Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Independence Contract Drilling, Inc. | d710079dex231.htm |

| EX-23.2 - EX-23.2 - Independence Contract Drilling, Inc. | d710079dex232.htm |

Table of Contents

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON AUGUST 7, 2014

Registration No. 333-196914

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 5

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Independence Contract Drilling, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 1381 | 37-1653648 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

11601 North Galayda Street

Houston, Texas 77086

(281) 598-1230

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Philip A. Choyce

Senior Vice President and Chief Financial Officer

11601 North Galayda Street

Houston, Texas 77086

(281) 598-1230

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| David C. Buck | J. Michael Chambers | |

| Melinda Brunger | David J. Miller | |

| Andrews Kurth LLP 600 Travis Street Suite 4200 Houston, Texas 77002 |

Latham & Watkins LLP 811 Main Street, Suite 3700 Houston, Texas 77002 (713) 546-5400 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell the securities described herein until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell the securities described herein and we are not soliciting offers to buy such securities in any state where such offer or sale is not permitted.

PROSPECTUS

(Subject to Completion) Issued August 7, 2014

10,000,000 Shares

Common Stock

Independence Contract Drilling, Inc. is offering 10,000,000 shares of its common stock. This is our initial public offering and no public market currently exists for our shares. We anticipate that the initial public offering price will be between $10.00 and $11.00 per share.

Two of our affiliates, Sprott Resource Corp. and 4D Global Energy Advisors SAS, have indicated that they each intend to purchase 600,000 shares of common stock in this offering.

Our common stock has been approved for listing on the New York Stock Exchange under the symbol “ICD,” subject to official notice of issuance.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 14.

PRICE $ A SHARE

| Price to |

Underwriting and |

Proceeds to |

||||||||||

| Per Share |

$ | $ | $ | |||||||||

| Total |

$ | $ | $ | |||||||||

| (1) | We refer you to “Underwriters (Conflicts of Interest)” beginning on page 105 of this prospectus for additional information regarding underwriting compensation. |

We have granted the underwriters the right to purchase up to 1,500,000 additional shares of common stock to cover over-allotments.

The Securities and Exchange Commission and state regulators have not approved or disapproved of the securities described herein, or determined if the information contained in this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock on or about , 2014 through the book-entry facilities of The Depository Trust Company.

| Morgan Stanley | RBC Capital Markets | Tudor, Pickering, Holt & Co. |

| Canaccord Genuity | Capital One Securities | Cowen and Company |

| FBR | IBERIA Capital Partners L.L.C. | Johnson Rice & Company L.L.C. |

, 2014

Table of Contents

Table of Contents

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by us or on behalf of us or to the information which we have referred you. Neither we nor the underwriters have authorized anyone to provide you with information different from that contained in this prospectus and any free writing prospectus. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the underwriters are offering to sell shares of common stock and seeking offers to buy shares of common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of any sale of the common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements.”

Until , 2014 (25 days after the commencement of our initial public offering), all dealers that buy, sell, or trade shares of our common stock, whether or not participating in our initial public offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

i

Table of Contents

Industry and Market Data

The market data and certain other statistical information used throughout this prospectus are based on independent industry publications, government publications and other published independent sources. Although we believe these third-party sources are reliable as of their respective dates, neither we nor the underwriters have independently verified the accuracy or completeness of this information. Some data is also based on our good faith estimates. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these publications.

Trademarks and Trade Names

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this prospectus is not intended to, and does not imply, a relationship with, or endorsement or sponsorship by us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names.

ii

Table of Contents

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully before making an investment decision, including the information included under the headings “Risk Factors,” “Cautionary Statement Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical financial statements and the notes to those financial statements appearing elsewhere in this prospectus. Unless otherwise indicated, all numbers of shares and per share amounts give effect to a 1.57-for-1 stock split in the form of a stock dividend on July 24, 2014. The information presented in this prospectus, unless otherwise indicated, assumes that the underwriters do not exercise their option to purchase additional shares of common stock.

Except as expressly stated or the context otherwise requires, the terms “we,” “us,” “our,” the “company,” “Successor” and “ICD” refer to Independence Contract Drilling, Inc., and the terms “GES,” “Predecessor” or “our predecessor” refer to Global Energy Services Operating, LLC. We currently have no subsidiaries.

This prospectus includes certain terms commonly used in the oil and natural gas drilling industry, which are defined elsewhere in Annex A to this prospectus.

Our Company

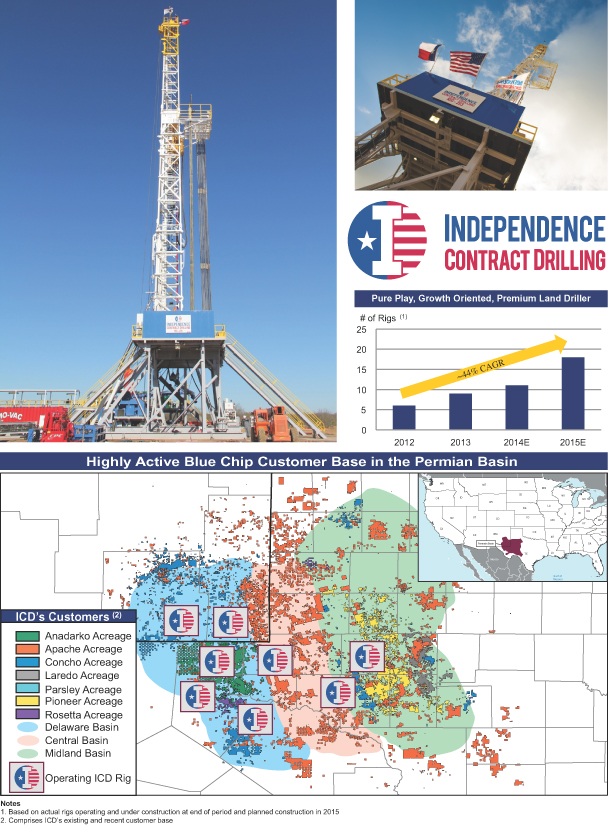

We provide land-based contract drilling services for oil and natural gas producers targeting unconventional resource plays in the United States. We construct, own and operate a premium fleet comprised entirely of newly constructed, technologically advanced, custom designed ShaleDriller™ rigs that are specifically engineered and designed to optimize the development of our customers’ most technically demanding oil and gas properties. All of our operating rigs are currently drilling in the Permian Basin, but our rigs have previously operated in the Mid-Continent region and Eagle Ford Shale. We are focused on creating stockholder and customer value through our commitment to operational excellence and our focus on safety. We believe that we are strategically positioned to take advantage of the ongoing land-rig replacement cycle as the industry upgrades legacy fleets with premium rigs. We believe we will be able to expand our fleet and grow our business due to the shortage of the type of premium rigs and drilling services that we provide.

