Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - BANCORPSOUTH INC | d807086dex991.htm |

| 8-K - 8-K - BANCORPSOUTH INC | d807086d8k.htm |

BancorpSouth, Inc.

Financial Information

As of and for the three months

ended September 30, 2014

Exhibit 99.2 |

Forward Looking Information

2

Certain

statements

contained

in

this

presentation

and

the

accompanying

slides

may

not

be

based

upon

historical

facts

and

are

“forward-looking

statements”

within

the

meaning

of

Section

27A

of

the

Securities

Act

of

1933,

as

amended,

and

Section

21E

of

the

Securities

Exchange

Act

of

1934,

as

amended.

These

forward-looking

statements

may

be

identified

by

their

reference

to

a

future

period

or

periods

or

by

the

use

of

forward-looking

terminology

such

as

“anticipate,”

“believe,”

“could,”

“estimate,”

“expect,”

“foresee,”

“hope”,

“intend,”

“may,”

“might,”

“plan,”

“will,”

or

“would”

or

future

or

conditional

verb

tenses

and

variations

or

negatives

of

such

terms.

These

forward-looking

statements

include,

without

limitation,

statements

relating

to

the

terms,

timing

and

closings

of

the

proposed

mergers

with

Ouachita

Bancshares

Corp.

and

Central

Community

Corporation,

the

Company’s

ability

to

satisfy

the

requirements

of

the

consent

order

issued

by

the

FDIC

and

the

Mississippi

Department

of

Banking

and

Consumer

Finance

(“Mississippi

Banking

Department”),

the

findings

and

results

of

the

investigation

by

the

Consumer

Financial

Protection

Bureau

(the

“CFPB”)

of

the

Company’s

fair

lending

practices,

the

impact

of

certain

claims

and

ongoing,

pending

or

threatened

litigation,

administrative

and

investigatory

matters,

the

Company’s

undertaking

and

performance

of

the

necessary

actions

to

remediate

and

fully

resolve

those

concerns

regarding

the

Company’s

procedures,

systems

and

processes

related

to

certain

of

its

compliance

programs,

including

its

Bank

Secrecy

Act

and

anti-money-laundering

programs,

that

have

been

identified

by

its

federal

bank

regulators,

the

acceptance

by

customers

of

Ouachita

Bancshares

Corp.

and

Central

Community

Corporation

of

the

Company’s

products

and

services

if

the

proposed

mergers

close,

non-accrual

loans

and

any

uncertainty

regarding

repayment,

or

determinations

of

impairment,

of

such

non-accrual

loans,

revenue

estimates

for

the

Company’s

operations

in

Houston,

Texas

following

the

closing

of

the

transaction

with

GEM,

the

retention

of

key

personnel,

Knox’s

continued

operations

and

generation

of

revenues,

the

Company’s

opportunities

to

grow

organically

and

through

acquisitions,

the

Company’s

ability

to

enhance

market

share

in

existing

markets

and

to

gain

acceptance

of

the

Company

generally

in

new

markets,

the

Company’s

focus

on

and

impact

of

cost-saving

initiatives,

the

Company’s

ability

to

improve

efficiency,

trends

in

the

Company’s

operating

expenses,

and

the

Company’s

use

of

non-

GAAP

financial

measures.

The

Company

cautions

you

not

to

place

undue

reliance

on

the

forward-looking

statements

contained

in

this

this

presentation

and

the

accompanying

slides

in

that

actual

results

could

differ

materially

from

those

indicated

in

such

forward-looking

statements

because

of

a

variety

of

factors.

These

factors

may

include,

but

are

not

limited

to,

the

ability

of

the

Company

to

resolve

to

the

satisfaction

of

its

federal

bank

regulators

those

identified

concerns

regarding

the

Company’s

procedures,

systems

and

processes

related

to

certain

of

its

compliance

programs,

including

its

Bank

Secrecy

Act

and

anti-money-laundering

programs,

the

Company’s

ability

to

comply

with

the

consent

order

issued

by

the

FDIC

and

the

Mississippi

Banking

Department,

the

findings

and

results

of

the

CFPB

in

its

review

of

the

Company’s

fair

lending

practices,

the

impact

of

certain

claims

and

ongoing,

pending

or

threatened

litigation,

administrative

and

investigatory

matters,

the

impact

of

the

loss

of

any

key

Company

personnel,

the

findings

and

results

of

the

Consumer

Financial

Protection

Bureau

in

its

review

of

the

Company’s

fair

lending

practices,

the

ability

of

the

Company,

Ouachita

Bancshares

Corp.

