Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Apollo Global Management, Inc. | d729996d8k.htm |

Investor Presentation

May 2014

Exhibit 99.1

Confidential – Not for distribution, in whole or in part, without the express

written consent of Apollo Global Management, LLC. Information contained

herein is as of March 31, 2014 unless otherwise noted |

Important

Notes

Regarding

the

Use

of

Index

Comparison:

Legal Disclaimer

1

This presentation is confidential and may not be distributed, transmitted or

otherwise communicated to others, in whole or in part, without the express consent of Apollo Global Management, LLC or any of its affiliates

(“Apollo”). This presentation does not constitute an offer to

sell, or the solicitation of an offer to buy, any security, product or service, including interests in the private investment funds discussed herein. The information

contained in this presentation may change at any time without notice and Apollo

does not have any responsibility to update the presentation to account for such change.

Apollo makes no representation or warranty, expressed or implied, with respect

to the accuracy, reasonableness, or completeness of any of the information contained herein, including, but not limited to, information obtained

from third parties. The information contained herein is not intended to provide,

and should not be relied upon for, accounting, legal or tax advice or investment recommendations.

Certain information contained herein may be “forward-looking” in

nature. Due to various risks and uncertainties, actual events or results or the actual performance of a Fund may differ materially from those reflected or

contemplated in such forward-looking information. As such, undue reliance

should not be placed on such information. Forward-looking statements may be identified by the use of terminology including, but not limited to,

“may,” “will,” “should,” “expect,”

“anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof or other variations thereon or comparable terminology.

“Assets Under Management,” or “AUM,” refers to the

investments we manage or with respect to which we have control, including capital we have the right to call from our investors pursuant to their capital commitments to

various funds. Our AUM equals the sum of: (i) the fair value of our private

equity investments plus the capital that we are entitled to call from our investors pursuant to the terms of their capital commitments; (ii) the net asset

value of our credit funds, other than certain collateralized loan obligations

and collateralized debt obligations, which have a fee generating basis other than mark-to-market value of the underlying assets, plus used or available

leverage and/or capital commitments; (iii) the gross asset values or net asset

values of our real estate entities and the structured portfolio vehicle investments included within the funds we manage, which includes the leverage used

by such structured portfolio vehicles; (iv) the incremental value associated

with the reinsurance investments of the portfolio company assets that we manage; and (v) the fair value of any other investments that we manage plus

unused credit facilities, including capital commitments for investments that may

require pre-qualification before investment plus any other capital commitments available for investment that are not otherwise included in the

clauses above. Our AUM measure includes Assets Under Management for which we

charge either no or nominal fees. Our definition of AUM is not based on any definition of Assets Under Management contained in our

operating agreement or in any of our Apollo fund management agreements. We

consider multiple factors for determining what should be included in our definition of AUM. Such factors include but are not limited to (1) our

ability to influence the investment decisions for existing and available assets;

(2) our ability to generate income from the underlying assets in our funds; and (3) the AUM measures that we use internally or believe are used by

other investment managers. Given the differences in the investment strategies

and structures among other alternative investment managers, our calculation of AUM may differ from the calculations employed by other investment

managers and, as a result, this measure may not be directly comparable to

similar measures presented by other investment managers.

Index performance and yield data are shown for illustrative purposes only and

have limitations when used for comparison or for other purposes due to, among

other matters, volatility, credit or other factors (such as number and types of

securities). It may not be possible to directly invest in one or more of these indices and the holdings of any fund managed by Apollo may differ

markedly from the holdings of any such index in terms of levels of

diversification, types of securities or assets represented and other significant factors. Indices are unmanaged, do not charge any fees or expenses, assume

reinvestment of income and do not employ special investment techniques such as

leveraging or short selling. No such index is indicative of the future results of any fund managed by Apollo.

Past performance is not indicative nor a guarantee of future returns. |

This presentation may contain forward looking statements that are within the

meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements include,

but are not limited to, discussions related to Apollo’s expectations

regarding the performance of its business, its liquidity and capital resources and other non-historical statements. These forward-looking statements are

based on management’s beliefs, as well as assumptions made by, and

information currently available to, management. When used in this presentation, the words “believe,” “anticipate,” “estimate,” “expect,” “intend”

and similar expressions are intended to identify forward-looking statements.

Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that

these expectations will prove to have been correct. These statements are subject

to certain risks, uncertainties and assumptions. We believe these factors include but are not limited to those described under the section entitled

“Risk Factors” in the Company’s Annual Report on Form 10-K

for the fiscal year ended December 31, 2013 and Quarterly Report on Form 10-Q for the three months ended March 31, 2014, each as filed with the

Securities and Exchange Commission (“SEC”), as such factors may be

updated from time to time in our periodic filings with the SEC, which are accessible on the SEC’s website as www.sec.gov. These factors should

not be construed as exhaustive and should be read in conjunction with the other

cautionary statements that are included in this presentation and in other SEC filings. We undertake no obligation to publicly update or

review any forward-looking statements, whether as a result of new

information, future developments or otherwise. Information contained herein may include information with respect to prior

investment performance of one or more Apollo funds or investments including gross and/or net internal rates of return (“IRR”). Information

with respect to prior performance, while a useful tool in evaluating

Apollo’s investment activities, is not necessarily indicative of actual results that may be achieved for unrealized investments. “Gross IRR” of a private

equity fund represents the cumulative investment-related cash flows for all

of the investors in the fund on the basis of the actual timing of investment inflows and outflows (for unrealized investment assuming disposition of

the respective “as of” dates referenced) aggregated on a gross basis

quarterly, and the return is annualized and compounded before management fees, carried interest and certain other fund expenses (including interest

incurred by the fund itself) and measures the returns on the fund’s

investments as a whole without regard to whether all of the returns would, if distributed, be payable to the fund’s investors. “Net IRR” of a private

equity fund means the gross IRR applicable to all investors, including related

parties which may not pay fees, net of management fees, organizational expenses, transaction costs, and certain other fund expenses (including

interest incurred by the fund itself); the realized and estimated unrealized

value is adjusted such that a percentage up to 20.0% of the unrealized gain is allocated to the general partner, thereby reducing the balance

attributable to fund investors’ carried interest all offset to the extent

of interest income, and measures returns based on amounts that, if distributed, would be paid to investors of the fund, to the extent that a private equity

fund exceeds all requirements detailed within the applicable fund agreement.

