Attached files

| file | filename |

|---|---|

| 8-K - 8-K - TIDEWATER INC | d786759d8k.htm |

| EX-99.2 - EX-99.2 - TIDEWATER INC | d786759dex992.htm |

Barclays CEO

Energy-Power Conference September 4, 2014

Jeffrey M. Platt

President & CEO

Joseph M. Bennett

EVP & Chief IRO

Exhibit 99.1 |

FORWARD-LOOKING STATEMENTS

In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of

1995, the Company notes that certain statements set forth in this presentation provide

other than historical information and are forward looking. The actual achievement of any

forecasted results, or the unfolding of future economic or business developments in a

way anticipated or projected by the Company, involve numerous risks and uncertainties that may

cause

the

Company’s

actual

performance

to

be

materially

different

from

that

stated

or

implied

in

the

forward-looking

statement. Among those risks and uncertainties, many of which are beyond the control of the

Company, include, without limitation, fluctuations in worldwide energy demand and oil and

gas prices; fleet additions by competitors and industry overcapacity; changes in capital

spending by customers in the energy industry for offshore exploration, development and

production; changing customer demands for different vessel specifications, which may make some of

our older vessels technologically obsolete for certain customer projects or in certain markets;

uncertainty of global financial

market

conditions

and

difficulty

accessing

credit

or

capital;

acts

of

terrorism

and

piracy;

significant

weather

conditions; unsettled political conditions, war, civil unrest and governmental actions, such as

expropriation or enforcement of customs or other laws that are not well-developed or

consistently enforced, especially in higher political risk countries where we operate;

foreign currency fluctuations; labor changes proposed by international conventions;

increased regulatory burdens and oversight; and enforcement of laws related to the environment,

labor and

foreign

corrupt

practices.

Readers

should

consider

all

of

these

risks

factors,

as

well

as

other

information contained

in the Company’s form 10-K’s and 10-Q’s.

Phone:

504.568.1010 |

Fax: 504.566.4580

Web site address:

www.tdw.com

Email:

connect@tdw.com

Barclays CEO Energy-Power Conference

TIDEWATER

601 Poydras Street, Suite 1500, New Orleans, LA 70130

2 |

•

Consistent goal of “Best in Class”

safety and compliance culture

•

History of earnings growth and solid returns

•

Continued solid financial position, with considerable ready

liquidity, a reasonable debt level, minor debt maturities

until FY2019 and expected reduced CAPX as major fleet

upgrade winds down

Key Tidewater Takeaways

Barclays CEO Energy-Power Conference

3

•

Largest “NEW” OSV fleet in the industry, operating in over

50 countries with ~9,000 employees worldwide

•

“Offshore” is and will continue to be relevant. Constructive

fundamental backdrop for the OSV industry |

Safety Record

Rivals Leading Companies Barclays CEO Energy-Power Conference

•

Safe Operations is Priority #1

•

Stop Work Obligation

•

Safety performance is 25% of mgt. incentive comp

4

TOTAL RECORDABLE INCIDENT RATES

Operating safely offshore is

like holding a snake by its head.

