Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ALLERGAN INC | d806607d8k.htm |

October 2014

Allergan

An Assessment of Valeant Pharmaceuticals

International, Inc. Performance

Exhibit 99.1 |

Important Information

Certain information contained in this presentation regarding Valeant

Pharmaceuticals International, Inc. (“Valeant”) is taken directly

from information publicly disclosed by Valeant and we do not make any representations or warranties,

either express or implied, with respect to such information’s accuracy or

completeness. In addition, certain other information contained in this

presentation is based on publicly available sources as of the date of this presentation,

and while we have no reason to believe that such information is not accurate, we

can provide no such assurances with respect thereto. The information in this

presentation represents the opinions of Allergan and investors and

stockholders

should

make

their

own

independent

investigations

of

the

matters

referenced

in

this

presentation

and

draw their own conclusions.

2 |

When

Analyzing Valeant’s Q3’14 Performance, We Believe Investors Should

Question: •

Organic growth rates and the quality and thoroughness of the data that Valeant

presents •

The lack of comprehensive product level disclosure including impact of alternative

fulfillment channels

•

Why do many of Valeant’s products appear to lose market share?

•

The sustainability of Valeant’s price increases, which by their own

admission, account for a significant portion of the company’s

growth •

Are Valeant’s stated Q3’14 growth rates positively affected by a weak

Q3’13 and are they reflective of the company’s true performance

going forward? •

Is Valeant’s B&L reporting (for comparison purposes) consistent with

B&L’s historical filings? •

Are post B&L acquisitions reported in B&L results?

•

Does the seeming decrease in value of the Medicis business in Valeant’s hands

raise concerns for other acquired businesses?

•

Can

Valeant

cut

more

costs

at

Allergan

than

it

has

done

in

prior

acquisitions

and

still

maintain

the

growth of the Allergan business?

What is the sustainability of Valeant’s business?

3 |

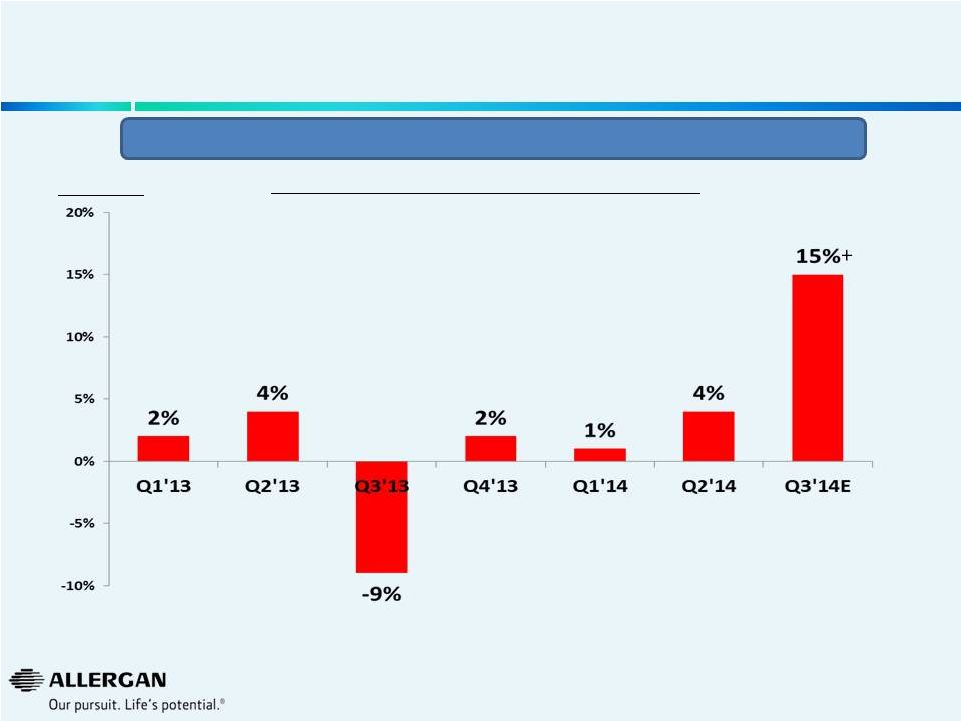

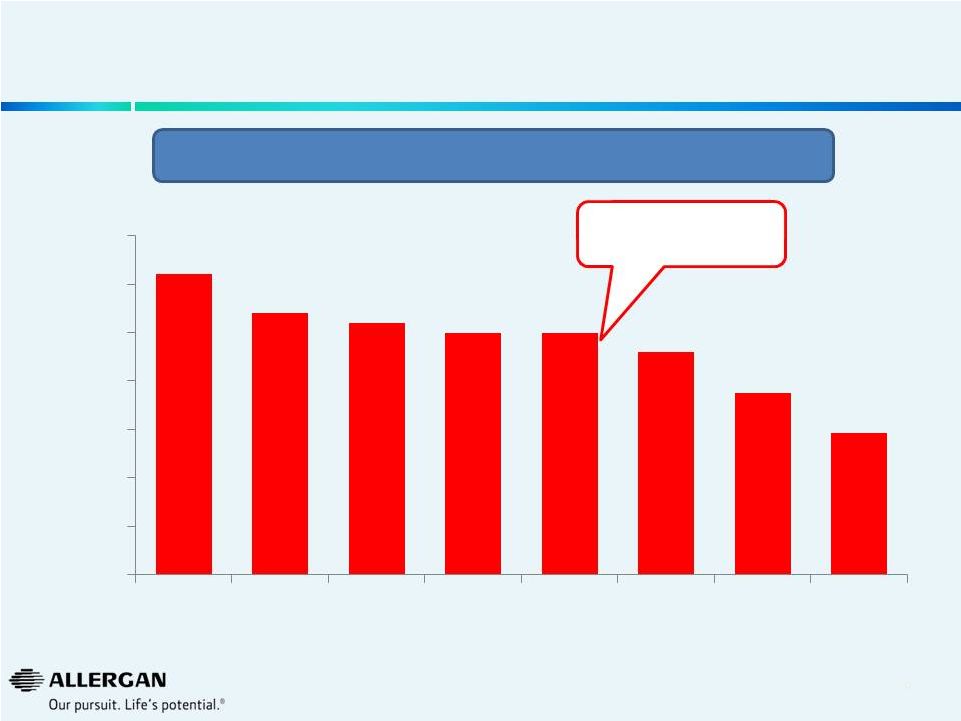

Valeant Quarterly Sales Growth

(as reported by Valeant)

4

We

believe

Q3’14

growth

is

positively

affected

by

a

weak

Q3’13

(B&L

acquisition

on

August

6,

2013)

Source: Valeant public filing on September 30, 2014.