This presentation is for informational purposes only and does not constitute an

offer to sell, or the solicitation of an offer to buy, any security, product, service of Apollo including any Apollo sponsored investment fund,

whether an existing or contemplated fund, for which an offer can be made only by

such fund’s Confidential Private Placement Memorandum and in compliance with applicable law.

Unless otherwise noted, information included herein is presented as of the dates

indicated. The information contained herein may change at any time without notice. Apollo does not have any responsibility to update the

presentation to account for such changes.

Apollo makes no representation or warranty, express or implied, with respect to

the accuracy, reasonableness or completeness of any of the information contained herein, including, but not limited to, information obtained

from third parties.

The information contained herein is not intended to provide, and should not be

relied upon for, accounting, legal or tax advice or investment recommendations.

Forward Looking Statements and Other Important Disclosures

2 |

Agenda

Topic

1)

Apollo Overview

2)

Segment update

3)

Financial Overview

4) Appendix

3 |

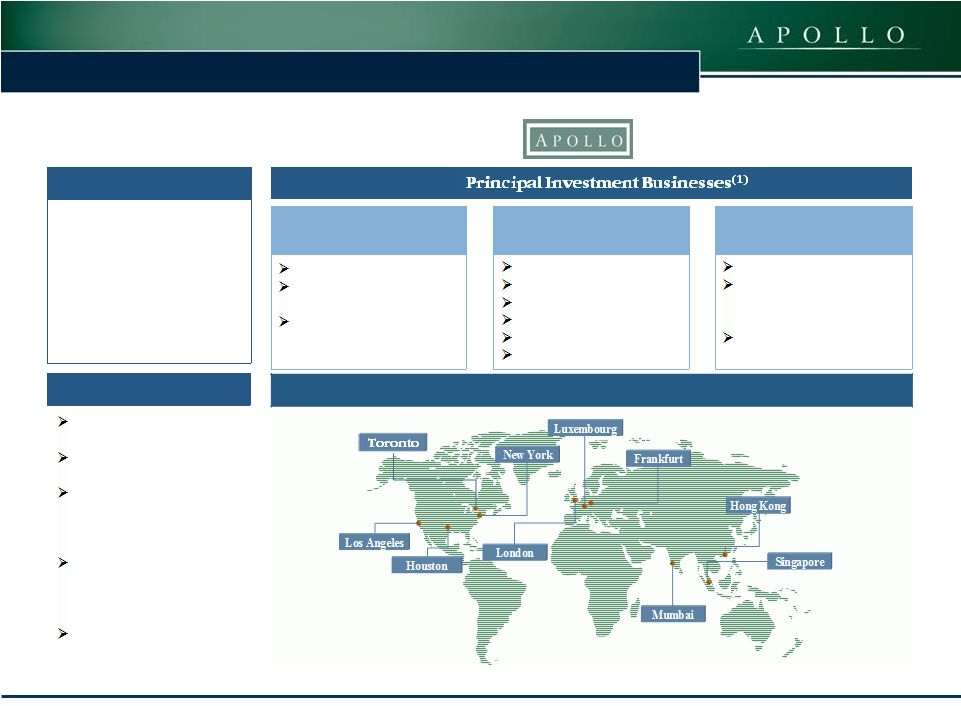

Firm Profile

Founded:

1990

AUM:

$159bn

Employees:

761

Invs. Prof.:

Global offices:

Key Attributes

Value-oriented

Contrarian

Opportunistic across

market cycles and capital

structures

Integrated platform across

asset classes and

geographies

Deep industry knowledge

Private Equity

$48bn AUM

Opportunistic buyouts

Distressed buyouts and

debt investments

Corporate carve-outs

1.

As of March 31, 2014.

Real Estate

$9bn AUM

Residential & Commercial

Global private equity and

distressed debt

investments

Performing fixed income

(CMBS, CRE loans)

Apollo Global Management Overview

Credit

$101bn AUM

U.S. Performing Credit

Opportunistic Credit

European Credit

Non-performing Loans

Structured Credit

Athene

302

Global Footprint

10

4 |

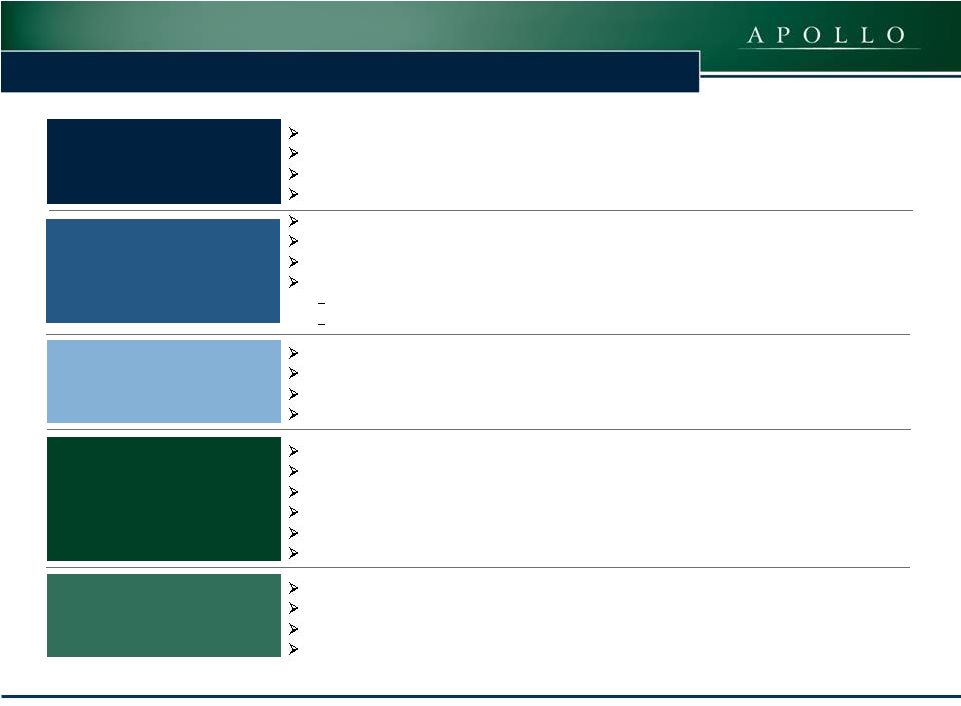

Apollo’s Key Strengths

Diverse and integrated

platform

Strong management

talent

Global fundraising and

originating capability

Strong, consistent

returns through cycles

Attractive financial

profile

Large, diversified, and scalable integrated platform spanning several asset

classes and geographies $159bn of AUM across private equity, credit, real

estate, and permanent capital vehicles 125+

funds

and

managed

accounts

across

multiple

asset

classes

(1)

