Attached files

| file | filename |

|---|---|

| EX-5.1 - EX-5.1 - Jason Industries, Inc. | d755966dex51.htm |

Table of Contents

As filed with the Securities and Exchange Commission on August 4, 2014

Registration No. 333-197412

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Jason Industries, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 3990 | 46-2888322 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

411 East Wisconsin Avenue

Suite 2100

Milwaukee, WI 53202

(414) 277-9300

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

William P. Schultz

General Counsel

411 East Wisconsin Avenue, Suite 2100

Milwaukee, WI 53202

(414) 277-9300

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

| Robert H. Friedman, Esq. Kenneth A. Schlesinger, Esq. Olshan Frome Wolosky LLP 65 East 55th Street New York, New York 10022 (212) 451-2300 |

Christian O. Nagler Kirkland & Ellis LLP 601 Lexington Avenue New York, New York 10022 (212) 446-4800 |

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Table of Contents

CALCULATION OF REGISTRATION FEE

|

| ||||||||

| Title of each class of securities to be registered |

Amount to be registered |

Proposed maximum offering price per unit |

Proposed maximum aggregate offering price |

Amount of registration fee | ||||

| Common Stock, par value $0.0001 per share, underlying Warrants |

13,993,773(1) | $12.00(2) | $167,925,276 | $21,629 | ||||

| Common Stock, par value $0.0001 per share |

3,485,623(3) | $10.40(4) | $36,250,480 | $4,670 | ||||

| Common Stock, par value $0.0001 per share |

7,283,333(5) | $10.40(6) | $75,746,664 | $9,757 | ||||

| Common Stock, par value $0.0001 per share |

3,653,100(7) | — (8) | — (8) | — (8) | ||||

| Warrants to purchase Common Stock |

1,150,000(9) | — (10) | — (10) | — (10) | ||||

| 8.0% Series A Convertible Perpetual Preferred Stock, par value $0.0001 per share |

66,868(11) | $1,000(12) | $66,868,000 | $8,613 | ||||

| TOTAL | $346,790,420 | $44,669(13) | ||||||

|

| ||||||||

|

| ||||||||

| (1) | Represents the issuance by the Registrant of (i) 17,250,000 shares of common stock underlying warrants originally sold as part of units in the Registrant’s initial public offering and (ii) 1,150,000 shares of common stock underlying warrants sold as part of the units issued in a private placement that closed simultaneously with the consummation of the Registrant’s initial public offering. Pursuant to Rule 416, there are also being registered such indeterminable additional shares of common stock as may be issued to prevent dilution as a result of stock splits, stock dividends or similar transactions. |

| (2) | Based on the exercise price of a warrant in accordance with Rule 457(g) under the Securities Act. |

| (3) | Represents the resale of shares of common stock that can be issued by the Registrant from time to time to the holders of an equivalent number of shares of common stock of JPHI Holdings Inc., a subsidiary of the Registrant (“JPHI”), upon the exchange by such holders of their shares of JPHI common stock for shares of common stock of the Registrant. |

| (4) | Estimated at $10.40 per share, the average of the high and low prices of the Registrant’s common stock as reported on The NASDAQ Stock Market on July 10, 2014, solely for the purpose of calculating the registration fee in accordance with Rule 457(f)(1) under the Securities Act. |

| (5) | Represents the resale of (i) 6,133,333 shares of common stock issued prior to our initial public offering and (ii) 1,150,000 shares of common stock sold as part of units issued in a private placement that closed simultaneously with the consummation of our initial public offering. |

| (6) | Estimated at $10.40 per share, the average of the high and low prices of the Registrant’s common stock as reported on The NASDAQ Stock Market on July 10, 2014, solely for the purpose of calculating the registration fee in accordance with Rule 457(c) under the Securities Act. |

| (7) | Represents the resale of 3,653,100 shares of common stock that can be issued upon conversion of the Registrant’s 8.0% Series A Convertible Perpetual Preferred Stock. |

| (8) | No fee pursuant to Rule 457(i) under the Securities Act. |

| (9) | Represents the resale of warrants to purchase common stock sold as part of units issued in a private placement that closed simultaneously with the consummation of our initial public offering. |

| (10) | No fee pursuant to Rule 457(g) under the Securities Act. |

| (11) | Represents the resale of (i) 45,000 shares of 8.0% Series A Convertible Perpetual Preferred Stock sold pursuant to a private placement which closed simultaneously with our initial business combination plus, (ii) as of July 10, 2014, an additional 21,868 shares of 8.0% Series A Convertible Perpetual Preferred Stock potentially issuable over the next five years as dividends. Pursuant to Rule 416, there are also being registered such indeterminable additional shares of common stock as may be issued to prevent dilution as a result of stock splits, stock dividends or similar transactions. |

| (12) | Calculated in accordance with Rule 457(i) under the Securities Act. |

| (13) | The Registrant previously paid a filing fee of $51,480 in connection with the initial filing of this Form S-1 Registration Statement. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a), may determine.

Table of Contents

The information contained in this prospectus is not complete and may be changed. No securities may be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these shares, and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated August 4, 2014

Preliminary Prospectus

JASON INDUSTRIES, INC.

13,993,773 Shares of Common Stock Issuable upon Exercise of Outstanding Warrants

14,422,056 Shares of Common Stock

1,150,000 Warrants to Purchase Common Stock

66,868 Shares of 8.0% Series A Convertible Perpetual Preferred Stock

This prospectus relates to the issuance by us of (i) 12,843,773 shares of our common stock, par value $0.0001 per share (the “Common Stock”) upon the exercise of warrants which were originally issued as part of units in our initial public offering (the “Public Warrants”), and (ii) 1,150,000 shares of Common Stock upon the exercise of warrants, which were originally issued as part of units in a private placement that closed simultaneously with the consummation of our initial public offering (the “IPO Placement Warrants” and, together with the Public Warrants, the “Warrants”). Each Warrant entitles the holder to purchase one share of our Common Stock at an exercise price of $12.00 per share. We will receive the proceeds from the exercise of the Warrants, but not from the sale of the underlying Common Stock.

This prospectus also relates to the resale of 14,422,056 shares of our Common Stock, 1,150,000 IPO Placement Warrants, and 66,868 shares of our 8.0% Series A Convertible Perpetual Preferred Stock, par value $0.0001 per share (the “Series A Convertible Preferred Stock”), by the selling security holders named in this prospectus or their permitted transferees. The shares of Common Stock being offered by the selling security holders consists of (i) 3,485,623 shares of Common Stock that can be issued from time to time to the holders of an equivalent number of shares of common stock (the “JPHI stock”) of our subsidiary, JPHI Holdings Inc., a Delaware corporation (“JPHI”), upon the exchange by such holders of JPHI stock for shares of our Common Stock (the “Rollover Shares”), (ii) 6,133,333 shares of Common Stock issued prior to our initial public offering (the “founder shares”), (iii) 1,150,000 shares of Common Stock sold as part of units issued in a private placement that closed simultaneously with the consummation of our initial public offering (the “IPO Placement Shares”), and (iv) 3,653,100 shares of Common Stock that can be issued upon conversion of our Series A Convertible Preferred Stock, which Series A Convertible Preferred Stock was issued in a private placement that closed simultaneously with our initial business combination (the “PIPE Investment”).

