Attached files

Table of Contents

As filed with the Securities and Exchange Commission on October 28, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

J. ALEXANDER’S HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Tennessee | 5812 | 47-1608715 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

3401 West End Avenue, Suite 260

Nashville, Tennessee 37203

(615) 269-1900

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Mark A. Parkey

Chief Financial Officer

3401 West End Avenue, Suite 260

Nashville, Tennessee 37203

(615) 269-1900

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| F. Mitchell Walker, Jr., Esq. Lori B. Morgan, Esq. Bass, Berry & Sims PLC 150 Third Avenue South Suite 2800 Nashville, Tennessee 37201 (615) 742-6200 |

Tracey A. Zaccone, Esq. Paul, Weiss, Rifkind, Wharton & Garrison LLP 1285 Avenue of the Americas New York, New York 10019 (212) 373-3000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one:)

| Large accelerated filer |

¨ |

Accelerated filer |

¨ | |||

| Non-accelerated filer |

x (Do not check if a smaller reporting company) |

Smaller reporting company |

¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee | ||

| Class A common stock, par value $0.001 per share |

$75,000,000 | $8,715 | ||

|

| ||||

|

| ||||

| (1) | Includes the offering price of any additional shares of Class A common stock that the underwriters have the right to purchase to cover over-allotments. |

| (2) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is neither an offer to sell these securities nor a solicitation of an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 28, 2014

PRELIMINARY PROSPECTUS

This is an initial public offering of J. Alexander’s Holdings, Inc. We are offering shares of our Class A common stock, par value $0.001 per share. Prior to this offering there has been no public market for our Class A common stock. We intend to file an application for our Class A common stock to be listed on the New York Stock Exchange under the symbol “JAXH.”

We currently estimate that the initial public offering price of our Class A common stock will be between $ and $ per share.

Immediately following this offering: (i) the holders of our Class A common stock will own 100% of the economic interests and hold approximately % of the voting power of J. Alexander’s Holdings, Inc.; and (ii) the holders of our Class B common stock, par value $0.001 per share, will own no economic interest in, but will hold approximately % of the voting power of, J. Alexander’s Holdings, Inc.

J. Alexander’s Holdings, Inc. is a holding company (i) whose sole asset will be approximately % of the economic interests of J. Alexander’s Holdings, LLC, our principal operating subsidiary, and (ii) which will also be the sole managing member of J. Alexander’s Holdings, LLC. The remaining economic interests in J. Alexander’s Holdings, LLC will be held by the holders of our Class B common stock and certain members of our management team, as further described herein.

We are an “emerging growth company” as defined under the federal securities laws and, as such, will be subject to reduced public company reporting requirements. See “Prospectus Summary—Implications of Being an Emerging Growth Company.”

Shares

J. ALEXANDER’S HOLDINGS, INC.

Class A Common Stock

Investing in our Class A common stock involves a high degree of risk. Please read “Risk Factors” beginning on page 20 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| PER SHARE | TOTAL |

|||||||

| Public offering price |

$ | $ | ||||||

| Underwriting discounts(1) |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

(1) We refer you to the “Underwriting” section of this prospectus for additional information regarding total underwriters compensation.

Delivery of the shares of Class A common stock is expected to be made on or about , 2014. We have granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase an additional shares of our Class A common stock.

| Stephens Inc. | KeyBanc Capital Markets | Stifel |

Prospectus dated , 2014

Table of Contents

Table of Contents

Table of Contents

Table of Contents

You should rely only on the information contained in this prospectus and in any free writing prospectus that we may provide to you in connection with this offering. Neither we nor any of the underwriters has authorized anyone to provide you with information different from, or in addition to, that contained in this prospectus or any such free writing prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. We can provide no assurance as to the reliability of any other information that others may give you. Neither we nor any of the underwriters is making an offer to sell or seeking offers to buy these securities in any jurisdiction where, or to any person to whom, the offer or sale is not permitted. The information in this prospectus is accurate only as of the date on the front cover of this prospectus and the information in any free writing prospectus that we may provide you in connection with this offering is accurate only as of the date of such free writing prospectus. Our business, financial condition, results of operations and prospects may have changed since those dates.

For investors outside the United States: Neither we nor any of the underwriters has taken any action to permit this offering outside of the United States or to permit the possession or distribution of this prospectus or any free writing prospectus we may provide in connection with this offering outside the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus and any such free writing prospectus outside of the United States.

i

Table of Contents

MARKET, RANKING AND OTHER INDUSTRY DATA

This prospectus contains industry and market data, forecasts and projections that are based on internal data and estimates, independent industry publications, reports by market research firms or other published independent sources. In particular, we have obtained information regarding the restaurant industry from the National Restaurant Association and Technomic, Inc. The National Restaurant Association (“NRA”) is the largest foodservice trade association in the world supporting nearly 500,000 restaurant businesses. Technomic, Inc. (“Technomic”) is a national consulting market research firm. Other industry and market data included in this prospectus are from internal analyses based upon data available from known sources or other proprietary research and analysis.

We believe these data to be reliable as of the date of this prospectus, but there can be no assurance as to the accuracy or completeness of such information. We have not independently verified the market and industry data obtained from these third-party sources. Our internal data and estimates are based upon information obtained from trade and business organizations, other contacts in the markets in which we operate and our management’s understanding of industry conditions. Though we believe this information to be true and accurate, such information has not been verified by any independent sources. You should carefully consider the inherent risks and uncertainties associated with the market and other industry data contained in this prospectus, including those discussed under the heading “Risk Factors.”

BASIS OF PRESENTATION

Our fiscal year ends on the Sunday closest to December 31, and each quarter typically consists of 13 weeks. The period January 2, 2012 through September 30, 2012 included 39 weeks of operations, and the period October 1, 2012 through December 30, 2012 included 13 weeks of operations. Fiscal year 2013 included 52 weeks of operations. Each of the nine months ended September 28, 2014 and September 29, 2013 included 39 weeks of operations. All financial information herein relating to periods prior to the completion of the reorganization transactions described herein is that of J. Alexander’s Holdings, LLC and its consolidated subsidiaries. Financial information through and including September 30, 2012, the date Fidelity National Financial, Inc. (“FNF”) acquired J. Alexander’s Corporation (“JAC”) for accounting purposes, is referred to as “Predecessor” company information, which has been prepared using the previous basis of accounting. The financial information for periods beginning October 1, 2012 is referred to as “Successor” company information and reflects the financial statement effects of recording fair value adjustments and the capital structure resulting from FNF’s acquisition of JAC.

Financial and operating information for all periods presented has been adjusted to reflect the impact of discontinued operations for comparative purposes.

References to our same store restaurants and same store sales or average weekly same store sales in this prospectus refer to sales from our restaurants in operation at the end of the period which have been open for longer than 18 consecutive months prior to the end of a specified period.

ii

Table of Contents

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

We own the trademarks, service marks and trade names that we use in connection with the operation of our business, including our corporate names, logos and website names. This prospectus may also contain trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. Solely for convenience, the trademarks, service marks, trade names and copyrights referred to in this prospectus are listed without the TM, SM, © and ® symbols, but we will assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors, if any, to these trademarks, service marks, trade names and copyrights.

