Attached files

| file | filename |

|---|---|

| 8-K/A - CURREENT REPORT ON FORM 8-K - DELTA AIR LINES, INC. | delta_8ka.htm |

Exhibit 99.1

2 This presentation contains various projections and other forward - looking statements which represent Delta’s estimates or expectations regarding future events. All forward - looking statements involve a number of assumptions, risks and uncertainties, many of which are beyond Delta’s control, that could cause the actual results to differ materially from the projected results. Factors which could cause such differences include, without limitation, business, economic, competitive, industry, regulatory, market and financial uncertainties and contingencies, as well as the “Risk Factors” discussed in Delta’s SEC filings. Caution should be taken not to place undue reliance on Delta’s forward - looking statements, which represent Delta’s views only as of the date of this presentation, and which Delta has no current intention to update. In this presentation, we will discuss certain non - GAAP financial measures. You can find the reconciliations of those measures to comparable GAAP measures on our website at delta.com. Safe Harbor

Delta: A High - Quality Company Richard Anderson Chief Executive Officer

A High - Quality Company America’s Best Run Airline Producing Top Line Growth That Increases Margins, Provides Superior Returns On Capital And Generates The Highest Free Cash Flow In The Industry Lowering Business Risk To Drive Sustainable Results By Strengthening The Balance Sheet To Investment Grade Quality And Having The Best Employee Relations Investing In The Future And Rewarding Our Owners With The Highest Cash Levels Returned In The Industry A high - quality S&P 500 industrial that delivers growing value for its employees, customers and investors 4

A High - Quality Company • 11 - 14% operating margins • 2014: 13% Operating Margin • Annual EPS growth of 10% - 15% after 2014 • 2014: 70% on pre - tax basis EPS Growth • 15 - 18% return on invested capital • 2014: 20% ROIC • $6 billion annual operating cash flow and $3 billion free cash flow • 2014: $6 billion operating cash flow and $3 billion+ free cash flow Cash Flow • $5 billion adjusted net debt by 2016 and pension at 80% funded status by 2020 • 2014: $7.2 billion adj. net debt at year - end Balance Sheet Long - Term Goals Strong progress toward our long - term goals of generating solid margins and cash flow, an investment grade balance sheet and sustainable shareholder returns 10 - 15% 11.6% 14.5% 15 - 18% Return on Invested Capital EPS Growth 12.3% 10 - 15% Delta - Goal Delta - Goal S&P 500 Industrials 2014 - 16 consensus S&P 500 Industrials 2014 - 16 consensus Note: All results exclude special items ; Delta ROIC reflects benefits of n et operating losses 5

The Path To Value Creation Delta S&P Industrials Free Cash Flow Delta S&P Industrials EPS Growth Note: S&P Industrials are 2014 - 16 consensus estimates obtained from FactSet. Delta P/E reflects benefit of NOLs. Delta S&P Industrials Forward Price/Earnings Delta S&P Industrials Free Cash Flow Yield Achieving our long - term goals and lowering risk across the business should result in improved valuation Delta S&P Industrials ROIC 10 - 15% 12.3% 15 - 18% 14.5% $3B+ $1.7B 9.6x 17.1x 10% 5.5% 6

Delivering Growing Value Ed Bastian President

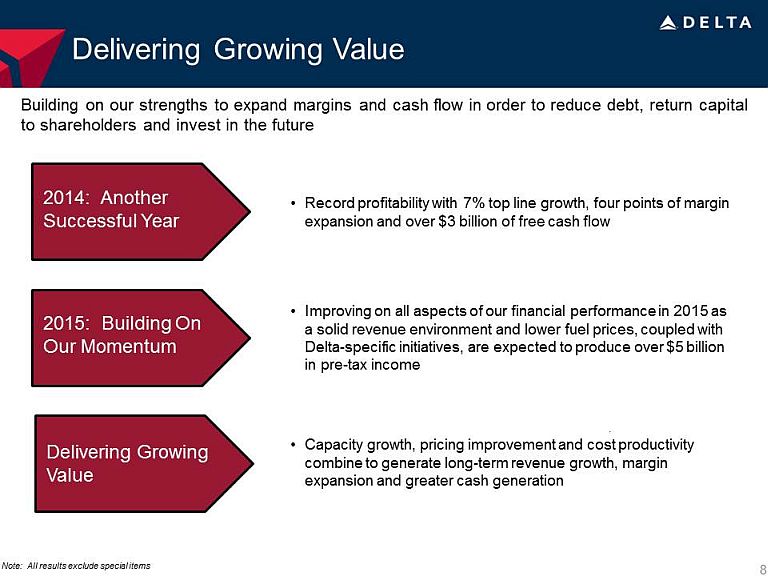

Delivering Growing Value 2014: Another Successful Year 2015: Building On Our Momentum Delivering Growing Value Building on our strengths to expand margins and cash flow in order to reduce debt, return capital to shareholders and invest in the future • Record profitability with 7% top line growth, four points of margin expansion and over $3 billion of free cash flow • Capacity growth, pricing improvement and cost productivity combine to generate long - term revenue growth, margin expansion and greater cash generation • Improving on all aspects of our financial performance in 2015 as a solid revenue environment and lower fuel prices, coupled with Delta - specific initiatives, are expected to produce over $5 billion in pre - tax income Note: All results exclude special items 8

2014: Another Record Year …Leads To Record Financial Results • Industry - leading operational performance • Strong improvements in customer satisfaction with increasing net promoter scores • Named “Airline of the Year” by Air Transport World, one of Fortune’s “Most Admired Companies”, “Best Airline” by Business Travel News for the fourth year in a row and “Most Preferred Corporate Carrier” by Morgan Stanley’s corporate travel survey • Increased revenue premium versus the industry • Non - fuel unit cost growth of 0.3% • Pre - tax income of $4.5 billion, an increase of 70% or $1.9 billion • Generated a 20% return on invested capital • Record earnings result in more than $1 billion profit sharing for Delta employees • $6 billion of operating cash flow and over $3 billion of free cash flow, allowing for $2 billion in debt reduction and $1.35 billion returned to shareholders Running A Reliable, Customer - Focused, Efficient Airline… Completing a record year with $4.5 billion of pre - tax earnings, over $3 billion of free cash flow and a 20% return on invested capital Note: All results exclude special items 9

