Attached files

| file | filename |

|---|---|

| 8-K - 8-K - KINDRED HEALTHCARE, INC | d817701d8k.htm |

| EX-99.2 - EX-99.2 - KINDRED HEALTHCARE, INC | d817701dex992.htm |

| EX-99.1 - EX-99.1 - KINDRED HEALTHCARE, INC | d817701dex991.htm |

Kindred

Healthcare Third Quarter Investor Update

November 6, 2014

Exhibit 99.3 |

Forward-Looking Statements

2

This presentation includes forward-looking statements within the meaning of Section 27A of

the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended.

These forward-looking statements include, but are not limited to, statements regarding the

proposed business combination transaction between Kindred Healthcare, Inc. (“Kindred” or the “Company”)

and Gentiva Health Services, Inc. (“Gentiva”) (NASDAQ:GTIV) (including financing of

the proposed transaction and the benefits, results, effects and timing of a transaction), all statements regarding

Kindred’s (and Kindred’s and Gentiva’s combined) expected future financial

position, results of operations, cash flows, dividends, financing plans, business strategy, budgets, capital expenditures,

competitive positions, growth opportunities, plans and objectives of management, and

statements containing the words such as “anticipate,” “approximate,” “believe,” “plan,” “estimate,” “expect,”

“project,” “could,” “would,” “should,”

“will,” “intend,” “may,” “potential,” “upside,” and other similar expressions. Statements in this presentation concerning the business outlook or future economic

performance, anticipated profitability, revenues, expenses, dividends or other financial

items, and product or services line growth of Kindred (and the combined businesses of Kindred and Gentiva),

together with other statements that are not historical facts, are forward-looking

statements that are estimates reflecting the best judgment of Kindred based upon currently available information.

Such forward-looking statements are inherently uncertain, and stockholders and other

potential investors must recognize that actual results may differ materially from Kindred’s expectations as a result

of a variety of factors, including, without limitation, those discussed below. Such

forward-looking statements are based upon management’s current expectations and include known and unknown risks,

uncertainties and other factors, many of which Kindred is unable to predict or control, that

may cause Kindred’s actual results, performance or plans with respect to Gentiva to differ materially from any

future results, performance or plans expressed or implied by such forward-looking

statements. These statements involve risks, uncertainties and other factors discussed below and detailed from time to

time in Kindred’s filings with the Securities and Exchange Commission (the

“SEC”).

Risks and uncertainties related to the proposed merger include, but are not limited to, the

risk that Gentiva’s stockholders do not approve the merger, potential adverse reactions or changes to business

relationships resulting from the announcement or completion of the merger, uncertainties as to

the timing of the merger, adverse effects on Kindred’s stock price resulting from the announcement or

completion of the merger, competitive responses to the announcement or completion of the

merger, the risk that healthcare regulatory, licensure or other approvals and financing required for the

consummation of the merger are not obtained or are obtained subject to terms and conditions

that are not anticipated, costs and difficulties related to the integration of Gentiva’s businesses and

operations with Kindred’s businesses and operations, the inability to obtain, or delays

in obtaining, cost savings and synergies from the merger, uncertainties as to whether the completion of the merger

or any transaction will have the accretive effect on Kindred’s earnings or cash flows

that it expects, unexpected costs, liabilities, charges or expenses resulting from the merger, litigation relating to the

merger, the inability to retain key personnel, and any changes in general economic and/or

industry-specific conditions.

In addition to the factors set forth above, other factors that may affect Kindred’s

plans, results or stock price are set forth in Kindred’s Annual Report on Form 10-K and in its reports on Forms 10-Q

and 8-K.

Many of these factors are beyond Kindred’s control. Kindred cautions investors that any

forward-looking statements made by Kindred are not guarantees of future performance. Kindred disclaims any

obligation to update any such factors or to announce publicly the results of any revisions to

any of the forward-looking statements to reflect future events or developments. Kindred has

provided information in this presentation to compute certain non-GAAP measurements for specified periods. A reconciliation of the non-GAAP measurements to the GAAP measurements is

included in this presentation and on Kindred’s website at

www.kindredhealthcare.com under the heading “investors.”

Additional

Information

This presentation does not constitute an offer to sell or the solicitation of an offer to buy

any securities or a solicitation of any vote or approval. This communication may be deemed to be solicitation

material in respect of the proposed merger between Kindred and Gentiva. In connection

with the proposed merger, Kindred intends to file a registration statement on Form S-4, containing a proxy

statement/prospectus, with the SEC. SHAREHOLDERS OF GENTIVA ARE URGED TO READ ALL

RELEVANT DOCUMENTS FILED WITH THE SEC, INCLUDING THE PROXY STATEMENT/PROSPECTUS, BECAUSE

THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED MERGER. Investors and

security holders will be able to obtain copies of the proxy statement/prospectus as well as other filings

containing information about Kindred and Gentiva, without charge, at the SEC’s website, www.sec.gov. Those documents, when filed, as well as Kindred’s other public filings with the SEC, may be

obtained without charge at Kindred’s website at

www.kindredhealthcare.com. Participants in Solicitation

Kindred and its directors and executive officers, and Gentiva and its directors and executive

officers, may be deemed to be participants in the solicitation of proxies from the holders of Gentiva common

stock in respect of the proposed merger. Information about the directors and executive

officers of Kindred is set forth in the proxy statement for Kindred’s 2014 Annual Meeting of Shareholders, which

was filed with the SEC on April 3, 2014. Information about the directors and executive

officers of Gentiva is set forth in the proxy statement for Gentiva’s 2014 Annual Meeting of Shareholders, which was

filed with the SEC on March 25, 2014. Investors may obtain additional information regarding

the interest of such participants by reading the proxy statement/prospectus regarding the proposed merger

when it becomes available. |

Kindred

Healthcare’s Third Quarter – Achievements and Opportunities

Continued Progress on Employee Engagement, Quality Assurance, Clinical

Outcomes and Patient Satisfaction Measures Across the Enterprise

Strong Third Quarter Results and Reaffirming Confidence in 2014 EPS Guidance

Continued Progress Advancing Integrated Care Market Strategy and

Development of Care Management Capabilities

Commencement of Growth Phase of Strategic Plan

(Repositioning and Recapitalization Complete)

Announced Definitive Agreement to acquire Gentiva, solidifying Kindred’s Position

as the Premier Post-Acute Healthcare Services Provider in the U.S.

3 |

Third

Quarter

–

Continuing

Operations

(1)

($ millions, except statistics)

•

Key Q3 operating metrics:

Strong revenue and operating income growth, up 6% and 7%, respectively, compared to prior

year Improved operating income and operating margins across all divisions, lower

interest costs and solid cost controls across the organization driving

year-over-year results Hospital same-store volumes up 3% over prior year,

cost Per Patient Day (“PPD”) up less than 1% over prior year

Strong sequential cash flows with core operating cash flows of $95 million and core free cash

flows were $72 million

4

(1)

Before certain disclosed items reconciled in the appendix.

