Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - WILLIS TOWERS WATSON PLC | d813108d8k.htm |

| EX-99.1 - EX-99.1 - WILLIS TOWERS WATSON PLC | d813108dex991.htm |

THIRD

QUARTER 2014 RESULTS

Willis Group Holdings

October, 2014

Exhibit 99.2 |

Important disclosures regarding forward-looking statements

1

This presentation contains certain “forward-looking statements” within the meaning of

Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of

1934, which are intended to be covered by the safe harbors created by those laws. These

forward-looking statements include information about possible or assumed future results of

our operations.

All statements, other than statements of historical facts, included in this document that address

activities, events or developments that we expect or anticipate may occur in the future,

including such things as our outlook, potential cost savings and accelerated adjusted operating margin

and adjusted earnings per share growth, future capital expenditures, growth in commissions and

fees, business strategies, competitive strengths, goals, the benefits of new initiatives, growth of our business and operations, plans, and references to future

successes are forward-looking statements. Also, when we use the words such as

‘anticipate’, ‘believe’, ‘estimate’, ‘expect’, ‘intend’, ‘plan’, ‘probably’, or similar expressions, we are

making forward-looking statements.

There are important uncertainties, events and factors that could cause our actual results or

performance to differ materially from those in the forward-looking statements contained in

this document, including the following: the impact of any regional, national or global political,

economic, business, competitive, market, environmental or regulatory conditions on our global

business operations; the impact of current global economic conditions on our results of operations and financial condition, including as a result of those associated with the

Eurozone, any insolvencies of or other difficulties experienced by our clients, insurance companies or

financial institutions; our ability to implement and fully realize anticipated benefits of our

new growth strategy and revenue generating initiatives; our ability to implement and realize anticipated benefits of any expense reduction initiative, including our ability to

achieve expected savings from the multi-year operational improvement program as a result of

unexpected costs or delays and demand on managerial, operational and administrative resources

and/or macroeconomic factors affecting the program; changes in the tax or accounting treatment of our operations and fluctuations in our tax rate; volatility or declines in

insurance markets and premiums on which our commissions are based, but which we do not control; our

ability to develop and implement technology solutions and invest in innovative product

offerings in an efficient and effective manner; our ability to continue to manage our significant indebtedness; our ability to compete in our industry; our ability to develop new

products and services; material changes in commercial property and casualty markets generally or the

availability of insurance products or changes in premiums resulting from a catastrophic event,

such as a hurricane; our ability to retain key employees and clients and attract new business; the timing or ability to carry out share repurchases and redemptions;

the timing or ability to carry out refinancing or take other steps to manage our capital and the

limitations in our long-term debt agreements that may restrict our ability to take these

actions; fluctuations in our earnings as a result of potential changes to our valuation allowance(s)

on our deferred tax assets; any fluctuations in exchange and interest rates that could affect

expenses and revenue; the potential costs and difficulties in complying with a wide variety of foreign laws and regulations and any related changes, given the global scope of our

operations; rating agency actions, including a downgrade to our credit rating, that could inhibit our

ability to borrow funds or the pricing thereof and in certain circumstances cause us to offer

to buy back some of our debt; a significant decline in the value of investments that fund our pension plans or changes in our pension plan liabilities or funding obligations; our

ability to achieve anticipated benefits of any acquisition or other transactions in which we may

engage, including any revenue growth or operational efficiencies; our ability to

effectively integrate any acquisition into our business; our inability to exercise full management

control over our associates, such as Gras Savoye; our ability to receive dividends or other

distributions in needed amounts from our subsidiaries; any potential impact from the US healthcare reform legislation; our involvement in and the results of any regulatory

investigations, legal proceedings and other contingencies; underwriting, advisory or reputational

risks associated with non-core operations as well as the potential significant impact our

non-core operations (including the Willis Capital Markets & Advisory operations) can have on

our financial results; our exposure to potential liabilities arising from errors and omissions

and other potential claims against us; the interruption or loss of our information processing systems,

data security breaches or failure to maintain secure information systems; and impairment of the

goodwill in one of our reporting units, in which case we may be required to record significant charges to earnings.

