Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________

FORM 10-Q

___________________________

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2014

Commission File Number 001-32337

DREAMWORKS ANIMATION SKG, INC.

(Exact name of registrant as specified in its charter)

Delaware | 68-0589190 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

1000 Flower Street

Glendale, California 91201

(Address of principal executive offices) (Zip code)

(818) 695-5000

(Registrant's telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | T | Accelerated filer | o |

Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x.

Indicate the number of shares outstanding of each of the registrant's classes of common stock: As of October 17, 2014, there were 77,381,395 shares of Class A common stock and 7,838,731 shares of Class B common stock of the registrant outstanding.

TABLE OF CONTENTS

Page | ||

PART I. | ||

Item 1. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II. | ||

Item 1. | ||

Item 1A. | ||

Item 2. | ||

Item 5. | ||

Item 6. | ||

Unless the context otherwise requires, the terms "DreamWorks Animation," the "Company," "we," "us" and "our" refer to DreamWorks Animation SKG, Inc., its consolidated subsidiaries, predecessors in interest and the subsidiaries and assets and liabilities contributed to it by the entity then known as DreamWorks L.L.C. ("Old DreamWorks Studios") on October 27, 2004 (the "Separation Date") in connection with our separation from Old DreamWorks Studios (the "Separation").

1

PART I—FINANCIAL INFORMATION

ITEM 1. | FINANCIAL STATEMENTS |

DREAMWORKS ANIMATION SKG, INC.

CONSOLIDATED BALANCE SHEETS

(Unaudited)

September 30, 2014 | December 31, 2013 | ||||||

(in thousands, except par value and share amounts) | |||||||

Assets | |||||||

Cash and cash equivalents | $ | 49,066 | $ | 95,467 | |||

Trade accounts receivable, net of allowance for doubtful accounts (see Note 7 for related party amounts) | 128,970 | 130,744 | |||||

Receivables from distributors, net of allowance for doubtful accounts (see Note 7 for related party amounts) | 285,722 | 283,226 | |||||

Film and other inventory costs, net | 1,015,198 | 943,486 | |||||

Prepaid expenses | 19,264 | 20,555 | |||||

Other assets (see Note 15 for related party amounts) | 49,089 | 23,385 | |||||

Investments in unconsolidated entities | 54,551 | 38,542 | |||||

Property, plant and equipment, net of accumulated depreciation and amortization | 182,047 | 186,670 | |||||

Deferred taxes, net | 243,332 | 221,920 | |||||

Intangible assets, net of accumulated amortization | 191,361 | 150,511 | |||||

Goodwill | 189,667 | 179,722 | |||||

Total assets | $ | 2,408,267 | $ | 2,274,228 | |||

Liabilities and Equity | |||||||

Liabilities: | |||||||

Accounts payable | $ | 8,299 | $ | 5,807 | |||

Accrued liabilities | 208,850 | 263,668 | |||||

Payable to former stockholder | 264,079 | 262,309 | |||||

Deferred revenue and other advances | 34,911 | 36,425 | |||||

Revolving credit facility | 205,000 | — | |||||

Senior unsecured notes | 300,000 | 300,000 | |||||

Total liabilities | 1,021,139 | 868,209 | |||||

Commitments and contingencies (Note 17) | |||||||

Equity: | |||||||

DreamWorks Animation SKG, Inc. Stockholders' Equity: | |||||||

Class A common stock, par value $0.01 per share, 350,000,000 shares authorized, 104,964,269 and 104,155,993 shares issued, as of September 30, 2014 and December 31, 2013, respectively | 1,050 | 1,042 | |||||

Class B common stock, par value $0.01 per share, 150,000,000 shares authorized, 7,838,731 shares issued and outstanding, as of September 30, 2014 and December 31, 2013 | 78 | 78 | |||||

Additional paid-in capital | 1,131,732 | 1,100,101 | |||||

Accumulated other comprehensive loss | (1,071 | ) | (600 | ) | |||

Retained earnings | 1,026,003 | 1,072,398 | |||||

Less: Class A Treasury common stock, at cost, 27,582,874 and 27,439,119 shares, as of September 30, 2014 and December 31, 2013, respectively | (771,660 | ) | (768,224 | ) | |||

Total DreamWorks Animation SKG, Inc. stockholders' equity | 1,386,132 | 1,404,795 | |||||

Non-controlling interests | 996 | 1,224 | |||||

Total equity | 1,387,128 | 1,406,019 | |||||

Total liabilities and equity | $ | 2,408,267 | $ | 2,274,228 | |||

See accompanying notes.

2

DREAMWORKS ANIMATION SKG, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

Three Months Ended | Nine Months Ended | ||||||||||||||

September 30, | September 30, | ||||||||||||||

2014 | 2013 | 2014 | 2013 | ||||||||||||

(in thousands, except per share amounts) | |||||||||||||||

Revenues (see Note 7 for related party amounts) | $ | 180,861 | $ | 154,549 | $ | 450,379 | $ | 502,633 | |||||||

Operating expenses (income): | |||||||||||||||

Costs of revenues | 103,719 | 86,639 | 335,734 | 293,406 | |||||||||||

Selling and marketing | 8,790 | 6,935 | 28,334 | 21,128 | |||||||||||

General and administrative | 54,957 | 45,869 | 153,393 | 136,206 | |||||||||||

Product development | 434 | 455 | 1,585 | 2,487 | |||||||||||

Change in fair value of contingent consideration | (4,955 | ) | — | (9,675 | ) | — | |||||||||

Other operating income (see Note 7 for related party amounts) | (2,673 | ) | (3,333 | ) | (6,662 | ) | (6,192 | ) | |||||||

Operating income (loss) | 20,589 | 17,984 | (52,330 | ) | 55,598 | ||||||||||

Non-operating income (expense): | |||||||||||||||

Interest (expense) income, net | (2,840 | ) | (769 | ) | (7,097 | ) | 871 | ||||||||

Other income, net | 298 | 2,847 | 3,369 | 4,889 | |||||||||||

(Increase) decrease in income tax benefit payable to former stockholder | (2,384 | ) | (283 | ) | 238 | (1,352 | ) | ||||||||

Income (loss) before loss from equity method investees and income taxes | 15,663 | 19,779 | (55,820 | ) | 60,006 | ||||||||||

Loss from equity method investees | 1,212 | 2,781 | 7,939 | 4,110 | |||||||||||

Income (loss) before income taxes | 14,451 | 16,998 | (63,759 | ) | 55,896 | ||||||||||

Provision (benefit) for income taxes | 2,587 | 6,919 | (17,279 | ) | 17,455 | ||||||||||

Net income (loss) | 11,864 | 10,079 | (46,480 | ) | 38,441 | ||||||||||

Less: Net (loss) income attributable to non-controlling interests | (64 | ) | 15 | (85 | ) | 547 | |||||||||

Net income (loss) attributable to DreamWorks Animation SKG, Inc. | $ | 11,928 | $ | 10,064 | $ | (46,395 | ) | $ | 37,894 | ||||||

Net income (loss) per share of common stock attributable to DreamWorks Animation SKG, Inc. | |||||||||||||||

Basic net income (loss) per share | $ | 0.14 | $ | 0.12 | $ | (0.55 | ) | $ | 0.45 | ||||||

Diluted net income (loss) per share | $ | 0.14 | $ | 0.12 | $ | (0.55 | ) | $ | 0.45 | ||||||

Shares used in computing net income (loss) per share | |||||||||||||||

Basic | 84,646 | 83,631 | 84,562 | 83,939 | |||||||||||

Diluted | 85,845 | 85,353 | 84,562 | 85,041 | |||||||||||

See accompanying notes.

3

DREAMWORKS ANIMATION SKG, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited)

Three Months Ended | Nine Months Ended | |||||||||||||||

September 30, | September 30, | |||||||||||||||

2014 | 2013 | 2014 | 2013 | |||||||||||||

(in thousands) | ||||||||||||||||

Net income (loss) | $ | 11,864 | $ | 10,079 | $ | (46,480 | ) | $ | 38,441 | |||||||

Other comprehensive income (loss), net of tax: | ||||||||||||||||

Foreign currency translation (losses) gains | (1,166 | ) | 1,153 | (471 | ) | (1,443 | ) | |||||||||

Comprehensive income (loss) | 10,698 | 11,232 | (46,951 | ) | 36,998 | |||||||||||

Less: Comprehensive (loss) income attributable to non-controlling interests | (64 | ) | 15 | (85 | ) | 547 | ||||||||||

Comprehensive income (loss) attributable to DreamWorks Animation SKG, Inc. | $ | 10,762 | $ | 11,217 | $ | (46,866 | ) | $ | 36,451 | |||||||

See accompanying notes.

