Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - Midway Gold Corp | mdw-20140930ex3128b1fe8.htm |

| EX-95 - EX-95 - Midway Gold Corp | mdw-20140930xex95.htm |

| EX-31.1 - EX-31.1 - Midway Gold Corp | mdw-20140930ex311902ed4.htm |

| EX-32 - EX-32 - Midway Gold Corp | mdw-20140930xex32.htm |

| EXCEL - IDEA: XBRL DOCUMENT - Midway Gold Corp | Financial_Report.xls |

UNITED STATES SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

||

|

For the quarterly period ended September 30, 2014 |

||

|

OR |

||

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

||

For the transition period from to

Commission file number: 001-33894

MIDWAY GOLD CORP.

(Exact name of registrant as specified in its charter)

|

British Columbia |

98-0459178 |

|

|

(State of other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

|

|

Suite 280 – 8310 South Valley Highway |

||

|

Englewood, Colorado |

80112 |

|

|

(Address of principal executive offices) |

(Zip Code) |

(720) 979-0900

(Registrant’s Telephone Number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer” and “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

Large accelerated filer ☐ Accelerated filer ☒ Non-accelerated filer ☐ Smaller Reporting Company ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) ☐ Yes ☒ No

Number of Common Shares outstanding at November 3, 2014: 174,919,068

TABLE OF CONTENTS

|

PART I – FINANCIAL INFORMATION |

4 | |

|

Item 1. |

Financial Statements |

4 |

|

Item 2. |

Management's Discussion and Analysis of Financial Condition and Results of Operations |

26 |

|

Item 3. |

Quantitative and Qualitative Disclosures about Market Risk. |

40 |

|

Item 4. |

Controls and Procedures |

40 |

|

PART II - OTHER INFORMATION |

41 | |

|

Item 1. |

Legal Proceedings |

41 |

|

Item 1A. |

Risk Factors |

41 |

|

Item 2. |

Unregistered Sale of Equity Securities and Use of Proceeds. |

42 |

|

Item 3. |

Defaults Upon Senior Securities |

42 |

|

Item 4. |

Mine Safety Disclosures |

42 |

|

Item 5. |

Other Information |

42 |

|

Item 6. |

Exhibits |

43 |

|

SIGNATURES |

44 | |

2

EXPLANATORY NOTE

All amounts in this interim report on Form 10-Q are expressed in Canadian dollars, unless otherwise indicated.

3

PART I – FINANCIAL INFORMATION

MIDWAY GOLD CORP.

CONSOLIDATED INTERIM BALANCE SHEETS

(Expressed in Canadian dollars, except shares) (unaudited)

|

September 30, |

December 31, |

|||||

|

2014 |

2013 |

|||||

|

Assets |

||||||

|

Current Assets: |

||||||

|

Cash and Cash Equivalents |

$ |

22,978,965 |

$ |

51,363,302 | ||

|

Amounts Receivable |

44,411 | 102,897 | ||||

|

Inventories (Note 3) |

486,238 |

- |

||||

|

Prepaid Expenses and Other Current Assets (Note 4) |

2,274,519 | 431,023 | ||||

|

Total Current Assets |

25,784,133 | 51,897,222 | ||||

|

Long Term Assets: |

||||||

|

Reclamation Deposits (Note 7) |

4,193,952 | 1,595,400 | ||||

|

Property, Equipment and Mine Development (Note 5) |

63,766,278 | 16,750,950 | ||||

|

Mineral Properties (Note 6) |

57,762,195 | 53,200,288 | ||||

|

Other Long Term Assets (Note 4) |

4,248,069 | 405,162 | ||||

|

Total Assets |

$ |

155,754,627 |

$ |

123,849,022 | ||

|

Liabilities and Stockholders’ Equity |

||||||

|

Current Liabilities: |

||||||

|

Accounts Payable and Accrued Liabilities (Note 15) |

$ |

8,343,044 |

$ |

2,879,730 | ||

|

Preferred Share Dividends Payable |

1,591,537 | 1,515,845 | ||||

|

Other Short Term Liabilities |

963,270 | 1,440,926 | ||||

|

Total Current Liabilities |

10,897,851 | 5,836,501 | ||||

|

Long Term Liabilities: |

||||||

|

Derivative Liability (Note 11) |

- |

8,189,720 | ||||

|

Asset Retirement Obligations (Note 7) |

3,532,475 | 51,967 | ||||

|

Other Long Term Liabilities |

305,805 | 121,689 | ||||

|

Total Liabilities |

14,736,131 | 14,199,877 | ||||

|

Redeemable Preferred Shares (Note 11) |

||||||

|

Series A Preferred Shares - Unlimited, No Par Value; |

||||||

|

Issued and Outstanding – 37,837,838 (2014 and 2013); |

||||||

|

Redemption Price - US$1.85 per share |

50,738,937 | 47,482,972 | ||||

|

Stockholders’ Equity (Note 10): |

||||||

|

Common stock authorized – unlimited, no par value; Issued and outstanding – 173,761,914 and 130,915,872 at September 30, 2014 and December 31, 2013, respectively |

174,934,487 | 140,834,370 | ||||

|

Additional Paid In Capital |

3,210,029 | 3,195,325 | ||||

|

Accumulated Other Comprehensive Income (Loss) (Note 13) |

9,220,156 | 2,126,923 | ||||

|

Accumulated Deficit |

(97,085,113) | (83,990,445) | ||||

|

Total Stockholders' Equity |

90,279,559 | 62,166,173 | ||||

|

Total Liabilities and Stockholders' Equity |

$ |

155,754,627 |

$ |

123,849,022 | ||

Commitments (Notes 7 and 14)

Subsequent Events (Notes 8 and 11)

The accompanying notes are an integral part of these unaudited consolidated interim financial statements.

4

MIDWAY GOLD CORP.

CONSOLIDATED INTERIM STATEMENTS OF OPERATIONS

(Expressed in Canadian dollars, except share and per share amounts) (unaudited)

|

Three Months Ended September 30, 2014 |

Three Months Ended September 30, 2013 |

Nine Months Ended September 30, 2014 |

Nine Months Ended September 30, 2013 |

|||||||||

|

Depreciation and Accretion |

$ |

242,907 |

$ |

140,960 |

$ |

583,104 |

$ |

382,215 | ||||

|

Write-down of Inventories |

266,054 |

- |

266,054 |

- |

||||||||

|

Mineral Exploration Expenditures (Schedule) |

1,202,264 | 1,605,830 | 2,525,784 | 4,185,765 | ||||||||

|

General & Administrative: |

||||||||||||

|

Consulting |

183,872 | 68,053 | 242,239 | 370,743 | ||||||||

|

Interest and Bank Charges |

1,124 | 825 | 2,944 | 2,186 | ||||||||

|

Investor Relations |

15,875 | 11,003 | 70,719 | 22,360 | ||||||||

|

Legal, Audit and Accounting |

249,088 | 396,032 | 832,890 | 3,094,750 | ||||||||

|

Office and Administration |

696,268 | 300,772 | 2,094,335 | 931,433 | ||||||||

|

Salaries and Benefits |

1,574,158 | 1,163,197 | 4,665,241 | 3,801,241 | ||||||||

|

Transfer Agent and Filing Fees |

45,856 | 208,721 | 177,363 | 342,146 | ||||||||

|

Travel |

70,031 | 69,178 | 247,575 | 250,391 | ||||||||

|

Operating Loss |

4,547,497 | 3,964,571 | 11,708,248 | 13,383,230 | ||||||||

|

Other Income (Expense): |

||||||||||||

|

Foreign Exchange Gain (Loss) |

(25,462) | (1,259,322) | (29,731) | 2,262,994 | ||||||||

|

Gain on Change in Fair Value of Derivative Liabilities (Note 11) |

- |

988,443 |

- |

15,574,007 | ||||||||

|

Interest and Investment Income |

4,861 | 40,397 | 28,660 | 128,188 | ||||||||

|

Loss on Sale of Equipment |

- |

(2,681) |

- |

(2,681) | ||||||||

|

Investment Write Down |

- |

(43,125) |

- |

(43,125) | ||||||||

|

Other Income (Expense) |

(35,957) | (15,590) | (175,237) | (24,393) | ||||||||

| (56,558) | (291,878) | (176,308) | 17,894,990 | |||||||||

|

Net Loss (Income) Before Income Tax |

4,604,055 | 4,256,449 | 11,884,556 | (4,511,760) | ||||||||

|

Income Tax Recovery (Expense) |

(477,245) | 272,628 | (1,210,112) | 2,179,077 | ||||||||

|

Net Loss (Income) |

$ |

5,081,300 |

$ |

3,983,821 |

$ |

13,094,668 |

$ |

(6,690,837) | ||||

|

Preferred Share Cumulative Dividend (Note 11) |

1,591,536 | 1,478,516 | 4,627,716 | 4,367,633 | ||||||||

|

Accretion of Redeemable Preferred Shares (Note 11) |

1,143,144 | 949,370 | 3,255,965 | 2,697,943 | ||||||||

|

Net Loss Attributable to Common Shareholders |

$ |

7,815,980 |

$ |

6,411,707 |

$ |

20,978,349 |

$ |

374,739 | ||||

|

Net Loss Per Share (Note 9) |

||||||||||||

|

Basic: |

||||||||||||

|

Weighted Average Number of Shares Outstanding |

172,870,093 | 129,605,544 | 150,039,147 | 128,840,275 | ||||||||

|

Net Loss Per Share |

$ |

0.05 |

$ |

0.05 |

$ |

0.14 |

$ |

- |

||||

|

Diluted: |

||||||||||||

|

Weighted Average Number of Shares Outstanding |

172,870,093 | 129,605,544 | 150,039,147 | 166,678,113 | ||||||||

|

Net Loss Per Share |

$ |

0.05 |

$ |

0.05 |

$ |

0.14 |

$ |

0.04 | ||||

The accompanying notes are an integral part of these unaudited consolidated interim financial statements.

