Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - CNB FINANCIAL CORP/PA | d808608d8k.htm |

Investor Meetings

November 2014

Exhibit 99.1 |

Forward-Looking Statements

This

presentation

includes

forward-looking

statements

within

the

meaning

of

Section

27A

of

the

Securities

Act

of

1933,

as

amended,

and

Section

21E

of

the

Securities

Exchange

Act

of

1934,

as

amended,

with

respect

to

the

financial

condition,

liquidity,

results

of

operations,

future

performance

and

business

of

CNB

Financial

Corporation.

These

forward-looking

statements

are

intended

to

be

covered

by

the

safe

harbor

for

“forward-looking

statements”

provided

by

the

Private

Securities

Litigation

Reform

Act

of

1995.

Forward-looking

statements

are

those

that

are

not

historical

facts.

Forward-looking

statements

include

statements

with

respect

to

beliefs,

plans,

objectives,

goals,

expectations,

anticipations,

estimates

and

intentions

that

are

subject

to

significant

risks

and

uncertainties

and

are

subject

to

change

based

on

various

factors

(some

of

which

are

beyond

our

control).

Forward-looking

statements

often

include

the

words

“believes,”

“expects,”

“anticipates,”

“estimates,”

“forecasts,”

“intends,”

“plans,”

“targets,”

“potentially,”

“probably,”

“projects,”

“outlook”

or

similar

expressions

or

future

conditional

verbs

such

as

“may,”

“will,”

“should,”

“would”

and

“could.”

Such

known

and

unknown

risks,

uncertainties

and

other

factors

that

could

cause

the

actual

results

to

differ

materially

from

the

statements,

include,

but

are

not

limited

to:

(i)

changes

in

general

business,

industry

or

economic

conditions

or

competition;

(ii)

changes

in

any

applicable

law,

rule,

regulation,

policy,

guideline

or

practice

governing

or

affecting

financial

holding

companies

and

their

subsidiaries

or

with

respect

to

tax

or

accounting

principles

or

otherwise;

(iii)

adverse

changes

or

conditions

in

capital

and

financial

markets;

(iv)

changes

in

interest

rates;

(v)

higher

than

expected

costs

or

other

difficulties

related

to

integration

of

combined

or

merged

businesses;

(vi)

the

inability

to

realize

expected

cost

savings

or

achieve

other

anticipated

benefits

in

connection

with

business

combinations

and

other

acquisitions;

(vii)

changes

in

the

quality

or

composition

of

our

loan

and

investment

portfolios;

(viii)

adequacy

of

loan

loss

reserves;

(ix)

increased

competition;

(x)

loss

of

certain

key

officers;

(xi)

continued

relationships

with

major

customers;

(xii)

deposit

attrition;

(xiii)

rapidly

changing

technology;

(xiv)

unanticipated

regulatory

or

judicial

proceedings

and

liabilities

and

other

costs;

(xv)

changes

in

the

cost

of

funds,

demand

for

loan

products

or

demand

for

financial

services;

and

(xvi)

other

economic,

competitive,

governmental

or

technological

factors

affecting

our

operations,

markets,

products,

services

and

prices.

Such

developments

could

have

an

adverse

impact

on

our

financial

position

and

our

results

of

operations.

The

forward-looking

statements

are

based

upon

management’s

beliefs

and

assumptions.

Any

forward-looking

statement

made

herein

speaks

only

as

of

the

date

of

this

presentation.

Factors

or

events

that

could

cause

our

actual

results

to

differ

may

emerge

from

time

to

time,

and

it

is

not

possible

for

us

to

predict

all

of

them.

We

undertake

no

obligation

to

publicly

update

any

forward-looking

statement,

whether

as

a

result

of

new

information,

future

developments

or

otherwise,

except

as

may

be

required

by

law.

