Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - China Integrated Energy, Inc. | v388082_ex31-1.htm |

| EX-31.2 - EXHIBIT 31.2 - China Integrated Energy, Inc. | v388082_ex31-2.htm |

| EX-32.1 - EXHIBIT 32.1 - China Integrated Energy, Inc. | v388082_ex32-1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment No. 2

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended: December 31, 2010

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from __________ to __________

Commission File No. 000-25413

| China Integrated Energy, Inc. |

| (Exact Name of Registrant as Specified in its Charter) |

| Delaware | 65-0854589 | |

| (State or Other Jurisdiction of | (I.R.S. Employer Identification No.) | |

| Incorporation or Organization) | ||

| 10F, Western International Square | ||

| 2 Gaoxin Road | ||

| Xi'an, Shaanxi Province, China | 710075 | |

| Address of Principal Executive | (Zip Code) |

Registrant’s telephone number, including area code: +86-29-65681111

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, par value $0.0001 per share | NASDAQ Capital Market | |

| (Title of Class) | (Name of exchange on which registered) |

Securities registered pursuant to section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer (Do not check if a smaller reporting company) ¨ | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of 11,891,746 shares held by non-affiliates of the issuer, based on the last sale price $8.30 of the common stock, as reported on the Nasdaq Capital Market on June 30, 2010, was $98,701,492.

As of August 29, 2014, there were 44,503,379 shares of the issuer’s common stock, par value $0.0001 per share, outstanding.

Documents incorporated by reference : None

TABLE OF CONTENTS

| i |

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements. These statements relate to future events or our future financial performance. We have attempted to identify forward-looking statements by terminology including “anticipates”, “believes”, “expects”, “can”, “continue”, “could”, “estimates”, “expects”, “intends”, “may”, “plans”, “potential”, “predict”, “should” or “will” or the negative of these terms or other comparable terminology. These statements are only predictions. Uncertainties and other factors may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels or activity, performance or achievements expressed or implied by these forward-looking statements.

| Item 1. | Business. |

Overview

We are a leading non-state-owned integrated energy company in China engaged in three business segments, the wholesale distribution of finished oil and heavy oil products, the production and sale of biodiesel and the operation of retail gas stations. Our major business segment is the wholesale distribution of finished oil and heavy oil products. We sell primarily gasoline, diesel and heavy oil in 16 provinces and municipalities through seven sales offices located in various regions of China. We also have four oil storage depots located in Shaanxi Province. Of the four oil storage depots, we own one, lease one and have the rights to use two of the depots through oil storage service agreements with the state-owned entities that own such depots. We are one of only four non-state-owned distributors in Shaanxi Province that are licensed to sell both finished oil and heavy oil products, and are a leading non-state-owned distributor in Shaanxi Province distributing all grades of gasoline, diesel and heavy oil. We currently enjoy convenient railway freight access enabling us to distribute our products to Sichuan, Guizhou and Yunnan Provinces. As a high volume distributor, we experience high inventory turnover with minimum inventory exposure, and have therefore been able to maintain a stable margin in our distribution business despite the volatility of global oil prices. We plan to grow our wholesale distribution of finished oil and heavy oil business by increasing our coverage area and further penetrating our existing customers and territories.

We operate two biodiesel production plants, one biodiesel production plant located in Tongchuan City, which has a 100,000 ton design capacity, but a 90,000 ton production capacity and another biodiesel plant in Chongqing City that has a 50,000-ton design capacity. The Chongqing biodiesel facility uses first generation biodiesel production technology, similar to the production process used in Tongchuan City’s production plant. At full capacity, our Chongqing biodiesel facility can achieve gross margins of approximately 30%. We have completed construction of an additional 50,000-ton biodiesel production plant adjacent to the existing plant in Tongchuan City, Shaanxi Province. However, due to a catalyst bottleneck that occurred in 2012, currently the new plant is not operational. We are working with a national chemical institute to replace the catalyst and/or find another solution so that we can continue operations at the new plant as soon as possible. We intend to deploy advanced second-generation production technology as a critical component of the new facility and estimate that we will be able to reduce production costs at the facility by approximately 20%.

We believe that we are one of the largest biodiesel producers in China measured by production capacity as of the end of 2010, and the only non-state-owned integrated biodiesel producer with a distribution license. We leverage our wholesale distribution channels to sell our biodiesel to our existing customers and to acquire new customers. We have been awarded four patents relating to the use of multiple feedstock interchangeably in first-generation biodiesel production. Our biodiesel feedstock includes non-edible seed oil, waste cooking oil and vegetable oil residue, most of which have limited alternative uses. Therefore, our biodiesel production is environmentally friendly and does not require valuable farmland to grow its feedstock. In addition to the feedstock used in our existing first-generation facility, the new second-generation facility will be able to utilize a diverse supply of raw materials, such as crop straw (including wheat straw, corn straw, cotton straw and weed), agricultural biomass waste (including tree branches and tree leaves), as well as other organic waste. This feedstock flexibility affords us better input cost controls. The second-generation biodiesel that will be produced at our new facility is expected to meet Europe IV fuel standards and can be mixed with both diesel and first-generation biodiesel at any ratio. Furthermore, the second-generation production technology is expected to allow us to recycle bio-residual and water used in the production process, meeting our environmental goals while delivering further cost reductions. Our biodiesel can be blended with regular petro-diesel and used by existing diesel engines with no change in engine performance.

| 1 |

In 2010, we operated thirteen retail gas stations. Of the thirteen retail gas stations, we own three and lease ten. The average annual sales volume of each gas station is approximately 8,000 tons, equivalent to approximately 2.7 million gallons. During 2011, four gas station leases were cancelled by Shaanxi Highway Services Co., Ltd. as part of the government's effort to reduce the number of gas stations leased to third party operators. The other two leased gas stations were terminated due to the owner's decision to sell the gas station in connection with a project undertaken by the local government to widen the road. With our distribution license and stable finished oil supply, we generate more stable and higher margins from our sale of finished oil at the retail gas stations than from our wholesale distribution of finished oil and heavy oil business, since we sell directly to retail end customers. We plan to continue to expand our portfolio of retail gas stations through leasing or acquisitions. We are continuously looking for high-traffic locations within and outside of Xi’an City to add to our retail gas station portfolio. Due to fierce competition from Petrochina, SINOPEC and Shell in the gas station market, our gas station acquisition target will focus on secondary cities and cities at the county level.

Our total sales revenues increased to $438.7 million for year ended December 31, 2010 from $289.6 million in the same period of 2009, representing an increase of 51.45%. Our net income increased to $53.8 million for the year ended December 31, 2010 from $37.9 million in the same period of 2009, representing an increase of 42.1%.

