Attached files

| file | filename |

|---|---|

| EX-32.1 - CERTIFICATION - XERIANT, INC. | banj_ex321.htm |

| EX-31.1 - CERTIFICATION - XERIANT, INC. | banj_ex311.htm |

| EXCEL - IDEA: XBRL DOCUMENT - XERIANT, INC. | Financial_Report.xls |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

(Mark One) |

|

|

|

|

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

|

For the fiscal year ended June 30, 2014 |

|

|

|

|

or |

|

|

|

|

|

¨ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

|

|

For the transition period from _____________ to _____________ |

Commission file number 000-54277

|

Banjo & Matilda, Inc. |

|

(Exact name of registrant as specified in its charter). |

|

Nevada |

27-1519178 |

|

|

State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) |

|

|

76 William Street Paddington, NSW 2021 Australia |

||

|

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: 011-61-2-8069-2665

Securities registered under Section 12(b) of the Act:

|

Title of each class: |

Name of each exchange on which registered: |

|

|

None |

None |

Securities registered under Section 12(g) of the Act:

Common Stock, $0.00001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes x No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

¨ |

Accelerated filer |

¨ |

|

Non-accelerated filer |

¨ |

Smaller reporting company |

x |

|

(Do not check if a smaller reporting company) |

|

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting and non-voting common equity of the registrant held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter ended December 31, 2013 was $4,195,628.

As of September 15, 2014, the registrant had outstanding 27,941,684 shares of common stock.

Documents Incorporated by Reference: None.

TABLE OF CONTENTS

|

|

Page | |||||

|

PART I |

||||||

|

|

|

|

||||

|

Item 1. |

Business |

3 |

||||

|

Item 1A. |

Risk Factors |

7 |

||||

|

Item 2. |

Properties |

13 |

||||

|

Item 3. |

Legal Proceedings |

13 |

||||

|

Item 4. |

Mine Safety Disclosures. |

13 |

||||

|

|

|

|||||

|

PART II |

13 |

|||||

|

|

|

|||||

|

Item 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

14 |

||||

|

Item 6. |

Selected Financial Data. |

15 |

||||

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

16 |

||||

|

Item 7A. |

Quantitative and Qualitative Disclosures About Market Risk. |

22 |

||||

|

Item 8. |

Financial Statements and SupplementaryData. |

22 |

||||

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. |

22 |

||||

|

Item 9A. |

Controls and Procedures. |

22 |

||||

|

Item 9B. |

Other Information |

23 |

||||

|

|

|

|||||

|

PART III |

23 |

|||||

|

|

|

|||||

|

Item 10. |

Directors, Executive Officers and Corporate Governance. |

24 |

||||

|

Item 11. |

Executive Compensation |

25 |

||||

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. |

28 |

||||

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

29 |

||||

|

Item 14. |

Principal Accounting Fees and Services. |

30 |

||||

|

|

|

|||||

|

PART IV |

31 |

|||||

|

|

|

|||||

|

Item 15. |

Exhibits, Financial Statement Schedules. |

31 |

||||

|

2

|

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Report”) contains “forward-looking statements” within the meaning of the Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Any statements about our expectations, beliefs, plans, predictions, forecasts, objectives, assumptions, or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipate,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends,” and similar words or phrases. Accordingly, these statements are only predictions and involve estimates, known and unknown risks, assumptions, and uncertainties that could cause actual results to differ materially from those expressed in them. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of several factors more fully described in Item 1A of this Report under the caption “Risk Factors” and elsewhere in this Report, including the exhibits hereto.

All forward-looking statements are necessarily only estimates of future results, and actual results may differ materially from expectations. The inclusion of this forward-looking information should not be regarded as a representation by us or any other person that the future plans, estimates, or expectations contemplated by us will be achieved. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, and financial needs. You are cautioned not to place undue reliance on such statements which should be read in conjunction with the other cautionary statements that are included elsewhere in this Report. Any forward-looking statement speaks only as of the date on which it is made and we undertake no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as may be required under applicable securities laws.

Use of Certain Defined Terms

Except where the context otherwise requires and for the purposes of this Report only:

|

· |

The “Registrant,” “the Company,” “we,” “our,” “us” and similar phrases refer to Banjo & Matilda, Inc., a Nevada corporation (formerly known as Eastern World Solutions, Inc.) which is a reporting company under the Exchange Act. |

|

· |

“Banjo & Matilda” and “B&M” refer to Banjo & Matilda Pty Ltd, a corporation organized under the laws of Australia and a wholly-owned subsidiary of the Registrant. |

|

· |

“Exchange Act” refers to the Securities Exchange Act of 1934, as amended. |

|

· |

“SEC” refers to the Securities and Exchange Commission. |

|

· |

“Securities Act” refers to the Securities Act of 1933, as amended. |

Item 1. Business

Acquisition of Banjo & Matilda Pty Ltd.

On November 14, 2013, the Registrant consummated a Share Exchange Agreement (the “Exchange Agreement”) with Banjo & Matilda Pty Ltd, a corporation organized under the laws of Australia (“Banjo & Matilda”) and the shareholders of Banjo & Matilda (“B&M Shareholders”). Pursuant to the Exchange Agreement, we acquired 100% of the issued and outstanding capital stock of Banjo & Matilda, making it a wholly-owned subsidiary of the Registrant (the “Transaction”). There was no prior relationship between the Company and any of its affiliates and Banjo & Matilda and any of its affiliates.

In consideration for the purchase of 100% of the issued and outstanding capital stock of Banjo & Matilda under the Exchange Agreement, the Registrant issued to the B&M Shareholders an aggregate of 18,505,539 restricted shares of the Registrant’s common stock.

On November 15, 2013, the Registrant entered into an employment agreement with each of the co-founders of Banjo & Matilda: Brendan Macpherson, the Chief Executive Officer of the Registrant, and Belinda Storelli Macpherson, the Chief Creative Officer of the Registrant. Each employment agreement has an initial term of three years and will automatically renew for additional term of three years. Either party may elect not to renew the Employment Agreement for an additional three year term by written notice delivered to the other party no later than August 30th of the final year of the term. In addition, either employee may terminate the employment agreement upon 30 days written notice.

|

3

|

Corporate History

Banjo & Matilda, Inc. was incorporated in Nevada on December 18, 2009 under the name Eastern World Group, Inc. On September 24, 2013, the Registrant changed its name to Banjo & Matilda, Inc.

Prior to the acquisition of Banjo & Matilda Pty Ltd. under the Exchange Agreement, the Registrant was a development stage company without any operating revenues or earnings. Most of the time and resources of then-management was spent organizing the Registrant, obtaining interim financing (including a public offering in December 2010 of a minimum of 1.5 million shares of common stock for $75,000 by former management of the Registrant) and developing a business plan.

Our Operations

As a result of the consummation of the Exchange Agreement, the Company’s operations and financial statements are now those of Banjo & Matilda and the financial statements presented herein for all periods prior to the consummation of the Exchange Agreement are those of Banjo & Matilda.