The selling security holders may offer, sell or distribute all or a portion of their securities publicly or through private transactions at prevailing market prices or at negotiated prices. We will not receive any of the proceeds from the sale of the securities owned by the selling security holders. We will bear all costs, expenses and fees in connection with the registration of these securities, including with regard to compliance with state securities or “blue sky” laws. The selling security holders will bear all commissions and discounts, if any, attributable to their sale of securities. See “Plan of Distribution” beginning on page 147 of this prospectus.

Our Common Stock and Warrants are quoted on The NASDAQ Stock Market under the symbols “JASN,” and “JASNW.” There is no established trading market for the Series A Convertible Preferred Stock. On August 1, 2014, the closing price of our Common Stock and Warrants was $10.41 and $1.40, respectively. As of August 1, 2014, we had 21,990,666 shares of Common Stock, 13,993,773 Warrants and 45,000 shares of Series A Convertible Preferred Stock issued and outstanding.

Our principal executive offices are located at 411 East Wisconsin Avenue, Suite 2100, Milwaukee, Wisconsin 53202, and our telephone number is (414) 277-9300.

INVESTING IN THESE SECURITIES INVOLVES CERTAIN RISKS. SEE “RISK FACTORS” ON PAGE 8.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Our securities are not being offered in any jurisdiction where the offer is not permitted under applicable local laws.

The date of this prospectus is , 2014

Table of Contents

| 2 | ||||

| 8 | ||||

| 32 | ||||

| 33 | ||||

| 33 | ||||

| 34 | ||||

| RATIO OF EARNINGS TO FIXED CHARGES AND TO FIXED CHARGES AND PREFERENCE DIVIDENDS |

35 | |||

| 36 | ||||

| UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

39 | |||

| 54 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

67 | |||

| 108 | ||||

| 115 | ||||

| 136 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

139 | |||

| 143 | ||||

| 148 | ||||

| 151 | ||||

| 159 | ||||

| 165 | ||||

| 165 | ||||

| 165 | ||||

| F-1 |

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information from that contained in this prospectus. We are not making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of this prospectus.

i

Table of Contents

This summary highlights certain information appearing elsewhere in this prospectus. For a more complete understanding of this offering, you should read the entire prospectus carefully, including the risk factors and the financial statements. Unless the context indicates otherwise, the terms “Jason,” “the Company,” “we,” “us” and “our” refer to Jason Industries, Inc., a Delaware corporation and its subsidiaries.

Background

We were originally formed in May 2013 as a blank check company under the name Quinpario Acquisition Corp. (“QPAC”) for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination involving QPAC and one or more businesses. Until the consummation of the Business Combination (as defined below), QPAC’s securities were traded on The NASDAQ Stock Market (“Nasdaq”) under the ticker symbols “QPAC,” “QPACU” and “QPACW.”

On June 30, 2014, we completed our initial business combination (the “Business Combination”) with Jason Incorporated pursuant to a stock purchase agreement dated as of March 16, 2014 (the “Purchase Agreement”) that provided for the acquisition of all of the capital stock of Jason Partners Holdings Inc., the indirect parent company of Jason Incorporated, by JPHI from Jason Partners Holdings LLC (“Seller”) and certain members of Seller. In connection with the Business Combination, we entered into new senior secured credit facilities with a syndicate of lenders led by Deutsche Bank AG New York Branch, as administrative agent, in the aggregate amount of approximately $460.0 million, which was primarily used to refinance Jason Incorporated’s existing indebtedness, pay transaction fees and expenses and pay a portion of the purchase price under the Purchase Agreement. The purchase price under the Purchase Agreement was also funded with cash held in our trust account, the contribution of Jason Partners Holdings Inc. common stock to JPHI by certain members of Seller and certain directors and management of Jason, including each of our named executive officers (collectively, the “Rollover Participants”) in exchange for JPHI stock, and the proceeds from the sale of Series A Convertible Preferred Stock in a private placement that closed simultaneously with the Business Combination, which we refer to as the PIPE Investment.

Following the Business Combination, Jason Incorporated became an indirect majority-owned subsidiary of ours and our only significant asset, with the Rollover Participants indirectly owning approximately 18.2% of Jason Incorporated and the Company indirectly owning approximately 81.8% of Jason Incorporated. Upon the closing of the Business Combination, we increased the size of our board of directors from six to nine directors and Jason Incorporated’s executive officers became our executive officers. We also changed our name from “Quinpario Acquisition Corp.” to “Jason Industries, Inc.” and continued the listing of our Common Stock and Warrants on Nasdaq under the symbols “JASN” and “JASNW,” respectively, effective July 1, 2014.

2

Table of Contents

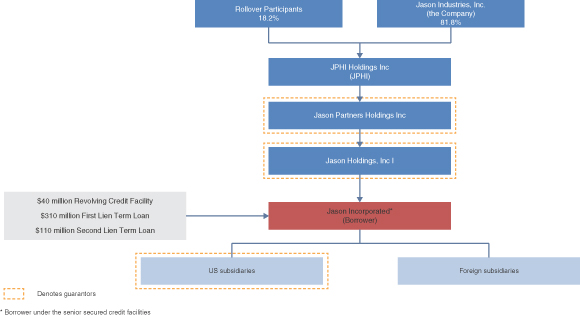

Organizational Chart

Presentation of Financial and Operating Data

The Business Combination will be accounted for using the acquisition method of accounting under the provisions of Accounting Standards Codification 805, “Business Combinations”. Accordingly, we are treated as the legal and accounting acquirer and Jason Partners Holdings Inc. is treated as the legal and accounting acquiree. However, Jason Partners Holdings Inc. is considered to be our accounting predecessor, and therefore unless otherwise indicated, the financial information and operating data presented in this prospectus is that of Jason Partners Holdings Inc. The historical financial statements of Quinpario Acquisition Corp. (a development stage company) for the year ended December 31, 2013 (audited) and the interim period ended March 31, 2014 (unaudited) are not included in this registration statement, but were included in the definitive proxy statement of Quinpario Acquisition Corp. filed with the Securities and Exchange Commission on June 16, 2014.

Our Company

We are a global industrial manufacturing company operating in the following industry sectors: agricultural, construction and industrial manufacturing. We operate in these sectors through four businesses: finishing, seating, acoustics and components. Jason Incorporated was founded in 1985 and today provides critical components and manufacturing solutions to customers across a wide range of end markets, industries and geographies through a global network of 33 manufacturing facilities and 16 sales offices, warehouses and joint venture facilities throughout the United States and 14 foreign countries. We are led by a corporate and business management team with an average of 25 years of experience and have embedded relationships with long standing customers, superior scale and resources and industry leading capability to design and manufacture specialized products on which our customers rely.

