Attached files

| file | filename |

|---|---|

| 8-K - 8-K - SIMON PROPERTY GROUP INC /DE/ | a2220794z8-k.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

Exhibit 99.1

SIMON PROPERTY GROUP

EARNINGS RELEASE & SUPPLEMENTAL INFORMATION

UNAUDITED SECOND QUARTER 2014

- (1)

- Includes reconciliation of consolidated net income to funds from operations.

| 2Q 2014 SUPPLEMENTAL |

|

1 |

| CONTACTS: | ||

| Liz Zale | 212-745-9623 Investors | |

| Les Morris | 317-263-7711 Media | |

FOR IMMEDIATE RELEASE

SIMON PROPERTY GROUP REPORTS SECOND QUARTER 2014 RESULTS AND

RAISES FULL YEAR 2014 GUIDANCE

INDIANAPOLIS, July 23, 2014 - Simon, a leading global retail real estate company, today reported results for the quarter and six months ended June 30, 2014.

RESULTS FOR THE QUARTER

- •

- Funds from Operations ("FFO") was $783.8 million, or $2.16 per diluted share, as compared to $766.3 million,

or $2.11 per diluted share, in the prior year period. Included in the second quarter 2014 results are $0.10 per diluted share of transaction costs related to the Washington Prime Group Inc.

("WPG") spin-off.

- •

- Net income attributable to common stockholders was $406.6 million, or $1.31 per diluted share, as compared to $339.9 million, or $1.10 per diluted share, in the prior year period.

RESULTS FOR THE SIX MONTHS

- •

- Funds from Operations ("FFO") was $1.649 billion, or $4.54 per diluted share, as compared to $1.508 billion,

or $4.16 per diluted share, in the prior year period.

- •

- Net income attributable to common stockholders was $748.2 million, or $2.41 per diluted share, as compared to $623.1 million, or $2.01 per diluted share, in the prior year period.

EFFECT OF WASHINGTON PRIME GROUP INC. SPIN-OFF

- •

- Results for the three months ended June 30, 2014 and 2013 include FFO per diluted share of $0.15 and $0.24,

respectively, from the WPG properties. Results for the six months ended June 30, 2014 and 2013 include FFO per diluted share of $0.40 and $0.48, respectively, from the WPG properties.

- •

- Excluding the WPG properties and the transaction costs related to the spin-off, growth in FFO per diluted share for the three and six month periods in 2014 was 12.8% and 15.2%, respectively.

| 2Q 2014 SUPPLEMENTAL |

|

2 |

EARNINGS RELEASE

"I am very pleased with our quarterly results as our strong momentum continued, with 5.6% quarterly growth in comparable property net operating income," said David Simon, Chairman and CEO. "It was also an eventful quarter with our completion of the Washington Prime Group spin-off and the re-launch of our brand. Based upon our results to date and expectations for the remainder of 2014, we are again increasing our full-year 2014 guidance."

COMPARABLE PROPERTY NET OPERATING INCOME

Comparable property NOI growth for the three months ended June 30, 2014 was 5.6%. The year-to-date growth for the six months ended June 30, 2014 was 5.5%. Comparable properties include U.S. Malls, Premium Outlets and The Mills, and excludes the WPG properties.

U.S. MALLS AND PREMIUM OUTLETS OPERATING STATISTICS

| |

AS OF JUNE 30, 2014 (1) |

AS PREVIOUSLY REPORTED JUNE 30, 2013 |

CHANGE | |||||

|---|---|---|---|---|---|---|---|---|

Occupancy (2) |

96.5% | 95.1% | +140 bps | |||||

Base Minimum Rent per sq. ft. (2) |

$ | 45.83 | $ | 41.41 | +10.7% | |||

Releasing Spread per sq. ft. (2)(3) |

$ | 11.06 | $ | 7.49 | +$3.57 | |||

Releasing Spread (percentage change) (2)(3) |

20.0% | 14.1% | +590 bps | |||||

Total Sales per sq. ft. (4) |

$ | 608 | $ | 577 | +5.4% | |||

- (1)

- Excludes Washington Prime Group Inc. properties.

- (2)

- Represents mall stores in Malls and all owned square footage in Premium Outlets.

- (3)

- Same space measure that compares opening and closing rates on individual spaces leased during trailing 12-month period.

- (4)

- Trailing 12-month sales per square foot for mall stores less than 10,000 square feet in Malls and all owned square footage in Premium Outlets.

DIVIDENDS

Today we announced that the Board of Directors declared a quarterly common stock dividend of $1.30 per share. This is a year-over-year increase of 13%. The dividend will be payable on August 29, 2014 to stockholders of record on August 15, 2014.

Simon's Board of Directors also declared the quarterly dividend on its 83/8% Series J Cumulative Redeemable Preferred Stock (NYSE: SPGPrJ) of $1.046875 per share, payable on September 30, 2014 to stockholders of record on September 16, 2014.

| 2Q 2014 SUPPLEMENTAL |

|

3 |

EARNINGS RELEASE

DEVELOPMENT ACTIVITY

On April 24th, we opened a 147,000 square foot, 50-store expansion of Desert Hills Premium Outlets that was 100% leased. The expansion features high-quality designer and name brands, many of which are the first in North America or unique to the region.

During the second quarter, construction started on three significant redevelopment and expansion projects:

- •

- The Fashion Centre at Pentagon City in Arlington (Washington, DC), Virginia - redevelopment and a 50,000 square

foot small shop expansion including restaurants

- •

- Chicago Premium Outlets in Aurora (Chicago), Illinois - 260,000 square foot expansion

- •

- Shisui Premium Outlets in Shisui (Chiba), Japan - 130,000 square foot expansion

Redevelopment and expansion projects, including the addition of new anchors, are underway at 32 properties in the U.S., Asia and Mexico.

Charlotte Premium Outlets in Charlotte, North Carolina will open on July 31st. The center will serve the greater Charlotte area and is fully leased with 400,000 square feet and 100 outlet stores featuring high-quality designer and name brands. Simon owns a 50% interest in this asset.

Formal groundbreaking at Gloucester Premium Outlets, a 375,000 square foot center in Gloucester, New Jersey serving the greater Philadelphia metropolitan area, is scheduled for August 7, 2014. The center is scheduled to open in August of 2015. Simon owns a 50% interest in this project.

Construction continues on three new Premium Outlets opening in 2014 and 2015:

- •

- Twin Cities Premium Outlets in Eagan (Minneapolis-St. Paul), Minnesota is a 410,000 square foot center scheduled to open

on August 14, 2014. Simon owns a 35% interest in this project.

- •

- Montreal Premium Outlets in Mirabel, Quebec, Canada is a 360,000 square foot center scheduled to open in October of 2014.

Simon owns a 50% interest in this project.

- •

- Vancouver Designer Outlet in Vancouver, British Columbia, Canada is a 242,000 square foot center scheduled to open in April of 2015. Simon owns a 45% interest in this project.

Simon's share of the costs of all development and redevelopment projects currently under construction is approximately $1.7 billion.

WASHINGTON PRIME GROUP INC.

On May 28, 2014, Simon completed the spin-off of 98 smaller malls and community centers to Washington Prime Group Inc. The results of operations of WPG are classified as discontinued operations for the three months and six months ended June 30, 2014 and 2013, respectively.

| 2Q 2014 SUPPLEMENTAL |

|

4 |

EARNINGS RELEASE

FINANCING ACTIVITY

In April, Simon amended and extended its $4.0 billion unsecured multi-currency revolving credit facility. The facility, which can be increased to $5.0 billion during its term, will initially mature on June 30, 2018 and can be extended for an additional year to June 30, 2019 at our sole option. The interest rate on the amended revolver is reduced to LIBOR plus 80 basis points from LIBOR plus 95 basis points. Simon has a combined $6.0 billion of total revolving credit capacity.

In conjunction with the spin-off of WPG, we retained approximately $1.0 billion of proceeds from unsecured and secured indebtedness which WPG incurred.

2014 GUIDANCE

Today we increased FFO guidance provided on May 29, 2014 by $0.05 to a range of $9.01 to $9.11 per diluted share for the year ending December 31, 2014, and also increased guidance for net income to a range of $4.61 to $4.71 per diluted share.

The following table provides the reconciliation for the expected range of estimated net income available to common stockholders per diluted share to estimated FFO per diluted share:

For the year ending December 31, 2014

| |

LOW END | HIGH END | |||||

|---|---|---|---|---|---|---|---|

Estimated net income available to common stockholders per diluted share |

$ | 4.61 | $ | 4.71 | |||

Depreciation and amortization including Simon's share of unconsolidated entities |

4.78 | 4.78 | |||||

Gain upon acquisition of controlling interests, sale or disposal of assets and interests in unconsolidated entities, net |

(0.38 | ) | (0.38 | ) | |||

| | | | | | | | |

Estimated FFO per diluted share |

$ | 9.01 | $ | 9.11 | |||

| | | | | | | | |

| | | | | | | | |

CONFERENCE CALL

Simon will hold a conference call to discuss the quarterly financial results today at 11:00 a.m. Eastern Time, Wednesday, July 23, 2014. Live streaming audio of the conference call will be accessible at investors.simon.com. An online replay will be available until August 6, 2014 at investors.simon.com.

SUPPLEMENTAL MATERIALS AND WEBSITE

Supplemental information on our second quarter 2014 performance is available at investors.simon.com. This information has also been furnished to the SEC in a current report on Form 8-K.

