Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - KEYCORP /NEW/ | d803929dex991.htm |

| EX-99.3 - EX-99.3 - KEYCORP /NEW/ | d803929dex993.htm |

| 8-K - FORM 8-K - KEYCORP /NEW/ | d803929d8k.htm |

| KeyCorp

Third Quarter 2014 Earnings Review

October 15, 2014

Beth E. Mooney

Chairman and

Chief Executive Officer

Don Kimble

Chief Financial Officer

Exhibit 99.2 |

| 2

FORWARD-LOOKING STATEMENTS AND ADDITIONAL

INFORMATION DISCLOSURE

This presentation contains forward-looking statements, including statements

about our financial condition, results of operations, asset quality trends,

capital levels and profitability. Forward-looking statements can often be

identified by words such as “outlook,” “goal,”

“objective,”

“plan,”

“expect,”

“anticipate,”

“assume,”

“intend,”

“project,”

“believe,”

or “estimate.”

Forward-looking statements represent management’s current

expectations and forecasts regarding future events. If underlying assumptions prove

to be inaccurate or unknown risks or uncertainties arise, actual results

could vary materially from these projections or expectations. Risks and

uncertainties include but are not limited to: (1) deterioration of commercial real estate market fundamentals; (2) declining asset prices; (3)

adverse changes in credit quality trends; (4) changes in local, regional and

international business, economic or political conditions; (5) the extensive

and increasing regulation of the U.S. financial services industry; (6) increasing

capital and liquidity standards under applicable regulatory rules; (7)

unanticipated changes in our liquidity position, including but not limited to,

changes in the cost of liquidity, our ability to enter the financial markets and

to secure alternative funding sources; (8) our ability to receive dividends from

our subsidiary, KeyBank; (9) downgrades in our credit ratings or those of

KeyBank; (10) operational or risk management failures by us or critical third-parties; (11) breaches of security or failures of our technology

systems

due to technological or other factors and cybersecurity threats;

(12) adverse judicial proceedings; (13) the occurrence of natural or man-made

disasters or conflicts or terrorist attacks; (14) a reversal of the U.S.

economic recovery due to economic, political or other shocks; (15) our ability to

anticipate interest rate changes and manage interest rate risk; (16) deterioration

of economic conditions in the geographic regions where we operate; (17) the

soundness of other financial institutions; (18) our ability to attract and retain talented executives and employees, to

effectively sell additional

products or services to new or existing customers, and to manage

our reputational risks; (19) our ability to timely and effectively implement our

strategic initiatives; (20) increased competitive pressure due to industry

consolidation; (21) unanticipated adverse effects of acquisitions and

dispositions of assets or businesses; and (22) our ability to develop and

effectively use the quantitative models we rely upon in our business planning.

We provide greater detail regarding these factors in our 2013 Form 10-K and

subsequent filings, which are available online at www.key.com/ir and

www.sec.gov. Forward-looking statements speak only as of the date they are made

and Key does not undertake any obligation to update the forward- looking

statements to reflect new information or future events. This presentation

also includes certain Non-GAAP financial measures related to “tangible common equity,”

“Tier 1 common equity,”

“pre-provision net

revenue,”

and “cash efficiency ratio.”

Management believes these ratios may assist investors, analysts

and regulators in analyzing Key’s financials.

Although Key has procedures in place to ensure that these measures are calculated

using the appropriate GAAP or regulatory components, they have limitations

as analytical tools and should not be considered in isolation, or as a substitute for analysis of results under

GAAP. For more

information on these calculations and to view the reconciliations to the most

comparable GAAP measures, please refer to the Appendix to this presentation

and to page 99 of our 2013 Form 10-K. |

3

Core revenue trends stable

-

Lower gains from principal investing and leveraged lease terminations

Total average loans up 5% from prior year

-

Linked quarter average impacted by seasonality, capital markets and strategic

exits Positive trends in several fee-based businesses

Expenses well-controlled

-

Down from prior year and previous quarter (excl. Pacific Crest and pension

charges) Asset quality remains strong, with NCOs below targeted range

NPAs down 28% from prior year

New business originations are higher quality than overall book

Remaining disciplined with structure and relationship focus

Strong Risk

Management

Committed to capital priorities: organic growth, dividends, repurchases,

opportunistic growth

Continuing to invest in and grow our businesses

-

Completed acquisition of Pacific Crest Securities, within 60 days of

announcement Repurchased $119 million in common shares in 3Q14

Positive

Operating

Leverage

Investor Highlights –

3Q14

Disciplined

Capital

Management |

4

Financial Review |

5

Financial Highlights

TE = Taxable equivalent, EOP = End of Period

(a)

From continuing operations

(b)

Year-over-year average balance growth

(c)

From consolidated operations

(d)

9-30-14 ratios are estimated

(e)

Non-GAAP measure: see Appendix for reconciliation

EPS –

assuming dilution

$ .23

$ .27

$ .26

$ .26

$ .25

Cash efficiency ratio

(e)

69.5

%

65.8

%

64.9

%

67.4

%

67.5

%

excl. efficiency and pension charges

66.0

63.4

63.9

65.1

63.6

Net interest margin (TE)

2.96

2.98

3.00

3.01

3.11

Return on average total assets

.92

1.14

1.13

1.08

1.12

Total loans and leases

5

%

6

%

4

%

3

%

5

%

CF&A loans

11

13

9

8

11

Deposits (excl. foreign deposits)

4

2

4

8

5

Tier 1 common equity

(d), (e)

11.3

%

11.3

%

11.3

%

11.2

%

11.2

%

Tier 1 risk-based capital

(d)

12.0

12.0

12.0

12.0

11.9

Tangible common equity to tangible assets

(e)