Overview

Banjo & Matilda Pty Ltd. was incorporated in Australia on May 27, 2009 as a Proprietary Company under the Corporations Act 2001. Banjo & Matilda is a designer, retailer and wholesaler of contemporary luxury knitwear that draws its inspiration from Australian heritage and beach lifestyle. Banjo & Matilda was founded by the wife and husband team of Belinda Storelli Macpherson and Brendan Macpherson in 2008 near Bondi Beach Australia, and launched its first line of knitwear in May 2008. Since then the brand has captured a very strong following amongst its customers, and is now working with key retailers and apparel industry partners to expand the brand and its offerings as a result of this success. Banjo & Matilda sells its products through its own website (www.banjoandmatilda.com) and wholesales to a growing list of key retailers in Australia, New Zealand, Europe, Canada and the United States. Retailers sell Banjo & Matilda’s knitwear both online and in their retail stores.

Banjo & Matilda’s core business has been the design and sale of premium contemporary cashmere knitwear for women; however, it expects to expand its product lines to include broader lifestyle offering including tops, blouses, dresses, skirts, accessories, home, men’s and children’s products. Banjo & Matilda’s current core market is women aged 25-55.

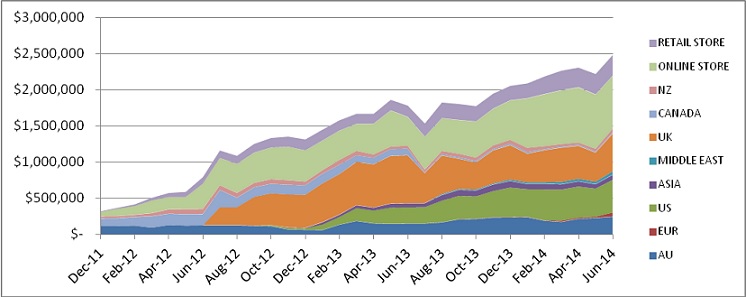

Revenue increased 31% from $1,724,181 in the year ending June 30, 2013 to $2,264,264 in the year ending June 30, 2014. Banjo & Matilda‘s loss from operations for the fiscal year ended June 30, 2014 was $362,377 compared to a profit from operations of $166,058 for the fiscal year ended June 30, 2013. While revenue and gross profit grew in the year ending June 30, 2014 significantly, as expected, the costs of financing and expenses of being public and investing in resources including people, systems, warehousing and selling & marketing to support the current and expected growth of the business increased our costs and reduced our profitability in the 2014 year.

Our Market

Knitwear represents a significant share of the total global apparel sales and more importantly is a staple item in our target customer’s wardrobe. Banjo & Matilda’s target customer group is mainly professional women in the 25 – 55 age bracket, who have a level of disposable income and typically are in double income households. Most of Banjo & Matilda’s sales have been in the 33 – 42 age group (36% of sales) and 43 – 52 age group (28% of sales). Women in the 23 – 32 age group make up approximately 25% of sales. Banjo & Matilda’s target customers exhibit a preference for “premium contemporary” clothing which is typically unique in design and origin, well designed and made, but not as expensive as traditional luxury branded products. The current target customer will occasionally purchase a luxury brand product and sometimes lower priced fast fashion products to add to their wardrobe, but will spend more of their clothing budget on “premium contemporary” products such as Banjo & Matilda. These customers also tend to be loyal to a brand that is aligned with their lifestyle.

Our Products

Banjo & Matilda currently offers a comprehensive line of premium contemporary cashmere knitwear for women. We also have a line of accessories, such as cashmere scarves, slippers, eye-masks and travel blankets. Each year Banjo & Matilda collaborates with a high profile artist or celebrity to create an exclusive limited edition cashmere sweater. In 2013, we collaborated with the singer Bryan Adams and prior collaborations included Australian businesswoman, television host, model and actress Elle Macpherson, controversial British artist Tracey Emin and Australian singer/songwriter, model and actress Natalie Imbrugila, and, most recently Gwyneth Paltrow’s successful lifestyle blog GOOP. The company is planning to expand its product lines to include broader lifestyle offering of tops, blouses, dresses, skirts, accessories, men’s and children’s products.

|

4

|

Product Design

Our product design efforts are led by Chief Creative Officer Belinda Macpherson who leads our design team. The design team identifies trends based on market intelligence and research and proactively seeks inspiration from the company’s Australian heritage and the relaxed beach lifestyle. We seek to combine exclusive cashmere yarn inspired by the “luxe” lifestyle and statement designs. Our designs reflect Ms. Macpherson’s unique aesthetic perspective and her desire to develop an accessible and understated luxury lifestyle brand.

Product Manufacturing

We do not own or operate any manufacturing facilities. We use third party contract manufacturers mostly in China, and have established a dedicated production office and personnel in China during the 2014 fiscal year to more closely manage our manufacturing. All yarns and fabrics are sourced from the most reputable suppliers. The materials used are mostly the highest grade that can be sourced mostly in China and for some products Australia and Italy. On occasion we use different suppliers outside of China. Banjo & Matilda works with a number of manufacturers, however most of our manufacturing was from four primary Chinese manufacturers producing approximately 99% of our products during the year ended June 30, 2014. During fiscal 2014, no single manufacturer produced more than approximately 23.2% of our products. Our manufacturers provide us with the speed to market necessary to respond quickly to changing trends and increased demand. We have developed a solid relationship with our manufacturers and take great care to ensure that they share Banjo & Matilda’s commitment to quality and ethics. We do not, however, have any long-term agreements requiring us to use any manufacturer, and no manufacturer is required to produce our products in the long-term. We regularly secure and test new manufacturing partners and believe that the services of additional, or other, manufacturers and/or suppliers of our fabrics can continue to be obtained with little or no additional expense to us and/or delay in the timeliness of our production process.

Product Distribution

During the fiscal 2014 year we consolidated our distribution activities to a central distribution center “DC” in Hong Kong and eliminated our Australian DC as Australian sales represent a diminishing portion of overall sales. In our HK DC we pay for dedicated staff, space, and pay a small management fee for fulfillment services in which our products are packaged and shipped to customers. Our DC in Hong Kong consolidates all of our products manufactured in China, packages the products by region and customer and then coordinates the shipping of our products. All wholesale orders are currently sent directly to customers from the HK DC, however we are in the process of opening a California USA DC specifically to consolidate USA customer wholesale orders and coordinate logistics and deliveries on the ground in the USA. This will mean all stock for USA orders will be shipped from our HK DC to our USA DC that will then coordinate the delivery to USA customers. All e-commerce online orders are shipped directly from our HK DC globally.

Product Marketing

We market our products in the following key ways:

Online

Banjo & Matilda markets its products online primarily through its website(s) www.banjoandmatilda.com and www.banjoandmatilda.com.au, social media, EDM (email direct mailing) campaigns, paid search engine marketing (SEM), online advertising (some strategic placement of online paid media), affiliate e-commerce and publisher web sites, and online PR (editorial placement in key online related web sites, and engagement with key fashion & lifestyle bloggers). The current largest contributor to growing online sales is the growth of the number of retail outelets at which our products are being offered. As our brand awareness and global customer base expands, it drives additional traffic to our websites and social media channels, driving our sales. The Company has a dedicated e-commerce team which analyzes and optimizes its web site to improve conversion from traffic to sale, average order value, and, driving lifetime value of the customer/repeat purchasing.