5

MIDWAY GOLD CORP.

Consolidated INTERIM StatementS of COMPREHENSIVE (Income) Loss

(Expressed in Canadian dollars) (unaudited)

|

Three Months Ended September 30, 2014 |

Three Months Ended September 30, 2013 |

Nine Months Ended September 30, 2014 |

Nine Months Ended September 30, 2013 |

|||||||||

|

Net Loss (Income) for the Period |

$ |

5,081,300 |

$ |

3,983,821 |

$ |

13,094,668 |

$ |

(6,690,837) | ||||

|

Other Comprehensive Loss (Income) |

||||||||||||

|

Unrealized Loss (Gain) on Investment |

- |

7,500 | 13,750 | |||||||||

|

Transfer of Realized Loss to Statement of Operations |

- |

(43,125) |

- |

(43,125) | ||||||||

|

Currency Translation Adjustment |

(6,791,616) | 1,180,729 | (7,093,233) | (677,747) | ||||||||

|

Other Comprehensive Loss (Income) |

(6,791,616) | 1,145,104 | (7,093,233) | (707,122) | ||||||||

|

Comprehensive Loss (Income) |

$ |

(1,710,316) |

$ |

5,128,925 |

$ |

6,001,435 |

$ |

(7,397,959) | ||||

The accompanying notes are an integral part of these unaudited consolidated interim financial statements.

6

MIDWAY GOLD CORP.

CONSOLIDATED INTERIM STATEMENTS OF CASH FLOWS

(Expressed in Canadian dollars) (unaudited)

|

Nine Months Ended September 30, 2014 |

Nine Months Ended September 30, 2013 |

||||

|

Cash Provided By (Used In): |

|||||

|

Operating Activities: |

|||||

|

Net Income (Loss) |

$ |

(13,094,668) |

$ |

6,690,837 | |

|

Items Not Involving Cash: |

|||||

|

Depreciation |

476,839 | 380,540 | |||

|

Accretion |

106,265 | 1,675 | |||

|

Stock-Based Compensation |

647,206 | 993,953 | |||

|

Unrealized Foreign Exchange Loss |

- |

64,711 | |||

|

Inventory Write Down |

266,054 |

- |

|||

|

Investment Write Down |

- |

43,125 | |||

|

Gain on Change in Fair Value of Derivative Liabilities |

- |

(15,574,007) | |||

|

Lease Abandonment and Amortization of Deferred Rent |

160,689 |

- |

|||

|

Deferred Income Tax Recovery |

- |

(3,237,223) | |||

|

Loss on Sale of Equipment |

- |

2,681 | |||

|

Change in Non-Cash Working Capital Items: |

|||||

|

Amounts Receivable |

133,984 | (42,002) | |||

|

Inventories |

(735,769) |

- |

|||

|

Prepaid Expenses and Other Current Assets |

(172,942) | (204,024) | |||

|

Accounts Payable and Accrued Liabilities |

(1,907,450) | 448,988 | |||

|

Other Short Term Liabilities |

(448,967) | 1,080,184 | |||

|

Total Operating Activities |

(14,568,759) | (9,350,562) | |||

|

Investing Activities: |

|||||

|

Mineral Property Acquisitions |

(715,403) | (1,482,858) | |||

|

Proceeds from Insurance |

1,638,150 | ||||

|

Additions to Property, Equipment and Mine Development |

(39,703,879) | (4,874,255) | |||

|

Reclamation Deposit |

(2,438,754) | 871,203 | |||

|

Total Investing Activities |

(41,219,886) | (5,485,910) | |||

|

Financing Activities: |

|||||

|

Common Stock Issued, Net of Issue Costs |

29,358,563 |

- |

|||

|

Preferred Share Dividends Paid |

(699,359) | (1,925,655) | |||

|

Deferred Financing Costs |

(3,700,236) | (52,515) | |||

|

Total Financing Activities |

24,958,968 | (1,978,170) | |||

|

Effect of Exchange Rate Changes On Cash: |

2,445,340 | 135,208 | |||

|

Decrease in Cash and Cash Equivalents |

(28,384,337) | (16,679,434) | |||

|

Cash and Cash Equivalents, Beginning of Period |

51,363,302 | 75,052,836 | |||

|

Cash and Cash Equivalents, End of Period |

$ |

22,978,965 |

$ |

58,373,402 | |

Supplemental Disclosures with Respect to Cash Flows (Note 16)

The accompanying notes are an integral part of these unaudited consolidated interim financial statements.

7

MIDWAY GOLD CORP.

CONSOLIDATED INTERIM STATEMENT OF STOCKHOLDERS’ EQUITY - CONTINUED

(Expressed in Canadian dollars) (unaudited)

|

Convertible Preferred Shares |

Stockholder’s Equity (Deficit) |

||||||||||||||||||||

|

Number of Preferred Shares |

Preferred Shares |

Number of Common Shares |

Common Stock |

Additional Paid-in Capital |

Accumulated Other Comprehensive Loss |

Accumulated Deficit |

Total Stockholders’ Equity |

||||||||||||||

|

Balance, December 31, 2012 |

37,837,838 |

$ |

44,261,122 | 128,451,298 |

$ |

138,304,344 |

$ |

11,418,155 |

$ |

(436,344) |

$ |

(92,896,376) |

$ |

56,389,779 | |||||||

|

Shares Issued: |

|||||||||||||||||||||

|

Exercise of Stock Options |

- |

- |

37,500 | 34,125 | (13,125) |

- |

- |

21,000 | |||||||||||||

|

Shares Issued For Dividends |

- |

- |

2,427,074 | 2,495,901 |

- |

- |

- |

2,495,901 | |||||||||||||

|

Share Issue Costs |

- |

(314) |

- |

- |

- |

- |

- |

- |

|||||||||||||

|

Stock-Based Compensation |

- |

- |

- |

- |

1,174,509 |

- |

- |

1,174,509 | |||||||||||||

|

Accretion of Cost of Redeemable Preferred Shares |

- |

3,500,736 |

- |

- |

(3,500,736) |

- |

- |

(3,500,736) | |||||||||||||

|

Preferred Shares Dividends Payable |

- |

(278,572) |

- |

- |

(5,883,478) |

- |

- |

(5,883,478) | |||||||||||||

|

Unrealized Loss on Investment |

- |

- |

- |

- |

- |

(13,750) |

- |

(13,750) | |||||||||||||

|

Write-off of Investment |

- |

- |

- |

- |

- |

43,125 | 43,125 | ||||||||||||||

|

Unrealized Foreign Exchange Gain |

- |

- |

- |

- |

- |

2,533,892 |

- |

2,533,892 | |||||||||||||

|

Net Income (Loss) |

- |

- |

- |

- |

- |

- |

8,905,931 | 8,905,931 | |||||||||||||

|

Balance, December 31, 2013 |

37,837,838 | 47,482,972 | 130,915,872 | 140,834,370 | 3,195,325 | 2,126,923 | (83,990,445) | 62,166,173 | |||||||||||||

|

Shares Issued: |

|||||||||||||||||||||

|

Public Offerings and Consent Fee |

- |

- |

36,949,243 | 27,853,910 |

- |

- |

- |

27,853,910 | |||||||||||||

|

Exercise of Stock Options |

- |

- |

1,967,500 | 2,393,542 | (938,541) |

- |

- |

1,455,001 | |||||||||||||

|

Shares Issued For Dividends |

- |

- |

3,929,299 | 3,852,665 |

- |

- |

- |

3,852,665 | |||||||||||||

|

Stock-Based Compensation |

- |

- |

- |

- |

647,206 |

- |

- |

647,206 | |||||||||||||

|

Accretion of Cost of Redeemable Preferred Shares |

- |

3,255,965 |

- |

- |

(3,255,965) |

- |

- |

(3,255,965) | |||||||||||||

|

Preferred Shares Dividends Payable |

- |

- |

- |

- |

(4,627,716) |

- |

- |

(4,627,716) | |||||||||||||

|

Reclassification of Derivative Liability |

- |

- |

- |

- |

8,189,720 |

- |

- |

8,189,720 | |||||||||||||

|

Unrealized Foreign Exchange Gain |

- |

- |

- |

- |

- |

7,093,233 |

- |

7,093,233 | |||||||||||||

|

Net Income (Loss) |

- |

- |

- |

- |

- |

- |

(13,094,668) | (13,094,668) | |||||||||||||

|

Balance, September 30, 2014 |

37,837,838 |

$ |

50,738,937 | 173,761,914 |

$ |

174,934,487 |

$ |

3,210,029 |

$ |

9,220,156 |

$ |

(97,085,113) |

$ |

90,279,559 | |||||||

The accompanying notes are an integral part of these unaudited consolidated interim financial statements.

