Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Hepion Pharmaceuticals, Inc. | a2220317zex-23_1.htm |

As filed with the Securities and Exchange Commission on June 2, 2014

Registration Statement No. 333-195884

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

CONTRAVIR PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

Delaware |

2834 (Primary Standard Industrial Classification Code Number) |

46-2783806 (I.R.S. Employer Identification Number) |

420 Lexington Avenue, Suite 300

New York, New York 10170

(212) 297-0020

(Address and telephone number of registrant's principal executive offices)

James Sapirstein

Chief Executive Officer

ContraVir Pharmaceuticals, Inc.

420 Lexington Avenue, Suite 300

New York, New York 10170

(212) 297-6149

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

Jeffrey J. Fessler, Esq. Stephen A. Cohen, Esq. Sichenzia Ross Friedman Ference LLP 61 Broadway, 32nd Floor New York, New York 10006 (212) 930-9700 |

Christopher S. Auguste, Esq. Kramer Levin Naftalis & Frankel LLP 1177 Avenue of the Americas New York, New York 10036 (212) 715-9100 |

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

The registrant is an "emerging growth company," as defined in Section 2(a) of the Securities Act. This registration statement complies with the requirements that apply to an issuer that is an emerging growth company.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED JUNE 2, 2014 |

Shares

Common Stock

We are offering shares of our common stock. We expect the public offering price of our shares of common stock will be between $ and $ per share.

Our common stock is presently quoted on the Over-the-Counter Bulletin Board, or OTCBB, under the symbol "CTRV." On May 30, 2014, the last reported sale price of our common stock on the OTCBB was $1.54 per share.

We are an "emerging growth company" as that term is used in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act, and, as such, may elect to comply with certain reduced public company reporting requirements for future filings.

Investing in our common stock involves a high degree of risk. Before investing in our common stock, you should carefully read the discussion of "Risk Factors" beginning on page 10.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| |

Per Share |

Total | |||||

|---|---|---|---|---|---|---|---|

Public offering price |

$ | $ | |||||

Underwriting discount(1) |

$ | $ | |||||

Offering proceeds to us, before expenses |

$ | $ | |||||

- (1)

- The underwriters will receive compensation in addition to the underwriting discount. See "Underwriting" beginning on page 88.

We have granted a 45-day option to the representative of the underwriters to purchase up to additional shares of common stock solely to cover over-allotments, if any.

The underwriters expect to deliver our shares of common stock in the offering on or about , 2014.

TABLE OF CONTENTS

You should rely only on the information provided in this prospectus or amendment thereto. We have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give to you. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of our common stock.

Unless the context requires otherwise, references to "ContraVir," our "company," "we," "us" or "our" refer to ContraVir Pharmaceuticals, Inc., a Delaware corporation and "Synergy" refers to Synergy Pharmaceuticals, Inc., a Delaware corporation, our former majority shareholder.

The following information is a summary of the prospectus and it does not contain all of the information you should consider before investing in our common stock. You should read the entire prospectus carefully, including the "Risk Factors" section and our financial statements and the notes relating to the financial statements, before making an investment decision.

Overview

We were incorporated in Delaware on May 15, 2013 for the purpose of holding certain FV-100 assets of Synergy. We were a majority-owned subsidiary of Synergy until February 18, 2014, the date Synergy completed the spinout of our shares of common stock. We are now an independent publicly traded company and Synergy retains no ownership interest in us.

We are a biopharmaceutical company focused primarily on the development of drugs to treat herpes zoster, or shingles, which is an infection caused by the reactivation of varicella zoster virus, or VZV. The varicella zoster virus is commonly known as chicken pox upon initial exposure to the virus. The virus can lay dormant in nerve endings for many years and if reactivated, causes a extremely painful condition called shingles. We are currently developing a compound called FV-100 for the treatment of shingles. FV-100 is an orally available small molecule, nucleoside analogue. Nucleoside analogs are capable of disrupting replication of the virus. FV-100 is a pro-drug of CF-1743, which means that FV-100 is more readily absorbed when given orally and then broken down to the active portion of the compound, or active moiety, CF-1743 upon entry to the blood stream. FV-100 is the compound under development for the treatment of shingles. Published preclinical studies demonstrate that FV-100 is significantly more potent based on plaque inhibition in VZV infected human embryonic lung cells (HEL cells) than currently marketed compounds acyclovir, valacyclovir, and famciclovir, the FDA-approved drugs used for the treatment of shingles. Preclinical studies further demonstrate that FV-100 has a more rapid onset of antiviral activity, and may fully inhibit the replication of VZV more rapidly than these drugs at significantly lower concentration levels. In addition, pharmacokinetic data from completed Phase 1 and 2 clinical trials suggest that FV-100 has the potential to demonstrate antiviral activity when dosed orally once-a-day at significantly lower blood levels than valacyclovir, acyclovir, and famciclovir (ICAR, 2008, abst. 137; ICAAC, 2008, abst. A-951; ICAR, 2009, abst. 105; ICAR, 2009, abst. 106).

FV-100 was previously in development by Inhibitex, Inc., or Inhibitex. In January 2012, Bristol-Myers Squibb Company, or BMS acquired Inhibitex. In August 2012, Synergy acquired the FV-100 assets from BMS. The FV-100 assets are licensed from University College Cardiff Consultants Limited ("Cardiff") pursuant to the terms of that certain Patent and Technology License Agreement, dated as of February 2, 2005, between Cardiff and Contravir Research Incorporated, an entity with no prior relationship with the Company, as amended March 27, 2007. After acquiring the FV-100 assets from BMS, Synergy did not engage in any clinical study of FV-100 or materially advance the development of FV-100.

The Phase 2 clinical trial for FV-100 was completed by Inhibitex in December 2010 (ICAAC, 2011, abst. G1-765). This trial represented the first clinical trial of FV-100 in shingles patients, and was a well-controlled, double blind study comparing two different dosing arms of FV-100 to an active control (valacyclovir). A total of 350 patients, aged 50 years and older, were enrolled in one of three treatment arms: 200 mg FV-100 administered once daily; 400 mg FV-100 administered once daily; and 1,000 mg valacyclovir administered three times per day.

In addition to further evaluating its safety and tolerability, the main objectives of the trial were to evaluate the potential therapeutic benefit of FV-100 in reducing the severity and duration of shingles-related pain, the incidence of post-herpetic neuralgia (burning pain that follows healing of the shingles rash), or PHN, and the time to lesion healing. The primary endpoint for the FV-100 study was developed by Inhibitex and was defined as a 25% reduction in the severity and duration of shingles-related pain during the first 30 days as compared to valacyclovir. The trial missed its primary endpoint, as the results

1

from the study showed a lack of statistical significance. There were, however, numerically favorable treatment differences compared to valacyclovir 1000 mg TID, particularly in those patients that received 400 mg FV-100, relative to valacyclovir patients, with respect to the primary endpoint: FV100 200 mg = 114.49 (p = 0.88); FV-100 400 mg = 110.31 (p = 0.55) vs. valacyclovir = 117.96. There were also favorable, non-statistically significant treatment differences observed for key secondary pain endpoints, including the reduction in the severity and duration of shingles-associated pain over 90 days (FV-100 400 mg showing a 14% relative reduction as compared to valacyclovir) and the incidence of PHN (FV-100 400 mg showing a 39% relative reduction as compared to valacyclovir). The secondary endpoints were not, however, powered to demonstrate statistically significant treatment differences between the arms. FV-100 was generally well tolerated at both dose levels, and demonstrated a similar adverse event profile as compared to valacyclovir.

