Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - OneMain Financial Holdings, Inc. | d793139dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on October 8, 2014

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

ONEMAIN FINANCIAL HOLDINGS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 6141 | 27-4393679 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

300 Saint Paul Place

Baltimore, MD 21202

(410) 332-3000

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

April O. Park

General Counsel

OneMain Financial Holdings, Inc.

300 Saint Paul Place

Baltimore, MD 21202

(410) 332-3000

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

| Richard D. Truesdell, Jr. Sophia Hudson Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Jeffrey D. Karpf Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, New York 10006 (212) 225-2000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer ¨ | ||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title Of Each Class Of Securities To Be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount Of Registration Fee | ||

| Common Stock, without par value |

$50,000,000 | $5,810 | ||

|

| ||||

|

| ||||

| (1) | Includes shares which the underwriters have the right to purchase to cover over-allotments. |

| (2) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 8, 2014

PRELIMINARY PROSPECTUS

Shares Common Stock $ per share

This is the initial public offering of shares of our common stock. We currently expect the initial public offering price to be between $ and $ per share of common stock. See “Use of Proceeds.”

Immediately following the completion of this offering, Citigroup Inc. will beneficially own between approximately % and % of our shares of common stock, depending on whether and the extent to which the underwriters exercise their over-allotment option.

We intend to apply to have our common stock listed on the New York Stock Exchange under the trading symbol “ .”

Investing in our common stock involves risks. See “Risk Factors” beginning on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Public Offering Price |

$ | $ | ||||||

| Underwriting Discounts and Commissions(1) |

$ | $ | ||||||

| Proceeds to OneMain (before expenses) |

$ | $ | ||||||

| (1) | See “Underwriting” for additional compensation to be paid to the underwriters. |

Citigroup Inc., or the selling stockholder, has granted the underwriters an option for a period of 30 days to purchase up to additional shares of common stock to cover over-allotments. Any proceeds resulting from the sale of shares by the selling stockholder, after deducting underwriting discounts, will be paid to the selling stockholder, and we will receive no proceeds from the exercise of the over-allotment option.

The underwriters expect to deliver the shares to purchasers on or about , 2014 through the book-entry facilities of The Depository Trust Company.

Sole Book-Running Manager

Citigroup

, 2014

Table of Contents

| Page | ||||

| ii | ||||

| 1 | ||||

| 9 | ||||

| 10 | ||||

| 15 | ||||

| 45 | ||||

| 47 | ||||

| 47 | ||||

| 48 | ||||

| 49 | ||||

| 51 | ||||

| 54 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

60 | |||

| 85 | ||||

| 98 | ||||

| 102 | ||||

| 115 | ||||

| 120 | ||||

| 121 | ||||

| 122 | ||||

| Material U.S. Federal Tax Considerations for Non-U.S. Holders of Our Common Stock |

130 | |||

| 132 | ||||

| 134 | ||||

| 136 | ||||

| 140 | ||||

| 140 | ||||

| 140 | ||||

| 140 | ||||

| F-1 | ||||

We, the selling stockholder and the underwriters have not authorized anyone to provide any information other than that contained or incorporated by reference in this prospectus or in any free writing prospectus prepared by or on behalf of us. We, the selling stockholder and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the selling stockholder are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus or any free writing prospectus is accurate as of any date other than the date of the relevant document. Our business, financial condition, results of operation or future growth prospectus may have changed since those dates.

i

Table of Contents

NON-GAAP FINANCIAL MEASURES AND OTHER INFORMATION

In this prospectus, we have included financial measures that are compiled in accordance with U.S. Generally Accepted Accounting Principles, or GAAP, as well as certain non-GAAP financial measures. These non-GAAP financial measures include:

| • | Adjusted pro forma net income from continuing operations is the pro forma net income from continuing operations giving effect to the Transactions (as defined in “Unaudited Pro Forma Combined Financial Information”) further adjusted for (i) the transfer of our real estate portfolio to an affiliate effective January 1, 2014 and (ii) the transfer of our servicing portfolio to an affiliate that occurred on January 6, 2014, in each case net of tax, as if each of the Transactions and the further adjustments had occurred on January 1, 2013. |

We refer to the (i) transfer of our real estate portfolio to an affiliate effective January 1, 2014 and (ii) transfer of our servicing portfolio to an affiliate on January 6, 2014 collectively as our 2014 exit from the real estate business. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Segment Overview.”

| • | Adjusted pro forma return on assets is the ratio of Adjusted pro forma net income from continuing operations to Adjusted average pro forma total assets. |

| • | Adjusted average pro forma total assets is the average pro forma total assets, giving effect to the Transactions and adjusted for our 2014 exit from the real estate business, as if each of the Transactions and the further adjustments had occurred on January 1, 2013. |

| • | Adjusted pro forma return on equity is the ratio of Adjusted pro forma net income from continuing operations to pro forma equity. |

These non-GAAP financial measures are supplemental measures of our performance and are not required by, or presented in accordance with, GAAP. We use the non-GAAP measures to provide us and other interested third parties a basis to better understand our ongoing operating results on a consistent basis. Other companies in our industry may calculate these measures differently than we do, limiting their usefulness as comparative measures.

The non-GAAP financial measures used in this prospectus have limitations as analytical tools, and you should not consider them in isolation or as a substitute for the analysis of our results as reported under GAAP. You should be aware that in the future we may incur expenses that are the same as, or similar to, the adjustments used in this prospectus. Our presentation of adjusted pro forma net income from continuing operations should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items.

Throughout this prospectus we also refer to the term “FICO score,” which means a credit score developed by Fair Isaac & Co. A FICO score is widely used as a means of evaluating the likelihood that credit users will pay their obligations. The range of FICO scores is 300-850, with a higher FICO score generally indicating a greater likelihood of repayment.

ii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary may not contain all of the information that you should consider before deciding to invest in our common stock. You should read this entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our combined financial statements, the notes to those statements and both our selected historical and pro forma combined financial data before making a decision to purchase our common stock. Some information in this prospectus contains forward-looking statements. See “Special Note Regarding Forward-Looking Statements.”

As used in this prospectus, all references in this prospectus to “OneMain,” the “Company,” “we,” “us,” “our,” “ours” or similar terms refer to OneMain Financial Holdings, Inc., a Delaware corporation, together with its consolidated subsidiaries. References to “Citi” refer to Citigroup Inc. and its subsidiaries other than OneMain.

OneMain Financial Overview

We are a leading consumer finance company in the United States, providing responsible solutions to credit-worthy individuals through our nationwide branch network and online channels. Our 100-plus year history and culture embodies our dedication to high-quality origination, underwriting and servicing of traditional, easily understood and transparent personal loans to primarily middle-income households. Our personal loans are fixed-rate, fixed-term and fixed-payment, which are attractive to our customers. We also offer optional products that protect customers in the event of unforeseen circumstances. We have been a stable and positive community presence using our industry-leading technology platform, proprietary underwriting process and data analytics to originate, price, manage, and monitor risk effectively through changing economic conditions. We have built a culture of compliance to anticipate, understand and embrace a changing regulatory environment. Our experienced management team, strong financial position, and adherence to our core values of customer advocacy, ethical leadership, ownership attitude, continuous improvement and personal development, position us well for future success and growth.

