Attached files

| file | filename |

|---|---|

| EX-31.1 - EXHIBIT 31.1 - Benefit Street Partners Realty Trust, Inc. | arcrftexhibit311q22014.htm |

| EX-31.2 - EXHIBIT 31.2 - Benefit Street Partners Realty Trust, Inc. | arcrftexhibit312q2014.htm |

| EX-32 - EXHIBIT 32 - Benefit Street Partners Realty Trust, Inc. | arcrftexhibit32q22014.htm |

| EXCEL - IDEA: XBRL DOCUMENT - Benefit Street Partners Realty Trust, Inc. | Financial_Report.xls |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

(Mark One)

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2014

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-55188

ARC Realty Finance Trust, Inc.

(Exact Name of Registrant as Specified in its Charter)

Maryland | 46-1406086 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

405 Park Avenue New York, New York | 10022 | |

(Address of Principal Executive Office) | (Zip Code) | |

(212) 415-6500

(Registrant’s Telephone Number, Including Area Code)

Not applicable

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one):

Large accelerated filer o | Accelerated filer o |

Non-accelerated filer o | Smaller reporting company x |

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The number of shares of the registrant's common stock, $0.01 par value, outstanding as of July 31, 2014 was 7,987,579.

TABLE OF CONTENTS

Page | |

PART I | |

PART II | |

PART I

Item 1. Financial Statements.

ARC REALTY FINANCE TRUST, INC.

CONSOLIDATED BALANCE SHEETS

June 30, 2014 | December 31, 2013 | ||||||

(Unaudited) | |||||||

ASSETS | |||||||

Cash | $ | 59,658 | $ | 178,030 | |||

Loans receivable, net | 141,546,674 | 30,831,571 | |||||

Mortgage-backed securities, at fair value | 14,517,950 | 5,005,000 | |||||

Accrued interest receivable | 675,901 | 126,118 | |||||

Prepaid expenses and other assets | 2,755,707 | 229,117 | |||||

Total assets | $ | 159,555,890 | $ | 36,369,836 | |||

LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||

Revolving line of credit with affiliate | $ | — | $ | 7,305,000 | |||

Revolving line of credit | 17,700,000 | — | |||||

Repurchase agreement | 11,601,000 | — | |||||

Accounts payable and accrued expenses | 2,906,661 | 1,737,882 | |||||

Distributions payable | 928,596 | 215,747 | |||||

Interest payable | 44,051 | 14,633 | |||||

Due to affiliate | — | 1,077,765 | |||||

Total liabilities | 33,180,308 | 10,351,027 | |||||

Preferred stock, $0.01 par value, 50,000,000 authorized, none issued and outstanding at June 30, 2014 and December 31, 2013 | — | — | |||||

Common stock, $0.01 par value, 300,000,000 shares authorized, 5,961,163 and 1,330,669 shares issued and outstanding as of June 30, 2014 and December 31, 2013, respectively | 59,533 | 13,267 | |||||

Additional paid-in capital | 129,364,322 | 26,620,266 | |||||

Accumulated other comprehensive income (loss) | 10,227 | (9,578 | ) | ||||

Accumulated deficit | (3,058,500 | ) | (605,146 | ) | |||

Total stockholders' equity | 126,375,582 | 26,018,809 | |||||

Total liabilities and stockholders' equity | $ | 159,555,890 | $ | 36,369,836 | |||

The accompanying notes are an integral part of these statements.

1

ARC REALTY FINANCE TRUST, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

Three Months Ended June 30, 2014 | Three Months Ended June 30, 2013 | Six Months Ended June 30, 2014 | Six Months Ended June 30, 2013 | ||||||||||||

Interest Income: | |||||||||||||||

Interest income | $ | 1,978,846 | $ | 66,076 | $ | 2,955,680 | $ | 66,077 | |||||||

Interest expense | 70,728 | 8,756 | 91,764 | 8,756 | |||||||||||

Net interest income | 1,908,118 | 57,320 | 2,863,916 | 57,321 | |||||||||||

Expenses: | |||||||||||||||

Acquisition fees | 863,452 | — | 1,122,452 | — | |||||||||||

Other expenses | 199,337 | 42,934 | 341,540 | 47,954 | |||||||||||

Professional fees | 77,684 | 18,089 | 190,844 | 18,089 | |||||||||||

Board expenses | 73,170 | 81,429 | 119,857 | 81,429 | |||||||||||

Insurance expense | 55,000 | 55,000 | 110,000 | 55,000 | |||||||||||

Loan loss provision | 41,138 | — | 127,600 | — | |||||||||||

Total expenses | 1,309,781 | 197,452 | 2,012,293 | 202,472 | |||||||||||

Income (loss) before income taxes | 598,337 | (140,132 | ) | 851,623 | (145,151 | ) | |||||||||

Income tax provision | 13,300 | — | 40,800 | — | |||||||||||

Net income (loss) | $ | 585,037 | $ | (140,132 | ) | $ | 810,823 | $ | (145,151 | ) | |||||

Basic net income (loss) per share | $ | 0.14 | $ | (1.37 | ) | $ | 0.26 | $ | (1.42 | ) | |||||

Diluted net income (loss) per share | $ | 0.14 | $ | (1.37 | ) | $ | 0.26 | $ | (1.42 | ) | |||||

Basic weighted average shares outstanding | 4,251,401 | 101,990 | 3,144,815 | 101,990 | |||||||||||

Diluted weighted average shares outstanding | 4,256,985 | 101,990 | 3,149,657 | 101,990 | |||||||||||

__________________________________________________________

N/A - Not Applicable as net loss would result in anti-dilutive presentation

The accompanying notes are an integral part of these statements.

2

ARC REALTY FINANCE TRUST, INC.

CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS' EQUITY

(Unaudited)

Common Stock | ||||||||||||||||||||||

Number of Shares | Par Value | Additional Paid-In Capital | Accumulated Other Comprehensive Income (Loss) | Accumulated Deficit | Total Stockholders' Equity | |||||||||||||||||

Balance, December 31, 2013 | 1,330,669 | $ | 13,267 | $ | 26,620,266 | $ | (9,578 | ) | $ | (605,146 | ) | $ | 26,018,809 | |||||||||

Issuance of common stock | 4,587,872 | 45,879 | 114,020,200 | — | — | 114,066,079 | ||||||||||||||||

Net income | — | — | — | — | 810,823 | 810,823 | ||||||||||||||||

Distributions declared | — | — | — | — | (3,264,177 | ) | (3,264,177 | ) | ||||||||||||||

Common stock issued through distribution reinvestment plan | 38,584 | 387 | 915,974 | — | — | 916,361 | ||||||||||||||||

Share-based compensation | 4,038 | — | 11,427 | — | — | 11,427 | ||||||||||||||||

Common stock offering costs, commissions and dealer manager fees | — | — | (12,203,545 | ) | — | — | (12,203,545 | ) | ||||||||||||||

Other comprehensive income | — | — | — | 19,805 | — | 19,805 | ||||||||||||||||

Balance, June 30, 2014 | 5,961,163 | $ | 59,533 | $ | 129,364,322 | $ | 10,227 | $ | (3,058,500 | ) | $ | 126,375,582 | ||||||||||

The accompanying notes are an integral part of this statement.