4

DREAMWORKS ANIMATION SKG, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

Nine Months Ended | |||||||

September 30, | |||||||

2014 | 2013 | ||||||

(in thousands) | |||||||

Operating activities | |||||||

Net (loss) income | $ | (46,480 | ) | $ | 38,441 | ||

Adjustments to reconcile net (loss) income to net cash (used in) provided by operating activities: | |||||||

Amortization and write-off of film and other inventory costs(1) | 298,096 | 254,489 | |||||

Amortization of intangible assets | 10,516 | 7,341 | |||||

Stock-based compensation expense | 8,387 | 14,483 | |||||

Amortization of deferred financing costs | 865 | 182 | |||||

Depreciation and amortization | 3,654 | 3,420 | |||||

Change in fair value of contingent consideration | (9,675 | ) | — | ||||

Revenue earned against deferred revenue and other advances | (43,143 | ) | (71,489 | ) | |||

Income related to investment contributions | (6,662 | ) | (14,033 | ) | |||

Loss from equity method investees | 7,939 | 4,110 | |||||

Deferred taxes, net | (19,658 | ) | 15,372 | ||||

Changes in operating assets and liabilities, net of the effects of acquisitions: | |||||||

Trade accounts receivable | 2,830 | 878 | |||||

Receivables from distributors | (2,011 | ) | 50,507 | ||||

Film and other inventory costs | (354,003 | ) | (323,967 | ) | |||

Intangible assets | — | 1,015 | |||||

Prepaid expenses and other assets | (21,145 | ) | (6,587 | ) | |||

Accounts payable and accrued liabilities | (46,553 | ) | 11,269 | ||||

Payable to former stockholder | 1,770 | (14,645 | ) | ||||

Income taxes payable/receivable, net | 2,510 | 3,115 | |||||

Deferred revenue and other advances | 72,117 | 96,538 | |||||

Net cash (used in) provided by operating activities | (140,646 | ) | 70,439 | ||||

Investing activities | |||||||

Investments in unconsolidated entities | (18,154 | ) | (14,720 | ) | |||

Purchases of property, plant and equipment | (26,263 | ) | (26,669 | ) | |||

Acquisitions of character and distribution rights | (51,000 | ) | — | ||||

Acquisitions, net of cash acquired | (12,605 | ) | (30,093 | ) | |||

Net cash used in investing activities | (108,022 | ) | (71,482 | ) | |||

Financing activities | |||||||

Proceeds from stock option exercises | 261 | — | |||||

Deferred financing costs | — | (7,718 | ) | ||||

Purchase of treasury stock | (3,580 | ) | (28,170 | ) | |||

Borrowings from revolving credit facility | 215,000 | 68,000 | |||||

Repayments of borrowings from revolving credit facility | (10,000 | ) | (233,000 | ) | |||

Borrowings from senior unsecured notes | — | 300,000 | |||||

Net cash provided by financing activities | 201,681 | 99,112 | |||||

Effect of exchange rate changes on cash and cash equivalents | 586 | (889 | ) | ||||

(Decrease) increase in cash and cash equivalents | (46,401 | ) | 97,180 | ||||

Cash and cash equivalents at beginning of period | 95,467 | 59,246 | |||||

Cash and cash equivalents at end of period | $ | 49,066 | $ | 156,426 | |||

Non-cash investing activities: | |||||||

Contingent consideration portion of business acquisition purchase price | $ | — | $ | 95,000 | |||

Intellectual property and technology licenses granted in exchange for equity interest | 6,057 | 12,007 | |||||

Services provided in exchange for equity interest | 682 | 2,026 | |||||

Total non-cash investing activities | $ | 6,739 | $ | 109,033 | |||

Supplemental disclosure of cash flow information: | |||||||

Cash paid (refunded) during the period for income taxes, net | $ | 70 | $ | (1,182 | ) | ||

Cash paid during the period for interest, net of amounts capitalized | $ | 14,039 | $ | — | |||

(1) Included within this amount is depreciation and amortization, interest expense and stock-based compensation previously capitalized to "Film and other inventory costs" (see Note 1). During the nine months ended September 30, 2014 and 2013, these amounts totaled $24,574 and $24,932, respectively.

See accompanying notes.

5

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

1. | Business and Basis of Presentation |

Business

The business of DreamWorks Animation SKG, Inc. ("DreamWorks Animation" or the "Company") is primarily devoted to the development, production and exploitation of animated films (and other audiovisual programs) and their associated characters in the worldwide theatrical, home entertainment, digital, television, merchandising, licensing and other markets. The Company continues to expand its library and increase the value of its intellectual property assets by developing and producing new television series, live performances and other non-theatrical content based on characters from its feature films. In addition, the Company has an extensive library of other intellectual property rights through its acquisition of Classic Media, which can be exploited in various markets. The Company's activities also include technology initiatives as it explores opportunities to exploit its internally developed software.

Distribution and Servicing Arrangements

The Company derives revenue from Twentieth Century Fox Film Corporation's worldwide (excluding China and South Korea) exploitation of its films in the theatrical and post-theatrical markets. Pursuant to a binding term sheet (the "Fox Distribution Agreement") entered into with Twentieth Century Fox and Twentieth Century Fox Home Entertainment, LLC (collectively, "Fox"), the Company has agreed to license Fox certain exclusive distribution rights and exclusively engage Fox to render fulfillment services with respect to certain of the Company's animated feature films and other audiovisual programs theatrically released during the five-year period beginning on January 1, 2013. As of July 1, 2014, Fox has also been licensed and engaged to render fulfillment services for the Company’s feature films theatrically released prior to January 1, 2013 in theatrical, non-theatrical, home entertainment and digital media. The rights licensed to, and serviced by, Fox will terminate on the date that is one year after the initial home video release date in the United States ("U.S.") of the last film theatrically released by Fox during such five-year period.

Also beginning in 2013, the Company's films are distributed in China and South Korea territories by separate distributors in each of these territories. The key terms of the Company's distribution arrangements with its Chinese and South Korean distributors are largely similar to those with Fox and Paramount such that the Company also recognizes revenues earned under these arrangements on a net basis. The Company's distribution partner in China is a subsidiary of Oriental DreamWorks Holding Limited ("ODW"), which is a related party.

Lastly, the Company continues to derive revenues from the distribution by Paramount Pictures Corporation, a subsidiary of Viacom Inc., and its affiliates (collectively, "Paramount") of its feature films released prior to January 1, 2013 pursuant to a distribution agreement and a fulfillment services agreement (collectively, the "Paramount Agreements"). As of July 1, 2014, the Company reacquired certain distribution rights to its feature films from Paramount, which rights have been licensed to Fox (as noted above). The amount paid to reacquire these rights was recorded as a definite-lived intangible asset (see Note 6). Paramount will continue to exploit and render fulfillment services in the television media for feature films released prior to January 1, 2013 until the date that is 16 years after such film's theatrical release, and will continue to exploit and service certain other agreements with Paramount's sublicensees that remain in place after July 1, 2014.

The Company generally retains all other rights to exploit its films, including commercial tie-in and promotional rights with respect to each film, as well as merchandising, interactive, literary publishing, music publishing and soundtrack rights. The Company's activities associated with its Classic Media properties and AwesomenessTV, Inc. ("ATV") business are not subject to the Company's distribution agreements with its theatrical distributors.

Basis of Presentation

The accompanying unaudited financial data as of September 30, 2014 and for the three and nine months ended September 30, 2014 and 2013 has been prepared by the Company pursuant to the rules and regulations of the Securities and Exchange Commission (the "SEC") and in accordance with U.S. generally accepted accounting principles ("U.S. GAAP") for interim financial information. Accordingly, certain information and footnote disclosures normally included in comprehensive financial statements have been condensed or omitted pursuant to such rules and regulations. The consolidated balance sheet as of December 31, 2013 was derived from the audited financial statements at that date, but does not include all the information and footnotes required by U.S. GAAP. These financial statements should be read in conjunction with the consolidated financial

6

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

statements and related notes included in the Company's Annual Report on Form 10-K for the year ended December 31, 2013 (the "2013 Form 10-K").

Except as described below, the accompanying unaudited consolidated financial statements reflect all adjustments, consisting of only normal recurring items, which in the opinion of management, are necessary for a fair statement for the periods shown. The results of operations for such periods are not necessarily indicative of the results expected for the full year, or for any future period, as fluctuations can occur based upon the timing of the Company's films' theatrical and home entertainment releases, and television series and specials broadcasts.

Reclassifications

Certain amounts in the prior period consolidated financial statements have been reclassified to conform to the Company's 2014 presentation.