Taking Momentum Into 2015 December quarter caps a successful year of top line growth, margin expansion and free cash flow generation Operating margin 11.5% - 12.5% PRASM change year over year Up 1.0 – 1.5 % Fuel price $2.63 - $2.68 CASM – Ex Fuel change year over year Up ~1% System capacity change year over year Up ~3.5% Note: Fuel price includes taxes, settled hedges, refinery contribution and excludes mark to market adjustments on open hedges; CASM – Ex Fuel un it cost excludes special items December Quarter 2014 Forecast 10

The Backdrop For 2015 Improving on all aspects of our financial performance in 2015 as a solid revenue environment, lower fuel prices and Delta - specific initiatives produce another record year Across The Industry At Delta • Modest economic growth globally, with best economies in North America driven by the strong dollar • Continued international headwinds from weakening euro and yen and Asian capacity growth in excess of demand • Solid corporate travel environment with Global Business Travel Association expecting 6 % increase in corporate travel spend • Market fuel prices of $2.10 - $2.20 per gallon – 7 0¢ lower than 2014 – representing a ~$3 billion run - rate savings in the future for Delta • Increasingly rational industry structure as merger integrations progress • Disciplined approach to capacity – modest system capacity growth of 2%, with domestic up 3% and international up less than 1% • Focus on bringing fuel savings to the bottom line – at current market prices, Delta’s net fuel benefit is $1.7 billion • Further margin expansion through higher revenues, lower fuel costs and continued non - fuel cost productivity • Top line growth driven by capacity growth plus pricing improvements • Upgauging and other cost initiatives keep non - fuel cost growth below 2% 11

$1.50 $2.00 $2.50 $3.00 $3.50 Jan Mar May Jul Sept Nov Fuel Declines Provide Earnings Tailwind At current market prices, fuel declines provide net $1.7 billion benefit to Delta • At current forward curve, Delta’s 2015 all - in fuel price is forecasted at $2.40 – $2.50 per gallon, including hedge and refinery impact – Each 1 ¢ change in fuel price is worth $40 million for Delta • Commercial organization focused on bringing fuel savings to the bottom line – No change to 2015 capacity plans in light of lower fuel prices • Hedge book allows for ~65% downward participation in 2015 while maintaining upside protection – With recent sharp decline in fuel prices, hedge book expected to produce $1.2 billion loss for 2015 at current market prices – Delta has full downside participation in 2016 Market Jet Fuel Prices 2014 actual 2015 forward curve 12 Note: Market fuel prices include taxes and transportation costs

A High - Quality Company • 11 - 14% operating margins • 2014: 13% Operating Margin • Annual EPS growth of 10% - 15% after 2014 • 2014: 70% on pre - tax basis EPS Growth • 15 - 18% return on invested capital • 2014: 20% ROIC • $6 billion annual operating cash flow and $3 billion free cash flow • 2014: $6 billion operating cash flow and $3 billion+ free cash flow Cash Flow • $5 billion adjusted net debt by 2016 and pension at 80% funded status by 2020 • 2014: $7.2 billion adj. net debt at year - end Balance Sheet Long - Term Goals Strong progress toward our long - term goals of generating solid margins and cash flow, an investment grade balance sheet and sustainable shareholder returns 10 - 15% 11.6% 14.5% 15 - 18% Return on Invested Capital EPS Growth 12.3% 10 - 15% Delta - Goal Delta - Goal S&P 500 Industrials 2014 - 16 consensus S&P 500 Industrials 2014 - 16 consensus Note: All results exclude special items ; Delta ROIC reflects benefits of NOLs 13

Continuing To Drive Margin Expansion Disciplined Capacity Growth • Drive capacity growth through better utilization of assets, producing more seat departures and higher capacity on a smaller fleet • Focus capacity growth on high - revenue, restricted/constrained markets Pricing Improvements • Investments in network, product and service producing sustainable revenue gains • Next phase of revenue initiatives focus on better customer segmentation and improved offerings for high - value customers Cost Productivity • Maximizing the benefits of scale throughout the network to improve cost efficiency • Focus on bringing fuel benefit to the bottom line • Leveraging supply chain, technology and maintenance expertise to improve productivity Capacity growth, pricing improvement and cost productivity combine to generate long - term revenue growth, margin expansion and greater cash generation 14

Top Line Growth Enhances Returns 15 Disciplined approach to growing the business drives higher earnings, cash flow and returns on capital for our shareholders • Capacity additions must be margin accretive, cash flow positive and not add incremental debt to the balance sheet • Producing higher capacity levels on a smaller fleet with low ownership cost generates better returns on invested capital • Limit fixed costs associated with capacity additions through better utilization of existing assets • Improved employee productivity allows for disciplined frontline hiring levels and limited merit headcount additions • Drive benefits of scale from merger and other initiatives, primarily in key domestic hubs • Seize unique opportunities in high - revenue, restricted/ constrained markets – New York, London, Los Angeles, etc. Contributes To Long - Term Financial Goals Leverages Our Strengths Limits Incremental Cost

Domestic Refleeting Improves Asset Utilization Higher domestic capacity levels on a lower capital base produce improvements in ROIC • 2015 domestic capacity growth driven by higher gauge and better asset utilization – 3% higher capacity on flat departures and 11 fewer aircraft • Increasing average seats per departure by 15% between 2012 and 2017: – Upgauging: Using 717, 737 - 900, and A321 deliveries to retire smaller gauge, less efficient aircraft – Modifications: Projects on over 110 aircraft in 2015, adding an average of nine seats per plane; over 450 aircraft have already been modified since 2007 • More efficient capacity generation drives margin expansion, cost productivity and better returns on invested capital • Mix of new and used aircraft keeps ownership costs low, allows flexibility to quickly and efficiently adjust capacity levels • Lowest ownership cost in the industry with lowest maintenance unit costs and best reliability Post - Merger Domestic Fleet Trends 80 90 100 110 120 Merger Close 2009 2010 2011 2012 2013 2014 2015 Note: Margin data Profit Margin Capacity Aircraft Quantity 114 86 99 Index value at merger close = 100 16

Corporate Customers Are Choosing Delta 7% 11% 6% 7% 9% 11% 11% 14% Total Other Business Services Technology Banking Automotive Media Financial Services Running a high - quality, customer - focused airline… …Produces strong gains in corporate revenues Momentum continues as corporate revenues have increased by 7% this year Source: Alphawise, Morgan Stanley Research YTD Ticketed Revenue vs Prior Year 17 6 7 7 6 6 5 5 4 1 1 1 1 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Leading Carrier Year Footprint Lift Quality of Product Reliability Price of Package 2015 Delta Delta Delta Delta Delta 2014 United United / Delta Delta Delta Delta 2013 United United Delta Delta Delta 2012 United United Delta Delta Delta 2011 Delta United Continental / Delta Continental Delta 2015 Morgan Stanley Global Corporate Travel Survey Business Travel News Survey

