Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - PERCEPTRON INC/MI | Financial_Report.xls |

| EX-23.1 - EX-23.1 - PERCEPTRON INC/MI | prcp-20140630ex2311c2736.htm |

| EX-32.2 - EX-32.2 - PERCEPTRON INC/MI | prcp-20140630ex3224ae1c7.htm |

| EX-31.2 - EX-31.2 - PERCEPTRON INC/MI | prcp-20140630ex312d31f00.htm |

| EX-23.2 - EX-23.2 - PERCEPTRON INC/MI | prcp-20140630ex2328765d9.htm |

| EX-32.1 - EX-32.1 - PERCEPTRON INC/MI | prcp-20140630ex32101e4f3.htm |

| EX-31.1 - EX-31.1 - PERCEPTRON INC/MI | prcp-20140630ex311cecef3.htm |

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2014OR

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________ to ________.

|

Commission File Number: 0-20206 |

||

|

PERCEPTRON, INC. |

||

|

(Exact Name of Registrant as Specified in Its Charter) |

||

|

Michigan |

|

38-2381442 |

|

(State or Other Jurisdiction of |

|

(I.R.S. Employer Identification No.) |

|

Incorporation or Organization) |

|

|

|

47827 Halyard Drive |

||

|

Plymouth, Michigan 48170-2461 |

||

|

(Address of Principal Executive Offices) |

||

|

(734) 414-6100 |

||

|

(Registrant’s telephone number, including area code) |

||

|

|

|

|

|

|

|

|

|

Securities registered pursuant to section 12(b) of the Act: |

||||

|

Title of Each Class Common Stock, $0.01 par value |

Name of Each Exchange on Which Registered |

|||

|

Rights to Purchase Preferred Stock |

The NASDAQ Stock Market LLC |

|||

|

(NASDAQ Global Market) |

||||

|

Securities registered pursuant to section 12(g) of the Act: None |

||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

Yes ☐ |

|

No ☒ |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

|

Yes ☐ |

|

No ☒ |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

Yes ☒ |

|

No ☐ |

Indicate by check mark whether the registrant has submitted electronically and posted on its website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

|

Yes ☒ |

|

No ☐ |

Indicate by check mark if disclosure of delinquent filers pursuant to item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer”, “accelerated filer”, and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer ☐ Accelerated Filer ☒ Non-Accelerated Filer ☐ Smaller Reporting Company ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

Yes ☐ |

|

No ☒ |

The aggregate market value of the voting stock held as of the registrant’s most recently completed second fiscal quarter by non-affiliates of the registrant, based upon the closing sale price of the Common Stock on December 31, 2013, as reported by the NASDAQ Global Market, was approximately $119,100,000 (assuming, but not admitting for any purpose, that all directors and executive officers of the registrant are affiliates).

The number of shares of Common Stock, $0.01 par value, issued and outstanding as of September 8, 2014, was 9,151,956.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following document, to the extent specified in this report, are incorporated by reference in Part III of this report:

|

Document |

|

Incorporated by reference in: |

|

Proxy Statement for 2014 |

|

|

|

Annual Meeting of Shareholders |

|

Part III, Items 10-14 |

1

PART I

ITEM 1:BUSINESS

General

Perceptron, Inc. (“Perceptron” or the “Company”) develops, produces and sells non-contact measurement and inspection solutions for industrial applications. Perceptron products provide solutions for manufacturing process control as well as sensor and software technologies for non-contact measurement, scanning and inspection applications. These products are used by the Company’s customers throughout the world to help manage their complex manufacturing processes to improve quality, shorten product launch times, reduce overall manufacturing costs and for digitizing and reverse engineering applications. The Company services multiple markets, with the largest being the automotive industry. The Company’s primary operations are in North America, Europe and Asia.

The Company’s products are categorized as follows:

In Process and Offline Measurement Solutions. Sales of these products involve the development, manufacture and installation of:

|

· |

In Process fixed and robot-mounted laser-based, non-contact dimensional gauging systems used in original equipment manufacturing plants and component supplier plants; and |

|

· |

In Process laser-based, non-contact systems that guide robots in a variety of automated assembly applications. |

|

· |

Offline fixed and robot-mounted laser-based, non-contact dimensional gauging systems used in original equipment manufacturing plants and component supplier plants. |

3D Scanning Products. Perceptron develops, manufactures and markets laser-based sensors and software used:

|

· |

As the critical sensing component on automotive assembly plant wheel-alignment machines, |

|

· |

As the critical component for 3-dimensional scanning on coordinate measurement machines (“CMM”) for the reverse engineering and inspection markets; and |

|

· |

As the critical component for 3-dimensional scanning on portable CMMs for the reverse engineering and inspection markets. |

Value Added Services. Perceptron also offers the following value added services:

|

· |

Training |

|

· |

Field Service |

|

· |

Launch Support Services |

|

· |

Consulting Services |

|

· |

Maintenance Agreements; and |

|

· |

Repairs. |

On August 30, 2012, the Company sold substantially all of the assets of its Commercial Products Business Unit (“CBU”). CBU financial information is presented as a discontinued operation in the financial statements included in this Form 10-K for fiscal year 2014 and prior year results are presented on a comparable basis.

The Company was incorporated in Michigan in 1981 and is headquartered at 47827 Halyard Drive, Plymouth, Michigan 48170-2461, (734) 414-6100. The Company also has operations in Munich, Germany; Voisins le Bretonneux, France; Barcelona, Spain; Sao Paulo, Brazil; Tokyo, Japan; Shanghai, China; Singapore and Chennai, India.

Markets

The Company primarily services the automotive manufacturing market but the Company’s technology is also applicable to a variety of other manufacturing industries. The Company has product offerings encompassing many manufacturing processes, including complex part assembly, automotive body construction, construction of automotive closures, closure installation and fitting, glass installation, adhesive and sealer application and laser cutting.

2

Products and Applications

In Process and Offline Measurement Solutions

All of the measurement solutions are based on Perceptron’s sensors and software. Solutions are developed by the Company’s engineers applying Helix® and TriCam® sensors with Vector software. Measurement solutions in fiscal 2014, 2013, and 2012 represented 85%, 84% and 80% of total sales, respectively.

AutoGauge®: These systems are used in the assembly and fabrication plants of many of the world’s leading automotive manufacturers to contain, correct and control the quality of complex assemblies. AutoGauge® systems are placed directly in the manufacturing line or near the line to automatically measure critical dimensional characteristics of parts using non-contact, laser triangulation sensors. AutoGauge® can be installed as a “multi-sensor system” with fixed-mounted sensors, as a “robotic system” utilizing only robot-mounted sensors, or as a “hybrid system” involving both fixed-mounted sensors and robot-mounted sensors. This ability provides manufacturers with the flexibility to measure multiple part types on a single manufacturing line while maintaining high-speed production rates.

AutoGauge® Plus: This system offers inline freeform surface scanning and discrete feature measurement in one solution. Users of AutoGauge® Plus can create a fully-customized gauging solution that automatically converts from collecting precise, discrete measurements to capturing complete 3D point clouds. AutoGauge® Plus delivers both the speed of in-line measurement and the data density of automated scanning.

AutoFit®: These systems are used in automotive manufacturing plants to contain, correct and control the fit of exterior body panels. The system automatically measures, records and displays the gap and flushness of parts most visible to the automobile consumer such as gaps between front and rear doors, hoods and fenders, and deck lids and rear quarter panels. The Company’s laser triangulation sensors have been enhanced to enable gap and flushness to be measured in multiple parts of the manufacturing process: in the body shop during assembly of non-painted vehicles, and in the final assembly area after the vehicle has been painted. AutoFit® has the ability to measure vehicles while in motion along the assembly line or in a stationary position.

