely affect our business and results of operations; |

• | our potential inability to retain and recruit experienced management and other key personnel, or the loss of key management personnel, may adversely affect our business and prospects for growth; |

• | the potential inability to protect our intellectual property, especially as we expand geographically, may adversely affect our competitive advantage; |

• | intellectual property-related litigation expenses and other costs resulting from infringement claims asserted against us by third parties may adversely affect our results of operations and our customer relations; |

• | our financing agreements contain restrictive and financial covenants that may adversely affect us; |

• | our dependence on certain suppliers may leave us temporarily without adequate access to raw materials or products; |

• | our operating results are seasonal and may further fluctuate due to severe weather conditions affecting the agricultural industry in various parts of the world; |

• | the limited availability and possible cost fluctuations of materials used in our products could adversely affect our gross margins; |

• | our reported results may be affected adversely by the implementation of new, or changes in the interpretation of existing, accounting principles or financial reporting requirements; and |

1

• | compliance with changing regulation of corporate governance and public disclosure will result in additional expenses to us and pose challenges for our management. |

Given these uncertainties, readers are cautioned not to place undue reliance on the forward-looking statements. We disclaim any obligation subsequently to revise or update forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

PART I

ITEM 1. | BUSINESS. |

General

Key Technology was founded in 1948 as a local producer of vegetable processing equipment. We have evolved into a worldwide supplier of process automation solutions to the food processing industry and other industries such as tobacco and pharmaceuticals. We were incorporated in 1982 as a result of a management buyout of our predecessor organization.

We and our operating subsidiaries design, manufacture, sell and service process automation systems that process product streams of discrete pieces to improve safety and quality. These systems integrate electro-optical automated inspection and sorting systems with process systems that include specialized conveying and preparation equipment. We provide parts and service for each of our product lines to customers throughout the world.

Net sales for the year ended September 30, 2014 were $118.3 million compared with $136.8 million for fiscal 2013 and $115.2 million for fiscal 2012. We reported a net loss for fiscal 2014 of $5.4 million, or $0.86 per diluted share, compared with net earnings of $4.0 million, or $0.69 per diluted share, for fiscal 2013 and net earnings of $0.4 million, or $0.08 per diluted share, for fiscal 2012. Export and international sales for the fiscal years ended September 30, 2014, 2013 and 2012 accounted for 48%, 45% and 45% of net sales in each year, respectively. Total assets at September 30, 2014 were $98.3 million compared to $114.6 million at September 30, 2013.

Industry Background

Food Processing Industry

Our primary market is the food processing industry where we apply our processing knowledge and application expertise to help customers improve quality, increase yield, and reduce cost. Our integrated sorting, conveying, and process automation systems are sold to small, medium and large-sized food processing companies for a range of specialized applications. Food processors generally experience thin profit margins and, therefore, are focused on increasing profitability and efficiency in their processing plants by improving the performance of their equipment and processing lines. In addition, food processors recognize the value of new technology and continue to demand innovative equipment that addresses food safety, quality, and automation to drive productivity in their plants.

Our strategy is to offer equipment solutions that reduce reliance on manual inspection and address the common food processing industry problems associated with high labor costs, workforce shortages, inadequate yields, inconsistent product quality and food safety. In highly developed markets, including those in North America and Western Europe, the substitution of automated processes for manual labor is well underway. Food processors in these regions typically appreciate the value of replacing manual labor with automated systems and look for systems that will help maximize yields, product quality and food safety. In developing countries, interest in automation is rising as food processors in these regions increasingly strive to compete in a global economy by improving product quality and food safety.

Within the food processing industry, the greatest opportunities for automated inspection systems have been in potatoes, vegetables, and fruits where the frequency and severity of foreign material and defects is highly variable, depending on the countless factors that affect crops. In addition, dried fruit and tree nuts are high value products and processors increasingly demand inspection and automation to increase profitability. We believe that many additional applications for our automated inspection systems exist in other food processing markets.

The principal potato market served by our systems is potato strips (commonly referred to as french fries in the United States). Potato strips have historically accounted for a very large portion of the frozen potato products produced in the U.S. and, with the expansion of American-style fast food chains in other countries, this market is growing internationally. Although we

2

have successfully been diversifying into other food and non-food markets in recent years to reduce dependence on this market, potato strips remain an important market along with other potato products such as wedges, curly fries, formed products, whole potatoes and potato chips.

Other important markets within the food processing industry are fruits and vegetables, including both fresh-cut produce and processed products that may ultimately be canned or frozen for institutional and retail customers. Because foreign material and product defects plague these field-harvested products, automated sorting enhances the quality and safety of the product while improving yields and reducing labor costs. Our principal fruit and vegetable markets are fresh, frozen, canned and dehydrated green beans, corn, carrots, peas, onions, berries, cranberries, pears and peaches, as well as ready-to-eat fresh-cut salads.

As a result of the acquisition of Visys NV in early 2013, we are able to offer a more comprehensive suite of products that address the dried fruit and nut market. Nut processors strive to produce various products (shelled or unshelled) that are free of foreign material, extraneous vegetative matter or out-of-specification nuts to increase the value of their product. Numerous technologies and methodologies are applied at various steps in the processing line to further increase this value. The processor’s quality objectives are achieved with our range of chute-fed sorting systems and, when combined with our mechanical grading systems, create an integrated product package.

We believe that selected areas of the food processing industry will continue to present opportunities for growth. In general, food processing companies remain financially viable, but are increasingly coming under pressure to increase profitability and improve product safety while maintaining or reducing prices for their own products. By offering equipment that increases yields, enhances product quality and food safety, and results in reduced processing costs, we believe we are well positioned to satisfy the needs of the food processing industry.

Cyclical and seasonal fluctuations in the potato, fruit, and vegetable processing industries cause us to experience some predictable seasonality of orders and shipments. Typically, orders and shipments for this industry tend to be lower during our first two fiscal quarters of the year than during the second half of the fiscal year. Other, less seasonal markets that are served by the company include snack, bakery, dairy, poultry, and seafood products, as well as non-food markets.

Non-food Industries – Tobacco, Pharmaceuticals and Nutraceuticals

Processors, manufacturers and packagers in several non-food industries are interested in automated inspection systems that reduce costs, increase yields, and improve product quality and safety. Our primary non-food markets include the tobacco industry, pharmaceuticals and nutraceuticals.

The tobacco industry typically accounts for less than 5% of our net sales. With systems that remove non-tobacco-related material from primary processing lines and threshing lines, we help tobacco processors maximize product quality. We have an original equipment manufacturer distribution agreement with Hauni Maschinenbau AG, a leading supplier of equipment to the tobacco industry. The agreement gives Hauni exclusive rights to market our equipment to tobacco processors worldwide and makes us the sole supplier of optical sorting equipment to Hauni for the tobacco market.