Our Strengths

The following competitive strengths have been the foundation of our strong performance, and we expect that they will continue to facilitate our future growth:

Vertically integrated business model

We believe our vertically integrated business model has the following benefits:

| · | Our existing wholesale and retail distribution channels facilitate sale of our biodiesel without sacrificing margin to third-party distributors; |

| · | We have a stable source of supply at lower cost for the production of biodiesel, better profitability, and enhanced control of our supply chain; and |

| · | Blending biodiesel with petro-diesel gives us pricing flexibility and a competitive advantage to gain market share from traditional distributors. |

Secured access to abundant, diversified, and low-cost raw materials for biodiesel production

We have access to a stable and diversified source of biodiesel raw materials. In addition to non-edible seed oil, we also use waste cooking oil and vegetable oil residue as raw material for the first-generation biodiesel production. We were awarded four patents for biodiesel production processes that enable us to use multiple sources of raw materials interchangeably. Between 2006 and 2013, we filed 14 patent applications with the SIPO, all of which are related to our biodiesel production. The SIPO has approved the four applications for utility model patents and one invention patent, allowed the three invention patent applications to pass preliminary examination and accepted the other patent applications for review. We maintain a flexible procurement model in which we adjust the relative quantities of each type of raw material we purchase, depending on their respective purchase prices, to minimize our raw material costs. In 2010, non-edible seed oil, vegetable oil residue and waste cooking oil accounted for approximately 21.8%, 37.5% and 40.7%, respectively of our raw material costs relating to our first-generation biodiesel production in Tongchuan City.

| 2 |

We are strategically located in Shaanxi Province in the northwestern region of China, where the mountainous terrain and abundant sunlight are especially suitable for planting non-edible oil plants such as Chinese prickly ash, cornel and Chinese pistache. Shaanxi Province has one of the largest areas of cultivation of Chinese prickly ash in China. The local farmers in Shaanxi have planted 2,460,000 mu (equivalent to 405,000 acres) of Chinese prickly ash, and 6,800,000 mu (equivalent to 1,120,000 acres) of Chinese pistache to produce over 430,000 tons of biodiesel. The Shaanxi Provincial Government plans to permit additional forest lands to be used solely for the planting of non-edible oil plants. We currently have secured access to non-edible seed oil for production of approximately 22,000 tons of biodiesel. We believe the abundant supply of feedstock currently available, in addition to the non-edible oil plants the government plans to permit farmers to cultivate, is sufficient for our current needs and will be sufficient for our increasing demands for raw materials after we increase our production capacity as planned.

We also have secured access to vegetable oil residue and waste cooking oil for production of approximately 78,000 tons of biodiesel through annual contracts with vegetable oil factories and waste cooking oil collecting centers.

We believe our biodiesel feedstock suppliers have a strong incentive to sell their products to us at competitive prices given that:

| · | There are very few alternative uses of non-edible oil seeds, vegetable oil residue and waste cooking oil; |

| · | We are the only non-state-owned biodiesel producer with commercial scale in northwestern China; and |

| · | We provide our suppliers with a legitimate means to dispose of waste cooking oil and vegetable oil residue. |

Established relationships with our suppliers and customers

We have been operating in the wholesale distribution of finished oil and heavy oil business since 1999 and have established strong relationships with our suppliers and customers. We believe that we have been one of the leading non-state-owned distributors of finished oil and heavy oil in Shaanxi Province. Our largest supplier, Shaanxi Yanchang Group, is the fourth largest oil company in China with over 10 million tons of refinery capacity. We have a long-standing relationship with Shaanxi Yanchang Group, which includes establishing representative offices with three oil refineries owned by Shaanxi Yanchang Group in Shaanxi Province.

We focus on customer satisfaction and believe that we have consistently delivered high quality products and services to our customers. We believe we have an established reputation among our customers and are able to maintain long-term relationships with them as evidenced by our customer retention rate and the increasing number of new customers. Our sales volume also increased significantly from 2007 through 2010.

We believe that both our suppliers and customers prefer to work with us for the following reasons:

| · | We are an established player with a large-scale operation and stable supply; |

| · | We have a strong financial position and provide flexibility in payment terms; and |

| · | We have a professional purchase and sales team, which is responsive to suppliers’ and customers’ needs. |

Early mover advantages

We were one of the first non-state-owned enterprises to engage in the wholesale distribution of finished oil and heavy oil products in Shaanxi Province. During the past 12 years, we have gradually built up our operational infrastructure, including extensive distribution channels, and four oil storage depots, plus we haveconvenient access to strategic railway lines. We have also obtained relevant licenses to conduct our wholesale distribution business, which has become increasingly more difficult for new entrants in our industry to obtain.

| 3 |

We believe that being an early mover in this industry has provided us the following advantages:

| · | Sales network. We have sales offices in seven locations with 36 full-time salespersons covering 16 provinces and municipalities in China. |

| · | Storage capability. We currently use four oil storage depots with total capacity of 59,000 m 3. We own one of the oil storage depots, lease one oil storage depot and have the rights to use two oil storage depots through oil storage service agreements. |

| · | Access to railway lines. We benefit from convenient access to railway lines that we use to transport and distribute our oil products from Shaanxi Province to Yunnan Province, Guizhou Province and Sichuan Province. We believe that we are currently the only enterprise in Shaanxi Province that has such a capability. |

| · | Wholesale distribution license. In June 2000, we were granted a wholesale distribution license to distribute finished oil products by the State Economic and Trade Commission. We are now one of the only four non-state-owned distributors that are licensed to distribute both finished oil and heavy oil products in Shaanxi Province. |

We believe that our wholesale distribution license and the operational infrastructure we have built help us to compete effectively and also form a barrier for any prospective new entrants into our industry.

Experienced management team with proven track record

We have an experienced management team led by Mr. Xincheng Gao, our chairman, chief executive officer and president. Mr. Gao has extensive experience in the research and marketing of oil products. In 1999, Mr. Gao founded Xi’an Baorun Industrial Development Co., Ltd. (Xi’an Baorun Industrial) to process and distribute finished oil and heavy oil products. Prior to founding Xi’an Baorun Industrial, Mr. Gao worked in the Oil and Chemicals Department of Shaanxi Province and Zhongtian Oil and Chemical Group, responsible for research and development and marketing. With Mr. Gao’s vision and leadership, we have grown from a traditional distributor of finished and heavy oil products to a leading non-state-owned integrated energy company. Our sales have grown from $289.6 million in 2009 to $438.7 million in 2010, while net income has grown from $37.9 million to $53.8 million over the same period.

Most of the members of our senior management team have worked together since 2005 and have an average of 10 years of experience in the oil business. We believe our management team’s in-depth market knowledge and strong track record in the oil market in China will enable us to take advantage of the anticipated growth in demand in the energy market.

| 4 |

Our Growth Strategies

Our key growth strategies include the following:

Continue to increase our biodiesel production capacity and improve control of the raw material supply

We have increased our biodiesel production capacity by 50,000 tons through construction of a new facility to supplement the demand for petro-diesel. We commenced construction on that new facility in the fourth quarter of 2009 and completed construction in the third quarter of 2011. Due to a catalyst bottleneck that occurred in 2012, the plant is not currently operational. We are working with a national chemical institute to replace the catalyst and/or find another solution so that we can continue operations. We have invested approximately $19 million in capital expenditures to accomplish this goal. In October 2010, we acquired Chongqing Tianrun Energy Development Co., Ltd., a 50,000-ton biodiesel plant. The Chongqing biodiesel facility uses first generation biodiesel production technology, similar to the production process used in the Tongchuan City production plant, which has a 100,000 ton design capacity, and a 90,000 ton production capacity. At full capacity, our Chongqing biodiesel facility can achieve gross margins of approximately 30%. We invested approximately $16.5 million in cash from cash on hand for the Chongqing biodiesel facility. We expect to benefit from the continued growth in overall energy consumption in China. We believe that we are one of the largest biodiesel producers in China based on production capacity at the end of 2010 and the only non-state-owned biodiesel producer with a distribution license. We continue to position ourselves as a leader in terms of capability, capacity and technology in this young biodiesel industry. Although we have secured abundant feedstock supply to support our current biodiesel production, we will continue to work with provincial and local agriculture administrations and environmental protection agencies for better cooperation and support for priority purchase of agricultural feedstock, waste cooking oil, and vegetable oil residue. We also will continue to work with leading universities and research institutes to develop alternative sources of feedstock to strengthen our supply chain and cost flexibility for biodiesel raw materials.

We have historically been able to secure a sufficient supply of raw materials and we will continue to work towards securing more long-term sources of raw materials and seeking new technology in the bio-energy field to improve production efficiency. We will continue pursuing strategic acquisitions that will quickly provide financial benefits to us. Our mid-term goal is establish a strong technological platform in biodiesel production and occupy more market share in the next few years.