CERTAIN DEFINITIONS

Unless otherwise expressly indicated in this prospectus or the context otherwise requires:

| • | references to “J. Alexander’s Holdings, Inc.” and the “issuer” refer to J. Alexander’s Holdings, Inc., a newly-formed Tennessee corporation, and not to any of its subsidiaries; |

| • | references to “J. Alexander’s Holdings, LLC,” and the “Operating LLC” refer to J. Alexander’s Holdings, LLC, a Delaware limited liability company, the sole owner of J. Alexander’s, LLC; |

| • | references to “J. Alexander’s, LLC” refer to J. Alexander’s, LLC, a Tennessee limited liability company, which is a wholly owned subsidiary of the Operating LLC and, together with its subsidiaries (which we refer to as our “Operating Subsidiaries”), conducts all of our business operations; J. Alexander’s, LLC is the successor upon conversion of JAC; |

| • | references to the “Company,” “we,” “us” and “our” refer to J. Alexander’s Holdings, Inc. and its consolidated subsidiaries, including J. Alexander’s Holdings, LLC and J. Alexander’s, LLC, giving effect to the reorganization transactions described below; |

| • | references to “FNFV” refer to Fidelity National Financial Ventures, LLC, a Delaware limited liability company and wholly owned subsidiary of FNF, and its predecessor, Fidelity National Special Opportunities, Inc., a Delaware corporation, which converted into FNFV in May 2014; |

| • | references to “Newport” refer to Newport Global Opportunities Fund AIV-A LP, a Delaware limited partnership, whose investment manager is Newport Global Advisors LP; and |

| • | references to “FNH” refer to Fidelity Newport Holdings, LLC, a Delaware limited liability company and a joint venture owned by FNFV, Newport and certain individuals. |

iii

Table of Contents

NON-GAAP FINANCIAL MEASURES

In this prospectus, we use the following financial measures that are not presented in accordance with generally accepted accounting principles in the United States (“GAAP”):

“Adjusted EBITDA,” defined as net income (loss) before interest expense, income tax (expense) benefit, depreciation and amortization, and adding asset impairment charges and restaurant closing costs, loss on disposals of fixed assets, transaction and integration costs, non-cash compensation, loss from discontinued operations, gain on debt extinguishment, pre-opening costs and certain unusual items, is a non-GAAP financial measure that we believe is useful to investors because it provides information regarding certain financial and business trends relating to our operating results. Adjusted EBITDA does not fully consider the impact of investing or financing transactions as it specifically excludes depreciation and interest charges, which should also be considered in the overall evaluation of our results of operations.

“Restaurant Operating Profit,” defined as net sales less restaurant operating costs, which are cost of sales, restaurant labor and related costs, depreciation and amortization of restaurant property and equipment, and other operating expenses, is a non-GAAP financial measure that we believe is useful to investors because it provides a measure of profitability for evaluation that does not reflect corporate overhead and other non-operating or unusual costs. “Restaurant Operating Profit Margin” is the ratio of Restaurant Operating Profit to net sales.

Our management uses Adjusted EBITDA and Restaurant Operating Profit to evaluate the effectiveness of our business strategies. We caution investors that amounts presented in this prospectus in accordance with the above definitions of Adjusted EBITDA or Restaurant Operating Profit may not be comparable to similar measures disclosed by other companies, because not all companies calculate these non-GAAP financial measures in the same manner. Adjusted EBITDA and Restaurant Operating Profit should not be assessed in isolation from, or construed as a substitute for, net income or net cash provided by operating, investing or financing activities, each as presented in accordance with GAAP.

A reconciliation of these non-GAAP financial measures to the closest GAAP measure is included in this prospectus under the heading “Prospectus Summary—Summary Historical and Unaudited Pro Forma Consolidated Financial and Other Data.”

iv

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that you should consider before deciding to invest in our Class A common stock. You should read this entire prospectus carefully, including the “Risk Factors” section and the financial statements and the notes to those statements, before making an investment decision. Some of the statements in this summary constitute forward-looking statements regarding us or our business or estimates regarding industry or market data. See “Forward-Looking Statements.”

Our Company

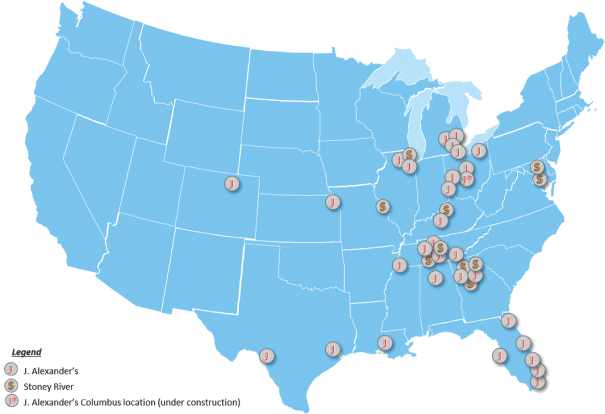

We are the owner and operator of two complementary upscale dining restaurant concepts: J. Alexander’s and Stoney River Steakhouse and Grill (“Stoney River”). For more than 20 years, the J. Alexander’s team has provided its guests a quality dining experience with a contemporary American menu and intense levels of service in a restaurant with an attractive ambiance. Beginning in February 2013, when the Stoney River concept became part of the J. Alexander’s organization, our team has brought our quality and professionalism to the steakhouse category, providing an upscale or fine dining experience at a polished casual price point. As of September 28, 2014, we operated 40 locations across 14 states.

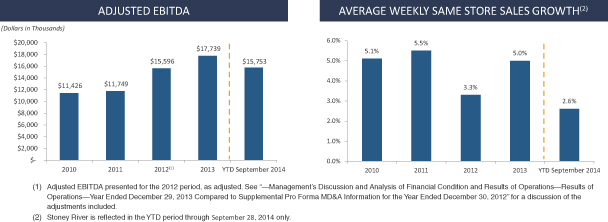

We believe our concepts deliver on our customers’ desire for freshly-prepared, high quality food and high quality service in a restaurant that feels “unchained” with architecture and design that varies from location to location. As a result, we have delivered strong growth in same store sales, average weekly sales, net sales and Adjusted EBITDA. Through our combination with Stoney River, we have grown from 33 restaurants across 13 states in 2008 to 40 restaurants across 14 states as of September 28, 2014. Our growth in same store sales since 2008 has allowed us to invest significant amounts of capital to drive growth through the continuous improvement of existing locations, the development of plans to open new restaurants and the hiring of personnel to support our growth plans. Our J. Alexander’s restaurants have generated 19 consecutive fiscal quarters of positive same store sales growth, which we believe demonstrates the strength of that concept. We have grown the average weekly sales at our J. Alexander’s concept from approximately $88,400 in 2008 to approximately $102,000 in 2013, representing an increase of 15.4% over that time period. We have also grown the average weekly sales at the Stoney River locations since February 2013, even while implementing significant operational and remodeling improvements. From 2008 to 2013, our total annual net sales (not including restaurants categorized as discontinued operations) increased from $137,622,000 to $188,223,000 and Adjusted EBITDA increased from $10,494,000 to $17,739,000. We generated net income of $105,000 and $2,901,000 in 2008 and 2013, respectively. For the nine-month period ending September 28, 2014, our net sales were $148,921,000 and our net income was $6,323,000. For a definition and reconciliation of Adjusted EBITDA, a non-GAAP financial measure, to net income, see “—Summary Historical and Unaudited Pro Forma Consolidated Financial and Other Data.”

1

Table of Contents

Our Concepts

J. Alexander’s

J. Alexander’s was founded in 1991 in Nashville, Tennessee and for over 20 years has offered a quality upscale dining experience with a contemporary American menu in an environment with an attractive ambiance. At J. Alexander’s, we pride ourselves on our attentive, courteous and highly professional service. The J. Alexander’s menu focuses on made-from-scratch menu items created with high quality, fresh ingredients. It features prime rib of beef, hardwood-grilled steaks, seafood and chicken, pasta, salads, soups, and assorted sandwiches, appetizers and desserts. Our menu is complemented by a broad wine list with several exclusive offerings. Our restaurants are open for lunch and dinner seven days a week and had an average check of $28.63 in 2013. As of September 28, 2014, we operated 30 J. Alexander’s locations and had one additional location under construction.