Our standardized fleet currently consists of eleven premium rigs. Of these eleven rigs, two are currently under construction and scheduled for completion in August and November of 2014, and one is being upgraded with an integrated multi-directional walking system scheduled for completion in October 2014. After this upgrade, nine of our eleven rigs will contain our integrated multi-directional walking system that is specifically designed to optimize pad drilling for our customers. We also have the option to upgrade our two non-walking rigs after completion of their existing contracts in 2015. Every ShaleDriller™ rig in our fleet is a 1500-hp, AC programmable rig (“AC rig”) designed to be fast-moving between drilling sites and is equipped with top drives, automated tubular handling systems and blowout preventer (“BOP”) handling systems. Nine of our eleven rigs are equipped with bi-fuel capabilities (they operate on either diesel or a natural gas-diesel blend). We currently intend to use a portion of the net proceeds from this offering and available borrowing capacity under our revolving credit facility to fund the construction of up to seven additional rigs for completion in 2015.

Our first rig began drilling in May 2012 and since that time, we have averaged 96% utilization. All of our operating rigs have been contracted prior to the completion of construction, and every rig has been constructed and commenced drilling operations in accordance with our customers’ delivery requirements. All of our eleven premium rigs are currently under contract with customers, and seven of our operating rigs are currently working under contracts that represent repeat business in which our customer has either renewed the contract or contracted a second rig. Although our ShaleDriller™ rig is capable of drilling in virtually any onshore area in the U.S., we currently focus our operations on unconventional resource plays located in geographic regions that we can efficiently support from our Houston, Texas facilities in order to maximize economies of scale.

1

Table of Contents

We believe our fleet standardization gives us several benefits, including:

| • | Consistent branding to customers, who can quickly understand the capabilities of our premium rigs rather than analyzing individual rig specifications within a non-uniform fleet; |

| • | More efficient crew training, improved safety and increased flexibility for crew deployment, as most tasks and skills are transferable across the entire fleet; and |

| • | Savings from lower maintenance spending, smaller inventories of spare items and reduced parts procurement costs due to interchangeability of assets among rigs. |

Our rigs are designed to optimize drilling results in challenging geological environments and incorporate features that improve safety, increase efficiency and reduce environmental impacts. In addition to the top drives and automated tubular handling systems with which all of our rigs are equipped, we believe the following designs and features maximize the value proposition of our ShaleDriller™ rig to our customers and will increase our ability to realize higher dayrates and utilization across industry cycles:

| • | AC Programmable. AC rigs use a variable frequency drive that allows precise computer control of motor speed during operations. This greater control of motor speed provides more precise drilling of the wellbore. Among other attributes, when compared to electrical silicon-controlled rectifier (“SCR”) rigs and mechanical rigs, AC rigs are electrically more efficient, produce consistent torque, utilize regenerative braking, and have digital controls and AC motors that require less maintenance. AC rigs allow our customers to drill faster, which, in general, eliminates reservoir permeability damage, and to drill wellbores that more precisely track planned trajectories without doglegs. This, in turn, minimizes open hole time and enables our customers to more effectively and efficiently run casing, cement and successfully complete their wells. |

| • | Pad Optimized, Multi-Directional Walking System. Our multi-directional walking system is engineered and designed as an integrated part of our ShaleDriller™ rig’s substructure to optimize pad drilling economics for our customers. Pad drilling involves the drilling of multiple wells from a single location, which provides benefits to the E&P company in the form of cost savings and accelerated cash flows. Our walking system allows our rigs to move in any direction quickly between wellheads, rapidly and efficiently adjust to misaligned wellbores, walk over raised wellheads, and increase operational safety due to fewer required rig up and rig down movements. We believe the advanced features of this walking system have enabled us to achieve higher premium dayrates and utilization. |

| • | Bi-Fuel Capable. Nine of our eleven ShaleDriller™ rigs are bi-fuel capable. Bi-fuel operations can offer a reduction in carbon emissions and provide significant fuel cost savings for our customers. |

| • | Efficient Mobilization Between Drilling Sites. A rig that can rapidly move between drilling sites has become increasingly desired by, and impactful to, E&P companies because it reduces cycle times allowing them to drill more wells in the same period of time. In addition to being specifically designed for moving between wells on a pad, our ShaleDriller™ rig is designed to move rapidly on conventional rig moves between drilling sites. Our custom designed substructure moves in a single semi-trailer load and allows for automated and rapid rig up and rig down without the use of cranes. This significantly reduces overall move time compared to a traditional substructure design, provides cost savings to our customers, and enables a safer rig up and rig down process. |

| • | 1500-hp Drawworks. All of our rigs are powered with 1500-hp drawworks, which we believe are well suited for the development of the vast majority of our customers’ unconventional resource assets. Compared to a 1000-hp or smaller rig, a 1500-hp rig has superior capability to handle extended drill strength lengths required to drill long horizontal wells, which are becoming more common in our markets. |

2

Table of Contents

| • | BOP Handling Systems. Our BOP handling system allows precise control and positioning of the BOP stack via remote control and removes the handling of the BOP stack from the critical path of well operations. BOP handling systems also enable the drilling rig to walk from well to well by suspending the BOP stack from the substructure. BOP handling systems provide a safer and more efficient BOP handling operation when compared to conventional methods, which require lifting of the BOP by third party rental equipment or through use of the rig’s traveling block. |

We have assembled what we believe is a highly motivated and experienced senior management and operational team with the goal of providing the maximum value proposition to our customers through a focus on safety and operational excellence. Members of our executive management and senior operational team bring an average of over 25 years of experience in the energy sector. As of June 30, 2014, our rigs were operated by field and rig-level managers with an average of over 16 years of experience.

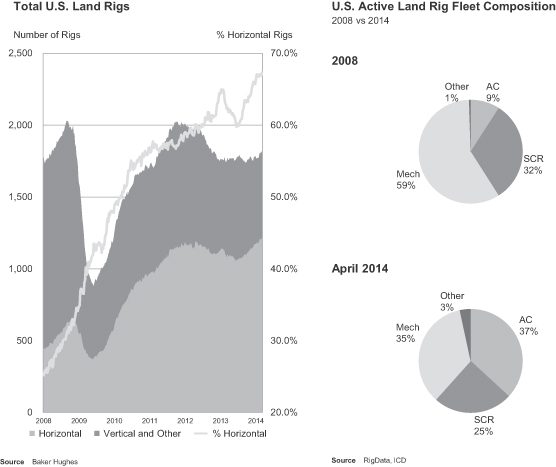

Industry Trends

Due to advances in drilling and completion techniques as well as favorable commodity prices, many E&P companies continue to invest substantial amounts of capital into onshore unconventional resource plays. As a result, land-based contract drilling providers have entered into a replacement cycle directed at replacing legacy SCR and mechanical rigs with premium rigs capable of meeting the increasing well complexity requirements of E&P companies. We believe the following industry trends have created a shortage of premium rigs and ongoing demand for our premium land-based contract drilling services:

| • | Continued increases in horizontal drilling activity; |

| • | Shift to developmental drilling; |

| • | Increased use of pad drilling; |

| • | Shift to longer lateral lengths; and |

| • | Significant investments by customers demanding operational efficiency and safety. |

Our Competitive Strengths

We believe the following competitive strengths allow us to provide our customers with an optimal value proposition:

Premium Rig Fleet with 100% High-Specification Rigs. We operate one of the newest, most technologically advanced fleets in the industry based on the percentage of our fleet meeting the specifications discussed below. All of our rigs are fast-moving, 1500-hp AC rigs. Our ShaleDriller™ rigs are capable of drilling long laterals at significant depths more quickly, safely and efficiently when compared to legacy SCR and mechanical rigs. Our rigs have drilled some of the longest horizontal wells to date in the Permian Basin, including a well with a lateral section in excess of 13,980 feet. Nine of our eleven rigs are equipped with, or being upgraded with, multi-directional walking systems capable of drilling on our customers’ most challenging pad drilling applications. We have the option to upgrade our two non-walking rigs upon completion of their existing term contracts in 2015. Utilizing the ShaleDriller’s™ multi-directional walking system, operators can complete one well, move to the next well location on a pad, and begin drilling in less than three hours. Our ShaleDriller™ rigs have successfully enabled batch drilling, and one is currently drilling on a pad designed for more than 40 wells where it has walked over 300 feet between wells. Nine of our eleven rigs are bi-fuel capable, and our two non-bi-fuel rigs can be rapidly converted to meet customer requirements. We believe a shortage remains of high-specification, AC programmable land drilling rigs like the ShaleDriller™ needed to develop unconventional resources efficiently. Since we began operations, our rig fleet has experienced overall fleet utilization of 96%, and our multi-directional walking rigs have experienced overall utilization exceeding 99%. We believe our fleet profile allows us to command premium dayrates and maintain higher fleet utilization compared to our competitors with legacy SCR and mechanical rigs, even during periods of reduced demand.

3

Table of Contents

Scalable and Cost Effective Rig Construction Process. We designed our ShaleDriller™ rig to meet the most challenging technical needs of our customers, and we oversee all aspects of its construction and branding. We construct our rigs utilizing a network, modular manufacturing process. We select key outside vendors who manufacture major components and subassemblies of our rigs to our engineering designs and specifications, with oversight by our quality assurance and control staff. Our drilling crews are intimately involved in our rig construction process. The drilling crew that will operate the rig assembles, tests and commissions the rig, rigs it down and moves with the rig to its initial drilling operation. We believe our rig construction approach provides us with several key advantages including:

| • | Control over our ShaleDriller™ brand, including control over all design and equipment changes; |

| • | Increased operational performance due to the seamless transition of our drilling rigs from construction to drilling; |

| • | Enhanced crew training and reinforcement of our culture of personal performance, accountability and teamwork as the rig crews acquire valuable knowledge of our ShaleDriller™ rig throughout the rig construction process; |

| • | The ability to stop or accelerate rig construction operations in response to market conditions without excessive financial or operational stress on us; and |

| • | Significant savings compared to costs associated with purchasing, commissioning and fully outfitting a rig from a third-party manufacturer. |

Strong Presence in Liquids-Rich Basins. All of our rigs are currently operating in the Permian Basin, which we believe provides the ideal “anchor” basin from which we can successfully grow and expand into other geographical areas. We have also operated in the Mid-Continent region and Eagle Ford Shale. We currently focus on these markets because they provide attractive economics for E&P companies, and we can support these operations logistically from our facilities in Houston, Texas. Each of these regions is experiencing growing demand for the type of premium drilling services that we provide through our technologically advanced fleet. We view the Permian Basin as an ideal “anchor” basin because of its existing infrastructure and high oil and liquids-rich natural gas content among multiple horizontal target horizons, or stacked formations, and the trend by Permian operators towards increased utilization of horizontal drilling techniques and pad drilling. We believe this production environment and the basin’s ongoing transition from SCR and mechanical rigs to more advanced and efficient rigs provides excellent growth opportunities for the utilization of our pad-optimized ShaleDriller™ rig.

Management Experience and Industry Relationships. Our management team brings a successful track record of starting and building profitable drilling, oilfield services and equipment manufacturing businesses, managing high-growth public companies, and executing successful growth and acquisition strategies. We believe this management experience and related industry relationships have provided us with credibility to targeted E&P customers with significant investments and activity in our target markets. All of our eleven premium rigs are currently under contract with customers, and seven of our operating rigs are currently working under contracts that represent repeat business in which our customer has either renewed the contract or contracted a second rig.

Strong Balance Sheet with Financial Flexibility. As of March 31, 2014, on an as adjusted basis after giving effect to this offering and use of proceeds, we would have cash on hand of approximately $65.2 million and $78.8 million in availability under our $125 million revolving credit facility. We believe the cash on our balance sheet, cash flows from operations and borrowing capacity under our revolving credit facility will be sufficient to fund our near-term growth plan and construct up to seven additional rigs for completion during 2015.

Culture of Ownership Focused on Operational Excellence and Safety. We believe that we have assembled a highly motivated, experienced team of skilled employees with a focus on safety and operational excellence. We

4

Table of Contents

believe our rig crews value the opportunity to work for a fast-growing premium contract driller under experienced leadership with new, modern drilling equipment. Our training encourages our rig crews to take ownership of their rigs beginning with their involvement in the construction process. We believe their in-depth knowledge of the rig and its capabilities allows them to immediately deliver superior value for our customers as soon as the rig begins operations in the field.

Our Business Strategy

Our principal business objectives are to profitably grow our business and increase stockholder value. We expect to achieve these objectives through the following strategies:

Continuing to Focus on Safety and Operational Efficiency. Our incentive compensation programs are designed to directly align all levels of our operations with our strategic goal of providing the highest level of service through a focus on safety and operational efficiency while maintaining a cost effective operating structure. We believe we are one of only a few land drilling contractors who have implemented a safety management system compliant with the U.S. Bureau of Safety and Environmental Enforcement’s SEMS II workplace safety rules. These workplace rules are independently developed standards applicable to offshore oil and natural gas operations in U.S. federal waters, which we believe also provide enhanced safety practices for our onshore activities. In addition, we have implemented proven training programs to enhance competency and prepare for future workforce needs. We intend to maintain and enhance our organizational culture to promote a safer work environment, and to maximize operational performance and value for our customers.

Capitalizing on Growth in Developmental Drilling in Unconventional Resource Plays. We intend to continue to focus our services in demanding unconventional resource plays with what we view as long-term development potential, where we believe our ShaleDriller™ rig and operating strategy will provide superior returns. Due to advances in drilling and completion technologies as well as favorable commodity prices, E&P companies continue to invest significant capital into onshore unconventional resource plays, which are economically more attractive relative to other domestic and international oil and natural gas opportunities. Our premium rigs’ features are specifically designed to efficiently and economically address the technical challenges posed by these and other resource plays where horizontal drilling is utilized.

Accelerating Expansion of our New-Build Rig Fleet. We believe that we are strategically positioned to take advantage of the shortage in our target markets of the type of premium rigs and contract drilling services we provide. Utilizing a portion of the proceeds from this offering, operating cash flow and borrowing capacity under our revolving credit facility, we intend to accelerate the expansion of our ShaleDriller™ rig fleet by constructing up to an additional seven rigs equipped with multi-directional walking systems for completion during 2015. Compared to our competitors, we have one of the newest, most advanced drilling fleets in our industry, and we do not own or operate any legacy drilling equipment. As a result, our advanced new-build rigs do not require costly upgrades to meet increasing customer demands in unconventional resource plays. Unlike our competitors with legacy SCR and mechanical rigs, we are not experiencing technical disruptions from the roll-out of new rigs with advanced features that we believe are reducing the utilization and profitability of legacy rigs.