(2)

Prior year EPS of $0.10 is pro forma to include incremental 9.7 million shares issued in the

June 2014 equity offering. Actual core EPS for Q3 ‘13 is $0.12.

Actual

Prior Year

% change

Revenues

$1,243

$1,175

+6%

Operating expenses

1,085

1,027

Core operating income (EBITDAR)

158

148

+7

Margin

12.7%

12.6%

Net income -

core

7

7

+7

Diluted EPS -

core

$0.11

$0.10

(2)

+10

Diluted EPS -

reported

$0.03

($0.31) |

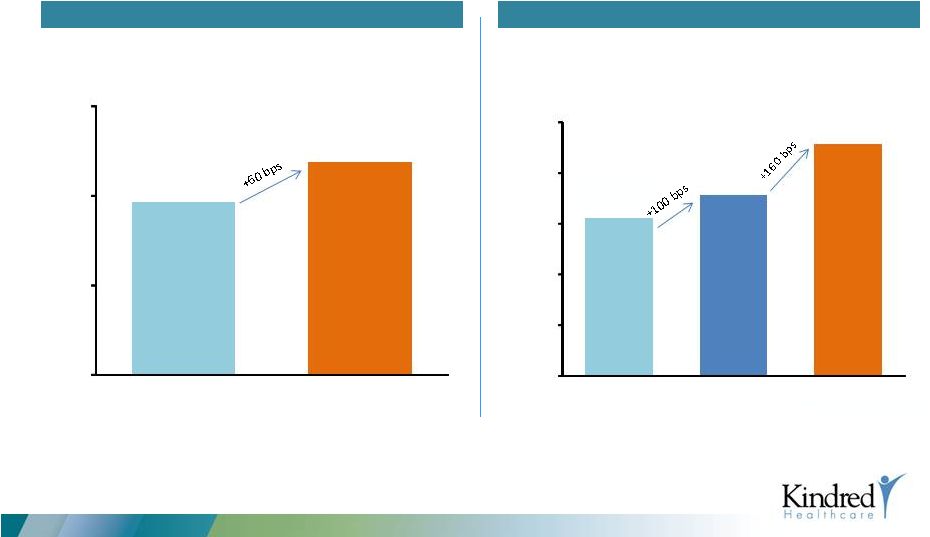

Core Operating

Margins (1)

Margin Expansion Across Enterprise Reflects Full Recovery from Reimbursement Cuts

5

(1)

Before certain disclosed items reconciled in the Appendix.

3Q13

3Q13

3Q13

3Q13

3Q14

3Q14

3Q14

3Q14

20.0%

11.9%

11.0%

4.0%

20.1%

13.1%

11.7%

8.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Hospitals

Nursing Centers

RehabCare

Kindred at Home |

$595

$609

$1,628

$1,642

$1,250

$1,350

$1,450

$1,550

$1,650

$1,750

$450

$500

$550

$600

$650

Q3 '13

Q3 '14

Q3 '13

Q3 '14

Hospital Division

$2.5 billion Revenues

(1)

$527 million Operating Income

(2)

Transitional Care Hospitals (certified as LTAC hospitals)

•

97

Transitional

Care

Hospitals

(3)

•

7,145

licensed

beds

(3)

Inpatient Rehabilitation Hospitals (IRFs)

•

5 IRFs

(3)

•

215 licensed beds

(3)

(1)

Revenues for the twelve months ended September 30, 2014 (divisional revenues before

intercompany eliminations). (2)

Operating income for the twelve months ended September 30, 2014.

(3)

As of September 30, 2014.

(4)

Before certain disclosed items reconciled in the Appendix.

•

Continued clinical success with low rates of

rehospitalizations, reduced employee

turnover and a strong online reputation

•

Strong results with same-store admissions

increase of 3% and less than 1% growth in

core operating costs per patient day

•

Strong operating income margin of 20.1%

(4)

6

Q3 Revenue

Revenue

($ millions)

Per Patient Day Revenues

Q3 Operating Income

(4)

($ millions)

$119

$122

$100

$110

$120

$130

Q3 '13

Q3 '14 |

•

2,264 sites of service served through

20,338 therapists

(3)

•

Including 102 hospital-based acute

rehabilitation units

(3)

•

RehabCare continues to deliver outstanding clinical

results and improved patient functional

improvement across sites of service

•

Year-over-year core operating income and margin

improvements

•

Added 90 net new skilled nursing rehabilitation

sites YTD through Q3 2014

$1.3 billion Revenues

(1)

$146 million Operating Income

(2)

(1)

Revenues for the twelve months ended September 30, 2014 (divisional revenues before

intercompany eliminations). (2)

Operating income for the twelve months ended September 30, 2014.

(3)

As of September 30, 2014.

7

Total Sites of Service

Productivity

2,139

2,264

0

600

1,200

1,800

2,400

2011

Q3 2014

80.4%

79.6%

0.0%

30.0%

60.0%

90.0%

2011

Q3 2014 |

Nursing Center

Division •

48 Transitional Care

Centers

(Sub-Acute

facilities

licensed

as

SNFs)

(3)

•

13 Nursing and Rehabilitation Centers

(with

Transitional

Care

Units)

(3)

•

12 Hospital-Based Sub-Acute Units

(3)

•

38

Skilled

Nursing

Centers

(Traditional

SNFs)

(3)

•

Strong operations with low nursing turnover

and improved performance on CMS 5-Star

Program

•

Nursing center division core operating

income increased 16%

(4)

primarily due to

growth in revenues

•

Operating margins significantly improved due

to increased reimbursement rates, ongoing

repositioning and cost control initiatives

•

Admissions up 4% compared to prior year

•

Declines in average length of stay (ALOS)

continue to weigh on average daily census

(ADC)

$1.1 billion Revenues

(1)

$147 million Operating Income

(2)

(1)

Revenues for the twelve months ended September 30, 2014 (divisional revenues before

intercompany eliminations). (2)

Operating income for the twelve months ended September 30, 2014.

(3)

As of September 30, 2014.

(4)

Before certain disclosed items reconciled in the Appendix.

8

Nursing

Center

Operating

Income

Margin

(4)

11.9%

13.2%

13.8%

14.3%

13.1%

10.0%

12.0%

14.0%

16.0%

Q3 2013

Q4 2013

Q1 2014

Q2 2014

Q3 2014 |

•

High rates of patient satisfaction for Home Health and

Hospice with nearly 50% of all home health locations

named to HomeCare Elite as top 25% of the nation’s

home health agencies

•

Kindred at Home division delivered 60% revenue growth

in the third quarter of 2014 and more than tripled core

operating income compared to prior year quarter

•

Focus on integration efforts has improved margin from

4.0%

(3)

in

Q3

2013

to

8.2%

(3)

in

Q3

2014

•

Combination with Gentiva creates largest home health

and hospice system in the U.S.

9

•

201

sites

of

service

in

13

states

(2)

•

4,900

caregivers

serving

17,300

patients

on

a daily basis

(2)

(1)

Annualized based upon revenues (before intercompany eliminations) and operating income for the

three months ended September 30, 2014. (2)

As of September 30, 2014.