We routinely post important information online at our investor relations website, investors.simon.com. We use this website, press releases, SEC filings, quarterly conference calls, presentations and webcasts to disclose material, non-public information in accordance with Regulation FD. We encourage members of the investment community to monitor these distribution channels for material disclosures. Any information accessed through our website is not incorporated by reference into, and is not a part of, this document

| 2Q 2014 SUPPLEMENTAL |

|

5 |

EARNINGS RELEASE

NON-GAAP FINANCIAL MEASURES

This press release includes FFO and comparable property net operating income growth, which are financial performance measures not defined by generally accepted accounting principles in the United States ("GAAP"). Reconciliations of these non-GAAP financial measures to the most directly comparable GAAP measures are included in this press release and in Simon's supplemental information for the quarter. FFO and comparable property net operating income growth are financial performance measures widely used in the REIT industry. Our definitions of these non-GAAP measures may not be the same as similar measures reported by other REITs.

FORWARD-LOOKING STATEMENTS

Certain statements made in this press release may be deemed "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Although the Company believes the expectations reflected in any forward-looking statements are based on reasonable assumptions, the Company can give no assurance that its expectations will be attained, and it is possible that actual results may differ materially from those indicated by these forward-looking statements due to a variety of risks, uncertainties and other factors. Such factors include, but are not limited to: the Company's ability to meet debt service requirements, the availability and terms of financing, changes in the Company's credit rating, changes in market rates of interest and foreign exchange rates for foreign currencies, changes in value of investments in foreign entities, the ability to hedge interest rate and currency risk, risks associated with the acquisition, development, expansion, leasing and management of properties, general risks related to retail real estate, the liquidity of real estate investments, environmental liabilities, international, national, regional and local economic conditions, changes in market rental rates, trends in the retail industry, relationships with anchor tenants, the inability to collect rent due to the bankruptcy or insolvency of tenants or otherwise, risks relating to joint venture properties, costs of common area maintenance, and the intensely competitive market environment in the retail industry, risks related to international activities, insurance costs and coverage, terrorist activities, changes in economic and market conditions and maintenance of our status as a real estate investment trust. The Company discusses these and other risks and uncertainties under the heading "Risk Factors" in our annual and quarterly reports filed with the SEC. The Company undertakes no duty or obligation to update or revise these forward-looking statements, whether as a result of new information, future developments, or otherwise unless required by law.

ABOUT SIMON

Simon is a global leader in retail real estate ownership, management and development and a S&P 100 company (Simon Property Group, NYSE:SPG). Our industry-leading retail properties and investments across North America, Europe and Asia provide shopping experiences for millions of consumers every day and generate billions in annual retail sales. For more information, visit simon.com.

| 2Q 2014 SUPPLEMENTAL |

|

6 |

Simon Property Group, Inc. and Subsidiaries

Unaudited Consolidated Statements of Operations

(Dollars in thousands, except per share amounts)

| |

FOR THE THREE MONTHS ENDED JUNE 30, |

FOR THE SIX MONTHS ENDED JUNE 30, |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 |

2013 |

2014 |

2013 |

|||||||||

REVENUE: |

|||||||||||||

Minimum rent |

$ | 728,486 | $ | 674,654 | $ | 1,450,768 | $ | 1,347,581 | |||||

Overage rent |

39,160 | 39,077 | 70,834 | 74,343 | |||||||||

Tenant reimbursements |

342,250 | 307,359 | 667,721 | 600,957 | |||||||||

Management fees and other revenues |

34,142 | 31,814 | 64,749 | 61,543 | |||||||||

Other income |

37,944 | 32,089 | 84,932 | 61,392 | |||||||||

| | | | | | | | | | | | | | |

Total revenue |

1,181,982 | 1,084,993 | 2,339,004 | 2,145,816 | |||||||||

| | | | | | | | | | | | | | |

EXPENSES: |

|||||||||||||

Property operating |

92,630 | 92,024 | 187,577 | 177,568 | |||||||||

Depreciation and amortization |

287,214 | 273,537 | 567,708 | 544,872 | |||||||||

Real estate taxes |

99,396 | 91,014 | 193,699 | 180,757 | |||||||||

Repairs and maintenance |

21,656 | 21,604 | 51,421 | 45,943 | |||||||||

Advertising and promotion |

38,149 | 27,552 | 60,768 | 46,674 | |||||||||

Provision for (recovery of) credit losses |

2,442 | (495) | 6,866 | 1,549 | |||||||||

Home and regional office costs |

44,958 | 36,956 | 80,246 | 71,850 | |||||||||

General and administrative |

15,599 | 15,421 | 30,454 | 29,930 | |||||||||

Other |

18,407 | 17,441 | 37,769 | 34,251 | |||||||||

| | | | | | | | | | | | | | |

Total operating expenses |

620,451 | 575,054 | 1,216,508 | 1,133,394 | |||||||||

| | | | | | | | | | | | | | |

OPERATING INCOME |

561,531 | 509,939 | 1,122,496 | 1,012,422 | |||||||||

Interest expense |

(254,930) | (266,229) | (509,164) | (537,535) | |||||||||

Income and other taxes |

(6,626) | (8,959) | (13,489) | (22,074) | |||||||||

Income from unconsolidated entities |

55,764 | 56,310 | 112,842 | 110,248 | |||||||||

Gain upon acquisition of controlling interests and sale or disposal of assets and interests in unconsolidated entities, net |

133,870 | 68,068 | 136,525 | 74,683 | |||||||||

| | | | | | | | | | | | | | |

Consolidated income from continuing operations |

489,609 | 359,129 | 849,210 | 637,744 | |||||||||

Discontinued operations |

26,022 | 41,396 | 67,524 | 97,249 | |||||||||

Discontinued operations transaction expenses |

(38,163) | — | (38,163) | — | |||||||||

| | | | | | | | | | | | | | |

CONSOLIDATED NET INCOME |

477,468 | 400,525 | 878,571 | 734,993 | |||||||||

Net income attributable to noncontrolling interests |

70,047 | 59,755 | 128,667 | 110,250 | |||||||||

Preferred dividends |

834 | 834 | 1,669 | 1,669 | |||||||||

| | | | | | | | | | | | | | |

NET INCOME ATTRIBUTABLE TO COMMON STOCKHOLDERS |

$ | 406,587 | $ | 339,936 | $ | 748,235 | $ | 623,074 | |||||

BASIC EARNINGS (LOSS) PER COMMON SHARE: |

|||||||||||||

Income from continuing operations |

$ | 1.34 | $ | 0.99 | $ | 2.33 | $ | 1.74 | |||||

Discontinued operations |

(0.03) | 0.11 | 0.08 | 0.27 | |||||||||

| | | | | | | | | | | | | | |

Net income attributable to common stockholders |

$ | 1.31 | $ | 1.10 | $ | 2.41 | $ | 2.01 | |||||

DILUTED EARNINGS (LOSS) PER COMMON SHARE: |

|||||||||||||

Income from continuing operations |

$ | 1.34 | $ | 0.99 | $ | 2.33 | $ | 1.74 | |||||

Discontinued operations |

(0.03) | 0.11 | 0.08 | 0.27 | |||||||||

| | | | | | | | | | | | | | |

Net income attributable to common stockholders |

$ | 1.31 | $ | 1.10 | $ | 2.41 | $ | 2.01 | |||||

| 2Q 2014 SUPPLEMENTAL |

|

7 |

Simon Property Group, Inc. and Subsidiaries

Unaudited Consolidated Balance Sheets

(Dollars in thousands, except share amounts)

| |

JUNE 30, 2014 |

DECEMBER 31, 2013 |

|||||

|---|---|---|---|---|---|---|---|

ASSETS: |

|||||||

Investment properties at cost |

$ | 30,951,535 | $ | 30,336,639 | |||

Less - accumulated depreciation |

8,568,672 | 8,092,794 | |||||

| | | | | | | | |

|

22,382,863 | 22,243,845 | |||||

Cash and cash equivalents |

1,665,817 | 1,691,006 | |||||

Tenant receivables and accrued revenue, net |

487,839 | 520,361 | |||||

Investment in unconsolidated entities, at equity |

2,523,431 | 2,429,845 | |||||

Investment in Klépierre, at equity |

2,002,587 | 2,014,415 | |||||

Deferred costs and other assets |

1,523,877 | 1,422,788 | |||||

Total assets of discontinued operations |

— | 3,002,314 | |||||

| | | | | | | | |

Total assets |

$ | 30,586,414 | $ | 33,324,574 | |||

| | | | | | | | |

| | | | | | | | |

LIABILITIES: |

|||||||

Mortgages and unsecured indebtedness |

$ | 21,901,060 | $ | 22,669,917 | |||

Accounts payable, accrued expenses, intangibles, and deferred revenues |

1,147,425 | 1,223,102 | |||||

Cash distributions and losses in partnerships and joint ventures, at equity |

1,116,301 | 1,050,278 | |||||

Other liabilities |

280,483 | 250,371 | |||||

Total liabilities of discontinued operations |

— | 1,117,789 | |||||

| | | | | | | | |

Total liabilities |

24,445,269 | 26,311,457 | |||||

| | | | | | | | |

Commitments and contingencies |

|||||||

Limited partners' preferred interest in the Operating Partnership and noncontrolling redeemable interests in properties |

25,537 | 190,485 | |||||

EQUITY: |

|||||||

Stockholders' Equity |

|||||||

Capital stock (850,000,000 total shares authorized, $0.0001 par value, 238,000,000 shares of excess common stock, 100,000,000 authorized shares of preferred stock): |

|||||||

Series J 8 3/8% cumulative redeemable preferred stock, 1,000,000 shares authorized, 796,948 issued and outstanding with a liquidation value of $39,847 |

44,226 |

44,390 |

|||||

Common stock, $0.0001 par value, 511,990,000 shares authorized, 314,340,625 and 314,251,245 issued and outstanding, respectively |

31 |

31 |

|||||

Class B common stock, $0.0001 par value, 10,000 shares authorized, 8,000 issued and outstanding |

— |

— |

|||||

Capital in excess of par value |

9,406,570 |

9,217,363 |

|||||

Accumulated deficit |

(4,049,079) | (3,218,686) | |||||

Accumulated other comprehensive loss |

(61,736) | (75,795) | |||||

Common stock held in treasury at cost, 3,583,299 and 3,650,680 shares, respectively |

