Attached files

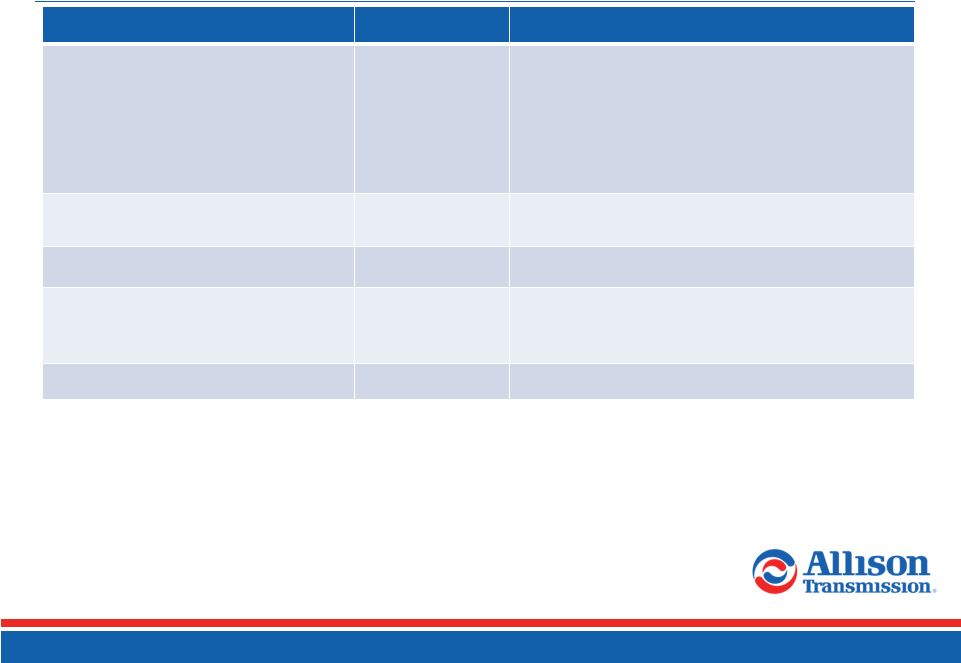

| file | filename |

|---|---|

| 8-K - FORM 8-K - Allison Transmission Holdings Inc | d764527d8k.htm |

| EX-99.1 - EX-99.1 - Allison Transmission Holdings Inc | d764527dex991.htm |

Q2

2014 Earnings Release Published July 23, 2014 (Earnings Conference Call July

24, 2014) Lawrence Dewey, Chairman, President & Chief Executive

Officer David Graziosi, Executive Vice President & Chief Financial

Officer Exhibit 99.2 |

2

Safe Harbor Statement

The

following

information

contains,

or

may

be

deemed

to

contain,

“forward-looking

statements”

(as

defined

in

the

U.S.

Private

Securities

Litigation

Reform

Act

of

1995).

The

words

“believe,”

“expect,”

“anticipate,”

“intend,”

“estimate”

and

other

expressions

that

are

predictions

of

or

indicate

future

events

and

trends

and

that

do

not

relate

to

historical

matters

identify

forward-looking

statements.

You

should

not

place

undue

reliance

on

these

forward-looking

statements.

Although

forward-looking

statements

reflect

management’s

good

faith

beliefs,

reliance

should

not

be

placed

on

forward-looking

statements

because

they

involve

known

and

unknown

risks,

uncertainties

and

other

factors,

which

may

cause

the

actual

results,

performance

or

achievements

to

differ

materially

from

anticipated

future

results,

performance

or

achievements

expressed

or

implied

by

such

forward-looking

statements.

Forward-looking

statements

speak

only

as

of

the

date

the

statements

are

made.

We

undertake

no

obligation

to

publicly

update

or

revise

any

forward-looking

statement,

whether

as

a

result

of

new

information,

future

events,

changed

circumstances

or

otherwise.

