Attached files

| file | filename |

|---|---|

| EX-31.2 - EX-31.2 - TRULIA, INC. | d729230dex312.htm |

| EX-23.1 - EX-23.1 - TRULIA, INC. | d729230dex231.htm |

| EX-32.1 - EX-32.1 - TRULIA, INC. | d729230dex321.htm |

| EX-31.1 - EX-31.1 - TRULIA, INC. | d729230dex311.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT 1934 |

For the fiscal year ended December 31, 2013

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-35650

Trulia, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 20-2958261 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) |

116 New Montgomery Street, Suite 300

San Francisco, California 94105

(Address of principal executive offices) (Zip Code)

415.648.4358

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Common Stock, par value $0.00001 per share |

The New York Stock Exchange | |

| (Title of each class) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act: Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of voting stock held by non-affiliates of the registrant was $650,347,273, as of the end of the registrant’s second fiscal quarter (based on the closing sales price for the common stock on the New York Stock Exchange on June 28, 2013). Shares of common stock held by each executive officer, director, and holder of 5% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of February 20, 2014, 36,823,070 shares of the registrant’s common stock, $0.00001 par value, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2014 Annual Meeting of stockholders are incorporated by reference in Part III of this Annual Report on Form 10-K where indicated. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended December 31, 2013.

Table of Contents

EXPLANATORY NOTE

Trulia, Inc. (“Trulia” or the “Company”) is filing this Amendment No. 1 on Form 10-K/A (this “Amendment”) to its Annual Report on Form 10-K for the year ended December 31, 2013 (the “Original Form 10-K”) solely for the purpose of correcting a typographical error in Part II, Item 6 – Selected Financial and Other Data. The “Revenue” amount reported for the year ended December 31, 2011 in the table labeled “Statement of Operations Data” of the Original Form 10-K was inadvertently reported as $35,518,000. The correct amount of $38,518,000 has been corrected herein.

In addition, the Company is including in this Amendment currently dated certifications from its Chief Executive Officer and Chief Financial Officer as required by Sections 302 and 906 of the Sarbanes-Oxley Act of 2002 as Exhibits 31.1 and 31.2 and Exhibit 32.1, respectively. The Company is also including in this Amendment a currently dated consent of the Company’s independent registered public accounting firm as Exhibit 23.1.

Except as described above, this Amendment does not modify or update disclosures presented in the Original Form 10-K, nor does it reflect events occurring after the filing of the Original Form 10-K or modify or update those disclosures. Accordingly, this Amendment should be read in conjunction with the Company’s filings with the Securities and Exchange Commission subsequent to the filing of the Original Form 10-K.

Table of Contents

Trulia Inc.

Annual Report on Form 10-K

For the Fiscal Year Ended December 31, 2013

Table of Contents

As used in this Annual Report on Form 10-K, the terms “the Company,” “we,” “us” and “our” refer to Trulia, Inc., unless the context indicates otherwise.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws, which statements involve substantial risks and uncertainties. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans or intentions. Forward-looking statements contained in this Annual Report on Form 10-K include, but are not limited to, statements about:

| • | our future financial performance, including our revenue, cost of revenue, gross profit or gross margin, operating expenses, ability to generate positive cash flow, and ability to achieve and maintain profitability; |

| • | the sufficiency of our cash and cash equivalents to meet our liquidity needs; |

| • | our ability to increase the number of consumers using our website and mobile applications; |

| • | our ability to attract and retain real estate professionals that subscribe to our products; |

| • | our ability to increase revenue from real estate professionals subscribing to our products; |

| • | our ability to attract and retain advertisers that purchase display advertising on our website; |

| • | the continued availability of home listing and other information relevant to the real estate industry; |

| • | the growth in the usage of our mobile applications and our ability to successfully monetize this usage; |

| • | our ability to develop and deploy new features and products and provide a superior user experience; |

| • | our ability to foster the growth of user-generated content; |

| • | our ability to capitalize on strategic and adjacent opportunities; |

| • | our ability to achieve the anticipated benefits of the Market Leader acquisition; |

| • | our ability to effectively integrate acquired businesses, such as Market Leader; |

| • | the effects of the market for real estate and general economic conditions on our business; and |

| • | the attraction and retention of qualified employees and key personnel. |

We caution you that the foregoing list may not contain all of the forward-looking statements made in this Annual Report on Form 10-K.

You should not rely upon forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report on Form 10-K primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations, and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties, and other factors described in the section titled “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. We cannot assure you that the results, events, and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events, or circumstances could differ materially from those described in the forward-looking statements.

1

Table of Contents

The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report on Form 10-K to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions, or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, or investments we may make.

2

Table of Contents

PART I

| Item 1. | Business |

Overview

Trulia is redefining the home search experience for consumers and changing the way that real estate professionals build their businesses. Our marketplace, delivered through the web and mobile applications, gives consumers powerful tools to research homes and neighborhoods and enables real estate professionals to efficiently market their listings and attract new clients. We believe we deliver the best home search experience by combining our superior user interface with our comprehensive database of real estate properties, local insights, and user-generated content. We also offer a comprehensive suite of free and subscription products that provide real estate professionals with access to transaction-ready consumers and help them to grow and manage their online presence. In the year ended December 31, 2013, we had 38.8 million monthly unique visitors. As of December 31, 2013, we had more than 437,000 active real estate professionals in our Trulia marketplace and 157,000 active real estate professionals using our Market Leader software and services. Approximately 59,700 of these real estate professionals were paying subscribers (assuming 20% overlap between Trulia subscribers and Marker Leader’s premium subscribers).

We empower consumers to make more informed housing decisions by delivering unparalleled insights and information on homes, neighborhoods, and real estate professionals through an intuitive and engaging user experience. Our large, continually refreshed, and searchable database contains more than 113.2 million properties, including 4.0 million homes for sale and rent. We supplement listings data with local information on schools, crime, and neighborhood amenities to provide unique insights into each community. In addition, we harness rich, insightful user-generated content from our active community of contributors, which includes consumers, local enthusiasts, and real estate professionals. With more than 11.8 million unique user contributions, we believe we have the largest collection of user-generated content on homes, neighborhoods, and real estate professionals.

