Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - CHC Group Ltd. | Financial_Report.xls |

| EX-31.2 - EXHIBIT-31.2 - CHC Group Ltd. | ex-312chcgroupltdq1fy15.htm |

| EX-32.2 - EXHIBIT-32.2 - CHC Group Ltd. | ex-322chcgroupltdq1fy15.htm |

| EX-32.1 - EXHIBIT-32.1 - CHC Group Ltd. | ex-321chcgroupltdq1fy15.htm |

| EX-31.1 - EXHIBIT-31.1 - CHC Group Ltd. | ex-311chcgroupltdq1fy15.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended July 31, 2014

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number: 001-36261

CHC Group Ltd.

(Exact name of registrant as specified in its charter)

Cayman Islands | 98-0587405 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

190 Elgin Avenue

George Town

Grand Cayman, KY1-9005

Cayman Islands

(Address of principal executive offices, zip code)

(604) 276-7500

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Accelerated filer | |

Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of July 31, 2014, there were 80,597,912 ordinary shares issued and outstanding, excluding unvested restricted shares of 744,501.

1

CHC GROUP LTD.

QUARTERLY REPORT ON FORM 10-Q

FOR THE QUARTER ENDED

July 31, 2014

TABLE OF CONTENTS

Page Number | ||

ITEM 1. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

ITEM 1. | ||

ITEM 1A. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

ITEM 5. | ||

ITEM 6. | ||

2

PART I—FINANCIAL INFORMATION

TRADEMARKS

CHC Helicopter and the CHC Helicopter logo are trademarks of CHC Capital (Barbados) Ltd, a wholly owned subsidiary of CHC Group Ltd. All other trademarks and service marks appearing in this Quarterly Report on Form 10-Q are the property of their respective holders. All rights reserved. The absence of a trademark or service mark or logo from this Quarterly Report on Form 10-Q does not constitute a waiver of trademark or other intellectual property rights of CHC Group Ltd., its subsidiaries, affiliates, licensors or any other persons.

GLOSSARY

Deepwater | Water depths of approximately 4,500 feet to 7,499 feet. |

Embedded equity | Embedded equity, an intangible asset, represents the amount by which the estimated market value of a leased helicopter exceeded the leased helicopter purchase option price at September 16, 2008, the acquisition date of the predecessor of our wholly owned subsidiary by First Reserve Management, L.P. (or First Reserve). Embedded equity is assessed on an ongoing basis for impairment. Impairment, if any, is recognized in the consolidated statements of operations. |

EMS | Emergency medical services. |

Heavy helicopter | A category of twin-engine helicopters that requires two pilots, can accommodate 16 to 26 passengers and can operate under instrument flight rules, which allow daytime and nighttime flying in a variety of weather conditions. The greater passenger capacity, larger cabin, longer flight range, and ability to operate in adverse weather conditions make heavy helicopters more suitable than single engine helicopters for offshore support. Heavy helicopters are generally utilized to support the oil and gas sector, construction and forestry industries and SAR and EMS customer requirements. |

Average HE count | Our heavy and medium helicopters, including owned and leased, are weighted at 100% and 50%, respectively, to arrive at a single HE count, excluding helicopters that are expected to be retired from the fleet. The average HE count for a period is calculated using a weighted average of the HE count for the beginning and end of each quarter included in that period. |

HE Rate | The Heavy Equivalent Rate, or the HE Rate, is the third-party operating revenue from the Helicopter Services segment (excluding reimbursable revenue) divided by a weighted average factor corresponding to the number of heavy and medium helicopters in our fleet. |

Long-term contracts | Contracts of three years or longer in duration. |

Medium helicopter | A category of twin-engine helicopters that generally requires two pilots, can accommodate eight to 15 passengers and can operate under instrument flight rules, which allow daytime and nighttime flying in a variety of weather conditions. The greater passenger capacity, longer flight range, and ability to operate in adverse weather conditions make medium helicopters more suitable than single engine helicopters for offshore support. Medium helicopters are generally utilized to support the oil and gas sector, construction and forestry industries and SAR and EMS customer bases in certain jurisdictions. Medium helicopters can also be used to support the utility and mining sectors, as well as certain parts of the construction and forestry industries, where transporting a smaller number of passengers or carrying light loads over shorter distances is required. |

MRO | Maintenance, repair and overhaul. |

New technology | When used herein to classify our helicopters, a category of higher-value, recently produced, more sophisticated and more comfortable helicopters, including Airbus Helicopters (formerly Eurocopter) EC225, EC135, EC145 and EC155; AgustaWestland’s AW139; and Sikorsky’s S76C+, S76C++ and S92A. |

OEM | Original equipment manufacturer. |

3

PBH | Power-by-the-hour. A program where a helicopter operator pays a fee per flight hour to an MRO provider as compensation for repair and overhaul of components required in order for the helicopter to maintain an airworthy condition. |

Rotables | Helicopter parts that can be repaired and reused such that they typically have an expected life approximately equal to the helicopters they support. |

SAR | Search and rescue. |

Ultra-deepwater | Water depths of approximately 7,500 feet or more. |

4

ITEM 1. FINANCIAL STATEMENTS

CHC Group Ltd.

Consolidated Balance Sheets

(Expressed in thousands of United States dollars except share and per share information)

(Unaudited)

April 30, 2014 | July 31, 2014 | ||||||

Assets | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 302,522 | $ | 119,928 | |||

Receivables, net of allowance for doubtful accounts of $2.3 million and $2.8 million, respectively | 292,339 | 292,109 | |||||

Income taxes receivable | 28,172 | 30,559 | |||||

Deferred income tax assets | 60 | 128 | |||||

Inventories (note 4) | 130,891 | 133,611 | |||||

Prepaid expenses | 27,683 | 29,953 | |||||

Other assets (note 5) | 49,209 | 48,444 | |||||

830,876 | 654,732 | ||||||

Property and equipment, net | 1,050,759 | 1,062,975 | |||||

Investments | 31,351 | 33,202 | |||||

Intangible assets | 177,863 | 175,984 | |||||

Goodwill | 432,376 | 426,410 | |||||

Restricted cash | 31,566 | 29,462 | |||||

Other assets (note 5) | 519,306 | 518,944 | |||||

Deferred income tax assets | 3,381 | 2,925 | |||||

Assets held for sale (note 3) | 26,849 | 28,866 | |||||

$ | 3,104,327 | $ | 2,933,500 | ||||

Liabilities and Shareholders' Equity | |||||||

Current liabilities: | |||||||

Payables and accruals | $ | 355,341 | $ | 341,197 | |||

Deferred revenue | 30,436 | 38,988 | |||||

Income taxes payable | 41,975 | 43,690 | |||||

Deferred income tax liabilities | 98 | 157 | |||||

Current facility secured by accounts receivable (note 2) | 62,596 | 51,749 | |||||

Other liabilities (note 6) | 55,170 | 54,507 | |||||

Current portion of long-term debt obligations (note 7) | 4,107 | 3,654 | |||||

549,723 | 533,942 | ||||||

Long-term debt obligations (note 7) | 1,546,155 | 1,480,604 | |||||

Deferred revenue | 81,485 | 79,863 | |||||

Other liabilities (note 6) | 287,385 | 273,889 | |||||

Deferred income tax liabilities | 10,665 | 11,009 | |||||

Total liabilities | 2,475,413 | 2,379,307 | |||||

Redeemable non-controlling interests (note 2) | (22,578 | ) | (15,216 | ) | |||

Capital stock: Par value $0.0001 (note 9): | |||||||

Authorized: 2,000,000,000; Issued: 80,519,484 and 80,597,912 | 8 | 8 | |||||

Additional paid-in capital (notes 9 and 10) | 2,039,371 | 2,042,602 | |||||

Deficit | (1,265,103 | ) | (1,307,203 | ) | |||

Accumulated other comprehensive loss | (122,784 | ) | (165,998 | ) | |||

651,492 | 569,409 | ||||||

$ | 3,104,327 | $ | 2,933,500 | ||||

See accompanying notes to interim consolidated financial statements.

See table in Note 2(a)(i) for certain amounts included in the Consolidated Balance Sheets related to variable interest entities.

5

CHC Group Ltd.