AutoScan®: These systems provide a fast, non-contact method of gathering data for the analysis of the surface contour of a part or product such as automotive closure panels including doors, deck lids, and hoods. These systems use robot-mounted sensors specifically designed to “scan” a part as the robot moves throughout its path. The AutoScan® system collects the “point cloud data” required for contour analysis and dimensional feature extraction. This allows the part’s shape to be automatically scanned and compared to a computer-generated design and to report specific measurements on the part.

AutoGuide®: These robot guidance systems were developed in response to the increasing use of robots for flexible, automated assembly applications. These systems utilize Perceptron sensors and measurement technology to improve the performance of robotic assembly operations. AutoGuide® systems calculate the difference between theoretical and actual relationships of a robot and the part being assembled and send compensation data, in six degrees of freedom, to the robot. Robotic applications supported by AutoGuide® include windshield insertion, roof loading, hinge mounting, door attachment, sealant application and many others.

Helix®: Is an innovative and versatile 3D metrology solution that enables manufacturers to perform their most challenging measurement tasks with greater ease and precision. Helix® solutions offer Intelligent Illumination® allowing the user to choose the quantity, density and orientation of the sensor's laser lines on an individual inspection point level without moving the sensor. By customizing the sensor's laser lines through a simple user interface, image acquisition is optimized on a feature-by-feature basis. The user can configure tightly spaced laser lines for small, complex features, increase the number of laser lines to robustly measure challenging materials, and alter the orientation of the laser lines to accommodate the differences between multiple parts manufactured on the same assembly line.

3D Scanning Products

3D Scanning Products in fiscal 2014, 2013, and 2012 represented 10%, 11% and 14% of total sales, respectively.

ScanWorks®: The Company provides ScanWorks® products to a variety of markets through third party original equipment manufacturers and value-added resellers. These products target the digitizing, reverse engineering, and inspection markets. ScanWorks® is a hardware/software component set that allows customers to add digitizing capabilities to their machines or systems. The use of the ScanWorks® software and the Contour Probe® sensor enables technicians to collect, display, manipulate and export large sets of “point cloud data” from optical tracking devices, portable CMMs or CMMs. The majority of ScanWorks® sales occur outside of the automotive industry.

3

ScanWorks®xyz: This product is a 3D scanning solution designed for retrofitting 3-axis machines. It features all of the components required to add non-contact scanning capability to 1-, 2- or 3-axis CMMs, computer numerical controls, and layout machines in a cost-effective manner. The retrofitting of these machines with ScanWorks®xyz allows end users to repurpose their existing equipment and increase their throughput by scanning more parts in less time.

WheelWorks®: WheelWorks® software and sensors offer a fast, accurate, non-contact method of measuring wheel position for use in automated or manual wheel alignment machines in automotive assembly plants. The Company supplies sensors and software to a number of wheel alignment equipment manufacturers in Europe, Asia and North America who in turn sell alignment systems to automotive manufacturers.

Value Added Services

Value Added Services: Value Added Services sales in fiscal 2014, 2013, and 2012 represented 5%, 5% and 6% of total sales, respectively. Value Added Services include training, field service, launch support services, consulting services, maintenance agreements and repairs.

Sales and Marketing

The Company markets its products directly to end user customers, and through manufacturing line builders, system integrators, value-added resellers and original equipment manufacturers.

The Company’s sales efforts are led by account managers who develop a close consultative selling relationship with the Company’s customers. The Company’s principal customers have historically been automotive manufacturing companies that the Company either sells to directly or through manufacturing line builders, system integrators or assembly equipment manufacturers. The Company’s products are typically purchased for installation in connection with retooling programs undertaken by these companies. Because sales are dependent on the timing of customers’ retooling programs, sales by customer vary significantly from year to year, as do the Company’s largest customers. For the fiscal years 2014, 2013 and 2012, approximately 43%, 46% and 51%, respectively, of net sales were derived from the Company’s four largest automotive end user customers. The Company also sells to manufacturing line builders, system integrators or original equipment manufacturers, who in turn sell to the Company’s automotive customers. For the fiscal years 2014, 2013 and 2012, approximately 16%, 7% and 13%, respectively, of net sales were to manufacturing line builders, system integrators and original equipment manufacturers for the benefit of the same four largest automotive end user customers in each respective year. During the fiscal year ended June 30, 2014, direct sales to Volkswagen Group accounted for approximately 30% of the Company’s total net sales. At June 30, 2014, accounts receivable from Volkswagen Group totaled approximately $4.7 million.

Manufacturing and Suppliers

The Company’s manufacturing operations consist primarily of pre- and final assembly of hardware components and the testing and integration of the Company’s software with the hardware components. The Company builds its products from a combination of commercially available parts and uniquely designed parts. The components are primarily manufactured by third parties. Individual components such as printed circuit boards are manufactured by third parties according to the Company’s designs. The Company believes a low level of vertical integration gives it significant manufacturing flexibility and minimizes total product costs.

The Company purchases certain component parts and assemblies from single source suppliers. With respect to most of its components, the Company believes that alternative suppliers are readily available. Component supply shortages in certain industries, including the electronics industry, have occurred in the past and are possible in the future due to imbalances in supply and demand. The Company uses global purchasing sources to minimize the risk of part shortages. The Company has not experienced significant component supply shortages from single source suppliers in recent years. Significant delays or interruptions in the delivery of components, assemblies or products by suppliers, or difficulties or delays in shifting manufacturing capacity to new suppliers, could have a material adverse effect on the Company.

International Operations

Europe: The Company’s European operations contributed approximately 47%, 43% and 32%, of the Company’s net sales during the fiscal years ended June 30, 2014, 2013, and 2012, respectively. The Company’s wholly-owned subsidiary, Perceptron Europe B.V. (“Perceptron B.V.”), formed in The Netherlands, holds a 100% equity interest in Perceptron (Europe) GmbH (“Perceptron GmbH”). Perceptron GmbH is located in Munich, Germany and is the operational headquarters for the European market. Perceptron GmbH holds a 100% interest in Perceptron E.U.R.L. located in Voisins le Bretonneux, France and a 100% interest in Perceptron Iberica SL located in Barcelona, Spain. At June 30, 2014, the Company employed 71 people in its European operations.

4

Asia: The Company’s Asian operations contributed approximately 23%, 21% and 22% of the Company’s net sales during the fiscal years ended June 30, 2014, 2013, and 2012, respectively. The Company operates direct sales, application and support offices in Tokyo, Japan; Shanghai, China; Singapore; and Chennai, India to service customers in Asia. At June 30, 2014, the Company employed 41 people in its Asian operations.

South America: The Company has a direct sales, application and support office in Sao Paulo, Brazil to service customers in South America. At June 30, 2014, the Company employed 5 people in its Brazilian operations.

The Company’s foreign operations are subject to certain risks typically encountered in such operations, including fluctuations in foreign currency exchange rates and controls, expropriation and other economic and local policies of foreign governments, and the laws and policies of the U.S. and local governments affecting foreign trade and investment. For information regarding net sales and identifiable assets of the Company’s foreign operations, see Note 12 of the Notes to the Consolidated Financial Statements, “Segment and Geographic Information”, included in item 8 of this report.

Competition

The Company believes that its products provide the best and most complete solutions for its customers in terms of system capabilities, levels of support, and competitive pricing for the value provided, which it believes are the principal competitive factors in its markets. The Company also believes it is further along in the development of its technology for certain of its products than any of its competition.