10.3

10.2

10.1

9.8

9.9

NCOs to average loans

.22

%

.22

%

.15

%

.27

%

.28

%

NPLs to EOP portfolio loans

.71

.71

.81

.93

1.01

Allowance for loan losses to EOP loans

1.43

1.46

1.50

1.56

1.62

Balance

Sheet

Growth

(a),

(b)

Capital

(c)

Asset

Quality

(a)

Financial

Performance

(a) |

6

Average total loans up 5% from prior year, driven

by CF&A up 11%

Linked quarter average balances impacted by

seasonality, capital markets and strategic exits

Total commitments continue to grow with

utilization relatively stable

High quality new loan originations: consistent with

moderate risk profile

Loan Growth

$ in billions

Highlights

Average Commercial, Financial & Agricultural Loans

Average Loans

Exit Portfolios

Home Equity & Other

Total Commercial

$ in billions

$55.8

$53.3 |

7

Improving Deposit Mix

Highlights

Funding Cost

Funding cost continues to improve

Transaction deposit balances up 6% from 3Q13

Growth from prior year reflects inflows from

commercial clients as well as commercial

mortgage servicing

Total CD maturities and average cost

–

2014 Q4: $1.5 billion at .46%

–

2015: $2.3 billion at .73%

–

2016 and beyond: $2.1 billion at 1.47%

Average

Deposits

(a)

$ in billions

Note: Transaction deposits include noninterest-bearing, as well as NOW and

MMDA (a)

Excludes deposits in foreign office

Cost of total deposits

(a)

Interest-bearing liability cost

CDs and other time deposits

Savings

Noninterest-bearing

NOW and MMDA

$67.7

$65.4 |

8

Net Interest Income and Margin

TE = Taxable equivalent

Highlights

Net Interest Income & Net Interest Margin Trend (TE)

Net interest income down 1% from prior year,

primarily due to lower asset yields

Modest growth from prior quarter reflects asset

growth, higher loan fees, improved funding cost

and more days in the quarter, which all offset lower

asset yields

Maintaining moderate asset sensitive position

–

Naturally asset sensitive balance sheet flows:

approximately 70% of loans variable rate

–

High quality investment portfolio with average

life of 3.6 years

–

Flexibility to quickly adjust interest rate risk

position

NIM Change (bps):

vs. 2Q14

Earnings asset mix / higher levels of liquidity

(.02)

Loan yield

(.02)

CD maturities / repricing

.02

Total Change

(.02)

Net interest income (TE)

NIM (TE)

$ in millions; continuing operations |

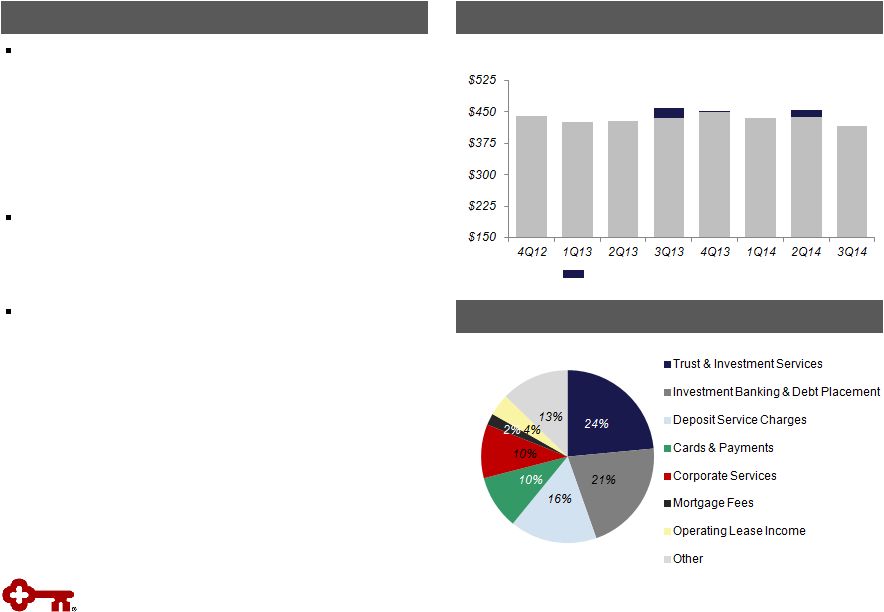

9

Noninterest Income

TE = Taxable equivalent

Highlights

Noninterest Income

Noninterest income down $42 MM from prior year:

–

Gains from leveraged lease termination and

principal investing $31 MM higher in 3Q13

–

Special servicing fees $6 MM lower

–

Posting order change in 4Q13 reduced service

charges by ~$5 MM vs. one year ago

Positive trends in several fee-based businesses

–

Trust and investment services and deposit

service charges up vs. 2Q14

Change from prior quarter (down $38 MM) reflects:

–

Gains from leveraged lease termination and

principal investing $35 MM higher in 2Q14

3Q14 Noninterest Income Diversity

$ in millions; continuing operations

(a)

Other includes corporate-owned life insurance, principal investing, etc.