Strengthen our relationship with key suppliers for finished oil and heavy oil and diversify our supply base

Stability of supply chain is one of the critical elements of a successful wholesale distributor of finished oil and heavy oil. We have had a long-term strong working relationship with Shaanxi Yanchang Group, our largest finished oil and heavy oil products supplier. We will also continue to maintain good relationships with other oil suppliers to ensure favorable pricing terms and a stable supply of oil products. In addition, we are also focused on exploring opportunities with new suppliers with significant oil resources and better pricing in different regions to diversify our supply chain and enhance our sales margin. We have found new vendors in Shandong and Xinjian Provinces to support our customers in those regions.

Expand our wholesale and retail distribution network through both organic growth and potential acquisitions

With stable and abundant oil supply, we will continue to expand our wholesale distribution of finished oil and heavy oil products by increasing the number of our regional sales offices and sales staff in various territories to develop new markets and a wider customer base. We will also continue penetrating existing territories to develop new customers and meet increased demand from our existing customers as their businesses grow. We will continue scouting high traffic locations to expand our portfolio of retail gas stations to create additional sales and higher profitability for our overall distribution channels. We foresee industry consolidation and believe that we are well-positioned to benefit from such market trends. We are in the position to acquire distressed competitors with working capital difficulties, if and when opportunities are presented.

Continue application process to obtain oil import/export license

In 2008, we submitted an application for an oil import/export license. In October 2013, we obtained the approval regarding the fuel oil import license from the foreign trade department of MOFCOM.

Enhance R&D efforts to improve biodiesel production technology and efficiency

We will continue investing resources and working closely with leading universities and research and development institutes that specialize in agricultural research to develop new technologies for more efficient and cost-effective biodiesel production. We will also continue to search for alternative feedstock to enhance the availability of raw materials and reduce costs of feedstock for biodiesel production.

| 5 |

Business Segments

Wholesale Distribution of Finished Oil and Heavy Oil Products

Oil supply

We sell on a wholesale basis a variety of oil products including gasoline, diesel, heavy oil and naphtha. Gasoline and diesel represent the majority of oil products consumed in China. Automobiles are the most important driver of gasoline consumption in China. Diesel is mainly used in vehicles and agricultural machines with diesel engines. Heavy oil is broadly used as fuel for ship boilers, heating furnaces, metallurgical furnaces and other industrial furnaces. Wholesale distribution of finished oil and heavy oil products accounted for approximately 62.3% of our total sales in 2010 and approximately 68.0% of our total sales in 2009.

Based on volume, we purchased approximately 49.9% of our gasoline and diesel oil products from our top five suppliers in 2010. During 2010, based on cost, we purchased approximately 20.3% (compared to 30.8% in 2009) of our gasoline and diesel oil products from Shaanxi Yanchang Group, with whom we have had a strong relationship since establishing Xi’an Baorun Industrial, which included establishing supply and purchasing stations with three oil refineries that are owned by Shaanxi Yanchang Group in Shaanxi Province. While we depend on Shaanxi Yanchang Group for the majority of our gasoline and oil supply needs, we are actively seeking other sources of oil supply and believe that we can find alternative suppliers with comparable terms within a reasonable amount of time without any significant disruption in our operations.

Storage

We use four oil storage depots, which in the aggregate have the capacity to store approximately 59,000 m 3 of oil products. We constructed one oil storage depot located within our biodiesel production facility in Tongchuan City, Shaanxi Province, lease one oil storage depot in Tongchuan City and have the rights to use two state-owned oil storage depots located in Xi’an City and Weinan City, Shaanxi Province through oil storage service agreements. The terms of the lease agreement and the oil storage service agreements range from two years to eight years and these agreements are renewable every two years. Two of the state-owned depots are located on railways that provide us convenient access for distributing our products.

Sales and Marketing

We developed a stable sales network for our products in 16 provinces and municipalities of China covering Shaanxi Province, Henan Province, Hebei Province, Shandong Province, Shanxi Province, Hunan Province, Hubei Province, Sichuan Province, Guizhou Province, Yunnan Province, Fujian Province, Xinjiang Province, Beijing, Guangxi Province, Gansu Province and Ningxia Hui Autonomous Region. We now employ 36 full-time salespersons in sales offices located in Chengdu City, Yingbuo City in Shandong Province and the cities of Yanglian, Lingtong, Shangqiao, Chengxiang, and Yongpin in Shaanxi Province. As our business expands, we intend to further expand our sales network and develop more sales channels. For our wholesale distribution of finished oil and heavy oil business segment, we plan to increase our distribution to an additional two provinces in the next 18 months, adding additional salespersons and establishing more regional sales offices. We plan to increase our sales volume through increasing our distribution footprint and further penetrating existing customers and business territories.

Customers

We currently sell our finished oil and heavy oil products to regional distributors in China that supply to industrial customers, retail service stations. We also provide finished oil products to our retail gas stations to directly sell to end users. We have adopted different terms for payment based upon the financial strength of the customer. For example, we have entered into agreements with PetroChina, SINOPEC, and other state-owned enterprises whereby we deliver products to agreed-upon locations and these customers agree to pay us after delivery. However, we require partial pre-payment in advance and cash on delivery from our customers that operate distributorships or own and operate private gas stations. These customers typically pay 10% to 15% of the total purchase price of the products to be delivered in advance, and when delivery takes place, they pay the remaining amounts owed. In 2010 and 2009, there was one customer that accounted for 25% or more of our sales. We did not experience any uncollectible accounts receivable or bad debt write-offs during 2007 through 2010.

For the years ended December 31, 2009 and 2010, our top five customers purchased approximately $113.2 million and $167.0 million of our products, representing approximately 39.1% and 38.1% of our sales during the period, respectively. China Petroleum and Chemical Corporation Chuanyu Trading Co., Ltd., our largest customer, accounted for approximately 25.4% and 26.6%of our sales in 2010 and 2009, respectively.

| 6 |

Competition

We are one of the only four non-state-owned enterprises licensed to distribute both finished oil and heavy oil products in Shaanxi Province. Although barriers to entry in our industry are high due to stringent licensing requirements and the need for significant storage capacity for products, we face competition from other established companies located in other provinces and within Shaanxi Province that also engage in the wholesale distribution of finished and heavy oils. Such companies may have greater financial resources, sales resources, storage capacity and transportation capacity than we do, and may have exclusive supply and purchase arrangements with suppliers as a result of long-term relationships.

In addition to SINOPEC and Petro China, we estimate that we have approximately ten major non-state-owned competitors in Shaanxi Province that also distribute finished oil products similar to ours, including Shaanxi Dongda Petro-Chemical Co., Ltd., Shaanxi Dayun Petrochemical Material Co., Ltd. and Baoji Huahai Industry Corp.

