Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Armada Hoffler Properties, Inc. | d738348d8k.htm |

REITWeek: NAREIT’s Investor Forum

June 2014

Exhibit 99.1 |

Forward

Looking Statement This presentation contains forward-looking statements

within the meaning of the Private Securities Litigation Reform Act of 1995 (set

forth in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the

Securities Exchange Act of 1934, as amended).

In particular, statements pertaining to our capital resources,

portfolio performance, results of operations and development pipeline contain

forward-looking statements.

Likewise, all of our statements regarding anticipated growth in

our funds from operations, core

funds from operations, adjusted funds from operations, funds available for distribution

and net operating income are forward-looking statements.

You can identify forward-looking statements by the use of forward-looking

terminology such as “believes,”

“expects,”

“may,”

“will,”

“should,”

“seeks,”

“approximately,”

“intends,”

“plans,”

“estimates”

or “anticipates”

or the negative of these words and phrases or similar words or phrases

which are predictions of or indicate future events or trends and

which do not relate solely to historical matters.

You can also identify forward-looking statements by discussions of strategy, plans

or intentions. Forward-looking statements involve numerous risks and

uncertainties and you should not rely on them as predictions of future events.

Forward-looking statements depend on assumptions, data or methods which may be

incorrect or imprecise and the Company may not be able to realize them. The Company

does not guarantee that the transactions and events described will happen as

described (or that they will happen at all). For further

discussion of risk factors and other events that could impact our future results,

please refer to the section entitled “Risk Factors”

in our most recent Annual Report on Form 10-K filed with the Securities and

Exchange Commission (the “SEC), and the documents subsequently filed by us

from time to time with the SEC. 2 |

ARMADA

HOFFLER TODAY A Different Kind of REIT

Solid Dividend Yield Today

Powerful Growth Engine for Tomorrow

>6%

yield

~$150M

development pipeline

every ~2 years

Unique

business

model

$1.4B

assets

developed

35

years

3 |

A

DIFFERENT KIND OF REIT: At a Glance

•

Full-service REIT focused on

institutional grade office, retail

and multifamily properties

–

25 properties

–

focused on Mid-Atlantic region

•

Diversified portfolio

•

NYSE: AHH, market cap ~$319M

as of 5/28/14

•

Enterprise value > $600M

•

Management and prior

owners own ~40%

Current portfolio &

development pipeline

Previous construction/

development projects

Office

Retail

Multifamily

Pipeline

Property

Key

Virginia

North Carolina

Maryland

Washington DC

4 |

A

DIFFERENT KIND OF REIT: Why Our Core Market is Attractive

America’s Top State

for Business –

2011

Virginia is One of the

Best States for Business

Virginia Beach –

2

nd

Most

Business-Friendly City in America

–

June 2013

“

”

“

”

“

”

•

Government named

Best-run City in U.S.

(Wall Street Journal, Jan.

2012)

•

2012 Tourism revenue $1.28

Billion

•

AAA Bond rating maintained

since 1938, longer than any

other state

•

Corporate income tax

of 6% not increased

since 1972

Hampton Roads

Virginia

•

33

rd

largest MSA in the

country

•

Only East Coast port

with 50’

deep and

unobstructed sea lanes

and channels

Virginia Beach

5 |

A

DIFFERENT KIND OF REIT: Hampton Roads Metropolitan Area –

Stable, Growing, Diversified

65% of NOI from operating portfolio falls

within this area

Top 3 largest cities in Virginia within

Hampton Roads MSA

–

Virginia Beach #1, Norfolk #2,

Chesapeake #3

Highly skilled labor pool

–

unemployment rate of 5.3% versus

U.S. national rate of 6.5% (December 2013)

Unique

economic

growth

driver

–

one

of

two

ports

prepared

for

Post-Panamax

ships

–

shipping, warehousing, distribution

–

defense and defense-related industries

6

CHARLOTTESVILLE

RICHMOND

WASHINGTON DC

RALEIGH

DURHAM

BALTIMORE

VIRGINIA BEACH

Hampton

Newport News

Chesapeake

Norfolk |

A

DIFFERENT KIND OF REIT: Unique Integrated Business Model

CONSTRUCTION

DEVELOPMENT

STABLE PORTFOLIO

ADVANTAGE

Delivers Sustainable Low Risk Growth

•

Reduces

development risk

•

Fee income

•

Growth pipeline

•

Wholesale equity

creation

•

High occupancy

•

Consistent cash flow

7 |

A

DIFFERENT

KIND

OF

REIT:

Integrated

Model

–

Delivers

Unique

Advantages

•

Low risk –

50-60% leased prior to breaking ground

•

Assets

developed

at

wholesale

cost

–

creates

equity

•

Focus on assets at “main and main”

at secondary and tertiary Mid-

Atlantic markets

•

Construction Division

-

Projects brand strength, drives opportunity, and mitigates

development risk

-

Fees from integrated construction business are consistently profitable

•

Spread between return on cost and market cap rates of 100-200

basis points

•

Diversified portfolio allows AHH to be opportunistic

8 |

A

DIFFERENT KIND OF REIT: Our Integrated Model in Action –

Virginia Beach Town Center

•

Transformative central business district

development with $500M developed since 2000

exclusively by Armada Hoffler

–

City of Virginia Beach has contributed $150M

–

51% of tenants are new to City of Virginia Beach

–

34% of tenants are new to Hampton Roads

–

Visited by 63% of summer visitors

•

Executed in close collaboration with the

City of Virginia Beach

•

On-going, 17-block, multi-phase development:

–

436,500 SF Office

–

300,000 SF Retail

–

342 Apartments

–

330 Hotel Rooms

•

Additional $83.7 million of Town Center

development included in our identified pipeline

Before

After

9 |

Multiple Growth Drivers

10

Stable Construction Income

that Drives Brand Recognition

and Opportunities

Development Pipeline

Strategic Acquisitions

2

3

4

Stable Portfolio with Organic

Growth Over Time

1 |

1)

STABLE PORTFOLIO Well Balanced Portfolio

Breakdown of NOI Contribution

Three months ended 3/31/14

11

Retail

38%

Multifamily

15%

General

Contracting

11%

Office

36% |

1)

STABLE PORTFOLIO We Attract the Best Tenants

High quality portfolio

*Representative

12

Office Tenants*

Retail Tenants* |

1)

