Attached files

| file | filename |

|---|---|

| EX-23.5 - EX-23.5 - TerraForm Power NY Holdings, Inc. | d672387dex235.htm |

| EX-23.1 - EX-23.1 - TerraForm Power NY Holdings, Inc. | d672387dex231.htm |

| EX-23.2 - EX-23.2 - TerraForm Power NY Holdings, Inc. | d672387dex232.htm |

| EX-23.4 - EX-23.4 - TerraForm Power NY Holdings, Inc. | d672387dex234.htm |

| EX-23.3 - EX-23.3 - TerraForm Power NY Holdings, Inc. | d672387dex233.htm |

| EX-23.8 - EX-23.8 - TerraForm Power NY Holdings, Inc. | d672387dex238.htm |

| EX-23.6 - EX-23.6 - TerraForm Power NY Holdings, Inc. | d672387dex236.htm |

| EX-23.7 - EX-23.7 - TerraForm Power NY Holdings, Inc. | d672387dex237.htm |

Table of Contents

As filed with the Securities and Exchange Commission on May 28, 2014

No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

TerraForm Power, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 4911 | 46-4780940 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

12500 Baltimore Avenue

Beltsville, Maryland 20705

(443) 909-7200

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Sebastian Deschler, Esq.

General Counsel

TerraForm Power, Inc.

12500 Baltimore Avenue

Beltsville, Maryland 20705

(443) 909-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Dennis M. Myers, P.C. | Kirk A. Davenport II | |

| Kirkland & Ellis LLP | Latham & Watkins LLP | |

| 300 North LaSalle | 885 Third Avenue | |

| Chicago, Illinois 60654 | New York, New York 10022 | |

| (312) 862-2000 | (212) 906-1200 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this

Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to registered additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Offering |

Amount of Registration Fee(3) | ||

| Class A Common Stock, $0.01 par value per share |

$50,000,000 | $6,440 | ||

|

| ||||

|

| ||||

| (1) | Includes the offering price of the shares of Class A Common Stock that may be sold if the option to purchase additional shares granted by us to the underwriters is exercised in full. |

| (2) | Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(o) of the Securities Act of 1933, as amended. |

| (3) | Calculated by multiplying 0.0001288 by the proposed maximum offering price. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated , 2014

Shares

TerraForm Power, Inc.

Class A Common Stock

This is an initial public offering of the Class A common stock of TerraForm Power, Inc. All of the shares of Class A common stock are being sold by TerraForm Power, Inc.

Prior to this offering, there has been no public market for our Class A common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to list our Class A common stock on the NASDAQ Global Select Market under the symbol “TERP.”

We will have two classes of common stock outstanding after this offering, Class A common stock and Class B common stock. Each share of Class A common stock entitles its holder to one vote on all matters presented to our stockholders generally. All of our Class B common stock will be held by SunEdison, Inc., or our “Sponsor,” or its controlled affiliates. Each share of Class B common stock entitles our Sponsor to 10 votes on all matters presented to our stockholders generally. Immediately following this offering, the holders of our Class A common stock will collectively hold 100% of the economic interests and % of the voting power in us and our Sponsor will hold the remaining % of the voting power in us. As a result, we will be a “controlled company” within the meaning of the corporate governance standards of the NASDAQ Global Select Market. We are an “emerging growth company” as the term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, have elected to comply with certain reduced public company reporting requirements.

See “Risk Factors” beginning on page 36 to read about factors you should consider before buying shares of our Class A common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discount |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

To the extent that the underwriters sell more than shares of Class A common stock, the underwriters have the option to purchase up to an additional shares from TerraForm Power, Inc. at the initial public offering price less the underwriting discount.

The underwriters expect to deliver the shares against payment in New York, New York on , 2014.

Goldman, Sachs & Co.

Barclays

Citigroup

Prospectus dated , 2014.

Table of Contents

| Page | ||||

| 1 | ||||

| 22 | ||||

| 32 | ||||

| 36 | ||||

| 75 | ||||

| 76 | ||||

| 77 | ||||

| 79 | ||||

| 80 | ||||

| 97 | ||||

| 109 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

112 | |||

| 135 | ||||

| 143 | ||||

| 168 | ||||

| 173 | ||||

| Security Ownership of Certain Beneficial Owners and Management |

179 | |||

| 181 | ||||

| 202 | ||||

| 209 | ||||

| 216 | ||||

| Material United States Federal Income Tax Consequences to Non-U.S. Holders |

218 | |||

| 223 | ||||

| 228 | ||||

| 228 | ||||

| 229 | ||||

| F-1 | ||||

We have not and the underwriters have not authorized anyone to provide you with any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you. We are offering to sell, and seeking offers to buy, shares of our Class A common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus or any free writing prospectus is accurate only as of its date, regardless of its time of delivery or the time of any sale of shares of our Class A common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2014 (25 days after the date of this prospectus), all dealers that buy, sell or trade our Class A common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Trademarks and Trade Names

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of SunEdison, Inc. and third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this prospectus is not intended to, and should not be read to, imply a relationship with or endorsement or

i

Table of Contents

sponsorship of us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names. See “Certain Relationships and Related Party Transactions—Licensing Agreement” for a description of the licensing agreement pursuant to which we have licensed the right to use the SunEdison name and logo, subject to certain exceptions and limitations.

This prospectus includes industry data and forecasts that we obtained from industry publications and surveys, public filings and internal company sources. Industry publications and surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy or completeness of the included information. Statements as to our market position and market estimates are based on independent industry publications, government publications, third party forecasts, management’s estimates and assumptions about our markets and our internal research. While we are not aware of any misstatements regarding the market, industry or similar data presented herein, such data involve risks and uncertainties and are subject to change based on various factors, including those discussed under the headings “Cautionary Statement Concerning Forward-Looking Statements” and “Risk Factors” in this prospectus.

As used in this prospectus, all references to watts (e.g., Megawatts, Gigawatts, MW, GW, etc.) refer to measurements of direct current, or “DC,” except where otherwise noted.

Certain Defined Terms

Unless the context provides otherwise, references herein to:

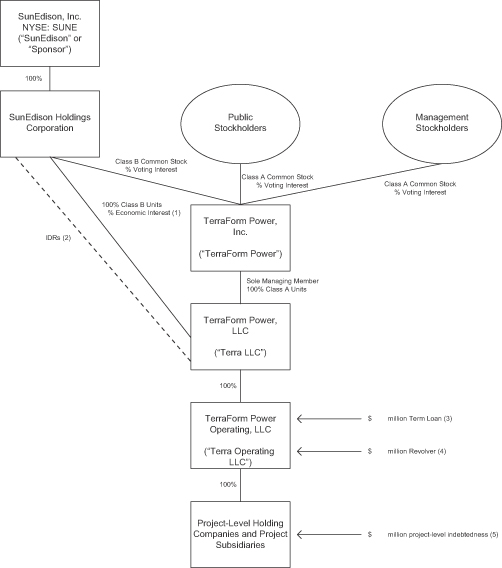

| • | “we,” “our,” “us,” “our company” and “TerraForm Power” refer to TerraForm Power, Inc., together with, where applicable, its consolidated subsidiaries after giving effect to the Organizational Transactions (as defined herein); |

| • | “Terra LLC” refers to TerraForm Power, LLC; |

| • | “Terra Operating LLC” refers to TerraForm Power Operating, LLC, a wholly owned subsidiary of Terra LLC; and |

| • | “SunEdison” and “Sponsor” refer to SunEdison, Inc. together with, where applicable, its consolidated subsidiaries. |

See “Summary—Organizational Transactions” for more information regarding our ownership structure.

ii

Table of Contents

The following summary highlights information contained elsewhere in this prospectus. It does not contain all the information you need to consider in making your investment decision. Before making an investment decision, you should read this entire prospectus carefully and should consider, among other things, the matters set forth under “Risk Factors,” “Selected Historical Combined Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our and our predecessor’s financial statements and related notes thereto appearing elsewhere in this prospectus.

