Attached files

| file | filename |

|---|---|

| EX-10.13 - EX-10.13 - Dave & Buster's Entertainment, Inc. | d735753dex1013.htm |

| EX-21.1 - EX-21.1 - Dave & Buster's Entertainment, Inc. | d735753dex211.htm |

| EX-10.11 - EX-10.11 - Dave & Buster's Entertainment, Inc. | d735753dex1011.htm |

| EX-23.1 - EX-23.1 - Dave & Buster's Entertainment, Inc. | d735753dex231.htm |

| EX-10.8 - EX-10.8 - Dave & Buster's Entertainment, Inc. | d735753dex108.htm |

| EX-10.14 - EX-10.14 - Dave & Buster's Entertainment, Inc. | d735753dex1014.htm |

Table of Contents

As filed with the Securities and Exchange Commission on September 8, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Dave & Buster’s Entertainment, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 5812 | 35-2382255 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

2481 Mañana Drive

Dallas, Texas 75220

(214) 357-9588

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Stephen M. King

Chief Executive Officer

Dave & Buster’s Entertainment, Inc.

2481 Mañana Drive

Dallas, Texas 75220

(214) 357-9588

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Corey R. Chivers, Esq. Alexander D. Lynch, Esq. Weil, Gotshal & Manges LLP 767 Fifth Avenue New York, New York 10153 (212) 310-8000 (Phone) (212) 310-8007 (Fax) |

Marc D. Jaffe, Esq. Ian D. Schuman, Esq. Latham & Watkins LLP 885 Third Avenue, Suite 1000 New York, New York 10022 (212) 906-1200 (Phone) (212) 751-4864 (Fax) |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| TITLE OF EACH CLASS OF SECURITIES TO BE REGISTERED |

PROPOSED MAXIMUM AGGREGATE |

AMOUNT OF REGISTRATION FEE (3) | ||

| Common Stock, $0.01 par value |

$100,000,000 | $12,880 | ||

|

| ||||

|

| ||||

| (1) | Includes shares of common stock that may be purchased by the underwriters under their option to purchase additional shares of common stock, if any. |

| (2) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) promulgated under the Securities Act of 1933, as amended. |

| (3) | A registration fee in the amount of $17,415 was previously paid by the registrant in connection with the filing of a Registration Statement on Form S-1 (Registration No. 333-175616) on July 15, 2011. Pursuant to Rule 457(p) under the Securities Act of 1933, as amended, the filing fee of $17,415 previously paid by the registrant is being used to offset the filing fee of $12,880 required for the filing of this Registration Statement. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion Dated September 8, 2014

PRELIMINARY PROSPECTUS

Shares

Dave & Buster’s Entertainment, Inc.

Common Stock

We are offering shares of our common stock. This is our initial public offering and no public market currently exists for our common stock. We expect the initial public offering price to be between $ and $ per share. We have applied to list our common stock on The NASDAQ Stock Market LLC (“NASDAQ”) under the symbol “PLAY.”

Dave & Buster’s Entertainment, Inc. is an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”).

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 19 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| PER SHARE | TOTAL | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions (1) |

$ | $ | ||||||

| Proceeds to us, before expenses |

$ | $ | ||||||

| (1) | We refer you to “Underwriting” beginning on page 119 of this prospectus for additional information regarding total underwriter compensation. |

Delivery of the shares of common stock is expected to be made on or about , 2014. We have granted the underwriters an option for a period of 30 days to purchase an additional shares of our common stock. If the underwriters exercise the option in full, the total underwriting discounts and commissions payable by us will be $ , and the total proceeds to us, before expenses, will be $ .

| Jefferies | Piper Jaffray | |||

| William Blair | Raymond James | Stifel |

| LOYAL3 Securities |

Preliminary Prospectus dated , 2014.

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| PAGE | ||||

| 1 | ||||

| 19 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 39 | ||||

| 41 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

47 | |||

| 71 | ||||

| 83 | ||||

| 90 | ||||

| 104 | ||||

| 106 | ||||

| 110 | ||||

| 114 | ||||

| CERTAIN MATERIAL UNITED STATES FEDERAL INCOME AND ESTATE TAX CONSIDERATIONS |

116 | |||

| 119 | ||||

| 125 | ||||

| 125 | ||||

| 125 | ||||

| F-1 | ||||

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is only accurate as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Table of Contents

BASIS OF PRESENTATION

Certain financial measures presented in this prospectus, such as Adjusted EBITDA, Adjusted EBITDA Margin, Store-level EBITDA and Store-level EBITDA margin, are not recognized terms under accounting principles generally accepted in the United States (“GAAP”). These measures exclude a number of significant items, including our interest expense and depreciation and amortization expense. For a discussion of the use of these measures and a reconciliation to the most directly comparable GAAP measures, see pages 13-18 “—Summary Historical Financial and Other Data.” We define high-volume dining and entertainment venues as those open for at least one full year and with average store revenues in excess of $5.0 million and define year one cash-on-cash return as year one Store-level EBITDA exclusive of allocated national marketing costs divided by net development costs. Net development costs include equipment, building, leaseholds and site costs, net of tenant improvement allowances received or receivable from landlords and excludes pre-opening costs and capitalized interest.

We operate on a 52 or 53 week fiscal year that ends on the Sunday after the Saturday closest to January 31. Each quarterly period has 13 weeks, except in a 53 week year when the fourth quarter has 14 weeks. All fiscal years presented herein consist of 52 weeks, except fiscal year 2012, which consisted of 53 weeks. All references to “2014,” “fiscal 2014,” “fiscal year 2014” or similar references relate to the 52 week period ending February 1, 2015. All references to “2013,” “fiscal 2013,” “fiscal year 2013” or similar references relate to the 52 week period ended February 2, 2014. All references to “2012,” “fiscal 2012,” “fiscal year 2012” or similar references relate to the 53 week period ended February 3, 2013. All references to “2011,” “fiscal 2011,” “fiscal year 2011” or similar references relate to the 52 week period ended January 29, 2012. All references to “2010,” “fiscal 2010,” “fiscal year 2010” or similar references relate to the combined results of the 244 day period ended January 30, 2011 and the 120 day period ended May 31, 2010. All references to “2009,” “fiscal 2009,” “fiscal year 2009” or similar references relate to the 52 week period ended January 31, 2010.

On June 1, 2010, Dave & Buster’s Entertainment, Inc. (“D&B Entertainment”), a newly-formed Delaware corporation owned by Oak Hill Capital Partners III, L.P. and Oak Hill Capital Management Partners III, L.P. (collectively, the “Oak Hill Funds”) acquired all of the outstanding common stock of Dave & Buster’s Holdings, Inc. (“D&B Holdings”). As a result of the acquisition and certain post-acquisition activity, the Oak Hill Funds directly control approximately 95.4% of D&B Entertainment’s outstanding common stock. GAAP requires operating results prior to the acquisition completed on June 1, 2010 to be presented as Predecessor’s results in the historical financial statements. Operating results subsequent to the acquisition are presented or referred to as Successor’s results in the historical financial statements. The presentation of combined Predecessor and Successor operating results (which is simply the arithmetic sum of the Predecessor and Successor amounts) is a non-GAAP presentation, which is provided as a convenience solely for the purpose of facilitating comparisons of the combined results with other annual periods presented.

