Attached files

| file | filename |

|---|---|

| EX-99.1 - EX 99.1 - Mexus Gold US | figure1santaelenareport.pdf |

| EX-32.1 - EX 32.1 - Mexus Gold US | ex321.htm |

| EX-99.1 - EX 99.1 - Mexus Gold US | figure1santaelenareport.htm |

| EX-31.1 - EX 31.1 - Mexus Gold US | ex311.htm |

U. S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

|

[X]

|

QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

|

For the quarterly period ended June 30, 2014

|

||

|

[ ]

|

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ___________ to _____________

MEXUS GOLD US

|

Nevada

|

000-52413

|

20-4092640

|

||

|

(State or other jurisdiction

|

(Commission File Number)

|

(IRS Employer

|

||

|

of Incorporation)

|

Identification Number)

|

|||

|

1805 N. Carson Street, #150

|

||||

|

Carson City, NV 89701

|

||||

|

(Address of principal executive offices)

|

||||

|

(916) 776 2166

|

||||

|

(Issuer’s Telephone Number)

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No ___

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule12b-2 of the Exchange Act.

|

Large accelerated filer [ ]

|

Accelerated filer [ ]

|

|

|

Non-accelerated filer [ ]

(Do not check if smaller reporting company)

|

Smaller reporting company [X]

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). No [X]

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS

Check whether the registrant filed all documents and reports required to be filed by Section 12, 13, or 15(d) of the Exchange Act of 1934 after the distribution of securities under a plan confirmed by a court.

|

Yes

|

[ ]

|

|

No

|

[ ]

|

APPLICABLE ONLY TO CORPORATE ISSUERS

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date: As of August 15, 2014, 256,472,578 shares of our common stock were issued and outstanding.

PART I

ITEM 1. FINANCIAL STATEMENTS

|

MEXUS GOLD US

|

|

CONSOLIDATED FINANCIAL STATEMENTS

|

|

June 30, 2014

|

|

(Unaudited)

|

|

MEXUS GOLD US AND SUBSIDIARIES

|

|

CONSOLIDATED BALANCE SHEETS

|

|

(Unaudited)

|

|

June 30, 2014

|

March 31, 2014

|

||||

|

ASSETS

|

|||||

|

CURRENT ASSETS

|

|||||

|

Cash

|

$ 911

|

$ -

|

|||

|

Prepaid and other assets

|

86,914

|

81,747

|

|||

|

Investment in marketable securities

|

108,996

|

150,114

|

|||

|

TOTAL CURRENT ASSETS

|

196,821

|

231,861

|

|||

|

FIXED ASSETS

|

|||||

|

Equipment, net of accumulated depreciation

|

1,461,095

|

1,567,165

|

|||

|

TOTAL FIXED ASSETS

|

1,461,095

|

1,567,165

|

|||

|

OTHER ASSETS

|

|||||

|

Deferred finance expense

|

419

|

3,503

|

|||

|

Equipment under construction

|

85,522

|

107,522

|

|||

|

Property costs

|

505,947

|

505,947

|

|||

|

TOTAL OTHER ASSETS

|

591,888

|

616,972

|

|||

|

TOTAL ASSETS

|

$ 2,249,804

|

$ 2,415,998

|

|||

|

LIABILITIES AND SHAREHOLDERS' EQUITY

|

|||||

|

CURRENT LIABILITIES

|

|||||

|

Bank overdraft

|

$ -

|

$ 4,053

|

|||

|

Accounts payable and accrued liabilities

|

77,695

|

75,006

|

|||

|

Accounts payable - related party

|

57,366

|

45,966

|

|||

|

Notes payable

|

390,502

|

351,502

|

|||

|

Note payable - related party

|

193,391

|

179,159

|

|||

|

Promissory notes

|

255,000

|

255,000

|

|||

|

Secured convertible promissory note (net of unamortized debt discount $9,560 and $88,644, respectively)

|

288,093

|

282,861

|

|||

|

Secured convertible promissory note derivative liability

|

306,141

|

954,410

|

|||

|

Warrant derivative liability

|

445,163

|

920,927

|

|||

|

TOTAL CURRENT LIABILITIES

|

2,013,351

|

3,068,884

|

|||

|

TOTAL LIABILITIES

|

2,013,351

|

3,068,884

|

|||

|

SHAREHOLDERS' EQUITY (DEFICIT)

|

|||||

|

Capital stock

|

|||||

|

Authorized

|

|||||

|

9,000,000 shares of preferred stock, $0.001 par value per share, nil issued and outstanding

|

-

|

-

|

|||

|

1,000,000 shares of Series A Convertible Preferred Stock, $0.001 par value per share

|

-

|

-

|

|||

|

500,000,000 shares of common stock, $0.001 par value per share

|

-

|

-

|

|||

|

Issued and outstanding

|

|||||

|

375,000 shares of Series A Convertible Preferred Stock (375,000 - March 31, 2014)

|

375

|

375

|

|||

|

254,902,064 shares of common stock (248,103,110 - March 31, 2014)

|

254,902

|

248,103

|

|||

|

Additional paid-in capital

|

14,575,582

|

14,104,432

|

|||

|

Share subscription payable

|

660,245

|

952,143

|

|||

|

Accumulated equity deficit

|

(15,267,497)

|

(16,011,903)

|

|||

|

Accumulated other comprehensive income

|

12,846

|

53,964

|

|||

|

TOTAL SHAREHOLDERS' EQUITY (DEFICIT)

|

236,453

|

(652,886)

|

|||

|

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY (DEFICIT)

|

$ 2,249,804

|

$ 2,415,998

|

|||

|

The accompanying notes are an integral part of these consolidated financial statements.

|

|||||

|

Three Months Ended June 30,

|

|||

|

2014

|

2013

|

||

|

REVENUES

|

|||

|

Revenues

|

$ 999

|

$ 109,317

|

|

|

Total revenues

|

999

|

109,317

|

|

|

Expenses

|

|||

|

General and administrative

|

129,280

|

189,786

|

|

|

Exploration costs

|

43,762

|

329,768

|

|

|

Stock-based expense - consulting services

|

57,000

|

37,500

|

|

|

Loss on sale of equipment

|

4,672

|

-

|

|

|

Loss on settlement of debt

|

48,050

|

-

|

|

|

Total operating expenses

|

282,764

|

557,054

|

|

|

OTHER INCOME (EXPENSE)

|

|||

|

Interest expense

|

(91,699)

|

(161,774)

|

|

|

Foreign exchange loss

|

(6,162)

|

(8,591)

|

|

|

Gain (loss) on derivative liabilities

|

1,124,033

|

(4,683)

|

|

|

1,026,172

|

(175,048)

|

||

|

NET INCOME (LOSS) FROM CONTINUING OPERATIONS

|

744,407

|

(622,785)

|

|

|

NET LOSS FROM DISCONTINUED OPERATIONS

|

-

|

(519,212)

|

|

|

NET INCOME (LOSS)

|

$ 744,407

|

$ (1,141,997)

|

|

|

OTHER COMPREHENSIVE LOSS

|

|||

|

Unrealized loss on marketable securities

|

(41,118)

|

-

|

|

|

(41,118)

|

-

|

||

|

COMPREHENSIVE INCOME (LOSS)

|

$ 703,289

|

$ (1,141,997)

|

|

|

BASIC LOSS PER SHARE FROM CONTINUING OPERATIONS

|

$ 0.003

|

$ (0.003)

|

|

|

BASIC LOSS PER SHARE FROM DISCONTINUED OPERATIONS

|

$ -

|

$ (0.002)

|

|

|

BASIC LOSS PER COMMON SHARE

|

$ 0.003

|

$ (0.005)

|

|

|

`

|

|||

|

WEIGHTED AVERAGE NUMBER OF COMMON SHARES

|

|||

|

OUTSTANDING- BASIC

|

251,862,541

|

213,659,127

|

|

|

The accompanying notes are an integral part of these consolidated financial statements.