In fiscal 2014, the pharmaceutical and nutraceutical industry, which is served by our pharmaceutical product line, SYMETIX®, also represented less than 5% of our net sales. SYMETIX’s optical inspection systems for softgels and tablets remove defects and foreign capsules and tablets from the product stream. These systems are of interest to brand owners, product manufacturers, and contract packers looking to assure product quality while reducing labor costs.

We own a 15% minority interest in Proditec SAS. Proditec, headquartered in France, is a leading manufacturer of automated, solid dose pharmaceutical inspection systems based on machine vision technology. With Proditec, we are promoting and selling inspection solutions in the pharmaceutical and nutraceutical markets.

3

Products

The following table sets forth sales by product category for the periods indicated (in thousands):

Fiscal Year Ended September 30, | |||||||||||||||||||||

2014 | 2013 | 2012 | |||||||||||||||||||

Automated inspection systems | $ | 55,829 | 47 | % | $ | 59,336 | 43 | % | $ | 46,586 | 40 | % | |||||||||

Process systems | 34,580 | 29 | % | 50,729 | 37 | % | 44,940 | 39 | % | ||||||||||||

Parts and service | 27,849 | 24 | % | 26,718 | 20 | % | 23,648 | 21 | % | ||||||||||||

Net sales | $ | 118,258 | 100 | % | $ | 136,783 | 100 | % | $ | 115,174 | 100 | % | |||||||||

Service and maintenance contracts are less than 10% of total net sales and are therefore summarized with parts and service.

The following table sets forth the percent of total gross margin contributed by each product category for the periods indicated:

Fiscal Year Ended September 30, | |||||||||

2014 | 2013 | 2012 | |||||||

Automated inspection systems | 48 | % | 44 | % | 40 | % | |||

Process systems | 16 | % | 28 | % | 28 | % | |||

Parts and service | 36 | % | 28 | % | 32 | % | |||

Total gross margin | 100 | % | 100 | % | 100 | % | |||

Automated Inspection Systems

Automated inspection systems are used in various applications to detect and remove defects and foreign material from the product stream and help processors improve quality and increase the value of their end product. Key offers a sophisticated range of digital sorting systems that recognize color, size, shape, structural properties, and chemical composition to detect the widest range of visible and invisible defects.

Depending on the needs of each application, our sorters can be designed with a combination of cameras and lasers to detect and remove a wide variety of defects and foreign material, which is an important contributor to food safety. When lasers are combined with high resolution cameras for superior shape, size, and color determination, the result is a high quality product sort. Advanced color and shape sorting can be accomplished with monochromatic or color cameras, coupled with powerful software algorithms. In addition, BioPrint® technology identifies defects and foreign material based on unique biological characteristics and achieves enhanced performance, even under high incoming defect loads, and detects invisible defects.

Sort-to-Grade™ technology for potato strip processing was introduced in January 2014 for our belt-fed sorters. This software-driven intelligence enables sorters to grade by count, sorting by length or size, accepting or rejecting each defective piece to control the quality of output to a defined grade, as defined by the processor.

Our popular belt-fed sorters - Optyx®, Tegra®, and Manta® - are primarily used in the fresh and frozen fruit, vegetable and potato products segments. Our chute-fed sorters, including the Visys Spyder®, Visys Python, and Visys Cayman®, and the jointly developed Taurys™, are ideal for sorting nuts, dried fruits, and frozen vegetables. Our other automated inspection systems include Veo™, an optical sorter designed specifically for seed corn; Tobacco Sorter™ systems used in tobacco threshing and primary processing; and ADR® automatic defect removal systems used in the potato strip industry.

In November 2013, the Company introduced VitiSort®, a new sorter designed for red wine grapes. This compact system, combines a MOG (material other than grape) removal shaker and optical sorting with an integral juice recovery system. The system removes any unwanted objects and other MOG from the product flow, which enables the winery to better control product quality.

We also offer automated inspection equipment for solid dose pharmaceuticals and nutraceuticals through our SYMETIX pharmaceutical product line. Available in a range of sizes, VeriSym® sorting systems inspect the color, size, and shape of tablets and softgels and automatically remove defects and foreign tablets or capsules from the product stream at rates of up to 1,000,000

4

tablets or capsules per hour. These inspection systems help product manufacturers and contract packers assure the quality of their finished product and are designed to replace batch processing systems historically used in this industry.

In July 2013, we signed an exclusive licensing agreement with EVK DI Kerschhaggl GmbH and Insort GmbH to deploy chemical imaging technology (CIT®) in our products, further enhancing our potato sorting capabilities. Additionally, an exclusive distribution agreement enables us to market Insort’s chemical imaging sorters to North American and global accounts in the potato industry.

We have a large installed base of automated inspection systems, which we support with upgrades to extend the life of the equipment and enable customers to continue operating at peak performance as technology advances. Upgrades often provide customers with a less capital intensive alternative to acquiring new automated inspection systems.

Process Systems

Conveying and processing equipment are utilized worldwide throughout many industries to move and process product within a production plant. The process systems group includes standard and custom designed equipment that conveys, dewaters, transfers, distributes, aligns, feeds, meters, separates, grades, cleans, washes, and polishes products. Our Smart Shaker® vibratory solutions, which include Iso-Flo®, Impulse®, and Horizon™ systems, combine gentle material handling with a wide variety of processing functions in addition to vibratory conveying. Rotary sizing and grading systems, Turbo-Flo® steam blanchers and SYMETIX equipment for pharmaceuticals and nutraceuticals, complete our conveying and processing equipment product line.

The mechanical sizing, sorting, separating, and grading equipment manufactured at the Company’s Redmond, Oregon facility is used in many food processing and fresh vegetable packing operations. These rotary sizing and grading technologies can remove oversized, undersized, and small irregular-shaped pieces of product from the line or separate product into predetermined size categories. Additionally, this equipment can remove field debris, broken pieces, seeds, juice, fines, and other targeted material.

Preparation Systems. We design and manufacture preparation systems to prepare a wide range of food products prior to cooking, freezing, canning, or other types of processing. Equipment in this group includes air cleaners, air coolers, vegetable metering and blending systems, and bulk handling equipment. This equipment represents our most mature product line. Sales of these solutions over the years have formed a customer base for sales of our other solutions and are also establishing a new customer base in developing markets. Preparation system revenues include a variety of third-party supplied equipment and installation services, which are sold as components of larger, integrated processing lines, for which we have assumed turn-key sales responsibility. In addition, the Company maintains an agreement with ABCO Industries to sell their thermal processing equipment through our distribution channels.

