Attached files

| file | filename |

|---|---|

| EX-4.1 - EX-4.1 - State National Companies, Inc. | a14-16967_1ex4d1.htm |

| EX-10.15 - EX-10.15 - State National Companies, Inc. | a14-16967_1ex10d15.htm |

| EX-23.1 - EX-23.1 - State National Companies, Inc. | a14-16967_1ex23d1.htm |

As filed with the Securities and Exchange Commission on October 22, 2014

Registration No. 333-197441

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3

TO

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

STATE NATIONAL COMPANIES, INC.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

6331 |

|

26-0017421 |

|

(State or other jurisdiction of |

|

(Primary Standard Industrial |

|

(I.R.S. Employer |

1900 L. Don Dodson Drive

Bedford, Texas 76021

(817) 265-2000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

David M. Cleff

Executive Vice President of Business Affairs,

General Counsel and Secretary

1900 L. Don Dodson Drive

Bedford, Texas 76021

(817) 265-2000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

J. Brett Pritchard

Locke Lord LLP

111 South Wacker Drive

Chicago, Illinois 60606

(312) 443-0700

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o |

|

Accelerated filer o |

|

Non-accelerated filer x |

|

Smaller reporting company o |

Calculation of Registration Fee

|

|

|

|

|

|

|

|

|

| |||

|

Common Stock, par value $0.001 per share |

|

30,728,500 |

|

$ |

10.75(1) |

|

$ |

322,686,750 |

|

$ |

41,541.74(1) |

(1) The amount of the registration fee consists of (i) $41,354.36, previously paid on July 15, 2014, in respect of 30,578,500 shares based on a proposed maximum offering price of $10.50 per share, which was the price per share of the most recent trade known to us on July 15, 2014, and (ii) $187.37, in respect of an additional 150,000 shares registered hereunder based on a proposed maximum offering price of $10.75 per share, which is the most recent trade known to us as of the date of this filing, which amount was also previously paid on July 15, 2014.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. Neither we nor the selling shareholders are using this prospectus to offer to sell these securities or to solicit offers to buy these securities in any jurisdiction where the offer or sale of the securities is not permitted.

Subject to Completion, Dated October 22, 2014

30,728,500 Shares of Common Stock, $0.001 Par Value Per Share

This prospectus relates solely to the resale of up to an aggregate of 30,728,500 shares of our common stock by the selling shareholders identified in this prospectus. The selling shareholders acquired the shares of common stock offered by this prospectus in a private placement in June 2014 in reliance on exemptions from registration under the Securities Act of 1933, as amended, and pursuant to our 2014 Stock Incentive Plan. We are registering the offer and sale of the shares of common stock to satisfy registration rights we have granted. See “Security Ownership of Certain Beneficial Owners, Management and Selling Shareholders” beginning on page 114 in this prospectus for a description of the selling shareholders.

The selling shareholders will receive all proceeds from their sale of shares of our common stock, and therefore we will not receive any of the proceeds from their sale of shares of our common stock. The shares which may be resold by the selling shareholders constituted approximately 69% of our issued and outstanding common stock on October 22, 2014.

Prior to the offering pursuant to this prospectus, there has been no public market for our common stock. Our common stock has been approved for listing on the NASDAQ Global Select Market under the symbol “SNC.”

Because all of the shares being offered under this prospectus are being offered by the selling shareholders, we cannot currently determine the price or prices at which our shares of common stock may be sold under this prospectus. We are aware that, prior to the date of this prospectus, certain qualified institutional buyers who purchased shares of our common stock in a private offering that closed in June 2014 have traded shares of our common stock through the FBR PlusTM System, which is operated by FBR Capital Markets & Co. (“FBR”), at prices per share ranging from $10.00 to $10.75 during the period from the closing of the private placement to October 1, 2014 (the date of the most recent trade known to us). Until shares of our common stock are regularly traded or listed on a national securities exchange, we expect that the selling shareholders initially will sell their shares at prices per share between $10.00 and $10.75, if any shares are sold, and thereafter at prevailing market prices or privately negotiated prices. See “Plan of Distribution.”

We are an “emerging growth company” under applicable Securities and Exchange Commission rules and will be eligible for reduced public company reporting requirements. See “Summary—We are an Emerging Growth Company.”

Investing in our common stock involves risks. You should read the section entitled “Risk Factors” beginning on page 14 for a discussion of certain risk factors that you should consider before investing in our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2014

|

|

|

Page |

|

|

|

|

|

|

ii | |

|

|

|

|

|

|

1 | |

|

|

|

|

|

|

14 | |

|

|

|

|

|

|

34 | |

|

|

|

|

|

|

34 | |

|

|

|

|

|

|

35 | |

|

|

|

|

|

|

36 | |

|

|

|

|

|

|

37 | |

|

|

|

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

|

41 |

|

|

|

|

|

|

72 | |

|

|

|

|

|

|

95 | |

|

|

|

|

|

|

103 | |

|

|

|

|

|

|

107 | |

|

|

|

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS, MANAGEMENT AND SELLING SHAREHOLDERS |

|

114 |

|

|

|

|

|

|

120 | |

|

|

|

|

|

|

122 | |

|

|

|

|

|

CERTAIN U.S. FEDERAL INCOME TAX CONSIDERATIONS FOR NON-U.S. HOLDERS |

|

129 |

|

|

|

|

|

|

133 | |

|

|

|

|

|

|

136 | |

|

|

|

|

|

|

139 | |

|

|

|

|

|

|

139 | |

|

|

|

|

|

|

139 | |

|

|

|

|

|

|

F-1 |

This Prospectus

You should rely only on the information contained in this prospectus. We have not authorized any other person to provide you with information that is different from that contained in this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. The selling shareholders are offering to sell and seeking offers to buy our common stock only in jurisdictions where such offers and sales are permitted. You should assume that the information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date. Information contained on our website, or any other website operated by us, is not part of this prospectus.

Frequently Used Terms

In this prospectus, unless the context suggests otherwise:

· references to “the Company,” “we,” “us” or “our” refer to State National Companies, Inc. and all of its consolidated subsidiaries;

· references to “State National” refer solely to State National Companies, Inc.;

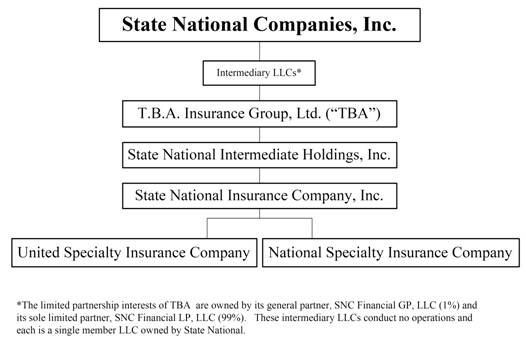

· references to our “insurance company subsidiaries” refer to State National Insurance Company, Inc., a Texas-domiciled insurance company (“SNIC”), and its wholly-owned subsidiaries, National Specialty Insurance Company, a Texas-domiciled insurance company (“NSIC”) and United Specialty Insurance Company, a Delaware-domiciled insurance company (“USIC”). State National Intermediate Holdings, Inc. (“SNIH”) is an indirect subsidiary of State National and an intermediate holding company of SNIC and its wholly-owned subsidiaries, NSIC and USIC;

· all share amounts indicated herein have been adjusted to reflect a 736 for 1 stock split in the form of a stock dividend of shares of our common stock that was effected prior to the completion of the private placement;

· references to “Program Services” refer to the business segment through which we leverage our “A” (Excellent) A.M. Best rating, expansive licenses and reputation to provide access to the U.S. property and casualty insurance market in exchange for a ceding fee;

· references to “expansive licenses” refer to the broad licensing of our insurance subsidiaries to write insurance in the U.S. SNIC and NSIC are admitted carriers licensed to write property and casualty business in all 50 states and the District of Columbia. USIC is an admitted carrier in Delaware and is eligible to write surplus lines in all 50 states and the District of Columbia.

