Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - EDGEWATER TECHNOLOGY INC/DE/ | Financial_Report.xls |

| EX-32 - EX-32 - EDGEWATER TECHNOLOGY INC/DE/ | d802834dex32.htm |

| EX-31.1 - EX-31.1 - EDGEWATER TECHNOLOGY INC/DE/ | d802834dex311.htm |

| EX-31.2 - EX-31.2 - EDGEWATER TECHNOLOGY INC/DE/ | d802834dex312.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | Quarterly report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 |

For the quarterly period ended September 30, 2014

or

| ¨ | Transition report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 |

for the transition period from to

Commission file number: 000-20971

EDGEWATER TECHNOLOGY, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 71-0788538 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

| 200 Harvard Mill Square, Suite 210 Wakefield, MA |

01880-3209 | |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code: (781) 246-3343

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ | Smaller reporting company | x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The number of shares of Common Stock of the Registrant, par value $.01 per share, outstanding at October 27, 2014 was 11,377,331.

Table of Contents

EDGEWATER TECHNOLOGY, INC.

FORM 10-Q FOR THE QUARTER ENDED SEPTEMBER 30, 2014

2

Table of Contents

PART I – FINANCIAL INFORMATION

| ITEM 1. | FINANCIAL STATEMENTS |

UNAUDITED CONDENSED CONSOLIDATED BALANCE SHEETS

(In Thousands, Except Per Share Data)

| September 30, 2014 |

December 31, 2013 |

|||||||

| ASSETS | ||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 25,816 | $ | 20,321 | ||||

| Accounts receivable, net of allowance of $150 |

24,075 | 19,842 | ||||||

| Deferred tax assets, net |

1,148 | 1,175 | ||||||

| Prepaid expenses and other current assets |

1,449 | 936 | ||||||

|

|

|

|

|

|||||

| Total current assets |

52,488 | 42,274 | ||||||

| Property and equipment, net |

1,142 | 1,437 | ||||||

| Intangible assets, net |

570 | 956 | ||||||

| Goodwill |

12,049 | 12,049 | ||||||

| Deferred tax assets, net |

26,965 | 29,097 | ||||||

| Other assets |

212 | 254 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 93,426 | $ | 86,067 | ||||

|

|

|

|

|

|||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 148 | $ | 680 | ||||

| Accrued liabilities |

17,366 | 14,326 | ||||||

| Deferred revenue |

1,672 | 1,715 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

19,186 | 16,721 | ||||||

| Other liabilities |

557 | 760 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

19,743 | 17,481 | ||||||

| Stockholders’ equity: |

||||||||

| Preferred stock, $.01 par value; 2,000 shares authorized, no shares issued or outstanding |

— | — | ||||||

| Common stock, $.01 par value; 48,000 shares authorized, 29,736 shares issued as of September 30, 2014 and December 31, 2013, 11,353 and 11,049 shares outstanding as of September 30, 2014 and December 31, 2013, respectively |

297 | 297 | ||||||

| Paid-in capital |

210,944 | 211,852 | ||||||

| Treasury stock, at cost, 18,383 and 18,687 shares at September 30, 2014 and December 31, 2013, respectively |

(120,576 | ) | (123,186 | ) | ||||

| Accumulated other comprehensive loss |

(168 | ) | (154 | ) | ||||

| Retained deficit |

(16,814 | ) | (20,223 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

73,683 | 68,586 | ||||||

|

|

|

|

|

|||||

| Total liabilities and stockholders’ equity |

$ | 93,426 | $ | 86,067 | ||||

|

|

|

|

|

|||||

See notes to the unaudited condensed consolidated financial statements.

3

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(In Thousands, Except Per Share Data)

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Revenue: |

||||||||||||||||

| Service revenue |

$ | 25,144 | $ | 21,389 | $ | 73,140 | $ | 62,684 | ||||||||

| Software revenue |

1,365 | 2,260 | 5,920 | 8,568 | ||||||||||||

| Reimbursable expenses |

2,220 | 1,750 | 6,505 | 5,523 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenue |

28,729 | 25,399 | 85,565 | 76,775 | ||||||||||||

| Cost of revenue: |

||||||||||||||||

| Project and personnel costs |

15,169 | 13,071 | 44,106 | 39,837 | ||||||||||||

| Software costs |

924 | 921 | 3,545 | 4,577 | ||||||||||||

| Reimbursable expenses |

2,220 | 1,750 | 6,505 | 5,523 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total cost of revenue |

18,313 | 15,742 | 54,156 | 49,937 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross profit |

10,416 | 9,657 | 31,409 | 26,838 | ||||||||||||

| Operating expenses: |

||||||||||||||||

| Selling, general and administrative |

8,353 | 7,590 | 24,431 | 23,231 | ||||||||||||

| Depreciation and amortization |

227 | 302 | 702 | 925 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total operating expenses |

8,580 | 7,892 | 25,133 | 24,156 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

1,836 | 1,765 | 6,276 | 2,682 | ||||||||||||

| Other expense (income), net |

146 | (81 | ) | 147 | 92 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before income taxes |

1,690 | 1,846 | 6,129 | 2,590 | ||||||||||||

| Tax provision |

714 | 74 | 2,721 | 293 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

$ | 976 | $ | 1,772 | $ | 3,408 | $ | 2,297 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Comprehensive income: |

||||||||||||||||

| Currency translation adjustments |

(35 | ) | (2 | ) | (14 | ) | (23 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total comprehensive income |

$ | 941 | $ | 1,770 | $ | 3,394 | $ | 2,274 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income per share: |

||||||||||||||||

| Basic net income per share of common stock |

$ | 0.09 | $ | 0.17 | $ | 0.31 | $ | 0.21 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted net income per share of common stock |

$ | 0.08 | $ | 0.14 | $ | 0.26 | $ | 0.19 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Shares used in computing basic net income per share of common stock |

11,197 | 10,732 | 11,092 | 10,800 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Shares used in computing diluted net income per share of common stock |

12,972 | 12,233 | 12,973 | 11,785 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

See notes to the unaudited condensed consolidated financial statements.

4

Table of Contents

UNAUDITED CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(In Thousands)

| Nine Months Ended September 30, |

||||||||

| 2014 | 2013 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: |

||||||||

| Net income |

$ | 3,408 | $ | 2,297 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

862 | 1,183 | ||||||

| Share-based compensation expense |

1,181 | 1,174 | ||||||

| Deferred income taxes |

2,159 | 25 | ||||||

| Lease abandonment |

(400 | ) | — | |||||

| Excess tax benefit from stock options |

206 | — | ||||||

| Changes in operating accounts: |

||||||||

| Accounts receivable |

(4,219 | ) | (749 | ) | ||||

| Prepaid expenses and other current assets |

(471 | ) | 262 | |||||

| Accounts payable |

(532 | ) | 5 | |||||

| Accrued liabilities and other liabilities |

3,237 | (371 | ) | |||||

| Deferred revenue |

(43 | ) | (1,507 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

5,388 | 2,319 | ||||||

|

|

|

|

|

|||||

| CASH FLOWS FROM INVESTING ACTIVITIES: |

||||||||

| Acquisition of intellectual property |

— | (200 | ) | |||||

| Capitalization of product development costs |

— | (289 | ) | |||||

| Purchases of property and equipment |

(183 | ) | (280 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(183 | ) | (769 | ) | ||||