We enable real estate professionals to better promote themselves and their listings, connect with transaction-ready consumers and manage ongoing relationships with potential buyers through our online and mobile marketing products, including personalized, customer-branded websites with multiple listing service integration that are optimized to generate consumer response. Our free products allow real estate professionals to build their personal brand by creating an online profile, contributing content to our marketplace, leveraging social media for endorsements, and establishing their presence through mobile features such as “check-ins.” Our subscription products provide a comprehensive end-to-end platform for real estate professionals, enabling them to increase their visibility, promote their listings in search results, target mobile users, generate more highly qualified leads from our large audience of transaction-ready consumers, and effectively manage these leads until a transaction has closed. We further enable real estate professionals to cultivate clients and leverage a library of sales and marketing materials in order to design, create, publish, and manage their own personalized marketing campaigns through our proprietary customer relationship management products. We believe that our consumer audience is highly motivated and ready to purchase homes, as supported by our surveys conducted between January 2013 and December 2013 in which 77% of over 485,000 respondents contacting real estate professionals through our marketplace indicated that they are planning to move in the next six months, and 44% of over 348,000 respondents stated that they are pre-approved for a mortgage. We believe that the combination of our compelling solution with our transaction-ready audience results in a high return on investment for real estate professionals who purchase our subscription products.

We are a leading mobile platform for the home search process and mobile devices are increasingly critical to consumers and real estate professionals. We have introduced iPhone, iPad, Android Phone, Android Tablet and Kindle Fire applications that provide tailored mobile experiences, which has led to rapid growth in the mobile use of our solution. In the year ended December 31, 2013, our aggregate mobile monthly unique visitors were 14.3 million across Trulia and our wholly owned subsidiary Market Leader, Inc., of which Trulia had over 13.0 million mobile monthly unique visitors, an increase of 92% over 2012. Our mobile users are more likely than our web users to contact real estate professionals through our marketplace.

3

Table of Contents

Our online marketplace is experiencing rapid growth. Monthly unique visitors to our marketplace increased to 38.8 million in the year ended December 31, 2013 from 23.1 million in the year ended December 31, 2012, or a 68% increase, and our subscribers increased to approximately 59,700 (assuming a 20% overlap with Market Leader’s premium subscribers) as of December 31, 2013 from 24,443 as of December 31, 2012, a 144% increase. We expect that our efforts to maintain or increase consumer traffic and subscribers are likely to include, among other things, significant increases to our marketing spending and significant expenditures to increase the number of our engineering and product development personnel. For example, we recently announced a national marketing campaign that is designed to attract serious home buyers and sellers to our marketplace and that we expect will enable us to connect even more transaction-ready consumers with real estate professionals.

We generate revenue primarily from sales of subscription products to real estate professionals. We also generate revenue from display advertising sold to leading real estate and consumer brand advertisers seeking to reach our attractive audience. For the years ended December 31, 2013, 2012 and 2011, we generated revenue of $143.7 million, $68.1 million and $38.5 million, respectively. During the same periods, we had net losses of $17.8 million, $10.9 million and $6.2 million, respectively.

Industry and Challenges

The residential real estate industry, which we estimate accounts for more than a trillion dollars in annual spending in the United States, is undergoing a profound transformation. Technology is changing the way that consumers search for homes and the way in which real estate professionals attract clients and build their businesses. In addition, as the U.S. housing market recovers from its recent unprecedented downturn, real estate professionals are seeking more effective ways to market themselves and achieve a greater return on their marketing investment. These trends present significant opportunities to capitalize on shifts in behavior.

Historically, consumers lacked readily available access to detailed and comprehensive information essential to making housing decisions, relying instead on disparate sources of information such as real estate professionals, local newspapers, and word of mouth. Over time, more information has become available online and, as a result, the Internet has become a primary source of research for housing decisions. According to a November 2012 survey by the National Association of Realtors, a trade organization for real estate professionals, 90% of home buyers used the Internet to research homes. Additionally, the use of mobile devices for home searches has become more prevalent. According to a 2012 survey by The Real Estate Book, a real estate website, 52% of respondents reported using a mobile device to look for homes, with 85% of non-users stating that they would consider using a mobile device for their next search.

As consumers increasingly research homes online, real estate professionals are shifting their marketing expenditures online to reach prospective clients. While initially these real estate professionals focused their spending on email, search, and creating websites with listings, now these professionals are increasingly using online real estate marketplaces to generate leads and using technology to manage their businesses.

With technology driving the home search process online, consumers, real estate professionals, and advertisers face distinct challenges. Consumers are challenged to effectively compile and use fragmented information, gain local insights, and obtain information on the go. Real estate professionals are challenged to reach today’s online consumers, target the right leads, manage their businesses while on the go, and optimize their marketing spend. Advertisers are challenged to efficiently reach the right consumers while maximizing the effectiveness of their advertising.

Market Opportunity

We believe that there are significant opportunities to address the challenges faced by consumers, real estate professionals, and advertisers. Borrell Associates, Inc., an advertising research and consulting firm, estimated in a September 2013 industry paper that $27.3 billion would be spent in 2013 on real estate-related marketing in the United States. According to a November 2012 survey by the National Association of Realtors, 90% of home

4

Table of Contents

buyers used the Internet to research homes. However, according to the Borrell Associates report, only 55.8% of the real estate marketing dollars in the United States were projected to be spent online in 2013. We believe that there is a disconnect between where marketing dollars are spent and where consumers research homes. Therefore, we expect that real estate-related marketing spend will continue to migrate online from traditional channels.

The Trulia Marketplace

Our marketplace provides the following key benefits for consumers, real estate professionals, and advertisers:

Key benefits for consumers

| • | Large, continually refreshed, searchable database of homes for sale and rent. We provide consumers with access to a large, continually refreshed, and searchable database of properties. We enable consumers to customize their searches with property-specific filters to obtain up-to-date listings that are rich with property facts, price, and sale data. |

| • | Trusted insights, social recommendations, and proprietary analytics that provide local context. We provide consumers with local insights, critical to a successful home search, not available elsewhere on an easy-to-use and comprehensive basis. These insights include information about schools, crime, neighborhood amenities, and real estate professionals. |

| • | Anytime and anywhere access. Our marketplace is accessible anytime and anywhere on the web and on major mobile platforms. Since the introduction of our first mobile application in 2008, mobile use of our marketplace has grown rapidly. |

Key benefits for real estate professionals

| • | Broad reach to transaction-ready consumers. We provide real estate professionals the ability to connect with our large audience of transaction-ready consumers at scale on the web and through our mobile applications. We believe that a large portion of consumers using Trulia do not use our primary competitors’ websites, and that this enables real estate professionals on Trulia to effectively identify and market themselves to consumers not easily found anywhere else. |

| • | Products that boost presence and deliver high-quality leads. Our free products enable real estate professionals to create and manage an online profile, promote their personal brand with consumers by contributing content to our marketplace, and leverage social media for endorsements. Our subscription products enable real estate professionals to boost their visibility, promote their listings in search results, and generate more high-quality leads from potential home buyers. |

| • | Comprehensive end-to-end software-as-a-service-based marketing services. We provide software-as-a-service customer relationship management (CRM) tools, personalized websites and marketing tools to help our real estate professional customers manage and cultivate prospects. By automating many of the repetitive tasks that are required in order to follow up and communicate with potential clients, these tools allow our customers to focus on transacting their current business while efficiently marketing their services to potential clients, maintaining a pipeline of future business opportunities. |

| • | Anytime and anywhere access to critical information and tools. We offer mobile applications designed specifically for real estate professionals to take their business on the go. Using our mobile applications, real estate professionals can access critical information that they need to conduct their business, including listings details, contacts, driving directions, and local information about neighborhoods. |

| • | Significant return on investment. We believe that our subscription products deliver a high return on investment to real estate professionals. |