About TerraForm Power, Inc.

We are a dividend growth-oriented company formed to own and operate contracted clean power generation assets acquired from SunEdison and unaffiliated third parties. Our business objective is to acquire high-quality contracted cash flows, primarily from owning solar generation assets serving utility, commercial and residential customers. Over time, we intend to acquire other clean power generation assets, including wind, natural gas, geothermal and hydro-electricity, as well as hybrid energy solutions that enable us to provide contracted power on a 24/7 basis. We believe the renewable power generation segment is growing more rapidly than other power generation segments due in part to the emergence in various energy markets of “grid parity,” which is the point at which renewable energy sources can generate electricity at a cost equal to or lower than prevailing electricity prices. We expect retail electricity prices to continue to rise due to increasing fossil fuel commodity prices, required investments in generation plants and transmission and distribution infrastructure and increasing regulatory costs. We believe we are well-positioned to capitalize on the growth in clean power electricity generation, both through project originations and transfers from our Sponsor as well as through acquisitions from unaffiliated third parties. We will benefit from the development pipeline, asset management experience and relationships of our Sponsor, which, as of March 31, 2014, had a 3.6 GW pipeline of development stage solar projects and approximately 1.9 GW of self-developed and third party developed solar power generation assets under management. Our Sponsor will provide us with a dedicated management team that has significant experience in clean power generation. We believe we are well-positioned for substantial growth due to the high-quality, diversification and scale of our project portfolio, the long-term power purchase agreements, or “PPAs,” we have with creditworthy counterparties, our dedicated management team and our Sponsor’s project origination and asset management capabilities.

Our initial portfolio will consist of solar projects located in the United States and its unincorporated territories, Canada, the United Kingdom and Chile with total nameplate capacity of 523.8 MW. All of these projects have long-term PPAs with creditworthy counterparties. The PPAs have a weighted average (based on MW) remaining life of 18 years as of March 31, 2014. We intend to rapidly expand and diversify our initial project portfolio by acquiring clean utility-scale and distributed generation assets located in the United States, Canada, the United Kingdom and Chile, each of which we expect will also have a long-term contracted PPA with a creditworthy counterparty. Growth in our project portfolio will be driven by our relationship with our Sponsor, including access to its project pipeline, and by our access to unaffiliated third party developers and owners of clean generation assets in our core markets.

Immediately prior to the completion of this offering, we will enter into a project support agreement, or the “Support Agreement,” with our Sponsor, which will require our Sponsor to offer us additional qualifying projects from its development pipeline that are projected to generate an aggregate of at least $175.0 million of cash available for distribution during the first 12 months following their respective

1

Table of Contents

commercial operations date, or “Projected FTM CAFD,” by the end of 2016. We refer to these projects as the “Call Right Projects.” Specifically, the Support Agreement requires our Sponsor to offer us:

| • | from the completion of this offering through the end of 2015, solar projects that are projected to generate an aggregate of at least $75.0 million of cash available for distribution during the first 12 months following their respective commercial operations date; and |

| • | during calendar year 2016, solar projects that are projected to generate an aggregate of at least $100.0 million of cash available for distribution during the first 12 months following their respective commercial operations date. |

If the amount of Projected FTM CAFD of the projects we acquire under the Support Agreement from the completion of this offering through the end of 2015 is less than $75.0 million, or the amount of Projected FTM CAFD of the projects we acquire under the Support Agreement during 2016 is less than $100.0 million, our Sponsor has agreed that it will continue to offer us sufficient Call Right Projects until the total aggregate Projected FTM CAFD commitment has been satisfied. The Call Right Projects that are specifically identified in the Support Agreement currently have a total nameplate capacity of 0.9 GW. We believe the currently identified Call Right Projects will be sufficient to satisfy a majority of the Projected FTM CAFD commitment for 2015 and between 15% and 40% of the Projected FTM CAFD commitment for 2016 (depending on the amount of project-level financing we use for such projects). The Support Agreement provides that our Sponsor is required to update the list of Call Right Projects with additional qualifying Call Right Projects from its pipeline until we have acquired projects under the Support Agreement that have the specified minimum amount of Projected FTM CAFD for each of the periods covered by the Support Agreement.

In addition, the Support Agreement grants us a right of first offer with respect to any solar projects (other than Call Right Projects) located in the United States and its unincorporated territories, Canada, the United Kingdom, Chile and certain other jurisdictions that our Sponsor decides to sell or otherwise transfer during the six-year period following the completion of this offering. We refer to these projects as the “ROFO Projects.” The Support Agreement does not identify the ROFO Projects since our Sponsor will not be obligated to sell any project that would constitute a ROFO Project. As a result, we do not know when, if ever, any ROFO Projects or other assets will be offered to us. In addition, in the event that our Sponsor elects to sell such assets, it will not be required to accept any offer we make to acquire any ROFO Project and, following the completion of good faith negotiations with us, our Sponsor may choose to sell such assets to a third party or not to sell the assets at all.

We believe we are well-positioned to capitalize on additional growth opportunities in the clean energy industry. Further, we believe that demand for renewable energy among our customer segments is accelerating due to the emergence of grid parity in certain segments of our target markets, the lack of commodity price risk in renewable energy generation and strong political and social support. In addition, growth is driven by the ability to locate renewable energy generating assets at a customer site, which reduces our customers’ transmission and distribution costs. We believe that we are already capitalizing on the favorable growth dynamics in the clean energy industry, as illustrated by the following examples:

| • | Grid Parity. We evaluate grid parity on an individual site or customer basis, taking into account numerous factors including the customer’s geographical location and solar availability, the terrain or roof orientation where the system will be located, cost to install, prevailing electricity rates and any demand or time-of-day use charges. One of our projects located in Chile provides approximately 100 MW of utility-scale power under a 20-year PPA with a mining company at a price below the current wholesale price of electricity in that region. We believe |

2

Table of Contents

| that additional grid parity opportunities will arise in other markets with growing energy demand, increasing power prices and favorable solar attributes. |

| • | Distributed Generation. We own and operate a 135.3 MW distributed generation platform with a footprint in the United States, Puerto Rico and Canada with commercial and residential customers, who currently purchase electricity from us under long-term PPAs at prices at or below local retail electricity rates. These distributed generation projects reduce our customers’ transmission and distribution costs because they are located on the customers’ sites. By bypassing the traditional electrical suppliers and transmission systems, distributed energy systems delink the customer’s electricity price from external factors such as volatile commodity prices and costs of the incumbent energy supplier. This makes it possible for distributed energy purchasers to buy electricity at predictable and stable prices over the duration of a long-term contract. |

As our addressable market expands, we expect there will be significant additional opportunities for us to own clean energy generation assets and provide contracted, reliable power at competitive prices to the customer segments we serve, which we believe will sustain and enhance our future growth.

We intend to use a portion of the cash available for distribution, or “CAFD,” generated by our project portfolio to pay regular quarterly cash dividends to holders of our Class A common stock. Our initial quarterly dividend will be set at $ per share of Class A common stock, or $ per share on an annualized basis. We established our initial quarterly dividend level based upon a targeted payout ratio by Terra LLC of approximately 85% of projected annual cash available for distribution. Our objective is to pay our Class A common stockholders a consistent and growing cash dividend that is sustainable on a long-term basis. Based on our forecast and the related assumptions and our intention to acquire assets with characteristics similar to those in our initial portfolio, we expect to grow our cash available for distribution and increase our quarterly cash dividends over time.

We intend to target a 15% compound annual growth rate in CAFD per unit over the three-year period following the completion of this offering. This target is based on, among other assumptions, our Sponsor satisfying its $175.0 million aggregate CAFD commitment to us in accordance with the Support Agreement on terms that enable us to achieve such targeted growth rate. While we believe our targeted growth rate is reasonable, it is based on estimates and assumptions regarding a number of factors, many of which are beyond our control. Prospective investors should read “Cash Dividend Policy,” including our financial forecast and related assumptions, and “Risk Factors,” including the risks and uncertainties related to our forecasted results, completion of construction of projects and acquisition opportunities, in their entirety.