· references to “issuing carrier” arrangements refer to our fronting business in our Program Services segment in which we write insurance on behalf of a capacity provider and then reinsure the risk under these policies with the capacity provider in exchange for ceding fees;

· references to “capacity providers” refer to the foreign and domestic reinsurers, insurers and institutional risk investors that access U.S. property and casualty insurance market through our Program Services or issuing carrier business;

· references to “GAs” refer to general agents who sell, control and administer books of insurance business that are supported by third-party reinsurers;

· references to “ceding fees” refer to the fees we collect and earn in our Program Services segment from our GAs to compensate us for acting as the issuing carrier. These fees do not represent compensation for underwriting and policy acquisition expenses, because we do not incur those costs in our issuing carrier arrangements;

· references to “Lender Services” refer to the business segment through which we provide CPI and certain ancillary insurance products to credit unions, banks and specialty finance companies;

· references to “CPI” refer to collateral protection insurance, which insures personal automobiles, light trucks, SUVs and other vehicles held as collateral for loans made by credit unions, banks and specialty finance companies;

· references to “reinsurer” refer to a company that assumes reinsurance risk;

· references to “quota share reinsurance” refer to reinsurance under which the insurer (the “ceding company”) transfers, or cedes, a fixed percentage of liabilities, premium and related losses for each policy covered on a pro rata basis in accordance with the terms and conditions of the relevant agreement; and

· “private placement” refers to our June 25, 2014 sale of 31,050,000 shares of our common stock in a private placement exempt from registration under the Securities Act of 1933, as amended (the “Securities Act”).

All of the trade names and trademarks included in this prospectus are the property of their respective owners.

Market and Industry Data

Market and industry data used in this prospectus have been obtained from independent sources and publications as well as from research reports prepared for other purposes. Forward-looking information obtained from these sources is subject to the same qualifications and additional uncertainties regarding the other forward-looking statements in this prospectus.

This summary highlights information contained elsewhere in this prospectus, but it does not contain all of the information that you may consider important in making your investment decision. Therefore, you should read the entire prospectus carefully, including, in particular, the “Risk Factors” section beginning on page 14 of this prospectus and the financial statements and related notes included elsewhere in this prospectus before making an investment decision.

Overview

We are a leading specialty provider of property and casualty insurance operating in two niche markets across the United States. In our Program Services segment, we leverage our “A” (Excellent) A.M. Best rating, expansive licenses and reputation to provide access to the U.S. property and casualty insurance market in exchange for a ceding fee. In our Lender Services segment, we specialize in providing collateral protection insurance, or CPI, which insures personal automobiles, light trucks, SUVs and other vehicles held as collateral for loans made by credit unions, banks and specialty finance companies. Our founding shareholders started our CPI business in 1973 and our Program Services business in 1979. Both of these businesses have a long track record of profitable operations.

Our Program Services segment generates significant fee income, in the form of ceding fees, by offering issuing carrier capacity to both specialty general agents or other producers (“GAs”), who sell, control, and administer books of insurance business that are supported by third parties that assume reinsurance risk, or reinsurers, domestic and foreign insurers and institutional risk investors (“capacity providers”) that want to access specific lines of U.S. property and casualty insurance business. Issuing carrier arrangements refer to our business in which we write insurance on behalf of a capacity provider and then reinsure the risk under these policies with the capacity provider in exchange for ceding fees. Our broad licensing authority, strong A.M. Best “A” (Excellent) rating, which is the third highest out of fifteen rating categories used by A.M. Best, and track record of over 25 years of profitable operations allow us to act as the policy-issuing carrier for business produced by GAs or insurers. According to A.M. Best, “A” ratings are assigned to insurers that have an excellent ability to meet their ongoing financial obligations to policyholders.

We reinsure substantially all of the underwriting and operating risks in connection with our issuing carrier arrangements to our capacity providers. In many cases, we hold significant collateral to secure the associated reinsurance recoverables. We have ceded over $10 billion in premiums over 25 years with no unpaid reinsurance recoverables. Because we generally only write in these lines on a fronting or issuing carrier basis, GAs and reinsurers can be confident that we will not compete with them with respect to the business they write through us. In exchange for providing our insurance capacity, licensing and rating to our GA and capacity provider clients, we receive ceding fees averaging in excess of 5% of gross written premiums. For the year ended December 31, 2013, our Program Services segment generated approximately $691 million in gross written premium, $32.9 million of earned ceding fees and $20.5 million in pre-tax income.

Our Lender Services segment generates premium from providing collateral protection insurance, or CPI, to our credit union, bank and specialty finance clients. Our principal product in this segment is CPI. Lenders purchase CPI to provide coverage for automobiles or other vehicles of borrowers who do not uphold their obligation to insure the collateral underlying the loan. Our lender clients pay us directly for CPI and then add the cost of CPI to the borrower’s loan. Our CPI business is fully vertically integrated: we manage all aspects of the CPI business cycle, including sales and marketing, policy issuance, policy administration, underwriting and claims handling. We believe that we are the only vertically integrated CPI provider focused primarily on this product offering, and that the breadth and flexibility of our services enable us to provide our lender clients with responsive and customized policy terms, services and reporting to better serve their needs. We service our CPI clients through InsurTrak, our proprietary technology platform that allows both us and our clients to track and manage a CPI program. We believe our InsurTrak system is highly scalable with the capacity to service a much larger volume of business without significant changes to the system. As of June 30, 2014, we had over 600 CPI clients and were servicing over 3.9 million CPI loans.

We have an exclusive relationship with CUNA Mutual to provide CPI. CUNA Mutual is a leading insurance company focused on providing a range of insurance products to credit unions in the U.S. This alliance provides us access to approximately 95% of the nation’s credit unions through CUNA Mutual’s substantial sales force and has

enabled us to achieve a leading market share of approximately 25% in our core credit union CPI market. We have recently amended our relationship with CUNA Mutual to increase our retention of the business subject to the alliance to 70% from 50% for policies written on or after July 1, 2014. In addition, our integrated CPI platform and InsurTrak have contributed to our ability to write business for credit unions, banks and specialty finance companies. We believe that banks and specialty finance companies present significant growth opportunities for this business. For the year ended December 31, 2013, our Lender Services segment generated $118.9 million in gross written premium, $87.8 million in net written premium and pre-tax income of $15.8 million.

