Attached files

| file | filename |

|---|---|

| 8-K - 8-K - POPULAR, INC. | d764133d8k.htm |

Exhibit 99.1 |

The

information contained in this presentation includes forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995. These forward-looking statements are

based on management’s current expectations and involve risks and

uncertainties that may cause the Company's actual results to differ materially

from any future results expressed or implied by such forward-looking

statements. Factors that may cause such a difference include, but are not

limited to (i) the rate of growth in the economy and employment levels, as well as

general business and economic conditions; (ii) changes in interest rates, as well

as the magnitude of such changes; (iii)

the

fiscal

and

monetary

policies

of

the

federal

government

and

its

agencies;

(iv)

changes

in

federal

bank

regulatory and supervisory policies, including required levels of capital; (v) the

relative strength or weakness of the consumer and commercial credit sectors

and of the real estate markets in Puerto Rico and the other markets in which

borrowers are located; (vi) the performance of the stock and bond markets; (vii) competition in the financial

services industry; (viii) possible legislative, tax or regulatory changes; (ix) the

impact of the Dodd-Frank Act on our businesses, business practice and

cost of operations; and (x) additional Federal Deposit Insurance Corporation

assessments. Other than to the extent required by applicable law, the Company

undertakes no obligation to publicly update or revise any

forward-looking statement. Please refer to our Annual Report on Form 10-K for the

year ended December 31, 2013 and other SEC reports for a discussion of those

factors that could impact our future results.

The

financial

information

included

in

this

presentation

for

the

quarter

ended

June

30,

2014

is

based

on

preliminary unaudited data and is subject to change.

Forward Looking Statements

1 |

NPLs increased by $4 million QoQ; ratio at 3.3%

NPL inflows excluding consumer loans down $54 million QoQ

NCOs

of

0.94%

compared

to

0.80%

last

quarter;

increase

of

$3

million

Reported

adjusted

net

income

of

$86

million

1

Strong

margins:

Popular,

Inc.

4.68%

2

adjusted;

BPPR 5.50%

Credit

(excluding

covered loans)

Capital

Earnings

Completed TARP repayment on July 2, 2014

2

1

GAAP Net Loss of $511 million. See appendix for a non GAAP to GAAP

reconciliation 2

Excludes

impact

of

$414

million

TARP

discount

amortization.

GAAP

Net

Income

Interest

Margin

of

(0.77%).

See

appendix

for

a

non

GAAP

to

GAAP

reconciliation |

TARP

& Capital-Update 3

Minimum Well

Capitalized Ratio

Q2 2014 Ratio

Pro-forma

Q2 2014 Exc. Tarp

3

Received approval for full TARP repayment without additional equity

Financed TARP repayment with existing holding company liquidity and the

proceeds from senior note offering

$450 million 5 year 7% senior unsecured

Hold Co. liquidity approximately $175 million post TARP; debt service coverage in

excess of 2 years with no maturities until 2019

Robust capital; Pro-forma Tier1 Common Equity ratio of 13.8%

Common

Tier

1

Capital

*

Tier 1 Capital

Total Capital

Leverage

5.0%

6.0%

10.0%

5.0%

13.5%

19.4%

20.7%

13.2%

13.8%

15.8%

17.1%

10.5%

*Actual and pro-forma Common Tier 1 Capital includes $414 million of

accelerated discount amortization related to the subsequent $935 million TARP repayment

