Attached files

| file | filename |

|---|---|

| EX-99.1 - EXHIBIT 99.1 - Midwest Cable, Inc. | dp50511_ex9901.htm |

| EX-99.7 - EXHIBIT 99.7 - Midwest Cable, Inc. | dp50511_ex9907.htm |

| EX-3.4 - EXHIBIT 3.4 - Midwest Cable, Inc. | dp50511_ex0304.htm |

| EX-99.3 - EXHIBIT 99.3 - Midwest Cable, Inc. | dp50511_ex9903.htm |

| EX-23.2 - EXHIBIT 23.2 - Midwest Cable, Inc. | dp50511_ex2302.htm |

| EX-99.8 - EXHIBIT 99.8 - Midwest Cable, Inc. | dp50511_ex9908.htm |

| EX-99.9 - EXHIBIT 99.9 - Midwest Cable, Inc. | dp50511_ex9909.htm |

| EX-99.2 - EXHIBIT 99.2 - Midwest Cable, Inc. | dp50511_ex9902.htm |

| EX-23.1 - EXHIBIT 23.1 - Midwest Cable, Inc. | dp50511_ex2301.htm |

| EX-3.2 - EXHIBIT 3.2 - Midwest Cable, Inc. | dp50511_ex0302.htm |

| EX-99.4 - EXHIBIT 99.4 - Midwest Cable, Inc. | dp50511_ex9904.htm |

| EX-99.6 - EXHIBIT 99.6 - Midwest Cable, Inc. | dp50511_ex9906.htm |

| EX-99.5 - EXHIBIT 99.5 - Midwest Cable, Inc. | dp50511_ex9905.htm |

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON OCTOBER 31, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Midwest Cable, Inc.

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware

|

4841

|

47-0973096

|

|

(State or Other Jurisdiction of

Incorporation or Organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification Number)

|

|

One Comcast Center

Philadelphia, Pennsylvania 19103-2838

(215) 286-1700

|

||

|

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

|

||

|

One Comcast Center

Philadelphia, Pennsylvania 19103-2838

(215) 286-1700

|

||

|

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

|

||

|

Copies to:

|

||||

|

Arthur R. Block, Esq.

Midwest Cable, Inc.

One Comcast Center

Philadelphia, Pennsylvania 19103-2838

(215) 286-1700

|

Deanna L. Kirkpatrick, Esq.

Davis Polk & Wardwell llp

450 Lexington Avenue

New York, New York 10017

(212) 450-4000

|

|||

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement and all other conditions to the proposed transactions described herein have been satisfied or waived, as applicable.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐ __________

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐ __________

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐ __________

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

|

|

Non-accelerated filer x (Do not check if a smaller reporting company)

|

Smaller reporting company ☐

|

|

CALCULATION OF REGISTRATION FEE

|

||

|

Title Of Each Class

Of Securities To Be Registered(1)

|

Estimated Maximum Aggregate Price(2)

|

Amount Of Registration Fee(2)

|

|

Class A common stock, par value $0.001 per share

|

$5,701,000,000

|

$662,456.20

|

|

Class A-1 common stock, par value $0.001 per share

|

||

|

(1)

|

This Registration Statement relates to an indeterminate amount of shares of Class A common stock, par value $0.001 per share and Class A-1 common stock, par value $0.001 per share, of Midwest Cable, Inc. (the “Registrant”), which will be distributed pursuant to a spin-off transaction to the holders of Comcast Corporation common stock as described in the prospectus forming a part of this Registration Statement.

|

|

(2)

|

Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(f)(2) under the Securities Act of 1933, as amended. The Registrant estimates that the book value of the shares to be registered is equal to $5,701,000,000, which represents the aggregate book value of the Registrant as of June 30, 2014, the latest practicable date prior to the filing of the Registration Statement. The book value upon which the registration fee is calculated does not indicate any anticipated market value upon issuance of the shares in the spin-off.

|

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

|

The information in this prospectus is not complete and may be changed. We may not issue these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

SUBJECT TO COMPLETION, DATED OCTOBER 31, 2014

PRELIMINARY PROSPECTUS

Shares of Class A

Shares of Class A-1

MIDWEST CABLE, INC.

Common Stock

Common Stock

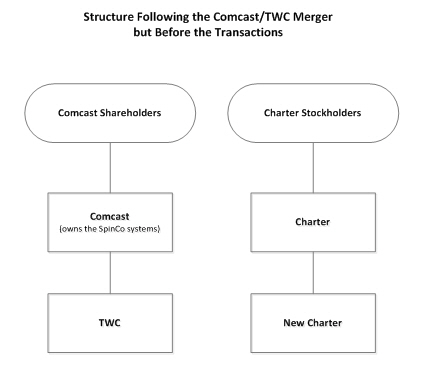

Comcast Corporation (“Comcast”) and Time Warner Cable Inc. (“TWC”) have entered into a merger agreement under which TWC will become a wholly owned subsidiary of Comcast. The merger agreement states that Comcast is prepared to divest up to approximately 3.0 million video subscribers of the combined company’s approximately 33.7 million video subscribers. Comcast has entered into a transactions agreement with Charter Communications, Inc. (“Charter”) to satisfy its undertaking in the merger agreement with respect to the divestiture of video subscribers. Among other things, the transactions agreement contemplates a spin-off of cable systems serving approximately 2.5 million existing Comcast video subscribers into Midwest Cable, Inc. (“SpinCo,” “we” or “us”), a newly formed entity and currently a wholly owned subsidiary of Comcast.

This prospectus is being furnished in connection with the planned distribution on a pro rata basis to holders of shares of Comcast Class A common stock, Class A Special common stock and Class B common stock (collectively, “Comcast common stock”) of all of our shares of Class A and Class A-1 common stock outstanding prior to the SpinCo merger described below. We refer to such planned distribution as the “spin-off.” Immediately prior to the spin-off, Comcast will contribute to us systems currently owned by Comcast serving approximately 2.5 million video subscribers in the Midwestern and Southeastern United States (the “SpinCo systems”), together with the related subscribers, the assets and liabilities primarily related to the SpinCo systems and certain other assets and liabilities.

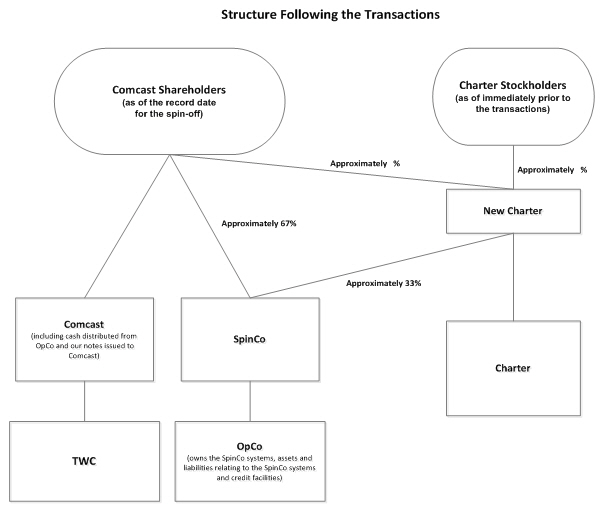

Following the spin-off, CCH I, LLC, a wholly owned subsidiary of Charter (“New Charter”), will convert into a corporation. A newly formed, wholly owned subsidiary of New Charter will merge with and into Charter with the effect that all shares of Charter will be converted into shares of New Charter, and New Charter will survive as the publicly traded parent company of Charter, which transaction is referred to in this prospectus as the “Charter reorganization.” Another newly formed, wholly owned subsidiary of New Charter will merge with and into us, with us surviving, which is referred to in this prospectus as the “SpinCo merger” (and, together with the spin-off, the “transactions”). As a result of the spin-off and SpinCo merger, Comcast’s shareholders as of the record date for the spin-off will own approximately 67% of us, and New Charter will own the remaining approximately 33%. In addition, as a result of the SpinCo merger, it is expected that Comcast’s shareholders as of the record date for the spin-off will own approximately % of New Charter. It is intended that the spin-off, together with certain related transactions, will qualify as a tax-free reorganization and a tax-free distribution and that the SpinCo merger will qualify as a tax-free transaction.