Line Solutions

Integrated Solutions. Our Integrated Solutions Group (ISG) provides integrated whole-line solutions. From pre-engineering and project definition to plant start-up, ISG offers complete turn-key solutions that can include the integration of third-party products along with Key’s sorting, conveying, and processing systems to meet the specific needs of each application. We leverage our industry expertise and strong engineering and project management capabilities to deliver complete integration services, all from a single source.

Parts and Service

We have a large installed base of inspection and processing systems, which generates potential business for our parts, service, and training programs. Our PROliance™ suite of support services, parts, protection plans and training solutions, provides spare parts and post-sale field and telephone-based repair services to support our customers’ routine maintenance requirements, seasonal equipment startup and winterization processes. Our field service personnel are geographically located around the world in locations close to customers enabling quick response time and regional technical support. We typically provide incidental system installation support services in the sale price of select systems, principally automated inspection systems.

RemoteMD™. RemoteMD is a real-time condition and monitoring and diagnostics analysis tool for G6 optical sorters - Manta, Optyx, and Tegra - as well as G6 ADR systems. RemoteMD proactively monitors the condition of the customer’s system, assesses the status, and alerts the customer if problems are detected. By automating detection and diagnosis, RemoteMD provides detailed information to our service technicians, which increases the first-time fix-rate, reduces in-plant service calls, speeds resolution time and enhances customer productivity. We offer three distinct levels of RemoteMD services as part of our comprehensive protection plans - SelectPRO, PlusPRO, and PremierPRO. Each of the three protection plans is sold via annual subscription.

5

Online Training. This program provides customers with an interactive multimedia curriculum covering selected optical inspection systems and vibratory conveyors. The flexible, web-based program offers a wide variety of self-paced training modules designed for operators, maintenance personnel, sanitation crews, supervisors, and others working with this equipment. Our Online Training Program includes modules that cover ADR hardware, Optyx hardware, Tegra hardware, G6 software, Iso-Flo vibratory conveyors, and a variety of industry-related compliance topics.

Research and Development

At September 30, 2014, our research and development department had 49 employees who conduct new product research and development and sustaining engineering for released products. Our technical staff includes electronic, optical, mechanical and software engineers, mathematicians and technical support personnel.

In fiscal 2014, our research and development expenses were approximately $11.6 million, compared to $9.6 million in fiscal 2013 and $8.3 million in fiscal 2012.

Manufacturing

We maintain manufacturing facilities in Walla Walla, Washington; Redmond, Oregon; Beusichem, The Netherlands; and Hasselt, Belgium. Our current manufacturing facilities and our product design and manufacturing processes integrate Computer Aided Engineering (CAE), Finite Element Analysis (FEA), Computer Aided Design (CAD), Computer Aided Manufacturing (CAM) and Computer Integrated Manufacturing (CIM) technologies. Manufacturing activities include process engineering; fabrication, welding, finishing and assembly of custom-designed stainless steel systems; camera and electronics assembly; subsystem assembly; and system test and integration. The following table provides a summary of our manufacturing locations and manufacturing floor space:

Location | Manufacturing Facility | Products/Services Produced |

Walla Walla, Washington | 132,000 square feet | Automated Inspection Systems Process Systems Parts and Service |

Redmond, Oregon | 17,000 square feet | Process Systems Parts and Service |

Beusichem, The Netherlands | 37,000 square feet | Process Systems Automated Inspection Systems Parts and Service |

Hasselt, Belgium | 13,000 square feet | Automated Inspection Systems Parts and Service |

We manufacture certain products to Underwriters Laboratories and United States Department of Agriculture standards. Certain of our products also comply with the Canadian Standards Association (CSA), European CE (Conformité Européene) and Electronic Testing Laboratory (ETL) safety standards. Certain products for the pharmaceutical/nutraceutical industry are FDA 21 CFR 11-compliant and designed using GAMP4 guidelines. Our domestic facilities were recertified to the ISO 9001:2008 standard in 2011.

Certain components and subassemblies included in our products are obtained from limited-source or sole-source suppliers. We attempt to ensure that adequate supplies are available to maintain manufacturing schedules. We may also use contract or third-party manufacturers to fulfill customer needs for ancillary products or equipment that we do not manufacture. We do not have long-term contracts with any of our suppliers. We also rely on third-party domestic and foreign suppliers for certain raw materials. Several of these suppliers are the single source of the raw material. We may be adversely affected in the event that these suppliers cease operations or if pricing terms become less favorable.

Sales and Marketing

We market our equipment worldwide both directly and through independent sales representatives. Sales by independent sales representatives generally account for between 20% and 30% of our annual consolidated net sales. In the United States, we operate sales offices in Walla Walla, Washington and Redmond, Oregon. Our international sales offices are: Key Technology B.V. and Visys N.V., which provide sales and service to European, Middle Eastern, Indian, and African customers; Key Technology Australia Pty Ltd., which provide sales and service to customers primarily in Australia and New Zealand; and Productos Key Mexicana S.

6

de R.L. de C.V., which provides sales and service to customers in Mexico, and Central and South America. We supply equipment from both product groups - automated inspection systems and process systems - to customers in our primary markets through common sales and distribution channels. In addition, we supply parts and service through our worldwide service organization.

Sales of most exports of products manufactured in the United States for shipment into international markets, other than Europe, have been denominated in U.S. dollars. Sales of products in Europe are typically denominated in Euros. As we expand our operations in Australia and Latin America, transactions denominated in the local currencies of these countries may increase. In connection with our export and international sales, we are subject to the risks of conducting business internationally, including unexpected changes in regulatory requirements; fluctuations in the value of the U.S. dollar, which could increase or decrease the sales prices in local currencies of our products in international markets; tariffs and other barriers and restrictions; and the requirements of complying with a variety of international laws. Additional information regarding domestic and international sales is set forth in Note 17 to the Company’s Consolidated Financial Statements for the fiscal year ended September 30, 2014.

During fiscal 2014, 2013 and 2012, sales to McCain Foods Limited represented approximately 10%, 11%, and 10% of total net sales, respectively. During fiscal 2013, sales to ConAgra Foods, Inc. represented 11% of total net sales. While we believe that our relationship with these customers is satisfactory, the loss of either of these customers could have a material adverse effect on our revenues and results of operations. Each of these customers represents a group of plants under common control. Generally, purchasing decisions for these customers are made at the individual plant level which may diversify the concentration of risk.

Backlog

Our backlog as of September 30, 2014 and September 30, 2013 was approximately $18.1 million and $25.2 million, respectively. We schedule production based on firm customer commitments and forecasted requirements. We include in backlog only those customer orders for which we have accepted purchase orders, or the equivalent.

