Attached files

| file | filename |

|---|---|

| 8-K - 8-K - AVIV REIT, INC. | d811133d8k.htm |

Exhibit 99.1

Third Quarter 2014 Results

| Table of Contents |

||||

| Earnings Release |

1-5 | |||

| Consolidated Statements of Operations |

6 | |||

| Reconciliations of Net Income to EBITDA, Adjusted EBITDA, FFO, Normalized FFO and AFFO |

7 | |||

| Consolidated Balance Sheets |

8 | |||

| Consolidated Statements of Cash Flows |

9-10 | |||

| Portfolio Summary |

11-13 | |||

| Investment Activity |

14 | |||

| Debt Summary and Capitalization |

15 | |||

| Common Share and OP Unit Weighted Average Amounts Outstanding |

16 | |||

| 2014 Guidance |

17 | |||

| Definitions and Footnotes |

18-19 | |||

Note: This earnings release and the related supplemental information contain certain non-GAAP financial measures that we believe are helpful in understanding our business, as further discussed herein. These financial measures, which include Funds From Operations, Normalized Funds From Operations, AFFO, EBITDA and Adjusted EBITDA, should not be considered as an alternative to net income, earnings per share or any other GAAP measurement of performance or as an alternative to cash flows from operating, investing or financing activities. Furthermore, these non-GAAP financial measures are not intended to be a measure of cash flow or liquidity. Information included in this supplemental package is unaudited. For a reconciliation of each such non-GAAP financial measure to the most directly comparable GAAP financial measure, please see page 7.

1

AVIV REIT REPORTS THIRD QUARTER 2014 RESULTS

$403 MILLION OF ACQUISITIONS YEAR-TO-DATE

CHICAGO, IL – October 31, 2014 – Aviv REIT, Inc. (NYSE: AVIV) today reported results for the third quarter ended September 30, 2014. All per share results are reported on a fully diluted basis.

Q3 Highlights

| • | $194.1 million of acquisitions |

| • | $99.8 million of SNF acquisitions at a blended initial cash yield of 9.2% |

| • | $82.0 million of ALF acquisitions at a blended initial cash yield of 8.0% |

| • | $12.3 million acquisition for land and entitlements for future identified new construction ALFs |

| • | Invested $24.6 million for property reinvestment and new construction |

| • | AFFO of $28.8 million, or $0.47 per share, a 9% increase over Q3 2013 |

| • | Adjusted EBITDA of $43.0 million, a 33% increase over Q3 2013 |

| • | Sold five properties for $0.8 million recording a net GAAP loss of $2.5 million |

Q4 Quarter-to-date Highlights

| • | $33.1 million of acquisitions |

| • | $4.6 million acquisition of one SNF at an initial cash yield of 10.0% |

| • | $28.5 million acquisitions of two SNFs at an initial cash yield of 9.0% |

Craig M. Bernfield, Aviv’s Chairman and Chief Executive Officer, said, “We are pleased with our third quarter performance. We have produced a significant volume of attractive investments, completing over $440 million year-to-date, already the most we have ever closed in a calendar year, significantly exceeding the $239 million of investments we completed in 2013. These investments include approximately $400 million of acquisitions and approximately $40 million of reinvestment and new construction projects, which are key to our commitment to owning high quality properties across our portfolio. We continue to acquire high-quality SNFs and ALFs with knowledgeable and experienced operators at attractive valuations, cash yields and coverages, all consistent with our track record. We are working on a number of identified acquisitions and other investments that we expect to close prior to year-end or in early 2015. We believe that we are in a great position to continue to grow given our operator relationships, market presence, liquidity, access to capital and cost of capital.”

Third Quarter 2014 Results

AFFO for the quarter ended September 30, 2014 was $28.8 million, or $0.47 per share, compared to $21.8 million, or $0.43 per share, for the quarter ended September 30, 2013, an increase of 9% per share. The growth in AFFO per share was driven primarily by the Company’s strong acquisition activity offset by the additional shares of common stock issued during the second quarter of 2014.

2

Adjusted EBITDA for the quarter ended September 30, 2014 was $43.0 million, compared to $32.4 million for the quarter ended September 30, 2013, an increase of 33%. Net income for the quarter ended September 30, 2014 was $12.0 million, or $0.20 per share, compared to $10.1 million, or $0.20 per share, for the quarter ended September 30, 2013.

Nine Months 2014 Results

AFFO for the nine months ended September 30, 2014 was $78.3 million, or $1.37 per share, compared to $58.6 million, or $1.28 per share, for the nine months ended September 30, 2013, an increase of 7%. The growth in AFFO per share was driven primarily by the Company’s strong acquisition activity.

Adjusted EBITDA for the nine months ended September 30, 2014 was $120.2 million, compared to $95.2 million for the nine months ended September 30, 2013, an increase of 26%. Net income for the nine months ended September 30, 2014 was $32.0 million, or $0.56 per share, compared to $12.0 million, or $0.26 per share, for the nine months ended September 30, 2013.

Portfolio Update

Acquisitions:

During the third quarter, the Company completed four transactions acquiring 12 properties and two land parcels in 4 states with 3 operators for $194.1 million, comprised of the following:

| • | Three SNFs in Missouri for $16.2 million triple-net leased to existing operator Diversicare at an initial cash yield of 10.0%. |

| • | Two ALFs and one SNF in Massachusetts for $82.0 million triple-net leased to existing operator Maplewood Senior Living, an operator of 12 facilities in three states, at an initial cash yield of 8.0%. |

| • | Two land parcels and entitlements for $12.3 million for future identified new construction ALFs. |

| • | Four post-acute and long-term care SNFs in Washington, an ALF in Washington and a campus in Idaho, which includes a SNF and an ALF, for a total price of $83.6 million. The SNF and ALF properties are triple-net leased to existing Aviv operator EmpRes at a blended initial cash yield of 9.0%. |

During the fourth quarter, the Company completed two transactions acquiring three properties for $33.1 million.

Year-to-date, the Company has completed 18 transactions acquiring 41 properties in 10 states with 9 operators for $403 million at a blended initial cash yield of 9.3%. The Company has also invested $40.6 million through September 30, 2014 for property reinvestment and new construction.