We write our insurance business through our three insurance company subsidiaries, which have expansive licenses to write insurance in the U.S. State National Insurance Company, Inc., or SNIC, and National Specialty Insurance Company, or NSIC, are admitted carriers licensed to write property and casualty business in all 50 states and the District of Columbia. United Specialty Insurance Company, or USIC, is an admitted carrier in Delaware and is eligible to write surplus lines in all 50 states and the District of Columbia. A surplus lines insurer is not directly regulated by the insurance departments in the states in which it writes and as a result has more latitude when insuring hard-to-place risks found in the surplus lines market. Having both admitted and surplus lines authority allows us to provide a broader and more flexible product offering in our issuing carrier business. These companies operate under an intercompany pooling agreement in order to take advantage of our strong “A” (Excellent) group rating from A.M. Best.

Our long history of profitable operations has enabled us to maintain our “A” (Excellent) A.M. Best rating while writing gross premiums in excess of $800 million in 2013 on approximately $145 million of shareholders’ equity, or over five times operating leverage at December 31, 2013. As of June 30, 2014, we had total assets of approximately $1.9 billion. The following table sets forth selected financial data for the periods presented:

|

|

|

Six Months Ended |

|

Year Ended |

| |||||||||||

|

($ in thousands) |

|

2014 |

|

2013 |

|

2013 |

|

2012 |

|

2011 |

| |||||

|

Program Services |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Gross written premium |

|

$ |

436,085 |

|

$ |

246,444 |

|

$ |

691,067 |

|

$ |

530,621 |

|

$ |

613,368 |

|

|

Net written premium |

|

(16 |

) |

(1,044 |

) |

(1,018 |

) |

1,141 |

|

2,431 |

| |||||

|

Ceding fees |

|

20,858 |

|

13,695 |

|

32,898 |

|

32,379 |

|

30,455 |

| |||||

|

Pre-tax income |

|

15,793 |

|

8,710 |

|

20,526 |

|

21,090 |

|

23,972 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Lender Services |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Gross written premium |

|

$ |

55,290 |

|

$ |

50,733 |

|

$ |

118,898 |

|

$ |

104,200 |

|

$ |

99,466 |

|

|

Net written premium |

|

40,690 |

|

37,854 |

|

87,791 |

|

78,024 |

|

77,872 |

| |||||

|

Pre-tax income (loss) |

|

(12,622 |

) |

5,543 |

|

15,793 |

|

9,924 |

|

8,623 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Consolidated |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Gross written premium |

|

$ |

491,375 |

|

$ |

297,176 |

|

$ |

809,965 |

|

$ |

634,821 |

|

$ |

712,834 |

|

|

Net written premium |

|

40,674 |

|

36,810 |

|

86,773 |

|

79,165 |

|

80,303 |

| |||||

|

Ceding fees |

|

20,858 |

|

13,695 |

|

32,898 |

|

32,379 |

|

30,455 |

| |||||

|

Pre-tax income (loss) |

|

(21,342 |

) |

3,843 |

|

25,498 |

|

20,537 |

|

32,877 |

| |||||

|

Net income (loss) |

|

(2,793 |

) |

1,788 |

|

22,711 |

|

15,882 |

|

27,906 |

| |||||

|

Adjusted net income (1) |

|

13,395 |

|

8,688 |

|

22,084 |

|

19,651 |

|

21,570 |

| |||||

(1) Adjusted net income is considered a non-GAAP financial measure because it reflects the following adjustments to net income, which is the most directly comparable measure calculated in accordance with GAAP: the pro forma provision for income taxes as if the Company had been treated as a C Corporation for each period presented, and the exclusion (net of tax benefit) of the increase in the Company’s deferred tax asset as a result of the conversion to C Corporation status, the amount of founder special compensation and the non-recurring offering-related expenses and contract modification expense related to the amendment to our alliance agreement with CUNA Mutual. Management believes this measure is helpful to investors because it provides comparability in evaluating core financial performance between periods. For a reconciliation showing the

effects of these adjustments to net income, see “Management’s Discussion and Analysis of Financial Condition and Results of Operation—Results of Operations—Consolidated Results of Operations.”

Our Business Segments and Services

We have two primary business segments, Program Services and Lender Services.

· Program Services — Our Program Services segment is an issuing carrier business. We leverage our “A” (Excellent) A.M. Best rating, expansive licenses and reputation to provide access to the U.S. property and casualty insurance market to capacity providers in exchange for a ceding fee. Through our issuing carrier business, we write a wide variety of insurance products, principally including general liability insurance, commercial liability insurance, commercial multi-peril insurance, property insurance and workers compensation insurance. We are able to reinsure substantially all of the underwriting and operating risks associated with our issuing carrier arrangements to our capacity providers. We mitigate the credit risk of our capacity providers generally by either selecting well capitalized, highly rated authorized reinsurers or requiring that the reinsurer post substantial collateral to secure the reinsured risks.

· Lender Services — Our Lender Services segment specializes in providing CPI, which insures personal automobiles and other vehicles held as collateral for loans made by credit unions, banks and specialty finance companies. Our lender clients pay us directly for CPI and then add the cost of CPI to the loans of borrowers who do not uphold their obligation to the lender to insure the collateral underlying the loan. We also provide ancillary insurance products that currently are not actively marketed.

Our Competitive Strengths

We believe that our specialized business model provides us with the following competitive strengths:

· Successful and Focused U.S. Specialty Platform. We have a track record of over 25 years of success in the CPI and issuing carrier markets in the U.S. with leading market positions in these two businesses. We believe that our focus on these two niche markets provides us with the opportunity for achieving superior long-term growth and profitability. Our pre-tax income in our Program Services segment was $24.0 million, $21.1 million and $20.5 million for the years ending December 31, 2011, 2012 and 2013, respectively. Our pre-tax income in our Lender Services segment was $8.6 million, $9.9 million and $15.8 million for the years ending December 31, 2011, 2012 and 2013, respectively.

· Efficient, Fee-Based Issuing Carrier Business Model. We have a specialized issuing carrier model providing specialty GAs and capacity providers with access to our “A” (Excellent) rating from A.M. Best, expansive licensing and reputation in exchange for ceding fees averaging in excess of 5% of gross premiums written. For 2013, our Program Services segment generated approximately $691 million of gross written premium and approximately $39.7 million of ceding fees, of which approximately $32.9 million was earned during 2013. We have ceded over $10 billion in premiums over 25 years with no unpaid reinsurance recoverables. We reinsure substantially all liabilities associated with our issuing carrier arrangements and require our GAs (with capacity providers either providing some of these services directly or being responsible for the performance by the GAs) to handle all the services associated with policy administration, claims handling, cash handling, underwriting and other traditional insurance company services. As a result, we generally retain little risk other than the credit risk of the capacity provider, and we incur minimal incremental expense on additional premium volume produced. Using our model, we are able to generate significant gross written premiums on a relatively small capital base compared to other insurance carriers. We believe that our long track record of success in this market and credibility with A.M. Best enables us to maintain our “A” rating with a relatively high operating leverage that we expect would be difficult for a competitor to obtain.

