Attached files

| file | filename |

|---|---|

| 8-K - 8-K - NTELOS HOLDINGS CORP. | d766266d8k.htm |

| EX-99.3 - EX-99.3 - NTELOS HOLDINGS CORP. | d766266dex993.htm |

| EX-99.1 - EX-99.1 - NTELOS HOLDINGS CORP. | d766266dex991.htm |

2Q14 Earnings Presentation

July 28, 2014

NASDAQ: NTLS

Exhibit 99.2 |

Presentation of Financial and Other Important Information

2

USE OF NON-GAAP FINANCIAL MEASURES

Included in this presentation are certain non-GAAP financial measures that are

not determined in accordance with US generally accepted accounting

principles (“GAAP”). These financial performance measures are not indicative of cash provided or used by operating activities and

exclude the effects of certain operating, capital and financing costs and may

differ from comparable information provided by other companies, and they

should not be considered in isolation, as an alternative to, or more meaningful than measures of financial performance determined in

accordance with US generally accepted accounting principles. These financial

performance measures are commonly used in the industry and are presented

because NTELOS believes they provide relevant and useful information to investors. NTELOS utilizes these financial

performance measures to assess its ability to meet future capital expenditure and

working capital requirements, to incur indebtedness if necessary,

and

to

fund

continued

growth.

NTELOS

also

uses

these

financial

performance

measures

to

evaluate

the

performance

of

its

business, for budget planning purposes and as factors in its employee compensation

programs. Adjusted EBITDA is defined as net income attributable to NTELOS

Holdings Corp. before interest, income taxes, depreciation and amortization, accretion of asset retirement obligations,

deferred SNA revenue, gain/loss on derivatives, net income attributable to

non-controlling interests, other expenses/income, equity based

compensation charges, business separation charges, certain employee separation

charges, gain/loss on sale of assets, secondary offering costs and net loss

from discontinued operations and costs related to the separation of the wireless and wireline companies.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Any

statements

contained

in

this

presentation

that

are

not

statements

of

historical

fact,

including

statements

about

our

beliefs

and

expectations,

are forward-looking

statements

and

should

be

evaluated

as

such.

The

words

“anticipates,”

“believes,”

“expects,”

“intends,”

“plans,”

“estimates,”

“targets,”

“projects,”

“should,”

“may,”

“will”

and similar words and expressions are intended to identify forward-looking

statements. Such forward-looking statements reflect, among other things,

our current expectations, plans and strategies, and anticipated financial results, all of

which are subject to known and unknown risks, uncertainties and factors that may

cause our actual results to differ materially from those expressed or

implied by these forward-looking statements. Many of these risks are beyond our ability to control or predict. Because of these

risks,

uncertainties

and

assumptions,

you

should

not

place

undue

reliance

on

these

forward-looking

statements.

Furthermore,

forward-looking

statements speak only as of the date they are made. We do not undertake any

obligation to update or review any forward-looking information, whether

as a result of new information, future events or otherwise. Important factors with respect to any such forward-looking statements,

including certain risks and uncertainties that could cause actual results to differ

from those contained in the forward-looking statements, include, but are

not limited to: our ability to attract and retain retail subscribers to our services; our dependence on our strategic relationship

with Sprint Corporation (“Sprint”); a potential increase in roaming rates

and wireless handset subsidy costs; rapid development and intense

competition in the telecommunications industry; our ability to finance, design,

construct and realize the benefits of any planned network technology

upgrade; our ability to acquire or gain access to additional spectrum; the potential to experience a high rate of customer turnover;

the potential for competitors to build networks in our markets; cash and capital

requirements; operating and financial restrictions imposed by our credit

agreement; adverse economic conditions; federal and state regulatory fees, requirements and developments; loss of ability to use

our current cell sites; our continued reliance on indirect channels of retail

distribution; our reliance on certain suppliers and vendors; and other

unforeseen

difficulties

that

may

occur.