Competition

The markets for automated inspection systems and process systems are highly competitive. We experience severe price competition across almost all our product lines. Other important competitive factors include performance, reliability, and customer support and service. We believe that we currently compete effectively with respect to these factors, although there can be no assurance that existing or future competitors will not introduce comparable or superior products at lower prices. Certain of our competitors may have substantially greater financial, technical, marketing and other resources. Other companies which sell products in certain of our markets include Heat & Control, Inc. and its subsidiaries; Tomra Systems ASA and its subsidiaries, BEST N.V. and Odenberg Inc.; Sortex Ltd.; Kiremko B.V.; Meyer Industries, Inc.; KMG Systems Ltd.; VDL Industrial Products B.V.; TNA Australia Pty. Ltd.; and BMA AG. We have also encountered additional smaller competitors entering our markets. As we enter new markets, we expect to encounter additional new competitors.

Patents and Trademarks

We currently hold 35 United States patents on various features of our products issued from 1994 through fiscal 2014, and 16 other national patents issued by other countries. The first of these patents will expire in fiscal 2015. Although we consider our patents to be important to our business, we believe these expirations will not have a significant effect on us. Of the numbers above, seven patents were issued in fiscal 2014. As of December 5, 2014, 23 United States patent applications and 41 other foreign national patent applications were pending. We have 63 registered trademarks and two pending application for trademarks.

We also attempt to protect our trade secrets and other proprietary information through proprietary information agreements and security measures with employees, consultants and others. The laws of certain countries in which our products are or may be manufactured or sold may not protect our products and intellectual property rights to the same extent as the laws of the United States.

Employees

At September 30, 2014, we had 553 full-time employees, including 314 in manufacturing and project engineering, 49 in research and development, 141 in marketing, sales and service, and 49 in general administration and finance. A total of 166 employees are located outside the United States. We also use temporary contract employees, which improves our ability to adjust manpower in response to changing demand for our products. Of the total number of employees at September 30, 2014, six were contract employees. None of our employees in the United States are represented by a labor union. The employees located at our facility in Beusichem, The Netherlands are represented by the Small Metal Union. We have never experienced a work stoppage, slowdown or strike.

7

Available Information

Our annual and quarterly reports and other filings with the United States Securities and Exchange Commission (“SEC”) are made available free of charge through the Investor Relations section of our website at www.key.net as soon as reasonably practicable after we file such material with the SEC. The information on or that can be accessed through our website is not a part of this Annual Report on Form 10-K.

8

ITEM 1A. | RISK FACTORS. |

In addition to the other information in this Annual Report on Form 10-K, the following risk factors should be considered carefully in evaluating our business because such factors may have a significant effect on our operating results and financial condition. As a result of the risk factors set forth below and the information presented elsewhere in this Annual Report on Form 10-K, actual results could differ materially from those included in any forward-looking statements.

Adverse changes in general economic conditions and disruption in financial markets may adversely affect the business of our customers and our business and results of operations.

Our business may be affected by uncertainties and general economic conditions beyond our control that may cause customers to defer or cancel new orders and sales commitments previously made. Uncertainty about the direction and relative strength of the economy in the United States and other important markets may be sufficient reason for customers to delay, defer or cancel purchase decisions, including decisions previously made. Economic difficulties in the United States and certain international markets could cause a decrease in the overall demand for our products.

Deterioration of national and global economic conditions and disruptions in credit and other financial markets could, among other things:

• | adversely affect our expansion plans, including possible acquisitions; |

• | impair the financial condition of some of our customers and suppliers, thereby increasing customer bad debts or non-performance by suppliers; |

• | adversely affect our ability to fund new product development necessary to meet future customer requirements; |

• | negatively affect global demand for our customers' products, particularly in the food industry, which could result in underutilization of our production facilities and a reduction of sales, operating income and cash flows; |

• | negatively affect our customers' ability to obtain financing, which could result in a reduction in sales, operating income and cash flows; |

• | negatively affect our return on cash and cash equivalents; |

• | make it more difficult or costly for us to obtain financing for our operations or investments; |

• | negatively affect the results of our risk management activities if we are required to record losses related to financial instruments or experience counterparty failure; |

• | require asset write-downs; or |

• | impair the financial viability of our insurers. |

The ongoing uncertainty and volatility in the global economy may adversely affect our operating results.

Our operations and performance depend on worldwide economic conditions. In particular, we may be affected by the continuing uncertainties associated with certain countries in the European Union and the austerity measures being implemented or contemplated. If global economic and market conditions, or economic and financial market conditions in Europe, the United States or other key markets, remain uncertain, persist, or deteriorate further, our customers may respond by suspending, delaying or reducing their capital expenditures, which may adversely affect our cash flows and results of operations. Furthermore, our customers may experience increased difficulty in obtaining credit to finance purchases of the Company's products. In addition, these conditions may affect the ability of our suppliers to provide goods and materials to us on a consistent and timely basis which may adversely affect our operations.

Adverse economic conditions in the food processing industry, either globally or regionally, may adversely affect our revenues.

The markets we serve, particularly in the food processing industry, are generally experiencing variable economic conditions. Additionally, varying consumer demand due to economic conditions or dietary trends, product supply, and excess plant capacity, most notably in the potato market, could result in reduced or deferred capital equipment purchases for our product lines. While we have reacted to these developments with applications directed toward the growing fresh vegetable and fruit industries as well as the pharmaceutical and nutraceutical industries, loss of business, particularly in the potato industry, would have a negative effect on our net sales and net earnings.

9

The loss of any of our significant customers could reduce our revenues and profitability.

We have significant, strategic customers and we anticipate that our operating results may continue to depend on these customers for the foreseeable future. The loss of any one of those customers, or a significant decrease in the volume of products they purchase from us, could adversely affect our revenues and materially adversely affect our profitability. Any difficulty in collecting outstanding amounts due from one of those customers may also harm our operating results. In addition, sales to any particular large customer may fluctuate significantly from quarter to quarter, causing fluctuations in our quarterly operating results.

Significant investments in unsuccessful research and development efforts could materially adversely affect our business.

The product solutions we offer are very complex, and we need to successfully develop new products in a global competitive environment. If we fail to accurately predict and meet future customer needs and preferences, fail to incorporate critical industry-leading technologies and solutions in our products, or fail to allocate our research and development funding to products with higher customer acceptance and growth prospects, we may find we have invested heavily in the development of products that do not lead to significant revenue. Failure to successfully develop new products may also cause existing or potential customers to choose competitors' products. Any of these events may reduce future revenues and adversely affect our competitive position. Even if we successfully innovate and develop new products and product enhancements, we may incur substantial costs in doing so, and our profitability may be reduced.