|

|||

|

MEXUS GOLD US AND SUBSIDIARIES

|

|

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

|

(Unaudited)

|

|

For the Three Months Ended June 30,

|

||

|

2014

|

2013

|

|

|

CASH FLOWS FROM OPERATING ACTIVITIES

|

||

|

Net income (loss)

|

$ 744,407

|

$ (1,141,997)

|

|

Loss from discontinued operations

|

-

|

519,212

|

|

Net income (loss) from continuing operations

|

744,407

|

(622,785)

|

|

Adjustments to reconcile net income (loss)

|

||

|

to net cash used in operating activities:

|

||

|

Depreciation and amortization

|

82,398

|

85,684

|

|

Loss on sale of equipment

|

4,672

|

-

|

|

Loss on settlement of debt

|

48,050

|

-

|

|

Stock-based compensation - services

|

57,000

|

37,500

|

|

Interest expense

|

91,699

|

161,774

|

|

Impairment of equipment included in exploration costs

|

-

|

7,500

|

|

Allowance for amount due from First Pursuit Silver de Mexico S. de R.L. de C.V.

|

-

|

|

|

Bad debt expense - related party

|

-

|

247,509

|

|

Gain (loss) on derivatives

|

(1,124,033)

|

4,683

|

|

Changes in operating assets and liabilities:

|

||

|

Prepaid and other assets

|

(5,167)

|

(1,573)

|

|

Accounts payable and accrued liabilities, including related parties

|

11,706

|

19,154

|

|

NET CASH USED IN OPERTATING ACTIVITIES

|

(89,268)

|

(60,554)

|

|

CASH FLOWS FROM INVESTING ACTIVITIES

|

||

|

Purchase of equipment

|

-

|

(1,200)

|

|

Purchase of equipment under construction

|

-

|

(45,903)

|

|

Issuance of notes receivable

|

-

|

(247,509)

|

|

Proceeds from sale of equipment

|

41,000

|

-

|

|

NET CASH PROVIDED BY (USED IN) INVESTING ACTIVITES

|

41,000

|

(294,612)

|

|

CASH FLOWS FROM FINANCING ACTIVITIES

|

||

|

Bank overdraft

|

(4,053)

|

-

|

|

Proceeds from issuance of notes payable

|

39,000

|

285,894

|

|

Payments on notes payable

|

-

|

(50,000)

|

|

Proceeds from issuance of convertible promissory notes

|

-

|

250,000

|

|

Advances from related party

|

14,232

|

42,350

|

|

Payment on advances from related party

|

-

|

(12,921)

|

|

Proceeds from issuance of common stock

|

-

|

338,900

|

|

NET CASH PROVIDED BY FINANCING ACTIVITIES

|

49,179

|

854,223

|

|

NET CASH USED IN OPERATING ACTIVITIES- DISCONTINUED OPERATIONS

|

-

|

(519,212)

|

|

INCREASE (DECREASE) IN CASH

|

911

|

(20,155)

|

|

CASH, BEGINNING OF PERIOD

|

-

|

104,701

|

|

LESS: CASH DISCONTINUED OPERATIONS END OF PERIOD

|

-

|

(1,388)

|

|

CASH, CONTINUING OPERATIONS AT THE END OF PERIOD

|

$ 911

|

$ 83,158

|

|

Supplemental disclosure of cash flow information:

|

||

|

Interest paid

|

$ -

|

$ 15,000

|

|

Taxes paid

|

$ -

|

$ -

|

|

Supplemental disclosure of non-cash investing and financing activities:

|

||

|

Shares issued for notes payable

|

$ 81,000

|

$ -

|

|

Shares issued and unissued for equipment purchase

|

$ -

|

$ 6,500

|

|

The accompanying notes are an integral part of these consolidated financial statements.

|

||

MEXUS GOLD US AND SUBSIDIARIES

Notes to Consolidated Financial Statements

June 30, 2014

(Unaudited)

|

1.

|

ORGANIZATION AND BUSINESS OF COMPANY

|

Mexus Gold US (the “Company”) was originally incorporated under the laws of the State of Colorado on June 22, 1990, as U.S.A. Connection, Inc. On October 28, 2005, the Company changed its’ name to Action Fashions, Ltd. On September 18, 2009, the Company changed its’ domicile to Nevada and changed its’ name to Mexus Gold US to better reflect the Company’s new planned principle business operations. The Company has a fiscal year end of March 31.

The Company is a mining company engaged in the evaluation, acquisition, exploration and advancement of gold, silver and copper projects in the State of Sonora, Mexico and the Western United States, as well as, the salvage of precious metals from identifiable sources.

|

2.

|

BASIS OF PREPARATION

|

Pursuant to the rules and regulations of the Securities and Exchange Commission for Form 10-Q, the consolidated financial statements, footnote disclosures and other information normally included in consolidated financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted. The consolidated financial statements contained in this report are unaudited but, in the opinion of management, reflect all adjustments, consisting of only normal recurring adjustments, necessary for a fair presentation of the consolidated financial statements. All significant inter-company accounts and transactions have been eliminated in consolidation. The results of operations for any interim period are not necessarily indicative of results for the full year. The consolidated balance sheet at March 31, 2014 has been derived from the audited consolidated financial statements at that date but does not include all of the information and footnotes required by accounting principles generally accepted in the United States of America for complete financial statements.

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Management reviews these estimates and assumptions on an ongoing basis using currently available information. Actual results could differ from those estimates.

Cash and Cash Equivalents

The Company considers highly liquid financial instruments purchased with a maturity of three months or less to be cash equivalents.

Per Share Data

Net loss per common share is computed by dividing net loss by the weighted average common shares outstanding during the period as defined by Financial Accounting Standards, ASC Topic 260, "Earnings per Share". Basic earnings per common share (“EPS”) calculations are determined by dividing net income by the weighted average number of shares of common stock outstanding during the year. Diluted earnings per common share calculations are determined by dividing net income by the weighted average number of common shares and dilutive common share equivalents outstanding. During periods when common stock equivalents, if any, are anti-dilutive they are not considered in the computation.

|

2.

|

BASIS OF PREPARATION (continued)

|

Fair Value of Financial Instruments

ASC Topic 820 defines fair value, establishes a framework for measuring fair value, and expands disclosures about fair value measurements.

Included in the ASC Topic 820 framework is a three level valuation inputs hierarchy with Level 1 being inputs and transactions that can be effectively fully observed by market participants spanning to Level 3 where estimates are unobservable by market participants outside of the Company and must be estimated using assumptions developed by the Company. The Company discloses the lowest level input significant to each category of asset or liability valued within the scope of ASC Topic 820 and the valuation method as exchange, income or use. The Company uses inputs which are as observable as possible and the methods most applicable to the specific situation of each company or valued item.

The Company's financial instruments consist of cash, accounts payable, accrued liabilities, advances, notes payable, and a loan payable. The carrying amount of these financial instruments approximate fair value due to either length of maturity or interest rates that approximate prevailing market rates unless otherwise disclosed in these financial statements.

Our investment in marketable securities is measured at fair value on a recurring basis using Level 1 inputs.

Our warrant derivative liability and secured convertible promissory note derivative liability is measured at fair value on a recurring basis using Level 3 inputs.

Interest rate risk is the risk that the value of a financial instrument might be adversely affected by a change in the interest rates. The notes payable, loans payable and secured convertible promissory notes have fixed interest rates therefore the Company is exposed to interest rate risk in that they could not benefit from a decrease in market interest rates. In seeking to minimize the risks from interest rate fluctuations, the Company manages exposure through its normal operating and financing activities.

Deferred Financing Costs

Deferred financing costs are amortized to interest expense based on the terms of the related debt instruments on a straight-line basis, which approximates the effective interest rate method.

Accounting for Derivative Instruments

Accounting standards require that an entity recognize all derivatives as either assets or liabilities in the statement of financial position and measure those instruments at fair value. A change in the market value of the financial instrument is recognized as a gain or loss in results of operations in the period of change.

Stock-based Compensation

The Company records stock based compensation in accordance with the guidance in ASC Topic 718 which requires the Company to recognize expenses related to the fair value of its employee stock option awards. This eliminates accounting for share-based compensation transactions using the intrinsic value and requires instead that such transactions be accounted for using a fair-value-based method. The Company recognizes the cost of all share-based awards on a graded vesting basis over the vesting period of the award.

ASC 505, "Compensation-Stock Compensation", establishes standards for the accounting for transactions in which an entity exchanges its equity instruments to non employees for goods or services. Under this transition method, stock compensation expense includes compensation expense for all stock-based compensation awards granted on or after January 1, 2006, based on the grant-date fair value estimated in accordance with the provisions of ASC 505.

|

2.

|

BASIS OF PREPARATION (continued)

|

Revenue Recognition

The Company recognizes revenues and the related costs when persuasive evidence of an arrangement exists, delivery and acceptance has occurred or service has been rendered, the price is fixed or determinable, and collection of the resulting receivable is reasonably assured.