3

ARC REALTY FINANCE TRUST, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

For the Six Months Ended June 30, 2014 | For the Six Months Ended June 30, 2013 | ||||||

Cash flows from operating activities: | |||||||

Net income (loss) | $ | 810,823 | $ | (145,151 | ) | ||

Adjustments to reconcile net income (loss) to net cash used in operating activities: | |||||||

Discount accretion and premium amortization, net | (101,710 | ) | (19,733 | ) | |||

Share-based compensation | 11,427 | 6,804 | |||||

Loan loss provision | 127,600 | — | |||||

Changes in assets and liabilities: | |||||||

Accrued interest receivable | (549,783 | ) | (24,631 | ) | |||

Prepaid expenses and other assets | (1,407,860 | ) | (33,153 | ) | |||

Accounts payable and accrued expenses | 1,165,004 | 7,987 | |||||

Interest payable | 29,418 | 129,441 | |||||

Net cash provided by (used in) operating activities: | $ | 84,919 | $ | (78,436 | ) | ||

Cash flows from investing activities: | |||||||

Loan investments | $ | (110,809,763 | ) | $ | (3,965,914 | ) | |

Mortgage-backed securities investments | (9,496,958 | ) | — | ||||

Principal repayments received on loan investments | 72,584 | 6,179 | |||||

Net cash used in investing activities | $ | (120,234,137 | ) | $ | (3,959,735 | ) | |

Cash flows from financing activities: | |||||||

Proceeds from issuances of common stock | $ | 114,066,079 | $ | 2,301,500 | |||

Payments of offering costs and fees related to common stock issuances | (12,203,545 | ) | (1,142,642 | ) | |||

Proceeds receivable from share sales | (1,118,730 | ) | — | ||||

Borrowings on revolving line of credit with affiliate | 5,550,000 | 1,950,000 | |||||

Repayments of revolving line of credit with affiliate | (12,855,000 | ) | — | ||||

Borrowings on revolving line of credit | 17,700,000 | — | |||||

Borrowings on repurchase agreement | 11,611,000 | — | |||||

Repayments of repurchase agreement | (10,000 | ) | — | ||||

Advances from (repayments to) affiliate | (1,077,765 | ) | 1,133,556 | ||||

Distributions paid | (1,631,193 | ) | (507 | ) | |||

Net cash provided by financing activities: | $ | 120,030,846 | $ | 4,241,907 | |||

Net change in cash | $ | (118,372 | ) | $ | 203,736 | ||

Cash, beginning of period | 178,030 | 573 | |||||

Cash, end of period | $ | 59,658 | $ | 204,309 | |||

Escrow deposits payable related to loan investments | $ | — | $ | 5,500 | |||

Interest paid | $ | 62,346 | $ | — | |||

Distributions payable | $ | 928,596 | $ | 17,755 | |||

Common stock issued through distribution reinvestment plan | $ | 916,361 | $ | 526 | |||

Reclassification of deferred offering costs to additional paid-in capital | $ | — | $ | 940,618 | |||

The accompanying notes are an integral part of these statements.

4

ARC REALTY FINANCE TRUST, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited)

Three Months Ended June 30, 2014 | Three Months Ended June 30, 2013 | Six Months Ended June 30, 2014 | Six Months Ended June 30, 2013 | ||||||||||||

Net income (loss) | $ | 585,037 | $ | (140,132 | ) | $ | 810,823 | $ | (145,151 | ) | |||||

Unrealized gain on available-for-sale securities | — | — | 19,805 | — | |||||||||||

Comprehensive income (loss) attributable to ARC Realty Finance Trust, Inc. | $ | 585,037 | $ | (140,132 | ) | $ | 830,628 | $ | (145,151 | ) | |||||

The accompanying notes are an integral part of these statements.

5

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

Note 1 - Organization and Business Operations

ARC Realty Finance Trust, Inc. (the “Company”) was incorporated in Maryland on November 15, 2012 and conducts its operations to qualify as a real estate investment trust for U.S. federal income tax purposes ("REIT") beginning with the filing of its tax return for the taxable year ended December 31, 2013. The Company is offering for sale a maximum of $2.0 billion of common stock, $0.01 par value per share, on a “reasonable best efforts” basis, pursuant to a registration statement on Form S-11 (the “Offering”) filed with the U.S. Securities and Exchange Commission (the “SEC”) under the Securities Act of 1933, as amended (the "Securities Act"). The Offering also covers the offer and sale of up to approximately $400.0 million in shares of common stock pursuant to a distribution reinvestment plan (the “DRIP”) under which common stockholders may elect to have their distributions reinvested in additional shares of the Company’s common stock. On May 14, 2013, the Company commenced business operations after raising in excess of $2.0 million of equity, the amount required for the Company to release equity proceeds from escrow.

For at least until February 12, 2015, which is two years from the effective date of the Offering, the per share purchase price in the Offering will be up to $25.00 per share (including the maximum allowed to be charged for commissions and fees) and the per share purchase price for shares issued under the DRIP will be $23.75 per share, which is 95% of the purchase price per share in the Offering. As of June 30, 2014, the aggregate value of all the common stock outstanding was $149.0 million based on a per share value of $25.00 (or $23.75 for shares issued under DRIP). Beginning with the filing of the Company's second Quarterly Report on Form 10-Q following February 12, 2015 ("NAV Pricing Date"), the Company will begin offering shares in the Offering and the DRIP at a per share purchase price that will vary quarterly and will be equal to the net asset value (“NAV”) divided by the number of shares outstanding as of the end of business on the first day of each fiscal quarter after giving effect to any share purchases or repurchases effected in the immediately preceding quarter (“per share NAV”) and applicable selling commissions and dealer manager fees will be added to the per share price for shares in the Company’s primary offering but not for the DRIP.

The Company has sold 8,888 shares of the Company's common stock to ARC Realty Finance Special Limited Partnership, LLC (the “Special Limited Partner”), an entity controlled by American Realty Capital VIII, LLC (the “Sponsor”) for $22.50 per share or a total of $0.2 million. Substantially all of the Company's business is conducted through ARC Realty Finance Operating Partnership, L.P. (the “OP”), a Delaware limited partnership. ARC Realty Finance Advisors, LLC (the “Advisor”), a Delaware limited liability company, is the Company’s advisor. The Company is the sole general partner and holds substantially all of the units of limited partner interests in the OP (“OP units”). Additionally, the Special Limited Partner contributed $2,020 to the OP in exchange for 90 units of limited partner interests in the aggregate OP ownership, which represents a nominal percentage of the aggregate OP ownership. The limited partner interests have the right to convert OP units for the cash value of a corresponding number of shares of the Company's common stock or, at the option of the OP, a corresponding number of shares of the Company's common stock, as allowed by the limited partnership agreement of the OP. The remaining rights of the limited partner interests do not include the ability to replace the general partner or to approve the sale, purchase or refinancing of the OP’s assets.

The Company was formed to acquire, originate and manage a diversified portfolio of commercial real estate debt investments secured by properties located both within and outside of the United States. The Company may also invest in commercial real estate securities and commercial real estate properties. Commercial real estate debt investments may include first mortgage loans, subordinated mortgage loans, mezzanine loans and participations in such loans. Commercial real estate securities may include commercial mortgage-backed securities (“CMBS”), senior unsecured debt of publicly traded REITs, debt or equity securities of other publicly traded real estate companies and collateralized debt obligations (“CDOs”).

The Company has no direct employees. The Company has retained the Advisor to manage the Company's affairs on a day-to-day basis. Realty Capital Securities, LLC (the “Dealer Manager”) serves as the dealer manager of the Offering. The Advisor and Dealer Manager are under common control with the parent of the Sponsor, as a result of which they are related parties and each of them have or will receive compensation and fees for services related to the Offering and the investment and management of the Company's assets. The Advisor and Dealer Manager have or will also receive fees during the Offering, acquisition, operational and liquidation stages of the Company.

Note 2 - Summary of Significant Accounting Policies

Basis of Accounting

The accompanying consolidated financial statements and related footnotes are unaudited and have been prepared in accordance with accounting principles generally accepted in the United States of America (‘‘GAAP’’) for interim financial

6

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

statements. The consolidated financial statements of the Company are prepared on an accrual basis of accounting. In the opinion of management, the interim data includes all adjustments, of a normal and recurring nature, necessary for a fair statement of the results for the periods presented. Interim period results may not be indicative of full year or future results. The unaudited consolidated financial statements do not include all information and notes required in annual audited financial statements in conformity with GAAP.