Consolidated Statements of Operations

(Expressed in thousands of United States dollars except share and per share information)

(Unaudited)

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Revenue | $ | 414,931 | $ | 460,648 | |||

Operating expenses: | |||||||

Direct costs | (343,106 | ) | (394,547 | ) | |||

Earnings from equity accounted investees | 2,391 | 2,677 | |||||

General and administration costs | (18,116 | ) | (21,662 | ) | |||

Depreciation | (32,057 | ) | (33,725 | ) | |||

Asset impairments (notes 3 and 5) | (7,324 | ) | (275 | ) | |||

Loss on disposal of assets | (1,122 | ) | (5,259 | ) | |||

(399,334 | ) | (452,791 | ) | ||||

Operating income | 15,597 | 7,857 | |||||

Interest on long-term debt | (38,708 | ) | (34,872 | ) | |||

Foreign exchange gain (loss) | (13,087 | ) | 4,908 | ||||

Other financing income (charges) (note 8) | 5,823 | (4,325 | ) | ||||

Loss before income tax | (30,375 | ) | (26,432 | ) | |||

Income tax expense (note 11) | (5,308 | ) | (7,887 | ) | |||

Net loss | $ | (35,683 | ) | $ | (34,319 | ) | |

Net earnings (loss) attributable to: | |||||||

Controlling interest | $ | (38,331 | ) | $ | (42,100 | ) | |

Non-controlling interests | 2,648 | 7,781 | |||||

Net loss | $ | (35,683 | ) | $ | (34,319 | ) | |

Net loss per ordinary share attributable to controlling interest - basic and diluted (note 9) | $ | (0.82 | ) | $ | (0.52 | ) | |

Weighted average number of shares outstanding - basic and diluted | 46,519,484 | 80,530,687 | |||||

See accompanying notes to interim consolidated financial statements.

6

CHC Group Ltd.

Consolidated Statements of Comprehensive Loss

(Expressed in thousands of United States dollars)

(Unaudited)

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Net loss | $ | (35,683 | ) | $ | (34,319 | ) | |

Other comprehensive income (loss): | |||||||

Net foreign currency translation adjustments | (28,037 | ) | (44,202 | ) | |||

Net change in defined benefit pension plan, net of income tax | 343 | 374 | |||||

Comprehensive loss | $ | (63,377 | ) | $ | (78,147 | ) | |

Comprehensive income (loss) attributable to: | |||||||

Controlling interest | $ | (65,433 | ) | $ | (85,314 | ) | |

Non-controlling interests | 2,056 | 7,167 | |||||

Comprehensive loss | $ | (63,377 | ) | $ | (78,147 | ) | |

See accompanying notes to interim consolidated financial statements.

7

CHC Group Ltd.

Consolidated Statements of Cash Flows

(Expressed in thousands of United States dollars)

(Unaudited)

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Cash provided by (used in): | |||||||

Operating activities: | |||||||

Net loss | $ | (35,683 | ) | $ | (34,319 | ) | |

Adjustments to reconcile net loss to cash flows provided by (used in) operating activities: | |||||||

Depreciation | 32,057 | 33,725 | |||||

Loss on disposal of assets | 1,122 | 5,259 | |||||

Asset impairments | 7,324 | 275 | |||||

Earnings from equity accounted investees less dividends received | (2,391 | ) | (2,174 | ) | |||

Deferred income taxes | 1,613 | 1,065 | |||||

Non-cash stock-based compensation expense | 117 | 3,231 | |||||

Amortization of lease related fixed interest rate obligations | (547 | ) | (91 | ) | |||

Amortization of long-term debt and lease deferred financing costs and debt extinguishment | 2,595 | 10,017 | |||||

Non-cash accrued interest income on funded residual value guarantees | (1,712 | ) | (1,348 | ) | |||

Mark to market gain on derivative instruments | (14,764 | ) | (8,408 | ) | |||

Non-cash defined benefit pension expense (income) (note 12) | 98 | (207 | ) | ||||

Defined benefit contributions and benefits paid | (17,686 | ) | (17,127 | ) | |||

Increase to deferred lease financing costs | (1,724 | ) | (1,278 | ) | |||

Unrealized loss (gain) on foreign currency exchange translation | 8,937 | (5,990 | ) | ||||

Other | 3,044 | 1,215 | |||||

Decrease in cash resulting from changes in operating assets and liabilities (note 14) | (26,671 | ) | (15,090 | ) | |||

Cash used in operating activities | (44,271 | ) | (31,245 | ) | |||

Financing activities: | |||||||

Sold interest in accounts receivable, net of collections | (6,446 | ) | (9,146 | ) | |||

Proceeds from issuance of senior unsecured notes | 300,000 | — | |||||

Long-term debt proceeds | 100,000 | 70,000 | |||||

Long-term debt repayments | (225,948 | ) | (71,371 | ) | |||

Redemption of senior secured notes | — | (70,620 | ) | ||||

Increase in deferred financing costs | (5,902 | ) | — | ||||

Related party loans (note 16(c)) | (25,148 | ) | — | ||||

Cash provided by (used in) financing activities | 136,556 | (81,137 | ) | ||||

Investing activities: | |||||||

Property and equipment additions | (104,385 | ) | (125,879 | ) | |||

Proceeds from disposal of property and equipment | 46,163 | 69,198 | |||||

Helicopter deposits net of lease inception refunds | (27,947 | ) | (14,780 | ) | |||

Restricted cash | (4,852 | ) | 1,605 | ||||

Cash used in investing activities | (91,021 | ) | (69,856 | ) | |||

Effect of exchange rate changes on cash and cash equivalents | (10,410 | ) | (356 | ) | |||

Change in cash and cash equivalents during the period | (9,146 | ) | (182,594 | ) | |||

Cash and cash equivalents, beginning of period | 123,801 | 302,522 | |||||

Cash and cash equivalents, end of period | $ | 114,655 | $ | 119,928 | |||

8

CHC Group Ltd.

Consolidated Statements of Shareholders' Equity (note 9)

(Expressed in thousands of United States dollars)

(Unaudited)

Three months ended July 31, 2013 | Capital stock | Additional paid-in capital | Deficit | Accumulated other comprehensive loss | Total shareholders' equity | Redeemable non- controlling interests | |||||||||||||||||

April 30, 2013 | $ | 5 | $ | 1,696,066 | $ | (1,092,555 | ) | $ | (89,835 | ) | $ | 513,681 | $ | (8,262 | ) | ||||||||

Foreign currency translation | — | — | — | (27,120 | ) | (27,120 | ) | (917 | ) | ||||||||||||||

Stock-based compensation expense (note 10) | — | 117 | — | — | 117 | — | |||||||||||||||||

Defined benefit plan, net of income tax | — | — | — | 18 | 18 | 325 | |||||||||||||||||

Net earnings (loss) | — | — | (38,331 | ) | — | (38,331 | ) | 2,648 | |||||||||||||||

July 31, 2013 | $ | 5 | $ | 1,696,183 | $ | (1,130,886 | ) | $ | (116,937 | ) | $ | 448,365 | $ | (6,206 | ) | ||||||||

Three months ended July 31, 2014 | Capital stock | Additional paid-in capital | Deficit | Accumulated other comprehensive loss | Total shareholders' equity | Redeemable non- controlling interests | |||||||||||||||||

April 30, 2014 | $ | 8 | $ | 2,039,371 | $ | (1,265,103 | ) | $ | (122,784 | ) | $ | 651,492 | $ | (22,578 | ) | ||||||||

Capital contribution by shareholder (note 2) | — | — | — | — | — | 195 | |||||||||||||||||

Foreign currency translation | — | — | — | (43,443 | ) | (43,443 | ) | (759 | ) | ||||||||||||||

Stock-based compensation expense (note 10) | — | 3,231 | — | — | 3,231 | — | |||||||||||||||||

Defined benefit plan, net of income tax | — | — | — | 229 | 229 | 145 | |||||||||||||||||

Net earnings (loss) | — | — | (42,100 | ) | — | (42,100 | ) | 7,781 | |||||||||||||||

July 31, 2014 | $ | 8 | $ | 2,042,602 | $ | (1,307,203 | ) | $ | (165,998 | ) | $ | 569,409 | $ | (15,216 | ) | ||||||||

See accompanying notes to interim consolidated financial statements.

9

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

1. | Significant accounting policies: |

(a) | Basis of presentation: |

The unaudited interim consolidated financial statements (“interim financial statements”) include the accounts of CHC Group Ltd. and its subsidiaries (the “Company”, “we”, “us” or “our”) after elimination of all significant intercompany accounts and transactions. The interim financial statements are presented in United States dollars and have been prepared in accordance with the United States Generally Accepted Accounting Principles (“US GAAP”) for interim financial information. Accordingly, the interim financial statements do not include all of the information and disclosures for complete financial statements.