Dispositions:

During the third quarter, the Company sold five properties for $763,000 recording a net GAAP loss of $2.5 million or $0.04 per share. These five properties were previously closed in conjunction with each local existing operator agreeing to continue to pay the remaining contractual rent owed of approximately $6.9 million under the cross-defaulted existing triple-net lease. The Company also recorded an impairment charge of $1.5 million in the third quarter on a property held for sale and expected to sell in the fourth quarter.

Year-to-date, the Company sold seven properties for $1.4 million recording $0.9 million of impairments and a net GAAP loss of $2.5 million related to such sales. Five of the seven properties were previously closed in conjunction with each local existing operator agreeing to continue to pay the remaining contractual rent owed of approximately $6.9 million under the cross-defaulted existing triple-net lease.

3

Balance Sheet and Liquidity

As of September 30, 2014, the Company had $16 million of cash, $425 million of availability on its $600 million unsecured credit facility and a net debt to Adjusted EBITDA ratio of 4.8. As of today, the Company has $220 million outstanding under its credit facility.

Dividends

On July 29, 2014, the Company announced that its Board of Directors declared a dividend for the third quarter of $0.36 per share. The dividend was paid in cash on October 10, 2014 to stockholders of record on September 26, 2014.

Full Year 2014 AFFO Guidance

The Company is reaffirming its AFFO guidance range of $1.89 to $1.93 per share for the full year 2014. The details underlying this guidance can be found on page 17 of this earnings release and supplemental information.

Conference Call and Webcast Information

In a separate press release issued today, Aviv announced that it has entered into a definitive agreement to merge with Omega Healthcare Investors, Inc.

In lieu of Aviv’s previously scheduled call to discuss third quarter earnings, Omega and Aviv will hold a joint conference call to discuss this transaction today at 8:30 a.m. Eastern Time (7:30 a.m. Central Time). The conference call is being webcast and can be accessed at Omega’s website at www.omegahealthcare.com and at Aviv’s website at www.avivreit.com or by dialing (877) 511-2891 for those within the United States. The Canadian toll-free dial-in number is (855) 669-9657. All other international participants can use the dial-in number (412) 902-4140. Ask the operator to be connected to the “Omega Healthcare Investors, Inc. and Aviv REIT, Inc. Merger Call.” A replay of the webcast will be available at approximately 11:30 a.m. Eastern Time today on Omega and Aviv’s websites or by calling (877) 344-7529, passcode 10055663. The webcast will be archived for 30 days.

About Aviv

Aviv REIT, Inc., based in Chicago, is a real estate investment trust that specializes in owning post-acute and long-term care SNFs and other healthcare properties. Aviv is one of the largest owners of SNFs in the United States and has been in the business for over 30 years. As of today, the Company owns 316 properties that are triple-net leased to 38 operators in 29 states.

For more information about the Company and the proposed merger transaction, please visit our website at www.avivreit.com or contact: Craig M. Bernfield, Chairman & Chief Executive Officer at 312-855-0930.

4

Forward-Looking Statements

The information presented herein includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements provide our current expectations or forecasts of future events. Forward-looking statements include statements about our expectations, beliefs, intentions, plans, objectives, goals, strategies, future events, performance and underlying assumptions and other statements that are not historical facts. Examples of forward-looking statements include all statements regarding our expected future financial position, results of operations, cash flows, liquidity, business strategy, projected growth opportunities and potential acquisitions and plans, objectives of management for future operations and completion of the proposed merger transaction. You can identify forward-looking statements by their use of forward-looking words, such as “may,” “will,” “anticipate,” “expect,” “believe,” “estimate,” “intend,” “plan,” “should,” “seek” or comparable terms, or the negative use of those words, but the absence of these words does not necessarily mean that a statement is not forward-looking.

These forward-looking statements are made based on our current expectations and beliefs concerning future events affecting us and are subject to uncertainties and factors relating to our operations and business environment, all of which are difficult to predict and many of which are beyond our control, that could cause our actual results to differ materially from those matters expressed in or implied by these forward-looking statements. Important factors, risks and uncertainties that could cause actual results to differ materially from our expectations include those disclosed under Part I, Item 1A, “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2013, Part II, Item 1A, “Risk Factors” in our Quarterly Report on Form 10-Q for the period ended March 31, 2014 and elsewhere in filings made by us with the Securities and Exchange Commission (SEC). These factors include, among others: uncertainties relating to the operations of our operators, including those relating to reimbursement by government and other third-party payors, compliance with regulatory requirements and occupancy levels; our ability to successfully engage in strategic acquisitions and investments; competition in the acquisition and ownership of healthcare properties; our ability to monitor our portfolio; environmental liabilities associated with our properties; our ability to re-lease or sell any of our properties; the availability and cost of capital; changes in interest rates; the amount and yield of any additional investments; changes in tax laws and regulations affecting real estate investment trusts (REITs); our ability to maintain our status as a REIT; and the other factors relating to the proposed merger transaction set forth in the press release relating to the proposed merger transaction issued on the date hereof.

There may be additional risks of which we are presently unaware or that we currently deem immaterial. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date as of which such statements are made. Forward-looking statements are not guarantees of future performance. Except as required by law, we do not undertake any responsibility to release publicly any revisions to these forward-looking statements to take into account events or circumstances that occur after the date as of which such statements are made or to update you on the occurrence of any unanticipated events which may cause actual results to differ from those expressed or implied by the forward-looking statements contained herein.

Additional Information about the Proposed Transaction and Where to Find It

This press release does not constitute an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any proxy, vote or approval. In connection with the proposed transaction, Omega and Aviv expect to prepare and file with the SEC a registration statement on Form S-4 containing a joint proxy statement/prospectus and other documents with respect to Omega’s proposed acquisition of Aviv. INVESTORS ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS (INCLUDING ALL AMENDMENTS AND SUPPLEMENTS THERETO) AND OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED TRANSACTION.