Traditional Media & Publicity

We engage publicists to drive editorial placement in fashion and related publications including (but not limited to), fashion and lifestyle magazines, news-papers and television. We have generated a significant amount of press in Australia (in excess of $10MM in editorial value over the past five years), and expect to do the same overtime in the United States and other key markets.

|

5

|

Believing that benevolence is the new luxury, we have developed a unique initiative called “The Sweater Exchange” that supports homeless woman and children (currently in Australia) by encouraging donations of pre-loved sweaters to our charity distribution partners who distribute these to women and children in need. The company works with a key media partners driving people to register with us to donate their pre-loved sweaters to charity, and in turn receive a discount voucher for Banjo & Matilda’s online store. In Australia we are inthe seventh year of this program. In 2014 the initiative donated over 5,000 sweaters to the homeless in Sydney and Melbourne and generated over 3,000 new subscribers to Banjo & Matilda. This has become an important touch point with many of our customers who are now strong supporters of the initiative, and is a program we will expand to other territories over time.

In store

Through our own store(s) all customers are encouraged to joining our mailing list by having their receipt sent to them, and our online store is promoted to them. Customers who purchase our products in our retail partner stores are encouraged through our swing tags to come to us directly. There are 203 retail outlets now stocking Banjo & Matilda at the end of September 2014, an increase of 1085% up from 18 stores as at December 2013.

Growth Strategy

In the next 12 months we expect to raise additional equity and debt to support our growth plans including: growing our product offering, continue to expand our wholesale retail network, grow online e-commerce sales, and continue to upgrade and add new systems and resources to support the growth plan.

Wholesale

There are 203 retail outlets now stocking Banjo & Matilda at the end of September 2014, an increase of 1085% up from 18 stores as at December 2013. The brand and products have established a foothold in the market and, over the next two years, we expect to be stocked in a substantial number of key major and specialty retailers around the world. New key wholesale customers have been secured each season since we began our wholesale program. We recently appointed a respected US / North American sales agency to specifically support growth of our North American sales. We have a dedicated international wholesale sales director and support team who oversee direct sales with our largest customers globally and key independent customers, and have begun to appoint sales agents to help us manage our growing base of independent specialty retailers. We are now stocked in major retailers such as Neiman Marcus, Net-a-porter, ShopBop, Intermix, Piperline, Anthropologie, David Jones, and many more. We are also now growing our key independent customer base that we expect over time will represent approximately 40% of all wholesale sales. Growing our wholesale customer base also drives awareness and brand positioning which supports our retail and online sales channels.

Online

Banjo & Matilda was an early adopter of the online channel. The Company now has 6 years of online sales data to aid in planning and focus investment with a proven correlation between database subscription, online visitation and sales. In addition to a comprehensive brand reach, subscriber acquisition and conversion, program, the core strategy is to bring customers into our “world”, and keep them as lifetime customers. We have a very loyal base of customers that have been acquired over time and frequently purchase every season (4-5 seasons per annum), and often multiple times each season.

Retail

The company operates a flagship retail store in Sydney Australia. It has recently opened a second Melbourne Australia “concept” store. Over time the company will open additional stores opportunistically. Once the company has reached critical mass in its wholesale business (around 400 retail outlets), it will contemplate a more aggressive retail store rollout.

Competition

Competition in the luxury knitwear industry is principally on the basis of brand image and recognition as well as product quality, style, price and distribution. Banjo & Matilda successfully competes on the basis of a premium brand image, unique designs, and attainable price points.

|

6

|

In line with a current trend growth in premium contemporary knitwear, the market is competitive. It includes increasing competition from established companies who are expanding their production and marketing of knitwear products, as well as from frequent new entrants to the market. We are in direct competition with brands such as Zadig & Voltaire, Missoni, Equipment and Vince among others. Some of these companies have substantially greater sales than Banjo & Matilda and have a larger global retail and wholesale presence. However, we believe the following strengths differentiate us from our competitors and are important to our success:

|

· |

Uniquely Designed Knitwear.Our products are fresh, fun and versatile. They offer discreet luxury and a relaxed lifestyle attitude. All designs have strong attention to detail, use high-grade yarns and materials, are well designed and fitting, finished well and are reasonably priced. |

|

· |

Unique Australian Brand Heritage & Lifestyle Brand. The brand reflects the aspirational freedom and freshness of the Australian new luxury beach lifestyle. The brand aims to be unpretentious yet still luxurious capturing and capitalizing on what has been dubbed the “new luxury” mega trend. |

|

|

|

|

|

|

|

An interesting shift in consumerism is subtly demanding a change in the retail industry’s definition of luxury. There was a time when “old luxury” was displayed by ownership of products of stature such as mansions, visible branding, expensive cars and extravagant jewelry. Now, a new class of consumers increasingly shows a preference for individuality and self-expression rather than status symbols. |

|

|

|

|

|

|

|

This “new luxury” encompasses products and services with higher levels of quality and taste than conventional goods in the category, but ones not so expensive as to be out of reach. |

|

|

|

|

|

|

|

Scott Keogh, CMO of Audi America defines the paradigm as follows: “Old Luxury is traditionally grounded in Europe. A Swiss watch, high quality, a traditional definition of prestige. New Luxury is evoking a ‘West Coast’ sensibility a more casual attitude … a sense of Zen and spirit.” |

|

|

|

|

|

|

|

Banjo & Matilda captures this essence in part due to its heritage as an Australian lifestyle luxury brand, but also because of its luxury casual design aesthetic. |

Intellectual Property

In August 2013, we registered our brand name and logo, Banjo & Matilda, with the IP Australia (which is the Australian Government agency that administers intellectual property such as trademarks). We believe we own the material trademarks used in connection with the marketing, distribution and sale of all of our products in Australia, the United States, and Europe (and in the other countries in which our products are currently or intended to be either sold or manufactured). We also own the (i) website URL’s including and associated to banjoandmatilda.com (as well as banjoandmatilda.au, banjoandmatilda.uk, thesweaterexchange.com etc.), (ii) account “@BanjoMatilda” on Twitter, (iii) account “#Banjoandmatilda” on Instagram and (iv) Facebook page “Banjo & Matilda”. We also maintain an account on Pininterest.com. As our products sales grow in other countries, we expect to secure the registration of our trademark in foreign jurisdictions, such as the United States, the U.K. and the European Union.

Employees

As of September 15, 2014, we had 13 employees, all of which are employed in Australia except one in Hong Kong. None of our employees is currently covered by a collective bargaining agreement. We have had no labor-related work stoppages and we believe our relations with our employees are excellent.