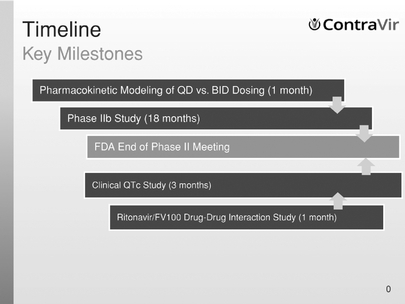

We are currently reviewing the clinical data from the Phase 2 trial and performing post hoc analyses, conducting additional market research, including unmet medical need, reimbursement, pricing, and competitive analyses, etc. We are also evaluating a number of clinical, regulatory and commercial pathways for the potential future development of FV-100. Based upon the analyses of the completed Phase 2 study coupled with the additional market research, we are developing a comprehensive clinical strategy for future development of FV-100 which is being implemented during fiscal 2014. Inhibitex filed for an Investigational New Drug application or IND (IND 102,011) on March 19, 2008, which was approved by the FDA on April 20, 2008. This IND was transferred from Inhibitex to its new sponsor, Synergy, on August 27, 2012 and subsequently transferred from Synergy to us in April 2014. As a result of this transfer, we will be able to run all clinical trials required to support FV-100 for the use in the treatment of shingles. Our intention is to conduct another phase 2 study which may take approximately 18-24 months to enroll. Following data analysis from that newly completed phase 2 study we intend on seeking a meeting with FDA to discuss the direction and scope of the subsequent phase 3 program.

From inception (May 15, 2013) through March 31, 2014, we generated no revenue.

Our Strengths – Advantages of FV-100 compared to approved drugs

We believe that we possess a number of competitive advantages that distinguish us from our competitors, including:

- •

- Potential effectiveness in patients who are present with shingles after 72 hours from the onset of an outbreak due

to our product working faster than competitive products. Note: current marketed therapies require initiation of treatment within 72 hours of onset of the shingles rash;

- •

- Potential to reduce pain to a greater extent over the first 90 days following initiation of therapy compared to the

competition;

- •

- Potential to reduce the incidence of post-herpetic neuralgia, or PHN;

- •

- A reduction in the number of doses per day to 1-2 as compared to 3-5 with the competition; and

- •

- Greater potency at eradicating the varicella zoster virus than the competition.

2

Our Strategy

Design and conduct clinical trials that establish the superiority of FV-100 over the existing standard of care from other existing drugs like valacyclovir.

Market Opportunity for the Treatment of shingles

VZV, a DNA virus and a member of the herpes virus group, is the virus that causes both chickenpox and herpes zoster, or shingles. Chickenpox, the initial infection caused by VZV in an individual, generally occurs during childhood and it is caused by exposure to another individual with an active infection. After the chickenpox infection subsides, VZV remains latent in the individual's nerves including the dorsal root and cranial nerve ganglia, and can re-emerge later in life. Therefore, shingles is typically not transmitted from one individual to the next, and only those individuals who have had chickenpox are generally at risk for shingles.

Although shingles can occur in any individual with a prior VZV infection, its incidence varies with its key risk factors, which are advanced age, immune system status and being female. Shingles is largely a disease of the aged or aging, with over 50% of all cases occurring in individuals over the age of 60, and approximately 80% occurring in individuals over the age of 40. A study in 2007 based upon data from 2000 implied that there were approximately 1 million new shingles cases that year. Due to the aging of the population in many industrialized countries, as well as the increasing use of immunosuppressive agents in transplant patients, patients with autoimmune diseases such as rheumatoid arthritis and the increased numbers of immunosuppressed patients from cancer therapy, the incidence of shingles has increased and is expected to continue to increase. A recent study from the Centers for Disease Control investigating medical claims data from MarketScan® databases from 1993-2006 indicated that the crude incidence of shingles cases increased 259% over that period of time. Furthermore, a study conducted by the Mayo Clinic suggests that the recurrence rate for shingles is approximately 6.2%, which reflects a much higher rate than prior studies, which assessed a shorter follow-up period. It is estimated that approximately 20-30% of all persons in the U.S. will suffer from shingles at some point during their lifetime.

The symptoms associated with shingles generally include localized lesions (rash and blisters) and pain. In many cases the patient may notice localized pain as a prodromal symptom or the time period which the disease process has begun but is not manifest with any clinical symptoms, prior to the appearance of any lesions; however, the first recognizable symptom of shingles is generally lesions that will continue to form for a week or two. Such skin lesions generally are found on one half of the body and follow the path of

3

nerves that emanate from the spinal cord around the torso (thoracic); however, the infection is also commonly found on the face, neck, lower back and in certain rare cases, systemically. Within several weeks, the lesions in the infected areas will typically begin to heal, and these dermatological symptoms generally will resolve within a month or less after the appearance of the first lesion. In rare instances, lesions may never appear, but localized pain will be present.

The pain associated with an episode of shingles is attributed to both the damage caused to the affected nerves by the replication of VZV and the inflammatory response associated with the infection. Pain symptoms are commonly described as a burning sensation, with bouts of stabbing and shooting pain, often set off by contact with the infected area. The majority of shingles patients experience such pain for several weeks in connection with their active infection, referred to as acute pain. For many patients, shingles-associated pain does not resolve when the lesions heal and the inflammation subsides, but, rather, continues for months, or possibly years. Persistent shingles-associated pain that lasts more than three to four weeks is referred to as sub-acute pain or neuralgia. Shingles-associated pain that persists more than three months is generally referred to as PHN, which is the most common and clinically relevant complication of shingles. Approximately 15-20% of all shingles patients experience PHN, although the incidence of PHN is more prevalent in patients over 50 years of age. Previous studies have established that additional risk factors for PHN include greater acute pain intensity during the initial 4 weeks, severity of the dermatological symptoms or lesions, and the presence and greater severity of localized pain prior to the appearance of the lesions or rash.

