Attached files

| file | filename |

|---|---|

| EX-3.2 - EX-3.2 - On Deck Capital, Inc. | d772825dex32.htm |

| EX-3.1 - EX-3.1 - On Deck Capital, Inc. | d772825dex31.htm |

| EX-10.3 - EX-10.3 - On Deck Capital, Inc. | d772825dex103.htm |

| EX-10.4 - EX-10.4 - On Deck Capital, Inc. | d772825dex104.htm |

| EX-23.1 - EX-23.1 - On Deck Capital, Inc. | d772825dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on December 4, 2014

Registration No. 333-200043

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

ON DECK CAPITAL, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 6199 | 42-1709682 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

1400 Broadway, 25th Floor

New York, New York 10018

(888) 269-4246

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Noah Breslow

Chief Executive Officer

1400 Broadway, 25th Floor

New York, New York 10018

(888) 269-4246

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Larry W. Sonsini Tony Jeffries Damien Weiss Wilson Sonsini Goodrich & Rosati, P.C. 650 Page Mill Road Palo Alto, California 94304 (650) 493-9300 |

Cory Kampfer General Counsel 1400 Broadway, 25th Floor New York, New York 10018 (888) 269-4246 |

Christopher J. Austin Andrew D. Thorpe Stephen C. Ashley Orrick, Herrington & Sutcliffe LLP 51 West 52nd Street New York, New York 10019 (212) 506-5000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of Each Class of Securities to be Registered |

Amount to be Registered |

Proposed Maximum Offering Price Per Share |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee(2) | ||||

| Common Stock, par value $0.005 per share |

11,500,000 | $18.00 | $207,000,000 | $24,054 | ||||

|

| ||||||||

|

| ||||||||

| (1) | Estimated pursuant to 457(a) under the Securities Act of 1933, as amended. Includes offering price of shares that the underwriters have the option to purchase. |

| (2) | The Registrant previously paid $17,430 in connection with the initial filing of the Registration Statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued December 4, 2014

10,000,000 Shares

COMMON STOCK

On Deck Capital, Inc. is offering 10,000,000 shares of its common stock. This is our initial public offering and no public market currently exists for our shares. We anticipate that the initial public offering price of our common stock will be between $16.00 and $18.00 per share.

Our common stock has been approved for listing on the New York Stock Exchange under the symbol “ONDK.”

We are an “emerging growth company” under the federal securities laws and are therefore subject to reduced public company reporting requirements. Investing in our common stock involves risks. See “Risk Factors” beginning on page 14.

PRICE $ A SHARE

| Price to |

Underwriting |

Proceeds to |

||||||||||

| Per Share |

$ | $ | $ | |||||||||

| Total |

$ | $ | $ | |||||||||

We have granted the underwriters the right to purchase up to an additional 1,500,000 shares of common stock.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on , 2014.

| MORGAN STANLEY | BofA MERRILL LYNCH |

J.P. MORGAN | DEUTSCHE BANK SECURITIES | JEFFERIES |

| RAYMOND JAMES | STIFEL | NEEDHAM & COMPANY | ||||

, 2014

Table of Contents

Table of Contents

You should rely only on the information contained in this prospectus or contained in any free writing prospectus prepared by or on behalf of us. Neither we nor the underwriters have authorized anyone to provide you with information different from, or in addition to, that contained in this prospectus or any related free writing prospectus. This prospectus is an offer to sell only the shares offered hereby but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date, regardless of its delivery. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside the United States: neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

-i-

Table of Contents

This summary overview of the key aspects of the offering identifies those aspects of the offering that are the most significant. This summary is qualified in its entirety by the more detailed information and financial statements included elsewhere in this prospectus. This summary may not contain all the information you should consider before investing in our common stock. You should carefully read this prospectus in its entirety before investing in our common stock, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus.

ON DECK CAPITAL, INC.

Our Company

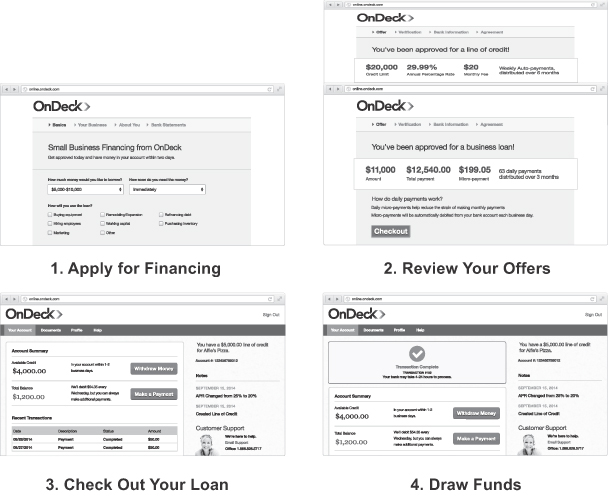

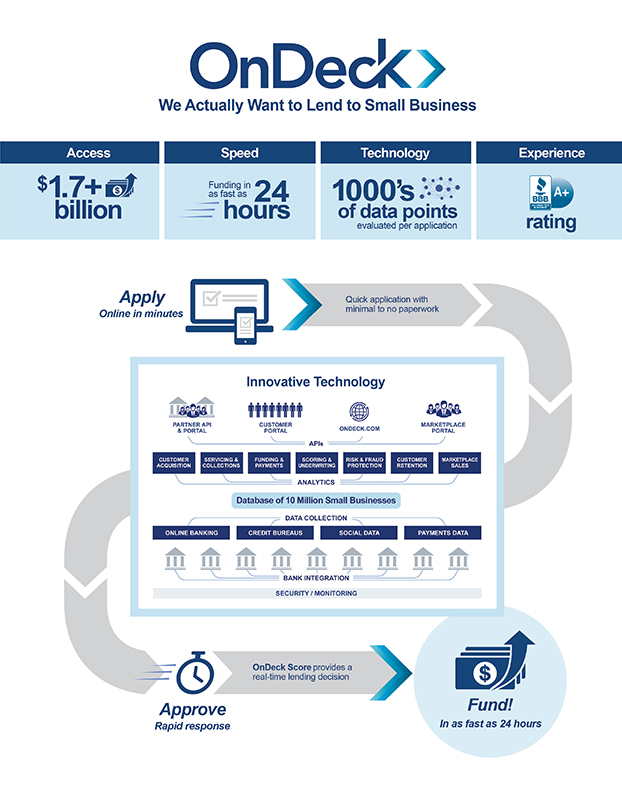

We are a leading online platform for small business lending. We are seeking to transform small business lending by making it efficient and convenient for small businesses to access capital. Enabled by our proprietary technology and analytics, we aggregate and analyze thousands of data points from dynamic, disparate data sources to assess the creditworthiness of small businesses rapidly and accurately. Small businesses can apply for a term loan or line of credit on our website in minutes and, using our proprietary OnDeck Score, we can make a funding decision immediately and transfer funds as fast as the same day. We have originated more than $1.7 billion in loans and collected more than 4.4 million customer payments since we made our first loan in 2007. Our loan originations have increased at a compound annual growth rate of 127% from 2011 to 2013 and had a year-over-year growth rate of 171% for the nine months ended September 30, 2014.

