Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - ALLERGAN INC | d758653dex991.htm |

| EX-99.3 - EX-99.3 - ALLERGAN INC | d758653dex993.htm |

| 8-K - FORM 8-K - ALLERGAN INC | d758653d8k.htm |

| EX-99.4 - EX-99.4 - ALLERGAN INC | d758653dex994.htm |

July

21, 2014 Allergan

A Specialist in the Biopharmaceutical

& Medical Device Industries

Exhibit 99.2 |

2

2

Forward-Looking Statements

®

& ™

Marks owned by Allergan, Inc.

JUVÉDERM

®

is

a

registered

trademark

of

Allergan

Industrie

SAS

All

other

products

are

registered

trademarks

of

their

respective

companies

This

presentation

contains

“forward-looking

statements,”

including

statements

regarding

product

acquisition

and

development,

regulatory

approvals, market potential, expected growth, operational efficiencies, a proposed

offer made by Valeant, and Allergan’s expected, estimated

or

anticipated

future

results,

including

Allergan’s

earnings

per

share

and

revenue

forecasts,

among

other

statements.

All

forward-looking statements herein are based on Allergan’s current

expectations of future events and represent Allergan’s judgment only as

of the date of this presentation. If underlying assumptions prove inaccurate or

unknown risks or uncertainties materialize, actual results could vary

materially from Allergan's expectations and projections. Therefore, you are cautioned not to rely on any of these forward-looking

statements and Allergan expressly disclaims any intent or obligation to update

these forward-looking statements except as required to do so by

law. Actual results may differ materially from Allergan’s current

expectations based on a number of factors affecting Allergan’s businesses,

including

changing

competitive,

market

and

regulatory

conditions;

the

timing

and

uncertainty

of

the

results

of

both

the

research

and

development and regulatory processes; domestic and foreign health care and cost

containment reforms, including government pricing, tax and reimbursement

policies; revisions to regulatory policies related to the approval of competitive generic products; technological advances

and

patents

obtained

by

competitors;

the

ability

to

obtain

and

maintain

adequate

protection

of

intellectual

property

rights;

the

performance

of new products, including obtaining government approval and consumer and physician

acceptance, the continuing acceptance of currently marketed products, and

consistency of treatment results among patients; the effectiveness of promotional and advertising campaigns; the

potential for negative publicity concerning any of Allergan’s products; the

timely and successful implementation of strategic initiatives, including

expansion of new or existing products into new markets; the results of any pending or future litigation, investigations or claims; the

uncertainty associated with the identification of, and successful consummation,

execution and integration of, external corporate development initiatives and

strategic partnering transactions; potential difficulties in manufacturing; and Allergan’s ability to obtain and

successfully maintain a sufficient supply of products to meet market demand in a

timely manner. In addition, matters generally affecting the U.S. and

international economies, including consumer confidence and debt levels, changes in interest and currency exchange rates,

political

uncertainty,

international

relations,

the

status

of

financial

markets

and

institutions,

impact

of

natural

disasters

or

geo-political

events

and the state of the economy worldwide, may materially affect Allergan’s

results. These and other risks and uncertainties affecting Allergan’s

businesses and operations may be found in Allergan’s most recently filed

Annual Report on Form 10-K and any subsequent Quarterly Reports on Form

10-Q, including under the heading “Risk Factors”. These

filings, as well as Allergan's other public filings with the U.S. Securities and

Exchange Commission (SEC), can be obtained without charge at

the

SEC's

web

site

at

www.sec.gov.

These

SEC

filings

are

also

available

at

Allergan’s

web

site

at

www.allergan.com

along

with

copies

of Allergan’s press releases and additional information about Allergan. For

further information, you can contact the Allergan Investor Relations

Department by calling 714-246-4636. ©

2014 Allergan, Inc.

All rights reserved. |

3

Allergan Continues to Execute &

Deliver

Increased Value to Stockholders

•

Continued strong performance and business momentum

•

Q2 and Q2 YTD sales growth of 16%

(1)

driven by strength across nearly all

product lines and geographies

•

Q2 and Q2 YTD EPS

(2)

growth in excess of 20%

•

Increase in both Sales & EPS

(2)

guidance for full year 2014

•

Execution of plan to drive further operational efficiencies & create a robust

platform for long-term sustainable growth

•

Streamline SG&A while continuing to focus on revenue growth

opportunities

•

Further enhance R&D productivity

•

Maintain robust double-digit revenue CAGR over long-term plan

•

Further enhanced long-term earnings outlook

•

Additional value from ongoing business development & capital return

(1)

Represents local currency sales growth

(2)

Non-GAAP Diluted Earnings per Share |

4

4

Another Outstanding Quarter Highlights the Strength of

Allergan’s Business Model

Q2 2014 Guidance

(Issued May 7)