The foregoing list of factors is not exhaustive and new factors may emerge from time to time that

could also affect actual performance and results. For additional information see also

Part I, Item 1A “Risk Factors” included in Willis’ Form 10-K for the year ended

December 31, 2013, and our subsequent filings with the Securities and Exchange Commission. Copies

are available online at http://www.sec.gov or on request from the Company.

Although we believe that the assumptions underlying our forward-looking statements are reasonable,

any of these assumptions, and therefore also the forward-looking statements based on these

assumptions, could themselves prove to be inaccurate. In light of the significant uncertainties inherent in the forward-looking statements included in this presentation,

our inclusion of this information is not a representation or guarantee by us that our objectives and

plans will be achieved. Our forward-looking statements speak only as of the date made

and we will not update these forward-looking statements unless the securities laws require us to do so. In light of these risks, uncertainties and assumptions, the forward-looking

events discussed in this presentation may not occur, and we caution you against unduly relying on

these forward-looking statements. |

Important disclosures regarding non-GAAP measures

This

presentation contains references to

"non-GAAP financial measures" as defined in Regulation G of SEC

rules. We present these measures because we

believe

they

are

of

interest

to

the

investment

community

and

they

provide

additional

meaningful

methods

of

evaluating

certain

aspects

of

the

Company’s operating performance from period to period on a basis that may not

be otherwise apparent on a generally accepted accounting principles (GAAP)

basis. These financial measures should be viewed in addition to, not in lieu of, the Company’s condensed consolidated income statements and

balance

sheet

as

of

the

relevant

date.

Consistent

with

Regulation

G,

a

description

of

such

information

is

provided

below

and

a

reconciliation

of

certain

of

such

items

to

GAAP

information

can

be

found

in

our

periodic

filings

with

the

SEC.

Our

method

of

calculating

these

non-GAAP

financial

measures

may

differ from other companies and therefore comparability may be limited.

Definitions of non-GAAP financial measures

We believe that investors’

understanding of the Company’s performance is enhanced by our disclosure of

the following non-GAAP financial measures. Our method of calculating

these measures may differ from those used by other companies and therefore comparability may be limited.

Organic commissions and fees growth

Organic commissions and fees growth excludes: (i) the impact of foreign currency

translation; (ii) the first twelve months of net commission and fee revenues

generated from acquisitions; and (iii) the net commission and fee revenues related to operations disposed of in each period presented, from

reported commissions and fees growth.

We

believe

organic

growth

in

commissions

and

fees

provides

a

measure

that

the

investment

community

may

find

helpful

in

assessing

the

performance

of

operations that were part of our operations in both the current and prior periods,

and provides a measure against which our businesses may be assessed in the

future. Underlying revenues, underlying total expenses, underlying salaries

and benefits, underlying operating income, underlying EBITDA, underlying net

income and underlying net income per diluted share

Underlying revenues, underlying total expenses, underlying salaries and benefits,

underlying operating income, underlying EBITDA, underlying net income and

underlying net income per diluted share are calculated by excluding the impact of certain items, including foreign currency translation, from

total revenue, total expenses, salaries and benefits, operating income, net (loss)

income and net (loss) income per diluted share, respectively, the most

directly comparable GAAP measures. We believe that excluding these items, as

applicable, from total revenue, total expenses, salaries and benefits,

operating

income

and

net

(loss)

income

and

net

(loss)

income

per

diluted

share,

provides

a

more

complete

and

consistent

comparative

analysis

of

our

results of operations.

