Attached files

| file | filename |

|---|---|

| 8-K - 8-K - NTELOS HOLDINGS CORP. | d744512d8k.htm |

NASDAQ: NTLS

Investor Presentation

June 2014

Exhibit 99.1 |

Presentation

of

Financial

and

Other

Important

Information

USE OF NON-GAAP FINANCIAL MEASURES

Included

in

this

presentation

are

certain

non-GAAP

financial

measures

that

are

not

determined

in

accordance

with

US

generally

accepted

accounting

principles

(“GAAP”).

These

financial

performance

measures

are

not

indicative

of

cash

provided

or

used

by

operating

activities

and

exclude

the

effects

of

certain

operating,

capital

and

financing

costs

and

may

differ

from

comparable

information

provided

by

other

companies,

and

they

should

not

be

considered

in

isolation,

as

an

alternative

to,

or

more

meaningful

than

measures

of

financial

performance

determined

in

accordance

with

US

generally

accepted

accounting

principles.

These

financial

performance

measures

are

commonly

used

in

the

industry

and

are

presented

because

NTELOS

believes

they

provide

relevant

and

useful

information

to

investors.

NTELOS

utilizes

these

financial

performance

measures

to

assess

its

ability

to

meet

future

capital

expenditure

and

working

capital

requirements,

to

incur

indebtedness

if

necessary,

and

to

fund

continued

growth.

NTELOS

also

uses

these

financial

performance

measures

to

evaluate

the

performance

of

its

business,

for

budget

planning

purposes

and

as

factors

in

its

employee

compensation

programs.

Adjusted

EBITDA

is

defined

as

net

income

attributable

to

NTELOS

Holdings

Corp.

before

interest,

income

taxes,

depreciation

and

amortization,

accretion

of

asset

retirement

obligations,

deferred

SNA

revenue,

gain/loss

on

derivatives,

net

income

attributable

to

non-controlling

interests,

other

expenses/income,

equity

based

compensation

charges,

business

separation

charges,

gain/loss

on

sale

of

assets,

secondary

offering

costs

and

net

loss

from

discontinued

operations

and

costs

related

to

the

separation

of

the

wireless

and

wireline

companies.

SPECIAL

NOTE

REGARDING

FORWARD-LOOKING

STATEMENTS

Any

statements

contained

in

this

presentation

that

are

not

statements

of

historical

fact,

including

statements

about

our

beliefs

and

expectations,

are

forward-looking

statements

and

should

be

evaluated

as

such.

The

words

“anticipates,”

“believes,”

“expects,”

“intends,”

“plans,”

“estimates,”

“targets,”

“projects,”

“should,”

“may,”

“will”

and

similar

words

and

expressions

are

intended

to

identify

forward-looking

statements.

Such

forward-looking

statements

reflect,

among

other

things,

our

current

expectations,

plans

and

strategies,

and

anticipated

financial

results,

all

of

which

are

subject

to

known

and

unknown

risks,

uncertainties

and

factors

that

may

cause

our

actual

results

to

differ

materially

from

those

expressed

or

implied

by

these

forward-looking

statements.

Many

of

these

risks

are

beyond

our

ability

to

control

or

predict.

Because

of

these

risks,

uncertainties

and

assumptions,

you

should

not

place

undue

reliance

on

these

forward-looking

statements.

Furthermore,

forward-looking

statements

speak

only

as

of

the

date

they

are

made.

We

do

not

undertake

any

obligation

to

update

or

review

any

forward-looking

information,

whether

as

a

result

of

new

information,

future

events

or

otherwise.