These

forward-looking

statements

are

subject

to

numerous

risks

and

uncertainties,

including,

but

not

limited

to:

risks

related

to

our

substantial

indebtedness;

our

participation

in

markets

that

are

competitive;

the

highly

cyclical

industries

in

which

certain

of

our

end

users

operate;

the

failure

of

markets

outside

North

America

to

increase

adoption

of

fully-automatic

transmissions;

the

concentration

of

our

net

sales

in

our

top

five

customers

and

the

loss

of

any

one

of

these;

future

reductions

or

changes

in

government

subsidies

for

hybrid

vehicles;

U.S.

defense

spending;

general

economic

and

industry

conditions;

the

discovery

of

defects

in

our

products,

resulting

in

delays

in

new

model

launches,

recall

campaigns

and/or

increased

warranty

costs

and

reduction

in

future

sales

or

damage

to

our

brand

and

reputation;

our

ability

to

prepare

for,

respond

to

and

successfully

achieve

our

objectives

relating

to

technological

and

market

developments

and

changing

customer

needs;

risks

associated

with

our

international

operations;

and

labor

strikes,

work

stoppages

or

similar

labor

disputes,

which

could

significantly

disrupt

our

operations

or

those

of

our

principal

customers.

Allison

Transmission

cannot

assure

you

that

the

assumptions

made

in

preparing

any

of

the

forward-

looking

statements

will

prove

accurate

or

that

any

long-term

financial

goals

will

be

realized.

All

forward-looking

statements

included

in

this

presentation

speak

only

as

of

the

date

made,

and

Allison

Transmission

undertakes

no

obligation

to

update

or

revise

publicly

any

such

forward-looking

statements,

whether

as

a

result

of

new

information,

future

events,

or

otherwise.

In

particular,

Allison

Transmission

cautions

you

not

to

place

undue

weight

on

certain

forward-looking

statements

pertaining

to

potential

growth

opportunities,

long-term

financial

goals

or

the

value

we

currently

ascribe

to

certain

tax

attributes

set

forth

herein.

Actual

results

may

vary

significantly

from

these

statements.

Allison

Transmission’s

business

is

subject

to

numerous

risks

and

uncertainties,

which

may

cause

future

results

of

operations

to

vary

significantly

from

those

presented

herein.

Important

factors

that

could

cause

actual

results

to

differ

materially

are

discussed

in

Allison

Transmission’s

Annual

Report

on

Form

10-K

for

the

year

ended

December

31,

2013. |

Non-GAAP Financial Information

3

We

use

Adjusted

net

income,

Adjusted

EBITDA,

Adjusted

EBITDA

excluding

technology-related

license

expenses,

Adjusted

EBITDA

margin,

Adjusted

EBITDA

margin

excluding

technology-related

license

expenses,

adjusted

free

cash

flow

and

free

cash

flow

to

evaluate

our

performance

relative

to

that

of

our

peers.

In

addition,

the

Senior

Secured

Credit

Facility

has

certain

covenants

that

incorporate

Adjusted

EBITDA.

However,

Adjusted

net

income,

Adjusted

EBITDA,

Adjusted

EBITDA

excluding

technology-related

license

expenses,

Adjusted

EBITDA

margin,

Adjusted

EBITDA

margin

excluding

technology-related

license

expenses,

adjusted

free

cash

flow

and

free

cash

flow

are

not

measurements

of

financial

performance

under

GAAP,

and

these

metrics

may

not

be

comparable

to

similarly

titled

measures

of

other

companies.

Adjusted

net

income

is

calculated

as

the

sum

of

net

income

(loss),

interest

expense,

net,

income

tax

expense

(benefit),

trade

name

impairment

and

amortization

of

intangible

assets,

less

cash

interest,

net

and

cash

income

taxes,

and

adjusted

for

certain

non-recurring

items.

Adjusted

EBITDA

is

calculated

as

the

sum

of

Adjusted

net

income,

cash

interest,

net,

cash

income

taxes,

depreciation

of

property,

plant

and

equipment

and

other

adjustments

as

defined

by

the

Senior

Secured

Credit

Facility

and

as

further

described

below.

Adjusted

EBITDA

excluding

technology-related

license

expenses

is

calculated

as

Adjusted

EBITDA

less

technology-related

license

expenses.