Valeant

Same

Store

Organic

Growth

with

Impact

of

Gx

% Growth Y/Y

+ |

We

Believe Valeant Has No Experience Managing Large, Sophisticated Brands

1

Valeant July 31, 2014 Second Quarter 2014 Financial Results Conference Call

Presentation We believe Valeant does not have experience with large, global

scale products and the requirements to ensure successful

commercialization Q2 2014 YTD

Sales as Reported by Valeant

1

$ in Millions, excludes products divested to Galderma

5 |

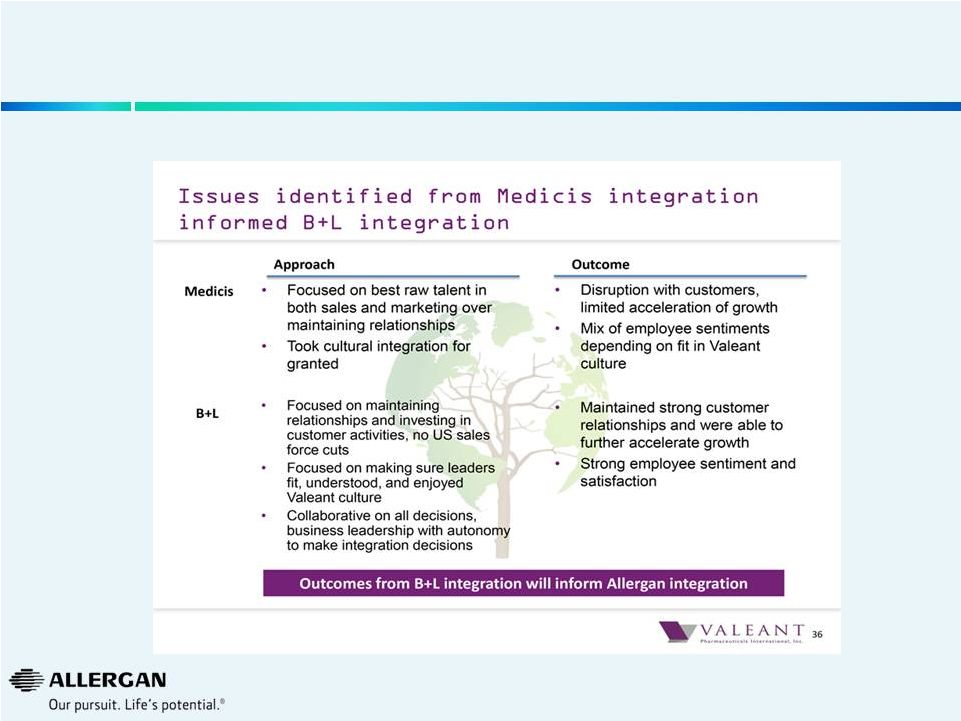

An

Assessment of Valeant’s Performance with Medicis and Bausch & Lomb

Businesses 6

Medicis Acquisition -

December 2012

36%

Bausch & Lomb Acquisition -

August 2013

49%

Synergies

Extracted

1

Company Filings, Wall Street research, the Wall Street Journal and FactSet as of

05/02/14. Bausch & Lomb is based on 2012A Operating expenditures per

B&L filings and announced synergies of $800M. Represents OPEX as a % of Sales.

1

1 |

We

Believe Medicis Performance Has

Deteriorated

Post Valeant Acquisition

7

Source: Valeant SEC Filing, September 2014

•

Valeant’s own assessment of Medicis acquisition |

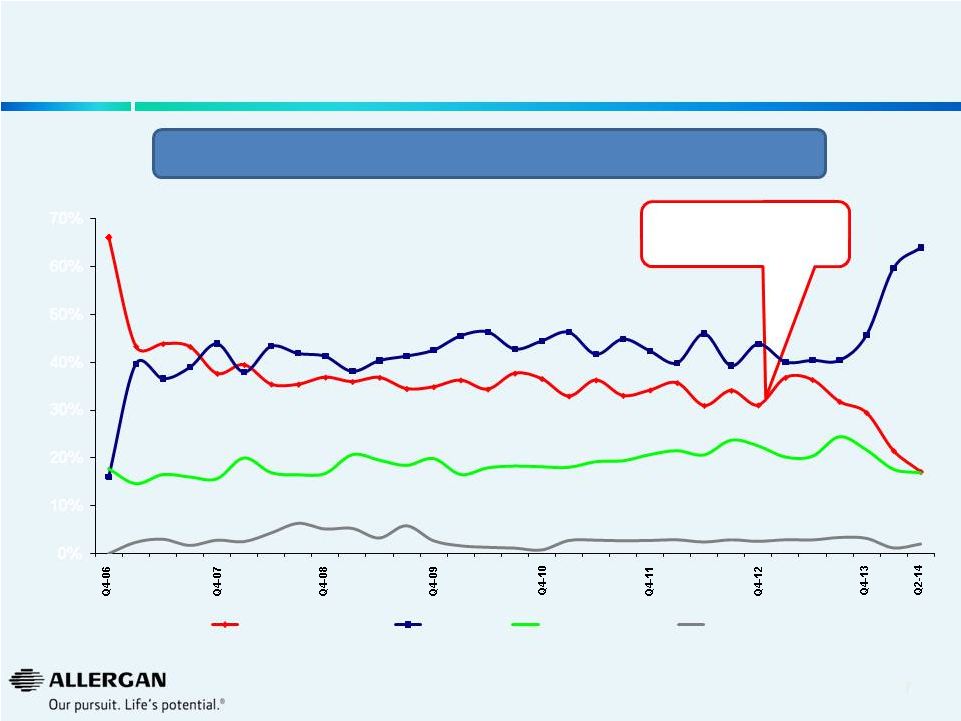

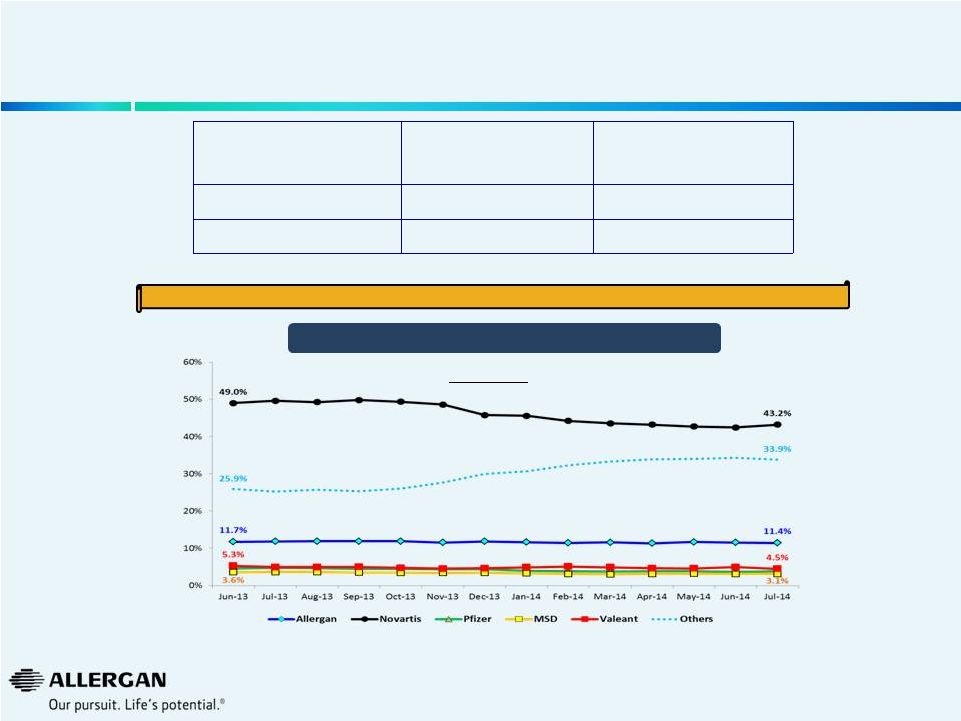

8

U.S. Dermal Facial Fillers Quarterly Market Share

Sources: Mixture of public information (earnings releases, earnings calls,

10K’s, 10Q’s), AGN internal data, syndicated marketing research

reports, analyst reports, GuidePoint Global. Note: Valeant completed the

sale of it’s facial injectable businesses to Galderma in July 2014.