Stoney River Steakhouse and Grill

Stoney River was founded in 1996 in Atlanta, Georgia and is a steakhouse concept that seeks to provide the quality and service of a fine dining steakhouse at a more reasonable price point. Stoney River has a high quality steakhouse menu, but unlike many steakhouse competitors, the menu is not “a la carte” and every steak comes with a side item. The menu is broader than many steakhouses, and includes house specialties ranging from pasta and chicken to shrimp, salmon and baby back ribs, complemented by an extensive wine list. Each restaurant is open seven days a week for dinner and had an average check of $41.11 in 2013. Stoney River has been a part of the J. Alexander’s organization since February 2013 and, as of September 28, 2014, we had 10 Stoney River locations.

Competitive Landscape

The full-service restaurant business is highly competitive and highly fragmented, and the number, size and strength of competitors vary widely by region. We believe restaurant competition is based on quality of food products, customer service, reputation, restaurant décor, location, reputation and price. Both of our restaurant concepts compete with a number of other restaurants within each market location, including both locally-owned restaurants and restaurants that are part of regional or national chains. J. Alexander’s also competes with regional and national restaurant chains that market to the upscale restaurant customer, such as Del Frisco’s Grill, Kona Grill and Seasons 52. The principal competitors for our Stoney River concept include locally-owned upscale steakhouses. Stoney River also competes with the national “white tablecloth” steakhouse chains that market to the upscale steakhouse customer, such as The Capital Grille, Smith & Wollensky, The Palm, Ruth’s Chris Steak House, Morton’s The Steakhouse, Del Frisco’s, and Fleming’s Prime Steakhouse and Wine Bar. Our concepts also compete with additional restaurants in the broader upscale and polished casual dining segments.

Our Strengths

Over our more than 20-year operating history, we have developed and refined the following strengths:

Two Distinct Yet Complementary Concepts

J. Alexander’s and Stoney River are concepts with more than 40 years of combined history, strong brand value and exceptional customer loyalty in their core markets. They both blend what we believe are the best attributes of fine and casual dining: a focus on high quality food made with fresh ingredients in a scratch kitchen, exceptional service, diverse menus and individualized interior and exterior design unique to each community. Each concept has a distinct identity, and the differentiation in menu and restaurant design is substantial enough that they can successfully operate in the same markets or retail locations.

2

Table of Contents

Delivering a Superior Dining Experience with the Highest Quality Service at a Reasonable Price Point

Our concepts seek to provide a high quality dining experience that appeals to a wide range of consumer tastes at reasonable price points, which we believe helps us cultivate long-term, loyal guests who place a premium on the price-value relationships that our concepts offer.

Premium, Freshly Made Cuisine

Both of our concepts are committed to preparing high quality food from innovative menus. We are selective in the grade and freshness of our ingredients and in our menu offerings. Substantially all the protein and vegetables we use are delivered fresh to our restaurants and are not frozen in transport or in storage prior to being served, and are predominately preservative and additive-free. Virtually all of our made-to-order menu items are prepared from scratch, including stocks, sauces and desserts made in-house daily. Our food menus are complemented by comprehensive wine lists that offer both familiar varietals as well as wines exclusive to our restaurants. While each menu has its own distinctive profile, both concepts strive to continuously innovate with new ingredients and local “farm-to-table” produce to provide limited-time featured items to keep the experience new and interesting for our guests. Quality control is a key part of our mission and we have developed a taste plate process at all of our restaurants whereby all of our menu items are taste-tested daily by restaurant managers to ensure they meet our presentation and taste standards.

Outstanding Service

Prompt, courteous and efficient service delivered by a knowledgeable staff is an integral part of the J. Alexander’s and Stoney River concepts. Our goal is to have all staff working together to achieve the highest guest satisfaction, and we believe our low table to server ratio, when coupled with team serving by a dedicated staff, ensures our guests receive exceptional service.

Sophisticated Experience

Our concepts use a variety of architectural designs and building finishes to create beautiful, upscale décor with contemporary and timeless finishes. We are aggressive with our repair and maintenance program in all locations, ensuring that no restaurant ever looks “highly trafficked” or dated. This results in a reduced need for periodic major remodels to reimage a given location to acceptable standards.

Attractive Unit Economics and Consistent Execution

We believe we have a long standing track record of consistently producing high average unit sales volumes and have proven the viability of both concepts in multiple markets and regions. We have successfully increased our average unit volumes at a compound annual growth rate of 2.9% from approximately $4,600,000 in 2008 to approximately $5,300,000 in 2013 for the J. Alexander’s concept. Our highest volume restaurant generated approximately $7,800,000 in net sales in 2013. From 2008 to 2013, we have increased our Restaurant Operating Profit Margin (as defined herein) at J. Alexander’s by 4.4% to 14.2%. Since we began operating Stoney River, we have been able to increase the average weekly sales and Restaurant Operating Profit Margin at our Stoney River restaurants even while implementing significant operational improvements and remodeling several locations. We believe that additional remodels of locations in both concepts will contribute to increases in same store sales. We are targeting average unit volumes and Restaurant Operating Profit Margins for new locations at maturity to exceed system-wide fiscal year 2013 levels for both concepts.

Strong Cultural Focus on Continuous Training

We believe that our stringent hiring standards, coupled with our extensive and continuous training programs for all employees, provide our guests with outstanding service at both of our concepts. We prefer to promote our

3

Table of Contents

restaurant managers to general managers and regional management from within the organization and currently 51% of those roles are filled by individuals promoted from within. We also seek to hire general manager prospects from top U.S. culinary and hospitality programs and train them in our systems and processes, which can be a three to five-year process. We believe that our hiring and training, and our focus on internal promotion help to ensure that our culture of excellent service is thoroughly disseminated throughout our organization.

Sophisticated and Scalable Back Office and Operations

Our back office and operations have developed over the last 20 years to provide us with advantages in our purchasing and shared services model. Most of our protein purchases are negotiated directly with our suppliers. Direct relationships with vendors provide us cost and flexibility advantages that may not be available from third party distributors. We also have a shared service model for our back office that has centralized certain functions for both concepts at our corporate headquarters. Services shared between our concepts include staff training and recruiting, real estate development, purchasing, human resources, information technology, finance and accounting. From our vendor team to our shared services model, we believe we have developed a scalable platform with the bench strength to support our planned growth with limited additions.

Experienced Management Team

We are led by a management team with significant experience in all aspects of restaurant operations. Our team of industry veterans at the executive level has an average of 29 years of restaurant experience. Our 40 general managers have an average tenure of approximately 9 years at J. Alexander’s and approximately 6.5 years at Stoney River as of August 2014. Despite a difficult economic environment, this management team has achieved 19 consecutive fiscal quarters of same store sales growth at the J. Alexander’s concept, improved restaurant-level performance, integrated Stoney River operations and established new restaurant development efforts.

Our Growth Strategies

We believe there are significant opportunities to grow our business, strengthen our competitive position and enhance our concepts through the implementation of the following strategies:

Deliver Consistent Same Store Sales Growth Through Continuing to Provide High Quality Food and Service

We believe we will be able to continue to generate same store sales growth by consistently providing an attractive price/value proposition for our guests through excellent service in an upscale environment. We remain focused on delivering freshly prepared, contemporary American cuisine, with exceptional quality and service for the price, while continuing to explore ways to increase the flexibility of dining options for our guests. We will continue to adapt to changing consumer tastes and incorporate local offerings to reinforce our boutique restaurant feel through limited-time featured food and drink offerings and potential menu additions. We also have a program of continuous investment in all of our locations to maintain our store images at the highest level to ensure a consistent guest experience across both concepts. We believe our level of repair and maintenance expense, coupled with our planned remodeling schedule, will also contribute to improvements in same store sales.