5

Table of Contents

Key benefits for advertisers

| • | Attractive audience. We believe our audience is highly attractive to consumer brand advertisers. A substantial portion of our audience is either college educated, has a household income above $75,000, or is in the 25 to 54 age group. U.S. consumers with these characteristics tend to spend more of their annual income on home maintenance, insurance, household furnishings, apparel and services, and entertainment than the average consumer, according to the Bureau of Labor Statistics 2012 Consumer Expenditure Survey, which makes our audience attractive for consumer brand advertisers. |

| • | Display advertising products that efficiently reach target consumers. We enable our advertisers to reach segments of our audience that are attractive to them. Advertisers benefit from improved reach, impact, relevancy, and measurement of their marketing campaigns in our marketplace. |

Our Strengths

We believe that our competitive advantage reflects the following strengths:

| • | Empower customers by delivering unparalleled insights and a superior user experience. We are one of the leading online real estate marketplaces and provide consumers with powerful tools and unique content that together deliver valuable insights into homes, neighborhoods, and real estate professionals. For example, our crime heat maps provide consumers with a view into neighborhood safety and our Facebook integration gives consumers recommendations on real estate professionals from people in their social network. We invest significant resources into technology development and product design to create a superior user interface that provides compelling features and rich functionality for our users. |

| • | Most Comprehensive Platform for Real Estate Professionals. We believe we have the most comprehensive, end-to-end platform for real estate professionals to grow and manage their businesses. We provide innovative lead generation products for real estate professionals to market themselves to consumers and generate new business. We also provide an integrated software platform with powerful analytics though which real estate professionals cultivate these leads and turn them into transactions. Moreover, we provide this comprehensive platform at scale, servicing five of the ten largest brokers and three of the largest real estate franchises in the United States. |

| • | Large, differentiated, transaction-ready audience. Our website and mobile applications have attracted 38.8 million monthly unique visitors in the year ended December 31, 2013 and, based on data from comScore, Inc., a marketing research company, a significant portion of our visitors do not visit our primary competitors’ websites. For instance, according to comScore, during each month in 2013 and 2012, more than 45% and 54%, respectively, of our audience did not visit Zillow.com. We believe that our audience is highly motivated and ready to purchase homes, as supported by our surveys conducted between January 2013 and December 2013 in which 77% of over 485,000 respondents contacting real estate professionals through our marketplace are planning to move in the next six months, and 44% of over 348,000 respondents stated that they are pre-approved for a mortgage. |

| • | Strong mobile monetization. We believe that we are one of the few companies that is monetizing its mobile products at a higher rate than web products. Since we launched our subscription product for mobile devices in May 2012, we have sold this product at prices that yield a higher average monthly revenue per subscriber than our subscription products that are not focused on mobile devices. In addition, our users are more likely to contact real estate professionals through our mobile applications than our website. |

| • | High ROI for real estate professionals. We believe our subscription products provide compelling value and a better return on investment than other marketing channels. On average, during the year ended December 31, 2013 paying subscribers received more than nine times the number of monthly leads compared to real estate professionals who only used our free products. |

| • | Powerful network effects driven by unique content. We benefit from a self-reinforcing network effect that helps build our brand, drives user engagement in our marketplace, and attracts more users to our |

6

Table of Contents

| website and mobile applications. Consumers post questions in our marketplace, attracting real estate professionals who add more content by answering these questions, which in turn attracts more consumers to our marketplace. |

| • | Big data and analytics platform. We employ proprietary advanced analytics and heuristics capabilities to aggregate, filter, and analyze large amounts of data from disparate sources that we have cultivated over the years. Our expertise in handling large amounts of externally-sourced data and combining it with user activity data collected from our marketplace allows us to improve the user experience by developing innovative new tools and new functionality. |

Our Strategy

Our goal is to build the leading online real estate marketplace. We intend to focus on the following key strategies in pursuit of our goal:

| • | Expand our audience and increase user engagement. We intend to grow our large, transaction-ready audience by expanding our marketing efforts to consumers who are in the market and ready to move and by continuing to offer superior products for consumers. We plan to launch a multi-channel marketing campaign in 2014 to drive increases in audience and user engagement. We plan to continuously enhance and refresh our database of homes, partner with third parties to add new and relevant local content, and encourage our users to contribute useful content. We also plan to develop new features and tools that deepen our users’ engagement with our website and mobile applications, and to promote and foster interaction in our vibrant user community. |

| • | Grow the number of real estate professionals in our marketplace. We intend to further penetrate the large base of more than 2.8 million real estate professionals in the United States by communicating the value proposition of our free and subscription products, growing our audience of transaction-ready consumers, and creating additional products. |

| • | Increase revenue. We plan to increase our revenue by selling more subscription and advertising products and by optimizing our pricing. |

| • | Increase brand awareness. We plan to launch a multi-channel marketing campaign in 2014 to drive awareness of our brand, especially among consumers in the market ready to move. We also plan to continue to grow our brand by providing our users with superior and innovative products. |

| • | Pursue strategic opportunities. We plan to pursue acquisitions of complementary businesses and strategic partnerships to help us execute on and accelerate our growth plans. |

| • | Pursue adjacent opportunities. We plan to pursue opportunities in a number of large adjacent markets, such as rentals, mortgages, home improvement, and agent tools, and to expand our business internationally. |

7

Table of Contents

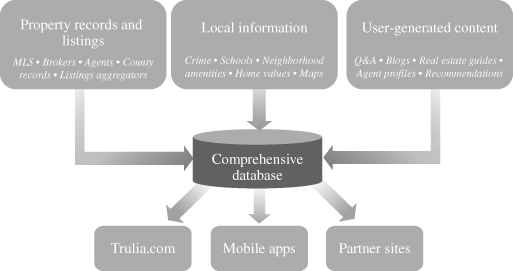

Data

Management of data is a critical component of our solution. We manage over one terabyte of data on a daily basis. For Trulia.com, our Trulia mobile applications and our Trulia partner network, the graphic below illustrates how we organize data as listings data, local information, and user-generated content:

Listings data

We refresh and supplement the Trulia listings database of over 113.2 million properties and for sale and for rent listings with data we receive from thousands of feeds on a daily basis. We receive feeds covering millions of new and existing for sale and for rent listings every day from MLSs, real estate brokerages, real estate agents, real estate listings aggregators, and other third parties. We also obtain detailed ownership and property data from vendors who collect and digitize information from public county records.