The 28 million small businesses in the United States are integral to the U.S. economy and the vibrancy of local communities, employing approximately 50% of the private workforce. Small business growth depends on efficient and frictionless access to capital, yet small businesses face numerous challenges that make it difficult to secure such capital. Small business owners are time and resource constrained, but the traditional borrowing process is time consuming and burdensome. Small businesses surveyed by the Federal Reserve Bank of New York indicated that the traditional funding process required them, on average, to dedicate 26 hours, contact 2.6 financial institutions and submit 2.7 loan applications. These challenges exist in part because it is inherently difficult to assess the creditworthiness of small businesses. Small businesses are a diverse group spanning many different industries, stages in development, geographies, financial profiles and operating histories, historically making it difficult to assess their creditworthiness in a uniform manner, and there is no widely-accepted credit score for small businesses. In addition, small businesses often seek small, short-term loans to fund short-term projects and investments, but traditional lenders may only offer loan products that feature large loan sizes, longer durations and rigid collateral requirements that are not well suited to their needs.

The small business lending market is vast and underserved. According to the FDIC, there were $178 billion in business loan balances under $250,000 in the United States in the second quarter of 2014, across 21.7 million loans. Oliver Wyman, a management consulting firm and business unit of Marsh & McLennan, estimates that there is a potential $80 to $120 billion in unmet demand for small business lines of credit, and we believe that there is also substantial unmet demand for other credit-related products, including term loans. We also believe that the application of our technology to credit assessment can stimulate additional demand for our products and expand the total addressable market for small business credit.

To better meet the capital needs of small businesses, we are seeking to use technology to transform the way this capital is accessed. We built our integrated platform specifically to meet their financing needs. Our platform touches every aspect of the customer lifecycle and a potential customer can complete an online application 24 hours a day, 7 days a week. Our proprietary data and analytics engine aggregates and analyzes thousands of online and offline data attributes and the relationships among those attributes to assess the creditworthiness of a

-1-

Table of Contents

small business in real time. The data points include customer bank activity shown on bank statements, government filings, tax and census data. In addition, in certain instances we also analyze reputation and social data. We look at both individual data points and relationships among the data, with each transaction or action being a separate data point that we take into account. A key differentiator of our solution is the OnDeck Score, the product of our proprietary small business credit scoring system. Both our data and analytics engine and the algorithms powering the OnDeck Score undergo continuous improvement to automate and optimize the credit assessment process, enabling more rapid and predictive credit decisions. Each loan that we make involves our proprietary automated underwriting process, and approximately two-thirds of our loans are underwritten using a fully-automated underwriting process that does not require manual review. Our platform supports same-day funding and automated loan repayment. This technology-enabled approach provides small businesses with efficient, frictionless access to capital.

We believe that the differences between our approach and the approach adopted by traditional lenders are what have allowed us to better address the challenges of small business lending. In our approach, manual underwriting has largely been replaced by an automated, data-driven approach to credit assessment. Expensive branch networks have been replaced by an online website for applications and account management. Service of consumers and businesses of all sizes has been replaced by a singular focus on small business. In addition, we are subject to less regulation than traditional lenders because we do not make loans to consumers nor do we take deposits. We believe that differences in our loan products allow us to better meet the needs of small businesses. Small business owners typically seek small, short-term loans so we offer term loan products that range in size from $5,000 to $250,000 and feature terms of 3 to 24 months versus traditional lenders that offer larger and longer term loans. At September 30, 2014, our outstanding loans had original loan balances ranging from $5,000 to $250,000. We also offer a line of credit product that can be approved more quickly than comparable products offered by traditional lenders. We believe that small business owners prefer predictability so we offer fixed interest amounts and automated daily or weekly repayments compared to traditional lenders that offer both fixed and variable rate loans with monthly repayments. We also believe that small business owners value flexibility so we don’t have the rigid collateral requirements that are typical of traditional lenders. All or substantially all of our term loans and lines of credit are currently collateralized through a security interest in our customers’ assets, but we do not require a minimum amount of collateral to make a loan. We intend to transition to unsecured lines of credit in the near future.

We lend to a wide variety of small businesses across more than 700 industries and in all 50 U.S. states and have recently begun lending in Canada. The top five states in which we originated loans in 2013 and in the nine months ended September 30, 2014 were California, Florida, New York, Texas and New Jersey, representing approximately 14%, 10%, 8%, 8% and 4% of our total loan originations for the year ended December 31, 2013 and approximately 15%, 9%, 8%, 8% and 4% of our total loan originations for the nine months ended September 30, 2014, respectively. Our most frequent customers are professional services firms, retailers, restaurants and food service companies, healthcare specialists and wholesalers. We also lend to customers with a range of financial and operating histories: our customers have a median of $568,000 in annual revenue, with 90% of our customers having between $150,000 and $3.2 million in annual revenue, and have been in business for a median of 7.5 years, with 90% in business between 2 and 31 years.

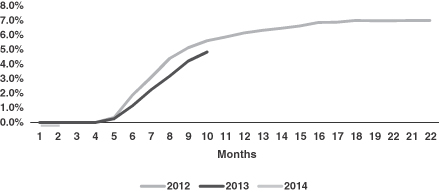

We believe that our product pricing has historically fallen between traditional bank loans to small businesses and certain non-bank small business financing alternatives such as merchant cash advances. The weighted average pricing on our term loan originations has declined over time, as measured by both average “Cents on Dollar” borrowed per month and APR, as shown in the table below.

| Q1 2013 |

Q2 2013 |

Q3 2013 |

Q4 2013 |

Q1 2014 |

Q2 2014 |

Q3 2014 |

||||||||||||||||||||||

| Average “Cents on Dollar” |

2.73 | ¢ | 2.71 | ¢ | 2.62 | ¢ | 2.60 | ¢ | 2.53 | ¢ | 2.38 | ¢ | 2.24 | ¢ | ||||||||||||||

| APR |

65.9 | % | 65.0 | % | 62.9 | % | 62.1 | % | 60.3 | % | 57.1 | % | 53.2 | % | ||||||||||||||

-2-

Table of Contents

We attribute this pricing shift to increased originations from our direct and strategic partner channels as a percentage of total originations, as well as our declining cost of funds rate. “Cents on Dollar” borrowed reflects the monthly interest paid by a customer to us for a loan, and does not include the loan origination fee and the repayment of the principal of the loan. Because many of our loans are short term in nature and APR is calculated on an annualized basis, we believe that small business customers tend to evaluate term loans primarily on a “Cents on Dollar” borrowed basis rather than APR.

We have a diverse and scalable set of funding sources. These include debt facilities, securitization of small business loans generated by OnDeck and the OnDeck Marketplace, a proprietary whole loan sale marketplace that allows institutional investors to directly purchase small business loans from us. We believe that having diverse sources of capital enables us to reduce our average cost of capital, provides multiple sources of capital in a variety of economic climates and provides increased flexibility as we seek to increase our loan originations. Affiliates of certain of our underwriters in this offering are participants in our various financing facilities and have acted in various administrative roles in connection with such facilities. For further information, see the section titled “Underwriters.”