In the opinion of management, these financial statements contain all adjustments, consisting of normal recurring accruals, necessary to present fairly the financial position, results of operations and cash flows for the periods indicated. Results of operations for the periods presented are not necessarily indicative of results of operations for the entire year.

The financial information as of April 30, 2014 is derived from our annual audited consolidated financial statements and notes for the fiscal year ended April 30, 2014. These interim financial statements should be read in conjunction with our consolidated financial statements and related notes for the fiscal year ended April 30, 2014, which are included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014 which was filed with the SEC on July 10, 2014.

(b) | Foreign currency: |

The currencies which most influence our foreign currency translations and the relevant exchange rates were:

Three months ended | |||||

July 31, 2013 | July 31, 2014 | ||||

Average rates: | |||||

£/US $ | 1.531101 | 1.693993 | |||

CAD/US $ | 0.970403 | 0.924214 | |||

NOK/US $ | 0.169238 | 0.164972 | |||

AUD/US $ | 0.949830 | 0.934843 | |||

€/US $ | 1.308394 | 1.361830 | |||

Period end rates: | |||||

£/US $ | 1.518227 | 1.688797 | |||

CAD/US $ | 0.972101 | 0.918274 | |||

NOK/US $ | 0.169340 | 0.159045 | |||

AUD/US $ | 0.895888 | 0.930028 | |||

€/US $ | 1.329348 | 1.338935 | |||

10

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

1. | Significant accounting policies (continued): |

(c) Recent accounting pronouncements adopted in the year:

On May 1, 2014, we adopted the accounting guidance on the financial statement presentation of an unrecognized tax benefit when a net operating loss carryforward, similar tax loss or tax credit carryforward exists. This new guidance did not have an impact on our consolidated financial statements.

(d) Recent accounting pronouncements not yet adopted:

Revenue recognition:

In May 2014, the FASB issued a comprehensive new revenue recognition standard which will supersede previous existing revenue recognition guidance. The standard creates a five-step model for revenue recognition to achieve the objective of recognizing revenue to depict the transfer of goods or services to a customer at an amount that reflects the consideration it expects to receive in exchange for those goods or services. The five-step model includes (1) identifying the contract, (2) identifying the separate performance obligations in the contract, (3) determining the transaction price, (4) allocating the transaction price to the separate performance obligations and (5) recognizing revenue when each performance obligation has been satisfied. The standard also requires expanded disclosures surrounding revenue recognition. The standard is effective for fiscal periods beginning after December 15, 2016 and early adoption is not permitted. Accordingly, we will adopt the standard on May 1, 2017. Companies are allowed to use either full retrospective or modified retrospective adoption. We are currently evaluating which transition approach to use and the impact of the adoption of this standard on our consolidated financial statements.

Share-based compensation:

In June 2014, the FASB issued guidance for accounting for share-based payments when the terms of an award provide that a performance target could be achieved after the requisite service period. The amendment requires that a performance target that effects vesting and that could be achieved after requisite service period be treated as a performance condition. The performance target should not be reflected in estimating the grant-date fair value of the award. Compensation cost should be recognized in the period in which it becomes probable that such performance condition would be achieved and should represent the compensation cost attributable to the period(s) for which the requisite service has already been rendered. The requisite service period ends when the employee can cease rendering service and still be eligible to vest in the award if the performance target is achieved. The standard is effective for fiscal periods beginning after December 15, 2015, and interim periods therein and early application is permitted. We will adopt the standard on May 1, 2016. We are currently evaluating the impact of the adoption of this standard on our consolidated financial statements.

Going concern:

In August 2014, the FASB issued a new standard that requires management to evaluate whether there are conditions or events that raise substantial doubt about an entity’s ability to continue as a going concern and to provide disclosures when certain criteria are met. The standard is effective for fiscal periods beginning after December 15, 2016, and interim periods therein and early application is permitted. We will adopt the standard on May 1, 2017. We do not expect the standard to have a material impact on our consolidated financial statements.

11

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

2. | Variable interest entities: |

(a) VIEs of which we are the primary beneficiary:

(i) Local ownership VIEs:

Certain areas of operations are subject to local governmental regulations that may limit foreign ownership of aviation companies. Accordingly, operations in certain jurisdictions may require the establishment of local ownership entities that are considered to be VIEs. The nature of our involvement with consolidated local ownership entities is as follows:

Note 3 to the consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014 contains a description of our principal involvement with VIEs and the accounting policies regarding determination of whether we are deemed to be the primary beneficiary. As of July 31, 2014, there have been no significant changes in either the nature of our involvement with, or the accounting policies associated with the analysis of, VIEs as described in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014.

The following table shows the redeemable non-controlling interests relating to the local ownership VIEs that are included in the consolidated financial statements.

April 30, 2014 | July 31, 2014 | ||||||

EEA Helicopters Operations B.V. | $ | (24,100 | ) | $ | (16,933 | ) | |

Atlantic Aviation Limited and Atlantic Aviation FZE | 1,522 | 1,717 | |||||

$ | (22,578 | ) | $ | (15,216 | ) | ||

Financial information of local ownership VIEs

All of the local ownership VIEs and their subsidiaries have the same purpose and are exposed to similar operational risks and are monitored on a similar basis by management. As such, the financial information reflected on the consolidated balance sheets and statements of operations for all local ownership VIEs has been presented in the aggregate below, including intercompany amounts with other consolidated entities:

April 30, 2014 | July 31, 2014 | ||||||

Cash and cash equivalents | $ | 61,272 | $ | 2,772 | |||

Receivables, net of allowance | 95,899 | 100,859 | |||||

Other current assets | 59,883 | 59,096 | |||||

Goodwill | 72,899 | 72,932 | |||||

Other long-term assets | 127,637 | 138,770 | |||||

Total assets | $ | 417,590 | $ | 374,429 | |||

Payables and accruals | $ | 115,686 | $ | 98,252 | |||

Intercompany payables | 305,843 | 185,764 | |||||

Other current liabilities | 36,111 | 28,993 | |||||

Accrued pension obligations | 67,410 | 60,558 | |||||

Long-term intercompany payables | 15,900 | 115,384 | |||||

Other long-term liabilities | 51,498 | 48,656 | |||||

Total liabilities | $ | 592,448 | $ | 537,607 | |||

12

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

2. | Variable interest entities (continued): |

(a) VIEs of which we are the primary beneficiary (continued):

(i) Local ownership VIEs (continued):

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Revenue | $ | 256,178 | $ | 300,506 | |||

Net earnings (loss) | (3,025 | ) | 13,701 | ||||

(ii) Accounts receivable securitization:

As described in Note 3(a)(ii) of the consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014, we enter into trade receivables securitization transactions to raise financing, through the sale of pools of receivables, or beneficial interests therein, to a VIE, Finacity Receivables – CHC 2009, LLC (“Finacity”), which we have determined we are required to consolidate as we are the primary beneficiary.

The following table shows the assets and the associated liabilities related to our secured debt arrangements that are included in the consolidated financial statements:

April 30, 2014 | July 31, 2014 | ||||||

Restricted cash | $ | 7,339 | $ | 10,238 | |||

Transferred receivables | 83,022 | 73,085 | |||||

Current facility secured by accounts receivable | 62,596 | 51,749 | |||||

(iii) Trinity Helicopters Limited:

As at July 31, 2014, we leased two helicopters from Trinity Helicopters Limited (“Trinity”), an entity considered to be a VIE.

(b) | VIEs of which we are not the primary beneficiary: |

(i) Local ownership VIEs:

Thai Aviation Services (“TAS”)

As described in Note 3(b)(i) of the consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014, we have a 29.9% interest in the ordinary shares of TAS, which we have determined to be a VIE that we are not required to consolidate as we are not the primary beneficiary.

The following table summarizes the amounts recorded for TAS in the consolidated balance sheets:

April 30, 2014 | July 31, 2014 | ||||||||||||||

Carrying amounts | Maximum exposure to loss | Carrying amounts | Maximum exposure to loss | ||||||||||||

Receivables, net of allowances | $ | 4,962 | $ | 4,962 | $ | 8,360 | $ | 8,360 | |||||||

Equity method investment | 21,548 | 21,548 | 23,792 | 23,792 | |||||||||||

As of July 31, 2013 and 2014, we leased nine and eight helicopters to TAS and provided crew, insurance, maintenance and base services. The total revenue earned from providing these services was $12.2 million, and $12.4 million for the three months ended July 31, 2013 and 2014, respectively.