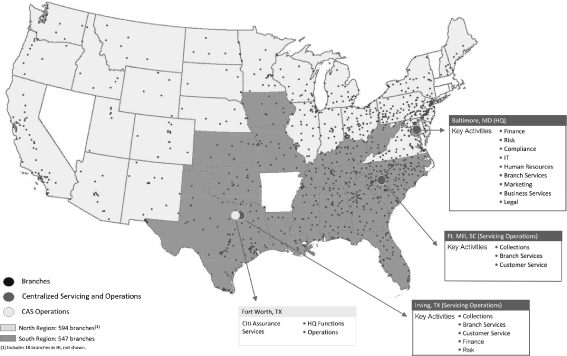

At the core of our business is a national, community-based network of 1,141 branches as of June 30, 2014, serving 1.3 million customer accounts across 43 states. This network is supported by our state-of-the-art technology platform that allows us to efficiently process applications and provide convenient self-service features for our customers. As of June 30, 2014, the network consists of a local, well-trained, front-end workforce of approximately 4,100 employees and is supported centrally by approximately 1,100 employees with additional functional support provided by Citi. Our captive insurance business, Citi Assurance Services, or CAS, is staffed by an additional workforce of approximately 215 employees. Our branch employees typically live in the communities they serve, and we believe our customers value the face-to-face interaction and the long-term relationships they build with our branch employees. This face-to-face interaction significantly enhances the value we provide to customers as we work together to assess their household budgets and ability to repay their loans. The knowledge gained and relationships built during the face-to-face interactions allow us to quickly service customers, while also improving our loan performance. Branches not only originate but also service loans through early-stage delinquency, which we view as a key aspect of our relationship-driven model. This relationship-driven model is further strengthened by our extensive and complementary centralized operations that deliver cost efficiencies and risk and compliance controls. Our experience suggests that combined, our branches and centralized operations are the most effective means for both serving our target customers and driving low default and delinquency rates in our loan portfolio.

Our customers are creditworthy and represent a unique segment of the middle-income market that is underserved by traditional banking institutions and can particularly benefit from our reationship-driven approach. Our customers typically come to us with a specific borrowing need. We believe our customers prefer and benefit

1

Table of Contents

from the face-to-face discussion of their household budgets and cash flow needs with our branch employees. Our customers value speed, convenience, service and funds availability as high priorities. Our customers have an average FICO score of 630 and an average income of $45,000.

During 2013, we advanced new funds totaling $3.2 billion, and at June 30, 2014, we had $8.2 billion of loans outstanding and 1.3 million customer accounts. For the year ended December 31, 2013, we had net income of $536 million, representing a return on assets of 5.4% and return on equity of 19.9%. For the six months ended June 30, 2014, we had net income of $287 million, representing a return on assets of 6.0% and a return on equity of 19.1%.

Our Strengths

Largest Consumer Finance Branch Network in the United States with Complementary Centralized Support Operations

Our business is large and well established with 1,141 branches as of June 30, 2014, serving 1.3 million customer accounts across 43 states. Our national, community-based branch network is the foundation of our relationship-driven business model and is the product of thoughtful market identifications and profitability analysis. Our centralized operations provide customer services, transaction processing and late-stage collection efforts, driving operating efficiencies and risk and compliance control. We believe the scale of our business, resulting operating efficiencies, proprietary industry knowledge and investment in regulatory compliance contribute significantly to our success and profitability.

Industry-Leading Technology Strategy and Platform

We believe that our technology platform is a strategic asset, and we maintain a well-defined technology strategy and investment plan to protect our competitive edge. Technology investments improve our speed of service and ability to respond to customer needs and help drive our efficiency, scale and stable operations. We use a centrally-run technology platform with proprietary applications for originations, servicing and collections to provide a seamless, real-time link between our branches and our centralized operations. The cornerstone of this platform is our internally developed, front-office processing platform that integrates our key business functions into a single, web-based solution. Additionally, our expanding digital capabilities are helping us service and grow our customer base.

Centralized Risk Analytics Supported by Our Proprietary, National Database

Our longevity and stability result from our focus on providing straightforward, traditional loan products and our conservative approach to originating loans. While our branches originate and service loans, our pricing, loan underwriting and approval decisions are made centrally through our risk management system. Our disciplined risk management model and advanced analytics effectively complement localized branch operations to drive low default and delinquency rates. We use a rigorous underwriting process that leverages industry and proprietary credit tools built using customer performance data from our national lending database. Our long-tenured and experienced branch staff complements our data-driven process.

Extensive Experience with Complex Regulatory Oversight and Strong Compliance Culture

We have extensive experience operating in a complex and highly regulated environment. We have built a robust compliance culture in the last decade and established processes and controls to monitor our legal and regulatory adherence. Our primary regulators are state regulators from whom we have state level licenses, the Board of Governors of the Federal Reserve System, or the Federal Reserve Board, and the Consumer Financial

2

Table of Contents

Protection Bureau, or the CFPB. In 2013, state regulators conducted exams of over 600 of our branches and centralized sites. In addition, as a subsidiary of a bank holding company, we have been closely examined a number of times by the Federal Reserve Board and continue to have regular interactions with them. We also have been examined several times by the CFPB, and we believe our business is well suited to address their requirements.

Robust Financial Performance

We increased our profitability in 2012 and 2013 with net income of $407 million and $536 million, a return on assets of 4.0% and 5.4% and an operating efficiency ratio of 34.8% and 32.5% in each of the two years, respectively. We believe our profitability can be attributed to our rigorous underwriting process, strong pricing and expense discipline, operational expertise and loyal customer base.

Seasoned Management with Extensive Industry Experience

We have highly experienced employees throughout all levels of our organization. Mary McDowell, our Chief Executive Officer and President, is an accomplished financial services executive with more than 30 years of experience in consumer finance and was the 2010-2011 Chair of the American Financial Services Association, the consumer credit industry’s trade organization. Senior leadership has an average of 24 years of experience in consumer finance and an average tenure of 18 years at OneMain and/or Citi. Our branch network employees and managers hold an average tenure of 11 and 14 years, respectively, and our district managers and area directors average 19 and 24 years of experience, respectively, when looking at their combined years of service at OneMain and Citi.