We process this wealth of data through our proprietary algorithms and heuristic data validation engine to sort, augment, and select the most up-to-date and accurate data to display. As a next step, we apply our search logic to the data, and overlay additional local information on schools, crime, neighborhood amenities, home values, and other community information. The final product is a complete profile of a property or listing with property facts, price data, local information, and agent contact information, which we publish in our marketplace in an intuitive and engaging user experience.

In addition, for our Market Leader solutions, we process data feeds from approximately 500 multiple listing services to populate the more than 126,000 real estate professional websites we host.

Local information

We inform consumers on what it is like to live in a neighborhood by delivering insights on schools, crime, neighborhood amenities, commute times, home values, historical earthquake, flood and other natural disaster data, and other community information.

| • | Schools. We provide information on schools by district, type, parent reviews, and ratings, which is based on data that we receive from third parties. We overlay this information onto our maps and color code the data points with a sliding color scale to differentiate between schools with low, medium, or high ratings. |

8

Table of Contents

| • | Crime. We receive raw data from third parties about the occurrence, type, location, and description of non-violent and violent crime. We conduct proprietary analysis on the data and aggregate our findings into a tabular format or into our proprietary crime heat map. Our crime heat map provides an overview, visualized through a sliding color scale of the incidence of crime in the area and highlights in callout text boxes the number of violent crimes in the area. |

| • | Enhanced map visualizations of natural disasters. We enable consumers to view historical earthquake and flood data, allowing them to assess the risk of these natural disasters on a block-by-block level. We also provide interactive natural hazard maps pinpointing areas across the United States that are prone to hurricanes, wildfires, and tornadoes. With these maps, users are able to visualize where their dream home is located relative to where natural hazards have hit. Our map visualizations are also fully integrated into our mobile offerings. |

| • | Neighborhood amenities. We provide the location, names, and ratings of nearby restaurants, grocery stores, banks, and gas stations on our maps based on data that we receive from Yelp. |

| • | Home values. Based on our analysis of the sales records and property information in our database, we have developed market- and local-level views of the trends in price, number of sales, and number of listings by property type and location, which we publish on our listings pages and on the Local Info section of our website in interactive chart formats and in our proprietary heat map format. |

| • | Other community information. We analyze data from the U.S. Census Bureau to provide users with information on how the median household and family income, age of homes, and commute times of a neighborhood compare to those of the city. |

Additionally, we have an agreement with Google to use its basic maps, over which we integrate our proprietary insights.

User-generated content

The user-generated data in our marketplace is organized under the Advice section of our website by type of content, questions and answers, blogs, real estate guides, and along topics relevant to our audience such as local information, tips on home buying and selling, and observed market trends. We also allow real estate professionals to publish their own profile and receive recommendations from their clients under the Find an Agent section of our website.

The content in our marketplace is generated by our vibrant community of users. Users can vote on the quality of content using our “thumbs up” or “thumbs down” icons and can follow the voting results. Additionally, users can “flag” inappropriate content on our site, which is escalated to our Trulia community team whose enforcement actions follow the terms and conditions for user-submitted content as published on our website.

Our Products for Consumers

Our products for consumers focus on helping them find the right home. Our consumer products are offered for free and provide a robust set of tools for evaluating where to live.

9

Table of Contents

Searchable database

Search

We maintain one of the largest searchable databases of homes for sale and rent in the United States. Our database includes more than 113.2 million properties with 4.0 million listings of homes for sale and rent. We provide users with the ability to search our database along a variety of parameters as described below:

| All Properties |

Sale properties only |

Rentals only |

Sold properties only | |||

| City Bedrooms Bathrooms Price range Square footage Property type Keyword search |

Open houses Year built Foreclosure type MLS ID |

Pets Amenities |

Time since sale date |

Our users can customize their search along as few or many features as they prefer and by keyword search of specific property attributes. From our search results, users have access to the detailed data on each home in our database, photos of the home, and the for sale or for rent listing information.

Additionally, we enhance our users’ experience by giving them the choice to display their search results in listings or map formats. The map format provides the added functionality of polygonal search, which enables users to delineate the precise area of their searches. We offer products that further enhance our users’ experience with visually impactful maps, graphics, and photos of homes and neighborhood characteristics.

Trulia Estimates

Trulia Estimates is our estimate of an off-market property’s value based on our proprietary analysis of relevant home data such as recent sales of similar homes and property facts. This search function allows users to conduct a precise search by street address to find our estimate of the value of that home. Additionally, home owners may claim their home in our database and edit their home’s specific facts and details so that our proprietary system can revise its estimated value.

Rich insights and content

We provide users with rich insights and content that are critical to a successful home search and that cannot be discovered through home listings data alone. We deliver these insights through the following products:

| • | Local Info. We aggregate local data from a variety of sources and make it more useful to our consumers through Google Maps overlays using our proprietary data visualization tools. These types of local insights include crime heat maps, historical earthquake, flood and other natural disaster data maps, school boundary and performance statistics, local amenity location and reviews through our integration with Yelp, and commute information. |

| • | Advice. We provide our users with insights on homes, neighborhoods, and real estate professionals based on the advice generated by our active community of contributors. Users of our marketplace can post questions and receive answers in the Trulia Voices portion of our website and also scour the collection of advice columns and blogs that other users post. With over 11.8 million unique user contributions and over 1.1 million topics discussed on Trulia Voices, we believe we have amassed the largest online collection of user-generated content in the U.S. residential real estate market. This gives our users access to the insights of consumers, local enthusiasts, and real estate professionals who are knowledgeable about the neighborhoods in which our users are searching. |

| • | Find an Agent. We provide consumers with a directory that includes more than 1.0 million real estate professionals that is searchable by location, name, and type of professional. Our platform integrates |

10

Table of Contents

| with Facebook to leverage the power of social networks for clients to recommend real estate professionals and for real estate professionals to take advantage of online “word of mouth” referrals. For example, a consumer searching for a real estate agent in our marketplace can quickly find whether someone in their social network has recommended an agent in a particular area in which they are looking. |

| • | Value information. Each property detail page features information and analytics on the property value, including price comparisons of similar properties based on median home sale data by neighborhood, zip code and city, price history and trends, and property taxes based on assessed property values. We believe this information helps users better assess the value of the property beyond what can be gleaned from price data alone. |

| • | Mortgage. Given the significant cost of a home purchase, we provide our users with guides on how to finance their purchase, information on mortgage rate trends, and calculators to determine their estimated mortgage payment based on the rates and terms quoted. |