Important

factors

with

respect

to

any

such

forward-looking

statements,

including

certain

risks

and

uncertainties

that

could

cause

actual

results

to

differ

from

those

contained

in

the

forward-looking

statements,

include,

but

are

not

limited

to:

our

ability

to

attract

and

retain

retail

subscribers

to

our

services;

our

dependence

on

our

strategic

relationship

with

Sprint

Corporation

(“Sprint”);

a

potential

increase

in

roaming

rates

and

wireless

handset

subsidy

costs;

rapid

development

and

intense

competition

in

the

telecommunications

industry;

our

ability

to

finance,

design,

construct

and

realize

the

benefits

of

any

planned

network

technology

upgrade;

our

ability

to

acquire

or

gain

access

to

additional

spectrum;

the

potential

to

experience

a

high

rate

of

customer

turnover;

the

potential

for

competitors

to

build

networks

in

our

markets;

cash

and

capital

requirements;

operating

and

financial

restrictions

imposed

by

our

credit

agreement;

adverse

economic

conditions;

federal

and

state

regulatory

fees,

requirements

and

developments;

loss

of

ability

to

use

our

current

cell

sites;

our

continued

reliance

on

indirect

channels

of

retail

distribution;

our

reliance

on

certain

suppliers

and

vendors;

and

other

unforeseen

difficulties

that

may

occur.

These

risks

and

uncertainties

are

not

intended

to

represent

a

complete

list

of

all

risks

and

uncertainties

inherent

in

our

business,

and

should

be

read

in

conjunction

with

the

more

detailed

cautionary

statements

and

risk

factors

included

in

our

SEC

filings,

including

our

most

recent

Annual

Report

filed

on

Form

10-K.

2 |

Leading “pure-play”

publicly traded regional wireless carrier

8.0

million

operational

market

POPs

;

6.0

million

covered

POPs;

468,000 subscribers

Exclusive wholesale network provider for Sprint in WV and

Western Va. through 2022

Branded retail business and wholesale business with significant

recurring revenue

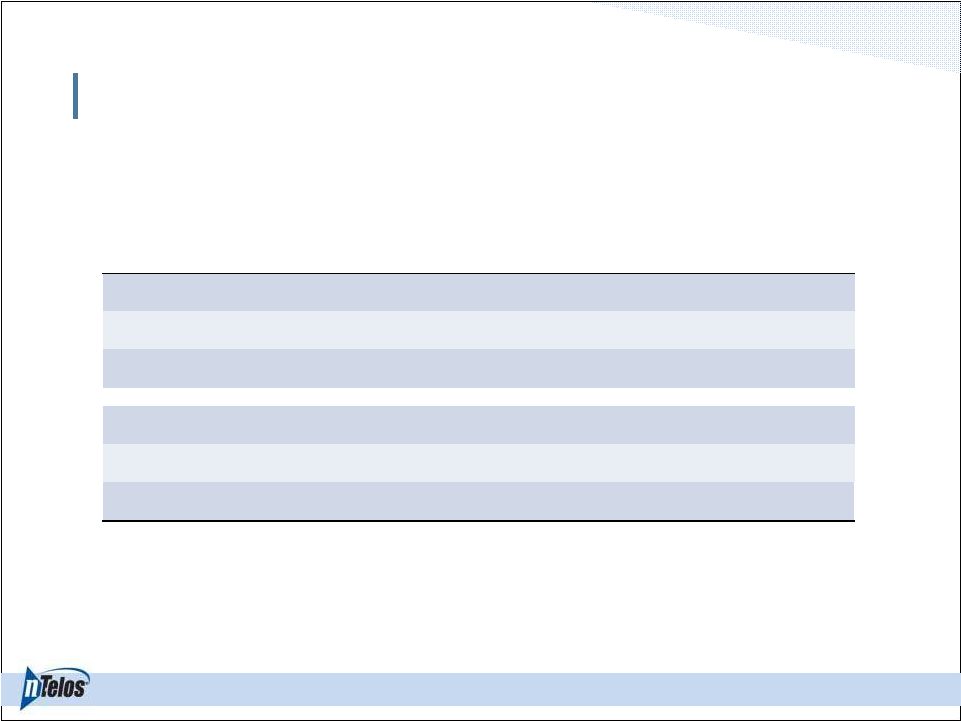

Company Overview

3

About nTelos

Headquarters

Waynesboro,

Va.