· Vertical Integration and Proprietary Technology in CPI Business. We believe that we are the only fully vertically integrated CPI provider focused primarily on this product offering, in that our operations cover sales, policy issuance, policy administration, underwriting, claims handling and all other aspects of the CPI business cycle. Our integration enables us to provide our lender clients with responsive and customized policy terms, services and reporting to better serve their needs. We believe that other CPI market participants that contract out distribution, policy issuance or other functions of the business are not as well positioned to adapt to market

and product changes and offer customized solutions as we are. In addition, our proprietary insurance tracking system, InsurTrak, delivers real-time visibility to us and our clients into current borrower insurance information. This versatile and scalable system can be easily customized for each client at little incremental cost to us. As of June 30, 2014, we were monitoring insurance status for approximately 3.9 million CPI loans for over 600 lender clients.

· Profitable, Low Risk Business Model. Through our specialized Program Services and Lender Services businesses, we are able to generate profits with limited underwriting risk in our insurance subsidiaries. We have operated our business profitably for over 25 years. We are able to do this in our Program Services business by generating significant ceding fees on gross premiums written and reinsuring substantially all of the risk inherent in the issuing carrier arrangement to our capacity providers, except for the credit risk of the capacity providers, which we mitigate by careful client selection, credit underwriting and, in many cases, significant collateral requirements. Our Program Services business earned ceding fees of approximately $32.9 million, $32.4 million and $30.5 million for the years ended December 31, 2013, 2012 and 2011, respectively. Because we control all aspects of the CPI business operations, we can readily customize our product coverage and reporting to each client. We underwrite each of our lender client accounts and have the ability to move quickly to reprice the business in response to market or financial changes. Our fully vertically integrated CPI business historically has had high frequency but low severity losses and has produced attractive net combined ratios of 85.1%, 91.4% and 93.1% for the years ended December 31, 2013, 2012 and 2011, respectively. The net combined ratio is the sum of the net loss ratio and the net expense ratio, as each is described below, and is a measure of the overall profitability of our Lender Services business, measuring its underwriting profitability and operational efficiency.

· Strong Competitive Position. We believe that our long track record with A.M. Best, insurance regulators and business partners, our specialized business model with significant operating leverage, our experience in assessing and monitoring credit risks and our willingness to refrain from writing primary business that competes with our capacity providers create meaningful market requirements for competitors that may desire to enter the Program Services business. We also believe that our fully vertically integrated CPI business, proprietary technology platform, access to approximately 95% of the credit union market through our exclusive relationship with CUNA Mutual and our 40-year track record of focusing on the CPI market give us a significant competitive advantage in our Lender Services business.

· Proven Leadership and Experienced Management Team. We have a highly experienced and capable management team that is led by Terry Ledbetter, our co-founder and Chairman, President and Chief Executive Officer. Our senior executives have an average of over 22 years of experience with us. Our management team enjoys strong relationships, experience and reputation with rating agencies, insurance regulators and business partners. Utilizing our profitable, specialized business model, our management has positioned us for further growth in the future.

Our Growth Strategies

We intend to continue our profitable growth by focusing on the following strategies:

· Capitalize on Positive Market Opportunities. We believe that recently improved macroeconomic conditions, including rate hardening in property and casualty insurance lines and increasing automobile sales, should provide us with more growth opportunities in both of our business segments. Recent downgrades of certain insurance companies have, and we believe that future downgrades of other insurance companies will, create increased demand for our issuing carrier capacities. We believe that the increased role of capital markets alternatives to reinsurance, the capitalization of recent hedge fund-backed reinsurers and the growth of the off-shore reinsurance market generally, including syndicates of Lloyd’s of London and Bermuda-based reinsurers, should drive demand for our services, as these firms typically do not have direct access to the U.S. market. In our CPI business, we believe that organic growth from our existing lender clients is, and potential new business from banks and specialty finance companies, will be, driven by overall growth in lenders’ portfolios as a result of rising automobile sales, higher average auto loan sizes and increasing credit availability.

· Expand Direct Relationships with Capacity Providers and Specialty GAs. Historically, our issuing carrier capacity has been constrained by the size of our capital base, and we have relied on our relationship-driven channels to generate new issuing carrier business with only a modest sales and marketing effort. In addition, we have historically relied on brokers to identify GAs in need of an issuing carrier. With the additional capital from the private placement, we can address what we believe is increased demand from domestic and international carriers and institutional risk investors. We are seeking to further institutionalize the sales process by building more direct relationships with GAs and capacity providers and by hiring fully-dedicated sales staff. Recent meetings by our senior executives with capacity providers in London and Bermuda and a direct marketing campaign with GAs have produced new business and viable leads. We plan to continue such efforts to further expand our issuing carrier business.

· Expand Our CPI Business within the Banking and the Specialty Finance Company Market. Because of our exclusive relationship with CUNA Mutual, we have focused our CPI business primarily on credit unions. As a result, our penetration in the CPI market for banks and specialty finance companies is low. However, we believe that the CPI market for banks, particularly regional and smaller banks, and specialty lenders is substantially larger than the credit union market and that the specialty finance company market is potentially more attractive to CPI providers due to higher incidences of borrowers’ failing to obtain or maintain the required insurance. We believe that the banking and specialty financing sector represents a significant growth opportunity for us. We recently have begun devoting additional sales and marketing efforts towards this market and are seeking to hire additional dedicated sales staff to address the bank and specialty lender markets. We expect these efforts to further increase the overall amount of CPI business we write.

Our History

The Ledbetter family founded a small general agency in 1973 selling CPI exclusively in Texas. By the late 1970s, the Company began to expand the CPI business beyond Texas.

We acquired the management contract for a Texas county mutual company (the “County Mutual”) in 1979 to accommodate the growth of its CPI business and to reduce operating costs. The management contract enabled us to retain the profits generated from business we originated. After acquiring the management contract for the County Mutual, we received inquiries from other carriers and GAs seeking to access the Texas non-standard automobile market, and recognized the opportunity to act as an issuing carrier. The volume of business that the County Mutual wrote as an issuing carrier grew significantly. Most of this business was non-standard automobile insurance in the state of Texas, and all of this business was 100% reinsured. No A.M. Best rating was required and the County Mutual was able to write at very high leverage ratios. At one time, the County Mutual wrote approximately $400 million of premium on approximately $2 million of capital and surplus. This high degree of leverage, the related reinsurer credit underwriting undertaken to support that leverage, and the significant collateral held against potential losses, were the foundation of our Program Services business model. After legislative changes reduced the advantages of the county mutual model, we sold the management contract controlling the County Mutual in 2009.