It’s

a

task

that

can’t

be

turned

loose

not

for

a

microsecond

or

an

accident will strike without pity. |

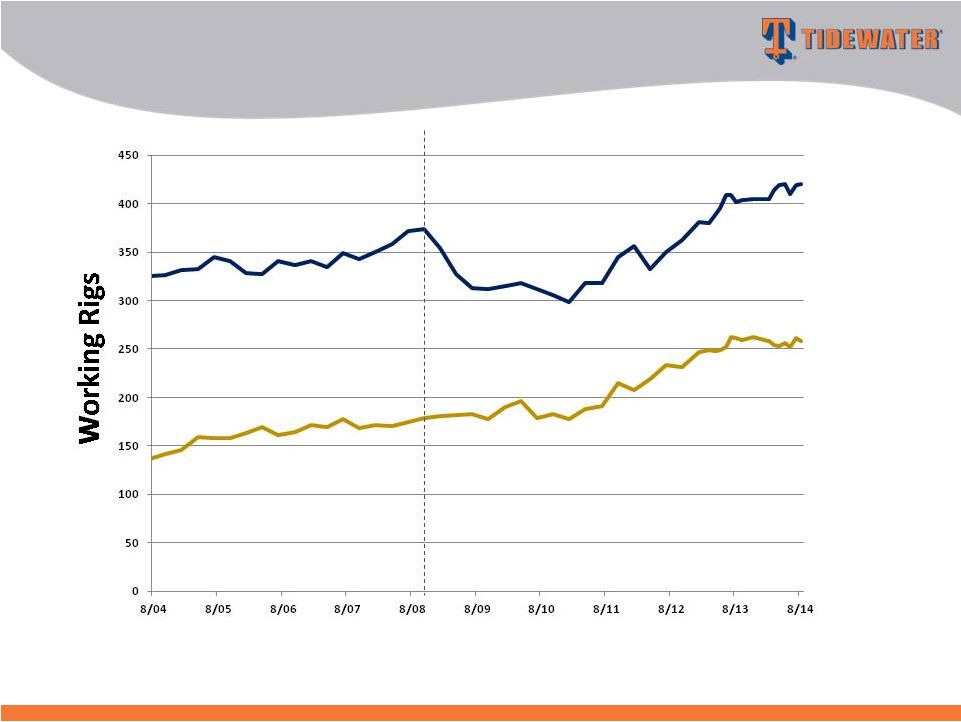

Source:

ODS-Petrodata Note: 42 “Other”

rigs, along with the Jackups and Floaters, provide a total working rig count of 720 in August

2014. 420

258

Prior peak (summer 2008)

Jackups

Floaters

Working Offshore Rig Trends

Barclays CEO Energy-Power Conference

5 |

Source:

ODS-Petrodata and Tidewater July 2008

(Peak)

Jan. 2011

(Trough)

August

2014

Working Rigs

603

538

720

Rigs Under

Construction

186

118

240

OSV Global

Population

2,033

2,599

3,203

OSV’s Under

Construction

736

367

459

OSV/Rig Ratio

3.37

4.83

4.45

Drivers of our Business “Peak to Present”

Barclays CEO Energy-Power Conference

6

Working offshore rig

count is expected to grow

Marketed

OSV

population

should decrease as

attrition exceeds

newbuild deliveries

OSV/Rig Ratio should

remain well balanced |

Source:

ODS-Petrodata and Tidewater As of August 2014, there are approximately 459 additional

AHTS and PSV’s (~14% of the global fleet) under construction.

Global fleet is estimated at 3,203 vessels, including ~700 vessels that are 25+

yrs old (25%). Vessels > 25 years old today

The Worldwide OSV Fleet

(Includes AHTs and PSVs only) Estimated as of August 2014

Barclays CEO Energy-Power Conference

7 |

Year

Built Deepwater vessels

Towing Supply/Supply

Other vessels

244 “New”

vessels –

6.9 avg yrs

21 “Traditional”

vessels –

26.7 avg yrs

Tidewater’s Active Fleet

As of June 30, 2014

Barclays CEO Energy-Power Conference

8 |

Source:

ODS-Petrodata and Tidewater Tidewater

Competitor #2

Competitor #3

Competitor #4

Competitor # 5

Competitor #1

Avg.

All Others (2,452 total

vessels for

400+ owners)

Vessel Population by Owner

(AHTS and PSVs only) Estimated as of August 2014

Barclays CEO Energy-Power Conference

9 |

Our Global

Footprint – Vessel Count by Region

(Excludes stacked vessels –

as of 6/30/14)

Barclays CEO Energy-Power Conference

10

Americas

69(26%)

SS Africa/Europe

128(48%)

MENA

44(17%)

Asia/Pac

24(9%) |

Our Global

Footprint – Vessel Class by Region

(Excludes stacked vessels –

as of 6/30/14)

Barclays CEO Energy-Power Conference

New

Avg.

Traditional

Vessels

NBV

Vessels

Deepwater

10

$15.2M

1

Towing Supply

31

$12.1M

0

Other

0

0

2

41

3

New

Avg.

Traditional

Vessels

NBV

Vessels

Deepwater

37

$28.7M

0

Towing Supply

43

$12.5M

2

Other

41

$1.8M

5

121

7

New

Avg.