There are a number of companies that sell similar and/or alternative technologies and methods into the same markets and regions as the Company. The Company believes that there may be other entities, some of which may be larger and have greater resources than the Company, that could develop technology and products, which could prove to be competitive with those of the Company. The Company also believes that certain existing or potential customers may be capable of internally developing their own technology. In addition, certain automotive original equipment manufacturers have not yet adopted in-line dimensional metrology into their assembly process and use a combination of hand-held gauges and off-line sampling of parts to control process variation in place of Perceptron’s technology. The Company believes these original equipment manufacturers represent an opportunity for further penetration and growth in the automotive industry. See Item 1A: “Risk Factors” titled “There are a number of companies offering competitive products in our markets, or developing products to compete with our products, which could result in a reduction in our revenues through lost sales or a reduction in prices”.

Backlog

As of June 30, 2014, the Company had a backlog of $39.3 million, compared to $30.4 million at June 30, 2013. Most of the backlog is subject to cancellation by the customer with penalty provisions. The level of order backlog at any particular time is not necessarily indicative of the future operating performance of the Company. The Company expects to be able to fill substantially all of the orders in its backlog by June 30, 2015.

Research and Development

In fiscal year 2014, research and development focused primarily on the Company’s innovative Helix® 3D metrology solution. Helix® solutions offer Intelligent Illumination®, a patented breakthrough that allows users to control the sensor's calibrated light source. By customizing the quantity, density, and orientation of the sensor's laser lines through a simple user interface, image acquisition is optimized on a feature-by-feature basis. The user can configure tightly spaced laser lines for small, complex features, increase the number of laser lines to robustly measure challenging materials, and alter the orientation of the laser lines to accommodate the differences between multiple parts manufactured on the same assembly line. That customization ability translates directly into better measurements, better information and better process control decisions. Helix® sensors offer an expansive measurement volume. A large measurement volume provides customers with more measurement points using fewer sensors than existing solutions. Helix® is expected, over time, to replace all of the Company’s current Measurement Solutions beginning with AutoGauge®.

As of June 30, 2014, 41 persons employed by the Company were focused primarily on research, development and engineering. For the fiscal years ended June 30, 2014, 2013 and 2012, the Company’s research, development and engineering expenses were $6.7 million, $6.8 million and $5.6 million, respectively.

Patents, Trade Secrets and Confidentiality Agreements

As of June 30, 2014, the Company owns 19 U.S. patents that have been granted to it, and has 3 U.S. patent applications pending, which relate to various products and processes manufactured, used, and/or sold by the Company. The Company also owns 4 foreign patents that have been granted to it in Europe, China and Japan and has 14 patent applications pending in foreign locations. The U.S. and foreign patents expire from 2016 through 2031. In addition, the Company holds perpetual

5

licenses to more than 25 other U.S. patents including rights to practice 7 U.S. patents for non-forest product related applications that were assigned to USNR in conjunction with the sale of the Forest Products business unit in 2002, and rights to practice 9 U.S. patents that were sold in conjunction with the sale of CBU in August 2012. The expiration dates for these licensed patents range from 2014 to 2030.

The Company has registered, and continues to register, various trade names and trademarks including Perceptron®, Powered by Perceptron®, AutoGauge®, AutoFit®, AutoGuide®, AutoScan®, AutoSolve®, Contour Probe®, ScanWorks®, TriCam®, WheelWorks®, Visual Fixturing®, Helix®, and Intelligent Illumination®, among others, which are used in connection with the conduct of its business.

Perceptron’s products include hardware (camera, lens, etc.) for scanning an image and imbedded software (extraction software algorithms) to convey the results of the scan to the customer. The hardware and software operate and are sold as one product. Perceptron generally does not market its software algorithms as a separate item distinct from the scanning product. The Company’s software products are copyrighted and generally licensed to customers pursuant to license agreements that restrict the use of the products to the customer’s own internal purposes on designated Perceptron equipment.

The Company also uses proprietary information and invention agreements and non-disclosure agreements with employees, consultants and other parties.

There can be no assurance that any of the above measures will be adequate to protect the Company’s intellectual property or other proprietary rights. Effective patent, trademark, copyright and trade secret protection may be unavailable in certain foreign countries.

In the past, the Company had been informed that certain of its customers had received allegations of possible patent infringement involving processes and methods used in the Company’s products. Certain of these customers, including customers who were parties to patent infringement suits relating to this matter, settled such claims. Management believes that the processes used in the Company’s products were independently developed without utilizing any previously patented process or technology.

Employees

As of June 30, 2014, the Company employed 245 persons, 242 of whom were employed on a full-time basis with 128 located in North America and the remainder distributed across the globe as identified above in International Operations. None of the employees are covered by a collective bargaining agreement and the Company believes its relations with its employees to be good.

Available Information

The Company’s Internet address is www.perceptron.com. On the website, the Company makes available, free of charge, its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports, as soon as reasonably practicable after the Company electronically files such material with, or furnishes it to, the Securities and Exchange Commission (“SEC”). These reports can be accessed through the “Investors” section of the Company’s website under “SEC Filings”. The information found on the Company’s website is not part of this or any report the Company files with, or furnishes to, the SEC.

ITEM 1A:RISK FACTORS

An investment in our Common Stock involves numerous risks and uncertainties. You should carefully consider the following information about these risks. Any of the risks described below could result in a significant or material adverse effect on our future results of operations, cash flows or financial condition. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently deem immaterial, also may become important factors that adversely affect our business in the future. We believe that the most significant of the risks and uncertainties we face are as follows:

Our revenues are highly influenced by the sale of products for use in the global automotive market, particularly by manufacturers based in the United States, China, and Western Europe. These manufacturers have experienced periodic downturns in their businesses that could adversely affect their level of purchases of our products.

Our revenues are highly influenced by the sale of products for use in the automotive industry, particularly to manufacturers based in the United States, China and Western Europe. As a result, our ability to sell our systems and solutions to automotive manufacturers and suppliers is affected by periodic downturns in the global automotive industry, such as those that occurred in 2009-2010 in the United States automotive industry.

6

New vehicle tooling programs are the most important selling opportunity for our automotive-related sales. The number and timing of new vehicle tooling programs can be influenced by a number of economic factors. Our customers only launch a limited number of new car programs in any given year because of the time and financial resources required. From a macro perspective we continue to assess the global economy and its likely effect on our automotive customers and markets served. We continue to view the automotive industry’s focus on introducing new vehicles more frequently to satisfy their customers’ changing requirements, as well as their continuing focus on improved quality, as positive indicators for new business. However, because of periodic economic downturns experienced by our customers, our customers could determine to reduce their number of new car programs. The automobile industry is a very cost competitive industry. Pricing pressures could adversely affect the margins we realize on the sale of our products, and ultimately, our profitability.

Global economic conditions may negatively impact our results of operations.

Our revenue levels are impacted by global economic conditions, as we have a significant business presence in many countries throughout the world. In 2009-2010, the global economic crisis resulted in significantly lower demand for our products, as our automotive customers experienced deterioration in their business. Although our business has recovered since that time, global economic conditions have not fully recovered in certain regions. The automotive industry, which represents our largest market, is particularly impacted by changing global economic conditions and consumer spending. As a result, a significant decline in global economic conditions could have a material adverse impact on our results of operations.

Current levels of market volatility adversely impact the market price of our Common Stock.

The capital and credit markets are subject to volatility and disruption. During such a period, the volatility and disruption could reach unprecedented levels, which would exert downward pressures on stock prices, including the market price of our Common Stock.

Our future success is dependent upon our ability to implement our long-term growth strategy.