8

MIDWAY GOLD CORP.

SCHEDULE OF MINERAL EXPLORATION EXPENDITURES

(Expressed in Canadian dollars) (unaudited)

|

Three Months Ended September 30, 2014 |

Three Months Ended September 30, 2013 |

Nine Months Ended September 30, 2014 |

Nine Months Ended September 30, 2013 |

|||||||||

|

Exploration costs incurred are summarized as follows: |

||||||||||||

|

Pan Project |

||||||||||||

|

Assays and Analysis |

$ |

33,252 |

$ |

1,358 |

$ |

33,252 |

$ |

1,358 | ||||

|

Engineering and Consulting |

1,462 | 31,427 | 1,462 | 65,781 | ||||||||

|

Environmental |

886 |

- |

886 | 32 | ||||||||

|

Field Office and Supplies |

1,098 | 126,622 | 2,814 | 208,812 | ||||||||

|

Legal and Accounting |

908 |

- |

908 | 6,076 | ||||||||

|

Property Maintenance and Taxes |

- |

- |

- |

1,200 | ||||||||

|

Reclamation Costs |

48 | (4,946) | 52 | 1,896 | ||||||||

|

Reproduction and Drafting |

- |

4,102 | 11 | 6,084 | ||||||||

|

Salaries and Labor |

47,959 | 378,504 | 50,472 | 999,378 | ||||||||

|

Travel, Transportation and Accommodation |

448 | 41,242 | 2,495 | 142,076 | ||||||||

| 86,061 | 578,309 | 92,352 | 1,432,693 | |||||||||

|

Gold Rock Project |

||||||||||||

|

Assays and Analysis |

- |

7,150 |

- |

124,361 | ||||||||

|

Drilling |

- |

- |

- |

413,109 | ||||||||

|

Engineering and Consulting |

96,956 | 33,036 | 138,292 | 181,366 | ||||||||

|

Environmental |

235,430 | 338,790 | 821,211 | 581,367 | ||||||||

|

Field Office and Supplies |

19,334 | 17,980 | 67,884 | 196,731 | ||||||||

|

Legal and Accounting |

15,349 | 114 | 19,665 | 16,111 | ||||||||

|

Property Maintenance and Taxes |

178,317 | 167,589 | 179,440 | 236,411 | ||||||||

|

Reclamation Costs |

355 | 84 | 562 | 6,600 | ||||||||

|

Reproduction and Drafting |

- |

704 | 2,174 | 2,381 | ||||||||

|

Salaries and Labor |

59,622 | 48,542 | 330,886 | 469,222 | ||||||||

|

Travel, Transportation and Accommodation |

2,543 | 15,280 | 18,886 | 66,935 | ||||||||

| 607,906 | 629,269 | 1,579,000 | 2,294,594 | |||||||||

|

Spring Valley Project |

||||||||||||

|

Engineering and Consulting |

11,924 |

- |

104,628 | (205) | ||||||||

|

Field Office and Supplies |

754 |

- |

15,017 | 160 | ||||||||

|

Legal and Accounting |

2,767 |

- |

21,215 | 3,627 | ||||||||

|

Property Maintenance and Taxes |

9,784 |

- |

9,784 |

- |

||||||||

|

Reclamation Costs |

18 |

- |

28 | 12 | ||||||||

|

Reproduction and Drafting |

- |

- |

1,536 | 4 | ||||||||

|

Salaries and Labor |

3,680 |

- |

54,257 | 1,195 | ||||||||

|

Travel, Transportation and Accommodation |

94 |

- |

8,191 | 121 | ||||||||

| 29,021 |

- |

214,656 | 4,914 | |||||||||

|

Tonopah Project |

||||||||||||

|

Engineering and Consulting |

- |

- |

- |

2,335 | ||||||||

|

Environmental |

- |

1,498 |

- |

2,271 | ||||||||

|

Field Office and Supplies |

2,398 | 931 | 3,390 | 1,166 | ||||||||

|

Legal and Accounting |

- |

- |

- |

30 | ||||||||

|

Property Maintenance and Taxes |

78,927 | 69,533 | 79,496 | 70,055 | ||||||||

|

Reclamation Costs |

56 | 10 | 58 | 281 | ||||||||

|

Reproduction and Drafting |

- |

- |

95 | 6 | ||||||||

|

Salaries and Labor |

10,284 | 6,074 | 23,087 | 7,575 | ||||||||

|

Travel, Transportation and Accommodation |

298 | 896 | 830 | 1,093 | ||||||||

| 91,963 | 78,942 | 106,956 | 84,812 | |||||||||

|

Sub-Total Balance Carried Forward |

$ |

814,951 |

$ |

1,286,520 |

$ |

1,992,964 |

$ |

3,817,013 | ||||

The accompanying notes are an integral part of these unaudited consolidated interim financial statements.

9

MIDWAY GOLD CORP.

SCHEDULE OF MINERAL EXPLORATION EXPENDITURES - CONTINUED

(Expressed in Canadian dollars) (unaudited)

|

Three Months Ended September 30, 2014 |

Three Months Ended September 30, 2013 |

Nine Months Ended September 30, 2014 |

Nine Months Ended September 30, 2013 |

|||||||||

|

Sub-Total Balance Brought Forward |

$ |

814,951 |

$ |

1,286,520 |

$ |

1,992,964 |

$ |

3,817,013 | ||||

|

Golden Eagle Project |

||||||||||||

|

Engineering and Consulting |

- |

- |

- |

3,212 | ||||||||

|

Field Office and Supplies |

17 | 6 | 1,193 | 500 | ||||||||

|

Legal and Accounting |

- |

- |

- |

66 | ||||||||

|

Property Maintenance and Taxes |

579 | 473 | 7,963 | 3,653 | ||||||||

|

Reproduction and Drafting |

- |

- |

134 | |||||||||

|

Salaries and Labor |

40 | 40 | 4,307 | 2,947 | ||||||||

|

Travel, Transportation and Accommodation |

2 | 6 | 687 | 240 | ||||||||

| 638 | 525 | 14,284 | 10,618 | |||||||||

|

Pinyon Project |

||||||||||||

|

Engineering and Consulting |

- |

- |

- |

273 | ||||||||

|

Field Office and Supplies |

2,258 | 907 | 2,566 | 4,384 | ||||||||

|

Legal and Accounting |

- |

- |

- |

480 | ||||||||

|

Property Maintenance and Taxes |

78,580 | 69,190 | 78,580 | 124,306 | ||||||||

|

Reclamation Costs |

53 | 10 | 53 | 36 | ||||||||

|

Reproduction and Drafting |

- |

- |

35 | 101 | ||||||||

|

Salaries and Labor |

5,376 | 5,920 | 8,428 | 26,968 | ||||||||

|

Travel, Transportation and Accommodation |

280 | 874 | 459 | 2,567 | ||||||||

| 86,547 | 76,901 | 90,121 | 159,115 | |||||||||

|

Property Investigations |

||||||||||||

|

Assays and Analysis |

- |

1,550 | 656 | 1,550 | ||||||||

|

Engineering and Consulting |

- |

258 | 29,226 | 11,229 | ||||||||

|

Field Office and Supplies |

7,831 |

- |

17,283 | 487 | ||||||||

|

Legal and Accounting |

- |

- |

- |

297 | ||||||||

|

Property Maintenance and Taxes |

272,501 | 240,076 | 273,629 | 185,012 | ||||||||

|

Reclamation Costs |

183 |

- |

193 |

- |

||||||||

|

Reproduction and Drafting |

- |

- |

982 |

- |

||||||||

|

Salaries and Labor |

18,642 |

- |

100,210 | 17 | ||||||||

|

Travel, Transportation and Accommodation |

971 |

- |

6,236 | 427 | ||||||||

| 300,128 | 241,884 | 428,415 | 199,019 | |||||||||

|

Total Mineral Exploration Expenditures |

$ |

1,202,264 |

$ |

1,605,830 |

$ |

2,525,784 |

$ |

4,185,765 | ||||

The accompanying notes are an integral part of these unaudited consolidated interim financial statements.