Exploration and Development Costs

Exploration costs incurred in locating areas of potential mineralization or evaluating properties or working interests with specific areas of potential mineralization are expensed as incurred. Development costs of proven mining properties not yet producing are capitalized at cost and classified as capitalized exploration costs under property, plant and equipment. Property holding costs are charged to operations during the period if no significant exploration or development activities are being conducted on the related properties. Upon commencement of production, capitalized exploration and development costs would be amortized based on the estimated proven and probable reserves benefited. Properties determined to be impaired or that are abandoned are written-down to the estimated fair value. Carrying values do not necessarily reflect present or future values.

Mineral Property Rights

Costs of acquiring mining properties are capitalized upon acquisition. Mine development costs incurred either to develop new ore deposits, to expand the capacity of mines, or to develop mine areas substantially in advance of current production are also capitalized once proven and probable reserves exist and the property is a commercially mineable property. Costs incurred to maintain current production or to maintain assets on a standby basis are charged to operations. Costs of abandoned projects are charged to operations upon abandonment. The Company evaluates the carrying value of capitalized mining costs and related property and equipment costs, to determine if these costs are in excess of their recoverable amount whenever events or changes in circumstances indicate that their carrying amounts may not be recoverable. Evaluation of the carrying value of capitalized costs and any related property and equipment costs would be based upon expected future cash flows and/or estimated salvage value in accordance with Accounting Standards Codification (ASC) 360-10-35-15, Impairment or Disposal of Long-Lived Assets.

|

3.

|

GOING CONCERN

|

The accompanying financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying consolidated financial statements, the Company has a limited operating history and limited funds and has an accumulated deficit of $15,267,497 at June 30, 2014. These factors, among others, may indicate that the Company may not be able to continue as a going concern.

The Company is dependent upon outside financing to continue operations. The financial statements do not include any adjustments that might result from the outcome of this uncertainty. It is management’s plans to raise necessary funds through a private placement of its common stock to satisfy the capital requirements of the Company’s business plan. There is no assurance that the Company will be able to raise the necessary funds, or that if it is successful in raising the necessary funds, that the Company will successfully execute its business plan.

The financial statements do not include any adjustments relating to the recoverability and classification of assets and/or liabilities that might be necessary should the Company be unable to continue as a going concern. The continuation as a going concern is dependent upon the ability of the Company to meet our obligations on a timely basis, and, ultimately to attain profitability.

|

4.

|

RECENT ACCOUNTING PRONOUNCEMENTS AFFECTING THE COMPANY

|

In June 2014, the FASB issued ASU 2014-10, Development Stage Entities (Topic 915): Elimination of Certain Financial Reporting Requirements. ASU 2014-10 eliminates the distinction of a development stage entity and certain related disclosure requirements, including the elimination of inception-to-date information on the statements of operations, cash flows and stockholders' equity. The amendments in ASU 2014-10 will be effective prospectively for annual reporting periods beginning after December 15, 2014, and interim periods within those annual periods, however early adoption is permitted. The Company adopted ASU 2014-10 during the quarter ended June 30, 2014, thereby no longer presenting or disclosing any information required by Topic 915.

|

6.

|

ACCOUNTS PAYABLE – RELATED PARTIES

|

During the three months ended June 30, 2014 and 2013, the Company incurred rent expense to Paul D. Thompson, the sole director and officer of the Company, of 11,400 and 11,400, respectively. At June 30, 2014 and March 31, 2014, $57,366 and $45,966 for this obligation is outstanding, respectively.

|

7.

|

NOTES PAYABLE

|

During the three months ended June 30, 2014, the Company received various cash advances of $39,000 from three investors. These advances are unsecured, earn interest at 10% per annum and are due within 90 days of issue. One-half of the cash advances received by the Company may be converted into shares of common stock of the Company, at the option of the holder, at either $0.03 per share or $0.04 per share depending on the date the cash advance was received.

Defaulted Senior Notes

On February 16, 2010, the Company made an unsecured Promissory Note Agreement with William McCreary in the amount of $2,500 at eight percent interest and due on demand or no later than September 1, 2010. The Company has not made the scheduled payments and is in default on this note as of December 31, 2011. The default rate on the note is eight percent. At June 30, 2014 and March 31, 2014, the balances on this note totalled $2,500 and $2,500, respectively. At June 30, 2014 and March 31, 2014, accrued interest of $3,235 and $3,185 on this note have been included in accounts payable and accrued liabilities, respectively.

|

8.

|

NOTES PAYABLE – RELATED PARTY

|

Notes due to Taurus Gold, Inc. are unsecured, non-interest bearing and due on demand. These notes were accumulated through a series of cash advances to the Company. Taurus Gold, Inc. is controlled by Paul D. Thompson, the sole director and officer of the Company. As of June 30, 2014 and March 31, 2014, notes payable due to Taurus Gold Inc. totalled $193,391 and $179,159, respectively.

|

9.

|

PROMISSORY NOTES

|

On April 18, 2013, the Company issued Promissory Notes for $255,000 in cash. The Notes bear interest of 4% per annum and are due on June 30, 2014. The Notes are secured by all of Mexus Gold US shares of stock in Mexus Resources S.A. de C.V. and a personal guarantee of Paul D. Thompson. In addition, a fee of 2,550,000 shares of common stock of the Company valued at $501,075 ($0.1965 per share) was paid to the Note holders on April 18, 2013. These financing fees are capitalized in the consolidated balance sheet as deferred finance expense and are being amortized on a straight-line basis, which approximates the effective interest rate method, as interest expense over the life of the Promissory Notes. As of June 30, 2014, the Company has not made the scheduled payments and is in default on these promissory notes. The default rate on the notes is seven percent. Accrued interest of $5,320 is included in accounts payable and accrued liabilities.

|

10.

|

SECURED CONVERTIBLE PROMISSORY NOTES

|

On June 12, 2013, the Company entered into a Securities Purchase Agreement with Typenex Co-Investment, LLC (“Typenex”), for the sale of an 8% Secured Convertible Promissory Notes (“Notes”) in the principal amount of $557,500 consisting of an initial tranche of $307,500 comprising of $250,000 of cash at closing, Typenex legal expenses in the amount of $7,500 and a $50,000 original issue discount and an additional tranche $250,000 in cash. On June 12, 2013 the Company closed on the initial tranche and received $250,000 in cash. On August 8, 2013, the Company closed on the second tranche and received $125,000 in cash. The Company has not closed on the final tranche for $125,000 in cash. The Company has no obligation to pay Typenex any amounts on the unfunded portion of the Note. The Notes have a maturity date that is thirteen months after the issuance date. Typenex has been granted a security interest in the property of the Company. At the option of the holder, all principal, costs, charges and interest amounts outstanding under all of the Notes shall be exchanged for shares of the Company’s common stock at the Conversion Price of $0.23 per share. The Conversion Price is subject to an anti-dilution adjustment in the event the Company at any time, while the Notes are outstanding, issues equity securities including common stock or any security convertible or exchangeable for shares of common stock for no consideration or for consideration less than $0.23 a share.

In conjunction with the issuance of the Notes on June 12, 2013, the Company issued a variable number of warrants of the Company’s common stock equal to $278,750 divided by the Market Price. Market Price is defined as the higher of (i) the closing price of the common stock of the Company on June 12, 2013, and (ii) the VWAP of the common stock for the trading day that is two days prior to the exercise date. The Exercise Price of the warrants are $0.24 per share. The Exercise Price is subject to an anti-dilution adjustment in the event the Company at any time, while the Warrants are outstanding, issues equity securities including common stock or any security convertible or exchangeable for shares of common stock for no consideration or for consideration less than $0.24 a share.

The anti-dilution protection for the Note and Warrants excludes (a) the Company’s issuance of securities in connection with strategic license agreements and other partnering arrangements so long as any such issuances are not for the purpose of raising capital and in which holders of such securities or debt are not at any time granted registration rights, and (b) the Company’s issuance of Common Stock or the issuance or grant of options to purchase Common Stock to employees, directors, officers and consultants, authorized by the Company’s board of directors in place on June 12, 2013. After three months after the issuance date, monthly installments are due on the Note payable at the option of the Company (i) in cash (ii) in shares of common stock of the Company discounted depending on the Company’s share price at either 30% or 35%, or (iii) in any combination of cash or shares.