In addition, the Company has historically presented exploitation costs (e.g., advertising and marketing) that are directly attributable to its feature films, television series/specials or live performances as a component of costs of revenues. Due to the Company's continued business diversification efforts and the growth in the variety of business lines in which the Company now operates, the Company's advertising and marketing efforts have become less correlated with its various revenue streams. As a result, the Company has determined that it is more meaningful to present all marketing and distribution expenses incurred directly by the Company as a single line item in its statements of operations. Such selling and marketing expenses primarily consist of advertising and marketing costs, promotion costs, distribution fees and sales commissions to outside third parties. To conform to the new presentation, the Company's statements of operations now includes a line item entitled "selling and marketing expenses," which consist of certain (i) distribution expenses incurred directly by the Company that were previously classified in costs of revenues and (ii) general, non-direct advertising and marketing expenses previously classified in a line item entitled "selling, general and administrative expenses." Distribution and marketing expenses that are incurred by the Company's primary distributors (such as Fox and Paramount) are not included in this new line item because the Company records revenues from these distributors only after the distributors have recouped such costs (refer to the Company's significant accounting policies in Note 2 of the Company's 2013 Form 10-K for further information).

Further, given the nature of the Company's business, the Company has determined that "gross profit" is no longer a meaningful metric. In order to align the financial statement presentation with the nature of the Company's business, the Company will no longer present this line item in its statements of operations.

Revision

As discussed in the immediately preceding section, the Company's statements of operations presentation historically included advertising and marketing expenses directly attributable to its feature films, television series/specials or live performances in costs of revenues to arrive at "gross profit" (as disclosed in Note 2 to the consolidated financial statements contained in the Company's 2013 Form 10-K). As a result, advertising and marketing expenses were incorrectly included in the computation of "gross profit." Accordingly, the Company has revised its prior presentation of advertising and marketing expenses appearing in the accompanying financial statements by decreasing costs of revenues (with a corresponding increase in the new line item entitled "selling and marketing expenses") for the three- and nine-month periods ended September 30, 2013 in the amount of $1.8 million and $9.7 million, respectively. The Company assessed the materiality of this revision on previously issued financial statements and concluded that the revision was not material to the consolidated financial statements because, among other things, there was no impact on previously reported operating income or net income, for any period presented. The Company will continue to revise the classification of previously reported advertising and marketing expenses as they are reported in future quarterly and annual filings.

Segment Gross Profit

The Company continues to believe that advertising and marketing expenses directly attributable to its feature films, television series/specials or live performances are an important component in the evaluation of segment profitability. Accordingly, the Company's segment gross profit continues to include the advertising and marketing expenses, as well as other selling and distribution expenses, previously included within costs of revenues. This does not change the amounts of the previously reported segment profitability metric used by the Company's chief operating decision maker to review segment profitability. See Note 14 for the Company's reportable segment disclosures.

7

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Consolidation

The consolidated financial statements of the Company present the financial position, results of operations and cash flows of DreamWorks Animation and its wholly-owned subsidiaries. The Company also consolidates less-than-wholly owned entities if the Company has a controlling financial interest in that entity. The Company uses the equity method of accounting for investments in companies in which it has a 50% or less ownership interest and has the ability to exercise significant influence. Such investments are presented as investments in unconsolidated entities on the Company's consolidated balance sheets (refer to Note 7 for further information of such investments). Prior to recording its share of net income or losses from equity method investees, investee financial statements are converted to U.S. GAAP. All significant intercompany accounts and transactions have been eliminated. Intra-entity profit related to transactions with equity method investees is eliminated until the amounts are ultimately realized.

In addition, the Company reviews its relationships with other entities to identify whether they are variable interest entities ("VIE") as defined by the Financial Accounting Standards Board ("FASB"), and to assess whether the Company is the primary beneficiary of such entity. If the determination is made that the Company is the primary beneficiary, then the entity is consolidated. As of September 30, 2014, the Company determined that it continued to have a variable interest in ODW as ODW does not have sufficient equity at risk (i.e., cash on hand to fund its operations) as a result of the timing of capital contributions to the entity in accordance with the Transaction and Contribution Agreement (see Note 7). However, the Company concluded that it is not the primary beneficiary of ODW as it does not have the ability to control ODW. As a result, it does not consolidate ODW into its financial statements. Refer to Note 7 for further discussion of how the Company accounts for its investment in ODW, including the Company's remaining contributions (which represent the maximum exposure to the Company).

The Company also determined that, as of September 30, 2014, it continued to have a variable interest in an entity that was created to operate and tour its live arena show that is based on its feature film How to Train Your Dragon, and that the Company is the primary beneficiary of this entity as a result of the Company's obligation to fund all losses. Accordingly, the Company's consolidated financial statements included the activities of the VIE. The consolidation of the VIE had an immaterial impact as of and for the three and nine months ended September 30, 2014 and 2013.

Film and Other Inventory Costs Amortization

Amortization and write-off of film and other inventory costs in any period includes depreciation and amortization, interest expense and stock-based compensation expense that were capitalized as part of film and other inventory costs in the period that those charges were incurred. The total amount of such expenses reflected as a component of amortization and write-off of film and other inventory costs for the nine months ended September 30, 2014 and 2013 is presented in the statements of cash flows.

Goodwill

The Company performs a goodwill impairment test on an annual basis, or sooner if indicators of impairment are identified. As of September 30, 2014, the Company did not identify any indicators of goodwill impairment. However, the Company did perform an interim goodwill impairment test as of June 30, 2014 (end of the prior quarter) related to the ATV reporting unit (as described below).

As of June 30, 2014, $118.2 million of total goodwill was attributable to the ATV reporting unit (“ATV Goodwill”). ATV Goodwill represented the excess of the purchase price over the identifiable acquired net assets as of the time of the acquisition of ATV. A large portion of ATV’s purchase price was derived from the fair value of the contingent consideration arrangement entered into in connection with the acquisition (see Note 3). As a result, the cash flow assumptions used for purposes of the goodwill impairment assessment are closely aligned with those used to determine the fair value of the contingent consideration. In connection with the fair value assessment of the contingent consideration as of June 30, 2014, the Company evaluated the revised forecasts for the acquired business, noting a decline in the forecasted earnings for the period applicable to the determination of the contingent consideration payment. Based on this information, the Company determined that an interim goodwill impairment test was necessary and, accordingly, performed a qualitative assessment (commonly referred to as Step 0) to determine whether it was more likely than not that the fair value of the reporting unit was below its carrying value. This assessment included a review of the forecast for periods extending beyond the contingent consideration performance period, which reflected a significant decline in forecasted earnings for certain of the reporting unit's revenue streams when compared to the forecasted amounts at the time of the initial valuation of ATV, as well as delays in the timing of revenue growth. Based on

8

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

this evaluation, the Company concluded that it was more likely than not that the fair value of the ATV reporting unit was less than the reporting unit's carrying amount and, accordingly, the Company proceeded with determining whether the reporting unit's fair value was greater than its carrying value (referred to as Step 1). The Company used the income approach to determine fair value and applied a blended discount rate of 35%. Because a key driver of fair value when applying the income approach is the forecast of future cash flows, the Company's determination of fair value was highly dependent on the level and timing of forecasted earnings and the resulting cash flows. Due to ATV’s limited operating history, there is significant uncertainty in the underlying estimates of ATV’s forecasted earnings. Changes in one or more of the key assumptions could lead to a different fair value of the reporting unit. For further discussion, see "Item 2—Management's Discussion and Analysis of Financial Condition and Results of Operations—Critical Accounting Policies and Estimates—Goodwill."

Upon completion of this analysis, the Company concluded that the fair value of the ATV reporting unit was greater than its carrying value by approximately 12% as of June 30, 2014 and, thus, ATV Goodwill was not impaired as of June 30, 2014.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. The most significant estimates made by management in the preparation of the financial statements relate to the following:

• | ultimate revenues and ultimate costs of film, television product and live performance productions; |

• | relative selling price of the Company's products for purposes of revenue allocation in multi-property licenses and other multiple deliverable arrangements; |

• | determination of fair value of assets and liabilities for the allocation of the purchase price in an acquisition; |

• | determination of the fair value of reporting units for purposes of testing goodwill for impairment; |

• | determination of fair value of non-cash contributions to investments in unconsolidated entities; |

• | useful lives of intangible assets; |

• | product sales that will be returned and the amount of receivables that ultimately will be collected; |

• | the potential outcome of future tax consequences of events that have been recognized in the Company's financial statements; |

• | loss contingencies and contingent consideration arrangements; and |

• | assumptions used in the determination of the fair value of equity-based awards for stock-based compensation or their probability of vesting. |

Actual results could differ from those estimates. To the extent that there are material differences between these estimates and actual results, the Company's financial condition or results of operations will be affected. Estimates are based on past experience and other assumptions that management believes are reasonable under the circumstances, and management evaluates these estimates on an ongoing basis.