For each shares of Comcast common stock outstanding as of 5:00 p.m., Eastern time, on , 2015, the record date for the spin-off (the “record date”), the holder will be entitled to receive shares of our Class A common stock and shares of our Class A-1 common stock. The distribution of our common stock will be made in book-entry form. Pursuant to the merger agreement for the SpinCo merger, each share of our Class A-1 common stock will be converted into a pro rata portion of the shares of New Charter common stock issued in the SpinCo merger. Following the SpinCo merger, we will have only shares of Class A common stock outstanding.

There is currently no trading market for our common stock. We have applied to list our Class A common stock on the NASDAQ Global Select Market under the symbol “GLCI.” Upon consummation of the SpinCo merger, we expect to change our legal name to GreatLand Connections Inc.

No action will be required of you to receive our common stock or New Charter common stock, which means that you will not be required to pay for our common stock that you receive in the spin-off or the New Charter common stock issued in the SpinCo merger and that you do not need to surrender or exchange any of your Comcast common stock in order to receive our common stock or New Charter common stock, or take any other action in connection with the spin-off.

In reviewing this prospectus, you should carefully consider the matters described under the caption “Risk Factors” beginning on page 8.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

WE ARE NOT ASKING YOU FOR A PROXY AND YOU ARE REQUESTED NOT TO SEND US A PROXY.

This prospectus does not constitute an offer to sell or the solicitation of an offer to buy any securities.

The date of this prospectus is , 2015

|

Page

|

Page

|

|||

In this prospectus, “SpinCo,” the “company,” “we,” “us” and “our” refer to Midwest Cable, Inc. and its combined subsidiaries, after giving effect to the transactions. In addition, in connection with the transactions, we expect to change our legal name to GreatLand Connections Inc. References to shares of our common stock refer to Class A and/or Class A-1 common stock as the context may require. We have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may provide you. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus.

This prospectus is being furnished solely to provide information to holders of Comcast common stock who will receive shares of our common stock in the spin-off. It is not to be construed as an inducement or encouragement to buy or sell any of our securities or any securities of Comcast. This prospectus describes our business, our relationships with Comcast and Charter and the transactions and provides other information to assist you in evaluating the benefits and risks of holding or disposing of our common stock that you will receive in the spin-off. You should be aware of certain risks relating to the transactions, our business, our indebtedness and ownership of our common stock, which are described under the heading “Risk Factors.”

This prospectus includes industry and market data that we obtained from periodic industry publications, third-party studies and surveys, filings of public companies in our industry and internal company surveys. These sources include government and industry sources. Industry publications and surveys generally state that the information contained therein has been obtained from sources believed to be reliable. Although we believe the industry and market data to be reliable as of the date of this prospectus, this information could prove to be inaccurate. Industry and market data could be wrong because of the method by which sources obtained their data and because information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. In addition, we do not know all of the assumptions regarding general economic conditions or growth that were used in preparing the sources relied upon or cited herein.

This summary highlights information contained elsewhere in this prospectus. You should read this entire prospectus carefully, especially the risks of owning our common stock discussed under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our combined financial statements and related notes to better understand the transactions and our business and financial position.

This prospectus also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks faced by us described below and elsewhere in this prospectus. See “Cautionary Statement Regarding Forward-Looking Statements.”

Our Company

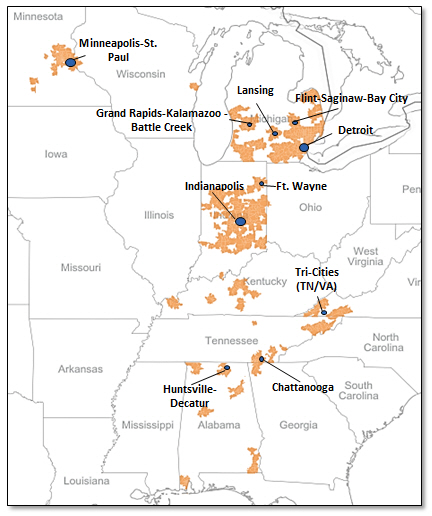

We were formed in May 2014 as a limited liability company and converted to a corporation in September 2014. We offer a variety of video, high-speed Internet and voice services (“cable services”) over our geographically-aligned cable distribution system to residential and commercial customers located in the Midwestern and Southeastern United States. As of June 30, 2014, we served approximately 2.5 million video customers, 2.3 million high-speed Internet customers and 1.2 million voice customers and passed approximately 6.3 million homes and businesses. As of June 30, 2014, we had customer relationships with approximately 2.7 million residential customers and 179,000 commercial customers.

We offer our cable services individually and in bundles. Our subscription rates and related charges vary according to the services and features customers receive and the type of equipment they use, and customers are typically billed in advance on a monthly basis. Our residential customers may generally discontinue service at any time, while commercial customers may only discontinue service in accordance with the terms of their contracts, which typically have two- to five-year terms.

The Transactions

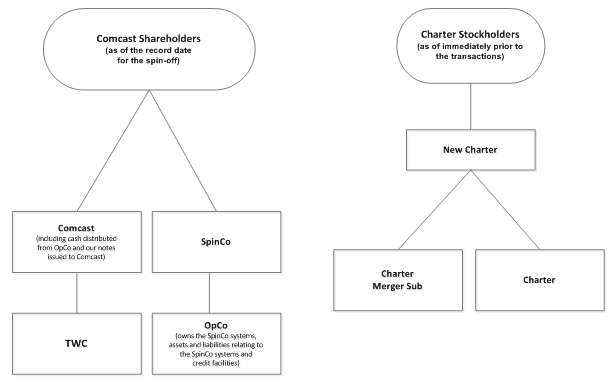

On February 12, 2014, Comcast and TWC entered into a merger agreement under which TWC will become a wholly owned subsidiary of Comcast. The merger agreement is subject to the satisfaction or waiver of certain conditions, including the receipt of applicable regulatory approvals, which may require the divestiture of certain assets. In furtherance of obtaining necessary regulatory approvals, the merger agreement states that Comcast is prepared to divest up to approximately 3.0 million video subscribers of the combined company’s approximately 33.7 million video subscribers. On April 25, 2014, Comcast entered into a transactions agreement with Charter to satisfy its undertaking in the merger agreement with respect to the divestiture of video subscribers. Among other things, the transactions agreement contemplates a contribution, spin-off and merger transaction resulting, upon completion of the transactions described therein, in the contribution of cable systems serving approximately 2.5 million existing Comcast video subscribers to us. We are a newly formed entity and currently a wholly owned subsidiary of Comcast. Following such contribution, we will hold and operate systems currently owned by Comcast serving approximately 2.5 million existing Comcast video subscribers in the Midwestern and Southeastern United States (the “SpinCo systems”), together with the related subscribers, the assets and liabilities primarily related to the SpinCo systems and certain other assets and liabilities, including bank debt and/or term loans (collectively, “credit facilities”). The spin-off will occur after the closing of the Comcast/TWC merger and will be made pro rata to holders of Comcast common stock as of the record date.