(106,748) | (117,897) | |||||

| | | | | | | | |

Total stockholders' equity |

5,233,264 | 5,849,406 | |||||

Noncontrolling interests |

882,344 | 973,226 | |||||

| | | | | | | | |

Total equity |

6,115,608 | 6,822,632 | |||||

| | | | | | | | |

Total liabilities and equity |

$ | 30,586,414 | $ | 33,324,574 | |||

| | | | | | | | |

| | | | | | | | |

| 2Q 2014 SUPPLEMENTAL |

|

8 |

Simon Property Group, Inc. and Subsidiaries

Unaudited Joint Venture Statements of Operations

(Dollars in thousands)

| |

FOR THE THREE MONTHS ENDED JUNE 30, |

FOR THE SIX MONTHS ENDED JUNE 30, |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 |

2013 |

2014 |

2013 |

|||||||||

REVENUE: |

|||||||||||||

Minimum rent |

$ | 427,899 | $ | 387,600 | $ | 852,684 | $ | 769,072 | |||||

Overage rent |

41,589 | 39,997 | 90,386 | 87,613 | |||||||||

Tenant reimbursements |

193,006 | 182,799 | 385,799 | 362,393 | |||||||||

Other income |

61,929 | 39,397 | 174,635 | 81,392 | |||||||||

| | | | | | | | | | | | | | |

Total revenue |

724,423 | 649,793 | 1,503,504 | 1,300,470 | |||||||||

OPERATING EXPENSES: |

|||||||||||||

Property operating |

131,643 | 120,462 | 293,064 | 233,539 | |||||||||

Depreciation and amortization |

142,047 | 122,981 | 294,195 | 246,595 | |||||||||

Real estate taxes |

52,797 | 48,060 | 107,588 | 100,678 | |||||||||

Repairs and maintenance |

15,944 | 15,576 | 35,585 | 31,118 | |||||||||

Advertising and promotion |

17,113 | 13,967 | 35,923 | 29,661 | |||||||||

Provision for credit losses |

970 | 375 | 4,078 | 1,512 | |||||||||

Other |

44,554 | 36,170 | 97,483 | 71,783 | |||||||||

| | | | | | | | | | | | | | |

Total operating expenses |

405,068 | 357,591 | 867,916 | 714,886 | |||||||||

| | | | | | | | | | | | | | |

OPERATING INCOME |

319,355 | 292,202 | 635,588 | 585,584 | |||||||||

Interest expense |

(150,059) |

(150,887) |

(301,696) |

(294,692) |

|||||||||

| | | | | | | | | | | | | | |

INCOME FROM CONTINUING OPERATIONS |

169,296 | 141,315 | 333,892 | 290,892 | |||||||||

Income from operations of discontinued joint venture interests |

2,094 |

2,892 |

5,079 |

6,629 |

|||||||||

Gain on disposal of discontinued operations, net |

— | 18,356 | — | 18,356 | |||||||||

| | | | | | | | | | | | | | |

NET INCOME |

$ | 171,390 | $ | 162,563 | $ | 338,971 | $ | 315,877 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

THIRD-PARTY INVESTORS' SHARE OF NET INCOME |

$ | 88,217 | $ | 94,949 | $ | 177,530 | $ | 178,715 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Our share of net income |

83,173 | 67,614 | 161,441 | 137,162 | |||||||||

Amortization of Excess Investment (A) |

(24,383) | (24,853) | (49,981) | (49,682) | |||||||||

Our Share of Income from Unconsolidated Discontinued Operations |

(307) | (206) | (652) | (499) | |||||||||

| | | | | | | | | | | | | | |

INCOME FROM UNCONSOLIDATED ENTITIES (B) |

$ | 58,483 | $ | 42,555 | $ | 110,808 | $ | 86,981 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

- Note:

- The

above financial presentation does not include any information related to our investment in Klépierre S.A.

("Klépierre").

For additional information, see footnote B.

| 2Q 2014 SUPPLEMENTAL |

|

9 |

Simon Property Group, Inc. and Subsidiaries

Unaudited Joint Venture Balance Sheets

(Dollars in thousands)

| |

JUNE 30, 2014 |

DECEMBER 31, 2013 |

|||||

|---|---|---|---|---|---|---|---|

ASSETS: |

|||||||

Investment properties, at cost |

$ | 15,842,291 | $ | 15,355,700 | |||

Less - accumulated depreciation |

5,280,359 | 5,080,832 | |||||

| | | | | | | | |

|

10,561,932 | 10,274,868 | |||||

Cash and cash equivalents |

756,563 | 781,554 | |||||

Tenant receivables and accrued revenue, net |

304,679 | 302,902 | |||||

Investment in unconsolidated entities, at equity |

28,517 | 38,352 | |||||

Deferred costs and other assets |

589,390 | 579,480 | |||||

Total assets of discontinued operations |

— | 281,000 | |||||

| | | | | | | | |

Total assets |

$ | 12,241,081 | $ | 12,258,156 | |||

| | | | | | | | |

| | | | | | | | |

LIABILITIES AND PARTNERS' DEFICIT: |

|||||||

Mortgages |

$ | 12,764,686 | $ | 12,753,139 | |||

Accounts payable, accrued expenses, intangibles, and deferred revenue |

980,159 | 834,898 | |||||

Other liabilities |

568,158 | 513,897 | |||||

Total liabilities of discontinued operations |

— | 286,252 | |||||

| | | | | | | | |

Total liabilities |

14,313,003 | 14,388,186 | |||||

Preferred units |

67,450 |

67,450 |

|||||

Partners' deficit |

(2,139,372) | (2,197,480) | |||||

| | | | | | | | |

Total liabilities and partners' deficit |

$ | 12,241,081 | $ | 12,258,156 | |||

| | | | | | | | |

| | | | | | | | |

Our Share of: |

|||||||

Partners' deficit |

$ | (541,435) | $ | (717,776) | |||

Add: Excess Investment (A) |

1,948,565 | 2,059,584 | |||||

Add: Our Share of investment in discontinued unconsolidated entities, at equity |

— | 37,759 | |||||

| | | | | | | | |

Our net investment in unconsolidated entities, at equity |

$ | 1,407,130 | $ | 1,379,567 | |||

| | | | | | | | |

| | | | | | | | |

- Note:

- The

above financial presentation does not include any information related to our investment in Klépierre.

For additional information, see footnote B attached hereto.

| 2Q 2014 SUPPLEMENTAL |

|

10 |

Simon Property Group, Inc. and Subsidiaries

Unaudited Reconciliation of Non-GAAP Financial Measures (C)

(Amounts in thousands, except per share

amounts)

| |

RECONCILIATION OF CONSOLIDATED NET INCOME TO FFO |

|

|

|

|

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

FOR THE THREE MONTHS ENDED JUNE 30, |

FOR THE SIX MONTHS ENDED JUNE 30, |

|

||||||||||||

| |

|

2014 |

2013 |

2014 |

2013 |

|

||||||||||

|

Consolidated Net Income (D) |

$ | 477,468 | $ | 400,525 | $ | 878,571 | $ | 734,993 | |||||||

|

Adjustments to Arrive at FFO: |

|||||||||||||||

|

Depreciation and amortization from consolidated properties |

314,500 | 314,622 | 637,104 | 627,207 | |||||||||||

|

Our share of depreciation and amortization from unconsolidated entities, including Klépierre |

128,461 | 124,828 | 275,718 | 246,377 | |||||||||||

|

Gain upon acquisition of controlling interests and sale or disposal of assets and interests in unconsolidated entities, net |

(133,870) | (68,068) | (136,767) | (88,835) | |||||||||||

|

Net income attributable to noncontrolling interest holders in properties |

(447) | (2,097) | (970) | (4,558) | |||||||||||

|

Noncontrolling interests portion of depreciation and amortization |

(966) | (2,204) | (1,864) | (4,377) | |||||||||||

|

Preferred distributions and dividends |

(1,313) | (1,313) | (2,626) | (2,626) | |||||||||||

| | | | | | | | | | | | | | | | | |

|

FFO of the Operating Partnership (E) |

$ | 783,833 | $ | 766,293 | $ | 1,649,166 | $ | 1,508,181 | |||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

|

Diluted Net Income Per Share to Diluted FFO Per Share Reconciliation: |

|||||||||||||||

|

Diluted net income per share |

$ | 1.31 | $ | 1.10 | $ | 2.41 | $ | 2.01 | |||||||

|

Depreciation and amortization from consolidated properties and our share of depreciation and amortization from unconsolidated entities, including Klépierre, net of noncontrolling interests portion of depreciation and amortization |

1.22 | 1.20 | 2.51 | 2.40 | |||||||||||

|

Gain upon acquisition of controlling interests and sale or disposal of assets and interests in unconsolidated entities, net |

(0.37) | (0.19) | (0.38) | (0.25) | |||||||||||

| | | | | | | | | | | | | | | | | |

|

Diluted FFO per share (F) |

$ | 2.16 | $ | 2.11 | $ | 4.54 | $ | 4.16 | |||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

|

|

|||||||||||||||

|

Details for per share calculations: |

|||||||||||||||

|

FFO of the Operating Partnership (E) |

$ | 783,833 | $ | 766,293 | $ | 1,649,166 | $ | 1,508,181 | |||||||

|

Diluted FFO allocable to unitholders |

(114,003) | (110,346) | (238,881) | (217,034) | |||||||||||

| | | | | | | | | | | | | | | | | |

|

Diluted FFO allocable to common stockholders (G) |

$ | 669,830 | $ | 655,947 | $ | 1,410,285 | $ | 1,291,147 | |||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

|

Diluted weighted average shares outstanding |

310,743 | 310,261 | 310,683 | 310,125 | |||||||||||

|

Weighted average limited partnership units outstanding |

52,861 | 52,194 | 52,625 | 52,130 | |||||||||||

| | | | | | | | | | | | | | | | | |

|

Basic and Diluted weighted average shares and units outstanding |

363,604 | 362,455 | 363,308 | 362,255 | |||||||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

|

Basic and Diluted FFO per Share (F) |

$ | 2.16 | $ | 2.11 | $ | 4.54 | $ | 4.16 | |||||||

|

Percent Change |

2.4% | 9.1% | |||||||||||||

| 2Q 2014 SUPPLEMENTAL |

|

11 |

Simon Property Group, Inc. and Subsidiaries

Footnotes to Unaudited Reconciliation of Non-GAAP Financial Measures

Notes:

- (A)

- Excess

investment represents the unamortized difference of our investment over equity in the underlying net assets of the related partnerships and joint

ventures shown therein. The Company generally amortizes excess investment over the life of the related properties.