Our Business and Growth Strategy

We are a leading branch-based consumer finance business in the United States, and our strategy is to enhance stockholder value by (1) maintaining our attractive profitability profile and (2) growing our business through new origination channels, capabilities and products, as follows:

Maintain Our Attractive Profitability by Focusing on Fundamental Aspects of Our Business

| • | Customer-Centric Strategy: Our customer-centric strategy is to continue to deliver responsible solutions consistent with fair lending principles to our customers to grow our market and gain market share. Improving the customer experience is the primary motivation for our investments in digital, product and service innovations. |

| • | Data-Driven, Analytical Approach to Profit Optimization: Data analysis is the core of our business engine, and the multi-decade history of consumer behavior that forms the backbone of our analytics gives us a strong competitive advantage. Our ability to link marketing activity, branch incentives, financial return and risk analytics to drive profitability forms the foundation of our strategy. We continuously improve our data collection, management and analytical capabilities to further expand growth possibilities and focus on the most profitable opportunities. |

| • | Highly Efficient and Scalable Operations: We believe that we are an industry leader in operating efficiency, and we remain diligent by continuously leveraging digital advancements and other opportunities to optimize our expense base. We test new branch models, layouts, locations and centralized support and distribution options on a regular basis to optimize employee focus on customers while maintaining efficiency. We design technology platforms for our centralized operations and branches that are scalable so that we may grow efficiently. |

| • | Diverse Funding Sources: We have the proven ability to finance our business from a variety of funding sources, including cash flows from operations and the capital markets in the form of two personal loan securitizations. |

3

Table of Contents

Grow Our Business Through New Origination Channels, Capabilities and Products

| • | Increase Personal Loan Volume through New Channels: We are growing volume by expanding outreach to new customers through physical and digital channels. On the physical front, we are focusing on customer referrals and partnerships with retailers and other institutions that cater to our core customer base. We are also growing leads through digital channels by extending our network of over 40 online partners (for example, our relationship with a leading “peer-to-peer” online lending platform), increasing volume through our dedicated online portal and leveraging channels such as social media. |

| • | Digital Sales and Service Enablement: We are developing new capabilities as part of our digital strategy to increase loan applications through all channels. We have been testing centralized capabilities to onboard new borrowers that complement our local presence and increase the volume of loans we make. These capabilities allow us to provide rapid response times to customers from both physical and digital channels, for inquiries and pre-closing services. We have launched 20 fully operating “Discovery Branches” to test new technologies, operating models and processes that increase our productivity, improve the customer experience, accelerate learning and speed deployment across the network. Discovery Branch learnings, along with our investments in new account and data management systems and enhanced web capabilities, are helping us create the flexibility to originate, fund and service loans online. |

| • | Broaden Our Product Offering: We believe that we can successfully offer additional complementary financial products to our customers. In 2013, approximately 65% of our customer base purchased optional products in addition to receiving a personal loan. We may either develop additional complementary financial products ourselves or distribute them on behalf of partners. We have achieved success with these strategies in the past. Leveraging our risk expertise and extensive branch network with expanded solutions has the potential to both increase the products available to existing customers and attract new customers. |

4

Table of Contents

Industry and Market Overview

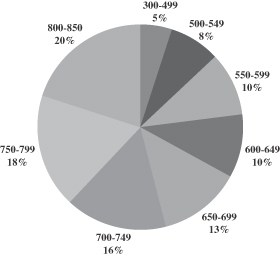

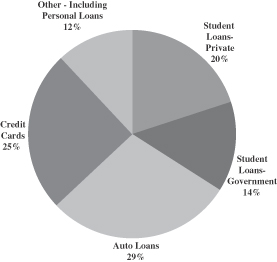

The U.S. consumer finance industry has approximately $3.1 trillion of outstanding borrowings and includes vehicle loans and leases, credit cards, student loans and personal loans. Our 1.3 million customer accounts represent a very small fraction of the approximately 115 million Americans that generally align with our customer base (FICO scores between 550 and 749). We believe that most of this population is underserved and provides an attractive market opportunity for our business.

| $3.1 Trillion Consumer Finance Industry | U.S. FICO Score Distribution | |

|

|

| |

| Sources: Federal Reserve Bank of New York; Federal Student Aid/U.S. Department of Education. As of March 2014. | Source: FICOTM Banking Analytics Blog. © Fair Issac Corporation. As of April 2014. | |

As a leading player in the highly-fragmented, non-prime consumer finance industry, we believe we are uniquely positioned to take advantage of this opportunity. Many existing consumer lenders operate at a regional level and typically have fewer than 200 branches and less than $2 billion in loans outstanding. With 1,141 branches and $8.2 billion loans outstanding as of June 30, 2014, our strategy is to maintain and expand our market share with our robust physical and online presence.

5

Table of Contents

Our History and Development

We have been operating since the founding of our predecessor, Commercial Credit Company, in 1912. Since our founding, we have grown both organically as well as through various acquisitions. Commercial Credit Company acquired Primerica in 1988, forming the Primerica Corporation, which acquired the Travelers Corporation in 1993. Following the merger of Travelers Group with Citicorp to form Citigroup Inc. in 1998, Commercial Credit was rebranded as CitiFinancial in 1999.

Prior to 2011, we were part of a larger business within Citi known as CitiFinancial North America, or CFNA, the U.S. business of which contained approximately $10 billion of personal loans and $15 billion of mortgage and real estate loans. In the middle of 2010, management decided to split the U.S. business of CFNA into two distinct business lines. OneMain, the go-forward business, retained the majority of U.S. personal loans and a portion of U.S. real estate loans. CitiFinancial Servicing was formed with the remaining portion that did not strategically align with OneMain’s go-forward origination and risk strategy. CitiFinancial Servicing was designed to support certain customers and loans that would benefit from expanded support, including loan modifications or restructurings, rather than originate loans. In effect, CitiFinancial Servicing became a liquidating business. For a discussion of the separation and how it and subsequent transactions are presented in our combined financial statements, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Segment Overview.”

The Transactions and Our Separation from Citi

Citi currently indirectly owns 100% of our common stock. After the completion of this offering, Citi will beneficially own % of our outstanding common stock (or % if the underwriters exercise their over-allotment option in full). Prior to this offering, we expect to declare a dividend of a $ million note, which we refer to as the Dividend Note, and issue the Dividend Note to Citi. We intend to repay the Dividend Note in full (plus any accrued and unpaid interest thereon) with the proceeds of this offering.

Upon the consummation of this offering, we will enter into a number of agreements with Citi that will govern our relationship with Citi. We refer to this offering, our establishment of a fully independent capital structure and the various other transactions relating to our separation from Citi as the “Transactions.” For more information relating to the Transactions, see “Unaudited Pro Forma Combined Financial Information.” For a discussion of certain risks associated with our separation from Citi, see “Risk Factors—Risks Relating to Our Organization and Structure.”

Debt Financings

Historically, we have funded our operations through cash from our operations and funding provided by Citi. The weighted average interest rate on our historical debt was 3.7% per annum for the year ended December 31, 2013. In April 2014 and July 2014, we raised capital through two securitizations of our loan portfolio. We have started to establish a fully independent capital structure and to finance our liquidity needs from a variety of third-party debt sources. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources” and “Description of Certain Indebtedness.” As we establish a fully independent capital structure, existing debt in some cases may be replaced by higher-cost funding provided by third-party sources. Pro forma for the Transactions at June 30, 2014, our debt outstanding would have by approximately $ billion, and for the year ended December 31, 2013 and the six months ended June 30, 2014, our interest expense would have by $ million and $ million, respectively, and our cost of funds would have from % to % per annum, respectively. See “Unaudited Pro Forma Combined Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of

6

Table of Contents

Operations—Business Trends and Conditions—Changing funding mix and increased funding costs” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Our Separation from Citi.”