We realize that we are vulnerable to fluctuations in the global automotive industry. Our future success is dependent upon our ability to implement our long-term strategy that includes expanding our customer base in our automotive markets and expanding into new markets. Currently, we are focusing on our plans to achieve sales growth in automotive markets through expansion in automotive markets in Asia and the expansion of our business with current customers in North America, South America and Europe. We also continue to explore opportunities for expansion into non-automotive markets through our existing and new products. However, there are a number of uncertainties involved in our long-term strategy over which we have no or limited control, including:

•The quality and cost of competitive products already in existence or developed in the future.

•The level of interest existing and potential new customers may have in our existing and new products and technologies.

•Our ability to resolve technical issues inherent in the development of new products and technologies.

•Our ability to identify and satisfy market needs.

•Our ability to identify satisfactory distribution networks.

•General product development and commercialization difficulties.

•Rapid or unexpected technological changes.

•General product demand and market acceptance risks.

•Our ability to successfully compete with alternative and similar technologies.

•Our ability to attract the appropriate personnel to effectively represent, install and service our products.

•The effect of economic conditions.

Even if we are able to expand our customer base and markets, the new revenues we derive may not offset declines in revenues from our current products. We also may not be able to generate profits from these new customers or markets at the same level as we generate from our current business. There can be no assurance that we will be able to expand our customer base and markets or successfully execute our strategies in a fashion to maintain or increase our revenues and profits.

A significant percentage of our revenues are derived from a small number of customers, so that the loss of any one of these customers could result in a significant reduction in our revenues and profits.

A majority of our revenues is derived from the sale of systems and solutions to a small number of customers that consist primarily of automotive manufacturers and suppliers in North America, Western Europe and Asia.

With such a large percentage of our revenues coming from such a small and highly concentrated group of customers, we are susceptible to a substantial risk of losing revenues if these customers stop purchasing our products or reduce their purchases

7

of our products. In addition, we have no control over whether these customers will continue to purchase our products, systems and solutions in volumes or at prices sufficient to generate profits for us.

Our future commercial success depends upon our ability to maintain a competitive technological position in our markets, which are characterized by continual technological change.

Technology plays a key role in the systems and solutions that we produce. Our ability to sell our products to customers is directly influenced by the technology used in our systems and solutions. With the rapid pace at which technology is changing, there is a possibility that our customers may require more technologically advanced systems and solutions than what we may be capable of producing.

Technological developments could render actual and proposed products or technologies of ours uneconomical or obsolete. There also is a possibility that we may not be able to keep pace with our competitors’ products. In that case, our competitors may make technological improvements to their products that make them more desirable than our products.

Our growth and future financial performance depend upon our ability to introduce new products and enhance existing products that include the latest technological advances and customer requirements. We may not be able to introduce new products successfully or achieve market acceptance for such products. Any failure by us to anticipate or respond adequately to changes in technology and customer preferences, or any significant delays in product development or introduction, could have a material adverse effect on our business. Accordingly, we believe that our future commercial success will depend upon our continued ability to develop and introduce new cost-effective products and maintain a competitive technological position.

We are dependent on proprietary technology. If our competitors develop competing products that do not violate our intellectual property rights or successfully challenge those rights, our revenues and profits may be adversely affected.

Our products contain features that are protected by patents, trademarks, trade secrets, copyrights, and contractual rights. Despite these protections, there is still a chance that competitors may use these protected features in their products as a result of our inability to keep our trade secrets confidential, or in violation of our intellectual property rights or following a successful challenge to those rights. The prosecution of infringement claims against third parties and the defense of legal actions challenging our intellectual property rights could be costly and require significant attention from management. Because of the small size of our management team, this could result in the diversion of management’s attention from day-to-day operations.

There also is a chance that competitors may develop technology that performs the same functions as our products without infringing upon our exclusive rights. It is possible that competitors may reverse engineer those features of our products that are not protected by patents, trademarks and trade secrets. If a competitor is able to reverse engineer an unprotected feature successfully, the competitor may gain an understanding of how the feature works and introduce similar products to compete with our products.

Because some of our products are sold in China, we are at risk of competitors misappropriating our intellectual property included in those products or reverse engineering those products. As a result, we may have a more limited ability, and significantly greater costs, to enforce our intellectual property rights in those products. Constant technological improvement of those products will be particularly important to keep the products competitive in their markets.

We are subject to risks related to litigation.

From time to time, we are subject to lawsuits and other claims arising out of our business operations. Adverse judgments in one or more of these lawsuits could require us to pay significant damage amounts. The outcome of lawsuits is inherently uncertain and typically a loss cannot be reasonably estimated or accrued by us relating to lawsuits. Accordingly, if the outcome of a legal proceeding is adverse to the Company, we would have to record a charge for the matter at the time the legal proceeding is resolved and generally in the full amount at which it is resolved. In addition, the expenses related to these lawsuits may be significant. Lawsuits can have a material adverse effect on our business and operating results, particularly where we have not established an accrual or a sufficient accrual for damages, settlements, or expenses. See “Item 3 – Legal Proceedings” and Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Critical Accounting Policies – Litigation and Other Contingencies” below for a discussion of the Company’s policies in accounting for lawsuits and other claims.

We could become involved in costly litigation alleging patent infringement.

In the past, we had been informed that certain of our customers have received allegations of possible patent infringement involving processes and methods used in our products. Certain of these customers, including one customer who was a party to a patent infringement suit relating to this matter, settled such claims. We believe that the processes used in our products were independently developed without utilizing any previous patented process or technology. However, it is possible that in the future

8

we or our customers could receive allegations of possible patent infringement or could be parties to patent infringement litigation relating to our products.

The defense of patent infringement litigation could be costly and require significant attention from management. Because of the small size of our management team, this could result in the diversion of management’s attention from day-to-day operations.

There are a number of companies offering competitive products in our markets, or developing products to compete with our products, which could result in a reduction in our revenues through lost sales or a reduction in prices.

We are aware of a number of companies in our markets selling products using similar or alternative technologies and methods. We believe that there may be other companies, some of whom may be substantially larger and have substantially greater resources than us, which may be engaged in the development of technology and products for some of our markets that could prove to be competitive with ours. We believe that the principal competitive factor in our markets is the total capability that a product offers. In some markets, a competitive price for the level of functionality and reliability provided are the principal competitive factors. While we believe that our products compete favorably, it is possible that these competitors could capture some of our sales opportunities or force us to reduce prices in order to complete the sale.

We believe that certain existing and potential customers may be capable of internally developing their own technology. This could cause a decline in sales of our products to those customers.

Our business depends on our ability to attract and retain key personnel.

Our success depends in large part upon the continued service of our executives and key employees, including those in engineering, technical, sales and marketing positions, as well as our ability to attract such additional employees in the future. At times and in certain geographic markets, competition for the type of highly skilled employees we require can be significant. The loss of key personnel or the inability to attract new qualified key employees could adversely affect our ability to implement our long-term growth strategy and have a material adverse effect on our business.

We may not be able to complete business opportunities and acquisitions and our profits could be negatively affected if we do not successfully operate those that we do complete.

We will evaluate from time to time business opportunities that fit our strategic plans. There can be no assurance that we will identify any opportunities that fit our strategic plans or will be able to enter into agreements with identified business opportunities on terms acceptable to us. The Company may incur significant due diligence and legal costs with no assurance that an acquisition or business opportunity will be consummated after incurring these costs. If we are unable to identify and complete acquisitions that fit our strategic plans, we may not be able to fully implement our expansion plans for the Company.