Ticker

NTLS

Exchange

NASDAQ

Price

$12.81

Market Cap

$278 million

Shares

21.7 million

52 Week Range

$11.20 –

$23.03

1

9.0 million licensed POPs

As of June 9, 2014

1 |

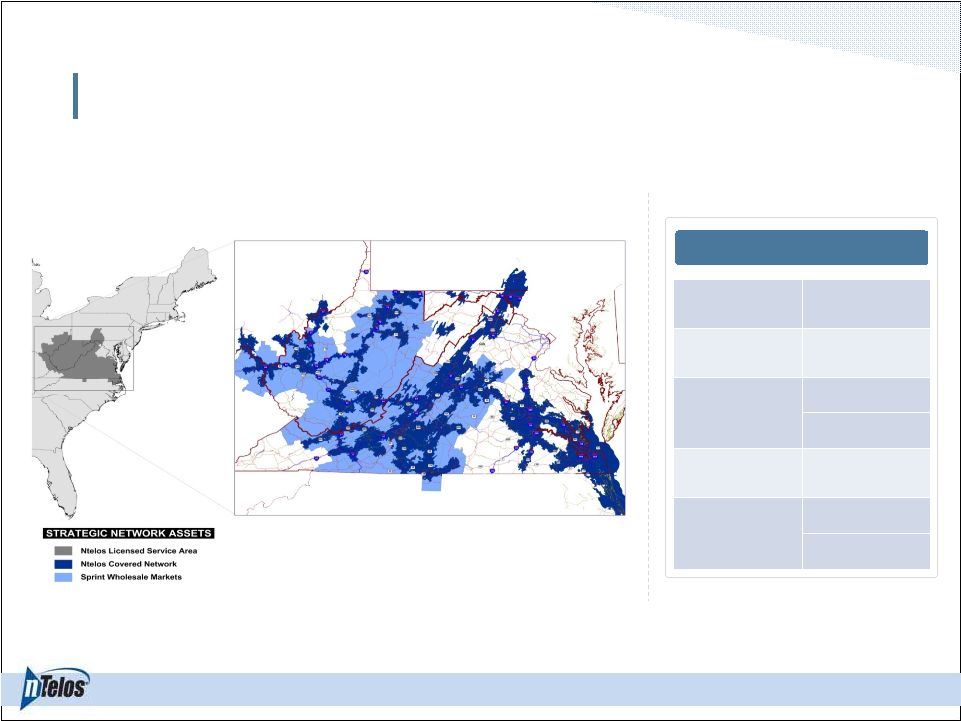

4

nTelos Network

Operational Footprint

Operational

POPs

8.0 million

Covered

POPs

6.0 million

MHz POPs

nTelos: 186.9M PCS

62.4M 2.5 GHz

Sprint: 69.4M PCS

20.3M 800 MHz

Total Cell

Sites

1,444

Spectrum

nTelos: AWS / PCS /

2.5 GHz

Sprint: 800 MHz /

PCS / 2.5 GHz |

5

Retail

Subscriber Base

Prepay

Retail

subscriber

base

comprised

of

two-thirds

postpay,

one-third

prepay

Postpay

Revenue

Retail

revenues

of

$81.4

million

in

1Q

14,

or

67%

of

total

revenues

Platform

130 branded retail locations

705 total points of distribution

Robust retail lineup including

iPhone, Samsung Galaxy, and

Moto X

nTelos

operates

the

postpay

business

under

NTELOS

brand

and

prepay

under

the

FRAWG

brand |

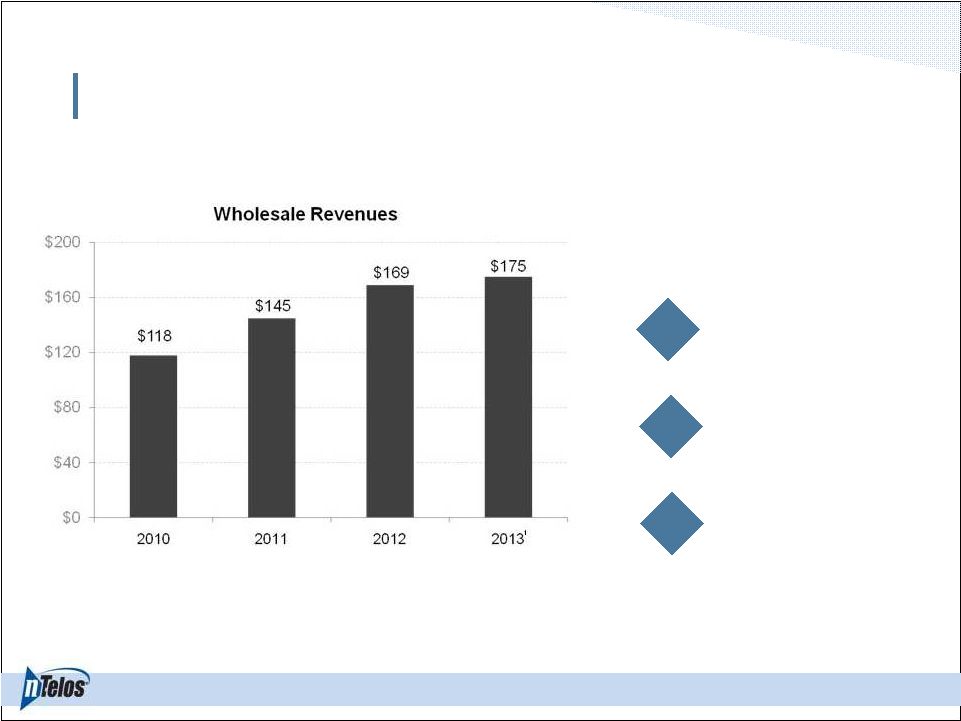

6

Wholesale

nTelos

provides

wholesale

services

to

other

wireless

carriers.

The

primary

source

of

wholesale

revenues

comes

from

the

Strategic

Network

Alliance

(SNA)

with

Sprint.

Wholesale Business

SNA covers 2.1 mm

covered POPs in West

Virginia and western

Virginia; 853

cell sites

SNA revenue accounted

for 97%

of wholesale

revenues in 1Q14

Wholesale and other

revenue accounted for

34%

of total revenues in

1Q14

1

Includes $9.0 million from September 2013 SNA Settlement with Sprint

|

Unique retail / wholesale business model

One

of

the

few

remaining

“pure-play”

regional

wireless

carriers

Value Drivers

7

Strategic

set

of

assets

–

network,

spectrum

portfolio,

retail

subscriber

base,

rural