Investors may obtain free copies of the registration statement, the joint proxy statement/prospectus and other relevant documents filed by Omega and Aviv with the SEC (if and when they become available) through the website maintained by the SEC at www.sec.gov. Copies of the documents filed by Omega with the SEC will also be available free of charge on Omega’s website at www.omegahealthcare.com and copies of the documents filed by Aviv with the SEC are available free of charge on Aviv’s website at www.avivreit.com.

Omega, Aviv and their respective directors and executive officers may be deemed to be participants in the solicitation of proxies from Omega’s and Aviv’s shareholders in respect of the proposed transaction. Information regarding Omega’s directors and executive officers can be found in Omega’s definitive proxy statement filed with the SEC on April 29, 2014. Information regarding Aviv’s directors and executive officers can be found in Aviv’s definitive proxy statement filed with the SEC on April 15, 2014. Additional information regarding the interests of such potential participants will be included in the joint proxy statement/prospectus and other relevant documents filed with the SEC in connection with the proposed transaction if and when they become available. These documents are available free of charge on the SEC’s website and from Omega and Aviv, as applicable, using the sources indicated above.

5

Aviv REIT, Inc.

Consolidated Statements of Operations

(unaudited, in thousands except share and per share data)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Revenues |

||||||||||||||||

| Rental income |

$ | 46,079 | $ | 31,693 | $ | 127,941 | $ | 99,206 | ||||||||

| Interest on loans and financing lease |

1,101 | 1,131 | 3,263 | 3,272 | ||||||||||||

| Interest and other income |

191 | 49 | 1,232 | 128 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

47,371 | 32,873 | 132,436 | 102,606 | ||||||||||||

| Expenses |

||||||||||||||||

| Interest expense incurred |

12,376 | 8,577 | 36,489 | 29,599 | ||||||||||||

| Amortization of deferred financing costs |

988 | 810 | 2,944 | 2,516 | ||||||||||||

| Depreciation and amortization |

11,522 | 8,302 | 31,470 | 24,399 | ||||||||||||

| General and administrative |

5,296 | 4,041 | 16,960 | 21,150 | ||||||||||||

| Transaction costs |

1,220 | 1,036 | 3,813 | 1,906 | ||||||||||||

| Loss on impairment |

1,479 | — | 2,341 | — | ||||||||||||

| Reserve for uncollectible loans and other receivables |

9 | 27 | 3,509 | 57 | ||||||||||||

| Loss (gain) on sale of assets, net |

2,445 | 13 | 2,458 | (26 | ) | |||||||||||

| Loss on extinguishment of debt |

— | — | 501 | 10,974 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total expenses |

35,336 | 22,806 | 100,485 | 90,575 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

12,035 | 10,067 | 31,951 | 12,031 | ||||||||||||

| Net income allocable to noncontrolling interests - operating partnership |

(2,344 | ) | (2,446 | ) | (6,662 | ) | (3,236 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income allocable to common stockholders |

$ | 9,691 | $ | 7,621 | $ | 25,289 | $ | 8,795 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings per common share: |

||||||||||||||||

| Basic: |

||||||||||||||||

| Net income allocable to common stockholders |

$ | 0.21 | $ | 0.20 | $ | 0.58 | $ | 0.27 | ||||||||

| Diluted: |

||||||||||||||||

| Net income allocable to common stockholders |

$ | 0.20 | $ | 0.20 | $ | 0.56 | $ | 0.26 | ||||||||

| Weighted average common shares outstanding: |

||||||||||||||||

| Basic |

47,213,612 | 37,271,714 | 43,576,705 | 32,408,843 | ||||||||||||

| Diluted |

60,967,867 | 50,838,529 | 57,127,784 | 42,101,077 | ||||||||||||

| Dividends declared per common share |

$ | 0.36 | $ | 0.36 | $ | 1.08 | $ | 0.744 | ||||||||

6

Aviv REIT, Inc.

Reconciliations of Net Income to EBITDA and Adjusted EBITDA1

(unaudited, in thousands)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Net income |

$ | 12,035 | $ | 10,067 | $ | 31,951 | $ | 12,031 | ||||||||

| Interest expense, net |

12,376 | 8,577 | 36,488 | 29,598 | ||||||||||||

| Amortization of deferred financing costs |

988 | 810 | 2,944 | 2,516 | ||||||||||||

| Depreciation and amortization |

11,522 | 8,302 | 31,470 | 24,399 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| EBITDA |

36,921 | 27,756 | 102,853 | 68,544 | ||||||||||||

| Loss on impairment |

1,479 | — | 2,341 | — | ||||||||||||

| Loss (gain) on sale of assets, net |

2,445 | 13 | 2,458 | (26 | ) | |||||||||||

| Transaction costs |

1,220 | 1,210 | 3,813 | 1,906 | ||||||||||||

| Write-off of straight-line rents |

— | 2,887 | 1,380 | 2,887 | ||||||||||||

| Non-cash stock-based compensation |

970 | 535 | 3,602 | 10,930 | ||||||||||||

| Loss on extinguishment of debt |

— | — | 501 | 10,974 | ||||||||||||

| Reserve for uncollectible loan receivables |

— | — | 3,211 | 11 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 43,035 | $ | 32,401 | $ | 120,159 | $ | 95,226 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | See definitions and footnotes on pages 18 and 19 |

Aviv REIT, Inc.