Deep industry knowledge

5

Multi-disciplined

and

dedicated

fundraising

team

–

PE

Fund

VIII

closed

with

$18.4bn

in

commitments

Diverse global investor base, including marquee LPs

Ability to fundraise and launch funds through the various economic cycles

Long-term

and

diversified

capital

base

(Athene,

PE,

managed

accounts,

etc)

Steady underlying level of fee income

Significant backlog of PE realizations

Variable compensation structure

Significant free cash flow generation

Ample liquidity

Debt / Fee-related EBITDA + 100% net realized carry ratio ~0.4x

Value-oriented, contrarian investor with superior returns

Successful

investment

track

record

across

economic

cycles

–

Firm

for

all

seasons

Apollo PE gross IRR of 39% and net IRR of 26%

Strong credit performance across asset classes

Managing partners worked together for more than 24 years

Collectively own >50% of the Company

Deep bench of investment professionals with strong alignment of interests with

investors Robust governance structure

Note: As of March 31, 2014.

1.

Fund

count

includes

only

those

greater

than

$100mm.

96% of total AUM in funds with contractual life of 7 years or more at

inception 7% of total AUM in permanent capital vehicles with unlimited

duration |

Apollo’s Integrated Business Model

6

Packaging

Chemicals

Cable

Leisure

Natural Resources

Development of industry insight

through:

Industry Insights

Management Relationships

Investment Opportunities

Credit

Investment Opportunities

Market Insights

Market Relationships

Private

Equity

Real

Estate

Over 300 current and former

portfolio companies

Strategic relationships with

industry executives

Significant relationships at

CEO, CFO and board level

Note: The listed companies are a sample of Apollo private equity and

credit investments. The list was compiled based on non-performance criteria and is not representative of all transactions of a given type or investment of any Apollo fund

generally, and are solely intended to be illustrative of the type of investments

across certain core industries that may be made by the Apollo funds. There can be no guarantees that any similar investment opportunities will be available or pursued by

Apollo in the future. The list contains companies which are not currently held

in any Apollo portfolio. Natural Resources is included in Private Equity segment for reporting purposes.

|

7

Chemicals

Consumer

& Retail

Distribution

&

Transportation

Financial &

Business

Services

Manufacturing

& Industrial

Media, Cable

& Leisure

Packaging &

Materials

Satellite &

Wireless

Commodities

Note: The listed companies are a sample of Apollo private equity and credit

investments. The list was compiled based on non-performance criteria and is not representative of all transactions of a given type or investment of any Apollo fund generally, and are solely intended to be

illustrative of the type of investments across certain core industries that may

be made by the Apollo funds. There can be no guarantees that any similar investment opportunities will be available or pursued by Apollo in the future. The list contains companies which are not currently

held in any Apollo portfolio.