and

Central

Community

Corporation

to

obtain

regulatory

approval

of

and

close

the

proposed

mergers,

the

potential

impact

upon

the

Company

of

the

delay

in

the

closings

of

these

proposed

mergers,

the

ability

of

the

Company

to

retain

key

personnel

after

the

closings

of

these

proposed

mergers

and

the

Knox

acquisition,

the

impact

of

the

Company’s

restructuring

of

its

management,

the

conditions

in

the

financial

markets

and

economic

conditions

generally,

the

adequacy

of

the

Company’s

provision

and

allowance

for

credit

losses

to

cover

actual

credit

losses,

the

credit

risk

associated

with

real

estate

construction,

acquisition

and

development

loans,

losses

resulting

from

the

significant

amount

of

the

Company’s

other

real

estate

owned,

limitations

on

the

Company’s

ability

to

declare

and

pay

dividends,

the

impact

of

legal

or

administrative

proceedings,

the

availability

of

capital

on

favorable

terms

if

and

when

needed,

liquidity

risk,

governmental

regulation,

including

the

Dodd-Frank

Act,

and

supervision

of

the

Company’s

operations,

the

short-term

and

long-term

impact

of

changes

to

banking

capital

standards

on

the

Company’s

regulatory

capital

and

liquidity,

the

impact

of

regulations

on

service

charges

on

the

Company’s

core

deposit

accounts,

the

susceptibility

of

the

Company’s

business

to

local

economic

or

environmental

conditions,

the

soundness

of

other

financial

institutions,

changes

in

interest

rates,

the

impact

of

monetary

policies

and

economic

factors

on

the

Company’s

ability

to

attract

deposits

or

make

loans,

volatility

in

capital

and

credit

markets,

reputational

risk,

the

impact

of

hurricanes

or

other

adverse

weather

events,

any

requirement

that

the

Company

write

down

goodwill

or

other

intangible

assets,

diversification

in

the

types

of

financial

services

the

Company

offers,

the

Company’s

ability

to

adapt

its

products

and

services

to

evolving

industry

standards

and

consumer

preferences,

competition

with

other

financial

services

companies,

risks

in

connection

with

completed

or

potential

acquisitions,

the

Company’s

growth

strategy,

interruptions

or

breaches

in

the

Company’s

information

system

security,

the

failure

of

certain

third-party

vendors

to

perform,

unfavorable

ratings

by

rating

agencies,

dilution

caused

by

the

Company’s

issuance

of

any

additional

shares

of

its

common

stock

to

raise

capital

or

acquire

other

banks,

bank

holding

companies,

financial

holding

companies

and

insurance

agencies,

other

factors

generally

understood

to

affect

the

assets,

business,

cash

flows,

financial

condition,

liquidity,

prospects

and/or

results

of

operations

of

financial

services

companies

and

other

factors

detailed

from

time

to

time

in

the

Company’s

press

releases

and

filings

with

the

Securities

and

Exchange

Commission.

Forward-looking

statements

speak

only

as

of

the

date

that

they

were

made,

and,

except

as

required

by

law,

the

Company

does

not

undertake

any

obligation

to

update

or

revise

forward-looking

statements

to

reflect

events

or

circumstances

after

the

date

of

this

this

presentation

and

the

accompanying

slides.

Unless

otherwise

noted,

any

quotes

in

this

this

presentation

and

the

accompanying

slides

can

be

attributed

to

company

management. |

Q3

Highlights As of and for the three months ended September 30, 2014

Net income of $28.8 million, or $0.30 per diluted share

Net operating income of $30.8 million, or $0.32 per diluted share

Progress toward remediating Bank Secrecy Act (“BSA”) and

anti-money-laundering (“AML”) compliance weaknesses

Incurred one-time pre-tax costs of $3.1 million during the quarter

Ongoing costs expected to total approximately $3 million annually

Generated net loan growth of $198.9 million, or 8.5% annualized

Net interest margin increased to 3.62%

Continued credit quality improvement

3 |

Recent

Quarterly Results Dollars in millions, except per share data

NM –

Not Meaningful

4

9/30/14

6/30/14

9/30/13

vs 6/30/14

Net interest revenue

105.6

$

103.1

$

100.2

$

2.5

%

5.4

%

Provision for credit losses

0.0

0.0

0.5

NM

(100.0)

Noninterest revenue

69.3

69.8

62.5

(0.8)