Principles of Consolidation and Basis of Presentation

The accompanying consolidated financial statements include the accounts of the Company, the OP and its subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation. In determining whether the Company has a controlling financial interest in a joint venture and the requirement to consolidate the accounts of that entity, management considers factors such as ownership interest, authority to make decisions and contractual and substantive participating rights of the other partners or members as well as whether the entity is a variable interest entity for which the Company is the primary beneficiary.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Management makes significant estimates regarding classification of investments, fair value measurements, credit losses and impairments of investments, and derivative financial instruments and hedging activities, as applicable.

Loans Receivable

Commercial real estate loans are intended to be held until maturity and, accordingly, are carried at cost, net of unamortized acquisition expenses, discounts or premiums and unfunded commitments. Real estate debt investments that are deemed to be impaired will be carried at amortized cost less a specific allowance for loan losses. Interest income is recorded on the accrual basis and related discounts, premiums, and acquisition expenses on investments are amortized over the life of the investment using the effective interest method. Amortization is reflected as an adjustment to interest income in the Company’s consolidated statements of operations.

Allowance for Loan Losses

The allowance for loan losses reflects management's estimate of loan losses inherent in the loan portfolio as of the balance sheet date. The reserve is increased through the "Loan loss provision" on the Company's consolidated statement of operations and is decreased by charge-offs when losses are confirmed through the receipt of assets such as cash in a pre-foreclosure sale or via ownership control of the underlying collateral in full satisfaction of the loan upon foreclosure or when significant collection efforts have ceased. The Company uses a uniform process for determining its allowance for loan losses. The allowance for loan losses includes a general, formula-based component and an asset-specific component.

General reserves are recorded when (i) available information as of each balance sheet date indicates that it is probable a loss has occurred in the portfolio and (ii) the amount of the loss can be reasonably estimated. The Company currently estimates loss rates based on historical realized losses experienced in the industry and takes into account current collateral and economic conditions affecting the probability or severity of losses when establishing the allowance for loan losses. The Company performs a comprehensive analysis of its loan portfolio and assigns risk ratings to loans that incorporate management's current judgments about their credit quality based on all known and relevant internal and external factors that may affect collectability. The Company considers, among other things, payment status, lien position, borrower financial resources and investment in collateral, collateral type, project economics and geographical location as well as national and regional economic factors. This methodology results in loans being segmented by risk classification into risk rating categories that are associated with estimated probabilities of default and principal loss. Ratings range from "1" to "5" with "1" representing the lowest risk of loss and "5" representing the highest risk of loss.

As of June 30, 2014, the Company had seventeen loan investments, all of which were performing as of June 30, 2014. The Company has established a $127,600 allowance for loan losses as of June 30, 2014. There are no specifically reserved loans in the portfolio as of June 30, 2014.

The asset-specific reserve component relates to reserves for losses on individual impaired loans. The Advisor considers a loan to be impaired when, based upon current information and events, it believes that it is probable that the Company will be unable to collect all amounts due under the contractual terms of the loan agreement. This assessment is made on a loan-by-loan

7

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

basis each quarter based on such factors as payment status, lien position, borrower financial resources and investment in collateral, collateral type, project economics and geographical location as well as national and regional economic factors. A reserve is established for an impaired loan when the present value of payments expected to be received, observable market prices, or the estimated fair value of the collateral (for loans that are dependent on the collateral for repayment) is lower than the carrying value of that loan.

For collateral dependent impaired loans, impairment is measured using the estimated fair value of collateral less the estimated cost to sell. The Advisor generally will use the income approach through internally developed valuation models to estimate the fair value of the collateral for such loans. In more limited cases, the Advisor will obtain external "as is" appraisals for loan collateral, generally when third party participations exist. Valuations will be performed or obtained at the time a loan is determined to be impaired and designated non-performing, and they will be updated if circumstances indicate that a significant change in value has occurred.

A loan is also considered impaired if its terms are modified in a troubled debt restructuring ("TDR"). A TDR occurs when a concession is granted and the debtor is experiencing financial difficulties. Impairments on TDR loans are generally measured based on the present value of expected future cash flows discounted at the effective interest rate of the original loan.

Income recognition will be suspended for loans at the earlier of the date at which payments become 90-days past due or when, in the opinion of the Advisor, a full recovery of income and principal becomes doubtful. Income recognition will be resumed when the suspended loan becomes contractually current and performance is demonstrated to have resumed. A loan will be written off when it is no longer realizable and legally discharged.

Real Estate Securities

On the acquisition date, all of the Company’s commercial real estate securities will be classified as available for sale, and will be carried at fair value, with any unrealized gains or losses reported as a component of accumulated other comprehensive income or loss. However, the Company may elect the fair value option for certain of its available for sale securities, and as a result, any unrealized gains or losses on such securities will be recorded as unrealized gains or losses on investments in the Company’s consolidated statement of operations, no such election has been made to date. Premiums or discounts on commercial real estate securities will be recognized using the effective interest method and recorded as an adjustment to interest income.

Impairment Analysis of Securities

Commercial real estate securities for which the fair value option has not been elected will be periodically evaluated for other-than-temporary impairment. If the fair value of a security is less than its amortized cost, the security will be considered impaired. Impairment of a security will be considered to be other-than-temporary when (i) the Advisor has the intent to sell the impaired security; (ii) it is more likely than not the Company will be required to sell the security; or (iii) the Advisor does not expect to recover the entire amortized cost of the security. If the Advisor determines that an other-than-temporary impairment exists and a sale is likely to occur, the impairment charge will be recognized as an “Impairment of assets” on the Company's consolidated statement of operations and comprehensive income or loss. If a sale is not expected to occur, the portion of the impairment charge related to credit factors will be recorded as an “Impairment of assets” on the Company's consolidated statement of operations and comprehensive income or loss with the remainder recorded as an unrealized gain or loss on investments reported as a component of accumulated other comprehensive income or loss.

Commercial real estate securities for which the fair value option has been elected will not be evaluated for other-than-temporary impairment as changes in fair value are recorded in the Company’s consolidated statement of operations and comprehensive income or loss, no such election has been made to date.

Fair Value of Financial Instruments

The Company is required to disclose the fair value of financial instruments for which it is practicable to estimate that value. The fair value of short-term financial instruments such as cash, accrued interest receivable, and accounts payable and accrued expenses approximate their carrying value on the accompanying consolidated balance sheets due to the monthly terms.

As of June 30, 2014, the Company had three CMBS investments. These investments are available for sale real estate securities which are recorded at fair value at June 30, 2014.

On May 15, 2013, the Company entered into a credit agreement for an unsecured $5.0 million revolving line of credit with AR Capital, LLC, the parent of the Sponsor (the “Revolver”). As of June 30, 2014, the Company had no outstanding principal balance under the Revolver, which bore interest at a fixed rate of 3.25% (See Note 5 - Debt). The Company did not exercise the

8

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

extension option provided under the terms of the Revolver and allowed it to mature on May 15, 2014. The Company did not have an outstanding balance on the date of maturity.

As of June 30, 2014, the Company had $11.6 million outstanding under its Master Repurchase Agreement (the "MRA") with JP Morgan Securities, LLC ("JPM"), which bears interest at a floating rate of London Interbank Offered Rate ("LIBOR") plus a spread. As of June 30, 2014, the weighted average interest rate was 1.368%, including LIBOR. (See Note 5 - Debt). As of June 30, 2014, the Company believes the carrying value of the JPM MRA approximates fair value due to the month-to-month term of the repurchase agreements.

As of June 30, 2014, the Company had $17.7 million outstanding under the Uncommitted Master Repurchase Agreement (the “JPM Repo Facility”) with JPMorgan Chase Bank, National Association. Advances under the JPM Repo Facility accrue interest at per annum rates equal to the sum of (i) the applicable LIBOR index rate plus (ii) a margin of between 2.25% to 4.50%, depending on the attributes of the purchased assets. As of June 30, 2014, the weighted average interest rate on advances was 4.653%. As of June 30, 2014, the Company believes the carrying value of the JPM Repo Facility approximates fair value due to JPM Repo Facility being finalized relatively close to June 30, 2014.

Cash and Cash Equivalents

Cash includes cash in bank accounts. The Company deposits cash with high quality financial institutions. These deposits are guaranteed by the Federal Deposit Insurance Company up to an insurance limit. Cash equivalents include short-term, liquid investments in a money market fund.