In 1984, we formed SNIC to write our CPI business directly. SNIC received an “A” (Excellent) rating from A.M. Best in 1993, and has maintained the rating for over 20 years. To utilize excess capital in SNIC, we expanded our issuing carrier operations outside of Texas.

In 1999, we acquired NSIC, an inactive insurance company licensed to write business in 21 states, and later expanded its licensing to all 50 states in order to write program business on an unrated basis. NSIC later became a subsidiary of SNIC in order to enjoy SNIC’s “A” (Excellent) A.M. Best rating. We formed USIC in 2006 to write coverage on an excess and surplus basis.

In July of 2009, we formed an exclusive relationship with CUNA Mutual, a leading provider of insurance products to credit unions. This alliance provides us with access to their sales force of approximately 200 people and over 95% of the credit union market and has significantly increased our CPI business. Additionally, over the last 15 years, we have expanded our CPI business through opportunistic acquisitions of multiple CPI agencies and books of business.

Our co-founders, Lonnie Ledbetter and Terry Ledbetter, have been instrumental in developing and growing our business. Prior to the completion of the private placement, management responsibilities were shared equally

between the co-founders, with Lonnie serving as Chairman and Chief Executive Officer and Terry serving as President. On a day-to-day basis, Lonnie led the Lender Services segment while Terry led the Program Services segment. In early 2013, Lonnie was diagnosed with cancer and has undergone treatment. Since then, Terry has assumed most of the day to day responsibilities for both segments of the Company. Upon completion of the private placement, Lonnie (age 71) retired and began a one-year consultancy with the Company, and Terry assumed the role of Chief Executive Officer and Chairman, in addition to his title of President.

Our Challenges and Risks

Our company and our business are subject to numerous risks. As part of your evaluation of our business, you should consider the challenges and risks we face in implementing our business strategies, as described in the section of this prospectus entitled “Risk Factors.” Some of the principal risks related to our business include the following:

· Reinsurer credit risk. In our Program Services segment, we write insurance on behalf of our capacity providers and reinsure substantially all of the risk under these policies in exchange for ceding fees. However, as the issuer of the policies, we remain directly liable to these policyholders. In 2013, we wrote insurance policies with approximately $691 million in gross written premiums through our issuing carrier business. If any of our reinsurers becomes insolvent, or otherwise refuses to pay policyholder claims in a timely manner, our liability for these claims could materially and adversely affect our financial condition and results of operations.

· A.M. Best rating. We rely on our “A” rating from A.M. Best to operate our issuing carrier business and our Lender Services business. There can be no assurances that our insurance subsidiaries will be able to maintain this rating. Any downgrade in ratings would likely adversely affect our business through the loss of certain existing and potential policyholders and the loss of relationships with clients that might move to other companies with higher ratings. If we lost our “A” rating, our capacity providers likely would seek a higher rated issuing carrier to write their business. Our Lender Services segment also would be adversely affected if a large number of our accounts were to require an insurer with an “A” rating.

· Regulatory risk. In our Program Services segment, we enter into issuing carrier arrangements with capacity providers that wish to access insurance markets in states in which they are not licensed. The capacity provider administers the business and reinsures substantially all of the risks, and we receive a ceding fee. Some state insurance regulators may object to issuing carrier arrangements. If regulators were to object to an issuing carrier arrangement, our Program Services business could be adversely affected. In our Lender Services segment, we provide lender-placed automobile insurance to financial institutions. A similar product, lender-placed residential hazard insurance, has come under increased regulatory scrutiny and has been subject to recent regulatory changes at both the federal and state levels. If lender-placed automobile insurance becomes subject to similar regulatory scrutiny and is affected by regulatory changes, our CPI business could be adversely affected. Either of these regulatory outcomes could have a material adverse effect on our business, financial condition and results of operations.

Subchapter S Corporation Status

Prior to the completion of the private placement, we elected for our parent company to be taxed for federal income tax purposes as a “Subchapter S corporation” under the Internal Revenue Code and our subsidiaries (other than our insurance subsidiaries and their intermediate holding company) to be pass-through entities for federal income tax purposes. As a result, prior to the completion of the private placement, the income for our parent company and pass-through subsidiaries was not subject to, and we did not pay, U.S. federal income taxes, and no provision or liability for federal or state income tax for our parent company has been included in our consolidated financial statements. Unless specifically noted otherwise, any amounts of our consolidated net income or our basic or diluted earnings per share presented in this prospectus, including in our consolidated financial statements and the accompanying notes appearing in this prospectus, do not reflect any provision for or accrual of any expense for federal income tax liability for our Company for any period presented. The tax provision, assets and liabilities that are reflected in our consolidated financial statements represent those for our insurance subsidiaries, SNIC, NSIC and USIC, and SNIH, as those entities are “C” corporations. Upon the completion of the private placement, our status as a Subchapter S corporation terminated and our income became subject to U.S. federal income taxes.

Corporate Structure

Our corporate structure is as follows:

Private Placement

On June 25, 2014, we completed the sale of an aggregate of 31,050,000 shares of our common stock in a private placement exempt from registration under the Securities Act, which we refer to in this prospectus as the private placement, and received net proceeds of approximately $280.6 million. In the private placement, FBR Capital Markets & Co., or FBR, acted as the initial purchaser for the shares sold to investors pursuant to Rule 144A and Regulation S under the Securities Act, and as placement agent for the shares sold to investors pursuant to Regulation D under the Securities Act. The shares of common stock were sold to investors at an offering price of $10.00 per share, except for 575,000 shares that were sold to FBR and an affiliate of FBR at a price of $9.30 per share, representing the offering price per share sold to other investors less the amount of the initial purchaser discount or placement agent fee per share in the private placement. We determined the offering price per share in the private placement in consultation with FBR. In making such determination we considered many factors, including our business strategy and the amount of capital we needed to raise in the private placement to implement our business strategy, the market demand for our stock and our capital structure.

Of the net proceeds from the private placement, we used approximately (i) $190.6 million to purchase 21,030,294 shares of our common stock from certain of our shareholders pursuant to a stock redemption agreement we entered into with them prior to the private placement at a per share price equal to the net proceeds, after allocable expenses, per share that we received from the private placement, (ii) $17.8 million to make pre-tax payments to CUNA Mutual pursuant to the recent amendment to our Collateral Protection Alliance Agreement with CUNA Mutual, which we refer to as the alliance agreement, to increase our retention of the business subject to the alliance and (iii) $50 million to contribute to the capital of our insurance subsidiaries. We intend to use the remainder of the net proceeds for general corporate purposes.

In connection with the private placement, we entered into a registration rights agreement for the benefit of the holders of the shares sold in the private placement, which are being registered pursuant to the registration statement of which this prospectus is a part. See “Description of Capital Stock—Registration Rights—Purchasers in the Private Placement.”