|

BPNA

Restructuring-Update •

California, Illinois and Central Florida transactions are on pace to close by YE

2014 Strategic focus going forward on NY metro and South Florida

regions Non cash goodwill write-down in Q2 of $187 million

•

US operational restructuring initiative progress also on track with expected

completion during Q1 2015

•

Continue to look at all remaining components of BPNA balance sheet for

opportunities to manage credit exposures and capital

Lower

risk

profile

and

smaller

balance

sheet

to

yield

additional

capital

4 |

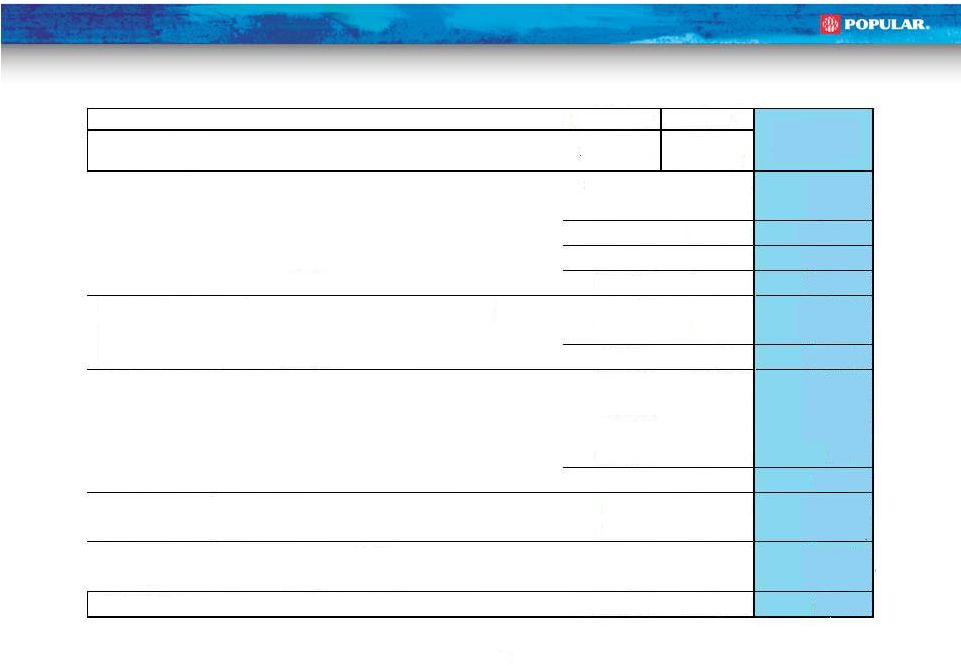

Financial Summary (unaudited)

5

See appendix for a non GAAP to GAAP reconciliation

Q2 2014

Q1 2014

Non GAAP

GAAP

In thousands

Adjusted

As

Reported

Net interest income

$354,687

$351,171

$3,516

Non Interest Income

118,050

120,238

(2,188)

Total revenues before FDIC loss share impact

472,737

471,409

1,328

FDIC loss-share income (expense)

(55,261)

(24,206)

(31,055)

Gross revenues

417,476

447,203

(29,727)

Provision for loan losses (excluding covered loans)

50,074

54,122

(4,048)

Provision for loan losses (covered loans)

11,604

25,714

(14,110)

Total provision for loan losses

61,678

79,836

(18,158)

Net revenues

355,798

367,367

(11,569)

Personnel costs

99,100

104,301

(5,201)

Other real estate owned (OREO) expenses

3,410

6,440

(3,030)

Other operating expenses

168,355

166,858

1,497

Total operating expenses

270,865

277,599

(6,734)

Income from continuing operations before tax

84,933

89,768

(4,835)

Income tax expense

10,400

23,264

(12,864)

Net Income from continuing operations

74,533

66,504

8,029

Income from discontinued operations, net of tax

11,634

19,905

(8,271)

Net income

$86,167

$86,409

($242)

Adjusted

Variance |

Capital

**Excess

capital

over

“well

capitalized”

Basel

I

threshold

*Averages

for

30

bank

holding

Companies

with

$50

billion

or

more

of

total

consolidated

assets,

consisting

of

19

firms

included

in

Comprehensive

Capital

Analysis

and

Review

(CCAR) and 11 firms included in Capital Plan Review (CapPR). Source SNL Financial

& FactSet.

Tier

1

Common

Equity

capital

ratio

of

13.5%

1

exceeds

current

CCAR

5%

target

by $2.0 billion

We

expect

to

remain

“well-capitalized”

under

Basel

III

rules

issued

by

the

Federal

Reserve

Capital Ratio %

Excess capital in $, billions

6

1

Pro-froma Tier 1 Common Equity capital ratio excluding TARP is 13.8%

13.5

19.4

20.7

10.3

10.9

12.1

14.8

8.7

Tier 1 Common

Tier 1 Capital

Total Capital

Tangible Common

Equity

BPOP Q2 2014

CCAR & CapPR Q1 2014 *

$2.0

$3.2

$2.6

Tier 1 Common

Tier

1

Capital

**

Total

Capital

** |

Non

Performing Assets •

NPLs HIP increased slightly by $4 million QoQ

•

NPAs, including covered loans, remained

flat at $956 million, QoQ

Overall stable led by strong credit quality in the US operations

7

*Q2 2014 NPL’s and NPL/total loans ratio excludes discontinued operations

Non-Performing Assets ($MM)