Expanding Customer Relationships. We target customers who have significant investments in our target markets, who value safe and efficient operations and who have the financial stability to drill through industry cycles and enter into long-term relationships with us. We believe there is significant opportunity to gain market share by providing our customers with superior service and advanced rig capabilities. We seek to deliver the best value to our customers through our dual focus on safety and operating efficiencies. Our existing and recent customer base includes high quality, well-known operators such as Anadarko Petroleum Corporation, Apache Corporation, BOPCO, L.P., COG Operating, LLC, a subsidiary of Concho Resources Inc., Laredo Petroleum, Inc., Newfield Exploration Company, Pioneer Natural Resources USA, Inc. and Rosetta Resources Operating,

5

Table of Contents

L.P. We will seek to diversify our customer base while maintaining strong relationships with existing top-tier customers in our target markets. We seek to balance the goals of maximizing the length of our customer contracts to provide stability and visibility into our future revenues, on the one hand, and seeking to balance our desire to maximize dayrates for our advanced rig fleet, on the other hand.

Predecessor and Corporate History

We were incorporated in November 2011 but did not have meaningful operations until March 2012. In March 2012, we acquired substantially all of the rig manufacturing and related field service assets and intellectual property (the “GES assets”) of Global Energy Services Operating, LLC (“GES”), including GES’ Houston-based manufacturing facility (the “Houston Facility”), which we currently use to construct our rig fleet. The Houston Facility is located on 14.6 acres in northwest Houston. The rig intellectual property acquired by us included the detailed rig designs, drawings and technical expertise associated with the engineering and construction of an established, fast-moving AC rig, which formed the basis for the design of our multi-directional walking ShaleDriller™ rig. We also hired substantially all of GES’ employees dedicated to the acquired operations. We believe this acquisition provided us with the necessary infrastructure and asset platform required to accelerate the introduction of our ShaleDriller™ rig into our target markets and secure initial contracts with key customers. In exchange for the GES assets, we issued approximately 1.6 million shares of our common stock and a warrant to purchase approximately 2.2 million shares of our common stock (the “GES Warrant”), and we assumed approximately $2.1 million of long-term indebtedness from GES. Because we had only limited operations before the GES acquisition and we succeeded to substantially all of the ongoing operations of GES, GES is considered our predecessor for accounting purposes.

Contemporaneously with the acquisition of the GES assets, we acquired cash balances and two drilling contracts from an affiliate, Independence Contract Drilling LLC (referred to as “RigAssetCo”) in exchange for approximately 2.4 million shares of our common stock. As a condition to the completion of these two transactions, we also closed a private placement of shares of our common stock resulting in net proceeds to us of $98.4 million. We used the net proceeds of the private placement primarily to continue the construction of our ShaleDriller™ rig fleet and expansion of our operating capacity, and to repay the indebtedness assumed from GES. We refer to the GES and RigAssetCo transactions, together with the private placement of common stock, collectively as the “GES Transaction.”

Risk Factors

An investment in our common stock involves a high degree of risk. You should consider carefully all of the risks described below, together with the other information contained in this prospectus, before making a decision to invest in our common stock. If any of the following events occur, our business, results of operations, financial condition and ability to timely and successfully implement our growth strategy (including planned rig construction) may be materially adversely affected. In that event, the value of our securities could decline, and you could lose all or part of your investment.

| • | We derive all our revenues from companies in the oil and gas exploration and production industry, a historically cyclical industry with levels of activity that are significantly affected by the levels and volatility in oil and gas prices. |

| • | Our limited operating history and growth of our business make it difficult to evaluate our business. |

| • | We cannot assure you that we will timely complete the construction of our planned additional rigs in 2014 and 2015. A significant delay in the completion of their construction could materially and adversely affect our ability to execute our growth strategy. |

6

Table of Contents

| • | Our growth strategy will likely require that we commit to the construction of new drilling rigs prior to securing an executed contract for its use. The inability to secure drilling contracts for our new rigs promptly following the completion of their construction could materially and adversely affect our financial condition. |

| • | Any loss of large customers could have a material adverse effect on our financial condition and results of operations. |

| • | Six of our current drilling contracts are scheduled to terminate in 2015. We cannot assure you that each of our existing contracts will be renewed with existing customers at favorable pricing, or if terminated, that we will be able to immediately secure a new contract with a new customer. |

| • | Our operations involve operating hazards, which if not insured or indemnified against, could adversely affect our results of operations and financial condition. |

| • | We operate in a highly competitive, fragmented industry in which price competition could reduce our profitability. |

| • | We face competition from many competitors with greater resources and greater ability to rapidly respond to changing customer requirements. |

| • | New technology may cause our drilling methods or equipment to become less competitive. |

| • | Reduced demand for or excess capacity of drilling services could adversely affect our profitability. |

| • | We depend on the services of key executives, the loss of whom could materially harm our business. |

| • | We depend on a limited number of vendors, some of which are thinly capitalized and the loss of any of which could disrupt our operations. |

| • | Federal and state legislative and regulatory initiatives related to hydraulic fracturing could result in operating restrictions or delays in the completion of oil and natural gas wells that may reduce demand for our activities and could adversely affect our financial position, results of operations and cash flows. |

For a discussion of these risks and other considerations that could negatively affect us, including risks related to this offering and our common stock, see “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements.”

Emerging Growth Company

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”). For as long as we are an emerging growth company, unlike public companies that are not emerging growth companies under the JOBS Act, we are not required to:

| • | provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002; |

| • | provide audited financial statements and related management’s discussion and analysis of financial condition and results of operations for periods preceding those contained in this prospectus; |

| • | comply with any new requirements adopted by the Public Company Accounting Oversight Board (the “PCAOB”) requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer; |

7

Table of Contents

| • | provide certain disclosure regarding executive compensation required of larger public companies or hold stockholder advisory votes on executive compensation required by the Dodd-Frank Wall Street Reform and Consumer Protection Act; or |

| • | obtain stockholder approval of any golden parachute payments not previously approved. |

We will cease to be an emerging growth company upon the earliest of:

| • | the last day of the fiscal year in which we have $1.0 billion or more in annual revenues; |

| • | the date on which we become a “large accelerated filer,” as defined in Rule 12b-2 promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which generally requires more than $700 million in market value of our common units held by non-affiliates as of June 30 of the year such determination is made; |

| • | the date on which we issue more than $1.0 billion of non-convertible debt over a three-year period; or |

| • | the last day of the fiscal year following the fifth anniversary of our initial public offering. |

We may choose to take advantage of some but not all of these reduced obligations. We have availed ourselves of the reduced reporting obligations with respect to financial statements, selected financial data, management’s discussion and analysis of financial condition and results of operations and executive compensation disclosure in this prospectus and expect to continue to avail ourselves of the reduced reporting obligations available to emerging growth companies in future filings. For as long as we take advantage of the reduced reporting obligations, the information that we provide shareholders may be different than information provided by other public companies in which you hold equity interests.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”), for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies.