Corporate Information

Our executive offices are located at 300 St. Paul Place, Baltimore, Maryland 21202, and our telephone number is (410) 332-3000. Our website address is www.onemainfinancial.com. The information on our website is not a part of this prospectus.

Risks Affecting Us

As part of your evaluation of our company, you should consider the risks associated with our business, regulation of our business, our indebtedness, our organization and structure and this offering. These risks include:

| • | Risks relating to our business, including: (i) our ability to access adequate sources of liquidity to fund operational requirements and satisfy financial obligations; (ii) the impact of macroeconomic conditions; (iii) insufficient allowance for loan losses; (iv) our ability to successfully manage our credit risk; (v) the identification of material weaknesses and significant deficiencies in our internal control over financial reporting; (vi) historical charge-off rates that may not be predictive of future charge-off rates; (vii) the effectiveness of our risk management processes and procedures, and the accuracy of the assumptions or estimates used in our models and in preparing our financial statements; (viii) the competition in the consumer finance industry; (ix) risks and uncertainties associated with our insurance operations; (x) failures or security breaches in our or third parties’ information systems or Internet platform or disruptions in the operations of our computer systems and data centers; (xi) our transition to, and quality of, new technology platforms; (xii) our ability to protect our intellectual property; (xiii) litigation and regulatory actions; (xiv) damage to our reputation; (xv) our ability to attract, retain and motivate key officers and employees; (xvi) misconduct by our employees or third parties that we employ; (xvii) potential future geographic concentrations of our loan portfolio; (xviii) requirements to repurchase loans from purchasers of loans that we sell or securitize; (xix) our ability to implement our growth strategy and realize the value of strategic investments; (xx) our ability to successfully develop new or enhanced products; and (xxi) natural disasters, acts of war or terrorism or other external events. |

| • | Risks relating to regulation, including: (i) significant and extensive regulation, supervision and examination of, and enforcement relating to, our business by governmental authorities; (ii) impact of the Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, and the impact of the CFPB’s regulation of our business; (iii) regulations and supervision by the Federal Reserve Board for as long as we are controlled by Citi for bank regulatory purposes; (iv) regulatory scrutiny resulting from selling loans, including charged off loans and loans where the borrower is in default; (v) the impact of state regulations in the states in which we conduct our business; (vi) regulations relating to privacy, information security and data protection; (vii) use of third-party vendors and ongoing third-party business relationships; and (viii) banking regulations that limit our business activities. |

| • | Risks relating to our indebtedness, including: (i) the size of our indebtedness, which could affect our ability to meet our obligations under our debt instruments and could impact our business; (ii) the impact of covenants in our debt instruments that may restrict our operations; (iii) the accuracy of the judgments and estimates used in assessing our liquidity; (iv) the potential impact to our funding and business resulting from a change in our credit ratings; (v) the impact of our securitizations and ability to access the securitizations market in the future; and (vi) repayment of the Dividend Note and compliance with its covenants. |

7

Table of Contents

| • | Risks relating to our organization and structure, including: (i) the interests of Citi conflicting with our interests and with those of our public stockholders, including you; (ii) the sufficiency of assets and resources that we acquire from Citi in our separation from Citi and the difficulties in separating our assets and resources from Citi in our separation from Citi; (iii) loss of some of our arrangements with Citi that existed before this offering; (iv) the impact on our business resulting from competition with Citi after this offering; (v) loss of association with Citi’s strong brand and reputation; (vi) certain of our directors experiencing conflicts of interest because of their positions with Citi; (vii) the limited liability of Citi and its directors and officers for breach of fiduciary duty to us or to you; (xiii) our combined historical financial data and pro forma combined financial data do not necessarily reflect future results; (ix) charges in connection with this offering and incremental costs of operating as a stand-alone public company; (x) the allocation of liabilities between us and Citi; (xi) our exemption from certain corporate governance requirements due to our status as a “controlled company” within the meaning of the New York Stock Exchange rules; (xii) Citi potentially selling a controlling interest in our company to a third party in a private transaction; (xiii) our reliance on our operating subsidiaries to provide us with the funds that are necessary to meet our financial obligations; (xiv) our intention to not pay dividends on our common stock in the foreseeable future; (xv) the insurance laws and regulations that may delay or impede purchases of our common stock; and (xvi) immediate dilution as a result of this offering. |

| • | Risks relating to this offering, including: (i) future sales of a substantial number of shares of our common stock; (ii) the development of an active trading market for our common stock; (iii) volatility of the price and trading volume of our common stock; (iv) resources and management attention required to meet the obligations associated with being a public company; and (v) our common stock is and will be subordinate to all of our existing and future indebtedness. |

For a discussion of these and other risks, see “Risk Factors.”

Prior to this offering, all of our outstanding common stock is indirectly owned by Citi. Citi will continue to own a majority of our outstanding common stock immediately following completion of this offering and we expect will receive $ million in connection with our repayment of the full amount due to Citi under the Dividend Note using the proceeds of this offering. If the underwriters exercise the over-allotment option, Citi will also receive all of the net proceeds from such exercise. In addition, prior to this offering we have had, and after this offering we will continue to have, numerous commercial and contractual arrangements with affiliates of Citi.

Citigroup Global Markets Inc., the sole book-running manager of this offering, is a wholly owned subsidiary of Citigroup Inc. Because Citigroup Global Markets Inc. is under common control with us and the selling stockholder, and because the selling stockholder, an affiliate of Citigroup Global Markets Inc., will receive at least 5% of the proceeds of this offering, a conflict of interest under Financial Industry Regulatory Authority, Inc., or FINRA, Rule 5121 is deemed to exist. This offering will be conducted in accordance with that rule. As required by FINRA Rule 5121, has agreed to act as the “qualified independent underwriter” for this offering and has participated in the preparation of, and has exercised the usual standards of “due diligence” in respect of, this prospectus.

See “Risk Factors—Risks Relating to Our Organization and Structure,” “Use of Proceeds” and “Underwriting—Conflicts of Interest.”

8

Table of Contents

| Common stock offered by us |

shares |

| Over-allotment option offered by Citigroup Inc. |

shares |

| Common stock to be outstanding after this offering |

shares ( shares if the underwriters exercise their over-allotment option in full) |

| Voting rights |

One vote per share |

| Use of proceeds |

We estimate that the net proceeds to us from this offering will be approximately $ million, based on an assumed public offering price of $ per share (the midpoint of the price range on the front cover of this prospectus), after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use the net proceeds from this offering to repay the Dividend Note in full (plus any accrued and unpaid interest thereon). Any proceeds resulting from the exercise of the over-allotment option will be paid to Citigroup Inc., and we will receive no proceeds from the exercise of the over-allotment option. See “Use of Proceeds.” |

| Dividend policy |

We do not intend to pay dividends on our common stock. |

| New York Stock Exchange (“NYSE”) symbol |

We intend to apply to have our shares of common stock listed on the NYSE under the trading symbol “ .” |

| Risk factors |

See “Risk Factors” beginning on page 15 of this prospectus and the other information included in this prospectus for a discussion of the factors you should consider carefully before deciding to invest in shares of our common stock. |

| Controlling stockholder |

Citigroup Inc. |

Unless we specifically state otherwise, all information in this prospectus, including information regarding the number of shares of our common stock outstanding:

| • | gives effect to our Amended and Restated Certificate of Incorporation that we intend to file prior to the consummation of this offering; |

| • | assumes an initial public offering price of $ per share (the midpoint of the price range set forth on the front cover of this prospectus); and |

| • | assumes the underwriters’ option to purchase additional shares of common stock from Citi has not been exercised. |