Enhanced Agreement With American Express Partnering with American Express since 1996 to create the world’s most valuable airline co - brand portfolio • New, multi - year contract with American Express continues growth momentum of Delta’s $2 billion co - brand revenue stream • Significantly improved economics achieved across multiple business lines including co - brand card, Membership Rewards, Sky Club, and Merchant Services – Early renewal increases effective rate by 15% starting in January 2015 and 20% over the new contract period – New agreement will double benefits to Delta over the next five years • Leveraging American Express’ unique position as both credit card provider and largest global travel agency 18

Strong Position In Heathrow Through Virgin Atlantic Virgin Atlantic partnership and equity stake expected to generate over $ 200 million in benefit for Delta in 2015 Glasgow Manchester London Heathrow London Gatwick Belfast DTW ORD MSP LAS LAX SFO SEA CUN MCO IAD JFK & EWR BOS ATL MIA PHL Additional Frequency New Market Operator Swap JFK - LHR #8 LAX - LHR #3 ATL - LHR #4 MIA - LHR #2 SFO - LHR #2 JFK - MAN LAS - GLA MCO - GLA ATL - MAN DTW - LHR EWR - LHR MCO - BFS PHL - LHR 2015 U.K. JV Network Changes • First year of joint venture has produced significant increase in JV network profitability – LHR unit revenues up 7% and JV margins improved by over 3 points on 4% capacity growth • Joint venture US - UK capacity to increase ~10% in 2015 to 39 peak daily round trips – Growth led by Virgin Atlantic, which will reallocate aircraft and Heathrow slots from its Pacific and Africa networks • Linking Virgin’s extensive UK network into Delta’s US hubs leverages scale at both carriers – Provides significant opportunity to improve yields, while providing better connecting opportunities for passengers 19

Restructuring The Pacific Network Restructuring our approach to serving the Pacific is largest margin improvement opportunity in the network • Continue to build domestic feed into Seattle hub, increasing to 120 peak daily departures in 2015 • Network offers one - stop service to 95% of West Coast to Asia traffic flows Leverage Domestic Network Scale • Reduce 2015 Pacific capacity levels by 6 - 8%, including a 15% reduction from Japan in light of weakening yen which is mitigated by expected 2015 yen hedge benefit of $145 million • Increase direct flights to non - Japan Asia by 10 - 15% Adjust Capacity Levels • Introduce smaller gauge aircraft into the market, allowing for complete retirement of 747 fleet by 2017 • Flying backfilled by A330s and A350s – a 15 - 20% reduction in seats per departure and >20% improvement in cost per seat Downgauge Flying • Recalibrate Narita hub to improve service for local passengers • Will serve 5 intra - Asia routes in 2015, down from 12 in 2009 Realign Narita Hub Goal to increase Pacific margins by 5 - 10 points over next 3 years 20

Delivering Growing Value 2014: Another Successful Year 2015: Building On Our Momentum Delivering Growing Value Building on our strengths to expand margins and cash flow in order to reduce debt, return capital to shareholders and invest in the future • Record profitability with 7% top line growth, four points of margin expansion and over $3 billion of free cash flow • Capacity growth, pricing improvement and cost productivity combine to generate long - term revenue growth, margin expansion and greater cash generation • Improving on all aspects of our financial performance in 2015 as a solid revenue environment and lower fuel prices, coupled with Delta - specific initiatives are expected to produce over $5 billion in pre - tax income Note: All results exclude special items 21

Running A Reliable, Customer - Focused Operation Gil West Chief Operating Officer

Delta Wins Best Airline 1 st Place Virgin America 2 nd Place Alaska 3 rd Place jetBlue 4 th Place Frontier 5 th Place Southwest 6 th Place American 7 th Place United 8 th Place Top Airlines For Overall Performance Note: Rankings determined by combining the airlines’ score in all categories. Southwest includes consolidated results for Southwest and AirTran; American includes consolidated results for American and US Airways. Source : airfarewatchdog, published 8/8/14 23

Delivering Top Tier Operational Results Top Of Industry Operational Performance 96.9% 98.1% 98.3% 98.5% 99.1% 94% 96% 98% 100% jetBlue American United Southwest Delta DOT Completion Factor 72.1% 73.4% 75.7% 77.7% 82.4% 65% 70% 75% 80% 85% 90% Southwest jetBlue United American Delta DOT On - Time 4.31 3.76 3.68 2.44 2.08 1.5 2.5 3.5 4.5 5.5 Southwest American United Delta jetBlue DOT Missed Bag Ratio (Per 100,000 enplanements) 24 Note: Figures cover the time period January 2014 through September 2014; American includes consolidated results for American and US Airways

40 102 146 2012 2013 2014 14 67 79 2012 2013 2014 5,647 3,134 1,244 792 472 2010 2011 2012 2013 2014 Driving Core Reliability Performance • Lowest fleet capital cost • Lower inventory ownership • Best reliability • Lowest maintenance CASM TechOps Leverage TechOps YTD Performance - 92% 464% 265% • 40% reduction in cancellations • 11% reduction in delays 100% Completion Factor Days 100% Maintenance Completion Factor Days Maintenance Cancellations 25 Note: Full year 2014 “Maintenance Cancellations” are estimated; “100% Maintenance Completion Factor Days ” and “100% Completion Factor Days” cover the time period January through November for each year presented.

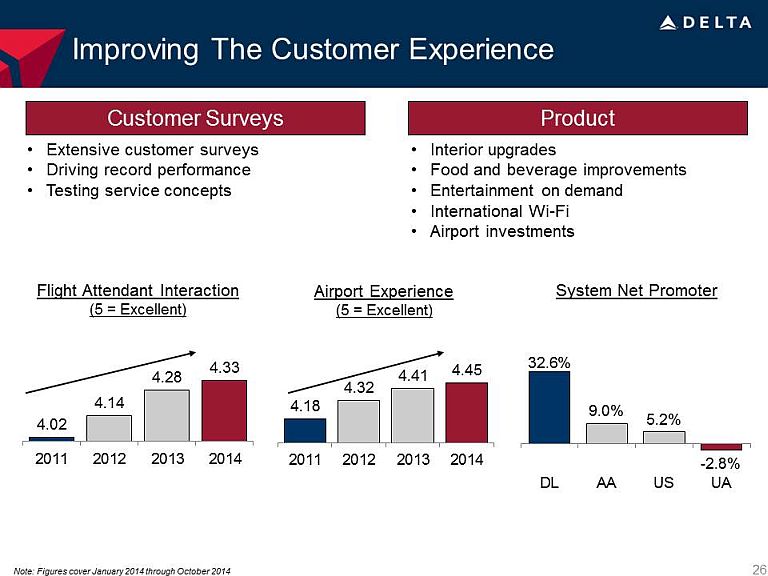

4.02 4.14 4.28 4.33 2011 2012 2013 2014 Improving The Customer Experience • Extensive customer surveys • Driving record performance • Testing service concepts Customer Surveys Product • Interior upgrades • Food and beverage improvements • Entertainment on demand • International Wi - Fi • Airport investments 4.18 4.32 4.41 4.45 2011 2012 2013 2014 Airport Experience (5 = Excellent) Flight Attendant Interaction (5 = Excellent) 26 32.6% 9.0% 5.2% - 2.8% DL AA US UA System Net Promoter Note: Figures cover January 2014 through October 2014