$1,725M -

$1,800M

$1.41 -

$1.44

16% -

18%

Actual Q2 2014

Results

$1,827M

$1.51

24%

Product Net Sales

Non-GAAP Diluted

EPS

Non-GAAP Diluted

YOY EPS Growth

Strong business momentum continued in 2nd quarter with record dollar sales

growth Depth

and

breadth

of

contribution

made

by

nearly

all

therapeutic

areas

and

geographies

Leverage of SG&A investments in a thoughtful & disciplined approach

|

5

5

Strong Business Momentum Continues to Accelerate

Sales & EPS Growth

* Sales growth in local currency retrospectively adjusted to exclude

Obesity Intervention Business. **

2012

EPS

growth

includes

the

2012

Obesity

impact

of

$0.10

and

the

2012

R&D

Tax

Credit

impact

of

$0.06.

2013

EPS

Growth

–

Restating

2012

to exclude the 2012 Obesity impact of $0.10 and including the 2012 R&D Tax

Credit impact of $0.06. FY 2012

FY 2013

YTD Q2 2014

Sales Growth*

10%

12%

16%

EPS Growth**

15%

16%

22%

Quarterly Sales & EPS Performance |

Allergan’s 2014 Full Year Earnings Outlook

Continues to Improve

FY 2014

Product Net Sales

Non-GAAP

Diluted EPS

Non-GAAP

Diluted EPS YOY

Growth

$6.8bn -

$7.0bn

$5.64 -

$5.73

18% -

20%

$6.7bn -

$7.0bn

$5.36 -

$5.48

12% -

15%

Feb. 5 Guidance

May 12 Guidance

July 21 Guidance

$6.9bn -

$7.1bn

$5.74 -

$5.80

20% -

22%

6 |

7

Overview of Today’s Plan to Restructure

Our

Operations & Processes

~13% reduction in

workforce

Site closures

~1,500 employees &

~250 vacant positions

3

Annual Cost reductions*

~ $475M

Our ongoing effort to improve efficiency and productivity will further increase

stockholder value

* Includes $27M of Gross Margin enhancements |

8

Driving Sustainable Operational Efficiencies

Without

Compromising Effectiveness

Organization Re-design

•

Refocusing our resources on the highest yielding initiatives

•

Right-sizing, adapting and simplifying our structure and processes

Selling, General and Administrative (SG&A)

•

Past strong investments have created critical mass that can now be leveraged

Research & Development (R&D)

•

Heavy concentration on programs already in clinic

From 1998 –

2014 Allergan Has Successfully Invested to Create Robust Top and Bottom Line Growth

•

Launched new markets, products and geographies

16% Sales CAGR

19% EPS CAGR

>2,000% Stock Price Appreciation

No compromise to our commercial

strategy and low impact to our long-term

revenue growth targets

Maintain strength in our R&D pipeline to

bring innovative therapies to patients

~$475M in annual operational efficiencies expected to be realized in 2015

(1)

(1)

(2)

(1)

Represents 1998 – 2014 CAGR. 2014 is midpoint of July 21, 2014 guidance. (2)

Calculation based on 1998 – July 18, 2014. |

9

Principles Behind Our Enduring Organization

Customer

Centricity

•

DTC spend preserved at 2014 levels in all priority

brands

DTC spend maintained ~$200M

•

Sales force maintained in all key areas

~ 94% of sales force remains intact

Reductions mainly in breast & glaucoma

•

Maintain education and training focus

Innovation

and

Pipeline

•

No changes to Phase 2/3 clinical pharmaceutical

R&D programs

•

Outsource to achieve efficiencies in non-core

areas (e.g. data management, global monitoring)