10

1. Nature and Continuance of Operations

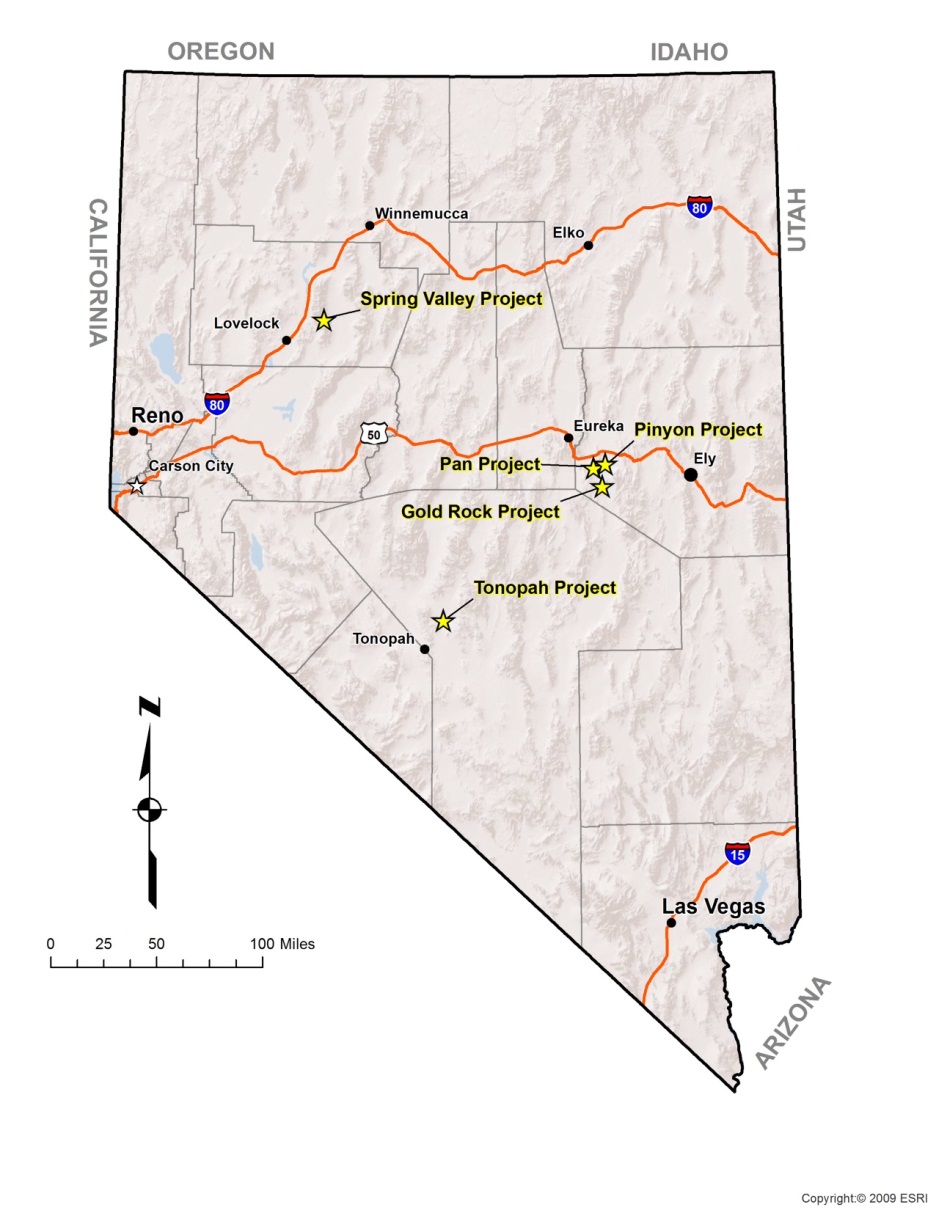

Midway Gold Corp. (the “Company”) was incorporated on May 14, 1996 under the laws of the Province of British Columbia and its principal business activities are the acquisition, exploration and development of mineral properties.

The Company has not generated any revenues from operations. These unaudited consolidated interim financial statements have been prepared on a going concern basis which assumes the Company will be able to realize its assets and discharge its liabilities in the normal course of business in the foreseeable future. The Company has incurred operating losses for the three and nine months ended September 30, 2014 of $4,547,497 and $11,708,248, respectively. Further operating losses are anticipated in the development of its business. Since inception of May 14, 1996 to September 30, 2014 the Company’s accumulated deficit totals $97,085,113. The Company’s cash on hand and working capital at September 30, 2014 is $22,978,965 and $14,886,282, respectively. The Company also has established an aggregate U.S.$55,000,000 senior secured credit facility consisting of a U.S.$45,000,000 project financing facility and a U.S.$10,000,000 cost overrun facility to fund development and construction of the Pan Project (Note 8).

Recoverability of amounts capitalized for the Company’s mineral properties, other than the Pan and Spring Valley Projects, are dependent upon the Company’s ability to raise funds or generate profits to enable funds to be available to complete exploration on the mineral properties, identify economically recoverable reserves and develop the mineral properties into profitable projects, or the receipt of adequate proceeds from the sale of such projects.

Recoverability of amounts capitalized for the Pan Project is dependent on the Company’s ability to draw on the Company’s debt facility, successfully complete construction and operate it profitably, or the receipt of adequate proceeds from any sale of the project. The Spring Valley project is subject to a joint venture agreement with Barrick Gold Exploration Inc., who is responsible for carrying the Company to production by funding and arranging financing for the Company’s share of cost of operations and mine exploration, development and construction expenses. The Company is responsible for funding costs incurred subsequent to commercial production. Barrick is also responsible for arranging financing for the Company’s share of the cost of operations and mine exploration, development and construction expenses.

2. Significant Accounting Policies

The consolidated interim financial statements included herein have been prepared by the Company, without audit, in accordance with the rules and regulations of the United States Securities and Exchange Commission (“SEC”) pursuant to Rule 10-01 of Regulation S-X. Certain information and footnote disclosures normally included in financial statements prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) have been condensed or omitted pursuant to such SEC rules and regulations, although the Company believes that the disclosures included are adequate to make the information presented not misleading. Certain reclassifications have been made to prior period financial statements to conform to the current period presentation.

In management’s opinion, the unaudited consolidated interim financial statements contained herein reflect all adjustments, consisting solely of normal recurring items, which are necessary for the fair presentation of our financial position, results of operations, and cash flows on a basis consistent with that of our prior audited consolidated financial statements, except as described below. The results of operations for interim periods may not be indicative of results to be expected for the full fiscal year. The Company’s 2013 Annual Report on Form 10-K includes a summary of significant accounting policies and should be read in conjunction with this Form 10-Q.

Inventories

As of September 30, 2014, inventories include ore on leach pads and materials and supplies. Ore on leach pad is carried at the lower of cost or net realizable value. Cost includes mining costs (ore and waste) including mine site overhead and depreciation and amortization. Net realizable value is computed using expected metal prices reduced for any further estimated processing, refining, and selling costs.

Materials and supplies are valued at the lower of weighted average cost or net realizable value. Cost includes applicable taxes and freight.

11

Foreign Currency Translation

Effective January 1, 2014, the functional currency of the Company’s Canadian operations changed from the Canadian dollar to the United States dollar (“U.S. dollar”) based upon significant changes in economic facts and circumstances, which included the receipt of the Record of Decision for the Pan Project in December 2013, the commencement of construction at the Pan Project in 2014, and recent and anticipated financings in U.S. dollars. These changes in economic facts and circumstances have resulted in the U.S. dollar being the currency of the primary economic environment in which the entity operates. The change in the functional currency of the Company’s Canadian operations has been applied prospectively with differences attributable to current-rate translation of non-monetary assets and liabilities at the date of change being reported through other comprehensive income. The reporting currency remains the Canadian dollar, and all amounts herein are expressed in Canadian dollars unless otherwise noted.

The financial statements of the Company’s operations are translated from their functional currency, the United States dollar, to the reporting currency, the Canadian dollar, using the current rate method. Assets and liabilities are translated using the current rate in effect at the balance sheet date and revenues and expenses are translated at the average rate for the period. Adjustments resulting from the translation, if any, are included in accumulated other comprehensive income (loss) in stockholders’ equity.

Recently Issued Accounting Pronouncements

In May 2014, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2014-09, “Revenue from Contracts with Customers (Topic 606)”. The amendments in ASU 2014-09 affects any entity that either enters into contracts with customers to transfer goods or services or enters into contracts for the transfer of nonfinancial assets unless those contracts are within the scope of other standards (e.g., insurance contracts or lease contracts). This ASU will supersede the revenue recognition requirements in Topic 605, Revenue Recognition, and most industry-specific guidance, and creates a Topic 606 Revenue from Contracts with Customers. The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The amendments are effective for annual reporting periods beginning after December 15, 2016, including interim periods within that reporting period. Early application is not permitted. The Company does not currently have revenue contracts with customers, but it will begin assessing the impact of such contracts as appropriate.