Adjusted

EBITDA

margin

is

calculated

as

Adjusted

EBITDA

divided

by

net

sales.

Adjusted

EBITDA

margin

excluding

technology-related

license

expenses

is

calculated

as

Adjusted

EBITDA

excluding

technology-related

license

expenses

divided

by

net

sales.

Free

cash

flow

is

calculated

as

net

cash

provided

by

operating

activities

less

capital

expenditures.

Adjusted

free

cash

flow

is

free

cash

flow

adjusted

for

non-recurring

items.

We

use

Adjusted

net

income

to

measure

our

overall

profitability

because

it

better

reflects

our

cash

flow

generation

by

capturing

the

actual

cash

interest

paid

and

cash

taxes

paid

rather

than

our

interest

expense

and

tax

expense

as

calculated

under

GAAP

and

excludes

the

impact

of

the

non-

cash

annual

amortization

of

certain

intangible

assets

that

were

created

at

the

time

of

the

Acquisition

Transaction.

We

use

Adjusted

EBITDA,

Adjusted

EBITDA

excluding

technology-related

license

expenses,

Adjusted

EBITDA

margin

and

Adjusted

EBITDA

margin

excluding

technology-

related

license

expenses

to

evaluate

and

control

our

cash

operating

costs

and

to

measure

our

operating

profitability.

We

use

adjusted

free

cash

flow

and

free

cash

flow

to

evaluate

the

amount

of

cash

generated

by

the

business

that,

after

the

capital

investment

needed

to

maintain

and

grow

our

business,

can

be

used

for

strategic

opportunities,

including

investing

in

our

business

and

strengthening

our

balance

sheet.

We

believe

the

presentation

of

Adjusted

net

income,

Adjusted

EBITDA,

Adjusted

EBITDA

excluding

technology-related

license

expenses,

Adjusted

EBITDA

margin,

Adjusted

EBITDA

margin

excluding

technology-related

license

expenses

and

adjusted

free

cash

flow

enhances

our

investors'

overall

understanding

of

the

financial

performance

and

cash

flow

of

our

business.