There is also no assurance that we will be able to effectively integrate businesses that we may acquire due to the significant challenges in consolidating functions and integrating procedures, personnel, product lines, technologies and operations in a timely and efficient manner. The integration process may require significant attention from management and devotion of resources. Because of the small size of our management team, this could result in the diversion of management’s attention from day-to-day operations and impair our relationships with current employees and customers.

We intend to finance any such business opportunities from available cash on hand, existing credit facilities, issuance of additional stock or additional sources of financing, as circumstances warrant. We could use a significant portion of our available cash on hand and incur substantial debt or other contingent liabilities in connection with these acquisition opportunities. The issuance of additional equity securities to finance an acquisition could be substantially dilutive to our stockholders. In addition, our profitability may suffer because of acquisition-related costs, debt service requirements or amortization costs for acquired intangible assets. In addition, if the business opportunities do not perform as expected, we could incur impairment charges related to goodwill or other intangibles acquired by us. If we are not successful in generating additional profits from these transactions, this dilution and these additional costs could cause our Common Stock price to drop.

We are expanding our foreign operations, increasing the possibility that our business could be adversely affected by risks of doing business in foreign countries.

We have significant operations outside of the United States and are currently implementing a strategy to expand our operations outside of the United States, especially in Asia.

Our foreign operations are subject to risks customarily encountered in such foreign operations. For instance, we may encounter fluctuations in foreign currency exchange rates, differences in the level of protection available for our intellectual property, the impact of differences in language and local business and social customs on our ability to market and sell our products in these markets, the inability to recruit qualified personnel in a specific country or region, more stringent employment regulations and

9

local labor conditions and difficulties in repatriating cash earned in other countries back to the United States. In addition, we may be affected by U.S. laws and policies that impact foreign trade and investment. Finally, we may be adversely affected by laws and policies imposed by foreign governments in the countries where we have business operations or sell our products. These laws and policies vary from jurisdiction to jurisdiction.

Because of our significant foreign operations, our revenues and profits can vary significantly as a result of fluctuations in the value of the United States dollar against foreign currencies.

Products that we sell in foreign markets are sometimes priced in currency of the country where the customer is located. To the extent that the dollar fluctuates against these foreign currencies, the prices of our products in U.S. dollars also will fluctuate. As a result, our return on the sale of our products may vary based on these fluctuations. Accordingly, we could experience unanticipated foreign currency gains or losses that could have a material impact on our results of operations.

We face various risks arising from the legal, regulatory and tax requirements imposed on our operations in the various countries in which we conduct our business operations.

We are subject to various risks relating to our compliance with existing and new laws, rules and regulations implemented in the countries in which we conduct our business operations, including anti-corruption, anti-bribery, tax, material composition of our products, such as restrictions on lead and other substances, environmental, safety and export control regulations.

We are subject to the United States Foreign Corrupt Practices Act, or FCPA, which generally prohibits companies and their intermediaries from making improper payments to foreign officials for the purpose of obtaining or keeping business or other benefits. As a result of our foreign operations, we may have contact with persons who are considered foreign officials under the FCPA, putting us at an increased risk of potential FCPA violations.

Our failure or inability to comply with any of these laws, rules or regulations could subject us to civil or criminal penalties, other remedial measures or financial or regulatory obligations that may adversely affect our results of operations, financial position, reputation or ability to conduct business. We may receive audit notices or other inquiries from governmental or regulatory authorities, and we may participate in voluntary disclosure programs, related to legal, regulatory or tax compliance matters. These audits, inquiries or disclosure programs or any non-compliance with applicable laws, rules or regulations could result in our incurring material expense, including investigation costs, defense costs, assessments and penalties, or other consequences that could materially adversely affect our results of operations, financial position, reputation or ability to conduct business.

Because a large portion of our revenues are generated from a limited number of sizeable orders, our revenues and profits may vary widely from quarter to quarter and year to year.

A large portion of our revenues are generated from a limited number of sizeable orders that are placed by a small number of customers. If the timing of these orders is delayed from one quarter to the next or from one year to the next, we may experience fluctuations in our quarterly and annual revenues and operating results. Because our order terms vary from project to project, the application of the Company’s revenue recognition accounting policies to those orders can cause the timing for our recognition of revenue from an order to vary significantly between orders. This may cause our revenues and operating results to vary significantly from quarter to quarter and year to year.

The amount of revenues that we earn in any given quarter may vary based in part on the timing of new vehicle programs in the global automotive industry. In contrast, many of our operating expenses are fixed and will not vary from quarter to quarter. As a result, our operating results may vary significantly from quarter to quarter and from year to year.

We could experience losses in connection with sales of our investments.

The Company has a long-term investment that was exchanged for preferred stock of a reinsurance company. This investment has not been registered under the Securities Act of 1933 and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements. The issuer of this security is not obligated to register the security. There is no regular trading market for these securities. As a result, we will have limited ability to liquidate the investment. This lack of liquidity, as well as negative changes in the financial condition of the issuer of the security and credit rating, has adversely impacted the value of the security. In the event that the financial condition of the issuer should continue to deteriorate, we may have to record additional impairment charges relating to the security, which would negatively impact our stockholders’ equity and net income. See Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources”.

The trading price of our stock has been volatile.

The following factors may affect the market price of our Common Stock, which can vary widely over time:

10

•announcements of new products by us;

•announcements of new products by our competitors;

•variations in our operating results;

•market conditions in the electronic and sensing industry and/or automotive industry;

•market conditions and stock prices in general; and

•the volume of our Common Stock traded.

Because of the limited trading in our Common Stock, it may be difficult for shareholders to dispose of a large number of shares of our Common Stock in a short period of time or at then current prices.

Because of the limited number of shares of our Common Stock outstanding and the limited number of holders of our Common Stock, only a limited number of shares of our Common Stock trade on a daily basis. This limited trading in our Common Stock makes it difficult to dispose of a large number of shares in a short period of time. In addition, it is likely that the sale by a shareholder of a large number of shares of our Common Stock over an extended period would depress the price of our Common Stock.

We may decide not to pay dividends on our common stock in the future.

Holders of our common stock are only entitled to receive such dividends when and if they are declared by our Board of Directors. Our Board of Directors may change the Company’s dividend policy and dividend amounts at any time, or discontinue the payment of dividends altogether, due to a number of factors, including covenants in the Company’s loan agreement requiring the approval of the Company’s bank prior to the payment of dividends above stated levels, the Company’s levels of available capital, the Company’s future operating results, or the determination to use or reserve the Company’s cash resources for other purposes. This could adversely affect the market price of our common stock.

We may be restricted under our loan agreement from paying higher dividends.

The Company’s Amended and Restated Credit Agreement allows the Company to declare and pay dividends of up to $2.5 million for each fiscal year, provided the Company maintains a minimum Tangible Net Worth as defined in the Credit Agreement. In the event the Board of Directors decided to declare a cash dividend in the future in excess of these levels, we would have to seek a waiver from the covenant in our bank agreement. Our bank may not be willing to waive the restriction.

As permitted under Michigan law, our directors are not liable to Perceptron for monetary damages resulting from their actions or inactions.

Under our articles of incorporation, as permitted under the Michigan Business Corporation Act, members of our Board of Directors are not liable for monetary damages for any negligent or grossly negligent action that the director takes, or for any negligent or grossly negligent failure of a director to take any action. However, a director will remain liable for:

•intentionally inflicting harm on Perceptron or its shareholders;

•distributions that the director makes in violation of the Michigan Business Corporation Act; and

•intentional criminal acts that the director commits.

However, we or our shareholders may seek an injunction, or other appropriate equitable relief, against a director. Finally, liability may be imposed against members of the Board of Directors under the federal securities laws.

