Attached files

| file | filename |

|---|---|

| 8-K - 8-K - BERKSHIRE HILLS BANCORP INC | a14-13101_18k.htm |

Exhibit 99.1

|

|

SunTrust Robinson Humphrey Financial Services Unconference May 21, 2014 |

|

|

Who We Are Full Service Regional Bank with a distinctive brand and culture, strong middle market opportunities and a solid foundation for growth Assets: $6.0 billion Loans: $4.2 billion Deposits: $4.2 billion Wealth AUM: $1.3 billion Annualized Revenue: $230 million Branches: 90 plus lending offices Footprint: New England and Central New York Market Capitalization: $600 million NYSE: BHLB 1 |

|

|

Q1 Results Summary Solid growth in revenues and core earnings (Q/Q) 7% net interest income growth 14% fee income growth 5% core EPS growth Integration of 20 acquired Central New York branches Added $440 million in deposits 60,000 new customers Ongoing loan growth 9% annualized commercial loan growth 11% annualized consumer loan growth 2 Note: Core EPS $0.42 in Q1 2014 vs. $0.40 in Q4 2013. GAAP EPS ($0.04) in Q1 2014 vs. $0.42 in Q4 2013 including impact of acquisition related charges and other net non-core items |

|

|

Current Initiatives Organic Revenue Growth Loans Commercial Emphasis Fee Income Pricing and Cross Sale Profitability Margin Expense Management Building for the Future Balance Sheet Positioning Capital Management 3 |

|

|

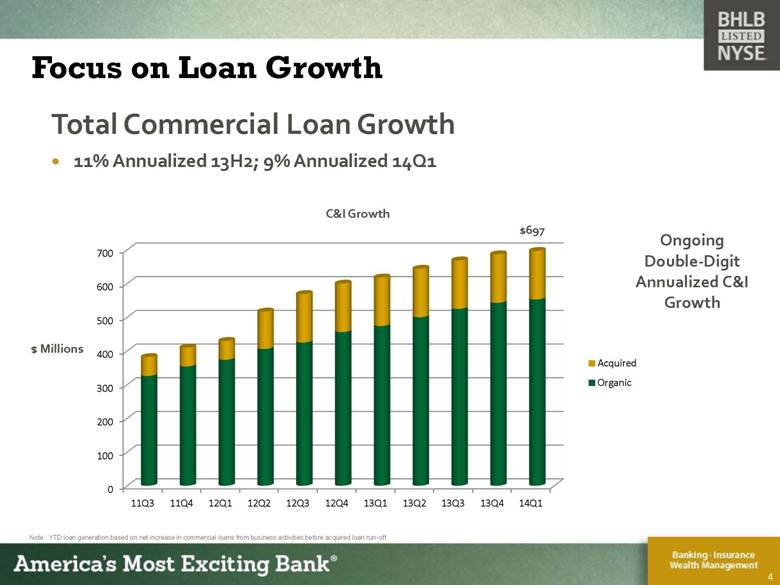

Focus on Loan Growth Total Commercial Loan Growth 11% Annualized 13H2; 9% Annualized 14Q1 $697 $ Millions Ongoing Double-Digit Annualized C&I Growth Note: YTD loan generation based on net increase in commercial loans from business activities before acquired loan run-off C&I Growth 4 700 600 500 400 300 200 100 0 11Q3 11Q4 12Q1 12Q3 12Q4 13Q1 13Q2 13Q3 13Q4 14Q1 Acquired Organic |

|

|

Focus on Loan Growth $ Millions 16% 15% 11% 10% Double Digit Annualized Loan Growth Note: First half of 2013 balances declined due to portfolio repositioning Multiple regions Leveraging deal flow from team recruitment Expanded cross sales across footprint Expanded specialty lending 5 1500 1300 1100 900 700 500 CRE C&I Consumer Mortgage 2Q13 3Q13 4Q13 1Q14 |

|

|

Focus on Loan Growth Success with recruited commercial lending teams in middle-market space driving growth Key Characteristics Established, well respected teams formerly attached to large banks focused outside of our regions Solid relationships within community Breakeven within first year Teams producing solid results 6 Albany Team ABL Team Contral MA Team Hartford Team Syracuse Team Eastern MA Team Leasing Team Albany Leader |

|

|

Focus on Loan Growth 7 Building the Retail Lending Platform Mortgage Consumer Lending Restructured Adding origination capacity Footprint opportunities Fee and portfolio focus Insurance and other cross-sales Auto loan growth Expanded footprint Managed by Syracuse team Cross-sell campaign to portfolio Increasing direct sales |

|

|

Focus on Fee Income Growth Emphasis on building fee income and enhancing cross-sell initiatives 60% growth FY13 19% growth FY13 Re-engineered across footprint New cross sell initiatives launched 18% growth FY13 New leadership and geographic reach 8 Wealth Management Retail Products Commercial Products Small Business Insurance Mortgage Banking |

|

|

Focus on Profitability Improved net interest margin in Q1- benefited from acquired deposits and active balance sheet management 3.35% margin 3.24% margin before purchased loan accretion 17 bp reduction in cost of funds; 7 bp reduction in cost of deposits 5% organic personal DDA growth Ongoing benefits from expense restructuring 5 branches consolidated in FY13; 4 branches in Q114 11% reduction in comp and occupancy - Q4 Y/Y Q1 expense growth includes branch acquisition and seasonal factors Balancing expense management with revenue initiatives Team recruitment De novo branches – Loudonville, NY in Q1 9 |