Mobile

Our products are accessible anytime and anywhere online and on mobile devices. We provide the following differentiated Trulia mobile applications for consumers on several major mobile platforms and devices:

| • | m.trulia.com: A mobile-optimized website accessible on mobile device browsers |

| • | Real Estate App: Our full-featured Trulia real estate mobile application, available on iPhone, iPad, Android Phone, Android Tablet and Kindle Fire. |

| • | Rental App: Our mobile application optimized for users looking to rent a home, which is available on iPhone, iPad, Android Phone, Android Tablet and Kindle Fire, and provides a mobile offering customized to the needs of our rapidly growing rentals audience. |

| • | Agents App: Our mobile application optimized for real estate professionals, available on iPhone and Android Phone. |

| • | Mortgage App: Our mobile application optimized for users looking for mortgage information, available on iPhone and iPad. |

Our Products for Real Estate Professionals

We sell three sets of products to real estate professionals on a subscription basis. The first set of products enables real estate professionals to promote themselves to potential buyers or sellers by targeting a local market area. Real estate professionals purchase subscriptions to these products for their desired city or zip code, at a fixed monthly price, for periods ranging from one month to one year, with pricing depending on demand, location, and the percentage of market share purchased or estimated number of leads. These products include:

| • | Trulia Local Ads. Real estate professionals can purchase local advertising on Trulia’s website by zip code or city and by share of a given market. This functionality enables them to enhance their presence in their chosen market and generate more leads. |

| • | Trulia Mobile Ads. Real estate professionals can purchase local advertising on our mobile applications and mobile website by zip code and by share of a given market. This functionality enables them to feature their profile and contact information on search results and listings, thereby enhancing their visibility with transaction-ready consumers. |

| • | Trulia Seller Ads. Real estate professionals can purchase differently priced Trulia Seller Ads packages to generate leads from consumers interested in selling their homes. This functionality enables them to market directly to sellers through a free home value report that features the real estate professional and includes useful valuation information, such as price history and comparable homes sold. |

11

Table of Contents

Our second set of products allows real estate professionals to receive prominent placement of their listings in our search results. Real estate professionals sign up for new subscriptions to this product at a fixed monthly price for periods that generally range from 1 month to 24 months. This set of products includes:

| • | Trulia Pro. Real estate agents can purchase one of three differently priced Trulia Pro packages to enhance their online presence, feature their listings in search results, and interact with potential clients more effectively. Benefits include enhanced lead generation, greater local lead rotation, featured listings, robust property pages, detailed contact information in search results, instant leads via mobile, and integrated recommendations with Facebook. We provide similar products to real estate brokers under the name Premium Listings. |

Our third set of products is our comprehensive software-as-a-service that allows real estate professionals to manage and cultivate clients and potential clients by automating daily tasks and efficiently marketing their services. We charge real estate professionals subscription fees for our software-as-a-service products. We also generate revenue through enterprise marketing agreements with real estate franchise networks. We provide a base level software-as-a-service product to all agents and/or brokerages in these franchise networks in exchange for certain minimum payments from the real estate franchise networks. We also generate revenue through the sale of premium software and marketing products to individual agents, teams and brokerage offices within these real estate franchise networks.

With our software-as-a-service-based marketing products, we offer a bundle of services that may include some or all of the following:

| • | Software-as-a-service, including customer relationship management (CRM) tools, personalized websites, marketing tools, and content designed to help real estate professionals build online relationships with prospective home buyers and sellers. |

| • | Marketplace products that utilize our advertising expertise and leverage our national real estate websites to produce leads in the local neighborhoods where real estate professionals do business. |

| • | Community and training services that enable real estate professionals to share and learn best practices to help them close more business with consumers. |

We also offer real estate professionals a set of free products that allows them to promote themselves and their listings online and to connect with consumers searching to buy or sell homes. Our free products include:

| • | Property listings. We offer real estate professionals the ability to reach a large, transaction-ready audience and the potential to acquire leads by listing their properties in our marketplace for free. |

| • | Mobile application. We have developed an Agent App for the iPhone and Android Phone that enables real estate professionals to manage their businesses anytime and anywhere. |

| • | Agent profile. Agents can create their own profile in our marketplace by posting contact information, photos, and qualifications, and can manage their brand by linking their profile to their activity on our forums and to Facebook. Agent profiles are posted on the Find an Agent section of our website. |

| • | Communities. Through our Trulia Voices forum and our Active Rain network, we enable real estate professionals to promote their presence by allowing them to connect meaningfully with consumers, network with other professionals, follow topics of interest to their audience, receive updates on neighborhoods, and broadcast their thoughts on our blogging platform. |

| • | Recommendations. We have built social search functionality into our Find an Agent database of agent profiles where users can sort agent profiles by number of recommendations. Additionally, real estate professionals can publish their recommendations on their Facebook Wall through integration with Facebook Connect. |

| • | Check-ins. Our real estate professionals can “check-in” on the Trulia mobile agent application to establish their presence at a property. |

12

Table of Contents

| • | Agent training and advice blogs. We publish two blogs, Trulia Pro and Trulia Corporate, written by real estate industry experts with whom we partner to provide tips, advice, and education for buyers, sellers, and renters. |

| • | Tools and widgets. We offer real estate professionals a number of tools and widgets that they can incorporate into their personal websites to display local real estate information such as a slideshow widget to play photos of properties or a widget to broadcast their contributions on Trulia Voices on their blog or website. |

Our Products for Advertisers

We sell display media advertising on a cost-per-impression and cost-per-click basis to national advertisers seeking to reach the large and attractive audience for our online properties and those of our publisher partners. We display their advertisements on our home page and on individual web pages through graphical displays and text links, and help these customers optimize their advertisements’ effectiveness through our robust targeting capabilities. We also offer display media advertising on our mobile website that is optimized for mobile device web browsers.

Seasonality

From time to time, we experience seasonality in subscription revenue and display advertising due to fluctuations in traffic to our website and mobile applications. During the fourth quarter of each year, traffic to our marketplace has historically declined and our revenue has historically grown more slowly than in other quarters or has declined sequentially. Conversely, we typically experience higher growth in traffic and revenue during the spring and summer months, when consumers are more likely to buy new homes. We expect that seasonality will continue to affect traffic in our marketplace, as well as our revenue from subscriptions and advertising.

We rely on advertising to attract consumers to our Market Leader websites and to generate traffic and leads on these websites. As a result, we are subject to seasonal fluctuations in advertising rates and marketing services. Changing consumer behavior at various times throughout the year affects our advertising expenses. We expect that seasonal fluctuations in advertising costs will affect our operating expenses, as well as our operating margins.