and

top

40

US

wireless markets

Actively investing in network and strategy to drive next phase of growth

Long

term

strategic

relationship

with

Sprint

–

provides

platform

for

stability,

growth

and

increased optionality |

Expand wholesale relationships

Partnerships

Investments –

Strategic Assets

Executing on wholesale / retail strategy

NTELOS Strategy –

Catalyst for Growth

8

Long term value creation and

cash flow generation

Improved strategic optionality

for all stakeholders

Sprint extension and expansion

Further collaboration with Sprint

DISH

Other opportunities

Improve retail margins to create value

Market and revenue share growth

Greater efficiencies

Focus on customer experience

Network

Devices

Differentiated value proposition

Sprint

Dish

Owned Spectrum

4G LTE Network

Recurring revenue

468,000 subscribers

1

2 |

Expand wholesale relationships

Partnerships

Investments –

Strategic Assets

Executing on wholesale / retail strategy

NTELOS Strategy –

Catalyst for Growth

9

Long term value creation and

cash flow generation

Sprint extension and expansion

Further collaboration with Sprint

DISH

Other opportunities

Improve retail margins to create value

Market and revenue share growth

Greater efficiencies

Focus on customer experience

Network

Devices

Differentiated value proposition

Sprint

Dish

Owned Spectrum

4G LTE Network

Recurring revenue

468,000 subscribers

1

2

Improved strategic optionality

for all stakeholders |

Retail Subscriber Growth

10

Addition of iconic device

Wholesale uncertainty

Platform for retail growth

Brand and retail revitalization

Source: UBS (US Wireless 411, May 20, 2014)

nTelos is the only regional wireless carrier to grow subscriber base since end of