|

|

Building for the Future Q2 Outlook 11 Core EPS stable or improving Target $0.42 or better GAAP EPS target the same Organic revenue drivers offsetting accretion runoff Commercial and consumer loan growth focus Volume growth vs. margin impacts Lower purchased loan accretion Loan yield management Fee income business lines Expense discipline Hold at current core expense levels |

|

|

Why Invest in Us Strong financial condition Diversified revenue drivers Established footprint in attractive markets Experienced leadership team AMEB culture Well positioned for growth Focused on long-term profitability goals and shareholder value 12 |

|

|

Appendix 13 |

|

|

Forward Looking Statements. This document contains certain forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. These statements include statements about anticipated financial results. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include words like "believe," "expect," "anticipate," "estimate," and "intend" or future or conditional verbs such as "will," "would," "should," "could" or "may.“ There are several factors that could cause actual results to differ significantly from expectations described in the forward-looking statements. For a discussion of such factors, please see Berkshire’s most recent reports on Forms 10-K and 10-Q filed with the Securities and Exchange Commission and available on the SEC's website at www.sec.gov. Berkshire does not undertake any obligation to update forward-looking statements made in this document. NON-GAAP FINANCIAL MEASURES. This presentation references non-GAAP financial measures incorporating tangible equity and related measures, and core earnings excluding merger and other non-recurring costs. These measures are commonly used by investors in evaluating business combinations and financial condition. GAAP earnings are lower than core earnings primarily due to non-recurring merger and systems conversion related expenses. Reconciliations are in earnings releases at www.berkshirebank.com. 14 |

|

|

Financial Performance & Goals 2010 2011 2012 2013 Financial Goals Core revenue growth 9% 31% 40% 13% 7 - 10%+ ann Net interest margin 3.28% 3.57% 3.62% 3.63% 3.30%+ Fee income/revenue 28% 24% 26% 22% 25%+ Efficiency ratio 71% 63% 59% 61% < 60% Core ROA 0.51% 0.80% 0.98% 0.88% 1%+ Core ROE 3.6% 5.8% 7.5% 6.9% 10%+ Core ROTE 7.6% 11.3% 13.8% 12.4% 15%+ Core EPS $1.00 $1.54 $1.98 $1.87 10%+ann growth Dividends/share $0.64 $0.65 $0.69 $0.72 Competitive yield Tangible BV per share $15.22 $15.53 $15.63 $16.27 5%+ ann growth Note: Core results exclude merger, divestiture, systems conversion, accounting correction and restructuring net charges after tax totaling $0.4 million in 2010, $10.4 million in 2011, $11.1 million in 2012 and $5.6million in 2013. GAAP EPS for those periods was $0.98, $0.97, $1.49 and $1.65 respectively. Core ROTE includes after-tax amortization of intangible assets in core return. Book value per share was $27.52, $26.09, $26.53 and $27.08 for the above respective periods. Financial goals are future run-rate targeted in stages over the medium term. 15 |

|

|

Non-Gaap Reconciliation Note: See footnote on page 16 for description of non-core items 16 (Dollars in thousands) 2010 2011 2012 2013 Net income 13,615 $ 17,348 $ 33,188 $ 41,143 $ Non-core revenue (net) - (2,113) (1,485) (6,045) Non-core expense (net) 447 19,928 18,019 15,348 Income taxes (87) (6,547) (6,114) (3,750) Net (income) loss from discontinued operations - (914) 637 - Total core income (A) 13,975 $ 27,714 $ 44,245 $ 46,696 $ Amortization of intangible assets (after tax) 1,813 $ 2,542 $ 3,203 $ 3,161 $ Total core tangible income (B) 15,788 $ 30,256 $ 47,448 $ 49,857 $ Total non-interest income 29,751 $ 35,803 $ 54,056 $ 58,232 $ Non-core revenue (net) - (2,113) (1,485) (6,045) Net interest income 76,947 106,520 143,388 168,752 Total core revenue 106,698 $ 140,210 $ 195,959 $ 220,939 $ Total non-interest expense 82,137 $ 116,442 $ 140,806 $ 157,359 $ Less: Non-core expense (net) (447) (19,928) (18,019) (15,348) Core non-interest expense 81,690 96,514 122,787 142,011 (Dollars in millions, except per share data) Total average assets (C) 2,743 $ 3,484 $ 4,532 $ 5,306 $ Total average equity (D) 383 $ 476 $ 586 $ 675 $ Total average intangible assets 174 207 242 272 Total average tangible equity (E) 209 $ 269 $ 344 $ 403 $ Total stockholders' equity, period-end 387 $ 552 $ 667 $ 678 $ Less: Intangible assets, period-end (173) (223) (274) (271) Total tangible stockholders' equity, period-end (F) 214 $ 329 $ 393 $ 407 $ Total shares outstanding, period-end ( thousands ) (G) 14,076 21,148 25,148 25,036 Average diluted shares outstanding ( thousands ) (H) 13,896 17,952 22,329 24,965 Core earnings per common share, diluted (A/H) 1.00 $ 1.54 $ 1.98 $ 1.87 $ Tangible book value per share, period-end (F/G) 15.22 $ 15.53 $ 15.63 $ 16.27 $ Core return on assets (A/C) 0.51 % 0.80 % 0.98 % 0.88 % Core return on equity (A/D) 3.65 5.76 7.52 6.92 Core return on tangible equity (B/E) 7.57 11.27 13.77 12.37 |

|

|

Notes: 17 |

|

|

Notes: 18 |

|

|

Notes: 19 |

|

|

If you have any questions, please contact: Allison O’Rourke 99 North Street Pittsfield, MA 01202 Investor Relations Officer (413) 236-3149 aorourke@berkshirebank.com |