Recently Adopted Accounting Pronouncements

In June 2014, the FASB issued ASU 2014-10, “Development Stage Entities (Topic 915)”. The amendments in ASU 2014-10 remove all incremental financial reporting requirements from U.S. GAAP for development stage entities, including the removal of Topic 915, Development Stage Entities, from the FASB Accounting Standards Codification. In addition, the ASU: (a) adds an example disclosure in Topic 275, Risks and Uncertainties, to illustrate one way that an entity that has not begun planned principal operations could provide information about the risks and uncertainties related to the company’s current activities; and (b) removes an exception provided to development stage entities in Topic 810, Consolidation, for determining whether an entity is a variable interest entity. As allowed by ASU 2014-10, the Company has early adopted ASU 2014-10 and impacts of its adoption have been reflected throughout the Company’s consolidated financial statements, with the significant effect being the elimination of disclosures of certain cumulative amounts incurred during the period from inception to the period end reporting date.

In July 2013, the FASB issued ASU No. 2013-11, Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists. The guidance requires an entity to present an unrecognized tax benefit, or a portion of an unrecognized tax benefit, in the financial statements as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss or tax credit carryforward, unless such tax loss or credit carryforward is not available at the reporting date under the tax law of the applicable jurisdiction to settle any additional income taxes resulting from the disallowance of a tax position. In the event that the tax position is disallowed or the tax law of the applicable jurisdiction does not require the entity to use, and the entity does not intend to use, the deferred tax asset for such purpose, the unrecognized tax benefit shall be presented in the financial statements as a liability and shall not be combined with deferred tax assets. The guidance is effective for annual reporting periods beginning after December 15, 2013, and interim periods within those annual periods, and is to be applied prospectively. The adoption of this standard did not have a material impact on the Company’s consolidated financial statements.

12

In March 2013, the FASB issued ASU 2013-05, “Parent's Accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity”, an amendment to FASB Accounting Standards Codification ("ASC") Topic 830, “Foreign Currency Matters” ("FASB ASC Topic 830"). The update clarifies that complete or substantially complete liquidation of a foreign entity is required to release the cumulative translation adjustment ("CTA") for transactions occurring within a foreign entity. However, transactions impacting investments in a foreign entity may result in a full or partial release of CTA even though complete or substantially complete liquidation of the foreign entity has not occurred. Furthermore, for transactions involving step acquisitions, the CTA associated with the previous equity-method investment will be fully released when control is obtained and consolidation occurs. This ASU is effective for fiscal years beginning after December 15, 2013. The adoption of this standard did not have a material impact on the Company’s consolidated financial statements.

In February 2013, the FASB issued ASU 2013-04, “Obligations Resulting From Joint and Several Liability Arrangements for Which the Total Amount of the Obligation is Fixed at the Reporting Date, an amendment to FASB ASC Topic 405, Liabilities” ("FASB ASC Topic 405"). The update requires an entity to measure obligations resulting from joint and several liability arrangements for which the total amount of the obligation is fixed as of the reporting date as the sum of the obligation the entity agreed to pay among its co-obligors and any additional amount the entity expects to pay on behalf of its co-obligors. This ASU is effective for annual and interim periods beginning after December 15, 2013 and is required to be applied retrospectively to all prior periods presented for those obligations that existed upon adoption of the ASU. The adoption of this standard did not have a material impact on the Company’s consolidated financial statements.

3. Inventories

The following table provides the components of inventories:

|

September 30, 2014 |

December 31, 2013 |

|||||

|

Materials and Supplies |

$ |

70,278 |

$ |

- |

||

|

Ore on Leach Pads |

415,960 |

- |

||||

|

$ |

486,238 |

$ |

- |

|||

The Company began placing ore on the leach pad during the three months ended September 30, 2014. The period-end market value of the Company’s production-related inventories is determined in part by using expected realizable gold prices and is highly sensitive to this input. The Company had a write-down of Ore on Leach Pads inventory of $266,054 during the three and nine months ended September 30, 2014. A decline in metal price levels and/or an increase in production costs per ounce of gold could result in, or contribute to, a future write-down of production-related inventories.

4. Prepaids and Other Assets

At September 30, 2014 and December 31, 2013, prepaids and other assets consisted of the following:

|

September 30, 2014 |

December 31, 2013 |

|||||

|

Prepaid Expenses and Other Current Assets |

||||||

|

Insurance Proceeds Receivable |

$ |

1,654,212 |

$ |

- |

||

|

Prepaid Expenses |

583,297 | 396,903 | ||||

|

Deposits |

37,010 | 34,120 | ||||

|

$ |

2,274,519 |

$ |

431,023 | |||

|

Other Long Term Assets |

||||||

|

Deferred Financing Costs |

$ |

4,138,031 |

$ |

299,902 | ||

|

Deposits |

110,038 | 105,260 | ||||

|

$ |

4,248,069 |

$ |

405,162 | |||

13

5. Property, Equipment and Mine Development

At September 30, 2014 and December 31, 2013, property, equipment and mine development consisted of the following:

|

September 30, |

December 31, |

|||||

|

2014 |

2013 |

|||||

|

Land |

$ |

617,047 |

$ |

585,974 | ||

|

Buildings and Leasehold Improvements |

802,059 | 761,670 | ||||

|

Computer Equipment and Software |

1,911,325 | 1,403,123 | ||||

|

Trucks and Autos |

445,404 | 422,975 | ||||

|

Office Equipment |

281,483 | 248,370 | ||||

|

Field Equipment |

1,033,910 | 287,447 | ||||

|

Mine Development |

60,727,734 | 14,511,873 | ||||

|

Subtotal |

65,818,962 | 18,221,432 | ||||

|

Accumulated Depreciation |

(2,052,684) | (1,470,482) | ||||

|

Totals |

$ |

63,766,278 |

$ |

16,750,950 | ||

Depreciation expense for the three and nine months ended September 30, 2014 was $181,519 and $476,839, respectively, compared to depreciation expense for the three and nine months ended September 30, 2013 of $140,323 and $380,540, respectively.

During the three months ended September 30, 2014 severe thunderstorms damaged portions of Mine Development assets at the Company’s Pan project resulting in a $3,334,212 write-down of Mine Development costs. Repairs of all damage has been completed as of September 30, 2014, with an estimated total cost of $3,853,001 to complete the repair work. Insurance proceeds of $1,638,150 were received during the three months ended September 30, 2014 and additional proceeds of $1,654,212 was receivable as of September 30, 2014 of which $1,125,900 was received subsequent to September 30, 2014 (Note 4). No net gain or loss resulted from the write down of the Mine Development costs and the recognition of insurance proceeds. Further proceeds that maybe received will be recognized upon final settlement of the insurance claim.

6. Mineral Properties

Details on the Company’s mineral properties are found in Note 7 to the audited consolidated financial statements for the year ended December 31, 2013.

|

September 30, |

December 31, |

|||||

|

Mineral Property |

2014 |

2013 |

||||

|

Pan |

$ |

37,990,656 |

$ |

35,831,787 | ||

|

Gold Rock |

2,315,823 | 1,885,212 | ||||

|

Spring Valley |

5,487,292 | 5,168,424 | ||||

|

Tonopah |

9,411,232 | 7,959,646 | ||||

|

Golden Eagle |

2,433,200 | 2,310,671 | ||||

|

Pinyon |

123,992 | 44,548 | ||||

|

Totals |

$ |

57,762,195 |

$ |

53,200,288 |

|

(a) |

Pan property, Nevada |

The Company acquired a mineral lease agreement for a 100% interest in certain of the Pan property claims which requires the Company to pay advance minimum royalties on an annual basis. The minimum advance royalties will be creditable against a sliding scale Net Smelter Returns (“NSR”) production royalty of between 2.5% and 4%. The Company must incur a minimum of U.S.$65,000 per year for work expenditures, including claim maintenance fees, during the term of the mining lease. On January 2, 2014, the Company paid advanced royalties of $245,768 (U.S.$231,072).

The Company also owns 100% of certain adjoining claims acquired by staking.

14

|

(b) |

Gold Rock property, Nevada |

Through a series of four royalty agreements and one assignment, the Company acquired claims that currently comprise the Gold Rock property. The royalty agreements are subject to sliding scale royalties on NSR ranging between 2% and 6% based upon gold price and advanced minimum royalty payments recoverable from commercial production. During the nine months ended September 30, 2014, the Company has paid $315,105 (U.S.$295,217) in advanced minimum royalty payments.

|

(c) |

Spring Valley property, Nevada |

The Company signed an exploration and option to joint venture agreement with Barrick Gold Exploration Inc. (“Barrick”), a wholly owned subsidiary of Barrick Gold Corporation, effective March 9, 2009, granting Barrick the exclusive right to explore, develop and earn an interest in the Spring Valley property. Barrick has completed the expenditure requirement of U.S.$38.0 million to earn a 70% interest in the Spring Valley property. The Company has elected to allow Barrick to earn an additional 5% interest (75% total) by carrying the Company to production and arranging financing for the Company’s share of the cost of operations and mine exploration, development and construction expenses. The cost that Barrick incurs from carrying the Company to production will be recouped by Barrick, plus interest, once commercial production has been established.