We are required to indemnify our officers and directors if they are involved in litigation as a result of their serving as officers or directors of Perceptron or as officers or directors of other corporations at our behest, which could reduce our profits and cash available to operate our business.

Our by-laws require us to indemnify our officers and directors. We may be required to pay judgments, fines and expenses incurred by an officer or director, including reasonable attorneys’ fees, as a result of actions or proceedings in which such officers or directors are involved by reason of being or having been an officer or director of Perceptron or other corporations at our behest.

Funds paid in satisfaction of judgments, fines and expenses would reduce our profits and may be funds we need for the operation of our business and the development of products. This could cause our stock price to drop.

A change in our effective tax rate can have a significant adverse impact on our business.

11

A number of factors may adversely impact our future effective tax rates, such as the future valuation of our deferred tax assets which are predominantly in the United States and are dependent on our ability to generate sufficient future taxable income in the United States; the geographic composition of our pre-tax income and the various tax rates in those countries; changes in available tax credits, changes in tax laws and rates, and the repatriation of earnings from outside the United States for which we have not previously provided for United States taxes. A change in our effective tax rate can adversely impact our net income.

We may have additional tax liabilities, which could adversely affect our results of operations.

We are subject to income taxes in the United States and foreign jurisdictions, including Germany and China. In determining our provisions for income taxes, we make judgments regarding various tax positions reported on our tax returns. As a result, there are transactions and calculations where the ultimate tax determination is uncertain. Our tax returns are regularly under audit by tax authorities. Because of these uncertain tax positions, the final determination of these tax audits could be materially different than is reflected in our financial statements and could have a material adverse effect on our provisions for income taxes, results of operations, or cash flows.

Our profits could be reduced as a result of our compliance with SEC rules relating to our internal control over financial reporting.

Current SEC rules require our independent registered public accounting firm auditing our financial statements to provide an attestation report on our internal control over financial reporting in our annual reports.

For the fiscal years 2009 through 2013, the Company was not required to have an attestation report from our independent registered public accounting firm on our internal controls. Because the Company’s common stock held by non-affiliates exceeded $75 million at December 31, 2013, we have to comply with these requirements in fiscal year 2014 and thereafter. We may have to expend significant resources in future fiscal years in connection with ongoing compliance with these requirements, which could adversely affect our profitability.

If management is not able to provide a positive report on our internal control over financial reporting, and our independent registered public accounting firm is not able to provide an unqualified opinion regarding our internal control over financial reporting, shareholders and others may lose confidence in our financial statements, which could cause our stock price to drop.

Because of our relatively small size, we are unable to have financial personnel in positions that are devoted solely to internal controls over financial reporting. However, management has had a continuous program in effect to evaluate and test internal controls through the utilization of outside, independent accountants.

In fiscal 2008 through fiscal 2014, management provided positive reports on our internal control over financial reporting and we received in fiscal 2008 and 2014 an unqualified opinion from our independent registered public accounting firm regarding our internal control over financial reporting. In fiscal 2009 through fiscal 2013, our auditors were not required to give an opinion on our internal control over financial reporting following SEC rules for companies that had a market value of common stock held by non-affiliates that was less than $75 million as of the companies’ second fiscal quarter in any given fiscal year. The Company’s Common Stock held by non-affiliates exceeded $75 million at December 31, 2013. Accordingly, we will comply with these requirements beginning in fiscal year 2014 and thereafter. There can be no positive assurance that, in the future, management will provide a positive report on our internal control over financial reporting or that we will receive an unqualified opinion from our independent registered public accounting firm regarding our internal control over financial reporting. In the event we identify significant deficiencies or material weaknesses in our internal controls that we cannot remediate in a timely manner, investors and others may lose confidence in the reliability of our financial statements. This could cause our stock price to drop.

If the subcontractors we rely on for component parts or products delay deliveries or fail to deliver parts or products meeting our requirements, we may not be able to deliver products to our customers in a timely fashion and our revenues and profits could be reduced.

We rely on subcontractors for certain components of our products, including outside subcontracting assembly houses to produce the circuit boards that we use in our products. As a result, we have limited control over the quality and the delivery schedules of components or products purchased from third parties. In addition, we purchase a number of component parts from single source suppliers. If our supplies of component parts or products meeting our requirements are significantly delayed or interrupted, or our subcontractors choose to terminate their supply contracts, we may not be able to deliver products to our customers in a timely fashion. This could result in a reduction in revenues and profits for these periods. The termination of or material change in the purchase terms of any single source supplier could have a similar impact on us. It is also possible, if our delay in delivering products to our customer is too long, the customer could cancel its order, resulting in a permanent loss of revenue and profit from that sale. Although we have not experienced significant supply shortages from single source suppliers in recent years, from time to time, we have experienced significant delays in the receipt of certain components.

12

Finally, although we believe that alternative suppliers are available, difficulties or delays may arise if we shift manufacturing capacity to new suppliers.

New regulations related to conflict minerals may adversely affect us.

The Dodd-Frank Wall Street Reform and Consumer Protection Act requires us to disclose whether our products contain “conflict minerals” mined from the Democratic Republic of Congo and adjoining countries (“DRC”), whether or not the components of our products are manufactured by us or third parties. In 2014, to meet the initial disclosure requirements, we began due diligence to determine the sources of the conflict minerals in our products. Because our supply chain is very complex, we may not be able to verify all the metals used in our products or the origin of all metals used in our products. The pricing, sourcing and availability of conflict minerals used in the manufacture of our products could be impacted by these new requirements. There are additional costs associated with complying with the disclosure requirements, such as costs related to our due diligence to determine the source of any conflict minerals used in our products. We may not be able to sufficiently verify the origins of all conflict metals used in our products and confirm that they are DRC conflict mineral free, which may adversely affect our reputations with our customers and shareholders.

Our failure to accurately forecast customer demand could result in excess or obsolete inventory and related write-downs or charges.

From time to time, we may strategically enter into non-cancelable commitments with vendors to purchase materials for our products in advance of demand to take advantage of favorable pricing or address concerns about long lead times for components used in our products that are purchased from third parties. Our failure to accurately forecast customer demand has led to, and may again in the future lead to, an increased risk of excess or obsolete inventory. This could result in write-downs of inventory and other related charges that would negatively affect our results of operations.

The occurrence of business system disruptions or information security breaches could adversely affect our business.

To our knowledge, we have not been subject to information security breaches; however, many other companies have experienced such breaches because of illegal hacking, computer viruses, or acts of vandalism or terrorism. While we have implemented security measures to protect against such breaches, it is possible that our security measures may not detect or prevent such breaches. Any such compromise to our information security could result in an interruption in our operations, the unauthorized publication of our confidential business or proprietary information, the unauthorized release of customer, vendor, or employee data, the violation of privacy or other laws, and the exposure to litigation, any of which could harm our business and operating results. A disruption to our management information systems could cause significant disruption to our business, including our ability to receive and ship orders, receive and process payments and timely report our financial results. Any disruption occurring with these systems may have a material adverse effect on our results of operations.

The Board of Directors has the right to issue up to 1,000,000 shares of preferred stock without further action by shareholders. The issuance of those shares could cause the market price of our Common Stock to drop significantly and could be used to prevent or frustrate shareholders’ attempts to replace or remove current management.

Although no preferred stock currently is outstanding, we are authorized to issue up to 1,000,000 shares of preferred stock. Preferred stock may be issued in one or more series, the terms of which may be determined at the time of issuance by the Board of Directors, without further action by shareholders, and may include voting rights (including the right to vote as a series on particular matters), the dividends payable thereon, liquidation payments, preferences as to dividends and liquidation, conversion rights and redemption rights. In the event that preferred stock is issued, the rights of the common stockholders may be adversely affected. This could result in a reduction in the value of our Common Stock.