- (B)

- The

Unaudited Joint Venture Statements of Operations do not include any operations or our share of net income or excess investment amortization related to

our investment in Klépierre. Amounts included in Footnotes D below exclude our share of related activity for our investment in Klépierre. For further information,

reference should be made to financial information in Klépierre's public filings and additional discussion and analysis in our Form 10-Q.

- (C)

- This

report contains measures of financial or operating performance that are not specifically defined by GAAP, including FFO and FFO per share. FFO is a

performance measure that is standard in the REIT business. We believe FFO provides investors with additional information concerning our operating performance and a basis to compare our performance

with those of other REITs. We also use these measures internally to monitor the operating performance of our portfolio. Our computation of these non-GAAP measures may not be the same as similar

measures reported by other REITs.

We determine FFO based upon the definition set forth by the National Association of Real Estate Investment Trusts ("NAREIT"). We determine FFO to be our share of consolidated net income computed in accordance with GAAP, excluding real estate related depreciation and amortization, excluding gains and losses from extraordinary items, excluding gains and losses from the sales or disposals of, or any impairment charges related to, previously depreciated retail operating properties, plus the allocable portion of FFO of unconsolidated joint ventures based upon economic ownership interest, and all determined on a consistent basis in accordance with GAAP.

We have adopted NAREIT's clarification of the definition of FFO that requires it to include the effects of nonrecurring items not classified as extraordinary, cumulative effect of accounting changes, or a gain or loss resulting from the sale or disposal of, or any impairment charges relating to, previously depreciated retail operating properties. We include in FFO gains and losses realized from the sale of land, outlot buildings, marketable and non-marketable securities, and investment holdings of non-retail real estate. However, you should understand that FFO does not represent cash flow from operations as defined by GAAP, should not be considered as an alternative to net income determined in accordance with GAAP as a measure of operating performance, and is not an alternative to cash flows as a measure of liquidity.

- (D)

- Includes

our share of:

- -

- Gains

on land sales of $5.6 million and $0.8 million for the three months ended June 30, 2014 and 2013, respectively,

$12.4 million and $1.2 million for the six months ended June 30, 2014 and 2013, respectively.

- -

- Straight-line adjustments to minimum rent of $13.3 million for the three months ended June 30, 2014 and 2013, respectively (including $0.2 million and ($0.2) million related to WPG), and $27.3 million and $26.1 million for the six months ended June 30, 2014 and 2013, respectively (including $0.3 million and ($0.1) million related to WPG).

| 2Q 2014 SUPPLEMENTAL |

|

12 |

- -

- Amortization

of fair market value of leases from acquisitions of $3.1 million and $5.6 million for the three months ended June 30, 2014

and 2013 respectively (including $0.1 million and $0.3 million related to WPG), and $8.5 million and $16.3 million for the six months ended June 30, 2014 and 2013,

respectively (including $0.3 million and $0.8 million related to WPG).

- -

- Debt

premium amortization of $5.3 million and $11.3 million for the three months ended June 30, 2014 and 2013, respectively (including

$0.1 million related to WPG for both periods), and $21.4 million and $22.2 million for the six months ended June 30, 2014 and 2013, respectively (including

$0.2 million related to WPG for both periods).

- (E)

- Includes

FFO of the operating partnership related to WPG of $19.7 million ($57.9 million from operations net of $38.2 million of

transaction expenses) and $87.5 million for the three months ended June 30, 2014 and 2013, respectively, and $108.0 million and $175.7 million for the six months ended

June 30, 2014 and 2013, respectively.

- (F)

- Includes

Basic and Diluted FFO per share related to WPG of $0.05 ($0.15 from operations net of $0.10 of transaction expenses) and $0.24 for the three months

ended June 30, 2014 and 2013, respectively, and $0.30 and $0.48 for the six months ended June 30, 2014 and 2013, respectively.

- (G)

- Includes Diluted FFO allocable to common stockholders related to WPG of $16.8 million and $74.9 million for the three months ended June 30, 2014 and 2013, respectively, and $92.4 million and $150.4 million for the six months ended June 30, 2014 and 2013, respectively.

| 2Q 2014 SUPPLEMENTAL |

|

13 |

Simon Property Group, Inc. (NYSE:SPG) is a self-administered and self-managed real estate investment trust ("REIT"). Simon Property Group, L.P., or the Operating Partnership, is our majority-owned partnership subsidiary that owns all of our real estate properties and other assets. In this package, the terms Simon, we, our, or the Company refer to, Simon Property, Inc., the Operating Partnership, and its subsidiaries. We are engaged primarily in the ownership, development and management of retail real estate properties including Malls, Premium Outlets®, The Mills®, and International Properties. At June 30, 2014, we owned or had an interest in 228 properties comprising 189 million square feet in North America, Asia and Europe. Additionally, we have a 28.9% ownership interest in Klépierre, a publicly traded, Paris-based real estate company, which owns shopping centers in 13 European countries.

This package was prepared to provide operational and balance sheet information as of June 30, 2014, for the Company and the Operating Partnership.

On May 28, 2014, we completed the spin-off of 98 smaller malls and community centers to Washington Prime Group Inc. (WPG), which is now an independent public company trading on the NYSE under the symbol "WPG". Results from the properties transferred to WPG (WPG properties) are included in our financial information as discontinued operations through May 28, 2014.

Certain statements made in this Supplemental Package may be deemed "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Although we believe the expectations reflected in any forward-looking statements are based on reasonable assumptions, we can give no assurance that our expectations will be attained, and it is possible that actual results may differ materially from those indicated by these forward-looking statements due to a variety of risks, uncertainties and other factors. Such factors include, but are not limited to: our ability to meet debt service requirements, the availability and terms of financing, changes in our credit rating, changes in market rates of interest and foreign exchange rates for foreign currencies, changes in value of investments in foreign entities, the ability to hedge interest rate and currency risk, risks associated with the acquisition, development, expansion, leasing and management of properties, general risks related to retail real estate, the liquidity of real estate investments, environmental liabilities, international, national, regional and local economic climates, changes in market rental rates, trends in the retail industry, relationships with anchor tenants, the inability to collect rent due to the bankruptcy or insolvency of tenants or otherwise, risks relating to joint venture properties, costs of common area maintenance, intensely competitive market environment in the retail industry, risks related to international activities, insurance costs and coverage, terrorist activities, changes in economic and market conditions and maintenance of our status as a real estate investment trust. We discuss these and other risks and uncertainties under the heading "Risk Factors" in our annual and quarterly periodic reports filed with the SEC. We may update that discussion in our periodic reports, but except as required by law, otherwise we undertake no duty or obligation to update or revise these forward-looking statements, whether as a result of new information, future developments, or otherwise.

Any questions, comments or suggestions regarding this Supplemental Information should be directed to Liz Zale, Senior Vice President of Corporate Affairs (lzale@simon.com or 212.745.9623) or Tom Ward, Vice President of Investor Relations (tom.ward@simon.com or 317.685.7330).

REPORTING CALENDAR

Below is a list of estimated dates for future announcements of results. Dates are subject to change.

Third Quarter 2014 |

October 22, 2014 | |

Fourth Quarter 2014 |

January 30, 2015 |

| 2Q 2014 SUPPLEMENTAL |

|

14 |

OVERVIEW

The Company's common stock and one issue of preferred stock are traded on the New York Stock Exchange under the following symbols:

Common Stock |

SPG | |||

8.375% Series J Cumulative Redeemable Preferred |

SPGPrJ |

CREDIT RATINGS

Standard & Poor's |

||||

Corporate |

A | (Stable Outlook) | ||

Senior Unsecured |

A | (Stable Outlook) | ||

Preferred Stock |

BBB+ | (Stable Outlook) | ||

Moody's |

|

|

||

Senior Unsecured |

A2 | (Stable Outlook) | ||

Preferred Stock |

A3 | (Stable Outlook) |

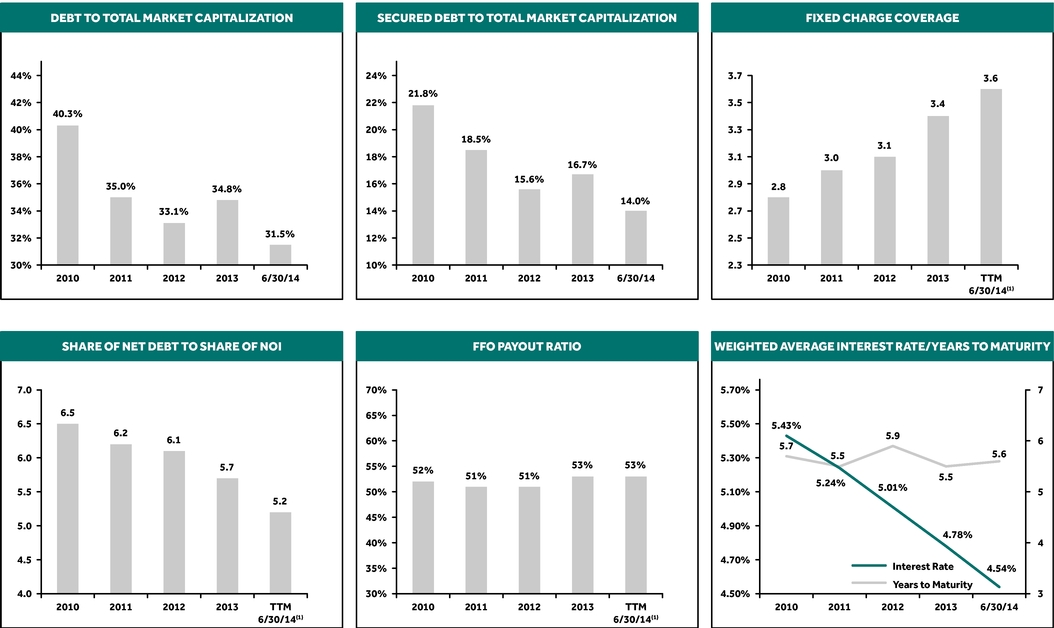

SENIOR UNSECURED DEBT COVENANTS (1)

| |

Required

|

Actual

|

Compliance

|

|||

|---|---|---|---|---|---|---|

Total Debt to Total Assets (1) |

£65% | 42% | Yes | |||

Total Secured Debt to Total Assets (1) |

£50% | 19% | Yes | |||

Fixed Charge Coverage Ratio |

>1.5X | 3.6X | Yes | |||

Total Unencumbered Assets to Unsecured Debt |

³125% | 243% | Yes |

- (1)