Pursue Disciplined New Restaurant Growth in Target Markets

We believe that J. Alexander’s and Stoney River have significant growth potential and we are in the early stages of our growth story. We have built a scalable infrastructure, successfully grown J. Alexander’s and completed the integration of the Stoney River locations. Historically, we have focused on organic growth, but in 2012, we began to establish a new restaurant development pipeline. The first of our new restaurant openings will occur in Columbus, Ohio in the fourth quarter of 2014. We believe there are significant opportunities to grow our concepts in both existing and new markets nationwide where we believe we can generate attractive unit economics.

4

Table of Contents

We are constantly evaluating potential sites for new restaurant openings and currently have approximately 30 locations in approximately 20 separate markets under various stages of review and development. We believe that having a large number of sites under review at any one time is necessary in order to meet our development goals. In our experience, sites under analysis often will not result in a new restaurant location for any number of reasons, including the delay or cancelation of larger development projects on which a future restaurant may depend, the loss of potential site locations to competitors, or our ultimate determination that a site under review is not appropriate for one of our concepts. We believe that the number of available and potential sites under review by us, the anticipated cost of opening a new restaurant location and the capital resources anticipated to be available to us following the completion of this offering, will support between four and seven new store openings annually starting in 2015. However, our ability to open any particular number of restaurants in any calendar year is dependent upon many factors, risks and uncertainties beyond our control as discussed more fully elsewhere in this prospectus under the heading “Risk Factors—Risks Related to Our Business.”

Leverage Our Infrastructure to Enhance Profitability

We believe we have a scalable infrastructure and can continue to expand our margins as we execute our strategy, particularly as we continue to improve the operations at the Stoney River locations. While both restaurant concepts have independent store-level operations, we use our shared services platform to conduct many of the training, quality control and administrative functions for both concepts. We believe this leverageable infrastructure will enhance our profitability as we grow. We believe we have the personnel in place to support our current growth plan without significant additional investments in infrastructure.

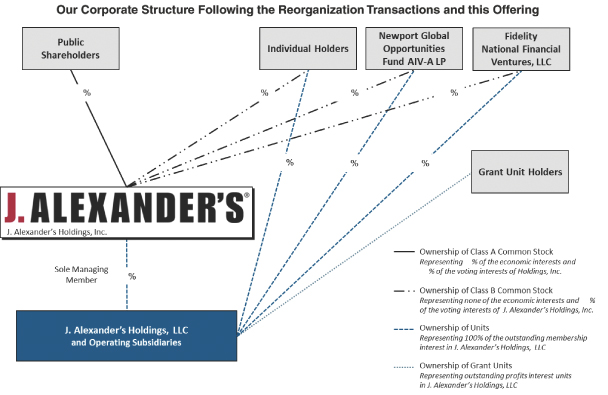

Class A Common Stock and Class B Common Stock

After completion of this offering, our outstanding capital stock will consist of shares of Class A common stock and shares of Class B common stock. Investors in this offering will hold shares of Class A common stock of J. Alexander’s Holdings, Inc., the sole managing member of J. Alexander’s Holdings, LLC. See “Description of Capital Stock.”

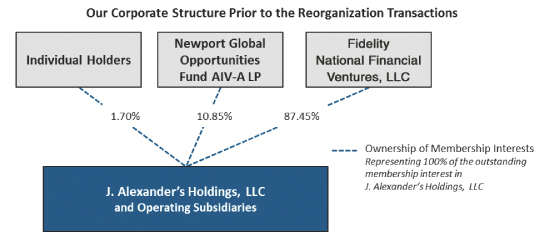

History and Corporate Structure

The first J. Alexander’s restaurant opened in 1991 in Nashville, Tennessee. From 1991 to 2012, J. Alexander’s was owned and operated by JAC, the predecessor to J. Alexander’s, LLC, and grew from a single location in 1991 to 33 restaurants located in Alabama, Arizona, Colorado, Florida, Georgia, Illinois, Kansas, Kentucky, Louisiana, Michigan, Ohio, Tennessee and Texas.

Stoney River was founded by a group of entrepreneurs in Atlanta, Georgia in 1996. In 2000, O’Charley’s, Inc. (“O’Charley’s”) acquired Stoney River, which at that time operated two restaurant locations in suburban Atlanta, Georgia. From 2000 until 2012, O’Charley’s owned and operated Stoney River, adding additional locations in Georgia, Illinois, Kentucky, Maryland, Missouri and Tennessee.

In April of 2012, FNFV acquired O’Charley’s and in May of that year transferred its ownership in O’Charley’s to FNH. In September of 2012, FNFV acquired JAC and in February 2013, JAC was transferred to J. Alexander’s Holdings, LLC (referred to herein as the “Operating LLC”), then a newly formed, wholly owned subsidiary of FNFV. In February of 2013, FNH transferred the Stoney River Assets (as defined herein) to the Operating LLC.

Corporate Structure

J. Alexander’s Holdings, Inc., the issuer in this offering, was incorporated in the State of Tennessee on August 15, 2014 for the purpose of this offering and to date has engaged only in activities in contemplation of this offering. Prior to the completion of this offering, all of our business operations are being conducted through the Operating LLC and its subsidiaries.

5

Table of Contents

In anticipation of this offering, beginning in August 2014 we commenced an internal restructuring that, following the completion of this offering, will result in the following:

| • | the formation of the issuer, and immediately prior to the closing of this offering, the amendment and restatement of its charter to authorize the issuance of two classes of common stock, Class A common stock and Class B common stock, which we collectively refer to as our “common stock,” and which will generally vote together as a single class on all matters submitted for a vote to shareholders; |

| • | the issuance of shares of Class A common stock by the issuer to the investors in this offering, the total voting power of which shares will be proportional to the percentage of Units (as defined below) held by the issuer; |

| • | the issuance of shares of Class B common stock by the issuer to the owners of the Operating LLC, including FNFV, Newport, and certain individual holders, which shares will not entitle the holders thereof to any of the economic rights (including rights to dividends and distributions upon liquidation) that will be provided to holders of Class A common stock, and the total voting power of which shares will be equal to the percentage of Units not held by the issuer; |

| • | the contribution by the issuer of the net cash proceeds received in this offering to the Operating LLC in exchange for a managing member’s membership interest in the Operating LLC; |

| • | the restatement of the current limited liability company agreement of the Operating LLC (referred to herein as the “Restated Operating Agreement”) to provide for the governance and control of the Operating LLC by the issuer as its sole managing member and to establish the terms upon which other holders of membership interests in the Operating LLC (referred to herein as “Units”) may exchange those Units, and a corresponding number of shares of Class B common stock, for, at the issuer’s option, either shares of Class A common stock on a one-for-one basis, subject to customary exchange rate adjustments for stock splits, stock dividends and reclassifications, or a cash payment; and |

| • | the adoption by the Operating LLC of the J. Alexander’s Holdings, LLC 2014 Management Incentive Plan (referred to herein as the “Profits Interest Incentive Plan”) and the grant of equity incentive awards to our management team and other key employees under such plan in the form of profits interests in the Operating LLC (referred to herein as “Grant Units”). |

Following the consummation of the reorganization transactions, this offering and the application of the net proceeds therefrom, the issuer will be a holding company and through its sole managing member interest, will control the business and affairs of the Operating LLC and its subsidiaries. The principal asset of the issuer will be its interest in the Operating LLC. In addition, following the consummation of the reorganization transactions and this offering, the issuer will be treated as a corporation for U.S. federal income tax purposes, while the Operating LLC will continue to be treated as a partnership for U.S. federal income tax purposes. As a result, holders of our Class A common stock will hold an equity interest in an entity that will be subject to entity-level federal income taxation, while holders of Units will hold an equity interest in an entity that will not itself be subject to U.S. federal income taxation.