The Company exercised its option to enter into a joint venture with Barrick as of February 23, 2014. With the formation of the joint venture agreement with Barrick, initial capital accounts were established by terms of the joint venture agreement, and Barrick is the manager of the joint venture.

|

(d) |

Tonopah property, Nye County, Nevada |

Through a series of agreements, amendments and payments the Company acquired a 100% interest in the Tonopah property. The acquisition is subject to a sliding scale royalty on NSR between 2% and 7% from any commercial production, based on changes in gold prices and an advance minimum royalty, recoverable from commercial production, of U.S.$300,000 per year payable on each August 15th. The Company entered into an agreement allowing payment of only U.S.$50,000 of the U.S.$300,000 payment due on August 15, 2014. The remaining U.S.$250,000, along with the August 15, 2015 U.S.$300,000 payment, will be paid subsequent to economic completion of the Pan project (Note 8). The Company is contractually obligated for both payments and has accrued these unpaid amounts in accrued liabilities.

|

(e) |

Golden Eagle property, Washington |

The Company purchased a 75% interest in the Golden Eagle, Washington project from Kinross Gold USA Inc. (“Kinross”) in August 2008, at a cost of $1,537,950 (U.S.$1,500,000) and purchased a 25% interest in the Golden Eagle project from Hecla Limited at a cost of $500,200 (U.S.$483,333). Kinross retained a 2% NSR royalty and was granted a first right of refusal to toll mill ore from the Golden Eagle property at their Kettle River Mill.

|

(f) |

Pinyon property, Nevada |

The Company entered into an earn-in agreement with Aurion Resources (“Aurion”) in November 2012 for claims. The Company can earn up to a 70% interest in the Pinyon property. The Company can also earn an additional 5% (75% total) by arranging mine financing. As of September 30, 2014 the Company has a spent a total of $377,466.

7. Reclamation and Remediation

The Company is required to post bonds with the Bureau of Land Management (“BLM”) for reclamation of planned mineral exploration and development programs associated with the Company’s mineral properties located in the United States. For the Spring Valley property, Barrick is responsible for bonding for the surface disturbance created by the exploration and development programs in which they are funding.

At September 30, 2014 and December 31, 2013 the Company had purchased surety contracts for reclamation bonds covering the Company’s exploration projects in the amount of U.S.$846,491. The surety contracts were renewed in May 2014 and are in place through May of 2015, at which point the Company can elect to renew the surety contracts or deposit the full cash amount of the reclamation bonds with the BLM.

15

As a part of the permitting process for the Pan Project, the Company is required to have a reclamation bond of approximately U.S.$15,300,000 held with the BLM. The Company purchased a surety contract for the reclamation bond, which amount requires the Company to deposit U.S.$3,700,000 into an escrow account as security for abandonment and remediation obligations, which has been recorded in reclamation deposits on the Consolidated Balance Sheet. The surety contract names the Company and several of its subsidiaries as indemnitors to the surety agreement. The holder of the surety contract may require, at its sole discretion that the Company make additional deposits to the escrow account of up to the U.S.$15,300,000 reclamation bond amount. The Company is required to maintain the escrow account until all abandonment and remediation obligations have been completed to the satisfaction of the BLM. Over the life of the Pan Project, prior to the completion of all abandonment and remediation obligations, the Company has the right to request a refund of a portion or all of the Pan Project reclamation deposit. Granting of the request is at the surety contract holder’s sole discretion.

At September 30, 2014 and December 31, 2013, $3,542,236 and $61,236, respectively, were accrued for reclamation obligations relating to the Company’s properties. A reconciliation of the Company’s asset retirement obligations for the nine months ended September 30, 2014 is as follows:

|

Balance as of December 31, 2013 |

$ |

61,236 |

|

Additions, Changes in Estimates and Other |

3,372,424 | |

|

Liabilities Settled |

- |

|

|

Accretion of Liability |

108,576 | |

|

Balance as of September 30, 2014 |

$ |

3,542,236 |

|

Less: Current Asset Retirement Obligations |

9,761 | |

|

Long-Term Asset Retirement Obligations |

$ |

3,532,475 |

Additions, changes in estimates and other during the nine months ended September 30, 2014 were related to construction of the Pan mine, which began in January 2014. Construction on several areas of the Pan mine plan are completed or are nearing completion as of September 30, 2014. The Company estimates that of the reclamation obligations as of September 30, 2014, approximately 94% of its total reclamation expenditures will occur during the years 2028 – 2039.

The current portion of reclamation and remediation liabilities of $9,761 and $9,269 at September 30, 2014 and December 31, 2013, respectively, are included in Accounts Payable and Accrued Liabilities on the accompanying consolidated interim balance sheets.

8. Debt

On July 18, 2014, the Company entered into a U.S.$55 million three-year senior secured project finance facility (the “Loan Facility”) with Commonwealth Bank of Australia (“CBA”) which will be used to fund continued development and construction of the Pan Project. The Loan Facility is comprised of two tranches: a project finance facility of U.S.$45 million, plus a cost overrun facility of U.S.$10 million. Advances under the project finance facility will bear interest at LIBOR plus 3.75% until economic completion, as defined in the Loan Facility agreement, and LIBOR plus 3.50% thereafter. Advances under the cost overrun facility will bear interest at the project finance facility rate plus 2.00%.

The Loan Facility will be secured by substantially all of the assets of the borrower (MDW Pan LLP, a wholly-owned subsidiary of the Company, and the owner of the Pan Project and related assets) and all other entities of the consolidated group. Upon achieving economic completion and meeting certain other requirements, security will be limited to the assets of MDW Pan LLP and guarantees from the Company and an affiliate. Pursuant to the Loan Facility, the Company’s ability to receive distributions from MDW Pan LLP for corporate general and administrative expenses, and other non-Pan expenditures is contingent upon satisfying certain conditions precedent and achieving various economic completion tests relating to, but not limited to, mine production, recoveries, sales, costs and sustainability over a three-month period. Economic completion must be achieved by September 30, 2015.

The Company’s ability to draw on the Loan Facility is contingent upon customary conditions precedent, including, but not limited to, funding any expected cost overruns on the Pan Project and establishment of an un-margined hedging program through CBA. The Company satisfied the gold hedging requirements on October 7, 2014 by entering into commitments to deliver to CBA, at a flat forward price of $1,200 per ounce, 80,500 ounces of gold over a 23-month period commencing in May 2015.

As of September 30, 2014, the Company has not drawn against the Loan Facility. The Loan Facility was amended on October 3, 2014, which provided for quarterly loan repayment terms to begin in June 2015 through the maturity date of March 31, 2017.

16

9. Net Loss (Income) Per Share

Basic loss (income) per common share is computed using the weighted-average number of common shares outstanding during the period. Diluted loss (income) per common share is calculated using the weighted-average number of common shares outstanding for the period and includes the dilutive effect of preferred shares, stock options and warrants.

The two-class method is used to calculate basic and diluted loss (income) per common share since preferred shares are a participating security under ASC 260 Earnings Per Share. The two-class method is an earnings allocation formula that determines income per share for each class of common stock and participating security according to dividends declared (or accumulated) and participation rights in undistributed earnings. Under the two-class method, basic loss (income) per common share is computed by dividing net loss (income) attributable to common shareholders after allocation of income to participating securities by the weighted-average number of common shares outstanding during the year. Diluted loss (income) per common share is computed using the more dilutive of the two-class method or the if-converted method. In periods of net loss, no effect is given to participating securities since they do not contractually participate in the losses of the Company.