10.8

Noninterest expense

133.7

128.0

129.4

4.5

3.3

Income before income taxes

41.2

45.0

32.9

(8.4)

25.4

Income tax provision

12.4

14.1

8.0

(11.9)

55.2

Net income

28.8

$

30.9

$

24.9

$

(6.8)

%

15.8

%

Net income per share: diluted

0.30

$

0.32

$

0.26

$

(6.3)

%

15.4

%

Three Months Ended

% Change

vs 9/30/13 |

Noninterest Revenue

Dollars in thousands

5

9/30/14

6/30/14

9/30/13

vs 6/30/14

Mortgage lending revenue

6,938

9,089

5,134

(23.7)

35.1

Credit card, debit card and merchant fees

8,972

8,567

8,834

4.7

1.6

Deposit service charges

13,111

12,437

13,679

5.4

(4.2)

Insurance commissions

29,246

28,621

23,800

2.2

22.9

Wealth management

5,961

5,828

6,057

2.3

(1.6)

Other

5,050

5,296

5,010

(4.6)

0.8

Total noninterest revenue

69,278

$

69,838

$

62,514

$

(0.8)

%

10.8

%

% of total revenue

39.6%

40.4%

38.4%

Three Months Ended

% Change

vs 9/30/13 |

Noninterest Expense

Dollars in thousands

NM –

Not Meaningful

6

9/30/14

6/30/14

9/30/13

vs 6/30/14

Salaries and employee benefits

77,453

74,741

73,532

3.6

5.3

Occupancy, net of rental income

10,313

10,245

10,360

0.7

(0.5)

Equipment

4,205

4,169

4,555

0.9

(7.7)

Deposit insurance assessments

2,125

2,035

3,325

4.4

(36.1)

Write-off and amortization of bond issue cost

12

12

2,907

0.0

(99.6)

Advertising & public relations

2,142

2,188

2,315

(2.1)

(7.5)

Foreclosed property expense

5,721

4,202

3,298

36.1

73.5

Data processing, telecom & computer software

7,476

7,972

7,189

(6.2)

4.0

Amortization of intangibles

1,126

1,148

686

(1.9)

64.1

Legal

2,620

3,002

4,626

(12.7)

(43.4)

Merger expense

188

1,009

0

(81.4)

NM

Postage and shipping

1,103

1,116

1,027

(1.2)

7.4

Other miscellaneous expense

19,215

16,115

15,577

19.2

23.4

Total noninterest expense

133,699

$

127,954

$

129,397

$

4.5

%

3.3

%

Non-operating items:

Merger expense

188

1,009

0

BSA-AML charge

3,069

0

0

Legal charge

0

0

1,750

Write off of unamortized TRUPS issue cost

0

0

2,885

Total

3,257

$

1,009

$

4,635

$

Three Months Ended

% Change

vs 9/30/13 |

Loan

Portfolio Dollars in millions

Net loans and leases

7

As of

9/30/14

6/30/14

9/30/13

Commercial and industrial

1,714

$

1,700

$

1,504

$

3.3

%

14.0

%

Real estate:

Consumer mortgages

2,191

2,072

1,931

22.9

13.5

Home equity

518

507

490

8.8

5.7

Agricultural

242

238

235

6.7

3.2

Commercial and industrial-owner occupied

1,509

1,506

1,422

0.8

6.1

Construction, acquisition and development

820

772

724

24.4

13.3

Commercial

1,917

1,902

1,795

3.1

6.8

Credit Cards

109

109

105

1.0

4.1

Other

491

507

567

(12.5)

(13.5)

Total

9,511

$

9,312

$

8,773

$

8.5

%

8.4

%

vs 9/30/13

% Change

vs 6/30/14

Annualized |

Mortgage and Insurance Revenue

Dollars in thousands

8

Mortgage Lending Revenue

9/30/14

6/30/14

3/31/14

12/31/13

9/30/13

Origination revenue

3,736

$

8,758

$

1,964

$

3,590

$

2,862

$

Servicing revenue

4,113

4,058

4,115

4,361

4,072

MSR payoffs/paydowns

(1,559)

(1,616)

(1,138)

(1,240)

(1,560)

MSR valuation adjustment

648

(2,111)

(1,547)

2,894

(240)