2 |

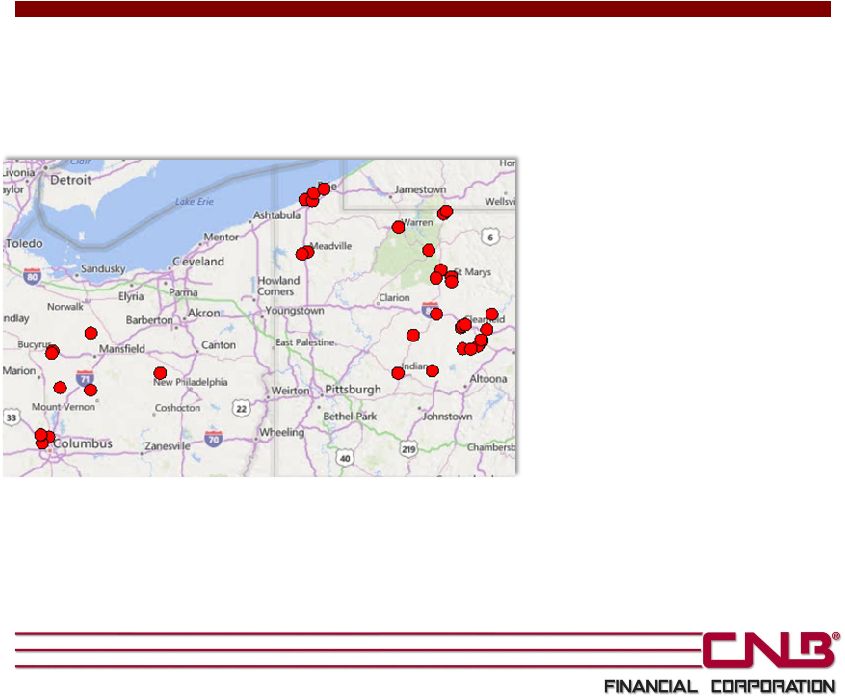

CNB

Financial Overview 3

Source: SNL Financial and company data. Information and data as

of September 30, 2014

CNB Financial is a full-service bank,

headquartered in Clearfield, PA, providing

services, including wealth and asset management,

to individuals, businesses, governments, and

institutional customers

As of September 30, 2014:

Operates 37 branches in North Central

Pennsylvania and Ohio through its principal

subsidiary, CNB Bank

CNB Bank is a regional independent community

bank operating:

Loan production offices in Hollidaysburg, PA and

Ashtabula, OH

Holiday Financial Services Corporation is a

consumer discount loan company with 13 offices

NASDAQ-listed under the symbol “CCNE”

•

Assets: $2.2 billion

•

Loans: $1.3 billion

•

Deposits: $1.9 billion

•

21 branches in North Central Pennsylvania

•

7 full-service branches through ERIEBANK, a

division of CNB Bank headquartered in Erie, PA

•

9 full-service branches through its newest

division FCBank, headquartered in Bucyrus,

Ohio |

Strong Balance Sheet Growth

•

Successfully closed on previously announced acquisition of FC Banc Corp. during the

fourth quarter of 2013 •

Loans of $1.3 billion at September 30, 2014 represent 28.9% growth over September

30, 2013, comprised of 25.0% from the FC acquisition and organic growth of

3.9% •

Deposits of $1.9 billion at September 30, 2014 represent 20.3% growth over

September 30, 2013, which is primarily attributable to the FC Banc Corp.

acquisition Profitability

•

Net income of $16.3 million for the nine months ended September 30, 2014, an

increase of 36.6% from the first nine months of 2013

•

Annualized return on assets of 1.01% and return on equity of 12.22%, as compared to

0.88% and 11.42%, respectively, for the nine months ended September 30,

2013 •

Net interest margin of 3.78% compared to 3.38% for the nine months ended September

30, 2013 Superior Asset Quality

•

Nonperforming assets to total assets of 0.55%

•

Net charge-offs to average loans of 0.09% for CNB Bank and 0.19% including

Holiday Financial Services Corp. •

Allowance for loan losses to loans of 1.35%

Capital

•

Tangible common equity to tangible assets of 7.04%*

•

Leverage ratio of 8.22%

•

Tier 1 Risk Based Ratio of 12.99%

•

Total Risk Based Capital Ratio of 14.24%

Financial Highlights –

YTD 2014

4

Note: Financial data as of or for the nine months ended September 30, 2014

*Please see the Appendix for a reconciliation of non-GAAP financial

information. |

2014

Initiatives Opened a CNB Bank loan production office in Blair County, PA

in April

Opened a FCBank full-service branch in Dublin, OH in July

Opened an ERIEBANK loan production office in Ashtabula, OH

in October

Construction of new ERIEBANK full-service branch in Erie, PA

that is scheduled to open in the first quarter of 2015

5 |

History of CNB Financial

6

1865

1934

1984

2005

2006

2008

2009

2010 2013

1865:

County

National Bank

of Clearfield

established

1934:

Reorganizes

through a stock

offering to existing

depositors

1984:

Forms

CNB

Financial Corporation

holding company

2005:

ERIEBANK is

formed

2005:

Purchases

assets

of Holiday Consumer

Discount Company and

forms Holiday Financial

Services Corporation

2006:

Conversion

to a state banking

charter

2010:

Joseph

Bower

becomes CEO after

retirement of William

Falger

2008-2009:

Receives

approval to raise $21

million via TARP;

CNB chooses not to

participate

2010:

Capital

raise of $34.5

million

2013:

Acquisition of

FC Banc Corp.

headquartered

in Bucyrus,

Ohio with $360

million in

assets |

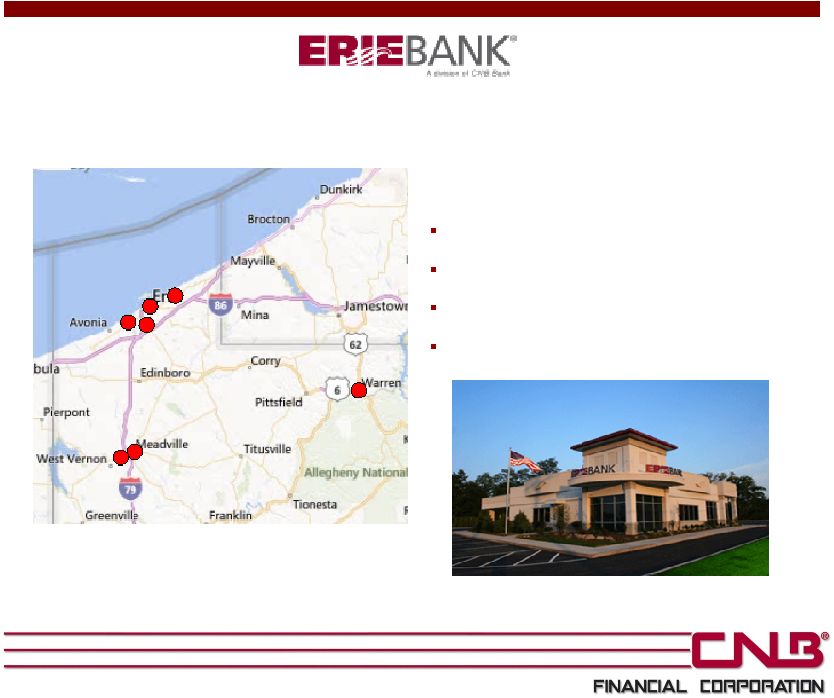

ERIEBANK, a division of CNB Bank, was created de novo in 2005

At September 30, 2014:

7

Seven branches

One loan production office

$414 million in loans

$614 million in deposits |

Expansion into Ohio

•

The acquisition of FC Banc Corp., which closed in the

fourth quarter of 2013, expanded CNB’s geographic

footprint into Central Ohio with meaningful size and

scale

–

Entry into 5 new markets, similar to those that CNB currently serves

–

$360 million in total assets; $248 million in loans; and $332 million in deposits

as of October 11, 2013

•

Opportunity to replicate CNB’s already successful ERIEBANK model in a market

conducive to CNB’s business plan

•

Significant opportunity for both organic and strategic growth going forward

•

EPS accretion projected in the first full combined year without significant TBV

dilution 8 |

CNB’s Experienced Management Team

Years at

Years in

Executive

Title

CCNE

Industry

Joseph B. Bower Jr.

President & Chief Executive Officer

17

21

Richard L. Greslick Jr.

EVP / Chief Operating Officer & Secretary

16

16

Joseph E. Dell Jr.