The transactions agreement has been approved by the boards of directors of both Comcast and Charter, and the TWC board of directors consented to the entry by Comcast into the transactions agreement, subject to the terms and conditions set forth in the consent between TWC and Comcast dated April 25, 2014 (the “TWC consent”), which include certain understandings of Comcast and TWC with respect to the receipt of required regulatory approvals under the merger agreement.

Comcast, Charter and we have also agreed to use reasonable best efforts to cause us to incur new indebtedness in an aggregate amount equal to 5.0 times the 2014 EBITDA of the SpinCo systems (as such term is defined by our financing sources for purposes of the financing), which indebtedness we currently estimate to be approximately $7.8 billion in the aggregate. The indebtedness will consist of (i) credit facilities to be used to fund cash distributions to Comcast and for our general corporate purposes and (ii) notes newly issued by us to Comcast, which notes will enable Comcast to complete a debt-for-debt exchange whereby one or more financial institutions will exchange debt securities of Comcast for our new notes held by Comcast, which exchange is referred to in this prospectus as the “debt-for-debt exchange.” Comcast anticipates that following the debt-for-debt exchange, the financial institutions will resell our notes that they receive in a Rule 144A private placement to qualified institutional buyers. As described below, completion of the debt-for-debt exchange is a condition to the transactions.

Immediately prior to the spin-off, Comcast will contribute to us the SpinCo systems, together with the related subscribers, the assets and liabilities primarily related to the SpinCo systems and certain other assets and liabilities, including credit facilities, a portion of the proceeds of which will have been distributed to Comcast prior to such contribution. In connection with such contribution and prior to the spin-off, we will issue notes and stock to Comcast. Following such contribution to us and the issuance of notes and stock, Comcast will distribute all of our Class A and Class A-1 common stock to holders of Comcast common stock as of the record date, which distribution is referred to as the “spin-off.” For each shares of Comcast common stock outstanding as of 5:00 p.m., Eastern time, on the record date, the holder will be entitled to receive shares of our Class A common stock and shares of our Class A-1 common stock. After the spin-off, Comcast will not have any ownership interest in us.

Immediately following the spin-off, CCH I, LLC, a wholly owned subsidiary of Charter (“New Charter”), will convert into a corporation. A newly formed, wholly owned subsidiary of New Charter will merge with and into Charter with the effect that all shares of Charter will be converted into shares of New Charter, and New Charter will survive as the publicly traded parent company of Charter, which transaction is referred to in this prospectus as the “Charter reorganization.” Another newly formed, wholly owned subsidiary of New Charter will merge with and into us, with us surviving, which is referred to in this prospectus as the “SpinCo merger” (and, together with the spin-off, the “transactions”). Pursuant to the SpinCo merger, (i) each share of our Class A-1 common stock will be converted into a pro rata portion of the shares of New Charter common stock issued in the SpinCo merger and (ii) New Charter will receive a number of shares of our Class A common stock that is equal to the number of shares of our Class A-1 common stock that have been converted into shares of New Charter common stock. Following the SpinCo merger, we will have only shares of Class A common stock outstanding. As a result of the spin-off and the SpinCo merger, Comcast’s shareholders as of the record date will own approximately 67% of us, and New Charter will own the remaining approximately 33%. In addition, as a result of the SpinCo merger, it is expected that Comcast’s shareholders as of the record date will own approximately % of New Charter. The actual number of shares of New Charter common stock that, following the SpinCo merger, will be owned by the holders of Comcast common stock as of the record date depends on a number of factors, some of which will not be known until close in time to the completion of the transactions. See “The Transactions—Background and Description of the Transactions.”

The consummation of the transactions is subject to a number of closing conditions, including, among others, completion of the merger between Comcast and TWC, the receipt of certain regulatory approvals, approval by Charter’s stockholders and certain conditions relating to the financing for the transactions. On October 8, 2014, the shareholders of Comcast approved the issuance of Comcast Class A common stock to TWC stockholders in the Comcast/TWC merger. On October 9, 2014, TWC stockholders approved the adoption of the Comcast/TWC merger agreement. For a more detailed description of the transactions and the closing conditions, see “The Transactions—Background and Description of the Transactions.”

At the closing of the transactions, we will have a board of nine directors, separated into three classes, selected as follows: (i) three independent directors that have been selected by Comcast and are reasonably acceptable to Charter, each of whom shall be in a separate class, (ii) three independent directors that have been selected by Comcast from a list of potential nominees provided by Charter, each of whom shall be in a separate class and (iii) three directors that have been designated by Charter, each of whom shall be in a separate class. At each annual stockholders’ meeting held thereafter, one class of directors will be up for election, and directors will be chosen by a plurality vote of the stockholders voting in the election for a term of three years to succeed those whose terms expire. For more information about our board of directors following the consummation of the transactions, see “Management.”

In addition, we will have an executive management team that will report to our board of directors. Our executive management team will consist of individuals that are independent from Charter and Comcast. See “Management.” Upon consummation of the SpinCo merger, we expect to change our legal name to GreatLand Connections Inc.

Risk Factors

This prospectus describes our business, our relationships with Comcast and Charter and the transactions and provides other information to assist you in evaluating the benefits and risks of holding or disposing of our common stock that you will receive in the spin-off. You should carefully consider all the information in this prospectus, including matters set forth under the heading “Risk Factors.”

|

|

·

|

We currently face a wide range of competitors, and newer technologies and services are driving changes in consumer behavior, which may increase the number of competitors we face. Our business and results of operations could be adversely affected if we do not compete effectively.

|

|

|

·

|

Programming expenses for our video services are increasing, and we expect such expenses to increase materially following the spin-off.

|

|

|

·

|

Our business depends on keeping pace with technological developments.

|

|

|

·

|

We are subject to regulation by federal, state and local authorities, which may impose additional costs and restrictions on our business.

|

|

|

·

|

We have no operating history as a separate company and may be unable to maintain our operating results at historical levels after becoming a stand-alone company.

|

|

|

·

|

In connection with the transactions, we expect to incur indebtedness, which could adversely affect our financial condition or business.

|

Material U.S. Federal Income Tax Consequences of the Spin-Off and the SpinCo Merger

It is intended that the spin-off, together with certain related transactions (including the debt-for-debt exchange), will qualify as a tax-free “reorganization” within the meaning of Section 368(a)(1)(D) of the Internal Revenue Code of 1986, as amended (the “Code”), and a tax-free distribution within the meaning of Section 355 of the Code and that the SpinCo merger, together with the Charter reorganization, will qualify as a tax-free transaction within the meaning of Section 351 of the Code. Assuming the spin-off and the SpinCo merger are so treated, in general, for U.S. federal income tax purposes, no gain or loss will be recognized by U.S. holders of Comcast common stock upon the receipt of our common stock in the spin-off and no gain or loss will be recognized by U.S. holders of our common stock upon the receipt of New Charter common stock in exchange for our common stock in the SpinCo merger, in each case, except for any gain or loss recognized with respect to cash received in lieu of a fractional share of our Class A-1 common stock or New Charter common stock.