These

risks

and

uncertainties

are

not

intended

to

represent

a

complete

list

of

all

risks

and

uncertainties

inherent in our business, and should be read in conjunction with

the more detailed cautionary statements and risk factors included in our SEC

filings, including our most recent Annual Report filed on Form

10-K. |

Agenda

3

Michael Huber, Chairman

Steb Chandor, Chief Financial Officer

Financial and Operational Highlights

Guidance Review

Q&A Session

Management Transition Update |

Rod will be nTelos’s principal executive officer and have responsibility for

day-to-day operations

Michael Huber, Chairman of the nTelos Board of Directors, will assume oversight of

strategic relationships and external communications, including with

investors Management Transition

4

Effective July 28, 2014, Jim Hyde resigned as President & CEO, and from Board

of Directors Rod Dir, currently an nTelos Director, will assume the role of

President and COO Three decades of wireless and telecommunications

experience Former COO of Cincinnati Bell |

Strategic Objectives

5

Implementing our

strategic

relationship with

Sprint to enhance

nTelos’s operations

Strengthening our

retail sales

performance

Improving our

processes and

becoming more

efficient

Increasing the

strategic relevance

of our assets |

Select Second Quarter Developments

6

Renewal of Sprint agreement

Postpay subscriber growth continues while prepay weakens

Retail wireless environment increasingly competitive

4G LTE roll out continues |

Provides access to Sprint’s 800 MHz/1.9 GHz/2.5 GHz spectrum and vendor

relationships Solidifies Sprint relationship through 2022 and allows for

additional collaboration Extended

SNA

Agreement

–

Beneficial

Impact

Contributes significant and recurring wholesale revenues to nTelos

Attracts high-value customers by facilitating a robust LTE experience in SNA

territory Provides 4G LTE nationwide roaming for nTelos retail

customers 7 |

Retail Growth Drivers Going Forward

8

nPower 2.0

Equipment Installment Plan (EIP)

4G LTE roll out

Prepay plan rate resets

Prices as of July 28, 2014 |

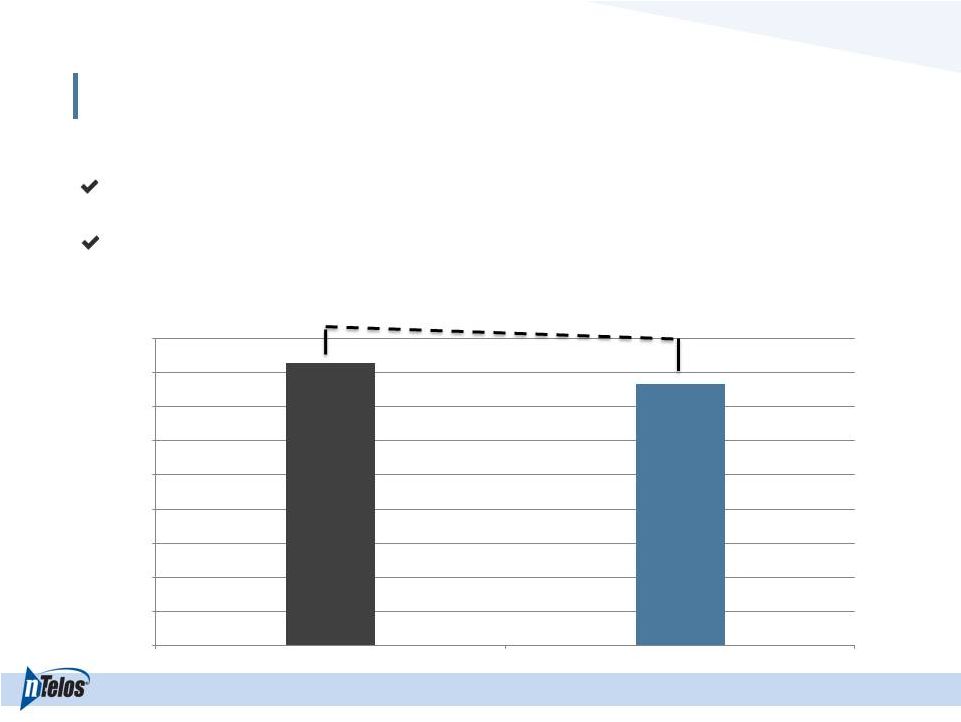

Operating Revenue Remains Steady

9

millions

-2%

2Q14 revenue decreased 2% from 2Q13 to $117.8 million

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

2Q 2013

2Q 2014

Retail

Wholesale & Other |

Retail Revenue Remains Stable

10

millions

+1%

2Q14 retail revenue decreased 2% sequentially and increased 1% from 2Q13 to $79.5