Preserve study protocol design and

Phase 2B & Phase 3 trials in-house

Culture

and values

•

Success continues to be driven by action-

oriented culture with a premium placed on

generating results

•

Rewire, right-size and reduce complexity /

layers within the organization

•

Optimize processes and speed of

decision

making

Commercial

•

Focus resources on highest ROI areas

•

Preserve customer facing headcount

•

Reduce

complexity

and

layers

within

the

organization

R&D

Principles Underpinning Allergan’s Plan

Allergan will not compromise

our successful business model

Maintains a robust platform for long-term sustainable growth

|

10

10

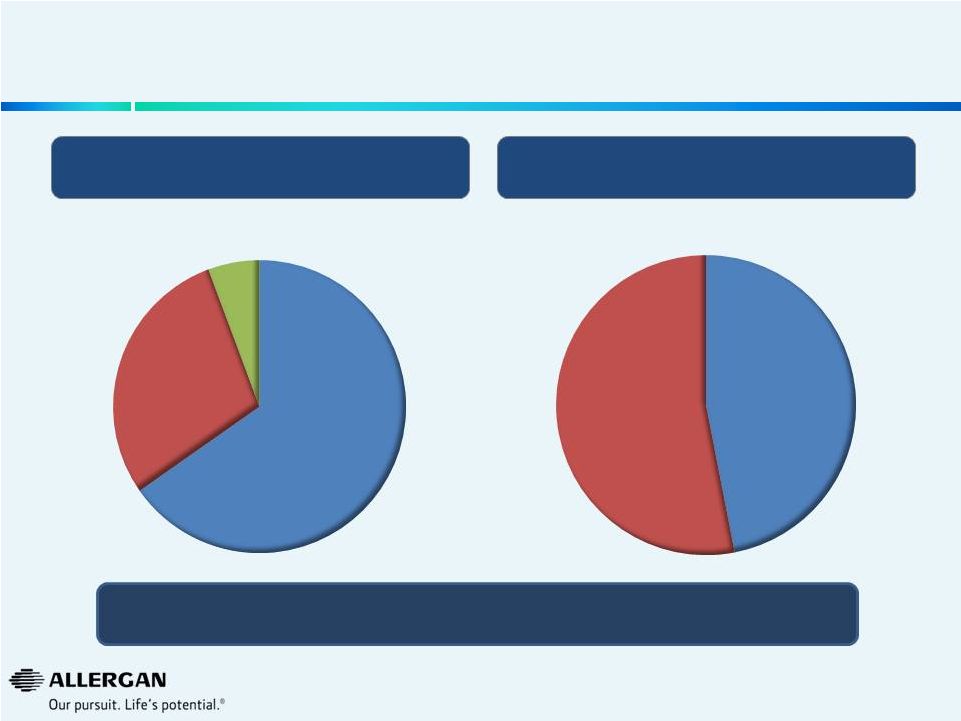

% of Operational Efficiencies from Headcount

Operational Efficiency Mix by P&L Line Item

~$475M Annual Cost Savings

To Be Realized in 2015

~

13%

Reduction

in

Allergan

Workforce

(1)

Implementation

expected

to

be

mostly

completed

in

2014

with

operational

efficiencies

expected to be fully realized in 2015 and beyond

Overview of Operational Efficiencies to be Realized

Gross Margin

6%

R&D

29%

SG&A

65%

Non

Headcount

53%

Headcount

47%

(1)

As part of the restructuring, Allergan will reduce its workforce by approximately 1,500 employees, or

approximately 13 percent of its current global headcount, and eliminate an additional

approximately 250 vacant positions

|

11

Operational Efficiencies Result in a ~13%

Reduction in Allergan

Workforce (1)

As of June 30, 2014. All headcount is rounded.

(2)

As

part

of

the

restructuring,

Allergan

will

reduce

its

workforce

by

approximately

1,500

employees,

or

approximately

13

percent of its current global headcount, and eliminate an additional approximately

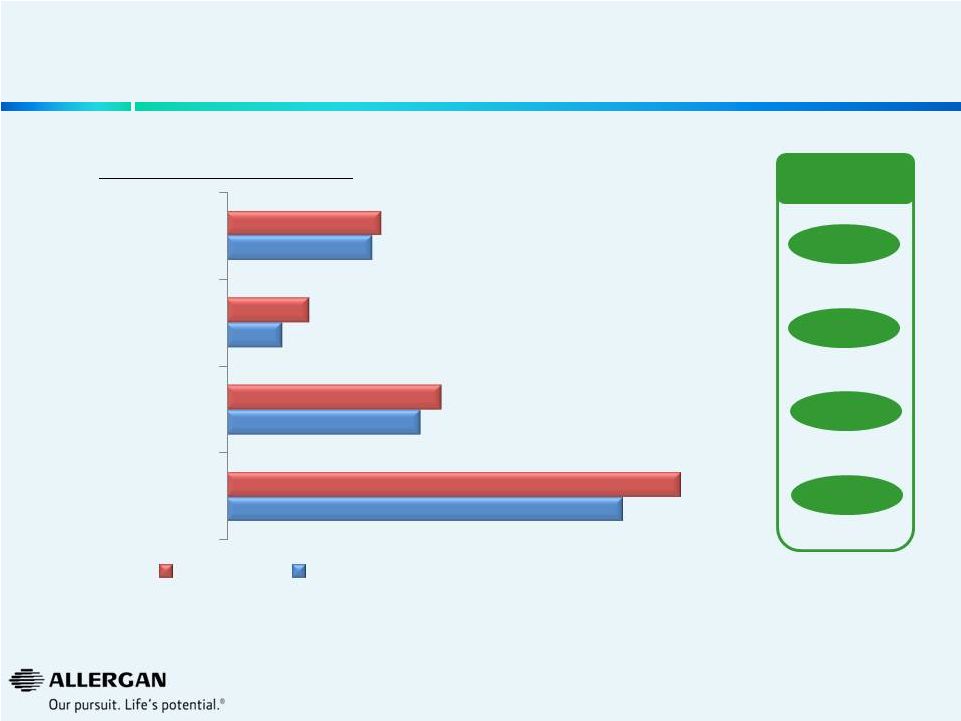

250 vacant positions Headcount (#’s are approximate) -6%

-33%

-10%

-13%

(1)