Leveraged lease termination gains

$417

$459

(a) |

10

Focused Expense Management

Noninterest Expense

$ in millions

Highlights

3Q14 Expense Detail

Expenses down 2% from prior year, benefitting

from continuous improvement efforts

Increase from prior quarter reflects:

–

Pension settlement charge and expenses

related to Pacific Crest Securities

FY 2014 expenses expected to be down a low-to-

mid single digit percentage from 2013

Focused on improving efficiency by growing

revenue and continuing to control expenses

Efficiency charges:

Pension charges:

$15

$37

$16

$22

$10

$ 2

$25

$24

$ in millions

$704

Efficiency charges $

15 All remaining expense 663

$ 678

2H14 expense guidance:

$680 -

$690 / quarter

$15

$20

Pension settlement

Efficiency charges

All remaining expense

Pacific Crest

$716

$689

Not included in guidance:

Pacific

Crest $ 6

Pension

settlement 20

$ 26

(a)

Non-GAAP measure: see Appendix for reconciliation

(b)

Excludes one-time gains of $54 million related to the

redemption of trust preferred securities

Cash Efficiency Ratio

(a)

Efficiency and pension charges, as a

% of revenue:

1.5%

1.5%

3.6%

3.9%

2.3%

1.0%

Cash efficiency ratio,

excluding efficiency

and pension charges

2.3%

3.5%

(b)

.8%

$704

$716 |

11

Efficiency Ratio: Driving to 60% and Below

Business plans and macroeconomic environment provide path to an

efficiency ratio below 60%

Cash

Efficiency

Ratio

(a)

Outlook

(a)

Non-GAAP measure: see Appendix for reconciliation

(b)

Assumes implied forward curve

2-3 year outlook: 60%

Long-term, committed to moving below 60%

(b) |

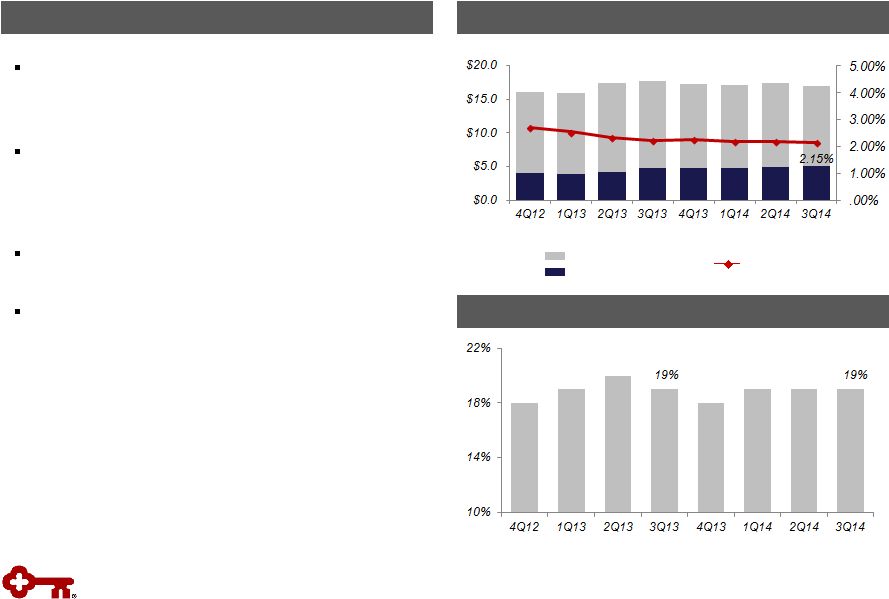

12

Nonperforming Assets

Net Charge-offs & Provision for Loan and Lease Losses

NPLs

NPLs to period-end loans

NCOs

Provision for loan and

lease losses

NCOs to average loans

$ in millions

$ in millions

NPLs held for sale,

OREO & other NPAs

Continued Improvement in Asset Quality

Highlights

Net loan charge-offs decreased 16% from 3Q13 to

$31 MM, or 22 bps of average loans

Total gross charge-offs down 37% from 3Q13 and

down 13% from 2Q14

Nonperforming assets down 28% from prior year

Net charge-offs expected to continue below the

targeted range for the remainder of the year

Allowance for Loan and Lease Losses

Allowance for loan and

lease losses to NPLs

Allowance for loan

and lease losses

$ in millions

$579

$418 |

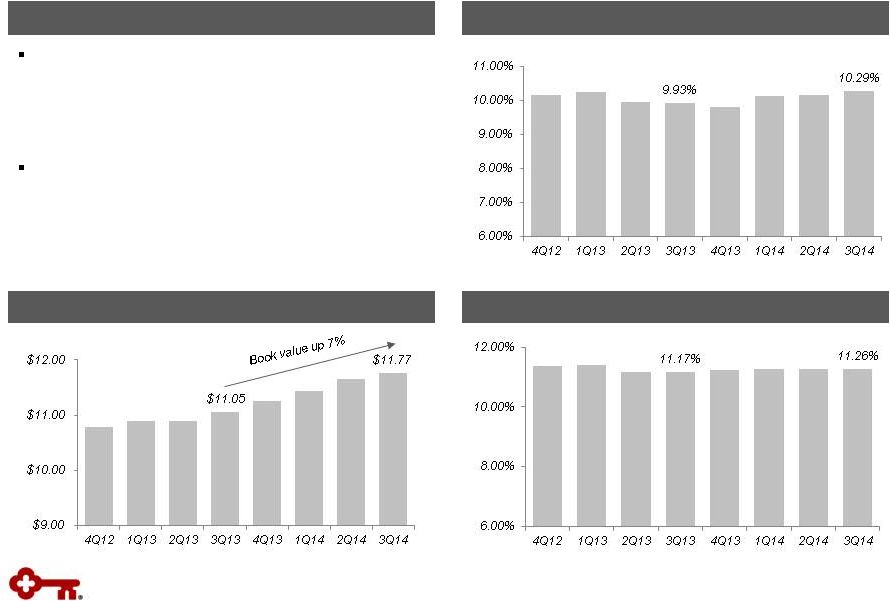

13

Disciplined capital management

–

Continuing to invest in and grow

businesses

–

Repurchased $119 MM in common shares

Ratios reflect the acquisition of Pacific Crest

Securities and the sale of residual interests in

education loan securitization trusts

Tangible Common Equity to Tangible Assets

(a)