You

should

not

consider

Adjusted

net

income,

Adjusted

EBITDA,

Adjusted

EBITDA

excluding

technology-related

license

expenses,

Adjusted

EBITDA

margin,

Adjusted

EBITDA

margin

excluding

technology-related

license

expenses,

adjusted

free

cash

flow

and

free

cash

flow

as

an

alternative

to

net

income

(loss),

determined

in

accordance

with

GAAP,

as

an

indicator

of

operating

performance,

or

as

an

alternative

to

net

cash

provided

by

operating

activities,

determined

in

accordance

with

GAAP,

as

an

indicator

of

Allison’s

cash

flow. |

4

Call Agenda

Q2 2014 Performance

Full Year 2014 Guidance Update |

5

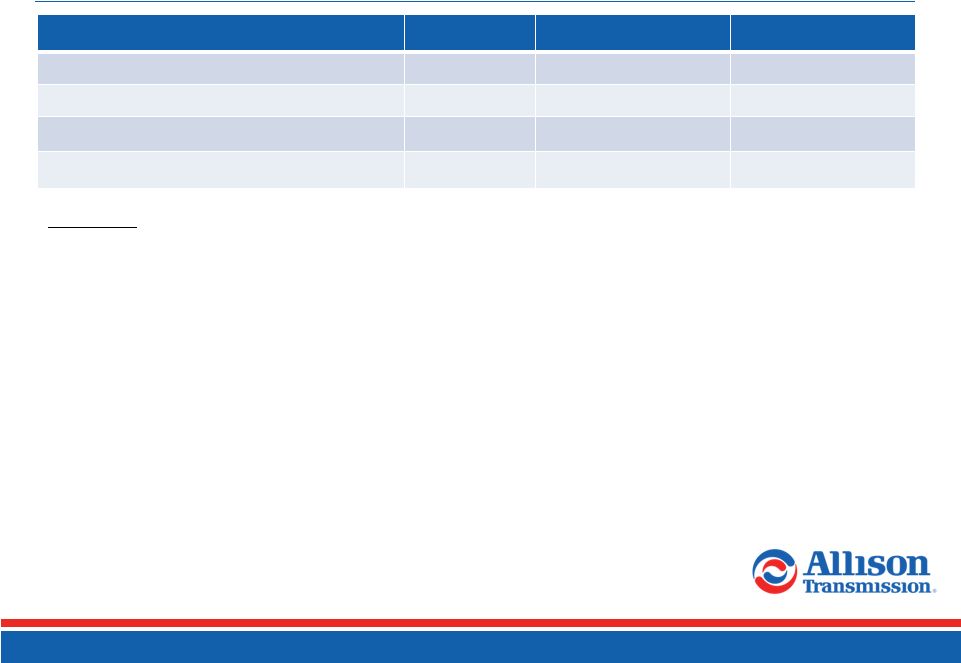

Q2 2014 Performance Summary

($ in millions)

Q2 2014

Q2 2013

% Variance

Net Sales

$536

$512

4.7%

Gross Margin %

44.5%

44.2%

+30 bps

Adjusted Net Income

(1)

$117

$89

30.4%

Adjusted Free Cash Flow

(1)

$132

$117

13.1%

Commentary

Net

Sales:

the

increase

was

principally

driven

by

the

continued

recovery

in

the

North

America

On-Highway

and

Off-

Highway

end

markets,

and

higher

demand

in

the

Service

Parts,

Support

Equipment

&

Other

end

market

partially

offset

by

lower

demand

in

the

Outside

North

America

end

markets

and

previously

contemplated

reductions

in

U.S.

defense

spending.

Gross

Margin:

the

increase

was

principally

driven

by

increased

net

sales

and

price

increases

on

certain

products

partially

offset

by

unfavorable

material

costs.

Adjusted

Net

Income:

the

increase

was

principally

driven

by

increased

net

sales,

price

increases

on

certain

products,

reduced

product

initiatives

spending

and

decreased

cash

interest

expense

partially

offset

by

unfavorable

material

costs.

Adjusted

Free

Cash

Flow:

the

increase

was

principally

driven

by

increased

net

cash

provided

by

operating

activities.

(1)

See Appendix for a reconciliation of Adjusted Net Income and Adjusted Free Cash

Flow. |

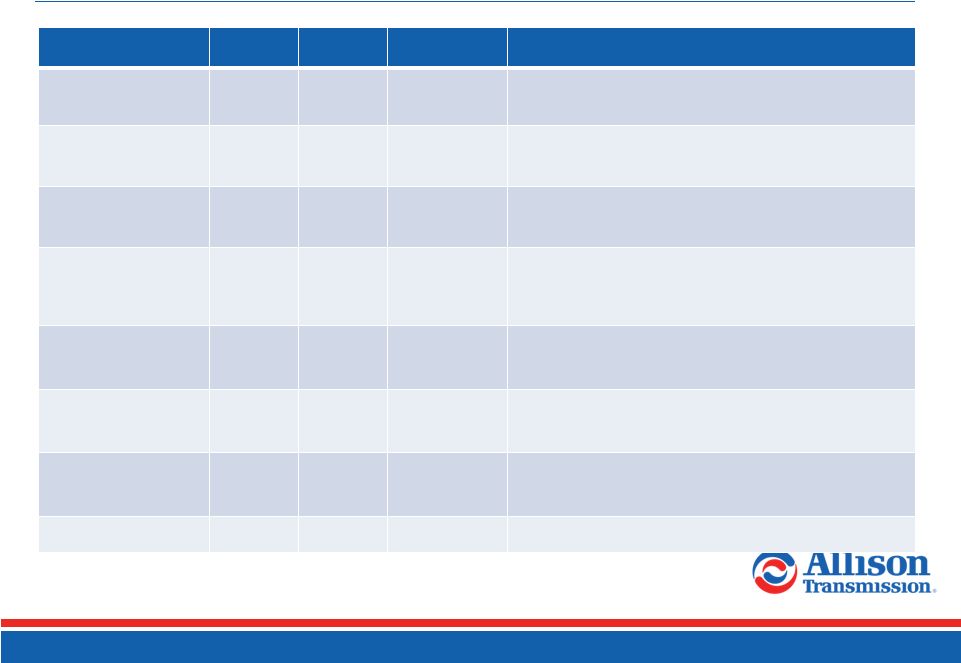

6

Q2 2014 Sales Performance

($ in millions)