|

|

|

|

|

|||||

| CASH FLOW FROM FINANCING ACTIVITIES: |

||||||||

| Purchases of treasury stock |

(962 | ) | (1,513 | ) | ||||

| Excess tax benefit from stock options |

(206 | ) | — | |||||

| Proceeds from employee stock plans and stock option exercises |

1,483 | 793 | ||||||

|

|

|

|

|

|||||

| Net cash provided by (used in) financing activities |

315 | (720 | ) | |||||

|

|

|

|

|

|||||

| Effects of exchange rates on cash |

(25 | ) | 6 | |||||

|

|

|

|

|

|||||

| Net increase in cash and cash equivalents |

5,495 | 836 | ||||||

| CASH AND CASH EQUIVALENTS, beginning of period |

20,321 | 16,651 | ||||||

|

|

|

|

|

|||||

| CASH AND CASH EQUIVALENTS, end of period |

$ | 25,816 | $ | 17,487 | ||||

|

|

|

|

|

|||||

| SUPPLEMENTAL DISCLOSURES OF CASH FLOW INFORMATION: |

||||||||

| Cash paid for income taxes |

$ | 539 | $ | 184 | ||||

|

|

|

|

|

|||||

| Issuance of restricted stock awards |

$ | 678 | $ | 1,051 | ||||

|

|

|

|

|

|||||

See notes to the unaudited condensed consolidated financial statements.

5

Table of Contents

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 1. | ORGANIZATION: |

Edgewater Technology, Inc. (“Edgewater”, the “Company”, “we”, or “our”) is a strategic consulting firm that brings a synergistic blend of classic consulting and product-based consulting services to its customer base. Headquartered in Wakefield, Massachusetts, we typically go to market both vertically by industry and horizontally by product/technology specialties and provide our customers with a wide range of business and technology offerings. We work with customers, primarily within North America, to reduce costs, improve process and increase revenue through the judicious use of technology.

In this Quarterly Report on Form 10-Q (the “Form 10-Q”), we use the terms “Edgewater,” “Edgewater Technology,” “we,” “our Company,” “the Company,” “our” and “us” to refer to Edgewater Technology, Inc. and its wholly-owned subsidiaries, which are described in our 2013 Annual Report on Form 10-K, as filed with the Securities and Exchange Commission (the “SEC”) on March 10, 2014 (the “2013 Form 10-K”).

| 2. | BASIS OF PRESENTATION: |

The accompanying unaudited condensed consolidated financial statements have been prepared by Edgewater pursuant to the rules and regulations of the SEC regarding interim financial reporting. Certain information and note disclosures normally included in annual financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been omitted pursuant to those rules and regulations, although we believe that the disclosures made are adequate to ensure the information presented is not misleading.

The accompanying unaudited condensed consolidated financial statements reflect all adjustments (which were of a normal, recurring nature) that, in the opinion of management, are necessary to present fairly our financial position, results of operations and cash flows as of and for the interim periods presented. All intercompany transactions have been eliminated in the accompanying unaudited condensed consolidated financial statements. These financial statements should be read in conjunction with the audited financial statements and notes thereto included in our 2013 Form 10-K.

The results of operations for the three and nine months ended September 30, 2014 are not necessarily indicative of the results to be expected for any future period or the full fiscal year. Our revenue and earnings may fluctuate from quarter-to-quarter based on factors within and outside our control, including variability in demand for information technology professional services, the length of the sales cycle associated with our service offerings, the number, size and scope of our projects and the efficiency with which we utilize our employees. Substantially all of our revenue is generated within North America.

Other comprehensive income consists of net income plus or minus any periodic currency translation adjustments.

| 3. | REVENUE RECOGNITION: |

Our Company recognizes revenue primarily through the provision of consulting services and the resale of third-party, off-the-shelf software and maintenance.

We generate revenue by providing consulting services under written service contracts with our customers. The service contracts we enter into generally fall into three specific categories: time and materials, fixed-price and retainer.

We consider amounts to be earned once evidence of an arrangement has been obtained, services are delivered, fees are fixed or determinable and collectability is reasonably assured. We establish billing terms at the time at which the project deliverables and milestones are agreed. Our standard payment terms are 30 days from invoice date. Out-of-pocket reimbursable expenses charged to customers are reflected as revenue.

When a customer enters into a time and materials, fixed-price or a periodic retainer-based contract, the Company recognizes revenue in accordance with its evaluation of the deliverables in each contract. If the deliverables represent separate units of accounting, the Company then measures and allocates the consideration from the arrangement to the separate units, based on vendor specific objective evidence (“VSOE”) of the value for each deliverable.

The revenue under time and materials contracts is recognized as services are rendered and performed at contractually agreed upon rates. Revenue pursuant to fixed-price contracts is recognized under the proportional performance method of accounting. We routinely evaluate whether revenue and profitability should be recognized in the current period. We estimate the proportional performance on our fixed-price contracts on a monthly basis utilizing hours incurred to date as a percentage

6

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 3. | REVENUE RECOGNITION: (Continued) |

of total estimated hours to complete the project. This method is used because reasonably dependable estimates of costs and revenue earned can be made, based on historical experience and milestones identified in any particular contract. If we do not have a sufficient basis to measure progress toward completion, revenue is recognized upon completion of performance, subject to any warranty provisions or other project management assessments as to the status of work performed.

Estimates of total project costs are continuously monitored during the term of an engagement. There are situations where the number of hours to complete projects may exceed our original estimate, as a result of an increase in project scope, unforeseen events that arise, or the inability of the client or the delivery team to fulfill their responsibilities. Accordingly, recorded revenues and costs are subject to revision throughout the life of a project based on current information and historical trends. Such revisions may result in increases or decreases to revenue and income and are reflected in the consolidated financial statements in the periods in which they are first identified.

If our initial estimates of the resources required or the scope of work to be performed on a contract are inaccurate, or we do not manage the project properly within the planned time period, a provision for estimated losses on incomplete projects is made. Any known or probable losses on projects are charged to operations in the period in which such losses are determined. A formal project review process takes place quarterly, although projects are continuously evaluated throughout the period. Management reviews the estimated total direct costs on each contract to determine if the estimated amounts are accurate, and estimates are adjusted as needed in the period identified. No losses were recognized on contracts during the three- or nine-month periods ended September 30, 2014 or 2013.

We also perform services on a periodic retainer basis under infrastructure service contracts, which include monthly hosting and support services. Revenue under periodic retainer-based contracts is recognized ratably over the contract period, as outlined within the respective contract. In the event additional services are required, above the minimum retained or contracted amount, then such services are billed on a time and materials basis.

Typically, the Company provides warranty services on its fixed-price contracts related to providing customers with the ability to have any “design flaws” remedied and/or have our Company “fix” routine defects. The warranty services, as outlined in the respective contracts, are provided for a specific period of time after a project is complete. The Company values the warranty services based upon historical labor hours incurred for similar services at standard billing rates. Revenue related to the warranty provisions within our fixed-price contracts is recognized as the services are performed or the revenue is earned. The warranty period is typically for a 30-60 day period after the project is complete.

Customer prepayments, even if nonrefundable, are deferred (classified as deferred revenue on the condensed consolidated balance sheets) and recognized over future periods as services are performed.