Restricted Cash

Restricted cash may primarily consist of escrow deposits for future debt service payments, taxes, insurance, property maintenance or other amounts collected with mortgage loan originations.

Share Repurchase Program

The Company has a Share Repurchase Program (the “SRP”) that enables stockholders to sell their shares to the Company. Under the SRP, stockholders may request that the Company redeem all or any portion of their holdings, subject to certain conditions described below, if such repurchase does not impair the Company's capital or operations.

Prior to the time that the Company’s shares are listed on a national securities exchange and until the NAV Pricing Date, the repurchase price per share will depend on the length of time stockholders have held such shares as follows: after one year from the purchase date — the lower of $23.13 and 92.5% of the amount they actually paid for each share; after two years from the purchase date — the lower of $23.75 and 95.0% of the amount they actually paid for each share; after three years from the purchase date — the lower of $24.38 and 97.5% of the amount they actually paid for each share; and after four years from the purchase date — the lower of $25.00 and 100% of the amount they actually paid for each share (in each case, as adjusted for any stock distributions, combinations, splits and recapitalizations).

Upon reaching the NAV Pricing Date, the price per share that the Company will pay to repurchase shares of the Company’s common stock on any business day will be the Company's per share NAV for the quarter, calculated after the close of business on the first business day of each quarter. Subject to limited exceptions, stockholders who redeem their shares of the Company's common stock within the first four months from the date of purchase will be subject to a short-term trading fee of 2% of the aggregate per share NAV of the shares of common stock received. Because the Company's per share NAV will be calculated quarterly, the redemption price may fluctuate between the redemption request day and the date on which the Company pays redemption proceeds.

Prior to reaching the NAV Pricing Date, the Company is only authorized to repurchase shares pursuant to the SRP using the proceeds received from the DRIP and other operating funds, if any, which may be reserved for this purpose at the board of directors' discretion. In addition, the board of directors' may reject a request for redemption, at any time. Purchases under the SRP by the Company will be limited in any calendar year to 5% of the weighted average number of shares outstanding during the prior year. Due to these limitations, the Company cannot guarantee that it will be able to accommodate all repurchase requests.

As of June 30, 2014, no shares of common stock had been repurchased or requested to be repurchased under the SRP. The Company funds repurchases from proceeds from the sale of common stock.

Distribution Reinvestment Plan

Pursuant to the DRIP, stockholders may elect to reinvest distributions by purchasing shares of common stock in lieu of receiving cash. No dealer manager fees or selling commissions are paid with respect to shares purchased pursuant to the DRIP.

9

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

Participants purchasing shares pursuant to the DRIP have the same rights and are treated in the same manner as if such shares were issued pursuant to the Offering. The board of directors may designate that certain cash or other distributions be excluded from the DRIP. The Company has the right to amend any aspect of the DRIP or terminate the DRIP with ten days’ notice to participants. Shares issued under the DRIP are recorded to equity in the balance sheet in the period distributions are declared. There have been 46,540 shares issued under the DRIP as of June 30, 2014.

Derivative Instruments

The Company may use derivative financial instruments to hedge all or a portion of the interest rate risk associated with its borrowings. Certain of the techniques used to hedge exposure to interest rate fluctuations may also be used to protect against declines in the market value of assets that result from general trends in debt markets. The principal objective of such agreements is to minimize the risks and/or costs associated with the Company’s operating and financial structure as well as to hedge specific anticipated transactions.

The Company will record all derivatives on the balance sheet at fair value. The accounting for changes in the fair value of derivatives depends on the intended use of the derivative, whether the Company has elected to designate a derivative in a hedging relationship and apply hedge accounting and whether the hedging relationship has satisfied the criteria necessary to apply hedge accounting. Derivatives designated and qualifying as a hedge of the exposure to changes in the fair value of an asset, liability, or firm commitment attributable to a particular risk, such as interest rate risk, are considered fair value hedges. Derivatives designated and qualifying as a hedge of the exposure to variability in expected future cash flows, or other types of forecasted transactions, are considered cash flow hedges. Derivatives may also be designated as hedges of the foreign currency exposure of a net investment in a foreign operation. Hedge accounting generally provides for the matching of the timing of gain or loss recognition on the hedging instrument with the recognition of the changes in the fair value of the hedged asset or liability that are attributable to the hedged risk in a fair value hedge or the earnings effect of the hedged forecasted transactions in a cash flow hedge. The Company may enter into derivative contracts that are intended to economically hedge certain of its risk, even though hedge accounting does not apply or the Company elects not to apply hedge accounting.

The accounting for subsequent changes in the fair value of these derivatives depends on whether each has been designated and qualifies for hedge accounting treatment. If the Company elects not to apply hedge accounting treatment, any changes in the fair value of these derivative instruments will be recognized immediately in gains or losses on derivative instruments in the Company's consolidated statement of operations and comprehensive income or loss. If the derivative is designated and qualifies for hedge accounting treatment, the change in the estimated fair value of the derivative is recorded in other comprehensive income or loss to the extent that it is effective. Any ineffective portion of a derivative's change in fair value will be immediately recognized in earnings.

Offering and Related Costs

Offering and related costs include all expenses incurred in connection with the Company’s Offering. Offering costs (other than selling commissions and the dealer manager fee) of the Company may be paid by the Advisor, the Dealer Manager or their affiliates on behalf of the Company. Offering costs were reclassified from deferred costs to stockholders' equity on the day the Company commenced its operations. Offering costs include all expenses incurred by the Company in connection with its Offering as of the balance sheet date presented. These costs include but are not limited to (i) legal, accounting, printing, mailing and filing fees; (ii) escrow service related fees; (iii) reimbursement of the Dealer Manager for amounts it may pay to reimburse the bona fide diligence expenses of broker-dealers; and (iv) reimbursement to the Advisor for a portion of the costs of its employees and other costs in connection with preparing supplemental sales materials and related offering activities. The Company is obligated to reimburse the Advisor or its affiliates, as applicable, for organizational and offering costs paid by them on behalf of the Company, notwithstanding that the Advisor is obligated to reimburse the Company to the extent organizational and offering costs (excluding selling commissions and the dealer manager fee) incurred by the Company in the Offering exceed 2% of gross offering proceeds. As a result, these costs are only a liability of the Company to the extent aggregate selling commissions, the dealer manager fees and other offering costs do not exceed 12% of the gross Offering proceeds determined at the end of the Offering (See Note 9 - Related Party Transactions and Arrangements).

Share-Based Compensation

The Company has a share-based incentive award plan which is accounted for under the guidance for share-based payments. The expense for such awards will be included in board expenses and will be recognized over the vesting period or when the requirements for exercise of the award have been met (See Note 11 - Share-Based Compensation).

Income Taxes

10

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

The Company conducts its operations to qualify as a REIT for U.S. federal income tax purposes beginning with its tax return for the taxable year ended December 31, 2013. If the Company qualifies for taxation as a REIT, it generally will not be subject to federal corporate income tax as long as it distributes at least 90% of its REIT taxable income to its stockholders. REITs are subject to a number of other organizational and operational requirements. However, even if the Company qualifies for taxation as a REIT, it may be subject to certain state and local taxes on its income and property, and federal income and excise taxes on its undistributed income.

Per Share Data

The Company calculates basic earnings per share by dividing net income attributable to the Company for the period by the weighted-average number of shares of common stock outstanding for that period. Diluted earnings per share reflects the potential dilution that that could occur from shares issuable in connection with the restricted stock plan and OP units, except when doing so would be anti-dilutive.

Reportable Segments

The Company conducts its business through the following segments:

• | The real estate debt business which is focused on originating, acquiring and asset managing commercial real estate debt investments, including first mortgage loans, subordinate mortgages, mezzanine loans and participations in such loans. |

• | The real estate securities business which is focused on investing in and asset managing commercial real estate securities primarily consisting of CMBS and may include unsecured REIT debt, CDO notes and other securities. |

See Note 14 - Segment Reporting for further information regarding the Company's segments.