Apollo’s Expertise – Nine Core Industries

|

|

|

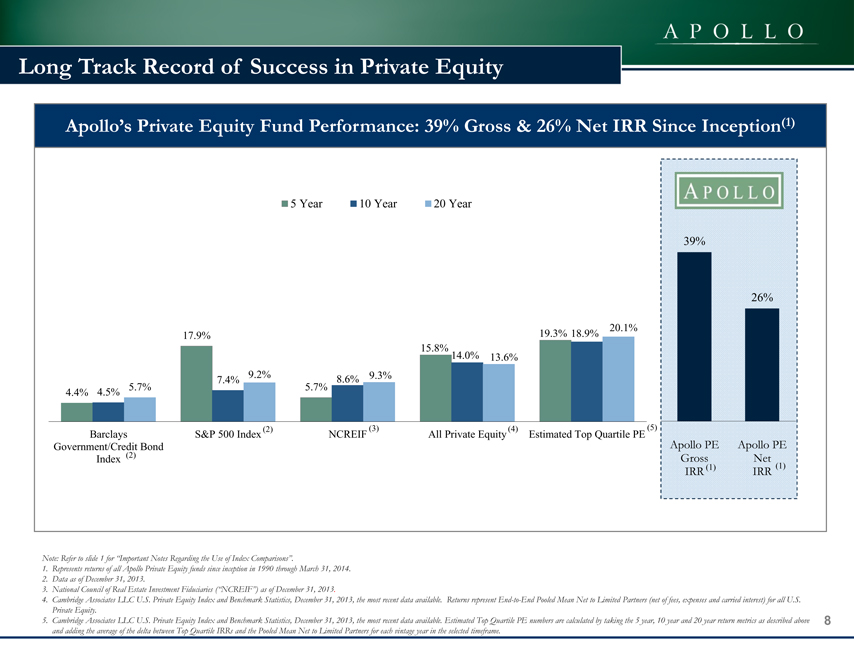

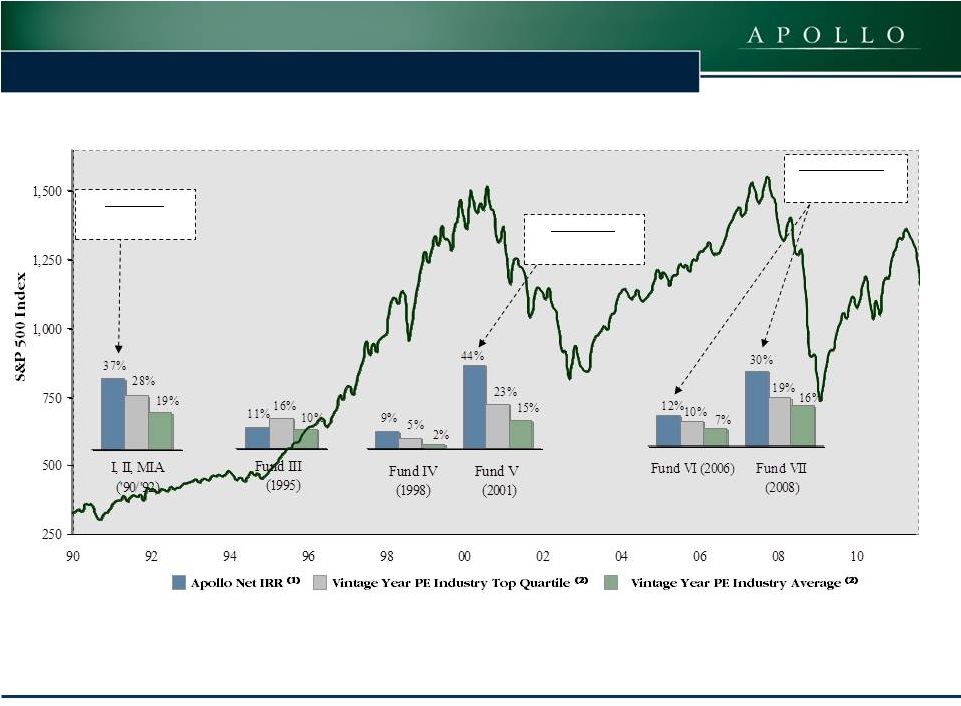

Long Track Record of Success in Private Equity

Apollo’s Private Equity Fund Performance: 39% Gross & 26% Net IRR Since Inception(1)

5 Year 10 Year 20 Year

39%

26%

17.9% 19.3% 18.9% 20.1%

15.8% 14.0% 13.6%

7.4% 9.2% 8.6% 9.3%

4.4% 4.5% 5.7% 5.7%

Barclays S&P 500 Index (2) NCREIF (3) All Private Equity (4) Estimated Top Quartile PE (5)

Government/Credit Bond Apollo PE Apollo PE

Index (2) Gross Net

IRR (1) IRR (1)

Note: Refer to slide 1 for “Important Notes Regarding the Use of Index Comparisons”.

1. Represents returns of all Apollo Private Equity funds since inception in 1990 through March 31, 2014.

2. Data as of December 31, 2013.

3. National Council of Real Estate Investment Fiduciaries (“NCREIF”) as of December 31, 2013.

4. Cambridge Associates LLC U.S. Private Equity Index and Benchmark Statistics, December 31, 2013, the most recent data available. Returns represent End-to-End Pooled Mean Net to Limited Partners (net of fees, expenses and carried interest) for all U.S. Private Equity.

5. Cambridge Associates LLC U.S. Private Equity Index and Benchmark Statistics, December 31, 2013, the most recent data available. Estimated Top Quartile PE numbers are calculated by taking the 5 year, 10 year and 20 year return metrics as described above and adding the average of the delta between Top Quartile IRRs and the Pooled Mean Net to Limited Partners for each vintage year in the selected timeframe.

| 8 |

|

|

|

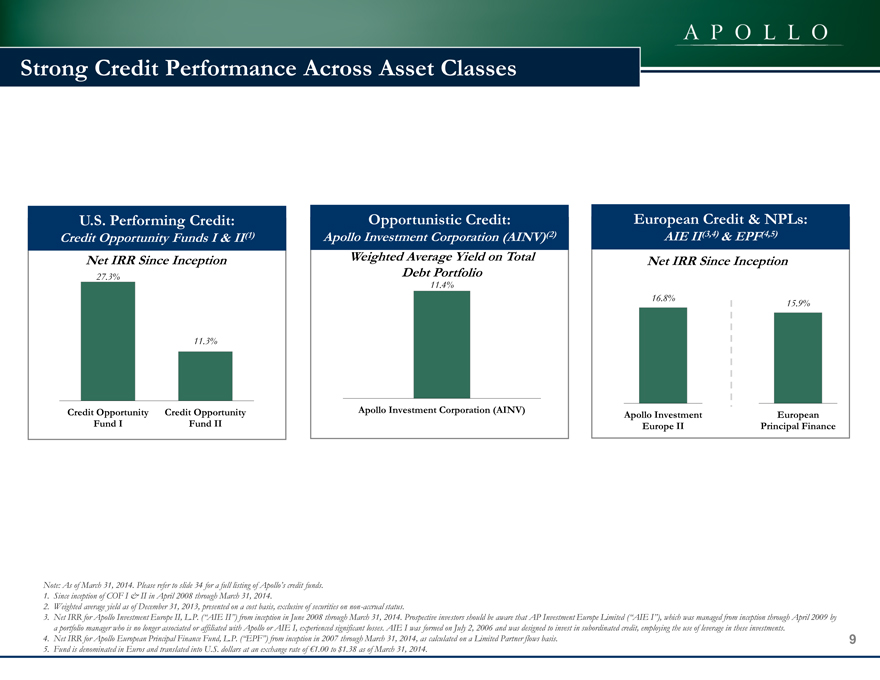

Strong Credit Performance Across Asset Classes

U.S. Performing Credit:

Credit Opportunity Funds I & II(1)

Net IRR Since Inception

27.3%

11.3%

Credit Opportunity Credit Opportunity

Fund I Fund II

Opportunistic Credit:

Apollo Investment Corporation (AINV)(2)

Weighted Average Yield on Total

Debt Portfolio

11.4%

Apollo Investment Corporation (AINV)

European Credit & NPLs:

AIE II(3,4) & EPF(4,5)

Net IRR Since Inception

16.8% 15.9%

Apollo Investment European

Europe II Principal Finance

Note: As of March 31, 2014. Please refer to slide 34 for a full listing of Apollo’s credit funds.

1. Since inception of COF I & II in April 2008 through March 31, 2014.

2. Weighted average yield as of December 31, 2013, presented on a cost basis, exclusive of securities on non-accrual status.

3. Net IRR for Apollo Investment Europe II, L.P. (“AIE II”) from inception in June 2008 through March 31, 2014. Prospective investors should be aware that AP Investment Europe Limited (“AIE I”), which was managed from inception through April 2009 by a portfolio manager who is no longer associated or affiliated with Apollo or AIE I, experienced significant losses. AIE I was formed on July 2, 2006 and was designed to invest in subordinated credit, employing the use of leverage in these investments.

4. Net IRR for Apollo European Principal Finance Fund, L.P. (“EPF”) from inception in 2007 through March 31, 2014, as calculated on a Limited Partner flows basis.

5. Fund is denominated in Euros and translated into U.S. dollars at an exchange rate of €1.00 to $1.38 as of March 31, 2014.