(2)

% Reduction

10,200

5,000

1,450

3,750

11,700

5,550

2,150

4,000

Total Company

All Other Functions

R&D

Sales Force

Post Operational Efficiencies Plan

Current |

12

$180M

$182M

$26M

$22M

$65M

Focus resources on highest

value opportunities

Streamline organization structure

Simplify processes and interfaces

Optimize site footprint

Enhance strategic sourcing

of goods and services

I

II

III

IV

V

$475M

Total Operational Efficiencies

Five Performance Improvement Levers

Drive

Further Operational Efficiencies |

13

13

Streamlining SG&A While Continuing to

Focus on Revenue Growth Opportunities

Focus resources on

highest value

opportunities

•

Invest

in

key

growth

drivers

(Retina,

Facial

Aesthetics,

RESTASIS

®

,

BOTOX

®

Chronic

Migraine

& Urology)

•

Rationalize spend in lower growth franchises (Breast & Glaucoma IOP

Drops) •

Rebalance

resources

in

favor

of

customer

facing

headcount

and

drive

commercial

excellence

Streamline

Organization

Structure

•

Optimize regional marketing structures and commercial support operations

•

Rationalize

global

functions

(e.g.

Market

Research

&

Medical

Affairs)

•

Reduce management layers and increase span of control (company-wide)

Simplify

Processes &

Interfaces

•

Clarify roles of global, regional and country organizations to speed

decision-making •

Enhance and expand use of regional shared service centers for high volume

transactional

services (e.g. Austin, TX, Westport, Ireland)

•

Reduce number of product promotional cycles and refocus marketing material

creation Enhance strategic

sourcing of goods

and services

•

Improve procurement of vendor services (e.g. advertising agencies and media

buying, market research)

2015 SG&A Operational Efficiencies: ~$310M

Optimize site footprint

•

Close Carlsbad, CA facility acquired in SkinMedica acquisition

•

Streamline commercial regional headquarter locations (Europe, Asia Pacific,

Latin America & Canada)

$145M

$112M

$6M

$38M

$9M |

14

14

R&D Project Rationalization & Increased Efficiencies

Rationalize Projects

$52m

Increase Efficiency

$86m

Outsource non-core functions

Consolidate global development sites

Right-size organization to

align with future R&D budgets

Consolidate R&D vendors

Refocus discovery on core areas of

expertise (e.g. Eye care & Biologics)

Cancel 4 current early stage

discovery projects

Cancel 4 pre-clinical projects with

projected approvals dates post 2020

Reduce investment in Breast franchise

innovation –

no impact pre 2020 |

15

15

•

Focus discovery resources in core areas of expertise (e.g. Eye Care and

Biologics) •

Focus

development

activities

on

high

value

projects

(e.g.

Retina,

Dry

Eye,

Fillers

and

new

BOTOX

®

indications)

•

Continue

to

implement

“quick

kill”

concept

•

Close Santa Barbara, CA and Medford, MA sites and relocate core activities to

other sites •

Consolidate development sites to enable scale and operational efficiency and

effectiveness (Europe, Asia Pacific)

•

Improve procurement of vendor services (e.g. Contract Research Organizations

(CRO’s)) Total 2015 R&D Operational Efficiencies: ~$138M

Further Enhancing R&D Productivity

•

Outsource select non-core functions (e.g. data management) to ensure

flexibility and scalability •

Consolidate duplicative activities within R&D (e.g. create centralized vendor

management group) •

Right-size organization for revised R&D spend

Focus resources on

highest value

opportunities

Streamline

Organization

Structure

Simplify

Processes &

Interfaces

Enhance strategic

sourcing of goods

and services

Optimize site footprint

•

Create single management structure across key R&D functions (e.g. project

management, clinical operations)

•

Integrate R&D IT into Corporate IT

$35M

$65M

$8M

$22M

$8M |

16

16

1 cpd for new indication

ph1

Maintain Rich, Highly Diversified Clinical R&D Pipeline

Post

Approval

Pre-Clinical

Phase I

Phase II –

POC

Phase II –

Confirmatory

Phase III

Registration

Discontinued

Allergan remains committed to an industry leading R&D engine

Limited number of pre-clinical projects have been

cancelled

(all with projected approval dates after 2020)