Our business has grown rapidly. In 2013, we originated $458.9 million of loans, representing year-over-year growth of 165%, and in the first nine months of 2014, we originated $788.3 million of loans, representing year-over-year growth of 171%, all while maintaining consistent credit quality. In 2013, we recorded gross revenue of $65.2 million, representing year-over-year growth of 155%, and in the first nine months of 2014, we recorded gross revenue of $107.6 million, representing year-over-year growth of 156%. During 2013 and the three months ended September 30, 2014, our Adjusted EBITDA was $(16.3) million and $2.6 million, respectively, our (loss) income from operations was $(19.3) million and $0.7 million, respectively and our net (loss) income was $(24.4) million and $0.4 million, respectively. See the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures” for a discussion and reconciliation of Adjusted EBITDA to net (loss) income. As of December 31, 2013 and September 30, 2014, our total assets were $235.5 million and $466.0 million, respectively and the unpaid principal balance on loans outstanding was $216.0 million and $422.1 million, respectively.

Industry Background and Trends

| • | Small Businesses are an Enormous Driver of the U.S. Economy. According to the U.S. Small Business Administration, there are 28 million small businesses in the United States, contributing approximately 45% of U.S. non-agricultural gross domestic product and employing approximately 50% of the private workforce. These small businesses help build vibrant communities with local character. |

| • | Small Businesses Need Capital to Survive and Thrive. We believe that small businesses depend on efficient and frictionless access to capital to purchase supplies and inventory, hire employees, market their businesses and invest in new potential growth opportunities. |

| • | Small Businesses are Unique and Difficult to Assess. Credit assessment is inherently difficult because small business data is constantly changing as the business evolves and is scattered across a myriad of online and offline sources, unlike consumer credit assessment where a lender can generally look to scores provided by consumer credit bureaus. |

| • | Small Businesses are not Adequately Served by Traditional Lenders. We believe traditional lenders face a number of challenges and limitations that make it difficult to address the capital needs of small businesses, such as: |

| • | Organizational and Structural Challenges. The costly combination of physical branches and manually intensive underwriting procedures makes it difficult for traditional lenders to efficiently serve small businesses. |

-3-

Table of Contents

| • | Technology Limitations. Many traditional lenders use legacy or third-party systems that are difficult to integrate or adapt to the shifting needs of small businesses. |

| • | Loan Products not Designed for Small Businesses. Small businesses are not well served by traditional loan products. We believe that traditional lenders often offer products characterized by larger loan sizes, longer durations and rigid collateral requirements. By contrast, small businesses often seek small loans for short-term investments. |

| • | Other Credit Products Have Significant Limitations. Certain additional products, including widely available business credit cards, provide small businesses with access to capital but may not be designed for their borrowing needs. For example, business credit cards may not have sufficient credit limits to handle the needs of the small business, particularly in the case of large, one-time projects such as capital improvements or expanding to a new location. In addition, certain business opportunities, such as discounts for paying with cash, and certain business expenses, such as payroll, rent or equipment leases, may not be payable with credit cards. Business credit cards are also typically not designed to fund many small business working capital needs. |

As a result, we believe that small businesses feel underserved by traditional lenders. According to the FDIC, the percentage of commercial and industrial loans with a balance less than $250,000 has declined from 20% of total dollars borrowed in 2004 to 13% in the second quarter of 2014. According to Oliver Wyman, 75% of small businesses are looking to borrow less than $50,000. In addition, according to the third quarter 2014 Wells Fargo-Gallup Small Business Index, only 32% of small businesses reported that obtaining credit was easy.

Challenges for Small Business Owners

| • | Small Business Owners are Time and Resource Constrained. We believe that small business owners lack many of the resources available to larger businesses and have fewer staff on which to rely for critical business issues. Time spent inefficiently may mean lost sales, extra expenses and personal sacrifices. |

| • | Traditional Lending is not Geared Towards Small Businesses. Traditional lenders do not meet the needs of small businesses for a number of reasons, including the following: |

| • | Time-Consuming Process. According to a Harvard Business School study, the traditional borrowing process includes application forms which are time consuming to assemble and complete, long in-person meetings during business hours and manual underwriting procedures that delay decisions. |

| • | Non-Tailored Credit Assessment. There is no widely-accepted credit score for small businesses. Traditional lenders frequently rely upon the small business owner’s personal credit as a primary indicator of the business’s creditworthiness, even though it is not necessarily indicative of the business’s credit profile. |

| • | Product Mismatch. Small businesses are not well served by traditional loan products. We believe that they often seek small loans for short-term investments, but traditional lenders may only offer loan products characterized by larger loan sizes, longer durations and rigid collateral requirements. |

| • | Alternatives to Traditional Bank Loans are Inadequate. Small businesses whose lending needs are not being met by traditional bank loans have historically resorted to a fragmented landscape of products, including merchant cash advances, credit cards, receivables factoring, equipment leases and home equity lines, each of which comes with its own challenges and limitations. |

-4-

Table of Contents

Modernization of Small Businesses

| • | Small Businesses are Embracing Technology. Small businesses are increasingly using online services to manage their operations. According to a survey by the National Small Business Association, 85% of small businesses purchase supplies online, 83% manage bank accounts online, 82% maintain their own website, 72% pay bills online and 41% use tablets for their business. We believe small business owners expect a user-friendly online borrowing experience. |

| • | The Digital Footprint of Small Businesses is Expanding. There is a vast amount of real-time digital data about small businesses that can be used to generate valuable insights that help better assess the creditworthiness of a small business. |

Our Solution

Our mission is to power the growth of small business through lending technology and innovation. We are combining our passion for small business with technology and analytics to transform the way small businesses access capital. Our solution was built specifically to address small businesses’ capital needs and consists of our loan products, our end-to-end integrated platform and the OnDeck Score. We offer two products to small businesses to enable them to access capital: term loans and lines of credit. Our proprietary, end-to-end integrated platform includes: our website, which allows small businesses to apply for a loan in minutes, 24 hours a day, 7 days a week; our proprietary data and analytics engine that analyzes thousands of data attributes from disparate sources to assess the real-time creditworthiness of a small business; the technology that enables seamless funding of our loans; and our daily and weekly collections and ongoing servicing systems. A key differentiator of our solution is the OnDeck Score, the product of our proprietary small business credit-scoring system. The OnDeck Score aggregates and analyzes thousands of data elements and attributes related to a business and its owners that are reflective of the creditworthiness of the business as well as predictive of its credit performance. Our proprietary data and analytics engine and the algorithms powering the OnDeck Score undergo continuous improvement through machine learning and other statistical techniques to automate and optimize the credit assessment process.

Our customers choose us because we provide the following key benefits:

| • | Access. By combining technology with comprehensive and relevant data that captures the unique aspects of small businesses, we are able to better assess the creditworthiness of small businesses and approve more loans. |

| • | Speed. Small businesses can submit an application online in as little as minutes. We are able to provide most loan applicants with a simple application process and an immediate approval decision and transfer funds as fast as the same day. |

| • | Customer Experience. Our U.S.-based internal salesforce and customer service representatives provide high tech, high touch, personalized support to our applicants and customers. Our team answers questions and provides assistance throughout the application process and the life of the loan. Our representatives are available Monday through Saturday before, during and after regular business hours to accommodate the busy schedules of small business owners. We also offer our customers credit education and consulting services and other value added services. Our commitment to provide a great customer experience has helped us earn a 71 Net Promoter Score, a widely used system of measuring customer loyalty, and consistently achieve A+ ratings from the Better Business Bureau. |

We generally require applicants to have been in business for at least one year and have revenue of at least $100,000 during the 12 months prior to submission of the application. We also consider a small business owner’s personal credit score, which we generally require to be 500 or higher, though once this criteria is met the personal credit score is not a significant component of the OnDeck Score. We do not consider a small business owner’s personal assets in deciding whether to approve an application.