Our Address

Our principal executive offices and a retail outlet are located at 76 William Street, Paddington, NSW 2021, Australia, and our telephone number is +61 2 8069-2665. Our corporate Internet address is banjoandmatildainvestors.com.

Item 1A. Risk Factors

An investment in our common stock involves a very high degree of risk. In evaluating us and our business, you should carefully consider the risks and uncertainties described below and the other information and our consolidated financial statements and related notes included herein. The risks provided below may not be all the risks we face. If any of events described in the risks below actually occurs, our financial condition or operating results may be materially and adversely affected, the price of our common stock may decline, perhaps significantly, and you could lose all or a part of your investment.

Risks Related to Our Business

Any material disruption of our information systems could disrupt our business and reduce our sales. We are dependent on information systems to operate our e-commerce websites, process transactions, respond to guest inquiries, manage inventory, purchase, sell and ship goods on a timely basis and maintain cost-efficient operations. Any material disruption or slowdown of our systems, including a disruption or slowdown caused by our failure to successfully upgrade our systems, system failures, viruses, computer “hackers” or other causes, could cause information, including data related to customer orders, to be lost or delayed which could result in delays in the delivery of products to our retail and wholesale customers or lost sales, which could reduce demand for our products and cause our sales to decline. If changes in technology cause our information systems to become obsolete, or if our information systems are inadequate to handle our growth, we could lose retail or wholesale customers.

|

7

|

The fluctuating cost of raw materials, particularly cashmere, could increase our cost of goods sold and cause our results of operations and financial condition to suffer. The fabric used to make our products is primarily cashmere, although we also use natural fibers, including cotton. Our costs for raw materials are affected by, among other things, weather, consumer demand, speculation on the commodities market, the relative valuations and fluctuations of the currencies of producer versus consumer countries and other factors that are generally unpredictable and beyond our control. Increases in the cost of raw materials, including petroleum or the prices we pay for our yarn, could have a material adverse effect on our cost of goods sold, results of operations, financial condition and cash flows.

The apparel industry is heavily influenced by general macroeconomic cycles that affect consumer spending, and a prolonged period of depressed consumer spending could have a material adverse effect on our business, financial condition and operating results. The apparel industry has historically been subject to cyclical variations, recessions in the general economy and uncertainties regarding future economic prospects that can affect consumer spending habits. Purchases of luxury items, such as our products, tend to decline during recessionary periods, when disposable income is lower. The success of our operations depends on a number of factors impacting discretionary consumer spending, including general economic conditions, consumer confidence, wages and unemployment, housing prices, consumer debt, interest rates, fuel and energy costs, taxation and political conditions. A continuation or worsening of the current weakness in the global economy or the economy in our key markets (Australia, the United States and Europe) may negatively affect consumer and wholesale purchases of our products and could have a material adverse effect on our business, financial condition and operating results.

Privacy breaches and other cyber security risks related to our e-commerce business could negatively affect our reputation, credibility and business. We are responsible for storing data relating to our customers and employees and rely on third parties for the operation of parts of our e-commerce website, banjoandmatilda.com, and for the various social media tools and websites we use as part of our marketing strategy. Our online store on our website is operated by a third-party provider. Consumers, lawmakers and consumer advocates alike are increasingly concerned over the security of personal information transmitted over the Internet, consumer identity theft and privacy. We require that our third-party service provider implements reasonable security measures to protect our customers’ identity and privacy. We do not, however, control these third-party service providers and cannot guarantee that no electronic or physical computer break-ins and security breaches will occur in the future. Likewise, our systems and technology are subject to the risk of system failures, viruses, “hackers” and other causes that are out of our control. Any perceived or actual unauthorized disclosure of personally identifiable information regarding our customers or website visitors could harm our reputation and credibility, reduce our online sales, impair our ability to attract website visitors and reduce our ability to attract and retain customers, and potentially expose us to significant related liability. Finally, we could incur significant costs in complying with the multitude of local, national and foreign laws regarding the use and unauthorized disclosure of personal information (to the extent they are applicable). We also may incur significant costs in our implementation of additional security measures to comply with applicable laws and industry standards and to further protect customer data.

The departure of our co-founders could have a material adverse effect on our business. We depend on the services and management experience of our co-founders, Belinda Storelli Macpherson and Brendan Macpherson, who have substantial experience and expertise in our business. In particular, Ms. Macpherson has provided design leadership to Banjo & Matilda since its inception. She is instrumental to our marketing and publicity strategy and is closely identified with both our brand and company. Our ability to maintain our brand image and leverage the goodwill associated with Ms. Macpherson may be damaged if we were to lose her services. We have an employment agreement with Ms. Macpherson, but she has the right to terminate her employment agreement at any time upon 30 days written notice. The employment agreement contains a covenant not to compete, but it is only applicable if her severance payments equal at least $100,000 and is limited to six months duration and geographically to within a five-mile radius of any location where we design, manufacture or sell our knitwear. Accordingly, Ms. Macpherson could terminate her employment agreement with us and within a short time engage in a competing business, which could materially adversely affect us. In addition, the leadership of Brendan Macpherson, our Chief Executive Officer, has been a critical element of Banjo & Matilda’s success. Mr. Macpherson also has the right, under his employment agreement with us, to terminate his employment at any time upon 30 days written notice The loss of services of Mr. Macpherson and/or Ms. Macpherson or any negative public perception with respect to, or relating to, the loss of one or more of these individuals could have a material adverse effect on our business, financial condition and operating results.

We are dependent on two distribution facilities. If one or more of our distribution facilities experiences operational difficulties or becomes inoperable, it could have a material adverse effect on our business, financial condition and operating results. We use distribution facilities in Hong Kong and in Alexandria, Australia. Our ability to meet the needs of our wholesale customers and our online retail customers depends on the proper operation of these distribution facilities. If either of these distribution facilities were to shut down or otherwise become inoperable or inaccessible for any reason, we could suffer a substantial loss of inventory and/or disruptions of deliveries to our wholesale customers and retail customers. In addition, we could incur significantly higher costs and longer lead times associated with the distribution of our products during the time it takes to reopen or replace the damaged facility. Any of the foregoing factors could have a material adverse effect on our business, financial condition and operating results.

|

8

|

If our manufacturing contractors fail to use acceptable, ethical business practices, our business and reputation could suffer. We do not own or operate any manufacturing facilities. We use third-party contract manufacturers, mostly in China. We require our manufacturing contractors to operate in compliance with applicable laws, rules and regulations regarding working conditions, employment practices and environmental compliance. Additionally, we impose upon our business partners operating guidelines that require additional obligations in those three areas in order to promote ethical business practices, and our staff and third parties we retain for such purposes periodically visit and monitor the operations of our manufacturing contractors to determine compliance. However, we do not control our manufacturing contractors or their labor and other business practices. If one of our manufacturing contractors violates applicable labor or other laws, rules or regulations or implements labor or other business practices that are generally regarded as unethical in our markets, such as Australia, Europe or the United States, the shipment of finished products to us could be interrupted, orders could be cancelled, relationships could be terminated and our reputation could be damaged. Any of these events could have a material adverse effect on our business, financial condition and operating results.