Software revenue represents the resale of certain third-party off-the-shelf software and maintenance and is recorded on a gross basis provided we act as a principal in the transaction, which we have determined based upon several factors, including, but not limited to, the fact that we have credit risk and we set the price to the end user. In the event we do not meet the requirements to be considered a principal in the software sale transaction and act as an agent, software revenue is recorded on a net basis.

Prior to the second quarter of 2013, we recorded substantially all of our software resale revenue on a gross basis (reporting the revenue and cost from the transaction in our consolidated statement of comprehensive income). However, beginning in the second quarter of 2013, due to changes in the nature of the terms of certain Microsoft Dynamics AX software resale arrangements (primarily related to the risk of credit loss and ability to establish pricing), we began to recognize a portion of our software resale revenue on a net basis (reporting only the net profit from the transaction as revenue in our consolidated statement of comprehensive income). We expect this trend to continue and also anticipate that the number of new software resale arrangements subject to these terms may increase in future periods. Additionally, the changes in the terms of the resale arrangements may, in certain situations, extend the timing of the recognition period (from full, immediate recognition of the gross margin on the transaction to recognition of the gross margin on the transaction over a three-year period) due to payment terms being spread over a multiple year period. This would reduce the amount of the software revenue and associated gross margin to be recognized by the Company in the initial period of the sale.

7

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 3. | REVENUE RECOGNITION: (Continued) |

The majority of the software sold by the Company is delivered electronically. For software that is delivered electronically, we consider delivery to have occurred when the customer either (a) takes possession of the software via a download (that is, when the customer takes possession of the electronic data on its hardware), or (b) has been provided with access codes that allow the customer to take immediate possession of the software on its hardware pursuant to an agreement or purchase order for the software.

The Company enters into multiple element arrangements which typically include software, post-contract support (or maintenance), and consulting services. Consistent with the software described above, maintenance that is in the form of a pass through transaction is recognized upon delivery of the software, as all related warranty and maintenance is performed by the primary software vendor and not the Company. Maintenance fee revenue for the Company’s software products, which is inconsequential in all years presented, is recognized ratably over the term of the arrangements, which are generally for a one-year period. The Company has established VSOE with respect to the services and maintenance provided based on the price charged when the services are sold separately and the stated renewal rate.

A significant amount of our 2013 software revenue is associated with the recognition of PI2 license revenue. In June 2012, Microsoft purchased the Company’s internally developed PI2 software and intellectual property (the “PI2 Solution”) for an aggregate purchase price of $3.25 million. The sale of the PI2 Solution was a significant multiple element contract. This contract included $3.25 million of license consideration and subsequent development and training services. At the time of the sale, we determined that the license did not have stand-alone value without the services, and accordingly we accounted for the license and related services as one unit. The Company recognized $614 thousand and $2.0 million in PI2 license revenue in the three- and nine-month periods ended September 30, 2013, respectively. No PI2-related revenue was recognized in the three or nine months ended September 30, 2014.

| 4. | SHARE-BASED COMPENSATION: |

Share-based compensation expense under all of the Company’s share-based plans was $369 thousand and $1.2 million for the three- and nine-month periods ended September 30, 2014, respectively. Share-based compensation expense under all of the Company’s share-based plans was $336 thousand and $1.2 million for the three- and nine-month periods ended September 30, 2013, respectively.

Cash received from the employee stock purchase plan (“ESPP”) and through stock option exercises was $656 thousand and $1.5 million during the three- and nine-month periods ended September 30, 2014, respectively. Cash received from ESPP and stock option exercises was $377 thousand and $793 thousand during the three- and nine-month periods ended September 30, 2013, respectively.

As of September 30, 2014, unrecognized compensation expense, net of estimated forfeitures, related to the unvested portion of all share-based compensation arrangements was approximately $1.9 million and is expected to be recognized over a weighted-average period of 1.3 years.

The Company intends to use previously purchased treasury shares for shares issued for options, restricted share awards and ESPP purchases. Shares may also be issued from authorized but unissued share reserves.

8

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 5. | INCOME TAXES: |

The Company recorded a tax provision of $714 thousand and $2.7 million for the three- and nine-month periods ended September 30, 2014, respectively. The reported tax expense for the three- and nine-month periods ended September 30, 2014 is based upon an estimated annual effective tax rate of 42.2% and 44.4%, respectively, related to our combined federal and state income tax rates, foreign income tax provisions, the recognition of U.S. deferred tax liabilities for differences between the book and tax basis of goodwill and other discrete items. The Company recorded a tax provision of $74 thousand and $293 thousand for the three- and nine-month periods ended September 30, 2013, respectively. The reported tax expense for the three- and nine-month periods ended September 30, 2013 is based upon an estimated annual effective tax rate of 4.0% and 11.3%, respectively.

The reported estimated annual effective tax rate for the three- and nine-month periods ended September 30, 2013 is lower than the statutory rate due to a full valuation allowance being provided against our deferred tax assets, which includes significant federal net operating loss carryforwards.

We assess the realizability of our deferred tax assets and assess the need for a valuation allowance on an ongoing basis. The periodic assessment of the net carrying value of our deferred tax assets under the applicable accounting rules is highly judgmental. We are required to consider all available positive and negative evidence in evaluating the likelihood that we will be able to realize the benefit of our deferred tax assets in the future. Such evidence includes scheduled reversals of deferred tax liabilities, projected future taxable income, tax planning strategies and the results of recent operations. Since this evaluation requires consideration of events that may occur some years into the future, there is significant judgment involved, and our conclusion could be materially different should certain of our expectations not transpire.

When assessing all available evidence, we consider the extent to which we have generated pre-tax income or losses over the most recent three-year period to be an important piece of objective evidence. During the year ended December 31, 2013, we emerged from a cumulative three year pre-tax loss position, which removed this important piece of negative evidence from our evaluation. As a result, we concluded the asset was realizable and we reversed $36.2 million of the previously established deferred tax asset valuation allowance.

Our policy is to classify interest and penalties related to unrecognized tax benefits as income tax expense. This policy has been consistently applied in all periods. During the three- and nine-month periods ended September 30, 2014, we recognized, as a part of income tax expense, $20 thousand and $60 thousand, respectively, in interest and penalties related to our unrecognized tax benefits. During the three- and nine-month periods ended September 30, 2013, we reduced income tax expense by $(88) thousand and $(45) thousand, respectively, from the reversal of previously recorded unrecognized state income tax-related tax benefits (and associated penalties and interest) as a result of the expiration of certain statutes of limitations.

We have reviewed the tax positions taken, or to be taken, in our tax returns for all tax years currently open to examination by a taxing authority. As of September 30, 2014, the gross amount of unrecognized tax benefits, exclusive of interest and penalties, was $108 thousand. We have identified no other uncertain tax positions for which it is reasonably possible that the total amount of unrecognized tax benefits will significantly increase or decrease within the twelve months ending September 30, 2015. We remain subject to examination until the statute of limitations expires for each respective tax jurisdiction.

| 6. | FAIR VALUE MEASUREMENT: |

We utilize the following valuation hierarchy for disclosure of the inputs to valuation used to measure fair value. This hierarchy prioritizes the inputs into three broad levels as follows:

| • | Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities. |

| • | Level 2 inputs are quoted prices for similar assets and liabilities in active markets or inputs that are observable for the asset or liability, either directly or indirectly through market corroboration, for substantially the full term of the financial instrument. |

| • | Level 3 inputs are unobservable inputs based on our own assumptions used to measure assets and liabilities at fair value. |

Classification of financial assets and liabilities within the hierarchy is determined based upon the lowest level input that is significant to the fair value measurement.