1857 Migraine

Derma-

tology

•

1 rosacea programs ph1

•

2 acne programs ph1

•

One early preclinical acne

program

•

One early pre

-clinical derm

program for a new indication

•

Bim Hair Growth

•

BTX Masseter

•

Medytox Aesthetic

•

BTX CFL Asia

•

BTX Forehead Lines

•

LATISSE

®

Brow

•

Oxymetazoline

Rosacea

•

ACZONE

X

•

BTX CFL

•

LATISSE

®

US

•

LATISSE

®

Japan

Urology

•

BTX PE

•

SER-120

•

BTX OAB

•

BTX NDO

Neurology

& Pain

•

AGN

-

ph1

•

BTX X with potential for higher

dose and/or longer duration

ph1

•

Senrebotase (TEM)

Pain

•

BTX Depression

•

BTX OA Pain

•

BTX New

Indication

•

Medytox

Therapeutic

•

BTX

Spasticity Adult

LL, Adult UL, Ped LL,

Ped UL

•

AGN-1763 BTX

LL Spasticity

•

“

SEMPRANA

®

”

Headache

•

BTX

Headache

Retina

•

Dual anti

-PDGF/VEGF

DARPin

®

•

1 retina

program

ph1

•

2 early preclinical retina

programs

•

DARPin

®

AMD

•

DARPin

®

DME

•

Brimo

DDS Dry

AMD

•

OZURDEX

®

RVO

China

•

OZURDEX

®

DME (Europe)

•

OZURDEX

®

RVO

•

OZURDEX

®

DME

3B

Anterior

Segment

•

1 NCE

for

Dry

Eye

ph1

•

1 cpd for new

indication

•

•

NCE Dry Eye

•

Androgen Front of

Eye

•

RESTASIS

®

X

•

LASTACAFT

®

Japan

•

RESTASIS

®

EU

•

1 cpd

for front of eye

indication

Glaucoma

•

NCE Glaucoma ph2

•

Combo glaucoma Japan

ph3

•

Bimatoprost

SR

•

LUMIGAN

®

UD

•

LUMIGAN

®

0.01%

EU

•

GANFORT™

UD

•

GANFORT™

China

®

ph2

AMD ph2 |

17

17

R&D Outsourcing Will Ensure Flexibility and Scalability

Strategic partnering with global

CROs for lower overhead & wages

Increased Outsourcing Across R&D for

More Nimble & Focused Development

PharmSci

Clin Ops

Biostatistics

Safety

In-house

Outsourced

Core functions retained

in-house

Allows flexibility and scale for

future R&D spend

Data Mgmt

Global

Monitoring

Global

Medical

Writing

Monitoring

Writing

Medical |

18

18

Total 2015 Gross Margin Operational Efficiencies: $27M*

Further Improvement in Gross Margin Efficiencies

•

Create a Global Supply Chain organization

•

Network optimization

•

Global Procurement

•

Re-design organization at each site and centre

Focus resources on

highest value

opportunities

Streamline

Organization

Structure

Simplify

Processes &

Interfaces

Enhance strategic

sourcing of goods

and services

Optimize site footprint

•

Manufacturing excellence program

•

Optimize activity at select sites

*~$50M by 2016 primarily due to inventory rollout |

19

Driving Sustainable Operational Efficiencies

Without

Compromising Effectiveness

No compromise to our commercial

strategy and low impact to our long-

term revenue growth targets

Maintain strength in our R&D

pipeline to bring innovative

therapies to patients

~$475M in annual operational efficiencies expected to be realized in 2015

Allergan 2014 -

2019

Double-Digit Sales CAGR

despite a ~50 b.p. reduction*

>20% EPS CAGR

2016 EPS -

~$10.00

Additional free cash flow of ~$18bn** and significant borrowing capacity to drive

strategic options and financial flexibility

* There

was

a

~50

basis

point

reduction

in

the

Sales

CAGR

(2014E

–

2019E)

between

guidance

provided

on

May 12, 2014 vs. the guidance provided on July 21, 2014.

** 2014 -

2019 |

20

20

Allergan’s Promising Outlook on Long-Term Organic Growth

Driven by New Product Innovation and Operational Excellence

2013A

2014E

Guidance

2019E

2015E

Guidance

Revenue

$6.2bn

EPS

$4.77

2016E

Guidance

2017E

2018E

* As a percentage of sales.