Our goal is to focus on markets with sustainable growth characteristics and where we believe we are, or have the opportunity to become, the industry leader. Our finishing business focuses on the production of industrial brushes, buffing wheels and buffing compounds that are used in a broad range of industrial and infrastructure applications. While our finishing business competes with numerous domestic and international companies across numerous product lines, the market is highly fragmented with most participants having single

3

Table of Contents

or limited product lines and serving specific geographic markets. We believe that resurgence in demand from the manufacturing, industrial and energy markets is driving demand for finishing products. In the long-term, the finishing market is closely tied to overall growth in industrial production, which we believe has fundamental and significant long-term growth potential. Our seating business supplies seating solutions to equipment manufacturers in the motorcycle, lawn and turf care, industrial, agricultural, construction and power sports end markets and is the sole supplier of original equipment manufacturer (“OEM”) seating to a major U.S.-based manufacturer of heavy motorcycles. The market for seating products is dominated by several large domestic and international participants who are often awarded contracts as the sole supplier for a particular product. Production and demand for motorcycles, lawn and garden equipment and construction equipment has rebounded since the recession and we expect activity to continue to improve in these sectors. The acoustics business manufactures engineered non-woven, fiber-based acoustical products for the North American auto industry. The market for automotive acoustical products is dominated by several large domestic and international participants who are often awarded contracts as the sole supplier for a particular automotive platform based on innovative styling, price or acoustical performance of their products. The components business is a diversified manufacturer of stamped, formed, expanded and perforated metal components and subassemblies for rail and filtration applications, outdoor power equipment, small gas engines and smart utility meters. Demand in the components market is influenced by the broader industrial manufacturing market, which we believe has fundamental and significant long-term growth potential, as well as trends in the perforated and expanded metal, smart meter, rail and outdoor power equipment industries. The market for component products is highly fragmented with most participants having single or limited product lines, serving specific geographic markets or providing niche capabilities applicable to a limited customer base.

We employ approximately 4,000 employees and manufacture products in 33 locations around the world. For the three months ended March 28, 2014 and year ended December 31, 2013, we generated net sales of $186.5 million and $680.8 million, respectively, income from operations of $11.8 million and $53.7 million, respectively, and adjusted EBITDA of $22.1 million and $79.8 million, respectively.

Additional Information

Our principal executive offices are located at 411 East Wisconsin Avenue, Suite 2100, Milwaukee, Wisconsin 53202, and our telephone number is (414) 277-9300. Our website is www.jasoninc.com.

Recent Developments

On May 6, 2014, we commenced a tender offer to purchase up to 9,200,000 of the Public Warrants at a purchase price of $0.75 per Warrant, which was subsequently increased to $1.00 per warrant on June 18, 2014 and $1.50 per Warrant on July 7, 2014, subject to certain conditions, including the consummation of the Business Combination. The Warrant Tender Offer expired on July 18, 2014 and a total of 4,406,277 warrants were validly tendered and not properly withdrawn for a total purchase price of approximately $6,609,000.

4

Table of Contents

The Offering

We are registering (i) the offer and sale by us of 13,993,773 shares of Common Stock underlying Warrants previously issued by the Company as Public Warrants and IPO Placement Warrants and (ii) the resale of 14,422,056 shares of Common Stock, 1,150,000 IPO Placement Warrants, and 66,868 shares of Series A Convertible Preferred Stock by the selling security holders named in this prospectus or their permitted transferees.

Issuance of Common Stock Underlying Warrants

| Shares to be issued upon exercise of Warrants |

13,993,773 shares of Common Stock underlying our Warrants. |

| Shares outstanding prior to exercise of Warrants |

21,990,666 shares of Common Stock as of July 11, 2014. |

| Shares to be outstanding assuming exercise of all Warrants |

35,984,439 shares of Common Stock. |

| Terms of Warrants |

Each Warrant entitles the holder to purchase one share of our Common Stock at an exercise price of $12.00 per share, subject to adjustment, at any time commencing on August 14, 2014, which is 12 months from the consummation of our initial public offering (“IPO”). The Warrants will expire at 5:00 p.m., New York time, on June 30, 2019 (which is five years after the completion of our initial business combination) or earlier upon redemption or liquidation. |

| Use of Proceeds |

We expect to receive $167,925,276 in net proceeds assuming the exercise of all of our Warrants at the exercise price of $12.00 per share. We intend to use these net proceeds for working capital and general corporate purposes. |

| Trading market and ticker symbol |

Our Warrants are quoted on Nasdaq under the symbol “JASNW.” |

Resale of Common Stock, IPO Placement Warrants and Series A Convertible Preferred Stock by Selling Security Holders

| Common Stock offered by the selling security holders |

We are registering 14,422,056 shares of Common Stock to be offered by the selling security holders named herein, which includes 3,485,623 Rollover Shares, 6,133,333 founder shares, 1,150,000 IPO Placement Shares and 3,653,100 shares of Common Stock that can be issued upon conversion of our Series A Convertible Preferred Stock. |

| IPO Placement Warrants offered by the selling security holders |

We are registering 1,150,000 IPO Placement Warrants to be offered by the selling security holder named herein. Each IPO Placement Warrant entitles the holder to purchase one share of our Common |

5

Table of Contents

| Stock at an exercise price of $12.00 per share, subject to adjustment, at any time commencing on August 14, 2014. The IPO Placement Warrants will expire at 5:00 p.m., New York time, on June 30, 2019 or earlier upon redemption or liquidation. |

| Series A Convertible Preferred Stock offered by the selling security holders |

We are registering 66,868 shares of Series A Convertible Preferred Stock to be offered by the selling security holders, including 21,868 shares of Series A Convertible Preferred Stock potentially issuable over the next five years as dividends. |

| Conversion of Series A Convertible Preferred Stock |

Each share of Series A Convertible Preferred Stock is convertible, at the holder’s option at any time, initially into 81.18 shares of our Common Stock (which is equivalent to an initial conversion price of approximately $12.32 per share), subject to specified adjustments as set forth in the Certificate of Designations, Preferences, Rights and Limitations of the Series A Convertible Preferred Stock (the “Certificate of Designations”). |

| In addition, the Company has the right, at its option, to cause all outstanding shares of the Series A Convertible Preferred Stock to be automatically converted into shares of Common Stock under certain circumstances and, if the Company undergoes certain fundamental changes, the Series A Convertible Preferred Stock will automatically be converted into Common Stock on the effective date of such fundamental change, in each case, as more fully described in “Description of Capital Stock—Series A Convertible Preferred Stock.” |

| Dividends on Series A Convertible Preferred Stock |

Holders of the Series A Convertible Preferred Stock are entitled to receive, when, as and if declared by the Company’s board of directors, cumulative dividends at the rate of 8.0% per annum (the dividend rate) on the $1,000 liquidation preference per share of the Series A Convertible Preferred Stock, payable quarterly in arrears on each dividend payment date. Dividends are paid in cash or, at the Company’s option, in additional shares of Series A Convertible Preferred Stock or a combination thereof. For more information, please read “Description of Capital Stock—Series A Convertible Preferred Stock.” |

| Terms of the offering |

The selling security holders will determine when and how they will dispose of the Common Stock, IPO Placement Warrants and Series A Convertible Preferred Stock registered under this prospectus for resale. |

| Securities outstanding prior to this offering |

21,990,666 shares of our Common Stock and 45,000 shares of our Series A Convertible Preferred Stock are issued and outstanding as of |