Our

analysis

suggests

there

has

been

a

rapid

erosion

of

purported

“durable”

Medicis

U.S.

Dermal

Filler

business

following

acquisition

&

implementation

of

Valeant

business

model.

8

Valeant’s acquisition of

Medicis in December 2012

66%

38%

37%

35%

37%

34%

31%

29%

17%

16%

44%

41%

43%

45%

42%

44%

46%

0%

10%

20%

30%

40%

50%

60%

70%

Valeant / Medicis

Allergan

Merz / Bioform

others

64% |

9

U.S. Dermal Facial Fillers Market Overview

9

All Numbers are Approximate

Q2’14

Sales ($M)

YOY

Growth

Market

Share

Q2’13

Market

Share

Q2’14

Total Market

$142

+7%

100%

100%

Allergan

$91

+69%

40%

64%

Valeant / Medicis

$24

-50%

36%

17%

Merz

$24

-11%

20%

17%

All Others

$3

-25%

4%

2%

Sources: Mixture of public information (earnings releases, earnings calls,

10K’s, 10Q’s), AGN internal data, syndicated marketing research

reports, analyst reports , GuidePoint Global.

•

Includes hyaluronic acids, collagens and particle polymer fillers. Does not

include silicone, investigational or minor miscellaneous products.

Valeant completed the sale of it’s facial injectable businesses to Galderma

in July 2014. |

10

Valeant / Medicis U.S. Topical Acne Market Share*

Source: IMS Class D10A + Tazorac, of which the vast majority is used for acne. IMS D10A

includes topical anti-acne preparations which includes branded and generic

products; this includes topical antibiotics, retinoids, combinations and others.

Excludes sales through alternative fulfillment channels not captured by IMS.

* Represents dollar market share

10

Valeant’s acquisition of

Medicis

in

December

2012

31%

27%

26%

25%

25%

23%

19%

15%

0%

5%

10%

15%

20%

25%

30%

35%

2008

2009

2010

2011

2012

2013

Q1'14

Q2'14

Our analysis suggests there has been a rapid erosion of purported “durable” Medicis’

U.S. Topical Acne business following acquisition & implementation of Valeant business

model. |

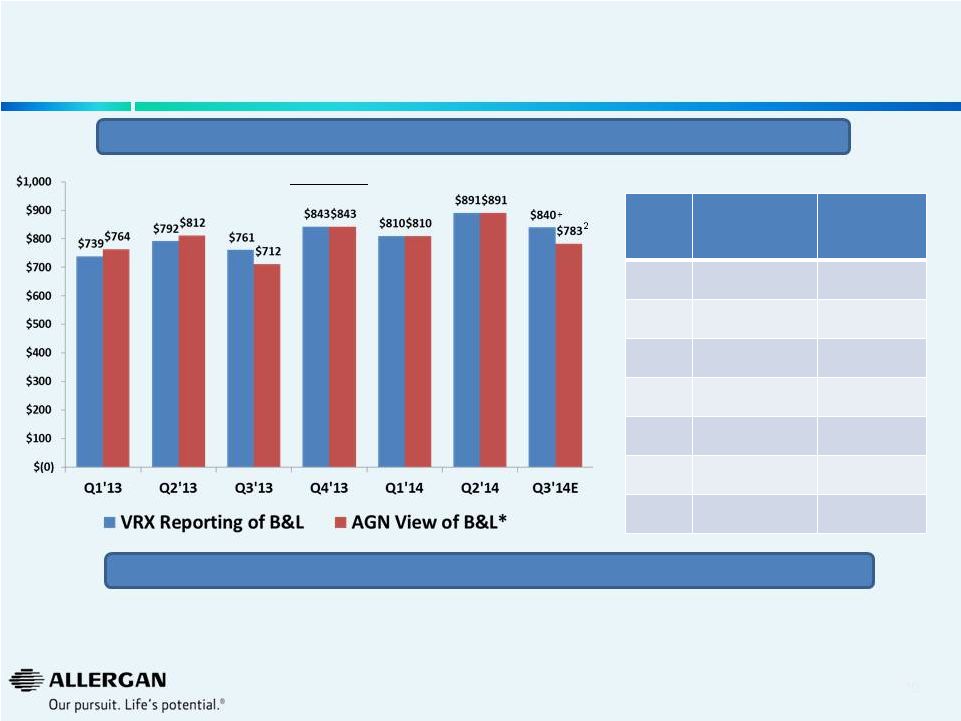

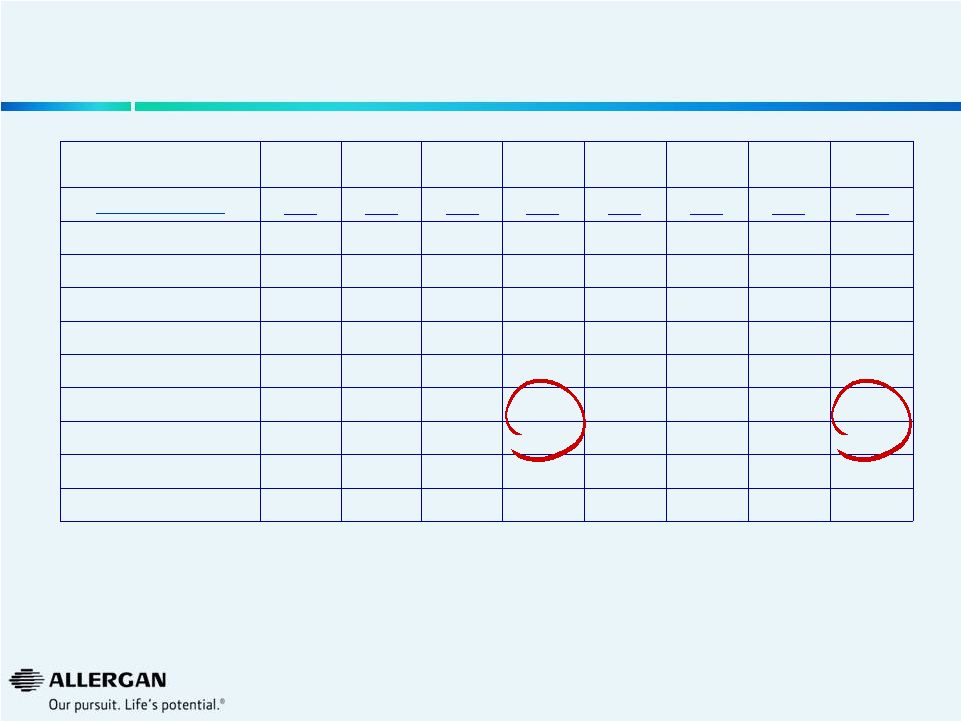

11

Is Valeant Incorporating Sales of Acquired Products in B&L

Sales Reporting?