Basic and diluted (income) loss per share for the three and nine months ended September 30, 2014 and 2013 are calculated as follows:

|

Three Months Ended |

Nine Months Ended |

|||||||||||

|

September 30, |

September 30, |

|||||||||||

|

2014 |

2013 |

2014 |

2013 |

|||||||||

|

Basic Loss (Income) Per Share: |

||||||||||||

|

Numerator: |

||||||||||||

|

Net Loss (Income) Attributable to Common Shareholders |

$ |

7,815,980 |

$ |

6,411,707 |

$ |

20,978,349 |

$ |

374,739 | ||||

|

Denominator: |

||||||||||||

|

Weighted-Average Common Shares For Basic Loss (Income) Per Share |

172,870,093 | 129,605,544 | 150,039,147 | 128,840,275 | ||||||||

|

Basic Loss (Income) Per Share |

$ |

0.05 |

$ |

0.05 |

$ |

0.14 |

$ |

- |

||||

|

Diluted Loss Per Share: |

||||||||||||

|

Numerator: |

||||||||||||

|

Net (Income) Loss Attributable to Common Shareholders |

$ |

7,815,980 |

$ |

6,411,707 |

$ |

20,978,349 |

$ |

374,739 | ||||

|

Effect of Gain on Change in Fair Value of Derivative Preferred Liability |

- |

- |

- |

14,427,439 | ||||||||

|

Effect of Accretion of Redeemable Preferred Shares |

- |

- |

- |

(2,697,943) | ||||||||

|

Effect of Preferred Shares Dividend |

- |

- |

- |

(4,367,633) | ||||||||

|

Effect of Canadian Corporate Dividend Tax |

- |

- |

- |

(1,061,992) | ||||||||

|

Diluted Loss |

$ |

7,815,980 |

$ |

6,411,707 |

$ |

20,978,349 |

$ |

6,674,610 | ||||

|

Denominator: |

||||||||||||

|

Weighted-Average Common Shares for Basic (Income) Loss Per Share |

172,870,093 | 129,605,544 | 150,039,147 | 128,840,275 | ||||||||

|

Effect of Dilutive Securities: |

||||||||||||

|

Preferred Series A shares |

- |

- |

- |

37,837,838 | ||||||||

|

Stock Options |

- |

- |

- |

- |

||||||||

|

Dilutive Potential Common Shares |

- |

- |

- |

37,837,838 | ||||||||

|

Total Shares |

172,870,093 | 129,605,544 | 150,039,147 | 166,678,113 | ||||||||

|

Diluted Loss Per Share |

$ |

0.05 |

$ |

0.05 |

$ |

0.14 |

$ |

0.04 | ||||

For the three and nine months ended September 30, 2014, 37,837,838 preferred shares that could be converted to shares of common stock were not included in the computation of diluted loss per common share, as the effect of doing so would have been anti-dilutive.

For the three and nine months ended September 30, 2014 and 2013, the effects of the assumed exercise of stock options of 3,598,161 and 4,134,167 shares of common stock, respectively, were excluded from the calculation of diluted net income per share as the effect would be anti-dilutive.

17

10. Share Capital

(a) The Company is authorized to issue an unlimited number of common shares and preferred shares.

(b) Share issuances

|

(i) |

On January 2, 2014, the Company issued 1,485,728 common shares in the amount of $1,284,431 for the payment of the Q4 2013 quarterly dividend on the Series A Preferred Shares (Note 11). |

|

(ii) |

On April 1, 2014, the Company issued 1,121,046 common shares in the amount of $1,298,573 for the payment of the Q1 2014 quarterly dividend on the Series A Preferred Shares (Note 11). |

|

(iii) |

On June 6, 2014, the Company issued 30,121,000 common shares upon the close of a “bought deal” public offering for U.S.$0.83 per share (the “June 6, 2014 Offering”). Gross proceeds of the June 6, 2014 Offering were $27,340,470 (U.S.$25,000,430). The Company incurred $2,053,544 (U.S.$1,889,020) in share issuance costs. Additionally, the Company issued 3,434,474 common shares in the amount of $3,117,431 (U.S.$2,850,613) for payment of the Series A Preferred Shareholders’ consent to issue shares in the June 6, 2014 Offering. |

|

(iv) |

On June 17, 2014, the Company issued 3,012,100 common shares as an over-allotment to the June 6, 2014 Offering for U.S.$0.83 per share. Gross proceeds of the over-allotment were $2,713,047 (U.S.$2,500,043). The Company incurred $146,063 (U.S.$134,595) in issuance costs. Additionally, the Company issued 381,669 common shares in the amount of $343,775 (U.S.$316,785) for payment of the Series A Preferred Shareholders’ consent to issue shares for the over-allotment of the June 6, 2014 Offering. |

|

(v) |

On July 2, 2014, the Company issued 1,322,525 common shares in the amount of $1,269,661 for the payment of the Q2 2014 quarterly dividend on the Series A Preferred Shares (Note 11). |

|

(vi) |

During the nine months ended September 30, 2014, the Company issued 1,967,500 common shares pursuant to the exercise of employee stock options. Proceeds received on the options exercised totalled $1,455,001. |

(c) Stock options

On June 20, 2013, the Company adopted the 2013 Stock and Incentive Plan (the “2013 Plan”) after approval of the 2013 Plan by the Company’s Shareholders at the Annual General and Special Meeting. The 2013 Plan is designed to replace the 2008 Stock Option Plan (the “Plan”); however, all outstanding option grants as of June 20, 2013 remain under the 2008 Stock Option Plan. Upon adoption of the 2013 Plan, the 2008 Stock Option Plan ceased to be available for the granting of new stock options.

The 2013 Plan permits a fixed aggregate number of common shares to be issuable under all awards under the 2013 Plan of 16,628,914 (“Award Cap”), which was equivalent to 10% of the Company’s common shares plus Series A Preferred Shares as of April 18, 2013. The total number of common shares issuable to insiders at any time and issued to insiders of the Company within any one-year period pursuant to stock options granted under the 2013 Plan, together with any other security based compensation arrangements of the Company, may not exceed 10% of the issued and outstanding common shares and preferred shares. The number of common shares issuable for Awards made under the 2008 Stock Option Plan is deducted from the Award Cap. The Award Cap represents the maximum number of shares issuable under both plans.

The exercise price of a stock option granted under the 2013 Plan will be determined by the Compensation Committee at the time the option is granted, but the exercise price may not be less than 100% of the fair market value of the Company’s common shares on the date of grant of such option. The fair market value is the closing price of one common share on the trading day of the date of grant on the NYSE MKT. Stock options granted under the 2013 Plan are subject to the following restrictions: (i) a promissory note is not permitted as payment for a stock option; (ii) the maximum term for stock options is 10 years from the date of grant; and (iii) unless otherwise fixed, stock options expire three months after the person to which they have been granted is terminated (12 months if due to death) or when options expire during a trading restriction, expiry is extended to the third trading day after a period during which trading in the common shares was prohibited or restricted pursuant to the policies of the Company.

The fair value of each option award is estimated on the date of grant using the Black-Scholes option pricing model. The option pricing model requires the input of subjective assumptions which are based on several different criteria. Expected volatility is based on the historical price volatility of the Company’s common stock. Expected dividend yield is assumed to be nil, as the Company has not paid dividends since inception on common shares. Expected forfeitures are calculated based upon historical experience of options. The expected life is estimated based on historical experience for options granted. Risk free interest rates are based on U.S. government obligations with a term approximating the expected life of the option.

18

The stock-based compensation for options vesting during the three and nine months ended September 30, 2014 and 2013 is included in the consolidated statement of operations as follows:

|

Three Months Ended |

Nine Months Ended |

|||||||||||

|

September 30, |

September 30, |

|||||||||||

|

2014 |

2013 |

2014 |

2013 |

|||||||||

|

Salaries and Benefits |

$ |

217,736 |

$ |

184,360 |

$ |

564,601 |

$ |

787,979 | ||||

|

Mineral Exploration Expenditures |

1,653 | 40,420 | 28,204 | 142,381 | ||||||||

|

Mine Development |

3,561 |

- |

18,594 |

- |

||||||||

|

Consulting |

5,435 | 17,484 | 35,807 | 63,593 | ||||||||

|

Total |

$ |

228,385 |

$ |

242,264 |

$ |

647,206 |

$ |

993,953 | ||||

2008 Stock Option Plan – TSX Stock Exchange

The estimated unrecognized compensation cost from unvested options as of September 30, 2014 was approximately $61,169, which is expected to be recognized over the remaining vesting period of 0.44 years, and has a weighted average remaining contractual term of 3.45 years.

The weighted-average grant date fair value of unvested options is summarized below for the nine months ended September 30, 2014 and 2013.

|

September 30, 2014 |

September 30, 2013 |

|||||

|

Unvested Beginning of Year |

$ |

0.55 |

$ |

2.12 | ||

|

Granted |

- |

0.55 | ||||

|

Vested |

0.55 | 0.63 | ||||

|

Expired |

(1.19) | (1.01) | ||||

|

Unvested End of Period |

$ |

0.55 |

$ |

0.82 | ||

The following table summarizes activity for compensatory stock options during the nine months ended September 30, 2014:

|

Number of Shares |

Weighted Average Exercise Price |

Aggregate Intrinsic Value |

Number of Shares Exercisable |

|||||||

|

Outstanding, January 1, 2014 |

9,645,834 |

$ |

1.27 |

$ |

632,800 | 8,122,490 | ||||

|

Granted |

- |

- |

- |

748,336 | ||||||

|

Exercised |

(1,967,500) | 0.74 |

- |

(1,967,500) | ||||||

|

Expired |

(1,440,001) | 1.64 |

- |

(1,193,331) | ||||||

|

Outstanding, September 30, 2014 |

6,238,333 |

$ |

1.36 |

$ |

979,825 | 5,709,995 | ||||

The following table summarizes information about outstanding compensatory stock options as of September 30, 2014:

|

Options Outstanding |

Options Exercisable |

||||||||||||||

|

Exercise Prices |

Number of Shares |

Remaining Contractual Life (years) |

Weighted Average Exercise Price |

Number Exercisable |

Weighted Average Exercise Price |

Aggregate Intrinsic Value |

|||||||||

|

$0.58 - $1.00 |

2,159,167 | 0.9 |

$ |

0.73 | 2,159,167 |

$ |

0.73 |

$ |

957,292 | ||||||

|

$1.01 - $1.60 |

1,721,666 | 3.4 | 1.16 | 1,193,328 | 1.17 | 22,533 | |||||||||

|

$1.61 - $2.10 |

2,357,500 | 2.1 | 2.08 | 2,357,500 | 2.11 |

- |

|||||||||

| 6,238,333 | 2.1 |

$ |

1.36 | 5,709,995 |

$ |

1.38 |

$ |

979,825 | |||||||

19

2013 Stock Option Plan – NYSE MKT Stock Exchange

The estimated unrecognized compensation cost from unvested options as of September 30, 2014 was approximately U.S.$517,433, which is expected to be recognized over the remaining vesting period of 2.76 years, and has a weighted average remaining contractual term of 4.66 years.