On June 12, 2013, the Company recorded a discount on the Note equal to the fair value of the warrant derivative liability and convertible promissory note derivative liability. This discount is amortized using the effective interest rate method over the term of the Note.

|

Three Months Ended June 30,

|

||

|

2014

|

2013

|

|

|

Cash advanced on closing of the initial tranche and second tranche

|

$ 375,000

|

$ -

|

|

Discounts on Note

|

||

|

Fair value of warrant derivative liability

|

(219,372)

|

-

|

|

Fair value of convertible promissory note liability

|

(75,218)

|

-

|

|

Loss on derivative liabilities

|

14,734

|

-

|

|

Conversion of principal and interest into shares of common stock

|

(169,444)

|

-

|

|

Amortization of discount on Note

|

362,393

|

-

|

|

$ 288,093

|

$ -

|

|

The Company did not pay the outstanding principal and interest due on July 12, 2014, the maturity date of the Notes, and the Notes went into default. See Note 15 – Subsequent Events.

|

11.

|

WARRANT DERIVATIVE LIABILITY

|

The Warrants are subject to anti-dilution adjustments that allow for the reduction in the Exercise Price in the event the Company subsequently issues equity securities including common stock or any security convertible or exchangeable for shares of common stock for no consideration or for consideration less than $0.24 a share. The Company accounted for the warrants in accordance with ASC Topic 815. Accordingly, the Warrants are not considered to be solely indexed to the Company’s own stock and, as such, recorded as a liability.

The Company’s warrant derivative liability has been measured at fair value at June 30, 2014 and March 31, 2014 using a binomial model. Since the Exercise Price contains an anti-dilution adjustment, the probability that the Exercise Price of the Notes would decrease as the share price decreased was incorporated into the valuation calculation. After June 12, 2013, the Company issued common stock for cash at a price of $0.0225 per share and the conversion price has been adjusted accordingly.

The inputs into the binomial model are as follows:

|

June 30, 2014

|

March 31, 2014

|

|

|

Closing share price

|

$0.045

|

$0.08

|

|

Conversion price

|

$0.0225

|

$0.0225

|

|

Risk free rate

|

1.25%

|

1.32%

|

|

Expected volatility

|

104%

|

142%

|

|

Dividend yield

|

0%

|

0%

|

|

Expected life

|

47 months

|

50 months

|

The fair value of the warrant derivative liability is $445,163 at June 30, 2014. The decrease in the fair value of the conversion option derivative liability of 475,764 is recorded as a gain in the consolidated statement of operations for the three months ended June 30, 2014.

|

12.

|

CONVERTIBLE PROMISSORY NOTE DERIVATIVE LIABILITY

|

The Notes are subject to anti-dilution adjustments that allow for the reduction in the Conversion Price in the event the Company subsequently issues equity securities including common stock or any security convertible or exchangeable for shares of common stock for no consideration or for consideration less than $0.23 a share. The Company accounted for the conversion option in accordance with ASC Topic 815. Accordingly, the Conversion Option is not considered to be solely indexed to the Company’s own stock and, as such, recorded as a liability.

The Company’s convertible promissory note derivative liability has been measured at fair value at June 12, 2013 and March 31, 2014 using a binomial model. Since the Conversion Price contains an anti-dilution adjustment, the probability that the Conversion Price of the Notes would decrease as the share price decreased was incorporated into the valuation calculation. After June 12, 2013, the Company issued common stock for cash at a price of $0.0225 per share and the conversion price has been adjusted accordingly.

The inputs into the binomial model are as follows:

|

June 30, 2014

|

March 31, 2014

|

|

|

Closing share price

|

$0.045

|

$0.08

|

|

Conversion price

|

$0.0225

|

$0.0225

|

|

Risk free rate

|

0.01%

|

0.10%

|

|

Expected volatility

|

24%

|

105%

|

|

Dividend yield

|

0%

|

0%

|

|

Expected life

|

1 month

|

4 month

|

The fair value of the conversion option derivative liability is $306,141 at June 30, 2014. The decrease in the fair value of the conversion option derivative liability of $648,269 is recorded as a gain in the unaudited consolidated condensed statement of operations for the year ended March 31, 2014.

|

13.

|

CONTINGENT LIABILITIES

|

An asset retirement obligation is a legal obligation associated with the disposal or retirement of a tangible long-lived asset that results from the acquisition, construction or development, or the normal operations of a long-lived asset, except for certain obligations of lessees. While the Company, as of June 30, 2014, does not have a legal obligation associated with the disposal of certain chemicals used in its leaching process, the Company estimates it will incur costs up to $50,000 to neutralize those chemicals at the close of the leaching pond.

|

14.

|

STOCKHOLDERS’ EQUITY

|

The stockholders’ equity of the Company comprises the following classes of capital stock as of June 30, 2014 and March 31, 2014:

Preferred Stock, $.001 par value per share; 9,000,000 shares authorized, 0 shares issued and outstanding at June 30, 2014 and March 31, 2014, respectively.

Series A Convertible Preferred Stock (‘Series A Preferred Stock”), $.001 par value share; 1,000,000 shares authorized: 375,000 shares issued and outstanding at June 30, 2014 and March 31, 2014.

Holders of Series A Preferred Stock may convert one share of Series A Preferred Stock into one share of Common Stock. Holders of Series A Preferred Stock have the number of votes determined by multiplying (a) the number of Series A Preferred Stock held by such holder, (b) the number of issued and outstanding Series A Preferred Stock and Common Stock on a fully diluted basis, and (c) 0.000006.

Common Stock, par value of $0.001 per share; 500,000,000 shares authorized: 254,902,064 and 248,103,110 shares issued and outstanding at June 30, 2014 and March 31, 2014, respectively. Holders of Common Stock have one vote per share of Common Stock held.

On April 1, 2014, the Company issued 342,063 shares of common stock valued at $29,075 ($0.085 per share) to Typenex Co-Investment, LLC for conversion of principal and interest of $12,500 and loss on settlement of debt of $16,576.

On April 16, 2014, the Company issued 1,053,553 shares of common stock valued at $63,213 ($0.060 per share) to Typenex Co-Investment, LLC for conversion of principal and interest of $38,500 and loss on settlement of debt of $24,713.

On April 18, 2014, the Company issued 3,056,805 shares of common stock to satisfy obligations under share subscription agreements for $157,492 in cash, $78,238 in services and $5,570 for settlement of accounts payable included in share subscriptions payable.

On May 1, 2014, the Company issued 1,427,500 shares of common stock to satisfy obligations under share subscription agreements for $92,245 in services and $15,354 in equipment included in share subscriptions payable.

On June 16, 2014, the Company issued 919,033 shares of common stock valued at $36,761 ($0.040 per share) to Typenex Co-Investment, LLC for conversion of principal and interest of $30,000 and loss on settlement of debt of $6,761.

Common Stock Payable

During the three months ended June 30, 2014, the Company issued subscriptions payable for 679,310 shares of common stock for services valued at $57,000 ($0.0839 per share).

|

|

15. SUBSEQUENT EVENTS

|

On July 3, 2014, the Company issued 1,103,370 shares of common stock to satisfy obligations under share subscription agreements for $39,503 in cash and $12,100 in services included in share subscriptions payable.

On July 31, 2014, the Company issued 467,133 shares of common stock valued at $19,153 ($0.041 per share) to Typenex Co-Investment, LLC for conversion of principal and interest of $12,000 and loss on settlement of debt of $7,153.

During the period from July 1, 2014 to August 15, 2014, the Company issued subscriptions payable for 1,016,666 shares of common stock for services valued at $30,500 ($0.030 per share).

Default of Secured Convertible Promissory Notes

On June 12, 2013, the Company entered into a Securities Purchase Agreement with Typenex Co-Investment, LLC (“Typenex”), for the sale of an 8% Secured Convertible Promissory Notes (“Notes”). See Note 10 – Secured Convertible Promissory Note. The Company did not pay the outstanding principal and interest due on July 12, 2014, the maturity date of the Notes, and the Notes went into default. On default, the Holders at their option may redeem the Notes in full or accelerate installments due on the Notes. The Holders may designate whether the installments are due in cash or discounted shares of common stock of the Company or a combination thereof. The default rate on the note is 22%.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION ANDRESULTS OF OPERATIONS

Cautionary Statement Concerning Forward-Looking Statements

The following discussion and analysis should be read in conjunction with our unaudited interim consolidated financial statements and related notes included in this report. This report contains “forward-looking statements.” The statements contained in this report that are not historic in nature, particularly those that utilize terminology such as “may,” “will,” “should,” “expects,” “anticipates,” “estimates,” “believes,” or “plans” or comparable terminology are forward-looking statements based on current expectations and assumptions.