We intend to cause Terra LLC to distribute its CAFD to holders of its units (including us as the sole holder of the Class A units and our Sponsor as the sole holder of the Class B units) pro rata, based on the number of units held, subject to the incentive distribution rights, or “IDRs,” held by our Sponsor that are described below. However, the Class B units held by our Sponsor are deemed “subordinated” because for a period of time, referred to as the Subordination Period, the Class B units will not be entitled to receive any distributions from Terra LLC until the Class A units and Class B1 units (which may be issued upon reset of IDR target distribution levels or in connection with acquisitions from our Sponsor or third-parties) have received quarterly distributions in an amount equal to $ per unit, or the “Minimum Quarterly Distribution,” plus any arrearages in the payment of the Minimum Quarterly Distribution from prior quarters. The practical effect of the subordination of the Class B units is to increase the likelihood that during the Subordination Period there will be sufficient CAFD to pay the Minimum Quarterly Distribution on the Class A units and Class B1 units (if any). See

3

Table of Contents

“Certain Relationships and Related Party Transactions—Amended and Restated Operating Agreement of Terra LLC—Distributions.”

Our Sponsor has further agreed to forego any distributions on its Class B units with respect to the third or fourth quarter of 2014 (i.e. distributions declared on or prior to March 31, 2015), and thereafter has agreed to a reduction of distributions on its Class B units until the expiration of the Distribution Forbearance Period. The amount of our Sponsor’s distribution reduction between March 31, 2015 and the end of the Distribution Forbearance Period is based on the percentage of the As Delivered CAFD compared to the expected CAFD attributable to the Contributed Construction Projects (and substitute projects contributed by our Sponsor). The practical effect of this forbearance is to ensure that the Class A units will not be effected by delays in completion of the Contributed Construction Projects. All of the projects in our initial portfolio have already reached their commercial operations date, or “COD,” or are expected to reach COD prior to the end of 2014, including the Contributed Construction Projects. For a description of the IDRs, the Subordination Period and the Distribution Forbearance Period, including the definitions of Subordination Period, As Delivered CAFD, Contributed Construction Projects, CAFD Forbearance Threshold and Distribution Forbearance Period see “Certain Relationships and Related Party Transactions—Amended and Restated Operating Agreement of Terra LLC—Distributions.”

About our Sponsor

We believe our relationship with our Sponsor provides us with the opportunity to benefit from our Sponsor’s expertise in solar technology, project development, finance, management and operations. Our Sponsor is a solar industry leader based on its history of innovation in developing, financing and operating solar energy projects and its strong market share relative to other U.S. and global installers and integrators. As of March 31, 2014, our Sponsor had a development pipeline of approximately 3.6 GW and solar power generation assets under management of approximately 1.9 GW, comprised of over 900 solar generation facilities across 12 countries. These projects were managed by a dedicated team using three renewable energy operation centers globally. As of March 31, 2014, our Sponsor had approximately 2,200 employees. After completion of this offering, our Sponsor will own 100.0% of Terra LLC’s outstanding Class B units and will hold all of the IDRs.

Purpose of TerraForm Power, Inc.

We intend to create value for holders of our Class A common stock by achieving the following objectives:

| • | acquiring long-term contracted cash flows from clean power generation assets with creditworthy counterparties; |

| • | growing our business by acquiring contracted clean power generation assets from our Sponsor and third parties; |

| • | capitalizing on the expected high growth in the clean power generation market, which is projected to require over $2.9 trillion of investment over the period from 2013 through 2020, of which $802 billion is expected to be invested in solar photovoltaic, or “PV,” generation assets; |

| • | creating an attractive investment opportunity for dividend growth oriented investors; |

| • | creating a leading global clean power generation asset platform, with the capability to increase the cash flow and value of the assets over time; and |

| • | gaining access to a broad investor base with a more competitive source of equity capital that accelerates our long-term growth and acquisition strategy. |

4

Table of Contents

Our Initial Portfolio and the Call Right Projects

The following table provides an overview of the assets that will comprise our initial portfolio:

| Project Names |

Location | Commercial |

Nameplate Capacity (MW)(2) |

# of Sites |

Project Origin(3) |

Offtake Agreements |

||||||||||||||||||

| Counterparty |

Counterparty Credit Rating(4) |

Remaining Duration of PPA (Years)(5) |

||||||||||||||||||||||

| Distributed Generation: |

||||||||||||||||||||||||

| U.S. Projects 2014 |

U.S. | Q2 2014-Q4 2014 | 46.5 | 42 | C | Various utilities, municipalities and commercial entities(6) |

A+, A1 | 19 | ||||||||||||||||

| Summit Solar Projects |

U.S. |

2007-2014 |

19.6 | 50 | A | Various commercial and governmental entities | A, A2 |

14 |

||||||||||||||||

| Canada | 2011-2013 |

3.8 | 7 | A | Ontario Power Authority | A-, Aa1 | 18 | |||||||||||||||||

| Enfinity |

U.S. | 2011-2013 | |

15.7 |

|

16 | A | Various commercial, residential and governmental entities | A, A2 | 18 | ||||||||||||||

| U.S. Projects 2009-2013 |

U.S. |

2009-2013 |

15.2 | 73 | C | Various commercial and governmental entities | BBB+, Baa1 |

|

16 |

| ||||||||||||||

| California Public Institutions |

U.S. |

Q4 2013-Q3 2014 |

13.5 | 5 | C | State of California Department of Corrections and Rehabilitation | AA, Aa2 |

|

20 |

| ||||||||||||||

| MA Operating |

U.S. | Q3 2013-Q4 2013 | 12.2 | 4 | A | Various municipalities | A+, A1 | 20 | ||||||||||||||||

| SunE Solar Fund X |

U.S. | 2010-2011 | 8.8 | 12 | C | Various utilities, municipalities and commercial entities | AA, Aa2 | 17 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Subtotal |

135.3 | 209 | ||||||||||||||||||||||

| Utility: |

||||||||||||||||||||||||

| Regulus Solar |

U.S. | Q4 2014 | 81.9 | 1 | C | Southern California Edison | BBB+, A3 | 20 | ||||||||||||||||

| North Carolina Portfolio |

U.S. |

Q4 2014 |

26.0 | 4 | C | Duke Energy Progress | BBB+, Baa2 | 15 | ||||||||||||||||

| Atwell Island |

U.S. | Q1 2013 | 23.5 | 1 | A | Pacific Gas & Electric Company | BBB, A3 |

24 | ||||||||||||||||

| Nellis |

U.S. | Q4 2007 | 14.1 | 1 | A | U.S. Government (PPA); Nevada Power Company (RECs)(6) | AA+, Aaa, BBB+, Baa2 |

14 | ||||||||||||||||

| Alamosa |

U.S. | Q4 2007 | 8.2 | 1 | C | Xcel Energy | A-, A3 | 14 | ||||||||||||||||

| CalRENEW-1 |

U.S. | Q2 2010 | 6.3 | 1 | A | Pacific Gas & Electric Company |

BBB, A3 | 16 | ||||||||||||||||

| SunE Perpetual Lindsay |

Canada |

Q3 2014 |

15.5 | 1 | C | Ontario Power Authority | A-, Aa1 | 20 | ||||||||||||||||

| Stonehenge Q1 |

U.K. | Q2 2014 | 41.1 | 3 | A | Statkraft AS |

A-, Baa1 | 15 | ||||||||||||||||

| Stonehenge Operating |

U.K. |

Q1 2013-Q2 2013 |

23.6 | 3 | A | Total Gas & Power Limited | NR, NR | 14 | ||||||||||||||||

| Says Court |

U.K. | Q2 2014 | 19.8 | 1 | C | Statkraft AS |

A-, Baa1 | 15 | ||||||||||||||||

| Crucis Farm |

U.K. | Q3 2014 | 16.1 | 1 | C | Statkraft AS |

A-, Baa1 | 15 | ||||||||||||||||

| Norrington |

U.K. | Q2 2014 | 11.2 | 1 | A | Statkraft AS |

A-, Baa1 | 15 | ||||||||||||||||

| CAP(7) |

Chile | Q1 2014 | 101.2 | 1 | C | Compañía Minera del Pacífico (CMP) | BBB-, NR | 20 | ||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Subtotal |