11

2

Sales Growth

VRX Reporting

of B&L

Sales Growth

AGN View

of B&L

Q1’13

5%

Q2’13

5%

Q3’13

-7%

Q4’13

9%

9%

Q1’14

10%

6%

Q2’14

13%

10%

Q3’14E

10%+

10%1

Are acquisitions (e.g. Croma, Beskon, Visudyne®, Macugen®) included in VRX view of

B&L? Sales $M

+

VRX Reporting of B&L: Product Sales used in Pro Forma Organic Growth as

disclosed in SEC filing on Sept. 30, 2014. * All data from Valeant public

filings. Bausch & Lomb Q1’12, Q2’12, Q1’13, Q2’13 from Bausch & Lomb financial statements included in VRX 6/10/13 and 10/21/13

8Ks. Q3’13 amount derived from subtracting other three quarters from FY13

amount per slide 150 of Valeant 5/28/14 presentation. Q3’12 amount derived from

subtracting other three quarters from FY12 amount per Bausch & Lomb audited

financial statements. Figures not adjusted for currency or divestitures. 1 Based on Sept. 24,

2014 Valeant press release 2

Calculated using 10% Q3’14 Bausch & Lomb update as provided by Valeant on Sept. 24, 2014 over

Q3’13 actual sales dollars based on AGN view of B&L We believe Q3’14

growth is positively affected by a weak Q3’13 (B&L acquisition on August 6, 2013)

|

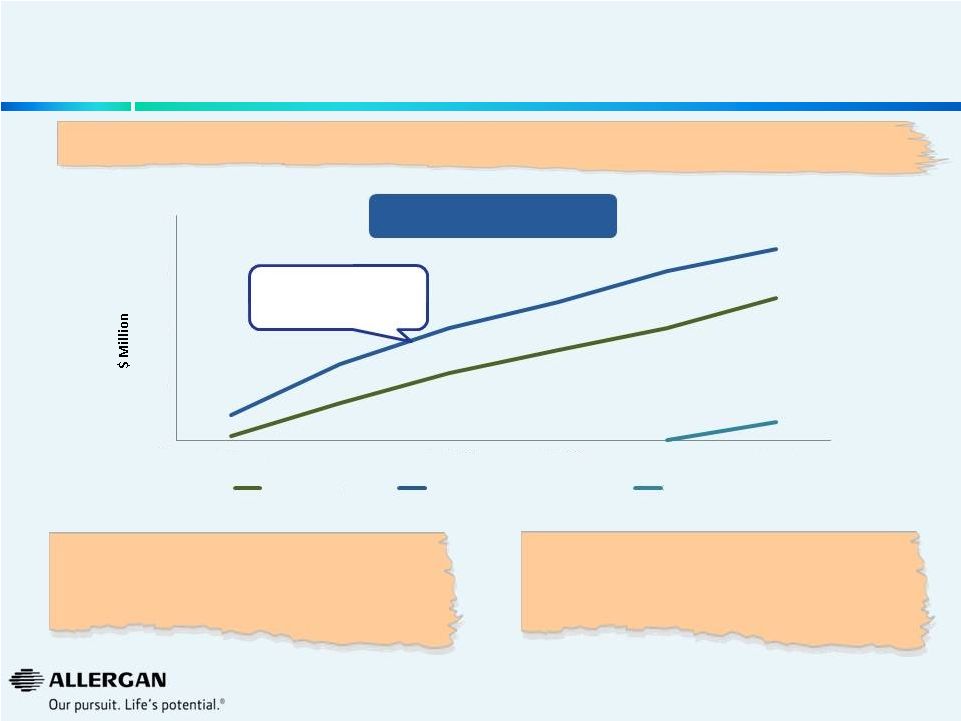

With

Even Greater Reduction of Expenses at B&L Relative to Medicis, What is the

Long-Term Growth Capacity for B&L? Q2 YTD 2014

1

Valeant

investor

presentations

&

public

filings,

IMS

and

Market

Scope

LLC

Quarterly

cataract

report

2

IMS & internal Allergan estimates.

3

Novartis / Alcon, J&J, Cooper public data triangulated with internal Allergan

estimates. 4

Estimates based upon Market Scope LLC Quarterly Cataract Report.

2

2

3

4

4

Global

In our view:

12

B&L

Product

Mix

1

Market

Growth

Weighted

Average

Pharmaceuticals

42%

9%

4%

Contact Lens Care

16%

-5%

-1%

Contact Lenses

24%

5%

1%

Refractive

3%

4%

0%

Cataract & Vitreoretinal

15%

6%

1%

Our Estimated Growth of B&L @ Constant Share

5%

•

If B&L were to maintain constant share at current market growth rates, growth potential

would be ~5%

•

Introduction of line extensions in surgical & consumer businesses will likely lead to

short- term acceleration of growth

•

In-market and ex-factory sales do not necessarily correlate

|

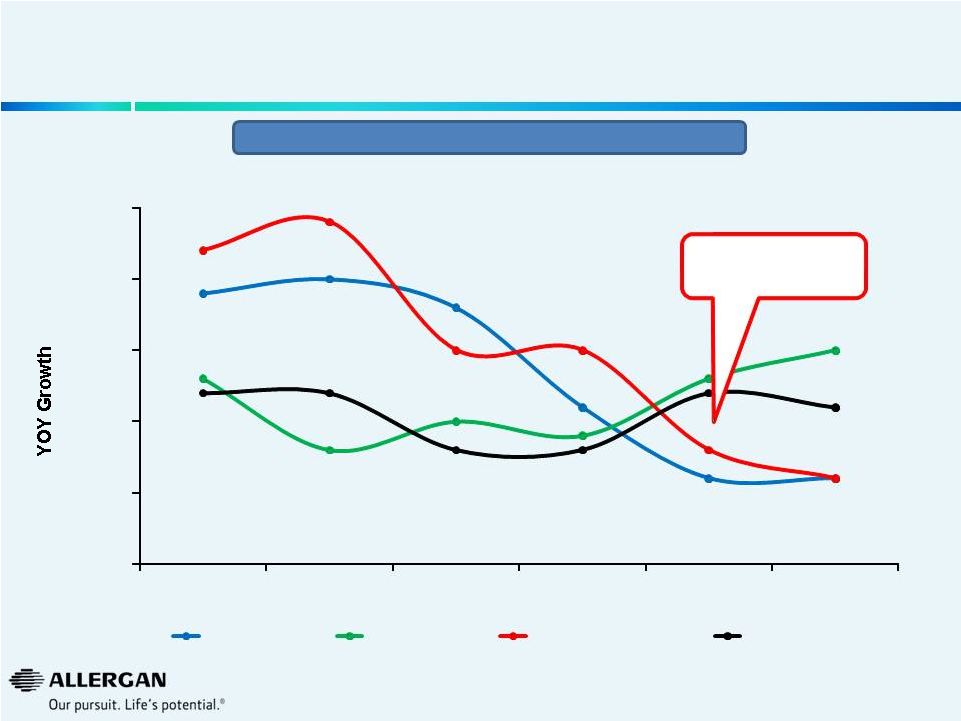

Global Rx Ophthalmics

Major Companies -

YOY Growth

13

Sources: IMS Global (53 countries) at Q2’14 constant exchange rates +

publicly available U.S. retina sales data Deceleration of Valeant / B&L

Growth 22%

24%

15%

15%

8%

6%

0%

5%

10%

15%

20%

25%

2009

2010

2011

2012

2013

YTD Q2'14

Novartis

Allergan

Valeant / B&L

Market

Valeant Acquisition

of B&L in August 2013 |

Source: Analysis based upon US IMS NPA Combined Retail Acquisition Dollars.