-5-

Table of Contents

Our Competitive Strengths

We believe the following competitive strengths differentiate us and serve as barriers for others seeking to enter our market:

| • | Significant Scale. Since we made our first loan in 2007, we have funded more than $1.7 billion in loans across more than 700 industries in all 50 U.S. states and have recently begun lending in Canada. |

| • | Proprietary Data and Analytics Engine. Our proprietary data and analytics engine and the OnDeck Score provide us with significant visibility and predictability in assessing the creditworthiness of small businesses and allow us to better serve more customers across more industries. With each loan application, each funded loan and each daily or weekly payment, our data set expands and our OnDeck Score improves. |

| • | End-to-End Integrated Technology Platform. We built our integrated platform specifically to meet the financing needs of small businesses. Our platform touches every aspect of the customer lifecycle, including customer acquisition, sales, scoring and underwriting, funding, and servicing and collections. We use our platform to underwrite, process and service all of our small business loans, regardless of distribution channel. |

| • | Diversified Distribution Channels. We are building brand awareness and enhancing distribution capabilities through diversified distribution channels, including direct marketing, strategic partnerships and funding advisors. Our direct marketing, strategic partner and funding advisor channels constituted 56.2%, 14.9% and 28.9% of our total number of loans, respectively, for the three months ended September 30, 2014, 54.4%, 13.4% and 32.3% of our total number of loans, respectively, for the nine months ended September 30, 2014 and 44.1%, 10.3% and 45.6% of our total number of loans, respectively, for the year ended December 31, 2013. Our internal salesforce contacts potential customers, responds to inbound inquiries from potential customers, and is available to assist all customers throughout the application process. Our loan underwriting generally includes the same process and stages without regard to loan origination channel. Our loan underwriting uses different parameters between the loan origination channels depending upon a variety of factors including, among many others, historical portfolio performance by loan origination channel and channel specific data availability. |

| • | High Customer Satisfaction and Repeat Customer Base. Our strong value proposition has been validated by our customers. We had a Net Promoter Score, a widely used system of measuring customer loyalty, of 71 in 2013, and we believe that strong customer satisfaction has played an important role in repeat borrowing by our customers. In 2013, 43.5% of loan originations were by repeat customers, who either replaced their existing loan with a new, usually larger, loan or took out a new loan after paying off their existing OnDeck loan in full. Thirty percent of our origination volume from repeat customers in 2013 was due to unpaid principal balances rolled from existing loans directly into such repeat originations. |

| • | Durable Business Model. Since we began lending in 2007, we have successfully operated our business through both strong and weak economic environments. Our real-time data, short duration loans, automated daily and weekly collection, risk management capabilities and unit economics enable us to react rapidly to changing market conditions and generate attractive financial results. |

| • | Differentiated Funding Platform. We source capital through multiple channels, including debt facilities, securitization and the OnDeck Marketplace, our proprietary whole loan sale platform for institutional investors. This diversity provides us with multiple, scalable funding sources, long-term capital commitments and access to flexible funding for growth. |

| • | 100% Small Business-Focused. We are passionate about small businesses. We have developed significant expertise over our seven-year operating history exclusively focused on assessing and delivering credit to small businesses. We believe this passion, focus and small business credit expertise provides us with significant competitive advantages. |

-6-

Table of Contents

Our Strategy for Growth

Our vision is to become the most trusted lender to small businesses, and to accomplish this, we intend to:

| • | Continue to Acquire Customers Through Direct Marketing and Sales. We plan to continue investing in direct marketing and sales to add new customers and increase our brand awareness. |

| • | Broaden Distribution Capabilities Through Partners. We plan to expand our network of partners, including banks, payment processors, funding advisors and small business-focused service providers, and leverage their relationships with small businesses to acquire new customers. |

| • | Enhance Data and Analytics Capabilities. We plan to make substantial investments in our data and analytics capabilities. Our data science team continually uncovers new insights about small businesses and their credit performance and considers new data sources for inclusion in our models, allowing us to evaluate and lend to more customers. |

| • | Expand Product Offerings. Following the successful recent introduction of our line of credit and 24-month term loan products, over time we plan to expand our offerings by introducing new credit-related products for small businesses. We may fund the expansion of our product offerings in part from the proceeds we receive from our initial public offering, or IPO, but we have not yet finalized the specific products we will introduce or established a particular timeline to expand our product offerings. |

| • | Extend Customer Lifetime Value. We believe we have an opportunity to increase revenue and loyalty from new and existing customers. We plan to introduce new features and product cross-sell capabilities to continue driving the increased use of our platform. |

| • | Targeted International Expansion. We believe there are opportunities to expand our small business lending in select countries outside of the United States and Canada. We may fund our international expansion in part from the proceeds we receive from our IPO, but we have not yet committed to any specified location or established a particular timeline to pursue this opportunity. |

Risks Affecting Us

Our business is subject to numerous risks and uncertainties, including those highlighted in the section titled “Risk Factors” beginning on page 14. These risks include, but are not limited to, the following:

| • | We have a limited operating history in an evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful. |

| • | Our recent, rapid growth may not be indicative of our future growth and, if we continue to grow rapidly, we may not be able to manage our growth effectively. |

| • | We have a history of losses and may not achieve consistent profitability in the future. |

| • | Worsening economic conditions may result in decreased demand for our loans, cause our customers’ default rates to increase and harm our operating results. |

| • | Many of our strategic partnerships are subject to termination options that, if terminated, could harm the growth of our customer base and negatively impact our financial performance. |

| • | To the extent that Funding Advisor Program partners or direct sales agents mislead loan applicants or are engaged in disreputable behavior, our reputation may be harmed and we may face liability. |

| • | Our business may be adversely affected by disruptions in the credit markets, including reduced access to credit. |

| • | If the information provided by customers to us is incorrect or fraudulent, we may misjudge a customer’s qualifications to receive a loan and our operating results may be harmed. |

| • | Our current level of interest rate spread may decline in the future. Any material reduction in our interest rate spread could reduce our profitability. |

-7-

Table of Contents

| • | An increase in customer default rates may reduce our overall profitability and could also affect our ability to attract institutional funding. Further, historical default rates may not be indicative of future results. |

| • | Our risk management efforts may not be effective. |

| • | We rely on our proprietary credit-scoring model in the forecasting of loss rates. If we are unable to effectively forecast loss rates, it may negatively impact our operating results. |

| • | Our allowance for loan losses is determined based upon both objective and subjective factors and may not be adequate to absorb loan losses. |

| • | We face increasing competition and, if we do not compete effectively, our operating results could be harmed. |

| • | The lending industry is highly regulated. Changes in regulations or in the way regulations are applied to our business could adversely affect our business. |

We are planning to implement certain enhanced compliance-related measures related to our funding advisor channel in addition to our existing measures. For example, we plan to expand the extent to which our funding advisor partners are required to submit to and conduct background checks and strengthen our contractual control over our funding advisors. In addition, we plan to add certain additional risk and compliance review processes related to the funding advisor channel. We have also recently hired a senior compliance officer whose responsibilities will include overseeing compliance matters involving our funding advisor channel.