Technology and Engineering

Product development and innovation are core pillars of our engineering culture that aims to delight our users and customers with our products. We provide our web and mobile products using a combination of in-house and third-party technology and products.

Big data and proprietary algorithms. We have developed our technology platform to handle data at large scale. On a daily basis, we process several million home listings from thousands of data feeds through our proprietary algorithms and heuristic data validation engine to sort, augment, and select the most up-to-date and accurate data to display.

Infrastructure. We currently manage our www.trulia.com website and mobile applications from four locations. The primary location where we host our production environment, is within a shared data center in Santa Clara, California. We also placed into service a second hosted facility, located in Denver, Colorado in 2013, where we support our production environment and provide redundancy, backup, and load balancing. We use a third hosted facility, located in Oakland, California, for production service backup and for our development environment. Our website and mobile applications are designed to have high availability, from the Internet connectivity providers we choose, to the servers, databases, and networking hardware that we deploy. Our Market Leader operations are hosted in Bellevue, Washington, at co-location facilities in Kent, Washington and at other locations operated by third parties. We design our systems such that the failure of any individual

13

Table of Contents

component is not expected to affect the overall availability of our platform. We also leverage content delivery networks and use other third-party cloud computing services, including map-related and ad serving services, to ensure fast and local access to content. We employ a host of encryption, antivirus, firewall, monitoring, and patch-management technology to protect and maintain our systems.

Innovation. In addition to our new product development efforts, we encourage technological advances by directing a portion of our engineering team’s time towards organized innovation days. Each quarter, our product managers and engineers share ideas and experiments and recruit their peers to join their projects to bring a new concept to life. As progress is shared with the larger group, these new ideas receive additional input and product planning and are frequently the basis of new products and features we offer.

Agile methodology and quality focus. Our software development methodology is agile and promotes teamwork, collaboration, and process adaptability throughout the life cycle of a development project. We believe this methodology yields robust, high quality, efficient, and nimble software development. We also invest heavily in the quality of our technology with robust testing at each stage in our development process.

In June 2012, we entered into a Platform Services Agreement with Move Sales, Inc., or ListHub, which provides us with a substantial portion of the unique listings in our marketplace. This agreement supersedes our prior agreement with ListHub for the provision by ListHub of listings to us. Under the terms of this agreement, ListHub grants to us a nonexclusive license to display listings on our platform and use these listings for the purpose of providing real estate professionals with information relating to lead generation management and advertising products. This agreement contains a 48-month term and renews automatically for additional one year terms unless canceled upon the provision of 90 days prior notice by either party. This agreement is not cancelable by ListHub except in the case of material uncured breach by us or our filing for bankruptcy, insolvency or assignment for the benefit of creditors, or if a receiver is appointed on our behalf.

We maintain our primary technology infrastructure at a facility in Santa Clara, California maintained by Equinix Operating Company, Inc., or Equinix. Equinix provides data center space to us under the terms of a master service agreement. This agreement terminates on the earlier of the date that it is terminated by either party or the last order made under the agreement terminates or expires. This agreement is not cancelable by Equinix except in the case of material uncured breach by us, the suspension by Equinix three or more times during any twelve month period of its services pursuant to the terms of this agreement, our liquidation, cessation to do business or insolvency, or the condemnation of the physical space subject to this agreement.

Marketing

Our principal marketing strategy has been to develop a superior user experience that will drive audience growth and brand recognition. We have not historically spent significantly on marketing programs, but have focused on organic and viral growth driven by our user base. We currently expect that our marketing and product development expenses are likely to significantly increase as we seek to attract additional consumers and real estate professionals to our marketplace. For example, we recently announced plans to launch a multi-channel, national marketing campaign in 2014 to drive awareness of our brand, especially among consumers in the market ready to move. As our consumer audience has grown, real estate professionals have followed consumers to Trulia. We have also grown our brand among real estate professionals and the real estate industry through tradeshow participation, social engagement, and ongoing education via webinars, newsletters, and word of mouth.

14

Table of Contents

In addition, our media outreach programs have been major drivers in growing our brand. We publish a series of blogs and actively use social media to share and spread content on a variety of topics to elevate our brand, including:

| • | Trends in the real estate market. We analyze publicly available data in combination with the rich data and content in our marketplace to create unique and proprietary insights on real estate trends, which we publish on our Trulia Trends blog. Our regularly published blogs and reports include: |

| • | Trulia Price Monitor and Trulia Rent Monitor. Our view on asking home sale and rent prices that is published monthly. |

| • | Housing Barometer. Our view of the state of the housing market that is published monthly. |

| • | Rent vs. Buy. Our analysis comparing the economics of renting versus buying that is published quarterly. |

| • | Metro Movers. Our observations of search trends for homes within the United States that is published quarterly. |

| • | Foreign Buyers. Our report on search trends for homes by people outside the United States that is published semi-annually. |

| • | Consumer Surveys. Our survey of consumers covering topics such as the “American Dream” of homeownership, attitudes about housing, and public policy that is published quarterly. |

These reports are used by, and our Chief Economist is quoted regularly in, major news outlets, including The Wall Street Journal, Bloomberg, The New York Times, Time Magazine, and U.S. News & World Report.

| • | Advice for real estate professionals. Our blogs for real estate professionals, Trulia Pro and Trulia Corporate, written by well-known real estate industry experts with whom we partner, elevate Trulia’s brand awareness amongst the community of real estate professionals. |

| • | Celebrity and luxury homes. Luxe Living is our blog dedicated to the latest developments on celebrity and luxury homes. This blog and its content have been featured on ExtraTV, E! News, US Weekly, The Los Angeles Times, and more. |

We also cultivate our brand awareness through social media channels, such as Facebook and Twitter. We expect that our efforts to maintain or increase consumer traffic and subscribers are likely to include, among other things, significant increases to our marketing spending and significant expenditures to increase the number of our engineering and product development personnel.

Customers

Real estate professionals that pay for our subscription products include:

| • | Agents, who collaborate with consumers, seek leads, and manage transactions; |

| • | Brokers, which recruit, train, and provide core real estate services to agents; and |

| • | National real estate franchisors, which provide real estate services to franchisees to enable the growth of their brand. |

The majority of our real estate professional subscribers are agents. As of December 31, 2013, we had more than 437,000 active real estate professionals in our Trulia marketplace and 157,000 active real estate professionals using our Market Leader software and services. Approximately 59,700 of these real estate professionals were paying subscribers (assuming a 20% overlap between Trulia subscribers and Market Leader’s premium subscribers). A key focus of our sales and marketing activities has been to further penetrate the large

15

Table of Contents

base of more than 2.8 million real estate professionals in the United States. If we are unable to increase the number of total subscribers in our marketplace, our revenue may not grow and our operating results could suffer.