In this prospectus, we refer to the transactions described above as the “reorganization transactions.” For a detailed description of the reorganization transactions, including a summary of the material terms and conditions of the documents and agreements adopted or entered into in connection with the reorganization transactions, please see “Our Corporate Structure” and “Certain Relationships and Related Party Transactions.”

After completion of this offering, the issuer will be a “controlled company” under the listing standards of the New York Stock Exchange (“NYSE”). For a description of the principal risks and uncertainties associated with our corporate structure and our status as a “controlled company” following this offering, see “Risk Factors—Risks Related to Our Structure.”

6

Table of Contents

The diagram below summarizes our organizational structure immediately after completion of the reorganization transactions, this offering and the application of the net proceeds from this offering (assuming an initial public offering price of $ per share, which is the mid-point of the estimated public offering range set forth on the cover page of this prospectus).

See “Our Corporate Structure,” “Certain Relationships and Related Party Transactions,” and “Description of Capital Stock” for more information on our corporate structure and the rights associated with our common stock, and Units and Grant Units of the Operating LLC.

Our Principal Equityholders

FNFV is a wholly owned subsidiary of FNF. FNF is a leading provider of title insurance, technology and transaction services to the real estate and mortgage industries. FNF is the nation’s largest title insurance company through its title insurance underwriters—Fidelity National Title, Chicago Title, Commonwealth Land Title, Alamo Title and National Title of New York—that collectively issue more title insurance policies than any other title company in the United States. FNF also provides industry-leading mortgage technology solutions and transaction services, including MSP®, the leading residential mortgage servicing technology platform in the U.S., through its majority-owned subsidiaries, Black Knight Financial Services, LLC and ServiceLink Holdings, LLC. In addition, FNF owns majority and minority equity investment stakes in a number of entities, including Remy International, Inc., Ceridian HCM, Inc., Comdata Inc., Digital Insurance, Inc., FNH and us.

Newport is a limited partnership private equity investment fund managed by Newport Global Advisors LP, a Delaware limited partnership (“Newport Global Advisors”) and its controlled affiliates. Newport Global Advisors is a registered investment advisor, with $525 million in assets under management.

7

Table of Contents

Agreements with Our Principal Equityholders

In addition to the documents and agreements described above that comprise the reorganization transactions, in connection with this offering, we intend to enter into certain additional agreements with our existing equity holders regarding aspects of our relationship with them following this offering, including a registration rights agreement. We will also be a party to a reimbursement agreement with FNF, the parent holding company of our largest shareholder, in which we will agree to reimburse FNF, at cost, for certain limited administrative services provided from time to time to us by FNF affiliated employees.

Upon the closing of this offering, we will enter into a tax receivable agreement with FNFV, Newport and other existing equityholders who also hold Units which will obligate us to make payments to such holders following an exchange of Units held by them for shares of our Class A common stock or, at our option, cash from the Operating LLC. The exchanges are expected to produce favorable tax benefits to us and would not be available to us in the absence of such exchanges. Payments will generally equal 85% of the cash savings in U.S. federal and state income tax that we actually realize as a result of these tax benefits for the period beginning with the remainder of the tax year in which the applicable exchange occurs and continuing for each succeeding tax year beginning on or before the sixth anniversary of the date of such exchange. We will retain the benefit of the remaining 15% of the U.S. federal and state tax savings actually realized during these tax years, and all of the U.S. federal and state tax savings for tax years beginning after those covered by the tax receivable agreement.

See “Certain Relationships and Related Party Transactions” for a complete description of the foregoing agreements.

Risk Factors

An investment in our Class A common stock involves a high degree of risk. Our ability to execute on our strategy also is subject to certain risks. These risks are discussed more fully in the section titled “Risk Factors” immediately following this prospectus summary. Some of the more significant challenges and risks include the following:

| • | the impact of, and our ability to react to, general economic conditions and changes in consumer preferences; |

| • | our ability to open new restaurants and operate them profitably, including our ability to locate and secure appropriate sites for restaurant locations, obtain favorable lease terms, attract customers to our restaurants or hire and retain personnel; |

| • | our ability to successfully develop and improve our Stoney River concept; |

| • | our ability to obtain financing on favorable terms, or at all; |

| • | the strain on our infrastructure caused by the implementation of our growth strategy; |

| • | the significant competition we face for customers, real estate and employees; |

| • | the impact of economic downturns or other disruptions in markets in which we have revenue or geographic concentrations within our restaurant base; |

| • | the impact of increases in the price of, and/or reductions in the availability of, commodities, particularly beef; and |

| • | the impact of negative publicity or damage to our reputation, which could arise from concerns regarding food safety and food-borne illnesses or other matters. |

The above list is not exhaustive. Before you invest in our Class A common stock, you should carefully consider all of the information in this prospectus, including matters set forth under the heading “Risk Factors” immediately following this prospectus summary.

8

Table of Contents

Corporate Information

We were incorporated in Tennessee on August 15, 2014. Our principal executive offices are located at 3401 West End Avenue, Suite 260 Nashville, Tennessee 37203, and our telephone number is (615) 269-1900. Our website address is www.jalexandersholdings.com. Our website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference in, and is not considered part of, this prospectus. You should not rely on any such information in making your decision whether to purchase our Class A common stock.

9

Table of Contents

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

We qualify as an emerging growth company as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

| • | a requirement to have only two years of audited financial statements and only two years of related selected financial data and management’s discussion and analysis of financial condition and results of operations disclosure; |

| • | an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”); |

| • | an exemption from new or revised financial accounting standards until they would apply to private companies and from compliance with any new requirements adopted by the Public Company Accounting Oversight Board (“PCAOB”) requiring mandatory audit firm rotation; |

| • | reduced disclosure about the emerging growth company’s executive compensation arrangements; and |

| • | no requirement to seek non-binding advisory votes on executive compensation or golden parachute arrangements. |

The JOBS Act permits emerging growth companies to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to “opt out” of this provision, and as a result, we plan to comply with new or revised accounting standards as required when they are adopted. This decision to opt out of the extended transition period is irrevocable.

We have elected to adopt certain of the reduced disclosure requirements available to emerging growth companies. As a result of these elections, the information that we provide in this prospectus may be different than the information you may receive from other public companies in which you hold equity interests. In addition, it is possible that some investors will find our Class A common stock less attractive as a result of our elections, which may result in a less active trading market for our Class A common stock and more volatility in our stock price.

We may take advantage of these provisions until we are no longer an emerging growth company. We will remain an emerging growth company until the earlier of (1) the last day of our fiscal year following the fifth anniversary of the completion of this offering, (2) the last day our first fiscal year in which we have total annual gross revenue of at least $1.0 billion, (3) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period, and (4) the date on which we are deemed to be a large accelerated filer, which means the market value of our common stock held by non-affiliates exceeds $700 million as of the last business day of our prior second fiscal quarter. During the period in which we remain an emerging growth company, we may choose to take advantage of some but not all of the reduced disclosure requirements described above.

10

Table of Contents

IMPLICATIONS OF BEING A CONTROLLED COMPANY

Upon completion of this offering, after giving effect to the reorganization transactions, FNFV and its affiliates will beneficially own approximately % of the voting power of our outstanding common stock, or % if the underwriters exercise their overallotment option in full.

As a result of its majority ownership, FNFV will have effective control over the outcome of votes on all matters requiring approval by our shareholders, including the election of directors, the adoption of amendments to our charter and bylaws and other significant corporate transactions, including a sale of control of us. These actions may be taken even if other shareholders oppose them.