Non-Performing Loans ($MM)

Covered NPLs decreased $8 million, reflective

of continued resolution efforts

NPL HFS increased $4 million QoQ

OREOs flat at $295 million vs. $296 million in

Q1 2014

$41

million

increase

in

PR,

mostly

mortgage

NPLs

$37

million

decline

in

US

operations

-

$28 million decline in commercial NPLs, driven by sales

and credit improvements

-

$10 million decline related to discontinued operations

932

971

1,142

852

866

1,026

1,101

1,293

1,500

2,084

2,245

2,402

2,448

2,539

2,623

2,489

2,314

2,277

2,254

2,365

2,311

2,178

2,120

2,002

1,419

992

944

956

956

2.1%

2.4%

1.9%

2.1%

2.5%

2.7%

3.3%

4.0%

5.7%

6.3%

6.9%

7.2%

6.0%

6.4%

6.4%

6.0%

5.8%

5.9%

6.3%

6.2%

5.9%

5.8%

5.5%

3.8%

2.7%

2.6%

2.6%

2.6%

2.6%

598

858

1,008

771

781

923

1,028

1,203

1,404

1,978

2,116

2,276

2,313

2,330

2,344

1,572

1,614

1,625

1,732

1,738

1,682

1,563

1,550

1,425

1,051

614

618

635

640

2.7%

3.1%

2.8%

2.9%

3.5%

3.9%

4.7%

5.6%

8.0%

8.7%

9.6%

10.0%

10.4%

10.6%

7.6%

7.9%

7.9%

8.4%

8.4%

8.2%

7.6%

7.5%

6.8%

4.9%

2.9%

2.9%

2.8%

2.9%

3.3%

Metrics exclude covered loans |

Total NPL Inflows ($MM)

NPL Inflows

•

Total NPL inflows down by $54 million, or 26%

QoQ

•

PR mortgage NPL inflows increased by $16

million QoQ

Mortgage NPL Inflows ($MM)

Commercial,

Construction

&

Legacy

NPL

Inflows

($MM)

Excludes consumer loans

Metrics exclude covered loans

8

PR commercial inflows down $63 million;

Q1 2014 included $52 million impact of a

single credit relationship that continues

current

US commercial inflows down $8 million

79

77

76

48

45

42

26

22

22

22

10

19

11

119

222

101

93

65

100

43

48

59

42

32

94

31 |

NCO

($MM) and NCO-to-Loan Ratio Metrics exclude covered loans

Provision ($MM) and Provision-to-NCO Ratio

9

690

693

690

665

649

636

622

584

529

526

538

543

526

129%

285%

42%

82%

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

Q1 14

Q2 14

ALLL

ALLL/NCO

ALLL/NPL

133

135

126

108

98

96

101

81

79

58

35

43

46

163

200

2.59%

0.94%

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

Q1 14

Q2 14

NCO

NPL Sale Charge-offs

NCO%

NPL Sale NCO%

96

151

124

83

82

84

86

58

55

55

48

47

50

149

169

72%

108%

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

Q1 14

Q2 14

PLL

NPL Sale PLL

PLL/NCO

NCOs increased slightly by $3 million QoQ

Q1 2014 included the effect of net recoveries in the US;

NCOs continue to track favorably

NCO ratio of 0.94% vs. 0.80% in Q1 2014; results

impacted by reclassification of the discontinued operations

Provision increased slightly by $3 million; $50 million in Q2

2014 vs. $47 million in Q1 2014

Provision to NCO of 108%, compared to 110% in Q1 2014

ALLL decreased by $16 million QoQ; ALLL to loans at

2.68% vs. 2.51% in Q1 2014

$28 million release

in the US

$20 million decrease related to the transfer to LHFS in the discontinued

operations

$32 million increase in PR

ALLL to NPL coverage ratio stable at 82% in Q2 2014 vs.