Reconciliations of Net Income to FFO, Normalized FFO and AFFO1

(unaudited, in thousands except per share data)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2014 | 2013 | 2014 | 2013 | |||||||||||||

| Net income |

$ | 12,035 | $ | 10,067 | $ | 31,951 | $ | 12,031 | ||||||||

| Depreciation and amortization |

11,522 | 8,302 | 31,470 | 24,399 | ||||||||||||

| Loss on impairment |

1,479 | — | 2,341 | — | ||||||||||||

| Loss (gain) on sale of assets, net |

2,445 | 13 | 2,458 | (26 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| FFO |

27,481 | 18,382 | 68,220 | 36,404 | ||||||||||||

| Loss on extinguishment of debt |

— | — | 501 | 10,974 | ||||||||||||

| Reserve for uncollectible loan receivables |

— | — | 3,211 | 11 | ||||||||||||

| Transaction costs |

1,220 | 1,210 | 3,813 | 1,906 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Normalized FFO |

28,701 | 19,592 | 75,745 | 49,295 | ||||||||||||

| Amortization of deferred financing costs |

988 | 810 | 2,944 | 2,516 | ||||||||||||

| Non-cash stock-based compensation |

970 | 535 | 3,602 | 10,930 | ||||||||||||

| Straight-line rental income, net |

(1,727 | ) | 1,227 | (3,420 | ) | (2,998 | ) | |||||||||

| Rental income from intangible amortization, net |

(132 | ) | (365 | ) | (539 | ) | (1,097 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| AFFO |

$ | 28,800 | $ | 21,799 | $ | 78,332 | $ | 58,646 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common shares and units outstanding, basic |

58,633 | 49,210 | 55,055 | 44,347 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average common shares and units outstanding, diluted |

60,968 | 50,839 | 57,128 | 45,818 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| AFFO per share and unit, basic |

$ | 0.49 | $ | 0.44 | $ | 1.42 | $ | 1.32 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| AFFO per share and unit, diluted |

$ | 0.47 | $ | 0.43 | $ | 1.37 | $ | 1.28 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | See definitions and footnotes on pages 18 and 19 |

7

Aviv REIT, Inc.

Consolidated Balance Sheets

(unaudited, in thousands except share data)

| September 30, 2014 |

December 31, 2013 |

|||||||

| Assets |

||||||||

| Income producing property |

||||||||

| Land |

$ | 171,098 | $ | 138,150 | ||||

| Buildings and improvements |

1,498,117 | 1,138,173 | ||||||

| Assets under direct financing leases |

11,262 | 11,175 | ||||||

|

|

|

|

|

|||||

| 1,680,477 | 1,287,498 | |||||||

| Less accumulated depreciation |

(175,983 | ) | (147,302 | ) | ||||

| Construction in progress and land held for development |

34,421 | 23,292 | ||||||

|

|

|

|

|

|||||

| Net real estate |

1,538,915 | 1,163,488 | ||||||

| Cash and cash equivalents |

15,834 | 50,764 | ||||||

| Straight-line rent receivable, net |

44,000 | 40,580 | ||||||

| Tenant receivables, net |

2,011 | 1,647 | ||||||

| Deferred finance costs, net |

17,651 | 16,643 | ||||||

| Loan receivables, net |

43,272 | 41,686 | ||||||

| Other assets |

15,805 | 15,625 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 1,677,488 | $ | 1,330,433 | ||||

|

|

|

|

|

|||||

| Liabilities and equity |

||||||||

| Secured loan |

$ | 13,478 | $ | 13,654 | ||||

| Unsecured notes payable |

652,410 | 652,752 | ||||||

| Line of credit |

175,000 | 20,000 | ||||||

| Accrued interest payable |

10,903 | 15,284 | ||||||

| Dividends and distributions payable |

21,078 | 17,694 | ||||||

| Accounts payable and accrued expenses |

11,894 | 10,555 | ||||||

| Tenant security and escrow deposits |

24,066 | 21,586 | ||||||

| Other liabilities |

10,419 | 10,463 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

919,248 | 761,988 | ||||||

| Equity: |

||||||||

| Stockholders’ equity |

||||||||

| Common stock (par value $0.01; 47,216,963 and 37,593,910 shares issued and outstanding, as of September 30, 2014 and December 31, 2013, respectively) |

472 | 376 | ||||||

| Additional paid-in-capital |

722,030 | 523,658 | ||||||

| Accumulated deficit |

(112,119 | ) | (89,742 | ) | ||||

|

|

|

|

|

|||||

| Total stockholders’ equity |

610,383 | 434,292 | ||||||

| Noncontrolling interests - operating partnership |

147,857 | 134,153 | ||||||

|

|

|

|

|

|||||

| Total equity |

758,240 | 568,445 | ||||||

|

|

|

|

|

|||||

| Total liabilities and equity |

$ | 1,677,488 | $ | 1,330,433 | ||||

|

|

|

|

|

|||||

8

Aviv REIT, Inc.

Consolidated Statements of Cash Flows

(unaudited, in thousands)

| Nine Months Ended September 30, | ||||||||

| 2014 | 2013 | |||||||

| Operating activities |

||||||||

| Net income |

$ | 31,951 | $ | 12,031 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

31,470 | 24,399 | ||||||

| Amortization of deferred financing costs |

2,944 | 2,516 | ||||||

| Accretion of debt premium |

(401 | ) | (377 | ) | ||||

| Straight-line rental income, net |

(3,420 | ) | (2,998 | ) | ||||

| Rental income from intangible amortization, net |

(539 | ) | (1,097 | ) | ||||

| Non-cash stock-based compensation |

3,602 | 10,930 | ||||||

| Loss (gain) on sale of assets, net |

2,458 | (26 | ) | |||||

| Non-cash loss on extinguishment of debt |

494 | 5,161 | ||||||

| Loss on impairment |

2,341 | — | ||||||

| Reserve for uncollectible loan and other receivables |

3,509 | 57 | ||||||

| Changes in assets and liabilities: |

||||||||

| Tenant receivables |

(662 | ) | (3,785 | ) | ||||

| Other assets |

(545 | ) | 1,058 | |||||

| Accounts payable and accrued expenses |

(6,395 | ) | (9,468 | ) | ||||

| Tenant security deposits and other liabilities |

3,281 | (2,006 | ) | |||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

70,088 | 36,395 | ||||||

| Investing activities |

||||||||

| Purchase of real estate |

(368,870 | ) | (38,076 | ) | ||||

| Proceeds from sales of real estate , net |

1,337 | 4,842 | ||||||

| Capital improvements |

(10,293 | ) | (9,909 | ) | ||||

| Development projects |

(30,316 | ) | (14,380 | ) | ||||

| Loan receivables received from others |

7,613 | 3,222 | ||||||

| Loan receivables funded to others |

(12,410 | ) | (2,707 | ) | ||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(412,939 | ) | (57,008 | ) | ||||

9

Aviv REIT, Inc.