Strong Capital

Highlights

Book Value per Share

(a)

Non-GAAP measure: see Appendix for reconciliations

(b)

9-30-14 ratio is estimated

Tier 1 Common Equity

(a), (b) |

2014

Outlook and Expectations Average Loans

•

LQA: mid-single digit growth, driven by

commercial loans

•

Mid-single digit growth vs. FY 2013

Net Interest Income

•

Relatively stable with 3Q14

•

Relatively stable from 2013, with slight

downward pressure from competitive

environment

Noninterest Income

•

Low double-digit percentage growth

from 3Q14, supported by stronger

market-related revenue and a full

quarter of Pacific Crest

•

Low single-digit growth compared to

prior year

Expense

•

Relatively stable with 3Q14 reported,

including Pacific Crest, pension,

seasonality and efficiency charges

•

Low to mid-single digit percentage

decline from 2013

Efficiency / Productivity

•

Positive operating leverage

•

Positive operating leverage

Asset Quality

•

Continued strong credit quality trends,

consistent with 3Q14 levels

•

Net charge-offs to average loans below

targeted

range

of

40

–

60

bps

Capital

•

Continued execution of capital plan

•

Disciplined execution of 2014 capital

plan, including dividends and share

repurchases

14

Guidance

ranges:

relatively

stable:

+/-

2%;

low

single-digit:

<5%;

mid-single

digit:

4%

-

6%;

low

double-digit:

10%

-

13%

4Q14

FY 2014 |

15

Appendix |

Progress on Targets for Success

(a)

Continuing operations, unless otherwise noted

(b)

Represents period-end consolidated total loans and loans held for sale

(excluding education loans in the securitization trusts for periods prior to third quarter

of 2014) divided by period-end consolidated total deposits (excluding

deposits in foreign office) (c)

Excludes intangible asset amortization; non-GAAP measure: see Appendix for

reconciliation 16

Balance Sheet

Efficiency

Moderate Risk

Profile

High Quality,

Diverse

Revenue Streams

Positive

Operating

Leverage

Disciplined

Capital

Management

Metrics

(a)

3Q14

2Q14

Targets

Loan

to

deposit

ratio

(b)

NCOs to average loans

Provision to average loans

Net interest margin

Noninterest income to total revenue

Cash

efficiency

ratio

(c)

Return on average assets

87%

87%

.22%

.22%

69.5%

65.8%

.92%

1.14%

.15%

.07%

2.96%

2.98%

42%

44%

90% -100%

40 -

60 bps

LT: >3.50%

LT: <60%

1.00% -1.25%

>40% |

•

Supporting businesses with

technology development

•

Driving talent management to

improve productivity

Focused on Driving Positive Operating Leverage

Revenue Growth

Expense Savings

Community

Bank

Corporate

Bank

•

Improving sales productivity

•

Strengthening product offering:

Hassle-Free

•

Enhancing online and mobile

channels

•

Optimizing branch channel

•

Driving greater efficiencies through

back and middle-office processes

Enterprise

•

Adding senior bankers:

existing

industry expertise and relationships

•

Strengthening commercial payment

product capabilities

•

Added technology vertical:

completed

Pacific Crest acquisition

•

Exiting international leasing

originations and reducing related cost

structure

•

Variablizing

cost:

utilization

of

third-

party partners

•

Rationalization of fixed income trading

platform

•

Improving operational effectiveness:

Lean Six Sigma, variablizing costs

•

Reducing occupancy costs

•

Right-sizing support activities

17

Executing action plans across our organization

Driving consumer sales

per

FTE

per

day:

up

>30% from prior year

Aggressive campaign to

add

bankers:

relationship

managers up ~15% from

prior year

(a)

Data as of 3Q14 unless otherwise noted

(a)

Includes impact of the acquisition of Pacific Crest Securities

Reducing occupancy:

plans to remove >15% of

corporate square footage

by 2016 |

Focused

Expense Management $2.82 B

$117 MM

$2.70 B

Low to mid-

single digit

decline year-

over-year

Continued cost savings enable investments and offset normal expense growth

(4) % –

(6) %

1 % –

2.5 %

1 % -

2%

(a)

(a)

Operating cost increase includes inflationary adjustments, annual merit increases,

etc. 2 % –

2.5 %

18

Note: Percentage ranges based upon 2014 expense plans and calculated from 2013

reported NIE |

19

Average Total Investment Securities

Highlights

Average AFS securities

$ in billions

High Quality Investment Portfolio

Portfolio composed primarily of GNMA and GSE-

backed MBS and CMOs

–

No private label MBS or financial paper

Currently reinvesting cash flows into GNMA

securities in preparation for upcoming

regulatory liquidity requirements

–

35% of total portfolio was GNMA at 9/30/14

Securities cash flows of $.9 billion in both 3Q14

and 2Q14

Average portfolio life at 9/30/14 of 3.6 years,

unchanged from 6/30/14

Securities to Total Assets

(b)

(a) Yield is calculated on the basis of amortized cost

(b) Includes end of period held-to-maturity and

available-for-sale securities Average yield

(a)

Average HTM securities

$17.7

2.23%

$17.0 |

Interest Rate Risk Management

Naturally Asset Sensitive Balance Sheet

Actively Managing Rate Risk

•

High quality

•

Fixed rate agency MBS and CMOs

•

Average maturity: 3.6 years

•

GNMAs total 35% of total portfolio

•

Reinvesting cash flows into GNMAs

$9

$15

$5

$5

Size of swap

portfolio

Modeled asset

sensitivity

~3%

0%

7%

$5

Flexibility to Adjust Rate

Sensitivity with Swaps

Loan Portfolio

Variable:

69%

Fixed:

31%

Deposits

Flexibility to adjust rate sensitivity for changes in balance

sheet growth/mix as well as interest rate outlook

Debt

hedges

A/LM

hedges

Investment Portfolio

Noninterest-

bearing: 37%

Interest-

bearing, non-

time: 54%

CDs:

9%

•

Maintaining

moderate

asset

sensitive

position

of

~3%

(a)

-

Assumes 200 basis point increase in short-term rates over a

12-month period

•

Utilize swaps for debt hedging and asset liability management

-

Fairly even pace of A/LM swap maturities

3Q14

Swaps

($ in B)

9/30/14

Notional Amt.