Traditional

Vessels

NBV

Vessels

Deepwater

9

$24.9M

0

Towing Supply

14

$11.6M

0

Other

1

$6.7M

0

24

0

Americas

SSAE

MENA

Asia/Pac

Vessel

count

info

is

as

of

6/30/14,

and

includes

leased

vessels.

Avg

NBV

excludes

the

impact

of

leased

vessels

which

have

no

NBV.

Average NBV of the total 21 Traditional vessels is $0.97M at 6/30/14.

11

New

Avg.

Traditional

Vessels

NBV

Vessels

Deepwater

32

$19.5M

0

Towing Supply

17

$10.6M

7

Other

9

$3.4M

4

58

11 |

Vessel Count (2) Total Cost (2)

Average Cost

per Vessel

Deepwater PSVs

102

$2,906m

$28.5m

Deepwater AHTSs

12

$387m

$32.3m

Towing Supply/Supply

111

$1,670m

$15.0m

Other

53

$227m

$4.3m

TOTALS:

278

$5,190m

(1)

$18.7m

.

At 6/30/14, 245 new vessels were in our fleet with ~6.9 year average age

Vessel Commitments

Jan. ’00 –

June ‘14

(1)

~$4.5b (87%) funded through 6/30/14

(2)

Vessel count and total cost is net of 26 vessel dispositions ($243M of original cost)

(2)

Vessel count and total cost is net of 25 vessel dispositions ($227m of original cost)

The Largest Modern OSV Fleet in the Industry

Barclays CEO Energy-Power Conference

12 |

Count

Deepwater PSVs

26

Deepwater AHTSs

-

Towing Supply/Supply

6

Other

1

Total

33

Vessels Under Construction*

As of June 30, 2014

Estimated

delivery

schedule

–

13

in

FY

’15,

17

in

FY

‘16

and

3

thereafter.

CAPX

of

$391m

in

FY

’15,

$244m

in

FY

‘16

and

$50m

thereafter.

…and More to Come

Barclays CEO Energy-Power Conference

13 |

The Upgrading

of the Tidewater Fleet (A 10 Year Review)

Barclays CEO Energy-Power Conference

Deepwater PSV

Deepwater PSV

Deepwater AHTS

Deepwater AHTS

Towing Supply

Towing Supply

Fleet information includes active vessels only.

CIP=Construction in Process.

New Fleet is defined as vessels built or acquired since 2000.

Current

Future

Vintage

DWT

Fleet

CIP

Fleet

Fleet

5,000-6,000

16

5

21

0

4,000-4,999

11

15

26

0

3,000-3,999

43

6

49

0

<3,000

6

0

6

1

76

26

102

1

Current

Future

Vintage

BHP

Fleet

CIP

Fleet

Fleet

25,000+

5

0

5

0

13,500-16,500

7

0

7

0

12

0

12

0

Current

Future

Vintage

BHP

Fleet

CIP

Fleet

Fleet

7,000-10,000

36

6

42

0

3,000-6,999

69

0

69

9

105

6

111

9

14

New

Vintage

Total

DWT

Fleet

Fleet

Fleet

5,000-6,000

0

0

0

4,000-4,999

4

0

4

3,000-3,999

12

2

14

<3,000

6

4

10

22

6

28

New

Vintage

Total

BHP

Fleet

Fleet

Fleet

25,000+

1

0

1

13,500-16,500

6

3

9

7

3

10

New

Vintage

Total

BHP

Fleet

Fleet

Fleet

7,000-10,000

5

25

30

3,000-6,999

23

146

169

28

171

199

3/31/05 Snapshot

6/30/14 Snapshot |

CAPX Expected

to Decrease from Recent High Levels

Barclays CEO Energy-Power Conference

Fiscal Year

15

Fiscal 2014 is exclusive of Troms acquisition

Amounts

in

Fiscal

2015-2017

represent

known

CAPX

on

only

the

33 vessels and 2 ROVs under construction as of 6/30/14.

Additional CAPX could occur, but trendline is expected down. |

As of June 30,

2014 Cash & Cash Equivalents

$53 million

Total Debt

$1,511 million

Shareholders Equity

$2,717 million

Net Debt / Net Capitalization

35%

Total Debt / Capitalization

36%

~$650 million of available liquidity as of 6/30/14, including $600 million of

unused capacity under the company’s revolving credit facility.