Excludes sales through alternative fulfillment channels not captured by

IMS. 1

Represents acquisition $ growth

We Believe Price is a Large Driver of Growth for

Select Valeant U.S. Pharmaceutical Businesses

Q2’14 YTD

Volume

Growth

Price

Growth

Total

Growth

1

Total U.S. B&L

3%

8%

11%

Branded U.S. B&L

(3%)

12%

9%

Generic U.S. B&L

11%

3%

14%

Q2’14 YTD

Volume

Growth

Price

Growth

Total

Growth

1

Total U.S.

(43%)

24%

(19%)

Branded U.S.

(50%)

26%

(24%)

Generic U.S.

93%

(5%)

88%

14

Our Analysis of Bausch & Lomb U.S. Rx In-Market Pharmaceutical Growth

Our Analysis of Valeant U.S. Rx In-Market Skin Care Growth

Sustainability of large price increases? |

We

Believe B&L in Europe is Struggling Post Valeant Acquisition Rx

Ophthalmics Rx Ophthalmics

YOY Growth

Pre Valeant

Takeover

Post Valeant

Takeover

Europe 28

8.3%

3.3%

Europe 5

8.0%

1.0%

Europe Rx Ophthalmic Market Share

15

Europe 28

We believe Valeant has lost share over the last twelve months in the Rx Ophthalmics

Market Source: IMS, US$ ‘000 @ constant currency,

Ex-Manufacturer Prices Pre Valeant Takeover: MAT growth August 2013 vs.

August 2012 Post Valeant Takeover:: MAT growth August 2014 vs. August

2013 Europe 5: Germany, France, UK, Italy & Spain

Europe 28: Europe 5, Turkey, South Africa, Poland, Greece, Egypt, Saudi Arabia,

Czech Republic, Hungary, Romania, Croatia, Sweden,

Finland,

Norway,

Denmark,

Belgium,

Netherlands,

Austria,

Switzerland

,

Portugal,

Ireland,

Russia,

Slovakia

&

Slovenia |

Valeant Europe Sales Weakness

Rx Ophthalmics

Source: IMS, at constant currency, Ex-Manufacturer Prices

We believe Valeant Sales Growth in Europe Rx Ophthalmics Continues to Show Negative

Trends 16

Valeant Europe 5

Valeant Europe 28

Europe 5: Germany, France, UK, Italy & Spain

Europe 28: Europe 5, Turkey, South Africa, Poland, Greece, Egypt, Saudi Arabia,

Czech Republic, Hungary, Romania, Croatia, Sweden,

Finland,

Norway,

Denmark,

Belgium,

Netherlands,

Austria,

Switzerland

,

Portugal,

Ireland,

Russia,

Slovakia

&

Slovenia

1.0%

3.1%

0.3%

2.8%

-2.5%

0.8%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

YOY Growth (July 2014)

MAT

YTD

Last 3 Months |

We

Believe Long-Term Performance of B&L Device Businesses Lag Market

Growth Source: Market Scope LLC Quarterly Cataract Report. In-Market

Growth. Back-up information contained in Appendix. U.S. IOL

Procedures Q3’12 to Q2’14

Market Growth

7%

VRX Growth

-2%

U.S. Phacoemulsification

Procedures

Q3’12 to Q2’14

Market Growth

7%

VRX Growth

-8%

U.S. Viscoelastic

Procedures

Q3’12 to Q2’14

Market Growth

-8%

VRX Growth

-22%

We

Believe

Valeant

has

a

weak

market

share

position

(ranks

#3

in

procedural

share)

in

each

of

these

categories

Valeant Acquisition of B&L in August 2013

17 |

What

is the True Underlying Performance of B&L U.S. Surgical Business in

Q3’14? 18

“U.S.

Ophthalmic

Surgical

business

is

currently

on

a

pace

to

show

approximately

15% growth from the third quarter of 2013 to the upcoming third quarter of

2014. This includes:

•

Greater than 70% growth for the cataract refractive business

•

Greater than 50% growth for Stellaris and Stellaris PC

•

Data showing that the U.S. surgical business is the fastest growing IOL

(intraocular lens) company when comparing first–quarter 2014 results

versus first–quarter 2013 (Data from Market Scope, an ophthalmic market

research firm)

•

In

the

second

quarter,

our

growth

has

more

than

doubled

that

of

the

market

in

procedures”

-

Valeant Voice, September 22, 2014 8K SEC Filing

|

U.S.

IOL Procedure Trends Source: Market Scope LLC Quarterly Cataract

Report Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

Market (000s)

889

951

869

909

916

964

879

954

Alcon

512

548

503

549

547

567

495

555

AMO

205

229

195

207

210

233

209

225

Valeant

113

113

104

100

116

125

128

111

others

60

60

66

54

43

39

47

64

Market Growth

3%

11%

1%

2%

3%

1%

1%

5%

Valeant Growth

-9%

3%

-1%

-19%

3%

10%

24%

11%

Valeant Share

12.7%

11.9%

11.9%

11.0%

12.7%

13.0%

14.6%

11.6%

19 |

We

Believe Valeant’s Forecasting Approach Raises Questions on Future Growth

Example: Glaucoma

No new products are

tracking to more than

$250MM globally

“We believe mgt's forecasts of $500M in the US and

~$1B globally are very aggressive and we don’t

understand how they get to these forecasts.”

(UBS, 9/26/14)

“I model ~$150M peak sales for this drug in my base

case. For me to raise my estimates on latanoprostene

bunod, I'd like to see clear differentiation vs

prostaglandins.”

(ISI, 9/25/14)

Global Sales (IMS)

Most Recent Glaucoma Launches

“This

product

[latanoprostene

bunod]

has

peak

sales

potential

of

~$500

million+

in

the

U.S.

alone

and

~$1

billion+

globally.”

(Valeant,

9/25/14)

20

Permission to use quotes was neither sought nor received.