Note 3 - Loans Receivable

The following table is a summary of the Company's loans receivable by class (in thousands):

June 30, 2014 | December 31, 2013 | ||||||

Mezzanine loans | $ | 102,631 | $ | 30,832 | |||

Subordinated loans | 15,431 | — | |||||

Senior loans | 23,613 | — | |||||

Total gross carrying value of loans | 141,675 | 30,832 | |||||

Provision for loan losses | 128 | — | |||||

Total loans receivable, net | $ | 141,547 | $ | 30,832 | |||

As of June 30, 2014, the Company has invested approximately $141.7 million in seventeen loan investments. For the six months ended June 30, 2014 the Company received scheduled principal repayments of $72,584 on the loans.

The Company currently estimates loss rates based on historical realized losses experienced in the industry and takes into account current collateral and economic conditions affecting the probability or severity of losses when establishing the allowance for loan losses. The Company recorded a general allowance for loan losses as of June 30, 2014 in the amount of $127,600. There are no impaired or specifically reserved loans in the portfolio as of June 30, 2014.

The following table presents the activity in the Company's provision for loan losses (in thousands):

Provision for loan losses at January 1, 2014 | $ | — | |

Provision for loan losses | 128 | ||

Charge-offs | — | ||

Recoveries | — | ||

Provision for loan losses at June 30, 2014 | $ | 128 | |

11

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

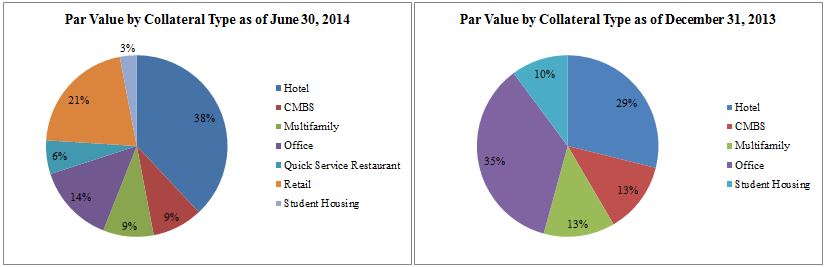

The Company's loans receivable portfolio was comprised of the following at June 30, 2014 (in thousands):

__________________________________________________________

Description | Location | Date of Investment | Maturity Date | Coupon | Original Face Amount | Face Amount | Premium (Discount)(1) | Carrying Value | ||||||||||||||||

W Hotel | Minneapolis, MN | May 2013 | May 2023 | Fixed | $ | 6,500 | $ | 6,410 | $ | (2,353 | ) | $ | 4,057 | |||||||||||

Regency Park Apartments | Austin, TX | September 2013 | September 2018 | Fixed | 5,000 | 5,000 | 48 | 5,048 | ||||||||||||||||

121 West Trade Office | Charlotte, NC | September 2013 | September 2016 | Floating | 9,000 | 9,000 | 67 | 9,067 | ||||||||||||||||

545 Madison Avenue | New York, NY | December 2013 | January 2024 | Fixed | 5,000 | 5,000 | 73 | 5,073 | ||||||||||||||||

Hampton Inn LaGuardia | East Elmhurst, NY | December 2013 | August 2023 | Fixed | 4,981 | 4,951 | (1,386 | ) | 3,565 | |||||||||||||||

Southern US Student Housing | Various | December 2013 | January 2024 | Fixed | 4,000 | 4,000 | 58 | 4,058 | ||||||||||||||||

Burger King Portfolio | Various | March 2014 | March 2024 | Fixed | 10,000 | 10,000 | (5 | ) | 9,995 | |||||||||||||||

Four Seasons Las Colinas | Irving, TX | March 2014 | March 2016 | Floating | 11,000 | 11,000 | 42 | 11,042 | ||||||||||||||||

Element Hotel | Irving, TX | March 2014 | August 2018 | Fixed | 3,000 | 3,000 | 22 | 3,022 | ||||||||||||||||

Green Hills Corporate Center | Reading, PA | April 2014 | May 2019 | Fixed | 7,000 | 7,000 | 34 | 7,034 | ||||||||||||||||

Cardinal Portfolio | Various | May 2014 | November 2016 | Floating | 5,410 | 5,410 | 26 | 5,436 | ||||||||||||||||

4550 Van Nuys Boulevard | Sherman Oaks, CA | May 2014 | June 2017 | Floating | 11,450 | 11,450 | (75 | ) | 11,375 | |||||||||||||||

Pinnacle at Encino Commons | San Antonio, TX | June 2014 | June 2024 | Fixed | 1,963 | 1,964 | 10 | 1,974 | ||||||||||||||||

Riverwalk II | Buffalo Grove, IL | June 2014 | May 2016 | Floating | 10,000 | 10,000 | 24 | 10,024 | ||||||||||||||||

Remington Apartments | Victoria, TX | June 2014 | July 2024 | Fixed | 3,480 | 3,480 | 17 | 3,497 | ||||||||||||||||

KinderCare Portfolio | Various | June 2014 | July 2016 | Floating | 12,300 | 12,300 | (62 | ) | 12,238 | |||||||||||||||

Fairmont Hotel | San Francisco, CA | June 2014 | June 2016 | Floating | 35,000 | 35,000 | 170 | 35,170 | ||||||||||||||||

Total | $ | 145,084 | $ | 144,965 | $ | (3,290 | ) | $ | 141,675 | |||||||||||||||

(1) Includes acquisition fees and expenses where applicable.

Credit Characteristics

As part of the Company's process for monitoring the credit quality of its loans, it performs a quarterly loan portfolio assessment and assigns risk ratings to each of its performing loans. The loans are scored on a scale of 1 to 5 as follows:

Investment Rating Summary Description

1 | Investment exceeding fundamental performance expectations and/or capital gain expected. Trends and risk factors since time of investment are favorable. |

2 | Performing consistent with expectations and a full return of principal and interest expected. Trends and risk factors are neutral to favorable. |

3 | Performing investments requiring closer monitoring. Trends and risk factors show some deterioration. |

4 | Underperforming investment with some loss of interest or dividend expected, but still expecting a positive return on investment. Trends and risk factors are negative. |

5 | Underperforming investment with expected loss of interest and some principal. |

12

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

All investments are assigned an initial risk rating of 2. As of June 30, 2014, the weighted average risk rating of loans was 2.0. As of June 30, 2014, the Company had no non-performing, non-accrual or impaired loans.

For the six months ended June 30, 2014, the activity in the Company's loan portfolio was as follows (in thousands):

Balance at December 31, 2013 | $ | 30,832 | |

Acquisitions and originations | 110,810 | ||

Principal repayments | (73 | ) | |

Discount accretion and premium amortization | 106 | ||

Provision for loan losses | (128 | ) | |

Balance at June 30, 2014 | $ | 141,547 | |

During the six months ended June 30, 2014, the Company invested approximately $110.8 million in eleven loans including $0.6 million of capitalized acquisition expenses.

Note 4 - Investment Securities

The following is a summary of the Company's investment securities by class (in thousands):

June 30, 2014 | December 31, 2013 | ||||||

CMBS | $ | 14,518 | $ | 5,005 | |||

Total fair value of investment securities | $ | 14,518 | $ | 5,005 | |||

As of June 30, 2014, the Company had three CMBS investments with a par value of approximately $14.5 million.