2011 Retail acceleration |

Retail Growth Drivers Going Forward

nControl

4G LTE service expansion

Device financing program (EIP)

Competitive handset lineup

Savings, Simplicity and Service

11 |

Partnerships

Investments –

Strategic Assets

Executing on wholesale / retail strategy

NTELOS Strategy –

Catalyst for Growth

12

Long term value creation and

cash flow generation

Improve retail margins to create value

Market and revenue share growth

Greater efficiencies

Focus on customer experience

Network

Devices

Differentiated value proposition

Sprint

Dish

Owned Spectrum

4G LTE Network

Recurring revenue

468,000 subscribers

1

2

Improved strategic optionality

for all stakeholders

Expand wholesale relationships

Sprint extension and expansion

Further collaboration with Sprint

DISH

Other opportunities |

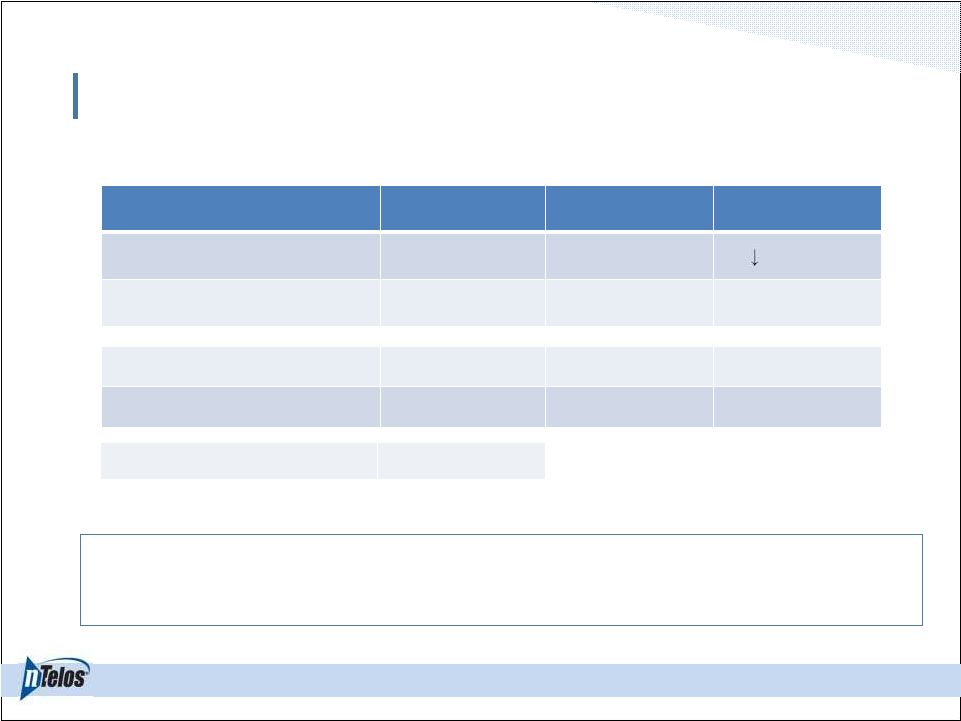

Sprint Agreement –

Platform For Growth

13

Terms

Previous SNA

Amended SNA (May 22, 2014)

Expiration

July 31, 2015

December 31, 2022

Coverage Area

•

2.1 mm covered POPs in West Virginia and western

Virginia

•

853 cell sites

•

36,800 square miles

•

2.1 mm covered POPs in West Virginia and western

Virginia

•

853 cell sites

•

36,800 square miles

Network

2G/3G

2G/3G/4G LTE / future feature upgrades

Spectrum

1.9 PCS (nTelos)

800/1.9/2.5 (nTelos & Sprint)