(Alcon)

(Alcon)

(Santen)

0

50

100

150

200

MAT Q2/09

MAT Q2/10

MAT Q2/11

MAT Q2/12

MAT Q2/13

MAT Q2/14

AZARGA (2008)

TAFLOTAN/ SAFLUTAN (2008)

SIMBRINZA (2013) |

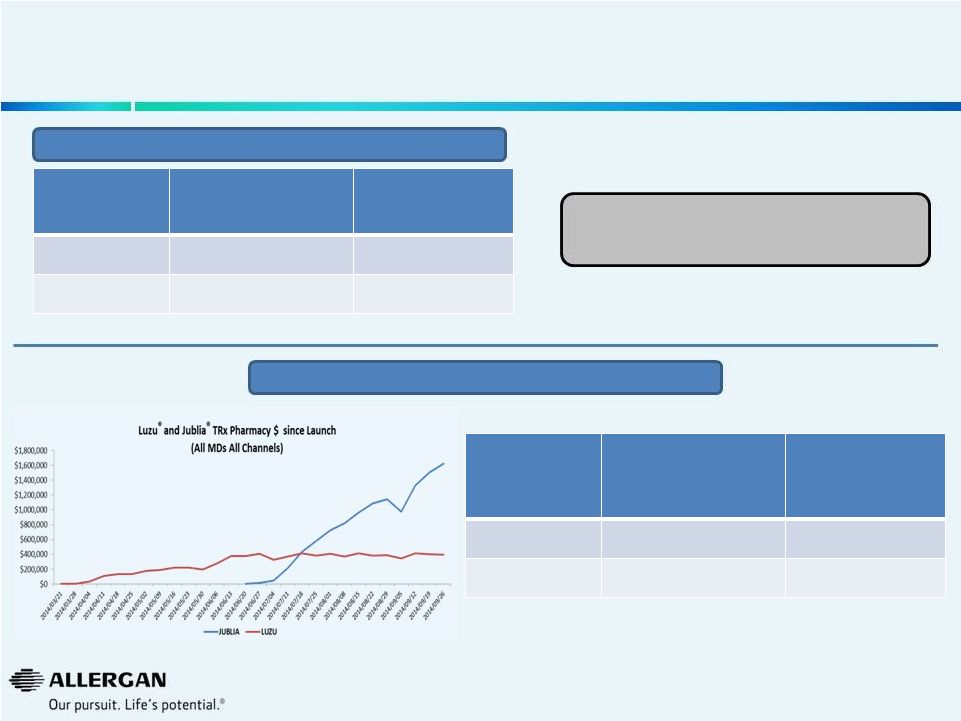

We

Believe Valeant’s Forecasting Approach Raises Questions on Future Growth

Example: Jublia

®

& Luzu

®

Valeant

Evaluate

Pharma

2

Jublia

®

$300 -

$800M

$300M

Luzu

®

$50 -

$75M

$88M

Peak Sales Estimates

All MD’s

All Channels

YTD TRx

Pharmacy $

(Sept. 26, 2104)

Annual Run

Rate

Jublia

®

$11.5M

$34.5M

Luzu

®

$7.9M

$15.8M

1

IMS, excludes sales through alternative fulfillment channels not captured by

IMS. 2

EvaluatePharma Worldwide sales estimates for 2020

3

IMS. 2003.

Prescription Trends

1

21

Prior market leader (Penlac Nail Lacquer)