Corporate Information

Our principal executive offices are located at 1400 Broadway, 25th Floor, New York, New York 10018, and our telephone number is (888) 269-4246. Our website is www.ondeck.com. Information contained on, or that can be accessed through, our website is not incorporated by reference into this prospectus, and you should not consider information on our website to be part of this prospectus. We were incorporated in Delaware in May 2006.

OnDeck, the OnDeck logo, OnDeck Score, OnDeck Marketplace and other trademarks or service marks of OnDeck appearing in this prospectus are the property of OnDeck. Trade names, trademarks and service marks of other companies appearing in this prospectus are the property of their respective holders. We have omitted the ® and ™ designations, as applicable, for the trademarks used in this prospectus.

We are an emerging growth company as defined in the Jumpstart Our Business Startups Act of 2012 and are therefore subject to reduced public company reporting requirements. We will remain an emerging growth company until the earliest to occur of: the last day of the fiscal year in which we have more than $1.0 billion in annual revenue; the date we qualify as a “large accelerated filer” with at least $700 million of equity securities held by non-affiliates; the issuance, in any three-year period, by us of more than $1.0 billion in non-convertible debt securities; and the last day of the fiscal year ending after the fifth anniversary of our initial public offering.

Offering Related Conversion

Upon the completion of this offering, we will no longer have any shares of preferred stock or preferred stock warrants outstanding. Upon completion of this offering, 47,451,644 shares of our preferred stock will automatically convert into shares of common stock. Also at such time, all outstanding preferred stock warrants will automatically convert into common stock warrants and the related liability will be reclassified to additional paid-in capital. The consideration we received in respect of the preferred stock outstanding at September 30, 2014 ranged from $0.37 to $14.71 per share and averaged $3.84 per share. Each share of preferred stock will convert into one share of common stock without the payment of additional consideration. In addition, certain shares of preferred stock were already repurchased and retired in 2013, when we voluntarily redeemed certain shares of Series A and Series B preferred stock for an aggregate price that was approximately $5.3 million in excess of the carrying amount. The portion of the redemption in excess of the carrying amount was recorded as a reduction to additional paid-in capital and added to net loss to arrive at net loss attributable to common stockholders in the calculation of loss per common share.

-8-

Table of Contents

| Common stock offered by us |

10,000,000 shares | |

| Common stock to be outstanding after this offering |

66,160,636 shares | |

| Option to purchase additional shares to be offered by us |

1,500,000 shares | |

| Use of proceeds |

We intend to use the net proceeds from this offering for general corporate purposes, including working capital, sales and marketing activities, data and analytics enhancements, product development, capital expenditures and to fund a portion of the loans made to our customers. We also may use a portion of the net proceeds to invest in or acquire complementary technologies, solutions or businesses and for targeted international expansion. However, we have no present agreements or commitments for any such investments, acquisitions or expansion. See the section titled “Use of Proceeds.” | |

| Concentration of ownership |

Upon completion of this offering, the executive officers, directors and 5% stockholders of our company and their affiliates will beneficially own, in the aggregate, approximately 60.5% of our outstanding capital stock. | |

| New York Stock Exchange trading symbol |

“ONDK” | |

The number of shares of our common stock to be outstanding after this offering is based on 56,160,636 shares of our common stock outstanding on an as-converted basis as of September 30, 2014, and excludes:

| • | 9,970,802 shares of common stock issuable upon the exercise of options outstanding as of September 30, 2014, with a weighted average exercise price of $3.75 per share and per share exercise prices ranging from $0.27 to $10.66; |

| • | 846,000 shares of common stock issuable upon the exercise of options granted after September 30, 2014, with a weighted average exercise price of $13.22 per share; |

| • | 7,200,000 shares of common stock reserved for issuance under our 2014 Equity Incentive Plan, which will become effective in connection with this offering; |

| • | 1,800,000 shares of common stock reserved for issuance under our 2014 Employee Stock Purchase Plan, which will become effective in connection with this offering; |

| • | 3,612,526 shares of common stock issuable upon the exercise of warrants outstanding as of September 30, 2014, with a weighted average exercise price of $6.94 per share and per share exercise prices ranging from $0.33 to $14.71; and |

| • | 2,000 shares of common stock issuable upon the exercise of one warrant issued after September 30, 2014, with an exercise price of $12.38 per share. |

Unless otherwise noted, the information in this prospectus reflects and assumes the following:

| • | a 2-for-1 forward stock split of our common stock and redeemable convertible preferred stock effected on November 26, 2014; |

-9-

Table of Contents

| • | the conversion of all outstanding shares of our redeemable convertible preferred stock as of September 30, 2014 into an aggregate of 47,451,644 shares of common stock immediately prior to the completion of this offering; |

| • | the filing of our amended and restated certificate of incorporation in connection with the completion of this offering; |

| • | no exercise of outstanding options or warrants; and |

| • | no exercise of the underwriters’ option to purchase additional shares. |

-10-

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables summarize our consolidated financial data. You should read the summary consolidated financial data set forth below in conjunction with our consolidated financial statements, the notes to our consolidated financial statements and the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained elsewhere in this prospectus.

The consolidated statements of operations data for the years ended December 31, 2012 and 2013 are derived from our audited consolidated financial statements included elsewhere in this prospectus. The consolidated statements of operations data for the nine months ended September 30, 2013 and 2014 and balance sheet data as of September 30, 2014 are derived from our unaudited consolidated interim financial statements included elsewhere in this prospectus. The unaudited consolidated financial data for the nine months ended September 30, 2013 and 2014 and as of September 30, 2014 includes all adjustments, consisting only of normal recurring accruals, that are necessary in the opinion of our management for a fair presentation of our financial position and results of operations for these periods. Our historical results are not necessarily indicative of the results that may be expected in any future period.