Principal Executive Offices and Internet Address

Our principal executive offices are located at 11601 North Galayda Street, Houston, Texas 77086, and our telephone number at that address is (281) 598-1230. Our website address is www.icdrilling.com. We expect to make our periodic reports and other information filed with or furnished to the Securities and Exchange Commission (the “SEC”) available free of charge through our website as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. The information on, or otherwise accessible through, our website or any other website does not constitute a part of this prospectus.

8

Table of Contents

The Offering

| Common stock offered by us |

10,000,000 shares. | |

| Common stock to be outstanding after our initial public offering(1) |

22,855,155 shares (or 24,355,155 shares, if the underwriters exercise in full the over-allotment option). | |

| Over-allotment option offered by us |

1,500,000 shares. | |

| Use of proceeds |

We expect to receive approximately $100.2 million of net proceeds from the sale of the common stock offered by us after deducting underwriting discounts and commissions and estimated offering expenses payable by us. | |

| We intend to use a portion of the net proceeds from this offering to repay outstanding amounts under our existing revolving credit facility. The remaining net proceeds will be used to finance the construction of additional drilling rigs and for working capital and general corporate purposes. Please read “Use of Proceeds.” | ||

| Conflicts of Interest |

A portion of the net proceeds from this offering will be used to repay borrowings under our revolving credit facility. Because affiliates of Morgan Stanley & Co. LLC and Capital One Securities, Inc. are lenders under our revolving credit facility and will each receive 5% or more of the net proceeds of this offering due to such repayment, each of Morgan Stanley & Co. LLC and Capital One Securities, Inc. are deemed to have a “conflict of interest” under Rule 5121 of the Financial Industry Regulatory Authority, Inc. (“FINRA”). As a result, this offering will be conducted in accordance with FINRA Rule 5121, which requires, among other things, that a “qualified independent underwriter” has participated in the preparation of and has exercised the standards of “due diligence” with respect to the registration statement and this prospectus. RBC Capital Markets, LLC has agreed to act as qualified independent underwriter for the offering and to undertake legal responsibilities and liabilities, of an underwriter under the Securities Act specifically including those inherent in Section 11 of the Securities Act. See “Use of Proceeds” and “Underwriters (Conflicts of Interest).” | |

| Dividend policy |

We do not anticipate paying any cash dividends on our common stock. In addition, our revolving credit facility places restrictions on our ability to pay cash dividends. Please read “Dividend Policy.” | |

9

Table of Contents

| Directed share program |

The underwriters have reserved for sale at the initial public offering price up to 5% of the common stock being offered by this prospectus for sale to our employees, executive officers, directors, director nominees, business associates and related persons who have expressed an interest in purchasing common stock in this offering. We do not know if these persons will choose to purchase all or any portion of these reserved shares, but any purchases they do make will reduce the number of shares available to the general public. Please read “Underwriters (Conflicts of Interest).” | |

| Risk factors |

You should carefully read and consider the information set forth under the heading “Risk Factors” beginning on page 14 and all other information set forth in this prospectus before deciding to invest in our common stock. | |

| Listing and trading symbol |

Our shares of common stock have been approved for listing on the New York Stock Exchange (the “NYSE”) under the symbol “ICD,” subject to official notice of issuance. | |

(1) The common stock to be outstanding after our initial public offering includes 457,255 shares of restricted common stock based on an assumed initial offering price equal to the highpoint of the price range presented on the cover page of this prospectus with an aggregate value of $5,029,800 to be issued by us to our officers and directors upon the consummation of this offering. The outstanding shares of common stock above excludes (a) 2,198,000 shares of common stock issuable upon the exercise of an outstanding warrant held by GES and (b) 2,719,640 shares of common stock reserved for issuance but unissued under our equity incentive plan, including options to purchase 963,196 shares of common stock issued thereunder and shares of common stock issuable upon grants pursuant to performance-based awards with an aggregate target value of $3,353,200 over a three-year performance period.

Unless we indicate otherwise or the context otherwise requires, all information in this prospectus assumes no exercise of the underwriters’ option to purchase additional shares of our common stock.

10

Table of Contents

Summary Historical Financial Data

The following tables summarize our historical financial data. We have derived our summary historical financial data as of and for the three months ended March 31, 2014 and March 31, 2013 from our unaudited financial statements included elsewhere in this prospectus, and as of and for the years ended December 31, 2013 and December 31, 2012 from our audited financial statements included elsewhere in this prospectus. Prior to completion of the GES Transaction on March 2, 2012, we did not have meaningful operations. We have derived the summary historical financial data of GES, our predecessor, for the period from January 1, 2012 through March 1, 2012 from their audited financial statement included elsewhere in this prospectus. Our predecessor’s line of business was substantially different from ours, and you should not evaluate our results based on our predecessor, or consider our results and those of our predecessor on a combined basis. Our historical results are not necessarily indicative of the results that we may achieve in the future. The following summary other financial and operating data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the historical financial statements and related notes included elsewhere in this prospectus.

| Successor | ||||||||||||||||||||

| Independence Contract Drilling, Inc. | ||||||||||||||||||||

| Three Months Ended | Year Ended | Predecessor | ||||||||||||||||||

| March 31, 2014 |

March 31, 2013 |

December 31, 2013 |

December 31, 2012 |

January 1, 2012 through March 1, 2012 |

||||||||||||||||

| (dollars in thousands, except operating data) |

||||||||||||||||||||

| Statement of operations data(1): |

||||||||||||||||||||

| Revenues |

$ | 13,549 | $ | 8,257 | $ | 42,786 | $ | 15,123 | $ | 7,698 | ||||||||||

| Operating costs |

8,777 | 5,937 | 28,401 | 15,400 | 6,973 | |||||||||||||||

| Selling, general and administrative |

2,094 | 2,098 | 8,911 | 7,813 | 1,383 | |||||||||||||||

| Depreciation and amortization |

3,416 | 2,125 | 10,186 | 5,904 | 92 | |||||||||||||||

| Asset impairment(2) |

4,650 | — | — | — | — | |||||||||||||||

| Gain on disposition of assets |

(189 | ) | (41 | ) | (55 | ) | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total cost and expenses |

18,748 | 10,119 | 47,443 | 29,117 | 8,448 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating loss |

(5,199 | ) | (1,862 | ) | (4,657 | ) | (13,994 | ) | (750 | ) | ||||||||||

| Interest expense, net |

(394 | ) | — | (257 | ) | (10 | ) | (15 | ) | |||||||||||

| Loss on forgiveness of related party balances(3) |

— | — | — | — | (6,063 | ) | ||||||||||||||

| Gain (loss) on warrant derivative(4) |

3 | (433 | ) | 1,035 | 3,655 | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loss before income taxes |

(5,590 | ) | (2,295 | ) | (3,879 | ) | (10,349 | ) | (6,828 | ) | ||||||||||

| Income tax benefit |

(1,885 | ) | (599 | ) | (1,882 | ) | (5,401 | ) | (2,149 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net loss |