pre-genericization

peaked

at

~$143M

3 |

Appendix |

Valeant has Taken Substantial Price Increases Over the Past Year

Product

Price Increases

Oct’13 to Oct’14

Timolol Maleate Ophthalmic Gel Forming Solution 0.25 %

146%

Targretin

142%

Syprine Oral Capsule 250 MG

88%

Wellbutrin XL Oral Tablet Extended Release 24 Hour 150 MG

72%

Arestin Dental Miscellaneous 1 MG

55%

Zovirax

33%

Elidel External Cream 1 %

26%

Istalol Ophthalmic Solution 0.5 %

25%

Lotemax

24%

Zirgan Ophthalmic Gel 0.15 %

17%

Alrex Ophthalmic Suspension 0.2 %

17%

Bepreve Ophthalmic Solution 1.5 %

16%

Zylet Ophthalmic Suspension 0.5-0.3 %

14%

Besivance Ophthalmic Suspension 0.6 %

14%

Xenazine Oral Tablet 12.5 MG

14%

Prolensa Ophthalmic Solution 0.07 %

13%

Solodyn Oral Tablet Extended Release 24 Hour 105 MG

9%

Lacrisert Ophthalmic Insert 5 MG

9%

Acanya External Gel 1.2-2.5 %

9%

Timoptic

6%

Source: Wolters Kluwer Price Rx®

Pro

All products are registered trademarks of Valeant

23 |

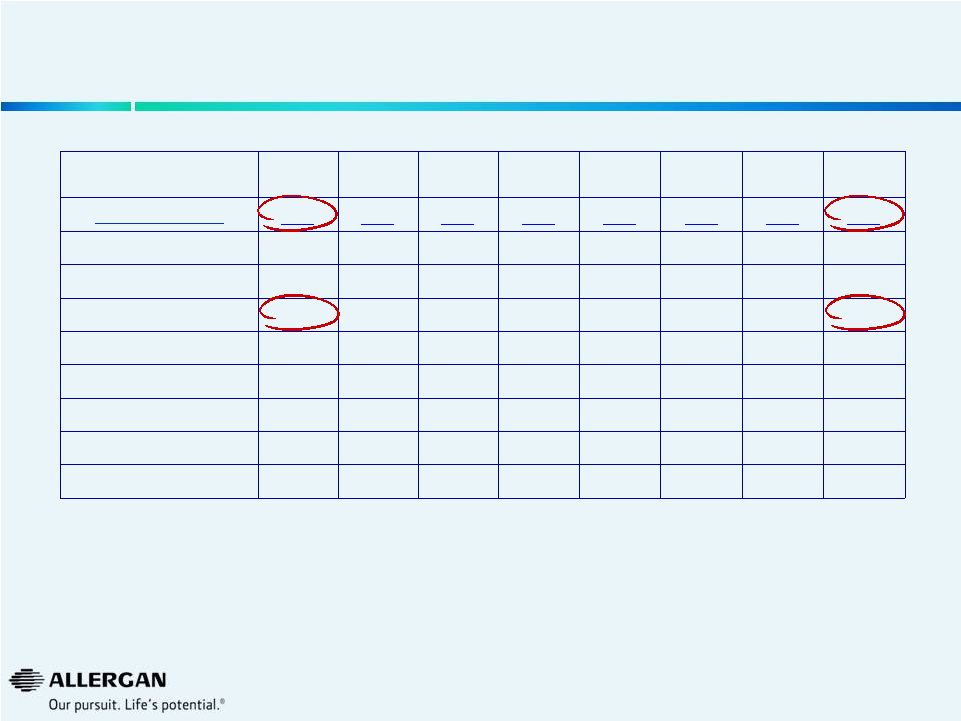

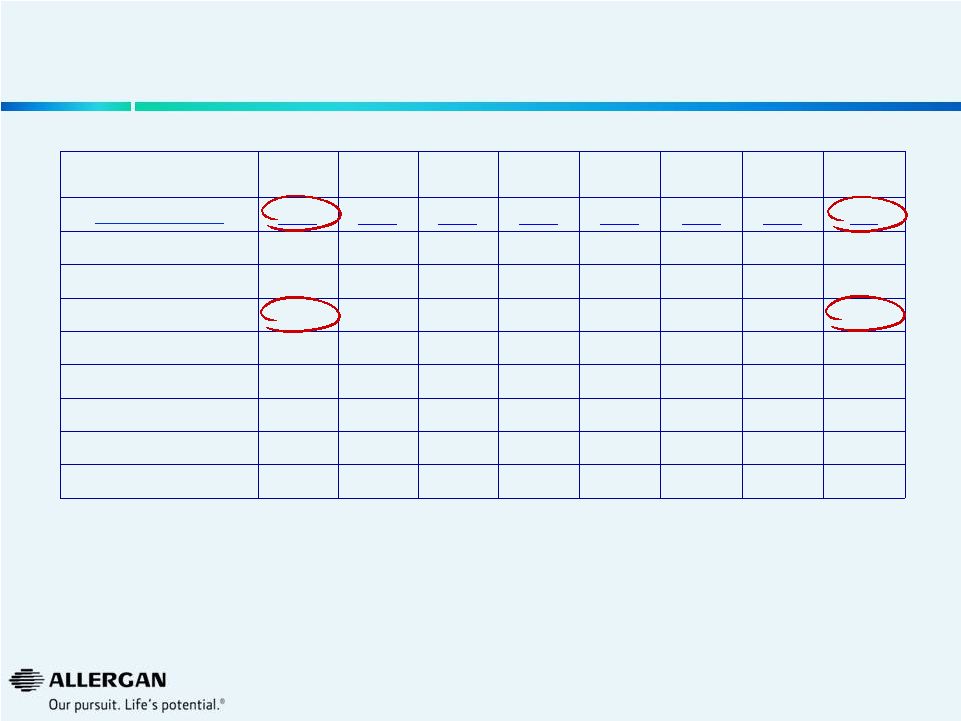

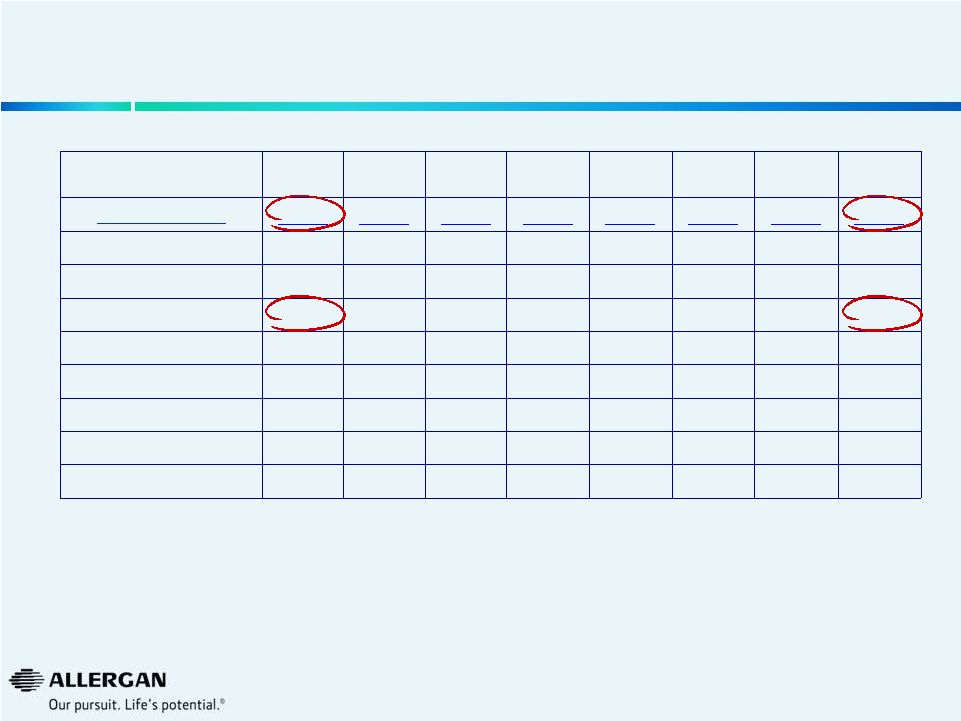

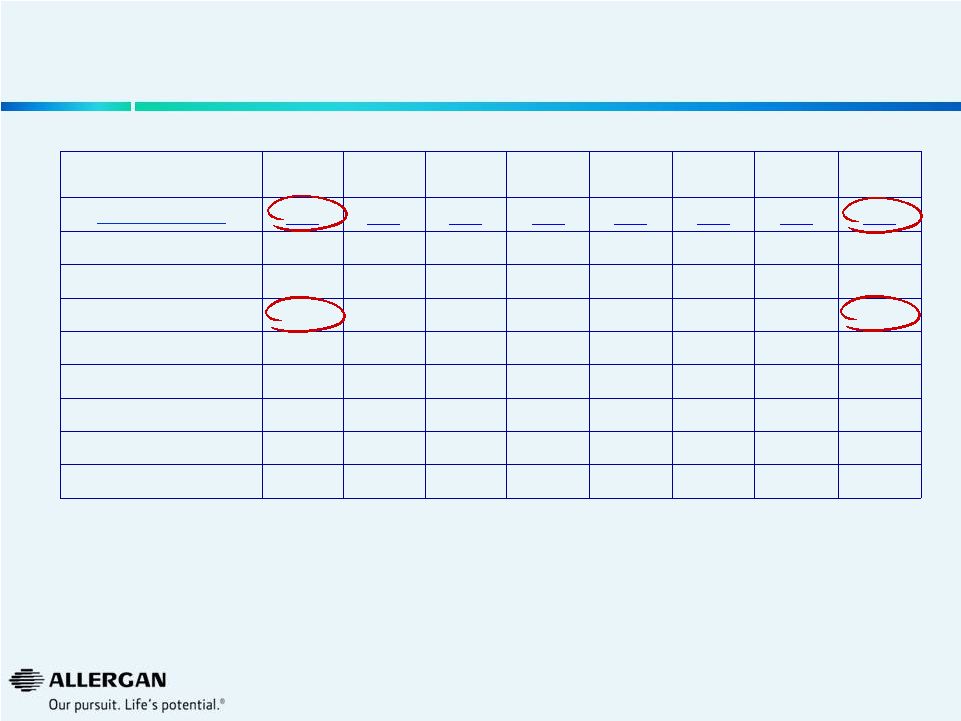

U.S.