We believe we have the following advantages over our competitors in this market:

| · | Oil wholesale distribution license. In June 2000, we were granted a wholesale distribution license to distribute finished oil products by the State Economic and Trade Commission. We are now one of the only four non-state-owned distributors that are licensed to distribute both finished oil and heavy oil products in Shaanxi Province. |

| · | Supply advantage. Shaanxi Yanchang Group, one of the four largest qualified crude oil and gas exploration enterprises in China, is our largest oil supplier. In Shaanxi Province, we are one of the only few entities that have established supplying and purchasing stations with Shaanxi Yanchang Group. |

| · | Railway access. We benefit from convenient access to a railway line in Shaanxi Province to distribute our oil products. We believe we are currently the only enterprise in Shaanxi Province that has railway access to distribute oil products directly to Yunnan, Guizhou and Sichuan Provinces. |

| · | Storage capability. We have an aggregate oil depot storage capacity of 59,000 m 3. Aside from the need for strong funding support, new entrants to this industry must also have significant storage capacity to be able to compete, which is a barrier to entry for new competitors. |

Production and Sale of Biodiesel

Production

In 2006, we built a 10,000 square meter biodiesel production facility with annual design capacity of 100,000 tons and production capacity of 90,000 tons. We commenced production at this facility in October 2007. The production of biodiesel is achieved through the effective performance of all equipment necessary for production. Initial production in 2008 required adjustments to equipment and a full debugging process. Our achievable utilization rate, after taking into account required periodic maintenance, is 90%. We have increased our biodiesel production capacity by 50,000 tons through construction of a new facility in Tongchuan City to supplement the demand for petro-diesel. We began construction on a new facility to increase capacity in the fourth quarter of 2009. Due to a catalyst bottleneck that occurred in 2012, this new facility is not currently operational. We are working with a national chemical institute to replace the catalyst and/or find another solution to commence operations. We have invested approximately $19 million in capital expenditures to accomplish this goal. In October 2010, we acquired Chongqing Tianrun Energy Development Co., Ltd., (“Chongqing Tianrun”) a 50,000-ton biodiesel plant. The Chongqing biodiesel facility uses first generation biodiesel production technology, similar to the production process used in our current 90,000-ton production plant. At full capacity, our Chongqing biodiesel facility can achieve gross margins of approximately 30%. .

Raw Material Supply

Shaanxi Province is one of the largest cultivators of Chinese prickly ash, an oil plant, in China. Together, the local farmers in Shaanxi Province have planted approximately 2,460,000 mu (equivalent to 405,000 acres) of Chinese prickly ash, and 6,800,000 mu (equivalent to 1,120,000 acres) of Chinese pistache. Even though we could satisfy all of our current feedstock demands solely with Chinese prickly ash, we diversify our feedstock supply with other oil plants, waste cooking oil and vegetable oil residue, because the costs of these raw materials are lower than Chinese prickly ash. There is also significant acreage of wild oil plants that grow throughout Shaanxi Province. However, because the feedstock available from the local associations currently satisfies our supply demands, we do not rely on any supplies of wild oil plants for our production needs. We believe that the abundant supply of feedstock currently available in Shaanxi Province is sufficient for our current needs and will be sufficient for our expanded demands for raw material once we expand our biodiesel production facility or acquire a new facility.

| 7 |

We have established cooperation relationships with two pre-processing factories that are affiliated with local agricultural associations for oil extraction from non-edible oil seeds or oil plant seeds. The purchasing contracts obligate the pre-processing factories to first offer to sell the feedstock to us. If the supply of feedstock is greater than our demand, they can then sell any remaining feedstock to other companies. We have access to a range of biodiesel raw materials. Besides non-edible seed oil, we can also use waste cooking oil and vegetable oil residue as raw material for the first generation of biodiesel production.

In addition to the feedstock used in our existing first-generation facility, the new second-generation facility will be able to utilize a diverse supply of raw materials, such as crop straw (including wheat straw, corn straw, cotton straw and weed), agricultural biomass waste (including tree branches and tree leaves), as well as other organic waste. This feedstock flexibility affords us better input cost controls.

Sales and Marketing

We continue to leverage our distribution infrastructure to sell our biodiesel to existing customers and to acquire new customers. The main advantages of biodiesel over petro-diesel are pricing, efficiency, safety (due to a higher flash point) and the fact that biodiesel is environmentally friendly. Our targeted markets are power plants, marine transportation companies, seaport operations and other industrial customers which consume large volumes of diesel fuel.

Customers

We primarily target oil product trading companies in China (i.e., sales subsidiaries of SINOPEC and PetroChina) and end users (i.e., gas stations, electric power companies and shipping companies) as our customers. Approximately 20% of the biodiesel we produce is blended with petro-diesel and sold to next tier oil distributors and gas stations. The remaining 80% is sold to power plants and marine transportation companies. We do not believe that our sales are affected by seasonality.

Competition

Currently, we are the only non-state owned biodiesel producer with a distribution license in China. We may face significant competition from current and future companies that intend to compete in the biodiesel market. In the area of biodiesel fuel production, we are not aware of the existence of any significant competitors in Shaanxi Province. However, we face competition from companies in other geographic areas in China and foreign competitors that export their biodiesel to China.

Operation of Retail Gas Stations

We sell all grades of gasoline and diesel at our seven retail gas stations. Our customers include automobile, bus and truck drivers. Our competitors are other privately owned and state-owned gas stations. Our advantages are that (i) as a well-established finished oil distributor, we have a stable and sufficient oil supply to support our retail gas station operations at a higher margin; (ii) we sell blended diesel with a blending ratio of 15.0% of biodiesel and 85.0% of petro-diesel to end customers at the same price as petro-diesel, which provides us with additional profitability from our retail gas station operations, and (iii) we maintain competitive pricing to attract customers. We will seek to continue to expand our retail gas station portfolio. Recently Exxon/Mobil and Shell Corporation have partnered with state-owned petroleum companies and one of our petroleum suppliers to aggressively acquire and expand retail gas station market. As a result of intense completion in acquiring private owned gas stations, the cost of acquiring or leasing gas station has significantly escalated. Advanced lease payment for the entire lease term is often required and necessary to secure a long term lease of a gas station.

Other Business Information

Research and Development

We own four utility model patents and one invention patent, we also have submitted nine other patent applications, of which three applications have passed preliminary examination and six applications have been accepted for review. We incurred insignificant amount in research and development expenditures for 2010 and 2009. We continue working with well-known universities and colleges and research centers to enhance current biodiesel production processes and develop next generation of biodiesel production technologies.

| 8 |

Intellectual Property

Our core technologies consist of: (i) one invention patents related to biodiesel production, and (ii) four utility model patents related to biodiesel production.

Between 2006 and 2014, we filed the following 14 patent applications listed below with the SIPO, all of which are related to our biodiesel production. The SIPO has approved the first four applications for utility model patents and the fifth invention patent, allowed the next three invention patent applications to pass preliminary examination and accepted the other patent applications for review.

| · | Application No. 200820221671.0 for a new gas-liquid distributor of material filling tower(Approved) |

| · | Application No. 200620137855.X for a new reaction vessel for preparing biodiesel and composite diesel(Approved) |

| · | Application No. 200620137854.5 for a new reaction equipment for preparing biodiesel(Approved) |

| · | Application No. 200820028705.4 for an anti-corrosion device for biodiesel esterification reaction(Approved) |

| · | Application No. 201110044616.5 for a biodiesel processing Method(Approved) |

| · | Application No. 201010294327.6 for a highly efficient synthesizing method and facility for high quality diesel (Preliminary Approved) |

| · | Application No. 201010294330.8 for a water gas transformation method and facility of high quality and efficiency (Preliminary Approved) |

| · | Application No. 201310128973.9 for a facility and method that employ high temperature alternating current arc to produce biomass synthesis gas (Preliminary Approved) |

| · | Application No. 200610152506.X for a new composite catalyst for preparing biodiesel(Accepted) |

| · | Application No. 200610152507.4 for a new technology for processing biodiesel with catalyst or splitting decomposition in liquid or gas face(Accepted) |

| · | Application No. 200610152508.9 for a biodiesel processing technique(Accepted) |

| · | Application No. 20081001784.8 for a new technique for producing biodiesel and its byproducts with molecular distillation(Accepted) |

| · | Application No. 200810017853.0 for a new technique for disposing biodiesel esterification reaction equipment with inert metal lead(Accepted) |

| · | Application No. 200810017849.4 for a new method for preparing biodiesel with supercritical technology(Accepted) |

We have patent protection for each of our utility model patents for a period of ten years from the date of filing. If our invention patents are approved, they will be valid for a period of 20 years from the date of filing. Upon expiration, the renewal process requires us to re-apply for patent protection.