- Covenants for indentures dated June 7, 2005 and later. Total Assets are calculated in accordance with the bond indenture and are essentially net operating income (NOI) divided by a 7.0% capitalization rate plus the value of other assets at cost.

| 2Q 2014 SUPPLEMENTAL |

|

15 |

SELECTED FINANCIAL AND EQUITY INFORMATION

(In thousands, except as noted)

| |

THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 |

2013 |

2014 |

2013 |

|||||||||

Financial Highlights |

|||||||||||||

Total Revenue - Consolidated Properties |

$ | 1,181,982 | $ | 1,084,993 | $ | 2,339,004 | $ | 2,145,816 | |||||

Consolidated Net Income |

$ |

477,468 |

$ |

400,525 |

$ |

878,571 |

$ |

734,993 |

|||||

Net Income Attributable to Common Stockholders |

$ | 406,587 | $ | 339,936 | $ | 748,235 | $ | 623,074 | |||||

Basic and Diluted Earnings per Common Share (EPS) |

$ | 1.31 | $ | 1.10 | $ | 2.41 | $ | 2.01 | |||||

Funds from Operations (FFO) of the Operating Partnership (1) |

$ |

783,833 |

$ |

766,293 |

$ |

1,649,166 |

$ |

1,508,181 |

|||||

Basic and Diluted FFO per Share (FFOPS) (2) |

$ | 2.16 | $ | 2.11 | $ | 4.54 | $ | 4.16 | |||||

Dividends/Distributions per Share/Unit |

$ |

1.30 |

$ |

1.15 |

$ |

2.55 |

$ |

2.30 |

|||||

|

Stockholders' Equity Information |

AS OF JUNE 30, 2014 |

AS OF DECEMBER 31, 2013 |

|||||

|---|---|---|---|---|---|---|---|

Limited Partners' Units Outstanding at end of period |

52,941 | 51,846 | |||||

Common Shares Outstanding at end of period |

310,765 | 310,609 | |||||

| | | | | | | | |

Total Common Shares and Limited Partnership Units Outstanding at end of period |

363,706 | 362,455 | |||||

| | | | | | | | |

| | | | | | | | |

Weighted Average Limited Partnership Units Outstanding |

52,625 | 52,101 | |||||

Weighted Average Common Shares Outstanding: |

|||||||

Basic and Diluted - for purposes of EPS and FFOPS |

310,683 | 310,255 | |||||

Debt Information |

|||||||

Share of Consolidated Debt |

$ | 21,814,826 | $ | 22,536,459 | |||

Share of Joint Venture Debt |

6,066,514 | 6,023,740 | |||||

Share of Debt from Discontinued Operations |

– | 962,157 | |||||

| | | | | | | | |

Share of Total Debt |

$ | 27,881,340 | $ | 29,522,356 | |||

| | | | | | | | |

| | | | | | | | |

Market Capitalization |

|||||||

Common Stock Price at end of period |

$ | 166.28 | (3) | $ | 152.16 | ||

Common Equity Capitalization, including Limited Partnership Units |

$ | 60,477,082 | $ | 55,151,110 | |||

Preferred Equity Capitalization, including Limited Partnership Preferred Units |

80,335 | 73,753 | |||||

| | | | | | | | |

Total Equity Market Capitalization |

$ | 60,557,417 | $ | 55,224,863 | |||

| | | | | | | | |

| | | | | | | | |

Total Market Capitalization - Including Share of Total Debt |

$ | 88,438,757 | $ | 84,747,219 | |||

Debt to Total Market Capitalization |

31.5% | 34.8% | |||||

- (1)

- Includes FFO of the operating partnership related to WPG properties of $19.7 million ($57.9 million from operations net of $38.2 million of transaction expenses) and $87.5 million for the three months ended June 30, 2014 and 2013, respectively, and $108.0 million and $175.7 million for the six months ended June 30, 2014 and 2013, respectively.

- (2)

- Includes Basic and Diluted FFO per share related to WPG properties of $0.05 ($0.15 from operations net of $0.10 of transaction expenses) and $0.24 for the three months ended June 30, 2014 and 2013, respectively, and $0.30 and $0.48 for the six months ended June 30, 2014 and 2013, respectively.

- (3)

- Reflects value after WPG spin-off.

| 2Q 2014 SUPPLEMENTAL |

|

16 |

PRO-RATA STATEMENT OF OPERATIONS

(In thousands)

| |

FOR THE THREE MONTHS ENDED JUNE 30, 2014 |

|

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

CONSOLIDATED |

NONCONTROLLING INTERESTS (1) |

OUR CONSOLIDATED SHARE |

OUR SHARE OF JOINT VENTURES |

OUR TOTAL SHARE |

FOR THE THREE MONTHS ENDED JUNE 30, 2013 OUR TOTAL SHARE |

|||||||||||||

REVENUE: |

|||||||||||||||||||

Minimum rent |

$ | 728,486 | $ | (3,263) | $ | 725,223 | $ | 208,201 | $ | 933,424 | $ | 849,479 | |||||||

Overage rent |

39,160 | (33) | 39,127 | 17,828 | 56,955 | 55,843 | |||||||||||||

Tenant reimbursements |

342,250 | (1,946) | 340,304 | 91,293 | 431,597 | 388,976 | |||||||||||||

Management fees and other revenues |

34,142 | – | 34,142 | – | 34,142 | 31,814 | |||||||||||||

Other income |

37,944 | (179) | 37,765 | 30,072 | 67,837 | 50,196 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total revenue |

1,181,982 | (5,421) | 1,176,561 | 347,394 | 1,523,955 | 1,376,308 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

EXPENSES: |

|||||||||||||||||||

Property operating |

92,630 | (939) | 91,691 | 58,967 | 150,658 | 142,225 | |||||||||||||

Depreciation and amortization |

287,214 | (966) | 286,248 | 98,075 | 384,323 | 357,146 | |||||||||||||

Real estate taxes |

99,396 | (589) | 98,807 | 25,464 | 124,271 | 112,403 | |||||||||||||

Repairs and maintenance |

21,656 | (181) | 21,475 | 7,545 | 29,020 | 28,549 | |||||||||||||

Advertising and promotion |

38,149 | (111) | 38,038 | 8,031 | 46,069 | 33,870 | |||||||||||||

Provision for (recovery of) credit losses |

2,442 | – | 2,442 | 495 | 2,937 | (394) | |||||||||||||

Home and regional office costs |

44,958 | – | 44,958 | – | 44,958 | 36,956 | |||||||||||||

General and administrative |

15,599 | – | 15,599 | – | 15,599 | 15,421 | |||||||||||||

Other |

18,407 | (930) | 17,477 | 20,262 | 37,739 | 31,752 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total operating expenses |

620,451 | (3,716) | 616,735 | 218,839 | 835,574 | 757,928 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

OPERATING INCOME |

561,531 | (1,705) | 559,826 | 128,555 | 688,381 | 618,380 | |||||||||||||

Interest expense |

(254,930) | 1,258 | (253,672) | (70,072) | (323,744) | (334,212) | |||||||||||||

Income and other taxes |

(6,626) | – | (6,626) | – | (6,626) | (8,959) | |||||||||||||

Income from unconsolidated entities |

55,764 | – | 55,764 | (58,483) | (2,719) | (2) | 13,755 | (2) | |||||||||||

Gain upon acquisition of controlling interests, sale or disposal of assets and interests in unconsolidated entities, net |

133,870 | – | 133,870 | – | 133,870 | 68,068 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Consolidated income from continuing operations |

489,609 | (447) | 489,162 | – | 489,162 | 357,032 | |||||||||||||

Discontinued operations |

26,022 | – | 26,022 | – | 26,022 | 41,396 | |||||||||||||

Discontinued operations transaction expenses |

(38,163) | – | (38,163) | – | (38,163) | – | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

CONSOLIDATED NET INCOME |

477,468 | (447) | 477,021 | – | 477,021 | 398,428 | |||||||||||||

Net income attributable to noncontrolling interests |

70,047 | (447) | 69,600 | – | 69,600 | (3) | 57,658 | ||||||||||||

Preferred dividends |

834 | – | 834 | – | 834 | 834 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

NET INCOME ATTRIBUTABLE TO COMMON STOCKHOLDERS |

$ | 406,587 | $ | – | $ | 406,587 | $ | – | $ | 406,587 | $ | 339,936 | |||||||

RECONCILIATION OF CONSOLIDATED NET INCOME TO FFO: |

|||||||||||||||||||

Consolidated Net Income |

$ | 477,468 | $ | – | $ | 477,468 | $ | 400,525 | |||||||||||

Adjustments to Consolidated Net Income to Arrive at FFO: |

|||||||||||||||||||

Depreciation and amortization from consolidated properties |

314,500 | – | 314,500 | 314,622 | |||||||||||||||

Our share of depreciation and amortization from unconsolidated entities, including Klépierre |

128,461 | 128,461 | 124,828 | ||||||||||||||||

Income from unconsolidated entities |

(56,071) | 56,071 | – | – | |||||||||||||||

Gain upon acquisition of controlling interests and sale or disposal of assets and interests in unconsolidated entities, net |

(133,870) | – | (133,870) | (68,068) | |||||||||||||||

Net income attributable to noncontrolling interest holders in properties |

(447) | – | (447) | (2,097) | |||||||||||||||

Noncontrolling interests portion of depreciation and amortization |

(966) | – | (966) | (2,204) | |||||||||||||||

Preferred distributions and dividends |

(1,313) | – | (1,313) | (1,313) | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | |

FFO of the Operating Partnership |

$ | 599,301 | $ | 184,532 | $ | 783,833 | $ | 766,293 | |||||||||||

Percentage of FFO of the Operating Partnership |

76.46% | 23.54% | 100.00% | 100.00% | |||||||||||||||

- (1)

- Represents our venture partners' share of operations on consolidated properties.