9

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 6. | FAIR VALUE MEASUREMENT: (Continued) |

As of September 30, 2014 and December 31, 2013, our only financial assets and liabilities required to be measured on a recurring basis were our money market investments.

The following table represents the Company’s fair value hierarchy for its financial assets and liabilities required to be measured on a recurring basis:

| Basis of Fair Value Measurements | ||||||||||||||||

| Balance | Quoted Prices in Active Markets for Identical Items (Level 1) |

Significant Other Observable Inputs (Level 2) |

Significant Unobservable Inputs (Level 3) |

|||||||||||||

| (In Thousands) | ||||||||||||||||

| Balance at September 30, 2014: |

||||||||||||||||

| Financial assets: |

||||||||||||||||

| Money market investment |

$ | 4,084 | $ | 4,084 | $ | — | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total financial assets |

$ | 4,084 | $ | 4,084 | $ | — | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Balance at December 31, 2013: |

||||||||||||||||

| Financial assets: |

||||||||||||||||

| Money market investment |

$ | 4,084 | $ | 4,084 | $ | — | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total financial assets |

$ | 4,084 | $ | 4,084 | $ | — | $ | — | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

No financial instruments were transferred into or out of Level 3 classification during the three-month period ended September 30, 2014.

As of September 30, 2014 and December 31, 2013, the fair values of our other financial instruments, which include cash and cash equivalents, accounts receivable and accounts payable, approximate the carrying amounts of the respective asset and/or liability due to the short-term nature of these financial instruments.

10

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 7. | GOODWILL AND INTANGIBLE ASSETS: |

There has been no change in the Company’s recorded goodwill balance during the three- or nine-month periods ended September 30, 2014 or 2013. Our annual goodwill and intangible assets measurement date is December 2.

We amortize our intangible assets that have finite lives using either the straight-line method or based on estimated future cash flows to approximate the pattern in which the economic benefit of the asset will be utilized. Amortization expense was $75 thousand and $226 thousand during the three- and nine-month periods ended September 30, 2014, respectively. Amortization expense was $101 thousand and $310 thousand during the three- and nine-month periods ended September 30, 2013, respectively. This amortization expense relates to certain non-competition covenants, trade names and customer lists, which expire at various times through 2016.

The Company recorded amortization from capitalized internally developed software (intellectual property) (reported as part of Cost of Revenue - software cost) of $53 thousand and $160 thousand during the three- and nine-month periods ended September 30, 2014, respectively. The Company recorded amortization from capitalized internally developed software (intellectual property) (reported as part of Cost of Revenue - software cost) of $77 thousand and $258 thousand during the three- and nine-month periods ended September 30, 2013, respectively.

Estimated annual amortization expense (including amortization expense associated with capitalized software costs) for the current year and the following four years ending December 31, is as follows:

| Amortization Expense |

||||

| (In Thousands) | ||||

| 2014 |

$ | 514 | ||

| 2015 |

$ | 266 | ||

| 2016 |

$ | 176 | ||

| 2017 |

$ | — | ||

| 2018 |

$ | — | ||

11

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 8. | ACCRUED EXPENSES AND OTHER LIABILITIES: |

Accrued liabilities as of September 30, 2014 and December 31, 2013 consisted of the following:

| September 30, 2014 |

December 31, 2013 |

|||||||

| (In Thousands) | ||||||||

| Accrued bonuses |

$ | 3,590 | $ | 3,126 | ||||

| Accrued vacation |

2,481 | 1,983 | ||||||

| Accrued payroll related liabilities |

2,534 | 1,682 | ||||||

| Accrued commissions |

2,884 | 2,765 | ||||||

| Accrued software expense |

685 | 1,093 | ||||||

| Income tax related accruals |

1,057 | 588 | ||||||

| Deferred rent |

458 | 513 | ||||||

| Short-term portion of lease abandonment accrual |

609 | 475 | ||||||

| Accrued sales and use tax |

290 | 275 | ||||||

| Other accrued expenses |

2,778 | 1,826 | ||||||

|

|

|

|

|

|||||

| Total |

$ | 17,366 | $ | 14,326 | ||||

|

|

|

|

|

|||||

Other long-term liabilities as of September 30, 2014 and December 31, 2013 consisted of the following:

| September 30, 2014 |

December 31, 2013 |

|||||||

| (In Thousands) | ||||||||

| Long-term portion of lease abandonment accrual |

$ | 557 | $ | 760 | ||||

|

|

|

|

|

|||||

| Total |

$ | 557 | $ | 760 | ||||

|

|

|

|

|

|||||

| 9. | NET INCOME PER SHARE: |

A reconciliation of net income and weighted average shares used in computing basic and diluted net income per share is as follows:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| (In Thousands, Except Per Share Data) | ||||||||||||||||

| Basic net income per share: |

||||||||||||||||

| Net income applicable to common shares |

$ | 976 | $ | 1,772 | $ | 3,408 | $ | 2,297 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common shares outstanding |

11,197 | 10,732 | 11,092 | 10,800 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic net income per share of common stock |

$ | 0.09 | $ | 0.17 | $ | 0.31 | $ | 0.21 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted net income per share: |

||||||||||||||||

| Net income applicable to common shares |

$ | 976 | $ | 1,772 | $ | 3,408 | $ | 2,297 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common shares outstanding |

11,197 | 10,732 | 11,092 | 10,800 | ||||||||||||

| Dilutive effects of stock options and restricted stock |

1,775 | 1,501 | 1,881 | 985 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common shares, assuming dilutive effect of stock options and restricted stock |

12,972 | 12,233 | 12,973 | 11,785 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Diluted net income per share of common stock |

$ | 0.08 | $ | 0.14 | $ | 0.26 | $ | 0.19 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

12

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 9. | NET INCOME PER SHARE: (Continued) |

Share-based awards, inclusive of all grants made under the Company’s equity plans, for which either the stock option exercise price or the fair value of the restricted share award exceeds the average market price over the period, have an anti-dilutive effect on earnings per share, and accordingly, are excluded from the diluted computations for all periods presented. Had such shares been included, shares for the diluted computation would have increased by approximately 303 thousand and 314 thousand in the three- and nine-month periods ended September 30, 2014, respectively. The diluted computation would have increased by approximately 478 thousand and 1.0 million in the three- and nine-month periods ended September 30, 2013, respectively. As of September 30, 2014 and 2013, there were approximately 4.0 million and 4.3 million share-based awards outstanding, respectively, under the Company’s equity plans.

| 10. | STOCK REPURCHASE PROGRAM: |

In December 2007, our Board of Directors (the “Board”) authorized a stock repurchase program for up to $5.0 million of common stock on the open market or through privately negotiated transactions from time-to-time through December 31, 2008 (the “Stock Repurchase Program”). The Board subsequently amended the Stock Repurchase Program, authorizing both an increase to and an extension of the Stock Repurchase Program. The Stock Repurchase Program, as amended, had a maximum purchase value of shares of $23.1 million (the “Purchase Authorization”) and was set to expire on September 19, 2014 (the “Repurchase Period”). On September 18, 2014, we announced that the Board had approved an extension of the Repurchase Period to September 25, 2015.