Wtd. Avg.

Maturity (Yrs.)

Receive

Rate

Pay

Rate

A/L Management

$ 9.3

1.8

.8%

.2%

Debt

4.5

4.0

2.5

.2

$ 13.8

1.3%

.2%

3Q14

$17 B

AFS: $12 B

HTM: $5 B

Balance sheet has relatively short duration and is

more impacted by the short-end of the curve

$14 B

20

Actively managing a naturally asset sensitive balance sheet

(a) Preliminary estimate |

21

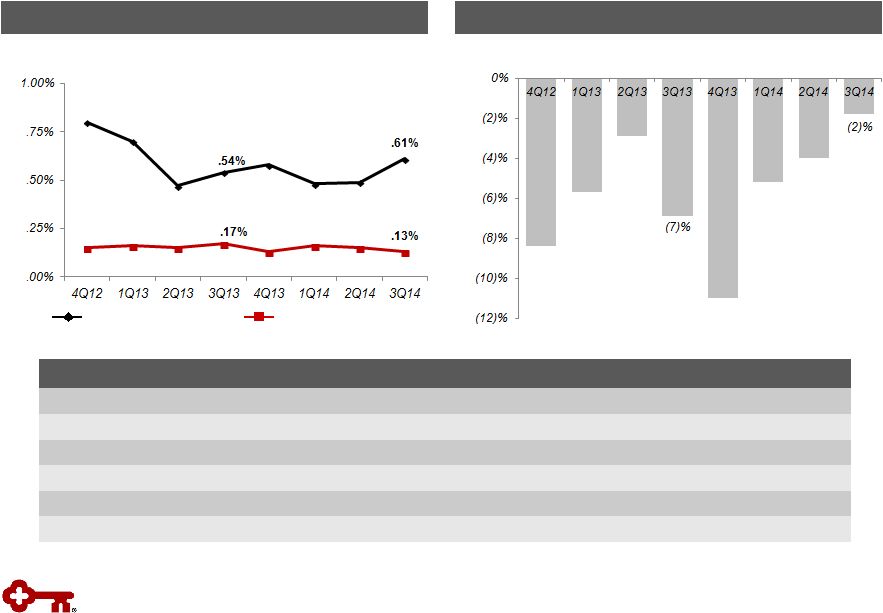

Asset Quality Trends

Quarterly

Change

in

Criticized

Outstandings

(a)

Delinquencies to Period-end Total Loans

(a)

Loan and lease outstandings

(b)

From continuing operations

30 –

89 days delinquent

90+ days delinquent

Metric

(b)

3Q14

2Q14

1Q14

4Q13

3Q13

Delinquencies to EOP total loans: 30-89 days

.61

%

.49

%

.48

%

.58

%

.54

%

Delinquencies to EOP total loans: 90+ days

.13

.15

.16

.13

.17

NPLs to EOP portfolio loans

.71

.71

.81

.93

1.01

NPAs to EOP portfolio loans + OREO + Other NPAs

.74

.74

.85

.97

1.08

Allowance for loan losses to period-end loans

1.43

1.46

1.50

1.56

1.62

Allowance for loan losses to NPLs

200.5

205.6

185.7

166.9

160.4

Continuing operations

Continuing operations |

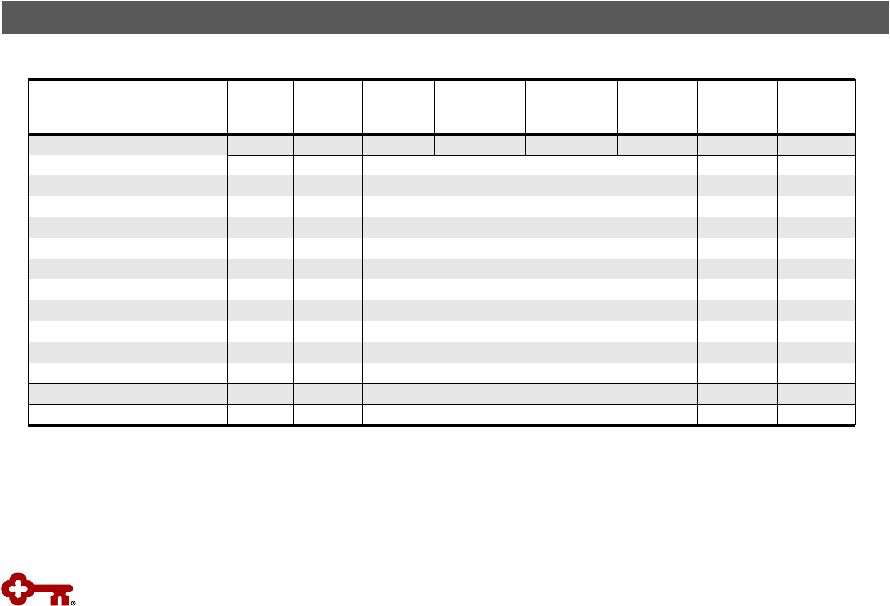

Period-

end loans

Average

loans

Net loan

charge-offs

Net loan

charge-offs

(b)