In addition, as a result of FNFV’s ownership, we qualify as a “controlled company” within the meaning of the corporate governance rules of the NYSE and, consistent with exemptions available to controlled companies, we have elected not to comply with certain corporate governance requirements, including the requirements that (i) a majority of the board of directors consist of independent directors and (ii) that the board of directors have compensation and nominating and corporate governance committees composed entirely of independent directors. Therefore, until such time as we transition to a board with a majority of independent directors, it is possible that our board of directors could be controlled by persons associated with FNFV.

Following this offering, the interests of FNFV may not always coincide with the interests of our other shareholders, and the concentration of control in FNFV will limit other shareholders’ ability to influence corporate matters. The concentration of ownership and voting power of FNFV may also delay, defer or even prevent any transaction involving a change in control of us and may make some transactions more difficult or impossible without their support. Further, FNFV could cause us to take actions including pursuing acquisitions, divestitures, financings or other transactions, that our other shareholders do not view as beneficial.

For additional discussion of the applicable limitations and risks that may result from our status as a controlled company, see “Risk Factors—Risks Related to Our Structure—We are a ‘controlled company’ within the meaning of the NYSE rules, and as a result, we qualify for, and will rely on, exemptions from certain corporate governance requirements. You will not have the same protections afforded to shareholders of companies that are subject to such requirements,” “Management—Overview of our Board Structure” and “Management—Independent Directors” and “—We are controlled by FNFV whose interests may differ from those of our public shareholders.”

11

Table of Contents

THE OFFERING

| Issuer |

J. Alexander’s Holdings, Inc. |

| Class A common stock offered by us |

shares. |

| Class A common stock to be outstanding after this offering |

shares. |

| Class B common stock to be outstanding after this offering |

shares. Each share of our Class B common stock will generally have one vote on all matters submitted to a vote of shareholders but will have no economic rights (including no rights to dividends or distributions upon liquidation). Shares of our Class B common stock will be issued to the holders of Units, other than the issuer, in an amount equal to the number of Units held by such holders. The aggregate voting power of the outstanding Class B common stock will be equal to the aggregate percentage of Units held by the holders of Units. See “Description of Capital Stock.” |

| Voting Rights |

One vote per share; Class A common stock and Class B common stock generally vote together as a single class on all matters submitted to a vote of shareholders. See “Description of Capital Stock.” |

| Exchange |

Holders of Units may exchange their Units (along with a corresponding number of shares of our Class B common stock) at any time upon written notice to us for, at the issuer’s option, either shares of our Class A common stock on a one-for-one basis, subject to customary exchange rate adjustments for stock splits, stock dividends and reclassifications, or a cash payment. When a Unit and the corresponding share of our Class B common stock are exchanged by a Unit holder for a share of Class A common stock, the Unit will become held by the issuer and the corresponding share of our Class B common stock will be canceled. An exchange of Units and shares of Class B common stock for shares of Class A common stock will trigger federal and state income tax liability on the excess of the value of shares of Class A common stock received over the holder’s tax basis for the Units and shares of Class B common stock exchanged. In addition, holders of Grant Units, after such Grant Units vest, may exchange their Grant Units for shares of our Class A common stock or a cash payment, at the issuer’s option, based on the value of the Operating LLC above a specified hurdle amount. Cash payments made on exchange, as well as the number of shares of Class A common stock issuable upon exchange of Grant Units, will be based on trading prices of our Class A common stock on the NYSE. See “Description of Capital Stock.” |

| Over-allotment option |

We have granted to the underwriters an option to purchase up to additional shares of Class A common stock from us at the initial public offering price (less underwriting discounts and |

12

Table of Contents

| commissions) to cover over-allotments, if any, for a period of 30 days from the date of this prospectus. |

| Use of proceeds |

We estimate that the net proceeds from the sale of our Class A common stock in this offering, after deducting the underwriting discount and estimated offering expenses payable by us, will be approximately $ million ($ million if the underwriters exercise their over-allotment option in full) based on an assumed initial public offering price of $ per share (the midpoint of the estimated public offering price range set forth on the cover page of this prospectus). |

| We intend to contribute the entire net proceeds of this offering to the Operating LLC in exchange for up to Units, at a purchase price per Unit equal to the initial public offering price per share of Class A common stock in this offering. We intend that the Operating LLC will use a portion of the net proceeds contributed to it to repay the entire amount of principal and interest (approximately $13,333,000) of the outstanding borrowings under our term loan with Pinnacle Bank and to repay the entire amount of principal and interest (approximately $24,035,000) of the outstanding borrowing under the FNF Note (as defined below). Any remaining net proceeds received by us will be used to continue to support our growth, primarily through opening new restaurants, and for working capital and general corporate purposes. See “Use of Proceeds.” |

| Dividend policy |

We do not intend to pay dividends on our Class A common stock or Class B common stock (which holds no economic interest in the issuer). We plan to retain any earnings for use in the operation of our business and to fund future growth. See “Dividend Policy.” |

| Proposed NYSE Symbol |

We intend to apply to have our Class A common stock listed on the NYSE under the symbol “JAXH.” |

| Risk Factors |

Investing in our Class A common stock involves a high degree of risk. See the “Risk Factors” section of this prospectus for a discussion of factors you should carefully consider before deciding to purchase shares of our Class A common stock. |

Except as otherwise indicated, all information in this prospectus:

| • | assumes no exercise of the underwriters’ option to purchase additional shares to cover over-allotments; |

| • | assumes shares of Class A common stock are reserved for issuance upon the exchange of Units held by FNFV, Newport and individuals that own Units (along with the corresponding number of shares of our Class B common stock); |

| • | assumes shares of Class A common stock are reserved for issuance upon the exchange of Grant Units or other equity awards, which may include profits interests pursuant to the Operating LLC’s Profits Interest Incentive Plan; and |

| • | assumes an initial public offering price of $ per share (the midpoint of the estimated public offering price range set forth on the cover page of this prospectus). |

13

Table of Contents

SUMMARY HISTORICAL AND UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL AND OTHER DATA

The following tables present J. Alexander’s Holdings, Inc.’s summary historical consolidated financial and operating data as of the dates and for the periods indicated. J. Alexander’s Holdings, Inc. was formed as a Tennessee corporation on August 15, 2014. J. Alexander’s Holdings, Inc. has not engaged in any business or other activities except in connection with its formation, the reorganization transactions and this offering. Accordingly, all financial and other information herein relating to periods prior to the completion of this offering is that of J. Alexander’s Holdings, LLC and its consolidated subsidiaries. Financial information through and including September 30, 2012 is referred to as “Predecessor” company information, which has been prepared using the previous basis of accounting. The financial information for periods beginning October 1, 2012 is referred to as “Successor” company information and reflects the financial statement effects of recording fair value adjustments and the capital structure resulting from FNFV’s acquisition of JAC. The summary consolidated financial data as of and for the years ended December 30, 2012 and December 29, 2013 are derived from the audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated financial data as of September 28, 2014 and for the nine months ended September 29, 2013 and September 28, 2014 are derived from the unaudited condensed consolidated financial statements included elsewhere in this prospectus. The results for the nine months ended September 29, 2013 and the nine months ended September 28, 2014 are not necessarily indicative of the results that may be expected for the entire year.

The summary unaudited pro forma consolidated financial data for the nine months ended September 28, 2014 and the fiscal year ended December 29, 2013 present our consolidated results of operations giving pro forma effect to the reorganization transactions, the offering and the contemplated use of proceeds of this offering as if they had occurred at the beginning of fiscal 2013. The pro forma adjustments are based upon available information and certain assumptions that are factually supportable and that we believe are reasonable in order to reflect on a pro forma basis, the impact of the reorganization transactions and this offering on the historical financial information of J. Alexander’s Holdings, LLC. The pro forma results are for informational purposes only and do not reflect the actual results that we would have achieved had we operated as a public company and are not indicative of our future results of operations. See “Unaudited Pro Forma Consolidated Financial Information”.