million

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

2Q 2013

2Q 2014 |

Wholesale/Other Revenue Impacted By SNA Rate Reset

11

millions

-8%

2Q14 wholesale/other revenue decreased 8% from 2Q13 to $38.3 million

2Q14 billed SNA revenue decreased 3% from 1Q14 to $38.0 million (reconciliation

provided in earnings release)

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

2Q 2013

2Q 2014 |

Total Subscribers

12

+1%

Subscribers up 1% year-over-year to approximately 458,100

1

Reflects

reduction

of

2,100

postpay

and

8,200

prepay

subscribers

from

Company-initiated

terminations

and

changes

in

business

rules

As of June 30, 2014, postpay subscribers made up 67% of subscriber base

1

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2Q 2013

Prepaid

Subscribers

Postpaid

Subscribers

2Q 2014 |

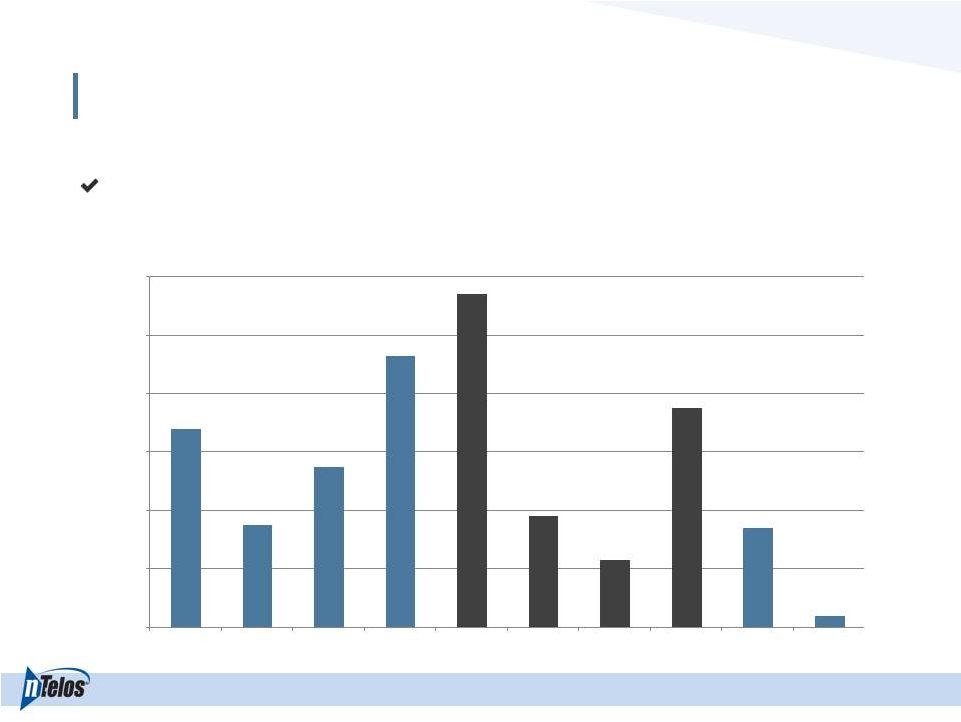

Subscribers –

Net Addition Trend

13

Tenth consecutive quarter of positive net adds

6,800

3,500

5,500

9,300

11,400

3,800

2,300

7,500

3,400

400

0

2,000

4,000

6,000

8,000

10,000

12,000

1Q 2012

2Q 2012

3Q 2012

4Q 2012

1Q 2013

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014 |

Average Revenue Per Account (ARPA)