The Company classified its CMBS investments as available-for-sale as of June 30, 2014. These investments are reported at fair value in the balance sheet with changes in fair value recorded in accumulated other comprehensive income or loss. The table below represents the fair value adjustment as described above (in thousands):

As of June 30, 2014 | |||||||||||||||||||

Amortized Cost | Unrealized Gains | Unrealized Losses | Net Fair Value Adjustment | Fair Value | |||||||||||||||

CMBS | $ | 14,508 | $ | 17 | $ | (7 | ) | $ | 10 | $ | 14,518 | ||||||||

Total | $ | 14,508 | $ | 17 | $ | (7 | ) | $ | 10 | $ | 14,518 | ||||||||

Note 5 - Debt

Revolving Line of Credit with Affiliate

On May 15, 2013, the Company entered into the Revolver which provides an unsecured $5.0 million line of credit. The Revolver bears interest at a per annum fixed rate of 3.25% and provides for quarterly interest payments. The Revolver matures in 1 year, subject to two successive extension terms by the Company of one year each. Principal may be drawn or repaid from time-to-time, in whole or in part, without premium or penalty and there are no unused facility fees. On July 17, 2013, the Company entered into an amendment to its Revolver. The amendment increased the aggregate financing available under the Revolver from $5.0 million to $10.0 million. The amendment did not change any of the other terms of the Revolver.

The Company did not exercise the extension options provided under the terms of the Revolver and allowed it to mature on May 15, 2014. The Company did not have an outstanding balance on the date of maturity. The Company incurred $7,468 and $16,881 in interest expense on the Revolver for the three and six months ended June 30, 2014, respectively. The Company incurred $7,987 of interest expense on the Revolver for the three and six months ended June 30, 2013, respectively.

Revolving Line of Credit

On June 18, 2014, the Company entered into the JPM Repo Facility. The JPM Repo Facility provides up to $150.0 million in advances, subject to adjustment, which the Company expects to use to finance the acquisition or origination of eligible loans, including first mortgage loans, junior mortgage loans, mezzanine loans, and participation interests therein. The initial maturity date of the JPM Repo Facility is June 18, 2016, with a one-year extension at the Company’s option, which may be exercised upon the satisfaction of certain conditions. The JPM Repo Facility acts in the manner of a revolving credit facility that can be

13

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

repaid as the Company’s assets are paid off and re-drawn with advances against new assets. The Company incurred no interest expense on the JPM Repo Facility for the three and six months ended June 30, 2013, respectively.

As of June 30, 2014, the Company had $17.7 million outstanding under the JPM Repo Facility. Advances under the JPM Repo Facility accrue interest at per annum rates equal to the sum of (i) the applicable LIBOR index rate plus (ii) a margin of between 2.25% to 4.50%, depending on the attributes of the purchased assets. As of June 30, 2014, the weighted average interest rate on advances was 4.653%. The Company incurred $24,693 in interest expense on the JPM Repo Facility for the three and six months ended June 30, 2014, respectively.

Repurchase Agreement

On January 2, 2014, the Company entered into the MRA with JPM. The MRA provides the Company with the ability to sell securities to JPM for liquidity while providing a fixed repurchase price for the same securities in the future.

As of June 30, 2014, the Company had $11.6 million outstanding under the MRA. The repurchase contracts on each security under the MRA mature monthly and terms are adjusted for current market rates as necessary. As of June 30, 2014, the weighted average interest rate on repurchase agreements in place was 1.368%. The Company incurred $31,482 and $43,106 in interest expense on the MRA for the three and six months ended June 30, 2014, respectively. The Company incurred no interest expense on the MRA for the three and six months ended June 30, 2013, respectively.

Note 6 - Net Income or Loss Per Share

The following table is a summary of the basic and diluted net income or loss per share computation for the three and six months ended June 30, 2014 and June 30, 2013, respectively:

Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||

2014 | 2013 | 2014 | 2013 | ||||||||||||

Basic and diluted net income (loss) | $ | 585,037 | $ | (140,132 | ) | $ | 810,823 | $ | (145,151 | ) | |||||

Basic weighted average shares outstanding | 4,251,401 | 101,990 | 3,144,815 | 101,990 | |||||||||||

Diluted weighted average shares outstanding | 4,256,985 | 101,990 | 3,149,657 | 101,990 | |||||||||||

Basic net income (loss) per share | $ | 0.14 | $ | (1.37 | ) | $ | 0.26 | $ | (1.42 | ) | |||||

Diluted net income per share | $ | 0.14 | $ | (1.37 | ) | $ | 0.26 | $ | (1.42 | ) | |||||

The Company had 8,088 common share equivalents as of June 30, 2014, which was comprised of 7,198 unvested restricted shares, 800 vested restricted shares and 90 OP units. Diluted net income per share assumes the conversion of all common share equivalents into an equivalent number of common shares, unless the effect is antidilutive. The common share equivalents were dilutive by $0.000396 per share for the six months ended June 30, 2014. The common share equivalents were antidilutive for the six months ended June 30, 2013.

Note 7 - Common Stock

As of June 30, 2014, the Company had approximately 6.0 million shares of common stock outstanding, including shares issued pursuant to the DRIP and unvested restricted shares, and had received total proceeds of approximately $146.4 million excluding shares issued pursuant to the DRIP and share-based compensation.

Distributions

In order to maintain its election to qualify as a REIT, the Company must currently distribute, at a minimum, an amount equal to 90% of its taxable income, without regard to the deduction for distributions paid and excluding net capital gains. The Company must distribute 100% of its taxable income (including net capital gains) to avoid paying corporate federal income taxes.

On May 13, 2013, the Company's board of directors authorized, and the Company declared a distribution, which is calculated based on stockholders of record each day during the applicable period at a rate of $0.00565068493 per day, based on a price of $25.00 per share of common stock. The Company's distributions are payable by the fifth day following each month end to stockholders of record at the close of business each day during the prior month. The first distribution payment was made on June 3, 2013, relating to the period from May 30, 2013 (15 days after the date of the first asset acquisition) through May 31, 2013. Distributions payments are dependent on the availability of funds. The board of directors may reduce the amount of distributions paid or suspend distribution payments at any time and therefore distributions payments are not assured.

14

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

The below table shows the distributions paid during the six months ended June 30, 2014.

__________________________________________________________________________

Payment Date | Weighted Average Shares Outstanding (1) | Amount Paid in Cash | Amount Issued under DRIP | ||||||||

January 2, 2014 | 1,458,470 | $ | 140,164 | $ | 73,844 | ||||||

February 3, 2014 | 1,973,014 | 170,660 | 85,496 | ||||||||

March 3, 2014 | 2,693,391 | 212,011 | 106,181 | ||||||||

April 1, 2014 | 3,273,194 | 304,405 | 162,723 | ||||||||

May 1, 2014 | 4,121,621 | 352,798 | 206,061 | ||||||||

June 2, 2014 | 5,363,713 | 451,155 | 282,056 | ||||||||

Total | $ | 1,631,193 | $ | 916,361 | |||||||

(1) This represents the weighted average shares outstanding for the period related to the respective payment date.

For the six months ended June 30, 2014, the Company paid cash distributions of $1,631,193 and had net income of $810,823. As of June 30, 2014, the Company had a distribution payable of $925,863 for distributions accrued in the month of June 2014 and an additional distribution payable of $2,733 accrued for the six months ended June 30, 2014 on all unvested restricted shares.

Note 8 - Commitments and Contingencies

Litigation

In the ordinary course of business, the Company may become subject to litigation or claims. There are no material legal proceedings pending or known to be contemplated against the Company.

Note 9 - Related Party Transactions and Arrangements

As of June 30, 2014, an entity wholly owned by the Sponsor owned 8,888 shares of the Company’s outstanding common stock.

The Company entered into the Revolver with an affiliate on May 15, 2013 (See Note 5 - Debt). The Company did not exercise the extension option provided under the terms of the Revolver and allowed it to mature on May 15, 2014. The Company did not have an outstanding balance on the date of maturity.

Fees Paid in Connection with the Offering

The Dealer Manager receives fees and compensation in connection with the sale of the Company’s common stock in the Offering. The Dealer Manager receives a selling commission of up to 7.0% of the per share purchase price of the Company's offering proceeds before reallowance of commissions earned by participating broker-dealers. In addition, the Dealer Manager receives up to 3.0% of the gross proceeds from the sale of shares, before reallowance to participating broker-dealers, as a dealer manager fee. The Dealer Manager may reallow its dealer manager fee to such participating broker-dealers. A participating broker-dealer may elect to receive a fee equal to 7.5% of the gross proceeds from the sale of shares (not including selling commissions and dealer manager fees) by such participating broker-dealer, with 2.5% thereof paid at the time of such sale and 1.0% thereof paid on each anniversary of the closing of such sale up to and including the fifth anniversary of the closing of such sale. If this option is elected, the dealer manager fee will be reduced to 2.5% of gross proceeds (not including selling commissions and dealer manager fees).