9

|

|

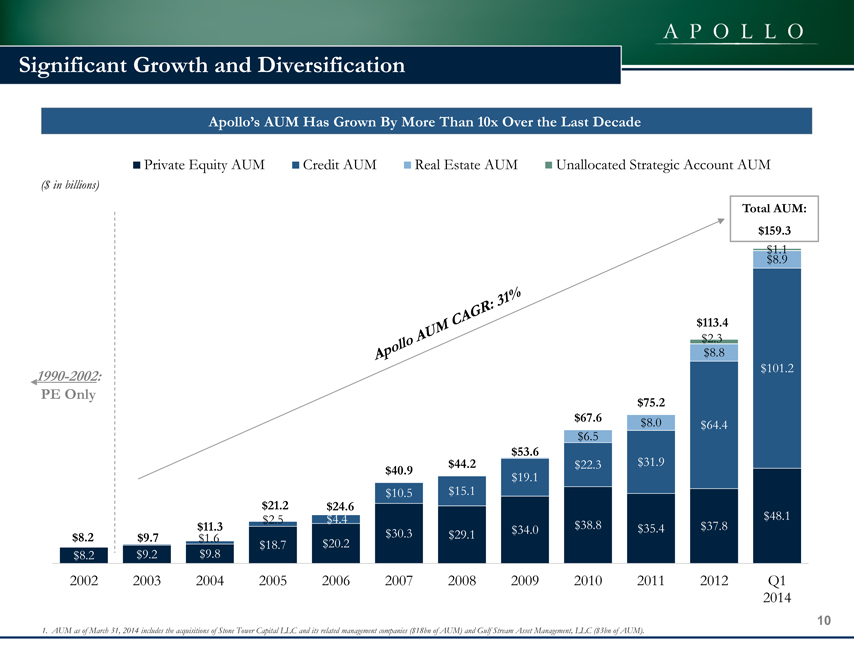

Significant Growth and Diversification

Apollo’s AUM Has Grown By More Than 10x Over the Last Decade

Private Equity AUM Credit AUM Real Estate AUM Unallocated Strategic Account AUM

($ in billions)

Total AUM:

$159.3

$1.1

$8.9

$113.4

$2.3

$8.8

1990-2002: $101.2

PE Only $75.2

$67.6 $8.0 $64.4

$6.5

$53.6

$40.9 $44.2 $22.3 $31.9

$19.1

$10.5 $15.1

$21.2 $24.6

$2.5 $4.4 $48.1

$ 11.3 $30.3 $29.1 $34.0 $38.8 $35.4 $37.8

$8.2 $9.7 $1.6 $18.7 $20.2

$8.2 $9.2 $9.8

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Q1

2014

1. AUM as of March 31, 2014 includes the acquisitions of Stone Tower Capital LLC and its related management companies ($18bn of AUM) and Gulf Stream Asset Management, LLC ($3bn of AUM).

10

|

|

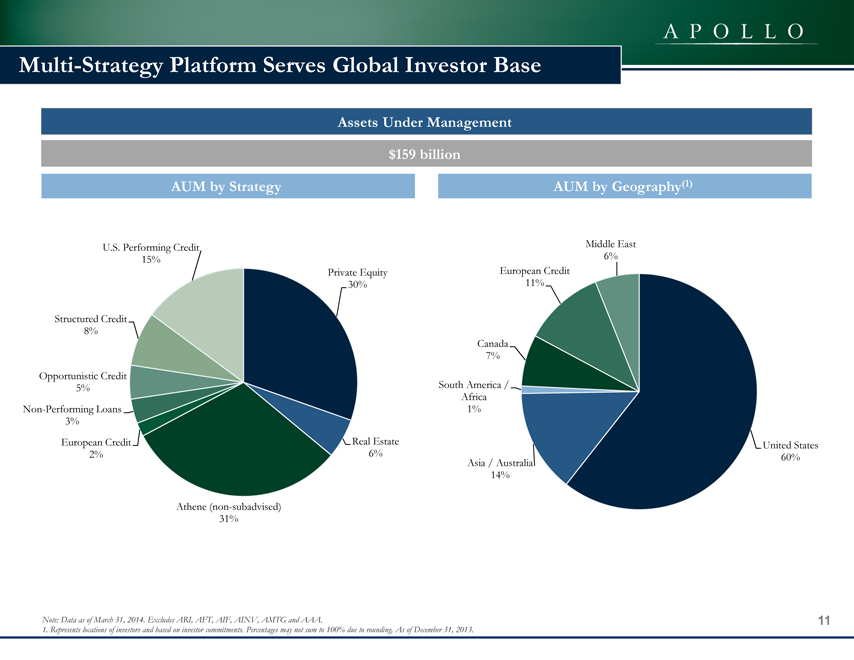

Multi-Strategy Platform Serves Global Investor Base

Assets Under Management

$159 billion

AUM by Strategy AUM by Geography(1)

U.S. Performing Credit

15%

Private Equity

30%

Structured Credit

8%

Opportunistic Credit

5%

Non-Performing Loans

3%

European Credit Real Estate

2% 6%

Athene (non-subadvised)

31%

Middle East

6%

European Credit

11%

Canada

7%

South America /

Africa

1%

United States

Asia / Australia 60%

14%

Note: Data as of March 31, 2014. Excludes ARI, AFT, AIF, AINV, AMTG and AAA.

1. Represents locations of investors and based on investor commitments. Percentages may not sum to 100% due to rounding. As of December 31, 2013.