2 |

3Q

2014 Underlying EPS growth 3

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 Underlying

business

performance

–

comprising

revenue

and

expense

growth

–

resulted

in

net

$(0.04)

reduction to EPS

Other items -

higher interest expense and tax rate, partly offset by contributions from

Associates and Noncontrolling Interests –

resulted in net $(0.01) reduction to underlying EPS

Underlying EPS down $0.05 cents year over year

Underlying business

performance = $(0.04)

-

Increased tax rate= $(0.01)

-

Associates = $0.01

-

Noncontrolling interests = $0.01

$0.34

$0.09

$(0.13)

$(0.02)

$0.01

$0.00

$(0.10)

$(0.08)

$(0.15)

$0.19

$0.14

$(0.04)

Q3 2013

Reported EPS

Loss on

Extinguishment

of Debt

Q3 2013

Underlying EPS

Increased

Commissions

and Fees

Increased

Expenses

Interest Expense

Other

Share count

Q3 2014

Underlying EPS

Foreign Currency

Movements

Operational

Improvement

Program

Q3 2014

Reported EPS |

$281

million generated through the first nine months of 2014 •

$85 million reduction from $366 million in year ago period

•

Year ago period benefited from significant non-recurring cash

inflows relating to close out of derivatives and current year

includes higher cash payments under the 2011 long-term

compensation plan

•

Partially offset by current year period reflecting increase in cash

collection of accounts receivable

YTD 2014 underlying EBITDA and cash generation

$636

$646

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 Underlying EBITDA down 1.5%

reflecting: Underlying revenue growth

International driven by emerging markets and Charles Monat

acquisition in Asia

North America growth in regions moderated by divestitures

Global reflects good growth in Reinsurance moderated by Willis

Insurance UK

Offset by underlying expense growth

Investments to drive sustained growth and support operations,

including Global Wealth Solutions and Connecting Willis

Other operating expense growth driven primarily by business

development costs

4

Net cash provided by operating activities

Underlying EBITDA

$ millions

$359

$362

$191

$187

$96

$87

YTD 2013

YTD 2014

1Q

2Q

3Q

$366

$281

Sept. 30

2013

Sept. 30

2014

$ millions

Net cash provided by operating activities |

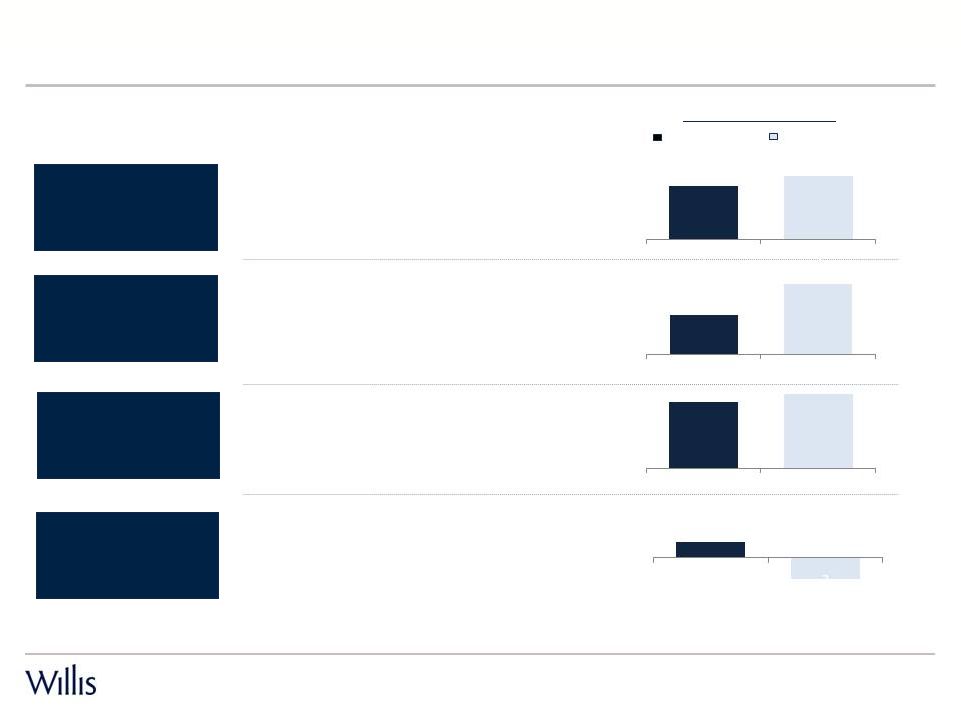

Reported

3Q 2014 Commissions and fees growth

5

•

Excellent result driven by growth in

emerging markets and Western

Europe

•

Growth led by International with solid

results in North America and

Reinsurance

•

Willis Re grew low-single digits, driven

by strong growth in North America

•

UK Insurance down mid-single digits:

•

Partly due to major construction

project in year ago quarter that did

not recur

•

Growth in geographic regions led by

Midwest and Atlantic

•

Human Capital up mid-single digits

•

Construction down due to lower projects

compared to prior year

Organic

Group

North

America

Global

International

% Growth

3Q 2014 vs. 3Q 2013

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 2.1%

2.5%

1

2

1.9%

3.4%

0.3%

-

0.4%

1

2

5.6%

6.3%

1

2

1

2 |

Underlying

expense

growth over

past 4

quarters:

Q314: 4.1%

Q214: 6.1%

Q114: 5.5%

Q413: 7.1%

(1)

Total underlying operating expense growth of 4.1%

3Q 2014 Total operating expenses

Q3 2014 total underlying operating expenses up $30 million, or 4.1%, largely driven

by growth in salary and benefits (~75% of total operating expenses)

Underlying expense rate of growth declined significantly in the third quarter

relative to previous three quarters

6

$ millions

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 (1) Represents expense growth

on an “apples to apples basis”, as if company had been accruing bonuses throughout 2012. Underlying expense growth was 10.7% |

$547

$569

$570

$575

$569

Q313

Q413

Q114

Q214

Q314

3Q 2014 Salaries and benefits

7

(1)

Q3 2013 has been rebased to current period exchange rates to remove the impact of

foreign currency movements when comparing periods Underlying salaries and

benefits ($ millions) $ millions

Q3 2013 Q3 2014 Change

•

Growth in underlying S&B of 4.0% in 3Q14

compared to prior year quarter

•

Increase driven by headcount growth and salary

reviews

•

Group headcount:

•

Up 2.2% Y-o-Y

•

Up 1.7% YTD with more than half of the

increase in Mumbai

•

Quarterly S&B is relatively flat over last four

quarters

•

2014 YTD headcount growth lower compared

to prior year period; growth rate in S&B

beginning to moderate

Reported S&B

$541

$ 569

Y-o-Y FX movement

(1)

6

-

Underlying S&B

$ 547

$ 569

4.0%

Full Time Employees (FTE)

17,900

18,300

2.2%

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 |

3Q

2014 Non-operating segment items and Corporate & other 8

•

Improved performance from Associates in 3Q14, primarily Gras Savoye

•

Increase in expense in the quarter represents $14 million of

foreign exchange loss on revaluation of non-functional currency

assets and liabilities

•

Taxes for 3Q14 impacted by a $4 million expense recorded to bring the tax

charge for the prior two quarters in line with our latest estimates for the full

year

Other

income/expense

Tax

Associates |

Balance sheet highlights

9

•

Share buyback program completed just after end of Q314

•

CapEx up due to investments in systems and infrastructure

•

Dividends increased 9% from year ago period

•

Acquisition of Charles Monat completed in 2Q14

•

Cash on hand up $33 million compared to 3Q13

•

Cash on hand down $140 million from year end 2013,

primarily due to the share buyback program and increased

cash dividends, offset by non-recurrence of $65 million debt

tender premium paid in 3Q13

Cash as of

Corporate Uses of Cash

$ millions

$ millions

$623

$796

$656

Sept. 30

2013

Dec. 31

2013

Sept. 30

2014

$30

$47

$200

$144

$157

$78

$81

2013 YTD

2014 YTD

Acquisitions

Share Buyback

Dividends

CapEx

$252

$

485 |

Operational Improvement Program and metrics

10

$ millions

2014

2015

2016

2017

Cumulative

2014-2017

Annualized

2018+

As of April, 2014 announcement

Expected Charge

$410

Expected Savings

$5

$45

$135

$235

$420

$300

Key metrics to be updated annually :

As of March 31, 2014

•

Ratio of full time employees (FTEs) in higher cost vs. lower cost near-shore

and off-shore centers

•

Ratio of square footage of real estate per FTE (indexed to 100)