Anticipated 4G LTE

Buildout Timeline

N/A

Expect to be completed no later than May 2017

Nationwide Roaming

2G/3G

2G/3G/4G LTE

Exclusivity

•

Exclusive wholesale provider in SNA territory

•

Can sign wholesale agreements with other carriers

•

Exclusive wholesale provider in SNA territory

•

Can sign wholesale agreements with other carriers

Equipment Vendor

Relationships

None

Leverage Sprint’s device and equipment relationships

Incremental

Investment

Agreed to build 3G EVDO network

Agreed

to

build

4G

LTE

network

($150mm

-

$175mm) |

Offers

nTelos

and

Sprint

customers

most

robust

LTE

experience

in

SNA

territory

Solidifies Sprint relationship for nine years and allows for additional

collaboration Extended Agreement –

Beneficial Impact

Contributes significant and recurring wholesale revenues to nTelos

Leverages Sprint’s spectrum holdings and vendor relationships

Provides nTelos with platform for additional wholesale business

opportunities 14

Attracts high-value customers to utilize network

Supports customer value by delivering Savings, Simplicity and Service

|

NTELOS Strategy –

Catalyst for Growth

15

Long term value creation and

cash flow generation

Improve retail margins to create value

Market and revenue share growth

Greater efficiencies

Focus on customer experience

Network

Devices

Differentiated value proposition

1

2

Partnerships

Investments

–

Strategic

Assets

Executing on wholesale / retail strategy

Sprint

Dish

Owned Spectrum

4G LTE Network

Recurring revenue

468,000 subscribers

Expand wholesale relationships

Sprint extension and expansion

Further collaboration with Sprint

DISH

Other opportunities

Improved strategic optionality

for all stakeholders |

Evolution of nTelos

16 |

Financial Overview |

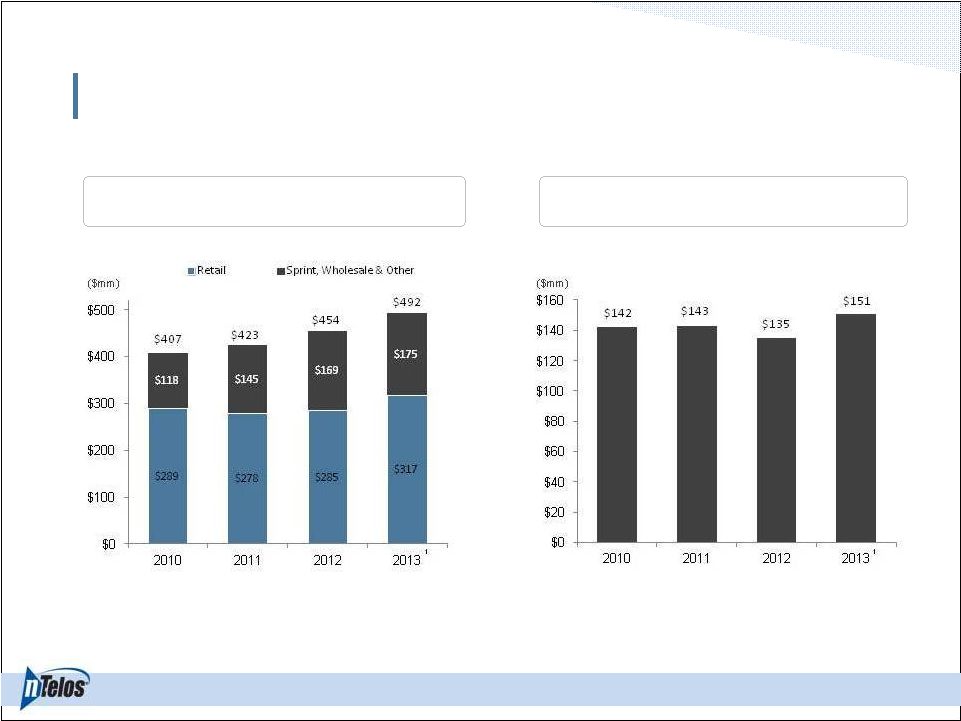

Historical Financial Overview

18

Revenue

Adjusted EBITDA

1

Includes $9.0 million of revenues and $9.6 million of EBITDA related to September