Phacoemulsification Procedure Trends Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

Market (000s)

889

951

848

915

912

954

879

954

Alcon

625

670

620

693

683

727

625

707

AMO

136

149

107

118

121

127

121

130

Valeant

128

131

121

104

108

100

133

118

Others

0

1

1

0

0

0

0

0

Valeant Growth

1%

12%

13%

-9%

-16%

-24%

10%

13%

Valeant Share

14.4%

13.8%

14.2%

11.4%

11.9%

10.5%

15.1%

12.3%

Source: Market Scope LLC Quarterly Cataract Report

24 |

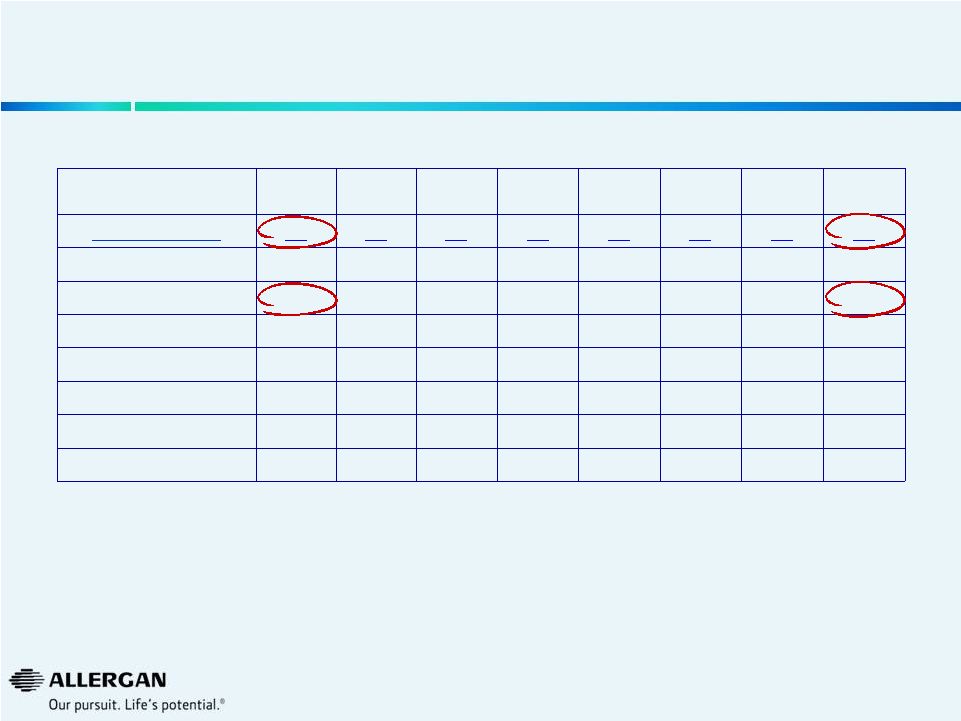

U.S.

Phaco Machine Installed Base Trends Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

Market (000s)

11.5

11.7

11.7

10.3

10.2

10.2

10.6

9.7

Alcon

8.3

8.6

8.7

7.6

7.4

7.2

7.3

6.6

AMO

2.0

1.8

1.8

1.6

1.8

2.0

2.1

1.9

Valeant

1.2

1.3

1.1

1.0

1.0

1.0

1.2

1.3

Others

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

Valeant Growth

-13%

-7%

-25%

-19%

-21%

-17%

7%

21%

Valeant Share

10.8%

10.7%

9.8%

10.0%

9.7%

10.2%

11.5%

12.9%

Source: Market Scope LLC Quarterly Cataract Report

25 |

U.S.

Viscoelastic Procedure Trends Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

Market (000s)

1,156

1,236

1,118

1,182

1,136

1,229

1,065

1,069

Alcon

800

787

712

792

783

845

718

740

AMO

180

220

192

217

210

233

207

174

Valeant

156

194

173

160

123

128

119

121

Others

20

36

41

13

21

22

21

34

Valeant Growth

2%

27%

7%

-4%

-22%

-34%

-31%

-24%

Valeant Share

13.5%

15.7%

15.5%

13.5%

10.8%

10.5%

11.2%

11.3%

Source: Market Scope LLC Quarterly Cataract Report

26 |

U.S.

Refractive Laser Procedure Trends Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

Market (000s)

141

141

158

157

137

139

159

155

AMO

80

81

91

85

76

77

87

83

Alcon

55

53

61

64

58

58

68

60

Valeant

5

6

6

6

2

2

1

5

others

1

1

1

1

1

1

3

7

Valeant Growth

2%

79%

39%

47%

-57%

-62%

-86%

-19%

Valeant Share

3.2%

4.3%

3.8%

4.0%

1.4%

1.7%

0.5%

3.2%

Source: Market Scope LLC Quarterly Cataract Report

27 |

U.S.

Refractive Keratome Procedure Trends Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

Market (000s)

117

120

145

130

119

122

130

126

AMO

63

65

78

68

62

60

70

68

Alcon

15

13

14

13

19

24

11

13

Valeant

6

10

15

15

9

11

11

12

others

32

32

39

34

28

28

38

34

Valeant Growth

-29%

5%

68%

130%

39%

6%

-21%

-20%

Valeant Share

5.4%

8.2%

10.1%

11.2%

7.4%

8.7%

8.8%

9.2%

Source: Market Scope LLC Quarterly Cataract Report

28 |

U.S.

Vitrectomy Machine Procedure Trends Q3-12

Q4-12

Q1-13

Q2-13

Q3-13

Q4-13

Q1-14

Q2-14

Market (000s)

80

83

82

78

81

80

73

84

Alcon

63

64

61

60

61

61

57

62

Valeant

13

17

14

12

14

13

12

14

others

4

2

7

7

7

6

4

7

Valeant Growth

63%

59%

22%

-3%

7%

-24%

-9%

20%

Valeant Share

16.1%

20.1%

16.6%

14.7%

16.8%

15.8%

16.9%

16.6%

Source: Market Scope LLC Quarterly Cataract Report

29 |

Important Information

Allergan, its directors and certain of its officers and employees are participants

in solicitations of Allergan stockholders. Information regarding the names

of Allergan's directors and executive officers and their respective

interests in Allergan by security holdings or otherwise is set forth in Allergan's

proxy statement for its 2014 annual meeting of stockholders, filed with the

SEC on March 26, 2014, as supplemented by the proxy information filed with

the SEC on April 22, 2014. Additional information can be found in Allergan's Annual

Report on Form 10-K for the year ended December 31, 2013, filed

with

the

SEC

on

February

25,

2014

and

its

Quarterly

Report

on

Form

10-Q

for

the

quarter

ended

June

30,

2014, filed with the SEC on August 5, 2014. To the extent holdings of

Allergan's securities have changed since the amounts printed in the proxy statement

for the 2014 annual meeting of stockholders, such changes have been

reflected on Initial Statements of Beneficial Ownership on Form 3 or

Statements of Change in Ownership on Form 4 filed with the SEC. These documents are

available free of charge at the

SEC’s

website

at

www.sec.gov.

STOCKHOLDERS

ARE

ENCOURAGED

TO

READ

ANY

ALLERGAN

PROXY

STATEMENT

(INCLUDING

ANY

SUPPLEMENTS THERETO) AND ANY OTHER RELEVANT DOCUMENTS THAT ALLERGAN MAY FILE WITH

THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT

INFORMATION. Stockholders will be able to obtain, free of charge, copies of

any proxy statement and any other documents filed by Allergan

with

the

SEC

at

the

SEC's

website

at

www.sec.gov.

In

addition,

copies

will

also

be

available

at

no

charge

at

the

Investors

section

of

Allergan's

website

at

www.allergan.com.

30 |

October 2014

Allergan

An Assessment of Valeant Pharmaceuticals

International, Inc. Performance |