388.5 | 20 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| Total Initial Portfolio |

523.8 | 229 | ||||||||||||||||||||||

|

|

|

|

|

|||||||||||||||||||||

| (1) | Represents actual or anticipated commercial operation date, as applicable, unless otherwise indicated. |

| (2) | Nameplate capacity represents the maximum generating capacity at standard test conditions of a facility multiplied by our percentage ownership of that facility (disregarding any equity interests held by any tax equity investor or lessor under any sale-leaseback financing or of any non-controlling interests in a partnership). Generating capacity may vary based on a variety of factors discussed elsewhere in this prospectus. |

| (3) | Projects which have been contributed by our Sponsor, or “Contributed Projects,” are reflected in the Predecessor’s combined consolidated historical financial statements, and are identified with a “C” above. A project which has been acquired or is probable of being acquired contemporaneously with the completion of this offering, an “Acquisition” or “Acquired Project,” is identified with an “A” above. |

5

Table of Contents

| (4) | For our distributed generation projects with one counterparty and for our utility-scale projects the counterparty credit rating reflects the counterparty’s or guarantor’s issuer credit ratings issued by Standard & Poor’s Ratings Services, or “S&P,” and Moody’s Investors Service Inc., or “Moody’s.” For distributed generation projects with more than one counterparty the counterparty credit rating represents a weighted average (based on nameplate capacity) credit rating of project’s counterparties that are rated by S&P, Moody’s or both. The percentage of counterparties that are rated by S&P, Moody’s or both (based on nameplate capacity) of each of our distributed generation projects is as follows: |

| • | U.S. Projects 2014: 82% |

| • | Summit Solar Projects (U.S.): 21% |

| • | Summit Solar Projects (Canada): 100% |

| • | Enfinity: 85% |

| • | U.S. Projects 2009-2013: 35% |

| • | California Public Institutions: 100% |

| • | MA Operating: 100% |

| • | SunE Solar Fund X: 89% |

| (5) | Calculated as of March 31, 2014. For distributed generation projects, the number represents a weighted average (based on nameplate capacity) remaining duration. For Nellis represents remaining duration of REC contract. |

| (6) | REC contract for the Nellis project, which represents over 90% of the expected revenues, has remaining duration of approximately 14 years. The PPA of the Nellis project has an indefinite term subject to one-year reauthorizations. |

| (7) | The PPA counterparty has the right, under certain circumstances, to purchase up to 40% of the project equity from us pursuant to a predetermined purchase price formula. See “Business—Our Portfolio—Initial Portfolio—Utility Projects—CAP.” |

The projects in our initial portfolio, as well as the Call Right Projects discussed below, were selected because they are located in the geographic locations we intend to initially target. All of the projects in our initial portfolio have, and all of the Call Right Projects have or will have, long-term PPAs with creditworthy counterparties that we believe will provide sustainable and predictable cash flows to fund the regular quarterly cash dividends that we intend to pay to holders of our Class A common stock. All the projects in our initial portfolio have already reached COD or are expected to reach COD prior to the end of 2014, while the Call Right Projects generally are not expected to reach COD until the fourth quarter of 2014 or later.

The Support Agreement has established an aggregate purchase price of $ million (subject to such adjustments as the parties may mutually agree) for the Call Right Projects set forth in the table below under the heading “Priced Call Right Projects.” This aggregate price was determined by good faith negotiations between us and our Sponsor. If we elect to purchase less than all of the Priced Call Right Projects, we and our Sponsor will negotiate prices for individual projects.

We will have the right to acquire additional Call Right Projects set forth in the table below under the heading “Unpriced Call Right Projects” at prices that will be determined in the future. The price for each Call Right Project will be the fair market value. The Support Agreement provides that we will work with our Sponsor to mutually agree on the fair market value, but if we are unable to, we and our Sponsor will engage a third party advisor to determine the fair market value, after which we have the right (but not the obligation) to acquire such Call Right Project. Until the price for a Call Right Asset is mutually agreed to by us and our Sponsor, in the event our Sponsor receives a bona fide offer for a Call Right Project from a third party, we will have the right to match any price offered by such third party and acquire such Call Right Project on the terms our Sponsor could obtain from the third party. After the price for a Call Right Asset has been agreed and until the total aggregate Projected FTM CAFD commitment has been satisfied, our Sponsor may not market, offer or sell that Call Right Asset to any third party without our consent. The Support Agreement will further provide that our Sponsor is required to offer us additional qualifying Call Right Projects from its pipeline on a quarterly basis until we have acquired projects under the Support Agreement that have the specified minimum amount of Projected FTM CAFD for each of the two periods covered by the Support Agreement. We cannot assure you that we will be offered these Call Right Projects on terms that are favorable to us. See “Certain Relationships and Related Party Transactions—Project Support Agreement” for additional information.

6

Table of Contents

The following table provides an overview of the Call Right Projects that are currently identified in the Support Agreement:

| Project Names(1) |

Location | Expected Acquisition Date(2) |

Nameplate Capacity (MW)(3) |

# of Sites | ||||||||

| Priced Call Right Projects: |

||||||||||||

| Ontario 2015 projects |

Canada | Q1 2015 - Q4 2015 | 13.2 | 22 | ||||||||

| UK project #1 |

U.K. | Q2 2015 | 43.0 | 1 | ||||||||

| UK project #2 |

U.K. | Q2 2015 |

25.0 | 1 | ||||||||

| UK project #3 |

U.K. | Q2 2015 |

13.0 | 1 | ||||||||

| UK project #4 |

U.K. | Q2 2015 | 12.0 | 1 | ||||||||

| UK project #5 |

U.K. | Q2 2015 |

11.5 | 1 | ||||||||

| UK project #6 |

U.K. | Q2 2015 |

8.7 | 1 | ||||||||

| UK project # 7 |

U.K. | Q2 2015 | 8.0 | 1 | ||||||||

| Chile 69MW project |

Chile | Q1 2015 | 69.0 | 1 | ||||||||

| Ontario 2016 projects |

Canada | Q1 2016 - Q4 2016 | 10.8 | 18 | ||||||||

| Chile 94MW project |

Chile | Q1 2016 | 94.0 | 1 | ||||||||

|

|

|

|

|

|||||||||

| Total Priced Call Right Projects |

308.2 | 49 | ||||||||||

| Unpriced Call Right Projects: |

||||||||||||

| US DG 2H2014 & 2015 projects |

U.S. | Q3 2014 - Q4 2015 | 105.7 | 92 | ||||||||

| US AP North Lake I |

U.S. | Q3 2015 | 26.0 | 1 | ||||||||

| US Victorville |

U.S. | Q3 2015 | 13.0 | 1 | ||||||||

| US Bluebird |

U.S. | Q2 2015 | 7.8 | 1 | ||||||||

| US Western project #1 |

U.S. | Q2 2016 | 156.0 | 1 | ||||||||

| US Southwest project #1 |

U.S. | Q2 2016 | 100.0 | 1 | ||||||||

| US Island project #1 |

U.S. | Q2 2016 | 65.0 | 1 | ||||||||

| US Southeast project #1 |

U.S. | Q1 2016 | 65.0 | 1 | ||||||||

| US DG 2016 projects |

U.S. | Q1 2016 - Q4 2016 | 42.8 | 7 | ||||||||

| US California project #1 |

U.S. | Q3 2016 | 44.8 | 1 | ||||||||

|

|

|

|

|

|||||||||

| Total Unpriced Call Right Projects |

626.1 | 107 | ||||||||||

|

|

|

|

|

|||||||||

| Total 2015 projects |

355.9 | 125 | ||||||||||

| Total 2016 projects |

578.4 | 31 | ||||||||||

|

|

|

|

|

|||||||||

| Total Call Right Projects |

934.3 | 156 | ||||||||||

|

|

|

|

|

|||||||||

| (1) | Our Sponsor may remove a project from the Call Right Project list effective upon notice to us if, in its reasonable discretion, a project is unlikely to be successfully completed. In that case, the Sponsor will be required to replace such project with one or more additional reasonably equivalent projects that have a similar economic profile. |