(3)

Before certain disclosed items reconciled in the Appendix.

(4)

Operating income for the twelve months ended December 31, 2013.

Revenue

($ millions)

Operating Income

($ millions)

$345 million Revenues

(1)

$27 million Operating Income

(1)

(1)

(1)

(4)

$225

$345

$0

$100

$200

$300

$400

2013

2014

$10

$27

$0

$10

$20

$30

2013

2014 |

Kindred and

Gentiva A Compelling Opportunity for

American Healthcare and Shareholders

10 |

Combination

Creates One of the Nation’s Premier Healthcare Services Providers

11

Leadership Among Premium Healthcare Service Providers

2014 Wall Street

Consensus Revenue

($ in billions)

Pro Forma

Post-Acute Providers

Alternate Site Providers

(4)

$7.1

$5.5

$3.8

$3.1

$2.4

$6.4

$12.7

$4.4

IPCM

DVA

EVHC

AMSG

SCAI

The acquisition of Gentiva further strengthens Kindred’s ability to serve

patients across the full continuum of care

($ in millions)

Kindred

Gentiva

Pro Forma

States

(1)

47

40

47

Locations

(1)

2,376

493

2,869

Employees

(1)

62,600

46,600

109,200

Revenue Guidance/Consensus

$5.1 billion

(2)

$2.0 billion

(2)

$7.1 billion

Patients Per Year

(3)

535,000

550,000

1,085,000

$1.2

$2.7

$1.6

(1)

As of September 30, 2014.

(2)

Per Kindred 2014 guidance as provided on November 5, 2014 and 2014 current average analyst

consensus estimates for Gentiva. (3)

Internal company data.

(4)

Twelve months ended (LTM) as of June 30, 2014 and pro forma for Skilled Healthcare

merger. (2) |

Revenues

(1)

$345 MM

Total States

(3)

13

Average Daily Census

(4)

17,300

Total Sites of Service

(3)

201

Home Health

141

Hospice

38

Personal Care

22

Total Caregivers

(3)

4,900

Revenues

(2)

$2.0 B

Total States

(3)

40

Average

Daily

Census

(4)

110,000

Total Sites of Service

(3)

493

Home Health

294

Hospice

165

Community Care

34

Total Caregivers

(3)

40,500

Revenues

(1) (2)

$2.3 B

Total States

41

Average Daily Census

127,300

Total Sites of Service

694

Home Health

435

Hospice

203

Community Care

56

Total Caregivers

45,400

Kindred at Home

Pro Forma Company

Combination creates

largest home health and

hospice system in the

United States

Gentiva

Kindred at Home

12

(1)

Annualized based upon revenues for the three months ended September 30, 2014 (divisional

revenues before intercompany eliminations). (2)

Current average analyst consensus estimate for 2014.

(3)

As of September 30, 2014.

(4)

Internal company data for Kindred and investor presentation for Gentiva.

Gentiva |

Gentiva

Integration Management Office Integration Operating Principles

Integration Operating Principles

Prevent disruption to patient care

Prevent harm to target revenue

streams

Retain key talent

Meet all reporting obligations

Ensure Day 1 Readiness

Achieve synergies

INPUTS

IMO steering committee

feedback

Future state objectives

Integration red flags /

anticipated

complexities

(1)

Lessons learned from previous

Kindred IMO

(1) As identified during due diligence.

13 |

Defining Day 1 Readiness

Day one readiness focuses on the details necessary to bring business functions

and processes into alignment at closing.

Focus Areas for Day 1 Readiness / Controls:

-

Payroll Continuity

-

Stability of revenue cycle functions:

-

Accounts receivable

-

Accounts payable

-

Financial Reporting (i.e. financial suite & systems)

-

Synergy Capture

-

Validated synergy

-

Identified initiatives for realizations

-

Developed execution plans for realization

To be completed

Assessment of

controls

Assessment of

systems

Consolidation

plan complete

Ready for Day 1

execution

Gentiva Integration Management Office

Defining Day One Readiness

14 |

Synergy

Initiative Development

Chris Consalus

Day 1 Readiness

and Transitional

Operating Models

Employee Retention

Functional integration workstreams

IT

People Services

Finance &

Procurement

Compliance &

Legal

Operations

Sales

Applications

Networks

Hosting

Charlie Wardrip /

Russ McDonough

Payroll

Organization

Structure

Benefits & Comp

Selection

Process

Jeff Jasnoff /

Ed Reisz

Accounting

Tax & Treasury

Financial

Reporting

Internal Audit

Purchasing

Mark Laemmle /

Todd Flowers /

Eric Slusser

Legal & Regulatory

Risk Mgt &

Compliance

External Affairs

Records Retention

Kelly Priegnitz /

Joe Landenwich

/ Suzanne

Riedman / John

Camperlengo

Care Mgt

Home Health

Reimbursement

Care Mgt

Hospice

Managed Care

Facilities

Jon Rousseau /

Todd Higgins /

Susan Sender /

David Causby

Identify Overlaps

Plan Organization

Structure

Plan sales force

rationalization

David Mikula /

Dean Johnson

Plans for Revenue

Synergies

Cross-functional

integration

workstreams

Integration team structure

Executive Sponsorship

Steve Cunanan, Scott Blanchette

IMO

Mark

Douglas

Gentiva

IMO

(support):

Janet

Nicoll

KPMG

Kindred / GTIV Advisory Team:

Operations –

Jon Rousseau / David

Causby Corporate Development

–

Doug Curnutte

Finance

–

Todd Higgins / Eric

Slusser Benefits & Compensation

–

Andrea Romisher

IS/IT

–

Vance Collins

Communications

–

Susan Moss / Paula

Shoemaker We

Have

Assembled

Functional

Teams,

as

Well

as

Teams

That

Will

Help

Us

Work

On

Key

Cross-Functional

Integration

Priorities

Communication &

Change

Management

Gentiva’s functional

IMO leader indicated

in orange font

Gentiva Integration Management Office

Integration Team Structure

15

IMO Lead: |

Transaction

Summary Purchase Price

•

$19.50 / share comprising $14.50 in cash and 0.257 shares of Kindred common stock

•

$1.8 billion total consideration, including assumption of net debt

Financial Profile

•

Pro Forma combined company revenues of approximately $7.1 billion and Operating Income or

EBITDAR

(1)

of $1.0 billion

•

Combination will enhance Kindred’s Revenue and Margin Growth Profile

Accretion

•

Immediately and significantly accretive to Kindred’s Earnings and Operating Cash Flows

(exclusive of transaction and integration costs)

Synergies

•

$70 million in expected cost synergies within two years with approximately $35 million

expected in first full year following the closing

(2)

•

Revenue synergies of more than $60 million expected over time

(approximately $20 –

$30 million expected in the first full year following the closing)

Financing

•

Fully committed financing from Citi and J.P. Morgan

•

Expect to use a combination of debt, equity and mandatory convertibles to maintain pro forma

Adjusted Debt to EBITDAR leverage

(3)

of approximately 5.5x at closing, assuming half of $70 million

run rate expected cost synergies

Expected Closing

•

Q1 2015

–

Already received Hart-Scott-Rodino clearance

16

Kindred to acquire Gentiva for $1.8 billion in a combination of cash and stock

(1)

EBITDAR, or operating income, is defined as earnings before interest, income taxes,

depreciation, amortization and rent. EBITDAR was computed by combining the mid point of

2014 guidance for Kindred as provided on November 5, 2014 (see enclosed reconciliation)

and 2014 current average analyst consensus estimates for Gentiva. In addition, pro forma EBITDAR includes full

run rate expected cost synergies of $70 million, and estimated annualized rent expense for

Gentiva of $41 million.