$ | (3,705 | ) | $ | (1,696 | ) | $ | (1,997 | ) | $ | (4,948 | ) | $ | (4,679 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cash flow data: |

||||||||||||||||||||

| Net cash provided by (used in) operating activities |

$ | (4,737 | ) | $ | 1,536 | $ | 5,997 | $ | (8,337 | ) | $ | (3,857 | ) | |||||||

| Net cash used in investing activities |

(11,968 | ) | (14,150 | ) | (59,273 | ) | (49,743 | ) | (18 | ) | ||||||||||

| Net cash provided by (used in) financing activities |

17,086 | (37 | ) | 18,599 | 95,486 | (25 | ) | |||||||||||||

| Balance sheet data: |

||||||||||||||||||||

| Total assets |

$ | 202,346 | $ | 163,988 | $ | 184,968 | $ | 167,436 | ||||||||||||

| Long-term debt |

38,097 | — | 19,780 | — | ||||||||||||||||

| Total liabilities |

60,625 | 20,472 | 40,096 | 22,736 | ||||||||||||||||

| Total stockholders’ equity |

$ | 141,721 | $ | 143,516 | 144,872 | 144,700 | ||||||||||||||

| Other financial and operating data: |

||||||||||||||||||||

| Adjusted EBITDA(2) |

$ | 3,315 | $ | 683 | $ | 7,280 | $ | (6,207 | ) | |||||||||||

| Number of completed rigs (end of period) |

6 | 4 | 7 | 4 | ||||||||||||||||

| Rig operating days |

607 | 327 | 1,745 | 472 | ||||||||||||||||

| Average number of operating rigs |

6.74 | 3.63 | 4.78 | 1.29 | ||||||||||||||||

| Rig utilization |

100 | % | 91 | % | 96 | % | 97 | % | ||||||||||||

| Average revenue per operating day |

$ | 20,918 | $ | 22,740 | $ | 21,351 | $ | 19,528 | ||||||||||||

| Average cost per operating day |

$ | 12,697 | $ | 13,187 | $ | 12,632 | $ | 15,787 | ||||||||||||

| Average rig margin per operating day |

$ | 8,221 | $ | 9,553 | $ | 8,719 | $ | 3,740 | ||||||||||||

| (1) | There are no other components of comprehensive income or loss. |

| (2) | Adjusted EBITDA is a supplemental non-GAAP measure. Please read below under “—Non-GAAP Financial Measure.” |

11

Table of Contents

| (2) | Represents asset impairment expense associated with damage sustained to the mast and other operating equipment of one of our non-walking rigs during the three months ended March 31, 2014. Please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Three Months Ended March 31, 2014 Compared to the Three Months Ended March 31, 2013—Asset Impairment.” |

| (3) | Represents amounts owed to our predecessor by its affiliate that were forgiven in the GES Transaction. |

| (4) | Represents a gain associated with the decrease in estimated fair value of the warrant to purchase approximately 2.2 million shares issued to GES in the GES Transaction. Please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Factors Affecting Comparability of Historical Operating and Financial Results.” |

Non-GAAP Financial Measure

Adjusted EBITDA is a supplemental non-GAAP financial measure that is used by management and external users of our financial statements, such as industry analysts, investors, lenders and rating agencies. We define “EBITDA” as earnings (or loss) before interest, taxes, depreciation, and amortization, and we define “Adjusted EBITDA” as EBITDA before stock-based compensation, gain/loss on warrant derivative liability and non-cash asset impairments. Adjusted EBITDA is not a measure of net income as determined by U.S. generally accepted accounting principles (“GAAP”).

Management believes Adjusted EBITDA is useful because it allows us and our stockholders to more effectively evaluate our operating performance and compare the results of our operations from period to period and against our peers without regard to our financing methods or capital structure. We exclude the items listed above from net income (loss) in calculating Adjusted EBITDA because these amounts can vary substantially from company to company within our industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. Adjusted EBITDA should not be considered an alternative to, or more meaningful than, net income (loss), the most closely comparable financial measure calculated in accordance with GAAP or as an indicator of our operating performance or liquidity. Certain items excluded from Adjusted EBITDA are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as stock-based compensation and the historic costs of depreciable assets, none of which are components of Adjusted EBITDA. Our presentation of Adjusted EBITDA should not be construed as an inference that our results will be unaffected by unusual or non-recurring items. Our computations of Adjusted EBITDA may not be comparable to other similarly titled measures of other companies.

12

Table of Contents

The following table presents a reconciliation of EBITDA and Adjusted EBITDA to net income (loss), the most closely comparable financial measure calculated in accordance with GAAP.

| Three Months Ended | Year Ended | |||||||||||||||

| March 31, 2014 | March 31, 2013 | December 31, 2013 | December 31, 2012 | |||||||||||||

| (in thousands) | ||||||||||||||||

| Net loss |

$ | (3,705 | ) | $ | (1,696 | ) | $ | (1,997 | ) | $ | (4,948 | ) | ||||

| Add back: |

||||||||||||||||

| Income tax benefit |

(1,885 | ) | (599 | ) | (1,882 | ) | (5,401 | ) | ||||||||

| Interest expense, net |

394 | — | 257 | 10 | ||||||||||||

| Depreciation and amortization |

3,416 | 2,125 | 10,186 | 5,904 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| EBITDA |

(1,780 | ) | (170 | ) | 6,564 | (4,435 | ) | |||||||||

| Stock-based compensation |

448 | 420 | 1,751 | 1,883 | ||||||||||||

| (Gain) loss on warrant derivative liability |

(3 | ) | 433 | (1,035 | ) | (3,655 | ) | |||||||||

| Non-cash asset impairment |

4,650 | — | — | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 3,315 | $ | 683 | $ | 7,280 | $ | (6,207 | ) | |||||||

|

|

|

|

|

|

|

|

|

|||||||||

Recent Developments

During the three months ended June 30, 2014, we completed the construction of our ninth ShaleDriller™ rig, which spudded its initial well on June 9, 2014 under a multi-year contract. The following summarizes certain operating data during this three-month period:

| Number of Completed Rigs (end of period)(1): |

8 | |||

| Rig Operating Days: |

636 | |||

| Average number of operating rigs: |

6.99 | |||

| Rig Utilization: |

100 | % |

| (1) | Excludes one completed rig undergoing an upgrade to add our multi-directional walking system to the rig. |

13

Table of Contents

An investment in our common stock involves a high degree of risk. You should consider carefully all of the risks described below, together with the other information contained in this prospectus, before making a decision to invest in our common stock. If any of the following events occur, our business, results of operations, financial condition and ability to timely and successfully implement our growth strategy (including planned rig construction) may be materially adversely affected. In that event, the value of our securities could decline, and you could lose all or part of your investment.

Risks Relating to the Oil and Gas Industry

We derive all our revenues from companies in the oil and gas exploration and production industry, a historically cyclical industry with levels of activity that are significantly affected by the levels and volatility in oil and gas prices.