| (2) | Represents date of actual or anticipated acquisition, unless otherwise indicated. |

| (3) | Nameplate capacity represents the maximum generating capacity at standard test conditions of a facility multiplied by our expected percentage ownership of such facility (disregarding equity interests of any tax equity investor or lessor under any sale-leaseback financing or any non-controlling interests in a partnership). Generating capacity may vary based on a variety of factors discussed elsewhere in this prospectus. |

7

Table of Contents

Cash Available for Distribution

The table below summarizes our estimated cash available for distribution per share of Class A common stock for the 12 months ending June 30, 2015 and December 31, 2015 based on our forecasts included elsewhere in this prospectus:

| Forecast for the 12 Months Ending | ||||||||

| June 30, 2015 |

December 31, 2015 |

|||||||

| (in thousands, except per share and project data) | (unaudited) | |||||||

| Assumed operational projects throughout period |

||||||||

| Cash available for distribution(1) |

$ | 64,300 | $ | 81,900 | ||||

| Cash available for distribution to holders of Class A shares |

||||||||

| Class A shares at period end |

||||||||

| Cash available for distribution per Class A share |

||||||||

| (1) | Cash available for distribution is not a measure of performance under U.S. generally accepted accounting principles, or “GAAP.” For a reconciliation of these forecasted metrics to their closest GAAP measure, see “Cash Dividend Policy—Estimate of Future Cash Available for Distribution” elsewhere in this prospectus. |

We define “cash available for distribution” or “CAFD” as net cash provided by operating activities of Terra LLC as adjusted for certain other cash flow items that we associate with our operations. It is a non-GAAP measure of our ability to generate cash to service our dividends. As calculated in this prospectus, cash available for distribution represents net cash provided by (used in) operating activities of Terra LLC (i) plus or minus changes in working capital, (ii) minus deposits into (or plus withdrawals from) restricted cash accounts required by project financing arrangements to the extent they decrease (or increase) cash provided by operating activities, (iii) minus cash distributions paid to non-controlling interests in our projects, if any, (iv) minus scheduled project-level and other debt service payments and repayments in accordance with the related borrowing arrangements, to the extent they are paid from operating cash flows during a period, (v) minus non-expansionary capital expenditures, if any, to the extent they are paid from operating cash flows during a period, (vi) plus cash contributions from our Sponsor pursuant to the Interest Payment Agreement, (vii) plus operating costs and expenses paid by our Sponsor pursuant to the Management Services Agreement to the extent such costs or expenses exceed the fee payable by us pursuant to such agreement but otherwise reduce our net cash provided by operating activities and (viii) plus or minus other operating items as necessary to present the cash flows we deem representative of our core business operations, with the approval of the audit committee. Our intention is to cause Terra LLC to distribute a portion of the cash available for distribution generated by our project portfolio as dividends each quarter, after appropriate reserves for our working capital needs and the prudent conduct of our business. For further discussion of cash available for distribution, including a reconciliation of net cash provided by (used in) operating activities to cash available for distribution and a discussion of its limitations, see footnote (2) under the heading “Summary Historical and Pro Forma Financial Data” elsewhere in this prospectus.

Industry Overview

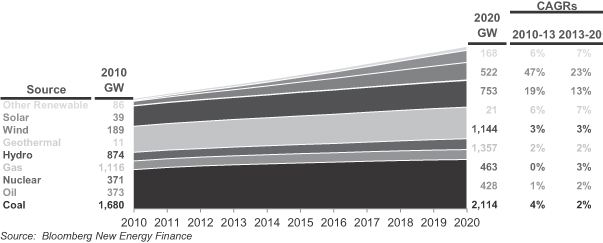

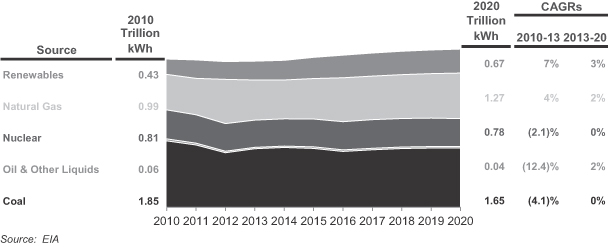

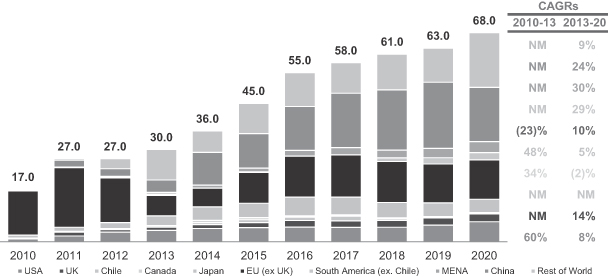

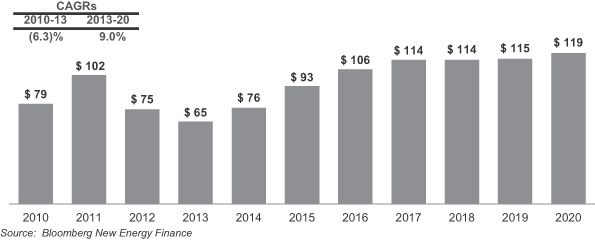

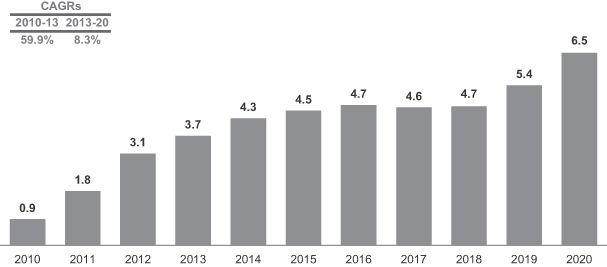

We expect to benefit from continued high growth in clean energy across the utility, commercial and residential customer segments. According to Bloomberg New Energy Finance, over 1,418 GW of clean power generation projects are expected to be installed globally over the period from 2013 through 2020, requiring an aggregate investment of over $2.9 trillion across the utility, commercial and residential markets.

8

Table of Contents

We believe the solar segment of the clean power generation industry is particularly attractive as declining solar costs and increasing grid electricity costs are accelerating the attainment of grid parity in various markets. Solar energy offers a compelling value proposition in markets that have reached grid parity because customers can typically purchase renewable energy for less than the cost of electricity generated by local utilities, pay little to no up-front cost and lock in long-term energy costs, insulating themselves from rising electricity rates. We expect a number of additional markets in our target geographies will reach grid parity in the coming years.

Solar energy benefits from highly predictable energy generation, the absence of fuel costs, proven technology and strong political and social support. In addition, solar generating assets are able to be located at a customer’s site which reduces the customer’s transmission and distribution costs. Finally, solar energy generation benefits from governmental, public and private support for the development of solar energy projects due to the environmentally friendly attributes of solar energy.