Due to the highly competitive nature of the apparel industry, our success depends on our ability to meet consumer demands, respond to fashion trends, and provide superior quality. There is intense competition in the sector of the apparel industry in which Banjo & Matilda participates. Banjo & Matilda competes with many other apparel companies, some of which are larger and have greater financial resources, more comprehensive product lines; longer-standing relationships with suppliers, manufacturers, and retailers; greater distribution and marketing capabilities; and, stronger brand recognition and loyalty than Banjo & Matilda. Our competitors’ greater capabilities in these areas may enable them to better differentiate their products from Banjo & Matilda, withstand periodic downturns in the apparel industry, compete more effectively on the basis of price and production and more quickly develop new products. Management of Banjo & Matilda believes in order to be successful in this industry we must be able to evaluate and respond to changing consumer demand and taste and to remain competitive in the areas of style and quality while operating within the significant domestic and foreign production and delivery constraints of the industry.

We cannot assure you that any business we acquire will benefit from its acquisition by us. We cannot assure you we will realize any of the perceived benefits to our business from the acquisition of Banjo & Matilda. The past performance of Banjo & Matilda is not necessarily indicative of future performance. The process of combining the organization of a private company into a public company such as ours involves certain risks, including exposure to unknown liabilities of the acquired company, and may cause fundamental changes to their business or in their operations. In addition, our operating results may be affected by the additional expenses we incur in integrating Banjo & Matilda into our organization and the significant increase in expenses relating to financial statement preparation and compliance with controls and procedures standards established by the Sarbanes-Oxley Act of 2002.

Our inability to successfully manage the growth of our business may have a material adverse effect on our business, results of operations and financial condition. We intend to continue our growth strategy to grow our online customer base and sales, wholesale customer base, expand our product offerings and add retail stores. Our ability to execute this growth strategy is subject to significant risks, some of which are beyond our control, including:

|

· |

the inherent uncertainty regarding general economic conditions |

|

|

· |

our ability to obtain adequate financing for our expansion plans |

|

|

· |

the degree of competition in new markets and its effect on our ability to attract new customers; and |

|

|

· |

our ability to recruit qualified personnel, in particular in areas where we face a great deal of competition |

Our future success will be highly dependent upon our ability to manage successfully the expansion of our operations. Our ability to manage and support our growth effectively will be substantially dependent on our ability to implement adequate improvements to our financial, inventory, and management controls, and hire sufficient numbers of effective financial, accounting, administrative, and management personnel. We may not succeed in our efforts to identify, attract and retain such personnel.

We are already highly leveraged and our growth strategies require significant capital investments and may require us to seek external financing, which may not be available on terms favorable to us. Our business operations and growth strategies require substantial capital investments, the availability of which depends on our ability to generate cash flow from operations, borrow funds on satisfactory terms and raise funds in the capital markets. Our ability to arrange for financing to support our capital expenditures and the cost of such financing are dependent on numerous factors, including general economic and capital markets conditions, interest rates and credit availability from banks or other lenders, many of which are beyond our control. In addition, increases in interest rates or the failure to obtain external financing on terms favorable to us will affect our financing costs and our results of operations. We are already highly leveraged and rely on capital contributions and loans from our principal shareholders and third parties, including: the $250,000 Convertible Note from Raymond Key secured by a lien on substantially all of our assets, two loans from KBM Worldwide Inc. in the amount, collectively, of $148,600; a $1.5 million trade facility with Sallyport Commercial Finance, a factoring and asset-based lending company; and a Loan Facility Agreement with Harboursafe Holdings (which company is controlled by our chief executive officer, Brendan Macpherson) in the amount of approximately $963,000, secured by our intellectual property. We may not be able to obtain future financing in amounts or on terms acceptable to us.

|

9

|

Fluctuations in exchange rates could adversely affect our business as well as result in foreign currency exchange losses in our U.S. dollar financials. The functional currency of Banjo & Matilda is Australian dollars. The accounts of Banjo & Matilda are maintained, and its financial statements are expressed, in Australian dollars. Such financial statements are translated into U.S. dollars with the Australian dollar as the functional currency. All assets and liabilities are translated at the exchange rate at the balance sheet date, stockholder’s equity is translated at the historical rates and income statement items are translated at the average exchange rate for the period. Transactions in foreign currencies are initially recorded at the functional currency rate ruling at the date of transaction. Any differences between the initially recorded amount and the settlement amount are recorded as a gain or loss on foreign currency transaction in the statements of operations. The resulting translation adjustments are reported under other comprehensive income as a component of shareholders’ equity. The value of the Australian dollar against the U.S. dollar and other currencies is affected by, among other things, changes in political and economic conditions and U.S. and Australian foreign exchange policies. Any material change in the exchange ratio between the Australian dollar and the U.S dollar may materially and adversely affect our reported amounts in U.S .dollars of cash flows, revenues, earnings and financial position and the value of, and any dividends payable to, our shares of common stock in U.S. dollars.

In addition, we sell our knitwear worldwide and purchases of our knitwear are made in foreign currencies and recorded in Australian dollars at exchange rates then in effect. We also transact business with wholesalers, retail outlets, manufacturers and distributors in various foreign countries, including China, Europe and the United States. Transactions are denominated in foreign currencies and recorded in Australian dollars at the rates of exchange in effect at the time of each transaction. Exchange gains and losses are recognized for the different foreign exchange rates applied when the foreign currency assets and liabilities are settled. Any material fluctuations in exchange rates between the Australian dollar and these foreign currencies could materially adversely affect our results of operations.

We are required to make significant estimates and assumptions in the preparation of our financial statements and our estimates and assumptions may not be accurate. The preparation of our financial statements in conformity with generally accepted accounting principles in the United States of America (“GAAP”) requires our management to make significant estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting periods. Critical estimates include, among other things, the collectability of accounts receivable, accounts payable, sales returns and recoverability of long-term assets. If our underlying estimates and assumptions prove to be incorrect, our financial condition and results of operations may be materially different from that reported in our financial statements.

Risks Related to Our Common Stock and Our Status as a Public Company

We may need to raise additional capital by sales of our common stock, which may adversely affect the market price of our common stock and your rights in us may be reduced. We will need to raise additional funds to expand our online sales, increase wholesale sales, expand our product lines and add retail stores. In order to satisfy our funding requirements we may consider issuing additional debt or equity securities. If we issue equity or convertible debt securities to raise such additional funds, our existing stockholders may experience dilution, and the new equity or debt securities may have rights, preferences and privileges senior to those of our existing stockholders. If we incur additional debt, it may increase our leverage relative to our earnings or to our equity capitalization, requiring us to pay additional interest expenses and potentially lower our credit ratings. We may not be able to market such issuances on favorable terms, or at all, in which case, we may not be able to develop or enhance our products, execute our business plan, take advantage of future opportunities or respond to competitive pressures.