Valacyclovir, acyclovir and famciclovir are oral antivirals currently indicated and approved by the FDA, and regulatory agencies in many other countries, for the treatment shingles. These drugs, available as generics, are referred to as "pan-herpetic" drugs, as they are used to treat infections caused by various herpes viruses, including herpes simplex 1 and 2, and VZV. Unlike those drugs, FV-100 only has antiviral activity against VZV, and not the other herpes viruses. Based upon an analysis by data compiled by IMS Health, Inc. ("IMS") on our behalf, and a recent utilization study of the use of Valtrex ® from 1994-2009 conducted by the FDA as well as other market research we have independently conducted, we estimate that 15-30% of the nearly 17 million retail prescriptions written for valacyclovir, acyclovir and famciclovir combined in 2009 were for the treatment of herpes zoster.

Risks Associated with Our Business

An investment in our common stock involves risks associated with our business. The following list of risk factors is not exhaustive. Please read carefully the risks relating to these and other matters described under "Risk Factors" beginning on page 10 and "Cautionary Statement Concerning Forward-Looking Statements" on page 44.

- •

- We will require substantial additional funding beyond the offering to which this prospectus relates to complete the

development and commercialization of FV-100 and/or any other potential product candidates, and such funding may not be available on acceptable terms or at all.

- •

- We have incurred losses since inception and anticipate that we will incur continued losses for the foreseeable future.

- •

- Our product candidate is in the early stages of development and its commercial viability remains subject to the successful

outcome of current and future preclinical studies, clinical trials, regulatory approvals and the risks generally inherent in the development of pharmaceutical product candidates. If we are unable to

successfully advance or develop our product candidate, our business will be materially harmed.

- •

- If the results of preclinical studies or clinical trials for our product candidate, including those that are subject to existing or future license or collaboration agreements, are unfavorable or delayed, we

4

- •

- If third party vendors upon whom we intend to rely on to conduct our preclinical studies or clinical trials do not perform

or fail to comply with strict regulations, these studies or trials of our product candidate may be delayed, terminated, or fail, or we could incur significant additional expenses, which could

materially harm our business.

- •

- We, and our collaborators, must comply with extensive government regulations in order to advance our product candidate

through the development process and ultimately obtain and maintain marketing approval for our products in the U.S. and abroad.

- •

- Delays in clinical testing could result in increased costs to us and delay our ability to generate revenue.

- •

- The regulatory approval processes of the FDA and comparable foreign authorities are lengthy, time consuming and inherently

unpredictable, and if we are ultimately unable to obtain regulatory approval for our product candidate, our business will be substantially harmed.

- •

- If our product candidate is unable to compete effectively with marketed drugs targeting similar indications as our product

candidate, our commercial opportunity will be reduced or eliminated.

- •

- If the manufacturers upon whom we rely fail to produce FV-100, in the volumes that we require on a timely basis, or fail

to comply with stringent regulations applicable to pharmaceutical drug manufacturers, we may face delays in the development and commercialization of our product candidate.

- •

- If government and third-party payers fail to provide adequate reimbursement or coverage for our products or those we

develop through collaborations, our revenues and potential for profitability will be harmed.

- •

- If a third party claims we are infringing on its intellectual property rights, we could incur significant expenses, or be

prevented from further developing or commercializing our product candidate.

- •

- Even if our product candidate receives regulatory approval, it may still face future development and regulatory

difficulties.

- •

- Healthcare reform measures could hinder or prevent our product candidate's commercial success.

could be delayed or precluded from the further development or commercialization of our product candidate, which could materially harm our business.

Implications of Being an Emerging Growth Company

We qualify as an "emerging growth company" as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

- •

- requirement to provide only two years of audited financial statements in addition to any required unaudited interim

financial statements with correspondingly reduced "Management's Discussion and Analysis of Financial Condition and Results of Operations" disclosure;

- •

- reduced disclosure about our executive compensation arrangements;

- •

- no non-binding advisory votes on executive compensation or golden parachute arrangements; and

- •

- exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting.

We have irrevocably elected not to use the extended transition period for complying with new or revised accounting standards under Section 102(b)(1) of the JOBS Act, and, therefore, we will be subject

5

to the same new or revised accounting standards as other public companies that are not emerging growth companies.

We may take advantage of these provisions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company on the date that is the earliest of (i) the last day of the fiscal year in which we have total annual gross revenues of $1 billion or more; (ii) the last day of our fiscal year following the fifth anniversary of the date of the distribution; (iii) the date on which we have issued more than $1 billion in nonconvertible debt during the previous three years; or (iv) the date on which we are deemed to be a large accelerated filer under the rules of the Securities and Exchange Commission.

To the extent that we continue to qualify as a "smaller reporting company," as such term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, after we cease to qualify as an emerging growth company, certain of the exemptions available to us as an emerging growth company may continue to be available to us as a smaller reporting company, including: (1) not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes Oxley Act; (2) scaled executive compensation disclosures; and (3) the requirement to provide only two years of audited financial statements, instead of three years.

6

We incorporated under the laws of the State of Delaware on May 15, 2013. Our fiscal year end is June 30. Our principal executive offices are located at 420 Lexington Avenue, Suite 300, New York, New York 10170. Our telephone number is (212) 297-6149. Our website address is www.contravir.com. The information contained on, or that can be accessed through, our website is not a part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

7

Common stock offered by us |

shares | |

Common stock to be outstanding immediately after this offering |

shares |

|

Over-allotment option |

The underwriters have an option for a period of 45 days to purchase up to additional shares of our common stock to cover over-allotments, if any. |

|

Use of proceeds |

We estimate that the net proceeds from this offering will be approximately $ million, or approximately $ million if the underwriters exercise their over-allotment option in full, at an assumed public offering price of $ per share, the midpoint of the range set forth on the cover page of this prospectus, after deducting the underwriting discount and estimated offering expenses payable by us. We intend to use the net proceeds from this offering as follows: to fund our planned Phase 2 clinical trials of FV-100 and general corporate purposes, including working capital. See "Use of Proceeds" for a more complete description of the intended use of proceeds from this offering. |

|

Risk Factors |

You should read the "Risk Factors" section starting on page 10 for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. |

|

OTCBB Trading Symbol |

CTRV |

The number of shares of our common stock outstanding after this offering excludes:

- •

- 2,142,270 shares of our common stock issuable upon exercise of outstanding options to purchase 2,142,270 shares of common

stock under our 2013 Equity Incentive Plan, or Plan, at a weighted average exercise price of $1.58 per share;

- •

- 4,742,648 shares of common stock issuable upon exercise of outstanding warrants at a weighted average exercise price of

$0.37 per share; and

- •

- shares of our common stock underlying the warrants to be issued to the representative of the underwriters in connection with this offering.

Unless otherwise indicated, all information in this prospectus assumes:

- •

- no exercise of the representative's warrants described above; and

- •

- no exercise by the underwriters of their option to purchase up to additional shares of our common stock to cover over-allotments, if any.