Our Business Strategy

Our primary business strategy is to increase the cash dividends we pay to the holders of our Class A common stock over time. Our plan for executing this strategy includes the following:

Focus on long-term contracted clean power generation assets. Our initial portfolio and any Call Right Projects that we acquire pursuant to the Support Agreement will have long-term PPAs with creditworthy counterparties. We intend to focus on owning and operating long-term contracted clean power generation assets with proven technologies, low operating risks and stable cash flows consistent with our initial portfolio. We believe industry trends will support significant growth opportunities for long-term contracted power in the clean power generation segment as various markets around the world reach grid parity.

Grow our business through acquisitions of contracted operating assets. We intend to acquire additional contracted clean power generation assets from our Sponsor and unaffiliated third parties to increase our cash available for distribution. The Support Agreement provides us with (i) the option to acquire the identified Call Right Projects, which currently represent an aggregate nameplate capacity of approximately 0.9 GW, and additional projects from SunEdison’s development pipeline that will be designated as Call Right Projects under the Support Agreement to satisfy the aggregate FTM CAFD commitment of $175.0 million and (ii) a right of first offer on the ROFO Projects. In addition, we expect to have significant opportunities to acquire other clean power generation assets from third party developers, independent power producers and financial investors. We believe our knowledge of the market, third party relationships, operating expertise and access to capital will provide us with a competitive advantage in acquiring new assets.

Attractive asset class. We intend to initially focus on the solar energy segment because we believe solar is currently the fastest growing segment of the clean power generation industry in which to own assets and deploy long-term capital due to the predictability of solar power cash flows. In particular, we believe the solar segment is attractive because there is no associated fuel cost risk and solar technology has become highly reliable and, based on the experience of our Sponsor, requires low operational and maintenance expenditures and a low level of interaction from managers. Solar projects also have an expected life which can exceed 30 to 40 years. In addition, the solar energy generation projects in our initial portfolio generally operate under long-term PPAs with terms of up to 20 years.

9

Table of Contents

Focus on core markets with favorable investment attributes. We intend to focus on growing our portfolio through investments in markets with (i) creditworthy PPA counterparties, (ii) high clean energy demand growth rates, (iii) low political risk, stable market structures and well-established legal systems, (iv) grid parity or the potential to reach grid parity in the near term and (v) favorable government policies to encourage renewable energy projects. We believe there will be ample opportunities to acquire high-quality contracted power generation assets in markets with these attributes. While our current focus is on solar generation assets in the United States and its unincorporated territories, Canada, the United Kingdom and Chile, we will selectively consider acquisitions of contracted clean generation sources in other countries.

Maintain sound financial practices. We intend to maintain our commitment to disciplined financial analysis and a balanced capital structure. Our financial practices will include (i) a risk and credit policy focused on transacting with creditworthy counterparties, (ii) a financing policy focused on achieving an optimal capital structure through various capital formation alternatives to minimize interest rate and refinancing risks, and (iii) a dividend policy that is based on distributing the cash available for distribution generated by our project portfolio (after deducting appropriate reserves for our working capital needs and the prudent conduct of our business). Our initial dividend was established based on our targeted payout ratio of approximately % of projected cash available for distribution. See “Cash Dividend Policy.”

Our Competitive Strengths

We believe our key competitive strengths include:

Scale and geographic diversity. Our initial portfolio and the Call Right Projects will provide us with significant diversification in terms of market segment, counterparty and geography. These projects, in the aggregate, represent 524.1 MW of nameplate capacity, which are expected to consist of 388.3 MW of nameplate capacity from utility projects and 135.3 MW of nameplate capacity of commercial, industrial, government and residential customers. Our diversification reduces our operating risk profile and our reliance on any single market or segment. We believe our scale and geographic diversity improve our business development opportunities through enhanced industry relationships, reputation and understanding of regional power market dynamics.

Stable high-quality cash flows. Our initial portfolio of projects, together with the Call Right Projects and third party projects that we acquire, will provide us with a stable, predictable cash flow profile. We sell the electricity generated by our projects under long-term PPAs with creditworthy counterparties. As of March 31, 2014, the weighted average (based on MW) remaining life of our PPAs was 18 years. All of our projects have highly predictable operating costs, in large part due to solar facilities having no fuel cost and reliable technology. Finally, based on our initial portfolio of projects, we do not expect to pay significant federal income taxes in the near term.

Newly constructed portfolio. We benefit from a portfolio of relatively newly constructed assets, with most of the projects in our initial portfolio having achieved COD within the past three years. All of the Call Right Projects are expected to achieve COD by the end of 2016. The projects in our initial portfolio and the Call Right Projects utilize proven and reliable technologies provided by leading equipment manufacturers and, as a result, we expect to achieve high generation availability and predictable maintenance capital expenditures.

10

Table of Contents

Relationship with SunEdison. We believe our relationship with our Sponsor provides us with significant benefits, including the following:

| • | Strong asset development and acquisition track record. Over the last five calendar years, our Sponsor has constructed or acquired solar power generation assets with an aggregate nameplate capacity of 1.4 GW and, as of March 31, 2014, was constructing additional solar power generation assets expected to have an aggregate nameplate capacity of approximately 504 MW. Our Sponsor has been one of the top five developers and installers of solar energy facilities in the world in each of the past four years based on megawatts installed. In addition, our Sponsor had a 3.6 GW pipeline of development stage solar projects as of March 31, 2014. Our Sponsor’s operating history demonstrates its organic project development capabilities and its ability to work with third party developers and asset owners in our target markets. We believe our Sponsor’s relationships, knowledge and employees will facilitate our ability to acquire operating projects from our Sponsor and unaffiliated third-parties in our target markets. |

| • | Project financing experience. We believe our Sponsor has demonstrated a successful track record of sourcing long duration capital to fund project acquisitions, development and construction. Since 2005, our Sponsor has raised approximately $5 billion in long-term non-recourse project and tax equity financing for hundreds of projects. We expect that we will realize significant benefits from our Sponsor’s financing and structuring expertise as well as its relationships with financial institutions and other providers of capital. |

| • | Management and operations expertise. We will have access to the significant resources of our Sponsor to support the growth strategy of our business. As of March 31, 2014, our Sponsor had over 1.9 GW of projects under management across 12 countries. Approximately 16.0% of these projects are third party power generation facilities, which demonstrates our Sponsor’s collaboration with multiple solar developers and owners. These projects utilize 30 different module types and inverters from 12 different manufacturers. In addition, our Sponsor maintains three renewable energy operation centers to service assets under management. Our Sponsor’s operational and management experience helps ensure that our facilities will be monitored and maintained to maximize their cash generation. |

Dedicated management team. Under the Management Services Agreement, our Sponsor has committed to provide us with a dedicated team of professionals to serve as our executive officers and other key officers. Our officers have considerable experience in developing, acquiring and operating clean power generation assets, with an average of over nine years of experience in the sector. For example, our Chief Executive Officer has served as the President of SunEdison’s solar energy business since November 2009. Our management team will also have access to the other significant management resources of our Sponsor to support the operational, financial, legal and regulatory aspects of our business.

Agreements with our Sponsor

We will enter into the following agreements with our Sponsor immediately prior to the completion of this offering. For a more comprehensive discussion of these agreements, see “Certain Relationships and Related Party Transactions.” For a discussion of the risks related to our relationship with our Sponsor, see “Risk Factors—Risks Related to our Relationship with our Sponsor.” In addition, we will amend Terra LLC’s operating agreement to provide for Class A units and Class B units and to convert our Sponsor’s interest in TerraForm Power’s common equity into Class B units and issue the IDRs to our Sponsor. As a result of holding Class B units and IDRs, subject to certain limitations during the Subordination Period and the Distribution Forbearance Period, our Sponsor will be entitled to share in

11

Table of Contents

distributions from Terra LLC to its unit holders. See “Certain Relationships and Related Party Transactions—Amended and Restated Operating Agreement of Terra LLC.”