13

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

2. | Variable interest entities (continued): |

(b)VIEs of which we are not the primary beneficiary:

(ii)Leasing entities:

Related party lessors

The lessor VIEs are considered related parties because they are partially financed through equity contributions from entities that have also invested in us. We have determined that the activity that most significantly impacts the economic performance of the related party lessor VIEs is the remarketing of the helicopter at the end of the lease term. As we do not have the power to make remarketing decisions, we have determined that we are not the primary beneficiary of the lessor VIEs.

As at July 31, 2013 and 2014, we had operating lease agreements for the lease of 31 helicopters and 31 helicopters, respectively, from individual related party entities considered to be VIEs. These transactions are carried out on an arm’s-length basis and are recorded at the exchange amounts.

The following table summarizes the amounts recorded in the consolidated statements of operations:

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Operating lease expense | $ | 12,621 | $ | 12,584 | |||

The following table summarizes the amounts recorded in the consolidated balance sheets:

April 30, 2014 | July 31, 2014 | ||||||

Payables and accruals | $ | 3,532 | $ | 3,694 | |||

Accounts receivable | 12,610 | 5,130 | |||||

Other VIE lessors

We have determined that the activity that most significantly impacts the economic performance of the lessor VIEs is the remarketing of the helicopters at the end of the lease term. As we do not have the power to make remarketing decisions, we have determined that we are not the primary beneficiary of the lessor VIEs.

As at July 31, 2013, we leased 26 helicopters from three different entities considered to be VIEs. As at July 31, 2014, we leased 65 helicopters from seven different entities considered to be VIEs. All 26 and 65 leases were considered to be operating leases as at July 31, 2013 and 2014, respectively.

14

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

3. | Assets held for sale: |

We have classified certain assets such as helicopters and buildings as held for sale as these assets are ready for immediate sale and management expects these assets to be sold within one year.

April 30, 2014 | July 31, 2014 | ||||||||||||

# Helicopters | # Helicopters | ||||||||||||

Helicopters held for sale: | |||||||||||||

Book value, beginning of period | 14 | $ | 30,206 | 11 | $ | 25,426 | |||||||

Classified as held for sale, net of impairment | 15 | 28,461 | 2 | 5,320 | |||||||||

Sales | (8 | ) | (18,369 | ) | (2 | ) | (7,000 | ) | |||||

Reclassified as held for use | (10 | ) | (14,264 | ) | (1 | ) | (490 | ) | |||||

Foreign exchange | (608 | ) | (177 | ) | |||||||||

Helicopters held for sale | 11 | 25,426 | 10 | 23,079 | |||||||||

Buildings held for sale | — | 1,423 | — | 5,787 | |||||||||

Total assets held for sale | $ | 26,849 | $ | 28,866 | |||||||||

The helicopters classified as held for sale are older technology helicopters that are being divested by us. The buildings classified as held for sale are the result of the buildings no longer being used in operations. During the three months ended July 31, 2014, one helicopter was reclassified to assets held for use as management determined that we would obtain a higher value from using this helicopter as parts within the business than selling it in the external market.

During the three months ended July 31, 2013 and 2014, we recorded impairment charges of $7.1 million and $0.2 million to write down the carrying value of 10 helicopters and two helicopters held for sale to their fair value less costs to sell, respectively. These amounts are included in asset impairments on the consolidated statements of operations. The fair value of assets held for sale is considered a Level 2 measurement in the fair value hierarchy as the measurement is based on third-party appraisals using market data.

4. | Inventories: |

April 30, 2014 | July 31, 2014 | ||||||

Work-in-progress for long-term maintenance contracts under completed contract accounting | $ | 3,790 | $ | 6,049 | |||

Consumables | 136,036 | 135,885 | |||||

Provision for obsolescence | (8,935 | ) | (8,323 | ) | |||

$ | 130,891 | $ | 133,611 | ||||

15

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

5. | Other assets: |

April 30, 2014 | July 31, 2014 | ||||||

Current: | |||||||

Helicopter operating lease funded residual value guarantees (a) | $ | 6,845 | $ | 12,695 | |||

Deferred financing costs | 8,986 | 8,978 | |||||

Mobilization costs | 8,776 | 10,532 | |||||

Residual value guarantee | 4,007 | 3,941 | |||||

Foreign currency embedded derivatives and forward contracts (note 13) | 3,111 | 2,081 | |||||

Prepaid helicopter rentals | 4,874 | 5,087 | |||||

Related party receivable (note 2(b)(ii)) | 12,610 | 5,130 | |||||

$ | 49,209 | $ | 48,444 | ||||

Non-current: | |||||||

Helicopter operating lease funded residual value guarantees (a) | $ | 208,870 | $ | 207,775 | |||

Helicopter deposits | 99,372 | 94,092 | |||||

Accrued pension asset | 45,816 | 53,446 | |||||

Deferred financing costs | 57,297 | 54,033 | |||||

Mobilization costs | 26,238 | 23,469 | |||||

Residual value guarantee | 15,695 | 14,722 | |||||

Security deposits | 34,923 | 36,591 | |||||

Pension guarantee assets | 9,835 | 9,304 | |||||

Prepaid helicopter rentals | 16,327 | 17,344 | |||||

Foreign currency embedded derivatives and forward contracts (note 13) | 3,624 | 7,131 | |||||

Other | 1,309 | 1,037 | |||||

$ | 519,306 | $ | 518,944 | ||||

(a) | Helicopter operating lease funded residual value guarantees: |

We believe that the helicopters will realize a value upon sale at the end of the lease terms sufficient to recover the carrying value of these guarantees, including accrued interest. In the event that helicopter values decline such that we do not believe funded residual value guarantees are recoverable, an impairment is recorded. No impairment was recorded for the three months ended July 31, 2013 and 2014.

16

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

6. | Other liabilities: |

April 30, 2014 | July 31, 2014 | ||||||

Current: | |||||||

Foreign currency embedded derivatives and foreign currency contracts (note 13) | $ | 16,057 | $ | 14,377 | |||

Deferred gains on sale-leasebacks of helicopters | 13,284 | 13,644 | |||||

Residual value guarantees | 524 | 1,204 | |||||

Contract inducement | 802 | 792 | |||||

Deferred helicopter proceeds | 23,347 | 23,448 | |||||

Other | 1,156 | 1,042 | |||||

$ | 55,170 | $ | 54,507 | ||||

Non-current: | |||||||

Accrued pension obligations | 122,430 | 114,760 | |||||

Deferred gains on sale-leasebacks of helicopters | 93,756 | 93,016 | |||||

Residual value guarantees | 28,359 | 27,679 | |||||

Foreign currency embedded derivatives and foreign currency contracts (note 13) | 13,317 | 9,367 | |||||

Insurance claims accrual | 11,809 | 12,656 | |||||

Contract inducement | 8,590 | 8,283 | |||||

Other | 9,124 | 8,128 | |||||

$ | 287,385 | $ | 273,889 | ||||

7. | Long-term debt obligations: |

Principal Repayment terms | Facility maturity dates | April 30, 2014 | July 31, 2014 | ||||||||

Senior secured notes (a) | At maturity | October 2020 | $ | 1,159,675 | $ | 1,095,528 | |||||

Senior unsecured notes | At maturity | June 2021 | 300,000 | 300,000 | |||||||

Other term loans: | |||||||||||

Airbus Helicopters Loan - 2.50% | At maturity | December 2015 | 2,417 | 2,349 | |||||||

EDC-B.A. CDOR rate (6 month) plus a 0.8% margin | Semi-annually | June 2014 | 495 | — | |||||||

Capital lease obligations | Quarterly | October 2017 - September 2025 | 55,780 | 54,461 | |||||||

Boundary Bay financing – 6.93% | Monthly | April 2035 | 31,895 | 31,920 | |||||||

Total long-term debt obligations | 1,550,262 | 1,484,258 | |||||||||

Less: current portion | (4,107 | ) | (3,654 | ) | |||||||

Long-term debt obligations | $ | 1,546,155 | $ | 1,480,604 | |||||||

17

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

7. | Long-term debt obligations (continued): |

(a) Senior secured notes:

During May 2014, one of our subsidiaries purchased $65.0 million of the senior secured notes on the open market at premiums ranging from 8.00% to 9.13% of the principal plus accrued and unpaid interest of $0.6 million. A loss on extinguishment of $7.4 million related to the redemption premium, the unamortized net discount on the secured notes and the unamortized deferred financing costs was recognized.