Insurance

We maintain property insurance for some of our premises and accidental liability insurance. We do not have any business liability, interruption or litigation insurance coverage for our operations in China. Although it is available, insurance companies in China offer limited business insurance products. We have determined that the risks of interruption, cost of such insurance and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to purchase such insurance. Therefore, we are subject to business and product liability exposure. Business or product liability claims or potential regulatory actions could materially and adversely affect our business and financial condition. We maintain director and officer liability insurance for our directors and executive officers.

| 9 |

Environmental Matters

We are subject to numerous foreign, environmental protection and health and safety laws governing, among other things, the generation, storage, use and transportation of hazardous materials; emissions or discharges of substances into the environment; and the health and safety of our employees. The cost of compliance with environmental laws, however, has not had, and based on current information and applicable laws, is not expected to have, a material adverse effect upon our capital expenditures, earnings or competitive position. All of our operations are in the Peoples Republic of China (“PRC”). We believe that we are in compliance with present environmental protection requirements in PRC in all material respects. Our production processes generate noise, waste water, gaseous wastes and other industrial wastes. We have installed various types of anti-pollution equipment in our facilities to reduce, treat, and where feasible, recycle the wastes generated in our production process. Our operations are subject to regulation and periodic monitoring by local environmental protection authorities in the PRC.

Employees

As of December 31, 2010, we had 402 full-time employees. Among them, 83 of our employees worked at our Xi’an headquarters; 82 at our biodiesel production facility in Chongqing City ;71 at our biodiesel production facility in Tongchuan City; 41 at our oil storage depots and 125 at our retail gas stations. We believe we have good relationships with our employees.

| 10 |

Industry and Market Overview

China Oil Markets

Industry Overview

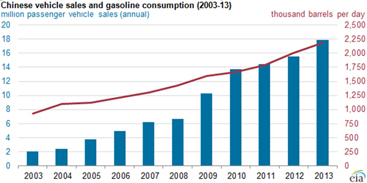

China is the world's second-largest consumer of oil and projected to move from second-largest net importer of oil to the largest in 2014.

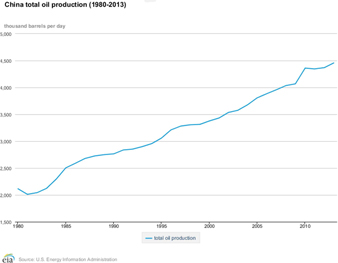

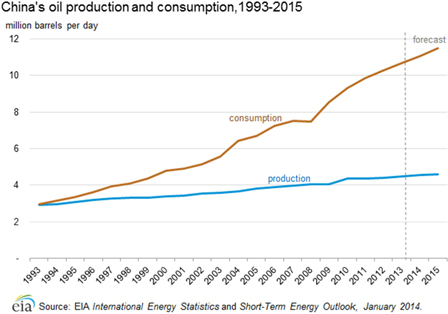

According to the Oil & Gas Journal (OGJ), as of January 2014, China holds 24.4 billion barrels of proven oil reserves, up over 0.7 billion barrels from the 2013 level and the highest in the Asia-Pacific region. China's total oil and liquids production, the fourth largest in the world, has risen by about 54% over the past two decades and serves only its domestic market. However, the production growth has not kept pace with demand growth during this period. In 2013, China produced an estimated 4.5 million barrels per day (bbl/d) of total oil liquids, of which 93% was crude oil. EIA forecasts China's oil production to rise to about 4.6 million bbl/d by the end of 2014. Over the longer term, EIA projects a steady growth for China's oil and liquids production, reaching 4.6 million bbl/d in 2020 and 5.6 million bbl/d by 2040. Most of the growth over the long term is from non-petroleum liquids such as gas-to-liquids, coal-to-liquids, kerogen, and biofuels, as crude oil production remains relatively flat.

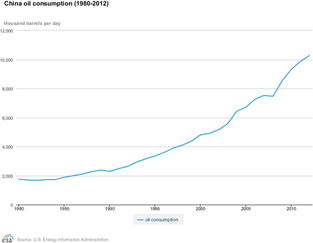

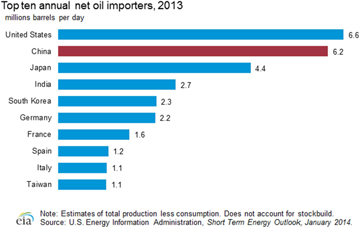

China's oil consumption growth has eased after a high of 14% in 2009, reflecting the effects of the most recent global financial and economic downturn. Despite the slower growth, the country still made up nearly a third of global oil demand growth in 2013, according to EIA estimates. China consumed an estimated 10.7 million bbl/d of oil in 2013, up 380 thousand bbl/d, or almost 4%, from 2012. In 2009, China became the second-largest net oil importer in the world behind the United States, and average net total oil imports reached 6.2 million bbl/d in 2013. Notably, for the fourth quarter of 2013, China actually became the largest global net importer of oil. EIA projects that China is likely to surpass the United States in net oil imports on an annual basis by 2014 as U.S. oil production and Chinese oil demand increase simultaneously. China's oil demand growth hinges on several factors, such as domestic economic growth and trade, power generation, transportation sector shifts, and refining capabilities. EIA forecasts that China's oil consumption will continue growing through 2014 at a moderate pace to approximately 11.1 million bbl/d, and its net oil imports will reach 6.6 million bbl/d compared to 5.5 million bbl/d for the United States.

| 11 |

As China's oil demand continues to outstrip production at home, oil imports have increased dramatically over the past decade, reaching record highs in 2013. To ensure adequate oil supply and mitigate geopolitical uncertainties, China has diversified its sources of crude oil imports in recent years. China imported 5.4 million bbl/d of crude oil on average in 2012, rising 7% from 5.1 million bbl/d in 2011, according to China's customs data and FGE. In 2013, import growth slowed to about 4.4% from 2012 levels, and crude oil imports averaged 5.6 million bbl/d. Crude imports now outweigh domestic supply, and they made up over half of total oil consumption in 2013. The government's current Five-Year plan targets oil imports reaching no more than 61% of its demand by the end of 2015. EIA expects China to import over 66% of its total oil by 2020 and 72% by 2040 as demand is expected to grow faster than domestic crude supply.

| 12 |

China's national oil companies dominate the oil and gas upstream and downstream sectors, although the government has granted international oil companies more access to technically challenging onshore and deep water offshore fields. China revised its oil price reform legislation in 2013 to further reflect international oil prices in the country's domestic demand.

The China National Petroleum Corporation (CNPC) and the China Petroleum and Chemical Corporation (Sinopec),these two conglomerates operate a range of local subsidiaries, and together control China's upstream and downstream oil markets. CNPC is the leading upstream player in China and, along with its publicly-listed arm, PetroChina, accounts for an estimated 53% and 75% of China's total oil and natural gas output, respectively, according to FACTS Global Energy (FGE). CNPC's current strategy is to integrate its sectors and capture more downstream market share. Sinopec, on the other hand, has traditionally focused on downstream activities, such as refining and distribution, with these sectors making up over 76% of the company's revenues in recent years. The company seeks to acquire more upstream assets to capture more value from oil and gas production and diversify its revenue sources.

Additional state-owned oil firms have emerged over the past several years. The China National Offshore Oil Corporation (CNOOC), which is responsible for offshore oil exploration and production, has seen its role expand as a result of growing attention to offshore zones. Also, the company has proven to be a growing competitor to CNPC and Sinopec by not only increasing its exploration and production (E&P) expenditures in the South China Sea, but also extending its reach into the downstream sector, particularly in the southern Guangdong Province.