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||

| 2012 | 2013 | 2013 | 2014 | |||||||||||||

| (in thousands, except share and per share data) | ||||||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||||||

| Revenue: |

||||||||||||||||

| Interest income |

$ | 25,273 | $ | 62,941 | $ | 41,073 | $ | 99,873 | ||||||||

| Gain on sales of loans |

— | 788 | — | 4,569 | ||||||||||||

| Other revenue |

370 | 1,520 | 1,004 | 3,131 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross revenue |

25,643 | 65,249 | 42,077 | 107,573 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cost of revenue: |

||||||||||||||||

| Provision for loan losses |

12,469 | 26,570 | 16,300 | 47,011 | ||||||||||||

| Funding costs |

8,294 | 13,419 | 9,400 | 12,531 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total cost of revenue |

20,763 | 39,989 | 25,700 | 59,542 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net revenue |

4,880 | 25,260 | 16,377 | 48,031 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating expenses: |

||||||||||||||||

| Sales and marketing |

6,633 | 18,095 | 13,566 | 21,799 | ||||||||||||

| Technology and analytics |

5,001 | 8,760 | 6,090 | 11,357 | ||||||||||||

| Processing and servicing |

2,919 | 5,577 | 3,746 | 5,928 | ||||||||||||

| General and administrative |

6,935 | 12,169 | 9,158 | 13,968 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total operating expenses |

21,488 | 44,601 | 32,560 | 53,052 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss from operations |

(16,608 | ) | (19,341 | ) | (16,183 | ) | (5,021 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other (expense) income: |

||||||||||||||||

| Interest expense |

(88 | ) | (1,276 | ) | (1,070 | ) | (274 | ) | ||||||||

| Warrant liability fair value adjustment |

(148 | ) | (3,739 | ) | (1,496 | ) | (9,122 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total other (expense) income |

(236 | ) | (5,015 | ) | (2,566 | ) | (9,396 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss before provision for income taxes |

(16,844 | ) | (24,356 | ) | (18,749 | ) | (14,417 | ) | ||||||||

| Provision for income taxes |

— | — | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss |

(16,844 | ) | (24,356 | ) | (18,749 | ) | (14,417 | ) | ||||||||

| Series A and Series B preferred stock redemptions |

— | (5,254 | ) | (5,254 | ) | — | ||||||||||

| Accretion of dividends on redeemable convertible preferred stock |

(3,440 | ) | (7,470 | ) | (5,414 | ) | (9,828 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss attributable to common stockholders |

$ | (20,284 | ) | $ | (37,080 | ) | $ | (29,417 | ) | $ | (24,245 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss per share of common stock—basic and diluted |

$ | (4.27 | ) | $ | (8.64 | ) | $ | (6.87 | ) | $ | (4.24 | ) | ||||

|

|

|

|

|

|

|

|

|

|||||||||

| Pro forma net loss per share of common stock—basic and diluted(1) |

$ | (0.60 | ) | $ | (0.11 | ) | ||||||||||

|

|

|

|

|

|||||||||||||

| Weighted average shares of common stock used in computing net loss per share—basic and diluted |

4,750,440 | 4,292,026 | 4,285,136 | 5,715,742 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average shares of common stock used in computing pro forma net loss per share—basic and diluted(1) |

43,088,994 | 51,167,768 | ||||||||||||||

|

|

|

|

|

|||||||||||||

-11-

Table of Contents

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||

| 2012 | 2013 | 2013 | 2014 | |||||||||||||

| (in thousands, except share and per share data) | ||||||||||||||||

| Stock-based compensation expense included above: |

||||||||||||||||

| Sales and marketing |

$ | 47 | $ | 118 | $ | 71 | $ | 325 | ||||||||

| Technology and analytics |

7 | 47 | 20 | 290 | ||||||||||||

| Processing and servicing |

9 | 30 | 15 | 126 | ||||||||||||

| General and administrative |

166 | 243 | 161 | 706 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total stock-based compensation expense |

$ | 229 | $ | 438 | $ | 267 | $ | 1,447 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other financial data: |

||||||||||||||||

| Adjusted EBITDA(2) |

$ | (14,834 | ) | $ | (16,258 | ) | $ | (14,152 | ) | $ | (726 | ) | ||||

| Adjusted net loss(3) |

$ | (16,467 | ) | $ | (20,179 | ) | $ | (16,986 | ) | $ | (3,848 | ) | ||||

| (1) | Pro forma basic and diluted net loss per share of common stock have been calculated assuming (i) the conversion of all outstanding shares of redeemable convertible preferred stock at December 31, 2013 and September 30, 2014 into an aggregate of 41,098,330 and 47,451,644 shares of common stock, respectively, as of the beginning of the applicable period or at the time of issuance, if later, (ii) the redemption of Series A and Series B preferred stock as of the beginning of the applicable period, and (iii) the reclassification of outstanding preferred stock warrants from liabilities to additional paid-in capital as of the beginning of the applicable period. |

| (2) | Adjusted EBITDA is not a financial measure prepared in accordance with GAAP. Adjusted EBITDA represents our net loss, adjusted to exclude interest expense associated with debt used for corporate purposes, income tax expense, depreciation and amortization, stock-based compensation expense and warrant liability fair value adjustment. Adjusted EBITDA does not adjust for funding costs, which represent the interest expense associated with debt used for lending purposes. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures” for more information and for a reconciliation of Adjusted EBITDA to net loss, the most directly comparable financial measure calculated in accordance with GAAP. |

| (3) | Adjusted net loss is not a financial measure prepared in accordance with GAAP. We define Adjusted net loss as net loss adjusted to exclude stock-based compensation expense and warrant liability fair value adjustment. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures” for more information and for a reconciliation of Adjusted net loss to net loss, the most directly comparable financial measure calculated in accordance with GAAP. |

| As of September 30, 2014 | ||||||||||||

| Actual | Pro forma(1) | Pro forma as adjusted(2) |

||||||||||

| (in thousands) | ||||||||||||

| Consolidated Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

$ | 22,642 | $ | 22,642 | $ | 176,742 | ||||||

| Restricted cash |

22,615 | 22,615 | 22,615 | |||||||||

| Loans, net of allowance for loan losses |

393,635 | 393,635 | 393,635 | |||||||||

| Loans held for sale |

2,653 | 2,653 | 2,653 | |||||||||

| Total assets |

466,007 | 466,007 | 620,107 | |||||||||

| Funding debt(3) |

347,204 | 347,204 | 347,204 | |||||||||

| Corporate debt(4) |

3,000 | 3,000 | 3,000 | |||||||||

| Total liabilities |

368,077 | 365,275 | 365,275 | |||||||||

| Total redeemable convertible preferred stock |

218,363 | — | — | |||||||||

| Total stockholders’ (deficit) equity |

(120,433 | ) | 100,732 | 254,832 | ||||||||

| (1) | The pro forma column reflects the conversion of all outstanding shares of convertible preferred stock at September 30, 2014 into 47,451,644 shares of common stock immediately prior to the closing of this offering. The consideration paid for each share of convertible preferred stock outstanding at September 30, 2014 ranged from $0.37 to $14.71 and averaged $3.84. Each share of preferred stock will convert into one share of common stock without the payment of additional consideration. The conversion of the convertible preferred stock and the warrant liability reduces total redeemable convertible preferred stock and total liabilities by $218.4 million and $2.8 million, respectively. |

-12-

Table of Contents

| (2) | The pro forma as adjusted column reflects the pro forma adjustments described in footnote (1) above and the sale by us of shares of common stock in this offering at an assumed initial public offering price of $17.00 per share, the midpoint of the price range set forth on the cover page of this prospectus, after deducting the underwriting discount and commissions and estimated offering expenses payable by us. A $1.00 increase (decrease) in the assumed initial public offering price of $17.00 per share would increase (decrease) each of pro forma as adjusted cash and cash equivalents, working capital, total assets and total stockholders’ equity by $9.3 million, assuming the number of shares we are offering, as set forth on the cover page of this prospectus, remains the same, after deducting the underwriting discount and commissions and estimated offering expenses payable by us. The pro forma as adjusted information is illustrative only, and we will adjust this information based on the actual initial public offering price, number of shares offered and other terms of this offering determined at pricing. |

| (3) | Funding debt is used to fund loan originations and is non-recourse to On Deck Capital, Inc. |

| (4) | Corporate debt is used to fund general corporate operations. |

-13-

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the following risks and all other information contained in this prospectus, including our consolidated financial statements and the related notes, before investing in our common stock. The risks and uncertainties described below are not the only ones we face, but include the most significant factors currently known by us that make the offering speculative or risky. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, also may become important factors that affect us. If any of the following risks materialize, our business, financial condition and results of operations could be materially harmed. In that case, the trading price of our common stock could decline, and you may lose some or all of your investment.