There is a limited public trading market for our common stock, which may have an unfavorable impact on our stock price and liquidity. Our common stock is not listed on any exchange; it is quoted on the OTCQB quotation service. We have not engaged a broker-dealer to make a market in our common stock. There has been a limited trading market for our common stock in the past and there can be no assurance that a trading market in our shares of common stock will develop and be sustained. The trading market for securities of companies quoted on the OTCQB or other quotation systems is substantially less liquid than the average trading market for companies listed on Nasdaq or a national securities exchange. The quotation of our shares on the OTCQB or other quotation system may result in a less liquid market available for existing and potential shareholders to trade shares of our common stock, could depress the trading price of our common stock and could have a long-term adverse impact on our ability to raise capital in the future. Holders of our common stock should be willing to hold onto their shares for a long period of time.

State securities laws may limit secondary trading, which may restrict the states in which and conditions under which you can sell the shares offered by this prospectus. Secondary trading in our common stock will not be possible in any state until the common stock is qualified for sale under the applicable securities laws of the state or there is confirmation that an exemption, such as listing in certain recognized securities manuals, is available for secondary trading in the state. If we fail to register or qualify, or to obtain or verify an exemption for the secondary trading of, the common stock in any particular state, the common stock could not be offered or sold to, or purchased by, a resident of that state. In the event that a significant number of states refuse to permit secondary trading in our common stock, the liquidity for the common stock could be significantly impacted thus causing you to realize a loss on your investment.

|

10

|

The Registrant’s board of directors designated a series of preferred stock without shareholder approval that has voting rights that adversely affect the voting power of holders of the Registrant’s common stock and may have an adverse effect on its stock price. The Registrant’s Certificate of Incorporation provides for the authorization of 100,000,000 shares of “blank check” preferred stock. Pursuant to our Articles of Incorporation, the Registrant’s Board of Directors is authorized to issue such “blank check” preferred stock with rights that are superior to the rights of stockholders of the Registrant’s common stock, including a conversion price then approved by our Board of Directors, which conversion price may be substantially lower than the market price of shares of the Registrant’s common stock, without stockholder approval. In connection with the Registrant’s employment agreement with its Chief Executive Officer, Brendan Macpherson, the Board of Directors authorized 1,000,000 shares of preferred stock with each share having 100 votes until Mr. Macpherson’s employment agreement expires or terminates. The Registrant issued the 1,000,000 shares of preferred stock to Mr. Macpherson pursuant to his employment agreement and, upon the filing of a certificate of designation for such preferred shares and the subsequent issuance of such shares, Mr. Macpherson gained voting control of the Registrant, which has a negative effect on the voting power of the holders of the Registrant’s common stock and may cause its stock price to decline.

Brendan Macpherson, our Chief Executive Officer, has significant influence over us, including control over decisions that require the approval of stockholders, which could limit your ability to influence the outcome of key transactions, including a change of control. Brendan Macpherson, our Chief Executive Officer, owns approximately 44% of our outstanding shares of common stock, and 1,000,000 shares of super-voting preferred stock until his employment agreement expires or terminates, and consequently has effective control over our business, including matters requiring the approval of our stockholders, such as election of directors, approval of significant corporate transactions and the timing and distribution of dividends, if any, on our common stock. In addition, Mr. Macpherson controls our policies and operations, including, among other things, the appointment of management, future issuances of our common stock or other securities, the incurrence of debt by us, and the entering into of extraordinary transactions.

Mr. Macpherson may have interests that do not align with the interests of our other stockholders, including with regard to pursuing acquisitions, divestitures, and other transactions that, in his judgment, could enhance his equity value, even though such transactions might involve risks to our other stockholders. For example, Mr. Macpherson could cause us to make acquisitions that increase our indebtedness. Mr. Macpherson will have effective control over our decisions to enter into such corporate transactions regardless of whether others believe that any transaction is in our best interests. Such control may have the effect of delaying, preventing, or deterring a change of control of our company, could deprive stockholders of an opportunity to receive a premium for their common stock as part of a sale of our company, and might ultimately affect the market price of our common stock.

We will incur significant costs as a result of operating as a public company, and our management will be required to devote substantial time to new compliance requirements, including establishing and maintaining internal controls over financial reporting, and we may be exposed to potential risks if we are unable to comply with these requirements. As a public company we will incur significant legal, accounting and other expenses under the Sarbanes-Oxley Act of 2002, together with rules implemented by the Securities and Exchange Commission and applicable market regulators. These rules impose various requirements on public companies, including requiring certain corporate governance practices. Our management and other personnel will need to devote a substantial amount of time to these requirements. Moreover, these rules and regulations will increase our legal and financial compliance costs and will make some activities more time-consuming and costly.

The Sarbanes-Oxley Act requires, among other things, that we maintain effective internal controls for financial reporting and disclosure controls and procedures. In particular, we must perform system and process evaluations and testing of our internal controls over financial reporting to allow management to report on the effectiveness of our internal controls over financial reporting, as required by Section 404 of the Sarbanes-Oxley Act. Compliance with Section 404 may require that we incur substantial accounting expenses and expend significant management efforts. We have concluded that our disclosure controls and procedures and our internal controls over financial reporting are not effective due to material weaknesses identified in our internal controls over financial reporting. These material weaknesses include: lack of a full-time Chief Financial Officer with accounting expertise, lack of a formal review process and ineffective oversight due to the lack of an audit committee comprised of independent directors. Remediating these weaknesses will require the expenditure of capital to hire additional staff and other measures. If we cannot take steps to timely remediate the weaknesses in our internal controls, the market price of our stock could decline if investors and others lose confidence in the reliability of our financial statements. Similarly, we could have difficulty attracting third-party lenders and market-makers in our common stock if such lenders or broker-dealers believe they cannot rely on our financial statements as materially accurate. In addition, we could be subject to sanctions or investigations by the SEC or other applicable regulatory authorities.

Our management is not familiar with the United States securities laws and our Chief Financial Officer is a part-time employee. Our management is generally unfamiliar with the requirements of the United States securities laws, our Chief Executive Officer and Chief Financial Officer, Brendan Macpherson, does not possess accounting expertise, and an external Chief Financial Officer with accounting experience only works for us on a part-time basis, all of which could adversely impact our ability to comply with legal, regulatory, and financial reporting requirements under the U.S. securities laws. Our management may not be able to implement programs and policies in an effective and timely manner to adequately respond to such legal, regulatory and reporting requirements, including the establishment and maintenance of internal control over financial reporting. Any such deficiencies, weaknesses or lack of compliance could have a materially adverse effect on our ability to comply with the reporting requirements of the Exchange Act, which are necessary to maintain public company status, and could result in investigations by the Securities and Exchange Commission, and other regulatory authorities that could be costly, divert management’s attention and disrupt our business, If we were to fail to fulfill those obligations, our ability to operate as a public company would be in jeopardy, in which event you could lose your entire investment in our company.