Industry consolidation could increase competition in the food processing equipment industry.

The food processing equipment industry has experienced recent consolidation. Consolidation by our competitors may enhance their production capacity, technological abilities, broaden their product lines and resources, and lower their cost structure and prices, causing us to be at a competitive disadvantage. Increased competition and our ability to respond effectively to any of these changing market conditions could result in significant price erosion, reduced revenue, lower margins, and loss of market share, any of which could adversely affect our net earnings.

We are subject to price competition that may reduce our profitability.

We face price sensitivity from customers as well as aggressive pricing by our competitors, particularly in periods of excess capacity. Recent consolidation among our primary competitors may also allow these competitors to compete more effectively on price. These conditions may require us to lower prices in order to be price-competitive. In addition, because of their purchasing volume, our larger customers can influence market participants to compete on price terms. Such customers also use their buying power to negotiate lower prices. Customers are also increasing the use of integrated supply chain sourcing solutions focused solely on immediate cost savings. If we are not able to offset resulting price reductions by improving operating efficiencies and reducing expenses, such price reductions may have an adverse effect on our profit margins and net earnings.

The timing and significance of major orders could result in significant fluctuation in quarterly and annual operating results.

The timing of our significant orders depends on a number of factors over which we may have little or no control, including the size and complexity of a potential order, the level of competition that we encounter in our sales activities, and our current and potential customers' internal budgeting and approval process. In addition, the industries we serve, particularly the potato market, have buying patterns that vary greatly between fiscal years. As a result, we may expend significant effort over a long period of time in an attempt to obtain an order, but ultimately not obtain the order, or the order ultimately received may be smaller than anticipated. Our orders from different customers vary from quarter to quarter, and a customer with a large order in one quarter may generate significantly lower orders in subsequent quarters. Due to the resulting fluctuations, we believe that quarter-to-quarter comparisons of our revenue and operating results may not be meaningful, and that these comparisons may not be an accurate indicator of our future performance. These fluctuations in orders will result in fluctuations in our annual operating results. Additonally, operating margins may be adversely affected by a reduction in sales or changes in product mix, and we may not be able to reduce our costs in a timely manner to adjust for the difference between actual and forecasted sales.

10

The failure of our independent sales representatives to perform as expected would harm our net sales.

Sales by independent sales representatives generally account for between 20% and 30% of our consolidated net sales. If our independent sales representatives fail to market, promote and sell our products adequately, our business will be adversely affected. Our independent sales representatives could reduce or discontinue sales of our products, sell competitor's product lines, or they may not devote adequate resources to selling our products in the volumes and within the time frames that we expect, any of which events could adversely affect our revenues and net earnings.

We have made, or may make, acquisitions or enter into distribution agreements or similar business relationships that could disrupt our operations and harm our operating results.

We have made, or may in the future make, acquisitions of businesses, or enter into distribution agreements or similar business relationships that offer products, services, or technologies that we believe would complement our business. These changes in our business present significant challenges and risks and there can be no assurances that we will manage these changes successfully. These changes in our business involve numerous risks, including:

• | significant potential expenditures of cash, stock, and management resources; |

• | difficulty achieving the potential financial and strategic benefits of the acquisition or business relationship; |

• | difficulties in integrating acquired operations or products, including the potential loss of key employees from the acquired business; |

• | difficulties of integrating different technologies into products and markets due to technological challenges; |

• | assumption of product liabilities, including warranty costs, for third-party products; |

• | increased costs due to required minimum purchase levels and commitments for payments to third parties; |

• | difficulties and costs associated with evaluating and integrating the information systems and internal control systems of the acquired business; |

• | possible future impairment of assets related to goodwill and other intangible assets resulting from an acquisition, and reduction in our future operating results from amortization of intangible assets; |

• | diversion of management's attention from our core business, including loss of management focus on marketplace development; |

• | adverse effects on existing business relationships with suppliers and customers, including the potential loss of suppliers and customers of the acquired business; |

• | assumption of liabilities, known and unknown, related to the acquired business in general, and litigation and other legal process involving the acquired business in particular, including intellectual property litigation risk; |

• | entering geographic areas or distribution channels in which we have limited or no prior experience; and |

• | those risks related to general economic and political conditions. |

There can be no assurance that attractive acquisition opportunities will be available to us, that we will be able to obtain financing for or otherwise consummate any acquisition, or that any acquisition that we do consummate will be successful.

Our international operations subject us to a number of risks that could adversely affect our revenues, operating results and growth.

We conduct business outside the United States, which subjects us to the risks inherent in international operations. In fiscal 2014, our international sales represented approximately 48% of our consolidated net sales, compared to approximately 45% of our consolidated net sales in fiscal 2013. Risks inherent in international operations include the following:

• | unexpected changes in regulatory and certification requirements; |

• | restrictive governmental actions (such as restrictions on the transfer or repatriation of funds and trade protection measures, including export duties and quotas, customs duties and tariffs, or trade barriers erected by either the United States or other countries where we do business); |

• | currency restrictions and exchange rate fluctuations; |

• | scrutiny of foreign tax authorities which could result in significant fines, penalties and additional taxes; |

• | changes in import or export licensing requirements; |

• | longer payment cycles; |

• | transportation delays; |

• | competitive pricing that we may experience internationally; |

• | challenges in implementing cost effective operating and manufacturing strategies in varied geographic regions; |

• | challenges in understanding how to effectively compete and meet customer requirements in different operating environments; |

11

• | ability to globalize solutions for our global customers; |

• | economic downturns, civil disturbances or political instability; |

• | geopolitical turmoil, including terrorism or war; |

• | difficulties and costs of staffing and managing geographically disparate operations; |

• | changes in labor standards; |

• | laws and business practices favoring local companies; |

• | limitations on our ability under local law to protect our intellectual property; |

• | changes in domestic and foreign tax rates and laws; and |

• | difficulty in obtaining sales representatives and servicing products in foreign countries, which may adversely affect sales in those countries. |

The occurrence of any of the above risks could adversely affect our revenues, operating results and growth.

Fluctuations in foreign currency exchange rates could result in unanticipated losses that could adversely affect our liquidity and results of operations.

We are exposed to foreign currency exchange rate fluctuations because a portion of our revenues, expenses, assets and liabilities are denominated in foreign currencies. Changes in foreign currency exchange rates affect our results of operations and financial position. We attempt to manage certain effects of foreign currency fluctuations by entering into short-term forward exchange contracts in situations where it is both possible and practical. In these instances, these contracts are designed to minimize specific foreign currency gains or losses, as the gains or losses on the derivative are intended to offset the losses or gains on the underlying exposure. However, these contracts do not cover our full exposure and, additionally, there is no guarantee that these forward contracts will fully protect against the foreign exchange fluctuations in the underlying exposure. Accordingly, we could experience foreign currency gains or losses that could have a material impact on our operating results.