SVP / Chief Lending Officer

1

30

Mark D. Breakey

EVP / Chief Credit Officer

23

29

Brian W. Wingard

SVP / Chief Financial Officer & Treasurer

6

6

Vincent C. Turiano

SVP / Operations

5

41

Leanne D. Kasseb

SVP / Marketing

18

20

Mary Ann Conaway

SVP / Human Resources

32

32

David J. Zimmer

President of ERIEBANK

9

30

J. Andrew Dale

President of FC Bank

1

27

9 |

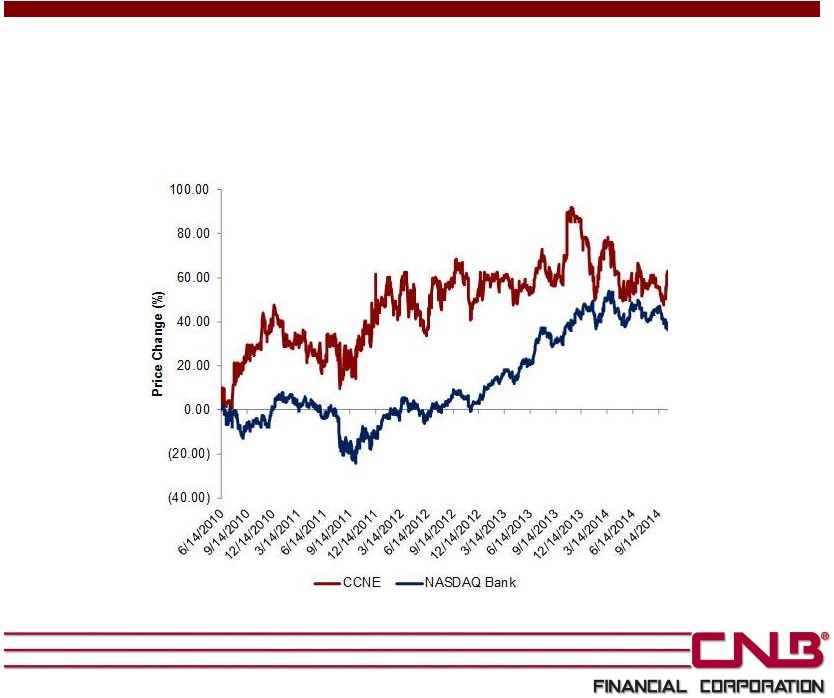

CNB

Stock Price Performance Since its follow-on offering in 2010, CNB has

outperformed the NASDAQ Bank Index

Source: SNL Financial. Price change from 6/14/10 to 10/17/14

10 |

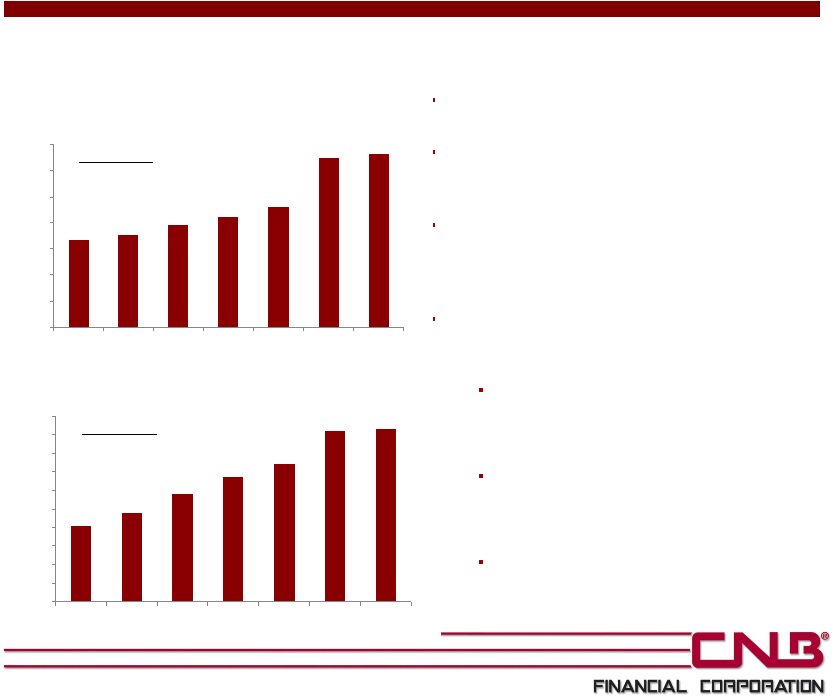

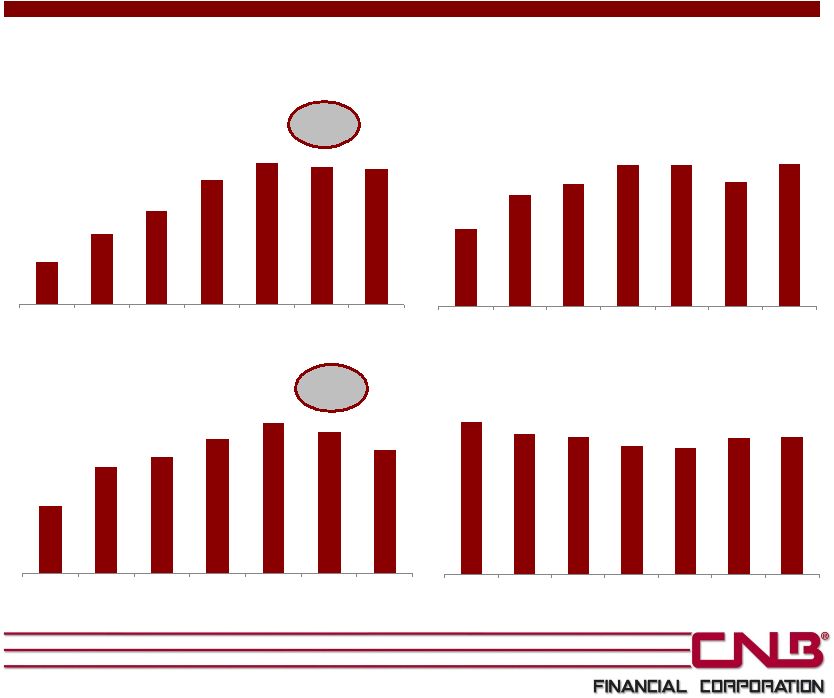

Strong organic loan and deposit growth

through the financial crisis and recession

Fundamental focus on originating loans in-

market and funding with local, low-cost core

deposits while maintaining asset quality

The Bank strives to be more customer-

driven than its competitors and builds long-

term customer relationships by being

reliable and competitively priced

Loans and deposits at September 30, 2014

are relatively flat compared to year-end

2013

Loan and deposit growth for the first nine

months of 2014 was 2.39% and 1.72%,

respectively, within CNB’s historical

markets

Loans and deposits acquired from FC

Banc Corp. have run off 1.07% and

2.07%, respectively, since December 31,

2013, within our expectations

During the next 12 months, CNB

anticipates moderate loan and deposit

growth across all of its markets

Strong Organic Loan and Deposit Growth

11

0

0

0

0

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Total Loans

5-Year CAGR:

Total

14.6%

Organic 9.9%

0

0

0

0

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Total Deposits

5-Year CAGR:

Total

17.2%

Organic 12.7% |

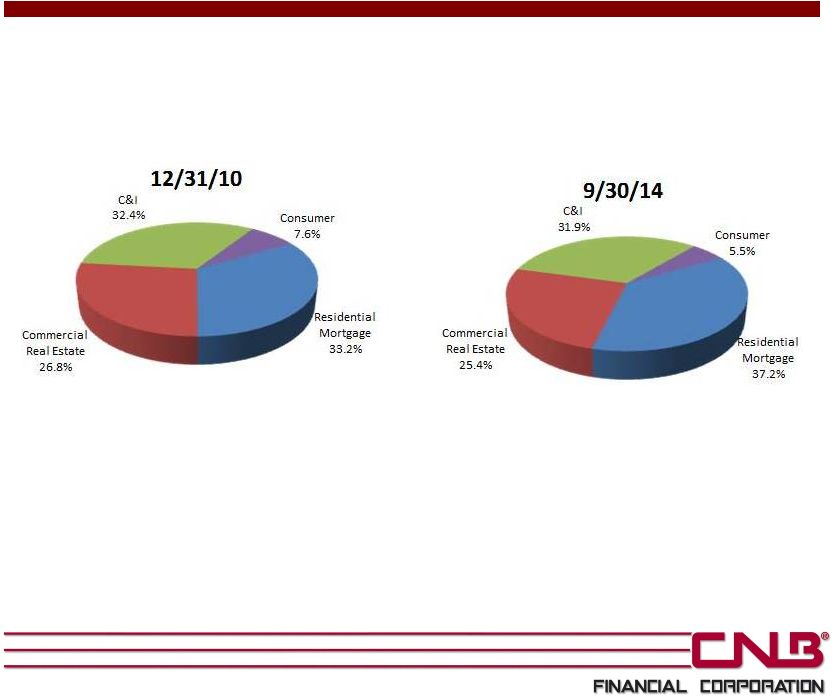

Diversified Loan Portfolio

$795 million

6.43% yield

12

$1.3 billion

5.28% yield |

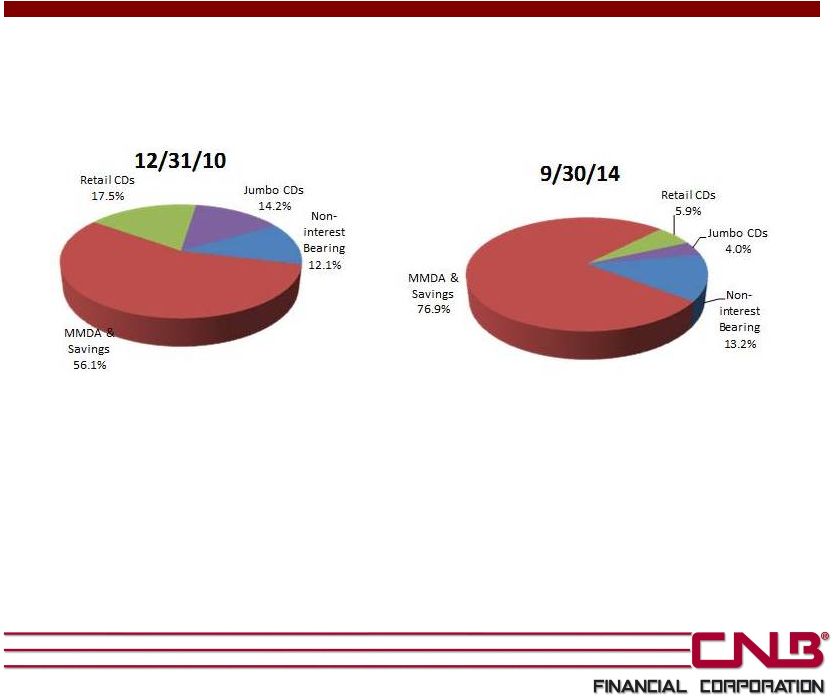

Attractive Deposit Mix

$1.2 billion

1.42% cost of deposits

13

$1.9 billion

0.51% cost of deposits |

Deposit Market Share

Source: SNL Financial. Deposit market share as of June 30, 2014

14

CNB Growth

Market Growth

Market

Rank

# of

Branches

CNB

Deposits

($000)

CNB Deposit

Market Share

(%)

Year over

Year (%)

5-Year

CAGR (%)

Total

Deposits in

Market

($000)

Year over

Year (%)

5-Year

CAGR (%)

Clearfield, PA

1

10

455,265

33.97

1.39

3.34

1,340,282

1.37

0.03

Erie, PA

5

4

408,166

9.31

(4.35)

24.86

4,382,281

3.64

5.23

Elk, PA

2

4

167,188

24.26

0.93

11.89

689,050

0.22

0.94

Crawford, PA

5

2

136,415

10.74

9.88

-

1,270,313

4.07

3.15

McKean, PA

3

3

122,367

14.90

0.16

11.62

821,456

(0.98)

3.30

Crawford, OH

2

2

120,590

16.81

(9.10)

1.66

717,532

(3.67)

0.82

Franklin, OH

17

3

107,979

0.24

(3.31)

14.18

44,791,832

5.79

8.60

Centre, PA

10

1

84,454

3.23

(0.22)

7.80

2,613,896

(2.49)

4.11

Warren, PA

4

1

58,448

7.50

(2.09)

15.80

778,847

(8.24)

1.92

Cambria, PA

10

1

51,820

1.87

0.20

4.96

2,775,698

0.17

1.47

Jefferson, PA

6

1

50,604

5.71

(16.26)

9.74

885,793

(0.49)

0.67

Knox, OH

6

1

37,364

4.94

1.80

3.97

756,899

2.76

2.92

Morrow, OH

4

1

31,116

15.51

(3.65)

2.86

200,664

1.56

2.09

Richland, OH

13

1

12,113

0.71

12.65

28.21

1,715,231

0.55

1.02

Holmes, OH

8

1

4,789

0.63

66.28

-

760,371

4.09

6.89

Indiana, PA

9

1

2,651

0.11

0.23

-

2,449,716

0.52

3.11

Total

37

1,851,329

2.77

(1.20)