2. | Recent Accounting Pronouncements |

In June 2014, the FASB issued an accounting standards update relating to the accounting for certain share-based awards. The accounting update states that, when the terms of an award provide that a performance target could be achieved after the requisite service period, the performance target should be treated as a performance condition that affects vesting and should not be reflected in the grant-date fair value. Companies are permitted to apply the guidance either prospectively to all awards granted or modified after the effective date or retrospectively to awards outstanding as of the beginning of the earliest annual period presented. The guidance is effective for the Company's fiscal year beginning January 1, 2016, with early adoption permitted. The Company adopted the new guidance upon issuance of the accounting standards update, which did not have an impact on its consolidated financial statements as the Company's existing accounting policy was already consistent with this guidance.

In May 2014, the FASB issued an accounting standards update to provide companies with a single model for use in accounting for revenue from contracts with customers. Once it becomes effective, the new guidance will replace most existing revenue recognition guidance in U.S. GAAP, including industry-specific guidance. The core principle of the model is to recognize revenue when control of goods or services transfers to the customer and in an amount that reflects the consideration that the Company expects to be entitled to in exchange for those goods or services that have transferred. Under current U.S. GAAP, the Company recognizes revenue when the risks and rewards of ownership transfer to the customer. In addition, the

9

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

guidance requires improved disclosures to help users of financial statements better understand the nature, amount, timing and uncertainty of revenue that is recognized and the related cash flows. The guidance is effective for the Company's fiscal year beginning January 1, 2017, including interim periods within that fiscal year. Early adoption is not permitted. Companies are permitted to either apply the guidance retrospectively to all prior periods presented or, alternatively, apply the guidance in the year of adoption with the cumulative effect recognized at the date of initial application (referred to as the modified retrospective approach). The Company is in the process of determining the method of adoption, as well as evaluating the impact that the new standard will have on its consolidated financial statements.

In July 2013, the FASB issued an accounting standards update relating to the presentation of unrecognized tax benefits. The accounting update requires companies to present a deferred tax asset net of related unrecognized tax benefits if there is a net operating loss or other tax carryforwards that would apply in settlement of the uncertain tax position. To the extent that an uncertain tax position would not be settled through a reduction of a net operating loss or other tax carryforwards, the unrecognized tax benefit will be presented as a liability. The guidance is effective for the Company's fiscal year beginning January 1, 2014, with early adoption permitted. The Company adopted the new guidance effective January 1, 2014. The adoption of this guidance did not have a material impact on the Company's consolidated financial statements.

3. | Acquisitions |

Recent Acquisitions

The Company entered into an Agreement and Plan of Merger and Reorganization (the "Big Frame Merger Agreement”) pursuant to which, on April 7, 2014 (the “Big Frame Closing Date”), a wholly-owned subsidiary of the Company merged with and into Big Frame, Inc. (“Big Frame”). As a result of this transaction, Big Frame became a wholly-owned subsidiary of the Company. Big Frame is an online multi-channel network that connects advertisers with highly engaged audiences. The goodwill that resulted from the acquisition represents the potential synergies between Big Frame and the Company’s multi-channel network presence on the Internet and is not deductible for tax purposes.

Additionally, on May 20, 2014, the Company acquired certain rights, properties and other items pertaining to Felix the Cat and related characters pursuant to an Asset Purchase Agreement. The acquisition was accounted for as a business combination due to the Company assuming certain licensing arrangements related to the rights. The goodwill that resulted from the acquisition represents potential synergies between the rights acquired and consumer product opportunities. The goodwill is deductible for tax purposes.

The Company’s total cash consideration for these two transactions totaled approximately $33.6 million. As a result of these transactions and the preliminary purchase price allocations, the primary assets acquired were identifiable intangible assets of $22.1 million and resulting goodwill of $10.4 million. The results of operations for these two acquisitions have been included in the Company’s consolidated financial statements since their respective closing dates and had an immaterial impact for the three and nine months ended September 30, 2014.

AwesomenessTV

On May 1, 2013, the Company entered into an Agreement and Plan of Merger (the "Merger Agreement") pursuant to which, on May 3, 2013 (the "ATV Closing Date"), a wholly-owned subsidiary of the Company ("the Merger Sub") merged with and into ATV. As a result of this transaction, ATV became a wholly-owned subsidiary of the Company. ATV is an online next-generation media production company that generates revenues primarily from online advertising sales and distribution of content through media channels such as theatrical, home entertainment and television.

Contingent Consideration

Pursuant to the Merger Agreement, the Company may be required to make future cash payments to ATV's former shareholders as part of the total purchase price to acquire ATV. The contingent consideration is based on whether ATV increases its adjusted earnings before interest expense, income taxes, depreciation and amortization ("EBITDA") over an adjusted EBITDA threshold, over a two-year period (which commenced on January 1, 2014). Adjustments to EBITDA for purposes of determining the contingent consideration earned include, but are not limited to: ATV's employee bonus plan, non-cash gains and losses (such as those related to foreign currency accounting and reversals of prior year accruals) and changes in the fair value of contingent payment liabilities resulting from the acquisition of ATV. The Company estimates the fair value of contingent consideration using significant unobservable inputs in a Monte-Carlo simulation model and bases the fair value on

10

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

the estimated risk-adjusted cost of capital of ATV's adjusted EBITDA following integration into the Company (an income approach). The estimate of the liability may fluctuate if there are changes in the forecast of ATV's future earnings or as a result of actual earnings levels achieved. Any changes in estimate of the contingent consideration liability will be reflected in the Company's results of operations in the period that the change occurs.

Under the Merger Agreement, the maximum contingent consideration that may be earned is $117.0 million. The estimate of contingent consideration liability was $96.5 million as of December 31, 2013 and $91.8 million as of June 30, 2014. Although, from June 30, 2014 to September 30, 2014, there were no material changes in ATV's forecasted adjusted EBITDA for the performance period, a large portion of the forecasted adjusted EBITDA is expected to occur in November and December 2014 in connection with certain potential licensing and distribution agreements. As a result, the Company included a probability-weighted factor in its determination of the fair value of the contingent consideration liability as of September 30, 2014, which led to the decrease in liability from $91.8 million as of June 30, 2014 to $86.8 million as of September 30, 2014. The change in estimate was recorded as a gain in the consolidated statements of operations. As of September 30, 2014, the discount rate and volatility applied were 17.5% and 37.4%, respectively. Using a discount rate of 25% or a volatility of 20%, as of September 30, 2014, would change the estimated fair value of the contingent consideration liability to $85.1 million and $92.1 million, respectively.

ATV's actual 2014 adjusted EBITDA may be significantly less or greater than the amounts currently forecasted, which could result in a large revision in the estimated fair value of the contingent consideration liability and have a material effect on the Company's results of operations. Significant decreases in ATV’s forecasted adjusted EBITDA could potentially also result in the Company recording a goodwill impairment charge.

In addition, the Company is currently conducting discussions with the former ATV shareholders regarding a potential agreed-upon payment to such shareholders in lieu of the contingent consideration specified in the Merger Agreement. There can be no assurances, however, that the Company will be able to reach an agreement with the former ATV shareholders regarding this payment. If such agreement is reached, the agreed-upon payment may be more or less than the Company’s current estimate of the fair value of the contingent consideration liability.

4. | Financial Instruments |

The fair value of cash and cash equivalents, accounts payable, advances and amounts outstanding under the revolving credit facility approximates carrying value due to the short-term maturity of such instruments and floating interest rates. As of September 30, 2014, the fair value of trade accounts receivable approximated carrying value due to the similarities in the initial and current discount rates. In addition, as of September 30, 2014, the fair value of the senior unsecured notes approximated carrying value as the current borrowing rate approximated the debt instrument's actual interest rate. The fair value of trade accounts receivable and the senior unsecured notes was determined using significant unobservable inputs by performing a discounted cash flow analysis and using current discount rates as appropriate for each type of instrument.

The Company has short-term money market investments which are classified as cash and cash equivalents on the consolidated balance sheets. The fair value of these investments at September 30, 2014 and December 31, 2013 was measured based on quoted prices in active markets.

11

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

5. | Film and Other Inventory Costs |

Film, television, live performance and other inventory costs consist of the following (in thousands):

September 30, 2014 | December 31, 2013 | ||||||

In release, net of amortization: | |||||||

Feature films | $ | 372,123 | $ | 285,238 | |||

Television series and specials | 51,496 | 58,631 | |||||

In production: | |||||||

Feature films | 372,665 | 474,609 | |||||

Television series and specials | 76,728 | 15,332 | |||||

In development: | |||||||

Feature films | 124,673 | 75,498 | |||||

Television series and specials | 298 | 1,500 | |||||

Product inventory and other(1) | 17,215 | 32,678 | |||||

Total film, television, live performance and other inventory costs, net | $ | 1,015,198 | $ | 943,486 | |||

____________________

(1) | This category includes $6.8 million and $24.8 million of capitalized live performance costs as of September 30, 2014 and December 31, 2013, respectively. In addition, as of September 30, 2014 and December 31, 2013, this category includes $8.7 million and $7.9 million, respectively, of physical inventory of certain DreamWorks Animation and Classic Media titles for distribution primarily in the home entertainment market. |

The Company anticipates that approximately 48% and 81% of the above "in release" film and other inventory costs as of September 30, 2014 will be amortized over the next 12 months and three years, respectively.