9

Table of Contents

SUMMARY COMBINED FINANCIAL AND OTHER DATA

The following table sets forth summary combined historical financial data as of and for the six months ended June 30, 2014 and 2013 and for the years ended December 31, 2013 and 2012. The summary combined historical statement of income data for the six months ended June 30, 2014 and 2013, and the summary combined historical statement of financial position data as of June 30, 2014 presented below has been derived from our unaudited condensed combined financial statements included elsewhere in this prospectus. The summary combined historical statement of income data for the years ended December 31, 2013 and 2012 and the summary combined historical statement of financial position data as of December 31, 2013 and 2012 presented below have been derived from our audited combined financial statements included elsewhere in this prospectus.

The following table sets forth the unaudited summary pro forma combined statement of income data for the six months ended June 30, 2014 that is derived from our unaudited condensed combined financial statements included elsewhere in this prospectus and gives effect to the Transactions (as defined in “Unaudited Pro Forma Combined Financial Information”) as if each had occurred on January 1, 2013. The unaudited summary pro forma combined statement of financial position data as of June 30, 2014 is derived from our unaudited condensed combined financial statements included in this prospectus and gives effect to the Transactions as if each had occurred on June 30, 2014. The following table also sets forth unaudited summary pro forma combined statement of income data for the year ended December 31, 2013 that is derived from our audited combined financial statements included elsewhere in this prospectus and gives effect to the Transactions as if each had occurred on January 1, 2013.

The unaudited summary pro forma combined financial data below is based upon available information and assumptions that we believe are reasonable. The unaudited summary pro forma combined financial data is for illustrative and informational purposes only and is not intended to represent the actual results that would have been achieved had the Transactions each occurred on the dates indicated. The unaudited summary pro forma combined financial data should not be considered representative of our future financial condition or results of operations.

Our separation from Citi and the establishment of a fully independent capital structure will result in financial results that are materially different from those reflected in the combined historical financial data that appears in this prospectus. For an understanding of how these changes will affect our results of operations, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Our Separation from Citi” and “Unaudited Pro Forma Combined Financial Information.”

10

Table of Contents

You should read the following summary information in conjunction with the information under “Selected Combined Historical Financial Data,” “Unaudited Pro Forma Combined Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our combined financial statements and the related notes included elsewhere in this prospectus.

Condensed Combined Statements of Income Information

| Pro Forma | Historical | Pro Forma | Historical | |||||||||||||||||||||

| Six

Months Ended June 30, |

Six Months Ended June 30, |

Year Ended December 31, |

Year Ended December 31, |

|||||||||||||||||||||

| 2014 | 2014 | 2013 | 2013 | 2013 | 2012 | |||||||||||||||||||

| (in millions of dollars, except share data) | ||||||||||||||||||||||||

| Interest revenue |

$ | $ | 1,015 | $ | 986 | $ | $ | 2,019 | $ | 1,982 | ||||||||||||||

| Interest expense |

114 | 116 | 228 | 264 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net interest revenue |

901 | 870 | 1,791 | 1,718 | ||||||||||||||||||||

| Non-interest revenue |

195 | 252 | 498 | 553 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total revenue, net of interest expense |

1,096 | 1,122 | 2,289 | 2,271 | ||||||||||||||||||||

| Provision for credit losses and for benefits and claims |

294 | 352 | 701 | 850 | ||||||||||||||||||||

| Operating expenses |

355 | 378 | 743 | 790 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income from continuing operations before income taxes |

447 | 392 | 845 | 631 | ||||||||||||||||||||

| Provision for income taxes |

160 | 144 | 309 | 224 | ||||||||||||||||||||

| Net income from continuing operations |

287 | 248 | 536 | 407 | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Loss from discontinued operations, net of taxes |

— | — | — | — | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income |

$ | $ | 287 | $ | 248 | $ | $ | 536 | $ | 407 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted pro forma net income from continuing operations(1) |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

| Weighted average shares outstanding (in thousands)(2) |

||||||||||||||||||||||||

| Basic |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

| Diluted |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

| Earnings per share(2) |

||||||||||||||||||||||||

| Basic |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

| Diluted |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

11

Table of Contents

Condensed Combined Statements of Financial Position Information

| Pro Forma | Historical | |||||||||||||||

| As of June 30, |

As of June 30, |

As of December 31, |

||||||||||||||

| 2014 | 2014 | 2013 | 2012 | |||||||||||||

| (in millions of dollars) | ||||||||||||||||

| Assets |

||||||||||||||||

| Cash and cash equivalents |

$ | $ | 291 | $ | 319 | $ | 369 | |||||||||

| Investments (at fair value) |

1,504 | 1,431 | 1,507 | |||||||||||||

| Loan receivables, net of unearned revenue and deferred cost |

8,156 | 8,575 | 8,447 | |||||||||||||

| Unearned premium and claims reserves |

(408 | ) | (416 | ) | (394 | ) | ||||||||||

| Accrued interest receivable |

84 | 92 | 114 | |||||||||||||

| Allowance for loan losses |

(604 | ) | (676 | ) | (686 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net consumer finance receivables |

7,228 | 7,575 | 7,481 | |||||||||||||

| Deferred tax assets, net |

260 | 256 | 221 | |||||||||||||

| Premises and equipment, net |

19 | 21 | 28 | |||||||||||||

| Other assets |

231 | 234 | 257 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total assets |

$ | $ | 9,533 | $ | 9,836 | $ | 9,863 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Liabilities and Parent Equity |

||||||||||||||||

| Related-party debt |

$ | $ | 4,619 | $ | 5,894 | $ | 6,037 | |||||||||

| Long-term debt |

760 | — | — | |||||||||||||

| Insurance policy and claim reserves |

471 | 483 | 505 | |||||||||||||

| Accounts payable, accrued expenses and other liabilities |

463 | 612 | 795 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total liabilities |

6,313 | 6,989 | 7,337 | |||||||||||||

| Total Parent equity |

3,220 | 2,847 | 2,526 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total liabilities and Parent equity |

$ | $ | 9,533 | $ | 9,836 | $ | 9,863 | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