11

12

Apollo Has a Clear Path for Continued Growth

Scaling Existing

Businesses

Strategic

Acquisitions and

Alliances

New Product

Development

Geographic

Expansion

Expand Distribution

Channels

Growth Strategies

Apollo will continue to identify opportunities to leverage its existing platform

and diversify into areas with meaningful synergies with its core

business Selected Examples

India PE and credit build-out

Asia build-out and joint ventures

London expansion

Retail closed end funds

Permanent capital vehicles (e.g., REITs)

High net worth raises for credit vehicles

Stone Tower

Gulf Stream

“Flagship”

credit funds

Emerging markets corporate credit

Managed accounts

Real estate mezzanine

Athene

Insurance-linked investment strategies

CLO platform

Energy credit

Favorable Secular Trends

Investors continue to increase

allocations to alternatives

Consolidation of relationships

with branded, scale investment

managers

Increasing constraints on the

global financial system

Emergence of unconstrained

credit as an asset class |

Agenda

Topic

1)

Apollo Overview

2)

Segment update

3)

Financial Overview

4) Appendix

13 |

|

|

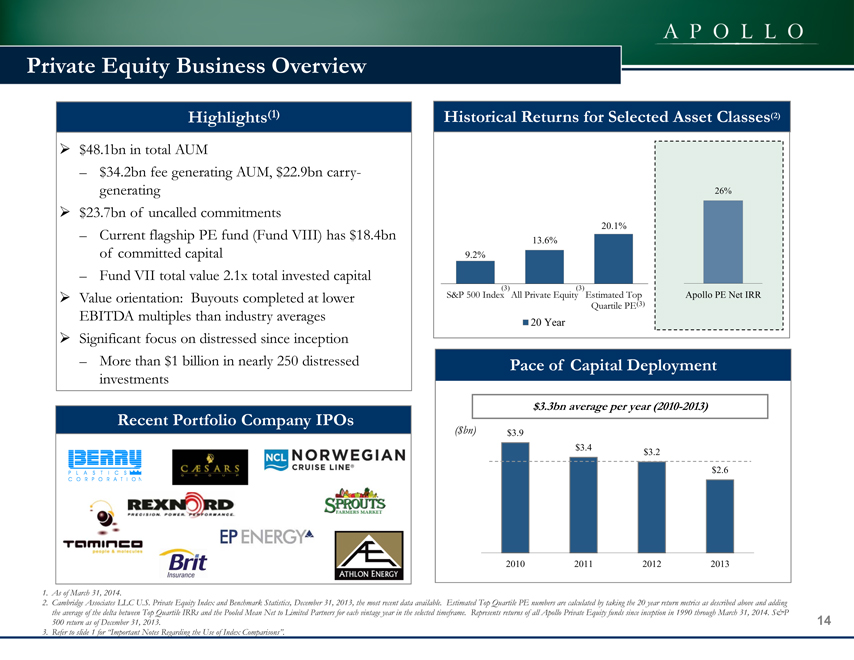

Private Equity Business Overview

Highlights(1)

$48.1bn in total AUM

– $34.2bn fee generating AUM, $22.9bn carry-generating $23.7bn of uncalled commitments

– Current flagship PE fund (Fund VIII) has $18.4bn of committed capital

– Fund VII total value 2.1x total invested capital Value orientation: Buyouts completed at lower EBITDA multiples than industry averages Significant focus on distressed since inception

– More than $1 billion in nearly 250 distressed investments

Historical Returns for Selected Asset Classes(2)

26%

20.1%

13.6%

9.2%

S&P 500 Index(3) All Private Equity(3) Estimated Top Apollo PE Net IRR

Quartile PE(3)

20 Year

Recent Portfolio Company IPOs

Pace of Capital Deployment

$3.3bn average per year (2010-2013)

($bn) $3.9

$3.4 $3.2

$2.6

2010 2011 2012 2013

1. As of March 31, 2014.

2. Cambridge Associates LLC U.S. Private Equity Index and Benchmark Statistics, December 31, 2013, the most recent data available. Estimated Top Quartile PE numbers are calculated by taking the 20 year return metrics as described above and adding the average of the delta between Top Quartile IRRs and the Pooled Mean Net to Limited Partners for each vintage year in the selected timeframe. Represents returns of all Apollo Private Equity funds since inception in 1990 through March 31, 2014. S&P 500 return as of December 31, 2013.

3. Refer to slide 1 for “Important Notes Regarding the Use of Index Comparisons”.

14

15

1990 -

1993

$3.4bn invested

2001 -

3Q03

$1.6bn invested

3Q07 –

2Q 2011

$15.5bn invested

Significant Outperformance During Downturns

1.

Represents net IRR for respective Apollo private equity fund as of March 31,

2014. Past performance not indicative of future results; please refer to slide 2 for the definition of net IRR.

2.

Thomson Reuters. Data as of September 30, 3013, the latest data currently

available. Top Quartile benchmarks represent the Upper Quartile Net IRRs for U.S. Buyout Funds of greater than $500 million by vintage year, unless otherwise noted. Vintage Year

Average represents the average net IRR for the same categories as with the Top

Quartile figures. See slide 1 for “Important Notes Regarding the Use of Index Comparisons in this Presentation”. |

|

|

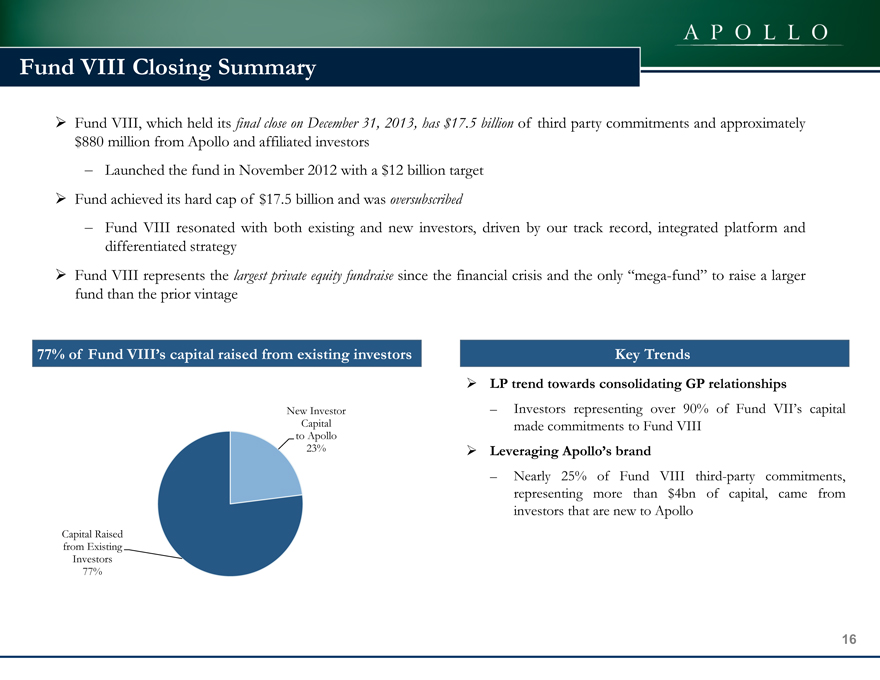

Fund VIII Closing Summary

Fund VIII, which held its final close on December 31, 2013, has $17.5 billion of third party commitments and approximately $880 million from Apollo and affiliated investors