As a result of the weaker-than-expected worldwide theatrical performance of Mr. Peabody and Sherman (released into the domestic theatrical market during March 2014), the Company performed an analysis as of March 31, 2014 to determine whether the unamortized film inventory costs exceeded fair value and was thus impaired. Key assumptions used in the fair value measurement were a discount rate of 7% and estimated remaining cash flows over a period of approximately 15 years. As a result of the analysis, the nine-month period ended September 30, 2014 includes an impairment charge of $57.1 million.

During the three months ended September 30, 2014, the Company also recorded other film impairment charges totaling $2.1 million, which were recorded as a component of costs of revenues. No impairment charges were recorded on film and other inventory costs during the nine months ended September 30, 2013.

12

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

6. | Intangible Assets |

As of September 30, 2014 and December 31, 2013, intangible assets included $69.2 million and $49.5 million, respectively, of indefinite-lived intangible assets. In addition, intangible assets were comprised of definite-lived intangible assets as follows (in thousands, unless otherwise noted):

Weighted Average Estimated Useful Life (in years) | Gross | Accumulated Amortization | Impact of Foreign Currency Translation | Net | |||||||||||||

As of September 30, 2014: | |||||||||||||||||

Character rights | 13.9 | $ | 99,000 | $ | (13,660 | ) | $ | 1,011 | $ | 86,351 | |||||||

Distribution rights | 11.2 | 30,000 | (811 | ) | — | 29,189 | |||||||||||

Programming content | 2.0 | 11,200 | (7,933 | ) | — | 3,267 | |||||||||||

Trademarks and trade names | 10.0 | 1,410 | (181 | ) | — | 1,229 | |||||||||||

Other intangibles | 4.4 | 2,700 | (575 | ) | — | 2,125 | |||||||||||

Total | $ | 144,310 | $ | (23,160 | ) | $ | 1,011 | $ | 122,161 | ||||||||

As of December 31, 2013: | |||||||||||||||||

Character rights | 13.9 | $ | 99,000 | $ | (8,663 | ) | $ | 1,754 | $ | 92,091 | |||||||

Programming content | 2.0 | 11,200 | (3,733 | ) | — | 7,467 | |||||||||||

Trademarks and trade names | 10.0 | 1,200 | (80 | ) | — | 1,120 | |||||||||||

Other intangibles | 2.0 | 500 | (167 | ) | — | 333 | |||||||||||

Total | $ | 111,900 | $ | (12,643 | ) | $ | 1,754 | $ | 101,011 | ||||||||

7. | Investments in Unconsolidated Entities |

The Company has made investments in entities which are accounted for under either the cost or equity method of accounting. These investments are classified as investments in unconsolidated entities in the consolidated balance sheets and consist of the following (in thousands, unless otherwise indicated):

Ownership | |||||||||

Percentage at | September 30, | December 31, | |||||||

September 30, 2014 | 2014 | 2013 | |||||||

Oriental DreamWorks Holding Limited | 45.45% | $ | 20,779 | $ | 16,389 | ||||

All Other | 17.5%-50.0% | 4,759 | 3,140 | ||||||

Total equity method investments | 25,538 | 19,529 | |||||||

Total cost method investments | 29,013 | 19,013 | |||||||

Total investments in unconsolidated entities | $ | 54,551 | $ | 38,542 | |||||

Under the equity method of accounting, the carrying value of an investment is adjusted for the Company's proportionate share of the investees' earnings and losses (adjusted for the amortization of any differences in the Company's basis, with respect to the Company's investment in ODW, compared to the Company's share of venture-level equity), as well as contributions to and distributions from the investee. The Company classifies its share of income or loss from investments accounted for under the equity method as income/loss from equity method investees in its consolidated statements of operations.

13

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

(Loss) income from equity method investees consist of the following (in thousands):

Three Months Ended | Nine Months Ended | ||||||||||||||

September 30, | September 30, | ||||||||||||||

2014 | 2013 | 2014 | 2013 | ||||||||||||

Oriental DreamWorks Holding Limited(1) | $ | (1,382 | ) | $ | (2,582 | ) | $ | (5,986 | ) | $ | (3,539 | ) | |||

All Other | 170 | (199 | ) | (1,953 | ) | (571 | ) | ||||||||

(Loss) income from equity method investees | $ | (1,212 | ) | $ | (2,781 | ) | $ | (7,939 | ) | $ | (4,110 | ) | |||

____________________

(1) | The Company currently records its share of ODW results on a one-month lag. Accordingly, the Company's consolidated financial statements include its share of losses incurred by ODW from December 1, 2013 to August 31, 2014. |

Oriental DreamWorks Holding Limited

On April 3, 2013 ("ODW Closing Date"), the Company formed a Chinese Joint Venture, ODW (or the "Chinese Joint Venture"), through the execution of a Transaction and Contribution Agreement, as amended, with its Chinese partners, China Media Capital (Shanghai) Center L.P. ("CMC"), Shanghai Media Group ("SMG") and Shanghai Alliance Investment Co., Ltd. ("SAIL", and together with CMC and SMG, the "CPE Holders"). In exchange for 45.45% of the equity of ODW, the Company has committed to making a total cash capital contribution to ODW of $50.0 million (of which $9.4 million had been funded as of September 30, 2014, with the balance to be funded over time) and non-cash contributions valued at approximately $100.0 million (of which approximately $32.7 million had been satisfied as of September 30, 2014). Such non-cash contributions include licenses of technology and certain other intellectual property of the Company, rights in certain trademarks of the Company, two in-development feature film projects developed by the Company and consulting and training services. During the nine months ended September 30, 2013, the Company's consolidated statements of operations included $7.8 million of revenues recognized in connection with non-cash contributions made to ODW. The Company's consolidated statements of operations included other operating income recognized in connection with non-cash contributions made to ODW of $2.7 million and $3.3 million during the three months ended September 30, 2014 and 2013, respectively, and $6.7 million and $6.2 million during the nine months ended September 30, 2014 and 2013, respectively.

As of September 30, 2014, the Company's remaining contributions consisted of the following: (i) $40.6 million in cash (which is expected to be funded over the next three years), (ii) two of the Company's in-development film projects, (iii) remaining delivery requirements under the licenses of technology and certain other intellectual property of the Company and (iv) approximately $6.9 million in consulting and training services. Some of these remaining contribution commitments will require future cash outflows for which the Company is not currently able to estimate the timing of contributions as this will depend on, among other things, ODW's operations.

Basis Differences. The Company's investment in ODW does not equal the venture-level equity (the amount recorded on the balance sheet of ODW) due to various basis differences. Basis differences related to definite-lived assets are being amortized based on the useful lives of the related assets. Basis differences related to indefinite-lived assets are not being amortized. The following are the differences between the Company's venture-level equity and the balance of its investment in ODW (in thousands):

September 30, 2014 | |||

Company's venture-level equity | $ | 46,253 | |

Technology and intellectual property licenses(1) | (14,388 | ) | |

Other(2) | (11,086 | ) | |

Total ODW investment recorded | $ | 20,779 | |

____________________

(1) | Represents differences between the Company's historical cost basis and the equity basis reflected at the venture-level (the amount recorded on the balance sheet of ODW) related to the Company's contributions of technology and intellectual property licenses. These basis differences arise because the contributed assets are recorded at fair value by ODW. |

(2) | Represents the Company's net contribution commitment due to ODW. |

14

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Other Transactions with ODW. The Company has various other transactions with ODW, a related party. The Company has entered into a distribution agreement with ODW for the distribution of the Company's feature films in China (beginning with The Croods). In addition, from time to time, the Company may provide consulting and training services to ODW, the charges of which are based on the Company's actual cost of providing such services. The Company's consolidated statements of operations included revenues earned through ODW's distribution of its feature films of $10.9 million and $12.9 million during the three- and nine-month periods ended September 30, 2014, respectively, and $1.1 million and $14.1 million during the three- and nine-month periods ended September 30, 2013, respectively. As of September 30, 2014 and December 31, 2013, the Company's consolidated balance sheets included receivables from ODW of $6.5 million and $3.8 million, respectively, which were classified as a component of trade accounts receivable, and $14.4 million and $16.7 million, respectively, which were classified as a component of receivables from distributors.