6

Table of Contents

| July 31, 2014. In addition, as of July 31, 2014, 13,993,773 shares of Common Stock are issuable upon exercise of 13,993,773 outstanding Warrants. |

| Securities outstanding after this offering |

43,123,162 shares of our Common Stock, which assumes the exercise of all Warrants, exchange of all JPHI stock into Common Stock, and the conversion of all shares of Series A Convertible Preferred Stock. The number of shares of Common Stock outstanding after this offering excludes the 3,473,435 shares of Common Stock available for future issuance under the Jason Industries, Inc. 2014 Omnibus Incentive Plan. |

| Use of Proceeds |

We will not receive any of the proceeds from the sale of shares of Common Stock, IPO Placement Warrants or Series A Convertible Preferred Stock by the selling security holders. However, we will receive proceeds from the exercise of IPO Placement Warrants if they are exercised by the selling security holder. We intend to use any proceeds for working capital and general corporate purposes. |

| Trading market and ticker symbol |

Our Common Stock and Warrants are quoted on Nasdaq under the symbols “JASN,” and “JASNW,” respectively. There has been no market for our Series A Convertible Preferred Stock and a public market may not develop, or, if any market does develop, it may not be sustained. Our Series A Convertible Preferred Stock is not listed on any exchange or quoted on the OTC Bulletin Board. |

For additional information concerning the offering, see “Plan of Distribution” beginning on page 147.

Risk Factors

Before investing in our securities, you should carefully read and consider the information set forth in “Risk Factors” beginning on page 8.

7

Table of Contents

Investing in our securities involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including our consolidated financial statements and related notes, before deciding whether to purchase any of our securities. Any of these risks may have a material adverse effect on our business, financial condition, results of operations and cash flows and our prospects could be harmed. In that event, the price of our securities could decline and you could lose part or all of your investment.

Risk Factors Relating to Our Business

Jason is affected by developments in the industries in which its customers operate.

Jason derives its revenues largely from customers in the following industry sectors: agricultural, construction and industrial manufacturing. Factors affecting any of these industries in general, or any of its customers in particular, could adversely affect Jason because its revenue growth largely depends on the continued growth of its customers’ businesses in their respective industries. These factors include:

| • | seasonality of demand for Jason’s customers’ products which may cause its manufacturing capacity to be underutilized for periods of time; |

| • | its customers’ failure to successfully market their products, to gain or retain widespread commercial acceptance of their products or to compete effectively in their industries; |

| • | loss of market share for Jason’s customers’ products, which may lead its customers to reduce or discontinue purchasing Jason’s products and to reduce prices, thereby exerting pricing pressure on Jason; |

| • | economic conditions in the markets in which Jason’s customers operate, in particular, the United States and Europe, including recessionary periods such as the global economic downturn; and |

| • | product design changes or manufacturing process changes that may reduce or eliminate demand for the components Jason supplies. |

Jason expects that future sales will continue to depend on the success of its customers. If economic conditions and demand for its customers’ products deteriorate, Jason may experience a material adverse effect on its business, operating results and financial condition.

Some of Jason’s business segments are cyclical. A downturn or weakness in overall economic activity can have a material negative impact on Jason.

Historically, sales of products that Jason manufactures have been subject to cyclical variations caused by changes in general economic conditions. During recessionary periods, such as the recent global economic recession, Jason has been adversely affected by reduced demand for its products. In addition, the strength of the economy generally may affect the rates of expansion, consolidation, renovation and equipment replacement in the industries Jason serves.

Volatility in the prices of raw materials and energy prices and our ability to pass along increased costs to our customers could adversely affect Jason’s results of operations.

The prices of raw materials critical to Jason’s business and performance, such as steel, are based on global supply and demand conditions. Certain raw materials used by Jason, including polyurethane foam, vinyl, plastics, steel, polyester fiber, bicomponent fiber and machined fiber are only available from a limited number of suppliers, and it may be difficult to find alternative suppliers at the same or similar costs. Although our contracts and long term arrangements with our customers generally do not expressly allow us to pass through increases in

8

Table of Contents

our raw materials, energy costs and other inputs to our customers, we endeavor to discuss price adjustments with our customers on a case by case basis where it makes business sense. While Jason strives to pass through the price of raw materials to its customers (other than increases in order amounts which are subject to negotiation), Jason may not be able to do so in the future, and volatility in the prices of raw materials may affect customer demand for certain products. In addition, Jason, along with its suppliers and customers, rely on various energy sources for a number of activities connected with its business, such as the transportation of raw materials and finished products. Energy and utility prices, including electricity and water prices, and in particular prices for petroleum-based energy sources, are volatile and have been on an upward trend. Increased supplier and customer operating costs arising from volatility in the prices of energy sources, such as increased energy and utility costs and transportation costs, could be passed through to Jason and it may not be able to increase its product prices sufficiently or at all to offset such increased costs. The impact of any volatility in the prices of energy or the raw materials on which Jason relies, including the reduction in demand for certain products caused by such price volatility, could result in a loss of revenue and profitability and adversely affect Jason’s results of operations.

Jason competes with numerous other manufacturers in each of its segments and competition from these providers may affect the profitability of Jason’s business.

The industries Jason serves are highly competitive. Jason competes with numerous companies that manufacture finishing, seating, automotive acoustics and components products. Many of Jason’s competitors have international operations and significant financial resources and some have substantially greater manufacturing, research and design and marketing resources than Jason. These competitors may, among others:

| • | respond more quickly to new or emerging technologies; |

| • | have greater name recognition, critical mass or geographic market presence; |

| • | be better able to take advantage of acquisition opportunities; |

| • | adapt more quickly to changes in customer requirements; |

| • | devote greater resources to the development, promotion and sale of their products; |

| • | be better positioned to compete on price for their products, due to any combination of low-cost labor, raw materials, components, facilities or other operating items, or willingness to make sales at lower margins than Jason; |

| • | consolidate with other competitors in the industry which may create increased pricing and competitive pressures on Jason’s business; and |

| • | be better able to utilize excess capacity which may reduce the cost of their products or services. |

Competitors with lower cost structures may have a competitive advantage when bidding for business with Jason’s customers. Jason also expects its competitors to continue to improve the performance of their current products or services, to reduce prices of their existing products or services and to introduce new products or services that may offer greater performance and improved pricing. Additionally, Jason may face competition from new entrants to the industry in which Jason operates. Any of these developments could cause a decline in sales and average selling prices, loss of market share of Jason’s products or profit margin compression.

Jason may not be able to manage the expansion of its operations effectively in order to achieve projected levels of growth.

Jason’s business plan calls for further expansion over the next several years. Jason anticipates that further development of its infrastructure and an increase in the number of its employees will be required to achieve Jason’s planned broadening of its product offerings and client base, improvements in its machines and materials used in its machines, and its planned international growth. In particular, Jason must increase its marketing and services staff to support new marketing and service activities and to meet the needs of both new and existing

9

Table of Contents

customers. Jason’s future success will depend in part upon the ability of its management to manage its growth effectively. If Jason’s management is unsuccessful in meeting these challenges, it may not be able to achieve its anticipated level of growth which would adversely affect Jason’s results of operations.

Jason may not be able to maintain its engineering, technological and manufacturing expertise.