/

average loans

(%)

Nonperforming

loans

(c)

Ending

allowance

(d)

Allowance /

period-end

loans

(d)

(%)

Allowance /

NPLs

(%)

9/30/14

3Q14

3Q14

3Q14

9/30/14

9/30/14

9/30/14

9/30/14

Commercial,

financial

and

agricultural

(a)

$ 26,683

$ 26,456

$

6 .09

$

47

$ 385

1.44

819.15

Commercial real estate:

Commercial Mortgage

8,276

8,142

(2)

(.10)

41

159

1.92

387.80

Construction

1,036

1,030

1

.39

14

28

2.70

200.00

Commercial lease financing

4,135

4,145

(1)

(.10)

14

55

1.33

392.86

Real estate –

residential mortgage

2,213

2,204

2

.36

81

22

.99

27.16

Home equity

10,663

10,658

7

.26

184

78

.73

42.39

Credit cards

724

716

9

4.99

1

32

4.42

N/M

Consumer other –

Key Community Bank

1,546

1,534

6

1.55

2

24

1.55

N/M

Consumer other –

Exit Portfolio

879

911

3

1.31

17

21

2.39

123.53

Continuing

total

(e)

$ 56,155

$ 55,796

$ 31

.22

$

401

$ 804

1.43

200.50

Discontinued operations

2,375

4,080

7

1.15

9

31

1.31

344.44

Consolidated total

$ 58,530

$ 59,876

$ 38

.26

$

410

$ 836

1.43

203.90

Credit Quality by Portfolio

Credit Quality

$ in millions

22

(a)

9-30-14

ending

loan

balances

include

$90

million

of

commercial

credit

card

balances;

9-30-14

average

loan

balances

include

$92

million

of

assets

from commercial credit cards

(b)

Net loan charge-off amounts are annualized in calculation

(c)

9-30-14 NPL amount excludes $14 million of purchased credit impaired

loans (d)

9-30-14 allowance by portfolio is estimated

(e)

9-30-14 ending loan balances include purchased loans of $143

million, of which $14 million were purchased credit impaired

N/M = Not meaningful |

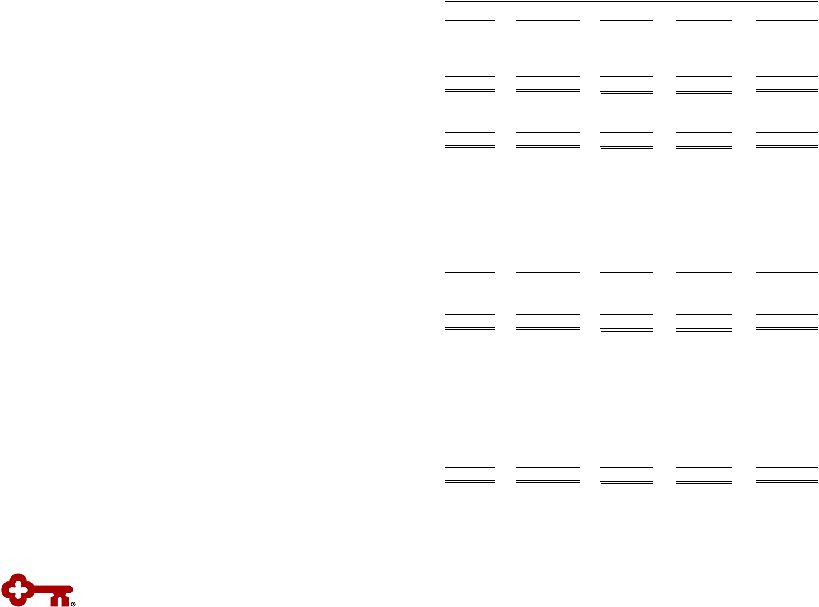

Vintage (% of Loans)

Loan

Balances

Average

Loan

Size ($)

Average

FICO

Average

LTV

(a)

% of

Loans

LTV>90%

2012 and

later

2011

2010

2009

2008 and

prior

Loans and lines

First lien

$

6,180 $ 65,817

772

67

%

.6

%

50

%

5%

3%

3%

39

%

Second lien

4,200

54,759

766

76

3.7

33

5

3

4

55

Community Bank

$ 10,380

60,443

770

70

1.8

43

5

3

4

45

Exit portfolio

283

17,253

729

80

31.6

1

-

-

-

99

Total home equity portfolio

$ 10,663

Nonaccrual loans and lines

First lien

$

94 $

61,645 720

73

%

1.0%

5

%

4%

3%

5%

83

%

Second lien

81

48,222

711

80

2.1

2

2

2

4

90

Community Bank

$

175 54,590

716

77

1.5

4

3

2

5

86

Exit portfolio

10

23,844

700

77

29.2

-

-

-

-

100

Total home equity nonaccruals

$

185 Third quarter net charge-offs (NCOs)

Community Bank

$

6 3

%

2%

4%

2%

89

%

% of average loans

.23

%

Exit Portfolio

$

1 -

-

-

-

100

% of average loans

1.37

%

(a) Average LTVs are at origination. Current average LTVs for Community Bank total

home equity loans and lines is approximately 71%, which compares to 71% at

the end of the second quarter of 2014. Home Equity Portfolio –

9/30/14

$ in millions, except average loan size

Home Equity Portfolio

Highlights

High quality portfolio

Community bank loans and lines: 97% of total portfolio; branch-

originated

–

60% first lien position

–

Average FICO score of 770

–

Average LTV at origination: 70%

$4.0 billion of the total portfolio are fixed rate loans that require

principal and interest payments; $6.7 billion are lines

$1.5 billion in lines outstanding (14% of the total portfolio)