Additional stockholder value generated from strong business momentum & further

operational efficiencies

Revenue

Growth

Double Digit

EPS

~$10.00

Revenue

$6.9 -

$7.1bn

EPS

$5.74 -

$5.80

EPS Growth

20% -

22%

Revenue

Growth

Double Digit

EPS

$8.20 -

$8.40 |

21

Strategic Options Available to Further Increase

Stockholder Value

•

Value from acquisitions

•

Value from capital return

•

Stock repurchases

•

“Special”

dividend

Additional free cash flow of ~$18bn

generated over strategic planning period |

Allergan’s Standalone Performance Continues To Create

Significant Near-Term and Long-Term Value for Stockholders

(3)

Low Estimate

-

Former

High Estimate

-

Former

Low Estimate

-

Current

High Estimate

-

Current

Pre-Operational

Efficiencies

(2)

Post-Operational

Efficiencies

(1)

22.5x NTM P/E Multiple

25.0x NTM P/E Multiple

Future Value Per Share Allergan

Low Estimate based on 22.5x NTM P/E

High Estimate based on 25.0x NTM P/E

$371

$316

$390

$351

150.00

200.00

250.00

300.00

350.00

$400.00

Current

12/31/2014

12/31/2015

12/31/2016

12/31/2017

12/31/2018

Note: Allergan multiple range (as a standalone company) is based on Wall Street Research as of

07/15/14. (1)

2014 based on July 21, 2014 EPS guidance of $5.74- $5.80, 2015 and 2016 based on guidance of

$8.20-$8.40 and $10.00, respectively, as stated on July 21, 2014. 2017 – 2019 is

implied using 2014-2019 CAGR of >20%.

(2)

2014 based on May 12, 2014 EPS guidance of $5.64 -$5.73, 2015 based on guidance of 20% -

25% YOY EPS growth as stated on May 12, 2014 and 2016 – 2019 assumes 20% YOY EPS growth. (3)

Current Allergan share price of $165.82 as of 07/17/14. (3)

2014 based on midpoint of EPS guidance issued on Feb. 5, 2014 of $5.36 - $5.48, 2015 assumes 22.5%

growth (midpoint of 20% - 25% growth). (4)

2014 based on midpoint of May 12, 2014 EPS guidance of $5.64 -$5.73, 2015 calculated using

midpoint of 20% - 25% YOY EPS growth as stated on May 12, 2014 and 2016 – 2019 assumes

20% YOY EPS growth. (5)

2014 based on midpoint of July 21, 2014 EPS guidance of $5.74- $5.80, 2015 based on

midpoint of $8.20-$8.40 as stated on July 21, 2014, 2016 based on $10.00 and 2017-

2019 is implied using 2014-2019 CAGR of >20%.

22 |

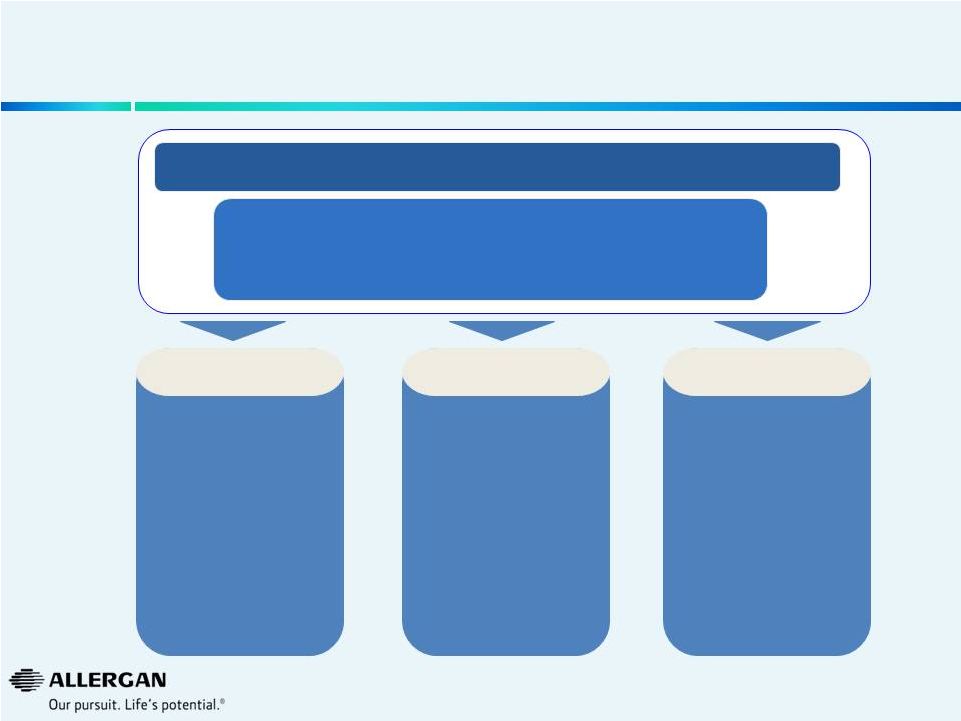

Value Drivers Available to Standalone Allergan to

Further Increase Stockholder Value

Potential

Future

Standalone

Stock Price

Value from Momentum in the Business

Value from Capital Return

Value from Pipeline Assets

Value from Ongoing Business Development

Current Stock

Price

Value Drivers Available to Allergan:

Value from Operational Efficiencies

23 |

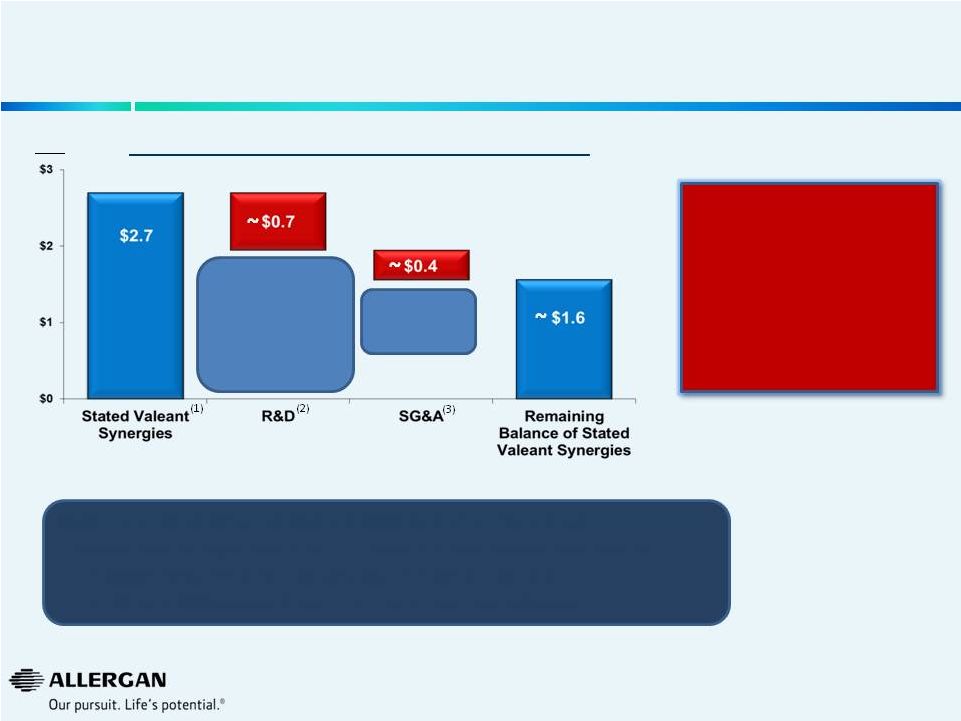

Allergan Actions Have Increased Standalone Value &

Significantly Reduced Synergies Available to Valeant

Reduction To Proposed Valeant Synergies*

Valeant’s purported $2.7bn of R&D and SG&A cuts are unrealistic

given: •

Valeant’s stated objectives in continuing certain R&D projects

post-closing •

the SG&A investments required to sustain Allergan’s products

•

the R&D and SG&A operational efficiencies announced by Allergan

Additional spend for

R&D programs that

Valeant claims to

continue post-closing

and Operational

Efficiencies

announced by

Allergan

Operational

Efficiencies

announced by

Allergan

$bn

Combination of higher

standalone value for Allergan

and Pro-forma impact of

Valeant’s reduced synergies

($1.1bn), has transferred

value from Valeant to

Allergan Stockholders

24

* Illustrative for 2015

(1)

Valeant SEC filings

(2)

Programs

Valeant

claims

to

continue

after

potential

post

closing

of

transaction.

Includes

all

Phase

3

pharmaceutical

programs

(including

DARPin®

&

Bimatoprost

Sustained

Release

Implant),

BOTOX®

Phase

2

&

3

programs,

Medytox

®,

Late-Stage Filler programs, IIT’s

(3)

Based on operational efficiencies announced on May 12, 2104 and July 21, 2014

|

Allergan Has an Enduring Vision and a Goal to Create an

Even Stronger Company

Revenue Goal: ~$12bn by 2019

•

Double

digit

sales

growth

(2014E

–

2019E)

•

>20%

EPS

CAGR

(2014E

–

2019E)