STABLE

PORTFOLIO

High

Occupancies

–

Historical

Outlook

Occupancy as of quarter end

Office Occupancy

Retail Occupancy

Multifamily Occupancy

Portfolios managed for long-term, stable cash flow

13

95.4%

50%

60%

70%

80%

90%

100%

10

11

12

13

14

1Q

93.4%

10

11

12

13

14

1Q

94.2%

10

11

12

13

14

1Q |

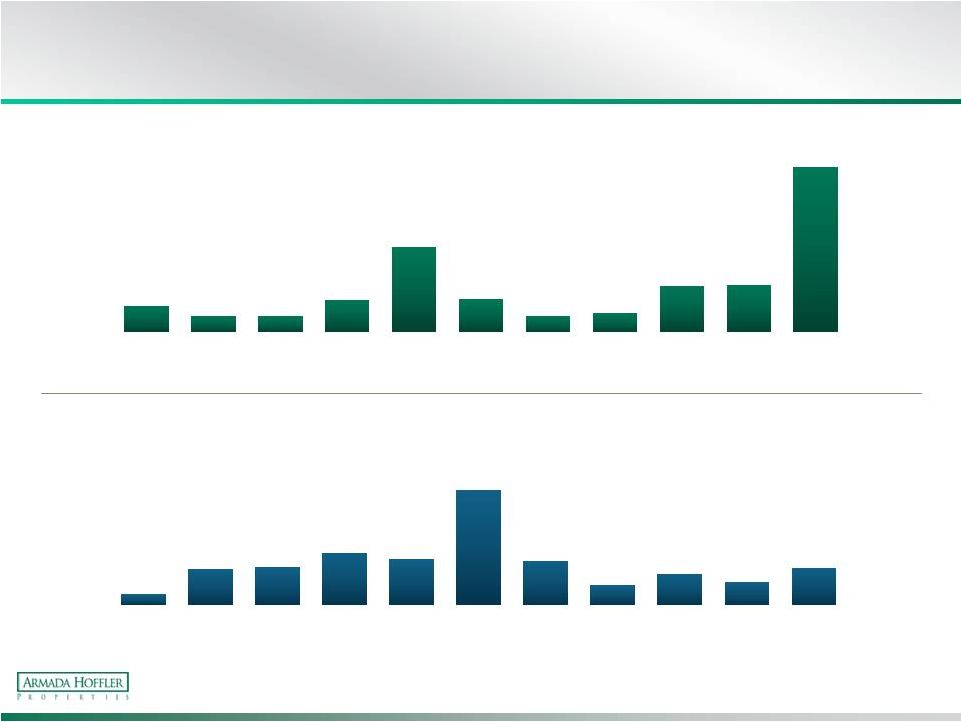

1)

STABLE PORTFOLIO Lease Renewals Actively Managed to Reduce Risk

As of 3/31/14

Year of Lease Expirations

Office Lease Expirations

(% Office Portfolio ABR)

(1)

Year of Lease Expirations

Retail Lease Terms

(% Retail Portfolio ABR)

(1)

14

5.2%

3.2%

3.2%

6.4%

17.0%

6.6%

3.8%

9.2%

9.4%

32.9%

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

There-

after

2.5%

8.0%

8.5%

11.6%

10.2%

25.3%

9.7%

4.4%

6.8%

5.1%

8.1%

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

There-

after

3.1% |

2)

Stable Construction Income that Drives Brand

Recognition and Opportunities

15 |

3)

DEVELOPMENT PIPELINE Extensive Experience Developing >$1.4B of

Properties Building

relationships and

credibility

Examples

16

Smith’s Landing

Blacksburg, VA

Mandarin Oriental Hotel,

Washington DC

Hampton University Proton

Therapy Institute

2900 K Street,

Washington DC

The Swedish Embassy,

Washington DC

Tyre Neck Harris Teeter

Portsmouth, VA

Richmond Tower

Richmond, VA

249 Central Park Retail,

Virginia Beach, VA |

3)

DEVELOPMENT PIPELINE Long Track Record of Successful Public-Private

Partnerships >20

partnerships

Unique competitive advantage

17 |

3)

DEVELOPMENT

PIPELINE

Our

Identified

Pipeline

–

Status

Today

Property

Location

Property

Type

Estimated

Cost

Stabilized Quarter

4525 Main Street

Virginia Beach, VA

Office

$

50,000

1Q 2016

Encore Apartments

Virginia Beach, VA

Multifamily

34,000

1Q 2016

Whetstone Apartments

Durham, NC

Multifamily

28,000

1Q 2016

Sandbridge Commons

Virginia Beach, VA

Retail

13,000

2Q 2016

Brooks Crossing

Newport News, VA

Office

8,000

3Q 2015

Greentree Shopping Center

Chesapeake, VA

Retail

6,000

3Q 2016

Liberty Apartments

Newport News, VA

Multifamily

30,700

3Q 2015

Oceaneering

Chesapeake, VA

Office

26,000

1Q

2015

Commonwealth of Virginia –

Chesapeake

Chesapeake, VA

Office

7,000

1Q

2015

Commonwealth of Virginia –

Virginia Beach

Virginia Beach, VA

Office

3,000

1Q

2015

Lightfoot Marketplace

Williamsburg, VA

Retail

24,000

2Q

2017

$

229,700

$ in thousands

As of 3/31/14

18 |

$ in

thousands Estimated

Cost

Estimated

Stabilized

NOI

Estimated

Return

on Cost

Projected

Value

Spread

The Company’s

Estimated Equity

Creation Excluding

JV Ownership

Identified Pipeline

$

139,000

$

11,400

8.20%

125 bps

$

23,903

Next Generation Pipeline

$

150,000

$

12,400

8.27%

150 bps

$

33,251

Liberty Apartments

$

30,700

(2)

$

2,000

-

Estimated Stabilized

Value / Weighted Average

$

319,700

$

25,800

8.24%

$

57,154

3) DEVELOPMENT PIPELINE

Pipelines Drive Shareholder Value Creation

Equity creation >$55M next 3-4 years

A Closer Look at the Identified and Next Generation Pipelines

(1)

Note 1:

The data reflects the Company’s current estimates, which may change as a result

of various factors. The Company can make no assurances that the estimates

below will actually be realized.