8. | Accrued Liabilities |

Accrued liabilities consist of the following (in thousands):

September 30, 2014 | December 31, 2013 | ||||||

Employee compensation | $ | 28,321 | $ | 65,625 | |||

Participations and residuals | 44,588 | 50,690 | |||||

Contingent consideration(1) | 87,659 | 97,545 | |||||

Interest payable | 2,781 | 7,849 | |||||

Income taxes payable | 2,623 | 118 | |||||

Deferred rent | 11,107 | 8,114 | |||||

Other accrued liabilities | 31,771 | 33,727 | |||||

Total accrued liabilities | $ | 208,850 | $ | 263,668 | |||

____________________

(1) | Primarily represents the Company's estimate of the amount of contingent consideration payable in connection with the acquisition of ATV (refer to Note 3 for further information). |

As of September 30, 2014, the Company estimates that over the next 12 months it will pay approximately $18.1 million of its accrued participation and residual costs.

9. | Deferred Revenue and Other Advances |

The following is a summary of deferred revenue and other advances included in the consolidated balance sheets as of September 30, 2014 and December 31, 2013 and the related amounts earned and recorded either as revenue in the consolidated statements of operations or recorded as an offset to other costs (as described below) for the three- and nine-month periods ended September 30, 2014 and 2013 (in thousands):

Amounts Earned | |||||||||||||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||

September 30, | December 31, | September 30, | September 30, | ||||||||||||||||||||

2014 | 2013 | 2014 | 2013 | 2014 | 2013 | ||||||||||||||||||

Deferred Revenue | $ | 9,238 | $ | 14,578 | $ | 2,482 | $ | 10,358 | $ | 18,747 | $ | 23,831 | |||||||||||

Strategic Alliance/Development Advances(1) | 2,918 | 1,667 | 7,683 | 8,010 | 23,050 | 23,900 | |||||||||||||||||

Other(2) | 22,755 | 20,180 | 6,089 | 20,790 | 32,214 | 49,407 | |||||||||||||||||

Total deferred revenue and other advances | $ | 34,911 | $ | 36,425 | |||||||||||||||||||

____________________

(1) | Of the total amounts earned against the "Strategic Alliance/Development Advances," for the three months ended September 30, 2014 and 2013, $2.8 million and $5.3 million, respectively, and $8.7 million and $13.2 million for the nine months ended September 30, 2014 and 2013, respectively, were capitalized as an offset to property, plant and equipment. Additionally, during the three months ended September 30, 2014, of the total amounts earned, $0.6 million, and for the nine months ended September 30, 2014 and 2013, $4.1 million and $1.3 million, respectively, were recorded as a reduction to other assets. During the nine months ended September 30, 2014 and 2013, $2.2 million and $1.4 |

15

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

million, respectively, were recorded as a reduction to prepaid expenses. During the three months ended September 30, 2014 and 2013, of the total amounts earned, $0.6 million and $0.4 million, respectively, and for the nine months ended September 30, 2014 and 2013, $2.2 million and $1.4 million, respectively, were recorded as a reduction to operating expenses.

(2) | Of the total amounts earned, for the nine months ended September 30, 2014, $14.0 million was recorded as a reduction to film and other inventory costs. |

10. | Financing Arrangements |

Senior Unsecured Notes. On August 14, 2013, the Company issued $300.0 million in aggregate principal amount of 6.875% Senior Notes due 2020 (the "Notes"). In connection with the issuance of the Notes, the Company entered into an indenture (the “Indenture”) with The Bank of New York Mellon Trust Company, N.A., as trustee, specifying the terms of the Notes. The Notes were sold at a price to investors of 100% of their principal amount and were issued in a private placement pursuant to the exemptions under Rule 144A and Regulation S under the Securities Act of 1933, as amended. The net proceeds from the Notes amounted to $294.0 million and a portion was used to repay the outstanding borrowings under the Company's revolving credit facility. The Notes are effectively subordinated to indebtedness under the revolving credit facility. Beginning on February 15, 2014, the Company is required to pay interest on the Notes semi-annually in arrears on February 15 and August 15 of each year. The principal amount is due upon maturity. The Notes are guaranteed by all of the Company's domestic subsidiaries that also guarantee its revolving credit facility.

The Indenture contains certain restrictions and covenants that, subject to certain exceptions, limit the Company's ability to incur additional indebtedness, pay dividends or repurchase the Company's common shares, make certain loans or investments, and sell or otherwise dispose of certain assets, among other limitations. The Indenture also contains customary events of default, which, if triggered, may accelerate payment of principal, premium, if any, and accrued but unpaid interest on the Notes. Such events of default include non-payment of principal and interest, non-performance of covenants and obligations, default on other material debt, failure to satisfy material judgments and bankruptcy or insolvency. If a change of control as described in the Indenture occurs, the Company may be required to offer to purchase the Notes from the holders thereof at a repurchase price equal to 101% of their principal amount, plus accrued and unpaid interest, if any, to, but not including, the date of repurchase.

At any time prior to August 15, 2016, the Company may redeem all or part of the Notes at a redemption price equal to the sum of (i) 100% of the principal amount thereof, plus (ii) a specified premium as of the date of redemption, plus (iii) accrued and unpaid interest to, but not including, the date of redemption, subject to the rights of holders of Notes on the relevant record date to receive interest due on the relevant interest payment date. On or after August 15, 2016, the Company may redeem all or a part of the Notes, at specified redemption prices plus accrued and unpaid interest thereon, to, but not including, the applicable redemption date, subject to the rights of holders of Notes on the relevant record date to receive interest due on the relevant interest payment date. In addition, at any time prior to August 15, 2016, the Company may redeem up to 35% of the Notes with the net proceeds of certain equity offerings at a redemption price equal to 106.875% of the principal amount thereof, in each case plus accrued and unpaid interest and additional interest, if any, thereon to, but not including, the redemption date.

Revolving Credit Facility. The Company has a revolving credit facility with a number of banks. On August 10, 2012, the Company and the facility banks terminated the then-existing credit agreement and entered into a new Credit Agreement ("New Credit Agreement"). The New Credit Agreement allows the Company to have outstanding borrowings up to $400.0 million at any one time, on a revolving basis. The Company may from time to time, so long as no default or event of default has occurred under the New Credit Agreement, increase the commitments under the New Credit Agreement by up to $50.0 million. Borrowings are secured by substantially all of the Company's assets. The New Credit Agreement requires the Company to maintain a specified ratio of total debt to total capitalization and a specified ratio of net remaining ultimates to facility exposure. In addition, subject to specified exceptions, the New Credit Agreement also restricts the Company and its subsidiaries from taking certain actions, such as granting liens, entering into any merger or other significant transactions, making distributions, entering into transactions with affiliates, agreeing to negative pledge clauses and restrictions on subsidiary distributions, and modifying organizational documents. The revolving credit facility also prohibits the Company from paying dividends on its capital stock if, after giving pro forma effect to such dividend, an event of default would occur or exist under the revolving credit facility. The Company is required to pay a commitment fee on undrawn amounts at an annual rate of 0.375%. Interest on borrowed amounts (per draw) is determined by reference to either i) the lending banks' base rate plus 1.50% per annum or ii) the London Interbank Offered Rate ("LIBOR") plus 2.50% per annum.

16

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

The following table summarizes information associated with the Company's financing arrangements (in thousands, except percentages):

Interest Expense | |||||||||||||||||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

Balance Outstanding at | Maturity Date | September 30, | September 30, | ||||||||||||||||||||||||

September 30, 2014 | December 31, 2013 | Interest Rate at September 30, 2014 | 2014 | 2013 | 2014 | 2013 | |||||||||||||||||||||

Senior Unsecured Notes | $ | 300,000 | $ | 300,000 | August 2020 | 6.875% | $ | 2,921 | $ | 955 | $ | 8,004 | $ | 955 | |||||||||||||

Revolving Credit Facility | $ | 205,000 | $ | — | August 2017 | 2.65% | $ | 804 | $ | 605 | $ | 1,645 | $ | 1,040 | |||||||||||||

Additional Financing Information

Interest Capitalized to Film Costs. Interest on borrowed funds that are invested in major projects with substantial development or construction phases is capitalized as part of the asset cost until the projects are released or construction projects are put into service. Thus, capitalized interest is amortized over future periods on a basis consistent with that of the asset to which it relates. During the three months ended September 30, 2014 and 2013, the Company incurred interest costs totaling $6.9 million and $4.0 million, respectively, of which $2.9 million and $2.3 million, respectively, were capitalized to film costs. During the nine months ended September 30, 2014 and 2013, the Company incurred interest costs totaling $19.2 million and $7.3 million, respectively, of which $8.7 million and $5.2 million, respectively, were capitalized to film costs.