Consolidated Statements of Cash Flows (continued)

(unaudited, in thousands)

| Nine Months Ended September 30, | ||||||||

| 2014 | 2013 | |||||||

| Financing activities |

||||||||

| Borrowings of debt |

$ | 283,000 | $ | 160,000 | ||||

| Repayment of debt |

(128,117 | ) | (353,203 | ) | ||||

| Payment of financing costs |

(4,588 | ) | (5,290 | ) | ||||

| Capital contributions |

60 | 425 | ||||||

| Proceeds from issuance of common stock |

221,720 | 303,600 | ||||||

| Cost of raising capital |

(10,551 | ) | (25,380 | ) | ||||

| Shares issued for settlement of vested stock and exercised stock options, net |

3,053 | — | ||||||

| Cash distributions to partners |

(12,449 | ) | (16,276 | ) | ||||

| Cash dividends to stockholders |

(44,207 | ) | (48,907 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by financing activities |

307,921 | 14,969 | ||||||

|

|

|

|

|

|||||

| Net decrease in cash and cash equivalents |

(34,930 | ) | (5,644 | ) | ||||

| Cash and cash equivalents: |

||||||||

| Beginning of period |

50,764 | 17,876 | ||||||

|

|

|

|

|

|||||

| End of period |

$ | 15,834 | $ | 12,232 | ||||

|

|

|

|

|

|||||

| Supplemental cash flow information |

||||||||

| Cash paid for interest |

$ | 41,728 | $ | 39,645 | ||||

| Supplemental disclosure of noncash activity |

||||||||

| Accrued dividends payable to stockholders |

$ | 17,009 | $ | — | ||||

| Accrued distributions payable to partners |

$ | 4,069 | $ | — | ||||

| Write-off of straight-line rent receivable |

$ | 1,380 | $ | 2,887 | ||||

| Write-off of deferred financing costs, net |

$ | 501 | $ | 5,161 | ||||

10

Aviv REIT, Inc.

Portfolio Summary1

Portfolio Composition

| Property Type |

Property Count |

Number of Beds |

Square Feet |

Investment (GBV) |

Annualized Cash Rent |

% of Total Rent |

||||||||||||||||||

| Skilled Nursing |

260 | 23,937 | 9,243 | $ | 1,359,715 | $ | 157,450 | 84.3 | % | |||||||||||||||

| Senior Housing |

32 | 2,387 | 1,573 | 263,038 | 23,550 | 12.6 | % | |||||||||||||||||

| Other Healthcare Properties |

21 | 196 | 218 | 57,724 | 5,766 | 3.1 | % | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

313 | 26,520 | 11,034 | $ | 1,680,477 | $ | 186,766 | 100.0 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Portfolio Performance

| EBITDARM Coverage |

EBITDAR Coverage |

Occupancy | Facility Revenue Mix | EBITDAR Margin |

||||||||||||||||||||||||

| Core Portfolio |

Private Pay | Medicare | Medicaid | |||||||||||||||||||||||||

| Skilled Nursing |

1.80x | 1.40x | 77.8 | % | 20.3 | % | 24.5 | % | 55.2 | % | 14.0 | % | ||||||||||||||||

| Senior Housing |

1.26x | 1.07x | 78.8 | % | 85.0 | % | 4.4 | % | 10.7 | % | 23.5 | % | ||||||||||||||||

| Other Healthcare Properties |

7.00x | 6.26x | 86.9 | % | 93.4 | % | 6.6 | % | 0.0 | % | 34.0 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total |

1.84x | 1.45x | 78.0 | % | 25.2 | % | 23.2 | % | 51.7 | % | 15.0 | % | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

State Diversification

| Investment | Annualized Rent | |||||||||||||||

| State |

Properties | (GBV) | $ | % | ||||||||||||

| Texas |

67 | $ | 288,900 | $ | 34,215 | 18.3 | % | |||||||||

| California |

39 | 182,048 | 20,999 | 11.2 | % | |||||||||||

| Ohio |

27 | 192,979 | 20,953 | 11.2 | % | |||||||||||

| Washington |

15 | 122,325 | 10,396 | 5.6 | % | |||||||||||

| Massachusetts |

10 | 88,118 | 9,837 | 5.3 | % | |||||||||||

| Pennsylvania |

10 | 79,654 | 9,361 | 5.0 | % | |||||||||||

| Missouri |

18 | 93,030 | 9,307 | 5.0 | % | |||||||||||

| Connecticut |

6 | 83,463 | 9,236 | 4.9 | % | |||||||||||

| Kentucky |

10 | 60,109 | 6,545 | 3.5 | % | |||||||||||

| Arkansas |

10 | 54,517 | 5,915 | 3.2 | % | |||||||||||

| Other 19 States |

101 | 435,334 | 50,002 | 26.8 | % | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 313 | $ | 1,680,477 | $ | 186,766 | 100.0 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Operator Diversification

| Properties | Investment (GBV) |

Annualized Rent | ||||||||||||||||||||||

| Operator (Location) |

Aviv | Total | $ | % | States | |||||||||||||||||||

| Daybreak (Denton, TX) |

51 | 69 | $ | 166,339 | $ | 22,013 | 11.8 | % | 2 | |||||||||||||||

| Saber (Bedford Heights, OH) |

30 | 79 | 185,908 | 21,320 | 11.4 | % | 6 | |||||||||||||||||

| EmpRes (Vancouver, WA) |

23 | 49 | 196,256 | 20,333 | 10.9 | % | 6 | |||||||||||||||||

| Maplewood (Westport, CT) |

12 | 12 | 176,632 | 16,632 | 8.9 | % | 3 | |||||||||||||||||

| Fundamental (Sparks, MD) |

17 | 75 | 148,754 | 14,310 | 7.7 | % | 8 | |||||||||||||||||

| Preferred Care (Plano, TX) |

17 | 111 | 68,982 | 10,701 | 5.7 | % | 12 | |||||||||||||||||

| Sun Mar (Brea, CA) |

13 | 25 | 71,122 | 9,121 | 4.9 | % | 1 | |||||||||||||||||

| Diversicare (Brentwood, TN) |

12 | 52 | 90,521 | 9,094 | 4.9 | % | 9 | |||||||||||||||||

| Providence (National City, CA) |

10 | 13 | 48,350 | 5,258 | 2.8 | % | 2 | |||||||||||||||||

| Deseret (Bountiful, UT) |

17 | 28 | 37,623 | 4,941 | 2.6 | % | 5 | |||||||||||||||||

| Other 28 Operators |

111 | 402 | 489,990 | 53,045 | 28.4 | % | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| 313 | 915 | $ | 1,680,477 | $ | 186,766 | 100.0 | % | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| (1) | Dollars and square feet in thousands. Data as of September 30, 2014. Coverage, occupancy, margin and revenue mix information is provided on a trailing twelve month basis through June 30, 2014. Annualized cash rent for leases in place as of September 30, 2014 and includes income from a deferred financing lease. |

Totals may not add due to rounding.