End Markets

Q2 2014

Q2 2013

% Variance

Commentary

North America On-Hwy

$243

$216

13%

Increased demand for Rugged Duty Series and Pupil

Transport/Shuttle Series models

North America Hybrid-

Propulsion Systems for

Transit Bus

$28

$27

4%

Increased demand principally driven by intra-year

movement in the timing of orders

North America Off-Hwy

$23

$8

188%

Increased demand driven by hydraulic fracturing

applications

Defense

$49

$58

(16%)

Continued reductions in U.S. defense spending to longer

term averages experienced during periods without active

conflicts partially offset by the recognition of previously

deferred tracked revenue

Outside North America

On-Hwy

$62

$75

(17%)

Weakness in China, Europe and South America

Outside North America

Off-Hwy

$24

$36

(33%)

Weaker demand conditions in the energy sector partially

offset by higher demand from the mining sector

Service Parts, Support

Equipment & Other

$107

$92

16%

Increased demand for North America service parts and

North America On-Highway support equipment

Total

$536

$512

5% |

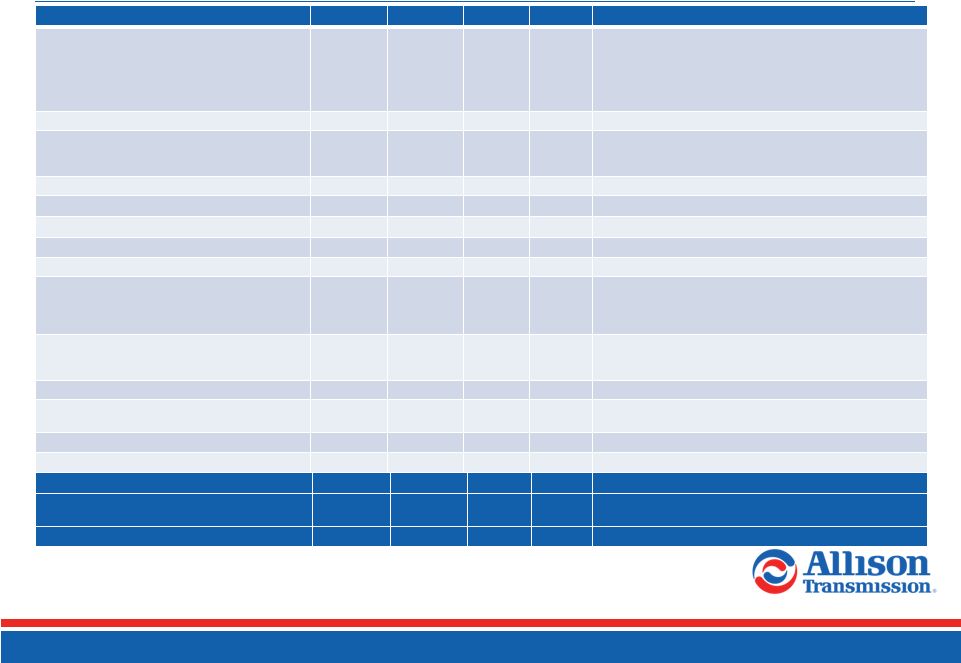

7

Q2 2014 Financial Performance

($ in millions, except share data)

Q2 2014

Q2 2013

$ Var

% Var

Commentary

Net Sales

$536.1

$512.1

$24.0

4.7%

Increase principally driven by the continued recovery in the North

America On-Highway and Off-Highway end markets, and higher

demand in the Service Parts, Support Equipment & Other end

market partially offset by lower demand in the Outside North

America end markets and previously contemplated reductions in

U.S. defense spending

Cost of Sales

$297.6

$286.0

($11.6)