The timing and amount of the purchases will be based upon market conditions, securities law considerations and other factors. The Stock Repurchase Program does not obligate the Company to acquire a specific number of shares in any period and may be modified, suspended, extended or discontinued at any time, without prior notice.

The Company repurchased a total of 142 thousand shares of common stock during the three- and nine-month periods ended September 30, 2014 at an aggregate purchase price of $962 thousand. The Company made no common stock repurchases during the three-month period ended September 30, 2013. The Company repurchased a total of 365 thousand shares of common stock during the nine-month period ended September 30, 2013 at an aggregate purchase price of $1.5 million. As of September 30, 2014, there was $9.1 million of purchase authorization remaining under the Stock Purchase Program.

| 11. | REVOLVING LINE OF CREDIT: |

In September 2013, the Company entered into a three-year secured revolving credit facility (the “Credit Facility”). The Credit Facility allows the Company to borrow up to $10.0 million and includes an additional accordion feature that allows the Company to request an additional $5.0 million as needed, extending the total credit facility borrowing capacity to $15 million over its three-year term. The Credit Facility is secured by the personal property of the Company and its domestic subsidiaries, and is subject to normal covenants. The Company was in compliance with all covenants as of September 30, 2014. Under the terms of the Credit Facility, any advances will accrue interest at a variable per annum rate of interest equal to, as elected by the Company, (i) the Prime Rate, or (ii) the LIBOR Rate plus 1.5%. Interest is due and payable, in arrears, on a monthly basis. The Company will be obligated to pay an annual commitment fee of 0.15% on the daily undrawn balance of the facility. Any amounts outstanding under the Credit Facility will be due on September 23, 2016. No amounts were drawn under this facility as of September 30, 2014.

| 12. | LEASE ABANDONMENT: |

In December 2011, the Company abandoned certain excess office space within its corporate headquarters in Wakefield, Massachusetts. As a result of the abandonment of such space, the Company incurred a non-cash operating charge of $2.2 million in the fourth quarter of 2011 and recorded a lease abandonment accrual (the short- and long-term portions of which are recorded within accrued expenses and other long-term liabilities within the condensed consolidated balance sheets). The lease abandonment charge was calculated based on the net of future contractually obligated lease payments and an estimate of potential sub-lease income (which took into account current market rates and occupancy levels). This analysis is reviewed and updated each reporting period. During the second quarter of 2014 the Company determined that an elimination of the

13

Table of Contents

EDGEWATER TECHNOLOGY, INC.

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 12. | LEASE ABANDONMENT: (Continued) |

estimated sub-lease income was warranted and, as a result, the Company recorded a non-cash operating expense charge of $400 thousand which was recorded within selling, general and administrative expenses in the condensed consolidated statement of comprehensive income for the nine-month period ended September 30, 2014. No changes were made to any lease abandonment assumptions during the three-month period ended September 30, 2014. The lease abandonment accrual totaled $1.2 million as of both September 30, 2014 and December 31, 2013.

| 13. | FULLSCOPE EMBEZZLEMENT: |

During the second quarter of 2010, the Company discovered embezzlement activities at Fullscope, one of its wholly-owned subsidiaries, which was acquired by the Company in December 2009 (the “Fullscope Embezzlement Issue”). Based upon the results of forensic accounting procedures, we identified that the embezzlement activities occurred for an extended period prior to our acquisition of Fullscope and also during the first and second quarter of 2010.

Since 2010 we have incurred certain embezzlement-related expenses associated with non-routine professional services and sales and use tax obligations.

The Company incurred the majority of its embezzlement-related expenses during fiscal 2010 in connection with its identification and investigation of the embezzlement activity. Embezzlement-related expenses incurred in the three- and nine-month periods ended September 30, 2014 were not material.

During the second quarter of 2014, the Company reached an agreement with the former Fullscope stockholders settling the Company’s outstanding escrow claims associated with the Fullscope acquisition (the “Settlement Agreement”). In connection with the Settlement Agreement, the Company received approximately $1.9 million in cash to satisfy the Company’s escrow claims. The settlement and collection of the escrow has been recorded within selling, general and administrative expense within the condensed consolidated statement of comprehensive income. As of September 30, 2014, the escrow account had a remaining balance of $250 thousand. This balance will remain in the escrow account until the second quarter of 2015 and will be utilized to cover any potential future sales and use tax exposure that may arise from subsequent state inquiry or audit. If no exposure is identified, then the remaining balance will be remitted to the former Fullscope stockholders. Amounts recovered, if any, will be recorded during the period in which settlement is determined to be probable of recovery from escrow.

14

Table of Contents

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following information should be read in conjunction with the information contained in the Unaudited Condensed Consolidated Financial Statements and notes thereto appearing elsewhere in this Quarterly Report on Form 10-Q. This Quarterly Report on Form 10-Q contains forward-looking statements that involve risks and uncertainties. See “Risk Factors” and “Special Note Regarding Forward-Looking Statements” included elsewhere herein. We use the terms “we,” “our,” “us,” “Edgewater” and “the Company” in this report to refer to Edgewater Technology, Inc. and its wholly-owned subsidiaries.

Edgewater is a strategic consulting firm that brings a synergistic blend of specialty services to drive transformational change that (1) improves process, (2) reduces costs and (3) increases revenue. Our solutions are tailored to the C-level executives in the upper mid-market and Global 2000.

We deliver our services across a broad range of industries. We work onsite with our clients, providing a full spectrum of services in the following areas: classic consulting and product-based consulting, primarily in enterprise performance management (“EPM”) and enterprise resource planning (“ERP”).

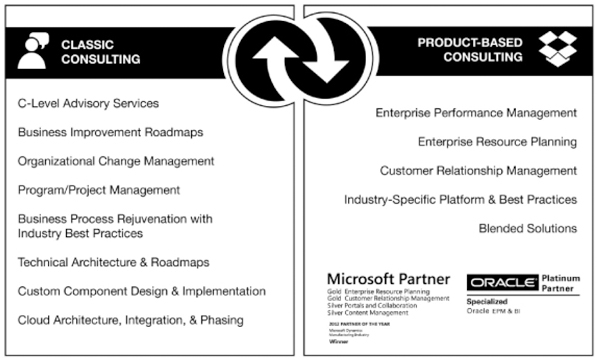

Our Services

Edgewater offers a full spectrum of services and expertise to ensure the success of our engagement. Our consulting services are consolidated into two major synergistic offerings: (1) Classic Consulting and (2) Product-Based Consulting.

The following diagram illustrates these offerings:

Edgewater has the proven expertise to plan, deliver and manage integration services that improve performance and maximize business results. We focus on deploying new systems and unlocking the value of the existing corporate assets. This proven expertise enables us to bring complex technologies and systems together while minimizing risk, leveraging our clients’ technology investments and delivering tailored solutions.