(2)

Excludes one-time integration costs. (3)

Pro forma Adjusted Debt to EBITDAR leverage was computed by dividing a numerator

comprised of estimated long-term debt at closing plus pro forma annual rent expense

multiplied by six, less unrestricted cash, by a denominator comprised of pro forma

EBITDAR.

|

17

Continued Confidence in 2014

Gentiva Performance

(1)

Per Gentiva November 5, 2014 earnings release, see reconciliation in

appendix. (2)

Based upon 2014 current average analyst consensus estimates.

Sustained Improvement in Financial and Operating Performance

Further Validates Our Acquisition Thesis

Q3 Reported

(1)

Confirmed 2014

Guidance

(1)

Consensus Estimates

(mean)

(2)

Revenue

$498.0 million

$1.96 -

2.00 billion

$1.99 billion

Adjusted EBITDA

$48.5 million

$183-195 million

$191 million |

Combined Company

Overview Confirmed Confidence in Gentiva Performance

Mid Point of 2014 Guidance/Consensus

($ in millions)

Kindred

(1)

Gentiva

(2)

Expected

Synergies

(3)

Pro Forma

Revenue

$5,100

$1,986

$7,086

EBITDAR

697

232

$70

999

EBITDAR Margin

13.7%

11.7%

14.1%

Rent

322

41

363

% of revenue

6.3%

2.1%

5.1%

EBITDA

375

191

70

636

EBITDA Margin

7.4%

9.6%

9.0%

(1)

Based upon the midpoint of earnings guidance for Kindred as of November 5, 2014.

(2)

Based upon 2014 current average analyst consensus estimates. Assumes annualized rent of $41

million. (3)

Estimated full run rate of cost synergies expected to be achieved within two years of

close. Excludes one-time transaction and integration costs. 18

Gentiva’s

announcement of

Q3 results and

confirmed EBITDA

guidance of

$183-195 million

further validates

our acquisition thesis

and diligence. |

Significant and

Immediate Accretion to Earnings and Cash Flows

19

Acquisition is significantly accretive at the contemplated transaction value and

financing structure on both an EPS and cash flow basis

(exclusive of transaction and integration costs)

(1)

Assumes pro forma share count of 85 million shares reflecting fully diluted shares at end of Q3

2014, share consideration as part of Gentiva transaction and the anticipated equity offering to finance the

transaction. Kindred expects the acquisition to be approximately

$0.40 to $0.60 accretive to pro forma earnings, on a run rate basis, once Gentiva is fully

integrated and expected synergies are fully realized in the second full year following

the closing. (2)

Based upon 2014 net income guidance for Kindred as provided on November 5, 2014 and 2014

current average analyst consensus estimates for Gentiva and adding back depreciation and amortization per

Kindred’s 2014 guidance and adding back depreciation and amortization based upon 2014

current average analyst consensus for Gentiva and annualized stock-based compensation and deferred financing cost

amortization for both Kindred and Gentiva. In addition, expected

full run rate estimated cost synergies, net of income taxes, of

$42 million ($70 million full run rate annual costs and operating synergies less

income taxes of $28 million) are included.

EPS Accretion

(1)

$0.40 –

$0.60

+

Acceleration of cost synergies

+

Increased revenue through clinical

integration

+

Incremental development activity fueled

by combined company cash flows

+

Enhanced managed care and ACO

opportunities from expanded integrated

national platform

Drivers for Potential Upside

Pro Forma Cash Flows ($ millions)

Operating Cash Flows

before dividends, changes

in working capital and

capital expenditures

(2)

$350 –

400

Less: Routine CapEx

$120 –

130

As adjusted

$230 –

270

Fully Integrated Run Rate |

Key

Highlights •

Expected to issue in aggregate ~$620 –

$720 million of equity to maintain

reasonable leverage

•

Expect to have shares outstanding of

~85 million at close

Financing Plan

20

Sources

($ millions)

New debt financing

$1,300 –

$1,400

New equity and mandatory

convertible securities issued

$200 –

$300

Equity issued to Gentiva

shareholders

~$200

Existing bank revolver draw

~$200

$2,000

Uses

($ millions)

Purchase Gentiva equity

$767

Retire Gentiva debt

~$1,050

Transaction fees & expenses

~$183

$2,000

Aggregate equity financing approximates

purchase price of Gentiva equity

–

Proactively raised $220 million in net

proceeds from June 2014 equity offering

–

Will issue Gentiva shareholders ~$200

million in Kindred stock as part of

purchase consideration

–

Plan to raise ~$200 – $300 million in

equity and / or mandatory convertible

securities between announcement and

close

|

Wrap-Up

21 |

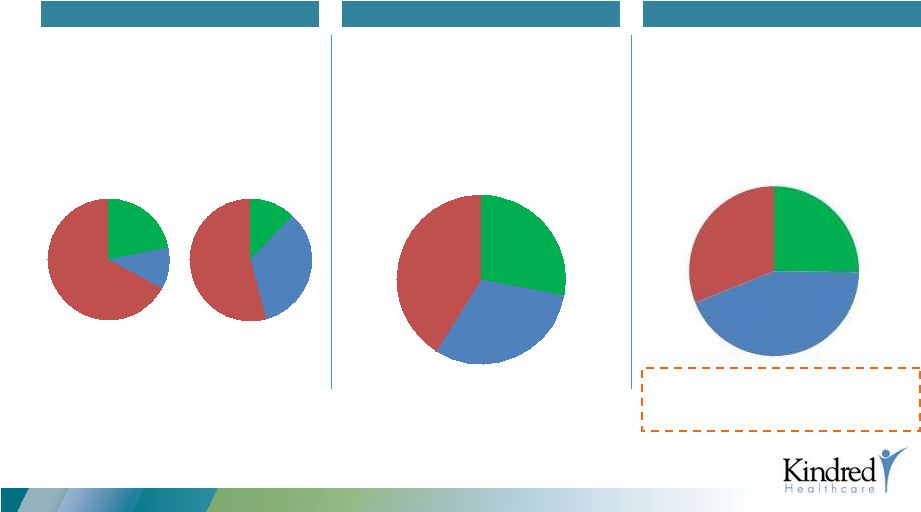

15%

Hospital

35%

Nursing

Rehab

18%

(1)

Kindred

revenues

before

intercompany

eliminations

as

reported

in

the

respective

Form

10-K.