8

You should read the following summary financial data together with our financial statements and the related notes included elsewhere in this prospectus and the "Selected Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" sections of this prospectus. The selected statements of operations data for the period from May 15, 2013 ("inception") to March 31, 2014, the nine months ended March 31, 2014, and the selected balance sheet data as of March 31, 2014 are derived from our unaudited financial statements and related notes included elsewhere in this prospectus. We have derived the statements of operations data for the period from May 15, 2013 (inception) to June 30, 2013, and the balance sheet data as of June 30, 2013, from our audited financial statements included elsewhere in this prospectus. Our financial status creates substantial doubt about our ability to continue as a going concern. Our historical results for any prior period are not necessarily indicative of results to be expected in any future period.

| |

Period from May 15, 2013 (inception) to June 30, 2013 |

Nine Months Ended March 31, 2014 |

Period from May 15, 2013 (inception) to March 31, 2014 |

|||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

|

(unaudited) |

(unaudited) |

|||||||

Statement of Operations Data: |

||||||||||

Revenues |

$ | — | $ | — | $ | — | ||||

Costs and Expenses |

||||||||||

Research and development |

17,740 | 95,353 | 113,094 | |||||||

General and administrative |

122,427 | 707,243 | 829,670 | |||||||

| | | | | | | | | | | |

Loss from Operations |

(140,167 | ) | (802,596 | ) | (942,764 | ) | ||||

| | | | | | | | | | | |

Interest expense |

328 | 12,946 | 13,273 | |||||||

Change in fair value of derivative instruments—warrants |

— | (8,846,434 | ) | (8,846,434 | ) | |||||

| | | | | | | | | | | |

Net loss |

$ | (140,495 | ) | $ | (9,661,976 | ) | $ | (9,802,471 | ) | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Net loss per share: basic and diluted |

$ | (0.02 | ) | $ | (0.89 | ) | ||||

| | | | | | | | | | | |

| | | | | | | | | | | |

Weighted-average number of shares used in per common share calculations: |

||||||||||

Basic and diluted |

9,000,000 | 10,904,873 | ||||||||

| |

As of March 31, 2014 | ||||||

|---|---|---|---|---|---|---|---|

| |

Actual | Pro Forma As Adjusted(1) |

|||||

Balance Sheet Data: |

|||||||

Cash(2) |

$ | 2,510,196 | $ | ||||

Total assets(2) |

2,643,495 | ||||||

Total liabilities |

9,985,855 | ||||||

Total stockholder's equity (deficiency)(2) |

(7,342,360 | ) | |||||

Working capital(2) |

2,367,784 | ||||||

- (1)

- Our

pro forma as adjusted balance sheet data as of March 31, 2014 gives effect to issuance and sale of the number of shares offered by us, as set

forth on the cover page of this prospectus, assuming a public offering price of $ per share (the midpoint of our expected offering range on the cover of this prospectus), after

deducting the estimated underwriting discount and our estimated offering expenses.

- (2)

- A $1.00 increase or decrease in the assumed initial public offering price of $ per share (the midpoint of our expected offering range on the cover of this prospectus) would increase (decrease) the amounts representing cash, working capital (deficiency), total assets and total stockholder's equity by $ .

9

An investment in our common stock involves a high degree of risk. Before making an investment decision, you should give careful consideration to the following risk factors, in addition to the other information included in this prospectus, including our financial statements and related notes, before deciding whether to invest in shares of our common stock. The occurrence of any of the adverse developments described in the following risk factors could materially and adversely harm our business, financial condition, results of operations or prospects. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business

We have incurred losses since inception, anticipate that we will incur continued losses for the foreseeable future and our independent registered public accounting firm's report, contained herein, includes an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern, indicating the possibility that we may not be able to operate in the future.

As of June 30, 2013 and March 31, 2014, we had an accumulated deficit of $140,495 and $9,802,471, respectively. We expect to incur significant and increasing operating losses for the next several years as we expand our research and development, continue our clinical trials of FV-100, acquire or license technologies, advance other product candidates into clinical development, complete clinical trials, seek regulatory approval and, if we receive FDA approval, commercialize our products. Primarily as a result of our losses and limited cash balances, our independent registered public accounting firm has included in its report an explanatory paragraph expressing substantial doubt about our ability to continue as a going concern. Our ability to continue as a going concern is contingent upon, among other factors, the sale of the shares of our common stock or obtaining alternate financing. We cannot provide any assurance that we will be able to raise additional capital.

If we are unable to secure additional capital, we may be required to curtail our research and development initiatives and take additional measures to reduce costs in order to conserve our cash in amounts sufficient to sustain operations and meet our obligations. These measures could cause significant delays in our clinical and regulatory efforts, which is critical to the realization of our business plan. The accompanying financial statements do not include any adjustments that may be necessary should we be unable to continue as a going concern. It is not possible for us to predict at this time the potential success of our business. The revenue and income potential of our proposed business and operations are currently unknown. If we cannot continue as a viable entity, you may lose some or all of your investment in our company.

We will require substantial additional funding which may not be available to us on acceptable terms, or at all. If we fail to raise the necessary additional capital, we may be unable to complete the development and commercialization of our product candidate, or continue our development programs.

We expect to significantly increase our spending to advance the preclinical and clinical development of our product candidate and launch and commercialize any product candidate for which we receive regulatory approval, including building our own commercial organizations to address certain markets. We will require additional capital for the further development and commercialization of our product candidate, as well as to fund our other operating expenses and capital expenditures.

We cannot be certain that additional funding will be available on acceptable terms, or at all. If we are unable to raise additional capital in sufficient amounts or on terms acceptable to us we may have to significantly delay, scale back or discontinue the development or commercialization of our product candidate. We may also seek collaborators for one or more of our current or future product candidates at an earlier stage than otherwise would be desirable or on terms that are less favorable than might otherwise be available. Any of these events could significantly harm our business, financial condition and prospects.

10

Our future capital requirements will depend on many factors, including:

- •

- the progress of the development of FV-100;

- •

- the number of product candidates we pursue;

- •

- the time and costs involved in obtaining regulatory approvals;

- •

- the costs involved in filing and prosecuting patent applications and enforcing or defending patent claims;

- •

- our plans to establish sales, marketing and/or manufacturing capabilities;

- •

- the effect of competing technological and market developments;

- •

- the terms and timing of any collaborative, licensing and other arrangements that we may establish;

- •

- general market conditions for offerings from biopharmaceutical companies;

- •

- our ability to establish, enforce and maintain selected strategic alliances and activities required for product

commercialization; and

- •

- our revenues, if any, from successful development and commercialization of our product candidate.

In order to carry out our business plan and implement our strategy, we anticipate that we will need to obtain additional financing from time to time and may choose to raise additional funds through strategic collaborations, licensing arrangements, public or private equity or debt financing, bank lines of credit, asset sales, government grants, or other arrangements. We cannot be sure that any additional funding, if needed, will be available on terms favorable to us or at all. Furthermore, any additional equity or equity-related financing may be dilutive to our stockholders, and debt or equity financing, if available, may subject us to restrictive covenants and significant interest costs. If we obtain funding through a strategic collaboration or licensing arrangement, we may be required to relinquish our rights to certain of our product candidate or marketing territories. Our inability to raise capital when needed would harm our business, financial condition and results of operations, and could cause our stock price to decline or require that we wind down our operations altogether.