Our advertising solutions are purchased by a diverse cross-section of brand advertisers that operate within the real estate ecosystem, and those that seek to reach our highly educated and affluent audience. In each of the years ended December 31, 2013, 2012, and 2011, the ten largest advertising partners for the respective period accounted for more than 65%, 63%, and 54%, respectively, of our media revenue.

No customer represented 10% or more of total revenue during the years ended December 31, 2013, 2012, and 2011. One customer accounted for 13.0% and 10.4% of our gross accounts receivable as of December 31, 2013 and 2012, respectively

Sales and Customer Support

We have dedicated sales teams that support our marketplace business and our display advertising business.

For our marketplace business, the majority of our sales are made by our inside sales team that sells our subscription products to real estate professionals. Our inside sales teams are located in our Bellevue, San Francisco, and Denver offices and attract new subscribers through a combination of outbound calling and inbound customer requests generated from our website and marketing activities. We also have a field sales team that sells our marketplace products at larger deal sizes to real estate brokers, franchisors, and builders.

For our display advertising business, we maintain a field sales team based in New York, to specifically target large advertising customers in the real estate and related content categories, such as insurance companies, mortgage providers, and home improvement companies, as well as other brand advertisers that seek to reach our audience. Our field sales team develops direct relationships with these advertisers and the agencies that serve them.

We place a high value on providing quality support to our users, marketplace subscribers, and advertisers. Our customer support team, based in Bellevue, San Francisco and Denver, responds to commercial and technical questions from our users and advertisers.

Competition

The markets in which we operate are highly competitive and fragmented. Consumers research homes through a variety of sources. Similarly, real estate professionals use a variety of marketing channels to promote themselves and find clients. Consequently, we face competition from a variety of direct and indirect channels, and we believe we compete favorably.

Competition for consumers

We compete to attract consumers to our websites and mobile applications primarily on the basis of the breadth and quality of listings; user experience; the breadth, depth, and relevance of the insights on homes, neighborhoods, and real estate professionals; brand and reputation; and the quality of mobile products.

Our principal competitors for consumers include:

| • | Print media, including local newspapers, magazines, and home/apartment guide publications; |

| • | Online real estate marketplaces such as Homes.com, MSN Real Estate, Realtor.com, Yahoo! Real Estate, and Zillow.com; |

| • | Online brokerage service providers such as Redfin and ZipRealty; |

| • | MLSs across the United States; |

16

Table of Contents

| • | Full-service real estate brokerage service providers such as Century 21 and Coldwell Banker; |

| • | Online rental listing providers such as ApartmentGuide.com, ApartmentList.com and Rent.com; |

| • | General online classifieds such as Craigslist; |

| • | Search engines such as Bing, Google, and Yahoo!; and |

| • | Websites of real estate brokerages and individual agents. |

Competition for real estate professionals

We compete for a share of real estate professionals’ overall marketing spend with traditional, offline media, and other online marketing channels. We compete primarily on the basis of the size and attractiveness of the consumer audience; quality and measurability of leads; perceived return on investment; effectiveness of marketing and workflow tools; and quality of mobile products.

Our principal competitors for real estate professionals include:

| • | Print media, including local newspapers, magazines, and home/apartment guide publications; |

| • | Other traditional media, including television and radio; |

| • | Other online real estate marketplaces; |

| • | Social networking services such as Facebook and Twitter; |

| • | Search engines such as Bing, Google, and Yahoo!; |

| • | Websites offering display advertising; |

| • | Email marketing software and tools; and |

| • | Providers of customer relationship management (CRM) software for real estate professionals. |

Competition for advertisers

We face competition to attract advertisers to market their products on our website. The basis of competition includes size, demographics, and overall attractiveness of an audience; pricing; and the ability to target desired audience segments.

Intellectual Property

We protect our intellectual property through a combination of trademarks, domain names, copyrights, trade secrets, and patents, as well as contractual provisions and restrictions on access to our proprietary technology.

We registered “Trulia” and the Trulia marker logo as trademarks in the United States and several other jurisdictions. We also hold thirty-six registered trademarks registered in the United States and five trademarks registered in Canada associated with our Market Leader business. We also have filed other trademark applications in the United States and certain other jurisdictions, and will pursue additional trademark registrations to the extent we believe it would be beneficial and cost effective.

We have five patents registered and nine patent applications pending in the United States and internationally, which seek to cover proprietary techniques relevant to our products. We intend to pursue additional patent protection to the extent we believe it would be beneficial and cost effective.

We currently hold the “Trulia.com,” “Marketleader.com,” “Housevalues.com” and “RealEstate.com” Internet domain names and various other related domain names.

17

Table of Contents

In addition to the protection provided by our intellectual property rights, we enter into confidentiality and proprietary rights agreements with our employees, consultants, contractors, and business partners. Our employees and contractors are also subject to invention assignment agreements. We further control the use of our proprietary technology and intellectual property through provisions in both our general and product-specific terms of use on our website.

Litigation or proceedings before the U.S. Patent and Trademark Office or other governmental authorities and administrative bodies in the United States and abroad may be necessary in the future to enforce our intellectual property rights, to protect our patent rights, trade secrets, and domain names and to determine the validity and scope of the proprietary rights of others. Our efforts to enforce or protect our proprietary rights may be ineffective and could result in substantial costs and diversion of resources, which could harm our business and operating results.

Employees

As of December 31, 2013, we had 1,036 employees, with 222 in technology, 710 in sales, marketing, and customer support, and 104 in general and administrative functions. We had 357 full-time employees in our San Francisco headquarters, 288 in our Denver location, 31 in our New York office, 349 in our Bellevue office and 11 of our employees work remotely. None of our employees is represented by a labor union with respect to his or her employment with us.

Additional Information

Trulia, Inc. was incorporated in Delaware in June 2005. Our principal executive offices are located at 116 New Montgomery Street, Suite 300, San Francisco, California 94105, and our telephone number is (415) 648-4358. Our website address is www.trulia.com. In addition, we maintain a Facebook page at www.facebook.com/trulia and a Twitter feed at www.twitter.com/trulia. Information contained on, or that can be accessed through, our website, Facebook page or Twitter feed does not constitute part of this Annual Report on Form 10-K.

Copies of annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) are available, free of charge, on our website as soon as reasonably practicable after we file such material electronically with or furnish it to the Securities and Exchange Commission (“SEC”). The SEC also maintains a website that contains our SEC filings. The address of the site is www.sec.gov.

18

Table of Contents

| Item 1A. | Risk Factors |

RISK FACTORS

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this Annual Report on Form 10-K, before making a decision to invest in our common stock. If any of the risks actually occur, our business, financial condition, operating results, and prospects could be materially and adversely affected. In that event, the trading price of our common stock could decline, and you could lose part or all of your investment.