Comparable store data presented in this prospectus relate to stores open at least 18 months as of the beginning of each of the relevant fiscal years and excludes information for our one franchised store located in Canada, which ceased operation as a Dave & Buster’s on May 31, 2013. Our store count data also excludes the one franchised store located in Canada. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

This prospectus also contains information regarding customer feedback, customer satisfaction, customer demographics and other similar items. This information is based upon data collected by us during the periods presented. This information is reported voluntarily by our customers and thus represents responses from only a portion of the total number of our customers. We have not independently verified any of the demographic information collected from our customers. Over the periods presented, we have changed the form of reward for completing a survey, which resulted in an increase in the percentage of completed surveys, but we do not believe this has materially impacted the results. In addition, over the periods presented, we have added and deleted questions from the questionnaires, but have not made any changes to questions eliciting responses relating to the results presented in the prospectus. We use the information collected as one measure of the performance of our stores and use it to assess the success of our initiatives to improve the quality of the product we offer.

ii

Table of Contents

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

We own or have rights to use the trademarks, service marks and trade names that we use in connection with the operation of our businesses. Our registered trademarks include Dave & Buster’s®, Power Card®, Eat Drink Play® and Eat & Play Combo®. Other trademarks, service marks and trade names used in this prospectus are the property of their respective owners.

Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus are listed without the ® and ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights (or the rights of the applicable licensors) to these trademarks, service marks and trade names.

INDUSTRY AND MARKET DATA

This prospectus includes industry and market data that we derived from internal company records, publicly available information and industry publications and surveys such as reports from KNAPP-TRACK™. Industry publications and surveys generally state that the information contained therein has been obtained from sources believed to be reliable. We believe this data is accurate in all material respects as of the date of this prospectus. You should carefully consider the inherent risks and uncertainties associated with the industry and market data contained in this prospectus.

KNAPP-TRACK is a monthly sales and customer count tracking service for the full-service restaurant industry in the United States, which tracks over 10,400 restaurants with over $32.1 billion in total sales. Each monthly KNAPP-TRACK report aggregates the change in comparable restaurant sales and customer counts compared to the same month in the preceding year from the competitive set of participants in the full service restaurant industry. We, as well as other restaurants, use the data included in the monthly KNAPP-TRACK report as one way of benchmarking our performance.

iii

Table of Contents

This summary highlights information contained elsewhere in this prospectus and may not contain all of the information that may be important to you. Before making an investment decision, you should read this entire prospectus, including our consolidated financial statements and the related notes included elsewhere herein. You should also carefully consider the information set forth under “Risk Factors.” In addition, certain statements include forward-looking information that is subject to risks and uncertainties. See “Cautionary Statement Regarding Forward-Looking Statements.” In this prospectus, unless the context otherwise requires, “we,” “us,” “our,” the “Company” and “Dave & Buster’s” refers to Dave & Buster’s Entertainment, Inc., its subsidiaries and any predecessor companies, collectively.

Company Overview

We are a leading owner and operator of high-volume venues in North America that combine dining and entertainment for both adults and families. The core of our concept is to offer our customers the opportunity to “Eat Drink Play and Watch” all in one location. Eat and Drink are offered through a full menu of “Fun American New Gourmet” entrées and appetizers and a full selection of non-alcoholic and alcoholic beverages. Our Play and Watch offerings provide an extensive assortment of entertainment attractions centered around playing games and watching live sports and other televised events. Our customers are a balanced mix of men and women, primarily between the ages of 21 and 39, and we believe we also serve as an attractive venue for families with children and teenagers. We believe we appeal to a diverse customer base by providing a highly customizable experience in a dynamic and fun setting.

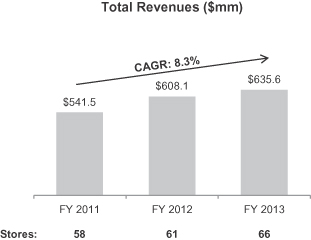

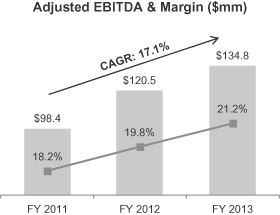

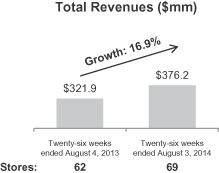

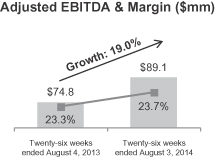

As of September 2, 2014, we owned and operated 69 stores in 26 states and Canada. For the twelve months ended August 3, 2014, we generated total revenues of $689.9 million, Adjusted EBITDA of $149.0 million (representing an Adjusted EBITDA margin of 21.6%) and a net loss of $7.7 million. For the twenty-six weeks ended August 3, 2014 and August 4, 2013, we generated total revenues of $376.2 million and $321.9 million, respectively, Adjusted EBITDA of $89.1 million and $74.8 million, respectively, and net income (loss) of $(2.4) million and $7.5 million, respectively. For fiscal 2013, we generated total revenues of $635.6 million, Adjusted EBITDA of $134.8 million (representing an Adjusted EBITDA margin of 21.2%) and net income of $2.2 million. For fiscal 2012 and fiscal 2011, we generated total revenues of $608.1 million and $541.5 million, respectively, Adjusted EBITDA of $120.5 million and $98.4 million, respectively, and net income (loss) of $8.8 million and $(7.0) million, respectively. From fiscal 2011 to fiscal 2013, total revenues and Adjusted EBITDA grew at a compound annual growth rate (“CAGR”) of 8.3% and 17.1%, respectively. We generated comparable store sales increases of 5.2%, 1.0%, 3.0% and 2.2% in the twenty-six weeks ended August 3, 2014 and fiscal 2013, 2012 and 2011, respectively.

|

|

1

Table of Contents

|

|

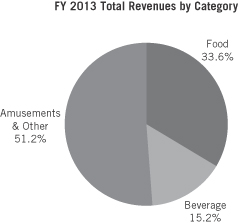

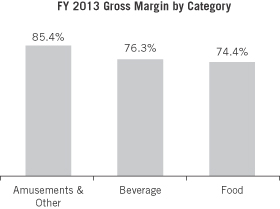

As a key feature of our business model, 51.2% of our total revenues for fiscal 2013 were from our amusement offerings, which have a relatively low variable cost component and contributed a gross margin of 85.4%. Combined with our food and beverage revenues, which comprised 48.8% of our total revenues and contributed a gross margin of 75.0% for fiscal 2013, we generated a total gross margin of 80.3%.

|

|

The formats and square footage of our stores are flexible, which we believe allows us to size new stores appropriately for each market as we grow. Our stores average 45,000 square feet and range in size between 16,000 and 66,000 square feet. We believe we have an attractive store economic model that enables us to generate high average store revenues and Store-level EBITDA. For our 55 comparable stores in fiscal 2013, our average revenues per store were $10.1 million, average Store-level EBITDA was $2.6 million and average Store-level EBITDA margin was 25.9%. Furthermore, for that same period, all of our comparable stores had positive Store-level EBITDA, with 89.1% of our stores generating more than $1.0 million of Store-level EBITDA each and 61.8% of our stores generating more than $2.0 million of Store-level EBITDA each.

Eat Drink Play and Watch—All Under One Roof

When our founders opened our first location in Dallas, Texas in 1982, they sought to create a brand with a fun, upbeat atmosphere providing interactive entertainment options for adults and families, while serving high-quality food and beverages. Since then we have followed the same principle for each new store, and in doing so we believe we have developed a distinctive brand based on our customer value proposition: “Eat Drink Play and Watch.” The interaction between playing games, watching sports, dining and enjoying our full-service bar areas is the defining feature of the Dave & Buster’s customer experience, and the layout of each store is designed to promote crossover between these activities. We believe this combination creates an experience that cannot be easily replicated at home or elsewhere without having to visit multiple destinations. Our locations are also designed to accommodate private parties, business functions and other corporate-sponsored events.