Various risks and uncertainties could cause actual results to differ materially from those expressed in forward-looking statements. Factors that could cause actual results to differ from expectations include, but are not limited to, those set forth under the section “Risk Factors” set forth in our Form 10-K filed with the SEC on July 15, 2013.

The forward-looking events discussed in this report, the documents to which we refer you and other statements made from time to time by us or our representatives, may not occur, and actual events and results may differ materially and are subject to risks, uncertainties, and assumptions about us. For these statements, we claim the protection of the “bespeaks caution” doctrine. All forward-looking statements in this document are based on information currently available to us as of the date of this report, and we assume no obligation to update any forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties, and other factors that may cause the actual results to differ materially from any future results, performance, or achievements expressed or implied by such forward-looking statements.

The Company

Mexus Gold US is an exploration stage mining company engaged in the evaluation, acquisition, exploration and advancement of gold, silver and copper projects in the State of Sonora, Mexico and the Western United States. Mexus Gold US is dedicated to protect the environment, provide employment and education opportunities for the communities that it operates in.

Our President and CEO, Paul Thompson, brings over 40 years experience in mining and mining development to Mexus Gold US. Mr. Thompson is currently recruiting additional management personnel for its Mexico, Nevada, and submarine Cable Recovery operations to assist in growing the company.

Our executive offices are located at, 1805 N. Carson Street, #150, Carson City, Nevada 89701. Our telephone number is (916) 776 2166.

We were originally incorporated under the laws of the State of Colorado on June 22, 1990, as U.S.A. Connection, Inc. On October 28, 2009, we changed our domicile to Nevada and changed our name to Mexus Gold US to better reflect our new business operations. Our fiscal year end is March 31st.

Description of the Business of Mexus Gold US

Mexus Gold US is engaged in the evaluation, acquisition, exploration and advancement of gold exploration and development projects in the state of Nevada and Mexico, as well as, the salvage of precious metals from identifiable sources. Our main activities in the near future will be comprised of our mining operations in Mexico.

Our mining opportunities located in the state of Nevada and the state of Sonora, Mexico will provide us with projects to recover gold, silver, copper and other precious metals. The cable salvage opportunity involves principally the recovery of copper and lead from abandoned cable previously utilized for communications purposes. Each of these opportunities are discussed further herein.

In addition, our management will look for opportunities to improve the value of the gold projects that we own or may acquire knowledge of or may acquire control through exploration drilling, introduction of technological innovations or acquisition with the goal of developing those properties into operating mines. We expect that emphasis on gold project acquisition and development will continue in the future.

Business Strategy

Our business plan was developed with the overriding goal of maximizing shareholder value through the exploration and development of our mineral properties, utilizing the extensive mining-related background and capabilities of our management consultants and advisors. To achieve this goal, our business plan focuses on the following prospective areas:

Mexus Gold Mining S.A. de C.V.

Effective March 31, 2011, we acquired Mexus Gold S.A. de C.V. We began funding the operations in Mexico and have instituted as small placer processing operation to evaluate various areas of interest within the project lands.

Mexus-Trinidad Joint Venture

In March, 2014, we sold our 50% interest in the Joint Venture to Atzek Mineral S.A. de C.V.

Caborca Project

Our Caborca Project is comprised of earlier-stage exploration on lands purchased in State of Sonora, Mexico.

Cable Salvage Operation

The Company has completed the first phase of its Cable Recovery Project in Alaskan waters. The cable which was recovered was smaller diameter cable which was excellent for testing the recovery equipment and vessels. The Company evaluated the project and plans to conduct exploration activities in an attempt to identify larger cable. Should those activities identify any cable suitable for salvage operations, the Company would determine the proper title and ownership of the cable and once such title is determined act accordingly as to whether or not a recovery operation is warranted.

Mergers and Acquisitions

We will routinely review merger and acquisition opportunities. An appropriate merger and acquisition opportunity must be accretive to the overall value of Mexus Gold US. Our primary focus will be on those opportunities involving precious metal production or near-term production with a secondary focus on other resource-based opportunities. Potential acquisition targets would include private and public companies or individual properties. Although our preference would be for candidates located in the United States and Mexico. Mexus Gold US will consider opportunities located in other countries where the geopolitical risk is acceptable.

Mining Operations

We classify our mineral properties into three categories: “Development Properties”, “Advanced Exploration Properties”, and “Other Exploration Properties”. Development Properties are properties where a decision to develop the property into a producing mine has been made. Advanced Exploration Properties are those properties where we retain a significant ownership interest or joint venture and where there has been sufficient drilling and analysis to identify and report proven and probable reserves or other mineralized material. We currently do not have a Development Property or Advanced Exploration Property. Other Exploration Properties are those that do not fall into the other categories. Please see below for information about our Other Exploration Properties.

Other Exploration Properties

Our Other Exploration Properties consist of the following:

Mining Properties Located in Mexico

The following properties are located in Mexico and owned by Mexus Gold S.A. de C.V., our wholly owned subsidiary:

Caborca Project

On January 5, 2011, Mexus Gold Mining S.A. de C.V. entered into a Purchase Agreement to purchase the Caborca Project. The Caborca Project consists of 7,400 acres (3,000 hectares) about 50 kilometers northwest of the City of Caborca, Sonora State, Mexico. The Caborca Project lies on claims filed by the owners of the Santa Elena Ranch, which controls the surface rights over the project claims. The claims lie near 112o 25' W, 31o 7.5" N. These claims were visited near the end of January, 2011. On or about July 11, 2011, we acquired five additional claims surrounding the Caborca Project consisting of approximately 1,000 additional acres.

We have been unable to locate geologic maps of the area from the Government Geological Survey. However, pursuant to our investigation of the project, the claims were found to be underlain by an igneous complex. The rocks observed included many types of granitic rocks, exhibiting porphyrytic textures, gneissic and equigrannular textures. Quartz was variable. At times quartz "eyes" were observed, that is porphyrytic quartz which many workers consider to be indicative of a porphyry environment. In other localities, no quartz was evident. When no quartz was present, the rock was equigrannular. Quartz veining was evident throughout the claim group. A mine was developed along a major quartz vein, called the Julio 2 Mine with the vein being called the Julio Vein.

There are multiple exploration targets on the Caborca Project. The two most important are the quartz stockwork zone and the Julio vein system. The first target will be the quartz stockwork zone area. A detailed drilling program will be scheduled to test the Julio vein system.

[Please refer to Exhibit 99.1]

FIGURE 1 – PRELIMINARY REPORT AND FIRST STAGE MAPPING

Ocho Hermanos – Guadalupe de Ures Project

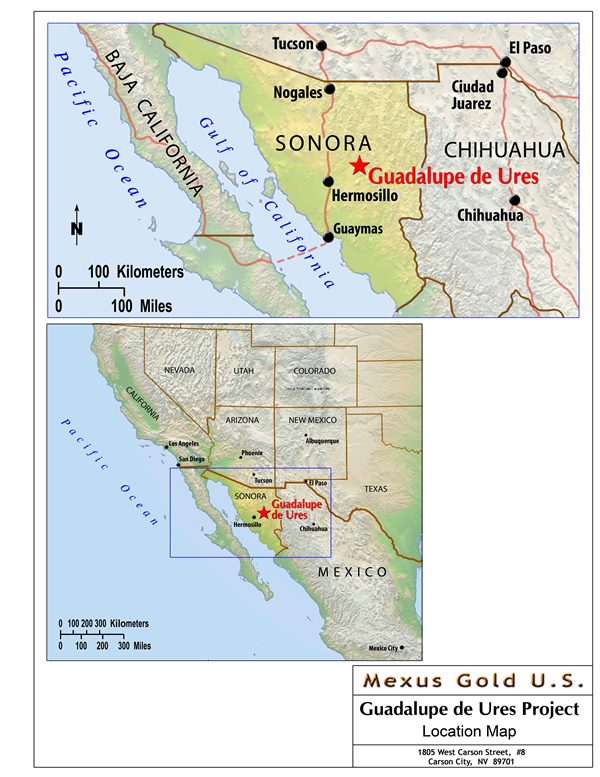

The Guadalupe de Ures Project is accessed from Hermosillo by driving via good paved road for 60 kilometers to the town of Guadalupe de Ures and then for 15 kilometers over dirt roads to the prospects. A base camp has been established near the town of Guadalupe de Ures using mainly trailers for accommodation, workshops and kitchen facilities.