The consummation of the spin-off, the debt-for-debt exchange, the SpinCo merger and the related transactions is conditioned upon the receipt of an opinion of tax counsel to the effect that such transactions qualify for their intended tax treatment. An opinion of tax counsel neither binds the IRS, nor precludes the IRS or the courts from adopting a contrary position. Comcast does not intend to obtain a ruling from the IRS on the tax consequences of the spin-off, SpinCo merger or any of the related transactions. If the spin-off, debt-for-debt exchange and/or the SpinCo merger fails to qualify for the intended tax treatment, Comcast and/or its shareholders will be subject to tax.

The tax consequences of the spin-off and SpinCo merger to you will depend on your particular circumstances. You should read the discussion in the section of this document entitled “Material U.S. Federal Income Tax Consequences of the Spin-Off and the SpinCo Merger” and consult your tax advisor for a full understanding of the tax consequences to you of the spin-off and SpinCo merger.

Corporate Information

We were formed in the State of Delaware as a limited liability company on May 27, 2014 and subsequently converted to a corporation on September 22, 2014. Prior to the transactions, our principal executive offices are located at One Comcast Center, Philadelphia, Pennsylvania 19103-2838 and our telephone number is (215) 286-1700. Our Internet website is www.greatlandconnections.com. Our website and the information contained therein or connected thereto is not incorporated into this prospectus or the registration statement of which it forms a part. Upon consummation of the SpinCo merger, we expect to change our legal name to GreatLand Connections Inc.

Please see “The Transactions” for a more detailed description of the matters summarized below.

Q: Why am I receiving this document?

A: You are receiving this document because you were a holder of shares of Comcast common stock on the record date for the spin-off and, as such, will be entitled to receive shares of our common stock upon completion of the spin-off described in this prospectus. We are sending you this document to inform you about the transactions and to provide you with information about us and our business and operations upon completion of the transactions.

Q: What do I have to do to participate in the spin-off?

A: Nothing. You will not be required to pay any cash or deliver any other consideration in order to receive the shares of our common stock that you will be entitled to receive upon completion of the spin-off. In addition, you are not being asked to provide a proxy with respect to any of your shares of Comcast common stock in connection with the transactions and you should not send us a proxy.

Q: Why is Comcast divesting its video subscribers and distributing our stock?

A: The spin-off is intended to satisfy Comcast’s undertaking in the TWC merger agreement, in which Comcast states that it is prepared to divest up to approximately 3.0 million video subscribers of the combined company’s approximately 33.7 million video subscribers.

Q: What is SpinCo?

A: SpinCo refers to our company, which is a wholly owned subsidiary of Comcast organized under the laws of Delaware. Immediately prior to the spin-off, Comcast will contribute to us all of the stock of a wholly owned subsidiary of Comcast (“OpCo”). At the time of the contribution, OpCo will hold the SpinCo systems, together with the related subscribers, the assets and liabilities primarily related to the SpinCo systems and certain other assets and liabilities, including credit facilities, a portion of the proceeds of which will have been distributed to Comcast prior to such contribution. Following the transactions, we will be a stand-alone entity that will hold cable systems serving approximately 2.5 million existing Comcast video subscribers in the Midwestern and Southeastern United States. Upon consummation of the SpinCo merger, we expect to change our legal name to GreatLand Connections Inc.

Q: What is the record date for the spin-off?

A: The record date for the spin-off is , 2015, and ownership will be determined as of 5:00 p.m., Eastern Time, on that date. When we refer to the record date in this prospectus, we are referring to that time and date.

Q: When will the spin-off occur?

A: The spin-off is expected to occur on or about , 2015.

Q: What will I receive in the spin-off?

A:. At the effective time of the spin-off, you will be entitled to receive shares of our Class A common stock and shares of our Class A-1 common stock in respect of each share of Comcast common stock held by you on the record date for the spin-off.

Q: How will shares of SpinCo be distributed to me?

A: At the effective time of the spin-off, we will instruct the distribution agent to make book-entry credits for the shares of Class A and Class A-1 common stock that you are entitled to receive. Since shares of our common stock will be in uncertificated book-entry form, you will receive share ownership statements in place of physical share certificates.

Q: How do the Class A and A-1 shares of SpinCo differ?

A:. Our shares of Class A and Class A-1 common stock are separate classes of stock with identical rights. See “Description of Capital Stock.” Pursuant to the merger agreement with New Charter, each share of our Class A-1 common stock will be converted into a pro rata portion of the shares of New Charter common stock issued in the SpinCo merger, and New Charter will receive a number of shares of our Class A common stock that is equal to the number of shares of our Class A-1 common stock that have been converted into shares of New Charter common stock. As a result, following the transactions, holders of Comcast common stock as of the record date will own approximately 67% of us, and New Charter will own the remaining approximately 33%. In addition, as a result of the SpinCo merger, it is expected that Comcast’s shareholders as of the record date will own approximately % of New Charter. The actual number of shares of New Charter common stock that, following the SpinCo merger, will be owned by the holders of Comcast common stock as of the record date depends on a number of factors, some of which will not be known until close in time to the completion of the transactions. See “The Transactions—Background and Description of the Transactions.”

Q: Why will I receive New Charter common stock?

A: In connection with the SpinCo merger, a newly formed, wholly owned subsidiary of New Charter will merge with and into us, with us surviving. In the SpinCo merger, New Charter will receive shares of our Class A common stock and Comcast’s shareholders as of the record date will receive shares of New Charter common stock. As a result of the SpinCo merger, it is expected that Comcast’s shareholders as of the record date will own approximately % of New Charter. The actual number of shares of New Charter common stock that, following the SpinCo merger, will be owned by holders of Comcast common stock as of the record date depends on a number of factors, some of which will not be known until close in time to the completion of the transactions. You will receive another prospectus with information describing New Charter’s business and providing other information to assist you in evaluating the benefits and risks of holding or disposing of New Charter common stock that you will receive in the SpinCo merger. See “The Transactions—Background and Description of the Transactions.”

Q: What are SpinCo’s financing arrangements?

A: Comcast, Charter and we have agreed to use reasonable best efforts to cause us, directly and through our subsidiaries, to incur new indebtedness in an aggregate amount equal to 5.0 times the 2014 EBITDA of the SpinCo systems (as such term is defined by our financing sources for purposes of the financing), which indebtedness we currently estimate to be approximately $7.8 billion in the aggregate. The indebtedness will consist of (i) credit facilities used to fund cash distributions to Comcast and for our general corporate purposes, and (ii) notes newly issued by us to Comcast, which notes will enable Comcast to complete the debt-for-debt exchange. As described below, completion of the debt-for-debt exchange is a condition to the transactions. Immediately prior to the spin-off, Comcast will contribute to us the SpinCo systems, together with the related subscribers, the assets and liabilities primarily related to the SpinCo systems and certain other assets and liabilities, including credit facilities, a portion of the proceeds of which will have been distributed to Comcast prior to such contribution. In connection with such contribution and prior to the spin-off, we will issue notes and stock to Comcast. See “The Transactions—Background and Description of the Transactions.”