Investing In Our Fleet For A Better Customer Experience • 757 - 200 (“E” subfleet) – New interior / flat - bed seats in Delta One cabin – 18 aircraft • 757 - 200 – New interior and standardization at 199 passengers – 56 aircraft • 757 - 300 – New interior, AVOD & satellite TV – 16 aircraft • A319 – New interior including AVOD & satellite TV – 57 aircraft • A320 – New interior – 69 aircraft • 737 - 800 – Standardize fleet with AVOD & satellite TV – 43 aircraft • Wi - Fi – ATG4 and International Wi - Fi Significant Product Investments Continue … 27

Driving Our Revenue Momentum Glen Hauenstein Chief Revenue Officer

The Path To Further Revenue Gains Leveraging our strengths to produce further revenue gains Give Customers What They Value Sell An Experience Build A Strong Brand • Optimize hub network to more efficiently serve domestic markets • Make investments to increase the range and quality of products available to customers • Refine core pricing to reflect the value of providing a customer - focused, reliable airline experience • Continue to increase ancillary revenues by allowing each passenger to customize their travel experience through segmented, Branded F are products • Change the SkyMiles program to maximize appeal, status and rewards for high value customers • Building a brand that embodies what customers value ensures that Delta grows its revenue premium and enables greater customer segmentation • Delta is an innovative, thoughtful and reliable airline for its customers 29

Giving Customers What They Value Drives Revenue Growth Investments in network, product and service have already produced solid, sustainable revenue gains with more room for growth Network Product Service • Optimizing capacity to leverage hub strengths and serve high revenue markets efficiently • Refleeting and product investments increase the range and quality of products for domestic and international customers • Operational reliability shows customers that we value their time 97% 100% 107% 2005 2010 YTD 2014 Delta Passenger Unit Revenue Vs A4A Average 10 pts $28.5B $31.8B $40B+ 2005 2010 2014E Total Revenue 40+% 9.5¢ 11.7¢ ~14.6¢ 2005 2010 2014E Passenger Unit Revenue 54% * *2005 numbers adjusted to include Northwest Airlines 30 * *

Investments In The Network To Improve Margin Optimize capacity to leverage hub strengths and serve high - revenue markets West Coast • Achieved the leading position in the world’s largest aviation market • Initiatives to date have created scale in key business markets and access to London Heathrow, driving Delta’s first profit in New York • Next phase of initiatives to grow premium revenues and expand margins by leveraging JV with Virgin Atlantic, improving fleet mix and continuing to invest in facilities at both JFK and LGA • Continue to develop Seattle hub as part of Pacific restructuring strategy – intra - west network now serves 95%+ of US/Canada West Coast to Asia demand • Refine Los Angeles hub with completion of schedule build - out and facility upgrades • Combined Los Angeles, Seattle and Salt Lake City positions provide unique West Coast network coverage • Completing major capacity investment in Latin America with profitability and margins improving as additions mature • Growth in 2015 is front loaded and focused on Mexico, Brazil and Caribbean, with entity growth tapering for the second half of the year • Enhancing alliances with GOL and Aeromexico to drive increased premium traffic in Brazil and Mexico New York West Coast Latin America 31

Higher Revenue Through Better Customer Segmentation Industry - leading consumer products in each of four Branded F are categories, allowing customers to tailor their travel experience Delta One / First Class Delta Comfort+ Main Cabin Basic Economy Delta One / First Class Main Cabin / Basic Economy Delta Comfort+ Delta One / First Class Best - in - class product that includes a spacious seat, pillow and blanket, food options, premium entertainment and priority boarding Delta Comfort+ A distinctive product designed for travelers who desire an elevated experience, including an upgraded snack basket, complimentary alcohol, early boarding, additional leg room, dedicated overhead bin space and free premium entertainment Main Cabin Best - in - market core product, including advance seat selection, access to Wi - Fi, snacks, complimentary entertainment, full Medallion benefits and premium cabin upgradability Basic Economy Best - in - class transportation targeted at price conscious consumers who are indifferent to flexibility or seat selection (and often buy at OTAs) Total Branded Fares opportunity estimated at $1.5 billion+ annually by 2018 32

Seat - Related Revenue Gains Branded Fares will continue momentum for seat - related revenues, including First C lass upsell and Delta Comfort+ • First Class revenue is expected to benefit from the continued annualization and expansion of post - purchase upsell • As Delta continues to upgauge its fleet, Delta Comfort+ seats will comprise a greater percentage of seat count; further upside from improvements in distribution and revenue management techniques Premium seats to drive over $1B in revenue in 2015, a $250M+ increase YoY 31% 36% 40% 45% 50% 2011 2012 2013 2014 2015 Goal Domestic Paid First Class Load Factor 18,417 18,420 19,131 18,467 24,264 2011 2013 2015 First Class / Delta One Delta Comfort+ 36,887 43,395 135% 33 First Class / Delta One / Delta Comfort+ Seats

Thoughtfully Rewarding Our Most Valuable Customers Changes to the SkyMiles program help to maintain our revenue premium and reduce seasonal revenue volatility • Earning miles for award travel based on spend aligns incentives to ensure that largest rewards, both in mileage and benefits, are offered to the customers who spend more with Delta • Flexible redemption makes more seats available to members while adding revenue during low demand periods • Improved SkyMiles program drives additional value into the Delta / American Express Relationship 34

Powerful Brand Drives Sustainable Revenue Premium Building a brand that embodies what customers value improves customer loyalty, enables customer segmentation and drives a sustainable revenue premium Innovative Thoughtful Reliable • Contemporary, progressive products so that customers trust that the Delta experience is better • Personally accountable to customers, so that they trust the company to have their best interests at heart • Greater consistency and sustained operational excellence, so that customers can depend on Delta A powerful brand that customers are willing to pay a premium to fly 35