85% in Q1 2014

Asset Quality

ALLL ($MM), ALLL-to-NCO and ALLL-to-NPL Ratios NPL

Sale PLL/NCO |

PR

Public Sector Exposure •

Loans to the Government of Puerto

Rico and Public Corporations are

either collateralized loans or

obligations that have a specific

source of income or revenues

identified for their repayment

10

•

Loans to various municipalities

backed by unlimited taxing power

or real and personal property taxes

collected within such municipalities

•

Our current direct exposure to the PR government, instrumentalities and

municipalities is $833 million, of which approximately $709 million is

outstanding, down $235 million QoQ PR Central Government &

Public Corporations

Municipalities

•

Indirect exposure of loans or

instruments that are payable by non-

governmental entities and have a

government guarantee to cover any

shortfall in collateral in the event of

borrower default. Majority are single-

family mortgage related.

Indirect Exposure

(In millions)

Loans

Securities

Total

Central Government

-

76

76

Public Corporations

PRASA

100

1

101

PREPA

75

-

75

PRHTA

-

-

-

OTHER

21

-

21

Total Central Govt & Public Corp.

196

77

273

as % of Tier 1 Capital

6%

Municipalities

374

62

436

Direct Government Exposure

570

139

709

Indirect Exposure

312

48

360 |

Driving

Shareholder Value 11

Capital

Earnings

Additional

Value

•

Robust capital with Tier 1 Common Equity of 13.5%

•

TARP repayment and BPNA transactions move us toward a more

active capital management process

•

Unique franchise in PR provides strong, stable revenue-

generating capacity

•

Continued stability in Popular’s credit metrics

•

EVTC ownership, BHD stake and restructured US operations

11 |

APPENDIX

APPENDIX |

Who We

Are – Popular, Inc.

Franchise

Franchise

•

Financial services company

•

Headquartered in San Juan, Puerto Rico

•

$37 billion in assets (top 40 bank holding

company in the U.S.)

•

$23 billion in total loans

•

$25 billion in total deposits

•

270 branches serving customers in Puerto

Rico, New York, California, Florida, Illinois,

U.S. Virgin Islands, and New Jersey

•

NASDAQ ticker symbol: BPOP

•

Market

Cap:

$3.54

billion

1

As of June 30, 2014

*Doing business as Popular Community Bank.

Summary

Summary

Corporate

Structure

Assets = $36.6 bn

Popular Auto,

Inc.

Banco Popular

de Puerto Rico

Popular

Securities, Inc.

Assets = $27 .6 bn

Assets = $8.3bn

Banco Popular

North America*

Puerto Rico operations

Selected equity investments

(first two under “corporate”

segment and third and fourth under PR):

Popular

Insurance, Inc.

Popular North

America, Inc.