Determination of Offering Price for This Offering

Because all of the shares being offered under this prospectus are being offered by the selling shareholders, we cannot currently determine the price or prices at which our shares of common stock may be sold under this prospectus. We are aware that, prior to the date of this prospectus, certain qualified institutional buyers who purchased shares of our common stock in a private offering that closed in June 2014, have traded shares of our common stock through the FBR PlusTM System, which is operated by FBR Capital Markets & Co. (“FBR”), at prices per share ranging from $10.00 to $10.75 during the period from the closing of the private placement to October 1, 2014 (the date of the most recent trade known to us). Until shares of our common stock are regularly traded or listed on a national securities exchange, we expect that the selling shareholders initially will sell their shares at prices per share between $10.00 and $10.75, if any shares are sold, and thereafter at prevailing market prices or privately negotiated prices. See “Plan of Distribution.”

We are an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart our Business Startups Act of 2012, commonly known as the JOBS Act. As an emerging growth company, we may take advantage of specified reduced disclosure obligations and reductions in other requirements that are otherwise applicable generally to public companies for up to five years following the effectiveness of the registration statement of which this prospectus is a part. We intend to take advantage of certain of the reduced disclosure requirements applicable to emerging growth companies, including the reduced executive compensation disclosure requirements and the exemption from the requirements under Section 404(b) of the Sarbanes-Oxley Act for auditor attestation relating to internal control over financial reporting. We would cease to be an emerging growth company if we have more than $1.0 billion in annual revenues, have more than $700 million in market value of our capital stock held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period. For the year ended December 31, 2013, we reported approximately $128.5 million in total revenue. As a result, for at least some period of years, our shareholders likely will not have the benefit of certain protective provisions and additional disclosures that would otherwise apply to most public companies.

Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. However, we are choosing to opt out of any extended transition period, and as a result we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for publicly reporting companies which are not emerging growth companies. Section 107 provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Company Information

Our executive offices are located at 1900 L. Don Dodson Drive, Bedford, Texas 76021 and our telephone number is (817) 265-2000. Our website address is www.statenational.com. Information contained on our website is not incorporated by reference into this prospectus, and such information should not be considered to be part of this prospectus.

The Offering

|

Common Stock Offered by the Selling Shareholders |

|

A total of up to 30,728,500 shares of our common stock. The selling shareholders may from time to time sell some, all or none of the shares of common stock pursuant to the registration statement of which this prospectus is a part. |

|

|

|

|

|

Shares of Common Stock Outstanding(1) |

|

44,247,102 |

|

|

|

|

|

Use of Proceeds |

|

The selling shareholders will receive all of the proceeds from the sale of shares of our common stock. We will not receive any proceeds from the sale of shares of our common stock by the selling shareholders. |

|

|

|

|

|

Dividend Policy |

|

We intend to commence the payment of a $0.01 per share cash dividend on a quarterly basis to our shareholders of record beginning in the fourth quarter of 2014 based on third quarter earnings. Any declaration and payment of dividends that may be approved by our board of directors will depend on many factors, including general economic and business conditions, our strategic plans, our financial results and condition, legal and regulatory requirements and other factors that our board of directors deems relevant. Our board of directors may eliminate the payment of future dividends at its discretion, without notice to our shareholders.

Prior to the completion of the private placement, we elected for our parent company to be taxed for federal income tax purposes as a “Subchapter S corporation” under the Internal Revenue Code and our subsidiaries (other than our insurance subsidiaries and their intermediate holding company) to be pass-through entities for federal income tax purposes. We historically made periodic cash distributions to our shareholders that included amounts necessary for them to pay their estimated personal U.S. federal income tax liabilities relating to the items of our income, gain, deductions and losses that pass through to them. Upon the completion of the private placement, State National became taxable as a “C” corporation and has discontinued the manner in which it previously made periodic distributions to its shareholders, including distributions to provide shareholders with funds to pay their estimated personal U.S. federal income tax liabilities. |

|

|

|

|

|

Stock Exchange Symbol |

|

Shares of our common stock are not currently listed on any national securities exchange. Our common stock has been approved for listing on the NASDAQ Global Select Market under the symbol “SNC.” |

|

|

|

|

|

Risk Factors |

|

Investing in our common stock involves a high degree of risk. For a discussion of factors you should consider in making an investment, see “Risk Factors” beginning on page 14. |

(1) Throughout this prospectus, unless the context expressly states otherwise, the number of shares of common stock outstanding excludes: (i) 2,783,873 shares of common stock issuable upon the exercise of stock options outstanding as of the date of this prospectus with a weighted average exercise price of $10.00 per share; and (ii) 1,585,627 additional shares of common stock available for future issuance under our 2014 Stock Incentive Plan.

In addition, throughout this prospectus, unless the context states otherwise, all share amounts give effect to a 736 for 1 stock split in the form of a stock dividend that was effected prior to the completion of the private placement.

Summary Historical Financial Data

The following tables set forth our summary historical consolidated financial information for the periods ended and as of the dates indicated. These selected historical consolidated results are not necessarily indicative of results to be expected in any future period.

You should read the following selected consolidated financial information together with the other information contained in this prospectus, including the section captioned “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes included elsewhere in this prospectus.

The income statement data for the years ended December 31, 2013, 2012 and 2011 are derived from our audited financial statements included elsewhere in this prospectus. The income statement data for the years ended December 31, 2010 and 2009 and the balance sheet data as of December 31, 2011, 2010 and 2009 are derived from our audited financial statements that are not included in this prospectus. The income statement data for the six months ended June 30, 2014 and 2013 and the balance sheet data as of June 30, 2014 are each derived from our unaudited condensed financial statements included elsewhere in this prospectus. Our unaudited consolidated condensed financial statements have been prepared on the same basis as our audited consolidated financial statements and, in our opinion, include all adjustments, consisting of only normal recurring adjustments, necessary for a fair presentation of such financial statements in all material respects. The results of any interim period are not necessarily indicative of results that may be expected for a full year or any future period.

|

($ in thousands, except |

|

For the six months ended |

|

For the years ended |

| |||||||||||||||||

|

for share information) |

|

2014 |

|

2013 |

|

2013 |

|

2012 |

|

2011 |

|

2010 |

|

2009 |

| |||||||

|

OPERATING RESULTS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

Gross written premium (1) |

|

$ |

491,375 |

|

$ |

297,176 |

|

$ |

809,965 |

|

$ |

634,821 |

|

$ |

712,834 |

|

$ |

668,353 |

|

$ |

675,619 |

|

|

Net written premium (1) |

|

40,674 |

|

36,810 |

|

86,773 |

|

79,165 |

|

80,303 |

|

88,598 |

|

92,209 |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

Premiums earned |

|

43,986 |

|

39,482 |

|

84,378 |

|

78,096 |

|

81,974 |

|

90,244 |

|

93,062 |

| |||||||

|

Ceding fees (2) |

|

20,858 |

|

13,695 |

|

32,898 |

|

32,379 |

|

30,455 |

|

31,010 |

|

33,179 |

| |||||||

|

Total revenues |

|

70,930 |

|

58,723 |

|

128,503 |

|

122,123 |

|

124,749 |

|

132,589 |

|

137,840 |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

Net cash from operating activities |

|

(18,141 |

) |

(6,447 |

) |

33,856 |

|

27,060 |

|

30,296 |

|

34,464 |

|

21,521 |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

Reconciliation of adjusted net income: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