2

Table of Contents

Eat

We seek to distinguish our food menu from other casual dining concepts with our strategy of offering “Fun American New Gourmet” entrées and appetizers. Our “Fun American New Gourmet” menu is intended to appeal to a broad spectrum of customers and include classic “American” offerings with a fun twist. We believe we offer high-quality meals, including gourmet pastas, choice-grade steaks, premium sandwiches, decadent desserts and health-conscious entrée options that compare favorably to those of other higher end casual dining operators. We believe our broad menu offers something for everyone and captures full meal, snacking and sports-viewing occasions. We plan to introduce new menu items three times per year that we believe reinforce the fun of the Dave & Buster’s brand. Our food revenues accounted for 33.6% of our total revenues during fiscal 2013.

Drink

Each of our locations also offers full bar service, including a variety of beers, signature cocktails, premium spirits and non-alcoholic beverages. We continually strive to innovate our beverage offering, adding new beverages three times per year, including the introduction of fun beverage platforms such as our adult Snow Cones, CoronaRitas and Berry Blocks cocktails. Beverage service is typically available throughout the entire store, allowing for multiple sales opportunities. We believe that our high margin beverage offering is complementary to each of the Eat, Play and Watch aspects of our brand. Our beverage revenues accounted for 31.1% of our total food and beverage revenues and 15.2% of our total revenues during fiscal 2013.

Play

A key aspect of the entertainment experience at Dave & Buster’s is the games in our Midway, which we believe are the core differentiating feature of our brand. The Midway in each of our stores is an area where we offer a wide array of amusement and entertainment options, typically with over 150 redemption and simulation games. Our amusement and other revenues accounted for 51.2% of our total revenues during fiscal 2013. Redemption games, which represented 78.7% of our amusement and other revenues in fiscal 2013, offer our customers the opportunity to win tickets that are redeemable at our “Winner’s Circle,” a retail-style space in our stores where customers can redeem the tickets won through play of our redemption games for prizes ranging from branded novelty items to high-end electronics. We believe this “opportunity to win” creates a fun and highly energized social experience that is an important aspect of the Dave & Buster’s in-store experience and cannot be easily replicated at home. Our video and simulation games, many of which can be played by multiple customers simultaneously and include some of the latest high-tech games commercially available, represented 16.7% of our amusement and other revenues in fiscal 2013. Other traditional amusements represented the remainder of our amusement and other revenues in fiscal 2013.

Watch

Sports-viewing is another key component of the entertainment experience at Dave & Buster’s. All of our stores have multiple large screen televisions and high quality audio systems providing customers with a venue for watching live sports and other televised events. In fiscal 2010, we initiated a program that evolved into “D&B Sports,” which is a more immersive viewing environment that provides customers with 100+ inch high definition televisions to watch televised events and enjoy our full bar and extensive food menu. We believe that we have created an attractive and comfortable environment that includes a differentiated and interactive viewing experience that offers a new reason for customers to visit Dave & Buster’s. Through continued development of the D&B Sports concept in new stores and additional renovations of existing stores, our goal is to build awareness of D&B Sports as “the best place to watch sports” and the “only place to watch the games and play the games.”

3

Table of Contents

Our Company’s Core Strengths

We believe we benefit from the following strengths:

Strong, Distinctive Brand With Broad Customer Appeal. We believe that the multi-faceted customer experience of “Eat Drink Play and Watch” at Dave & Buster’s, supported by our national marketing, has helped us create a widely recognized brand with no direct national competitor that combines all four elements in the same way. In markets where we have stores, over 95% of casual dining consumers stated that they are aware of our brand as a dining and entertainment venue. Our customer research shows that our brand appeals to a balanced mix of male and female adults, primarily between the ages of 21 and 39, as well as families and teenagers. Based on customer survey results, we also believe that the average household income of our customers is approximately $80,000, which we believe represents an attractive demographic.

Multi-Faceted Customer Experience Highlights Our Value Proposition. We believe that our combination of interactive games, attractive television viewing areas, high-quality dining and full-service beverage offerings, delivered in a highly-energized atmosphere, provides a multi-faceted customer experience that cannot be easily replicated at home or elsewhere without having to visit multiple destinations. We aim to offer our customers a value proposition comparable or superior to many of the separately available dining and entertainment options. We are continuously working with game manufacturers and food providers to create new games and food items at compelling price points to retain and generate customer traffic and improve the customer experience. Our value proposition is enhanced by what we consider to be innovative marketing initiatives, including our Eat & Play Combo (a promotion that provides a discounted Power Card in combination with select entrées), Super Charge Power Card offerings (when purchasing or adding value to a Power Card, the customer is given the opportunity to add 25% more chips to the Power Card for a small upcharge), Half-Price Game Play (every Wednesday, from open to close, we reduce the price of every game in the Midway by one-half), Everyone’s a Winner (a limited-time offer providing a prize to every customer that purchases or adds value to a Power Card in the amount of $10 or more) and free game play promotions to feature the introduction of our new games. We believe these initiatives have helped increase customer visits and encourage customers to participate more fully across our broad range of food, beverage and entertainment offerings.

Vibrant, Contemporary Store Design That Integrates Entertainment and Dining. We believe we continue to benefit from enhancements to the Dave & Buster’s brand through our store design and D&B Sports initiatives, which began in fiscal 2011. Our new store design provides a contemporary, engaging atmosphere for our customers that includes clearly differentiated spaces designed to convey each component of our customer value proposition: “Eat Drink Play and Watch.” These store design changes include a modern approach to the finishes and layout of the store, which we believe encourages participation across each of the store’s elements. The oversized graphics and images throughout the store are intended to communicate our brand personality by being fun, contemporary and larger-than-life. The dining room décor includes booth seating and table seating and colorful artwork, often featuring local landmarks. Our Winner’s Circle provides a retail-like environment where customers can redeem their tickets for prizes. All of our new locations opened since the beginning of fiscal 2011 incorporate our new store design. We believe the introduction and continued expansion of our D&B Sports concept, currently incorporated in approximately half of our store base, provides an attractive opportunity to market our broader platform to new and existing customers through a year-round calendar of programming and promotions tied to popular sporting events and sport-related activities. The large television screens, comfortable seating, a full menu of food and beverages and artwork often featuring images of local sports teams and sports icons help create what we believe to be an exciting environment for watching sports programming. We have also strategically invested over $52.8 million since the beginning of fiscal 2011 to introduce D&B Sports and modernize the exteriors, front lobbies, bars, dining areas and “Winner’s Circles” of select locations. As of September 2, 2014, we have remodeled three stores during fiscal 2014 and by the end of fiscal 2014, approximately 65% of our stores will either be new or remodeled to adopt our new store design. All of the new or remodeled stores contain an upgraded venue for watching live sports and other televised events, and approximately 87% of these stores contain the D&B Sports concept.

4

Table of Contents

History of Margin Improvement. We have a proven track record of identifying operational efficiencies and implementing cost saving initiatives and have increased our Adjusted EBITDA margins by approximately 510 basis points from fiscal 2010 to the twelve months ended August 3, 2014. We expect our continued focus on operating margins at individual locations and the deployment of best practices across our store base to yield incremental margin improvements, although there is no guarantee that this will occur. We believe we are well-positioned to continue to increase margins and remain focused on identifying additional opportunities to reduce costs. We are currently testing an eTicket initiative, which is a paperless ticket distribution system that we plan to roll out to all of our stores during fiscal 2015. We estimate that our eTicket initiative will result in annual savings in excess of $3.0 million. We leverage our investments in technology, such as our labor scheduling system and our proprietary technology linking games with Power Cards, to increase the overall performance of our stores while also enhancing the customer experience. Power Cards are magnetic stripe cards that enable a customer to play our games. A customer purchases “chips” that are used to play our games and are loaded to a Power Card at an automated kiosk or by an employee. Our business model has a relatively lower proportion of variable costs versus fixed costs compared to our competitors. We believe this creates operating leverage and gives us the potential to further improve margins and deliver greater earnings from expected future increases in comparable store sales and new store growth. Under our current cost structure, we estimate that we will realize more than 50% flow through to Adjusted EBITDA from any comparable store sales growth.