China's largest oil fields

Shaanxi Province, where our company is located, is in proximity to the Changqing oilfield, one of China’s largest oil and gas reserves, and to the southwestern region of China, where there is a significant shortage of finished oil products. The annual capacity of Changqing oilfield is about 22.6 million tons. Shaanxi Yanchang Group has built refineries for an aggregate annual capacity of approximately 14.0 million.

New Pricing Regime to Counter Refined Oil Shortage

For the past nine years, China’s refined oil market has been operating as a managed market-based system. China has kept retail prices of finished oil products fixed to protect consumers against rising costs while most Western countries have allowed prices to be set by market supply and demand. The fixed-price system often leads to fuel shortages as the profits of domestic oil refineries are squeezed when the cost of crude oil rises but the selling prices of refined oil products are fixed. Effective as of January 1, 2009, the NDRC implemented a new pricing regime for refined oil products, aimed to link domestic oil prices more closely to changes in the global crude oil prices in a controlled manner. Under this pricing regime, the domestic selling price of refined oil products are determined on the basis of the corresponding international crude oil prices and by taking into consideration the average domestic processing costs, taxes, selling expenses and an appropriate profit margin. There were eight pricing adjustments in 2009 and four pricing adjustments in 2010. NDRC implemented a new pricing regime to better reflect fluctuations in global oil prices effective as of March 26, 2013, the new system will shorten the current 22-day adjustment period to 10 days and remove the 4 percent limit, ushering in a more market-based mechanism that could better reflect production costs and energy shortages.

| 13 |

China's largest oil fields are mature, and production has peaked, leading companies to invest in techniques to sustain oil flows at the mature fields, while also focusing on developing largely untapped reserves in the western interior provinces and offshore fields.

After bolstering domestic oil output in 2010, China has experienced more moderate oil production growth since then. China boosted its domestic oil output by over 7% in 2010, after incremental growth in the previous two decades. Oil production in 2013 reached nearly 4.5 million bbl/d, about 50% higher than the level two decades ago. Approximately 81% of Chinese current crude oil production capacity is located onshore, while 19% of crude oil production is from shallow offshore reserves. New offshore production, enhanced oil recovery (EOR) of older onshore fields, and small discoveries in existing basins are the main contributors to incremental production increases. China's NOCs are investing a great deal in EOR techniques such as water injection, polymer flooding, and steam flooding, among others, to offset oil production declines from these mature, onshore fields.

China’s Retail Gas Stations

With China’s rapid economic development, continuous improvement in transportation infrastructure and rapid increase in motor vehicle ownership, the number of gas stations in China has been increasing.

As China has gradually opened the retail market for finished oil and for wholesale crude oil since January 2005, the rapid development of private oil companies, foreign-funded enterprises, and second-tier stated-owned companies have formed a balance among state-owned companies, private companies, and foreign companies, which are the three strongest powers in the market.

As of the end of 2012, there were 96,313 gas stations in China, an increase of 875 or 0.9% over the previous year. Of those, 51,854 or 53.8% are state owned, 42,425 or 44.1% are privately owned, and 2,034 or 2.1% are foreign capital funded. Of the total, 9,840 or 10.2% were owned or franchised by PetroChina and 30,836 or 32.0% were owned or franchised by Sinopec.

As for the location of the 96,313 gas stations, 3.0% are located on highways, 32.6% are on the national and provincial roads, 26.6% are on county or village roads, 25.5% are in cities, 11.0% are in rural areas, and 1.2% are in water or other areas.

Source: Oil circulation industry analysis report for 2012

To further boost the industry consolidation for competitive resources, state-owned companies, such as Sinopec and PetroChina, accelerated their acquisition of gas stations. At the end of 2011, Sinopec had 30,121 gas stations, with owned and directly operated gas stations increasing by 10,000 since the year 2000. PetroChina had nearly 20,000 gas stations in 2011. The market for private gas stations may keep shrinking in future, driving the private station owners to focus on rural areas and county or village roads.

China’s Biodiesel Market

Biodiesel

Biodiesel is a cleaner-burning and renewable fuel produced from animal fats, vegetable oil, and waste cooking oil. The chemical properties of biodiesel are very similar to those of petro-diesel, and biodiesel has the potential for replacing petro-diesel in many applications. Biodiesel is made through a chemical process called transesterification, which separates the glycerin from the fat or vegetable oil. The process generates two products - methyl esters (the chemical name for biodiesel) and glycerin (a byproduct with value for use in soaps and other products).

| 14 |

Biodiesel contains no petroleum, but it can be blended at any ratio with petro-diesel to create a biodiesel blend. It can be used in compression-ignition (diesel) engines with little or no modification. Biodiesel provides a number of benefits compared to diesel, including:

| · | No sulfur dioxide emission, a major component of acid rain, and emits less carbon dioxide than traditional diesel; |

| · | Reduction of smoke particulates; |

| · | Biodegradable and breaks down as fast as sugar; |

| · | Better lubrication which reduces engine wear; |

| · | Safer to use, handle and store due to its high flash point; and |

| · | Produced from renewable energy sources. |

Favorable Market Dynamics Support Long-Term Growth

In response to the rise in global oil prices, global warming and other environmental awareness issues, the PRC government has begun to encourage renewable energy consumption and has implemented various policies to support the production of biodiesel. The PRC government plans to increase its consumption of biofuel, of which two million tons are estimated to be biodiesel, and its proportion of renewable energy consumption to approximately 15.0% of China’s total energy consumption in 2020 from approximately 7.5% in 2005. In 2010, the China government also targeted reducing carbon dioxide emission per unit of GDP by 40% - 45% by 2020.

Biodiesel is classified as an “encouraged industry” by the NDRC. Businesses engaged in biodiesel production are entitled to receive certain benefits and incentives extended by the government, such as grants and interest-free loans.

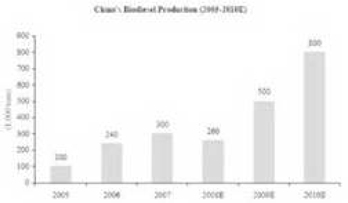

However, China’s biodiesel industry is still underdeveloped, which we believe provides opportunities for us in this market. The following table sets forth the production volume of biodiesel in China from 2005 through 2007 and forecasts for 2008 through 2010.

Source: China Biodiesel Industry Investment Value Report 2008, China Venture

In February 2005, China enacted the Renewable Energy Law , which aims to promote the development and utilization of renewable energy, improve the energy structure, diversify energy supplies, safeguard energy security, protect the environment and realize sustainable development of the economy and society. This legislation states that fuel retail businesses must begin to include “biological liquid fuel” in their sales or they will be subject to fines as China is seeking to reduce its dependence on fossil fuels in its diesel transportation vehicles. In the twelfth five year economic plan, Chinese government also promotes renewable energy industries including bio-fuel industry to reduce dependency of import of crude oil from abroad and improve environmental preservation. As a result of promotion of alternative energy, the China government encourages a B-5 standard blending 5% of biodiesel with 98% of petro-diesel for transportation fuel in February 2011.

| 15 |

The government is preparing to push forward a pilot project in 150 to 200 cities during the Twelfth Five-year period to make better use or proper disposal of the kitchen waste. Experts called for policies to control the disposal of waste cooking oil and to supply the waste oil to biodiesel companies.