14

Table of Contents

Financial information for all periods presented has been adjusted to reflect discontinued operations for comparative purposes. The following summary consolidated financial data should be read together with the audited consolidated financial statements, unaudited condensed consolidated financial statements, the unaudited pro forma consolidated financial information, and accompanying notes and information under the caption “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

| Pro Forma | Pro Forma | Successor | Successor | Predecessor | Successor | |||||||||||||||||||||||||

| Dollars in thousands, except Average Weekly Same Store Sales |

Nine Months Ended |

Year Ended December 29, 2013 |

Year Ended December 29, 2013(1) |

October 1, 2012 to December 30, 2012(1) |

January 2, 2012 to September 30, 2012(1) |

Nine Months Ended | ||||||||||||||||||||||||

| September 28, 2014 |

September 28, 2014(1) |

September 29, 2013(1) |

||||||||||||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||||||||

| Net sales |

$ | 188,223 | $ | 40,341 | $ | 116,555 | $ | 148,921 | $ | 138,146 | ||||||||||||||||||||

| Cost of sales |

61,432 | 12,883 | 36,858 | 47,440 | 45,201 | |||||||||||||||||||||||||

| Restaurant labor and related costs |

59,032 | 12,785 | 38,050 | 45,743 | 43,986 | |||||||||||||||||||||||||

| Depreciation and amortization of restaurant property and equipment |

7,228 | 1,425 | 4,117 | 5,703 | 5,328 | |||||||||||||||||||||||||

| Other operating expenses |

39,016 | 7,849 | 23,175 | 30,330 | 28,924 | |||||||||||||||||||||||||

| General and administrative expense |

11,981 | 2,330 | 8,109 | 10,271 | 9,206 | |||||||||||||||||||||||||

| Pre-opening expense |

— | — | — | 162 | — | |||||||||||||||||||||||||

| Transaction and integration expenses |

(217 | ) | 183 | 4,537 | 326 | (275 | ) | |||||||||||||||||||||||

| Asset impairment charges and restaurant closing costs |

2,094 | — | — | 4 | 2,090 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Total operating expenses |

180,566 | 37,455 | 114,846 | 139,979 | 134,460 | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Operating income |

7,657 | 2,886 | 1,709 | 8,942 | 3,686 | |||||||||||||||||||||||||

| Interest expense |

2,888 | 187 | 1,174 | 2,223 | 2,132 | |||||||||||||||||||||||||

| Other, net |

3,055 | 26 | (161 | ) | 96 | 3,024 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Income from continuing operations before income taxes |

7,824 | 2,725 | 374 | 6,815 | 4,758 | |||||||||||||||||||||||||

| Income tax (expense) benefit |

(138 | ) | (1 | ) | 79 | (161 | ) | (220 | ) | |||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||||

| Loss from discontinued operations, net |

— | — | (4,785 | ) | (506 | ) | (1,412 | ) | (331 | ) | (4,758 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net income (loss) |

— | — | $ | 2,901 | $ | 2,218 | $ | (959 | ) | $ | 6,323 | $ | (400 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Income from continuing operations attributable to non-controlling interests |

||||||||||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||||

| Income from continuing operations attributable to J. Alexander’s Holdings, Inc. |

||||||||||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||||||||

| Balance Sheet Data |

||||||||||||||||||||||||||||||

| Cash and cash equivalents |

— | — | $ | 18,069 | $ | 11,127 | $ | 6,853 | $ | 22,964 | $ | 11,217 | ||||||||||||||||||

| Working capital (deficit)(2) |

— | — | 1,001 | (640 | ) | (1,416 | ) | 5,286 | (840 | ) | ||||||||||||||||||||

| Total assets |

— | — | 151,101 | 132,749 | 83,872 | 157,542 | 145,820 | |||||||||||||||||||||||

| Total debt |

— | — | 34,640 | 20,654 | 17,648 | 33,352 | 35,069 | |||||||||||||||||||||||

| Total membership equity |

— | — | 88,455 | 91,394 | 42,508 | 94,712 | 85,154 | |||||||||||||||||||||||

15

Table of Contents

| Successor | Successor | Predecessor | Successor | |||||||||||||||||||

| Dollars in thousands, except Average Weekly Same Store |

Year Ended December 29, 2013(1) |

October 1, 2012 to December 30, 2012(1) |

January 2, 2012 to September 30, 2012(1) |

Nine Months Ended | ||||||||||||||||||

| September 28, 2014(1) |

September 29, 2013(1) |

|||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||||

| Net cash provided by operating activities |

$ | 15,907 | $ | 5,656 | $ | 3,036 | $ | 12,433 | $ | 6,166 | ||||||||||||

| Net cash used in investing activities |

(6,126 | ) | (1,159 | ) | (2,608 | ) | (6,182 | ) | (3,666 | ) | ||||||||||||

| Net cash used in financing activities |

(2,839 | ) | (223 | ) | (7,941 | ) | (1,356 | ) | (2,410 | ) | ||||||||||||

| Capital expenditures |

6,610 | 1,159 | 2,535 | 6,062 | 4,249 | |||||||||||||||||

| Restaurant Operating Profit(4) |

21,515 | 5,399 | 14,355 | 19,705 | 14,707 | |||||||||||||||||

| Restaurant Operating Profit Margin(5) |

11.4 | % | 13.4 | % | 12.3 | % | 13.2 | % | 10.6 | % | ||||||||||||

| Adjusted EBITDA(6) |

17,739 | 4,662 | 11,184 | 15,753 | 12,103 | |||||||||||||||||

| Adjusted EBITDA Margin(7) |

9.4 | % | 11.6 | % | 9.6 | % | 10.6 | % | 8.8 | % | ||||||||||||

| Operating Data: |

||||||||||||||||||||||

| J. Alexander’s: |

||||||||||||||||||||||

| Restaurants (end of period) |

30 | 33 | 33 | 30 | 30 | |||||||||||||||||

| Total same store restaurants (end of period)(3) |

30 | 31 | 31 | 30 | 30 | |||||||||||||||||

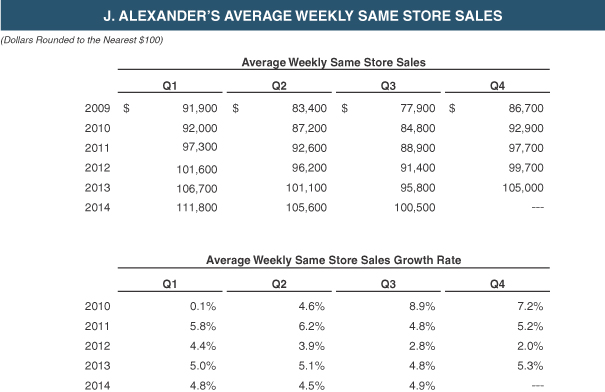

| Average Weekly Same Store Sales |

$ | 102,200 | $ | 99,700 | $ | 96,400 | $ | 106,000 | $ | 101,200 | ||||||||||||

| Change in Average Weekly Same Store Sales(3) |

5.0 | % | 2.0 | % | 3.8 | % | 4.7 | % | 5.0 | % | ||||||||||||

| Stoney River: |

||||||||||||||||||||||

| Restaurants (end of period) |

10 | — | — | 10 | 10 | |||||||||||||||||

| Total same store restaurants (end of period)(3) |

10 | — | — | 10 | 10 | |||||||||||||||||

| Average Weekly Same Store Sales |

$ | 64,200 | — | — | $ | 64,000 | $ | 62,300 | ||||||||||||||

| Change in Average Weekly Same Store Sales(3) |

— | — | — | 2.7 | % | — | ||||||||||||||||

| (1) | We utilize a 52- or 53-week accounting period which ends on the Sunday closest to December 31, and each quarter typically consists of 13 weeks. The period January 2, 2012 to September 30, 2012, included 39 weeks of operations, and the period October 1, 2012 to December 30, 2012, included 13 weeks of operations. Fiscal year 2013 included 52 weeks of operations. Each of the nine-month periods ended September 28, 2014 and September 29, 2013 included 39 weeks of operations. |

| (2) | Defined as total current assets minus total current liabilities. |

| (3) | We consider a restaurant to be comparable in the first full accounting period following the eighteenth month of operations. Changes in same store restaurant sales reflect changes in sales for the same store group of restaurants over a specified period of time. |