Our existing and new products may not compete successfully in either current or new markets, which would adversely affect our sales and operating results.

Our future success and growth is dependent upon our ability to develop, manufacture, market, and sell products and services in certain food processing markets as well as to introduce new products into other existing and potential markets. Customers have also become increasingly concerned about their return on investment, energy conservation, sanitation and food safety, and market solutions need to be cognizant of these considerations. There can be no assurance we can successfully and profitably penetrate these potential markets or expand into new international markets with our current or future products. In addition, new product introductions and enhancements of existing products may reduce demand for our existing products or delay purchases by customers awaiting arrival of our new products. As new or enhanced products are introduced, we must successfully manage the transition from existing products. There are also inherent risks in developing new technologies, entering new markets, and expanding in our existing markets including:

• | length of time and cost for development of these technologies and markets; |

• | development of the technological capability to address the requirements and performance specifications of new and existing markets; |

• | our ability to manufacture our products in various geographies, which may affect our success in certain emerging markets; |

• | our ability to design products for ease of manufacturability and service; |

• | our ability to manufacture and sell our new products at sustainable gross margins; |

• | product reliability issues related to both new technology and adapting existing products to operate in new or rugged operating environments at customer sites; |

• | design or manufacturing flaws that may lead to increased product liability or warranty claims; and |

• | failure to meet performance specifications, which could damage our profitability and the reputation of our products. |

Advances in technology by competitors may adversely affect our sales and profitability.

The rapidly changing needs of the markets for our products demand constant innovation. Competitors may be able to adapt or develop technologies to create or enhance product offerings that directly compete with our products. Advances in technology may also remove some barriers to market entry, enabling additional competitors to enter our markets. These innovations could cause our products to become less competitive or obsolete, and decrease our sales and profits, having a material adverse effect on our business and financial condition. There can be no assurance that we will be able to continue to develop new products to compete effectively in the future.

12

Our expansion into new markets, increasingly complex projects and applications, and integrated product offerings could increase our cost of operations and reduce gross margins and profitability.

Our growth strategy includes expansion into new product and geographic markets, complex projects and applications, and integrated product offerings to provide turnkey solutions to customers. As a result, we may encounter new types of competition and be required to develop new sales channels. Development of such markets and turnkey solutions is likely to require sustained investment, increase our cost of sales, reduce our gross margins to the extent products purchased from others are integrated into our product offerings, reduce margins due to competition or market conditions, and result in overall reduced profitability. We are also likely to encounter technical challenges and increased costs related to the integration of products from multiple vendors, adaptation and installation of products in larger and more complex plants, ensuring product performance in more difficult operating environments, and meeting unfamiliar customer requirements and performance specifications. Despite rigorous testing and quality processes, newly developed or enhanced products or solutions may encounter challenges during or after their initial introduction or installation. We may also encounter increased warranty costs, performance issues and liability risks from products we sell but do not manufacture.

Our inability to obtain products and components from suppliers would adversely affect our ability to manufacture and market our products.

In certain instances, we depend on original equipment manufacturers and other suppliers of components included in our products for the timely delivery of our integrated turnkey products. As we develop new products and solutions, we may become more dependent on original equipment manufacturers in the future. Such suppliers may experience problems beyond our control, which may disrupt our ability to deliver our products to our customers and damage our relationships with current and future customers. These risks may include varying lead times, supplier capacity, delayed shipments, and quality control problems. In addition, supplier pricing may change and be higher than anticipated. As a result of these and other factors, our revenues and profit margins may be adversely affected.

Our information systems, computer equipment and information databases are critical to our business operations and any damage or disruptions could adversely affect our business and results of operations.

Our operations are dependent on our ability to protect our information systems, computer equipment and information databases from systems failures. Such failures could be caused by internal or external events, such as incursions by intruders or hackers, computer viruses, failures in hardware or software, power fluctuations or cyber terrorists. The failure of these systems to perform as anticipated for any reason or any significant breach of security could disrupt our business and result in numerous adverse consequences, including reduced effectiveness and efficiency of operations, increased overhead costs and loss of important information, which could have a material adverse effect on our business and results of operations.

Our potential inability to retain and recruit experienced management and other key personnel, or the loss of key management personnel, may adversely affect our business and prospects for growth.

Our success depends in part on the skills and experience of our employees. The loss of services of such employees could adversely affect our business until suitable replacements can be found. In addition, our corporate headquarters is located in Walla Walla, Washington, a small, relatively remote geographic location. As such, there may be a limited number of individuals locally with the requisite skill and experience, and we have from time-to-time experienced difficulty recruiting individuals from larger metropolitan areas. The seasonal and cyclical nature of our business may also adversely affect our ability to attract suitable replacements.

Consequently, we may not be able to retain and recruit a sufficient number of qualified individuals on acceptable terms to maintain our business or achieve planned growth. Our success also depends, to a significant degree, upon the continued individual and collective contributions of our management team. A limited number of individuals have primary responsibility for managing our business, including our relationships with key customers. These individuals are integral to our success based on their expertise and knowledge of our business and products. The loss of the services of members of the management team and other key employees for any reason could have a material adverse effect on our business.

13

The potential inability to protect our intellectual property, especially as we expand geographically, may adversely affect our competitive advantage.

Our competitive position may be affected by our ability to protect our proprietary technology. We have obtained certain patents and have filed a number of patent applications. We also anticipate filing patent applications for protection of our future products and technology. There can be no assurance that any such patents will provide meaningful protection for our product innovations, or that the issuance of a patent will give us any material advantage over our competition in connection with any of our products. We may experience additional intellectual property risks in international markets where we may lack patent protection or experience challenges to our intellectual property. The patent laws of other countries differ from those of the U.S. as to the patentability of our products and processes. Moreover, the degree of protection afforded by foreign patents may be different from that of U.S. patents.

Intellectual property-related litigation expenses and other costs resulting from infringement claims asserted against us by third parties may adversely affect our results of operations and our customer relations.

The technologies used by us may infringe the patents or proprietary technology of others. There is also a trend toward aggressive, strategic enforcement of intellectual property rights. As a result, there is a risk that we would be subject to infringement claims which, regardless of validity, could:

• | be expensive, time consuming and divert management attention away from normal business operations; |

• | require us to pay monetary damages or enter into non-standard royalty and licensing agreements; |

• | require us to modify our product sales and development plans; or |

• | require us to satisfy indemnification obligations to our customers. |

Regardless of whether these claims have any merit, they can be burdensome to defend or settle and can harm our business and reputation.