The table below shows the fees incurred from the Dealer Manager associated with the Offering during the three and six months ended June 30, 2014 and 2013, respectively, and the associated payable as of June 30, 2014 and December 31, 2013 (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | Payable as of | ||||||||||||||||||||||

2014 | 2013 | 2014 | 2013 | June 30, 2014 | December 31, 2013 | |||||||||||||||||||

Total commissions and fees incurred from the Dealer Manager | $ | 6,976 | $ | 20 | $ | 10,827 | $ | 20 | $ | 119 | $ | 12 | ||||||||||||

15

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

The Advisor, its affiliates and entities under common control with the Advisor receive compensation and reimbursement for services relating to the Offering, including transfer agency services provided by an affiliate of the Dealer Manager. The table below shows compensation and reimbursement the Advisor and its affiliates incurred for services relating to the Offering during the three and six months ended June 30, 2014 and 2013, respectively, and the associated payable as of June 30, 2014 and December 31, 2013 (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | Payable as of | ||||||||||||||||||||||

2014 | 2013 | 2014 | 2013 | June 30, 2014 | December 31, 2013 | |||||||||||||||||||

Total compensation and reimbursement for services provided by the Advisor and affiliates | $ | 450 | $ | 191 | $ | 811 | $ | 635 | $ | 1,338 | $ | 1,047 | ||||||||||||

The payables as of June 30, 2014 and December 31, 2013 in the table above are included in accounts payable and accrued expenses on the Company's consolidated balance sheets.

The Company is responsible for organizational and offering costs from the ongoing Offering, excluding commissions and dealer manager fees, up to a maximum of 2.0% of gross proceeds received from its ongoing Offering of common stock, measured at the end of the Offering. Organizational and offering costs in excess of the 2.0% cap as of the end of the Offering are the Advisor's responsibility. As of June 30, 2014, organizational and offering costs exceeded 2.0% of gross proceeds received from the Offering by $1.7 million, due to the ongoing nature of the Offering and that many expenses were paid before the Offering commenced.

Fees Paid in Connection with the Operations of the Company

The Advisor receives an acquisition fee of 1.0% of the principal amount funded by the Company to acquire or originate commercial real estate debt or the amount invested in the case of other commercial real estate investments. The Advisor may be also be reimbursed for acquisition expenses incurred related to selecting, evaluating, originating and acquiring investments on the Company's behalf and the Company may incur third party acquisition expenses. In no event will the total of all acquisition fees and expenses payable exceed 4.5% of the principal amount funded with respect to a particular investment or exceed 1.5% of the total principal amount funded, cumulatively on all investments, after the Company has completed the Offering. During the three and six months ended June 30, 2014, the acquisition fees of $0.9 million and $1.1 million have been recognized in the consolidated statement of operations. In addition, over the same periods, the Company capitalized $0.4 million and $0.6 million of acquisition expenses, which will be amortized over the life of each investment using the effective interest method. During the three and six months ended June 30, 2013, the acquisition fees and expenses of $58,743 were capitalized and are being amortized over the life of each investment using the effective interest method.

The Company will pay the Advisor an annual asset management fee equal to 0.75% of the cost of the Company's assets. Upon reaching the NAV Pricing Date, the asset management fee will be based on the lower of 0.75% of the costs of the Company's assets and 0.75% of the quarterly NAV. The amount of the asset management fee will be reduced to the extent that the amount of distributions declared during the six month period ending on the last day of the calendar quarter immediately preceding the date such asset management fee is payable, exceeds the funds from operations (“FFO”), as adjusted, for the same period. For purposes of this determination, FFO, as adjusted, is FFO before deducting (i) acquisition fees and related expenses; (ii) non-cash restricted stock grant amortization, if any; and (iii) impairments of real estate related investments, if any (including loans receivable and other debt investments). FFO, as adjusted, is not the same as FFO. During the three and six months ended June 30, 2014 and June 30, 2013, no asset management fees were incurred or waived.

Effective June 1, 2013, the Company entered into an agreement with the Dealer Manager to provide strategic advisory services and investment banking services required in the ordinary course of the Company's business, such as performing financial analysis, evaluating publicly traded comparable companies and assisting in developing a portfolio composition strategy, a capitalization structure to optimize future liquidity options and structuring operations. The Company amortizes the cost of $0.9 million associated with this agreement into "Other expense" on the consolidated statements of operations over the estimated remaining life of the Offering.

The table below depicts related party fees and reimbursements in connection with the operations of the Company for the three and six months ended June 30, 2014 and 2013, respectively, and the associated payable as of June 30, 2014 and

16

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

December 31, 2013 (in thousands):

Three Months Ended June 30, | Six Months Ended June 30, | Payable as of | ||||||||||||||||||||||

2014 | 2013 | 2014 | 2013 | June 30, 2014 | December 31, 2013 | |||||||||||||||||||

Acquisition fees and expenses | $ | 1,295 | $ | 59 | $ | 1,692 | $ | 59 | $ | 708 | $ | 202 | ||||||||||||

Advisory and investment banking fee | 135 | 38 | 271 | 38 | — | 316 | ||||||||||||||||||

Total related party fees and reimbursements | $ | 1,430 | $ | 97 | $ | 1,963 | $ | 97 | $ | 708 | $ | 518 | ||||||||||||

The payables as of June 30, 2014 and December 31, 2013 in the table above are included in accounts payable and accrued expenses on the Company's consolidated balance sheets.

In order to improve operating cash flows and the ability to pay distributions from operating cash flows, the Advisor may elect to waive certain fees. Because the Advisor may waive certain fees, cash flows from operations that would have been paid to the Advisor may be available to pay distributions to stockholders. The fees that may be forgiven are not deferrals and accordingly, will not be paid to the Advisor in cash. The Advisor did not waive any fees during the three and six months ended June 30, 2014 or 2013, respectively. In certain instances, to improve the Company’s working capital, the Advisor may elect to absorb a portion of the Company’s costs. The Advisor did not absorb any expenses during the three and six months ended June 30, 2014 or 2013, respectively.

The Company will reimburse the Advisor’s costs of providing administrative services, subject to the limitation that the Company will not reimburse the Advisor for any amount by which the Company's operating expenses (including the asset management fee) at the end of the four preceding fiscal quarters exceeds the greater of (i) 2.0% of average invested assets or (ii) 25.0% of net income other than any additions to reserves for depreciation, bad debt or other similar non-cash reserves and excluding any gain from the sale of assets for that period. Additionally, the Company will reimburse the Advisor for personnel costs in connection with other services during the operational stage, in addition to paying an asset management fee; however, the Company will not reimburse the Advisor for personnel costs in connection with services for which the Advisor receives acquisition fees or disposition fees. For the three and six months ended June 30, 2014 and 2013, no administrative costs of the Advisor were reimbursed for any period in connection with the operations of the Company.

The Advisor at its election may also contribute capital to enhance the Company’s cash position for working capital and distribution purposes. Any contributed capital amounts are not reimbursable to the Advisor. Further, any capital contributions are made without any corresponding issuance of common or preferred shares. The Advisor did not contribute capital to enhance the Company's cash position for working capital or distribution purposes during the six months ended June 30, 2014 and 2013.

Fees Paid in Connection with the Liquidation of Assets or Listing of the Company's Common Stock or Termination of the Advisory Agreement

The Company will pay a disposition fee of 1.0% of the contract sales price of each commercial real estate loan or other investment sold, including mortgage-backed securities or collateralized debt obligations issued by a subsidiary of the Company as part of a securitization transaction. The Company will not be obligated to pay a disposition fee upon the maturity, prepayment, workout, modification or extension of commercial real estate debt unless there is a corresponding fee paid by the borrower, in which case the disposition fee will be the lesser of (i) 1.0% of the principal amount of the debt prior to such transaction; or (ii) the amount of the fee paid by the borrower in connection with such transaction. If the Company takes ownership of a property as a result of a workout or foreclosure of a loan, it will pay a disposition fee upon the sale of such property.