We have a limited operating history in an evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful.

We have a limited operating history in an evolving industry that may not develop as expected. Assessing our business and future prospects is challenging in light of the risks and difficulties we may encounter. These risks and difficulties include our ability to:

| • | increase the number and total volume of term loans and lines of credit we extend to our customers; |

| • | improve the terms on which we lend to our customers as our business becomes more efficient; |

| • | increase the effectiveness of our direct marketing, as well as our strategic partner and funding advisor program customer acquisition channels; |

| • | increase repeat borrowing by existing customers; |

| • | successfully develop and deploy new products; |

| • | successfully maintain our diversified funding strategy, including through the OnDeck Marketplace and future securitization transactions; |

| • | favorably compete with other companies that are currently in, or may in the future enter, the business of lending to small businesses; |

| • | successfully navigate economic conditions and fluctuations in the credit market; |

| • | effectively manage the growth of our business; |

| • | successfully expand our business into adjacent markets; and |

| • | successfully expand internationally. |

We may not be able to successfully address these risks and difficulties, which could harm our business and cause our operating results to suffer.

Our recent, rapid growth may not be indicative of our future growth and, if we continue to grow rapidly, we may not be able to manage our growth effectively.

Our gross revenue grew from $25.6 million in 2012 to $65.2 million in 2013 and from $42.1 million for the nine months ended September 30, 2013 to $107.6 million for the nine months ended September 30, 2014. We expect that, in the future, even if our revenue continues to increase, our rate of revenue growth will decline.

In addition, we expect to continue to expend substantial financial and other resources on:

| • | personnel, including significant increases to the total compensation we pay our employees as we grow our employee headcount; |

| • | marketing, including expenses relating to increased direct marketing efforts; |

-14-

Table of Contents

| • | product development, including the continued development of our platform and OnDeck Score; |

| • | diversification of funding sources, including through OnDeck Marketplace; |

| • | office space, as we increase the space we need for our growing employee base; and |

| • | general administration, including legal, accounting and other compliance expenses related to being a public company. |

In addition, our historical rapid growth has placed, and may continue to place, significant demands on our management and our operational and financial resources. Finally, our organizational structure is becoming more complex as we add additional staff, and we will need to improve our operational, financial and management controls as well as our reporting systems and procedures. If we cannot manage our growth effectively our financial results will suffer.

We have a history of losses and may not achieve consistent profitability in the future.

We generated net losses of $16.8 million, $24.4 million, $18.7 million and $14.4 million in 2012, 2013 and for the nine months ended September 30, 2013 and 2014, respectively. As of September 30, 2014, we had an accumulated deficit of $119.7 million. We will need to generate and sustain increased revenue levels in future periods in order to become profitable, and, even if we do, we may not be able to maintain or increase our level of profitability. We intend to continue to expend significant funds to expand our marketing and sales operations, increase our customer service and general loan servicing capabilities, meet the increased compliance requirements associated with our transition to and operation as a public company, lease additional space for our growing employee base, upgrade our data center infrastructure and expand into new markets. In addition, we record our loan loss provision as an expense to account for the possibility that all loans may not be repaid in full. Because we incur a given loan loss expense at the time that we issue the loan, we expect the aggregate amount of this expense to grow as we increase the number and total amount of loans we make to our customers.

Our efforts to grow our business may be more costly than we expect, and we may not be able to increase our revenue enough to offset our higher operating expenses. We may incur significant losses in the future for a number of reasons, including the other risks described in this prospectus, and unforeseen expenses, difficulties, complications and delays, and other unknown events. If we are unable to achieve and sustain profitability, the market price of our common stock may significantly decrease.

Worsening economic conditions may result in decreased demand for our loans, cause our customers’ default rates to increase and harm our operating results.

Uncertainty and negative trends in general economic conditions in the United States and abroad, including significant tightening of credit markets, historically have created a difficult environment for companies in the lending industry. Many factors, including factors that are beyond our control, may have a detrimental impact on our operating performance. These factors include general economic conditions, unemployment levels, energy costs and interest rates, as well as events such as natural disasters, acts of war, terrorism and catastrophes.

Our customers are small businesses. Accordingly, our customers have historically been, and may in the future remain, more likely to be affected or more severely affected than large enterprises by adverse economic conditions. These conditions may result in a decline in the demand for our loans by potential customers or higher default rates by our existing customers. If a customer defaults on a loan payable to us, the loan enters a collections process where our systems and collections teams initiate contact with the customer for payments owed. If a loan is subsequently charged off, we generally sell the loan to a third-party collection agency and receive only a small fraction of the remaining amount payable to us in exchange for this sale.

There can be no assurance that economic conditions will remain favorable for our business or that demand for our loans or default rates by our customers will remain at current levels. Reduced demand for our loans would

-15-

Table of Contents

negatively impact our growth and revenue, while increased default rates by our customers may inhibit our access to capital, hinder the growth of our OnDeck Marketplace and negatively impact our profitability. Furthermore, we have received a large number of applications from potential customers who do not satisfy the requirements for an OnDeck loan. If an insufficient number of qualified small businesses apply for our loans, our growth and revenue could decline.

Many of our strategic partnerships are nonexclusive and subject to termination options that, if terminated, could harm the growth of our customer base and negatively affect our financial performance. Additionally, these partners are concentrated and the departure of a significant partner could have a negative impact on our operating results.

We rely on strategic partners for referrals of an increasing portion of the customers, to whom we issue loans and our growth depends in part on the growth of these referrals. In 2012 and 2013 and for the nine months ended September 30, 2013 and 2014, loans issued to customers referred to us by our strategic partners constituted 5.5%, 9.2%, 9.5% and 12.7% of our total loan originations, respectively. Many of our strategic partnerships do not contain exclusivity provisions that would prevent such partners from providing leads to competing companies. In addition, the agreements governing these partnerships contain termination provisions that, if exercised, would terminate our relationship with these partners. These agreements also contain no requirement that a partner refer us any minimum number of leads. There can be no assurance that these partners will not terminate our relationship with them or continue referring business to us in the future, and a termination of the relationship or reduction in leads referred to us would have a negative impact on our revenue and operating results.

In addition, a small number of strategic partners refer to us a significant portion of the loans made within this channel. In 2012 and 2013 and for the nine months ended September 30, 2013 and 2014, loans issued to customers referred to us by our top 4 strategic partners constituted 4.7%, 6.8%, 6.8% and 9.4% of our total loan originations, respectively. In the event that one or multiple of these significant strategic partners terminated our relationship or reduced the number of leads provided to us, our business would be harmed.