(2)

Per Kindred 2014 guidance as provided on November 5, 2014 and 2014 current average analyst

consensus estimates for Gentiva. Kindred has Significantly Diversified its

Service Offerings & Transformed its Business Mix

•

Combination with Gentiva uniquely positions Kindred as one of the leading healthcare providers

in the U.S. across a broad spectrum of critical services

–

Fundamentally different company today that is at the forefront of a changing healthcare

delivery system –

Results in a suite of services better positioned to help patients and drive shareholder

value Yesterday

Today

Tomorrow

•

A focused operator of nursing facilities

and hospitals

–

Diversified post-acute service

offerings through acquisition of

RehabCare

•

Right-sized operational footprint, yielding

a focused approach across key integrated

care markets

–

Negotiation with Ventas to exit

certain assets and sold others

•

Acquisition of Gentiva results in a well-

balanced portfolio of integrated service

offerings

–

Addition of Gentiva accelerates

capabilities to provide population

health and take risk

2010

2012

Kindred at Home 0%

Kindred at Home 2%

LTM 9/30/2014

Kindred at Home 6%

Pro Forma Kindred

(2)

22

Kindred

at Home

32%

Nursing

21%

Hospital

48%

Rehab

25%

Nursing

45%

Hospital

33%

Rehab

20%

Nursing

47%

Hospital

42%

Rehab

11% |

(1)

Based upon current average analyst Consensus estimates for 2014 and 2015 for both Kindred and

Gentiva, including $60 million of annual run rate revenue synergies. (2)

Before certain disclosed items as reconciled in the appendix.

(3)

Based

upon

mid

point

of

2014

earnings

guidance

for

Kindred

as

of

November

5,

2014.

(4)

Based

upon

mid

point

of

2014

earnings

guidance

for

Kindred

as

of

November

5,

2014

and

based

upon

current

average

analyst

Consensus

estimates

for

Gentiva

(includes EBITDA impact of full run rate of $70 million of expected cost synergies).

Kindred has Successfully Shifted its Business to Faster

Growing Businesses, Improving Margins,

Profitability and Operating Cash Flows

Improves Margin and Profitability

Enhances Growth Profile

2014 –

2015 Revenue Growth

(1)

23

EBITDA Margin

(4)

(2)

(3)

3.9%

4.5%

0.0%

2.0%

4.0%

6.0%

Kindred

Kindred + Gentiva

6.1%

7.4%

9.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Kindred 2011

Kindred 2014

Kindred + Gentiva

PF 2014 |

(1)

Based

upon

mid

point

of

2014

earnings

guidance

for

Kindred

as

of

November

5,

2014.

(2)

Based upon mid point of 2014 current average analyst consensus estimates for Gentiva. Assumes

annualized rent of $41 million. (3)

Leases capitalized using 6x rent, equity represents market cap and funded debt calculated as of

December 31 for 2010 and 2012. (4)

Rent expense for the twelve months ended September 30, 2014 capitalized at 6x, funded debt and

closing share price at September 30, 2014, respectively. (5)

Pro forma values shown as of 12/31/2014 and include $1.6bn of additional debt and $363mm of

annual rent expense based upon mid point of 2014 earnings guidance for

Kindred

as

of

November

5,

2014

and

an

estimate

of

annualized

rent

expense

of

$41

million

for

Gentiva.

Pro

forma

value

based

on

fully

diluted

Kindred

shares

outstanding plus newly issued shares as part of the transaction at Kindred share price of

$21.24 on October 30, 2014. Kindred has Developed a Balanced

and Flexible Capital Structure

•

Increasing traditional debt while deleveraging lease exposure will continue to drive

long-term strategic flexibility and create shareholder value

–

Rent as a percent of revenue declines from 6.3%

(1)

for Kindred today to 5.2%

(1)(2)

Yesterday

(3)

Today

(4)

Tomorrow

(5)

•

RehabCare transaction materially

shifted Kindred’s capital structure,

financed by the issuance of traditional

financial debt

•

Recent negotiations with Ventas further

reduced capitalized leases by greater

than $600 million

•

Q1 refinancing added capacity,

improved terms and Financial Flexibility

•

Gentiva transaction continues to shift

Kindred’s capital structure towards

more traditional debt/equity mix

•

Strong deleveraging profile

Equity

22%

Debt

11%

Cap.

Leases

67%

Equity

12%

Debt

34%

Cap.

Leases

54%

~5.5x net adj leverage at close with goal

to delever below 5.0x over the next

two years

24

2010

2012

As of September 30, 2014

Pro Forma Kindred

Equity

27%

Debt

32%

Cap.

Leases

41%

Equity

25%

Debt

44%

Cap.

Leases

31% |

Kindred Has

Delivered Attractive Financial Performances

25

Operating Margin

(1)

:

12.7%

14.0%

13.6%

13.7%

Share Price & Dividends

($ millions)

Closing Share Price

Cumulative Dividends

Despite sequential years of significant

reimbursement cuts and a wholesale

restructuring of the Company’s business and

capital structure, the Company has delivered on

its promise to its patients, customers,

teammates and shareholders!

$4.2

$4.9

$4.8

$5.1

$7.1

2011

2012

2013

2014

2014 PF

Revenue

($ billions)

Operating Income

(1)

($ millions)

$11.77

$10.82

$19.74

$21.24

$0.24

$0.60

12/31/2011

12/31/2012

12/31/2013

10/30/2014

14.1%

(1)Before certain disclosed items as reconciled in the Appendix.

(2)Reimbursement cuts totaled $70 million.

(3)Reflects midpoint of Company’s November 5, 2014 earnings guidance.

(4)Assumes Gentiva was acquired on January 1, 2014, and amount for Gentiva is based upon

current analyst consensus estimates.

In

addition,

pro

forma

EBITDAR

includes

full

run

rate

expected

cost

synergies

of

$70

million,

and

estimated

annualized rent expense for Gentiva of $41 million.

(2)

(3)

(3)

(4)

(4)

Kindred and

Gentiva

Kindred and

Gentiva

$529

$679

$658

$697

$999

2011

2012

2013

2014

2014 PF |

Kindred Is

Helping to Shape the Future of American Healthcare

•

As the U.S. population ages, demand for patient-centered healthcare is growing

rapidly –

and Kindred is pioneering an integrated approach to address this

demand –

implementing a better model to improve clinical outcomes and patient

safety, smooth care transitions and lower costs

•

Kindred’s “Continue

The

Care”

strategy delivers the services that patients need

across the full spectrum of care, from transitional inpatient hospitalization,

to post-acute rehab and skilled nursing services, to home health and hospice care

•

Kindred is growing to implement this strategy and fostering innovation to provide

more patients, in more communities, with high quality, integrated, patient-

centered care in the lowest-cost setting

26

The merger of Kindred and Gentiva accelerates the development of

this integrated approach to

patient care, creating significant value for both companies’

patients,

employees and shareholders |

Q & A

27

*

*

* |

Appendix

28

*

*

*

*

*

*

*

*

*

*

* |

Explanation of

Non-GAAP Measures In addition to the results provided in accordance with GAAP,

Kindred Healthcare, Inc. (the "Company") has provided information in this presentation to

compute certain non-GAAP measurements for the three months ended September 30, 2014 and

2013, the twelve months ended September 30, 2014, December 31, 2013, 2012 and 2011

before certain charges or on a core basis and on a pro forma basis. A reconciliation of the non-GAAP measurements to

the GAAP measurements is included in this presentation.