As a provider of land-based contract drilling services, our business depends on the level of exploration and production activity by oil and gas companies operating in the U.S., and in particular, the regions where we actively market our contract drilling services. The oil and gas exploration and production industry is a historically cyclical industry characterized by significant changes in the levels of exploration and development activities. Oil and gas prices and market expectations of potential changes in those prices significantly affect the levels of those activities. Worldwide political, regulatory, economic, and military events as well as natural disasters have contributed to oil and gas price volatility and are likely to continue to do so in the future. Any prolonged reduction in the overall level of exploration and development activities in the U.S. and the regions where we market our contract drilling services, whether resulting from changes in oil and gas prices or otherwise, could materially and adversely affect us in many ways by negatively impacting:

| • | our revenues, cash flows and profitability; |

| • | the fair market value of our drilling rig fleet and other assets; |

| • | our ability to obtain additional debt and equity capital required to implement our rig construction and growth strategy, and the cost of that capital; and |

| • | our ability to retain skilled rig personnel whom we need to implement our growth strategy. |

Depending on the market prices of oil and gas, oil and gas exploration and production companies may cancel or curtail their drilling programs and may lower production spending on existing wells, thereby reducing demand for our services. Many factors beyond our control affect oil and gas prices, including, but not limited to:

| • | the cost of exploring for, producing and delivering oil and gas; |

| • | the discovery and development rate of new oil and gas reserves, especially shale and other unconventional gas resources for which we market our rigs; |

| • | the rate of decline of existing and new oil and gas reserves; |

| • | available pipeline and other oil and gas transportation capacity; |

| • | the levels of oil and gas storage; |

| • | the ability of oil and gas exploration and production companies to raise capital; |

| • | economic conditions in the U.S. and elsewhere; |

| • | actions by the Organization of Petroleum Exporting Countries; |

| • | political instability in the Middle East and other major oil and gas producing regions; |

| • | governmental regulations, sanctions and trade restrictions, both domestic and foreign; |

| • | domestic and foreign tax policy; |

14

Table of Contents

| • | weather conditions in the U.S.; |

| • | the pace adopted by foreign governments for the exploration, development and production of their national reserves; |

| • | the price of foreign imports of oil and gas; |

| • | the overall supply and demand for oil and gas; and |

| • | the development of alternate energy sources and the long-term effects of worldwide energy conservation measures. |

Oil and natural gas prices have been volatile historically and, we believe, will continue to be so in the future. During 2009, oil and natural gas prices fell significantly below the levels seen in late 2008, and while oil prices have improved since 2009, natural gas prices have remained depressed. For example, the average closing price for the Cushing WTI Spot Oil Price for each calendar year since 2009 has ranged from $61.65/bbl to $97.91/bbl. The average closing price for the Henry Hub Natural Gas Spot Price for each calendar year since 2009 has ranged from $2.75/mcf to $4.48/mcf. Future declines and volatility in oil and gas prices could materially and adversely affect our business, results of operations, financial condition and growth strategy.

Oil and natural gas prices, and market expectations of potential changes in these prices, significantly impact the level of worldwide drilling and production services activities. Reduced demand for oil and natural gas generally results in lower prices for these commodities and may impact the economics of planned drilling projects and ongoing production projects, resulting in the curtailment, reduction, delay or postponement of such projects for an indeterminate period of time. When drilling and production activity and spending decline, both dayrates and utilization have also historically declined. Declines in oil and natural gas prices and the general economy could materially and adversely affect our business, results of operations, financial condition and growth strategy.

In addition, if oil and natural gas prices decline, companies that planned to finance exploration, development or production projects through the capital markets may be forced to curtail, reduce, postpone or delay drilling activities, and also may experience an inability to pay suppliers. Adverse conditions in the global economic environment could also impact our vendors’ and suppliers’ ability to meet obligations to provide materials and services in general. If any of the foregoing were to occur, it could have a material adverse effect on our business and financial results and our ability to timely and successfully implement our growth strategy.

Risks Related to our Business

Our limited operating history and growth of our business make it difficult to evaluate our business.

We were formed in November 2011. As a result, there is only limited historical financial and operating information available upon which to base your evaluation of our performance. In addition, the growth in our business to date and the expected continued growth and number of operating rigs will make historical performance less representative of performance in future periods.

A significant delay in the completion of the construction of our planned additional rigs in 2014 and 2015 could materially and adversely affect our ability to execute our growth strategy.

Following completion of this offering, we expect to have approximately $33.4 million in cash and $89.2 million of availability under our $125.0 million revolving credit facility available to us to fund our growth strategy. Our borrowing base under this revolving credit facility will increase upon each of our additional rigs placed into service and spudding of its initial well. Our growth strategy requires us to invest significant funds in the construction of new ShaleDriller™ rigs and the skilled crews and personnel necessary to operate these rigs. We also will be required to invest significant capital into our facilities and the corporate infrastructure and overhead necessary to operate and manage a publicly-traded company.

15

Table of Contents

We expect to have eleven rigs operating by the end of 2014 and to complete the construction of up to an additional seven rigs by the end of 2015. It typically takes six to seven months to order and receive long lead time items and construct a ShaleDriller™ rig, with a significant portion of the costs required to be invested at the beginning of the process in order to procure the longer lead time items, such as variable frequency drive (“VFD”) houses and drillers cabins, masts and substructures, motors, blowout preventers (“BOPs”), top drives and drill pipe.

While we intend to immediately begin investing the proceeds from this offering into the construction of our state-of-the-art ShaleDriller™ rigs, we cannot assure you of the quantity and timing of the construction and completion of those rigs. The speed at which we will be able to construct rigs is dependent on a variety of factors, including our ability to obtain favorable drilling contracts, our ability to continue to successfully ramp-up rig construction at our facility, and our ability to acquire certain critical rig components from third party vendors. If we experience significant delays in the implementation of our business strategy, our growth strategy and long-term results of operations and financial condition could be adversely affected.

Our growth strategy will likely require that we commit to the construction of new drilling rigs prior to securing an executed contract for its use. The inability to secure drilling contracts for our new rigs promptly following the completion of their construction could materially and adversely affect our financial condition.

We currently do not have a drilling contract for any of our additional planned newbuild rigs. Because much of the equipment and parts required for the construction of our rigs must be ordered in advance, our growth strategy will likely require that we make significant purchases of equipment, and commit to constructing our rigs, prior to having executed customer contracts for their use. If we are unable to timely secure drilling contracts for all of our newly constructed rigs, it could materially and adversely affect our financial condition.

Any loss of large customers could have a material adverse effect on our financial condition and results of operations.

Our customer base consists of exploration and production companies that drill oil and gas wells in the United States in the regions where we market our rigs. We currently have executed eleven drilling contracts (including for two rigs under construction) with seven different customers, including Apache Corporation, BOPCO, L.P., COG Operating, LLC, a subsidiary of Concho Resources Inc., Elevation Resources LLC, Laredo Petroleum, Inc., Parsley Energy, LP and Pioneer Energy Resources USA, Inc., each of whom constitutes more than 10% of our existing revenues. Furthermore, it is likely that we will continue to derive a significant portion of our revenue from a relatively small number of customers in the future. Daywork contracts in the contract drilling industry typically do not obligate those customers to order additional services from the drilling contractor beyond those for which they have currently contracted. If a major customer decided not to continue to use our services or to terminate an existing contract, or if there is a change of management or ownership of a major customer, revenue would decline and our business, results of operations, financial condition and growth strategy could be adversely affected.