To the extent that Funding Advisor Program partners or direct sales agents mislead loan applicants or are engaged in disreputable behavior, our reputation may be harmed and we may face liability.

We rely on third-party independent advisors, including business loan brokers, which we call Funding Advisor Program partners, or FAPs, for referrals of a substantial portion of the customers to whom we issue loans. In 2012 and 2013 and for the nine months ended September 30, 2013 and 2014, loans issued to customers whose applications were submitted to us via the FAP channel constituted 75.1%, 56.4%, 56.8% and 44.3% of our total loan originations, respectively. Historically, our practice has been to conduct a personal criminal background check on one of the authorized representatives of all prospective FAPs as one element of the FAP application process; however, we have not performed such checks on all employees or agents of a FAP who might be involved in the marketing and sale of our products and we have not conducted any background checks with respect to any FAPs that joined the Funding Adviser Program before 2010 or who had an annual revenue greater than $15 million. Going forward, we plan to expand the extent to which our funding advisor partners are required to submit to and conduct background checks. Because FAPs earn fees on a commission basis, FAPs may have incentive to mislead loan applicants, facilitate the submission by loan applicants of false application data or engage in other disreputable behavior so as to earn additional commissions on those inaccurate loan applications. While we strictly prohibit, by policy and contract, all FAPs from charging customers any additional un-authorized fees, it is possible that some FAPs may attempt to charge such fees despite our prohibition. We also rely on our direct sales agents for customer acquisition in our direct marketing channel, and these sales agents may also engage in disreputable behavior to increase our customer base. If FAPs or our direct sales agents mislead our customers or engage in any other disreputable behavior, our customers are less likely to be satisfied with their experience and to become repeat customers, and we may be subject to costly and time-consuming litigation, each of which could harm our reputation and operating performance. We recently have been subject to negative publicity related to our FAP channel,

-16-

Table of Contents

including regarding the alleged backgrounds of certain of their employees. If we continue to experience such negative publicity, our ability to continue to increase our revenue could be impaired and our business could otherwise be materially and negatively impacted.

We are planning to implement certain enhanced contractual provisions and compliance-related measures related to our funding advisor channel, including enhanced screening procedures. While these measures are intended to improve certain aspects of how we work with funding advisors and how they work with our customers, we cannot assure you that the measures will be timely implemented, whether they will work as intended, that other compliance-related concerns will not emerge in the future, that the funding advisors will agree to and will comply with these measures, and that these measures will not negatively impact our business from this channel, including our financial performance, or have other unintended or negative impacts on our business.

We pay commissions to our strategic partners and FAPs upfront and generally do not recover them in the event the related loan or line of credit is eventually charged-off.

We pay commissions to strategic partners and FAPs on the term loans and lines of credit we originate through these channels. We pay these commissions at the time the term loan is funded or line of credit account is opened. However, we generally do not require that this commission be repaid to us in the event of a default on a term loan or line of credit. While we generally discontinue working with strategic partners and FAPs that refer customers to us that ultimately have unacceptably high levels of defaults, to the extent that our strategic partners and FAPs are not at risk of forfeiting their commissions in the event of defaults, they may to an extent be indifferent to the riskiness of the potential customers that they refer to us.

Our business may be adversely affected by disruptions in the credit markets, including reduced access to credit.

We depend on debt facilities and other forms of debt in order to finance most of the loans we make to our customers. However, we cannot guarantee that these financing sources will continue to be available beyond the current maturity date of each debt facility, on reasonable terms or at all. As the volume of loans that we make to customers on our platform increases, we may require the expansion of our borrowing capacity on our existing debt facilities and other debt arrangements or the addition of new sources of capital. The availability of these financing sources depends on many factors, some of which are outside of our control. We may also experience the occurrence of events of default or breaches of financial or performance covenants under our debt agreements, which could reduce or terminate our access to institutional funding. In addition, we began selling loans to third parties via our OnDeck Marketplace in October 2013 and completed our first securitization transaction in May 2014. There can be no assurance that investors will continue to purchase our loans via our OnDeck Marketplace or that we will be able to successfully access the securitization markets again. Furthermore, because we only recently began accessing these sources of capital, there is a greater possibility that these sources of capital may not be available in the future. In the event of a sudden or unexpected shortage of funds in the banking system, we cannot be sure that we will be able to maintain necessary levels of funding without incurring high funding costs, a reduction in the term of funding instruments or the liquidation of certain assets. If we were to be unable to arrange new or alternative methods of financing on favorable terms, we may have to curtail our origination of loans, which could have a material adverse effect on our business, financial condition, operating results and cash flow.

If the information provided by customers to us is incorrect or fraudulent, we may misjudge a customer’s qualification to receive a loan and our operating results may be harmed.

Our lending decisions are based partly on information provided to us by loan applicants. To the extent that these applicants provide information to us in a manner that we are unable to verify, the OnDeck Score may not accurately reflect the associated risk. In addition, data provided by third-party sources is a significant component of the OnDeck Score and this data may contain inaccuracies. Inaccurate analysis of credit data that could result from false loan application information could harm our reputation, business and operating results.

-17-

Table of Contents

In addition, we use identity and fraud checks analyzing data provided by external databases to authenticate each customer’s identity. There is a risk, however, that these checks could fail, and fraud may occur. We may not be able to recoup funds underlying loans made in connection with inaccurate statements, omissions of fact or fraud, in which case our revenue, operating results and profitability will be harmed. Fraudulent activity or significant increases in fraudulent activity could also lead to regulatory intervention, negatively impact our operating results, brand and reputation and require us to take steps to reduce fraud risk, which could increase our costs.

Our current level of interest rate spread may decline in the future. Any material reduction in our interest rate spread could reduce our profitability.

We earn a substantial majority of our revenues from interest payments on the loans we make to our customers. Financial institutions and other funding sources provide us with the capital to fund these term loans and lines of credit and charge us interest on funds that we draw down. In the event that the spread between the rate at which we lend to our customers and the rate at which we borrow from our lenders decreases, our financial results and operating performance will be harmed. The interest rates we charge to our customers and pay to our lenders could each be affected by a variety of factors, including access to capital based on our business performance, the volume of loans we make to our customers, competition and regulatory requirements. These interest rates may also be affected by a change over time in the mix of the types of products we sell to our customers and investors and a shift among our channels of customer acquisition. Interest rate changes may adversely affect our business forecasts and expectations and are highly sensitive to many macroeconomic factors beyond our control, such as inflation, recession, the state of the credit markets, changes in market interest rates, global economic disruptions, unemployment and the fiscal and monetary policies of the federal government and its agencies. Any material reduction in our interest rate spread could have a material adverse effect on our business, results of operations and financial condition.

If the choice of law provisions in our loan agreements are found to be unenforceable, we may be found to be in violation of state interest rate limit laws.

Although the federal government does not currently regulate the maximum interest rates that may be charged on private loan transactions, many states have enacted interest rate limit laws specifying the maximum legal interest rate at which loans can be made in the state. We apply Virginia law to the underlying agreement for loans that we originate because our loans are underwritten and entered into in the state of Virginia, where our underwriting, servicing, operations and collections teams are headquartered.