In August 2011, the government announced the first group of cities for the pilot project to make better use or proper disposal of the kitchen waste. Included were 33 cities and districts. The plans submitted by the pilot cities aim to: (a) create systems to optimize the process to collect, transport, dispose, and reuse kitchen waste; (b) adopt and apply solutions to dispose of the waste oils and fats, solid waste, and liquids together as a whole; and (c) explore fundamental solutions to achieve the proper disposal and reuse of the kitchen waste. On October 31, 2012, the list of the second group of cities, including 16 cities, for the pilot project was announced to make better use or proper disposal of kitchen waste.

With the government’s support and the market as guidance, the biodiesel industry in China is still likely to realize another rapid development during the Twelfth Five-year period (2011-2015).

Governmental Regulation

Finished Oil and Heavy Oil Distribution

We have been engaging in the wholesale distribution of finished and heavy oil business in the PRC since 2000. Prior to 2006, significant gaps existed in the laws and regulations on finished oil markets, and the relevant rules for this industry were, to some extent, inconsistent and subject to the discretion of the relevant government authorities.

In 2006, greater specificity was added to the rules for commercial activities in the finished oil market with the enactment of the Measures on the Administration of the Finished Oil Market (promulgated on December 4, 2006 by the Ministry of Commerce of the people’s Republic of China (MOFCOM) and effective as of January 1, 2007), or the Measures. This regulation provides comprehensive details on the finished oil wholesale and resale application procedures, qualification requirements, and rules for annual inspections. Enterprises (foreign or domestic-funded) meeting certain requirements can submit applications to the MOFCOM for a certificate of approval to conduct gasoline and diesel (including biodiesel) wholesale, retail and storage businesses.

The first step required in applying to engage in the wholesale of finished oil is a preliminary examination by the provincial MOFCOM where the enterprise is located. Thereafter, the provincial MOFCOM will forward the application materials together with its opinions on the preliminary examination to the MOFCOM, which will then decide on whether to grant the Certificate of Approval for the Wholesale of Finished Oil.

An enterprise applying to engage in the finished oil wholesale business must, among other requirements, possess the following:

| (i) | long-term and stable supply of finished oil; |

| (ii) | a legal entity with a registered capital of no less than RMB 30 million; |

| (iii) | a finished oil depot, which shall have a capacity not smaller than 10,000 m3 , conforming to the local urban and rural planning requirements, and be approved by other relevant administrative departments; and |

| (iv) | facilities for unloading finished oil such as conduit pipes, special railway lines, and transportation vehicles with a capacity of 10,000 tons or more to transport refined oil on the highway or over water to ports. |

In practice, it has become increasingly difficult for enterprises (particularly foreign-funded enterprises) to meet the requirement (iii) above. As both the number of available oil depots and state land and resources are reaching full capacity, it is more of a challenge to obtain a finished oil depot with a capacity not smaller than 10,000 m3 .

| 16 |

The application procedure for the retail of finished oil is similar to that for wholesale except that the preliminary examination takes place at the administrative department for commerce at the municipal level, and the certificate of approval is issued at the provincial level.

An enterprise applying to engage in the finished oil retail business must, among other requirements, possess the following:

| (i) | long-term and stable channels to finished oil supply and a supply agreement with an enterprise that has been qualified to engage in the wholesale business of finished oil for a period of three years or more in line with its business scale; |

| (ii) | qualified professional and technical personnel to handle inspections, metrology, storage and fire safety and the safe production of finished oil; and |

| (iii) | gas stations designed and built to comply with the relevant national standards and approved by the relevant administrative department. |

Xi’an Baorun Industrial has the certificates of approval for both the wholesale and retail of finished oil, including for the retail of finished oil at each of its seven retail gas stations. As such, we do not have to rely on other companies to distribute the biodiesel fuel that we produce.

Enterprises possessing certificates of approval are subject to annual inspection by the relevant provincial MOFCOM which will review:

| (i) | the execution and performance of finished oil supply agreements; |

| (ii) | the operation results of the enterprise for the previous year; |

| (iii) | whether the enterprise and its supporting facilities are in compliance with the technical requirements under the Measures; and |

| (iv) | the current measures, among other measures, being taken by the enterprise regarding quality control, metrology, fire safety, security and environmental protection. |

If we pass the annual inspection, the certificates of approval we hold will continue to be valid. An enterprise failing an annual inspection will be ordered to rectify all deficiencies within a certain time limit by the MOFCOM and/or its provincial branches. If such deficiencies have not been rectified within the specified time limit, its certificates of approval shall be revoked by the original issuing authority.

Pricing for Finished Oil

The NDRC regulates domestic oil prices as part of its macro-management over the economy in order to control dramatic fluctuations in oil prices.

The Administrative Measures on Oil Prices ( trial implementation ) promulgated by the NDRC on May 7, 2009 stipulates that the NDRC will adjust domestic finished oil prices when the international market price for crude oil changes more than four percent over 22 consecutive working days. By contrast, crude oil prices are determined solely by enterprises engaging in this industry.

NDRC implemented a new pricing regime to better reflect fluctuations in global oil prices effective as of March 26, 2013, the new system will shorten the current 22-day adjustment period to 10 days and remove the 4 percent limit, ushering in a more market-based mechanism that could better reflect production costs and energy shortages. Domestic prices will remain unchanged if price changes in international oil markets are less than 50 RMB per metric ton, according to the NDRC.

| 17 |

The NDRC adjusts domestic finished oil prices by modifying the retail price cap for gasoline and diesel in all provinces, autonomous regions, and directly administered municipalities. Thereafter, the administrative authorities at the provincial level adjust the wholesale price caps by deducting RMB 30 per ton from the corresponding retail price caps. Where there are no specific contractual arrangements for a supplier’s delivery to a retailer, the wholesale price caps may be further deducted to take into account the retailer’s transportation cost among other expenses.

The Administrative Measures on Oil Prices stipulates that the domestic finished oil prices shall be calculated according to the normal profit rate for refiners when the crude oil price on the international market is lower than $80 per barrel. When the international crude oil market price exceeds $130 per barrel, the NDRC will adopt certain fiscal and tax policies to ensure the continuing production and supply of refined oil products. Further, gasoline and diesel prices will only be increased slightly (if at all) in consideration of manufacturers and consumers, as well as the stability of the national economy.

The exact formula for calculating finished oil prices domestically has not been published. However, the NDRC has stated that such formula is based on the weighted average of the international market prices, together with the average domestic processing costs, taxes, fees incurred in distribution channels, and suitable profits for refiners. Moreover, the NDRC adjusts the cost index seasonally in accordance with the actual situation with respect to prices.

Biodiesel

The Standing Committee of the National People’s Congress promulgated the Renewable Energy Law on February 28, 2005, which took effect as of January 1, 2006. The purpose of this law is to facilitate the development and utilization of renewable energy, including biological liquid fuel and energy crops. Under Article 16, oil-selling enterprises shall include biological liquid fuel conforming to the national standards into their fuel-selling systems, in accordance with the regulations of the energy authorities at the national or provincial level. An oil-selling enterprise that fails to include biological liquid fuel into their fuel-selling systems in accordance with the national standards will be liable for any resulting losses to a biological liquid fuel production enterprise. Further, the energy authorities at the national or provincial level shall order such oil-selling enterprise to rectify the non-conformance within a stipulated period of time, and impose a fine less than the amount of the said resulting losses if the rectification is not made.

Environmental Protection

The relevant PRC governmental authorities set national and local environmental protection standards, as well as examine and issue approvals on environmental aspects of different stages of various projects. We are required to file an environmental impact statement, or in some cases, an environmental impact assessment outline, to obtain such approvals. The filing must demonstrate that the project in question conforms to applicable environmental standards. Generally speaking, environmental protection bureaus will issue approvals and permits for projects using modern pollution control measurement technology.