come to end of draw period in the next four years

–

Proactive communication and client outreach initiated

near end of draw period

23 |

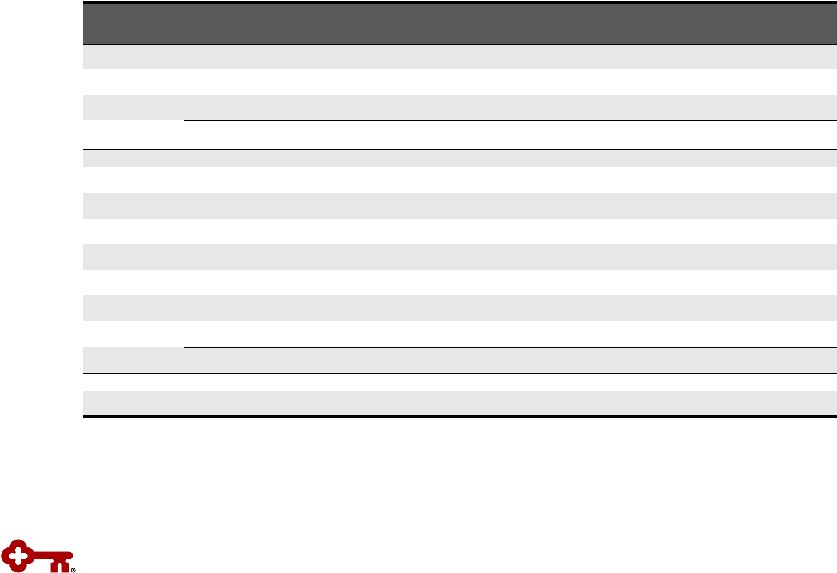

Balance Outstanding

Change

Net Loan Charge-offs

Balance on

Nonperforming Status

9-30-14

6-30-14

9-30-14

vs.

6-30-14

3Q14

(c)

2Q14

(c)

9-30-14

6-30-14

Residential properties –

homebuilder

$ 11

$ 19

$ (8)

$ 1

-

$

10 $ 7

Marine and RV floor plan

7

23

(16)

-

-

5

6

Commercial

lease

financing

(a)

1,046

1,154

(108)

(1)

$ (5)

1

3

Total commercial loans

1,064

1,196

(132)

-

(5)

16

16

Home equity –

Other

283

300

(17)

1

1

10

11

Marine

828

888

(60)

2

5

16

15

RV and other consumer

57

61

(4)

1

(1)

1

1

Total consumer loans

1,168

1,249

(81)

4

$ 5

27

27

Total exit loans in loan portfolio

$ 2,232

$ 2,445

$ (213)

$ 4

-

$ 43

$ 43

Discontinued operations –

education lending

business (not included in exit loans above)

(b)

$ 2,375

$ 4,162

$ (1,787)

$ 7

$ 7

$ 9

$ 19

$ in millions; average balances

(a)

Includes (1) the business aviation, commercial vehicle, office products,

construction and industrial leases; (2) Canadian lease financing portfolios;

(3) European lease financing portfolios; and (4) all remaining balances related to

lease in, lease out; sale in, lease out; service contract leases; and

qualified technological equipment leases.

(b)

June 30, 2014 balance includes loans in Key’s consolidated education loan

securitization trusts (c)

Credit amounts indicate recoveries exceeded charge-offs

$ in millions

Exit Loan Portfolio

Exit Loan Portfolio

24 |

Three months ended

9-30-14

6-30-14

3-31-14

12-31-13

9-30-13

Tangible common equity to tangible assets at period end

Key shareholders’

equity (GAAP)

$

10,509

$

10,504

$

10,403

$

10,303

$

10,206

Less:

Intangible assets

(a)

1,105

1,008

1,012

1,014

1,017

Preferred Stock, Series A

(b)

282

282

282

282

282

Tangible common equity (non-GAAP)

$

9,122

$

9,214

$

9,109

$

9,007

$

8,907

Total assets (GAAP)

$

89,770

$

91,798

$

90,802

$

92,934

$

90,708

Less:

Intangible assets

(a)

1,105

1,008

1,012

1,014

1,017

Tangible assets (non-GAAP)

$

88,665

$

90,790

$

89,790

$

91,920

$

89,691

Tangible common equity to tangible assets ratio (non-GAAP)

10.29

%

10.15

%

10.14

%

9.80

%

9.93

%

Tier 1 common equity at period end

Key shareholders’

equity (GAAP)

$

10,509

$

10,504

$

10,403

$

10,303

$

10,206

Qualifying capital securities

340

339

339

339

340

Less:

Goodwill

1,051

979

979

979

979

Accumulated

other

comprehensive

income

(loss)

(c)

(366)

(328)

(367)

(394)

(409)

Other assets

(d)

110

86

84

89

96

Total Tier 1 capital (regulatory)

10,054

10,106

10,046

9,968

9,880

Less:

Qualifying capital securities

340

339

339

339

340

Preferred Stock, Series A

(b)

282

282

282

282

282

Total Tier 1 common equity (non-GAAP)

$

9,432

$

9,485

$

9,425

$

9,347

$

9,258

Net risk-weighted assets (regulatory)

(e)

$

83,787

$

84,287

$

83,637

$

83,328

$

82,913

Tier 1 common equity ratio (non-GAAP)

(e)

11.26

%

11.25

%

11.27

%

11.22

%

11.17

%

Pre-provision net revenue

Net interest income (GAAP)