15

Table of Contents

The following are Edgewater’s service categories with sample services:

Classic consulting services

| • | CFO advisory services |

| • | Business improvement roadmaps |

| • | Organizational change management |

| • | Program/project management |

| • | Business process rejuvenation and integrated social media best practices |

| • | Specialized operational, due diligence and technology management expertise to mergers and acquisitions, private equity and venture capital |

| • | Strategic advice, costing, estimates to complete, failing or failed programs or project initiatives |

| • | Independent package selection and Request for Information or Proposal process design and implementation |

| • | Technical architecture and roadmaps |

| • | CIO advisory services |

| • | Strategic technology selections |

| • | Technical evaluation and design |

| • | Custom component design and implementation |

| • | Customer intelligence solutions using web/mobile analytics combined with social intelligence |

| • | Cloud architecture, integration and phasing solutions |

| • | On-going support services |

| • | Infrastructure optimization and redesign, disaster recovery and business continuity specialized design and assistance |

Product-based consulting services

| • | Business transformation through the use of packaged software solutions |

| • | Enterprise performance management with Oracle budgeting, planning, consolidation and strategic finance both on premise and in the cloud |

| • | Enterprise resource planning with Microsoft Dynamics AX targeted in process and discrete manufacturing verticals such as CPG, IEM, Chemical, Pharmaceuticals and Food and Beverage |

| • | Customer relationship management with Microsoft Dynamics CRM both on premise and in the cloud |

| • | Industry specific platform and best practice solutions |

| • | Blended solutions; Microsoft CRM/XRM and specialized custom solutions |

| • | Business intelligence analytics |

| • | Design, development and introduction of IP that helps “verticalize” channel product stacks |

| • | Support and training services |

In addition to the above services, the Company also provides synergistic services in the area of data management and analytics. Examples of such services include the following:

Enterprise information management services

| • | Provide for data related matters: master data management, data governance, logical and physical data base design, data warehouse strategies and design |

| • | Provide practical data architectures and roadmaps to support transactional systems and enterprise performance management through advanced analytics |

| • | Provide forms of data manipulation, transformation and quality services |

Analytics services

| • | Advise on lead derivation of key financial and operational performance indicators and correlate their measurement, visualization and action for a given organization |

| • | Advise on opportunities for the use of predictive techniques, external data and benchmarks to improve business performance measurement and forecasting |

| • | Advise on the creation and adoption of analytics architectures, roadmaps and supporting organizations |

| • | Advise, design and roadmap analytics-based near real-time to real-time alerting strategies and implementations |

16

Table of Contents

Our consultants are expected to travel and to be onsite with the customer to provide the highest level of service and support in all of these endeavors. We provide varying degrees of customer project assistance and will incorporate customer resources for technology transfer or cost optimization purposes. Independent teams and proper project process and delineation provide conflict-free transition points among all key service offerings as well as independent entry points. Leads for all offerings are internally driven with assistance from the respective vendors for software product solutions.

Factors Influencing Our Results of Operations

Revenue. The Company derives its service revenue from time and materials-based contracts, fixed-price contracts and retainer-based arrangements. Time and materials-based contracts represented 89.6% and 91.6% of service revenue for the three- and nine-month periods ended September 30, 2014, respectively. Time and materials-based contracts represented 89.9% and 91.4% of service revenue for the three- and nine-month periods ended September 30, 2013, respectively. Revenue under time and materials contracts is recognized as services are rendered and performed at contractually agreed upon rates. Fixed-price contracts represented 6.3% and 4.2% of service revenue for the three- and nine-month periods ended September 30, 2014, respectively. Fixed-price contracts represented 7.4% and 5.6% of service revenue for the three- and nine-month periods ended September 30, 2013, respectively. Revenue pursuant to fixed-price contracts is recognized under the proportional performance method of accounting. Retainer-based contracts represented 4.1% and 4.2% of service revenue during the three- and nine-month periods ended September 30, 2014, respectively. Retainer-based contracts represented 2.7% and 3.0% of service revenue during the three- and nine-month periods ended September 30, 2013, respectively. Revenue under retainer-based contracts is recognized ratably over the contract period, as outlined within the respective contract.

Estimates of total project costs are continuously monitored during the term of an engagement. There are situations where the number of hours to complete projects may exceed (or be less than) our original estimate, as a result of an increase (or decrease) in project scope, unforeseen events that arise, or the inability of the client or the delivery team to fulfill their responsibilities. Accordingly, recorded revenues and costs are subject to revision throughout the life of a project based on current information and historical trends. Such revisions may result in increases or decreases to revenue and income and are reflected in the consolidated financial statements in the periods in which they are first identified.

We anticipate that software revenue will continue to represent a meaningful portion of our revenues. Our reported software revenue represents the resale of certain third-party off-the-shelf software and related maintenance (primarily relates to the resale of Microsoft Dynamics AX product) and has historically been recorded on a gross basis provided we act as principal in the transaction, whereby we have credit risk and we set the price to the end user. In the event we do not meet the requirements to be considered a principal in the software sale transaction and act as an agent, software revenue is recorded on a net basis.

Software revenue is recognized upon delivery, except in the infrequent situation where the Company provides maintenance services, in which case the related maintenance is recognized ratably over the maintenance period (while the software revenue is recognized upon delivery). Software revenue is expected to fluctuate between quarters, dependent on our customers’ demand for such third-party off-the-shelf software. Fluctuations in software revenue may have an impact upon our periodic operating performance, including gross margin.

Prior to the second quarter of 2013, we recorded substantially all of our software resale revenue on a gross basis (reporting the revenue and cost from the transaction in our consolidated statement of comprehensive income). However, beginning in the second quarter of 2013, due to changes in the nature of the terms of certain Microsoft Dynamics AX software resale arrangements (primarily the risk of credit loss and ability to establish pricing), we began to recognize a portion of our software resale revenue on a net basis (reporting only the net profit from the transaction as revenue in our consolidated statement of comprehensive income). We expect this trend to continue and also anticipate that the number of new software resale arrangements subject to these terms may increase in future periods. Additionally, the changes in the terms of the resale arrangements may, in certain situations, extend the timing of the recognition period (from full, immediate recognition of the gross margin on the transaction to recognition of the gross margin on the transaction over a three-year period) due to payment terms being spread over a multiple year period. This would reduce the amount of the software revenue and associated gross margin to be recognized by the Company in the initial period of the sale.

Operating Expenses. The largest portion of our operating expenses consists of cash and non-cash compensation and benefits associated with our project consulting personnel and related expenses. Non-cash compensation includes share-based compensation expense arising from restricted stock and option grants to employees. Project personnel expenses also consist of payroll costs and related benefits associated with our professional staff. Other related expenses include travel, subcontracting costs, third-party vendor payments and non-billable expenses associated with the delivery of services to our

17

Table of Contents

customers. We consider the relationship between project personnel expenses and service revenue to be an important measure of our operating performance. The relationship between project personnel expenses and service revenue is driven largely by the chargeability of our consultant base, the prices we charge our customers and the non-billable costs associated with securing new customer engagements and developing new service offerings. The remainder of our recurring operating expense is composed of expenses associated with the development of our business and the support of our customer-serving professionals, such as professional development and recruiting, marketing and sales, and management and administrative support. Professional development and recruiting expenses consist primarily of recruiting and training content development and delivery costs. Marketing and sales expenses consist primarily of the costs associated with the development and maintenance of our marketing materials and programs. Management and administrative support expenses consist primarily of the costs associated with operations, including finance, information systems, human resources, facilities (including the rent of office space) and other administrative support for project personnel.