At July 31, 2014, we were in compliance with all long-term debt obligations covenants.

8. | Other financing income (charges): |

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Amortization of deferred financing costs | $ | (3,758 | ) | $ | (1,887 | ) | |

Loss on debt extinguishment | — | (7,444 | ) | ||||

Net gain on fair value of derivative financial instruments | 14,227 | 7,503 | |||||

Amortization of guaranteed residual values | (1,608 | ) | (1,041 | ) | |||

Interest expense | (5,268 | ) | (5,163 | ) | |||

Interest income | 4,057 | 6,090 | |||||

Other | (1,827 | ) | (2,383 | ) | |||

$ | 5,823 | $ | (4,325 | ) | |||

9. | Capital stock and net loss per ordinary share: |

Capital Stock:

On January 3, 2014, the majority shareholder of the Company approved the following capital stock restructuring transactions which were effective immediately:

• | a subdivision of the authorized and issued ordinary shares of capital stock by a factor of 10,000 increasing the authorized and issued ordinary shares of capital stock to 20,000,000,000,000 and 18,607,793,610,000, respectively, while reducing the par value per share from $1.00 to $0.0001; |

• | the surrender of 18,607,747,090,516 of the issued ordinary shares of capital stock resulting in the issued ordinary shares of capital stock being reduced to 46,519,484, each with a par value of $0.0001; |

• | the cancellation of 19,998,500,000,000 of the unissued authorized ordinary shares of capital stock, reducing the authorized capital stock to 1,500,000,000, each with a par value of $0.0001; and |

• | the increase of the authorized capital stock by $50,000 (such increase being in the form of 500,000,000 preferred shares of capital stock, each with a par value of $0.0001) resulting in an aggregate authorized capital stock of $200,000 divided into 1,500,000,000 ordinary shares of capital stock, each with a par value of $0.0001 and 500,000,000 preferred shares of capital stock with a par value of $0.0001. |

All capital stock and additional paid-in capital amounts and per share information reflects the consummation of the above capital stock restructuring transactions. Such adjustments include calculations of our weighted average number of ordinary stock and net loss per ordinary share.

18

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

9. | Capital stock and net loss per ordinary share (continued): |

On January 16, 2014, we completed the initial public offering, or IPO, of 31,000,000 ordinary shares of capital stock at a price of $10.00 per share, raising approximately $289.4 million, net of underwriting costs of $16.3 million and other costs directly related to the IPO of $4.3 million. The net proceeds were allocated $3.1 thousand to the capital stock of the Company and $289.4 million to additional paid-in capital.

On February 20, 2014, the underwriters in our IPO exercised an option to purchase 3,000,000 ordinary shares of capital stock at a price of $10.00 per share, raising approximately $28.4 million, net of underwriting costs of $1.6 million. The net proceeds were allocated $28.4 million to additional paid-in capital.

As described in Note 10(b), 78,428 ordinary shares of capital stock were issued on the exercise and net settlement of service vesting stock options and service vesting shares during the three months ended July 31, 2014.

Net loss per ordinary share:

The following table sets forth the computation of basic and diluted net loss per ordinary share:

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Loss attributable to controlling interest | $ | (38,331 | ) | $ | (42,100 | ) | |

Weighted average number of ordinary stock outstanding – basic and diluted | 46,519,484 | 80,530,687 | |||||

Details of our stock based compensation plans are presented in Note 10 of these interim consolidated financial statements. Securities potentially issuable as part of these plans were not included in the computation of diluted loss per ordinary share because to do so would have been antidilutive for the periods presented.

10. | Stock-based compensation: |

We maintain three stock-based compensation plans: CHC Group Ltd. 2013 Omnibus Incentive Plan (“2013 Incentive Plan”), 2011 Management Equity Plan (“2011 Plan”), and Share Incentive Plan (“2008 Plan”). Note 17 to the consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014 contains descriptions of the plans, the nature and terms of the awards and the methods and assumptions utilized in estimating the fair value of the awards.

As of July 31, 2014, there have been no significant changes to the plans, the nature and terms of the awards or the fair value estimates, as described in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014.

During the three months ended July 31, 2014, there have been no significant activities under the 2011 Plan and 2008 Plan. During the three months ended July 31, 2014, awards have been granted, exercised and forfeited under the 2013 Incentive Plan, as described below.

(a) 2013 Incentive Plan new awards:

As described in Note 17(a) of the consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014, certain eligible employees were granted stock options, time-based restricted share units ("RSUs") and performance-based restricted share units ("PB RSUs").

19

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

10. | Stock-based compensation (continued): |

(a) 2013 Incentive Plan new awards (continued):

The following table provides information about the 2013 Incentive Plan stock options activity.

July 31, 2014 | ||||||||||

Outstanding number of instruments | Weighted average exercise price | Weighted remaining contractual life | Weighted average grant date fair value | |||||||

Outstanding, beginning of period | 2,537,522 | $ | 10.00 | — | $ | — | ||||

Granted | 29,499 | 8.21 | — | — | ||||||

Forfeited | (199,768 | ) | 10.00 | — | — | |||||

Outstanding, end of period | 2,367,253 | $ | 9.98 | 9.5 years | $ | 4.12 | ||||

Exercisable, end of period | — | |||||||||

The following table provides information about the 2013 Incentive Plan RSUs activity.

July 31, 2014 | ||||||||||

Outstanding number of instruments | Weighted average exercise price | Weighted remaining contractual life | Weighted average grant date fair value | |||||||

Outstanding, beginning of period | 1,062,668 | $ | — | — | $ | — | ||||

Granted | 12,180 | — | — | — | ||||||

Forfeited | (39,334 | ) | — | — | — | |||||

Outstanding, end of period | 1,035,514 | $ | — | 2.5 years | $ | 9.98 | ||||

Exercisable, end of period | — | |||||||||

The following table provides information about the 2013 Incentive Plan PB RSUs activity.

July 31, 2014 | ||||||||||

Outstanding number of instruments | Weighted average exercise price | Weighted remaining contractual life | Weighted average grant date fair value | |||||||

Outstanding, beginning of period | 403,284 | $ | — | — | $ | — | ||||

Forfeited | (33,334 | ) | — | — | — | |||||

Outstanding, end of period | 369,950 | $ | — | 2.5 years | $ | 12.60 | ||||

Exercisable, end of period | — | |||||||||

(b) | 2013 Incentive Plan exchanged awards: |

As described in Note 17(a) and 17(b) of the consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014, the majority of the members of the 2011 Plan exchanged their performance options under the 2011 Plan for either share price performance options or share price performance shares under the 2013 Incentive Plan and their time and performance options under the 2011 plan for either service vesting stock options or service vesting shares under the 2013 Incentive Plan.

20

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

10. | Stock-based compensation (continued): |

(b) | 2013 Incentive Plan exchanged awards (continued): |

During the three months ended July 31, 2014, 22,580 of the service vesting stock options and 97,255 of the service vesting shares vested. The vested options and shares were exercised and net share settled. Under net settlement procedures, upon the settlement date, shares were withheld to cover the required withholding tax. The number of shares to be withheld was determined based on the value of the instruments on the settlement date using the closing price of our ordinary shares of capital stock on that day, or the preceding last trading day if the settlement date is a non-trading day. The remaining amounts were delivered to the recipient as ordinary shares of capital stock. These shares withheld by us as a result of the net settlement of service vesting stock options and service vesting shares are no longer considered issued and outstanding, thereby reducing our ordinary shares outstanding used to calculate net loss per ordinary share. These ordinary shares were returned to the reserves and are available for future issuance under the 2013 Incentive Plan.

The following table provides information about the 2013 Incentive Plan service vesting stock options activity.

July 31, 2014 | ||||||||||

Outstanding number of instruments | Weighted average exercise price | Weighted remaining contractual life | Weighted average grant date fair value | |||||||

Outstanding, beginning of period | 46,403 | $ | 0.0001 | — | $ | — | ||||

Exercised | (22,580 | ) | 0.0001 | — | — | |||||

Outstanding, end of period | 23,823 | $ | 0.0001 | 9.5 years | $ | 10.00 | ||||

Exercisable, end of period | — | |||||||||

The following table provides information about the 2013 Incentive Plan share price performance options activity.