14

ARPA

Subscribers Per Account

2Q14 ARPA up 3% year-over-year to $137.20

2Q14 postpay subscribers per account of 2.2

+3%

$133.34

$136.90

$136.88

$137.47

$137.20

2.0

2.1

2.2

2.3

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

$140.00

$160.00

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014

Subscribers Per Account |

Operational Expenses

15

($ in millions)

2Q14

2Q13

Cost of sales and services

$47.4

$42.6

Customer operations

$31.3

$30.0

Corporate operations

$9.2

$7.8

Depreciation & Amortization

$19.9

$20.4

Gain on Sale of Intangible Assets

-

($4.4)

$107.9

$96.3

Increase of 12% (or 7% excluding the 2013 one-time gain) driven by higher

retention and network costs |

Adjusted EBITDA

16

millions

Recent EBITDA performance reflects:

Increased network expense associated with LTE upgrade

Increased retention expense driven by upgrades

Steady overall revenues

$41

$46

$27

$34

$34

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

2Q 2013

3Q 2013

4Q 2013

1Q 2014

2Q 2014 |

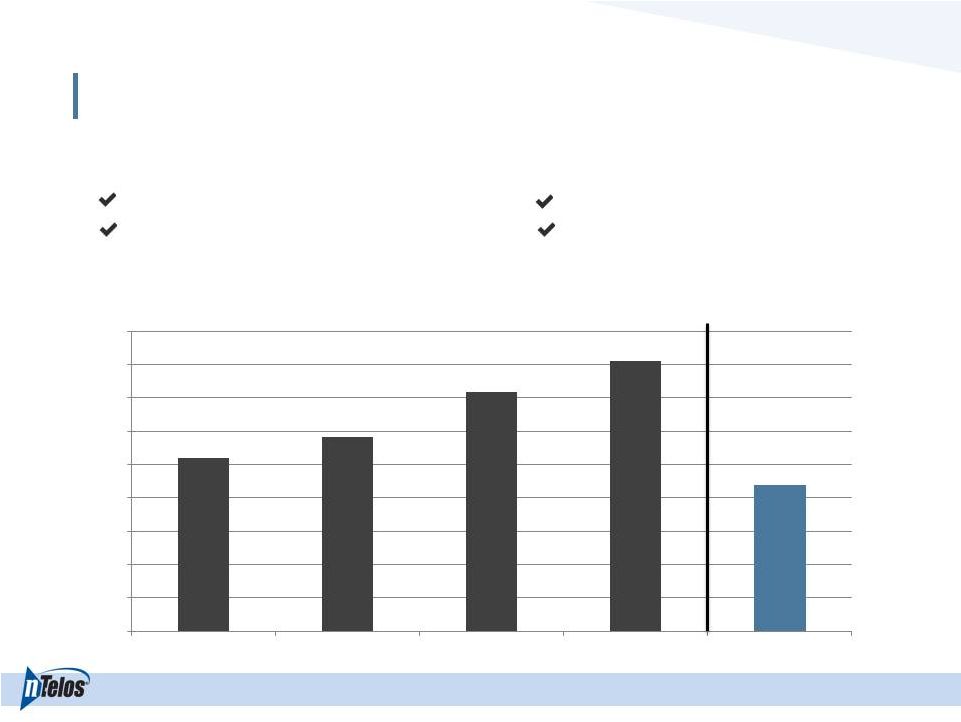

Capital Investment

17

millions

Catalysts:

2011-2012 Cell site expansion

2013-2014 Initial LTE deployment

Status:

1,445 cell sites as of June 30, 2014

LTE network covers over 2.8 million POPs

$52

$58

$72

$81

$44

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

FY 2010

FY 2011

FY 2012

FY 2013

YTD 2014 |

Capitalization Overview

($ in millions)

June 30, 2014

Cash, unrestricted

$108.3

Total Debt

$527.8

Net Debt

$419.5

LTM Adjusted EBITDA

$140.6

Secured Term Loan

$526.9

Net Debt Leverage

3.0x

18 |

Guidance (as of July 28, 2014)

19

For the year ended December 31, 2014 (unchanged):

Adjusted

EBITDA

of

$128

-

$135

million

CapEx

of

$110

-

$120

million |

Summary

20

Implementing our

strategic

relationship with

Sprint to enhance

nTelos’s operations

Strengthening our

retail sales

performance

Improving our

processes and

becoming more

efficient

Increasing the

strategic relevance

of our assets |

Questions & Answers |

Appendix |

Adjusted EBITDA Reconciliation

23

NTELOS Holdings Corp.