11

Aviv REIT, Inc.

Portfolio Summary

State Occupancy1

| State |

Aviv Occupancy |

State Average |

Variance | |||||||||

| Texas |

72.9 | % | 72.2 | % | 0.7 | % | ||||||

| California |

91.5 | % | 85.0 | % | 6.5 | % | ||||||

| Ohio |

76.1 | % | 84.2 | % | (8.1 | %) | ||||||

| Washington |

85.1 | % | 80.5 | % | 4.6 | % | ||||||

| Massachusetts |

90.7 | % | 86.9 | % | 3.8 | % | ||||||

| Pennsylvania |

85.4 | % | 90.2 | % | (4.8 | %) | ||||||

| Missouri |

70.6 | % | 71.7 | % | (1.1 | %) | ||||||

| Connecticut |

98.2 | % | NA | NA | ||||||||

| Kentucky |

83.9 | % | 87.6 | % | (3.7 | %) | ||||||

| Arkansas |

71.8 | % | 71.4 | % | 0.4 | % | ||||||

Lease Maturity Schedule2

| Year |

Number of Properties |

% of Total Rent |

||||||

| 2014 |

0 | 0.0 | % | |||||

| 2015 |

4 | 0.9 | % | |||||

| 2016 |

3 | 1.3 | % | |||||

| 2017 |

16 | 3.1 | % | |||||

| 2018 |

29 | 9.8 | % | |||||

| Thereafter |

258 | 84.9 | % | |||||

|

|

|

|

|

|||||

| Total |

310 | 100.0 | % | |||||

|

|

|

|

|

|||||

| (1) | Occupancy information as of June 30, 2014. State occupancy represents nursing facility occupancies per American Health Care Association. Aviv only has assisted living properties in Connecticut. |

| (2) | Excludes three development properties with rent start dates in the future. |

12

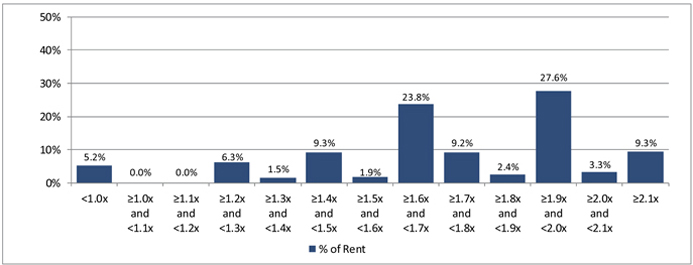

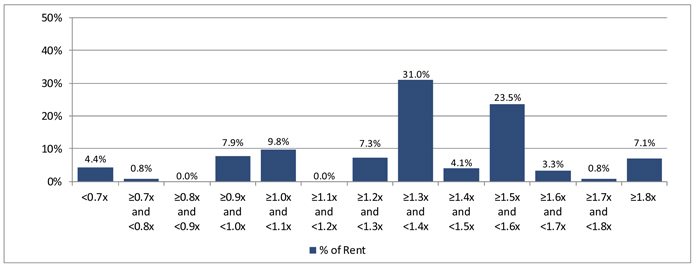

Aviv REIT, Inc.

Portfolio Summary as of September 30, 2014

EBITDARM Coverage Distribution

EBITDAR (4% Mgmt Fee) Coverage Distribution

13

Aviv REIT, Inc.

Investment Activity as of September 30, 2014

(in thousands)

2014 Property Reinvestment and New Construction

| Period |

Property Reinvestment |

New Construction |

Total | |||||||||

| Third quarter |

$ | 5,027 | $ | 19,597 | $ | 24,624 | ||||||

| Second quarter |

3,422 | 5,023 | 8,445 | |||||||||

| First quarter |

1,844 | 5,696 | 7,540 | |||||||||

|

|

|

|||||||||||

| $ | 40,609 | |||||||||||

|

|

|

|||||||||||

New Construction Projects

| Operator - Location |

Property Type |

Beds | Expected Opening Date |

Construction in Progress at 9/30/2014 |

Remaining Costs to be Spent |

Total Expected Cost |

Expected Yield |

|||||||||||||||

| Maplewood - Bethel, CT |

ALF | 80 | Q1 2015 | $ | 16,550 | $ | 3,715 | $ | 20,265 | 9.5 | % | |||||||||||

| Care Meridian - numerous locations |

— | — | — | 628 | 3,084 | 3,712 | 9.5 | % | ||||||||||||||

| Property reinvestment - numerous locations |

— | — | — | 1,540 | 1,840 | 3,380 | — | |||||||||||||||

| Land held for development |

— | — | — | 15,703 | — | 15,703 | — | |||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||

| Total |

$ | 34,421 | $ | 8,639 | $ | 43,060 | ||||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||||

2014 Acquisitions

| Period |

Property Type | Location | Beds | Amount | Initial Cash Yield |

|||||||||||

| Third quarter1 |

SNF, ALF | 2 states | 1,420 | $ | 181,800 | 8.7 | % | |||||||||

| Second quarter |

SNF | 4 states | 1,110 | 82,650 | 9.8 | % | ||||||||||

| First quarter |

SNF, ALF, ILF | 4 states | 1,497 | 104,420 | 10.0 | % | ||||||||||

|

|

|

|

|

|

|

|||||||||||

| Total |

4,027 | $ | 368,870 | 9.3 | % | |||||||||||

|

|

|

|

|

|

|

|||||||||||

| (1) | Excludes $12.3 million paid for two land parcels and entitlements for the construction of two ALFs and a 50-unit expansion to an existing ALF. |

14

Aviv REIT, Inc.