We regularly review our fees for services, professional compensation and overhead costs to ensure that our services and compensation are competitive within the industry and that our overhead costs are balanced with our revenue levels. In addition, we monitor the progress of projects with customer senior management. We manage the activities of our professionals by closely monitoring engagement schedules and staffing requirements. However, a rapid decline in the demand for the professional services that we provide could result in lower utilization of our professionals than we planned. In addition, because most of our customer engagements are terminable by our customers without penalty, an unanticipated termination of a customer project could require us to maintain underutilized employees. While professional staff levels must be adjusted to reflect active engagements, we must also maintain a sufficient number of consulting professionals to oversee existing customer engagements and to participate in sales activities to secure new customer assignments.

Fullscope Embezzlement Expenses. Since fiscal 2010, we have incurred certain non-routine professional service-related expenses associated with our identification of embezzlement activities at Fullscope, one of our wholly-owned subsidiaries (the “Fullscope Embezzlement Issue”). We incurred a majority of our embezzlement-related expenses during fiscal 2010 in connection with our identification and investigation of the embezzlement activity.

During the fourth quarter of 2012, the Company began to file tax returns and pay sales and use tax liabilities related to the Fullscope Embezzlement (which were created by the methods employed by a former employee of Fullscope to conceal the discovered fraudulent activity). The Company has made payments totaling $1.4 million associated with the sales and use tax liabilities. As of March 31, 2014, we had completed the process of making initial payments to settle the identified pre-acquisition sales and use tax exposure.

During the second quarter of 2014, the Company reached an agreement with the former Fullscope stockholders settling the Company’s outstanding escrow claims associated with the Fullscope acquisition (the “Settlement Agreement”). In connection with the Settlement Agreement, the Company received approximately $1.9 million in cash to satisfy the Company’s escrow claims. As of September 30, 2014, the escrow account had a remaining balance of $250 thousand. This balance will remain in the escrow account until the second quarter of 2015 and will be utilized to cover any potential future sales and use tax exposure that may arise from subsequent state inquiry or audit. If no exposure is identified, then the remaining balance will be remitted to the former Fullscope stockholders. Amounts recovered, if any, will be recorded during the period in which settlement is determined to be probable of recovery from escrow.

Lease Abandonment. In December 2011, the Company abandoned certain excess office space within its corporate headquarters in Wakefield, Massachusetts. As a result of the abandonment of such space, the Company incurred a non-cash operating charge of $2.2 million in the fourth quarter of 2011 and established a lease abandonment accrual (the short- and long-term portions of which are recorded within accrued expenses and other long-term liabilities within the consolidated balance sheets). The lease abandonment charge was calculated based on the net of future contractually obligated lease payments and an estimate of potential sub-lease income (which took into account current market rates and occupancy levels). This analysis is reviewed and updated each reporting period. During the second quarter of 2014 the Company determined that a change in the estimated sub-lease income was warranted and, as a result, the Company recorded a non-cash operating expense charge of $400 thousand, directly associated with our initial sub-lease assumptions, which has been recorded within selling, general and administrative expenses in the condensed statement of comprehensive income for the nine-month period ended September 30, 2014. No changes were made to any lease abandonment assumptions during the three-month period ended September 30, 2014. The lease abandonment accrual totaled $1.2 million as of both September 30, 2014 and December 31, 2013.

Company Performance Measurement Systems and Metrics. The Company’s management monitors and assesses its operating performance by evaluating key metrics and indicators on an ongoing basis. For example, we regularly review performance information related to annualized revenue per billable consultant, periodic consultant utilization rates, gross

18

Table of Contents

profit margins, average bill rates and billable employee headcount. Edgewater has also developed internal Enterprise Performance Management systems which aid us in measuring our operating performance and consultant utilization rates. The matching of sales opportunities to available skill sets in our consultant base is one of our greatest challenges and therefore, we monitor consultant utilization closely. These metrics, along with other operating and financial performance metrics, are used in evaluating management’s overall performance. These metrics and indicators are discussed in more detail under “Results for the Three and Nine Months Ended September 30, 2014, Compared to Results for the Three and Nine Months Ended September 30, 2013,” included elsewhere in this Quarterly Report on Form 10-Q.

19

Table of Contents

Results for the Three and Nine Months Ended September 30, 2014, Compared to Results for the Three and Nine Months Ended September 30, 2013

The financial information that follows has been rounded in order to simplify its presentation. The amounts and percentages below have been calculated using the detailed financial information contained in the unaudited condensed consolidated financial statements, the notes thereto, and the other financial data included in this Quarterly Report on Form 10-Q.

The following table sets forth the percentage of total revenue of items included in our unaudited condensed consolidated statements of operations:

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Revenue: |

||||||||||||||||

| Service revenue |

87.5 | % | 84.2 | % | 85.5 | % | 81.6 | % | ||||||||

| Software revenue |

4.8 | % | 8.9 | % | 6.9 | % | 11.2 | % | ||||||||

| Reimbursable expenses |

7.7 | % | 6.9 | % | 7.6 | % | 7.2 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenue |

100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||

| Cost of revenue: |

||||||||||||||||

| Project and personnel costs |

52.8 | % | 51.5 | % | 51.6 | % | 51.9 | % | ||||||||

| Software costs |

3.2 | % | 3.6 | % | 4.1 | % | 5.9 | % | ||||||||

| Reimbursable expenses |

7.7 | % | 6.9 | % | 7.6 | % | 7.2 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total cost of revenue |

63.7 | % | 62.0 | % | 63.3 | % | 65.0 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross profit |

36.3 | % | 38.0 | % | 36.7 | % | 35.0 | % | ||||||||

| Operating expenses: |

||||||||||||||||

| Selling, general and administrative |

29.1 | % | 29.9 | % | 28.6 | % | 30.3 | % | ||||||||

| Depreciation and amortization |

0.8 | % | 1.2 | % | 0.8 | % | 1.2 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total operating expenses |

29.9 | % | 31.1 | % | 29.4 | % | 31.5 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

6.4 | % | 6.9 | % | 7.3 | % | 3.5 | % | ||||||||

| Other expense (income), net |

0.5 | % | (0.4 | )% | 0.1 | % | 0.1 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before income taxes |

5.9 | % | 7.3 | % | 7.2 | % | 3.4 | % | ||||||||

| Income tax provision |

2.5 | % | 0.3 | % | 3.2 | % | 0.4 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

3.4 | % | 7.0 | % | 4.0 | % | 3.0 | % | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Revenue. Total revenue increased by $3.3 million, or 13.1%, to $28.7 million during the three-month period ended September 30, 2014, compared to total revenue of $25.4 million in the three-month period ended September 30, 2013. Total revenue increased by $8.8 million, or 11.4%, to $85.6 million during the nine-month period ended September 30, 2014, compared to total revenue of $76.8 million in the nine-month period ended September 30, 2013. With respect to the comparative changes in year-over-year total revenue, service revenue during the third quarter of 2014 increased by $3.8 million, or 17.6%, to $25.1 million compared to $21.4 million during the comparative 2013 quarterly period, while service revenue during the nine-month period ended September 30, 2014 increased by $10.5 million, or 16.7%, to $73.1 million, compared to service revenue of $62.7 million during the nine-month period ended September 30, 2013. Software revenue represented $1.4 million, or 4.8% of total revenue, during the three-month period ended September 30, 2014, compared to $2.3 million, or 8.9% of total revenue, during the third quarter of 2013 and was $5.9 million, or 6.9% of total revenue, during the nine-month period ended September 30, 2014, compared to $8.6 million, or 11.2% of total revenue, during the first nine months of 2013.