Six of our current drilling contracts are scheduled to terminate in 2015. If we are unable to renew our current drilling contracts at favorable pricing, or alternatively secure new contracts at favorable pricing, it could have a material and adverse effect on our results of operations and financial condition.

All of our current drilling contracts have original or current extended terms of between 12 and 24 months. In any event, our contracts provide that our customers may terminate at any time upon payment to us of an “early termination payment.” Six of our current drilling contracts have terms expiring in 2015. Our customers have no obligation to extend the term of any drilling contract and may elect to release the rig. We cannot assure you that any particular contract will be renewed, or if terminated, that a replacement contract could be immediately secured. The failure to renew or timely replace one or more of our existing drilling contracts could have a material and adverse effect on our results of operations and financial condition.

16

Table of Contents

Our operations involve operating hazards, which if not insured or indemnified against, could adversely affect our results of operations and financial condition.

Our operations are subject to the many hazards inherent in the drilling and well services industries, including the risks of:

| • | personal injury and loss of life; |

| • | blowouts; |

| • | cratering; |

| • | fires and explosions; |

| • | loss of well control; |

| • | collapse of the borehole; |

| • | damaged or lost drilling equipment; and |

| • | damage or loss from extreme weather and natural disasters. |

Any of these hazards can result in substantial liabilities or losses to us from, among other things:

| • | suspension of operations; |

| • | damage to, or destruction of, our property and equipment and that of others; |

| • | damage to producing or potentially productive oil and gas formations through which we drill; and |

| • | environmental damage. |

Although, we seek to protect ourselves from some but not all operating hazards through insurance coverage, some risks are either not insurable or insurance is available only at rates that we consider uneconomical. Depending on competitive conditions and other factors, we attempt to obtain contractual protection against uninsured operating risks from our customers. However, customers who provide contractual indemnification protection may not in all cases maintain adequate insurance or otherwise have the financial resources necessary to support their indemnification obligations. Our insurance or indemnification arrangements may not adequately protect us against liability or loss from all the hazards of our operations. For example, during March 2014, we experienced damage to the mast of one of our operating rigs that removed the rig from operations for a period of time, during which we were not compensated. We do not carry loss of business insurance for this rig being out of service.

We maintain insurance against some, but not all, of the potential risks affecting our operations and only in coverage amounts and deductible levels that we believe to be economical. Our insurance coverage includes deductibles which must be met prior to recovery. Additionally, our insurance is subject to exclusions and limitations, and there is no assurance that such coverage will adequately protect us against liability from all potential consequences and damages. The occurrence of a significant event that we have not fully insured or indemnified against or the failure of a customer to meet its indemnification obligations to us could materially and adversely affect our results of operations and financial condition. Furthermore, we may be unable to maintain adequate insurance in the future at rates we consider reasonable. Incurring a liability for which we are not fully insured or indemnified could have a material adverse effect on our financial condition and results of operations.

We operate in a highly competitive, fragmented industry in which price competition could reduce our profitability.

We encounter substantial competition from other drilling contractors. The markets in which we operate have intensified as recent mergers among E&P companies have reduced the number of available customers.

Contract drilling companies compete primarily on a regional basis, and the intensity of competition may vary significantly from region to region at any particular time. Most drilling services contracts are awarded on the basis of competitive bids, which also results in price competition.

17

Table of Contents

In addition to pricing and rig availability, the principal competitive factors in our markets are reputation for safety, service quality, rig availability, responsiveness, experience, technology and equipment quality. The success of our business will depend on our ability to offer safe and highly efficient operations, the quality and efficiency of our rigs and the skills and experience of our rig crews.

As a result of competition, we may lose market share or be unable to maintain or increase prices for our present services or to acquire additional business opportunities, which could have a material adverse effect on our business, results of operations, financial condition and ability to implement our growth strategy. In addition, the failure to maintain an adequate safety record could harm our ability to secure new drilling contracts. As a relatively new contract driller with limited operating history, there can be no assurance that we will be able to maintain the reputation for safety and quality required to successfully compete against our competition.

We face competition from many competitors with greater resources and greater ability to rapidly respond to changing customer requirements.

We compete with large national and multi-national companies that have longer operating histories, greater financial, technical and other resources and greater name recognition than we do. Several of our competitors provide a broader array of services and have a stronger presence in more geographic markets.

Furthermore, some of our competitors’ greater capabilities in these areas may enable them to better withstand industry downturns, compete more effectively on the basis of price and technology, retain skilled rig personnel, and build new rigs or acquire and refurbish existing rigs so as to be able to place rigs into service more quickly than us in periods of high drilling demand.

In addition, we compete with several smaller companies capable of competing effectively on a regional or local basis. Smaller competitors may be able to respond more quickly to new or emerging technologies and services and changes in customer requirements.

Finally, some E&P companies have begun performing horizontal and directional drilling on their wells using their own equipment and personnel. Any increase in the development and utilization of in-house drilling capabilities by our customers could decrease the demand for our services and have a material adverse impact on our business.

New technology may cause our drilling methods or equipment to become less competitive.

The drilling industry is subject to the introduction of new drilling and completion methods and equipment using new technologies, some of which may be subject to patent protection. Changes in technology or improvements in competitors’ equipment could make our equipment less competitive or require significant capital investments to build and maintain a competitive advantage. Further, we may face competitive pressure to design, implement or acquire certain new technologies at a substantial cost. Some of our competitors have greater financial, technical and personnel resources that may allow them to implement new technologies before we can. If we are unable to implement new and emerging technologies on a timely basis or at an acceptable cost, it may have a material adverse effect on our business, results of operations, financial condition and growth strategy.

Federal and state legislative and regulatory initiatives related to hydraulic fracturing could result in operating restrictions or delays in the completion of oil and natural gas wells that may reduce demand for our activities and could adversely affect our financial position, results of operations and cash flows.

Hydraulic fracturing is a commonly used process that involves injection of water, sand, and certain chemicals to fracture the hydrocarbon-bearing rock formation to allow flow of hydrocarbons into the wellbore. The adoption of any federal, state or local laws or the implementation of regulations or ordinances restricting or increasing the costs of hydraulic fracturing could potentially increase our costs of operations and cause a decrease in drilling activity levels in the Permian Basin and other unconventional resource plays and an associated decrease in demand for our rigs and service, any or all of which could adversely affect our financial position, results of operations and cash flows.

18

Table of Contents

The federal Energy Policy Act of 2005 amended the Underground Injection Control provisions of the federal Safe Drinking Water Act (“SDWA”) to exclude certain hydraulic fracturing practices from the definition of “underground injection.” The Environmental Protection Agency (the “EPA”) has asserted regulatory authority over certain hydraulic fracturing activities involving diesel fuel and published guidance relating to such practices in February 2014. Congress has considered bills to repeal the exemption for hydraulic fracturing from the SDWA, which would have the effect of allowing the EPA to promulgate new regulations and permitting requirements for hydraulic fracturing, potentially including chemical disclosure requirements. At the state level, several states in which we operate have adopted regulations requiring the disclosure of certain information regarding hydraulic fracturing fluids.