Strong

Financial

Position

Provides

Strategic Optionality

Barclays CEO Energy-Power Conference

16 |

Debt Maturities

as of 6/30/14 Limited for Several Years

Barclays CEO Energy-Power Conference

Fiscal Year

17 |

**

EPS in Fiscal 2004 is exclusive of the $.30 per share after tax impairment charge. EPS in Fiscal 2006 is

exclusive of the $.74 per share after tax gain from the sale of six KMAR vessels. EPS in Fiscal

2007 is exclusive of $.37 per share of after tax gains from the sale of 14 offshore tugs. EPS in Fiscal 2010 is

exclusive of $.66 per share Venezuelan provision, a $.70 per share tax benefit related to

favorable resolution of tax litigation and a $0.22 per share charge for the proposed settlement

with the SEC of the company’s FCPA matter. EPS in Fiscal 2011 is exclusive of total $0.21 per share charges for settlements with

DOJ and Government of Nigeria for FCPA matters, a $0.08 per share charge related to participation in a

multi-company U.K.-based pension plan and a $0.06 per share impairment charge related to

certain vessels. EPS in Fiscal 2012 is exclusive of $0.43 per share goodwill impairment charge. EPS in Fiscal 2014 is

exclusive of $0.87 per share goodwill impairment charge.

Adjusted Return

On Avg. Equity 4.3% 7.2%

12.4%

18.9% 18.3%

19.5% 11.4% 5.0%

4.3% 5.9% 7.0%

Adjusted EPS**

Adjusted EPS**

History of Earnings Growth & Solid

Through-Cycle Return

Barclays CEO Energy-Power Conference

18 |

Impact of $7.4

million of retroactive revenue recorded in September 2012 quarter is excluded from 9/12 average dayrates and

included in the respective March 2012 and June 2012 quarterly average dayrates. Utilization