The Company's earnings presentation also includes financial measures referred to as operating

income, or EBITDAR, and earnings before interest, income taxes, depreciation and

amortization ("EBITDA"). The Company's management uses EBITDAR or EBITDA as meaningful measures of operational performance

in addition to other measures. The Company uses EBITDAR or EBITDA to assess the relative

performance of its operating divisions as well as the employees that

operate

these

businesses.

In

addition,

the

Company

believes

these

measurements

are

important

because

securities

analysts

and

investors

use

these

measurements to compare the Company's performance to other companies in the healthcare

industry. The Company believes that income (loss) from continuing

operations

is

the

most

comparable

GAAP

measure.

Readers

of

the

Company's

financial

information

should

consider

income

(loss)

from

continuing operations as an important measure of the Company's financial performance because

it provides the most complete measure of its performance. EBITDAR or EBITDA should be

considered in addition to, not as a substitute for, or superior to, financial measures based upon GAAP as an

indicator of operating performance. A reconciliation of EBITDAR or EBITDA to income (loss)

from continuing operations provided is included in this presentation.

The

pro

forma

EBITDAR

total

of

$1.0

billion

included

in

this

presentation

includes

a

2014

EBITDAR

estimate

of

$232

million

for

Gentiva,

which

is based upon Gentiva's 2014 current average analyst consensus estimates. In addition, pro

forma EBITDAR includes full run rate expected cost synergies of $70 million from the

transaction. Also in this presentation, the Company provides the financial measure of

free cash flows excluding certain items. The Company recognizes that free cash

flows

excluding

certain

items

is

a

non-GAAP

measurement

and

is

not

intended

to

replace

the

presentation

of

the

Company’s

cash

flows

in

accordance

with

GAAP. The Company believes that this non-GAAP measurement provides important information

to investors related to the amount of discretionary cash flows that are available for

other investing and financing activities. In addition, management uses free cash flows excluding certain items in making

decisions related to acquisitions, development capital expenditures, dividends, long-term

debt repayments and other uses. The Company believes net cash flows provided by

operating activities is the most comparable GAAP measure. Readers of the Company’s financial information should consider net cash

flows provided by operating activities as an important measure of the Company’s financial

performance because it provides the most complete measure of its performance.

Free cash flows excluding certain items should be considered in addition to, not as a

substitute for, or superior to, financial measures based

upon

GAAP

as

an

indicator

of

operating

performance.

A

reconciliation

of

net

cash

flows

provided

by

operating

activities

to

free

cash

flows

excluding

certain items is included in this presentation.

29 |

Reconciliation

of Earnings Guidance (a)

Continuing Operations

($ Millions, except per chare amounts)

30

As of November 5, 2014

Low

High

Revenues

5,100

$

5,100

$

Operating income (EBITDAR)

692

$

702

$

Rent

322

322

EBITDA

370

380

Depreciation and amortization

157

157

Interest, net

92

92

Income from continuing operations before income taxes

121

131

Provision for income taxes

44

48

Income from continuing operations

77

83

Earnings attributable to noncontrolling interests

(18)

(18)

Income from continuing operations attributable to the Company

59

65

Allocation to participating unvested restricted stockholders

(2)

(2)

Available to common stockholders

57

$

63

$

Earnings per diluted share

0.98

$

1.08

$

Shares used in computing earnings per diluted share

58.3

58.3

As of November 5, 2014

Various non-cash expenses included in earnings guidance above:

Low

High

Amortization of stock-based compensation

13

$

13

$

Amortization of deferred financing fees

8

8

Straight-line rent expense

9

9

(a)

The earnings guidance excludes the effect of reimbursement changes, debt refinancing costs,

severance, retirement, retention and restructuring costs, customer bankruptcy costs,

litigation costs, transaction costs, any further acquisitions or divestitures, any

impairment charges, any further issuances of common stock, debt or mandatory

convertible equity securities in conjunction with the Gentiva transaction and any

repurchases of common stock. |

Reconciliation

of Non-GAAP Measures 31

($ Thousands)

Three months ended

September 30,

2014

2013

Detail of charges:

Severance, retirement and other restructuring costs

($1,686)

($1,894)

Customer bankruptcy

(1,857)

-

Facility closing costs

-

(6,043)

Litigation costs

-

(23,850)

Debt refinancing charges (other operating expenses)

-

(459)

Transaction costs

(4,114)

(613)

Debt refinancing charges (interest expense)

-

(96)

(7,657)

(32,955)

Income tax benefit

2,391

9,767

Charges net of income taxes

(5,266)

(23,188)

Allocation to participating unvested restricted stockholders

133

-

Available to common stockholders

($5,133)

($23,188)

Weighted average diluted shares outstanding

62,902

52,323

Diluted loss per common share related to charges

($0.08)

($0.44)

Reconciliation of operating income (EBITDAR) before charges:

Operating income (EBITDAR) before charges

$158,270

$148,245

Detail of charges excluded from core operating results:

Severance, retirement and other restructuring costs

(1,686)

(1,894)

Customer bankruptcy

(1,857)

-

Facility closing costs

-

(6,043)

Litigation costs

-

(23,850)

Debt refinancing charges (other operating expenses)

-

(459)

Transaction costs

(4,114)

(613)

(7,657)

(32,859)

Reported operating income (EBITDAR)

$150,613

$115,386

Reconciliation of income from continuing operations before charges:

Amounts attributable to Kindred stockholders:

Income from continuing operations before charges

$7,040

$6,585

Charges net of income taxes

(5,266)

(23,188)

Reported income (loss) from continuing operations

$1,774

($16,603)

Reconciliation of diluted income per common share from continuing operations

before charges:

Diluted income per common share before charges (a)

$0.11

$0.12

Charges net of income taxes

(0.08)

(0.44)

Other

-

0.01

Reported diluted income (loss) per common share from continuing operations

$0.03

($0.31)

Weighted average diluted shares used to compute income per common share

from continuing operations before charges

62,902

52,333

Pro forma diluted income per common share before charges

$0.10

Weighted average diluted shares used to compute pro forma income per

common share from continuing operations before charges (b)

61,954

Reconciliation of effective income tax rate before charges:

Effective income tax rate before charges

32.4%

30.5%

Impact of charges on effective income tax rate

1.0%

-1.3%

Reported effective income tax rate

33.4%

29.2%

(a)

(b)