11.52

66,949,861

4.01

6.48 |

0

0

0

0

64.83

59.91

58.54

54.96

53.67

58.19

58.76

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y*

2014 YTD

Efficiency Ratio

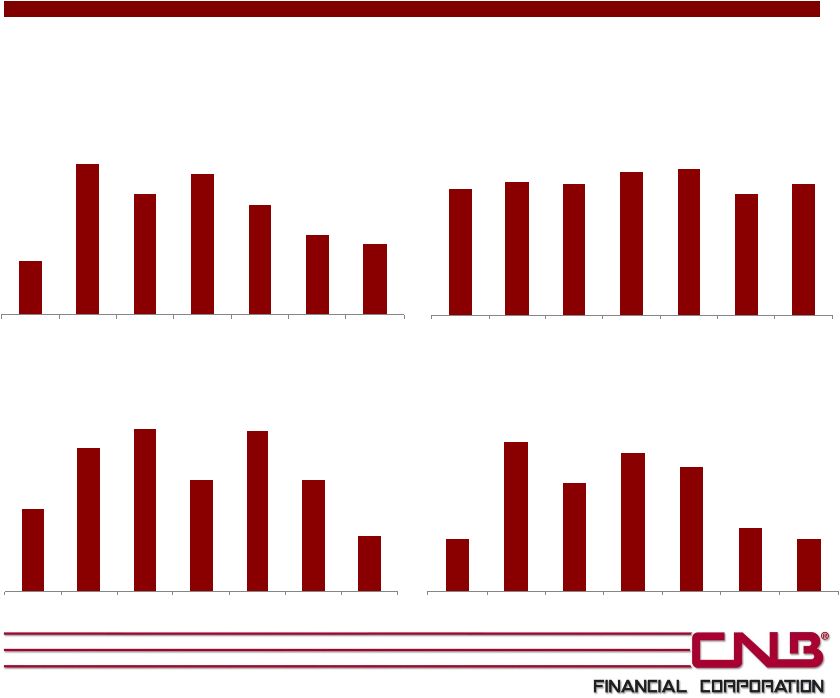

Improved Profitability

* Note 2013 full year net income includes one-time merger costs related to the

acquisition of FC Banc Corp. 2014 YTD is for the nine months ended September

30, 2014 15

0

0

0

0

$5,235

$8,512

$11,316

$15,104

$17,136

$16,679

$16,331

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y*

2014 YTD

Net Income

5-Year

CAGR

+27.7%

0

0

0

0

0.55

0.79

0.87

1.00

1.00

0.88

1.01

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y*

2014 YTD

ROAA

0

0

0

0

$0.61

$0.98

$1.06

$1.23

$1.38

$1.29

$1.13

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y*

2014 YTD

Diluted EPS

5-Year

CAGR

+16.2% |

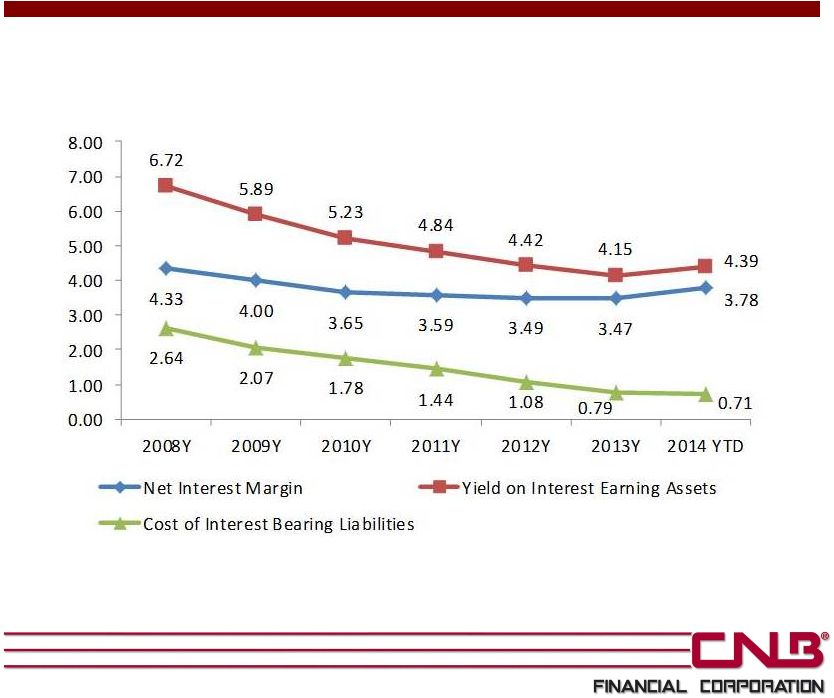

Stable Net Interest Margin

16 |

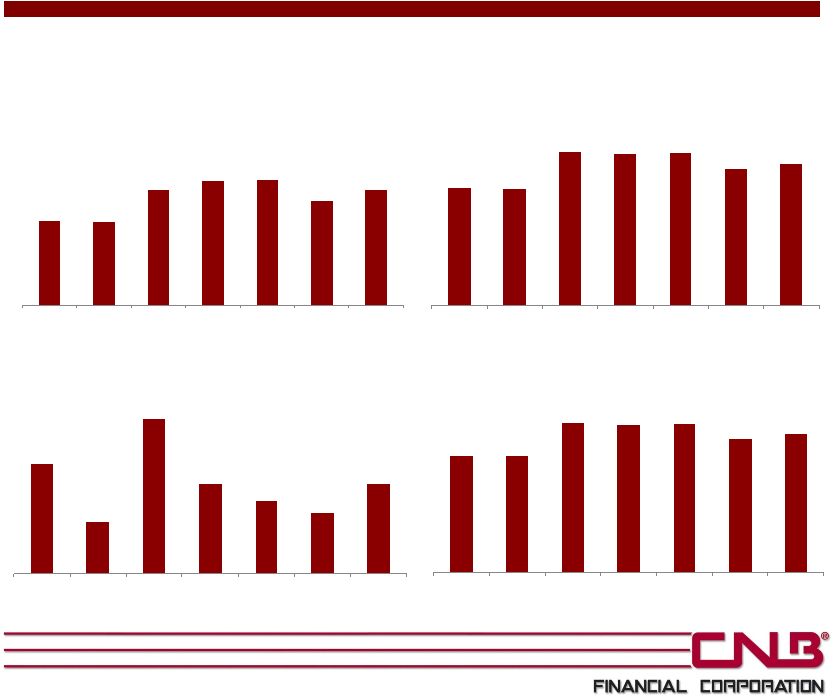

Superior Asset Quality

Source: SNL Financial. NPAs excluded restructured loans. Texas ratio defined as NPA

& Loans 90+/ Tangible Common Equity* + Allowance for Loan Losses.