Delivering On Our Financial Goals Paul Jacobson Chief Financial Officer

• Strong operating cash flow funds $2 - $3 billion reinvestment in the business annually while generating over $3 billion of free cash flow • Disciplined capital process to ensure return and payback targets are met • Solid cost performance with 2014 non - fuel unit costs increasing less than 1% on 3% higher capacity • Focused on productivity throughout the total cost structure • Balanced capital allocation drives value to shareholders by de - risking the enterprise and returning cash to shareholders Delivering On Our Financial Goals Managing Our Costs Staying Disciplined With Capital Balanced Capital Deployment Building a durable franchise with consistent cost performance, a strong balance sheet and balanced capital allocation 37

Maintaining Our Cost Performance Pipeline of initiatives in place to maintain non - fuel unit cost growth below 2% annually 4.6% 2.4% 0.3% 2012 2013 2014E 2015E 0 - 2% Non - Fuel Unit Cost Growth Excludes special items Solid financial plan in place to deliver second consecutive year of sub - 2% unit cost growth • Benefits from upgauging, maintenance savings and commercial productivity initiatives provide foundation to build upon in 2015 – Upgauging : Improved operating leverage to be achieved as modifications continue next year and increase the gauge on over 110 aircraft – Refleeting : Retirement of 747s, older 757s and domestic 767s drive almost $200 million of maintenance savings in 2015 – Maintenance: Ongoing utilization of part - out materials – Supply Chain: Leveraging scale to improve contract terms – Technology : Improves front - line productivity and delivers an improved customer experience • Additional focus on keeping fixed cost base low – Nearly 60% of all - in unit costs (including fuel) are variable 38

Actively Managing Delta’s Largest Expense Multi - faceted approach to managing Delta’s $11 billion fuel bill involves hedging, the refinery and logistics expertise • Goal is to generate an 8 - 10 ¢ advantage to industry average • Hedging program sacrifices some downside participation to protect against spikes in commodity prices in a cost - efficient manner • The refinery increases supply of jet fuel to the market which results in lower prices while also serving as a hedge against crack spreads – So far this quarter, jet cracks are up $2.50 per barrel compared to last year, and the refinery is projected to lower our fuel expense by $70 million • Logistics expertise creates opportunities to drive efficiency and value through the fuel supply chain Average Fuel Price DAL vs Industry $3.26 $3.07 $2.88 $3.25 $3.12 $2.97 2012 2013 2014E Delta Industry (ex DAL) 39

NOLs Are Valuable Asset • Net operating loss carryforwards are applied against taxable income, which is usually lower than reported book income – Equates to a longer runout period of the net operating loss carryforwards • Working to minimize tax exposure and preserve net operating loss carryforwards – Accelerated cash contributions to pension plans have preserved nearly $200 million of NOLs to date – Accelerated depreciation on long - lived assets allows for further preservation of our NOLs • 2015 book tax rate is estimated at ~38% and consistent with 2014 • NOLs will defer payment of cash taxes through 2017 $ 16.3B $ 15.3B $ 12.4B 2012 2013 2014E Net Operating Loss Carry Forwards Active management of our net operating loss carryforwards will defer the payment of cash taxes for several years 40

Disciplined Reinvestment In The Business Strong operating cash flow funds appropriate level of reinvestment while allowing for significant free cash flow generation 2015E 2016E 2017E 2018E 2019E Other Fleet/Mods Capital Expenditures • Disciplined capital process with senior management approval for capital requests greater than $1 million ensuring that investments meet 15 – 18% return on invested capital target with a typical payback of less than 2 years • Capital expenditures projected at $2 - $3 billion per year or ~50% of operating cash flow – Targeting $2.8 billion of capital expenditures for 2015 • Capital spend 2015 – 2019 primarily focused on new aircraft – Capital plans include flexibility to adjust spending levels if necessary • New deliveries cover refleeting of widebodies and large narrowbodies – 150 new aircraft to be delivered over next five years, including widebodies needed for Pacific restructuring – Maintain diversified fleet strategy consisting of new and opportunistic purchase of used aircraft New Aircraft Deliveries 25 38 42 36 9 $2 - $3 Billion Annually 41

Generating Solid Cash Flows From The Business $2.6 $3.8 $4.1 $4.8 $4.1 $2.9 $1.8 $1.3 $1.2 $0.9 $2.1 $2.6 $1.2 $1.3 $1.3 $2.0 $2.9 $2.2 $(2.0) $(1.0) $- $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E CapEx Operating Cash Flow Capital Spending and Operating Cash Flow ($B) Note: Includes pre - merger NWA; Excludes special items Since 2010, Delta has generated more than $9 billion in free cash flow while making prudent investments in the business 42

Balanced Capital Deployment Drives Value Reinvest In The Business • ~50% of operating cash flow reinvested in the business • Plan to invest $2 - $3 billion annually into fleet, products, facilities and technology Strengthen The Balance Sheet • Over $4 billion in debt reduction in last two years • Addressing pension with $500 million in excess contributions made to date • Moving toward investment grade with three upgrades in last 18 months • Only two notches away from achieving investment grade Return Cash To Shareholders • Returned $1.7 billion in first 18 months of program, including $1.35 billion in 2014 • On track to complete $2 billion repurchase authorization by end of 2015, one year ahead of expiration Balanced approach to capital deployment has driven significant value for shareholders in the past two years 43

Paying Down Debt Remains A Priority Clear path to achieve $5 billion debt target in 2016, resulting in $1 billion of run - rate interest savings versus 2009 $ 17.0B $ 15.0B $ 12.9B $ 11.7B $ 9.4B $ 7.2B < $6.0B 2009 2010 2011 2012 2013 2014E 2015E Adjusted Net Debt Interest $1.3B $1.2B $1.1B $1.0B $850M $650M $475M Expense 44

2013 2014 2015E Proactively Managing Our Pension Obligations • Pension funding remains manageable, with required funding levels at ~$700 million per year – Expect to contribute incremental $250 million in 2015, which will bring total incremental contributions to $750 million since 2013 • Incremental funding and acceleration of required funding helps lower pension expense – 2015 pension expense estimated at $200 million, $35 million lower than 2014 • Expense includes impact of higher liability due to interest rates and mortality table adjustments • Goal remains to achieve 80% funded status by 2020, despite headwinds from declining interest rates and actuarial changes $ 354M $ 234M $200M 2013 2014 2015E Pension Funding Pension Expense $915M $920M $920M Pension funding remains stable while pension expense continues to decline 45