Note 2:

Purchase price.

19 |

4)

ACQUISITION STRATEGY Execute on Strategic and Opportunistic Acquisitions

•

Properties located within or adjacent to our Mid-Atlantic footprint

•

Strong occupancy and stable cash flow

•

Credit-quality tenants

•

Smooth lease rollover with long-term anchor tenants

•

Seller interested in exchanging equity in property for AHH Operating

Partnership Units (OP Units)

•

Value add opportunities

20 |

FINANCIAL HIGHLIGHTS

First Quarter 2014 Highlights

Financial

•

Funds From Operations (“FFO”) of $6.5 million, or

$0.20 per diluted share.

•

Core FFO of $7.1 million, or $0.22 per diluted share.

•

Occupancy increased slightly to 94.5%, compared to

94.4% as of December 31, 2013.

•

Cash dividend of $0.16 per share payable on July 10,

2014 to stockholders of record on July 1, 2014.

•

Core debt to annualized Core EBITDA -

6.9x

•

Weighted average interest rate of 3.6% and average

loan term to maturity of 9.7 years

•

Approximately 46% of debt was fixed as of March 31st

but taking into account LIBOR interest rates caps

approximately 83% of debt was fixed or hedged.

Operational

•

Eleven properties under development including

675,000 square feet of office and retail space and

686 multifamily units.

•

$165.9 million of new construction contract work,

including the Harbor Point project in Baltimore,

Maryland, and $193.3 million of backlog.

•

Anthropologie will be opening a 9,000 square foot

store at the Town Center of Virginia Beach in the

fourth quarter of 2014.

•

In May, the Company announced two new

development projects, both with the Commonwealth

of Virginia, for a total of 47,000 square feet. Both

properties will be 100% leased for 12 years starting

in early 2015.

•

In April, the Company announced Lightfoot

Marketplace, a new shopping center in Williamsburg,

Virginia that will be anchored by Harris Teeter on a

20-year lease.

21 |

FINANCIAL HIGHLIGHTS

Track Record of Financial Results

3Q13

4Q13

1Q14

FFO

$ 5,185

$6,652

$6,475

FFO per share

0.16

0.21

0.20

Core FFO

$ 6,554

$7,098

$7,065

Core FFO per share

0.20

0.22

0.22

AFFO

$ 6,358

$6,000

$6,187

AFFO per share

0.20

0.19

0.19

22

$ in thousands, except per share |

FINANCIAL HIGHLIGHTS

Debt Maturity

23

$ in thousands

As of 3/31/14

Interest Rate Cap Agreements At or Below 1.50%

Effective Date

Maturity Date

Strike Rate

Notional Amount

May 31, 2012

May 29, 2015

1.09%

$9,068

September 1, 2013

March 1, 2016

1.50%

40,000

October 4, 2013

April 1, 2016

1.50%

18,500

March 14, 2014

March 1, 2017

1.25%

50,000

Total Interest Rate Caps at or Below 11.50%

$117,568

Fixed Debt Outstanding

145,729

Total Fixed Interest Rate Debt (including caps)

$263,297

Fixed Interest Rate Debt as a % of Total

83%

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

2014

2015

2016

2017

2018 and

thereafter |

FINANCIAL HIGHLIGHTS

2014 Outlook

24

Current Parameters

Previous Parameters

As of May 13, 2014

As of February 20, 2014

(1Q14 Earnings Release)

(4Q13 Earnings Release)

Total Core FFO

(excluding the impact from non-stabilized projects)

In-line with full-year 2013 FFO

In-line with full-year 2013 FFO

Non-stabilized projects -

negative impact to FFO

(excluded from Core FFO)

Approximately $1.5 million

Approximately $1.5 million

General & administrative expense

Approximately $7.8 million

Approximately $7.8 million

Third party construction company annual segment

gross profit

Approximately $4.0 million

Approximately $4.0 million |

REITWeek: NAREIT’s Investor Forum

June 2014 |