The PRC national and local environmental laws and regulations impose fees for the discharge of waste substances above prescribed levels, require the payment of fines for serious violations and provide that the PRC national and local governments may, at their own discretion, close or suspend any facility which fails to comply with orders requiring it to cease or improve operations causing environmental damage.

In accordance with the requirements of the environmental protection laws of the PRC, we have installed the necessary environmental protection equipment, adopted advanced environmental protection technologies, established responsibility systems for environmental protection and reported to and registered with the relevant local environmental protection department.

In addition, to the best of our knowledge, we have complied with the necessary environmental procedures with respect to the construction of our biodiesel factory. The governmental authorities reviewed the environmental impact report prepared on our behalf by a professional institution that we retained prior to the commencement of construction. In January 2008, after the completion of construction, we obtained environmental approvals from the governmental authorities.

| 18 |

Dangerous Chemicals

PRC laws and regulations on dangerous chemicals require that a Safe Production Permit, or the Permit, be obtained for all facilities used to manufacture dangerous chemicals. We obtained the Safe Production Permit in April 2007, which is valid for a period of three years. It can thereafter be renewed for an additional three years, provided that the facility has not had any fatalities from accidents and has passed periodic inspections by the local administrative authorities for work safety during the term of the Permit.

Foreign-invested Enterprises Engaging in Oil-related Businesses

Under the Catalogue of Industries for Guiding Foreign Investment , jointly promulgated by the MOFCOM and the NDRC on October 31, 2007 and effective as of December 1, 2007, each of the wholesale of oil products, the construction and operation of petrol stations and the production of liquid biofuels ( i.e. , fuel ethanol, biodiesel) falls within the restricted category for foreign investment. Foreign investors can only engage in commercial activities involving liquid biofuels or retail of finished oil (where the foreign investor possesses 30 or more gas stations or where it sells different brands of oil through different distributors) through a joint venture with a Chinese partner, and the Chinese partner must hold a controlling interest in the joint venture. As a result of these restrictions, we conduct our business in the PRC via a domestic entity, Xi’an Baorun Industrial, established by three PRC citizens. Please refer to “Our History and Corporate Structure - Corporate Structure - Contractual Agreements with Xi’an Baorun Industrial” for more information regarding our control relationship with Xi’an Baorun Industrial.

| 19 |

SAFE Regulations Pertaining to Overseas-Listed Companies

Circular 75

The SAFE issued the Circular on Issues Relevant to Foreign Exchange Control with Respect to the Round-trip Investment of Funds Raised by Domestic Residents Through Offshore Special Purpose Vehicles , or Circular 75, on October 21, 2005. Circular 75 requires PRC residents and citizens to register with their local SAFE branches before establishing or acquiring the control of any company outside of China by using domestic assets or equities for the purpose of equity financing. PRC residents and citizens who are stockholders of offshore special purpose companies established before November 1, 2005 were required to conduct overseas investment registration with the local SAFE branches before March 31, 2006. Further, PRC residents and citizens must register all major changes relating to capitalization (including overseas equity or convertible bonds financing) within 30 days upon the occurrence of such changes.

On May 29, 2007, the SAFE issued the Operating Procedures for the Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Corporate Financing and Roundtrip Investment Through Offshore Special Purpose Vehicles . This regulation clarifies some outstanding issues with respect to Circular 75, and adds various implementing rules. Specifically, it provides for seven schedules to be established by the SAFE in order to track registration requirements for offshore fundraising and roundtrip investments.

Failure to comply with the registration procedures set forth in Circular 75 and any other rules and regulations may result in restrictions on the relevant PRC subsidiary, including the payment of dividends and other distributions to its offshore parent or affiliate and the capital inflow from the offshore entity. Non-compliance may also subject relevant PRC residents to penalties under PRC foreign exchange administration regulations, and may result in liability under PRC law for foreign exchange evasion.

Stock Option Rules

On March 28, 2007, the SAFE promulgated the Application Procedures of Foreign Exchange Administration for Domestic Individuals Participating in an Overseas-Listed Company’s Employee Stock Holding or Stock Option Plan , or the Stock Option Rules. The Stock Option Rules stipulate that PRC individuals who have been granted stock options and other types of stock-based awards by an overseas listed company are required to obtain approval from their local SAFE branches through an agent of the overseas listed company (generally its PRC subsidiary or a financial institution).

The failure by any entities or PRC individuals to complete their SAFE registration pursuant to the requirement of the SAFE or its local branches or the Individual Foreign Exchange Rules may subject these entities or PRC individuals to fines and legal sanctions, and may also limit our ability to contribute additional capital into our PRC subsidiaries, limit our PRC subsidiaries’ ability to distribute dividends to their shareholders or otherwise materially adversely affect their business.

As a company listed on a stock exchange in the United States, we and our PRC directors, management personnel, employees, consultants and employees of our equity investee who have been granted share options and other awards under our equity incentive plan are subject to the Stock Option Rules.

| 20 |

Our History and Corporate Structure

The following diagram illustrates our corporate structure.

Company History

We were incorporated in the State of Delaware in July 1998 under the corporate name “A.M.S. Marketing, Inc.” and in October 2003, we changed our name to “International Imaging Systems, Inc.” Until January 2007, we were engaged in the business of marketing pre-owned, brand name photocopy machines and employee leasing. We then began to pursue an acquisition strategy to acquire an undervalued business that demonstrated room for growth.

We acquired Baorun China Group Limited, or Baorun Group, pursuant to a Share Exchange Agreement, dated October 23, 2007 with Baorun Group, Redsky Group and Princeton Capital Group LLP, or Princeton Capital Group, Castle Bison, Inc. and Stallion Ventures, LLC. Together, Redsky Group and Princeton Capital Group owned shares constituting 100% of the issued and outstanding ordinary shares of Baorun Group. Pursuant to the terms of the Share Exchange Agreement, Redsky Group and Princeton Capital Group transferred to us all of their shares in Baorun Group in exchange for the issuance of 22,454,545 shares of our common stock to Redsky Group and 1,500,000 shares of our common stock to Princeton Capital Group. As a result of this share exchange, Baorun Group became our wholly owned subsidiary, and Redsky Group and Princeton Capital Group acquired an aggregate of approximately 94.11% of our common stock.

On November 15, 2007, through a merger of a wholly owned subsidiary, China Bio Energy Holding Group Co., Ltd., our corporate name was changed from “International Imaging Systems, Inc.” to “China Bio Energy Holding Group Co., Ltd.” On September 17, 2009, we changed our name to “China Integrated Energy, Inc.”

During the year ended December 31, 2010, Xi’an Baorun acquired Chongqing Tianrun Energy Development Co., Ltd. (“Chongqing Tianrun”), XianyangJinzheng Oil Sales Co., Ltd. (“XianyangJinzheng”), Xinyuan Gas Station (“Xinyuan”) and ShenmuErlintuHongtu Oil Co., Ltd. (“Shenmu”) for a total cash consideration of approximately $16.5 million, $10.0 million, $4.5 million and $9.2 million, respectively. After these acquisitions, Chongqing Tianrun, XianyangJinzheng, Xinyuan and Shenmu became wholly-owned subsidiaries of Xi’an Baorun.

| 21 |

Corporate Structure

We operate our business through certain contractual agreements between Redsky Industrial and Xi’an Baorun Industrial. Redsky Industrial is our indirect wholly owned subsidiary that is a registered wholly foreign owned enterprise in the PRC. Xi’an Baorun Industrial is based in Xi’an, Shaanxi Province, and owned by three Chinese citizens, including our chairman, chief executive officer and president, Mr. Xincheng Gao, who owns a 70% equity interest in Xi’an Baorun Industrial.

Contractual Agreements with Xi’an Baorun Industrial