The markets for Jason’s products are characterized by changing technology and evolving process development. The continued success of Jason’s business will depend upon its ability to:

| • | hire, retain and expand its pool of qualified engineering and technical personnel; |

| • | maintain technological leadership in its industry; |

| • | successfully anticipate or respond to changes in manufacturing processes in a cost-effective and timely manner; and |

| • | successfully anticipate or respond to changes in cost to serve in a cost-effective and timely manner. |

Jason cannot be certain that it will develop the capabilities required by its customers in the future. The emergence of new technologies, industry standards or customer requirements may render Jason’s equipment, inventory or processes obsolete or uncompetitive. Jason may have to acquire new technologies and equipment to remain competitive. The acquisition and implementation of new technologies and equipment may require Jason to incur significant expense and capital investment, which could reduce its margins and affect its operating results. When Jason establishes or acquires new facilities, it may not be able to maintain or develop its engineering, technological and manufacturing expertise due to a lack of trained personnel, effective training of new staff or technical difficulties with machinery. Failure to anticipate and adapt to customers’ changing technological needs and requirements or to hire and retain a sufficient number of engineers and maintain engineering, technological and manufacturing expertise may have a material adverse effect on Jason’s business.

Jason may encounter difficulties in completing or integrating acquisitions, which could adversely affect its operating results.

Jason expects to expand its presence in new end markets, expand its capabilities and acquire new customers, some of which may occur through acquisitions. These transactions may involve acquisitions of entire companies, portions of companies, the entry into joint ventures and acquisitions of businesses or selected assets. Potential challenges related to Jason’s acquisitions and joint ventures include:

| • | paying an excessive price for acquisitions and incurring higher than expected acquisition costs; |

| • | difficulty in integrating acquired operations, systems, assets and businesses; |

| • | difficulty in implementing financial and management controls, reporting systems and procedures; |

| • | difficulty in maintaining customer, supplier, employee or other favorable business relationships of acquired operations and restructuring or terminating unfavorable relationships; |

| • | ensuring sufficient due diligence prior to an acquisition and addressing unforeseen liabilities of acquired businesses; |

| • | making acquisitions in new end markets, geographies or technologies where Jason’s knowledge or experience is limited; |

| • | failing to realize the benefits from goodwill and intangible assets resulting from acquisitions which may result in write-downs; |

| • | failing to achieve anticipated business volumes; and |

| • | making acquisitions which force Jason to divest other businesses. |

10

Table of Contents

Any of these factors could prevent Jason from realizing the anticipated benefits of an acquisition, including additional revenue, operational synergies and economies of scale. Jason’s failure to realize the anticipated benefits of acquisitions could adversely affect its business and operating results.

Acquisitions, expansions or infrastructure investments may require Jason to increase its level of indebtedness or issue additional equity.

Should Jason desire to consummate significant additional acquisition opportunities, undertake significant additional expansion activities or make substantial investments in its infrastructure, Jason’s capital needs would increase and it may need to increase available borrowings under its credit facilities or access public or private debt and equity markets. There can be no assurance, however, that Jason will be successful in raising additional debt or equity on terms that it would consider acceptable.

An increase in the level of indebtedness could, among other things:

| • | make it difficult for Jason to obtain financing in the future for acquisitions, working capital, capital expenditures, debt service requirements or other purposes; |

| • | limit Jason’s flexibility in planning for or reacting to changes in its business; |

| • | affect Jason’s ability to pay dividends; |

| • | make Jason more vulnerable in the event of a downturn in its business; and |

| • | affect certain financial covenants with which Jason must comply in connection with its credit facilities. |

Additionally, a further non pro rata equity issuance would dilute your ownership interest.

If Jason fails to develop new and innovative products or if customers in its markets do not accept them, Jason’s results would be negatively affected.

Jason’s products must be kept current to meet its customers’ needs. To remain competitive, Jason therefore must develop new and innovative products on an ongoing basis. If Jason fails to make innovations or the market does not accept Jason’s new products, its sales and results would suffer. Jason invests significantly in the research and development of new products. These expenditures do not always result in products that will be accepted by the market. To the extent they do not, whether as a function of the product or the business cycle, Jason will have increased expenses without significant sales to benefit it. Failure to develop successful new products may also cause potential customers to purchase competitors’ products, rather than invest in products manufactured by Jason.

The potential impact of failing to deliver products on time could increase the cost of the products.

In most instances, Jason guarantees that it will deliver a product by a scheduled date. If Jason subsequently fails to deliver the product as scheduled, Jason may be held responsible for cost impacts and/or other damages resulting from any delay. To the extent that these failures to deliver may occur, the total damages for which Jason could be liable could significantly increase the cost of the products; as such, Jason could experience reduced profits or, in some cases, a loss for that contract. Additionally, failure to deliver products on time could result in damage to customer relationships, the potential loss of customers, and reputational damage which could impair Jason’s ability to attract new customers.

Increasing costs of doing business in many countries in which Jason operates may adversely affect its business and financial results.

Increasing costs such as labor and overhead costs in the countries in which Jason operates may erode its profit margins and compromise its price competitiveness. Historically, the low cost of labor in certain of the countries in which Jason operates had been a competitive advantage but labor costs in these countries, such as

11

Table of Contents

China, have been increasing. Jason’s profitability also depends on its ability to manage and contain its other operating expenses such as the cost of utilities, factory supplies, factory space costs, equipment rental, repairs and maintenance and freight and packaging expenses. In the event Jason is unable to manage any increase in its labor and other operating expenses in an environment where revenue does not increase proportionately, Jason’s financial results would be adversely affected.

Jason’s international scope will require it to obtain financing in various jurisdictions.

Jason operates manufacturing facilities in the United States and 11 foreign countries, which creates financing challenges for it. These challenges include navigating local legal and regulatory requirements associated with obtaining debt or equity financing in the respective foreign jurisdictions in which Jason operates. In the event that Jason is not able to obtain financing on satisfactory terms in any of these jurisdictions, it could significantly impair its ability to run its foreign operations on a cost effective basis or to grow such operations. Failure to manage such challenges may adversely affect Jason’s business and results of operations.

Security breaches and other disruptions could compromise Jason’s information and expose it to liability, which would cause its business and reputation to suffer.

In the ordinary course of business, Jason collects and stores sensitive data, including its proprietary business information and that of its customers, suppliers and business partners, as well as personally identifiable information of its customers and employees, in its data centers and on its networks. The secure processing, maintenance and transmission of this information is critical to Jason’s operations and business strategy. Despite Jason’s security measures, its information technology and infrastructure may be vulnerable to malicious attacks or breached due to employee error, malfeasance or other disruptions, including as a result of rollouts of new systems. Any such breach could compromise Jason’s networks and the information stored there could be accessed, publicly disclosed, lost or stolen. Any such access, disclosure or other loss of information could result in legal claims or proceedings and/or regulatory penalties, disrupt Jason’s operations, damage its reputation, and/or cause a loss of confidence in its products and services, which could adversely affect its business.

Jason has operations in many countries and such operations may be subject to a number of risks specific to these countries.