•

Franchise leadership: #1 or #2 in every category

Our earnings growth is

founded on quality net

sales growth

In short, our profit

comes from serving the

needs of physicians and

their patients

Customer-centric

We have a unique

employee culture that

drives our success

Action orientated and

flexible with a premium

placed on generating

results

Culture & Values

We have an enduring

model for the future

founded on an R&D

pipeline that is informed

by our intimate

knowledge of our

customers and the

franchises in which we

choose to operate

Innovation

25 |

26

26

Allergan’s promising outlook on long-term growth driven by new product

innovation and operational excellence:

—

Additional free cash flow of ~$18bn to drive strategic options and financial

flexibility —

5-year double digit revenue growth and >20% EPS CAGR

Investor

community

has

realized

an

increase

in

Allergan

value

as

our

management

team

has

and will continue to enhance business performance and outlook

To further enhance stockholder value, Allergan remains focused on ongoing value

driving opportunities

Allergan

management

team

best

equipped

to

deliver

significant

value

for

stockholders

–

our

track record speaks for itself

Conclusions

Allergan management and Board of Directors are committed to delivering

the highest value for stockholders |

27

Reconciliation of Selected Non-GAAP Financial Measures

“GAAP” refers to financial information presented in accordance with generally accepted

accounting principles in the United States.

In this presentation, Allergan included historical non-GAAP financial measures, as defined in

Regulation G promulgated by the Securities and Exchange Commission, with respect to estimates

for the year ended December 31, 2013, and the corresponding periods for 1999 through 2012. The

information for 2012 and 2011 has been retrospectively adjusted to reflect the obesity

intervention unit, which was sold on December 2, 2013, as discontinued operations.

Allergan believes that its presentation of historical non-GAAP financial measures provides

useful supplementary information to investors. The presentation of historical non-GAAP financial

measures is not meant to be considered in isolation from or as a substitute for results prepared in

accordance with GAAP.

In this presentation, Allergan reported certain financial measures including “Adjusted

Sales”, “Adjusted SG&A”, “Adjusted R&D”, “Adjusted

EPS”, “Pro forma Growth” and “Sales Growth at constant exchange rates” as

adjusted for Non-GAAP items. Allergan uses these financial measures to enhance the investor’s

overall understanding of the financial performance and prospects for the future of

Allergan’s core business activities. Specifically, Allergan believes that a report

of these financial measures provides consistency in Allergan’s financial reporting and

facilitates the comparison of results of core business operations between its current, past and

future periods. Adjusted Sales, Adjusted SG&A, Adjusted R&D, Adjusted EPS, Pro forma Growth and Sales

Growth are the primary indicators management uses for planning and forecasting in future

periods. Allergan also uses Adjusted Sales, Adjusted R&D and Adjusted EPS for

evaluating management performance for compensation purposes.

A reconciliation of non-GAAP items may be found under the heading “Non-GAAP Financial

Reconciliation” in the investor

relations

section

of

the

www.Allergan.com

website. |

28

28

Important Information

Allergan, its directors and certain of its officers and employees are participants in solicitations of

Allergan stockholders. Information regarding the names of Allergan's directors and executive

officers and their respective interests in Allergan by security holdings or otherwise is set

forth in Allergan's proxy statement for its 2014 annual meeting of stockholders, filed with the

SEC on March 26, 2014, as supplemented by the proxy information filed with the SEC on April 22,

2014. Additional information can be found in Allergan's Annual Report on Form 10-K for the

year ended December 31, 2013, filed with the SEC on February 25, 2014 and its Quarterly Report

on Form 10-Q for the quarter ended March 31, 2014, filed with the SEC on May 7, 2014. To the extent

holdings of Allergan's securities have changed since the amounts printed in the proxy statement for

the 2014 annual meeting of stockholders, such changes have been reflected on Initial Statements

of Beneficial Ownership on Form 3 or Statements of Change in Ownership on Form 4 filed with the

SEC. These documents are STOCKHOLDERS ARE ENCOURAGED TO READ ANY ALLERGAN SOLICITATION STATEMENT (INCLUDING

ANY SUPPLEMENTS THERETO) AND ANY OTHER RELEVANT DOCUMENTS THAT ALLERGAN MAY FILE

WITH THE SEC CAREFULLY AND IN THEIR ENTIRETY BECAUSE THEY WILL CONTAIN IMPORTANT

INFORMATION. Stockholders will be able to obtain, free of charge, copies of any solicitation statement

and any

www.sec.gov.

www.allergan.com.

available

free

of

charge

at

the

SEC’s

website

at

other

documents

filed

by

Allergan

with

the

SEC

at

the

SEC's

website

at

www.sec.gov.

In

addition,

copies

will

also

be

available

at

no

charge

at

the

Investors

section

of

Allergan's

website

at |

July

21, 2014 Allergan

A Specialist in the Biopharmaceutical

& Medical Device Industries

29 |