On a year-over-year basis, the increase in quarterly and year-to-date service revenue is reflective of the comparative increase in billable consultant utilization, combined with an increase in billable consultant headcount. Billable consultant utilization was 77.3% and 77.6% during the three and nine months ended September 30, 2014, respectively, compared to 71.1% and 72.0% during the three- and nine-month periods ended September 30, 2013, respectively. Billable headcount, excluding contractors, increased by 20, to 325 as of September 30, 2014, compared to 305 as of September 30, 2013.

20

Table of Contents

The increase in utilization was driven by the improved pipeline activity and project signings in the fourth quarter of 2013 and the first half of 2014, which positioned the Company for a strong 2014. On a sequential quarterly basis, service revenue in the third quarter of 2014 increased by $631 thousand, or 2.6%, compared to the second quarter of 2014. The sequential quarterly increase in service revenue is the result of continued strength in billable consultant utilization, while increasing billable headcount through the use of contractors. The use of external contractors increased during the third quarter of 2014 in an effort to maintain an appropriately scaled workforce necessary to support the growth in delivery demands associated with the growth in our 2014 quarterly and year-to-date service revenue.

The existence of intellectual property (IP) design and build capabilities in our strategic offerings mix has had a positive impact on our lead generation and overall sales activity. We plan to continue to build out intellectual property in the healthcare, insurance and manufacturing verticals, as well as in our EPM service offering, in future periods.

As described above, utilization, which is a measure of our ability to generate revenue from our consultants, increased to 77.3% during the third quarter of 2014, compared to 71.1% during the third quarter of 2013. Billable headcount, excluding contractors, increased by 20 during the third quarter of 2014, compared to the third quarter of 2013. The Company proactively manages its reliance on external resources, while maintaining appropriate levels of staff to service existing customer demand and effectively respond to proposal activity. On a sequential quarterly basis utilization remained consistent while billable headcount (including contractors) increased.

Annualized service revenue per billable consultant, as adjusted for utilization, was $359 thousand and $370 thousand during the three-month periods ended September 30, 2014 and 2013, respectively. Annualized service revenue per billable consultant, as adjusted for utilization, was $363 thousand and $357 thousand during the nine-month periods ended September 30, 2014 and 2013, respectively. The periodic fluctuations in our annualized service revenue per billable consultant metric continue to reflect the changes in the mix of our service offering revenue generated by our current engagements.

During the three- and nine-month periods ended September 30, 2014, software revenue totaled $1.4 million and $5.9 million, or 4.8% and 6.9% of total revenue, respectively, compared to software revenue of $2.3 million and $8.6 million, or 8.9% and 11.2%, respectively, in the three- and nine-month periods ended September 30, 2013. Our software revenue is primarily related to our resale of Microsoft Dynamics AX ERP software and maintenance. Software revenue is expected to fluctuate on an annual period to period basis dependent upon our customers’ demand for such third-party off-the-shelf software. We anticipate that software revenue will continue to represent a meaningful portion of annual revenues in future years. Because of this, we believe that periodic fluctuations in the amount of software revenue recognized by the Company may have a material impact upon our gross margins.

In June 2012, Microsoft purchased the Company’s internally developed PI2 software and intellectual property (the “PI2 Solution”) for an aggregate purchase price of $3.25 million. The sale of the PI2 Solution was a significant multiple element contract. This contract included $3.25 million of license consideration and subsequent development and training services. At the time of the sale, we determined that the license did not have stand-alone value without the services, and accordingly we accounted for the license and related services as one unit. The Company recognized $614 thousand and $2.0 million in PI2 license revenue in the three- and nine-month periods ended September 30, 2013, respectively. The PI2 Solution arrangement was completed during the fourth quarter of 2013 and therefore no future revenue will be generated from the PI2 Solution.

Prior to the second quarter of 2013, we recorded substantially all of our software resale revenue on a gross basis (reporting the revenue and cost from the transaction in our consolidated statement of comprehensive income). However, beginning in the second quarter of 2013, due to changes in the nature of the terms of certain Microsoft Dynamics AX software resale arrangements (primarily the risk of credit loss and ability to establish pricing), we began to recognize a portion of our software resale revenue on a net basis (reporting only the net profit from the transaction as revenue in our consolidated statement of comprehensive income). We expect this trend to continue and also anticipate that the number of new software resale arrangements subject to these terms may increase in future periods. Additionally, the changes in the terms of the resale arrangements may, in certain situations, extend the timing of the recognition period (from full, immediate recognition of the gross margin on the transaction to recognition of the gross margin on the transaction over a three-year period) due to payment terms being spread over a multiple year period. This would reduce the amount of the software revenue and associated gross margin to be recognized by the Company in the initial period of the sale.

Generally, we are reimbursed for our out-of-pocket expenses incurred in connection with our customers’ consulting projects. Reimbursed expense revenue increased to $2.2 million compared to $1.8 million for the three-month periods ended September 30, 2014 and 2013, respectively. Reimbursed expense revenue increased to $6.5 million for the nine-month period ended September 30, 2014, as compared to $5.5 million in the comparative 2013 year-to-date period. The aggregate amount of reimbursed expenses will fluctuate from period-to-period depending on the number of billable consultants as well the location of our customers, the general fluctuation of travel costs, such as airfare, and the number of our projects that require travel.

21

Table of Contents

The number of customers the Company served during the nine-month period ended September 30, 2014 totaled 370, as compared to 354 customers during the nine-month period ended September 30, 2013. During the first nine months of 2014, we secured first-time engagements with a total of 67 new customers, compared to 74 new customer engagements during the first nine months of 2013.

Cost of Revenue. Cost of revenue primarily consists of project personnel costs principally related to salaries, payroll taxes, employee benefits, software costs and travel expenses for personnel dedicated to customer projects. These costs represent the most significant expense we incur in providing our services. In total, cost of revenue increased by $2.6 million, or 16.3%, to $18.3 million for the three-month period ended September 30, 2014, compared to $15.7 million in the comparative 2013 quarterly period. Cost of revenue increased by $4.2 million, or 8.4%, to $54.2 million during the nine-month period ended September 30, 2014 compared to $49.9 million in the comparative 2013 period.

The primary drivers of the 2014 year-over-year quarterly and year-to-date increase in total cost of revenue, on an absolute dollar basis, were related to an increase in salary- and fringe-related expenses (primarily associated with the increase in billable consultant headcount), an increase in expense associated with billable consultant revenue share programs (which is directly attributable to the growth in service revenue) and an increase in contractor expense (as the number of contractors utilized increased by 25 compared to the quarter ended September 30, 2013). During the third quarter 2014 we increased our reliance on external contractors as a direct result of increased project delivery demands associated with the growth in our quarterly and year-to-date service revenue. We have in the past (and will continue to do so in the future) utilized contractors as a means to support project delivery needs during periods of growth. The Company maintained 325 billable consultants (excluding contractors) as of the quarter ended September 30, 2014, compared to 305 billable consultants (excluding contractors) as of September 30, 2013.