The preferred stock could be issued to discourage, delay or prevent a change in control of Perceptron. This may be beneficial to our management or Board of Directors in a hostile tender offer or other takeover attempt and may have an adverse impact on shareholders who may want to participate in the tender offer or who favor the takeover attempt.

Our common stock rights plan could be used to discourage hostile tender offers.

We maintain a common stock rights plan. Under the plan, if any person acquires 15% or more of our outstanding Common Stock, our shareholders, other than the acquirer, will have the right to purchase shares of our Common Stock at half their market price. The common stock rights plan discourages potential acquirers from initiating tender offers for our Common Stock without the approval of the Board of Directors. This may be beneficial to our management or Board of Directors in a hostile tender offer or other takeover attempt and may have an adverse impact on shareholders who may want to participate in the tender offer or who favor the takeover attempt.

13

ITEM 1B:UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 2:PROPERTIES

Perceptron’s principal domestic facility consists of a 70,000 square foot building located in Plymouth, Michigan, owned by the Company. In addition, the Company leases a 1,576 square meter facility in Munich, Germany and leases office space in Voisins le Bretonneux, France; Sao Paulo, Brazil; Tokyo, Japan; Singapore; Shanghai, China; and Chennai, India. The Company believes that its current facilities are sufficient to accommodate its requirements through fiscal 2015.

ITEM 3:LEGAL PROCEEDINGS

On July 19, 2013, a civil suit was filed against the Company by 3CEMS, a Cayman Islands and People’s Republic of China corporation, with the U.S. District Court for the Eastern District of Michigan. The suit alleged that the Company breached its contractual obligations by failing to pay for component parts to be used to manufacture optical video scopes for the Company’s discontinued Commercial Products Business Unit. 3CEMS alleged that it purchased the component parts in advance of the receipt of orders from the Company based upon instructions they claimed to have received from the Company. The suit alleged damages of not less than $4.5 million. Effective December 6, 2013, a Tolling Agreement (the “Tolling Agreement”) was entered into between the Company and 3CEMS. The Tolling Agreement provided that 3CEMS would dismiss the suit against the Company without prejudice, permitting the parties to continue to discuss the dispute outside of litigation. On January 13, 2014, based upon 3CEMS’ voluntary dismissal, the Court entered an order of dismissal of the suit against the Company without prejudice. The Company has agreed that should 3CEMS subsequently seek to assert claims against the Company related to such suit the Company will not oppose the claims based on the statute of limitations or any other time-based defense, based upon the passage of time from July 19, 2013 to the date the Tolling Agreement is terminated. The Tolling Agreement terminates on December 31, 2014 or, if earlier upon 20 days’ notice by either party. See Note 5 of the Notes to the Consolidated Financial Statements, “Contingencies”, included in Item 8 of this report.

ITEM 4:MINE SAFETY DISCLOSURES

Not applicable.

14

PART II

ITEM 5:MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES

Perceptron’s Common Stock is traded on The NASDAQ Stock Market’s Global Market under the symbol “PRCP”. The following table shows the reported high and low sales prices of Perceptron’s Common Stock for fiscal 2014 and 2013:

|

Prices |

|||||

|

Fiscal 2014 |

Low |

High |

|||

|

Quarter through September 30, 2013 |

$ |

6.86 |

$ |

11.73 | |

|

Quarter through December 31, 2013 |

$ |

9.01 |

$ |

14.89 | |

|

Quarter through March 31, 2014 |

$ |

11.53 |

$ |

18.24 | |

|

Quarter through June 30, 2014 |

$ |

10.00 |

$ |

13.60 | |

|

Fiscal 2013 |

|||||

|

Quarter through September 30, 2012 |

$ |

4.98 |

$ |

6.26 | |

|

Quarter through December 31, 2012 |

$ |

4.91 |

$ |

6.31 | |

|

Quarter through March 31, 2013 |

$ |

5.68 |

$ |

9.30 | |

|

Quarter through June 30, 2013 |

$ |

6.60 |

$ |

8.05 | |

On May 21, 2014, the Board of Directors declared an annual dividend of fifteen cents ($0.15) per share of Common Stock. The annual dividend was paid on June 26, 2014 to shareholders of record at the close of business on June 5, 2014.

On May 7, 2013, the Board of Directors declared an annual dividend of fifteen cents ($0.15) per share of Common Stock. The annual dividend was paid on June 27, 2013 to shareholders of record at the close of business on June 6, 2013.

On September 27, 2012, the Board of Directors declared a special dividend of twenty-five cents ($0.25) per share of Common Stock. The special dividend was paid on November 1, 2012 to shareholders of record at the close of business on October 10, 2012.

The Company’s Amended and Restated Credit Agreement allowed the Company to declare and pay dividends of up to $3.7 million in fiscal 2013 and up to $2.5 million for each fiscal year thereafter, provided the Company maintains a minimum Tangible Net Worth as defined in the Credit Agreement. The Company may change the dividend policy and dividend amounts at any time, or discontinue the payment of dividends altogether. See “Item 1A – Risk Factors – We may decide not to pay dividends on our common stock in the future” and “We may be restricted under our loan agreement from paying higher dividends.”

The approximate number of shareholders of record on September 8, 2014, was 156.

The information pertaining to the securities the Company has authorized for issuance under equity plans is hereby incorporated by reference to Item 12, "Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters – Equity Compensation Plan Information”. For more information about the Company’s equity compensation plans, see Note 8 of the Notes to the Consolidated Financial Statements, “Stock Based Compensation”, included in Item 8 of this report.