Our financing agreements contain restrictive and financial covenants that may adversely affect us.

Certain of our financing agreements require us to comply with various restrictive covenants and contain financial covenants that require us to comply with specified financial ratios and tests. Our failure to meet these covenants could result in default under these agreements. At September 30, 2014, we were not in compliance with certain of our loan covenants. In the event of default and our inability to obtain a waiver of the default, all amounts outstanding under the loan agreements could be declared immediately due and payable and we would lose the ability to provide customers standby letters of credit and lose our ability to utilize short-term credit facilities. As a result, the failure to comply with these covenants could adversely affect our results of operations and financial condition.

Our dependence on certain suppliers may leave us temporarily without adequate access to raw materials or products.

We rely on third-party domestic and foreign suppliers for certain raw materials. Several of these suppliers are the single source of the raw material. As we develop new and more technologically advanced products, our reliance on single source providers may increase. We do not have long-term contracts with any supplier. We may be adversely affected in the event that these suppliers cease operations or if pricing terms become less favorable. The loss of a key vendor may force us to purchase our necessary raw materials and components in the open market, which may not be possible or may be at higher prices, until we could secure another source. There is no assurance that the terms of any subsequent supply arrangements we may enter into would be as favorable as the supply arrangements we currently have in place. If we are unable to replace a key supplier, we may face delays in delivering finished products, which could have an adverse effect on our sales, financial performance and reputation.

Our operating results are seasonal and may further fluctuate due to severe weather conditions affecting the agricultural industry in various parts of the world.

A large portion of our customer base processes agricultural products and its demand for our products and solutions fluctuates seasonally. These fluctuations can be independent of the effects of changes in general economic conditions. Consequently, we generally experience lower sales and net income in our first two fiscal quarters. As a result of these seasonal and quarterly fluctuations, comparisons of our sales and operating results between different quarters within a single fiscal year may not necessarily provide meaningful comparisons.

14

In addition, in the event of severe weather conditions, geological events or other natural disasters that negatively affect the production of growers, such as prolonged droughts, serious floods or earthquakes, and crop diseases, the food processing industry may not invest in a particular year or years in new equipment in the affected locations. As a result, our revenues, results of operations and cash flows could be materially adversely affected.

The limited availability and possible cost fluctuations of materials used in our products could adversely affect our gross margins.

Certain basic materials, such as stainless steel, are used extensively in our product fabrication processes. Such basic materials have, in the past, been subject to worldwide shortages or price fluctuations related to the supply of, or demand for, raw materials, such as nickel, which are used in their production by our suppliers. A significant increase in the price or decrease in the availability of one or more of these components, subassemblies or basic materials could adversely affect our results of operations.

Our reported results may be affected adversely by the implementation of new, or changes in the interpretation of existing, accounting principles or financial reporting requirements.

Our financial reporting complies with Generally Accepted Accounting Principles (“GAAP”) in the United States, and GAAP is subject to change over time. If new rules or interpretations of existing rules require us to change our financial reporting, our reported results of operations and financial condition could be affected substantially by the new requirements, which could include requirements to restate historical financial statements, and our management may need to devote significant time and financial resources to comply with evolving standards, which may lead to increased general and administrative expenses and a diversion of management time and attention.

Compliance with changing regulation of corporate governance and public disclosure will result in additional expenses to us and pose challenges for our management.

Changing laws, regulations and standards relating to corporate governance and public disclosure, including the Dodd-Frank Wall Street Reform and Consumer Protection Act and the rules and regulations promulgated under that act, the Sarbanes-Oxley Act and SEC regulations, have created uncertainty for public companies and significantly increased the costs and risks associated with accessing the U.S. public markets. Our management will need to devote significant time and our financial resources to comply with both existing and evolving standards for public companies, which will lead to increased general and administrative expenses and a diversion of management time and attention.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

15

ITEM 2. | PROPERTIES |

We own or lease the following properties:

Location | Purpose | Square Feet | Owned or Leased | Lease Expires | Renewal Period |

Walla Walla, Washington | Corporate office, manufacturing, research and development, sales and marketing, administration | 173,000 | Owned | n/a | n/a |

Walla Walla, Washington | Customer Visitor Center, equipment demonstration facility | 31,500 | Leased | 2015 | Two five-year renewal periods |

Redmond, Oregon | Manufacturing, research and development, sales, administration | 19,000 | Leased | 2022 | Two five-year renewal periods |

Beusichem, The Netherlands | Manufacturing, sales and marketing, administration | 45,000 | Leased | 2020 | Five years |

Beusichem, The Netherlands | Warehouse | 11,000 | Leased | 2020 | Five years |

Hasselt, Belgium | Manufacturing, sales and marketing, research and development, administration | 19,500 | Leased | 2016 | Three years |

We also have leased office space for sales and service and other activities in Walla Walla, Washington; Sacramento, California; Dingley, Australia; Querétaro, Mexico; and Rotselaar and Hasselt, Belgium.

We consider all of our properties suitable for the purposes for which they are used.

ITEM 3. | LEGAL PROCEEDINGS. |

From time-to-time the Company is named as a defendant in legal proceedings arising out of the normal course of its business. As of December 5, 2014, the Company was not a party to any material legal proceedings.

ITEM 4. | MINE SAFETY DISCLOSURE. |

Not Applicable.

16

PART II

ITEM 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Market Information

Shares of our common stock are quoted on The NASDAQ Global Market under the symbol “KTEC”. The following table shows the high and low sales prices per share of our common stock, as reported on NASDAQ, by quarter for the two most recent fiscal years ending September 30, 2014:

Stock price by quarter | High | Low | ||||||

Fiscal year ended September 30, 2014 | ||||||||

First Quarter | $ | 15.40 | $ | 13.56 | ||||

Second Quarter | $ | 14.74 | $ | 10.75 | ||||

Third Quarter | $ | 14.70 | $ | 11.50 | ||||

Fourth Quarter | $ | 13.25 | $ | 11.95 | ||||

Fiscal year ended September 30, 2013 | ||||||||

First Quarter | $ | 10.71 | $ | 8.19 | ||||

Second Quarter | $ | 13.09 | $ | 10.14 | ||||

Third Quarter | $ | 16.40 | $ | 12.35 | ||||

Fourth Quarter | $ | 15.50 | $ | 12.21 | ||||

We had approximately 1,352 beneficial owners of our common stock, of which 133 are of record, as of December 5, 2014.