Continuing To Strengthen The Balance Sheet Significant progress toward achieving investment grade metrics 12% 20% 29% 2012 2013 2014E 2015E 34% - 36% S&P Industrial Average Median BBB 34% BB 25% S&P Industrial Average Median BBB 8.2x BB 4.8x S&P Industrial Average Median BBB 2.3x BB 3.2x FFO / Debt EBITDA / Interest Debt / EBITDA 5.9x 3.4x 2.7x 2012 2013 2014E 2015E 2.7x 3.6x 5.2x 2012 2013 2014E 2015E Delta’s 2012 and 2013 metrics shown above are sourced from S&P’s website. Delta’s forecasted 2014 and 2015 metrics apply S&P ’s calculation methodology to Delta’s internal forecasts. Benchmarks are based on Three Year US Industrial Average Medians as of 12/08/13, sourced from S&P’s website. Funds from operations, adjusted (“FFO”) represents operating income plus depreciation & amortization and imputed operating le ase depreciation and adjustments for other noncash items; Debt, adjusted represents total debt and capital lease obligations plus the imputed present value of operating leases and tax effec ted postretirement benefit obligations and is generally adjusted for S&P’s calculation of Delta’s surplus cash; EBITDA, adjusted represents earnings before interest, taxes, depreciation & amortization (i ncluding imputed operating lease interest and depreciation) and adjustments for other noncash items; Interest, adjusted represents interest expense, net, amortization of debt discount, net, im puted operating lease interest, and pension interest costs net of the expected return on plan assets. 5.5x – 6.0x 2.0x – 2.5x 46

…is now competing on capital returns Will return more than 40% of free cash flow to shareholders in 2014 17% 42% 2013 2014 Strong Commitment To Returning Cash To Shareholders Capital Returns As A Percentage Of Free Cash Flow Cash Returned To Shareholders $ 100M $ 250M $ 250M $ 1,100M 2013 2014 Dividends Share Repurchases $350M $1,350M • Returned $1.35 billion to shareholders in 2014, a $1 billion increase over 2013 • $250 million returned through dividends – Represents our long - term commitment to return cash to our shareholders – 50 % increase to dividend during 2014 • $1.1 billion returned through share repurchases – Completed $850 million of $2 billion repurchase authorization, including $500 million in December quarter – Plan to complete remainder of current authorization by end of 2015, one year ahead of schedule – Share repurchase program provides flexibility to return additional cash to shareholders – Minimum of $1.5 billion to be returned in 2015 • Will update in May 2015 47

Continuing T o De - Risk The Business Lower Business Risk • Better revenue generation through capacity discipline, top line diversification and international joint ventures • Lower fixed cost structure Lower Labor Risk • Industry - leading labor relations with a strong pay - for - performance culture Lower Fuel Risk • Refinery investment, actively - managed hedging program and team with significant external oil/gas expertise Lower Financial Risk • Reduced debt by $10 billion over past five years while also proactively addressing pension obligations A company positioned to produce solid profitability and cash flows throughout the business cycle Taking risk out of the business produces more sustainable, consistent results 48

The Path to Value Creation Delta S&P Industrials Free Cash Flow Delta S&P Industrials EPS Growth Note: S&P Industrials are 2014 - 16 consensus estimates obtained from FactSet. Delta P/E reflects benefit of NOLs. Delta S&P Industrials Forward Price/Earnings Delta S&P Industrials Free Cash Flow Yield Achieving our long - term goals and lowering risk across the business should result in improved valuation Delta S&P Industrials ROIC 10 - 15% 12.3% 15 - 18% 14.5% $3B+ $1.7B 9.6x 17.1x 10% 5.5% 49

| 50 |

Non-GAAP Financial Measures

Delta sometimes uses information ("non-GAAP financial measures") that is derived from the Consolidated Financial Statements, but that is not presented in accordance with accounting principles generally accepted in the U.S. (“GAAP”). Under the U.S. Securities and Exchange Commission rules, non-GAAP financial measures may be considered in addition to results prepared in accordance with GAAP, but should not be considered a substitute for or superior to GAAP results. The tables below show reconciliations of non-GAAP financial measures used in this presentation to the most directly comparable GAAP financial measures.

Forward Looking Projections. Delta is unable to reconcile certain forward-looking projections to GAAP as the nature or amount of special items cannot be estimated at this time.

Operating Margin, adjusted

Delta excludes MTM adjustments and restructuring and other items from operating margin for the reasons described below:

Mark-to-market adjustments on fuel hedges recorded in periods other than the settlement period ("MTM adjustments"). MTM adjustments are based on market prices at the end of the reporting period for contracts settling in future periods. Such market prices are not necessarily indicative of the actual future value of the underlying hedge in the contract settlement period. Therefore, excluding these adjustments allows investors to better understand and analyze the company’s core operational performance in the periods shown.

Restructuring and other items. Restructuring and other items include fleet and other charges, severance and related costs and a litigation settlement in 2014. Because of the variability in restructuring and other items, the exclusion of this item is helpful to investors to analyze the company’s recurring core operational performance in the periods shown.

| (Projected) Three Months Ended December 2014 | (Projected) 2014 | |||

| Operating margin | (2.6) - (1.6)% | 8% | ||

| Items excluded: | ||||

| MTM adjustments | 14.0% | 4% | ||

| Restructuring and other items | 0.1% | 1% | ||

| Operating margin, adjusted | 11.5 to 12.5% | 13% |

| 51 |

Pre-Tax Income & Margin, excluding special items

Delta excludes special items from pre-tax income (also referred to as pre-tax earnings), pre-tax margin and other measures because management believes the exclusion of these items is helpful to investors to evaluate the company’s recurring core operational performance in the periods shown. Therefore, we adjust for these amounts to arrive at more meaningful financial measures. Special items excluded in the tables below showing the reconciliation of pre-tax income and margin, excluding special items are restructuring and other items and MTM adjustments (for the same reason as discussed above in operating margin, adjusted) and the following:

Loss on extinguishment of debt and other. Because of the variability in loss on extinguishment of debt and other, the exclusion of this item is helpful to investors to analyze the company’s recurring core operational performance in the periods shown.