The Company may pay the Advisor an annual subordinated performance fee of 15.0% of the excess of the Company's total return to stockholders in any year, which such total return exceeds 6.0% per annum, provided that in no event will the annual subordinated performance fee exceed 10.0% of the aggregate total return for such year. This fee will be payable only upon the sale of assets, distributions or other event which results in the return on stockholders’ capital exceeding 6.0% per annum.

If the Company is not listed on an exchange, the Company will pay a subordinated participation in the net sale proceeds of the sale of real estate assets of 15.0% of remaining net sale proceeds after return of capital contributions to investors plus payment to investors of a 6.0% cumulative, pre-tax non-compounded return on the capital contributed by investors.

If the Company is listed on an exchange, the Company will pay a subordinated incentive listing distribution of 15.0% of the amount by which the adjusted market value of real estate assets plus distributions exceeding the aggregate capital

17

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

contributed by investors plus an amount equal to a 6.0% cumulative, pre-tax, non-compounded annual return to investors. Neither the Advisor nor any of its affiliates can earn both the subordinated participation in the net sale proceeds and the subordinated listing distribution.

Upon termination or non-renewal of the advisory agreement, the Advisor shall be entitled to receive distributions from the OP, pursuant to a special limited partnership interest, equal to 15.0% of the amount by which the sum of the Company's adjusted market value plus distributions exceeds the sum of the aggregate capital contributed by investors plus an amount equal to an annual 6.0% cumulative, pre-tax non-compounded return to investors. In addition, the Advisor may elect to defer its right to receive a subordinated distribution upon termination until either a listing on a national securities exchange or other liquidity event occurs.

During the three and six months ended June 30, 2014 and 2013, no fees were paid for any period in connection with the liquidation of assets, listing of the Company's common stock or termination of the advisory agreement.

The Company cannot assure that it will provide the 6.0% return specified above, but the Advisor will not be entitled to the subordinated performance fee, subordinated participation in net sale proceeds, subordinated incentive listing distribution or subordinated distribution upon termination of the advisory agreement unless investors have received a 6.0% cumulative, pre-tax non-compounded return on their capital contributions.

The Company has also established a restricted share plan for the benefit of employees (if the Company ever has employees), directors, employees of the Advisor and its affiliates (See Note 11 - Share-Based Compensation).

Note 10 - Economic Dependency

Under various agreements, the Company has engaged the Advisor, its affiliates and entities under common control with the Advisor to provide certain services that are essential to the Company, including asset management services, asset acquisition and disposition decisions, transfer agency services, the sale of shares of the Company’s common stock available for issue, as well as other administrative responsibilities for the Company including accounting services, transaction management and investor relations.

As a result of these relationships, the Company is dependent upon the Advisor and its affiliates. In the event that these entities are unable to provide the Company with the respective services, the Company will be required to find alternative providers of these services.

Note 11 - Share-Based Compensation

Restricted Share Plan

The Company has an employee and director incentive restricted share plan (the “RSP”), which provides the Company with the ability to grant awards of restricted shares to the Company’s directors, officers and employees (if the Company ever has employees), employees of the Advisor and its affiliates, employees of entities that provide services to the Company, directors of the Advisor or of entities that provide services to the Company or certain consultants to the Company and the Advisor and its affiliates. The total number of common shares granted under the RSP shall not exceed 5.0% of the Company’s authorized common shares pursuant to the Offering and in any event will not exceed 4.0 million shares (as such number may be adjusted for stock splits, stock distributions, combinations and similar events).

Restricted share awards entitle the recipient to receive common shares from the Company under terms that provide for vesting over a specified period of time or upon attainment of pre-established performance objectives. Such awards would typically be forfeited with respect to the unvested shares upon the termination of the recipient’s employment or other relationship with the Company. Restricted shares may not, in general, be sold or otherwise transferred until restrictions are removed and the shares have vested. Holders of restricted shares may receive cash distributions prior to the time that the restrictions on the restricted shares have lapsed. Any distributions payable in common shares shall be subject to the same restrictions as the underlying restricted shares. The fair value of the restricted shares will be expensed over the vesting period of five years.

The RSP also provides for the automatic grant of 1,333 restricted shares of common stock to each of the independent directors, without any further action by the Company’s board of directors or the stockholders, on the date of initial election to the board of directors and on the date of each annual stockholder’s meeting. Restricted stock issued to independent directors will vest over a five-year period with 20.0% of the granted shares vesting upon each of the first, second, third, fourth and fifth anniversaries of the applicable grant date.

18

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)

As of June 30, 2014, the Company had granted 7,998 restricted shares to its independent directors. Which were comprised of 7,198 unvested restricted shares and 800 vested restricted shares as of June 30, 2014. Based on a share price of $22.50, the compensation expense associated with the restricted share grants was $6,114 and $10,551, for the three and six months ended June 30, 2014. For the three and six months ended June 30, 2013, the compensation expense associated with the restricted share grants was $6,804.

Other Share-Based Compensation

The Company may issue common stock in lieu of cash to pay fees earned by the Company's directors at each director's election. There are no restrictions on the shares issued since these payments in lieu of cash relate to fees earned for services performed. During the three and six months ended June 30, 2014, 39 shares were issued to one of the Company's independent directors for services performed and compensation expense of $876 was incurred.

Note 12 - Fair Value of Financial Instruments

GAAP establishes a hierarchy of valuation techniques based on the observability of inputs utilized in measuring financial instruments at fair values. GAAP establishes market-based or observable inputs as the preferred source of values, followed by valuation models using management assumptions in the absence of market inputs. The three levels of the hierarchy are described below:

• | Level I - Inputs are unadjusted, quoted prices in active markets for identical assets or liabilities at the measurement date. |

• | Level II - Inputs (other than quoted prices included in Level I) are either directly or indirectly observable for the asset or liability through correlation with market data at the measurement date and for the duration of the instrument’s anticipated life. |

• | Level III - Inputs reflect management’s best estimate of what market participants would use in pricing the asset or liability at the measurement date. Consideration is given to the risk inherent in the valuation technique and the risk inherent in the inputs to the model. |

The determination of where an asset or liability falls in the above hierarchy requires significant judgment and factors specific to the asset or liability. In instances where the determination of the fair value measurement is based on inputs from different levels of the fair value hierarchy, the level in the fair value hierarchy within which the entire fair value measurement falls is based on the lowest level input that is significant to the fair value measurement in its entirety. The Company evaluates its hierarchy disclosures each quarter and depending on various factors, it is possible that an asset or liability may be classified differently from quarter to quarter.

The Company has implemented valuation control processes to validate the fair value of the Company's financial instruments measured at fair value including those derived from pricing models. These control processes are designed to assure that the values used for financial reporting are based on observable inputs wherever possible. In the event that observable inputs are not available, the control processes are designed to assure that the valuation approach utilized is appropriate and consistently applied and the assumptions are reasonable. Refer to the Company's Annual Report on Form 10-K for the year ended December 31, 2013 for further discussion of the Company's valuation control process.

CMBS

CMBS investments are valued utilizing both observable and unobservable market inputs. These factors include projected future cash flows, ratings, subordination levels, vintage, remaining lives, credit issues, recent trades of similar securities and the spreads used in the prior valuation. The Company obtains current market spread information where available and uses this information in evaluating and validating the market price of all CMBS. Depending upon the significance of the fair value inputs used in determining these fair values, these securities are classified in either Level II or Level III of the fair value hierarchy. As of June 30, 2014, the Company received broker quotes on each CMBS investment used in determining the fair value. As of June 30, 2014, the Company's CMBS investments have been classified as Level II due to the observable nature of many of the market inputs.

19

ARC REALTY FINANCE TRUST, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

June 30, 2014

(Unaudited)