Our prospects are largely dependent on the success of FV-100, which was the subject of a Phase II clinical trial that failed to meet its primary endpoints. While we seek to determine the implications, if any, of the Phase II results on our FV-100 product candidate and consider other potential strategic pathways, there can be no assurance we will be able to successfully advance or develop our FV-100 product candidate and if we are unable to further develop or obtain regulatory approval, our business will be materially harmed.

In December 2010, Inhibitex, Inc., a previous owner of the FV-100 assets, announced that in a pivotal Phase II clinical trial of FV-100, an oral antiviral compound being developed to treat herpes zoster, more commonly referred to as shingles, failed to meet its primary endpoint. Since we received the FV-100 assets from Synergy, we have not engaged in any clinical study of FV-100 or materially advanced the development of FV-100. We are currently conducting various analyses of our preclinical and clinical data related to FV-100, as well as analyzing the various lots of clinical trial material used in the Phase II trials in an effort to determine whether the results of the Phase II trial were a consequence of one or more factors, including the potency and consistency of the clinical trial material, the change in the dosing schedule, and selection of the patient population studied and the appropriateness of the primary efficacy endpoint used in the clinical trial to determine the effectiveness of the treatments. If we are unable to successfully advance or develop our FV-100 product candidate, it will have a material adverse effect on our business.

11

Our product candidate is in the early stages of development and its commercial viability remains subject to the successful outcome of current and future preclinical studies, clinical trials, regulatory approvals and the risks generally inherent in the development of a pharmaceutical product candidate. If we are unable to successfully advance or develop our product candidate, our business will be materially harmed.

In the near-term, failure to successfully advance the development of FV-100 may have a material adverse effect on us. To date, we have not successfully developed or commercially marketed, distributed or sold any product candidate. The success of our business depends primarily upon our ability to successfully advance the development of FV-100 through preclinical studies and clinical trials, have these product candidate approved for sale by the FDA or regulatory authorities in other countries, and ultimately have this product candidate successfully commercialized by us or a strategic collaborator. We cannot assure you that the results of our ongoing preclinical studies or clinical trials will support or justify the continued development of our product candidate, or that we will receive approval from the FDA, or similar regulatory authorities in other countries, to advance the development of our product candidate.

Our product candidate must satisfy rigorous regulatory standards of safety and efficacy before we can advance or complete their clinical development or they can be approved for sale. To satisfy these standards, we must engage in expensive and lengthy preclinical studies and clinical trials, develop acceptable manufacturing processes, and obtain regulatory approval of our product candidate. Despite these efforts, our product candidate may not:

- •

- offer therapeutic or other medical benefits over existing drugs or other product candidates in development to treat the

same patient population;

- •

- be proven to be safe and effective in current and future preclinical studies or clinical trials;

- •

- have the desired effects;

- •

- be free from undesirable or unexpected effects;

- •

- meet applicable regulatory standards;

- •

- be capable of being formulated and manufactured in commercially suitable quantities and at an acceptable cost;

or

- •

- be successfully commercialized by us or by collaborators.

Even if we demonstrate favorable results in preclinical studies and early-stage clinical trials, we cannot assure you that the results of late-stage clinical trials will be favorable enough to support the continued development of our product candidate. A number of companies in the pharmaceutical and biopharmaceutical industries have experienced significant delays, setbacks and failures in all stages of development, including late-stage clinical trials, even after achieving promising results in preclinical testing or early-stage clinical trials. Accordingly, results from completed preclinical studies and early-stage clinical trials of our product candidate may not be predictive of the results we may obtain in later-stage trials. Furthermore, even if the data collected from preclinical studies and clinical trials involving our product candidate demonstrates a satisfactory safety and efficacy profile, such results may not be sufficient to support the submission of a New Drug Application, or NDA or a biologics license application, or BLA to obtain regulatory approval from the FDA in the U.S., or other similar regulatory agencies in other jurisdictions, which is required to market and sell the product.

Our product candidate will require significant additional research and development efforts, the commitment of substantial financial resources, and regulatory approvals prior to advancing into further clinical development or being commercialized by us or collaborators. We cannot assure you that our product candidate will successfully progress through the drug development process or will result in a commercially viable product. We do not expect our product candidate to be commercialized by us or collaborators for at least several years.

12

Our product candidate may exhibit undesirable side effects when used alone or in combination with other approved pharmaceutical products or investigational new drugs, which may delay or preclude its further development or regulatory approval, or limit its use if approved.

Throughout the drug development process, we must continually demonstrate the safety and tolerability of our product candidate to obtain regulatory approval to further advance their clinical development or to market them. Even if our product candidate demonstrates biologic activity and clinical efficacy, any unacceptable adverse side effects or toxicities, when administered alone or in the presence of other pharmaceutical products, which can arise at any stage of development, may outweigh its potential benefit. In preclinical studies and clinical trials we have conducted to date, our product candidate has demonstrated an acceptable safety profile, although these studies and trials have involved a small number of subjects or patients over a limited period of time. We may observe adverse or significant adverse events or drug-drug interactions in future preclinical studies or clinical trials of this product candidate, which could result in the delay or termination of its development, prevent regulatory approval, or limit its market acceptance if it is ultimately approved.

If the actual or perceived therapeutic benefits of FV-100 are not sufficiently different from existing generic drugs currently used to treat shingles or reduce or prevent shingles-associated pain and PHN, we may terminate the development of FV-100 at any time, or our ability to generate significant revenue from the sale of FV-100, if approved, may be limited and our potential profitability could be harmed.

Valacyclovir, famciclovir and acyclovir are existing generic drugs currently marketed to treat shingles patients. Generic drugs are compounds that have no remaining patent protection, and generally have an average selling price substantially lower than drugs that are protected by patents and intellectual property rights. Unless a patented drug can differentiate itself from generic drugs treating the same condition or disease in a clinically meaningful manner, the existence of generic competition in any indication may impose significant pricing pressure on patented drugs. Accordingly, if at any time we believe that FV-100 may not provide meaningful therapeutic benefits, perceived or real, over these existing generic drugs, we may delay or terminate its future development. We cannot provide any assurance that later-stage clinical trials of FV-100 will demonstrate any meaningful therapeutic benefits over existing generic drugs sufficient to justify its continued development. Further, if we successfully develop FV-100 and it is approved for sale, we cannot assure you that any real or perceived therapeutic benefits of FV-100 over generic drugs will result in it being, accepted for sale by insurance company formularies, prescribed by physicians or commanding a price higher than the existing generic drugs.

If the results of preclinical studies or clinical trials for our product candidate, including those that are subject to existing or future license or collaboration agreements, are unfavorable or delayed, we could be delayed or precluded from the further development or commercialization of our product candidate, which could materially harm our business.