2013 SNA Settlement with Sprint . |

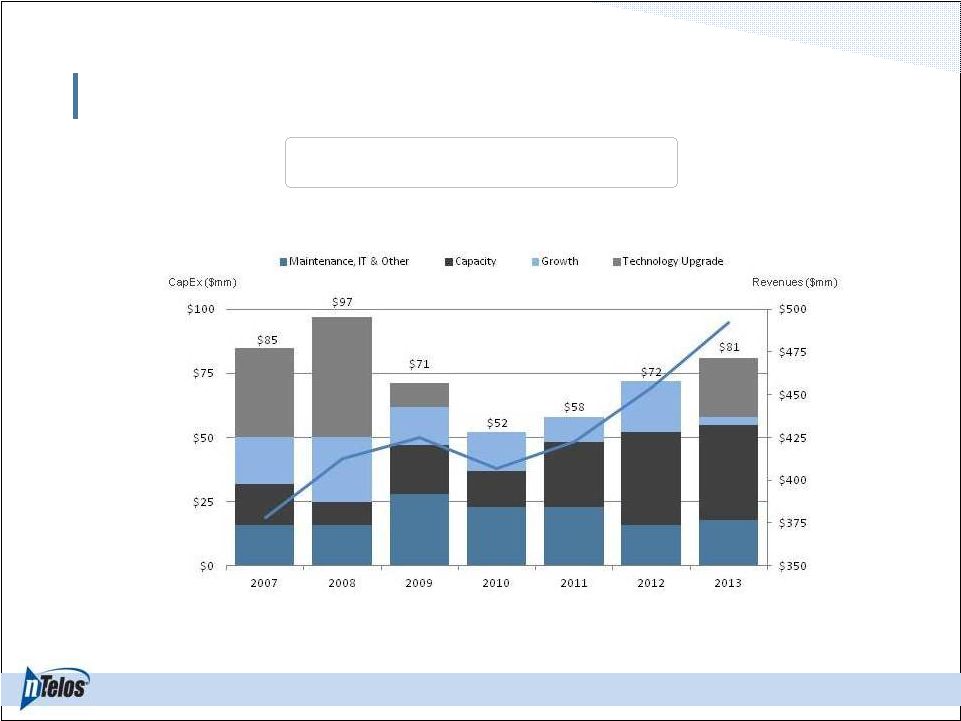

Capital Expenditure

19

CapEx vs. Revenues

Note: Excludes wireline revenue generated and capex incurred prior to October 2011

business separation |

Capitalization Overview

20

($ in millions)

March 31, 2014

Cash, unrestricted

$121.0

Total Debt

$528.9

Net Debt

$407.9

LTM Adjusted EBITDA

$147.4

Secured Term Loan

$528.0

Net Debt Leverage

2.8x |

Business Outlook

21

($ in millions)

2014 (Old)

2014 (New)

2015E

SNA Adjusted Revenue

(1)

~ $160

$150-$154

5% -

10%

Incremental SNA LTE CapEx

(2)

N/A

$25

$50-$60

Adjusted EBITDA

(1)

$140-$150

$128-$135

Flat

Total CapEx

$85-$95

$110-$120

$110-$125

1

SNA Adjusted Revenue and Adjusted EBITDA are adjusted for the impact of

recognizing a portion of the billed SNA contract revenues on a

straight

line

basis.

The

deferred

SNA

contract

revenue

for

2014

and

2015

is

expected

to

be

$8.2

million

and

$11.0

million,

respectively.