stats exclude stacked vessels. Active Vessel Dayrates & Utilization by Segment

Barclays CEO Energy-Power Conference

19 |

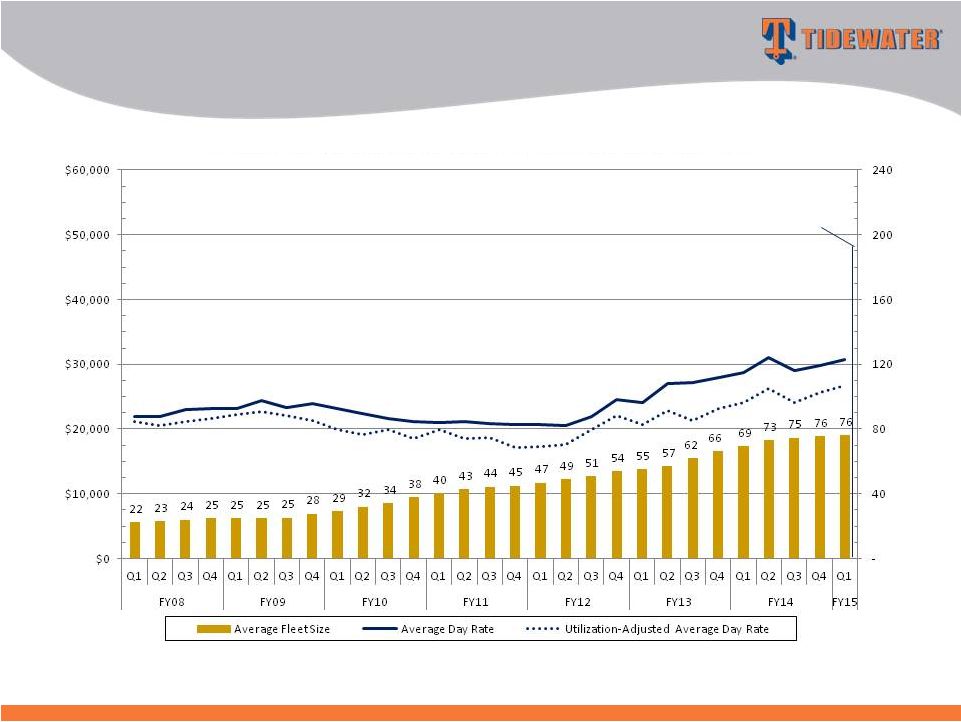

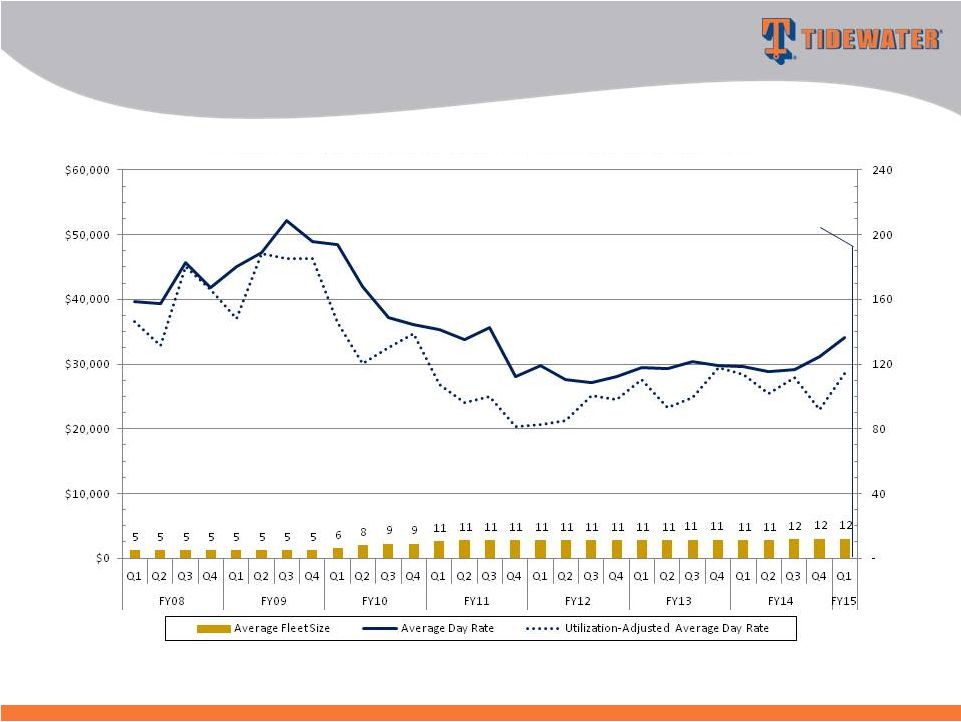

Q1 Fiscal 2015

Avg Day Rate: $30,802

Utilization: 86.8%

$185 million, or 49%, of Vessel Revenue in Q1 Fiscal 2015

New Vessel Trends by Vessel Type

Deepwater PSVs

Barclays CEO Energy-Power Conference

20

Average Day Rate, Adjusted Average Day Rate, and Average Fleet Size

|

Q1 Fiscal 2015

Avg Day Rate: $34,116

Utilization: 83.5%

$31 million, or 8%, of Vessel Revenue in Q1 Fiscal 2015

New Vessel Trends by Vessel Type

Deepwater AHTS

Barclays CEO Energy-Power Conference

21

Average Day Rate, Adjusted Average Day Rate, and Average Fleet Size

|

Q1 Fiscal 2015

Avg Day Rate: $15,519

Utilization: 84.9%

$126 million, or 33%, of Vessel Revenue in Q1 Fiscal 2015

New Vessel Trends by Vessel Type

Towing Supply/Supply Vessels

Barclays CEO Energy-Power Conference

22

Average Day Rate, Adjusted Average Day Rate, and Average Fleet Size

|

Recent delivery

of six work-class remotely operated vehicles (ROV),

and two more on order.