Store Model Generates Favorable Store Economics and Strong Returns. We believe our store model offering entertainment, food and beverages provides certain benefits in comparison to traditional restaurant concepts, as reflected by our average store revenues of $10.1 million and average Store-level EBITDA margins of 25.9% for comparable stores in fiscal 2013. Our entertainment offerings have low variable costs and produced gross margins of 85.4% for fiscal 2013. With approximately half of our revenues from entertainment, we have less exposure than traditional restaurant concepts to food costs, which represented only 8.6% of our revenues in fiscal 2013. Our business model generates strong cash flow that we can use to execute our growth strategy. We believe the combination of our Store-level EBITDA margins, our refined new store formats and the fact that our stores open with high volumes that drive margins in year one will help us achieve our targeted average year one cash-on-cash returns of approximately 35% and five-year average cash-on-cash returns in excess of 25% for both our large format and small format store openings, although there is no guarantee such results will occur. The 15 stores that we have opened since the beginning of 2008 (that have been open for more than 12 months as of August 3, 2014) have generated average year one cash-on-cash returns of 42.9%. For stores opened since 2009 that have been open for more than 12 months, we have also experienced an increase in average year one cash-on-cash returns, by vintage, including our six stores opened in fiscal 2011 and fiscal 2012, which have generated average year one cash-on-cash returns of 52.4%.

Commitment to Customer Satisfaction. We aim to enhance our combination of food, beverage and entertainment offerings through our service philosophy of providing a high quality and consistent customer experience through dedicated training and development of our team members and a corporate culture that encourages employee engagement. As a result, we have experienced significant improvement in our Guest Satisfaction Survey results since we began the surveys in 2007. In 2013, 82.0% of respondents to our Guest Satisfaction Survey rated us “Top Box” (score of 5 out of a possible 5) in “Overall Experience” and 83.8% of respondents rated us “Top Box” in “Intent to Recommend.” By comparison, in 2007, 44.0% of respondents rated us “Top Box” in “Overall Experience” and 64.8% of respondents rated us “Top Box” in “Intent to Recommend.” We utilize our loyalty program to market directly to members with promotional emails and location-based marketing. Through our loyalty program, we email offers and coupons to members and notify them of new games, food, drinks and local events. In addition, members can earn game play credits based on the dollar amount of qualifying purchases at our stores. We expect that as our loyalty program grows it will be an important method of maintaining customers’ connection with our brand and further drive customer satisfaction.

5

Table of Contents

Experienced Management Team. We believe we are led by a strong senior management team averaging over 25 years of experience with national brands in all aspects of casual dining and entertainment operations. In 2006, we hired our Chief Executive Officer, Stephen King. From fiscal 2006 to the twelve months ended August 3, 2014, under the leadership of Mr. King, Adjusted EBITDA has grown by 111.4%, Adjusted EBITDA margins have increased by approximately 780 basis points and employee turnover and customer satisfaction metrics have improved significantly. Our management team has invested approximately $4.0 million of cash in the equity of Dave & Buster’s and currently owns 2.7% of our outstanding common stock. We believe that our management team’s prior experience in the restaurant and entertainment industries combined with its experience at Dave & Buster’s provides us with insights into our customer base and enables us to create the dynamic environment that is core to our brand.

Our Growth Strategies

The operating strategy that underlies the growth of our concept is built on the following key components:

Pursue New Store Growth. We will continue to pursue what we believe to be a disciplined new store growth strategy in both new and existing markets where we feel we are capable of achieving consistently high store revenues and Store-level EBITDA margins as well as strong cash-on-cash returns. We believe that the Dave & Buster’s brand is currently significantly under-penetrated, as internal studies and third-party research suggests a total store potential in the United States and Canada in excess of 200 stores (including our 69 existing stores), approximately three times our current store base. We believe our new store opportunity is split fairly evenly between large format and small format stores. We plan to open seven to eight stores in fiscal 2014, including four stores we have already opened, which we expect will be financed with available cash and operating cash flows. Thereafter, we believe that we can continue opening new stores at an annual rate of approximately 10% of our then existing store base.

Our new store expansion strategy is driven by a site selection process that allows us to evaluate and select the location, size and design of our stores based on consumer research and analysis of operating data from sales in our existing stores. Our site selection process and flexible store design enable us to customize each store with the objective of maximizing return on capital given the characteristics of the market and the location. Our large format stores are 30,001 to 45,000 square feet in size and our small format stores span 25,000 to 30,000 square feet, which provides us the flexibility to enter new smaller markets and further penetrate existing markets. These formats also provide us with the ability to strategically choose between building new stores and converting existing space, which can be more cost efficient for certain locations. We are targeting average year one cash-on-cash returns of approximately 35% for both our large format and small format stores. To achieve this return for large format stores, we target average net development costs of approximately $8.3 million and first year store revenues of approximately $11.6 million. For small format stores, we target average net development costs of approximately $6.0 million and average first year store revenues of approximately $7.5 million. Additionally, we target average year one Store-level Adjusted EBITDA margins, excluding allocated national marketing costs, of approximately 28%, for both large format and small format stores.

Grow Our Comparable Store Sales. We intend to grow our comparable store sales by seeking to differentiate the Dave & Buster’s brand from other food and entertainment alternatives, through the following strategies:

| n | Provide our customers the latest exciting games. We believe that our Midway games are the core differentiating feature of the Dave & Buster’s brand, and staying current with the latest offerings creates new content and excitement to drive repeat visits and increase length of customer stay. We plan to continue to update approximately 10% of our games each year and seek to buy games that will resonate with our customers and drive brand relevance due to a variety of factors, including their large scale, eye-catching appearance, virtual reality features, association with recognizable brands or the fact that they cannot be easily replicated at home. We aim to leverage our investment in games by packaging our new game introductions and focusing our marketing spending to promote these events. We also plan to continually elevate the redemption experience in our “Winner’s Circle” with prizes that |

6

Table of Contents

| we believe customers will find more attractive, which we expect will favorably impact customer visitation and game play. |

| n | Leverage D&B Sports. In 2010, we initiated a program to improve our sports-viewing as part of our strategy to enhance our entertainment offering and increase customer traffic and frequency by creating another reason to visit Dave & Buster’s. This initiative evolved into the D&B Sports concept, which has been incorporated into all new stores opened since the beginning of fiscal 2013 and will continue to be incorporated into all new stores. In the fall of 2013, we launched a national advertising campaign for D&B Sports promoting Dave & Buster’s as the “only place to watch the games and play the games.” We intend to continue leveraging our investments in D&B Sports by building awareness of Dave & Buster’s as “the best place to watch sports” through national cable advertising. In addition, we are strategically expanding our year-round sporting and pay-per-view content to drive increased traffic and capture a higher share of the sports-viewing customer base. |

| n | Food and beverage offerings with broad appeal. Our menu has a variety of items, from hamburgers to steaks to seafood, that represent our “Fun American New Gourmet” strategy. We aim to ensure a pipeline for three new product launches each year, aligning with the timing of our new game launches. This strategy has been well received by our customers as the percentage of customers rating our food quality as “Excellent” was 79.6% in fiscal 2013, an increase of 480 basis points compared to fiscal 2011, and an increase of 4,170 basis points since fiscal 2007. Similarly, the percentage of customers rating our beverage quality as “Excellent” in fiscal 2013 was 82.3%, an increase of 490 basis points compared to fiscal 2011, and an increase of 4,250 basis points since fiscal 2007. |