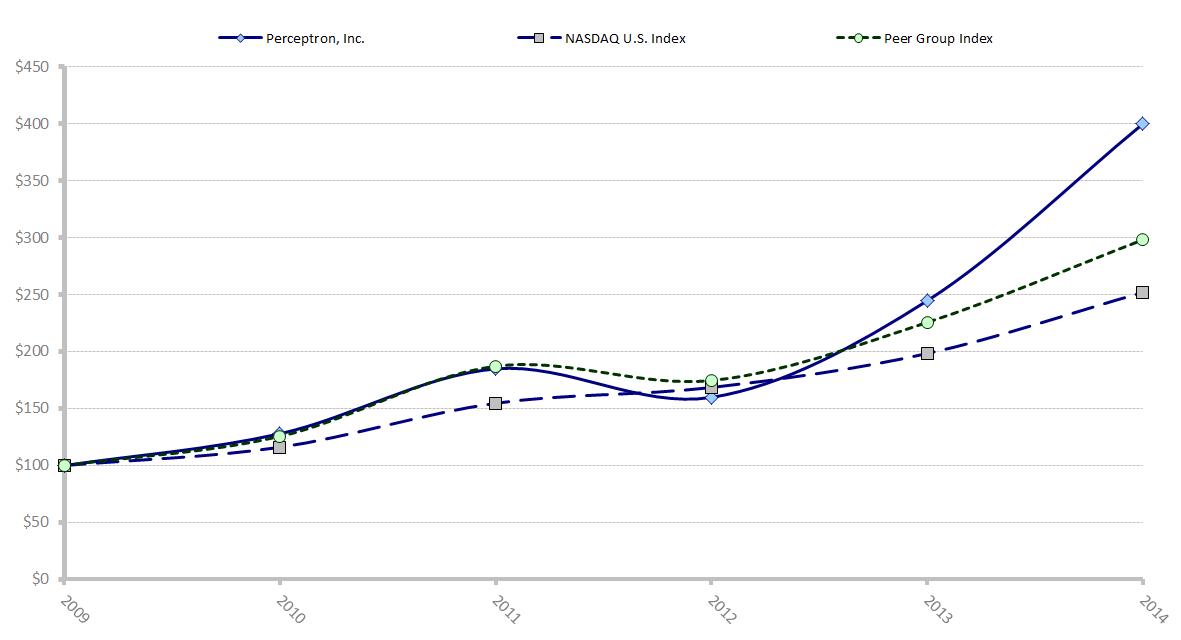

STOCK PRICE PERFORMANCE GRAPH

The following graph compares the cumulative 5-year total return attained by shareholders on the Company’s Common Stock relative to the cumulative total returns of The Nasdaq Stock Market (U.S.) Index (the “Nasdaq U.S. Index”) and a peer group of companies consisting of all U.S. exchange traded companies with standard industrial classification codes 3823 (Industrial Instruments for Measurement, Display, and Control of Process Variables; and Related Products), 3827 (Optical Instruments and Lenses) and 3829 (Measuring and Controlling Devices) (the “Peer Group Index”). The returns of each company in the Peer Group Index have been weighted according to their respective stock market capitalization. The graph assumes that the value of the investment in the Company’s Common Stock, the Peer Group Index and the Nasdaq U.S. Index was $100 on June 30, 2009 and that all dividends were reinvested.

15

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Perceptron, Inc., the Nasdaq U.S. Index,

and a Peer Group Index

* $100 invested on June 30, 2009 in stock or index, including reinvestment of dividends. Fiscal year ending June 30.

|

CUMULATIVE TOTAL RETURN |

|||||||||||

|

6/30/2009 |

6/30/2010 |

6/30/2011 |

6/30/2012 |

6/30/2013 |

6/30/2014 |

||||||

|

Perceptron, Inc. |

100.00 | 127.91 | 184.88 | 159.88 | 244.78 | 400.22 | |||||

|

Nasdaq U.S. Index |

100.00 | 116.08 | 154.72 | 168.57 | 198.38 | 252.10 | |||||

|

Peer Group Index |

100.00 | 125.54 | 187.23 | 174.71 | 225.72 | 298.29 | |||||

The graph displayed above is presented in accordance with applicable legal requirements. Shareholders are cautioned against drawing any conclusions from the data contained in the graph, as past results are not necessarily indicative of future performance. The graph in no way reflects the Company’s forecast of future financial performance.

The Peer Group consists of the following companies: Schmitt Industries, Inc. (SMIT), Esterline Technologies Corp. (ESL), MKS Instruments, Inc. (MKSI), Sensata Technologies Holding NV (ST), Hurco Companies Inc. (HURC), Abaxis, Inc. (ABAX), II-VI Incorporated (IIVI), Electro-Sensors Inc. (ELSE), KLA–Tencor Corp. (KLAC), Orbotech Ltd. (ORBK), Mocon Inc. (MOCO), Thermo Fisher Scientific, Inc. (TMO), Nova Measuring Instruments Ltd. (NVMI), Sypris Solutions Inc. (SYPR), Camtek, Ltd (CAMT), Mesa Laboratories Inc. (MLAB), Rudolph Technologies Inc. (RTEC), Metro Storm Limited (MTSXY), Sutron Corporation (STRN), Cognex Corp. (CGNX), Faro Technologies Inc. (FARO), Clearsign Combustion Corp. (CLIR), Geospace Technologies Corporation (GEOS), Rockwell Automation Inc. (ROK), Cubic Corporation (CUB), Landauer Inc. (LDR), Trimble Navigation Limited (TRMB), Roper Industries Inc. (ROP), MTS Systems Corporation (MTSC), CyberOptics Corp. (CYBE), Measurement Specialties Inc. (MEAS), Sequenom Inc. (SQNM), Danaher Corp. (DHR), Image Sensing Systems, Inc. (ISNS) and Nanometrics Incorporated (NANO).

16

ITEM 6:SELECTED FINANCIAL DATA

The selected statement of operations and balance sheet data presented below are derived from the Company’s consolidated financial statements and should be read in conjunction with the Company’s consolidated financial statements and notes thereto and Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in this report.

|

Fiscal Years Ended |

||||||||||||||

|

June 30, |

||||||||||||||

|

Statement of Operations Data |

2014 |

2013 |

2012 |

2011 |

2010 |

|||||||||

|

(In Thousands, Except Per Share Amounts) |

||||||||||||||

|

Net sales |

$ |

59,612 |

$ |

60,886 |

$ |

57,379 |

$ |

50,847 |

$ |

40,199 | ||||

|

Gross profit |

24,849 | 28,120 | 24,170 | 22,622 | 16,126 | |||||||||

|

Operating income (loss) |

2,942 | 6,866 | 5,596 | 3,386 | (2,118) | |||||||||

|

Income (loss) from continuing operations |

||||||||||||||

|

before income taxes |

3,002 | 7,531 | 5,375 | 4,103 | (1,676) | |||||||||

|

Income from continuing operations |

2,427 | 6,130 | 2,827 | 2,650 | 70 | |||||||||

|

Discontinued operations |

- |

80 | (3,160) | (824) | (875) | |||||||||

|

Net income (loss) |

2,427 | 6,210 | (333) | 1,826 | (805) | |||||||||

|

Earnings (loss) per basic share: |

||||||||||||||

|

Continuing operations |

$ |

0.27 |

$ |

0.72 |

$ |

0.34 |

$ |

0.30 |

$ |

0.01 | ||||

|

Discontinued operations |

- |

0.01 | (0.38) | (0.09) | (0.10) | |||||||||

|

Net income (loss) |

$ |

0.27 |

$ |

0.73 |

$ |

(0.04) |

$ |

0.21 |

$ |

(0.09) | ||||

|

Earnings (loss) per diluted share: |

||||||||||||||

|

Continuing operations |

$ |

0.26 |

$ |

0.71 |

$ |

0.34 |

$ |

0.29 |

$ |

0.01 | ||||

|

Discontinued operations |

- |

0.01 | (0.38) | (0.09) | (0.10) | |||||||||

|

Net income (loss) |

$ |

0.26 |

$ |

0.72 |

$ |

(0.04) |

$ |

0.20 |

$ |

(0.09) | ||||

|

Weighted average common shares outstanding: |

||||||||||||||

|

Basic |

8,983 | 8,512 | 8,433 | 8,879 | 8,923 | |||||||||

|

Diluted |

9,210 | 8,588 | 8,433 | 9,050 | 8,923 | |||||||||

|

As of June 30, |

||||||||||||||

|

Balance Sheet Data |

2014 |

2013 |

2012 |

2011 |

2010 |

|||||||||

|

(In Thousands, Except Per Share Amounts) |

||||||||||||||

|

Working capital |

$ |

46,454 |

$ |

41,294 |

$ |

35,923 |

$ |

40,349 |

$ |

36,854 | ||||

|

Total assets |

80,066 | 73,639 | 66,259 | 69,301 | 64,037 | |||||||||

|

Shareholders' equity |

62,780 | 56,895 | 52,259 | 55,480 | 53,476 | |||||||||

|

Annual dividend declared per common share |

$ |

0.15 |

$ |

0.15 |

$ |

- |

$ |

- |

$ |

- |

||||

|

Special dividend declared per common share |

- |

0.25 |

- |

- |

- |

|||||||||

|

Total dividends declared per common share |

$ |

0.15 |

$ |

0.40 |

$ |

- |

$ |

- |

$ |

- |