Project Support Agreement. Pursuant to the Support Agreement, our Sponsor will provide us with the right, but not the obligation, to purchase for cash certain solar projects from its project pipeline with aggregate Projected FTM CAFD of at least $175.0 million by the end of 2016. Specifically, the Support Agreement requires our Sponsor to offer us:

| • | from the completion of this offering through the end of 2015, solar projects that have Projected FTM CAFD of at least $75.0 million; and |

| • | during calendar year 2016, solar projects that have Projected FTM CAFD of at least $100.0 million. |

If the amount of Projected FTM CAFD of the projects we acquire under the Support Agreement from the completion of this offering through the end of 2015 is less than $75.0 million, or the amount of Projected FTM CAFD of the projects we acquire under the Support Agreement during 2016 is less than $100.0 million, our Sponsor has agreed that it will continue to offer us sufficient Call Right Projects until the total aggregate Projected FTM CAFD commitment has been satisfied. We have agreed to pay cash for each Call Right Project that we acquire, unless we and our Sponsor otherwise mutually agree to stock consideration. The Support Agreement provides that we will work with our Sponsor to mutually agree on the fair market value of each Call Right Project within a reasonable time after it is added to the list of identified Call Right Projects. If we are unable to agree on the fair market value, we and our Sponsor will engage a third-party advisor to determine the fair market value, after which we will have the right (but not the obligation) to acquire such Call Right Project. Until the price for a Call Right Asset is mutually agreed, including after the determination by a third-party advisor, if applicable, in the event our Sponsor receives a bona fide offer for a Call Right Project from a third party, our Sponsor must give us notice of such offer in reasonable detail and we will have the right to acquire such project on terms substantially similar to those our Sponsor could have obtained from such third party, but at a price no less than the price specified in the third-party offer. After the price for a Call Right Asset has been agreed and until the total aggregate Projected FTM CAFD commitment has been satisfied, our Sponsor may not market, offer or sell that Call Right Asset to any third party without our consent.

The Support Agreement provides that our Sponsor is required to offer us additional qualifying Call Right Projects from its pipeline on a quarterly basis until we have acquired projects under the Support Agreement that have the specified minimum amount of Projected FTM CAFD for each of the periods covered by the Support Agreement. These additional Call Right Projects must satisfy certain criteria. In addition, our Sponsor may remove a project from the Call Right Project list if, in its reasonable discretion, the project is unlikely to be successfully completed, effective upon notice to us. In that case, the Sponsor will be required to replace such project with one or more additional reasonably equivalent projects that have a similar economic profile. Generally, we may exercise our call right with respect to any Call Right Project identified in the Support Agreement at any time until 30 days prior to COD for that Call Right Project. If we exercise our option to purchase a project under the Support Agreement, our Sponsor is required to sell us that project on or about the date of its COD unless we agree to a different date.

In addition, our Sponsor has agreed to grant us a right of first offer on any of the ROFO Projects that it determines to sell or otherwise transfer during the six-year period following the completion of this offering. Under the terms of the Support Agreement, our Sponsor will agree to negotiate with us in good faith, for a period of 30 days, to reach an agreement with respect to any proposed sale of a ROFO Project for which we have exercised our right of first offer before it may sell or otherwise transfer

12

Table of Contents

such ROFO Project to a third party. However, our Sponsor will not be obligated to sell any of the ROFO Projects and, as a result, we do not know when, if ever, any ROFO Projects will be offered to us. In addition, in the event that our Sponsor elects to sell ROFO Projects, it will not be required to accept any offer we make and may choose to sell the assets to a third party or not sell the assets at all.

Under our related party transaction policy, the prior approval of our Corporate Governance and Conflicts Committee will be required for each material transaction with our Sponsor under the Support Agreement. See “—Conflicts of Interest” below.

Management Services Agreement. Pursuant to the Management Services Agreement, our Sponsor will provide or arrange for the provision of operational, management and administrative services to us and our subsidiaries, and we will pay our Sponsor a base management fee as follows: (i) no fee for the remainder of 2014, (ii) 2.5% of Terra LLC’s CAFD in 2015, 2016 and 2017 (not to exceed $4.0 million in 2015 or $7.0 million in 2016 or $9.0 million in 2017), and (iii) an amount equal to our Sponsor’s actual cost for providing services pursuant to the terms of the Management Services Agreement in 2018 and thereafter. We and our Sponsor may agree to adjust the management fee as a result of a change in the scope of services provided under the Management Services Agreement. In addition, in the event that TerraForm Power, Terra LLC, Terra Operating LLC or any of our subsidiaries refers a solar power development project to our Sponsor prior to our Sponsor’s independent identification of such opportunity, and our Sponsor thereafter develops such solar power project, our Sponsor will pay us an amount equal to $40,000 per MW multiplied by the nameplate capacity, determined as of the COD of such solar power project (not to exceed $30.0 million in the aggregate in any calendar year). The prior approval of our Corporate Governance and Conflicts Committee will be required for each material transaction with our Sponsor under the Management Services Agreement unless such transaction is expressly contemplated by the agreement.

Repowering Services ROFR Agreement. Immediately prior to the completion of this offering, TerraForm Power, Terra LLC and Terra Operating LLC, collectively, the “Service Recipients,” will enter into a Repowering Services Agreement with our Sponsor, pursuant to which our Sponsor will be granted a right of first refusal to provide certain services, including (i) repowering operating solar generation projects and providing related services to analyze, design and replace or improve any of the solar power generation projects through the modification of the relevant solar energy system and (ii) such other services as may from time to time reasonably requested by the Service Recipients related to any such repowerings, collectively, the “Repowering Services.”

Interest Payment Agreement. Terra LLC and Terra Operating LLC will enter into the Interest Payment Agreement with our Sponsor, pursuant to which our Sponsor will agree to pay all of the scheduled interest on our new term loan facility, or the “Term Loan,” through 2017, up to an aggregate of million over such period. Our Sponsor will not be obligated to pay any amounts payable under the Term Loan in connection with an acceleration of the indebtedness thereunder. Any amounts payable by our Sponsor under the Interest Payment Agreement that are not remitted when due will remain due (whether on demand or otherwise) and interest will accrue on such overdue amounts at a rate per annum equal to the interest rate then applicable under the Term Loan. In addition, Terra LLC will be entitled to set off any amounts owing by SunEdison pursuant to the Interest Payment Agreement against any and all sums owed by Terra LLC to SunEdison under the distribution provisions of the amended and restated operating agreement of Terra LLC, and Terra LLC may pay such amounts to Terra Operating LLC.

Operating Agreements. Our contributed projects were or are being built pursuant to engineering, procurement and construction, or “EPC,” contracts, and will be operated and maintained

13

Table of Contents

pursuant to operations and maintenance, or “O&M,” contracts with affiliates of our Sponsor. Under the EPC contracts, the relevant Sponsor affiliates provide liquidated damages to cover delays in project completions, as well as market standard warranties, including performance ratio guarantees, designed to ensure the expected level of electricity generation is achieved, for periods that range between two and five years after project completion depending on the relevant market. The O&M contracts cover comprehensive preventive and corrective maintenance services for a fee as defined in such agreement. The applicable Sponsor affiliates also provide generation availability guarantees of 99% for a majority of the projects covered by such O&M Agreements (on a MW basis), designed to ensure the expected level of power plant operation is achieved, and related liquidated damage obligations. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Metrics—Operating Metrics—Generation Availability” for a description of “generation availability.”

Conflicts of Interest. While our relationship with our Sponsor and its subsidiaries is a significant strength, it is also a source of potential conflicts. As discussed above, our Sponsor and its affiliates will provide important services to us, including assisting with our day-to-day management and providing individuals who are dedicated to serve as our executive officers and other key officers. Our management team, including our officers, will remain employed by and, in certain cases, will continue to serve as an executive officer or other senior officer of, SunEdison or its affiliates. Our officers will also generally continue to have economic interests in our Sponsor following this offering. However, pursuant to the Management Services Agreement, our officers will be dedicated to running our business. These same officers may help our board of directors and, in particular, our Corporate Governance and Conflicts Committee evaluate potential acquisition opportunities presented by our Sponsor under the Support Agreement. As a result of their employment by, and economic interest in, our Sponsor, our officers may be conflicted when advising our board or Corporate Governance and Conflicts Committee or otherwise participating in the negotiation or approval of such transactions.