| n | Grow our special events usage. The special events portion of our business represented 12.3% of our total revenues in fiscal 2013. We believe our special events business is an important sampling and promotional opportunity for our customers because many customers are experiencing Dave & Buster’s for the first time. We plan to leverage our existing special events sales force and call center to attract new corporate customers. In addition, we introduced online booking for social parties in order to provide additional convenience in booking events for our customers and look to expand its functionality over time. |

| n | Enhance brand awareness and generate additional visits to our stores through marketing and promotions. We believe offering new items from each of the “Eat Drink Play and Watch” pillars will keep the brand relevant to customers and drive traffic and frequency. We have identified five key promotional periods throughout the year when we feature this “New News” in national advertising. To increase national awareness of our brand, we plan to continue to invest a significant portion of our marketing expenditures in national cable television and radio advertising focused on promoting our capital investments in new games, D&B Sports and new food and beverage offerings. We also have customized local store marketing programs to increase new visits and repeat visits to individual locations. We will continue to utilize our loyalty program and digital efforts to communicate promotional offers directly to our most passionate brand fans, and we are aggressively optimizing our search engine and social marketing efforts. We also leverage our investments in technology across our marketing platform, including in-store marketing initiatives to drive incremental sales throughout the store. |

| n | Drive Customer Frequency Through Greater Digital and Mobile Connectivity. We believe that there is a significant potential to increase customer frequency by enhancing the in-store and out-of-store customer experience via digital and mobile strategic initiatives as well as through implementing enhanced technology. We intend to leverage our growing loyalty database as well as continue to invest in mobile game systems (game applications for mobile devices, such as smartphones and tablets), second screen sports-watching apps (applications for mobile devices, allowing our customers to enhance their sports-watching experience by, for example, accessing information about the live sporting event being watched or by playing along with the live sporting event) and social games (game applications that allow our customers to play online together, whether competitively or cooperatively) to create customer connections and drive recurring customer visitation. |

7

Table of Contents

Expand the Dave & Buster’s Brand Internationally. We believe that in addition to the growth potential that exists in North America, the Dave & Buster’s brand can also have significant appeal in certain international markets. We are currently assessing these opportunities while maintaining a conservative and disciplined approach towards the execution of our international development strategy. As such, we have retained the services of a third-party consultant to assist in identifying and prioritizing potential markets for expansion as well as potential franchise or joint venture partners. Thus far, we have identified our international market priorities and begun the process of identifying potential international partners within select markets. The market priorities were developed based on a specific set of criteria to ensure we expand our brand into the most attractive markets. Our goal is to sign an agreement with our first international partner by the end of fiscal 2014 and we are targeting our first international opening outside of Canada in 2016.

The Refinancing

On July 25, 2014, we entered into a new senior secured credit facility that provides a $530.0 million term loan facility and a $50.0 million revolving credit facility. The proceeds of the new senior secured credit facility were used to refinance in whole the prior senior secured credit facility (of which $143.5 million was outstanding as of July 25, 2014), repay in full $200 million aggregate principal amount of the 11.0% senior notes due June 1, 2018, repay all outstanding 12.25% senior discount notes due February 15, 2016 ($150.2 million accreted value as of July 25, 2014) and pay related premiums, interest and expenses. We refer to these transactions collectively as the “Refinancing.”

Use of Proceeds

We intend to use the net proceeds from this offering to repay a portion of term loan debt outstanding under the new senior secured credit facility, as well as to pay accrued interest and related expenses. After giving effect to the application of the proceeds from this offering, our aggregate indebtedness will be approximately $ million on an as adjusted basis as of August 3, 2014. See “Use of Proceeds” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources.”

Corporate History

We opened our first store in Dallas, Texas in 1982 and since then we have expanded our portfolio nationally to 69 company-owned stores across 26 states and Canada as of September 2, 2014.

From 1997 to early 2006, we operated as a public company under the leadership of our founders, David “Dave” Corriveau and James “Buster” Corley. In March 2006, Dave & Buster’s, Inc. was acquired by Dave & Buster’s Holdings, Inc. (“D&B Holdings”), a holding company controlled by affiliates of Wellspring Capital Partners III, L.P. (“Wellspring”) and HBK Main Street Investors L.P. (“HBK”). In connection with the acquisition of Dave & Buster’s, Inc. by Wellspring and HBK, Dave & Buster’s, Inc.’s common stock was delisted from the New York Stock Exchange. In addition, since 2006, our management team has been led by our Chief Executive Officer, Stephen King.

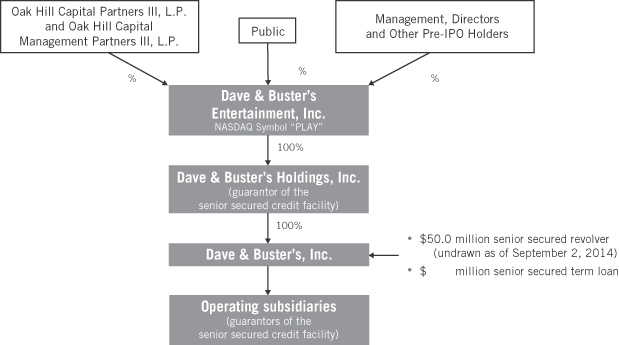

On June 1, 2010, Dave & Buster’s Entertainment, Inc., a newly-formed Delaware corporation owned by Oak Hill Capital Partners III, L.P. and Oak Hill Capital Management Partners III, L.P. (collectively, the “Oak Hill Funds” and together with their manager, Oak Hill Capital Management, LLC, and its related funds, “Oak Hill Capital Partners”), acquired all of the outstanding common stock (the “Acquisition”) of D&B Holdings from Wellspring and HBK. In connection therewith, Games Merger Corp., a newly-formed Missouri corporation and an indirect wholly owned subsidiary of Dave & Buster’s Entertainment, Inc., merged (the “Merger”) with and into D&B Holdings’ wholly owned, direct subsidiary, Dave & Buster’s, Inc. (with Dave & Buster’s, Inc. being the surviving corporation in the Merger). As a result of the Acquisition and certain post-acquisition activity, the Oak Hill Funds directly control approximately 95.4% of our outstanding common stock and have the right to appoint certain members of our Board of Directors, and certain members of our Board of Directors and management control approximately 4.5% of our outstanding common stock. The remaining 0.1% is owned by a former member of management. Upon completion of this offering, the Oak Hill Funds will beneficially own

8

Table of Contents

approximately % of our outstanding common stock, or % if the underwriters exercise their option to purchase additional shares in full, and certain members of our Board of Directors and our management will beneficially own approximately % of our common stock, or % if the underwriters exercise their option to purchase additional shares in full. The Oak Hill Funds will continue to own a majority of the voting power of our outstanding common stock. As a result, we will be a “controlled company” within the meaning of the corporate governance standards of NASDAQ. See “Principal Stockholders.”

Ownership Structure

The following chart gives effect to our ownership structure after this offering and the use of net proceeds therefrom(1):

| (1) | Assumes an offering at a price per share of $ , the midpoint of the price range set forth on the cover of this prospectus, and excludes the exercise of the option to purchase additional shares. See also “Use of Proceeds.” |

Oak Hill Capital Partners

Oak Hill Capital Partners is a private equity firm managing funds with more than $8 billion of initial capital commitments from leading entrepreneurs, endowments, foundations, corporations, pension funds and global financial institutions. Since its inception 28 years ago, the professionals at Oak Hill Capital Partners and its predecessors have invested in more than 70 significant private equity transactions across broad segments of the U.S. and global economies. Oak Hill Capital Partners applies an industry-focused approach to investing across four core sectors: Consumer, Retail & Distribution; Industrials; Media & Communications; and Services. Oak Hill Capital Partners works actively in partnership with management teams to implement strategic and operational initiatives to create franchise value. Dave & Buster’s represents a core investment theme of the firm’s Consumer, Retail & Distribution team, which has experience investing in the restaurant and specialty retail sectors, including prior investments in Duane Reade, Caribbean Restaurants, The Container Store, NSA International and TravelCenters of America, and a current investment in Earth Fare.