Reconciliation of Net Income Attributable to NTELOS Holdings Corp. to Adjusted EBITDA

(In thousands)

2Q14

1Q14

4Q13

3Q13

2Q13

Net Income Attributable to NTELOS Holdings Corp.

484

$

1,286

$

(784)

$

10,583

$

9,386

$

Net income attributable to noncontrolling interests

373

436

403

588

541

Net Income

857

1,722

(381)

11,171

9,927

Interest expense

8,315

7,959

7,504

7,480

7,398

Income taxes

640

1,110

80

8,340

6,380

Other expense (income), net

92

1,072

161

431

(151)

Operating income

9,904

11,863

7,364

27,422

23,554

Depreciation and amortization

19,929

19,067

17,486

16,559

20,443

Gain on sale of intangible assets

-

-

-

-

(4,442)

Accretion of asset retirement obligations

331

315

171

135

173

Equity-based compensation

1,283

1,311

1,330

1,442

1,460

SNA Straight Line Adjustment

2,043

1

-

-

-

-

Other

874

2

1,367

3

375

4

-

-

Adjusted EBITDA

34,364

$

33,923

$

26,726

$

45,558

$

41,188

$

See Form 8-K filed with the SEC on March 18, 2014 for

additional information. 4

4Q13 $0.4 million related to secondary offering cost.

3

2014 includes $1.4 million charge related to certain employee separation

expenses. 1

Adjustment for impact of recognizing a portion of the billed SNA contract on a

straight line basis 2

2Q 2014 includes $0.9 million legal costs related to new Sprint agreement.

|

ARPA Reconciliation

24

ARPA Reconciliation - Postpay

Average Monthly Revenue per Account (ARPA) ¹

2Q14

1Q14

4Q13

3Q13

2Q13

FY 2013

FY 2012

(In thousands, except for accounts and ARPA)

Operating revenues

117,795

$

122,082

$

121,766

$

130,912

$

119,859

$

491,882

$

453,989

$

Less: prepay service revenues

(16,206)

(16,960)

(16,956)

(16,478)

(16,182)

(65,300)

(58,036)

Less: equipment revenues

(6,560)

(7,491)

(6,573)

(6,541)

(5,499)

(25,251)

(30,078)

Less: wholesale and other adjustments

(37,900)

(40,018)

(40,525)

(50,142)

(41,179)

(172,764)

(165,765)

Postpay service revenues

57,129

$

57,613

$

57,712

$

57,751

$

56,999

$

228,567

$

200,110

$

Average number of postpay accounts

138,800

139,700

140,500

140,600

142,500

141,700

141,700

Postpay ARPA

137.20

$

137.47

$

136.88

$

136.90

$

133.34

$

134.43

$

117.65

$

¹

Average

monthly

revenue

per

account

(ARPA)

is

computed

by

dividing

postpay

service

revenues

per

period

by

the

average

number

of

postpay

accounts

during

that

period.

As

defined,

ARPA

may

not

be

similar

to

ARPA

measures

of

other

companies,

is

not

a

measurement

under

GAAP

and

should

be

considered

in

addition

to,

but

not

as

a

substitute

for,

the

information

contained

in

the

Company’s

consolidated

Income

Statement.

The

Company

closely

monitors

the

effects

of

new

rate

plans

and

service

offerings

on

ARPA

in

order

to

determine

their

effectiveness.

ARPA

provides

management

useful

information

concerning

the

appeal

of

NTELOS

rate

plans

and

service

offerings

and

the

Company’s performance in attracting and retaining high-value customers.

|

2Q14 Earnings Presentation

July 28, 2014

NASDAQ: NTLS |