Net income (loss) |

|

$ |

(2,793 |

) |

$ |

1,788 |

|

$ |

22,711 |

|

$ |

15,882 |

|

$ |

27,906 |

|

$ |

26,040 |

|

$ |

20,814 |

|

|

Plus (less): Provision for income taxes to reflect change to C corporation status (3) |

|

3,957 |

|

589 |

|

(6,938 |

) |

(2,980 |

) |

(6,779 |

) |

(5,762 |

) |

(3,854 |

) | |||||||

|

Less: Recognition of deferred tax asset upon conversion to C corporation (4) |

|

14,460 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||||

|

Plus: Founder special compensation (5) (6) |

|

11,160 |

|

6,311 |

|

6,311 |

|

6,749 |

|

443 |

|

4,929 |

|

2,815 |

| |||||||

|

Plus: Offering-related expenses (6) |

|

4,441 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||||

|

Plus: Contract modification expense (6) (8) |

|

11,090 |

|

— |

|

— |

|

— |

|

— |

|

— |

|

— |

| |||||||

|

Adjusted net income (7) |

|

$ |

13,395 |

|

$ |

8,688 |

|

$ |

22,084 |

|

$ |

19,651 |

|

$ |

21,570 |

|

$ |

25,207 |

|

$ |

19,775 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

SHARE INFORMATION |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

|

Basic earnings per share |

|

$ |

(0.08 |

) |

$ |

0.05 |

|

$ |

0.66 |

|

$ |

0.46 |

|

$ |

0.82 |

|

$ |

0.76 |

|

$ |

0.61 |

|

|

Diluted earnings per share |

|

(0.08 |

) |

0.05 |

|

0.66 |

|

0.46 |

|

0.82 |

|

0.76 |

|

0.61 |

| |||||||

|

Basic weighted average shares outstanding |

|

34,455,221 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

| |||||||

|

Diluted weighted average shares outstanding |

|

34,455,221 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

|

34,176,896 |

| |||||||

|

|

|

As of |

| |

|

($ in thousands) |

|

2014 |

| |

|

FINANCIAL CONDITION |

|

|

| |

|

Total investments and cash and cash equivalents |

|

$ |

317,954 |

|

|

Deferred income taxes, net |

|

25,042 |

| |

|

Total assets |

|

1,900,203 |

| |

|

|

|

|

| |

|

Total liabilities |

|

1,674,824 |

| |

|

|

|

|

| |

|

Common stock |

|

44 |

| |

|

Additional paid in capital |

|

218,605 |

| |

|

Retained earnings |

|

2,745 |

| |

|

Accumulated other comprehensive income |

|

3,985 |

| |

|

Total shareholders’ equity |

|

$ |

225,379 |

|

(1) The CPI premiums written presented in this document reflect the effects of the allowance for policy cancellations, including any adjustments related to re-estimation of the allowance. As such, the CPI premiums written are those that we expect to earn, which we refer to as “stick premiums,” while those that are expected to cancel are included in the allowance for policy cancellations.

(2) Ceding fees are fees we receive in the Program Services segment in exchange for providing access to the U.S. property and casualty insurance market and are based on the gross premiums we write on behalf of our GA and capacity provider clients. We earn ceding fees in a manner consistent with the recognition of the gross earned premium on the underlying insurance policies, generally on a pro-rata basis over the terms of the policies reinsured. Typically, the reinsured policies have a term of one year. Ceding commissions earned on Lender Services business are not included as ceding fees. CUNA Mutual’s ceding commission is included as a partial offset to commission expense.

(3) Upon the completion of the private placement, our parent company’s status as a Subchapter S corporation terminated and our consolidated income became fully subject to U.S. federal income taxes. This adjustment represents estimated income taxes as if the Company had been treated as a C Corporation for each period presented. The estimated tax was calculated assuming the Company’s blended statutory federal and state income tax rates of 37.7% and 38.1% for the periods ended June 30, 2014 and 2013, respectively, and 38.1%, 37.2%, 35.7%, 35.5% and 34.1% for the years ended December 31, 2013, 2012, 2011, 2010 and 2009, respectively.

(4) As a result of the Company’s conversion to a C Corporation, the deferred tax asset increased by approximately $14.5 million primarily due to the effects of eliminating deferred tax balances on the insurance subsidiaries related to intercompany transactions. This excludes the tax effect related to contract modification expense as discussed in note (8) below.

(5) During the periods presented, we made special compensation payments to our co-founders and principal executive officers, Lonnie Ledbetter and Terry Ledbetter in recognition of their service to our Company. We refer to these payments as “Founder special compensation.” Following the completion of the private placement, we no longer pay Founder special compensation, as Lonnie Ledbetter has retired, and the bonus compensation for the remainder of 2014 for Terry Ledbetter, who now serves as our Chairman, President and Chief Executive Officer, will be determined based on 2014 performance goals. See “Executive Compensation—Executive Incentive Plans.”

(6) Founder special compensation, offering-related expenses, and contract modification expense are shown net of the estimated tax benefit for each period presented. The estimated tax was calculated assuming the Company’s blended statutory federal and state income tax rates of 37.7% and 38.1% for the periods ended June 30, 2014 and 2013, respectively, and 38.1%, 37.2%, 35.7%, 35.5% and 34.1% for the years ended December 31, 2013, 2012, 2011, 2010 and 2009, respectively.

(7) Adjusted net income is considered a non-GAAP financial measure because it reflects the following adjustments to net income, which is the most directly comparable measure calculated in accordance with GAAP: the pro forma provision for income taxes as if the Company had been treated as a C Corporation for each period presented, and the exclusion (net of tax benefit) of the increase in the Company’s deferred tax asset as a result of the conversion to C Corporation status, the amount of founder special compensation and the non-recurring offering-related expenses and contract modification expense related to the amendment to our alliance agreement with CUNA Mutual. Management believes this measure is helpful to investors because it provides comparability in evaluating core financial performance between periods. Management uses adjusted net income to evaluate core financial performance against historical results without the effect of these items.

(8) In connection with the recent amendment to the alliance agreement with CUNA Mutual, we agreed to pay CUNA Mutual $17.8 million. As a result, we recorded contract modification expense of $17.8 million, or $11.1 million net of tax benefit.

An investment in our common stock involves a high degree of risk. Before making an investment decision, you should carefully consider each of the following risk factors and all of the other information set forth in this prospectus. If any one or more of the risks discussed in this prospectus actually occurs, our business, financial condition, results of operations and prospects could be materially and adversely affected, the price of shares of our common stock could decline significantly, and you may lose all or a part of your investment. The risk factors described below are not the only ones that may affect us. Additional risks and uncertainties of which we are currently unaware or that we currently deem immaterial may also adversely affect our business, financial condition, results of operations and prospects. See “Cautionary Statement Concerning Forward-Looking Statements.”