12

Table of Contents

Other Financial and Statistical Data

| Pro Forma | Historical | Pro Forma | Historical | |||||||||||||||||||||

| At and for the Six Months Ended June 30, |

At and for the Six Months Ended June 30, |

At and for the Year Ended December 31, |

At and for the Years Ended December 31, |

|||||||||||||||||||||

| 2014 | 2014 | 2013 | 2013 | 2013 | 2012 | |||||||||||||||||||

| (in millions of dollars, except ratio, share and other data) | ||||||||||||||||||||||||

| Financial Position Data |

||||||||||||||||||||||||

| Personal loan receivables |

$ | $ | 8,156 | $ | 7,792 | $ | $ | 8,112 | $ | 7,890 | ||||||||||||||

| Average personal loan receivables |

8,023 | 7,719 | 7,837 | 7,836 | ||||||||||||||||||||

| Total assets |

9,533 | 9,762 | 9,836 | 9,863 | ||||||||||||||||||||

| Average assets(3) |

9,685 | 9,813 | 9,850 | 10,231 | ||||||||||||||||||||

| Total Parent equity |

3,220 | 2,742 | 2,847 | 2,526 | ||||||||||||||||||||

| Average equity(3) |

3,034 | 2,634 | 2,687 | 2,512 | ||||||||||||||||||||

| Equity to assets(4) |

33.78 | % | 28.09 | % | 28.94 | % | 25.61 | % | ||||||||||||||||

| Debt to equity(5) |

1.67x | 2.04x | 2.07x | 2.39x | ||||||||||||||||||||

| Selected Performance Data |

||||||||||||||||||||||||

| Net income |

287 | 248 | 536 | 407 | ||||||||||||||||||||

| Net interest margin |

901 | 870 | 1,791 | 1,718 | ||||||||||||||||||||

| Efficiency ratio(6) |

32.39 | % | 33.69 | % | 32.46 | % | 34.79 | % | ||||||||||||||||

| Personal loan performance |

||||||||||||||||||||||||

| Loan yield(7) |

24.75 | % | 24.04 | % | 24.13 | % | 23.38 | % | ||||||||||||||||

| Risk-adjusted yield(8) |

18.29 | % | 17.11 | % | 17.83 | % | 17.14 | % | ||||||||||||||||

| Net charge offs |

6.46 | % | 6.92 | % | 6.30 | % | 6.24 | % | ||||||||||||||||

| 30+ days past due as a % of personal loan receivables, end of period |

3.78 | % | 3.44 | % | 4.10 | % | 4.05 | % | ||||||||||||||||

| 90+ days past due as a % of personal loan receivables, end of period |

2.12 | % | 2.00 | % | 2.42 | % | 2.42 | % | ||||||||||||||||

| Return on assets(9) |

5.98 | % | 5.10 | % | 5.44 | % | 3.98 | % | ||||||||||||||||

| Return on equity(10) |

19.08 | % | 18.99 | % | 19.95 | % | 16.20 | % | ||||||||||||||||

| Adjusted pro forma net income from continuing operations(1)(11) |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

| Adjusted pro forma return on assets(1)(11)(12) |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

| Adjusted pro forma return on equity(1)(11)(13) |

N/A | N/A | N/A | N/A | ||||||||||||||||||||

| Other Data |

||||||||||||||||||||||||

| Active personal loan customer accounts |

1,318,678 | 1,321,089 | 1,343,538 | 1,365,986 | ||||||||||||||||||||

| Number of branches |

1,141 | 1,158 | 1,155 | 1,222 | ||||||||||||||||||||

| (1) | We present Adjusted pro forma net income from continuing operations as a supplemental measure of our performance. This measure provides us and other interested third parties a basis to better understand our ongoing operating results on a consistent basis. We define Adjusted pro forma net income from continuing operations as pro forma net income from continuing operations giving effect to the Transactions (as defined in “Unaudited Pro Forma Combined Financial Information”) adjusted for our 2014 exit from the real estate business, as if each of the Transactions and our 2014 exit from the real estate business had occurred on January 1, 2013. We refer to (i) the transfer of our real estate portfolio to an affiliate effective January 1, 2014 and (ii) the transfer of our servicing portfolio to an affiliate on January 6, 2014 collectively as our 2014 exit from the real estate business. Adjusted pro forma net income from continuing operations should not be considered in isolation or as a substitute for net income or other income statement data prepared in accordance with GAAP. Our presentation of Adjusted pro forma net income from continuing operations below should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. The following table provides the reconciliation of our Pro forma net income from continuing operations under “Unaudited Pro Forma Combined Financial Information” to Adjusted pro forma net income from continuing operations for the periods presented: |

| Pro Forma | ||||||||

| Six Months

Ended June 30, 2014 |

Year Ended December 31, 2013 |

|||||||

| (unaudited) | ||||||||

| (in millions of dollars) | ||||||||

| Pro forma net income from continuing operations |

$ | $ | ||||||

| Adjustments: |

||||||||

| Transfer of real estate portfolio |

||||||||

| Transfer of real estate servicing portfolio |

||||||||

|

|

|

|

|

|||||

| Adjusted pro forma net income from continuing operations |

$ | $ | ||||||

|

|

|

|

|

|||||

13

Table of Contents

| (2) | Weighted average shares outstanding gives effect to our Amended and Restated Certificate of Incorporation that we intend to file prior to the consummation of this offering. |

| (3) | Average pro forma financial data gives effect to the Transactions as if they had occurred on January 1, 2013. |

| (4) | Equity to assets is the Total Parent equity divided by Total assets. |

| (5) | Debt to equity is the sum of Related-party debt, Short-term borrowings and Long-term debt divided by Total Parent equity. |

| (6) | Efficiency ratio is Operating expenses divided by Total revenue, net of interest expense. |

| (7) | Loan yield is personal loan finance charges divided by Average personal loan receivables. For six-month amounts, personal loan finance charges for the six months ended June 30, 2014 and 2013, respectively, are annualized by dividing the personal loan finance charges for such periods by the number of days elapsed in the year, and then multiplying by the number of days in the year. |

| (8) | Risk-adjusted yield is the Loan yield less Net charge offs. |

| (9) | Return on assets is Net income divided by Average total assets. For six-month amounts, Net income for the six months ended June 30, 2014 and 2013, respectively, is annualized by dividing Net income for such periods by the number of days elapsed in the year, and then multiplying by the number of days in the year. |

| (10) | Return on equity is Net income divided by Average equity. For six-month amounts, Net income for the six months ended June 30, 2014 and 2013, respectively, is annualized by dividing Net income for such periods by the number of days elapsed in the year, and then multiplying by the number of days in the year. |

| (11) | Adjusted pro forma combined financial data give effect to the Transactions and our 2014 exit from the real estate business as if each of the Transactions and the further adjustments had occurred on January 1, 2013 for amounts calculated using average financial position data. |

| (12) | Adjusted pro forma return on assets is defined as the ratio of Adjusted pro forma net income from continuing operations to Adjusted average pro forma total assets. We define Adjusted average pro forma total assets as the average pro forma total assets, adjusted for our 2014 exit from the real estate business as if each of the Transactions and the further adjustments had occurred on January 1, 2013. The following table provides the reconciliation of Average pro forma total assets to Adjusted average pro forma total assets for the periods presented. See also “Unaudited Pro Forma Combined Financial Information” for the pro forma combined statements of financial position information. |

| Pro Forma | ||||||||

| Six Months

Ended June 30, 2014 |

Year Ended December 31, 2013 |

|||||||

| (unaudited) | ||||||||

| (in millions of dollars) | ||||||||

| Average pro forma total assets |

$ | $ | ||||||

| Adjustment: |

||||||||

| Transfer of real estate portfolio |

||||||||

|

|

|

|

|

|||||

| Adjusted average pro forma total assets |

$ | $ | ||||||

|

|

|

|

|

|||||

| (13) | Adjusted pro forma return on equity is defined as the ratio of Adjusted pro forma net income from continuing operations to pro forma equity. |

14

Table of Contents

Investing in our common stock involves substantial risks. You should carefully consider the following risk factors that may affect our business, future operating results and financial condition, as well as the other information set forth in this prospectus before making a decision to invest in our common stock. If any of the following risks actually occurs, our business, financial condition or results of operations would likely be materially adversely affected. In such case, the trading price of our common stock would likely decline, and you may lose all or part of your investment.