- (2)

- Our Total Share of the remaining results from unconsolidated entities represents our share of net results related to our investment in Klépierre.

- (3)

- Represents limited partners' interest in the Operating Partnership.

| 2Q 2014 SUPPLEMENTAL |

|

17 |

PRO-RATA STATEMENT OF OPERATIONS

(In thousands)

| |

FOR THE SIX MONTHS ENDED JUNE 30, 2014 |

|

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

CONSOLIDATED |

NONCONTROLLING INTERESTS (1) |

OUR CONSOLIDATED SHARE |

OUR SHARE OF JOINT VENTURES |

OUR TOTAL SHARE |

FOR THE SIX MONTHS ENDED JUNE 30, 2013 OUR TOTAL SHARE |

|||||||||||||

REVENUE: |

|||||||||||||||||||

Minimum rent |

$ | 1,450,768 | $ | (6,560) | $ | 1,444,208 | $ | 413,162 | $ | 1,857,370 | $ | 1,694,031 | |||||||

Overage rent |

70,834 | (73) | 70,761 | 38,414 | 109,175 | 110,852 | |||||||||||||

Tenant reimbursements |

667,721 | (4,170) | 663,551 | 182,536 | 846,087 | 762,362 | |||||||||||||

Management fees and other revenues |

64,749 | – | 64,749 | – | 64,749 | 61,543 | |||||||||||||

Other income |

84,932 | (334) | 84,598 | 85,788 | 170,386 | 98,318 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total revenue |

2,339,004 | (11,137) | 2,327,867 | 719,900 | 3,047,767 | 2,727,106 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

EXPENSES: |

|||||||||||||||||||

Property operating |

187,577 | (2,201) | 185,376 | 132,706 | 318,082 | 274,646 | |||||||||||||

Depreciation and amortization |

567,708 | (1,863) | 565,845 | 206,278 | 772,123 | 712,217 | |||||||||||||

Real estate taxes |

193,699 | (1,208) | 192,491 | 50,998 | 243,489 | 225,397 | |||||||||||||

Repairs and maintenance |

51,421 | (421) | 51,000 | 16,996 | 67,996 | 59,812 | |||||||||||||

Advertising and promotion |

60,768 | (203) | 60,565 | 16,443 | 77,008 | 59,875 | |||||||||||||

Provision for credit losses |

6,866 | (62) | 6,804 | 2,015 | 8,819 | 2,379 | |||||||||||||

Home and regional office costs |

80,246 | – | 80,246 | – | 80,246 | 71,850 | |||||||||||||

General and administrative |

30,454 | – | 30,454 | – | 30,454 | 29,930 | |||||||||||||

Other |

37,769 | (1,764) | 36,005 | 43,347 | 79,352 | 62,377 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total operating expenses |

1,216,508 | (7,722) | 1,208,786 | 468,783 | 1,677,569 | 1,498,483 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

OPERATING INCOME |

1,122,496 | (3,415) | 1,119,081 | 251,117 | 1,370,198 | 1,228,623 | |||||||||||||

Interest expense |

(509,164) | 2,445 | (506,719) | (140,309) | (647,028) | (671,313) | |||||||||||||

Income and other taxes |

(13,489) | – | (13,489) | – | (13,489) | (22,074) | |||||||||||||

Income from unconsolidated entities |

112,842 | – | 112,842 | (110,808) | 2,034 | (2) | 23,267 | (2) | |||||||||||

Gain upon acquisition of controlling interests and sale or disposal of assets and interests in unconsolidated entities, net |

136,525 | – | 136,525 | – | 136,525 | 74,683 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Consolidated income from continuing operations |

849,210 | (970) | 848,240 | – | 848,240 | 633,186 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Discontinued operations |

67,524 | – | 67,524 | – | 67,524 | 97,249 | |||||||||||||

Discontinued operations transaction expenses |

(38,163) | – | (38,163) | – | (38,163) | – | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

CONSOLIDATED NET INCOME |

878,571 | (970) | 877,601 | – | 877,601 | 730,435 | |||||||||||||

Net income attributable to noncontrolling interests |

128,667 | (970) | 127,697 | – | 127,697 | (3) | 105,692 | ||||||||||||

Preferred dividends |

1,669 | – | 1,669 | – | 1,669 | 1,669 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

NET INCOME ATTRIBUTABLE TO COMMON STOCKHOLDERS |

$ | 748,235 | $ | – | $ | 748,235 | $ | – | $ | 748,235 | $ | 623,074 | |||||||

RECONCILIATION OF CONSOLIDATED NET INCOME TO FFO: |

|||||||||||||||||||

Consolidated Net Income |

$ | 878,571 | $ | – | $ | 878,571 | $ | 734,993 | |||||||||||

Adjustments to Consolidated Net Income to Arrive at FFO: |

|||||||||||||||||||

Depreciation and amortization from consolidated properties |

637,104 | – | 637,104 | 627,207 | |||||||||||||||

Our share of depreciation and amortization from unconsolidated entities, including Klépierre |

275,718 | 275,718 | 246,377 | ||||||||||||||||

Income from unconsolidated entities |

(113,494) | 113,494 | – | – | |||||||||||||||

Gain upon acquisition of controlling interests and sale or disposal of assets and interests in unconsolidated entities, net |

(136,767) | – | (136,767) | (88,835) | |||||||||||||||

Net income attributable to noncontrolling interest holders in properties |

(970) | – | (970) | (4,558) | |||||||||||||||

Noncontrolling interests portion of depreciation and amortization |

(1,864) | – | (1,864) | (4,377) | |||||||||||||||

Preferred distributions and dividends |

(2,626) | – | (2,626) | (2,626) | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | |

FFO of the Operating Partnership |

$ | 1,259,954 | $ | 389,212 | $ | 1,649,166 | $ | 1,508,181 | |||||||||||

Percentage of FFO of the Operating Partnership |

76.40% | 23.60% | 100.00% | 100.00% | |||||||||||||||

- (1)

- Represents our venture partners' share of operations from consolidated properties.

- (2)

- Our Total Share of income from unconsolidated entities represents our share of net results related to our investment in Klépierre.

- (3)

- Represents limited partners' interest in the Operating Partnership.

| 2Q 2014 SUPPLEMENTAL |

|

18 |

PRO-RATA BALANCE SHEET

(In thousands)

| |

AS OF JUNE 30, 2014 |

|

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

CONSOLIDATED |

NONCONTROLLING INTERESTS |

OUR CONSOLIDATED SHARE |

OUR SHARE OF JOINT VENTURES |

OUR TOTAL SHARE |

AS OF DECEMBER 31, 2013 OUR TOTAL SHARE |

|||||||||||||

ASSETS: |

|||||||||||||||||||

Investment properties, at cost |

$ | 30,951,535 | $ | (128,158) | $ | 30,823,377 | $ | 10,025,641 | $ | 40,849,018 | $ | 39,792,597 | |||||||

Less - accumulated depreciation |

8,568,672 | $ | (51,708) | 8,516,964 | $ | 2,515,766 | 11,032,730 | 10,399,807 | |||||||||||

| | | | | | | | | | | | | | | | | | | | |

|

22,382,863 | (76,450) | 22,306,413 | 7,509,875 | 29,816,288 | 29,392,790 | |||||||||||||

Cash and cash equivalents |

1,665,817 | (3,600) | 1,662,217 | 361,418 | 2,023,635 | 2,053,790 | |||||||||||||

Tenant receivables and accrued revenue, net |

487,839 | (1,812) | 486,027 | 147,580 | 633,607 | 660,235 | |||||||||||||

Investment in unconsolidated entities, at equity |

2,523,431 | – | 2,523,431 | (2,523,431) | – | – | |||||||||||||

Investment in Klépierre, at equity |

2,002,587 | – | 2,002,587 | – | 2,002,587 | 2,014,415 | |||||||||||||

Deferred costs and other assets |

1,523,877 | (7,177) | 1,516,700 | 335,951 | 1,852,651 | 1,723,503 | |||||||||||||

Total assets of discontinued operations |

– | – | – | – | – | 3,041,057 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total assets |

$ | 30,586,414 | $ | (89,039) | $ | 30,497,375 | $ | 5,831,393 | $ | 36,328,768 | $ | 38,885,790 | |||||||

LIABILITIES: |

|||||||||||||||||||

Mortgages and unsecured indebtedness |

$ | 21,901,060 | $ | (86,234) | $ | 21,814,826 | $ | 6,066,514 | $ | 27,881,340 | $ | 28,560,199 | |||||||