Risks Relating to Our Program Services Segment

We may not be able to recover amounts due from our reinsurers, which would adversely affect our financial condition.

In our Program Services segment, we write insurance on behalf of our capacity providers and reinsure on a quota share basis 100% of the risk under these policies with these carriers in exchange for ceding fees. Because we cede all of these risks to capacity providers, we generally hold no net reserves for losses or loss adjustment expenses that might arise as a result of claims made under these policies. However, as the issuer of the policies, we remain directly liable to these policyholders. In 2013, we wrote insurance policies with approximately $691 million in gross written premiums through our fronting, or issuing carrier, business.

We reinsure substantially all of the underwriting and operating risks in connection with our issuing carrier arrangements to our capacity providers. We take the risk of insolvency or other failure to pay by a capacity provider. We generally select either well capitalized, highly rated authorized capacity providers or we require the capacity providers to post substantial collateral to secure the reinsured risks. However, if any of our capacity providers becomes insolvent, or otherwise refuses to reimburse these policyholders for losses paid (or us, to the extent we reimburse these or pay policyholders or pay other claims directly) in a timely manner, our liability for these claims could materially and adversely affect our financial condition and results of operations. We often hold collateral to protect us against a capacity provider’s failure to pay claims. However, collateral may not be sufficient to cover our liability for these claims, and we may not be able to cause the capacity provider to deliver additional collateral.

As of June 30, 2014, we held approximately $1.6 billion in collateral securing approximately $1.1 billion in reinsurance recoverables. In addition, we have approximately $366.2 million of unsecured reinsurance recoverables. Our reinsurance recoverables are based on estimates, and our actual liabilities may exceed the amount that we are able to recover from our capacity providers or any collateral securing the liabilities. This could occur because the loss experience based on the policy terms is higher than expected or due to litigation, regulatory or other extra-contractual liabilities.

If we fail to realize a reinsurance recoverable owed under these arrangements due to insolvency, dispute with reinsurers as to the meaning or enforceability of reinsurance arrangements or other unwillingness or inability of any of our reinsurers to meet their obligations to us, or due to our inability to access sufficient collateral to cover our liabilities, our business, financial condition, results of operations or prospects could be materially and adversely affected. For additional information, see “Business—Reinsurance.”

If market conditions cause our reinsurance to be more costly or difficult to obtain, we may be required to bear increased risks or reduce the level of our underwriting commitments.

In our Program Services segment, we provide access to the U.S. property and casualty markets in exchange for a ceding fee through our issuing carrier business by providing access to our “A” (Excellent) A.M. Best rating, expansive licensing and reputation. As part of our business strategy for our Program Services segment, we reinsure substantially all underwriting risk, credit risk and business risk related to our issuing carrier business. We may be unable to maintain our current reinsurance arrangements or to obtain other reinsurance in adequate amounts and at favorable rates, particularly if reinsurers become unwilling or unable to support our specialized issuing carrier model in the future. In recent years, our Program Services segment has benefitted from favorable market conditions,

including growth in the role of GAs and of offshore and other alternative sources of reinsurance. A decline in the availability of reinsurance, increases in the cost of reinsurance or a decreased level of activity by GAs could limit the amount of issuing carrier business we could write and materially and adversely affect our business, financial condition, results of operations and prospects.

Regulators may challenge our use of fronting arrangements in states in which our capacity providers are not licensed.

We enter into fronting, or issuing carrier, arrangements with GAs and domestic and foreign insurers that want to access specific U.S. property and casualty insurance business in states in which such capacity provider is not licensed or is not authorized to write particular lines of insurance. The capacity provider or the GA administers the business, settles all claims and reinsures 100% of the risks. We receive a ceding fee, but generally do not share in the profits or losses of the business we write for the capacity provider. Some state insurance regulators may object to our issuing carrier arrangements. In certain states, including Florida and Kentucky, the Insurance Commissioner has the authority to prohibit an authorized insurer from acting as an issuing carrier for an unauthorized insurer. In addition, insurance departments in states in which there is no statutory or regulatory prohibition against an authorized insurer acting as an issuing carrier for an unauthorized insurer, such as New York, could deem the assuming insurer to be transacting insurance business without a license and the issuing carrier to be aiding and abetting the unauthorized sale of insurance.

If regulators in any of the states where we conduct our issuing carrier business were to prohibit or limit the arrangement, we would be prevented or limited from conducting that business for which a capacity provider is not authorized in those states, unless and until the capacity provider is able to obtain the necessary licenses. This could have a material and adverse effect on our business, financial condition results of operations and prospects. In particular, we do significant business in Florida. See “We write at least half of our Program Services business in several key states and adverse developments in these key states could have a material and adverse effect on our business, financial condition, results of operations and prospects.”

Notwithstanding these state law restrictions on ceding insurers, the Nonadmitted and Reinsurance Reform Act (“NRRA”) contained in The Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”) provides that all laws of a ceding insurer’s nondomestic state (except those with respect to taxes and assessments on insurers or insurance income) are preempted to the extent that they otherwise apply the laws of the state to reinsurance agreements of nondomestic ceding insurers. The NRRA places the power to regulate reinsurer financial solvency primarily with the reinsurer’s domiciliary state and requires credit for reinsurance to be recognized for a nondomestic ceding company if it is allowed by the ceding company’s domiciliary state. A state insurance regulator might not view the NRRA as preempting a state regulator’s determination that an unauthorized reinsurer must obtain a license or that a statute prohibited our doing a fronting business. However, such a determination or a conflict between state law and the NRRA could cause regulatory uncertainty about our issuing carrier business, which could have a material and adverse effect on our business, financial condition, results of operations and prospects.

Changes in state insurance regulation could materially and adversely affect our business.

Some states have adopted changes to their insurance laws and regulations that permit insurers to obtain credit for reinsurance from reinsurers who are able to post reduced collateral if they satisfy certain requirements, including specific rating criteria. We require many of our capacity providers to post collateral to secure their reinsurance obligations. If regulatory changes are adopted in the states in which our insurance subsidiaries are domiciled that permit non-admitted reinsurers to post reduced or no collateral in order for the insurer to obtain credit for that reinsurance, it may become more difficult for us to obtain collateral from our capacity providers who meet the applicable rating agency requirements or the capacity providers may no longer need to utilize our issuing carrier arrangements, which could materially and adversely affect the amount of business that we can write.

We depend on a limited number of capacity providers and GAs for a large portion of our gross written premium in our Program Services segment, and the loss of business provided by any one of them could materially and adversely affect us.

Our Program Services segment offers issuing carrier arrangements to both general agents, or GAs, who sell, control, and administer books of insurance business that are supported by third-party reinsurers seeking access to

U.S. property and casualty insurance business, and domestic and foreign insurers, which we collectively refer to as “capacity providers,” that want to access specific U.S. property and casualty insurance business.