* Please see the Appendix for a reconciliation of non-GAAP financial

information 17

0

0

0

0

0.42

1.17

0.93

1.09

0.85

0.62

0.55

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

NPAs/Assets

0

0

0

0

1.29

1.37

1.35

1.48

1.51

1.25

1.35

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Allowance for Loan Losses/

Gross Loans

0

0

0

0

7.06

20.30

14.82

18.85

16.90

8.64

7.04

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Texas Ratio

0

0

0

0

0.28

0.49

0.56

0.38

0.55

0.38

0.19

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y*

2014 YTD

NCOs/Average Loans |

Strong Capital Levels

18

* Please see the Appendix for a reconciliation of non-GAAP financial

information. 0

0

0

0

5.12

5.08

7.05

7.61

7.63

6.34

7.04

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Tangible Common

Equity/Tangible Assets*

0

0

0

0

8.40

7.87

8.81

8.22

8.06

7.96

8.22

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Leverage Ratio

0

0

0

0

10.80

10.70

14.13

13.89

14.03

12.51

12.99

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Tier 1 Risk Based Ratio

0

0

0

0

12.00

11.95

15.38

15.14

15.28

13.72

14.24

2008Y

2009Y

2010Y

2011Y

2012Y

2013Y

Sep-14

Total Risk Based Ratio |

CNB’s Growth Strategy

Organic / De Novo Growth Strategy

Acquisition Strategy

Expand our presence into new

markets that fit our business

model (e.g. FCBank)

Bring significant talent

19

Intend to grow organically in the

FCBank market through new offices

and additional lenders

Continued growth of ERIEBANK by

focusing on retail and commercial

relationship banking as well as

private banking

Continue to open loan production

offices to fill-in our markets

M&A is not a priority in our growth

strategy; however, we will remain

opportunistic and would consider a

transaction that would: |

Appendix

20 |

Non-GAAP Financial Reconciliation

21

Year ended December 31,

($ in thousands)

2008

2009

2010

2011

2012

2013

30-Sep-14

Total Shareholders' Equity

$62,467

$69,409

$109,645

$131,889

$145,364

$164,911

$181,617

Less Goodwill

10,821

10,821

10,821

10,821

10,946

27,194

27,194

Less Other Intangible Assets

185

85

-

-

-

4,583

3,677

Tangible Common Equity

$51,461

$58,503

$98,824

$121,068

$134,418

$133,134

$150,746

Total Assets

$1,016,518

$1,161,591

$1,413,511

$1,602,207

$1,773,079

$2,131,289

$2,172,974

Less Goodwill

10,821

10,821

10,821

10,821

10,946

27,194

27,194

Less Other Intangible Assets

185

85

-

-

-

4,583

3,677

Tangible Assets

$1,005,512

$1,150,685

$1,402,690

$1,591,386

$1,762,133

$2,099,512

$2,142,103

Total Shareholders' Equity / Total Assets

6.15%

5.98%

7.76%

8.23%

8.20%

7.74%

8.36%

Tangible Common Equity / Tangible Assets

5.12%

5.08%

7.05%

7.61%

7.63%

6.34%

7.04%

Tangible

common

equity

to

tangible

assets

is

a

non-GAAP

financial

measure

calculated

using

GAAP

amounts.

Tangible

common

equity

is

calculated

by

excluding

the

balance

of

goodwill

and

other

intangible

assets

from

the

calculation

of

shareholders’

equity.

Tangible

assets

is

calculated

by

excluding

the

balance

of

goodwill

and

other

intangible

assets

from

the

calculation

of

total

assets.

CNB

believes

that

this

non-GAAP

financial

measure

provides

information

to

investors

that

is

useful

in

understanding

our

financial

condition.

Because

not

all

companies

use

the

same

calculations

of

tangible

common

equity

and

tangible

assets,

this

presentation

may

not

be

comparable

to

other

similarly

titled

measures

calculated

by

other

companies.

A

reconciliation

of

this

non-GAAP

financial

measure

is

provided

below. |