Debt Summary and Capitalization as of September 30, 2014

Debt Maturities

| Year |

Senior Unsecured Notes |

Line of Credit | Mortgage Debt |

Total Debt |

||||||||||||

| 2014 |

$ | — | $ | — | $ | 40 | $ | 40 | ||||||||

| 2015 |

— | — | 165 | 165 | ||||||||||||

| 2016 |

— | — | 174 | 174 | ||||||||||||

| 2017 |

— | — | 183 | 183 | ||||||||||||

| 2018 |

— | 175,000 | 192 | 175,192 | ||||||||||||

| Thereafter |

650,000 | — | 10,367 | 660,367 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Subtotal |

650,000 | 175,000 | 11,121 | 836,121 | ||||||||||||

| (Discounts) and premiums, net |

2,410 | — | 2,357 | 4,767 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total debt |

$ | 652,410 | $ | 175,000 | $ | 13,478 | $ | 840,888 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted average interest rate |

6.0 | % | ||||||||||||||

|

|

|

|||||||||||||||

| Weighted average maturity in years |

5.4 | |||||||||||||||

|

|

|

|||||||||||||||

Fixed and Floating Rate Debt

| Amount | % of Total | |||||||

| Fixed rate debt |

||||||||

| Senior unsecured notes |

$ | 652,410 | 77.6 | % | ||||

| Mortgage debt |

13,478 | 1.6 | % | |||||

|

|

|

|

|

|||||

| Total fixed rate debt |

665,888 | 79.2 | % | |||||

| Floating rate debt |

||||||||

| Revolver |

175,000 | 20.8 | % | |||||

|

|

|

|

|

|||||

| Total debt |

$ | 840,888 | 100.0 | % | ||||

|

|

|

|

|

|||||

Covenants for Senior Unsecured Notes1

| Covenant |

Requirement | Q3 2014 | Q4 2013 | |||||||

| Total debt / total assets |

No greater than 60% | 45 | % | 46 | % | |||||

| Secured debt / total assets |

No greater than 40% | 1 | % | 2 | % | |||||

| Interest coverage |

No less than 2.00x | 3.20x | 3.16x | |||||||

| Unencumbered assets / unsecured debt |

No less than 150% | 212 | % | 185 | % | |||||

Total Market Capitalization

| Shares/units Outstanding |

9/30/2014 Closing Price |

Value | ||||||||||

| Common stock and OP units |

58,665 | $ | 26.35 | $ | 1,545,823 | |||||||

| Total debt |

840,888 | |||||||||||

|

|

|

|||||||||||

| Total market capitalization |

$ | 2,386,710 | ||||||||||

|

|

|

|||||||||||

Dollars and shares/units in thousands

| (1) | Covenants are calculated in accordance with the indenture governing the senior unsecured notes. |

15

Aviv REIT, Inc.

Common Share and OP Unit

Weighted Average Amounts Outstanding

| Q3 2014 | Q3 2013 | YTD Q3 2014 |

YTD Q3 2013 |

|||||||||||||

| Weighted Average Amounts Outstanding for EPS Purposes: |

||||||||||||||||

| Common shares - basic |

47,213,612 | 37,271,714 | 43,576,705 | 32,408,843 | ||||||||||||

| Effect of dilutive securities: |

||||||||||||||||

| OP units |

11,419,777 | 11,938,420 | 11,478,543 | 8,221,330 | ||||||||||||

| Stock options |

2,155,075 | 1,599,302 | 1,953,632 | 1,454,735 | ||||||||||||

| Restricted stock units |

179,403 | 29,093 | 118,904 | 16,169 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total common shares - diluted |

60,967,867 | 50,838,529 | 57,127,784 | 42,101,077 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Weighted Average Amounts Outstanding for FFO, Normalized FFO and AFFO Purposes: |

||||||||||||||||

| Common shares - basic |

47,213,612 | 37,271,714 | 43,576,705 | 32,408,843 | ||||||||||||

| OP units |

11,419,777 | 11,938,420 | 11,478,543 | 11,938,420 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total common shares and OP units |

58,633,389 | 49,210,134 | 55,055,248 | 44,347,263 | ||||||||||||

| Effect of dilutive securities: |

||||||||||||||||

| Stock options |

2,155,075 | 1,599,302 | 1,953,632 | 1,454,735 | ||||||||||||

| Restricted stock units |

179,403 | 29,093 | 118,904 | 16,169 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total common shares and units - diluted |

60,967,867 | 50,838,529 | 57,127,784 | 45,818,167 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Period Ending Amounts Outstanding: |

||||||||||||||||

| Common shares (includes restricted stock) |

47,248,463 | 37,319,023 | ||||||||||||||

| OP units |

11,416,426 | 11,938,420 | ||||||||||||||

|

|

|

|

|

|||||||||||||

| Total common shares and units |

58,664,889 | 49,257,443 | ||||||||||||||

|

|

|

|

|

|||||||||||||

16

Aviv REIT, Inc.

2014 Guidance

| Expected 2014 Per Share | ||

| Per diluted common share: |

||

| Net income |

$0.86 - $0.90 | |

| Depreciation and amortization |

0.75 | |

| Loss on impairment |

0.04 | |

| Loss on sale of assets, net |

0.04 | |

|

| ||

| FFO |

$1.69 - $1.73 | |

| Loss on extinguishment of debt |

0.01 | |

| Reserve for uncollectible loan receivables |

0.06 | |

| Transaction costs |

0.07 | |

|

| ||

| Normalized FFO |

$1.83 - $1.87 | |

| Amortization of deferred financing costs |

0.07 | |

| Non-cash stock-based compensation |

0.08 | |

| Straight-line rental income, net |

(0.08) | |

| Rental income from intangible amortization, net |

(0.01) | |

|

| ||

| AFFO |

$1.89 - $1.93 | |

|

| ||

| Weighted average common shares and units - diluted |

58.2 million | |

17

Aviv REIT, Inc.