|

11

|

If a trading market in our common stock ever develops, the market price of our common stock can become volatile, leading to the possibility of its value being depressed at a time when you may want to sell your holdings. If a trading market in our common stock develops, the market price of our common stock could become volatile. Numerous factors, many of which are beyond our control, may cause the market price of our common stock to fluctuate significantly. These factors include:

|

· |

our earnings releases, actual or anticipated changes in our earnings, fluctuations in our operating results or our failure to meet the expectations of financial market analysts and investors; |

|

· |

changes in financial estimates by us or by any securities analysts who might cover our stock; |

|

· |

speculation about our business in the press or the investment community; |

|

· |

significant developments relating to our relationships with our wholesale customers or suppliers; |

|

· |

stock market price and volume fluctuations of other publicly traded companies and, in particular, those that are in our industry; |

|

· |

customer demand for our products or luxury goods in general; |

|

· |

investor perceptions of our industry in general and Banjo & Matilda in particular; |

|

· |

the operating and stock performance of comparable companies; |

|

· |

general economic conditions and trends; |

|

· |

changes in accounting standards, policies, guidance, interpretation or principles; |

|

· |

loss of external funding sources; |

|

· |

sales of our common stock, including sales by our directors, officers or significant stockholders; and |

|

· |

additions or departures of key personnel. |

Securities class action litigation is often instituted against companies following periods of volatility in their stock price. Should this type of litigation be instituted against us, it could result in substantial costs to us and divert our management’s attention and resources. Moreover, securities markets may from time to time experience significant price and volume fluctuations for reasons unrelated to the operating performance of particular companies. These market fluctuations may adversely affect the price of our common stock and other interests in our Company at a time when you want to sell your interest in us.

We do not intend to pay dividends for the foreseeable future. We have never declared or paid any cash dividends on our common stock and do not intend to pay any cash dividends in the foreseeable future. We anticipate that we will retain all of our future earnings for use in the development of our business and for general corporate purposes. Any determination to pay dividends in the future will be at the discretion of our board of directors. Accordingly, investors must rely on sales of their common stock after price appreciation, which may never occur, as the only way to realize any future gains on their investments.

Our common stock is considered “a penny stock” and, as a result, it may be difficult to trade a significant number of shares of our common stock. The Securities and Exchange Commission (“SEC”) has adopted regulations that generally define “penny stock” to be an equity security that has a market price of less than $5.00 per share, subject to specific exemptions. Since our common stock has been eligible for quotation on the OTC markets (such as the bulletin board), the market price of our common stock has been less than $5.00 per share. We expect the market price for our common stock will remain less than $5.00 per share for the foreseeable future and, therefore, may be a “penny stock” according to SEC rules. This designation requires any broker or dealer selling these securities to disclose certain information concerning the transaction, obtain a written agreement from the purchaser and determine that the purchaser is reasonably suitable to purchase the securities. These rules may restrict the ability of brokers or dealers to sell our common stock and may affect the ability of investors hereunder to sell their shares. In addition, because our stock is quoted on the OTC markets, investors may find it difficult to obtain accurate quotations of the stock and may experience a lack of buyers to purchase such stock or a lack of market makers to support the stock price.

|

12

|

As a former shell company, holders of restricted shares of our common stock cannot rely on Rule 144 to resell their shares until the conditions of the rule are met. Prior to the consummation of the Exchange Agreement, we were considered a shell company. As a result, we are subject to the provisions of Rule 144(i) which limit reliance on Rule 144 by shareholders owning stock in a shell company (or a former shell company). Under current interpretations, unregistered shares issued after we first became a shell company cannot be resold under Rule 144 until the following conditions are met:

|

· |

We cease to be a shell company; |

|

· |

We remain subject to the Exchange Act reporting obligations; |

|

· |

We file all required Exchange Act reports during the preceding 12 months; and |

|

· |

At least one year has elapsed from the time we filed our “Form 10 information” reflecting the fact that we ceased to be a shell company. |

Consequently, until the first anniversary of the filing of our Current Report on Form 8-K, filed November 18, 2013, reflecting that we ceased to be a shell company, holders of restricted shares of our common stock cannot rely on Rule 144 to sell such shares, and may do so then only if we have then filed all required Exchange Act reports during the preceding 12 months.

Since our principal assets are located in Australia, and none of our officers and directors are residents of the United States, it may be difficult or impossible for you to bring an action against us or against these individuals in Australia in the event that you believe that your rights have been infringed under the securities laws or otherwise, or to enforce any judgments rendered against us or our officers and/or directors. Our principal assets are located in Australia, and all of our officers and directors are not residents of the United States. Therefore, it may be difficult to effect service of process on such persons in the United States, and it may be difficult to enforce any judgments rendered by any courts of the United States against us or these officers and directors. Furthermore, it may be difficult or impossible for you to bring an action against us or against these individuals in Australia in the event that you believe that your rights have been infringed under the securities laws or otherwise. Even if you are successful in bringing an action of this kind, the laws of Australia may render you unable to enforce a judgment against our assets or the assets of our directors or officers that are not residents of the United States. There is doubt as to the enforceability in the Commonwealth of Australia, in original actions or in actions for enforcement of judgments of U.S. courts, of civil liabilities predicated solely upon federal or state securities laws of the U.S., especially in the case of enforcement of judgments of U.S. courts where the defendant has not been properly served in Australia. As a result of all of the above, our shareholders may have more difficulty in protecting their interests through actions against our management, directors or major shareholders compared to shareholders of a corporation doing business entirely within the United States.

Item 2. Properties

Banjo & Matilda leases a 1,076 square foot showroom located at 76 William Street, Paddington, New South Wales, Australia, where it also maintains its principal executive offices. Banjo & Matilda’s lease for this space expires on October 14, 2014, with an option to renew the lease for an additional three-year period. The monthly fixed rent for this space is approximately $4,433 per month. Management believes that the facilities are adequate for the Company’s current needs and for the foreseeable future. In addition, Banjo & Matilda uses a fulfillment service in Hong Kong that consolidates all of products manufactured in China. The cost of storage of our products by this fulfillment service company is included in our monthly fee.

Management believes the terms of the leases are consistent with market standards and were arrived at through arm’s-length negotiation.

Item 3. Legal Proceedings

We are not a party to any pending litigation and to our knowledge, no such litigation is contemplated or threatened. To our knowledge, none of our directors, officers, 5% shareholders or affiliates are party to any legal proceedings that would have a material adverse effect on our business, financial condition or operating results.

Item 4. Mine Safety Disclosures.

Not Applicable.

|

13

|

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

Our common stock is quoted on the OTCQB under the symbol “BANJ” (prior to November 14, 2013 the stock was quoted under the symbol “ESRN”). The OTCQB is a quotation service that displays real-time quotes, last-sale prices, and volume information in over-the-counter (“OTC”) equity securities. An OTCQB equity security generally is an equity that is not listed or traded on Nasdaq or a national securities exchange.