(4.1%)

Gross Profit

$238.5

$226.1

$12.4

5.5%

Increase principally driven by increased net sales and price

increases on certain products partially offset by unfavorable

material cost

Operating Expenses

Selling, general and administrative expenses

$85.1

$85.6

$0.5

0.6%

Engineering –

research and development

$21.2

$22.8

$1.6

7.0%

Decrease principally driven by reduced product initiatives spending

Total operating expenses

$106.3

$108.4

$2.1

1.9%

Operating Income

$132.2

$117.7

$14.5

12.3%

Interest Expense, net

($36.6)

($33.3)

($3.3)

(9.9%)

Increase principally driven by less favorable mark-to-market

adjustments for interest rate derivatives partially offset by debt

repayments and lower LIBOR swap and senior secured credit

facility rates

Other Expense, net

($0.9)

($2.6)

$1.7

65.4%

Decrease principally driven by gains on derivative contracts and

favorable foreign exchange partially offset by lower grant program

income

Income Before Income Taxes

$94.7

$81.8

$12.9

15.8%

Income Tax Expense

($37.5)

($31.3)

($6.2)

(19.8%)

Change in effective tax rate principally driven by the change in

discrete activity

Net Income

$57.2

$50.5

$6.7

13.3%

Diluted Earnings Per Share

$0.31

$0.26

$0.05

19.2%

Q2 2014: 181.6M shares; Q2 2013: 189.9M shares

Adjusted EBITDA

(1)

$186.1

$171.6

$14.5

8.4%

Adjusted EBITDA excluding technology-related

license expenses

(1)

$186.1

$171.6

$14.5

8.4%

Adjusted Net Income

(1)

$116.6

$89.4

$27.2

30.4%

(1)

See Appendix for a reconciliation from Net Income. |

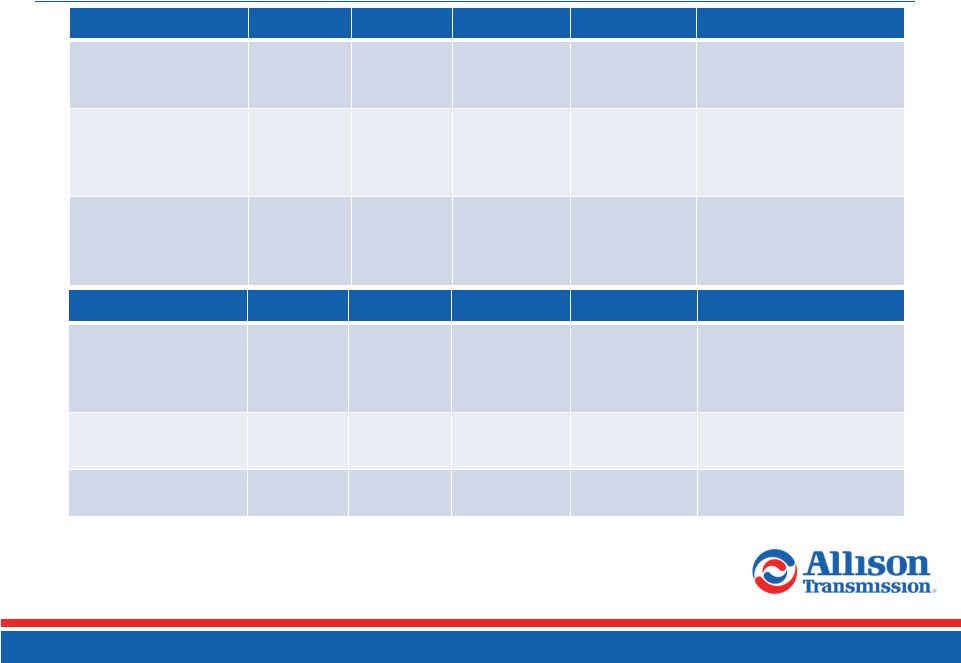

Q2 2014

Cash Flow Performance ($ in millions)