U.S. banking operations

Transaction processing,

business processes

outsourcing

14.8% stake

Adjusted EBITDA of $181.2

million for the twelve months

ended March 31, 2014

Dominican

Republic bank

15.82% stake

2013

approximate net

income $111

million

PRLP 2011 Holdings

Construction and

commercial loans vehicle

24.9% stake

PR Asset Portfolio 2013-1

International, LLC

Construction, commercial

loans and OREOs vehicle

24.9% stake

13

1 |

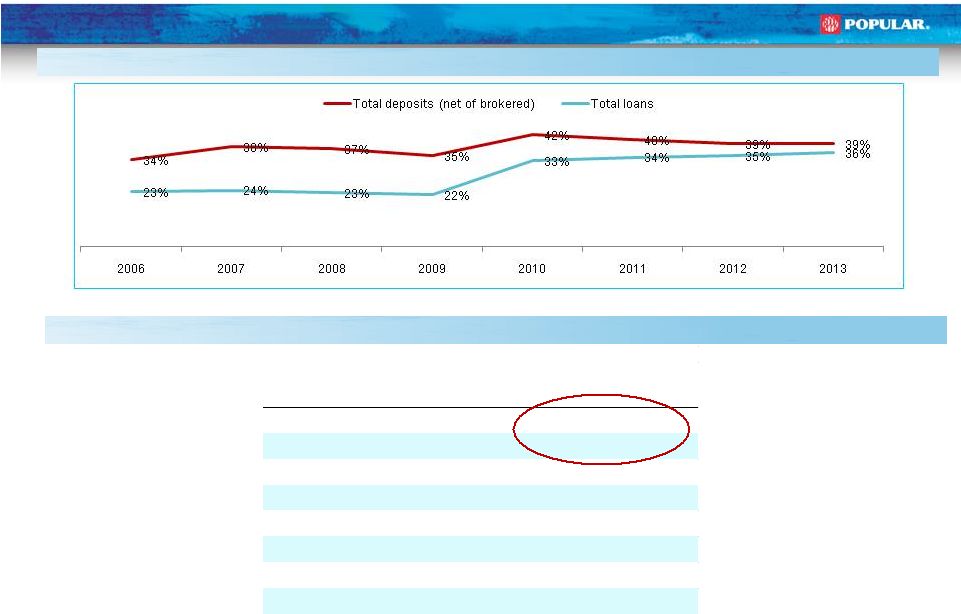

Market

Leadership in Puerto Rico Popular’s Market Share Trend

Puerto Rico Market Share by Category

14

Total Deposits (Net of Brokered)

1

39%

Total Loans

1

36%

Commercial & Construction Loans

1

39%

Credit Cards

1

52%

Mortgage Loan Production

1

31%

Personal Loans

1

31%

Auto Loans/Leases

3

17%

Assets Under Management

3

15%

Category

Market

Position as of

Q1 2014

Market Share

as of Q1 2014

Source: Puerto Rico Office of the Commissioner of Financial Institutions & 10K

reports; Mortgage origination data is not publicly available; Figures

presented for BPPR and competitors were provided internally; Personal Loans:

As a group, Credit Unions represent the largest competitor with 52% market

share (115 Credit Unions were in business as of March 30, 2014 guaranteed by

COSSEC) |

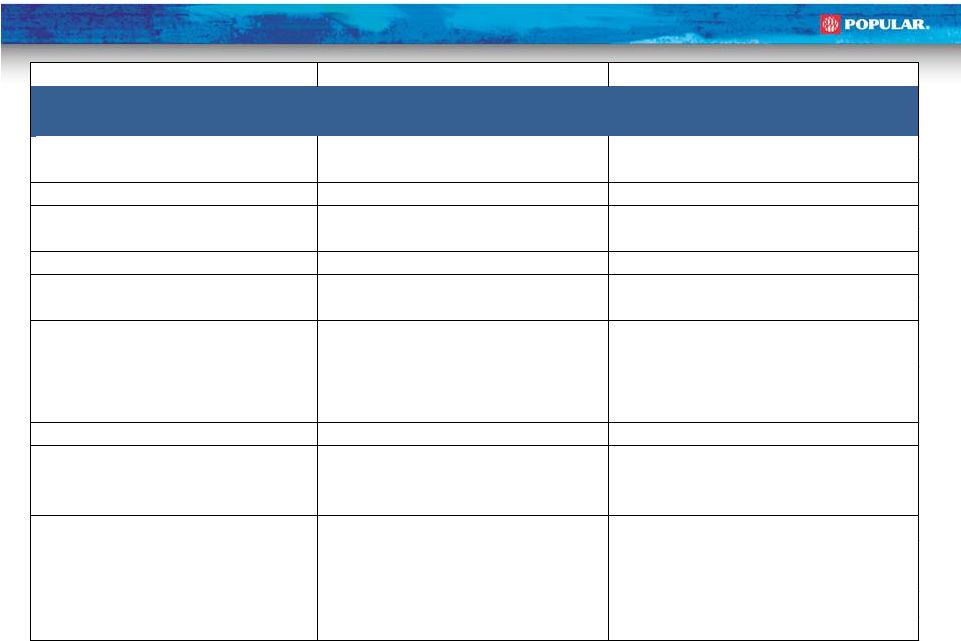

PR

& US Business 15

1

Excludes covered loans

2

Excludes discontinued operations as of June 30, 2014

$ in millions (unaudited)

Q2 2014

Q1 2014

Variance

Q2 2014

Q1 2014

Variance

Net Interest Income

$334

$328

$6

$49

$51

($2)

Non Interest Income

38

68

(30)

18

11

7

Gross Revenues

372

396

(24)