After completion of this offering, the Oak Hill Funds will continue to own a majority of the voting power of our outstanding common stock. See “Principal Stockholders.” We will also enter into a new stockholders’ agreement with the Oak Hill Funds in connection with this offering. As a result, the Oak Hill Funds will hold

9

Table of Contents

the power to elect a majority of the seats on our Board of Directors and will have certain designation and nomination rights upon the completion of this offering. The Oak Hill Funds will be entitled to designate directors to serve on the Board of Directors proportionate to the Oak Hill Funds’ (or one or more of their affiliates, to the extent assigned thereto) aggregate ownership of the outstanding shares of our common stock, at any meeting of stockholders at which directors are to be elected to the extent that the Oak Hill Funds do not have such proportionate number of director designees then serving on the Board of Directors; provided that for so long as the Oak Hill Funds (or one or more of their affiliates, to the extent assigned thereto), individually or in the aggregate, own 5% or more of the voting power of the outstanding shares of our common stock, the Oak Hill Funds will be entitled to designate one director designee to serve on the Board of Directors at any meeting of stockholders at which directors are to be elected to the extent that the Oak Hill Funds do not have a director designee then serving on the Board of Directors. Such proportionate number of director designees will be determined by taking the product of the Oak Hill Funds’ (or one or more of their affiliates, to the extent assigned thereto) aggregate ownership of the outstanding shares of our common stock multiplied by the then current number of directors on our Board of Directors (rounded up to the next whole number to the extent the product does not equal a whole number). The Oak Hill Funds’ director designees will initially be J. Taylor Crandall, Kevin M. Mailender and Tyler J. Wolfram and, therefore, the Oak Hill Funds will be entitled to designate additional directors in order for Oak Hill to have its proportionate number of director designees. We will expand the size of our Board of Directors if necessary to provide for such proportionate representation. Subject to applicable law and applicable NASDAQ rules, the stockholders’ agreement will also provide that the Oak Hill Funds will be entitled to nominate the members of the Nominating and Corporate Governance Committee. In addition, subject to applicable law and applicable NASDAQ rules, each other committee of our Board of Directors, other than the Audit Committee, will consist of at least one member designated by the Oak Hill Funds. When conflicts arise between the interests of the Oak Hill Funds or their affiliates and the interests of our stockholders, these directors may not be disinterested. The representatives of the Oak Hill Funds on our Board of Directors, by the terms of our amended and restated certificate of incorporation and stockholders’ agreement, are not required to offer us any transaction opportunity of which they become aware and could take any such opportunity for themselves or offer it to other companies in which they have an investment, unless such opportunity is expressly offered to them solely in their capacity as our directors (and therefore may be free to compete with us in the same business or similar business). Pursuant to the new stockholders’ agreement, the Oak Hill Funds and their affiliates will be reimbursed for certain costs and expenses. See “Certain Relationships and Related Transactions—New Stockholders’ Agreement” and “Risk Factors—Risks Related to our Capital Structure—Conflicts of interest may arise because some of our directors are principals of our principal stockholder.”

Corporate Information

Our corporate headquarters is located at 2481 Mañana Drive, Dallas, Texas, and our telephone number is (214) 357-9588. Our website is www.daveandbusters.com. Information contained on our website does not constitute a part of this prospectus.

10

Table of Contents

THE OFFERING

| Shares of Common Stock Offered by us |

shares ( shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Shares of Common Stock to be Outstanding After This Offering |

shares ( shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Option to Purchase Additional Shares |

The underwriters have an option to purchase from us up to a maximum of additional shares of our common stock. The underwriters can exercise this option at any time within 30 days from the date of this prospectus. |

| Use of Proceeds |

We estimate that the net proceeds to us from the offering of shares, after deducting underwriting discounts and estimated offering expenses, will be approximately $ million, assuming the shares are offered at $ (the midpoint of the price range set forth on the cover of this prospectus). We intend to use the net proceeds from this offering to repay a portion of term loan debt outstanding under the new senior secured credit facility, as well as to pay accrued interest and related expenses. See “Use of Proceeds.” |

| Dividend Policy |

We do not anticipate paying any dividends on our common stock, however, we may change this policy in the future. See “Dividend Policy.” |

| Proposed NASDAQ Symbol |

“PLAY” |

| LOYAL3 platform |

At our request, the underwriters have reserved up to % of the common stock to be sold by us in this offering to be offered through the LOYAL3 platform at the initial public offering price. See “Underwriting.” |

| Risk Factors |

You should carefully read and consider the information set forth under “Risk Factors” beginning on page 19 of this prospectus and all other information set forth in this prospectus before investing in our common stock. |

Unless otherwise indicated, the number of shares of common stock to be outstanding after this offering:

| n | excludes shares of our common stock issuable upon exercise of outstanding stock options under the Dave & Buster’s Entertainment, Inc. 2010 Management Incentive Plan (the “2010 Stock Incentive Plan”); and |

| n | excludes shares of our common stock reserved for issuances under our 2014 Omnibus Incentive Plan (the “2014 Stock Incentive Plan”) and issuable upon the exercise of options that we intend to grant to certain executive officers as of the time of this offering, including the named executive officers as described in “Executive Compensation—Compensation Discussion and Analysis—Elements of Compensation—Long-term Incentive Plan.” |

Unless otherwise noted, the information in this prospectus:

| n | gives effect to a for 1 stock split of our common stock prior to the consummation of this offering (rounded to the nearest whole share); |

11

Table of Contents

| n | gives effect to our amended and restated certificate of incorporation, which will be in effect prior to the consummation of this offering; |

| n | assumes no exercise of the underwriters’ option to purchase from us up to additional shares; and |

| n | assumes an initial public offering price of $ per share, the midpoint of the price range set forth on the cover of this prospectus. |

Risks Associated With Our Business

Our business is subject to numerous risks, which are highlighted in the section entitled “Risk Factors.” These risks represent challenges to the successful implementation of our strategy and the growth of our business. Some of these risks are:

| n | our ability to open new stores and operate them profitably; |

| n | changes in discretionary spending by consumers and general economic conditions; |

| n | our ability to compete favorably in the out-of-home and home-based entertainment and restaurant markets; |

| n | unauthorized use of our intellectual property; |

| n | potential claims for infringing the intellectual property right of others and the costs related to such claims; |

| n | damage to our brand or reputation; |

| n | failure or destruction of our information systems and other technology that support our business; |

| n | seasonality of our business and the timing of new openings and other events; |

| n | availability and cost of food and other supplies; and |

| n | our ability to operate our stores and obtain and maintain licenses and permits necessary for such operation in compliance with applicable laws and regulations. |

For a discussion of these and other risks you should consider before making an investment in our common stock, see the section entitled “Risk Factors.”

12

Table of Contents

SUMMARY HISTORICAL FINANCIAL AND OTHER DATA

Set forth below are our summary consolidated historical and as adjusted financial and other data for the periods ending on and as of the dates indicated.

Dave & Buster’s Entertainment, Inc. has no material assets or operations other than 100% ownership of the outstanding common stock of D&B Holdings. D&B Holdings has no material assets or operations other than 100% ownership of the outstanding common stock of Dave & Buster’s, Inc.