16

Table of Contents

| (4) | Restaurant Operating Profit is a metric used by management to measure operating performance at the restaurant level. Restaurant Operating Profit represents net income (loss) before losses from discontinued operations, income tax (expense) benefit, interest expense, gain on extinguishment of debt, stock option expense, general and administrative costs, asset impairment charges and restaurant closing costs, transaction and integration expenses, and other, net non-operating income or expense. Management believes this measure is useful to investors because it allows for an assessment of our operating performance without the effect of general and administrative expenses and other non-operating or unusual costs incurred at the corporate level. The following table presents a reconciliation of Restaurant Operating Profit to net income (loss) for all periods presented: |

| Successor | Predecessor | Successor | ||||||||||||||||||||

| (Dollars in thousands) | Year Ended December 29, 2013 |

October 1, 2012 to December 30, 2012 |

January 2, 2012 to September 30, 2012 |

Nine Months Ended | ||||||||||||||||||

| September 28, 2014 |

September 29, 2013 |

|||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||

| Net income (loss) |

$ | 2,901 | $ | 2,218 | $ | (959 | ) | $ | 6,323 | $ | (400 | ) | ||||||||||

| Loss from discontinued operations, net |

4,785 | 506 | 1,412 | 331 | 4,758 | |||||||||||||||||

| Income tax (expense) benefit |

(138 | ) | (1 | ) | 79 | (161 | ) | (220 | ) | |||||||||||||

| Interest expense |

2,888 | 187 | 1,174 | 2,223 | 2,132 | |||||||||||||||||

| Gain on extinguishment of debt |

(2,938 | ) | — | — | — | (2,938 | ) | |||||||||||||||

| Stock option expense |

— | — | 229 | — | — | |||||||||||||||||

| Other, net |

(117 | ) | (26 | ) | (68 | ) | (96 | ) | (86 | ) | ||||||||||||

| General and administrative expenses |

11,981 | 2,330 | 8,109 | 10,271 | 9,206 | |||||||||||||||||

| Asset impairment charges and restaurant closing costs |

2,094 | — | — | 4 | 2,090 | |||||||||||||||||

| Transaction and integration expenses |

(217 | ) | 183 | 4,537 | 326 | (275 | ) | |||||||||||||||

| Pre-opening expense |

— | — | — | 162 | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Restaurant Operating Profit |

$ | 21,515 | $ | 5,399 | $ | 14,355 | $ | 19,705 | $ | 14,707 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (5) | “Restaurant Operating Profit Margin” is the ratio of Restaurant Operating Profit to net sales. |

17

Table of Contents

| (6) | Adjusted EBITDA is a financial measure that management uses to evaluate operating performance and the effectiveness of its business strategies. Adjusted EBITDA is defined as net income (loss) before interest expense, income tax (expense) benefit, depreciation and amortization, and adding asset impairment charges and restaurant closing costs, loss on disposals of fixed assets, transaction and integration costs, non-cash compensation, loss from discontinued operations, gain on debt extinguishment, pre-opening costs and certain unusual items. Management believes Adjusted EBITDA is a useful metric for investors because it provides a comparative assessment of our operating performance relative to our performance based on our results under GAAP, while isolating the effects of some items that vary from period to period without any correlation to core operating performance. Specifically, Adjusted EBITDA allows for an assessment of our operating performance without the effect of non-cash depreciation and amortization expenses or our ability to service or incur indebtedness. The following table presents a reconciliation of Adjusted EBITDA to net income (loss) for all periods presented: |

| Successor | Successor | Predecessor | Successor | |||||||||||||||||||

| Year Ended December 29, 2013 |

October 1, 2012 to December 30, 2012 |

January 2, 2012 to September 30, 2012 |

Nine Months Ended | |||||||||||||||||||

| (Dollars in thousands) | September 28, 2014 |

September 29, 2013 |

||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||

| Net income (loss) |

$ | 2,901 | $ | 2,218 | $ | (959 | ) | $ | 6,323 | $ | (400 | ) | ||||||||||

| Income tax (expense) benefit |

(138 | ) | (1 | ) | 79 | (161 | ) | (220 | ) | |||||||||||||

| Interest expense |

2,888 | 187 | 1,174 | 2,223 | 2,132 | |||||||||||||||||

| Depreciation and amortization |

7,483 | 1,470 | 4,164 | 5,954 | 5,496 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

13,410 | 3,876 | 4,300 | 14,661 | 7,448 | |||||||||||||||||

| Asset impairment charges and restaurant closing costs |

2,094 | — | — | 4 | 2,090 | |||||||||||||||||

| Loss on disposals of fixed assets |

406 | 62 | 218 | 148 | 301 | |||||||||||||||||

| Transaction and integration costs |

(217 | ) | 183 | 4,537 | 326 | (275 | ) | |||||||||||||||

| Non-cash compensation |

199 | 35 | 717 | 121 | 719 | |||||||||||||||||

| Loss from discontinued operations, net |

4,785 | 506 | 1,412 | 331 | 4,758 | |||||||||||||||||

| Gain on debt extinguishment |

(2,938 | ) | — | — | — | (2,938 | ) | |||||||||||||||

| Pre-opening expense |

— | — | — | 162 | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 17,739 | $ | 4,662 | $ | 11,184 | $ | 15,753 | $ | 12,103 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (7) | “Adjusted EBITDA Margin” is defined as the ratio of Adjusted EBITDA to net sales. |

The following table presents a reconciliation of Adjusted EBITDA to net income (loss) for the predecessor periods indicated below, which are reflected in the Adjusted EBITDA graph included above under “Prospectus Summary—Our Company” and “Business” elsewhere in this prospectus. The financial data for the years ended January 2, 2011 and January 1, 2012 have been derived from the audited consolidated financial statements of our predecessor that are not included in this prospectus.

18

Table of Contents

| Predecessor | Predecessor | |||||||

| (Dollars in thousands) | Year Ended January 1, 2012 |

Year Ended January 2, 2011 |

||||||

| Net income (loss) |

$ | 857 | $ | 2,795 | ||||

| Income tax (expense) benefit |

(290 | ) | 2,352 | |||||

| Interest expense |

1,664 | 1,853 | ||||||

| Depreciation and amortization |

5,619 | 5,682 | ||||||

|

|

|

|

|

|||||

| EBITDA |

8,430 | 7,978 | ||||||

| Asset impairment charges and restaurant closing costs |

— | — | ||||||

| Loss on disposals of fixed assets |

276 | 299 | ||||||

| Transaction and integration costs |

— | — | ||||||

| Non-cash compensation |

962 | 869 | ||||||

| Loss from discontinued operations, net |

2,081 | 2,281 | ||||||

| Gain on debt extinguishment |

— | — | ||||||

| Pre-opening expense |

— | — | ||||||

|

|

|

|

|

|||||

| Adjusted EBITDA |

$ | 11,749 | $ | 11,426 | ||||

|

|

|

|

|

|||||