In order to further advance the development of, and ultimately receive regulatory approval to sell, our product candidate, we must conduct extensive preclinical studies and clinical trials to demonstrate their safety and efficacy to the satisfaction of the FDA or similar regulatory authorities in other countries, as the case may be. Preclinical studies and clinical trials are expensive, complex, can take many years to complete, and have highly uncertain outcomes. Delays, setbacks, or failures can occur at any time, or in any phase of preclinical or clinical testing, and can result from concerns about safety or toxicity, a lack of demonstrated efficacy or superior efficacy over other similar products that have been approved for sale or are in more advanced stages of development, poor study or trial design, and issues related to the formulation or manufacturing process of the materials used to conduct the trials. The results of prior preclinical studies or clinical trials are not necessarily predictive of the results we may observe in later stage clinical trials. In many cases, product candidate in clinical development may fail to show desired safety and efficacy

13

characteristics despite having favorably demonstrated such characteristics in preclinical studies or earlier stage clinical trials.

In addition, we may experience numerous unforeseen events during, or as a result of, preclinical studies and the clinical trial process, which could delay or impede our ability to advance the development of, receive regulatory approval for, or commercialize our product candidate, including, but not limited to:

- •

- communications with the FDA, or similar regulatory authorities in different countries, regarding the scope or design of a

trial or trials;

- •

- regulatory authorities (including an Institutional Review Board) or IRBs not authorizing us to commence or conduct a

clinical trial at a prospective trial site;

- •

- enrollment in our clinical trials being delayed, or proceeding at a slower pace than we expected, because we have

difficulty recruiting patients or participants dropping out of our clinical trials at a higher rate than we anticipated;

- •

- our third party contractors, upon whom we rely for conducting preclinical studies, clinical trials and manufacturing of

our trial materials, may fail to comply with regulatory requirements or meet their contractual obligations to us in a timely manner;

- •

- having to suspend or ultimately terminate our clinical trials if participants are being exposed to unacceptable health or

safety risks;

- •

- IRBs or regulators requiring that we hold, suspend or terminate our preclinical studies and clinical trials for various

reasons, including non-compliance with regulatory requirements; and

- •

- the supply or quality of drug material necessary to conduct our preclinical studies or clinical trials being insufficient, inadequate or unavailable.

Even if the data collected from preclinical studies or clinical trials involving our product candidate demonstrate a satisfactory safety and efficacy profile, such results may not be sufficient to support the submission of a NDA or BLA to obtain regulatory approval from the FDA in the U.S., or other similar foreign regulatory authorities in foreign jurisdictions, which is required to market and sell the product.

If third party vendors upon whom we intend to rely on to conduct our preclinical studies or clinical trials do not perform or fail to comply with strict regulations, these studies or trials of our product candidate may be delayed, terminated, or fail, or we could incur significant additional expenses, which could materially harm our business.

We have limited resources dedicated to designing, conducting and managing preclinical studies and clinical trials. We intend to rely on third parties, including clinical research organizations, consultants and principal investigators, to assist us in designing, managing, monitoring and conducting our preclinical studies and clinical trials. As of the date hereof, we have not entered into any contracts with third party vendors for any studies to be conducted. We intend to rely on these vendors and individuals to perform many facets of the drug development process, including certain preclinical studies, the recruitment of sites and patients for participation in our clinical trials, maintenance of good relations with the clinical sites, and ensuring that these sites are conducting our trials in compliance with the trial protocol and applicable regulations. If these third parties fail to perform satisfactorily, or do not adequately fulfill their obligations under the terms of our agreements with them, we may not be able to enter into alternative arrangements without undue delay or additional expenditures, and therefore the preclinical studies and clinical trials of our product candidate may be delayed or prove unsuccessful. Further, the FDA may inspect some of the clinical sites participating in our clinical trials in the U.S., or our third-party vendors' sites, to determine if our clinical trials are being conducted according to Good Clinical Practices or GCPs. If we or the FDA determine that our third-party vendors are not in compliance with, or have not conducted our clinical trials according to, applicable regulations we may be forced to delay, repeat or terminate such clinical trials.

14

We have limited capacity for recruiting and managing clinical trials, which could impair our timing to initiate or complete clinical trials of our product candidate and materially harm our business.

We have limited capacity to recruit and manage the clinical trials necessary to obtain FDA approval or approval by other regulatory authorities. By contrast, larger pharmaceutical and bio-pharmaceutical companies often have substantial staffs with extensive experience in conducting clinical trials with multiple product candidates across multiple indications. In addition, they may have greater financial resources to compete for the same clinical investigators and patients that we are attempting to recruit for our clinical trials. To the best of our knowledge, the following companies are potential competitors as we develop FV-100: Epiphany Biosceinces, Inc., Astellas Pharma US, Inc., GlaxoSmithKline plc and Janus Pharmaceuticals, Inc. Specifically, we are aware that valomaciclovir is being developed by Epiphany Pharmaceuticals and has completed Phase IIb clinical trials for VZV infections. To our knowledge, other potential competitors are in earlier stages of development for VZV infections. If potential competitors are successful in completing drug development for their product candidates and obtain approval from the FDA, they could limit the demand for FV-100.

As a result, we may be at a competitive disadvantage that could delay the initiation, recruitment, timing, completion of our clinical trials and obtaining regulatory approvals, if at all, for our product candidate.

We, and our collaborators, must comply with extensive government regulations in order to advance our product candidate through the development process and ultimately obtain and maintain marketing approval for our products in the U.S. and abroad.

The product candidates that we, or our collaborators, are developing require regulatory approval to advance through clinical development and to ultimately be marketed and sold, and are subject to extensive and rigorous domestic and foreign government regulation. In the U.S., the FDA regulates, among other things, the development, testing, manufacture, safety, efficacy, record-keeping, labeling, storage, approval, advertising, promotion, sale and distribution of pharmaceutical and biopharmaceutical products. Our product candidate is also subject to similar regulation by foreign governments to the extent we seek to develop or market them in those countries. We, or our collaborators, must provide the FDA and foreign regulatory authorities, if applicable, with preclinical and clinical data, as well as data supporting an acceptable manufacturing process, that appropriately demonstrate our product candidate' safety and efficacy before they can be approved for the targeted indications. Our product candidate has not been approved for sale in the U.S. or any foreign market, and we cannot predict whether we or our collaborators will obtain regulatory approval for any product candidate we are developing or plan to develop. The regulatory review and approval process can take many years, is dependent upon the type, complexity, novelty of, and medical need for the product candidate, requires the expenditure of substantial resources, and involves post-marketing surveillance and vigilance and ongoing requirements for post-marketing studies or Phase 4 clinical trials. In addition, we or our collaborators may encounter delays in, or fail to gain, regulatory approval for our product candidate based upon additional governmental regulation resulting from future legislative, administrative action or changes in FDA policy or interpretation during the period of product development. Delays or failures in obtaining regulatory approval to advance our product candidate through clinical development, and ultimately commercialize them, may:

- •

- adversely impact our ability to raise sufficient capital to fund the development of the program candidate;

- •

- adversely affect our ability to further develop or commercialize our product candidate;

- •

- diminish any competitive advantages that we or our collaborators may have or attain; and

- •

- adversely affect the receipt of potential milestone payments and royalties from the sale of our products or product revenues.