July 31, 2014 | ||||||||||

Outstanding number of instruments | Weighted average exercise price | Weighted remaining contractual life | Weighted average grant date fair value | |||||||

Outstanding, beginning of period | 178,961 | $ | 10.00 | — | $ | — | ||||

Forfeited | (29,861 | ) | 10.00 | — | — | |||||

Outstanding, end of period | 149,100 | $ | 10.00 | 9.5 years | $ | 3.86 | ||||

Exercisable, end of period | — | |||||||||

The following table provides information about the 2013 Incentive Plan service vesting shares activity.

July 31, 2014 | ||||||||||

Outstanding number of instruments | Weighted average exercise price | Weighted remaining contractual life | Weighted average grant date fair value | |||||||

Outstanding, beginning of period | 243,279 | $ | — | — | $ | — | ||||

Exercised | (97,255 | ) | — | — | — | |||||

Outstanding, end of period | 146,024 | $ | — | 2.0 years | $ | 10.00 | ||||

Exercisable, end of period | — | |||||||||

21

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

10. | Stock-based compensation (continued): |

(b) | 2013 Incentive Plan exchanged awards (continued): |

The following table provides information about the 2013 Incentive Plan share price performance shares activity.

July 31, 2014 | ||||||||||

Outstanding number of instruments | Weighted average exercise price | Weighted remaining contractual life | Weighted average grant date fair value | |||||||

Outstanding, beginning of period | 649,011 | $ | — | — | $ | — | ||||

Forfeited | (50,541 | ) | — | — | — | |||||

Outstanding, end of period | 598,470 | $ | — | 9.5 years | $ | 4.53 | ||||

Exercisable, end of period | — | |||||||||

During the three months ended July 31, 2013 and 2014, we recorded stock-based compensation expense of $0.1 million and $3.6 million respectively, in the statements of operations.

As at July 31, 2014, $20.1 million of unamortized stock-based compensation remains to be recognized.

11. | Income taxes: |

During the three months ended July 31, 2013 and 2014, we recorded income tax expense of $5.3 million and $7.9 million resulting in effective tax rates of (17.5)% and (29.8)%, respectively. During the three months ended July 31, 2014, there was an additional accrual of $1.3 million for a new uncertain tax position. The remaining income tax expense reflects primarily the current corporate income taxes in taxable jurisdictions and withholding taxes. For most jurisdictions we determined that the deferred tax assets are not more likely than not to be realized and therefore we continue to recognize a valuation allowance in respect of these deferred tax assets.

As of July 31, 2014, there was $27.7 million in unrecognized tax benefits, of which $20.8 million would have an impact on the effective tax rate, if recognized.

The total amount of interest and penalties accrued on the consolidated balance sheet at April 30, 2014 and July 31, 2014 was $7.1 million and $8.0 million, respectively.

12. | Employee pension plans: |

The net defined benefit pension plan expense (income) is as follows:

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Current service cost | $ | 5,006 | $ | 5,400 | |||

Interest cost | 7,921 | 8,705 | |||||

Expected return on plan assets | (12,438 | ) | (13,823 | ) | |||

Amortization of net actuarial and experience losses | 432 | 520 | |||||

Amortization of past service credits | (88 | ) | (146 | ) | |||

Employee contributions | (735 | ) | (863 | ) | |||

$ | 98 | $ | (207 | ) | |||

22

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

13. | Derivative financial instruments and fair value measurements: |

We are exposed to foreign exchange risk primarily from our subsidiaries which incur revenue and operating expenses in currencies other than US dollars with the most significant being Pound Sterling, Norwegian Kroner, Canadian dollars, Australian dollars and Euros. We monitor these exposures through our cash forecasting process and regularly enter into foreign exchange forward contracts to manage our exposure to fluctuations in expected future cash flows related to transactions in currencies other than the functional currency.

The outstanding foreign exchange forward contracts are as follows:

Notional | Fair value | Maturity | |||||||

April 30, 2014 | |||||||||

Purchase contracts to sell US dollars and buy Canadian dollars | CAD | 235,000 | $ | (10,925 | ) | May 2014 to Nov 2016 | |||

Purchase contracts to sell US dollars and buy Euros | € | 42,051 | 2,291 | July 2014 to Oct 2014 | |||||

Purchase contracts to sell Pounds Sterling and buy Euros | € | 54,000 | (2,547 | ) | May 2014 to Dec 2016 | ||||

July 31, 2014 | |||||||||

Purchase contracts to sell US dollars and buy Canadian dollars | CAD | 218,000 | $ | (8,025 | ) | Aug 2014 to Apr 2017 | |||

Purchase contracts to sell US dollars and buy Euros | € | 28,034 | (548 | ) | Oct 2014 to Dec 2014 | ||||

Purchase contracts to sell Pounds Sterling and buy Euros | € | 46,000 | (4,212 | ) | Aug 2014 to Dec 2016 | ||||

We enter into long-term revenue agreements, which provide for pricing denominated in currencies other than the functional currency of the parties to the contract. This pricing feature was determined to be an embedded derivative which has been bifurcated for valuation and accounting purposes. The embedded derivative contracts are measured at fair value and included in other assets or other liabilities.

The following tables summarize the financial instruments measured at fair value on a recurring basis excluding cash and cash equivalents and restricted cash:

April 30, 2014 | |||||||||||||||

Quoted prices in active markets for identical assets (Level 1) | Significant other observable inputs (Level 2) | Significant unobservable inputs (Level 3) | Fair value | ||||||||||||

Financial assets: | |||||||||||||||

Other assets, current: | |||||||||||||||

Foreign currency forward contracts | $ | — | $ | 2,306 | $ | — | $ | 2,306 | |||||||

Foreign currency embedded derivatives | — | 805 | — | 805 | |||||||||||

Other assets, non-current: | |||||||||||||||

Foreign currency forward contracts | — | 192 | — | 192 | |||||||||||

Foreign currency embedded derivatives | — | 3,432 | — | 3,432 | |||||||||||

$ | — | $ | 6,735 | $ | — | $ | 6,735 | ||||||||

23

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

13. | Derivative financial instruments and fair value measurements (continued): |

April 30, 2014 | |||||||||||||||

Quoted prices in active markets for identical assets (Level 1) | Significant other observable inputs (Level 2) | Significant unobservable inputs (Level 3) | Fair value | ||||||||||||

Financial liabilities: | |||||||||||||||

Other liabilities, current: | |||||||||||||||

Foreign currency forward contracts | $ | — | $ | (8,373 | ) | $ | — | $ | (8,373 | ) | |||||

Foreign currency embedded derivatives | — | (7,684 | ) | — | (7,684 | ) | |||||||||

Other liabilities, non-current: | |||||||||||||||

Foreign currency forward contracts | — | (5,306 | ) | — | (5,306 | ) | |||||||||

Foreign currency embedded derivatives | — | (8,011 | ) | — | (8,011 | ) | |||||||||

$ | — | $ | (29,374 | ) | $ | — | $ | (29,374 | ) | ||||||

July 31, 2014 | |||||||||||||||

Quoted prices in active markets for identical assets (Level 1) | Significant other observable inputs (Level 2) | Significant unobservable inputs (Level 3) | Fair value | ||||||||||||

Financial assets: | |||||||||||||||

Other assets, current: | |||||||||||||||

Foreign currency forward contracts | $ | — | $ | 69 | $ | — | $ | 69 | |||||||

Foreign currency embedded derivatives | — | 2,012 | — | 2,012 | |||||||||||

Other assets, non-current: | |||||||||||||||

Foreign currency forward contracts | — | 352 | — | 352 | |||||||||||

Foreign currency embedded derivatives | — | 6,779 | — | 6,779 | |||||||||||

$ | — | $ | 9,212 | $ | — | $ | 9,212 | ||||||||

July 31, 2014 | |||||||||||||||

Quoted prices in active markets for identical assets (Level 1) | Significant other observable inputs (Level 2) | Significant unobservable inputs (Level 3) | Fair value | ||||||||||||

Financial liabilities: | |||||||||||||||

Other liabilities, current: | |||||||||||||||

Foreign currency forward contracts | $ | — | $ | (8,784 | ) | $ | — | $ | (8,784 | ) | |||||

Foreign currency embedded derivatives | — | (5,593 | ) | — | (5,593 | ) | |||||||||

Other liabilities, non-current: | |||||||||||||||

Foreign currency forward contracts | — | (4,422 | ) | — | (4,422 | ) | |||||||||

Foreign currency embedded derivatives | — | (4,945 | ) | — | (4,945 | ) | |||||||||

$ | — | $ | (23,744 | ) | $ | — | $ | (23,744 | ) | ||||||

24

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

13. | Derivative financial instruments and fair value measurements (continued): |

Inputs to the valuation methodology for Level 2 measurements include publicly available forward notes, credit spreads and US dollars or Euro interest rates, and inputs are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. There were no transfers between categories in the fair value hierarchy.