For purposes of computing diluted earnings per common share before charges, income from

continuing operations before charges was reduced by $0.2 million for both the three

months ended September 30, 2014 and 2013, and $1.2 million and $1.4 million for the

nine months ended September 30, 2014 and 2013, respectively, for the allocation of

income to participating unvested restricted stockholders. Includes the incremental 9.7

million shares, on a weighted average basis, issued in connection with the Company's

equity offering completed in June 2014. |

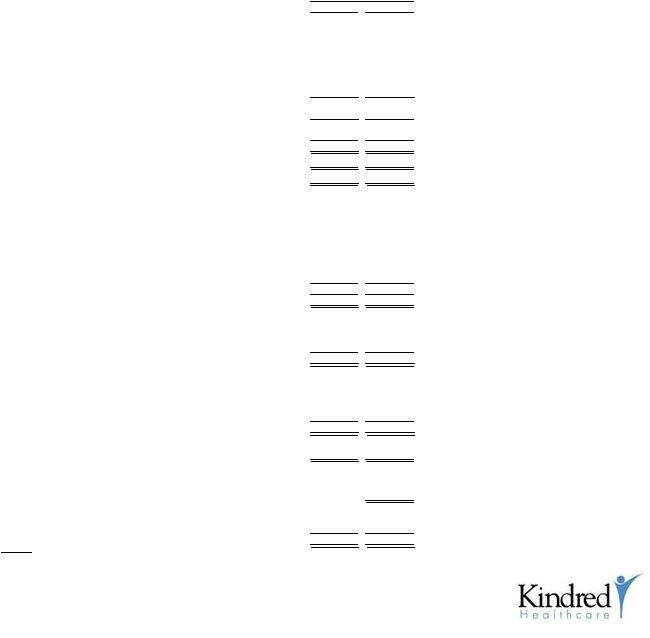

Reconciliation

of Non-GAAP Measures (continued) 32

($ Thousands)

Twelve

2013 Quarters

2014 Quarters

Months ended

First

Second

Third

Fourth

First

Second

Third

Sept. 30, 2014

Revenues:

Hospital division

657,814

$

606,604

$

594,154

$

606,988

$

646,458

$

632,156

$

609,452

$

2,495,054

$

Nursing center division

270,205

264,847

265,696

270,080

277,902

280,255

279,561

1,107,798

Rehabilitation division:

Skilled nursing rehabilitation services

258,750

249,647

245,330

243,280

254,255

253,989

247,042

998,566

Hospital rehabilitation services

74,523

69,777

68,296

74,017

73,964

75,324

74,808

298,113

333,273

319,424

313,626

317,297

328,219

329,313

321,850

1,296,679

Care management division

51,621

53,039

53,801

66,466

87,704

87,986

86,186

328,342

1,312,913

1,243,914

1,227,277

1,260,831

1,340,283

1,329,710

1,297,049

5,227,873

Eliminations:

Skilled nursing rehabilitation services

(28,657)

(28,660)

(28,151)

(28,157)

(29,646)

(30,031)

(30,788)

(118,622)

Hospital rehabilitation services

(23,609)

(23,223)

(22,520)

(22,123)

(23,233)

(22,855)

(22,172)

(90,383)

Nursing centers

(1,213)

(1,001)

(1,161)

(875)

(662)

(860)

(776)

(3,173)

(53,479)

(52,884)

(51,832)

(51,155)

(53,541)

(53,746)

(53,736)

(212,178)

1,259,434

$

1,191,030

$

1,175,445

$

1,209,676

$

1,286,742

$

1,275,964

$

1,243,313

$

5,015,695

$

Income (loss) from continuing operations:

Operating income (loss):

Hospital division

147,493

$

129,366

$

112,483

$

126,788

$

145,395

$

132,878

$

121,744

$

526,805

$

Nursing center division

29,145

36,018

31,505

35,585

38,471

36,880

36,179

147,115

Rehabilitation division:

Skilled nursing rehabilitation services

13,239

21,623

(7,209)

14,260

18,328

19,982

17,552

70,122

Hospital rehabilitation services

18,132

19,573

18,215

18,005

19,820

20,084

18,273

76,182

31,371

41,196

11,006

32,265

38,148

40,066

35,825

146,304

-

Care

management division 2,786

3,961

1,085

2,131

4,697

7,065

6,789

20,682

Corporate:

Overhead

(45,585)

(43,196)

(39,157)

(48,557)

(44,050)

(48,365)

(45,173)

(186,145)

Insurance subsidiary

(509)

(384)

(482)

(539)

(406)

(443)

(637)

(2,025)

(46,094)

(43,580)

(39,639)

(49,096)

(44,456)

(48,808)

(45,810)

(188,170)

Impairment charges

(187)

(438)

(441)

(76,127)

-

-

-

(76,127)

Transaction costs

(944)

(108)

(613)

(447)

(683)

(4,496)

(4,114)

(9,740)

Operating income (EBITDAR)

163,570

166,415

115,386

71,099

181,572

163,585

150,613

566,869

Rent

(76,519)

(77,324)

(76,762)

(80,921)

(81,048)

(80,209)

(80,192)

(322,370)

EBITDA

87,051

89,091

38,624

(9,822)

100,524

83,376

70,421

244,499

Depreciation and amortization

(41,598)

(38,554)

(36,507)

(37,547)

(39,337)

(39,442)

(39,023)

(155,349)

Interest, net

(28,074)

(27,600)

(24,389)

(23,900)

(25,616)

(78,081)

(22,173)

(149,770)

Income (loss) from continuing operations

before income taxes

17,379

22,937

(22,272)

(71,269)

35,571

(34,147)

9,225

(60,620)

Provision (benefit) for income taxes

6,505

9,208

(6,510)

(20,522)

13,585

(13,082)

3,079

(16,940)

10,874

$

13,729

$

(15,762)

$

(50,747)

$

21,986

$

(21,065)

$

6,146

$

(43,680)

$ |

33

($ Thousands)

Reconciliation of Non-GAAP Measures

(continued)

Three months ended September 30, 2014

Charges

Severance

Before

and other

Customer

Transaction

As

charges

restructuring

bankruptcy

costs

Total

reported

Income from continuing operations:

Operating income (loss):

Hospital division

122,361

$

(617)

$

-

$

-

$

(617)

$

121,744

$

Nursing center division

36,662

(483)

-

-

(483)

36,179

Rehabilitation division:

Skilled nursing rehabilitation services

17,390

162

-

-

162

17,552

Hospital rehabilitation services

20,130

-

(1,857)

-

(1,857)

18,273

37,520

162

(1,857)

-

(1,695)

35,825

Care management division

7,110

(321)

-

-

(321)

6,789

Corporate:

Overhead

(44,746)

(427)

-

-

(427)

(45,173)

Insurance subsidiary

(637)

-

-

-

-

(637)

(45,383)

(427)

-

-

(427)

(45,810)

Transaction costs

-

-

-

(4,114)

(4,114)

(4,114)

Operating income (EBITDAR)