15

Furthermore, any regulatory approvals, if granted, may later be withdrawn. If we or our collaborators fail to comply with applicable regulatory requirements at any time, or if post-approval safety concerns arise, we or our collaborators may be subject to restrictions or a number of actions, including:

- •

- delays, suspension or termination of clinical trials related to our products;

- •

- refusal by regulatory authorities to review pending applications or supplements to approved applications;

- •

- product recalls or seizures;

- •

- suspension of manufacturing;

- •

- withdrawals of previously approved marketing applications; and

- •

- fines, civil penalties and criminal prosecutions.

Additionally, at any time we or our collaborators may voluntarily suspend or terminate the preclinical or clinical development of a product candidate, or withdraw any approved product from the market if we believe that it may pose an unacceptable safety risk to patients, or if the product candidate or approved product no longer meets our business objectives. The ability to develop or market a pharmaceutical product outside of the U.S. is contingent upon receiving appropriate authorization from the respective foreign regulatory authorities. Foreign regulatory approval processes typically include many, if not all, of the risks and requirements associated with the FDA regulatory process for drug development and may include additional risks.

We have limited experience in the development of small molecule antiviral product candidate and therefore may encounter difficulties developing our product candidate or managing our operations in the future.

Our lead product candidate, FV-100, is a chemical compound, also referred to as a small molecule. We have limited experience in the discovery, development and manufacturing of these small molecule antiviral compounds. In order to successfully develop this product candidate, we must continuously supplement our research, clinical development, regulatory, medicinal chemistry, virology and manufacturing capabilities through the addition of key employees, consultants or third-party contractors to provide certain capabilities and skill sets that we do not possess.

Furthermore, we have adopted an operating model that largely relies on the outsourcing of a number of responsibilities and key activities to third-party consultants, and contract research and manufacturing organizations in order to advance the development of our product candidate. Therefore, our success depends in part on our ability to retain highly qualified key management, personnel, and directors to develop, implement and execute our business strategy, operate the company and oversee the activities of our consultants and contractors, as well as academic and corporate advisors or consultants to assist us in this regard. We are currently highly dependent upon the efforts of our management team. In order to develop our product candidate, we need to retain or attract certain personnel, consultants or advisors with experience in the drug development activities of small molecules that include a number of disciplines, including research and development, clinical trials, medical matters, government regulation of pharmaceuticals, manufacturing, formulation and chemistry, business development, accounting, finance, human resources and information systems. We are highly dependent upon our senior management and scientific staff, particularly James Sapirstein, our Chief Executive Officer. The loss of services of Mr. Sapirstein or one or more of our other members of senior management could delay or prevent the successful completion of our planned clinical trials or the commercialization of our product candidate.

Our success depends in part on our continued ability to attract, retain and motivate highly qualified management, clinical and scientific personnel and on our ability to develop and maintain important relationships with leading academic institutions, clinicians and scientists. The competition for qualified personnel in the biotechnology and pharmaceuticals field is intense. We will need to hire additional

16

personnel as we expand our clinical development and commercial activities. While we have not had difficulties recruiting qualified individuals, to date, we may not be able to attract and retain quality personnel on acceptable terms given the competition for such personnel among biotechnology, pharmaceutical and other companies. Although we have not experienced material difficulties in retaining key personnel in the past, we may not be able to continue to do so in the future on acceptable terms, if at all. If we lose any key managers or employees, or are unable to attract and retain qualified key personnel, directors, advisors or consultants, the development of our product candidate could be delayed or terminated and our business may be harmed.

We will need to obtain FDA approval of any proposed product brand names, and any failure or delay associated with such approval may adversely impact our business.

A pharmaceutical product cannot be marketed in the U.S. or other countries until we have completed rigorous and extensive regulatory review processes, including approval of a brand name. Any brand names we intend to use for our product candidate will require approval from the FDA regardless of whether we have secured a formal trademark registration from the U.S. Patent and Trademark Office, or the PTO. The FDA typically conducts a review of proposed product brand names, including an evaluation of potential for confusion with other product names. The FDA may also object to a product brand name if the FDA believes the name inappropriately implies medical claims. If the FDA objects to any of our proposed product brand names, we may be required to adopt an alternative brand name for our product candidate. If we adopt an alternative brand name, we would lose the benefit of our existing trademark applications for such product candidate and may be required to expend significant additional resources in an effort to identify a suitable product brand name that would qualify under applicable trademark laws, not infringe the existing rights of third parties and be acceptable to the FDA. We may be unable to build a successful brand identity for a new trademark in a timely manner or at all, which would limit our ability to commercialize our product candidate.

Clinical trials involve a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials may not be predictive of future trial results.

Our product candidate may not prove to be safe and efficacious in clinical trials and may not meet all the applicable regulatory requirements needed to receive regulatory approval. In order to receive regulatory approval for the commercialization of our product candidate, we must conduct, at our own expense, extensive preclinical testing and clinical trials to demonstrate safety and efficacy of this product candidate for the intended indication of use. Clinical testing is expensive, can take many years to complete, if at all, and its outcome is uncertain. Failure can occur at any time during the clinical trial process.

The results of preclinical studies and early clinical trials of new drugs do not necessarily predict the results of later-stage clinical trials. The design of our clinical trials is based on many assumptions about the expected effects of our product candidate, and if those assumptions are incorrect it may not produce statistically significant results. Preliminary results may not be confirmed on full analysis of the detailed results of an early clinical trial. Product candidates in later stages of clinical trials may fail to show safety and efficacy sufficient to support intended use claims despite having progressed through initial clinical testing. The data collected from clinical trials of our product candidate may not be sufficient to support the filing of an NDA or to obtain regulatory approval in the United States or elsewhere. Because of the uncertainties associated with drug development and regulatory approval, we cannot determine if or when we will have an approved product for commercialization or achieve sales or profits.

Delays in clinical testing could result in increased costs to us and delay our ability to generate revenue.

We may experience delays in clinical testing of our product candidate. We do not know whether planned clinical trials will begin on time, will need to be redesigned or will be completed on schedule, if at all. Clinical trials can be delayed for a variety of reasons, including delays in obtaining regulatory approval

17

to commence a clinical trial, in securing clinical trial agreements with prospective sites with acceptable terms, in obtaining institutional review board approval to conduct a clinical trial at a prospective site, in recruiting patients to participate in a clinical trial or in obtaining sufficient supplies of clinical trial materials. Many factors affect patient enrollment, including the size of the patient population, the proximity of patients to clinical sites, the eligibility criteria for the clinical trial, competing clinical trials and new drugs approved for the conditions we are investigating. Clinical investigators will need to decide whether to offer their patients enrollment in clinical trials of our product candidate versus treating these patients with commercially available drugs that have established safety and efficacy profiles. Any delays in completing our clinical trials will increase our costs, slow down our product development, timeliness and approval process and delay our ability to generate revenue.