Risks Relating to Our Business

An inability to access adequate sources of liquidity, or to do so on favorable terms, may adversely affect our capital structure and our ability to fund operational requirements and satisfy financial obligations.

We have historically funded our operations through cash from our operations and funding provided by Citi. We intend to establish a fully independent capital structure and finance our liquidity needs through various sources of third-party debt. In April 2014 and July 2014 we successfully executed two securitization transactions. As we establish an independent capital structure, existing funding from Citi in some cases may be replaced by higher-cost funding provided by third-party sources.

While financial market conditions have stabilized and, in many cases, improved since the financial crisis that began in 2008, there can be no assurance that significant disruptions, uncertainties and volatility will not occur in the future. If we do not have sufficient liquidity because we are unable to obtain access to credit or complete additional securitizations on favorable terms and in a timely manner, we may not be able to meet our obligations. If we maintain or are required to maintain too much liquidity, our business, results of operations and financial condition could be adversely affected.

The availability of financing will depend on a variety of factors such as financial market conditions generally, including the availability of credit to the financial services industry, our performance and credit ratings and the performance of our securitized portfolios. Disruptions, uncertainty or volatility in the capital or credit markets may limit our ability to obtain additional financing or refinance maturing liabilities on desired terms in a timely manner or at all. It may also be more difficult or costly for us to obtain funds when we are no longer a wholly owned subsidiary of Citi. As a result, we may be forced to delay obtaining funding or be forced to issue or raise funding on undesirable terms, which could significantly reduce our financial flexibility and cause us to contract or restrict our business growth, all of which could have a material adverse effect on our results of operations and financial conditions.

There can be no assurances that we will be able to complete additional securitizations. The extent to which we will securitize our loans in the future will depend in part upon the conditions in the securities markets in general and the consumer loan asset-backed securities market in particular, the overall credit quality of our loans, the conformity of the loans and our securitization program to rating agency requirements, the costs of securitizing our loans and the legal, regulatory, accounting and tax requirements governing securitization transactions. In the event we are unable to refinance existing asset-backed securities with new securities or there are structural and regulatory constraints on our ability to refinance these asset-backed securities with other funding, we would be required to rely on different sources for funding. A prolonged inability to securitize our loans or to refinance our asset-backed securities would have a material adverse effect on our business, liquidity, cost of funds and financial condition. In addition, following completion of this offering, it may be more difficult for us to securitize our loans if investors view us as a weaker sponsor once we are no longer wholly owned by Citi. To compensate, our future issuances of asset-backed securities may need to provide for a higher interest rate or provide additional credit enhancements. These factors may increase the costs of securitizing our loans relative to our historical costs.

15

Table of Contents

Macroeconomic conditions could have a material adverse effect on our business, our customers, results of operations, financial condition and stock price.

Key macroeconomic conditions historically have affected our business, our results of operations and financial condition and our customers and are likely to affect them in the future. While certain economic conditions in the United States have shown signs of improvement, economic growth has been slow and uneven as consumers continue to be affected by high unemployment rates, slowly recovering housing values and continuing concerns about the level of U.S. government debt and fiscal actions that may be taken to address this. A prolonged period of slow economic growth, significant deterioration in economic conditions or elevated unemployment levels would likely affect the ability of customers to pay amounts owed to us, and could have a material adverse effect on our business, results of operations and financial condition.

A substantial majority of our customers are subprime or non-prime borrowers, each of which has lower collection rates and is subject to higher loss rates than prime borrowers. Subprime and non-prime borrowers have historically been, and may in the future become, more likely to be affected, or more severely affected, by adverse macroeconomic conditions, particularly unemployment. If our borrowers default under an unsecured loan, we will bear a risk of loss of principal and if under a secured loan, we will bear this risk to the extent of any deficiency between the value of the collateral and the outstanding principal and accrued but unpaid interest of the loan, which could adversely affect our cash flow from operations. Additionally, under certain circumstances, we may be required to repurchase those loans we have securitized. See “—If our loans fail to meet certain criteria or characteristics or under other circumstances, we may be required to repurchase the loans that we sell or securitize, which could adversely affect our results of operations, financial condition and liquidity” below. The cost to service our loans may also increase without a corresponding increase in our interest income.

Macroeconomic conditions may also cause net income to fluctuate and diverge from expectations of securities analysts and investors, who may have differing assumptions regarding the impact of these conditions on our business, and this may adversely impact the trading price of our common stock.

If aspects of our business, including the quality of our borrowers, are significantly affected by economic changes or any other conditions in the future, we cannot be certain that our policies and procedures for underwriting, processing and servicing loans will adequately adapt to such changes. If we fail to adapt to changing economic conditions or other factors, or if such changes affect our borrowers’ capacity to repay their loans, our results of operations, financial condition and liquidity would be materially adversely affected.

Our risk management processes and procedures may not be effective in mitigating our risks.

We have established processes and procedures intended to identify, measure, monitor and control the types of risk to which we are subject, including credit risk, market risk, liquidity risk, strategic risk and operational risk. Credit risk is the risk of loss that arises when a borrower fails to meet the terms of a loan. Market risk is the risk of loss due to changes in external market factors such as interest rates and prepayment rates. Liquidity risk is the risk that a company’s financial condition or overall safety and soundness are adversely affected by an inability, or perceived inability, to meet funding obligations and support business growth. Strategic risk is the risk from changes in the business environment, improper implementation of decisions or inadequate responsiveness to changes in the business environment. Operational risk is the risk of loss arising from inadequate or failed processes, people or systems, external events (for example, natural disasters) or compliance, reputational or legal matters and includes those risks as they relate directly to our company as well as to third parties with whom we contract or otherwise do business. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Quantitative and Qualitative Disclosure about Market Risk,” “Business—Credit” and “Business—Operational Controls” for additional information on the types of risks that affect our business.

16

Table of Contents

We seek to monitor and control our risk exposure through a framework that includes our risk appetite, enterprise risk assessment process, risk policies, procedures and controls, reporting requirements, credit risk culture and governance structure. Management of our risks in some cases depends upon the use of analytical and/or forecasting models, including the proprietary scoring we use to supplement FICO scores when evaluating potential borrowers. If the models that we use to manage risk are ineffective at predicting future losses or are otherwise inadequate, we may incur unexpected losses or otherwise be adversely affected. In addition, the information we use in managing our credit and other risk may be inaccurate or incomplete as a result of error or fraud, both of which may be difficult to detect and avoid. There may also be risks that exist, or that develop in the future, that we have not appropriately anticipated, identified or mitigated including when processes are changed or new products and services are introduced. If our risk management framework does not effectively identify and control our risks, we could suffer unexpected losses or be adversely affected, and that could have a material adverse effect on our business, results of operations and financial condition.