Q: Will the SpinCo Class A common stock be listed on a securities exchange?

A: We have applied to list our Class A common stock on the NASDAQ Global Select Market under the symbol “GLCI.”

Q: Do I need to do anything in connection with the exchange of my shares of Class A-1 SpinCo common stock for shares of New Charter common stock?

A: No. Our shares of Class A-1 common stock will automatically be converted into a pro rata portion of the shares of New Charter common stock issued in the SpinCo merger upon consummation of the SpinCo merger.

Q: Once the transactions are consummated what shares will I hold?

A: Following consummation of the transactions, holders of Comcast common stock as of the record date will continue to hold their Comcast common stock in addition to approximately 67% of our Class A common stock, or shares of our Class A common stock for every shares of Comcast’s Class A, Class A Special and Class B common stock you hold as of the record date. In addition, as a result of the SpinCo merger, it is expected that holders of Comcast common stock as of the record date will hold approximately % of New Charter. The actual number of shares of New Charter common stock that, following the SpinCo merger, will be owned by the holders of Comcast common stock as of the record date depends on a number of factors, some of which will not be known until close in time to the completion of the transactions. See “The Transactions—Background and Description of the Transactions.”

Q: How will fractional shares be treated?

A: You will not receive fractional shares of our Class A common stock or New Charter common stock in the transactions. The distribution agent will aggregate and sell on the open market the fractional shares of our Class A common stock that would otherwise be issued in the transactions, and if you would be entitled to receive a fractional share of our Class A common stock in connection with the transactions, you will instead receive the net cash proceeds of the sale attributable to such fractional share. If you would be entitled to receive a fractional share of New Charter common stock in connection with the transactions, you will instead receive an amount in cash determined by multiplying the volume-weighted average price of shares of Charter common stock for the 60 consecutive calendar days ending on the last trading day immediately prior to the closing of the transactions by such fractional share of New Charter common stock. You may receive fractional shares of our Class A-1 common stock in the transactions. Such fractional shares will automatically convert into shares of New Charter common stock immediately following the spin-off.

Q: What are the U.S. federal income tax consequences to me of the transactions?

A: Except with respect to cash you receive in lieu of fractional shares of our Class A common stock or New Charter common stock, we expect the transactions to qualify for tax-free treatment to you for U.S. federal income tax purposes. See “Material U.S. Federal Income Tax Consequences of the Spin-Off and the SpinCo Merger.”

Q: How will SpinCo’s common stock trade?

A: There is currently no public market for our Class A common stock. We anticipate that trading will commence on a “when issued” basis on or shortly prior to the record date for the spin-off. When-issued trading in the context of a spin-off refers to a sale or purchase of securities effected on or before the spin-off date and made conditionally because the securities of the spun-off entity have not yet been distributed. We expect “regular-way” trading of our Class A common stock to begin on the first trading day following the completion of the spin-off.

Q: Do I have appraisal rights?

A: No, holders of Comcast common stock do not have any appraisal rights in connection with the spin-off.

Q: Who is the transfer agent for SpinCo common stock?

A: is the transfer agent for our common stock.

Q: How does my ownership in Comcast change as a result of the transactions?

A: Your ownership of Comcast will not be impacted by the transactions.

Q: Will Comcast control SpinCo after consummation of the transactions?

A: No. Following consummation of the transactions, holders of Comcast common stock as of the record date will own approximately 67% of us, and New Charter will own the remaining approximately 33%. Comcast will have no remaining interest in us, and for the first eight years following consummation of the transactions, subject to certain limited exceptions, Comcast will be prohibited from owning more than one percent of our common stock.

This prospectus describes our business, our relationships with Comcast and Charter and the transactions and provides other information to assist you in evaluating the benefits and risks of holding or disposing of our common stock that you will receive in the spin-off. You should carefully consider the following risks and all of the other information set forth in this prospectus. If any of the following risks actually occurs, our business, financial condition or results of operations would likely suffer. The trading price of our common stock could decline due to any of these risks, and you may lose all or part of your investment.

This prospectus also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks faced by us described below and elsewhere in this prospectus. See “Cautionary Statement Regarding Forward-Looking Statements.”

Risks Related to Our Business

We currently face a wide range of competitors, and our business and results of operations could be adversely affected if we do not compete effectively.

We operate in an intensely competitive, consumer-driven and rapidly changing environment and compete with a growing number of companies that provide a broad range of communications products and services and entertainment, news and information content to consumers. Technological changes are further intensifying and complicating the competitive landscape and influencing consumer behavior, which is discussed in the risk factor immediately below, “—Newer technologies and services are driving changes in consumer behavior, which may increase the number of competitors we face and adversely affect our businesses.”

Competition for the cable services we offer consists primarily of direct broadcast satellite (“DBS”) providers, which have a national footprint and compete in all our service areas, and phone companies, which overlap approximately half of our service areas and are continuing to expand their fiber-based networks. We also compete with other providers of traditional cable services in some of the areas we serve and with satellite master antenna television (“SMATV”) systems. All of these companies typically offer features, pricing and packaging for services comparable to our cable services. Furthermore, some of our phone company competitors have their own wireless facilities and may expand their cable service offerings to include bundled wireless offerings, which may have an adverse impact on our competitive position, business and results of operations. Additionally, in May 2014, AT&T, our largest phone company competitor, announced its intention to acquire DirecTV, the nation’s largest DBS provider. If completed, this transaction will create an even larger competitor for our cable services that will have the ability to expand its cable service offerings to include bundled wireless offerings.

There continue to be new entrants, some with significant financial resources, that potentially may compete on a larger scale with our cable services. These new entrants include companies that offer services that enable Internet video streaming and downloading of video programming, some of which charge a nominal or no fee for access to their content. Additionally, Google has launched high-speed Internet and video services in a limited number of areas outside of our footprint, and some local municipalities are launching their own fiber-optic high-speed Internet services.

For a more detailed description of the competition facing our business, see “Business—Competition.” There can be no assurance that we will be able to compete effectively against existing or new competitors or that competition will not have an adverse effect on our business.

Newer technologies and services are driving changes in consumer behavior, which may increase the number of competitors we face and adversely affect our businesses.

Newer technologies and services, particularly alternative methods for the distribution, sale and viewing of content, have been, and will likely continue to be, developed that further increase the number of competitors that we face for our cable services. These technologies and services are also driving changes in consumer behavior as consumers seek more control over when, where and how they consume content and access communications services. While we will attempt to adapt to changing consumer behavior by adding additional video on demand content and offering some of that content and live programming online, newer services and technologies that may compete with our video services include digital distribution services and devices that offer Internet video streaming and downloading of movies, television shows and other video programming that can be viewed on television sets, computers, smartphones and tablets. Some of these services charge a nominal or no fee for access to their content, which could adversely affect demand for our video services, including for premium networks and our DVR and video on demand services. Newer services in wireless Internet technology, such as 4G wireless broadband services and Wi-Fi networks, and devices such as wireless data cards, tablets, smartphones and mobile wireless routers, may compete with our high-speed Internet services. Our voice services continue to face increased competition from wireless and Internet-based phone services as more people choose to replace their traditional wireline phone service with these phone services. The success of any of these ongoing and future developments or our failure to effectively anticipate or adapt to emerging technologies or changes in consumer behavior, including among younger consumers, could have an adverse effect on our competitive position, business and results of operations.