We have a limited operating history in an evolving industry, which makes it difficult to evaluate our future prospects and may increase the risk that we will not be successful.

We have a limited operating history in an evolving industry that may not develop as expected. Assessing our business and future prospects is challenging in light of the risks and difficulties we may encounter. These risks and difficulties include our ability to:

| • | increase the number of consumers using our websites and mobile applications; |

| • | continue to obtain home listing information, as well as information on schools, crime, commute times, neighborhood amenities, rental prices and historical earthquake and flood data; |

| • | increase the number of real estate professionals subscribing to our products; |

| • | increase the revenue from real estate professionals subscribing to our products; |

| • | increase the revenue from advertisers on our websites; |

| • | successfully develop and deploy new features and products; |

| • | encourage and foster the growth of user-generated content; |

| • | increase our brand awareness among consumers and real estate professionals; |

| • | successfully compete with other companies that are currently in, or may in the future enter, the business of providing residential real estate information online and on mobile applications, as well as with companies that provide this information offline; |

| • | successfully compete with existing and future providers of other forms of offline, online, and mobile advertising; |

| • | successfully compete with existing and future providers of customer relationship management (CRM) tools and other solutions that help real estate professionals manage and grow their businesses; |

| • | successfully navigate fluctuations in the real estate market; |

| • | effectively manage the growth of our business; |

| • | successfully expand our business into adjacent markets, such as rentals, mortgages, and home improvement; |

| • | successfully integrate companies we may acquire or have acquired, including Market Leader; and |

| • | successfully expand internationally. |

If the demand for residential real estate information online does not develop as we expect, or if we fail to address the needs of consumers, real estate professionals, or advertisers, our business will be harmed. We may not be able to successfully address these risks and difficulties, which could harm our business and cause our operating results to suffer.

19

Table of Contents

We have a history of losses and we may not achieve or maintain profitability in the future.

We have not been profitable on a quarterly or annual basis since we were founded, and as of December 31, 2013, we had an accumulated deficit of $64.9 million. We expect to make significant future investments in the development and expansion of our business which may not result in increased revenue or growth. In addition, as a public company, we have incurred and expect that we will continue to incur significant legal, accounting, and other expenses that we did not incur as a private company. As a result of these increased expenditures, we must generate and sustain increased revenue to achieve and maintain future profitability. While our revenue has grown in recent periods, this growth may not be sustainable and we may not achieve sufficient revenue to achieve or maintain profitability. We may incur significant losses in the future for a number of reasons, including slowing demand for our products, a decrease in the growth rate of our monthly unique visitors, increasing competition, weakness in the residential real estate market, our inability to effectively integrate acquired businesses, such as Market Leader, as well as other risks described in this Annual Report on Form 10-K, and we may encounter unforeseen expenses, difficulties, complications and delays, and other unknown factors. Accordingly, we may not be able to achieve or maintain profitability and we may continue to incur significant losses in the future, and this could cause the price of our common stock to decline.

If real estate professionals do not continue to subscribe to our products, or we are unable to attract new subscribers, our business and operating results would be harmed.

We rely primarily on subscriptions purchased by real estate professionals to generate a substantial portion of our marketplace revenue. Marketplace revenue accounted for 79%, 70% and 61% of our revenue in the years ended December 31, 2013, 2012 and 2011, respectively. We generally offer subscriptions for periods between one month to 24 months, with most real estate professionals preferring to subscribe for periods shorter than 12 months. Our ability to attract and retain real estate professionals as subscribers, and to generate subscription revenue, depends on a number of factors, including:

| • | our ability to attract transaction-ready consumers to our websites and mobile applications; |

| • | the number of unique visitors using our websites and mobile applications; |

| • | the quality of the leads that we provide to our subscribers; |

| • | the number of leads that we provide to our subscribers; |

| • | the rate of adoption of our software-as-a-service based products; |

| • | the success of our marketing relationships with leading national real estate franchise networks; |

| • | the success of our efforts to upsell customers from promotional offers to higher revenue services; |

| • | the success of any increased marketing and product development efforts directed at attracting additional consumers and real estate professionals to our marketplace; |

| • | the strength of the real estate market; |

| • | the competition for real estate professionals’ marketing dollars; and |

| • | the strength of our brand. |

A key focus of our sales and marketing activities has been to further penetrate the large base of more than 2.8 million real estate professionals in the United States. As of December 31, 2013, we had more than 437,000 active real estate professionals in our Trulia marketplace and 157,000 active real estate professionals using our Market Leader software and services. Approximately 59,700 of these real estate professionals were paying subscribers (assuming a 20% overlap between Trulia subscribers and Market Leader’s premium subscribers). We spend a considerable portion of our operating expenses on sales and marketing activities. Our sales and marketing expenses were our largest operating expenses in the years ended December 31, 2013 and 2012. Sales and marketing expenses reflect many of the costs that we incur in acquiring new subscribers and retaining

20

Table of Contents

existing subscribers, and we expect that sales and marketing expenses will continue to significantly increase in absolute dollars as we seek to grow the number of subscribers in our marketplace. If we are unable to increase the number of total subscribers in our marketplace, our revenue may not grow and our operating results could suffer.

Real estate professionals may not continue to subscribe with us if we do not deliver a strong return on their investment in subscriptions, and we may not be able to replace them with new subscribers. In addition, real estate professionals associated with our real estate franchise network partners may choose not to use our premium services if they are unable to convert leads we provide into closed sales, resulting in a loss of incremental revenue associated with our premium services. In addition, real estate professionals sometimes do not renew their subscriptions with us because of dissatisfaction with our products. This may occur for a number of reasons, including because we have made changes to our products or services, which we do periodically. If subscribers do not renew their subscriptions with us with the same or higher subscription fees, or at all, or if we are unable to attract new subscribers, our business and operating results would be harmed.

Further, although a majority of our revenue in the years ended December 31, 2013 and 2012 was generated from subscriptions purchased by real estate professionals, we cannot be certain that subscribers will renew their subscriptions with us and that we will be able to achieve the same or higher amounts of subscription revenue in the future.

Our ability to increase the number of subscribers to our services also depends, to some degree, on whether we can increase the inventory of marketing products and services available for us to sell in different geographic markets. If we are unable to create additional inventory by offering new services or reconfiguring our existing services, we may not be able to grow the number of subscribers to our services quickly or at all. Even if we are able to offer new services or reconfigure our existing services, there is no guarantee that new subscribers will purchase them or existing subscribers will be satisfied with the changes we make. For instance, in March 2013 we initiated an inventory expansion program of offering additional advertising slots on our real estate listing detail pages to feature more than one subscriber. While this allowed us to sell additional subscriptions in a given location, some existing subscribers did not like the change and elected not to renew their subscriptions.