•

Ratio of desks per FTE (indexed to 100)

As of October, 2014 update

Expected Spend

$40

$130

$240

$410

Expected Savings

$8

$60

$135

$235

$420

$300

80:20

100

100 |

Summary

11

Organic C&F

growth

Focused

M&A

Expense

discipline +

OIP

Earnings

growth

Margin

expansion

Improved

cash flow

•

Disciplined approach to expense management

•

Reduced net headcount additions

•

Encouraging early actions within the OIP

•

$300 million of annualized savings at end of

Program

•

Global presence

•

Connecting Willis

•

Innovation

•

Delivering better solutions for clients and driving

new business

•

High quality, specialized firms with leading positions

•

Recent examples include:

•

Charles Monat

•

Max Mattheissen

•

SurePoint Reinsurance Advisors

•

IFG’s Irish pension and financial advisory business

|

APPENDICES |

YTD

2014 Underlying EPS growth 13

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 Underlying business performance, together

with improved contributions from Associates, total to $nil per share

Other items -

increased tax rate $(0.15), increased share count $(0.04), increased interest

expense $(0.03), negatively impact underlying EPS in the YTD period

Underlying EPS down $0.20 YTD 2014 vs. YTD 2013, negatively impacted by higher tax

rate and increased share count

-

Deferred tax valuation allowance

= $(0.12)

-

Venezuela devaluation = $(0.07)

-

Loss on disposal = $(0.01)

-

Associates = $0.05

-

Increased interest expense = $(0.03)

-

Noncontrolling interests = $0.01

-

Other income /expense =$0.01

$0.34

$0.21

$0.45

$(0.50)

$0.04

$(0.15)

$(0.04)

$(0.16)

$(0.09)

$(0.20)

$1.67

$2.22

$2.02

$1.57

YTD 2013

Reported EPS

Loss on

Extinguishment

of Debt

Expense

Reduction

Initiative

YTD 2013

Underlying EPS

Increased

Commissions

and Fees

Increased

Expenses

Other

Increased Tax

Rate

Increased share

count

YTD 2014

Underlying EPS

Foreign

Currency

Movements

Operational

Improvement

Program

Other

YTD 2014

Reported EPS

Underlying business

performance =$(0.05) |

Reported

YTD 2014 Commissions and fees growth

14

•

Very strong growth driven by increase in

emerging markets and solid

performance in Western Europe

•

Good growth despite challenging market

conditions in Reinsurance and moderating

rates across almost all markets

•

Mid-single digit growth in reinsurance

(led by North America)

•

Willis Insurance UK is lagging as UK

Retail continues in turnaround and

Specialties suffers from difficult

comparisons due to large projects in

prior year

•

Good growth driven by solid performances

by most regions and bolstered by growth

in

two

largest

practices

–

Employee

Benefits and Construction

Organic

Group

North

America

Global

International

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 1

2

1

2

1

2

3.3%

4.4%

3.2%

1.9%

6.0%

6.5%

3.9%

3.8%

% Growth

YTD 2014 vs. YTD 2013 |

5.2%

underlying

total

operating

expense

growth

driven

by

S&B

and

other

operating

expenses

YTD 2014 Total operating expenses

15

$ millions

Salaries

and

benefits

up

5.1%

driven

by

investments

in

headcount

to

support

business

growth,

together with salary reviews

Other operating expenses up 6.5% driven by increased business development expenses

and systems related expenditure

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 $30

$(46)

$1

$83

$30

$2

$20

$2,218

$2,201

$2,316

$2,336

YTD 2013

Reported

Foreign

Currency

Movement

Expense

Reduction

Initiative

Debt

Extinguishment

Fees

YTD 2013

Underlying

Salaries and

Benefits

Other Operating

Expenses

Depreciation &

Amortization

YTD 2014

Underlying

Operational

Improvement

Program

YTD 2014

Reported |

$1,631

$570

$575

$569

$1,714

YTD13

Q114

Q214

Q314

YTD14

$ millions

YTD2013 YTD2014 Change

Reported S&B

$1,638

$ 1,714

Expense Reduction Initiative

(29)