Definitions and Footnotes

EBITDARM Coverage: Represents EBITDARM, which the Company defines as earnings before interest, taxes, depreciation, amortization, rent expense and management fees allocated by the operator to one of its affiliates, of our operators for the applicable period, divided by the rent paid to the Company by its operators during each period.

EBITDAR Coverage: Represents EBITDAR, which the Company defines as earnings before interest, taxes, depreciation, amortization and rent expense, of its operators for the applicable period, divided by the rent paid to Aviv by its operators during such period. Assumes a management fee of 4%.

EBITDAR Margin: Represents the operator’s EBITDAR for the applicable period divided by the operator’s total revenue for the applicable period.

Enterprise Value: Represents equity market capitalization plus net debt. Equity market capitalization is calculated as the number of shares of common stock and units multiplied by the closing price of the Company’s common stock on the last day of the period presented. Net debt represents total debt less cash and cash equivalents.

Portfolio Occupancy: Represents the average daily number of beds at the Company’s properties that are occupied during the applicable period divided by the total number of beds at the Company’s properties that are available for use during the applicable period.

Property Type: ALF = assisted living facility; LTACH = long-term acute care hospital; MOB = medical office building; TBI = traumatic brain injury facility; SNF = skilled nursing facility

State Average Occupancy: Represents the Nursing Facility State Occupancy Rate as reported by American Health Care Association (AHCA). AHCA occupancy data is calculated by dividing the sum of all facility patients in the state occupying certified beds by the sum of all the certified beds in the state reported at the time of the survey corresponding to the period presented. Aviv occupancy represents the state occupancy for the entire portfolio.

Yield: Represents annualized contractual or projected income to be received in cash divided by investment amount.

Portfolio metrics and other statistics are not derived from Aviv’s financial statements but are operating statistics that the Company derives from reports that it receives from its operators pursuant to Aviv’s triple-net leases. As a result, the Company’s portfolio metrics typically lag its own financial statements by approximately one quarter. In order to determine Aviv’s portfolio metrics for the period presented, the metrics are stated only with respect to properties owned by the Company and operated by the same operator for the portion of the period Aviv owned the properties and exclude assets held for sale, closed properties, properties under construction and, with certain exceptions for shorter periods, properties within 24 months of completion of construction. Accordingly, EBITDARM coverage, EBITDAR coverage, EBITDAR margin, portfolio occupancy and quality mix for the twelve months ended June 30, 2014 included 277 core properties of the 304 properties in the Company’s portfolio as of June 30, 2014.

When Aviv refers to the “total rent” of its portfolio, the Company is referring to the total monthly rent due under all of its triple-net leases as of the date specified, calculated based on the first full month following the specified date. Aviv calculates “annualized rent” for properties during a period by utilizing the amount of rent under contract as of the last day of the period and assume that amount of rent was received in respect of such property throughout the entire period.

Non-GAAP Financial Measures

In addition to the results of operations presented in this release, we use financial measures in this release that are derived on the basis of methodologies other than in accordance with United States generally accepted accounting principles (GAAP). We derive these non-GAAP measures as follows:

| • | FFO is defined by the National Association of Real Estate Investment Trusts, or NAREIT, as net income (computed in accordance with GAAP), excluding gains and losses from sales of property (net) and impairments of depreciated real estate, plus real estate depreciation and amortization (excluding amortization of deferred financing costs) and after adjustments for unconsolidated partnerships and joint ventures. Applying the NAREIT definition to our financial statements results in FFO representing net income before depreciation and amortization, loss on impairment, and gain (loss) on sale of assets (net). |

| • | Normalized FFO represents FFO before loss on extinguishment of debt, reserve for uncollectible loan receivables, transaction costs and severance costs. |

| • | AFFO represents Normalized FFO before amortization of deferred financing costs, non-cash stock-based compensation, straight-line rental income (net) and rental income from intangible amortization (net). |

| • | EBITDA represents net income before interest expense (net), amortization of deferred financing costs and depreciation and amortization. |

| • | Adjusted EBITDA represents EBITDA before loss on impairment of assets, (loss) gain on sale of assets (net), transaction costs, write-off of straight-line rents, non-cash stock-based compensation, loss on extinguishment of debt and reserve for uncollectible loan receivables. |

18

Aviv REIT, Inc.

Definitions and Footnotes

Our management uses FFO, Normalized FFO, AFFO, EBITDA and Adjusted EBITDA as important supplemental measures of our operating performance and liquidity. FFO is intended to exclude GAAP historical cost depreciation and amortization of real estate and related assets, which assumes that the value of real estate assets diminishes ratably over time. Historically, however, real estate values have risen or fallen with market conditions. The term FFO was designed by the real estate industry to address this issue and as an indicator of our ability to incur and service debt. Because FFO, Normalized FFO and AFFO exclude depreciation and amortization unique to real estate, impairment, gains and losses from property dispositions and extraordinary items and because EBITDA and Adjusted EBITDA exclude certain non-cash charges and adjustments and amounts spent on interest and taxes, they provide our management with performance measures that, when compared year over year or with other REITs, reflect the impact to operations from trends in occupancy rates, rental rates, operating costs, development activities and, with respect to FFO, Normalized FFO and AFFO, interest costs, in each case providing perspective not immediately apparent from net income. In addition, we believe that FFO, Normalized FFO, AFFO, EBITDA and Adjusted EBITDA are frequently used by securities analysts, investors and other interested parties in the evaluation of REITs.

We offer these measures to assist the users of our financial statements in assessing our financial performance and liquidity under GAAP, but these measures are non-GAAP measures and should not be considered measures of liquidity, alternatives to net income or indicators of any other performance measure determined in accordance with GAAP, nor are they indicative of funds available to fund our cash needs, including our ability to make payments on our indebtedness. In addition, our calculations of these measures are not necessarily comparable to similar measures as calculated by other companies that do not use the same definition or implementation guidelines or interpret the standards differently from us. Investors should not rely on these measures as a substitute for any GAAP measure, including net income, cash flows provided by operating activities or revenues.

19