The statement of operations and cash flows data for each of the fiscal years ended February 2, 2014, February 3, 2013 and January 29, 2012 were derived from our audited consolidated financial statements included elsewhere in this prospectus. The statement of operations and cash flows data for each of the twenty-six week periods ended August 3, 2014 and August 4, 2013 and the balance sheet data as of August 3, 2014 were derived from our unaudited consolidated financial statements included elsewhere in this prospectus. In the opinion of management, the unaudited consolidated financial statements include all normal recurring adjustments necessary to present fairly the data for such periods and as of such dates.

We operate on a 52 or 53 week fiscal year that ends on the Sunday after the Saturday closest to January 31. Each quarterly period has 13 weeks, except in a 53 week year when the fourth quarter has 14 weeks. All fiscal years presented herein consist of 52 weeks, except fiscal year 2012, which consisted of 53 weeks.

Our historical results are not necessarily indicative of future results of operations. The summary of historical financial and other data should be read in conjunction with “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our historical consolidated financial statements and the notes related thereto, included elsewhere in this prospectus. All dollar amounts are presented in thousands except per share amounts.

13

Table of Contents

| TWENTY-SIX WEEKS ENDED |

FISCAL YEAR ENDED | |||||||||||||||||||

| AUGUST 3, 2014 |

AUGUST 4, 2013 |

FEBRUARY 2, 2014 |

FEBRUARY 3, 2013 |

JANUARY 29, 2012 |

||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Revenues: |

||||||||||||||||||||

| Food and beverage revenues |

$ | 177,898 | $ | 153,272 | $ | 310,111 | $ | 298,421 | $ | 272,606 | ||||||||||

| Amusement and other revenues |

198,310 | 168,606 | 325,468 | 309,646 | 268,939 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total revenues |

376,208 | 321,878 | 635,579 | 608,067 | 541,545 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating costs: |

||||||||||||||||||||

| Cost of products: |

||||||||||||||||||||

| Cost of food and beverage |

45,690 | 38,273 | 77,577 | 73,019 | 65,751 | |||||||||||||||

| Cost of amusement and other |

27,244 | 24,263 | 47,437 | 46,098 | 41,417 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total cost of products |

72,934 | 62,536 | 125,014 | 119,117 | 107,168 | |||||||||||||||

| Operating payroll and benefits |

85,120 | 72,546 | 150,172 | 145,571 | 130,875 | |||||||||||||||

| Other store operating expenses |

114,142 | 98,761 | 199,537 | 192,792 | 175,993 | |||||||||||||||

| General and administrative expenses |

20,069 | 17,922 | 36,440 | 40,356 | 34,896 | |||||||||||||||

| Depreciation and amortization expense |

34,673 | 33,650 | 66,337 | 63,457 | 54,277 | |||||||||||||||

| Pre-opening costs |

4,292 | 2,842 | 7,040 | 3,060 | 4,186 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating costs |

331,230 | 288,257 | 584,540 | 564,353 | 507,395 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income |

44,978 | 33,621 | 51,039 | 43,714 | 34,150 | |||||||||||||||

| Interest expense, net |

23,696 | 23,861 | 47,809 | 47,634 | 44,931 | |||||||||||||||

| Loss on debt retirement |

25,986 | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) before provision (benefit) for income taxes |

(4,704 | ) | 9,760 | 3,230 | (3,920 | ) | (10,781 | ) | ||||||||||||

| Provision (benefit) for income taxes |

(2,287 | ) | 2,308 | 1,061 | (12,702 | ) | (3,796 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | (2,417 | ) | $ | 7,452 | $ | 2,169 | $ | 8,782 | $ | (6,985 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) per share of common stock: |

||||||||||||||||||||

| Basic |

$ | (16.38 | ) | $ | 50.52 | $ | 14.70 | $ | 59.54 | $ | (45.58 | ) | ||||||||

| Diluted |

$ | (16.38 | ) | $ | 49.40 | $ | 14.34 | $ | 58.55 | $ | (45.58 | ) | ||||||||

| Weighted average number of shares outstanding: |

||||||||||||||||||||

| Basic |

147,586 | 147,506 | 147,512 | 147,506 | 153,250 | |||||||||||||||

| Diluted |

147,586 | 150,850 | 151,256 | 150,000 | 153,250 | |||||||||||||||

14

Table of Contents

| TWENTY-SIX WEEKS ENDED |

FISCAL YEAR ENDED | |||||||||||||||||||

| AUGUST 3, 2014 |

AUGUST 4, 2013 |

FEBRUARY 2, 2014 |

FEBRUARY 3, 2013 |

JANUARY 29, 2012 |

||||||||||||||||

| As Adjusted Consolidated Statements of Operations Data (1): |

||||||||||||||||||||

| As adjusted net income (loss) |

$ | $ | ||||||||||||||||||

| As adjusted net income (loss) per share: |

||||||||||||||||||||

| Basic |

$ | $ | ||||||||||||||||||

| Diluted |

$ | $ | ||||||||||||||||||

| As adjusted weighted average shares outstanding: |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

| Diluted |

||||||||||||||||||||

| Statement of Cash Flow Data: |

||||||||||||||||||||

| Cash provided by (used in): |

||||||||||||||||||||

| Operating activities |

$ | 10,451 | $ | 66,332 | $ | 109,878 | $ | 82,796 | $ | 72,777 | ||||||||||

| Investing activities |

(59,352 | ) | (45,559 | ) | (105,677 | ) | (78,488 | ) | (70,502 | ) | ||||||||||

| Financing activities |

76,172 | (1,568 | ) | (2,238 | ) | (1,875 | ) | (2,998 | ) | |||||||||||

| AS OF AUGUST 3, 2014 | ||||||

| ACTUAL | AS ADJUSTED (2) | |||||

| Balance Sheet Data: |

||||||

| Cash and cash equivalents |

$ | 65,351 | ||||

| Net working capital (3) |

9,486 | |||||

| Property and equipment, net |

406,411 | |||||

| Total assets |

908,124 | |||||

| Total debt, net of unamortized discount |

528,681 | |||||

| Stockholders’ equity |

148,600 | |||||

| TWENTY-SIX WEEKS ENDED |

FISCAL YEAR ENDED | |||||||||||||||||||

| AUGUST 3, 2014 |

AUGUST 4, 2013 |

FEBRUARY 2, 2014 |

FEBRUARY 3, 2013 |

JANUARY 29, 2012 |

||||||||||||||||

| Store-level Data: |

||||||||||||||||||||

| Stores open at end of period (4) |

69 | 62 | 66 | 61 | 58 | |||||||||||||||

| Comparable stores (5) |

57 | 55 | 55 | 54 | 52 | |||||||||||||||

| Comparable store sales increase (6) |

5.2 | % | 0.5 | % | 1.0 | % | 3.0 | % | 2.2 | % | ||||||||||

| Store-level EBITDA (7) |

$ | 104,012 | $ | 88,035 | $ | 160,856 | $ | 150,587 | $ | 127,509 | ||||||||||

| Store-level EBITDA margin (8) |

27.6 | % | 27.4 | % | 25.3 | % | 24.8 | % | 23.5 | % | ||||||||||

15

Table of Contents

| TWENTY-SIX WEEKS ENDED |

FISCAL YEAR ENDED | |||||||||||||||||||

| AUGUST 3, 2014 |

AUGUST 4, 2013 |

FEBRUARY 2, 2014 |

FEBRUARY 3, 2013 |

JANUARY 29, 2012 |

||||||||||||||||

| Other Data: |

||||||||||||||||||||

| Adjusted EBITDA (9) |

$ | 89,059 | $ | 74,838 | $ | 134,790 | $ | 120,478 | $ | 98,372 | ||||||||||

| Adjusted EBITDA margin (10) |

23.7 | % | 23.3 | % | 21.2 | % | 19.8 | % | 18.2 | % | ||||||||||

| Capital additions (11): |

||||||||||||||||||||

| New store |

$ | 30,082 | $ | 27,375 | $ | 72,301 | $ | 32,795 | $ | 43,951 | ||||||||||

| Operating initiatives, including remodels |

9,920 | 13,094 | 21,930 | 21,946 | 10,380 | |||||||||||||||

| Games |

7,601 | 6,384 | 11,413 | 10,090 | 7,196 | |||||||||||||||

| Maintenance |

5,122 | 4,254 | 14,238 | 13,858 | 11,419 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total capital additions |