FIGURE 2 - LOCATION MAP

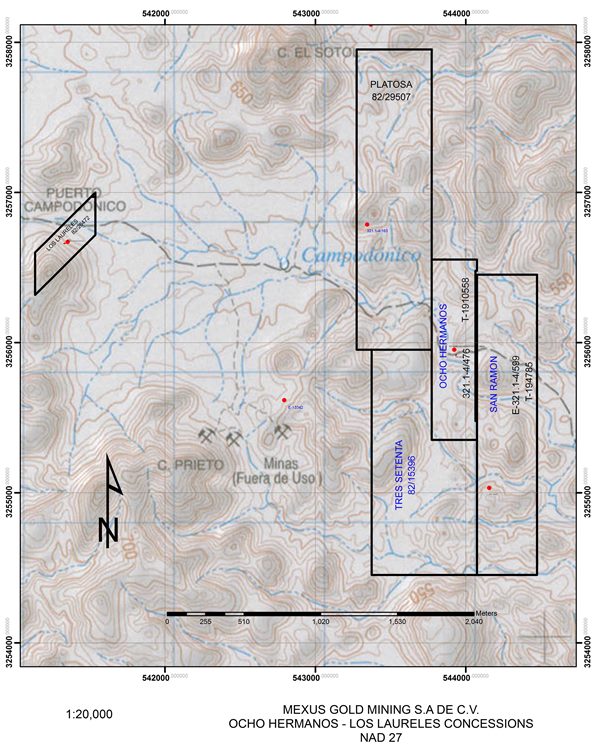

The Ocho Hermanos Project (also called the Guadalupe de Ures Project) consists of the “Ocho Hermanos” and "San Ramon" claims which are covered by the Sales and Production Contract dated the 4th day of July, 2009 between “Minerales Ruta Dorado de RL de CV” (seller) and “Mexus Gold Mining S.A. de C.V.”, a wholly owned subsidiary of Mexus Gold US (buyer). The Ocho Hermanos Claim consists of 34.9940 hectares (1 acre = 0.4047 hectares) or 86.4690 acres while the San Ramon Claim consists of 80 hectares (197.6773 acres).(Figure 4)

The term of the agreement is 5 years. During the term Mexus must pay 40% of the net revenue received for minerals produced to the seller. At the conclusion of the 5 years, the lease can be purchased for USD 50,000.

Minerales Ruta Dorado de RL de CV is a duly constituted Mexican Company and as such can hold mining claims in Mexico.

FIGURE 3 - OCHO HERMANOS

PROJECT AREA CLAIM MAP

Mexus did not perform any systematic sampling or any systematic drilling and because of this did not set up a formal QA/QC program. All of the samples were submitted to Certified Laboratories (ALS - Chemex in Hermosillo or American Assay in Reno, Nevada) which insert their own QA/QC samples/duplicates. Also the laboratories run duplicates and blanks from each batch fired The sequence of events so far are the following:

Mexus found a previously mined area with interesting values – Ocho Hermanos Mexus began to submit characterization samples to the above noted assay laboratories, in order to determine the range of Au - Ag values present Mexus then began an investigation into recovery options by using material taken from the areas with the better values.

The above work was completed before any systematic exploration was done because if no recovery method could be found relatively quickly, the project would move more slowly because of the lead time involved, Mexus began work on an Environmental Impact Statement for the likely operational area (a total of 4 hectares to begin). In order to complete the EIS, figures for estimated tonnages were submitted to cover the hoped for volume. To date, no suitable recovery method was found due primarily to the partial oxidation of the principally sulfide deposit

The Environmental Permits run for 35 years so there is time for further investigation

The main geologic feature of this project area is an apparent “manto” sulfide zone composed primarily of galena with some pyrite, arsenopyrite and possibly phyrrotite. Above this zone there is an oxide zone composed of iron and lead oxides. The sulfides themselves are partially oxidized. Reconnaissance and characterization samples taken indicated sporadically high gold and silver values. The deposit occurs in shallow water sediments (principally quartzites, with some limestone and shales) and can be best characterized as a skarn type deposit due to the presence of intrusive rocks within 1 kilometer.

Given the complex nature of the sulfide deposit and the partial oxidization of the material (indicated by the presence of yellow colored lead oxides), a satisfactory recovery method has not yet been found. Consequently, at this time, no further systematic work beyond the initial reconnaissance and characterization sampling has been completed. The entire project was essentially put on hold until a suitable recovery method is found, which is a continuing effort and at this time is being pursued by member of the faculty at the University of Sonora in Hermosillo. The faculty member teaches metallurgy and assay practices at the University. After a suitable recovery method has been identified, the process will need to be confirmed by a certified metallurgical testing laboratory.

The Environmental Permits detail all of the affected flora and fauna. The land is presently used for cattle grazing and the surface rights are owned by the community of Guadelupe de Ures. An agreement is in place with Mexus Gold Mining S.A. de C.V. for surface access and disturbance. The Environmental Permit concludes that no permanent damage or degradation of the present land use will result from the intended activity on the lands. At present, the Environmental Permits cover a total of 4 hectares - 3 hectares cover the initial site of the mineral as presently understood and 1 hectare is permitted for the erection of a suitable extraction plant.

No known contamination from past mining activities was found or is known to locals. The historic workings consisted of a few shallow adits and pits. In the course of obtaining the Environmental Permission the permit stipulated that properly lined ponds etc must be used to prevent any potential surface or ground water contamination from any proposed activities.

Only separation is proposed to be conducted on site if found to be possible, while final metal recovery will be conducted at a properly licensed and certified metal refining facility. Current efforts to find suitable recovery methods are being conducted off site in a University laboratory. Up sizing the process, if found, will be completed by a licensed, certified metallurgical laboratory.

Figures of the proposed permitted sites are attached. These were extracted from the environmental permit

application.

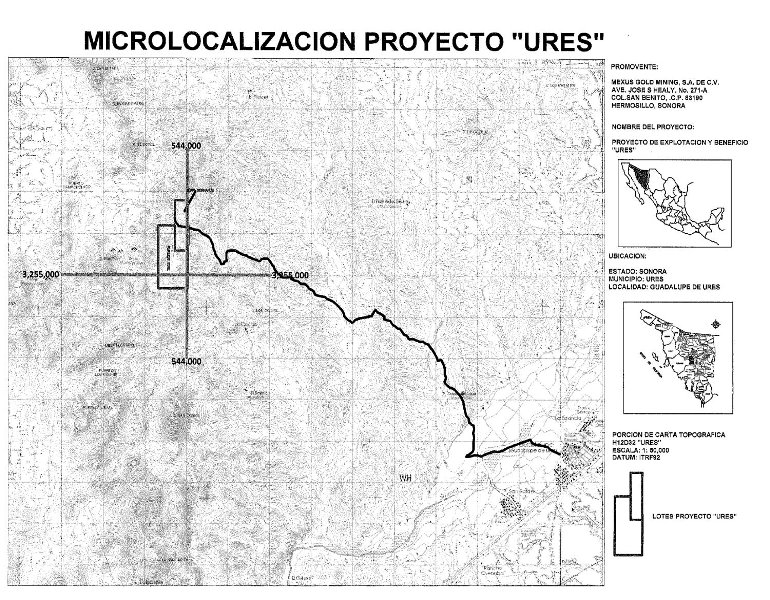

FIGURE 4- MICROLOCALIZACION PROYECTO “URES MINING DISTRICT”