| (Projected) | ||||||||||||||||

| (in billions) | 2014 | 2013 | Change | |||||||||||||

| Pre-tax income | $ | 1.8 | $ | 2.5 | ||||||||||||

| Items excluded: | ||||||||||||||||

| Restructuring and other items | 0.7 | 0.4 | ||||||||||||||

| MTM adjustments | 1.7 | (0.3 | ) | |||||||||||||

| Loss on extinguishment of debt and other | 0.3 | – | ||||||||||||||

| Pre-tax income, excluding special items | $ | 4.5 | $ | 2.6 | $ | 1.9 | 70% | |||||||||

| (Projected) | ||||||||||||

| 2014 | 2013 | Change | ||||||||||

| Pre-tax margin | 4.5% | 6.7% | ||||||||||

| Items excluded: | ||||||||||||

| Restructuring and other items | 1.8% | 1.1% | ||||||||||

| MTM adjustments | 4.3% | (0.7)% | ||||||||||

| Loss on extinguishment of debt and other | 0.6% | – | ||||||||||

| Pre-tax margin, excluding special items | 11.2% | 7.1% | 4.1 pts | |||||||||

| (Projected) | ||||||||||||

| (in millions, except per share data) | 2014 | 2013 | Change | |||||||||

| Pre-tax income, excluding special items | $ | 4,522 | $ | 2,675 | ||||||||

| Weighted average diluted shares | 847 | 858 | ||||||||||

| Pre-tax income per diluted share | $ | 5.34 | $ | 3.12 | 70% | |||||||

| 52 |

Return on Invested Capital

Delta presents return on invested capital as management believes this metric is helpful to investors in assessing the company’s ability to generate returns using its invested capital and as a measure against the industry. Return on invested capital is adjusted total operating income divided by average invested capital.

| (Projected) | ||||

| (in billions, except % of return) | 2014 | |||

| Adjusted Book Value of Equity | $ | 18.5 | ||

| Average Adjusted Net Debt | 8.2 | |||

| Average Invested Capital | $ | 26.7 | ||

| Adjusted Total Operating Income | $ | 5.4 | ||

| Return on Invested Capital | 20% | |||

Operating Cash Flow, adjusted

Delta presents operating cash flow, adjusted because management believes adjusting for these amounts provides a more meaningful financial measure for investors. Special items excluded in the tables below showing the reconciliation of operating cash flow, adjusted are:

Reimbursements for build-to-suit leased facilities. These reimbursements for build-to-suit leased facilities effectively reduce net cash provided by operating activities and related capital expenditures.

Northwest operating cash flow. Included the Northwest Airlines operating cash flow as if the company’s merger with Northwest Airlines had occurred at the beginning of the period presented because management believes this metric is helpful to investors to evaluate the company’s combined operating cash flows and provide a more meaningful comparison to our post-merger amounts.

| (Projected) | ||||||||||||||||

| (in billions) | 2014 | 2013 | 2012 | 2008 | ||||||||||||

| Net cash provided by operating activities | $ | 5.5 | $ | 4.5 | $ | 2.5 | $ | (1.7 | ) | |||||||

| Reimbursements for build-to-suit leased facilities | (0.1 | ) | – | – | – | |||||||||||

| Incremental pension payments | 0.3 | – | – | – | ||||||||||||

| AMEX loan repayment | 0.3 | – | – | – | ||||||||||||

| SkyMiles used pursuant to advance purchase under AMEX agreement | – | 0.3 | 0.3 | – | ||||||||||||

| Northwest operating cash flow | – | – | – | 0.2 | ||||||||||||

| Operating cash flow, adjusted | $ | 6.0 | $ | 4.8 | $ | 2.8 | $ | (1.5 | ) | |||||||

| 53 |

Free Cash Flow

Delta presents free cash flow because management believes this metric is helpful to investors to evaluate the company's ability to generate cash that is available for use for debt service or general corporate initiatives.

| (Projected) | ||||

| (in billions) | 2014 | |||

| Net cash provided by operating activities (GAAP) | $ | 5.5 | ||

| Less: | ||||

| Capital expenditures and other | $ | (2.3 | ) | |

| Total free cash flow | $ | 3.2 | ||

| Capital Returns | $ | 1.35 | ||

| Capital Returns as a % of free cash flow | 42% | |||

| (Projected) | ||||||||||||||||

| For the period | ||||||||||||||||

| January 1, 2010 - | ||||||||||||||||

| (in billions) | 2013 | December 31, 2014 | ||||||||||||||

| Net cash provided by operating activities (GAAP) | $ | 4.5 | $ | 18.1 | ||||||||||||

| Net cash used in investing activities (GAAP) | $ | (2.7 | ) | $ | (10.5 | ) | ||||||||||

| Adjustments: | ||||||||||||||||

| Proceeds from sale of property and investments and other | – | (0.7 | ) | |||||||||||||

| Purchase of short-term investments | – | 1.8 | ||||||||||||||

| SkyMiles used pursuant to advance purchase under AMEX agreement | 0.3 | 0.6 | ||||||||||||||

| Cash used in investing | (2.4 | ) | (8.8 | ) | ||||||||||||

| Total free cash flow | $ | 2.1 | $ | 9.3 | ||||||||||||

| Capital Returns | $ | 0.35 | ||||||||||||||

| Capital Returns as a % of free cash flow | 17% | |||||||||||||||

| 54 |

Adjusted Net Debt

Delta uses adjusted total debt, including aircraft rent, in addition to long-term adjusted debt and capital leases, to present estimated financial obligations. Delta reduces adjusted debt by cash, cash equivalents and short-term investments, resulting in adjusted net debt, to present the amount of assets needed to satisfy the debt. Management believes this metric is helpful to investors in assessing the company’s overall debt profile.

Hedge margin postings. Management has included margin postings to counterparties as we believe this inclusion removes the impact of current market volatility on our unsettled hedges and is a better representation of the continued progress we have made on our debt initiatives.