The carrying values of the other financial instruments, which are measured at other than fair value, approximate fair value due to the short terms to maturity, except for non-revolving debt obligations, the fair values of which are as follows:

April 30, 2014 | July 31, 2014 | |||||||||||||

Fair value | Carrying value | Fair value | Carrying value | |||||||||||

Senior secured notes | $ | 1,254,825 | $ | 1,159,675 | $ | 1,187,875 | $ | 1,095,528 | ||||||

Senior unsecured notes | 311,250 | 300,000 | 316,890 | 300,000 | ||||||||||

The fair value of the senior secured and unsecured notes are determined based on market information provided by third parties which is considered to be a Level 2 measurement in the fair value hierarchy.

14. | Supplemental cash flow information: |

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Cash interest paid | $ | 1,653 | $ | 16,155 | |||

Cash taxes paid | 11,525 | 8,181 | |||||

Assets acquired through non-cash capital leases | 9,101 | — | |||||

Change in cash resulting from changes in operating assets and liabilities:

Three months ended | |||||||

July 31, 2013 | July 31, 2014 | ||||||

Receivables, net of allowance | $ | 6,547 | $ | (8,282 | ) | ||

Income taxes receivable and payable | (5,211 | ) | (683 | ) | |||

Inventories | (4,370 | ) | (7,643 | ) | |||

Prepaid expenses | (13,739 | ) | (2,666 | ) | |||

Payables and accruals | (19,781 | ) | (12,070 | ) | |||

Deferred revenue | 13,334 | 11,163 | |||||

Other assets and liabilities | (3,451 | ) | 5,091 | ||||

$ | (26,671 | ) | $ | (15,090 | ) | ||

15. | Guarantees: |

We have provided limited guarantees to third parties under some of our operating leases relating to a portion of the residual helicopter values at the termination of the leases, which have terms expiring between fiscal 2015 and 2024. Our exposure under the asset value guarantees including guarantees in the form of funded and unfunded residual value guarantees, rebateable advance rentals and deferred payments is approximately $245.2 million and $250.0 million as at April 30, 2014 and July 31, 2014, respectively.

25

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

16. | Related party transactions: |

(a) | Related party leasing transactions and balances: |

During the three months ended July 31, 2014, we engaged in leasing transactions with VIEs related to our majority shareholder (note 2).

(b) | Balances with our majority shareholder: |

At April 30, 2014 and July 31, 2014, $2.0 million in payables and accruals is due to our majority shareholder.

(c) | Repayment of related party loans: |

On June 24, 2013, we repaid $25.1 million of related party loans to companies under common control with our majority shareholder. The loan bore interest at 4.5% per annum.

On July 16, 2013, we borrowed $25.0 million from companies under common control with our majority shareholder. On July 19, 2013, the loan was repaid. The loan bore interest at 4.5% per annum.

17. | Commitments: |

We have helicopter operating leases with 21 lessors for 171 helicopters and 19 lessors for 170 helicopters included in our fleet at April 30, 2014 and July 31, 2014, respectively. As at July 31, 2014, these leases had expiry dates ranging from fiscal 2015 to 2025. We have the option to purchase the majority of the helicopters for agreed amounts that do not constitute bargain purchase options, but have no commitment to do so. With respect to such leased helicopters, substantially all of the costs of major inspections of airframes and the costs to perform inspections, major repairs and overhauls of major components are at our expense. We either perform this work internally through our own repair and overhaul facilities or have the work performed by an external repair and overhaul service provider.

At July 31, 2014, we have commitments with respect to operating leases for helicopters, buildings, land and equipment. The minimum lease rentals required under operating leases are payable in the following amounts over the following years ended July 31:

Helicopter operating leases | Building, land and equipment operating leases | Total operating leases | |||||||||

2015 | $ | 284,444 | $ | 18,082 | $ | 302,526 | |||||

2016 | 272,789 | 15,352 | 288,141 | ||||||||

2017 | 251,072 | 13,842 | 264,914 | ||||||||

2018 | 238,043 | 10,858 | 248,901 | ||||||||

2019 | 219,736 | 8,441 | 228,177 | ||||||||

Thereafter | 372,990 | 54,875 | 427,865 | ||||||||

$ | 1,639,074 | $ | 121,450 | $ | 1,760,524 | ||||||

As at July 31, 2014, we have committed to purchase 25 new helicopters and the total required additional expenditure for these helicopters is approximately $615.2 million. These helicopters are expected to be delivered in fiscal 2015 ($270.5 million), 2016 ($229.0 million) and 2017 ($115.7 million) and will be deployed in our Helicopter Services segment. We intend to enter into leases for these helicopters or purchase them outright upon delivery from the manufacturer. Additionally, we have committed to purchase $53.2 million of helicopter parts by October 31, 2015 and $100.0 million of heavy helicopters from Airbus Helicopters prior to December 31, 2016.

26

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

17. | Commitments (continued): |

The terms of certain of the helicopter lease agreements impose operating and financial limitations on us. Such agreements limit the extent to which we may, among other things, incur indebtedness and fixed charges relative to our level of consolidated adjusted earnings before interest, taxes, depreciation and amortization.

Generally, in the event of a covenant breach, a lessor has the option to terminate the lease and require the return of the helicopter, with the repayment of any arrears of lease payments plus the present value of all future lease payments and certain other amounts which could be material to our financial position. The helicopter would then be sold and the surplus, if any, returned to us. Alternatively we could exercise our option to purchase the helicopter. As at July 31, 2014, we were in compliance with all financial covenants.

18. | Contingencies: |

One or more of our subsidiaries are, from time to time, named as defendants in lawsuits arising in the ordinary course of our business. Such disputes may involve, for example, breach of contract, employment, wrongful termination and tort claims. We maintain adequate insurance coverage to respond to most claims. We cannot predict the outcome of any such lawsuits with certainty, but our management team does not expect the outcome of pending or threatened legal matters to have a material adverse impact on our financial condition.

In addition, from time to time, we are involved in tax and other disputes with various government agencies. The following summarizes certain of these pending disputes:

In 2006, we voluntarily disclosed to the U.S. Office of Foreign Asset Control, or OFAC, that one or more of our subsidiaries formerly operating as Schreiner Airways may have violated applicable US laws and regulations by re-exporting to Iran, Sudan, and Libya certain helicopters, related parts, map data, operation and maintenance manuals, and helicopter parts for third-party customers. OFAC’s investigation is ongoing and we continue to fully cooperate. Should the US government determine that these activities violated applicable laws and regulations, we or our subsidiaries could be subject to civil or criminal penalties, including fines and/or suspension of the privilege to engage in trading activities involving goods, software and technology subject to the US jurisdiction. At July 31, 2014, it is not possible to determine the outcome of this matter, or the significance, if any, to our business, financial condition and results of operations.

On May 2, 2008, Brazilian customs authorities seized one of our helicopters (customs value of $10.0 million) as a result of allegations that we violated Brazilian customs law by failing to ensure our customs agent and the customs agent’s third-party shipping company followed approved routing of the helicopter during transport. We secured release of the helicopter and are disputing through court action any claim for penalties associated with the seizure and the alleged violation. We have preserved our rights by filing a civil action against our customs agent for any losses that may result. At July 31, 2014, it is not possible to determine the outcome of this matter, or the significance, if any, to our business, financial condition and results of operations.

Our Brazilian subsidiary is disputing claims from the Brazilian tax authorities that it was not entitled to certain credits in 2004 and 2007. The tax authorities are seeking up to $4.8 million in additional taxes plus interest and penalties. We believe that based on our interpretation of tax legislation and well established aviation industry practice we are in compliance with all applicable tax legislation and plan to defend this claim vigorously. At July 31, 2014, it is not possible to determine the outcome of this matter or the significance, if any, to our business, financial condition and result of operations.

Our Brazilian subsidiary is also disputing assessments from the municipal governments in Macae and Cabo Frio related to cross-border flights and invoicing. The municipalities are seeking up to $5.0 million in taxes and penalties. We do not believe the Company is liable for these amounts and will continue to dispute these assessments through administrative and judicial processes. At July 31, 2014, it is not possible to determine the outcome of this matter or the significance, if any, to our business, financial condition and result of operations.