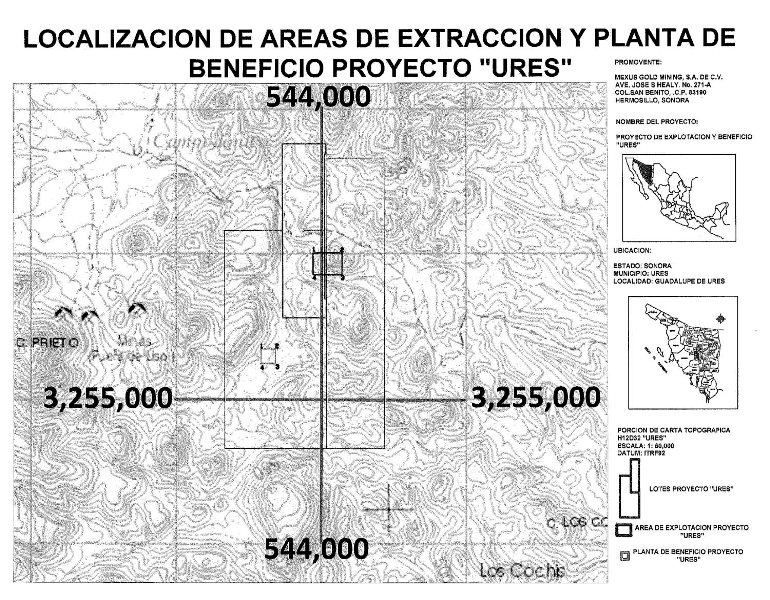

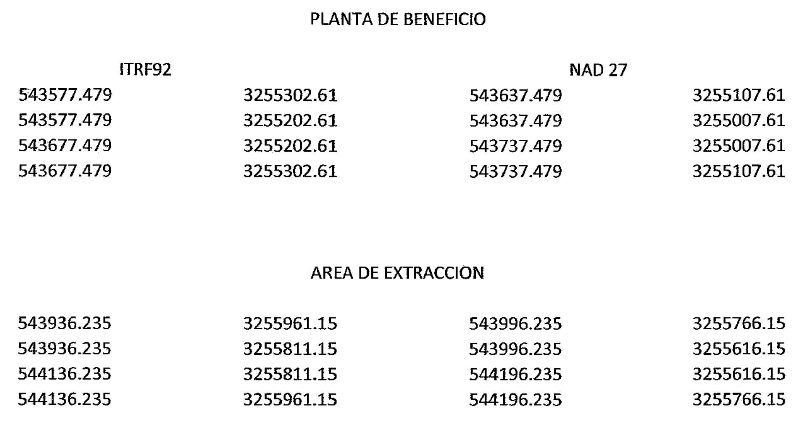

FIGURE 5 – LOCALIZACION DE AREAS DE EXTRACCION

FIGURE 6 - PLANTA DE BENEFICIO

AREA DE EXTRACCION

370 Area

This zone is composed of a sedimentary sequence (limestone, quartzite, shale) intruded by dacite and diorite as well as rhyolite. The dacite exhibits argillic alterations as well as silicification (quartz veins). The entire area is well oxidized on the surface. This is an area of classic disseminated low grade gold and silver mineralization. Surface grab sample assays show 0.14 grams per ton to as high as 29.490 grams per ton gold. This area is an important area for potentially defining an open pit heap leach project.

El Scorpion Project Area

This area has several shear zones and veins which show copper and gold mineralization’s. Recent assays of an 84’ drill hole shows 1.750% per ton to .750% per ton of copper and 3.971 grams per ton to 0.072 grams per ton of gold. Another assay of rock sample from the area shows greater than 4.690% per ton copper. This land form distribution appears to be synonymous to the ideal porphyry deposit at Baja La Alumbrera, Argentina.

Los Laureles

Los Laureles is a vein type deposit mainly gold with some silver and copper. Recent assays from grab samples show gold values of 67.730 grams per ton gold, 38.4 grams per ton silver, 2,800 grams per ton copper.

As of the date of this Report, we have opened up old workings at the Los Laureles claim and have discovered a gold carrying vein running north and south into the mountain to the south.

Mining Properties located in the state of Nevada

Lida Mining District

The Lida Project is located in south central Nevada, approximately 20 miles south-west of Goldfield. The project area is accessed by proceeding 15 miles south of Goldfield along US Highway 95 to Lida Junction. Then by proceeding west along Nevada State Route 266 for 19 miles to Lida, Nevada, the project site. This mining property was fully impaired in the accounting records of the Company on March 31, 2013.

Cable Salvage Operation

Our examination of the information provided to us and our accumulation of data has identified the most prospective area to begin our salvage operations is the near coast areas of Alaska. The initial recovery operations will be comprised of acquiring two and one-half inch diameter cable with a weight of eight and one-half pounds. We are satisfied that we will be able to comply with all permits and notifications to the appropriate governmental authorities regarding the salvage operations.

The Company has completed the first phase of its Cable Recovery Project in Alaskan waters. The cable which was recovered was smaller diameter cable which was excellent for testing the recovery equipment and vessels. The Company evaluated the project and plans to conduct exploration activities in an attempt to identify larger cable. Should those activities identify any cable suitable for salvage operations, the Company would determine the proper title and ownership of the cable and once such title is determined act accordingly as to whether or not a recovery operation is warranted.

Employees

Mexus Gold US has no employees at this time. Consultants with specific skills are utilized to assist with various aspects of the requirements of activities such as project evaluation, property management, due diligence, acquisition initiatives, corporate governance and property management. If we complete our planned activation of the Nichols Property Exploration and Drilling Program, Cable Salvage Operations and operations of the Mexican mining properties, our total workforce will be approximately 30 persons. Mr. Paul D. Thompson is our sole officer and director.

Competition

Mexus Gold US competes with other mining companies in connection with the acquisition of gold properties. There is competition for the limited number of gold acquisition opportunities, some of which is with companies having substantially greater financial resources than Mexus Gold US. As a result, Mexus Gold US may have difficulty acquiring attractive gold projects at reasonable prices.

Management of Mexus Gold US believes that no single company has sufficient market power to affect the price or supply of gold in the world market.

Legal Proceedings

There are no legal proceedings to which Mexus Gold US or Mexus Gold S.A. de C.V. is a party or of which any of our properties are the subject thereof.

Property Interests, Mining Claims and Risk

Property Interests and Mining Claims

Our exploration activities are conducted in the state of Nevada and Mexico. Mineral interests may be owned in this state by (a) the United States, (b) the state itself, or (c) private parties. Where prospective mineral properties are owned by private parties, or by the state, some type of property acquisition agreement is necessary in order for us to explore or develop such property. Generally, these agreements take the form of long term mineral leases under which we acquire the right to explore and develop the property in exchange for periodic cash payments during the exploration and development phase and a royalty, usually expressed as a percentage of gross production or net profits derived from the leased properties if and when mines on the properties are brought into production. Other forms of acquisition agreements are exploration agreements coupled with options to purchase and joint venture agreements. Where prospective mineral properties are held by the United States, mineral rights may be acquired through the location of unpatented mineral claims upon unappropriated federal land. If the statutory requirements for the location of a mining claim are met, the locator obtains a valid possessory right to develop and produce minerals from the claim. The right can be freely transferred and, provided that the locator is able to prove the discovery of locatable minerals on the claims, is protected against appropriation by the government without just compensation. The claim locator also acquires the right to obtain a patent or fee title to his claim from the federal government upon compliance with certain additional procedures.

Mining claims are subject to the same risk of defective title that is common to all real property interests. Additionally, mining claims are self-initiated and self-maintained and therefore, possess some unique vulnerabilities

not associated with other types of property interests. It is impossible to ascertain the validity of unpatented mining claims solely from an examination of the public real estate records and, therefore, it can be difficult or impossible to confirm that all of the requisite steps have been followed for location and maintenance of a claim. If the validity of a patented mining claim is challenged by the BLM or the U.S. Forest Service on the grounds that mineralization has not been demonstrated, the claimant has the burden of proving the present economic feasibility of mining minerals located thereon. Such a challenge might be raised when a patent application is submitted or when the government seeks to include the land in an area to be dedicated to another use.

In addition, our operations in Mexico are subject to the rules and regulations of Mexico which is generally governed by the Ministry of Economy. While the Mexican laws have generally become more favorable to US related mining interests, as in the US, it will be difficult or impossible to confirm that all of the requisite steps have been followed for location and maintenance of a claim and we have hired Mexican legal counsel to assist us with our Mexican operations.

Reclamation

We may be required to mitigate long-term environmental impacts by stabilizing, contouring, re-sloping and re-vegetating various portions of a site after mining and mineral processing operations are completed. These reclamation efforts will be conducted in accordance with detailed plans, which must be reviewed and approved by the appropriate regulatory agencies.