-

Y-o-Y FX movement

(1)

22

-

Underlying S&B

$1,631

$1,714

5.1%

Full Time Employees (FTE)

17,900

18,300

2.2%

YTD 2014 Salaries and benefits

16

(1)

YTD

2013 has been rebased to current period exchange rates to remove the impact of

foreign currency movements when comparing periods Underlying salaries and

benefits ($ millions)

•

Growth in underlying S&B of 5.1% YTD in 2014

compared to prior year

•

Increase driven by increased headcount and

salary reviews

•

Group headcount:

•

Up 2.2% Y-o-Y

•

Up 1.7% YTD with more than half of the

increase in Mumbai

•

YTD increase driven by investments in

revenue-producing talent, as well as client

service and risk management capabilities

•

Quarterly S&B expense is relatively level

throughout first three quarters of 2014

•

Sequential slowing of S&B growth rate

•

Y-o-Y increase of 4.0% in Q3 vs 6.3%

in Q2 and 5.0% in Q1

See important disclosures regarding non-GAAP measures on page 2 and

reconciliations starting on page 17 |

Important disclosures regarding non-GAAP measures

17

Commissions and fees analysis

2014

2013

Change

Foreign

currency

translation

Acquisitions

and

disposals

Organic

commissions

and fees

growth

($ millions)

%

%

%

%

Three months ended

September 30, 2014

North America

$328

$322

1.9

-

(1.5)

3.4

International

190

180

5.6

(4.2)

3.5

6.3

Global

290

289

0.3

1.3

(0.6)

(0.4)

Total

$808

$791

2.1

(0.4)

-

2.5

2014

2013

Change

Foreign

currency

translation

Acquisitions

and

disposals

Organic

commissions

and fees

growth

($ millions)

%

%

%

%

Nine months ended

September 30, 2014

North America

$1,037

$1,004

3.3

(0.1)

(1.0)

4.4

International

691

652

6.0

(2.0)

1.5

6.5

Global

1,100

1,066

3.2

1.6

(0.3)

1.9

Total

$2,828

$2,722

3.9

0.2

(0.1)

3.8 |

Important disclosures regarding non-GAAP measures

18

Operating income to underlying operating income

For prior periods, underlying measures have been rebased to current period exchange

rates to remove the impact of foreign currency movements when comparing

periods 2013

2014

($ millions)

1Q

2Q

3Q

YTD

1Q

2Q

3Q

YTD

Total revenue

$1,051

$890

$795

$2,736

$1,097

$935

$812

$2,844

excluding:

Foreign currency movements

3

5

(3)

5

-

-

-

-

Underlying revenue

$1,054

$895

$792

$2,741

$1,097

$935

$812

$2,844

Operating income

$281

$167

$70

$518

$326

$148

$34

$508

excluding:

Operational improvement program

-

-

-

-

-

3

17

20

Expense reduction initiative

46

-

-

46

-

-

-

-

Fees related to extinguishment of debt

-

-

1

1

-

Foreign currency movements

(4)

(11)

(10)

(25)

-

-

-

-

Underlying operating income

$323

$156

$61

$540

$326

$151

$51

$528

Operating margin (operating income as a

percentage of total revenue)

26.7%

18.8%

8.8%

18.9%

29.7%

15.8%

4.2%

17.9%

Underlying operating margin (underlying operating

income as a percentage of underlying total revenue)

30.6%

17.4%

7.7%

19.7%

29.7%

16.1%

6.3%

18.6% |

Important disclosures regarding non-GAAP measures

19

Net income (loss) to underlying net income

2013

2014

($ millions, except per share data)

1Q

2Q

3Q

YTD

1Q

2Q

3Q

YTD

Net income (loss)

$219

$105

($27)

$297

$246

$47

($7)

$286

Excluding the following, net of tax:

Operational improvement program

-

-

-

-

-

2

14

16

Venezuela currency devaluation

-

-

-

-

-

13

-

13

Deferred tax valuation allowance

-

-

-

-

-

21

-

21

Expense reduction initiative

38

-

-

38

-

-

-

-

Loss on extinguishment of debt

-

-

60

60

-

Fees related to debt extinguishment

-

-

1

1

-

Net loss on disposal of operations

-

-

-

-

2

-

-

2

Foreign currency movements

(6)

(5)

(18)

(29)

-

-

-

-

Underlying net income

$251

$100

$16

$367

$248

$83

$7

$338

Diluted shares outstanding

176

178

180

178

182

182

181

182

Net income (loss) per diluted share

$ 1.67

$1.35

$0.26

($0.04)

$1.57

Underlying net income per diluted share

$2.22

$1.36

$0.49

$0.14

$2.02

$1.24

$0.59

$0.59

$1.46

($0.15)

$0.19

For prior periods, underlying measures (other than EPS) have been rebased to current period exchange

rates to remove the impact of foreign currency movements when comparing periods. In the current

three and nine month periods only, underlying EPS excludes the $0.10 and $0.16 respectively, negative

year over year impact of foreign currency movements in order to assist comparability to EPS figures

that have been disclosed in prior periods. |

2013

2014

($ millions)

1Q

2Q

3Q

YTD

1Q

2Q

3Q

YTD

Net income (loss)

$219

$105

($27)

$297

$246

$47

($7)

$286

Add back:

Net income (loss) attributable to

noncontrolling interests

4

2

-

6

4

1

(1)

4

Interest in earning of associates,

net of tax

(15)

3

1

(11)

(19)

3

(3)

(19)

Income tax charge

48

29

11

88

63

59

2

124

Interest expense

31

32

30

93

32

35

34

101

Other expense (income)

(6)

(4)

(5)

(15)

-

3

9

12

Loss on extinguishment of debt

-

-

60

60

-

-

-

-

Depreciation

26

21

21

68

23

24

23

70

Amortization

14

14

14

42

13

12

13

38

EBITDA

$321

$202

$105

$628

$362

$184

$70

$616

Adjusting items:

Operational improvement program

-

-

-

-

-

3

17

20

Expense reduction initiative

41

-

-

41

-

-

-

-

Fees related to debt extinguishment

-

-

1

1

-

-

-

Foreign currency movements

(3)

(11)

(10)

(24)

-

-

-

-

Underlying EBITDA

$359

$191

$96

$646

$362

$187

$87

$636

Important disclosures regarding non-GAAP measures

20

Net income (loss) to underlying EBITDA

For prior periods, underlying measures have been rebased to current period exchange

rates to remove the impact of foreign currency movements when comparing

periods |

Important disclosures regarding non-GAAP measures

21

Reported total expenses to underlying total expenses, and

Reported salaries and benefits to underlying salaries and benefits

For prior periods, underlying measures have been rebased to current period exchange

rates to remove the impact of foreign currency movements when comparing

periods 2013

2014

(In millions)

1Q

2Q

3Q

YTD

1Q

2Q

3Q

YTD

Reported total expenses

$770

$723

$725

$2,218

$771

$787

$778

$2,336

Excluding:

Operational improvement program

-

-

-

-

-

(3)

(17)

(20)

Expense reduction initiative

(46)

-

-

(46)

-

-

-

-

Fees related to extinguishment of debt

-

-

(1)

(1)

-

-

-

-

Foreign currency movements

7

16

7

30

-

-

-

-

Underlying total expenses

$731

$739

$731

$2,201

$771

$784

$761

$2,316

Reported salaries and benefits

$568

$529

$541

$1,638

$570

$575

$569

$1,714

Excluding:

Expense reduction initiative

(29)

-

-

(29)

-

-

-

-

Foreign currency movements

4

12

6

22

-

-

-

-

Underlying salaries and benefits

$543

$541

$547

$1,631

$570

$575

$569

$1,714 |

IR

Contacts Peter Poillon

Tel: +1 212 915-8084

Email: peter.poillon@willis.com

Mark Jones

Tel: +1 212 915-8796

Email: mark.p.jones@willis.com

22 |