| (Projected) | ||||||||||||||||||||||||||||||||||||||||||||||

| (in billions) | December 31, 2014 | December 31, 2013 | December 31, 2012 | December 31, 2011 | December 31, 2010 | December 31, 2009 | ||||||||||||||||||||||||||||||||||||||||

| Debt and capital lease obligations | $ | 9.3 | $ | 11.3 | $ | 12.7 | $ | 13.8 | $ | 15.3 | $ | 17.2 | ||||||||||||||||||||||||||||||||||

| Plus: unamortized discount, net from purchase accounting and fresh start reporting | 0.1 | 0.4 | 0.5 | 0.6 | 0.6 | 1.1 | ||||||||||||||||||||||||||||||||||||||||

| Adjusted debt and capital lease obligations | $ | 9.4 | $ | 11.7 | $ | 13.2 | $ | 14.4 | $ | 15.9 | $ | 18.3 | ||||||||||||||||||||||||||||||||||

| Plus: 7x last twelve months' aircraft rent | 1.6 | 1.5 | 1.9 | 2.1 | 2.7 | 3.4 | ||||||||||||||||||||||||||||||||||||||||

| Adjusted total debt | 11.0 | 13.2 | 15.1 | 16.5 | 18.6 | 21.7 | ||||||||||||||||||||||||||||||||||||||||

| Less: cash, cash equivalents and short-term investments | (3.8 | ) | (3.8 | ) | (3.4 | ) | (3.6 | ) | (3.6 | ) | (4.7 | ) | ||||||||||||||||||||||||||||||||||

| Less: hedge margin postings | (0.5 | ) | – | – | – | – | – | |||||||||||||||||||||||||||||||||||||||

| Adjusted net debt | $ | 7.2 | $ | 9.4 | $ | 11.7 | $ | 12.9 | $ | 15.0 | $ | 17.0 | ||||||||||||||||||||||||||||||||||

| 55 |

Non-Fuel Unit Cost or Cost per Available Seat Mile ("CASM-Ex")

We exclude the following items from consolidated CASM to evaluate the company’s core unit cost performance:

Aircraft fuel and related taxes. The volatility in fuel prices impacts the comparability of year-over-year non-fuel financial performance. The exclusion of aircraft fuel and related taxes from this measure (including our regional carriers) allows investors to better understand and analyze our non-fuel costs and our year-over-year financial performance.

Ancillary businesses. Our ancillary businesses include aircraft maintenance and staffing services we provide to third parties and our vacation wholesale operations. Because these businesses are not related to the generation of a seat mile, we exclude the costs related to these sales to provide a more meaningful comparison of the costs of our airline operations to the rest of the airline industry.

Profit sharing. We exclude profit sharing because this exclusion allows investors to better understand and analyze our recurring cost performance and provides a more meaningful comparison of our core operating costs to the airline industry.

Restructuring and other items. We exclude restructuring and other items from CASM for the same reasons described above under the heading Pre-Tax Income & Margin, excluding special items.

Refinery cost of sales. Delta’s refinery segment provides jet fuel to the airline segment from its own production and from jet fuel obtained through agreements with third parties. Activities of the refinery segment are primarily for the benefit of the airline. However from time to time, the refinery sells fuel by-products to third parties. Because the cost is unrelated to the generation of a seat mile, Delta excludes the cost of these sales to provide a more meaningful comparison of the costs of the airline operations to the rest of the airline industry.

| (Projected) | |||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | ||||||||||||||

| CASM | 15.65 | ¢ | 14.77 | ¢ | 14.97 | ¢ | 14.12 | ¢ | |||||||||

| Items excluded: | |||||||||||||||||

| Aircraft fuel and related taxes | (5.40 | ) | (4.92 | ) | (5.31 | ) | (5.01 | ) | |||||||||

| Ancillary businesses | (0.32 | ) | (0.32 | ) | (0.38 | ) | (0.37 | ) | |||||||||

| Profit sharing | (0.45 | ) | (0.22 | ) | (0.16 | ) | (0.11 | ) | |||||||||

| Restructuring and other items | (0.27 | ) | (0.17 | ) | (0.20 | ) | (0.10 | ) | |||||||||

| Refinery cost of sales | (0.05 | ) | – | – | – | ||||||||||||

| CASM-Ex | 9.16 | ¢ | 9.14 | ¢ | 8.92 | ¢ |

8.53 | ¢ | |||||||||

| Year-over-year change | 0.3% | 2.4% | 4.6% | ||||||||||||||

| Three Months Ended | ||||||||

| (Projected) | ||||||||

| December 2014 | December 2013 | |||||||

| CASM | 16.93 | ¢ |

14.97 | ¢ | ||||

| Items excluded: | ||||||||

| Aircraft fuel and related taxes | (6.66 | ) | (4.86 | ) | ||||

| Ancillary businesses | (0.38 | ) | (0.32 | ) | ||||

| Profit sharing | (0.43 | ) | (0.21 | ) | ||||

| Restructuring and other items | 0.02 | (0.29 | ) | |||||

| Refinery cost of sales | (0.11 | ) | – | |||||

| CASM-Ex | 9.37 | ¢ |

9.29 | ¢ | ||||

| Year-over-year change | 1% | |||||||

| 56 |

Average Fuel Price Per Gallon, adjusted

Delta excludes MTM adjustments from average fuel price per gallon for the same reason described above under the heading operating margin, adjusted.

| (Projected) | ||||||||||||||

| Three Months Ended | (Projected) | |||||||||||||

| December 2014 | 2014 | 2013 | 2012 | |||||||||||

| Average fuel price per gallon | $4.07 to $4.12 | $ | 3.33 | $ | 3.00 | $ | 3.25 | |||||||

| MTM adjustments | (1.44) | (0.45 | ) | 0.07 | 0.01 | |||||||||

| Average fuel price per gallon, adjusted | $2.63 to $2.68 | $ | 2.88 | $ | 3.07 | $ | 3.26 | |||||||

Total Combined Revenue and Passenger Unit Revenue

Delta presents combined revenues and passenger unit revenue for Delta and Northwest Airlines because management believes this metric is helpful to investors to evaluate the company's revenue metrics and provide a more meaningful comparison to our post-merger amounts.

| (in billions, except unit revenue) | 2005 | |||

| Delta revenue | $ | 16.2 | ||

| Northwest revenue | 12.3 | |||

| Total combined revenue | $ | 28.5 | ||

| (in billions) | 2005 | |||

| Delta passenger revenue | $ | 14.6 | ||

| Northwest passenger revenue | 8.9 | |||

| Total combined passenger revenue | $ | 23.5 | ||

| Delta available seat miles | 156.8 | |||

| Northwest available seat miles | 91.9 | |||

| Total combined available seat miles | 248.7 | |||

| Total combined passenger unit revenue | 9.5 | ¢ | ||

| 57 |

Capital Spending

Delta presents combined capital spending as if the company’s merger with Northwest Airlines had occurred at the beginning of the period presented because management believes this metric is helpful to investors to evaluate the company’s combined investing activities and provide a more meaningful comparison to our post-merger amounts.

| (in billions) | 2013 | 2008 | ||||||

| Delta capital expenditures (GAAP) | $ | 2.6 | $ | 1.5 | ||||

| Investment in Virgin Atlantic | 0.3 | – | ||||||

| Northwest capital expenditures | – | 1.1 | ||||||

| Total combined capital spending | $ | 2.9 | $ | 2.6 | ||||

| 58 |