Our programming expenses may increase materially following the spin-off.

Prior to the spin-off, programming expenses for our video services were our largest single expense item, even with the benefit of lower rates obtained by Comcast due to its scale as being the nation’s largest cable operator. Following the spin-off, we will not receive the benefit of Comcast’s lower programming rates. We expect that we will obtain our programming primarily through Charter’s programming arrangements, as well as through some direct relationships with programmers. As a result, our programming expenses may increase materially due to the loss of benefits attributable to Comcast’s scale.

Programming expenses for our video services are increasing, which could adversely affect our businesses.

The multichannel video provider industry has experienced continued increases in the cost of programming, especially sports programming, which we expect will continue for the foreseeable future. Our programming expenses may also increase as we add programming to our video services or distribute existing programming to more of our customers or through additional delivery platforms, such as video on demand or online video applications. Additionally, in the past few years, we have begun paying certain local broadcast television stations in exchange for their required consent for the retransmission of broadcast network programming to our video services customers; we expect to continue to be subject to increasing demands for payment and other concessions from local broadcast television stations. If we are unable to raise our customers’ rates or offset programming cost increases through the sale of additional services, the increasing cost of programming could have an adverse impact on our results of operations. Moreover, as our contracts with content providers expire, there can be no assurance that they will be renewed on acceptable terms or that they will be renewed at all, in which case we may be unable to provide such content as part of our video services, and our businesses and results of operations could be adversely affected.

We face risks inherent in our commercial business.

We are focused on growing our commercial services business and expect to maintain or increase expenditures on technology, equipment and personnel focused on the commercial business. Commercial business customers often require service level agreements and generally have heightened customer expectations for reliability of services. If our efforts to build the infrastructure to scale the commercial business are not successful, the growth of our commercial services business would be limited. We depend on interconnection and related services provided by certain third parties for the growth of our commercial business. As a result, our ability to implement changes as the services grow may be limited. If we are unable to meet these service level requirements or expectations, our commercial business could be adversely affected.

Our business depends on keeping pace with technological developments.

Our success is, to a large extent, dependent on our ability to acquire, develop, adopt and leverage new and existing technologies, and our competitors’ use of certain types of technology and equipment may provide them with a competitive advantage. For example, some companies and municipalities are building advanced fiber-optic networks that provide very fast Internet access speeds, and wireless Internet technologies continue to evolve rapidly to allow for greater speed and reliability. We expect other advances in communications technology to occur in the future. If we choose technology or equipment that is not as effective or attractive to consumers as that employed by our competitors, if we fail to employ technologies desired by consumers before our competitors do so, or if we fail to execute effectively on our technology initiatives, our business and results of operations could be adversely affected. We also may incur increased costs if changes in the products and services that our competitors offer require that we offer certain of our existing services or enhancements at a lower or no cost to our customers or that we make additional research and development expenditures, which could have an adverse effect on our businesses.

We are subject to regulation by federal, state and local authorities, which may impose additional costs and restrictions on our businesses.

Federal, state and local governments extensively regulate the video services industry and may increase the regulation of the Internet service and Voice over Internet Protocol (“VoIP”) service industries. We expect that legislative enactments, court actions and regulatory proceedings will continue to clarify, and in some cases may adversely affect, the rights and obligations of cable operators and other entities under the Communications Act of 1934, as amended (the “Communications Act”), and other laws. Failure to comply with the laws and regulations applicable to our businesses could result in administrative enforcement actions, fines, and civil and criminal liability. For a more extensive discussion of the significant risks associated with the regulation of our business, see “Business—Legislation and Regulation.”

Changes to existing statutes, rules, regulations, or interpretations thereof, or adoption of new ones, could have an adverse effect on our business.

Legislators and regulators at all levels of government frequently consider changing, and sometimes do change, existing statutes, rules, regulations, or interpretations thereof, or prescribe new ones. Any future legislative, judicial, regulatory or administrative actions may increase our costs or impose additional restrictions on our businesses. For example, in 2014, the FCC launched a rulemaking to adopt new “open Internet” regulations applicable to broadband Internet service providers (“ISPs”) such as us. Among other things, the FCC has proposed requirements to enhance required disclosures regarding network management, performance and commercial terms of the service; bar broadband ISPs from blocking access to lawful content, applications, services or non-harmful devices; and bar wireline broadband ISPs such as us from discriminating in a commercially unreasonable manner in transmitting lawful network traffic. The FCC has also invited comment on proposals to reclassify broadband Internet service as a “telecommunications service,” which would subject it to traditional common carriage regulation under Title II of the Communications Act, potentially including rate regulation and a prohibition or restriction on arrangements between us and Internet content, application, and service providers, which could have a material adverse effect on our business and results of operations. The FCC is also considering the appropriate regulatory framework for VoIP service, including whether that service should be regulated under Title II. While we cannot predict what rules the FCC will adopt as part of these rulemakings, any changes to the regulatory framework for our high-speed Internet or VoIP services could have a negative impact on our business and results of operations.

Tax legislation and administrative initiatives or challenges to our tax positions could adversely affect our results of operations and financial condition.

We operate cable systems in locations across several states and, as a result, we are subject to the tax laws and regulations of federal, state and local governments. From time to time, various legislative and/or administrative initiatives may be proposed that could adversely affect our tax positions. There can be no assurance that our effective tax rate or tax payments will not be adversely affected by these initiatives. As a result of state and local budget shortfalls due primarily to the recession as well as other considerations, certain states and localities have imposed or are considering imposing new or additional taxes or fees on our services or changing the methodologies or base on which certain fees and taxes are computed. Such potential changes include additional taxes or fees on our services, which could impact our customers, combined reporting and other changes to general business taxes, central/unit-level assessment of property taxes and other matters that could increase our income, franchise, sales, use and/or property tax liabilities. In addition, federal, state and local tax laws and regulations are extremely complex and subject to varying interpretations. There can be no assurance that our tax positions will not be challenged by relevant tax authorities or that we would be successful in any such challenge.

A decline in advertising expenditures or changes in advertising markets could negatively impact our businesses.

A decline in advertising expenditures could negatively impact our results of operations. Declines can be caused by the economic prospects of specific advertisers or industries, by increased competition for the leisure time of audiences and audience fragmentation, by the growing use of new technologies, or by the economy in general, any of which may cause advertisers to alter their spending priorities based on these or other factors. Further, natural disasters, wars, acts of terrorism, or other significant adverse news events could lead to a reduction in advertising expenditures as a result of uninterrupted news coverage and general economic uncertainty.

We rely on network and information systems, properties and other technologies, and a disruption, cyber attack, failure or destruction of such networks, systems, properties or technologies may disrupt or have an adverse effect on our business.

Network and information systems and other technologies, including those related to our network management and customer service operations, are critical to our business activities. Network and information systems-related events, including those caused by us or by third parties, such as computer hackings, cyber attacks, computer viruses, worms or other destructive or disruptive software, process breakdowns, denial of service attacks, malicious social engineering or other malicious activities, or any combination of the foregoing, or power outages, natural disasters, terrorist attacks or other similar events, could result in a degradation or disruption of our services, excessive call volume to call centers or damage to our properties, equipment and data. These events also could result in large expenditures to repair or replace the damaged properties, networks or information systems or to protect them from similar events in the future.