Notwithstanding the significance of the services to be rendered by our Sponsor or its designated affiliates on our behalf in accordance with the terms of the Management Services Agreement or of the assets which we may elect to acquire from our Sponsor in accordance with the terms of the Support Agreement or otherwise, our Sponsor will not owe fiduciary duties to us or our stockholders and will have significant discretion in allocating acquisition opportunities (except with respect to the Call Right Projects and ROFO Projects) to us or to itself or third parties. Under the Management Services Agreement, our Sponsor will not be prohibited from acquiring operating assets of the kind that we seek to acquire. See “Risk Factors—Risks Related to our Relationship with our Sponsor.”

Any material transaction between us and our Sponsor (including the proposed acquisition of any assets pursuant to the Support Agreement) will be subject to our related party transaction policy, which will require prior approval of such transaction by our Corporate Governance and Conflicts Committee. That committee will be comprised of at least three directors, each of whom will satisfy the requirements for independence under applicable laws and regulations of the Securities and Exchange Commission, or the “SEC,” and the rules of the NASDAQ Global Select Market. See “Risk Factors—Risks Related to our Relationship with our Sponsor,” “Certain Relationships and Related Party Transactions—Procedures for Review, Approval and Ratification of Related-Person Transactions; Conflicts of Interest” and “Management—Committees of the Board of Directors—Corporate Governance and Conflicts Committee” for a discussion of the risks associated with our organizational and ownership structure and corporate strategy for mitigating such risks.

14

Table of Contents

Organizational Transactions

Formation Transactions

TerraForm Power, Inc. is a Delaware corporation formed on January 15, 2014 by SunEdison to serve as the issuer of the Class A common stock offered hereby. In connection with the formation of TerraForm Power, certain employees of SunEdison who will perform services for us were granted equity incentive awards under the TerraForm Power, Inc. 2014 Second Amended and Restated Long-Term Incentive Plan, or the “2014 Incentive Plan,” in the form of restricted shares of TerraForm Power. See “Executive Officer Compensation—Equity Incentive Awards.”

TerraForm Power, LLC is a Delaware limited liability company formed on February 14, 2014 as a wholly owned indirect subsidiary of SunEdison to own and operate through its subsidiaries a portfolio of contracted clean power generation assets acquired and to be acquired from SunEdison and unaffiliated third parties. Following its formation and prior to the completion of this offering: (i) SunEdison and its subsidiaries will contribute to Terra LLC the solar energy projects developed by SunEdison that are included in our initial portfolio, which we refer to as the “Initial Asset Transfers,” or “Contributed Projects” and (ii) Terra LLC will complete the acquisitions of the solar energy projects developed by third parties that are included in our initial portfolio, which we refer to as the “Project Acquisitions” or “Acquired Projects.” On March 28, 2014, Terra LLC entered into a new $250.0 million term loan Bridge Facility, or the “Bridge Facility,” to provide funding for the Initial Project Acquisitions. Through an amendment dated May 15, 2014, the size of the term loan bridge facility was increased to $400.0 million.

We collectively refer to these transactions as the “Formation Transactions.”

Offering Transactions

In connection with and, in certain cases, concurrently with the completion of, this offering, based on an assumed initial public offering price of $ per share, which is the midpoint of the range listed on the cover of this prospectus:

| • | we will amend and restate TerraForm Power’s certificate of incorporation to provide for both Class A common stock, Class B common stock and Class B1 common stock (which may be issued upon a reset of IDR target distribution levels or in connection with acquisitions from our Sponsor or third parties), at which time SunEdison’s interest in TerraForm Power‘s common equity will be converted into shares of Class B common stock and interests in Terra LLC (as described below) and the restricted shares issued under the 2014 Incentive Plan will automatically convert into a number of shares of Class A common stock that represent an aggregate % economic interest in TerraForm Power, subject to certain adjustments to prevent dilution; |

| • | we will amend Terra LLC’s operating agreement to provide for Class A units, Class B units and Class B1 units (which may be issued upon a reset of IDR target distribution levels or in connection with acquisitions from our Sponsor or third parties) and to convert our Sponsor’s interest in TerraForm Power’s common equity into Class B units, issue the IDRs to our Sponsor and appoint TerraForm Power as the sole managing member of Terra LLC; |

| • | TerraForm Power will issue shares of its Class A common stock to the purchasers in this offering (or shares if the underwriters exercise in full their option to purchase additional shares of Class A common stock) in exchange for net proceeds of approximately $ million (or approximately $ million if the underwriters exercise in full their option |

15

Table of Contents

| to purchase additional shares of Class A common stock), after deducting underwriting discounts and commissions but before offering expenses (all of which will be paid by SunEdison); |

| • | TerraForm Power will use all of the net proceeds from this offering to purchase newly issued Class A units of Terra LLC, representing % of Terra LLC’s outstanding membership units (or % if the underwriters exercise in full their option to purchase additional shares of Class A common stock); |

| • | Terra LLC will use such proceeds to repay certain project-level indebtedness, to repay a portion of the Bridge Facility (including accrued interest) and to pay fees and expenses associated with the Term Loan and Revolver; we will also use a portion of the proceeds for the acquisition of certain projects through our Sponsor. Any remaining proceeds will be used for general corporate purposes, which may include future acquisitions of solar assets from our Sponsor pursuant to the Support Agreement or from third parties; |

| • | Terra Operating LLC will enter into a new $ million revolving credit facility, or the “Revolver,” which will remain undrawn at the completion of this offering, and the $ million Term Loan to refinance any remaining borrowings under the Bridge Facility; and |

| • | TerraForm Power will enter into various agreements with our Sponsor, including the Support Agreement, the Management Services Agreement, the Repowering Services ROFR Agreement and the Interest Payment Agreement. |

We collectively refer to the foregoing transactions as the “Offering Transactions” and, together with the Formation Transactions, as the “Organizational Transactions.”

Immediately following the completion of this offering:

| • | TerraForm Power will be a holding company and the sole material asset of TerraForm Power will be the Class A units of Terra LLC; |

| • | TerraForm Power will be the sole managing member of Terra LLC and will control the business and affairs of Terra LLC and its subsidiaries; |

| • | TerraForm Power will hold Class A units of Terra LLC representing approximately % of Terra LLC’s total outstanding membership units (or %, if the underwriters exercise in full their option to purchase additional shares of Class A common stock); |

| • | SunEdison, through a wholly owned subsidiary, will own Class B units of Terra LLC representing approximately % of Terra LLC’s total outstanding membership units (or %, if the underwriters exercise in full their option to purchase additional shares of Class A common stock); |

| • | SunEdison or one of its wholly-owned subsidiary, will be the holder of the IDRs; |

| • | SunEdison, through the ownership by a subsidiary of our Class B common stock, will have % of the combined voting power of all of our common stock and, through such subsidiary’s ownership of Class B units of Terra LLC, will hold, subject to the limitation on distributions to holders of Class B units during the Distribution Forbearance Period, approximately % of the economic interest in our business (or % of the combined voting power of our common stock and a % economic interest in our business if the underwriters exercise in full their option to purchase additional shares of Class A common stock); |

| • | the purchasers in this offering will own shares of our Class A common stock, representing % of the combined voting power of all of our common stock and, through our |

16

Table of Contents

| ownership of Class A units of Terra LLC, approximately % of the economic interest in our business (or % of the combined voting power of our common stock and a % economic interest if the underwriters exercise in full their option to purchase additional shares of Class A common stock). |