Jason’s international operations across many different jurisdictions may be subject to a number of risks specific to these countries, including:

| • | less flexible employee relationships which can be difficult and expensive to terminate; |

| • | labor unrest; |

| • | political and economic instability (including war and acts of terrorism); |

| • | inadequate infrastructure for its operations (i.e. lack of adequate power, water, transportation and raw materials); |

| • | health concerns and related government actions; |

| • | risk of governmental expropriation of its property; |

| • | less favorable, or relatively undefined, intellectual property laws; |

| • | unexpected changes in regulatory requirements and laws; |

| • | longer customer payment cycles and difficulty in collecting trade accounts receivable; |

| • | export duties, tariffs, import controls and trade barriers (including quotas); |

| • | adverse trade policies or adverse changes to any of the policies of either the United States or any of the foreign jurisdictions in which Jason operates; |

12

Table of Contents

| • | adverse changes in tax rates or regulations; |

| • | legal or political constraints on its ability to maintain or increase prices; |

| • | burdens of complying with a wide variety of labor practices and foreign laws, including those relating to export and import duties, environmental policies and privacy issues; |

| • | inability to utilize net operating losses incurred by Jason’s foreign operations against future income in the same jurisdiction; |

| • | economies that are emerging or developing, that may be subject to greater currency volatility, negative growth, high inflation, limited availability of foreign exchange and other risks; and |

| • | ability to repatriate cash on a tax effective basis. |

These factors may harm Jason’s results of operations, and any measures that Jason may implement to reduce the effect of volatile currencies and other risks of its international operations may not be effective. In Jason’s experience, entry into new international markets requires considerable management time as well as start-up expenses for market development, hiring and establishing office facilities before any significant revenue is generated. As a result, initial operations in a new market may operate at low margins or may be unprofitable.

Jason’s international sales and operations are subject to applicable laws relating to trade, export controls and foreign corrupt practices, the violation of which could adversely affect its operations.

Jason must comply with all applicable international trade, customs, export controls and economic sanctions laws and regulations of the United States and other countries. Jason is also subject to the Foreign Corrupt Practices Act and other anti-bribery laws that generally bar bribes or unreasonable gifts to foreign governments or officials. Changes in trade sanctions laws may restrict Jason’s business practices, including cessation of business activities in sanctioned countries or with sanctioned entities, and may result in modifications to compliance programs. Violation of these laws or regulations could result in sanctions or fines and could have a material adverse effect on Jason’s financial condition, results of operations and cash flows.

Failure to successfully complete or integrate joint ventures into Jason’s existing operations could have an adverse impact on its business, financial condition and results of operations.

Jason regularly evaluates its joint ventures. Potential issues associated with these joint ventures could include, among other things, Jason’s ability to realize the full extent of the benefits or cost savings that it expects to realize as a result of the formation of a joint venture within the anticipated time frame, or at all; receipt of necessary consents, clearances and approvals in connection with a joint venture; and diversion of management’s attention from base strategies and objectives. In Jason’s joint ventures, it shares ownership and management responsibility of a company with one or more parties who may or may not have the same goals, strategies, priorities or resources as Jason does and joint ventures are intended to be operated for the benefit of all co-owners, rather than for Jason’s exclusive benefit. In addition, joint ventures outside of the United States increase exposure to risks associated with operations outside of the United States, including fluctuations in exchange rates and compliance with laws and regulations outside the United States. If a joint venture is not successfully completed or integrated into Jason’s existing operations, financial condition and results of operations could be adversely impacted.

Jason is subject to risks of currency fluctuations and related hedging operations, and the appreciation of the currencies of countries in which Jason conducts its manufacturing operations, particularly the Euro, may negatively affect the profitability of its business.

Jason reports its financial results in U.S. dollars. Approximately 20% of Jason’s net sales are in currencies other than the U.S. dollar. Changes in exchange rates among other currencies, especially the Euro, to the U.S. dollar may negatively affect Jason’s net sales, cost of sales, gross profit and net income where Jason’s expenses

13

Table of Contents

and revenues are denominated in different currencies. Jason cannot predict the effect of future exchange rate fluctuations. Jason may from time to time use financial instruments, primarily short-term forward contracts, to hedge Euro and other currency commitments arising from foreign currency obligations. Jason does not have a fixed hedging policy currently. Where possible, Jason endeavors to match its non-functional currency exchange requirements to its receipts. If Jason’s hedging activities are not successful or if Jason changes or reduces these hedging activities in the future, it may experience significant unexpected expenses from fluctuations in exchange rates.

Jason depends on its key executive officers, managers and skilled personnel and may have difficulty retaining and recruiting qualified employees.

Jason’s success depends to a large extent upon the continued services of its executive officers, senior management personnel, managers and other skilled personnel and its ability to recruit and retain skilled personnel to maintain and expand its operations. Jason could be affected by the loss of any of its executive officers who are responsible for formulating and implementing Jason’s business plan and strategy, and who have been instrumental in its growth and development. In addition, in order to manage Jason’s growth, it will need to recruit and retain additional management personnel and other skilled employees. However, competition is high for skilled technical personnel among companies that rely on engineering and technology, and the loss of qualified employees or an inability to attract, retain and motivate additional skilled employees required for the operation and expansion of its business could hinder Jason’s ability to conduct design, engineering and manufacturing activities successfully and develop marketable products. Jason may not be able to attract the skilled personnel it requires or retain those whom it has trained at its own cost. If Jason is not able to do so, its business and its ability to continue to grow could be negatively affected.

Many of Jason’s customers do not commit to long-term production schedules, which makes it difficult for Jason to schedule production accurately and achieve maximum efficiency of its manufacturing capacity.

Generally, Jason’s customers do not commit to long-term contracts. Many of its customers do not commit to firm production schedules and Jason continues to experience reduced lead-times in customer orders. Additionally, customers may change production quantities or delay production with little lead-time or advance notice. Therefore, Jason relies on and plans its production and inventory levels based on its customers’ advance orders, commitments or forecasts, as well as Jason’s internal assessments and forecasts of customer demand. The volume and timing of sales to Jason’s customers may vary due to, among others:

| • | variation in demand for or discontinuation of its customers’ products; |

| • | its customers’ attempts to manage their inventory; |

| • | design changes; |

| • | changes in Jason’s customers’ manufacturing strategies; and |

| • | acquisitions of or consolidation among customers. |

The variations in volume and timing of sales make it difficult to schedule production and optimize utilization of manufacturing capacity. This uncertainty may require Jason to increase staffing and incur other expenses in order to meet an unexpected increase in customer demand, potentially placing a significant burden on Jason’s resources. Additionally, an inability to respond to such increases may cause customer dissatisfaction, which may negatively affect Jason’s customers’ relationships.

Further, in order to secure sufficient production scale, Jason may make capital investments in advance of anticipated customer demand. Such investments may lead to low utilization levels if customer demand forecasts change and Jason is unable to utilize the additional capacity. Because fixed costs make up a large proportion of Jason’s total production costs, a reduction in customer demand can have a significant adverse impact on its gross profits and operating results. Additionally, Jason orders materials and components based on customer forecasts

14

Table of Contents

and orders and suppliers may require it to purchase materials and components in minimum quantities that exceed customer requirements, which may have an adverse impact on Jason’s gross profits and operating results. In the past, anticipated orders from some of Jason’s customers have failed to materialize and delivery schedules have been deferred as a result of changes in its customers’ business needs. Jason has also allowed long-term customers to delay orders to absorb excess inventory. Such order fluctuations and deferrals may have an adverse effect on Jason’s business, operating results and financial conditions.