We rely extensively on models to manage many aspects of our business, and if they are not accurate or are misinterpreted, it could have a material adverse effect on our business, results of operations and financial condition.

We rely extensively on models to manage many aspects of our business, including liquidity and capital planning, customer selection, credit and other risk management, pricing, reserving and collections management. Our models, including the proprietary scoring we use to supplement FICO scores when evaluating potential borrowers, may prove in practice to be less predictive than we expect for a variety of reasons, including as a result of errors in constructing, interpreting or using the models or the use of inaccurate assumptions (including failures to update assumptions appropriately or in a timely manner). Our assumptions may be inaccurate for many reasons including that they often involve matters that are inherently difficult to predict and beyond our control (for example, macroeconomic conditions and their impact on customer behavior) and they often involve complex interactions between a number of dependent and independent variables, factors and other assumptions. The errors or inaccuracies in our models may be material and could lead us to make incorrect or sub-optimal decisions in managing our business, and this could have a material adverse effect on our business, results of operations and financial condition.

Our business depends on our ability to successfully manage our credit risk, and failing to do so may result in higher charge-off rates.

Our success depends on our ability to manage our credit risk. The models and approaches we use to manage our credit risk may not accurately predict future charge offs for various reasons discussed in the preceding risk factor.

We remain subject to conditions in the consumer finance environment, and our ability to manage credit risk and avoid higher charge-off rates also may be adversely affected by economic conditions that may be difficult to predict, such as the recent financial crisis. Although delinquencies and charge offs remained stable in 2012 and 2013, they both may increase in the future and are likely to increase materially if economic conditions deteriorate. There can be no assurance that our credit underwriting and risk management strategies will enable us to avoid higher charge-off rates, or that our allowance for loan losses will be sufficient to cover actual losses.

A customer’s ability to repay us can be negatively impacted by increases in their payment obligations to other lenders under mortgage, credit card and other loans. In addition, a customer’s ability to repay us can be negatively impacted by a restricted availability of credit to consumers generally, including reduced and closed lines of credit. Customers with insufficient cash flow to fund daily living expenses and lack of access to other sources of credit may be more likely to default on their payment obligations to us, resulting in higher losses in our portfolio. Our collection operations may not compete effectively to secure more of customers’ diminished cash flow than other competing creditors.

17

Table of Contents

Our ability to manage credit risk also may be adversely affected by legal or regulatory changes (such as bankruptcy laws and collection regulations), competitors’ actions and consumer behavior, as well as inadequate collection operations staffing, techniques, models and performance of vendors such as collection agencies.

Our allowance for loan losses may prove to be insufficient to cover losses on our loans.

We maintain an allowance for loan losses (a reserve established through a provision for losses charged to expense) that we believe is adequate to cover losses inherent in our existing portfolio. The process for establishing an allowance for loan losses is critical to our results of operations and financial condition and requires complex models and judgments, including forecasts of economic conditions. Changes in economic conditions affecting borrowers, new information regarding our loans and other factors, both within and outside of our control, may require an increase in the allowance for loan losses. We may underestimate or miscalculate our incurred losses and fail to maintain an allowance for loan losses sufficient to account for these losses. In cases where we modify a loan, if the modified loans do not perform as anticipated, we may be required to establish additional allowances on these loans.

Moreover, our regulators and independent auditors, as part of their supervisory or review and independent audit functions, periodically review our methodology, models and the underlying assumptions, estimates and assessments we use for calculating, and the adequacy of, our allowance for loan losses. For more information relating to the findings of our independent auditors, see “—If we are unable to achieve and maintain effective internal control over financial reporting, this could have a material adverse effect on our business” below. Our regulators and independent auditors, based on their judgment, may conclude that we should modify our methodology or models, increase our allowance for loan losses and/or recognize further losses.

We periodically review and update our methodology, models and the underlying assumptions, estimates and assessments we use to establish our allowance for loan losses to reflect our view of current conditions. We cannot assure you that our loan loss reserves will be sufficient to cover actual losses. Future increases in the allowance for loan losses or recognized losses (as a result of any internal review or update, regulatory guidance or otherwise) will result in a decrease in net income and capital and could have a material adverse effect on our business, results of operations and financial condition.

If we are unable to achieve and maintain effective internal control over financial reporting, this could have a material adverse effect on our business.

Effective internal controls over financial reporting are necessary for us to provide reliable financial reports and, together with adequate disclosure controls and procedures, are designed to prevent fraud or material error. Any failure to implement current internal controls or required new or improved controls, or difficulties encountered in their implementation could cause us to fail to meet our reporting obligations. Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, requires management of public companies to develop and implement internal controls over financial reporting and evaluate the effectiveness thereof. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of our financial statements will not be prevented or detected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control over financial reporting that is less severe than a material weakness, yet important enough to merit attention by those responsible for oversight of our financial reporting.

In our 2011 and 2012 audits, our independent auditors identified a material weakness in the internal controls related to the methodology, accounting and management of loan loss reserves. In particular, the material weakness related to the lack of review over reserve models that showed data input errors, incorrect application of updated methodologies, inaccurate forecasting and calculation errors. The 2012 audit also identified a significant deficiency in the internal controls related to intercompany accounts not being properly reviewed and reconciled, resulting in a single accounting error where retained earnings were unintentionally recorded as a liability when OneMain and CitiFinancial Servicing were a combined entity under CFNA in 2011.

18

Table of Contents

In our 2013 audit, our independent auditors determined that progress had been made to enhance our controls and as a result, the material weakness relating to the loan loss reserves from the 2012 audit was reduced to a significant deficiency at December 31, 2013. The significant deficiency related to the documented level of precision in our process used to calculate the allowance for loan losses. We are taking action to remediate this issue and improve our loan loss methodologies and procedures, but we cannot assure you that our management of our loan loss reserves will continue to improve.

The discovery of a material weakness and the disclosure of that fact, even if quickly remedied, could reduce the market value of shares of our common stock. Additionally, the existence of any material weakness or significant deficiency requires management to devote significant time and incur significant expense to remediate any such material weaknesses or significant deficiency and management may not be able to remediate any such material weaknesses or significant deficiency in a timely manner. Undetected material weaknesses in our internal controls could lead to financial statement restatements, which could have a material adverse effect on our business, financial condition and results of operation.

Our historical charge-off rates may not be predictive of our future charge-off rates.

Our historical net charge-off and delinquency rates may not be predictive of our future net charge-off and delinquency rates. Prior to 2011, we were part of a larger business within Citi known as CFNA. CitiFinancial Servicing, a business designed to support certain customers and loans that would benefit from expanded support, including loan modifications or restructurings rather than originate loans, was split from us and is reflected in discontinued operations in our combined financial statements for the year ended December 31, 2011. Therefore, our financial results do not reflect the CitiFinancial Servicing charge-off rates.