We have not historically paid dividends on our common stock. The board of directors presently intends to continue its policy of retaining earnings for reinvestment in our operations.

Issuer Purchases of Equity Securities

The following table provides information about purchases made by us or on our behalf during the quarter ended September 30, 2014 of equity securities registered by us under Section 12 of the Exchange Act.

Period | Total Number of Shares Purchased(1) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | |||||||

July 1-31, 2014 | — | — | — | ||||||||

August 1-31, 2014 | 110 | $ | 13.16 | — | |||||||

September 1-30, 2014 | — | — | — | ||||||||

Total | 110 | $ | 13.16 | — | 429,202(2) | ||||||

(1) | Includes shares of restricted stock surrendered to satisfy tax withholding obligations by plan participants under our employee stock incentive plans. The shares were subsequently canceled. |

(2) | We initiated a new stock repurchase program effective May 30, 2012. We were authorized to purchase up to 500,000 shares of our common stock under the program. The timing of any repurchases and the exact number of shares of common stock to be purchased will be determined by us and will depend on market conditions and other factors. The program does not incorporate a fixed expiration date. |

17

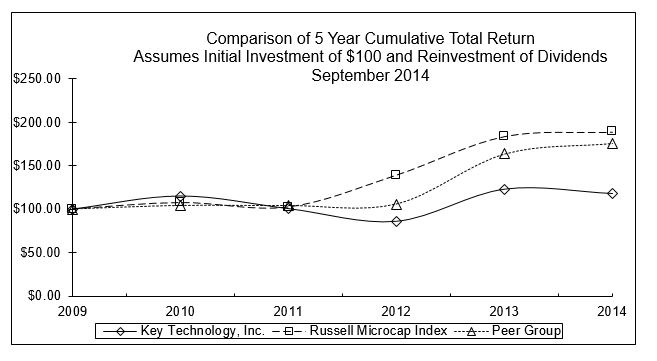

STOCK PERFORMANCE GRAPH

COMPARISON OF FIVE-YEAR CUMULATIVE TOTAL RETURN

AMONG KEY TECHNOLOGY, INC., THE RUSSELL MICROCAP INDEX, AND PEER GROUP

2009 | 2010 | 2011 | 2012 | 2013 | 2014 | |||||||||||||

Key Technology, Inc. | $ | 100.00 | $ | 114.84 | $ | 100.44 | $ | 86.04 | $ | 122.67 | $ | 117.69 | ||||||

Russell Microcap Index | 100.00 | 107.43 | 102.24 | 139.30 | 184.05 | 189.17 | ||||||||||||

Peer Group | 100.00 | 104.03 | 103.89 | 105.75 | 163.61 | 175.92 | ||||||||||||

PEER GROUP: Cognex Corporation, Perceptron, Inc., Flir Systems, Inc., John Bean Technologies Corporation, Tomra Systems, Inc., Isra Vision AG.

18

ITEM 6. | SELECTED FINANCIAL DATA. |

The selected consolidated financial information set forth below for each of the five years in the period ended September 30, 2014 has been derived from our audited consolidated financial statements. The information below should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations and our Consolidated Financial Statements and the Notes thereto as provided in Item 7 and Item 8, respectively, of this Annual Report on Form 10-K.

Fiscal Year Ended September 30, | |||||||||||||||||||||

2014 | 2013 | 2012 | 2011 | 2010 | |||||||||||||||||

(in thousands, except per share data) | |||||||||||||||||||||

Statement of Operations Data: | |||||||||||||||||||||

Net sales | $ | 118,258 | $ | 136,783 | $ | 115,174 | $ | 116,328 | $ | 115,804 | |||||||||||

Cost of sales | 83,961 | 90,739 | 79,339 | 78,531 | 75,651 | ||||||||||||||||

Gross profit | 34,297 | 46,044 | 35,835 | 37,797 | 40,153 | ||||||||||||||||

Operating expenses | 42,309 | 40,213 | 34,867 | 35,310 | 34,896 | ||||||||||||||||

Gain (loss) on disposition of assets | 7 | 42 | (15 | ) | 4 | 77 | |||||||||||||||

Income (loss) from operations | (8,005 | ) | 5,873 | 953 | 2,491 | 5,334 | |||||||||||||||

Other income (expense) | (242 | ) | (460 | ) | (359 | ) | (542 | ) | (172 | ) | |||||||||||

Earnings (loss) from continuing operations before income taxes | (8,247 | ) | 5,413 | 594 | 1,949 | 5,162 | |||||||||||||||

Income tax (benefit) expense | (2,834 | ) | 1,402 | 145 | 495 | 1,524 | |||||||||||||||

Net earnings (loss) | $ | (5,413 | ) | $ | 4,011 | $ | 449 | $ | 1,454 | $ | 3,638 | ||||||||||

Earnings (loss) per share | – basic | $ | (0.86 | ) | $ | 0.69 | $ | 0.08 | $ | 0.27 | $ | 0.69 | |||||||||

– diluted | $ | (0.86 | ) | $ | 0.69 | $ | 0.08 | $ | 0.27 | $ | 0.69 | ||||||||||

Cash dividends per share | $ | — | $ | — | $ | — | $ | — | $ | — | |||||||||||

Shares used in per share calculation | – basic | 6,295 | 5,836 | 5,390 | 5,311 | 5,277 | |||||||||||||||

– diluted | 6,295 | 5,855 | 5,399 | 5,329 | 5,293 | ||||||||||||||||

Balance Sheet Data: | |||||||||||||||||||||

Cash and cash equivalents and short-term investments | $ | 9,741 | $ | 17,601 | $ | 23,755 | $ | 28,754 | $ | 29,096 | |||||||||||

Working capital | 38,203 | 42,338 | 44,136 | 42,484 | 41,475 | ||||||||||||||||

Property, plant and equipment, net. | 16,652 | 17,259 | 18,370 | 19,433 | 16,821 | ||||||||||||||||

Total assets | 98,345 | 114,624 | 86,354 | 94,405 | 91,267 | ||||||||||||||||

Current portion of long-term debt | 804 | 871 | 364 | 345 | 333 | ||||||||||||||||

Long-term debt, less current portion | 4,733 | 5,612 | 4,833 | 5,197 | 5,542 | ||||||||||||||||

Shareholders' equity | 68,168 | 73,125 | 59,430 | 58,774 | 56,338 | ||||||||||||||||

19

ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

Introduction

We and our wholly-owned subsidiaries design, manufacture and sell process automation systems integrating electro-optical inspection, sorting and process systems. We manufacture products in Walla Walla, Washington; Redmond, Oregon; Beusichem, The Netherlands; and Hasselt, Belgium.

Overview