Accounts payable, accrued expenses, intangibles, and deferred revenues |

1,147,425 | (4,091) | 1,143,334 | 582,746 | 1,726,080 | 1,628,779 | |||||||||||||

Cash distributions and losses in partnerships and joint ventures, at equity |

1,116,301 | – | 1,116,301 | (1,116,301) | – | – | |||||||||||||

Other liabilities |

280,483 | (357) | 280,126 | 298,434 | 578,560 | 521,910 | |||||||||||||

Total liabilities of discontinued operations |

– | – | – | – | – | 1,194,291 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total liabilities |

24,445,269 | (90,682) | 24,354,587 | 5,831,393 | 30,185,980 | 31,905,179 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Commitments and contingencies |

|||||||||||||||||||

Limited partners' preferred interest in the Operating Partnership and noncontrolling redeemable interests in properties |

25,537 | – | 25,537 | – | 25,537 | 162,243 | |||||||||||||

EQUITY: |

|||||||||||||||||||

Stockholders' equity |

|||||||||||||||||||

Capital stock |

|||||||||||||||||||

Series J 83/8% cumulative redeemable preferred stock |

44,226 | – | 44,226 | – | 44,226 | 44,390 | |||||||||||||

Common stock, $.0001 par value |

31 | – | 31 | – | 31 | 31 | |||||||||||||

Class B common stock, $.0001 par value |

– | – | – | – | – | – | |||||||||||||

Capital in excess of par value |

9,406,570 | – | 9,406,570 | – | 9,406,570 | 9,217,363 | |||||||||||||

Accumulated deficit |

(4,049,079) | – | (4,049,079) | – | (4,049,079) | (3,218,686) | |||||||||||||

Accumulated other comprehensive loss |

(61,736) | – | (61,736) | – | (61,736) | (75,795) | |||||||||||||

Common stock held in treasury at cost |

(106,748) | – | (106,748) | – | (106,748) | (117,897) | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total stockholders' equity |

5,233,264 | – | 5,233,264 | – | 5,233,264 | 5,849,406 | |||||||||||||

Noncontrolling interests |

882,344 | 1,643 | 883,987 | – | 883,987 | 968,962 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total equity |

6,115,608 | 1,643 | 6,117,251 | – | 6,117,251 | 6,818,368 | |||||||||||||

| | | | | | | | | | | | | | | | | | | | |

Total liabilities and equity |

$ | 30,586,414 | $ | (89,039) | $ | 30,497,375 | $ | 5,831,393 | $36,328,768 | $ | 38,885,790 | ||||||||

BASIS OF PRESENTATION:

We present balance sheet and income statement data on a pro-rata basis reflecting our proportionate economic ownership of each asset in our portfolio. The consolidated amounts shown are prepared on a consistent basis with our consolidated financial statements. Our Share of Joint Ventures column was derived on a property-by-property basis by applying the same percentage interests used to arrive at our share of net income during the period and applying them to all financial statement line items of each property. A similar calculation was performed for noncontrolling interests.

| 2Q 2014 SUPPLEMENTAL |

|

19 |

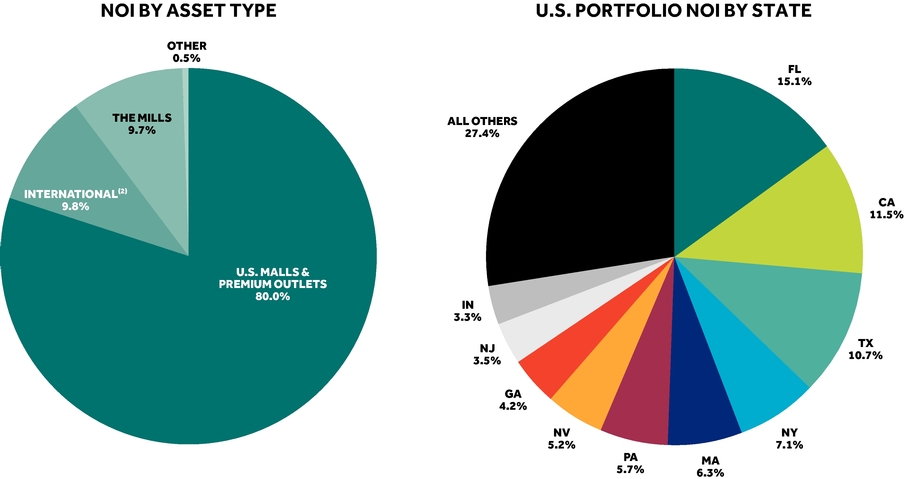

NET OPERATING INCOME (NOI) COMPOSITION (1)

For the Six Months Ended June 30, 2014

|

|||

- (1)

- Based on our share of total NOI and does not reflect any property, entity or corporate-level debt. Does not include WPG properties.

- (2)

- Includes Klépierre, international Premium Outlets and international Designer Outlets.

| 2Q 2014 SUPPLEMENTAL |

|

20 |

RECONCILIATIONS OF NON-GAAP FINANCIAL MEASURES

(In thousands, except as noted)

RECONCILIATION OF NET INCOME TO NOI |

|||||||||||||

The following schedule reconciles net income to NOI and provides our calculation of comparable property NOI. |

|||||||||||||

|

|||||||||||||

| |

THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 |

2013 |

2014 |

2013 |

|||||||||

Reconciliation of NOI of consolidated properties: |

|||||||||||||

Consolidated Net Income |

$ | 477,468 | $ | 400,525 | $ | 878,571 | $ | 734,993 | |||||

Discontinued operations |

(26,022) | (41,396) | (67,524) | (97,249) | |||||||||

Discontinued operations transaction expenses |

38,163 | — | 38,163 | — | |||||||||

Income and other taxes |

6,626 | 8,959 | 13,489 | 22,074 | |||||||||

Interest expense |

254,930 | 266,229 | 509,164 | 537,535 | |||||||||

Income from unconsolidated entities |

(55,764) | (56,310) | (112,842) | (110,248) | |||||||||

Gain upon acquisition of controlling interests and sale or disposal of assets and interests in unconsolidated entities, net |

(133,870) | (68,068) | (136,525) | (74,683) | |||||||||

| | | | | | | | | | | | | | |

Operating Income |

561,531 | 509,939 | 1,122,496 | 1,012,422 | |||||||||

Depreciation and amortization |

287,214 | 273,537 | 567,708 | 544,872 | |||||||||

| | | | | | | | | | | | | | |

NOI of consolidated properties |

$ | 848,745 | $ | 783,476 | $ | 1,690,204 | $ | 1,557,294 | |||||

Reconciliation of NOI of unconsolidated entities: |

|||||||||||||

Net Income |

$ | 171,390 | $ | 162,563 | $ | 338,971 | $ | 315,877 | |||||

Interest expense |

150,059 | 150,887 | 301,696 | 294,692 | |||||||||

Income from operations of discontinued joint venture interests |

(2,094) | (2,892) | (5,079) | (6,629) | |||||||||

Gain on disposal of discontinued operations |

— | (18,356) | — | (18,356) | |||||||||

| | | | | | | | | | | | | | |

Operating Income |

319,355 | 292,202 | 635,588 | 585,584 | |||||||||

Depreciation and amortization |

142,047 | 122,981 | 294,195 | 246,595 | |||||||||

| | | | | | | | | | | | | | |

NOI of unconsolidated entities |

$ | 461,402 | $ | 415,183 | $ | 929,783 | $ | 832,179 | |||||

Total consolidated and unconsolidated NOI from continuing operations |

$1,310,147 | $ | 1,198,659 | $2,619,987 | $ | 2,389,473 | |||||||

Adjustments to NOI: |

|||||||||||||

NOI of discontinued consolidated properties |

68,953 | 100,052 | 169,828 | 200,556 | |||||||||

NOI of discontinued unconsolidated properties |

6,969 | 10,259 | 17,445 | 22,068 | |||||||||

| | | | | | | | | | | | | | |

Total NOI of our portfolio |

$ | 1,386,069 | $ | 1,308,970 | $ | 2,807,260 | $ | 2,612,097 | |||||

Change in NOI from prior period |

5.9% | 4.0% | 7.5% | 5.7% | |||||||||

Add: Our share of NOI from Klépierre |

53,189 | 74,319 | 120,065 | 141,881 | |||||||||

Less: Joint venture partners' share of NOI from continuing operations |

237,443 | 223,133 | 477,666 | 448,633 | |||||||||

Less: Joint venture partners' share of NOI from discontinued operations |

5,139 | 7,758 | 12,998 | 16,861 | |||||||||

| | | | | | | | | | | | | | |

Our share of NOI |

$ | 1,196,676 | $ | 1,152,398 | $ | 2,436,661 | $ | 2,288,484 | |||||

Increase in our share of NOI from prior period |

3.8% | 7.4% | 6.5% | 11.2% | |||||||||

Total NOI of our portfolio |

$ | 1,386,069 | $ | 1,308,970 | $ | 2,807,260 | $ | 2,612,097 | |||||

NOI from non comparable properties (1) |

237,959 | 221,614 | 538,465 | 460,931 | |||||||||

| | | | | | | | | | | | | | |

Total NOI of comparable properties (2) |

$ | 1,148,110 | $ | 1,087,356 | $ | 2,268,795 | $ | 2,151,166 | |||||

Increase in NOI of U.S. Malls, Premium Outlets and The Mills that are comparable properties |

5.6% | 5.5% | |||||||||||

- (1)

- NOI excluded from comparable property NOI relates to WPG properties, international properties, other retail properties, TMLP properties, any of our non-retail holdings and results of our corporate and management company operations, NOI of U.S. Malls, Premium Outlets and The Mills not owned and operated in both periods under comparison and excluded income noted in footnote 2 below.