As of September 30, 2014, the Company was in compliance with all applicable financial debt covenants.

17

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

11. | Income Taxes |

Set forth below is a reconciliation of the components that caused the Company's provision/benefit for income taxes (including the statement of operations line item "Increase/decrease in income tax benefit payable to former stockholder") to differ from amounts computed by applying the U.S. Federal statutory rate of 35% for the three and nine months ended September 30, 2014 and 2013.

Three Months Ended | Nine Months Ended | ||||||||||

September 30, | September 30, | ||||||||||

2014 | 2013 | 2014 | 2013 | ||||||||

Provision for income taxes (combined with increase/decrease in income tax benefit payable to former stockholder)(1) | |||||||||||

U.S. Federal statutory rate | 35.0 | % | 35.0 | % | 35.0 | % | 35.0 | % | |||

U.S. state taxes, net of Federal benefit | (6.5 | ) | (1.4 | ) | 3.5 | (1.8 | ) | ||||

Export sales exclusion/manufacturer's deduction(2) | 17.8 | (1.7 | ) | 0.2 | — | ||||||

Research and development credit(2) | — | (1.9 | ) | — | (4.8 | ) | |||||

Federal energy tax credit(3) | — | (2.3 | ) | — | (2.2 | ) | |||||

Executive compensation | (10.7 | ) | 3.1 | (6.8 | ) | 3.2 | |||||

Stock-based compensation | 22.6 | 11.8 | (5.9 | ) | 4.3 | ||||||

Non-controlling interests | 4.9 | — | 0.1 | — | |||||||

Change in fair value of contingent consideration | (26.2 | ) | — | 4.9 | — | ||||||

Losses from an equity method investee | (8.6 | ) | — | (2.2 | ) | — | |||||

Other | 1.2 | (0.9 | ) | (1.4 | ) | (0.8 | ) | ||||

Effective tax rate (combined with increase/decrease in income tax benefit payable to former stockholder)(1) | 29.5 | % | 41.7 | % | 27.4 | % | 32.9 | % | |||

Less: change in income tax benefit payable to former stockholder(1): | |||||||||||

U.S. state taxes, net of Federal benefit | 0.6 | — | — | — | |||||||

Export sales exclusion/manufacturer's deduction(2) | (17.8 | ) | 1.3 | (0.2 | ) | (0.3 | ) | ||||

Return-to-provision | 0.8 | (2.2 | ) | (0.2 | ) | (0.7 | ) | ||||

Other | 2.3 | (0.8 | ) | — | (1.4 | ) | |||||

Total change in income tax benefit payable to former stockholder(1) | (14.1 | )% | (1.7 | )% | (0.4 | )% | (2.4 | )% | |||

Effective tax rate | 15.4 | % | 40.0 | % | 27.0 | % | 30.5 | % | |||

____________________

(1) | As a result of a partial increase in the tax basis of the Company's tangible and intangible assets attributable to transactions entered into by affiliates controlled by a former stockholder at the time of the Company's 2004 initial public offering, the Company may pay reduced tax amounts to the extent it generates sufficient taxable income in the future. The Company is obligated to remit to an affiliate of the former stockholder 85% of any realized cash savings in U.S. Federal income tax, California franchise tax and certain other related tax benefits. Refer to the Company's 2013 Form 10-K for a more detailed description. |

(2) | The American Taxpayer Relief Act of 2012 (the "Act"), enacted on January 2, 2013, included extensions to many expiring corporate income tax provisions. The Act included a two-year extension of research and development credits and other federal tax incentives, which were to be retroactively applied beginning with January 1, 2012 and ending on December 31, 2013. The Company recognized the effects of the retroactive changes in its results for the three months ended March 31, 2013 (the period of enactment). |

(3) | The Company's policy for accounting for investment tax credits is to recognize the income tax benefit in the year that the credit is generated. |

The Company's federal income tax returns for the tax years ended December 31, 2007 through 2009 are currently under examination by the Internal Revenue Service, and all subsequent tax years remain open to audit. The Company's California state tax returns for all years subsequent to 2007 remain open to audit. The Company's India subsidiary's income tax returns are currently under examination for the tax years ended March 31, 2011 through 2013.

18

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

12. | Stockholders’ Equity and Non-controlling Interests |

Class A Common Stock

Stock Repurchase Program. In July 2010, the Company's Board of Directors terminated the then-existing stock repurchase program and authorized a new stock repurchase program pursuant to which the Company may repurchase up to an aggregate of $150.0 million of its outstanding stock. During the three and nine months ended September 30, 2014 and the three months ended September 30, 2013, the Company did not repurchase any shares of its Class A Common Stock. During the nine months ended September 30, 2013, the Company repurchased 1.3 million shares of its outstanding Class A Common Stock for $25.0 million under the July 2010 authorization. As of September 30, 2014, the Company's remaining authorization under the current stock repurchase program was $100.0 million.

Non-controlling Interests

The Company's consolidated balance sheets include non-controlling interests, which are presented as a separate component of equity. A non-controlling interest represents the other equity holder's interest in a joint venture that the Company consolidates. The net income or loss attributable to the non-controlling interests is presented in the Company’s consolidated statements of operations. There is no other comprehensive income or loss attributable to the non-controlling interests.

The following table presents the changes in equity for the nine-month periods ended September 30, 2014 and 2013 (in thousands):

DreamWorks Animation SKG, Inc. Stockholders' Equity | Non-controlling Interests | Total Equity | |||||||||

Balance as of December 31, 2013 | $ | 1,404,795 | $ | 1,224 | $ | 1,406,019 | |||||

Stock option exercises | 12,167 | — | 12,167 | ||||||||

Stock-based compensation | 19,379 | — | 19,379 | ||||||||

Purchase of treasury shares | (3,343 | ) | — | (3,343 | ) | ||||||

Foreign currency translation adjustments | (471 | ) | — | (471 | ) | ||||||

Distributions to non-controlling interest holder | — | (143 | ) | (143 | ) | ||||||

Net loss | (46,395 | ) | (85 | ) | (46,480 | ) | |||||

Balance as of September 30, 2014 | $ | 1,386,132 | $ | 996 | $ | 1,387,128 | |||||

Balance as of December 31, 2012 | $ | 1,345,616 | $ | 630 | $ | 1,346,246 | |||||

Stock-based compensation | 26,968 | — | 26,968 | ||||||||

Purchase of treasury shares | (28,170 | ) | — | (28,170 | ) | ||||||

Foreign currency translation adjustments | (1,443 | ) | — | (1,443 | ) | ||||||

Distributions to non-controlling interest holder | — | (45 | ) | (45 | ) | ||||||

Net income | 37,894 | 547 | 38,441 | ||||||||

Balance as of September 30, 2013 | $ | 1,380,865 | $ | 1,132 | $ | 1,381,997 | |||||

13. | Stock-Based Compensation |

The Company recognizes compensation costs for equity awards granted to its employees based on each award's grant-date fair value. Most of the Company's equity awards contain vesting conditions dependent upon the completion of specified service periods or achievement of established sets of performance criteria. Compensation cost for service-based equity awards is recognized ratably over the requisite service period. Compensation cost for certain performance-based awards is recognized using a graded expense-attribution method. The Company has granted performance-based awards where the value of the award upon vesting will vary depending on the level of performance ultimately achieved (for example, during the year ended December 31, 2013, the Company granted awards that vest only if the Company achieves positive earnings before interest and taxes for the year ending December 31, 2014). The Company recognizes compensation cost for these awards based on the level of performance expected to be achieved. The Company will recognize the impact of any change in estimate in the period of the change.

19

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Generally, equity awards are forfeited by employees who terminate prior to vesting. However, certain employment contracts for certain executive officers provide for the acceleration of vesting in the event of a change in control or specified termination events. The Company currently satisfies exercises of stock options and stock appreciation rights, the vesting of restricted stock and the delivery of shares upon the vesting of restricted stock units with the issuance of new shares.

The impact of stock options (including stock appreciation rights) and restricted stock awards on net income (excluding amounts capitalized) for the three- and nine-month periods ended September 30, 2014 and 2013, respectively, were as follows (in thousands):

Three Months Ended | Nine Months Ended | ||||||||||||||

September 30, | September 30, | ||||||||||||||

2014(2) | 2013 | 2014 | 2013 | ||||||||||||

Total stock-based compensation | $ | (34 | ) | $ | 4,646 | $ | 8,387 | $ | 14,483 | ||||||

Tax impact(1) | — | (1,937 | ) | (2,298 | ) | (4,765 | ) | ||||||||

Reduction in net income, net of tax | $ | (34 | ) | $ | 2,709 | $ | 6,089 | $ | 9,718 | ||||||

____________________

(1) | Tax impact is determined at the Company's combined effective tax rate, which includes the statement of operations line item "Increase/decrease in income tax benefit payable to former stockholder" (see Note 11). |

(2) | Reflects the reversal of certain stock-based compensation expense due to a change in the estimated probability that certain performance-based equity awards will vest. |

Stock-based compensation cost capitalized as a part of film costs was $3.3 million and $4.1 million for the three-month periods ended September 30, 2014 and 2013, respectively, and $10.6 million and $12.4 million for the nine-month periods ended September 30, 2014 and 2013, respectively.