In addition, we may obtain certain confidential, proprietary and personal information about our customers, personnel and vendors, and may provide this information to third parties, in connection with our business. While we obtain assurances that these third parties will protect this information, there is a risk that this information may be compromised. Any security breaches, such as misappropriation, misuse, leakage, falsification or accidental release or loss of information maintained in our information technology systems, including customer, personnel and vendor data, could damage our reputation and require us to expend significant capital and other resources to remedy any such security breach, and could cause regulators to impose fines or other remedies for failure to comply with relevant customer privacy rules.

The risk of these systems-related events and security breaches occurring continues to intensify in many lines of business, and our line of business may be at a disproportionately heightened risk of these events occurring, due to the nature of our business and the fact that we maintain certain information necessary to conduct our business in digital form stored on cloud servers. In the ordinary course of our business, there are frequent attempts to cause such systems-related events and security breaches, and we have experienced a few minor systems-related events that, to date, have not resulted in any significant degradation or disruption to our network or information systems or our services or operations. While Comcast developed and maintained systems seeking to prevent systems-related events and security breaches from occurring, we will be transitioning from Comcast’s systems following the spin-off. Additionally, the development and maintenance of these systems is costly and requires ongoing monitoring and updating as technologies change and efforts to overcome security measures become more sophisticated. Despite any efforts to prevent these events and security breaches, there can be no assurance that they will not occur in the future or will not have an adverse effect on our business. Moreover, the amount and scope of insurance we maintain against losses resulting from any such events or security breaches may not be sufficient to cover our losses or otherwise adequately compensate us for any disruptions to our business that may result, and the occurrence of any such events or security breaches could have an adverse effect on our business.

Weak economic conditions may have a negative impact on our business.

A substantial portion of our revenue comes from customers whose spending patterns may be affected by prevailing economic conditions. Weak economic conditions, including unemployment and a weak housing market, or increases in price levels generally due to inflationary pressures, could adversely affect demand for any of our products and services and have a negative impact on our results of operations. For example, customers may reduce the level of cable services to which they subscribe, or may discontinue subscribing to one or more of our cable services. This risk may be increased by the expanded availability of free or lower cost competitive services, such as Internet video streaming and downloading services, or substitute services for our high-speed Internet and phone services, such as mobile phones, smartphones and Wi-Fi networks. Weak economic conditions also may have a negative impact on our advertising revenue. Additionally, because we have concentrations of customers in the Detroit, St. Paul-Minneapolis and Indianapolis designated market areas (“DMAs”), any disproportionate economic weakness in those DMAs as compared to the nation as a whole could have an adverse effect on our business. Weak economic conditions and turmoil in the global financial markets may also impair the ability of third parties to satisfy their obligations to us. Further, any disruption in the global financial markets may affect our ability to obtain financing on acceptable terms. If economic conditions deteriorate, our businesses may be adversely affected.

We may be unable to obtain necessary hardware, software and operational support.

We depend on vendors to supply us with a significant amount of the hardware, software and operational support necessary to provide certain of our services. Some of these vendors represent our primary source of supply or grant us the right to incorporate their intellectual property into some of our hardware and software products. If any of these vendors experience operating or financial difficulties, if our demand exceeds their capacity or if they are otherwise unable to meet our specifications or provide the equipment or services we need in a timely manner or at reasonable prices, our ability to provide some services may be adversely affected.

We may be unable to maintain intellectual property protection for our products and services.

We depend on patent, copyright, trademark and trade secret laws and licenses to establish and maintain our intellectual property rights in technology and the products and services used in our operating activities. Any of our intellectual property rights could be challenged or invalidated, or such intellectual property rights may not be sufficient to permit us to continue to use certain intellectual property, which could result in discontinuance of certain product or service offerings or other competitive harm, our incurring substantial monetary liability or being enjoined preliminarily or permanently from further use of the intellectual property in question. The occurrence of any such event could have an adverse effect on our business.

Our cable system franchises are subject to non-renewal or termination. The failure to renew a franchise in one or more key markets could adversely affect our business.

Our cable systems generally operate pursuant to franchises, permits and similar authorizations issued by a state or local governmental authority controlling public rights-of-way. Many franchises establish comprehensive facilities and service requirements, as well as specific customer service standards and monetary penalties for noncompliance. In many cases, franchises are terminable if the franchisee fails to comply with significant provisions set forth in the franchise agreement governing system operations. Franchises are generally granted for fixed terms and must be periodically renewed. Franchising authorities may resist granting a renewal if either past performance or the prospective operating proposal is considered inadequate. Franchise authorities often demand concessions or other commitments as a condition to renewal. In some instances, local franchises have not been renewed at expiration, and we have operated and are operating under either temporary operating agreements or without a franchise while negotiating renewal terms with the local franchising authorities.

The traditional cable franchising regime has recently undergone significant change as a result of various federal and state actions. Some state franchising laws do not allow us to immediately opt into favorable statewide franchising. In many cases, state franchising laws will result in fewer franchise imposed requirements for our competitors who are new entrants than for us, until we are able to opt into the applicable state franchise.

We cannot assure you that we will be able to comply with all significant provisions of our franchise agreements and certain of our franchisers have from time to time alleged that we have not complied with these agreements. Additionally, we cannot assure you that we will be able to renew, or to renew as favorably, our franchises in the future. A termination of or a sustained failure to renew a franchise in one or more key markets could adversely affect our business in the affected geographic area.

The effect of changes to healthcare laws in the United States may increase the number of employees who choose to participate in our healthcare plans, which may significantly increase our healthcare costs and negatively impact our financial results.

In 2010, the Patient Protection and Affordable Care Act was signed into law in the United States to require health care coverage for many uninsured individuals and expand coverage to those already insured. The healthcare reform law will require us to offer healthcare benefits to all full-time employees (including full-time hourly employees) that meet certain minimum requirements of coverage and affordability, or face penalties. If we elect to offer such benefits we may incur substantial additional expense. If we fail to offer such benefits, or the benefits we elect to offer do not meet the applicable requirements, we may incur penalties. The healthcare reform law also requires individuals to obtain coverage or face individual penalties, so employees who are currently eligible but elect not to participate in our healthcare plans may find it more advantageous to do so when such individual mandates take effect. It is also possible that by making changes or failing to make changes in the healthcare plans offered by us we will become less competitive in the market for our labor. Finally, implementing the requirements of healthcare reform is likely to impose additional administrative costs. The costs and other effects of these new healthcare requirements cannot be determined with certainty, but they may significantly increase our healthcare coverage costs and could materially adversely affect our business, financial condition and results of operations.

Risks Related to the Transactions

We have no operating history as a separate company and may be unable to maintain our operating results at historical levels after becoming a stand-alone company.