The regulatory approval processes of the FDA and comparable foreign authorities are lengthy, time consuming and inherently unpredictable, and if we are ultimately unable to obtain regulatory approval for our product candidate, our business will be substantially harmed.

The time required to obtain approval by the FDA and comparable foreign authorities is unpredictable but typically takes many years following the commencement of clinical trials and depends upon numerous factors, including the substantial discretion of the regulatory authorities. In addition, approval policies, regulations, or the type and amount of clinical data necessary to gain approval may change during the course of a product candidate's clinical development and may vary among jurisdictions. We have not obtained regulatory approval for any product candidate and it is possible that our existing product candidate or any product candidate we may seek to develop in the future will ever obtain regulatory approval.

Our product candidate could fail to receive regulatory approval for many reasons, including the following:

- •

- the FDA or comparable foreign regulatory authorities may disagree with the design or implementation of our clinical

trials;

- •

- we may be unable to demonstrate to the satisfaction of the FDA or comparable foreign regulatory authorities that a product

candidate is safe and effective for its proposed indication;

- •

- the results of clinical trials may not meet the level of statistical significance required by the FDA or comparable

foreign regulatory authorities for approval;

- •

- the FDA or comparable foreign regulatory authorities may disagree with our interpretation of data from preclinical studies

or clinical trials;

- •

- the data collected from clinical trials of our product candidate may not be sufficient to support the submission of an NDA

or other submission or to obtain regulatory approval in the United States or elsewhere;

- •

- the FDA or comparable foreign regulatory authorities may fail to approve the manufacturing processes or facilities of

third-party manufacturers with which we contract for clinical and commercial supplies;

- •

- the FDA or comparable foreign regulatory authorities may fail to approve the companion diagnostics we contemplate

developing with partners; and

- •

- the approval policies or regulations of the FDA or comparable foreign regulatory authorities may significantly change in a manner rendering our clinical data insufficient for approval.

18

This lengthy approval process as well as the unpredictability of future clinical trial results may result in our failing to obtain regulatory approval to market our product candidate, which would significantly harm our business, results of operations and prospects.

In addition, even if we were to obtain approval, regulatory authorities may approve our product candidate for fewer or more limited indications than we request, may not approve the price we intend to charge for our products, may grant approval contingent on the performance of costly post-marketing clinical trials, or may approve a product candidate with a label that does not include the labeling claims necessary or desirable for the successful commercialization of that product candidate. Any of the foregoing scenarios could materially harm the commercial prospects for our product candidate.

We, as a newly formed entity, have not previously submitted a biologics license application, or BLA, or a New Drug Application, or NDA, to the FDA, or similar drug approval filings to comparable foreign authorities, for our product candidate, and we cannot be certain that our product candidate will be successful in clinical trials or receive regulatory approval. Further, our product candidate may not receive regulatory approval even if they are successful in clinical trials. If we do not receive regulatory approvals for our product candidate, we may not be able to continue our operations. Even if we successfully obtain regulatory approvals to market one or more of our product candidates, our revenues will be dependent, in part, upon our collaborators' ability to obtain regulatory approval of the companion diagnostics to be used with our product candidate, as well as the size of the markets in the territories for which we gain regulatory approval and have commercial rights. If the markets for patients that we are targeting for our product candidate are not as significant as we estimate, we may not generate significant revenues from sales of such products, if approved.

We plan to seek regulatory approval and to commercialize our product candidate, directly or with a collaborator, worldwide including the United States, the European Union and other additional foreign countries which we have not yet identified. While the scope of regulatory approval is similar in other countries, to obtain separate regulatory approval in many other countries we must comply with numerous and varying regulatory requirements of such countries regarding safety and efficacy and governing, among other things, clinical trials and commercial sales, pricing and distribution of our product candidate, and we cannot predict success in these jurisdictions.

We may be required to suspend or discontinue clinical trials due to unexpected side effects or other safety risks that could preclude approval of our product candidate.

Our clinical trials may be suspended at any time for a number of reasons. For example, we may voluntarily suspend or terminate our clinical trials if at any time we believe that they present an unacceptable risk to the clinical trial patients. In addition, the FDA or other regulatory agencies may order the temporary or permanent discontinuation of our clinical trials at any time if they believe that the clinical trials are not being conducted in accordance with applicable regulatory requirements or that they present an unacceptable safety risk to the clinical trial patients.

Administering any product candidate to humans may produce undesirable side effects. These side effects could interrupt, delay or halt clinical trials of our product candidate and could result in the FDA or other regulatory authorities denying further development or approval of our product candidate for any or all targeted indications. Ultimately, some or all of our product candidates may prove to be unsafe for human use. Moreover, we could be subject to significant liability if any volunteer or patient suffers, or appears to suffer, adverse health effects as a result of participating in our clinical trials.

If we fail to comply with healthcare regulations, we could face substantial enforcement actions, including civil and criminal penalties and our business, operations and financial condition could be adversely affected.

As a developer of pharmaceuticals, even though we do not intend to make referrals of healthcare services or bill directly to Medicare, Medicaid or other third-party payers, certain federal and state

19

healthcare laws and regulations pertaining to fraud and abuse, false claims and patients' privacy rights are and will be applicable to our business. We could be subject to healthcare fraud and abuse laws and patient privacy laws of both the federal government and the states in which we conduct our business. The laws include:

- •

- the federal healthcare program anti-kickback law, which prohibits, among other things, persons from soliciting, receiving

or providing remuneration, directly or indirectly, to induce either the referral of an individual, for an item or service or the purchasing or ordering of a good or service, for which payment may be

made under federal healthcare programs such as the Medicare and Medicaid programs;

- •

- federal false claims laws which prohibit, among other things, individuals or entities from knowingly presenting, or

causing to be presented, claims for payment from Medicare, Medicaid, or other third-party payers that are false or fraudulent, and which may apply to entities like us which provide coding and billing

information to customers;

- •

- the federal Health Insurance Portability and Accountability Act of 1996, which prohibits executing a scheme to defraud any

healthcare benefit program or making false statements relating to healthcare matters and which also imposes certain requirements relating to the privacy, security and transmission of individually

identifiable health information;

- •

- the Federal Food, Drug, and Cosmetic Act, which among other things, strictly regulates drug manufacturing and product

marketing, prohibits manufacturers from marketing drug products for off-label use and regulates the distribution of drug samples; and

- •

- state law equivalents of each of the above federal laws, such as anti-kickback and false claims laws which may apply to items or services reimbursed by any third-party payer, including commercial insurers, and state laws governing the privacy and security of health information in certain circumstances, many of which differ from each other in significant ways and often are not preempted by federal laws, thus complicating compliance efforts.