The weighted-average U.S.$ grant date fair value of unvested options is summarized below for the nine months ended September 30, 2014 and 2013.

|

September 30, 2014 |

September 30, 2013 |

|||||

|

Unvested Beginning of Year |

$ |

0.41 |

$ |

- |

||

|

Granted |

0.44 | 0.44 | ||||

|

Vested |

0.47 |

- |

||||

|

Expired |

(0.56) |

- |

||||

|

Unvested End of Period |

$ |

0.42 |

$ |

0.44 | ||

The following table summarizes activity for compensatory stock options during the nine months ended September 30, 2014, values in U.S.$, except share amounts:

|

Number of Shares |

Weighted Average Exercise Price |

Aggregate Intrinsic Value |

Number of Shares Exercisable |

|||||||

|

Outstanding, January 1, 2014 |

399,000 |

$ |

0.87 |

$ |

- |

- |

||||

|

Granted |

1,756,005 | 1.07 |

- |

562,333 | ||||||

|

Exercised |

- |

- |

- |

- |

||||||

|

Expired |

(261,628) |

- |

- |

(250,000) | ||||||

|

Outstanding, September 30, 2014 |

1,893,377 |

$ |

0.96 |

$ |

38,210 | 312,333 | ||||

The following table summarizes information about outstanding compensatory stock options as of September 30, 2014, values in U.S.$, except share amounts:

|

Options Outstanding |

Options Exercisable |

||||||||||||||

|

Exercise Prices |

Number of Shares |

Remaining Contractual Life (years) |

Weighted Average Exercise Price |

Number Exercisable |

Weighted Average Exercise Price |

Aggregate Intrinsic Value |

|||||||||

|

$0.56 - $1.00 |

1,876,702 | 4.69 |

$ |

0.90 | 312,333 |

$ |

0.92 |

$ |

38,210 | ||||||

|

$1.01 - $1.60 |

16,675 | 4.31 | 1.03 |

- |

- |

- |

|||||||||

| 1,893,377 | 4.69 |

$ |

0.96 | 312,333 |

$ |

0.92 |

$ |

38,210 | |||||||

d) Share purchase warrants:

There were no outstanding warrants as of September 30, 2014.

As of December 31, 2013, there were 6,130,781 warrants outstanding with an exercise price of U.S.$1.85 per share and each warrant entitled the holder to purchase one additional common share until January 6, 2014. All warrants expired on January 6, 2014 unexercised. U.S. GAAP requires the value of share purchase warrants issued with an exercise price denominated in a currency other than the Company’s Canadian dollar functional currency to be considered as a liability and this liability is stated at fair value each reporting period. As of December 31, 2013, the fair value of the warrant liability was adjusted to zero based upon the stock price of $0.81 compared to the exercise price of $1.85 and only six days remaining on the warrants term. As of September 30, 2013, the fair value of the warrant liability was adjusted to $112,847. The gain of $476,790 and $1,053,534 related to the change in the fair value of the warrants has been reported in “Gain on change in fair value of derivative liabilities” within Other Income in the Consolidated Statement of Operations for the three and nine months ended September 30, 2013, respectively.

During the nine months ended September 30, 2014, the Company did not issue any warrants.

20

11. Redeemable Preferred Shares

In December 2012, the Company issued 37,837,838 Series A Preferred Shares at U.S.$1.85 per share for gross proceeds of $68,936,000 (U.S.$70,000,000) by way of a private placement. The Company incurred a total of $641,333 in share issuance costs, of which the Company proportionately allocated $229,753 to an embedded derivative liability and, the remaining share issuance costs of $411,580 were netted against the redeemable preferred shares on the Consolidated Balance Sheet. The Series A Preferred Shares are a participating security as defined under ASC 260, in that the security participates in dividends with common stock and has rights to earnings (additional-paid-in-capital in the absence of earnings) that otherwise would have been available to common shareholders. There is an eight percent (8%) annual dividend, compounding monthly, payable quarterly on the Series A Preferred Shares. At the Company’s option, it may pay the 8% dividend with common shares, net of withholding taxes, in-lieu of cash, based on the closing price of the Company’s common shares as quoted by the NYSE MKT on the trading day immediately prior to the payment date.

Details of dividends paid or declared to date are as follows:

|

Dividend |

Date Declared |

Record Date |

Dividend Per Share |

Total Dividend |

Payment Date |

Payment Type (1) |

||||||||

|

Preferred Series A Holders |

3/11/2013 |

3/25/2013 |

$ |

0.04 |

$ |

1,699,140 |

4/1/2013 |

Cash |

||||||

|

Preferred Series A Holders |

6/20/2013 |

6/24/2013 |

0.04 | 1,479,868 |

7/2/2013 |

1,166,930 Shares |

||||||||

|

Preferred Series A Holders |

9/17/2013 |

9/23/2013 |

0.04 | 1,467,197 |

10/1/2013 |

1,260,144 Shares |

||||||||

|

Preferred Series A Holders |

12/19/2013 |

12/23/2013 |

0.04 | 1,515,845 |

1/2/2014 |

1,485,728 Shares |

||||||||

|

Preferred Series A Holders |

3/25/2014 |

3/28/2014 |

0.04 | 1,536,547 |

4/1/2014 |

1,121,046 Shares |

||||||||

|

Preferred Series A Holders |

6/18/2014 |

6/27/2014 |

0.04 | 1,499,632 |

7/2/2014 |

1,322,525 Shares |

||||||||

|

Preferred Series A Holders |

9/19/2014 |

9/26/2014 |

0.04 | 1,591,537 |

10/1/2014 |

1,157,154 Shares |

||||||||

|

$ |

0.28 |

$ |

10,789,766 |

|

(1) |

Dividends denoted as paid in shares require the issuance of shares and the payment of withholding taxes in cash. |

Canadian tax legislation requires a corporate tax to be paid on all cash or in-kind dividends declared and paid by a Canadian entity on taxable preferred shares. The dividends declared since the offering in December 2012 have resulted in Canadian corporate “Part VI.1” tax of $2,712,925, $1,762,136 of which has been remitted as of September 30, 2014. The Company is entitled to a deduction for tax purposes equal to 3.5 times Part VI.1 taxes paid. Therefore, future Canadian corporate tax savings, if realized, should approximately offset the preferred dividend tax expense.

During the three and nine months ended September 30, 2014 the Company incurred $477,245 and $1,210,112 of Part VI.1 tax expense, respectively. During the three and nine months ended September 30, 2013 the Company incurred $309,801 and $1,061,992 of Part VI.1 tax expense, respectively.

The holders of each Series A Preferred Share are able to convert the shares into a common share on a one-for-one basis at any time. After December 13, 2013, the Company can pro-ratably force conversion of the shares into common shares on a one-for-one basis provided that the weighted average price of the common shares exceeds U.S.$3.70 on each trading day during 20 consecutive trading days immediately prior to both the delivery of an applicable mandatory conversion notice and the applicable mandatory conversion date. From December 13, 2017, the Company or each holder of Series A Preferred Shares has the right, exercisable by 30 days' notice in writing, to redeem or to require the Company to redeem at their issue price of U.S.$1.85 per share any portion of the Series A Preferred Shares plus accumulated unpaid dividends for cash.

If the outstanding Series A Preferred Shares had been converted as of September 30, 2014, 37,837,838 common shares would have been issued and the fair value of those common shares based upon the closing price on the NYSE MKT as of September 30, 2014 of U.S.$1.04 would have been U.S.$39,351,351. If the common share price was above U.S.$1.85, there would be no change to the number of common shares issued upon conversion.

Holders of the Series A Preferred Shares, have the right to nominate and elect, voting as a separate class, one (1) director to the Company’s Board. If the size of the Company’s Board is increased beyond seven (7) members, increases will occur in increments of two (2) and the “Preferred Governance Majority” will have the right to designate one (1) of the two additional director nominees for election or appointment as director. The Preferred Governance Majority has the right to fill any vacancy of the preferred shareholder director position.

21