The following table sets forth the number and weighted average grant-date fair value of equity awards granted during the three- and nine-month periods ended September 30, 2014 and 2013:

Three Months Ended | Nine Months Ended | ||||||||||||

September 30, | September 30, | ||||||||||||

Number Granted | Weighted Average Grant-Date Fair Value | Number Granted | Weighted Average Grant-Date Fair Value | ||||||||||

(in thousands) | |||||||||||||

2014 | |||||||||||||

Restricted stock and restricted stock units | 334 | $ | 20.02 | 793 | $ | 24.35 | |||||||

2013 | |||||||||||||

Restricted stock and restricted stock units | 327 | $ | 27.58 | 754 | $ | 22.53 | |||||||

As of September 30, 2014, the total compensation cost related to unvested equity awards granted to employees (excluding equity awards with performance objectives not probable of achievement) but not yet recognized was approximately $56.8 million and will be amortized on a straight-line basis over a weighted average period of 1.8 years.

14. | Reportable Segments |

The Company's current reportable segments are the following: Feature Films, Television Series and Specials and Consumer Products. Feature Films consists of the development, production and exploitation of feature films in the theatrical, television, home entertainment and digital markets. Television Series and Specials consists of the development, production and exploitation of television, direct-to-video and other non-theatrical content in the television, home entertainment and digital markets. Consumer Products consists of the Company's merchandising and licensing activities related to the exploitation of its intellectual property rights. Operating segments that are not separately reportable are categorized in "All Other" and include ATV and live performances.

20

Table of Contents

DREAMWORKS ANIMATION SKG, INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Segment performance is evaluated based on revenues and segment gross profit. The Company does not allocate assets to each of its operating segments, nor does the Company's chief operating decision maker evaluate operating segments using discrete asset information. Information on the reportable segments and a reconciliation of total segment revenues and segment gross profit to consolidated financial statements are presented below (in thousands):

Three Months Ended | Nine Months Ended | |||||||||||||||

September 30, | September 30, | |||||||||||||||

2014 | 2013 | 2014 | 2013 | |||||||||||||

Revenues | ||||||||||||||||

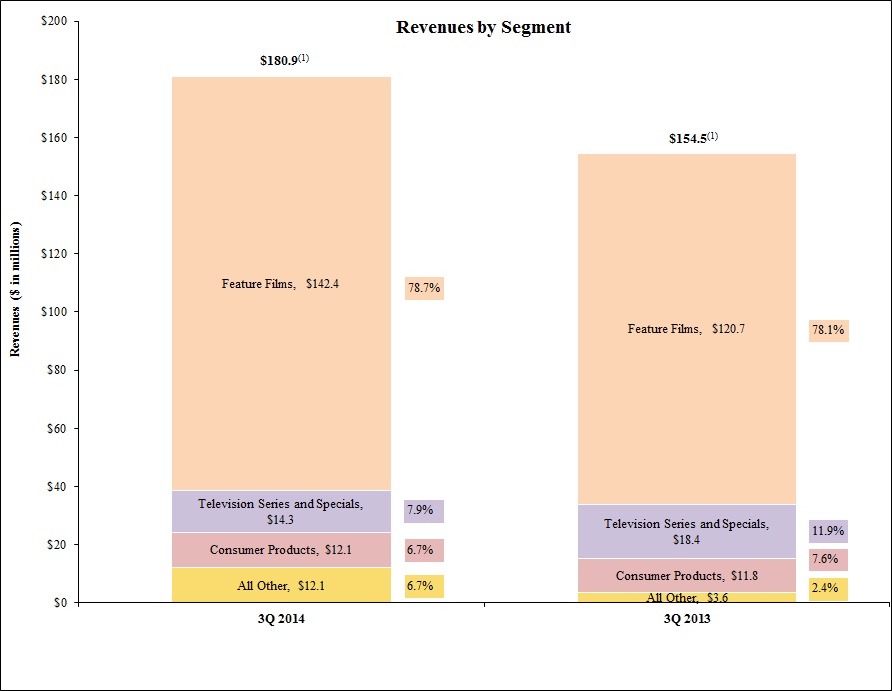

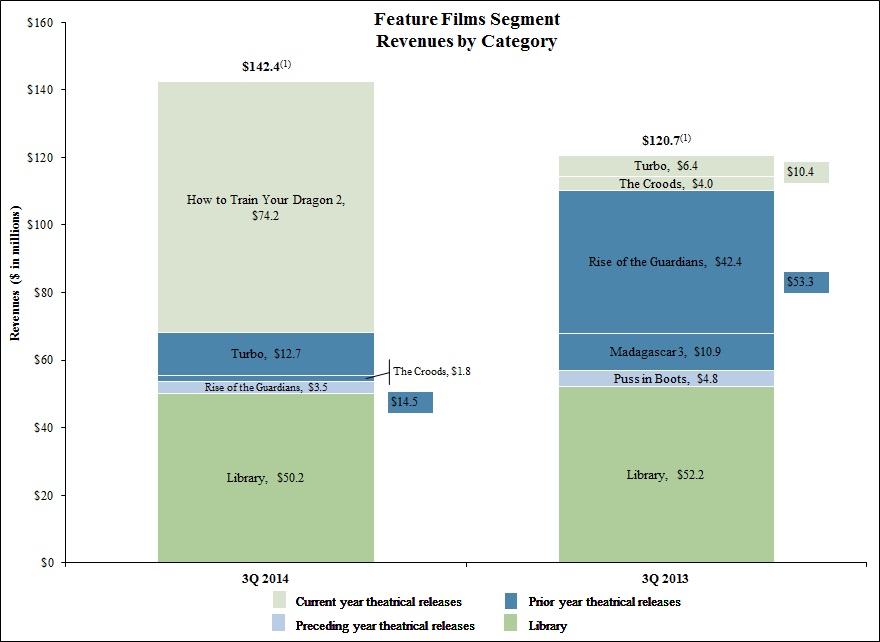

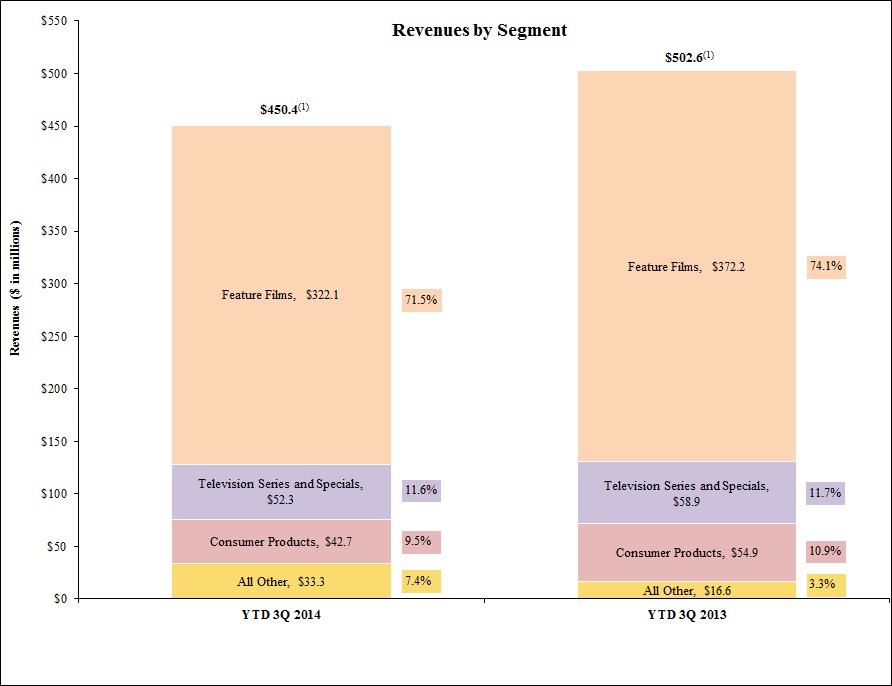

Feature Films | $ | 142,410 | $ | 120,742 | $ | 322,132 | $ | 372,188 | ||||||||

Television Series and Specials | 14,322 | 18,376 | 52,241 | 58,875 | ||||||||||||

Consumer Products | 12,062 | 11,791 | 42,723 | 54,904 | ||||||||||||

All Other | 12,067 | 3,640 | 33,283 | 16,666 | ||||||||||||