67

62

5

Provision (non-covered)

74

54

20

(25)

-

(25)

Provision (covered)

12

26

(14)

-

-

-

Provision for loan losses

86

80

6

(25)

-

(25)

Operating expenses

223

221

2

40

40

-

Income tax

(8)

30

(38)

1

1

-

Net Income from continuing

operations

71

65

6

51

21

30

(Loss) Income from discontinued

operations, net of tax

-

-

-

(182)

20

(202)

Net Income (loss)

$71

$65

$6

($131)

$41

($172)

NPLs (HIP) ¹

$574

$532

$42

$66

$103

($37)

NPLs (HIP + HFS) ¹

574

533

$41

70

103

(33)

Loan loss reserve ¹

466

435

$31

60

108

(48)

Assets

2

$27,647

$27,734

($87)

$8,299

$8,793

($494)

Loans (HIP) 2

18,590

18,831

(241)

3,779

5,649

(1,870)

Loans (HIP + HFS)

2

18,683

18,924

(241)

3,784

5,651

(1,867)

Deposits

2

21,144

21,245

(101)

3,819

6,067

(2,248)

NIM

5.50%

5.49%

0.01%

3.25%

3.41%

-0.16%

PR

US |

1

Covered

loans

represent

loans

acquired

in

the

Westernbank

FDIC-assisted

transaction

that

are

covered

under

FDIC

loss

sharing

agreements.

2

Total

Basic

and

diluted

EPS,

including

discontinued

operations

was

$(4.98)

3 Excludes impact of $414 million TARP discount amortization. GAAP Net Income

Interest Margin of (0.77%). 16

GAAP Reconciliation Q2 2014

(Unaudited)

US GAAP

Non GAAP

(In thousands)

Actual

Tarp discount

amortization and

Income Tax

adjustments

Goodwill

impairment and

restructuring

charges

Adjusted

Net interest (expense) income

$ (59,381)

$

(414,068) $ 354,687

Provision

for

loan

losses

–

non-covered

loans

50,074

-

-

50,074

Provision

for

loan

losses

–

covered

loans

1

11,604

-

-

11,604

Net interest (expense) income after provision for loan losses

(121,059)

(414,068)

-

293,009

FDIC loss share income (expense)

(55,261)

-

-

(55,261)

Other non-interest income

118,050

-

-

118,050

Operating expenses

275,439

-

4,574

270,865

(Loss) income from continuing operations before income tax

(333,709)

(414,068)

(4,574)

84,933

Income tax (benefit) expense

(4,124)

(14,524)

10,400

(Loss) income from continuing operations

$ (329,585)

$

(399,544)

$

(4,574) $ 74,533

(Loss) income from discontinued operations, net of tax

$ (181,729)

$

-

$ (193,363)

$ 11,634

Net (loss) income

$ (511,314)

$

(399,544) $ (197,937)

$ 86,167

EPS from continuing operations-Basic

(3.21)

$

2

EPS from continuing operations-Diluted

(3.21)

$

2

NIM, adjusted

4.68%

3

Tangible book value per share (quarter end)

35.84

$

Market price (quarter end)

34.18

$

-

$ |

Consolidated Credit Summary (Excluding Covered Loans)

1

Excluding provision for loan losses and net write-downs related to the asset

sale $ in millions

Q2 13

Loans Held in Portfolio (HIP)

$19,635

$21,612

$21,612

$21,427

$21,522

Performing HFS

93

94

109

123

180

NPL HFS

4

1

1

2

11

Total Non Covered Loans

19,732

21,707

21,722

21,552

21,713

Non-performing loans (NPLs)

$640

$635

$598

$618

$614

Commercial

$281

$310

$282

$320

$328

Construction

$22

$22

$24

$29

$45

Legacy

$8

$12

$15

$24

$28

Mortgage

$286

$252

$233

$203

$172

Consumer

$43

$39

$44

$42

$41

NPLs HIP to loans HIP

3.26%

2.94%

2.77%

2.88%

2.85%

Net charge-offs (NCOs)

$46

$43

$35

$58

$79

Commercial

$12

$12

$16

$21

$41

Construction

($1)

($2)

($2)

($5)

($2)

Legacy

($1)