Price Range of Common Stock

Our fiscal year end changed from December 31 to June 30 in connection with the Exchange Agreement with Banjo & Matilda Ltd. in November 2013. The following table shows: (i) for the last two quarters of the fiscal year ended June 30, 2014, the high and low bid prices per share of our common stock as reported by the OTCQB quotation service; (ii) for the calendar year ended December 31, 2013, high and low quarterly sales prices; and (iii) for the calendar year ended December 31, 2012, high and low quarterly bid prices. The information for calendar years 2012 and 2013 was provided to us by the Financial Industry Regulatory Authority and the Interent. Over-the-counter quotations reflect inter-dealer prices, without retail mark-up or mark-down or commissions. These quotations may not necessarily reflect actual transactions.

| High Bid | Low Bid | |||||||

|

Fiscal Year ended June 30, 2014 |

|

|

|

|

||||

|

Third quarter: January 1, 2014 to March 31, 2014 |

$ |

0.2500 |

$ |

0.1500 |

||||

|

Fourth quarter: April 1, 2014 to June 30, 2014 |

$ |

0.4200 |

$ |

0.2002 |

||||

|

|

|

|

||||||

|

High Sale |

Low Sale |

|||||||

|

Calendar Year ended December 31, 2013 |

|

|

|

|

||||

|

First quarter January 1, 2013 to March 31, 2013 |

$ |

1.20 |

$ |

0.40 |

||||

|

Second quarter April 1, 2013 to June 30, 2013 |

$ |

1.10 |

$ |

0.52 |

||||

|

Third quarter July 1, 2013 to September 30, 2013 |

$ |

1.00 |

$ |

0.51 |

||||

|

Fourth quarter October 1, 2013 to December 31, 2013 |

$ |

0.75 |

$ |

0.25 |

||||

| High Bid | Low Bid | |||||||

|

Calendar Year ended December 31, 2012 |

|

|

|

|

||||

|

First quarter ended March 31, 2012 |

$ |

0.30 |

$ |

0.30 |

||||

|

Second quarter ended June 30, 2012 |

$ |

0.30 |

$ |

0.30 |

||||

|

Third quarter ended September 30, 2012 |

$ |

0.30 |

$ |

0.30 |

||||

|

Fourth quarter ended December 31, 2012 |

$ |

0.30 |

$ |

0.30 |

||||

Our Transfer Agent

We have appointed Olde Monmouth Stock Transfer Company, with offices at 200 Memorial Parkway, Atlantic Highlands, New Jersey 07716, phone number 732-872-2727, as transfer agent for our shares of common stock. The transfer agent is responsible for all record-keeping and administrative functions in connection with our shares of common stock.

Holders

As of September 15, 2014, there are approximately125 holders of record for the Registrant’s common stock. There are a total of 27,941,684 shares of common stock outstanding of which 12,332,561 are issued to a trust controlled by Brendan Macpherson, our Chief Executive Officer and director.

Dividends

We have not declared any cash dividends, nor do we intend to do so. We are not subject to any legal restrictions respecting the payment of dividends, except that they may not be paid to render us insolvent. Dividend policy will be based on our cash resources and needs and it is anticipated that all available cash will be needed for our operations in the foreseeable future.

|

14

|

Penny Stock Regulations

The SEC has adopted regulations which generally define so-called “penny stocks” to be an equity security that has a market price less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exemptions. The Registrant’s common stock is a “penny stock” and is subject to Rule 15g-9 under the Exchange Act, or the Penny Stock Rule. This rule imposes additional sales practice requirements on broker-dealers that sell such securities to persons other than established customers and “accredited investors” (generally, individuals with a net worth in excess of $1,000,000 or annual incomes exceeding $200,000, or $300,000 together with their spouses). For transactions covered by Rule 15g-9, a broker-dealer must make a special suitability determination for the purchaser and have received the purchaser's written consent to the transaction prior to sale. As a result, this rule may affect the ability of broker-dealers to sell our securities and may affect the ability of purchasers to sell any of our securities in the secondary market, thus possibly making it more difficult for us to raise additional capital.

For any transaction involving a penny stock, unless exempt, the rules require delivery, prior to any transaction in penny stock, of a disclosure schedule required by the SEC relating to the penny stock market. Disclosure is also required to be made about sales commissions payable to both the broker-dealer and the registered representative and current quotations for the securities. Finally, monthly statements are required to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stock.

There can be no assurance that the Registrant’s common stock will qualify for exemption from the Penny Stock Rule. Even if the Registrant’s common stock were exempt from the Penny Stock Rule, the Registrant would remain subject to Section 15(b)(6) of the Exchange Act, which gives the SEC the authority to restrict any person from participating in a distribution of penny stock, if the SEC finds that such a restriction would be in the public interest.

Rule 144

Prior to completion of the closing under the Exchange Agreement, the Registrant was considered a shell company. As a result, the Registrant is subject to the provisions of Rule 144(i) which limit reliance on Rule 144 by shareholders owning stock in a shell company (or a former shell company). Under current interpretations, unregistered shares issued after the Registrant first became a shell company cannot be resold under Rule 144 until the following conditions were met:

|

· |

The registrant ceases to be a shell company; |

|

· |

The Registrant remains subject to the Exchange Act reporting obligations; |

|

· |

The Registrant files all required Exchange Act reports during the preceding 12 months; and |

|

· |

At least one year has elapsed from the time the Registrant files “Form 10 information” reflecting the fact that the Registrant ceased to be a shell company. |

Consequently, until the first anniversary of the filing of the Registrant’s Current Report on Form 8-K, filed November 18, 2013, holders of the Registrant’s common stock cannot rely on Rule 144 to sell restricted shares of common stock.

Securities Authorized for Issuance under Equity Compensation Plans

The Registrant does not have any equity compensation plans and accordingly there are no shares authorized for issuance under an equity compensation plan.

Issuer Purchases of Our Equity Securities

No repurchases of our common stock were made by our company or its affiliates during the fourth quarter of our fiscal year ended June 30, 2014. There have been no recent sales of unregistered securities by us which have not already been reported in an 8-K or 10-Q.

Item 6. Selected Financial Data.

Not applicable because we are a smaller reporting company.

|

15

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion of our financial condition and results of operations should be read in conjunction with the audited and unaudited financial statements and the notes to those statements included elsewhere in this Report. This discussion contains forward-looking statements that involve risks and uncertainties. You should specifically consider the various risk factors identified in this Report that could cause actual results to differ materially from those anticipated in these forward-looking statements.

Company background

Founded in 2008 by Sydney designer Belynda Macpherson and her husband, Brendan Macpherson, Banjo & Matilda designs, manufactures, sells and distributes premium contemporary knitwear.

Because of the brand’s fresh designs, premium quality and irreverent Australian brand heritage, it has gained a loyal following by customers, the media, celebrities and retail partners alike.

Since 2008 the Company’s products have been sold through its e-commerce retail store into 16 countries and growing, and a physical retail store location in Sydney, Australia as well as temporary “pop up” concept stores. In addition, products are distributed through wholesale to key retail accounts in Australia, North America, Canada, United Kingdom, the Middle East and Europe.

The brand has experienced strong and consistent year-on-year revenue growth.

Growth opportunity