- (2)

- Comparable properties are U.S. Malls, Premium Outlets and The Mills that were owned in both of the periods under comparison. Excludes lease termination income, interest income, land sale gains and the impact of significant redevelopment activities.

| 2Q 2014 SUPPLEMENTAL |

|

21 |

RECONCILIATIONS OF NON-GAAP FINANCIAL MEASURES

(In thousands, except as noted)

RECONCILIATION OF FFO TO FUNDS AVAILABLE FOR DISTRIBUTION (OUR SHARE) |

|||||||||||||

|

|||||||||||||

| |

THREE MONTHS ENDED JUNE 30, 2014 |

PER SHARE AMOUNT |

SIX MONTHS ENDED JUNE 30, 2014 |

PER SHARE AMOUNT |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

FFO |

$ | 783,833 | $ | 2.16 | $ | 1,649,166 | $ | 4.54 | |||||

Non-cash impacts to FFO (1) |

4,622 | 0.01 | (5,041 | ) | (0.01 | ) | |||||||

| | | | | | | | | | | | | | |

FFO excluding non-cash impacts |

788,455 | $ | 2.17 | 1,644,125 | $ | 4.53 | |||||||

Tenant allowances |

(45,199 | ) | (0.12 | ) | (85,262 | ) | (0.23 | ) | |||||

Operational capital expenditures |

(24,257 | ) | (0.07 | ) | (31,216 | ) | (0.09 | ) | |||||

| | | | | | | | | | | | | | |

Funds available for distribution |

$ | 718,999 | $ | 1.98 | $ | 1,527,647 | $ | 4.21 | |||||

- (1)

- Non-cash impacts to FFO include:

| |

THREE MONTHS ENDED JUNE 30, 2014 |

|

SIX MONTHS ENDED JUNE 30, 2014 |

|

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Deductions: |

||||||||||||||

Straight-line rent |

(13,263 | ) | (27,311 | ) | ||||||||||

Fair value of debt amortization |

(5,286 | ) | (21,421 | ) | ||||||||||

Fair market value of lease amortization |

(3,008 | ) | (8,456 | ) | ||||||||||

Additions: |

||||||||||||||

Stock based compensation expense |

15,664 | 29,470 | ||||||||||||

Mortgage, financing fee and terminated swap amortization expense |

10,515 | 22,677 | ||||||||||||

| | | | | | | | | | | | | | ||

|

4,622 | (5,041 | ) | |||||||||||

This report contains measures of financial or operating performance that are not specifically defined by generally accepted accounting principles (GAAP) in the United States, including FFO, diluted FFO per share, funds available for distribution, net operating income (NOI), and comparable property NOI. FFO and NOI are performance measures that are standard in the REIT business. We believe FFO and NOI provide investors with additional information concerning our operating performance and a basis to compare our performance with the performance of other REITs. We also use these measures internally to monitor the operating performance of our portfolio. Our computation of these non-GAAP measures may not be the same as similar measures reported by other REITs.

The non-GAAP financial measures used in this report should not be considered as alternatives to net income as a measure of our operating performance or to cash flows computed in accordance with GAAP as a measure of liquidity nor are they indicative of cash flows from operating and financial activities. Reconciliations of other non-GAAP measures used in this report to the most-directly comparable GAAP measure are included in the tables on pages 21 and 22 and in the Earnings Release for the latest period.

| 2Q 2014 SUPPLEMENTAL |

|

22 |

OTHER INCOME, OTHER EXPENSE AND CAPITALIZED INTEREST

(In thousands)

| |

THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 |

2013 |

2014 |

2013 |

|||||||||

Consolidated Properties |

|||||||||||||

Other Income (1) |

|||||||||||||

Interest and dividend income |

$ | 2,678 | $ | 2,187 | $ | 5,178 | $ | 3,998 | |||||

Lease settlement income |

1,138 | 305 | 12,022 | 1,918 | |||||||||

Gains on land sales |

4,945 | 654 | 12,155 | 1,095 | |||||||||

Other (2) |

29,183 | 28,943 | 55,577 | 54,381 | |||||||||

| | | | | | | | | | | | | | |

Totals |

$ | 37,944 | $ | 32,089 | $ | 84,932 | $ | 61,392 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Other Expense (1) |

|||||||||||||

Ground rent |

$ | 10,992 | $ | 10,755 | $ | 19,949 | $ | 20,886 | |||||

Professional fees and other |

7,415 | 6,686 | 17,820 | 13,365 | |||||||||

| | | | | | | | | | | | | | |

Totals |

$ | 18,407 | $ | 17,441 | $ | 37,769 | $ | 34,251 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

|

|||||||||||||

|

Capitalized Interest (1) |

THREE MONTHS ENDED JUNE 30, |

SIX MONTHS ENDED JUNE 30, |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2014 |

2013 |

2014 |

2013 |

|||||||||

Interest Capitalized during the Period: |

|||||||||||||

Our Share of Consolidated Properties |

$ | 3,092 | $ | 4,604 | $ | 6,414 | $ | 8,361 | |||||

Our Share of Joint Venture Properties |

$ | 124 | $ | 157 | $ | 196 | $ | 432 | |||||

- (1)

- Excludes WPG properties in all periods presented as those items are reported as discontinued operations.

- (2)

- Includes ancillary property revenues, gift cards, marketing, media, parking and sponsorship revenues and other miscellaneous income items.

| 2Q 2014 SUPPLEMENTAL |

|

23 |

U.S. MALLS AND PREMIUM OUTLETS OPERATING INFORMATION (1)

| |

AS OF JUNE 30, | ||||||

|---|---|---|---|---|---|---|---|

| |

2014 |

2013 |

|||||

Total Number of Properties |

181 | 183 | |||||

Total Square Footage of Properties (in millions) |

154.2 |

155.1 |

|||||

Ending Occupancy (2): |

|||||||

Consolidated Assets |

96.9% | 96.2% | |||||

Unconsolidated Assets |

95.5% | 95.5% | |||||

Total Portfolio |

96.5% | 96.1% | |||||

Total Sales per Square Foot (PSF) (3): |

|||||||

Consolidated Assets |

$596 | $ | 598 | ||||

Unconsolidated Assets |

$650 | $ | 666 | ||||

Total Portfolio |

$608 | $ | 612 | ||||

Base Minimum Rent PSF (4): |

|||||||

Consolidated Assets |

$44.46 | $42.03 | |||||

Unconsolidated Assets |

$49.66 | $49.82 | |||||

Total Portfolio |

$45.83 | $43.94 | |||||

Releasing Activity for the Trailing Twelve Month Period Ended:

|

|

TOTAL RENT PSF |

|

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

|

SQUARE FOOTAGE OF OPENINGS |

OPENING RATE PSF (5) |

CLOSING RATE PSF (5) |

RELEASING SPREAD (5) |

||||||||||||

6/30/14 |

7,174,353 | $ | 66.28 | $ | 55.22 | $ | 11.06 | 20.0% | ||||||||

3/31/14 |

6,653,281 | $ | 65.89 | $ | 54.42 | $ | 11.47 | 21.1% | ||||||||

12/31/13 |

6,697,286 | $ | 67.06 | $ | 56.72 | $ | 10.34 | 18.2% | ||||||||

9/30/13 |

6,587,881 | $ | 65.86 | $ | 56.50 | $ | 9.36 | 16.6% | ||||||||

6/30/13 |

6,366,443 | $ | 64.84 | $ | 56.08 | $ | 8.76 | 15.6% | ||||||||

3/31/13 |

6,268,787 | $ | 63.61 | $ | 55.16 | $ | 8.45 | 15.3% | ||||||||

Occupancy Cost as a Percentage of Sales (6): |

||||||||||||||||

6/30/14 |

11.6% | |||||||||||||||

3/31/14 |

11.4% | |||||||||||||||

|

11.3% |

|||||||||||||||

9/30/13 |

11.2% | |||||||||||||||

6/30/13 |

11.2% | |||||||||||||||

3/31/13 |

11.1% | |||||||||||||||

- (1)

- Because this information excludes WPG properties, it differs from previously reported historical information.

- (2)

- Ending Occupancy is the percentage of total owned square footage (GLA) which is leased as of the last day of the reporting period. We include all company owned space except for mall anchors, mall majors, mall freestanding and mall outlots in the calculation.

- (3)

- Total Sales PSF is defined as total sales of the tenants open and operating in the center during the reporting period divided by the associated company owned and occupied GLA on a trailing 12-month basis. Includes tenant sales activity for all months a tenant is open within the trailing 12-month period. In accordance with the standard definition of sales for regional malls adopted by the International Council of Shopping Centers, only stores with less than 10,000 square feet are included for malls. All company owned space is included for Premium Outlets.

- (4)

- Base Minimum Rent PSF is the average base minimum rent charge in effect for the reporting period for all tenants that would qualify to be included in Ending Occupancy as defined above.

- (5)

- Releasing Spread is a "same space" measure that compares opening and closing rates on individual spaces, including spaces greater than 10,000 square feet. The Opening Rate is the average of the initial cash Total Rent PSF for spaces leased during the trailing 12-month period, and includes new leases and existing tenant renewals, amendments and relocations (including expansions and downsizings). The Closing Rate is the average of the final cash Total Rent PSF as of the month the tenant terminates or closes. Total Rent PSF includes Base Minimum Rent, common area maintenance (CAM) and base percentage rent. It includes leasing activity on all spaces occupied by tenants that would qualify to be included in Ending Occupancy as defined above as long as the opening and closing dates are within 24 months of one another.

- (6)

- Occupancy Cost as a Percentage of Sales is the trailing 12-month Base Minimum Rent, plus all applicable ancillary charges, plus overage rent, if applicable (based on last 12 months of sales), divided by the trailing 12-month Total Sales PSF for the same tenants.

| 2Q 2014 SUPPLEMENTAL |

|

24 |

THE MILLS AND INTERNATIONAL OPERATING INFORMATION

| |

AS OF JUNE 30, | ||||||