158,270

(1,686)

(1,857)

(4,114)

(7,657)

150,613

Rent

(80,192)

-

-

-

-

(80,192)

EBITDA

78,078

(1,686)

(1,857)

(4,114)

(7,657)

70,421

Depreciation and amortization

(39,023)

-

-

-

-

(39,023)

Interest, net

(22,173)

-

-

-

-

(22,173)

Income from continuing operations

before income taxes

16,882

(1,686)

(1,857)

(4,114)

(7,657)

9,225

Provision for income taxes

5,470

(923)

(1,017)

(451)

(2,391)

3,079

11,412

$

(763)

$

(840)

$

(3,663)

$

(5,266)

$

6,146

$

|

34

Reconciliation of Non-GAAP Measures

(continued)

($ Thousands)

Three months ended September 30, 2013

Charges

Severance

Before

and

Facility

Debt

Transaction

As

charges

retirement

closing

Litigation

refinancing

costs

Total

reported

Income (loss) from continuing operations:

Operating income (loss):

Hospital division

118,710

$

-

$

(5,527)

$

(700)

$

-

$

-

$

(6,227)

$

112,483

$

Nursing center division

31,569

-

(64)

-

-

-

(64)

31,505

Rehabilitation division:

Skilled nursing rehabilitation services

15,941

-

-

(23,150)

-

-

(23,150)

(7,209)

Hospital rehabilitation services

18,503

(288)

-

-

-

-

(288)

18,215

34,444

(288)

-

(23,150)

-

-

(23,438)

11,006

Care management division

2,138

(601)

(452)

-

-

-

(1,053)

1,085

Corporate:

Overhead

(37,693)

(1,005)

-

-

(459)

-

(1,464)

(39,157)

Insurance subsidiary

(482)

-

-

-

-

-

-

(482)

(38,175)

(1,005)

-

-

(459)

-

(1,464)

(39,639)

Impairment charges

(441)

-

-

-

-

-

-

(441)

Transaction costs

-

-

-

-

-

(613)

(613)

(613)

Operating income (EBITDAR)

148,245

(1,894)

(6,043)

(23,850)

(459)

(613)

(32,859)

115,386

Rent

(76,762)

-

-

-

-

-

-

(76,762)

EBITDA

71,483

(1,894)

(6,043)

(23,850)

(459)

(613)

(32,859)

38,624

Depreciation and amortization

(36,507)

-

-

-

-

-

-

(36,507)

Interest, net

(24,293)

-

-

-

(96)

-

(96)

(24,389)

Income (loss) from continuing operations

before income taxes

10,683

(1,894)

(6,043)

(23,850)

(555)

(613)

(32,955)

(22,272)

Provision (benefit) for income taxes

3,257

(2,044)

(5,805)

(756)

(599)

(563)

(9,767)

(6,510)

7,426

$

150

$

(238)

$

(23,094)

$

44

$

(50)

$

(23,188)

$

(15,762)

$ |

Reconciliation

of Non-GAAP Measures (continued)

($ Thousands)

35

2013

2012

2011

Detail of charges:

One-time bonus

(19,842)

$

$ -

$ -

Severance, retirement and other restructuring costs

(12,558)

(8,730)

(18,259)

Litigation costs

(30,850)

(5,000)

-

Impairment charges

(76,082)

(107,899)

(73,554)

Transaction costs

(2,112)

(2,231)

(33,937)

Lease cancellation charges (rent expense)

-

(1,691)

(1,819)

Debt refinancing charges (interest expense)

(1,461)

-

(13,802)

(142,905)

(125,551)

(141,371)

Income tax benefit

43,893

12,795

34,427

Charges net of income taxes

(99,012)

(112,756)

(106,944)

Allocation to participating unvested restricted stockholders

-

-

-

Available to common stockholders

($99,012)

($112,756)

($106,944)

Reconciliation of EBITDAR before charges:

Operating income (EBITDAR) before charges

$657,914

$679,488

$528,902

Rent

311,526

303,564

276,540

EBITDA

346,388

375,924

252,362

Detail of charges excluded from core operating results:

One-time bonus

(19,842)

-

-

Severance, retirement and other restructuring costs

(12,558)

(8,730)

(18,259)

Litigation costs

(30,850)

(5,000)

-

Impairment charges

(76,082)

(107,899)

(73,554)

Transaction costs

(2,112)

(2,231)

(33,937)

(141,444)

(123,860)

(125,750)

Reported operating income (EBITDAR)

$516,470

$555,628

$403,152

Reconciliation of income from continuing operations before charges:

Amounts attributable to Kindred stockholders:

Income from continuing operations before charges

$53,216

$65,891

$40,482

Charges net of income taxes

(99,012)

(112,756)

(106,944)

Reported loss from continuing operations

($45,796)

($46,865)

($66,462) |

Three months

ended September 30,

2014

2013

Reconciliation of net cash flows provided by operating

activities to free cash flows:

Net cash flows provided by operating activities

$90,039

$110,750

Adjustments to remove certain payments (including payments

made for discontinued operations) included in net cash flows

provided by operating activities:

Capitalized lender fees related to debt refinancing

-

4,589

Severance, retirement and retention

1,271

1,181

Transaction costs

4,565

6,362

5,836

12,132

Benefit of reduced income tax payments resulting from

certain payments

(1,269)

(3,013)

4,567

9,119

Net cash flows provided by operating activities excluding certain items

94,606

119,869

Less:

Routine capital expenditures

(21,263)

(23,152)

Development capital expenditures

(1,570)

(3,235)

(22,833)

(26,387)

Free cash flows excluding certain items

$71,773

$93,482

Reconciliation of Non-GAAP Measures

(continued)

($ Thousands)

36 |

Gentiva

Non-GAAP Disclosure (1)

37

Third quarter

2014

Adjusted EBITDA

$48.5

Cost savings initiatives and acquisition and integration activities

(0.5)

Impact of closed locations

(0.3)

Impact of merger related expenses

(1.6)

EBITDA

46.1

Depreciation and Amortization

(7.3)

Interest Expense and Other, net

(24.7)

(Loss)/Income Before Income Taxes

14.1

Income Tax Benefit / (Expense)

(5.6)

Equity in net loss of CareCentrix

(0.5)

Net (Loss)/Income

8.0

Less: Net Income Attributable to Noncontrolling

Interests -

Net (Loss) / Income Attributable to Gentiva Shareholders

$8.0

A reconciliation of Adjusted EBITDA and adjusted net income attributable to Gentiva

shareholders to net income, the most directly comparable GAAP measure, is not accessible

on a forward-looking basis without unreasonable effort due to inherent

difficulities in predicting the charges for cost savings initiatives and acquisition

and integration activities, the results of discontinued operations and the impact of

any future acquisitions or divestitures, which can fluctuate significantly and may

have a significant impact on net income.

(1) Per Gentiva November 5, 2014 earnings release.

($ Millions)

(1) |

Kindred

Healthcare Third Quarter Investor Update

November 6, 2014 |