Total mortgage lending revenue

6,938

$

9,089

$

3,394

$

9,605

$

5,134

$

Production volume

305,730

$

291,010

$

197,110

$

222,282

$

341,854

$

Purchase money production

244,584

$

241,538

$

143,890

$

160,043

$

229,042

$

Mortgage loans sold

225,444

$

264,478

$

143,213

$

200,665

$

371,271

$

Margin on loans sold

1.66%

3.31%

1.37%

1.79%

0.77%

Insurance Commission Revenue

Property and casualty commissions

22,746

$

21,576

$

19,987

$

15,588

$

18,372

$

Life and health commissions

5,128

5,549

5,010

4,525

4,061

Risk management income

708

617

705

648

628

Other

664

879

5,897

636

739

Total insurance commissions

29,246

$

28,621

$

31,599

$

21,397

$

23,800

$

Three Months Ended |

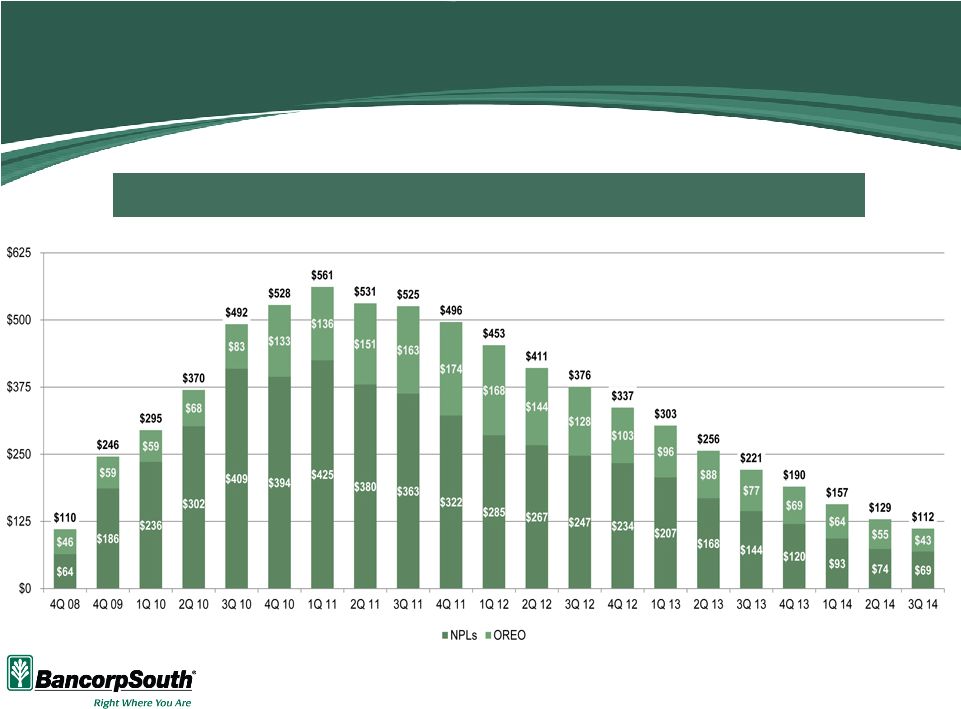

NPLs

decreased $4.7 million, or 6.4%, and NPAs declined $17.3 million,

or 13.4%, quarter over quarter OREO decreased $12.6 million, or 22.7%, quarter

over quarter Near-term delinquencies declined to $24.4 million

No provision for credit losses recorded, which is consistent with no

recorded provision for the second quarter of 2014 and a decline from

$0.5 million for the third quarter of 2013

Net charge-offs were $3.2 million for the third quarter compared with

$2.6 million for the second quarter of 2014 and $7.6 million for

the third

quarter of 2013

58% of non-accrual loans were paying as agreed

Credit Quality Highlights

As

of

and

for

the

three

months

ended

September

30,

2014

“Paying

as

agreed”

includes

loans

that

are

less

than

30

days

past

due

with

payments

occurring

at

least

quarterly

9 |

NPA

Improvement Dollars

in

millions

NPLs

consist

of

nonaccrual

loans,

loans

90+

days

past

due

and

restructured

loans

NPAs

consist

of

NPLs

and

other

real

estate

owned

Total NPAs Have Declined Approximately 50% in the Last 12 Months

10 |

Summary

Non-Financial Highlights

Progress toward remediating BSA/AML compliance weaknesses

Loan production office openings

•

Opened second office in Houston, TX market

•

Chattanooga, TN

Financial Highlights

Meaningful net loan growth

Improvement in net interest margin

Growth in certain non-interest revenue sources

Continued credit quality improvement

Q&A

11 |