We have no operating history as a separate, stand-alone company. We cannot assure you that as a separate company, our operating results will continue at historic levels. Prior to the transactions, we, as part of Comcast, the nation’s largest cable operator, were able to procure products and services on favorable terms. As a stand-alone company, we may not be able to obtain the same favorable terms and could incur additional costs to obtain the same products and services. Additionally, as a stand-alone company, we will incur additional costs to make investments to replicate or outsource certain systems, infrastructure, and functional expertise that are currently provided by Comcast. In connection with the transactions, we will enter into a services agreement with Charter pursuant to which Charter will provide certain services to us with respect to certain of our systems, including but not limited to corporate, network operations, engineering and IT, voice operations, field operations support services, customer services, billing and collections, product services, marketing services, sales, business intelligence and intellectual property licensing (the “Charter services agreement”). The Charter services agreement will require us to pay Charter the actual, economic costs of providing services to us and to reimburse Charter for out-of-pocket costs incurred in providing the services. In addition, in consideration for certain rights, including the rights to purchase goods and services, and the rights to obtain programming services, under Charter’s third party procurement and programming agreements, we will pay Charter a quarterly service charge of 4.25% of our quarterly gross revenues. The Charter services agreement will have an initial term of three years, automatically renewable for one-year terms unless either party gives notice of non-renewal at least one year prior to the end of the initial, or any renewal, term. The Charter services agreement will also be terminable by either party for customary for-cause events and in certain other circumstances. See “Arrangements Among Us, Comcast and Charter.” We cannot assure you that if the services agreement is terminated, we will be able to enter into other agreements on terms favorable or acceptable to us. Any additional or increased costs we incur to maintain our systems, infrastructure and functional expertise may have a material adverse effect on our business.

Historically, our business has been operated as part of Comcast’s cable communications business, and Comcast has performed many corporate functions for our operations, including managing financial and human resources systems, internal auditing, investor relations, treasury services, select accounting functions, finance and tax administration, benefits administration, legal, governmental relations and regulatory functions. Following the transactions, Comcast will provide support to us with respect to certain of these functions for periods specified in the transition services agreement and various other agreements, as discussed further under the section entitled “Arrangements Among Us, Comcast and Charter.” However, we will need to replicate certain systems, infrastructure and personnel to which we will no longer have access after the separation from Comcast, and the costs of such activities may exceed the costs we have historically incurred or that we will pay to Comcast during the transition period.

As a stand-alone company, we expect to expend additional time and resources to comply with rules and regulations that do not currently apply to us.

Currently, we are not directly subject to the reporting and other requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Following the effectiveness of the registration statement of which this prospectus forms a part, we will be directly subject to such reporting and other obligations under the Exchange Act, and we expect to be compliant with the applicable requirements of Section 404 of the Sarbanes-Oxley Act of 2002, which will require, in the future, annual management assessments of the effectiveness of our internal control over financial reporting and a report by our independent registered public accounting firm addressing the effectiveness of these controls. These reporting and other obligations will place significant demands on our management and our administrative and operational resources, including accounting resources.

Our historical and pro forma financial information may not be indicative of our future results as a separate company.

The historical and pro forma financial information we have included in this prospectus may not reflect what our results of operations, financial position and cash flows would have been had we been a separate company during the periods presented or be indicative of what our results of operations, financial position, and cash flows may be in the future when we are a separate company. Our historical financial information reflects allocations for services historically provided by Comcast, and we expect these allocated costs to be different from the actual costs we will incur for these services in the future as a separate company. In some instances, the costs incurred for these services as a separate company may be higher than the share of total Comcast expenses allocated to our business historically. For example, as a separate company, we expect our programming expenses will increase materially due to the loss of benefits attributable to Comcast’s scale.

The historical financial information does not reflect the increased costs associated with being a stand-alone company, including changes that we expect in our cost structure, personnel needs, financing, and operations of our business as a result of the transactions.

In addition, the pro forma financial information we have included in this prospectus is based in part upon a number of estimates and assumptions. These estimates and assumptions may prove not to be accurate, and accordingly, our pro forma financial information should not be assumed to be indicative of what our financial condition or results of operations actually would have been as a separate company and may not be a reliable indicator of what our financial condition or results of operations actually may be in the future.

For additional information about our past financial performance and the basis of presentation of our financial statements, see “Selected Historical Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our combined financial statements and related notes.

The combined post-distribution value of Comcast, our and New Charter shares of common stock may not equal or exceed the pre-distribution value of Comcast shares of common stock.

After the transactions, we expect that Comcast Class A and Class A Special common stock will continue to be traded on the NASDAQ Global Select Market. We have applied to list our Class A common stock on the NASDAQ Global Select Market, and New Charter common stock is expected to be listed on the NASDAQ Global Select Market. We cannot assure you that the combined trading prices of Comcast Class A or Class A Special common stock, as applicable, and our Class A common stock and New Charter common stock that is issued to holders of Comcast common stock after the transactions, as adjusted for any changes in the combined capitalization of the companies, will be equal to or greater than the applicable trading price of Comcast Class A or Class A Special common stock prior to the transactions. Until the market has fully evaluated the business of Comcast without our business and potentially thereafter, the prices at which Comcast Class A and Class A Special common stock trade may fluctuate significantly. Similarly, until the market has fully evaluated our business and the business of New Charter and potentially thereafter, the prices at which our Class A common stock and New Charter common stock trade may fluctuate significantly.

The transactions are subject to certain conditions, and therefore the transactions may not be consummated on the terms or timeline currently contemplated.

The consummation of the transactions is subject to a number of closing conditions, including, among others, completion of the merger between Comcast and TWC, the receipt of certain regulatory approvals, approval by Charter’s stockholders and certain conditions relating to the financing for the transactions. On October 8, 2014, the shareholders of Comcast approved the issuance of Comcast Class A common stock to TWC stockholders in the Comcast/TWC merger. On October 9, 2014, TWC stockholders approved the adoption of the Comcast/TWC merger agreement. Comcast and Charter may be unable to obtain the necessary approvals or otherwise satisfy the conditions required to consummate the transactions on a timely basis or at all. If Comcast is unable to consummate the transactions, Comcast may be required to pursue an alternative transaction to divest subscribers on terms which differ from the terms of the transactions, and there is no assurance as to when any such alternate disposition transaction would be consummated.

After the transactions, certain members of management, directors and stockholders may face actual or potential conflicts of interest.

After the transactions, our management and directors and the management and directors of Comcast and New Charter may own our Class A common stock, as well as common stock in Comcast and New Charter. This ownership overlap could create, or appear to create, potential conflicts of interest when our management and directors and New Charter’s management and directors face decisions that could have different implications for us and New Charter. For example, potential conflicts of interest could arise in connection with the resolution of any dispute among us, Comcast and New Charter regarding the terms of the agreements governing the transactions and our relationships with Comcast and New Charter thereafter. See “Arrangements Among Us, Comcast and Charter.” Potential conflicts of interest may also arise out of any commercial arrangements that we, Comcast or New Charter may enter into in the future.

In addition, although we and Charter will operate independently of one another and more than a majority of our directors will be independent under applicable stock exchange and SEC rules, our board of directors and the board of directors of Charter will have members in common after the transactions. The overlap of our board with the board of directors of Charter could create actual or potential conflicts of interest.

The indemnification arrangements we entered into with Comcast in connection with the transactions may require us to divert cash to satisfy indemnification obligations to Comcast. In addition, Comcast’s indemnity to us may not be sufficient to insure us against the full amount of liabilities for which it will be allocated responsibility, and Comcast may not be able to satisfy its indemnification obligations to us in the future.