Q2 2014

Q2 2013

$ Variance

% Variance

Commentary

Net Cash Provided by

Operating Activities

$143

$130

$13

10.6%

Principally driven by increased

net sales

CapEx

$12

$13

($1)

(12.1%)

Capital spending in line with

prior year

Adjusted Free Cash

Flow

(1)

$132

$117

$15

13.1%

Principally driven by increased

cash provided by operating

activities

($ in millions)

Q2 2014

Q2 2013

$ Variance

% Variance

Commentary

Operating Working

Capital

(2)

Percentage

of LTM Sales

11.2%

10.4%

N/A

80 bps

Principally driven by increased

net sales

Cash Paid for Interest

$39

$50

($11)

(21.0%)

Principally driven by debt

repayments and refinancing,

and timing

Cash Paid for Income

Taxes

$1

$2

($1)

(44.4%)

Foreign payments timing

(1)

See Appendix for a reconciliation of Adjusted Free Cash Flow.

(2)

Operating

Working

Capital

=

A/R

+

Inventory

–

A/P.

8 |

9

Full Year 2014 Guidance Update

Guidance

Commentary

Net Sales Growth from 2013

4 to 6 percent

In

the

second

half

of

2014

we

expect

net

sales

to

increase

on

a

year-over-year

basis

principally

driven

by

improved

demand

conditions

in

the

North

America

On-Highway

and

Off-Highway

end

markets,

weakness

in

the

Outside

North

America

On-Highway

end

market

and

previously

contemplated

reductions

in

U.S.

defense

spending

Adjusted EBITDA Margin excluding

technology-related license expenses

32.5 to 34.0

percent

Principally driven by sales mix and volume timing

Adjusted Free Cash Flow ($ in millions)

$385 to $425

$2.12 to $2.34 per diluted share

CapEx

($ in millions)

Maintenance

New Product Programs

$55 to $60

$5 to $10

Subject

to

timely

completion

of

development

and

sourcing

milestones

Cash Income Taxes ($ in millions)

$10 to $15

U.S.

income

tax

shield

and

net

operating

loss

utilization |

APPENDIX

Non-GAAP Financial Information

*

*

*

*

*

*

*

*

*****

*****

*****

*****

*****

*****

*****

*****

*****

**** |

11

(1) Includes

charges

or

income

related

to

legacy

employee

benefits,

shared

income

with

General

Motors,

benefit

plan

adjustments,

transitional

costs

to

establish

Allison

as

a

stand-alone

entity,

pension

curtailment

adjustments,

employee

stock

compensation

expense,

service

fees

paid

to

Allison’s

Sponsors

and

an

adjustment

for

the

settlement

of

litigation

which

originated

with

the

Predecessor

but

was

assumed

by

the

Company

as

part

of

the

Acquisition

Transaction.

$ in millions, Unaudited

Last twelve

months ended

June 30,

2009

2010

2011

2012

2013

2013

2014

2014

Net (loss) income

($323.9)

$29.6

$103.0

$514.2

$165.4

$50.5

$57.2

$196.7

plus:

Interest expense,

net

234.2

277.5

217.3

151.2

132.9

33.3

36.6

137.4

Cash interest expense

(242.5)

(239.1)

(208.6)

(167.3)

(159.2)

(49.6)

(39.2)

(148.2)

Income tax expense (benefit)

41.4

53.7

47.6

(298.0)

100.7

31.3

37.5

117.2

Cash income

taxes

(5.5)

(2.2)

(5.8)

(10.7)

(3.8)

(1.8)

(1.0)

(3.9)

Fee to terminate services agreement with Sponsors

—

—

—

16.0

—

—

—

—

Technology-related investment expenses

—

—

—

14.4

5.0

—

—

2.5

Public offering expenses

—

—

—

6.1

1.6

0.6

0.8

2.1

Trade name

impairment

190.0

—

—

—

—

—

—

—

Amortization of intangible

assets

155.9

154.2

151.9

150.0

105.3

25.1

24.7

99.7

Adjusted net

income

$49.6

$273.7

$305.4

$375.9

$347.9

$89.4

$116.6

$403.5

Cash interest expense

242.5

239.1

208.6

167.3

159.2

49.6

39.2

148.2

Cash income

taxes

5.5

2.2

5.8

10.7

3.8

1.8

1.0

3.9

Depreciation of property, plant and equipment

105.9

99.6

103.8

102.5

98.7

25.0

24.1

96.4

(Gain)/loss on redemptions and repayments of long-term debt

(8.9)