Risk

Our success depends on our ability to recover precious metals, process them, and successfully sell them for more than the cost of production. The success of this process depends on the market prices of metals in relation to our costs of production. We may not always be able to generate a profit on the sale of gold or other minerals because we can only maintain a level of control over our costs and have no ability to control the market prices. The total cash costs of production at any location are frequently subject to great variation from year to year as a result of a number of factors, such as the changing composition of ore grade or mineralized material production, and metallurgy and exploration activities in response to the physical shape and location of the ore body or deposit. In addition costs are affected by the price of commodities, such as fuel and electricity. Such commodities are at times subject to volatile price movements, including increases that could make production at certain operations less profitable. A material increase in production costs or a decrease in the price of gold or other minerals could adversely affect our ability to earn a profit on the sale of gold or other minerals. Our success depends on our ability to produce sufficient quantities of precious metals to recover our investment and operating costs.

Distribution Methods of the Products

The end product of our operations will usually be doré bars. Doré is an alloy consisting of gold, silver and other precious metals. Doré is sent to refiners to produce bullion that meets the required market standard of 99.95% pure gold. Under the terms of refining agreements we expect to execute, the doré bars are refined for a fee and our share of the refined gold, silver and other metals are credited to our account or delivered to our buyers who will then use the refined metals for fabrication or held for investment purposes.

General Market

The general market for gold has two principal categories, being fabrication and investment. Fabricated gold has a variety of end uses, including jewelry, electronics, dentistry, industrial and decorative uses, medals, medallions and official coins. Gold investors buy gold bullion, official coins and jewelry. The supply of gold consists of a combination of current production from mining and the draw-down of existing stocks of gold held by governments, financial institutions, industrial organizations and private individuals.

Patents, trademarks, licenses, franchises, concessions, royalty agreements, or labor contracts, including duration;

We do not have any designs or equipment which is copyrighted, trademarked or patented.

Effect of existing or probable governmental regulations on the business

Government Regulation

Government Regulation

Mining operations and exploration activities are subject to various national, state, provincial and local laws and regulations in the United States, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters. We have obtained or have pending applications for those licenses, permits or other authorizations currently required to conduct our exploration and other programs. We believe that Mexus Gold US is in compliance in all material respects with applicable mining, health, safety and environmental statutes and the regulations passed thereunder in the Nevada and United States and in any other jurisdiction in which we will operate. We are not aware of any current orders or directions relating to Mexus Gold US with respect to the foregoing laws and regulations.

Our operations in Mexico are subject to the rules and regulations of Mexico which is generally governed by the Ministry of Economy. While the Mexican laws have generally become more favorable to US related mining interests, as in the US, it will be difficult or impossible to confirm that all of the requisite steps have been followed for location and maintenance of a claim and we have hired Mexican legal counsel to assist us with our Mexican operations.

Environmental Regulation

Our gold projects are subject to various federal and state laws and regulations governing protection of the environment. These laws are continually changing and, in general, are becoming more restrictive. It is our policy to conduct business in a way that safeguards public health and the environment. We believe that the actions and operations of Mexus Gold US will be conducted in material compliance with applicable laws and regulations. Changes to current state or federal laws and regulations in Nevada, where we operate currently, or in jurisdictions where we may operate in the future, could require additional capital expenditures and increased operating and/or reclamation costs. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could impact the economics of our projects.

Research and Development

We do not foresee any immediate future research and development costs.

Costs and effects of compliance with environmental laws

Our gold projects are subject to various federal and state laws and regulations governing protection of the environment. These laws are continually changing and, in general, are becoming more restrictive. It is our policy to conduct business in a way that safeguards public health and the environment. We believe that our operations are and will be conducted in material compliance with applicable laws and regulations. The economics of our current projects consider the costs and expenses associated with our compliance policy.

Changes to current state or federal laws and regulations in Nevada, where we operate currently, or in jurisdictions where we may operate in the future, could require additional capital expenditures and increased operating and/or reclamation costs. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could impact the economics of our projects.

Results of Operations

The following management’s discussion and analysis of operating results and financial condition of Mexus Gold US is for the three month periods ended June 30, 2014 and 2013. All amounts herein are in U.S. dollars.

Three Months Ended June 30, 2014 compared with the Three Months Ended June 30, 2013

We had a net income during the three months ended June 30, 2014 of $744,407 compared to a net loss of $1,141,997 during the same period in 2013. The increase in net income is attributable to the decrease in (i) Exploration Costs – a $286,006 decrease in exploration costs primarily attributable to the Joint Venture Agreement entered into between Mexus Gold US, Mexus Gold Mining, Minerals La Negra S. de R.L. de C.V. and Trinidad Pacifica S. de R.L. de C.V. on November 1, 2012. Mexus US Gold’s interest in the Joint Venture Agreement was sold in the fourth quarter of fiscal 2014 and reported as discontinued operations in the consolidated financial statements. (ii) Gain on derivative liabilities – a $1,128,716 increase primarily due to a decrease in the share price of common stock of the Company and the decreased expected life of conversion options and warrants.

Revenue

For the three months ended June 30, 2014, we had revenues of $999 compared to $109,317 for the three months ended June 30, 2013. The decrease in revenue was due to discontinued operations related to the Joint Venture Agreement.

Operating Expenses

Total operating expenses decreased to $282,764 during three months ended June 30, 2014, compared to $557,054 for the three months ended June 30, 2013. The decrease in operating expenses was due to a reduction in mining operations through the exploration activities of our properties and general administrative expenses.

Other Income (Expense)

We reported $1,026,172 of other income during the three months ended June 30, 2014 compared to $175,048 other expenses during the same period in 2013.

The increase in other income is mainly attributable to:

(a) Decrease in interest expense. The decrease in interest expense is due to a decrease in the amortization of deferred finance costs.

(b) The fair value of the secured convertible promissory note derivative and warrant derivative liabilities is $751,304 at June 30, 2014. The decrease in the fair value of the derivative liabilities of 1,124,033 is recorded as a gain in the unaudited consolidated statement of operations for the three months ended June 30, 2014.

Liquidity and Capital Resources

At June 30, 2014, we had cash of $911 compared to $0 at March 31, 2014.

Our equipment decreased to $1,461,095 at June 30, 2014, compared to $1,567,165 at March 31, 2014. The decrease in equipment is largely due to depreciation expense of $82,398 during the three months ended June 30, 2014.

Our mineral properties had no change during the three months period.

Equipment under construction decreased to $85,522 at June 30, 2014, compared to $107,522 at March 31, 2014. The decrease in equipment under construction was due to sale of equipment during the three months ended June 30, 2014.

Total assets decreased to $2,249,804 at June 30, 2014, compared to $2,415,998 at March 31, 2014. The majority of the decrease in assets relates to the decrease in the fair value of marketable securities and depreciation of equipment.

Our total liabilities decreased to $2,013,351 at June 30, 2014, compared to $3,068,884 as of March 31, 2014. The decrease in our total liabilities can be primarily attributed the decrease in the fair value of secured convertible promissory note derivative and warrant derivative liabilities

The Company is dependent upon outside financing to continue operations. It is management’s plans to raise necessary funds through a private placement of its common stock to satisfy the capital requirements of the Company’s business plan. There is no assurance that the Company will be able to raise the necessary funds, or that if it is successful in raising the necessary funds, that the Company will successfully execute its business plan.

Future goals

The Caborca Properties have become our primary focus after our installation of a small placer recovery plant to conduct tests on prospective placer areas and determine the viability of the placer deposits while we conducted evaluations of the other Mexico properties. We have added additional equipment which will allow the continuation of mining operations of the placer deposits.

The Company has now scheduled the installation of a crushing/milling recovery plant for the high grade Julio quartz deposit as a result of the values of the assay analysis from the deposit which range from 0.250 to 5.5 ounces of gold per ton.

Therefore, our goal for the current year is to increase the cash flow of the placer mining operation, continue the drilling program which begun during 2011, initialize mining operations on the Julio quartz deposit while we conduct a thorough geological study by an independent geological firm of the future potential of other vein deposits located near the Julio deposit.

Foreign Currency Transactions

The majority of our operations are located in United States and most of our transactions are in the local currency. We plan to continue exploration activities in Mexico and therefore we will be exposed to exchange rate fluctuations. We do not trade in hedging instruments and a significant change in the foreign exchange rate between the United States Dollar and Mexican Peso could have a material adverse effect on our business, financial condition and results of operations.

Off-balance Sheet Arrangements

The Company does not have any off-balance sheet arrangements that have or are reasonably likely to have a current or future effect on the Company’s financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that is material to investors.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

As a “smaller reporting company” as defined by Item 10 of Regulation S-K, the Company is not required to provide this information.

ITEM 4(T). CONTROLS AND PROCEDURES