2

Remaining $75.0 million to $90.0 million of Incremental SNA LTE CapEx spend in

2016-2017. Note: FY 2014 (New) Adjusted EBITDA and Total CapEx

ranges as of May 22, 2014. Cash (3/31/14)

$121 |

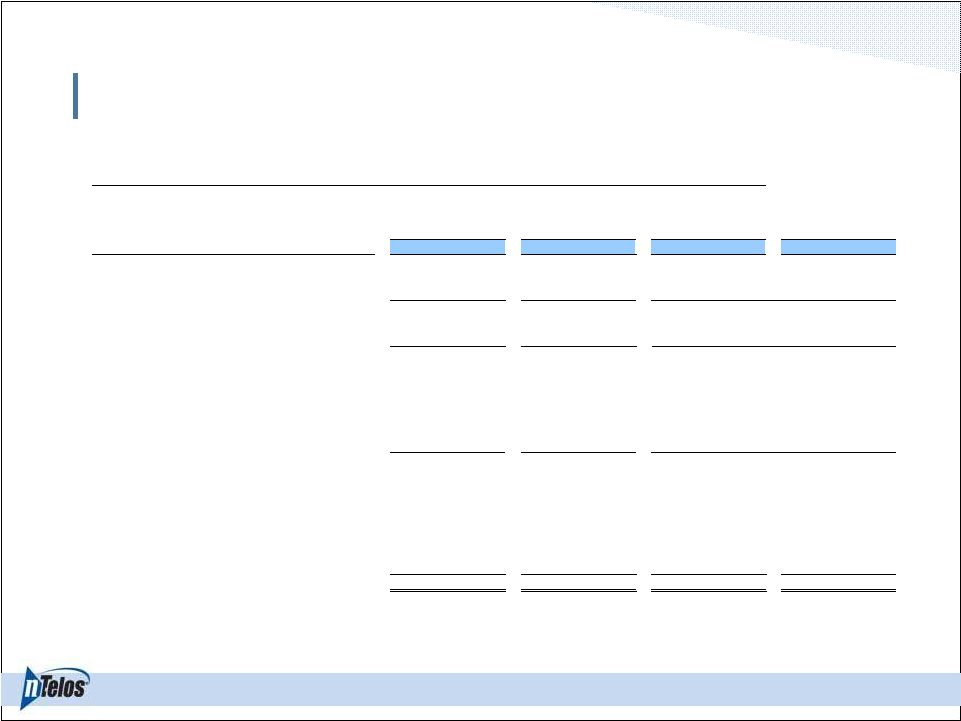

Appendix |

23

Adjusted EBITDA Reconciliation

NTELOS Holdings Corp.

Reconciliation of Net Income Attributable to NTELOS Holdings Corp. to Adjusted EBITDA

Year Ended:

(In thousands)

2013

2012

2011

2010

Net Income Attributable to NTELOS Holdings Corp.

24,678

$

18,387

$

(23,715)

$

44,808

$

Net income attributable to noncontrolling interests

2,061

1,941

(1,769)

(1,417)

Net Income

26,739

20,328

(21,946)

46,225

Discontinued operations, net

-

-

(45,386)

16,882

Income from continuing operations

26,739

20,328

23,440

29,343

Interest expense

29,743

22,944

23,380

24,728

Loss (gain) on derivatives

-

-

264

147

Income taxes

18,544

12,676

16,363

20,251

Corporate financing fees

-

-

1,567

-

Other expense (income), net

810

7,194

1,240

413

Operating income

75,836

63,142

66,254

74,882

Depreciation and amortization

72,944

63,258

63,083

58,016

Gain on sale of intangible assets

(4,442)

-

-

-

Accretion of asset retirement obligations

622

637

658

770

Equity-based compensation

5,553

6,029

6,072

5,270

Acquisition related charges

-

-

-

2,815

Business separation and advisory charges

375

1,660

6,997

352

Adjusted EBITDA

150,888

$

134,726

$

143,064

$

142,105

$

1

Charges for legal and consulting services in connection with the separation of the Company's

wireless and wireline operations in 2011. 2

Charges for advisory fees for secondary offering in 2013.

2

1

1

1 |