Tidewater’s New Subsea Business

Barclays CEO Energy-Power Conference

23 |

•

Continue to improve upon stellar safety and compliance programs

•

Maintain solid balance sheet and financial flexibility to deal with

industry uncertainties and seize opportunities when presented

•

Disciplined deployment of cash to expand vessel and ROV

fleet capabilities

•

Return capital to shareholders through dividends and

opportunistic share repurchases

Tidewater’s Future

Barclays CEO Energy-Power Conference

24 |

Barclays CEO

Energy-Power Conference September 4, 2014

Jeffrey M. Platt

President & CEO

Joseph M. Bennett

EVP & Chief IRO |

Appendix

Barclays CEO Energy-Power Conference

26 |

Maintain

Maintain

Financial Strength

Financial Strength

EVA-Based Investments

EVA-Based Investments

On Through-cycle Basis

On Through-cycle Basis

Deliver Results

Deliver Results

Financial Strategy Focused on Creating

Long-Term Shareholder Value

Barclays CEO Energy-Power Conference

27 |

Over a 15-year

period, Tidewater has invested ~$5.2 billion in CapEx, and paid out ~$1.3 billion through

dividends and share repurchases. Over the same period, CFFO and

proceeds from dispositions were ~$3.9

billion and ~$800 million, respectively.

$ in millions

CFFO

Fiscal Year

Fleet Renewal & Expansion Largely

Funded by CFFO

Barclays CEO Energy-Power Conference

28

$0

$100

$200

$300

$400

$500

$600

$700

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

CAPX

Dividend

Share Repurchase |

Note:

Vessel

operating

margin

is

defined

as

vessel

revenue

less

vessel

operating

expenses

Prior peak period (FY2009)

averaged quarterly revenue of

$339M, quarter operating

margin of $175.6M at 51.8%

Total Revenue and Margin

Fiscal 2008-2015

Barclays CEO Energy-Power Conference

29 |

Vessel Cash Operating

Margin ($) Vessel Cash Operating Margin (%)

$164 million Vessel Margin in Q1

FY2015 (99% from New Vessels)

Q1 FY2015 Vessel Margin: 43%

Cyclical Upturn should Drive Margin Expansion

Barclays CEO Energy-Power Conference

30 |

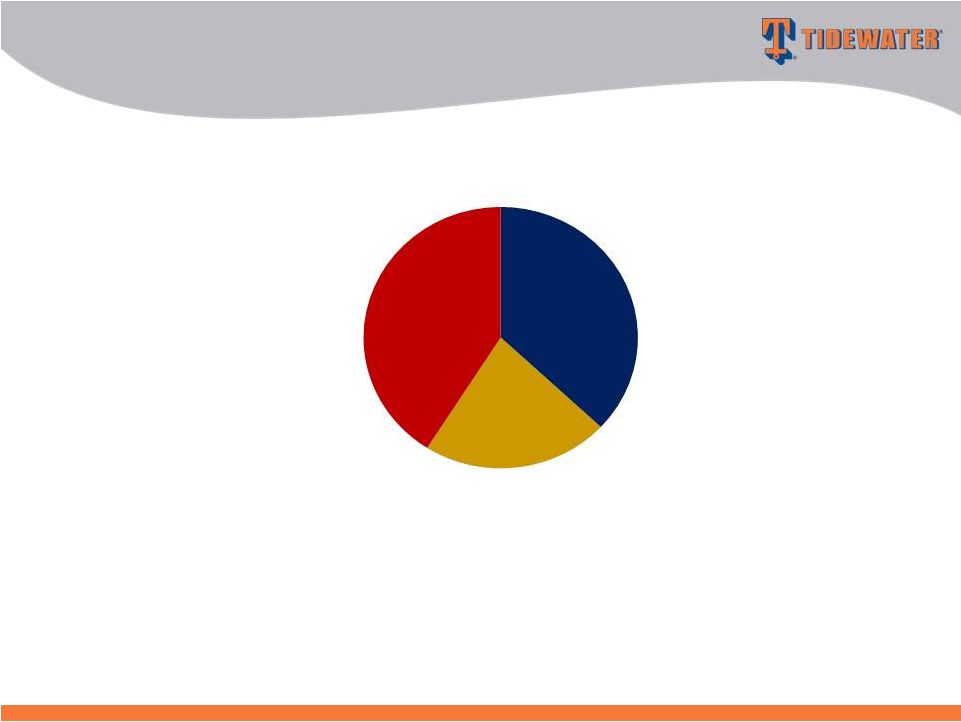

Our top 10 customers

in Fiscal 2014 (4 Super Majors, 4 NOC’s, 1 IOC’s and 1 independent) accounted for 62%

of our revenue Current Revenue Mix

Quality of Customer Base

Barclays CEO Energy-Power Conference

31

Super Majors

37%

NOC's

22%

Others

41% |