Jason may incur additional expenses and delays due to technical problems or other interruptions at its manufacturing facilities.

Disruptions in operations due to technical problems or other interruptions such as floods or fire could adversely affect the manufacturing capacity of Jason’s facilities. Such interruptions could cause delays in production and cause it to incur additional expenses such as charges for expedited deliveries for products that are delayed. Additionally, Jason’s customers have the ability to cancel purchase orders in the event of any delays in production and may decrease future orders if delays are persistent. Additionally, to the extent that such disruptions do not result from damage to Jason’s physical property, these may not be covered by its business interruption insurance. Any such disruptions may adversely affect Jason’s operations and its financial results.

The operations of Jason’s manufacturing facilities may be disrupted by union activities and other labor-related problems.

Jason has labor unions at certain of its facilities. As of March 28, 2014, Jason had approximately 630 unionized personnel in the United States. For such employees, Jason has entered into collective bargaining agreements with the respective labor unions. In the future, such agreements may limit Jason’s ability to contain increases in its labor costs as its ability to control future labor costs depends partly on the outcome of wage negotiations with its employees. Any future collective bargaining agreements may lead to further increases in Jason’s labor costs. Although Jason’s employees in certain other facilities are currently not unionized, there can be no assurance that they will continue to remain as such.

Union activities and other labor-related problems not linked to union activities may disrupt Jason’s operations and adversely affect its business and results of operations. Jason cannot provide any assurance that it will not be affected by any such labor unrest, or increase in labor cost, or interruptions to the operations of its existing manufacturing plants or new manufacturing plants that Jason may set up in the future. Any disruptions to Jason’s manufacturing facilities as a result of labor-related disturbances could affect its ability to meet delivery and efficiency targets resulting in an adverse effect on Jason’s customer relationships and its financial results. Such disruptions may not be covered by Jason’s business interruption insurance.

Any disruption in Jason’s information systems could disrupt its operations and would be adverse to its business and financial operations.

Jason depends on various information systems to support its customers’ requirements and to successfully manage its business, including managing orders, supplies, accounting controls and payroll. Any inability to successfully manage the procurement, development, implementation or execution of Jason’s information systems and back-up systems, including matters related to system security, reliability, performance and access, as well as any inability of these systems to fulfill their intended purpose within Jason’s business, could have an adverse effect on its business and financial performance. Such disruptions may not be covered by Jason’s business interruption insurance.

Natural disasters, epidemics and other events outside Jason’s control, and the ineffective management of such events, may harm its business.

Some of Jason’s facilities are located in areas that may be affected by natural disasters such as hurricanes, earthquakes, water shortages, tsunamis and floods. All facilities are subject to other natural or man-made

15

Table of Contents

disasters such as fires, acts of terrorism, failures of utilities and epidemics. If such an event were to occur, Jason’s business could be harmed due to the event or its inability to effectively manage the effects of the particular event. Potential harms include the loss of business continuity, the loss of business data and damage to infrastructure.

Jason’s production could be severely affected if its employees or the regions in which its facilities are located are affected by a significant outbreak of any disease or epidemic. For example, a facility could be closed by government authorities for a sustained period of time, some or all of its workforce could be unavailable due to quarantine, fear of catching the disease or other factors, and local, national or international transportation or other infrastructure could be affected, leading to delays or loss of production. In addition, Jason’s suppliers and customers are subject to similar risks, which could lead to a shortage of components or a reduction in Jason’s customers’ demand for its services.

Jason relies on a variety of common carriers to transport its materials from its suppliers, and to transport products from Jason to its customers. Problems suffered by any of these common carriers, whether due to a natural disaster, labor problem, act of terrorism, increased energy prices or some other issue, could result in shipping delays, increased costs or some other supply chain disruption and could therefore have a material adverse effect on Jason’s operations.

In addition, some of Jason’s facilities possess certifications, machinery, equipment or tooling necessary to work on specialized products that its other locations lack. If work is disrupted at one of these facilities, it may not be practicable or feasible to transfer such specialized work to another facility without significant costs and delays. Thus, any disruption in operations at a facility possessing specialized certifications, machinery, equipment or tooling could adversely affect Jason’s ability to provide products to its customers and thus negatively affect its relationships and financial results.

Political and economic developments could adversely affect Jason’s business.

Increased international political instability and social unrest, evidenced by the threat or occurrence of terrorist attacks, enhanced national security measures and the related decline in consumer confidence may hinder Jason’s ability to do business. Any escalation in these events or similar future events may disrupt its operations or those of its customers and suppliers and could affect the availability of raw materials and components needed to manufacture Jason’s products or the means to transport those materials to manufacturing facilities and finished products to customers. These events have had and may continue to have an adverse effect, generally, on the world economy and consumer confidence and spending, which could adversely affect Jason’s revenue and operating results. The effect of these events on the volatility of the world financial markets could in future lead to volatility of the market price of Jason’s securities and may limit the capital resources available to Jason, its customers and suppliers.

Sales of Jason’s products may result in exposure to product liability, intellectual property infringement and other claims.

Jason’s manufactured products can expose it to potential liabilities. For instance, Jason’s manufacturing businesses expose it to potential product liability claims resulting from injuries caused by defects in products it designs or manufactures, as well as potential claims that products Jason designs or processes it uses infringe on third-party intellectual property rights. Such claims could subject Jason to significant liability for damages, subject the infringing portion of its business to injunction and, regardless of their merits, could be time-consuming and expensive to resolve. Jason may also have greater potential exposure from warranty claims and product recalls due to problems caused by product design. Although Jason has product liability insurance coverage, it may not be sufficient to cover the full extent of its product liability, if at all, and may also be subject to the satisfaction of a deductible amount of up to $250,000. A successful product liability claim in excess or outside of Jason’s insurance coverage or any material claim for which insurance coverage was denied or limited and for which indemnification was not available could have a material adverse effect on Jason’s business, results of operations and/or financial condition.

16

Table of Contents

Jason may experience work-related accidents that may expose it to liability claims.

Due to the nature of its operations, Jason is subject to the risks of its employees being exposed to industrial-related accidents at its premises. If such accidents occur in the future, Jason may be required to pay compensation and may also suffer reputational harm. Under such circumstances, Jason’s business and financial performance could be adversely affected.

If Jason’s manufacturing processes and products do not comply with applicable statutory and regulatory requirements, or if Jason manufactures products containing design or manufacturing defects, demand for its products may decline and Jason may be subject to liability claims.