($5)

($5)

$2

($1)

Mortgage

$10

$9

$8

$13

$16

Consumer

$26

$28

$18

$27

$26

Write-downs bulk sale

$0

$0

$0

$0

$200

Write-downs discontinued operations

$20

NCOs to average loans HIP

0.94%

0.80%

0.66%

1.08%

1.47%

1

Provision for loan losses (PLL)

$50

$47

$48

$55

$55

1

PLL to average loans HIP

1.02%

0.88%

0.89%

1.03%

1.02%

1

PLL to NCOs

1.08x

1.10x

1.35x

0.95x

0.69x

1

Allowance for loan losses (ALL)

$526

$543

$538

$526

$529

ALL to loans HIP

2.68%

2.51%

2.49%

2.46%

2.46%

ALL to NPLs HIP

82.26%

85.40%

90.05%

85.19%

86.14%

Q2 14

Q1 14

Q4 13

Q3 13

17 |

De-risked Loan Portfolios

•

PR has derisked its commercial loan

portfolio by reducing its exposure in asset

classes with historically high loss content

Commercial portfolio, including

construction, has decreased from 55%

of total loans held-in-portfolio to 41%

Construction portfolio is down by 89%

since Q4 2007

SME1 lending is down by 55% from

Q4 2007

•

Collateralized exposure now represents a

larger portion of consumer loan portfolio

•

Unsecured loans credit quality has

improved as overall FICO scores have

increased

Loan Composition (Held-in Portfolio)

1

Small and Medium Enterprise

2

NCOs

distribution

represents

the

percentage

allocation

of

NCOs

from

Q1

2008

through

Q2

2014

per

each

loan

category

Legacy portfolio is comprised of certain commercial, construction and lease financings lending

products exited by the US. PR Commercial & Construction

Distribution 18

$ in millions

Q4 2007

Q2 2014

Q4 2007

Q2 2014

Q4 2007

Q2 2014

Variance

Commercial

$7,774

$6,299

$4,515

$1,857

$12,288

$8,156

($4,133)

Consumer

3,552

3,416

1,698

510

5,249

3,926

(1,323)

Mortgage

2,933

5,458

3,139

1,206

6,071

6,664

593

Construction

1,231

136

237

43

1,468

179

(1,289)

Leases

814

547

-

-

814

547

(267)

Legacy

-

-

2,130

163

2,130

163

(1,967)

Total

$16,304

$15,856

$11,718

$3,779

$28,021

$19,635

($8,386)

Puerto Rico

US

Total

NCOs

($mm)

(%)

($mm)

(%)

($mm)

(%)

Distribution

CRE SME

$2,938

33%

$1,541

24%

($1,397)

-48%

23%

C&I SME

1

2,287

25%

827

13%

(1,460)

-64%

28%

C&I Corp

1,592

18%

1,915

30%

323

20%

6%

Construction

1,231

14%

136

2%

(1,095)

-89%

37%

CRE Corp

892

10%

1,955

30%

1,063

119%

4%

Multifamily

64

1%

62

1%

(2)

-3%

2%

Total

$9,004

$6,436

($2,568)

-29%

100%

Q4 2007

Q2 2014

Variance

1

2 |

Popular, Inc. Credit Ratings

•

Our senior unsecured ratings have remained stable:

•

Moody’s:

B2

Negative (Revised May 2014)

•

Fitch:

BB-

Stable Outlook (Reaffirmed December 2013)

•

S&P:

B+

Stable Outlook

•

May 2014: Moody’s downgraded BPOP to B2; outlook revised to negative

•

February 2014: Moody's placed BPOP on review for downgrade

•

October 2013: Moody’s revised outlook to negative

•

January

2013:

Fitch

raised

to

BB-

from

B+;

outlook

revised

to

stable

•

December 2012: Moody’s downgraded BPOP to B1; stable outlook assigned

•

April 2012: Moody’s placing most of the PR banks under review with the

possibility of downgrades, due to the state of the Puerto Rico economy

•

January 2012: Fitch raised BPOP’s outlook to positive

•

December

2011:

S&P

raised

its

ratings

on

BPPR

to

BB

from

BB-

and

changed

outlook to stable given revised bank criteria to regional banks

19

19 |

|