27

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

18. | Contingencies (continued): |

In the United Kingdom, the Ministry for Transport is investigating potential wrongdoing involving two ex-employees in conjunction with the SAR-H bid award processes. This arose from our self-reporting potential improprieties by these individuals upon their discovery in 2010. The SAR-H bid process was subsequently canceled. We will continue to cooperate in all aspects of the investigation. On July 30, 2014, the UK Treasury Solicitors filed a claim for bid recovery costs of £17.8 million ($30.1 million) against us and other parties involved in our canceled bid. We dispute the bases for the claim and intend to vigorously defend against it. At July 31, 2014, it is not possible to determine the outcome of this matter, or the significance, if any, to our business, financial condition and results of operations.

19. | Segment information: |

We operate under the following segments:

• | Helicopter Services; |

• | Heli-One; |

• | Corporate and other. |

We have provided information on segment revenues and Adjusted EBITDAR because these are the financial measures used by the Company’s chief operating decision maker (“CODM”) in making operating decisions and assessing performance. Transactions between operating segments are at standard industry rates.

During the three months ended July 31, 2014, we changed our internal reporting structure to allocate certain direct maintenance and supply chain costs previously reported in the Heli-One segment to the Helicopter Services segment. Under the previous reporting, Heli-One provided maintenance services to the Helicopter Services segment under the terms of a Power by Hour (“PBH”) contract. Costs incurred by Heli-One to provide services under the PBH contract were reported in the Heli-One segment, whether they related to maintenance costs performed internally by Heli-One or to services contracted from external third parties. Under the new reporting, all third-party maintenance costs are reflected in the Helicopter Services segment. Maintenance services provided by Heli-One to Helicopter Services are separately reflected for each repair or overhaul of engines and components completed (“MRO contract”) as opposed to a PBH contract basis.

The new reporting structure presentation is reflected in the three months ended July 31, 2013 and July 31, 2014 segment results. The MRO contract services provided by Heli-One to Helicopter Services are accounted for using a completed contract revenue recognition method in the three months ended July 31, 2014. For the three months ended July 31, 2013, the MRO contract services are accounted for using a percentage completion method, as it was not practical to determine results for this period using the completed contract method of revenue recognition. We are unable to quantify the impact of the difference between percentage completion and completed contract on the three months ended July 31, 2013. Otherwise, the accounting policies of the segments and the basis of accounting for transactions between segments are the same as those described in the summary of significant accounting policies in Note 2 of the consolidated financial statements included in our Annual Report on Form 10-K for the fiscal year ended April 30, 2014.

Information on segment assets has not been disclosed as this information is not reviewed by the CODM.

The Helicopter Services segment includes flying operations around the world serving offshore oil and gas, EMS/SAR and other industries and the management of the fleet.

Heli-One, the maintenance, repair and overhaul segment, includes facilities in Norway, Canada, Poland, and the United States that provide helicopter maintenance, repair and overhaul services for our fleet and for an external customer base in Europe, Asia and North America.

Corporate and other includes corporate office costs in various jurisdictions and is not considered a reportable segment.

28

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

19. | Segment information (continued): |

Three months ended July 31, 2013 | |||||||||||||||||||

Helicopter Services | Heli-One | Corporate and other | Inter-segment eliminations | Consolidated | |||||||||||||||

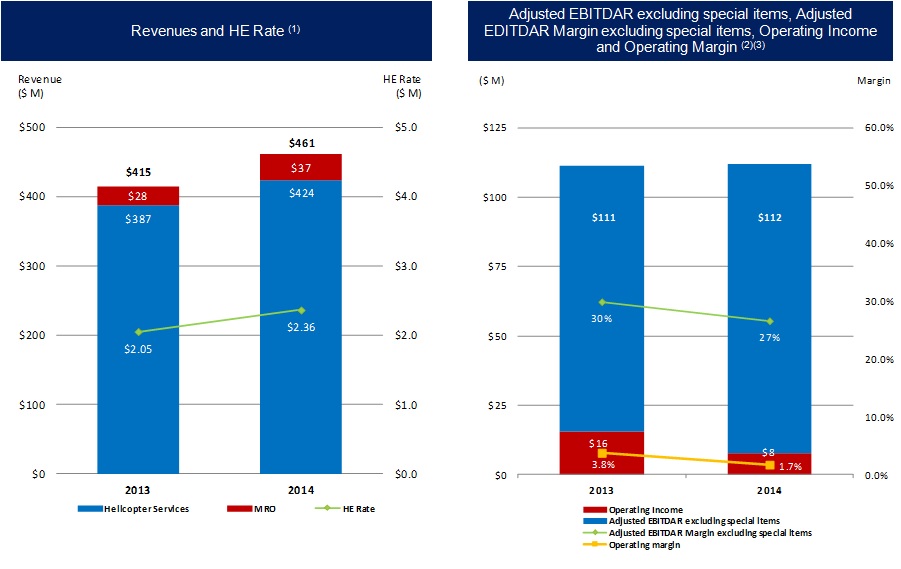

Revenue from external customers | $ | 387,302 | $ | 27,629 | $ | — | $ | — | $ | 414,931 | |||||||||

Add: Inter-segment revenues | — | 37,211 | — | (37,211 | ) | — | |||||||||||||

Total revenue | 387,302 | 64,840 | — | (37,211 | ) | 414,931 | |||||||||||||

Direct costs (i) | (263,626 | ) | (60,644 | ) | — | 36,443 | (287,827 | ) | |||||||||||

Earnings from equity accounted investees | 2,391 | — | — | — | 2,391 | ||||||||||||||

General and administration costs | — | — | (18,116 | ) | — | (18,116 | ) | ||||||||||||

Adjusted EBITDAR (ii) | 126,067 | 4,196 | (18,116 | ) | (768 | ) | 111,379 | ||||||||||||

Helicopter lease and associated costs | (55,279 | ) | — | — | — | (55,279 | ) | ||||||||||||

Depreciation | (32,057 | ) | |||||||||||||||||

Asset impairments (iii) | (7,324 | ) | |||||||||||||||||

Loss on disposal of assets | (1,122 | ) | |||||||||||||||||

Operating income | 15,597 | ||||||||||||||||||

Interest on long-term debt | (38,708 | ) | |||||||||||||||||

Foreign exchange loss | (13,087 | ) | |||||||||||||||||

Other financing income | 5,823 | ||||||||||||||||||

Income tax expense | (5,308 | ) | |||||||||||||||||

Net loss | $ | (35,683 | ) | ||||||||||||||||

(i) | Direct costs in the segment information presented excludes helicopter lease and associated costs. In the consolidated statement of operations these costs are combined. |

(ii) | Adjusted EBITDAR is defined as earnings before interest, taxes, depreciation, amortization, helicopter lease and associated costs, asset impairments, gain (loss) on disposal of assets, foreign exchange gain (loss) and other financing income (charges) or total revenue plus earnings from equity accounted investees less direct costs, excluding helicopter lease and associated costs, and general and administration expenses. |

(iii) | Asset impairments of $7.3 million relate to the Helicopter Services segment. |

29

CHC Group Ltd.

Notes to Interim Consolidated Financial Statements (Unaudited)

(Tabular amounts expressed in thousands of United States dollars unless otherwise noted, except share and per share information)

19. | Segment information (continued): |

Three months ended July 31, 2014 | |||||||||||||||||||

Helicopter Services | Heli-One | Corporate and other | Inter-segment eliminations | Consolidated | |||||||||||||||

Revenue from external customers | $ | 423,711 | $ | 36,937 | $ | — | $ | — | $ | 460,648 | |||||||||

Add: Inter-segment revenues | — | 23,981 | — | (23,981 | ) | — | |||||||||||||

Total revenue | 423,711 | 60,918 | — | (23,981 | ) | 460,648 | |||||||||||||

Direct costs (i) | (299,587 | ) | (55,642 | ) | — | 23,962 | (331,267 | ) | |||||||||||

Earnings from equity accounted investees | 2,677 | — | — | — | 2,677 | ||||||||||||||

General and administration costs | — | — | (21,662 | ) | — | (21,662 | ) | ||||||||||||

Adjusted EBITDAR (ii) | 126,801 | 5,276 | (21,662 | ) | (19 | ) | 110,396 | ||||||||||||

Helicopter lease and associated costs | (63,280 | ) | — | — | — | (63,280 | ) | ||||||||||||

Depreciation | (33,725 | ) | |||||||||||||||||