(3.3)

16.0

22.1

0.8

—

—

0.8

Dual power inverter module extended coverage

11.4

(1.9)

—

9.4

(2.4)

—

—

(2.4)

UAW Local 933 signing bonus

—

—

—

8.8

—

—

—

—

Benefit plan re-measurement

—

—

—

2.3

—

—

—

—

Unrealized (gain) loss on commodity hedge contracts

(5.8)

0.3

6.5

(1.0)

1.5

0.6

(1.2)

(1.5)

Unrealized (gain) loss on foreign exchange

—

(0.2)

0.3

0.1

2.3

(0.1)

1.7

3.2

Premiums and expenses on tender offer for long-term debt

—

—

56.9

—

—

—

—

—

Restructuring charges

47.9

—

—

—

1.0

1.0

0.7

0.7

Reduction of supply contract liability

—

(3.4)

—

—

—

—

—

—

Other, net

(1)

53.2

10.9

8.6

7.0

13.8

4.3

4.0

13.4

Adjusted

EBITDA

$501.3

$617.0

$711.9

$705.1

$626.6

$171.6

$186.1

$666.2

Adjusted EBITDA excluding technology-related license expenses

$501.3

$617.0

$711.9

$717.1

$632.6

$171.6

$186.1

$669.5

Net Sales

$1,766.7

$1,926.3

$2,162.8

$2,141.8

$1,926.8

$512.1

$536.1

$1,987.0

Adjusted EBITDA

margin

28.4%

32.0%

32.9%

32.9%

32.5%

33.5%

34.7%

33.5%

Adjusted EBITDA margin excl technology-related license expenses

28.4%

32.0%

32.9%

33.5%

32.8%

33.5%

34.7%

33.7%

Three months ended

June 30,

For the year ended December 31,

Non-GAAP Reconciliations

(1 of 2)

Adjusted Net Income and Adjusted EBITDA reconciliation

|

12

$ in millions, Unaudited

Last twelve

months ended

June 30,

2009

2010

2011

2012

2013

2013

2014

2014

Net Cash Provided by Operating Activities

$168.7

$388.9

$469.2

$497.5

$453.5

$129.7

$143.4

$511.1

(Deductions) or Additions:

Long-lived assets

(88.2)

(73.8)

(96.9)

(123.9)

(74.4)

(13.2)

(11.6)

(71.3)

Fee to terminate services agreement with Sponsors

—

—

—

16.0

—

—

—

—

Technology-related license expenses

—

—

—

12.0

6.0

—

—

3.3

2009 Non-Recurring Activity

61.0

—

—

—

—

—

—

—

Adjusted Free Cash Flow

$141.5

$315.1

$372.3

$401.6

$385.1

$116.5

$131.8

$443.1

Net

Sales

$1,766.7

$1,926.3

$2,162.8

$2,141.8

$1,926.8

$512.1

$536.1

$1,987.0

Adjusted Free Cash Flow (% to Net Sales)

8.0%

16.4%

17.2%

18.8%

20.0%

22.7%

24.6%

22.3%

Three months ended

June 30,

For the year ended December 31,

(1)

2009

adjusted

for

certain

non-recurring

activity:

(a)

capitalized

accrued

interest

on

Senior

Toggle

Notes

($29)

million,

(b)

cash

restructuring

charge

$51

million,

(c)

accounts

payable

early

payments

$3

million,

(d)

delayed

accounts

receivable

receipts

$19

million

and

(e)

Lehman

LIBOR

swap

settlement

$17

million.

Non-GAAP Reconciliations

(2 of 2)

Adjusted Free Cash Flow reconciliation

(1) |