Jason’s designs, manufacturing processes and facilities need to comply with applicable statutory and regulatory requirements. Jason may also have the responsibility to ensure that products it designs satisfy safety and regulatory standards including those applicable to its customers and to obtain any necessary certifications. In addition, Jason’s customers’ products and the manufacturing processes that Jason uses to produce them are often highly complex. As a result, products that Jason manufactures may at times contain manufacturing or design defects, and its manufacturing processes may be subject to errors or not be in compliance with applicable statutory and regulatory requirements or demands of its customers. Defects in the products Jason manufactures or designs, whether caused by a design, manufacturing or component failure or error, or deficiencies in its manufacturing processes, may result in delayed shipments to customers, replacement costs or reduced or cancelled customer orders. If these defects or deficiencies are significant, Jason’s business reputation may also be damaged. The failure of the products that Jason manufactures or its manufacturing processes and facilities to comply with applicable statutory and regulatory requirements may subject Jason to legal fines or penalties and, in some cases, require Jason to shut down or incur considerable expense to correct a manufacturing process or facility. In addition, these defects may result in liability claims against Jason or expose it to liability to pay for the recall of a product or to indemnify its customers for the costs of any such claims or recalls which they face as a result of using items manufactured by Jason in their products. Even if Jason’s customers are responsible for the defects, they may not assume, or may not have resources to assume, responsibility for any costs or liabilities arising from these defects, which could expose Jason to additional liability claims.

Compliance or the failure to comply with regulations and governmental policies could cause Jason to incur significant expense.

Jason is subject to a variety of local and foreign laws and regulations including those relating to labor and health and safety concerns and import/export duties and customs. Such laws may require Jason to pay mandated compensation in the event of workplace accidents and penalties in the event of incorrect payments of duties or customs. Additionally, Jason may need to obtain and maintain licenses and permits to conduct business in various jurisdictions. If Jason or the businesses or companies it acquires have failed or fail in the future to comply with such laws and regulations, then Jason could incur liabilities and fines and its operations could be suspended. Such laws and regulations could also restrict Jason’s ability to modify or expand its facilities, could require it to acquire costly equipment, or could impose other significant expenditures.

If Jason’s products are subject to warranty claims, its business reputation may be damaged and it may incur significant costs.

Jason generally provides warranties to its customers for manufacturing defects where Jason’s products do not conform to the specifications stipulated by its customers. A successful claim for damages arising as a result of such defects or deficiencies may affect Jason’s business reputation. In addition, a successful claim for which Jason is not insured or where the damages exceed insurance coverage, or any material claim for which insurance coverage is denied or limited and for which indemnification is not available, could have a material adverse effect on Jason’s business, operating results and financial condition. In addition, as Jason pursues new end-markets, warranty requirements will vary and Jason may be less effective in pricing its products to appropriately capture the warranty costs.

17

Table of Contents

Jason is or may be required to obtain and maintain quality or product certifications for certain markets.

In some countries, Jason’s customers require or prefer that it obtain certain certifications for its products and testing facilities with regard to specifications/quality standards. For example, Jason is required to obtain American Railroad Association approval for certain of its products. Consequently, Jason needs to obtain and maintain the relevant certifications so that its customers are able to sell their products, which are manufactured by Jason, in these countries. If Jason is unable to meet and maintain the requirements needed to secure or renew such certifications, it may not be able to sell its products to certain customers and its financial results may be adversely affected.

Jason’s income tax returns are subject to review by taxing authorities, and the final determination of its tax liability with respect to tax audits and any related litigation could adversely affect its financial results.

Although Jason believes that its tax estimates are reasonable and that it prepares its tax filings in accordance with all applicable tax laws, the final determination with respect to any tax audits, and any related litigation, could be materially different from Jason’s estimates or from its historical income tax provisions and accruals. The results of an audit or litigation could have a material effect on operating results and/or cash flows in the periods for which that determination is made. In addition, future period earnings may be adversely impacted by litigation costs, settlements, penalties, and/or interest assessments. Jason is undergoing tax audits in various jurisdictions and it regularly assesses the likelihood of an adverse outcome resulting from such examinations to determine the adequacy of its tax reserves.

Failure of Jason’s customers to pay the amounts owed to it in a timely manner may adversely affect its financial condition and operating results.

Jason generally provides payment terms ranging from 30 to 50 days. As a result, Jason generates significant accounts receivable from sales to its customers, representing 47% and 38% of current assets as of March 28, 2014 and December 31, 2013, respectively. Accounts receivable from sales to customers were $110.4 million and $77.0 million as of March 28, 2014 and December 31, 2013, respectively. As of March 28, 2014, the largest amount owed by a single customer was approximately 10% of total accounts receivable. As of March 28, 2014, Jason’s allowance for doubtful accounts was approximately $2.2 million. If any of Jason’s significant customers have insufficient liquidity, Jason could encounter significant delays or defaults in payments owed to it by such customers, and Jason may need to extend its payment terms or restructure the receivables owed to it, which could have a significant adverse effect on its financial condition. Any deterioration in the financial condition of Jason’s customers will increase the risk of uncollectible receivables. Global economic uncertainty could also affect Jason’s customers’ ability to pay its receivables in a timely manner or at all or result in customers going into bankruptcy or reorganization proceedings, which could also affect Jason’s ability to collect its receivables.

New regulations related to conflict minerals may force Jason to incur additional expenses and affect the manufacturing and sale of its products.

The Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), signed into law on July 21, 2010, includes Section 1502, which requires the SEC to adopt additional disclosure requirements related to certain minerals sourced from the Democratic Republic of Congo and surrounding countries, or “conflict minerals,” for which such conflict minerals are necessary to the functionality of a product manufactured, or contracted to be manufactured, by an SEC reporting company. The metals covered by the final rules, adopted on August 22, 2012, are commonly referred to as “3TG” and include tin, tantalum, tungsten and gold. Implementation of the new disclosure requirements could affect the sourcing and availability of some of the minerals used in the manufacture of Jason’s products. Jason’s supply chain is complex, and if Jason is not able to conclusively verify the origins for all conflict minerals used in its products or that its products are “conflict free,” Jason may face reputational challenges with its customers or investors. Furthermore, Jason may also encounter challenges to satisfy customers who require that its products be certified as “conflict free,” which could place Jason at a competitive disadvantage if it is unable to do so. Additionally, as there may be only a limited number

18

Table of Contents

of suppliers offering “conflict free” metals, Jason cannot be sure that it will be able to obtain necessary metals from such suppliers in sufficient quantities or at competitive prices. Jason could incur significant costs related to the compliance process, including potential difficulty or added costs in satisfying the disclosure requirements. Jason’s first report thereon is expected to be required in 2015.

Jason’s failure to comply with environmental laws could adversely affect its business and financial condition.

Jason is subject to various federal, state, local and foreign environmental laws and regulations, including regulations governing the use, storage, discharge and disposal of hazardous substances used in its manufacturing processes.

Jason is also subject to laws and regulations governing the recyclability of products, the materials that may be included in products, and its obligations to dispose of these products after end-users have finished with them. Additionally, Jason may be exposed to liability to its customers relating to the materials that may be included in the components that Jason procures for its customers’ products. Any violation or alleged violation by Jason of environmental laws could subject it to significant costs, fines or other penalties.

Jason is also required to comply with an increasing number of product environmental compliance regulations focused on the restriction of certain hazardous substances. Non-compliance could result in significant costs and penalties.

In addition, increasing governmental focus on climate change may result in new environmental regulations that may negatively affect Jason, its suppliers and its customers by requiring Jason to incur additional direct costs to comply with new environmental regulations, as well as additional indirect costs as a result of its customers or suppliers passing on additional compliance costs. These costs may adversely affect Jason’s operations and financial condition.

Environmental liabilities that may arise in the future could be material to Jason.