$

575

$

573

$

563

$

583

$

578

Plus:

Taxable-equivalent adjustment

6

6

6

6

6

Noninterest income (GAAP)

417

455

435

453

459

Less:

Noninterest expense (GAAP)

704

689

662

712

716

Pre-provision net revenue from continuing operations (non-GAAP)

$

294

$

345

$

342

$

330

$

327

GAAP to Non-GAAP Reconciliation

$ in millions

25

a)

Three months ended September 30, 2014, June 30, 2014, March 31, 2014, December 31,

2013, and September 30, 2013 exclude $72 million, $79 million, $84 million,

$92 million, and $99 million of period-end purchased credit card receivable intangible assets, respectively

b)

Net of capital surplus

c)

Includes net unrealized gains or losses on securities available for sale (except

for net unrealized losses on marketable equity securities), net gains or losses on cash

flow hedges, and amounts resulting from the application of the applicable

accounting guidance for defined benefit and other postretirement plans

d)

Other assets deducted from Tier 1 capital and net risk-weighted assets consist

of disallowed intangible assets (excluding goodwill) and deductible portions of

nonfinancial equity investments. There were no disallowed deferred tax

assets at September 30, 2014, June 30, 2014, March 31, 2014, December 31, 2013, and

September 30, 2013

e)

9-30-14 amount is estimated |

Three months ended

9-30-14

6-30-14

3-31-14

12-31-13

9-30-13

Average tangible common equity

Average

Key

shareholders’

equity

(GAAP)

$

10,473

$

10,459

$

10,371

$

10,272

$

10,237

Less:

Intangible assets (average)

(a)

1,037

1,010

1,013

1,016

1,019

Preferred Stock, Series A (average)

291

291

291

291

291

Average tangible common equity (non-GAAP)

$

9,145

$

9,158

$

9,067

$

8,965

$

8,927

Return on average tangible common equity from continuing operations

Net

income

(loss)

from

continuing

operations

attributable

to

Key

common

shareholders (GAAP)

$

197

$

242

$

232

$

229

$

229

Average tangible common equity (non-GAAP)

9,145

9,158

9,067

8,965

8,927

Return on average tangible common equity from continuing operations

(non-GAAP) 8.55

%

10.60

%

10.38

%

10.13

%

10.18

%

Return on average tangible common equity consolidated

Net income (loss) attributable to Key common shareholders (GAAP)

$

204

$

214

$

236

$

224

$

266

Average tangible common equity (non-GAAP)

9,145

9,158

9,067

8,965

8,927

Return on average tangible common equity consolidated (non-GAAP)

8.85

%

9.37

%

10.56

%

9.91

%

11.82

%

Cash efficiency ratio

Noninterest expense (GAAP)

$

704

$

689

$

662

$

712

$

716

Less:

Intangible asset amortization (GAAP)

10

9

10

10

12

Adjusted noninterest expense (non-GAAP)

$

694

$

680

$

652

$

702

$

704

Net interest income (GAAP)

$

575

$

573

$

563

$

583

$

578

Plus:

Taxable-equivalent adjustment

6

6

6

6

6

Noninterest income (GAAP)

417

455

435

453

459

Total taxable-equivalent revenue (non-GAAP)

$

998

$

1,034

$

1,004

$

1,042

$

1,043

Cash efficiency ratio (non-GAAP)

69.5

%

65.8

%

64.9

%

67.4

%

67.5

%

GAAP to Non-GAAP Reconciliation

(continued)

$ in millions

(a)

Three months ended September 30, 2014, June 30, 2014, March 31, 2014, December 31,

2013, and September 30, 2013 exclude $76 million, $82 million, $89 million,

$96 million, and $103 million of average purchased credit card receivable intangible assets, respectively

26 |

KeyCorp & Subsidiaries

$ in billions

Quarter ended

September 30, 2014

Tier 1 common equity under current regulatory rules

$

9.4 Adjustments from current regulatory rules

to the Regulatory Capital Rules: Deferred tax assets and PCCRs

(b)

(.1)

Common

equity

Tier

1

anticipated

under

the

Regulatory

Capital

Rules

(c)

$

9.3 Total risk-weighted assets under

current regulatory rules

$

83.8 Adjustments from current regulatory rules to the

Regulatory Capital Rules: Loan commitments <1 year

1.0

Past Due Loans

.1

Mortgage servicing assets

(d)

.5

Deferred tax assets

(d)

.3

Other

1.5

Total risk-weighted assets anticipated under the Regulatory Capital

Rules

$

87.2 Common Equity Tier 1 ratio under the Regulatory Capital

Rules 10.7

%

(a)

Common

equity

Tier

1

capital

is

a

non-generally

accepted

accounting

principle

(GAAP)

financial

measure

that

is

used

by

investors,

analysts

and

bank regulatory agencies to assess the capital position of financial services

companies. Management reviews Common Equity Tier 1 along with other

measures of capital as part of its financial analyses (b)

Includes the deferred tax asset subject to future taxable income

for realization, primarily tax credit carryforwards, as well as

the deductible portion

of purchased credit card receivables

(c)

The

anticipated

amount

of

regulatory

capital

and

risk-weighted

assets

is

based

upon

the

federal

banking

agencies’

Regulatory

Capital

Rules

(as

fully phased-in on January 1, 2019); Key is subject to the Regulatory

Capital Rules under the “standardized approach”

(d)

Item is included in the 10%/15% exceptions bucket calculation and is

risk-weighted at 250% Table may not foot due to rounding

27

Common Equity Tier 1 Under the Regulatory Capital

Rules (estimated)

(a) |