$ | 52,725 | $ | 51,107 | $ | 119,882 | $ | 78,689 | $ | 72,946 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | As adjusted consolidated statement of operations data gives effect to (i) a for 1 stock split of our common stock prior to the completion of this offering, (ii) the Refinancing as described in “—The Refinancing” and (iii) the receipt and application of $ of net proceeds to us from this offering based on an initial public offering price of $ per share (the mid-point of the range set forth on the cover of this prospectus) as described in “Use of Proceeds,” as if they had occurred on February 4, 2013 with respect to fiscal year 2013 and February 3, 2014 with respect to the twenty-six weeks ended August 3, 2014. As adjusted net income (loss) reflects (i) the net decrease in interest expense resulting from the prepayment of $ principal amount of our indebtedness as described in “Use of Proceeds, ” (ii) premiums, interest and expenses related to the Refinancing of $ and (iii) the tax effects of these changes on income before taxes. The as adjusted consolidated statements of operations data is not necessarily indicative of what our results of operations would have been if the transaction had been completed as of the date indicated, nor is such data necessarily indicative of our results of operations for any future period. |

The table below provides a summary of net income (loss) used in the calculation of basic and diluted net income per common share calculated on an as adjusted basis (in thousands).

| TWENTY-SIX WEEKS ENDED |

FISCAL YEAR ENDED |

|||||||

| AUGUST 3, 2014 |

FEBRUARY 2, 2014 |

|||||||

| Net income (loss) |

$ | (2,417 | ) | $ | 2,169 | |||

| Reduction of interest expense |

||||||||

| Loss on debt retirement |

25,986 | — | ||||||

| Increase in income tax expense |

||||||||

|

|

|

|

|

|||||

| As adjusted net income |

$ | $ | ||||||

|

|

|

|

|

|||||

| (2) | The as adjusted balance sheet data gives effect to the receipt and application of $ of net proceeds to us from this offering as described in “Use of Proceeds,” as if it had occurred as of August 3, 2014. The as adjusted balance sheet data is not necessarily indicative of what our financial position would have been if the transaction had been completed as of the date indicated, nor is such data necessarily indicative of our financial position for any future date. |

| (3) | Defined as total current assets minus total current liabilities. |

| (4) | Our location in Nashville, Tennessee, which temporarily closed from May 2, 2010 to November 28, 2011 due to flooding, is included in our store count for all periods presented. Our Kensington/Bethesda, Maryland location (which permanently closed on August 12, 2014) is included in store counts for all periods presented. Also included in the store counts as of January 29, 2012 is a store in Dallas, Texas which permanently closed on December 17, 2012. |

| (5) | “Comparable stores” are stores open at least 18 months as of the beginning of each of the relevant fiscal years, excluding our one franchised store located in Canada, which ceased operation as a Dave & Buster’s on May 31, 2013. Our fiscal 2014 comparable stores exclude the Kensington/Bethesda, Maryland location, which permanently closed on August 12, 2014. |

| (6) | “Comparable store sales increases” reflect the year-over-year changes, on a calendar week basis, for the stores as defined as comparable in (5) above. |

16

Table of Contents

| (7) | “Store-level EBITDA” is defined by us as net income (loss), plus interest expense (net), loss on debt retirement, provision (benefit) for income taxes, depreciation and amortization expense, general and administrative expenses and pre-opening costs, as shown in the table below. We use Store-level EBITDA to measure operating performance and returns from opening new stores. Similar to Adjusted EBITDA, Store-level EBITDA is not defined under GAAP and does not purport to be an alternative to net income as a measure of operating performance. |

| We believe that Store-level EBITDA is another useful measure in evaluating our operating performance because it removes the impact of general and administrative expenses, which are not incurred at the store level, and the costs of opening new stores, which are non-recurring at the store-level, and thereby enables the comparability of the operating performance of our stores for the periods presented. We also believe that Store-level EBITDA is a useful measure in evaluating our operating performance within the entertainment and dining industry because it permits the evaluation of store-level productivity, efficiency and performance, and we use Store-level EBITDA as a means of evaluating store financial performance compared with our competitors. However, because this measure excludes significant items such as general and administrative expenses and pre-opening costs, as well as our interest expense and depreciation and amortization expense, which are important in evaluating our consolidated financial performance from period to period, the value of this measure is limited as a measure of our consolidated financial performance. Our calculation of Store-level EBITDA for the periods is presented below: |

| TWENTY-SIX WEEKS ENDED |

FISCAL YEAR ENDED | |||||||||||||||||||

| AUGUST 3, 2014 |

AUGUST 4, 2013 |

FEBRUARY 2, 2014 |

FEBRUARY 3, 2013 |

JANUARY 29, 2012 |

||||||||||||||||

| Net income (loss) |

$ | (2,417 | ) | $ | 7,452 | $ | 2,169 | $ | 8,782 | $ | (6,985 | ) | ||||||||

| Interest expense, net |

23,696 | 23,861 | 47,809 | 47,634 | 44,931 | |||||||||||||||

| Loss on debt retirement |

25,986 | — | — | — | — | |||||||||||||||

| Provision (benefit) for income taxes |

(2,287 | ) | 2,308 | 1,061 | (12,702 | ) | (3,796 | ) | ||||||||||||

| Depreciation and amortization expense |

34,673 | 33,650 | 66,337 | 63,457 | 54,277 | |||||||||||||||

| General and administrative expenses |

20,069 | 17,922 | 36,440 | 40,356 | 34,896 | |||||||||||||||

| Pre-opening costs |

4,292 | 2,842 | 7,040 | 3,060 | 4,186 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Store-level EBITDA |

$ | 104,012 | $ | 88,035 | $ | 160,856 | $ | 150,587 | $ | 127,509 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (8) | “Store-level EBITDA margin” represents Store-level EBITDA divided by total revenues. Store-level EBITDA margin allows us to evaluate operating performance of each store across stores of varying size and volume. |

| (9) | “Adjusted EBITDA” is calculated as net income (loss), plus interest expense (net), loss on debt retirement, provision (benefit) for income taxes, depreciation and amortization expense, loss on asset disposal, share-based compensation, currency transaction (gain) loss, pre-opening costs, reimbursement of affiliate and other expenses, change in deferred amusement revenue and ticket liability estimations, transaction and other costs. |

Adjusted EBITDA is presented because we believe that it provides useful information to investors regarding our operating performance and our capacity to incur and service debt and fund capital expenditures. We believe that Adjusted EBITDA is used by many investors, analysts and rating agencies as a measure of performance. In addition, Adjusted EBITDA is approximately equal to “EBITDA” as defined in our senior secured credit facility and our presentation of Adjusted EBITDA is consistent with that reported to our lenders to allow for leverage-based assessments. By reporting Adjusted EBITDA, we provide a basis for comparison of our business operations between current, past and future periods by excluding items that we do not believe are indicative of our core operating performance. Adjusted EBITDA is a metric utilized to measure performance-based bonuses paid to our executive officers and certain managers.