– Launched the fund in November 2012 with a $12 billion target Fund achieved its hard cap of $17.5 billion and was oversubscribed

– Fund VIII resonated with both existing and new investors, driven by our track record, integrated platform and differentiated strategy Fund VIII represents the largest private equity fundraise since the financial crisis and the only “mega-fund” to raise a larger fund than the prior vintage

77% of Fund VIII’s capital raised from existing investors

New Investor Capital to Apollo 23%

Capital Raised from Existing 77% Investors

Key Trends

LP trend towards consolidating GP relationships

– Investors representing over 90% of Fund VII’s capital made commitments to Fund VIII

Cross-selling the Apollo platform

– Approximately 7% of Fund VIII third-party commitments, representing more than $1bn of capital, came from Apollo investors that had not previously invested in Apollo private equity funds

Leveraging Apollo’s brand

– Nearly 25% of Fund VIII third-party commitments, representing more than $4bn of capital, came from investors that are new to Apollo

16

|

|

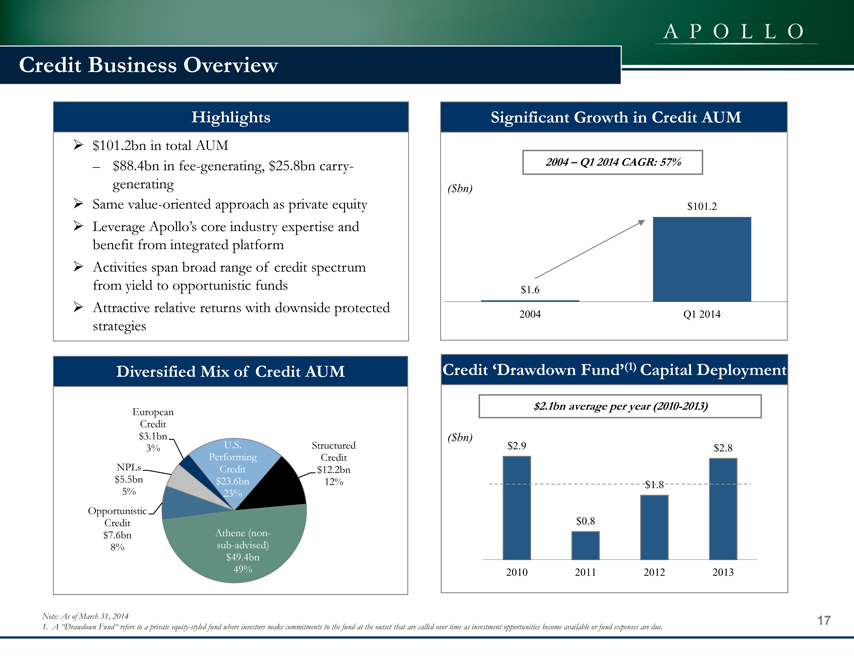

Credit Business Overview

Highlights

$101.2bn in total AUM

– $88.4bn in fee-generating, $25.8bn carry-generating Same value-oriented approach as private equity

Leverage Apollo’s core industry expertise and benefit from integrated platform Activities span broad range of credit spectrum from yield to opportunistic funds Attractive relative returns with downside protected strategies

Significant Growth in Credit AUM

2004 – Q1 2014 CAGR: 57%

($bn)

$101.2

$1.6

2004 Q1 2014

Diversified Mix of Credit AUM

European

Credit

$3.1bn

3% U.S. Structured

Performing Credit

NPLs Credit $12.2bn

$5.5bn $23.6bn 12%

5% 23%

Opportunistic

Credit

$7.6bn Athene (non-

8% sub-advised)

$49.4bn

49%

Credit ‘Drawdown Fund’(1) Capital Deployment

$2.1bn average per year (2010-2013)

($bn)

$2.9 $2.8

$1.8

$0.8

2010 2011 2012 2013

Note: As of March 31, 2014

1. A “Drawdown Fund” refers to a private equity-styled fund where investors make commitments to the fund at the outset that are called over time as investment opportunities become available or fund expenses are due.

17

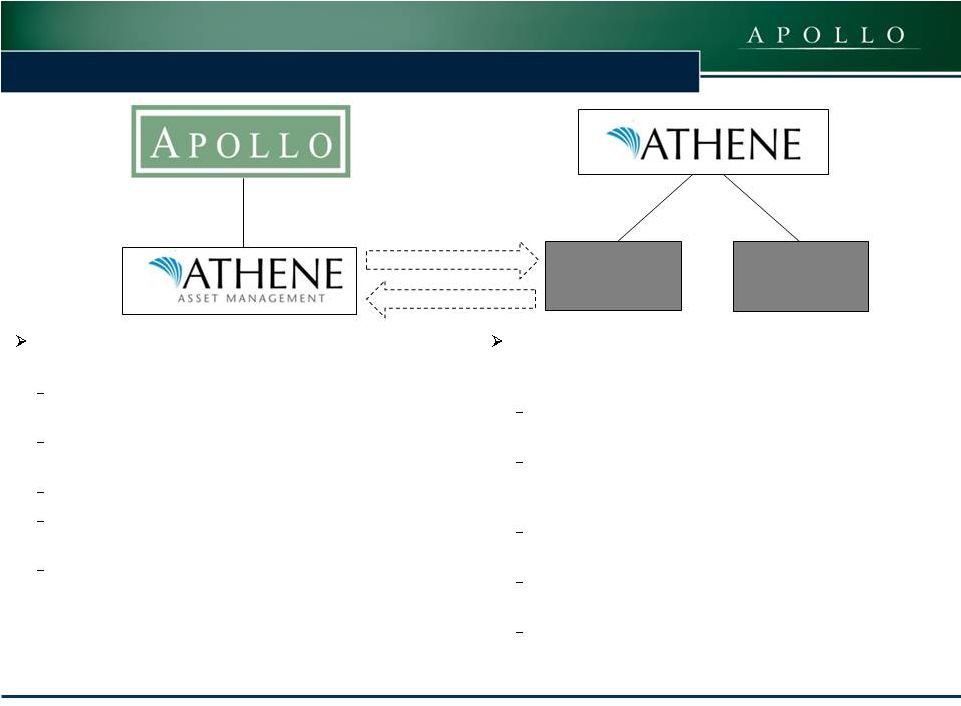

Athene Holding Ltd. (“Athene”) is an insurance holding company

focused

on

fixed

annuities

with

approximately

$59bn

in

assets

and

was founded in 2009

Earns the spread between its investment return on assets and

the rate on its liabilities

Originally funded through an Apollo-sponsored permanent

capital vehicle (AP Alternative Assets, L.P.; NYSE Euronext:

AAA)

Led by seasoned management team with significant insurance

experience

Completed transformative Aviva USA acquisition in October

2013, adding approximately $44bn of AUM

Seeks to grow annuity liabilities through three primary

channels; retail issuance, institutional issuance, and acquisition

Athene Asset Management, L.P. (AAM) is a subsidiary of

Apollo and is included within the Credit segment

Provides asset allocation services, direct asset management

services, and a suite of other services to Athene

Team of full-time dedicated investment professionals with

deep experience in asset allocation

100% of Athene’s portfolio is allocated by AAM

Approximately 17% of Athene’s portfolio directly managed

by Apollo through sub-advisory agreements

Apollo business model designed to scale in-line with

Athene’s assets

Assets

Services

Liabilities

Assets

Athene: Differentiated & Strategically Important Growth Driver

18 |

|

|

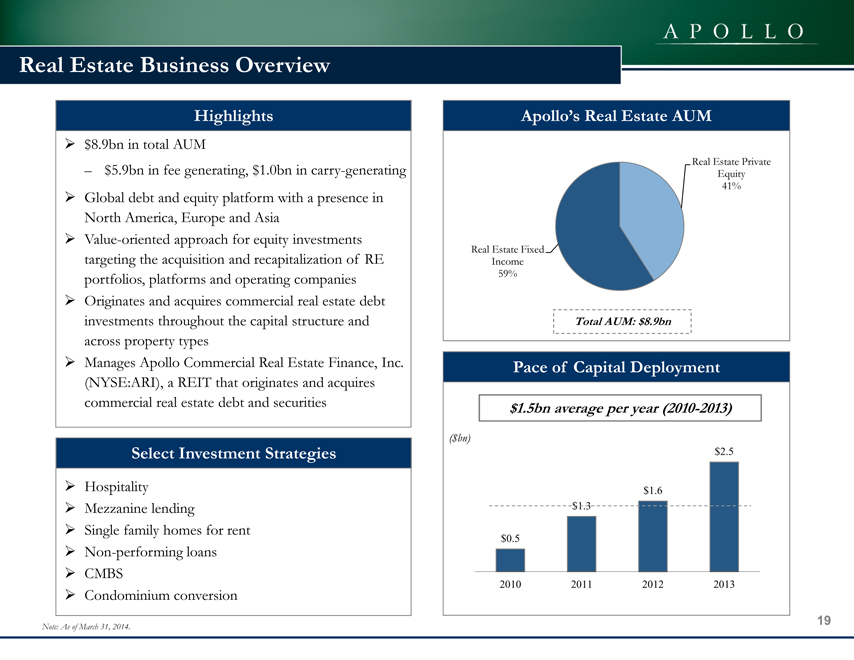

Real Estate Business Overview

Highlights

$8.9bn in total AUM

$5.9bn in fee generating, $1.0bn in carry-generating

Global debt and equity platform with a presence in North America, Europe and Asia

Value-oriented approach for equity investments targeting the acquisition and recapitalization of RE portfolios, platforms and operating companies

Originates and acquires commercial real estate debt investments throughout the capital structure and across property types

Manages Apollo Commercial Real Estate Finance, Inc. (NYSE:ARI), a REIT that originates and acquires commercial real estate debt and securities

Apollo’s Real Estate AUM

Real Estate Private

Equity

41%

Real Estate Fixed

Income

59%

Total AUM: $8.9bn

Select Investment Strategies

Hospitality

Mezzanine lending

Single family homes for rent

Non-performing loans

CMBS

Condominium conversion

Pace of Capital Deployment

$1.5bn average per year (2010-2013)

($bn)

$2.5

$1.6

$1.3

$0.5

2010 2011 2012 2013

Note: As of March 31, 2014.

19

Agenda

Topic

1)

Apollo Overview

2)

Segment update

3)

Financial Overview

4) Appendix

20 |

Financial Management Philosophies

Financially conservative

–

Manage leverage and interest coverage ratios prudently

–

Generate significant free cash flow

Focus on Management Business margins and liquidity

–

Stable non-performance based management revenue

–

Disciplined expenditure on compensation and non-compensation

–

Maintain sufficient liquidity in order to service debt obligations and maintain

appropriate cash balances Flexible dividend policy

–

Flexible policy allowing management discretion to retain earnings for

operational or investment needs Committed to maintaining a strong investment

grade rating 21 |

22

($mm, except per share data)

2011

2012

2013

LTM Q1

2014

Management

business

ENI

–

(pre-tax)

$76

$223

$331

$417

Incentive

business

ENI

(loss)

–

(pre-tax)

(377)

1,411

1,797

1,188

ENI income tax provision

21

159

238

260

Total after-tax ENI (loss)

($322)

$1,476

$1,889

$1,344

Total after-tax ENI (loss) per share

($0.86)

$3.82

$4.80

$3.40

Fee-related EBITDA

197

339

438

560

Fee-related EBITDA + 100% net realized carry

$531

$890

$1,915

$2,103

Distributions

declared

(1)

$314

$539

$1,627

$1,645

Distributions declared per share

$0.83

$1.35

$3.95

$3.43

1.

Amounts include distributions to Class A shareholders, non-controlling

interest in AOG and distribution equivalents on participating securities

Strong Mgt. Business Growth & Significant Free Cash Flow |

Robust Growth in Fee-Generating AUM

23

($mm)

2011

2012

2013

Q1 2014

Total AUM

$75

$113

$161

$159

39.6%

Fee-generating AUM

$58

$82

$128

$129

42.3%

Fee-generating

AUM

by

Segment:

Private equity

$28

$28

$34

$34

9.2%

Credit

27

50

88

88

70.7%

Real estate

4

4

6

6

25.5%

Total

$58

$82

$128

$129

42.3%

CAGR

(2011-Q1

2014) |

|

|

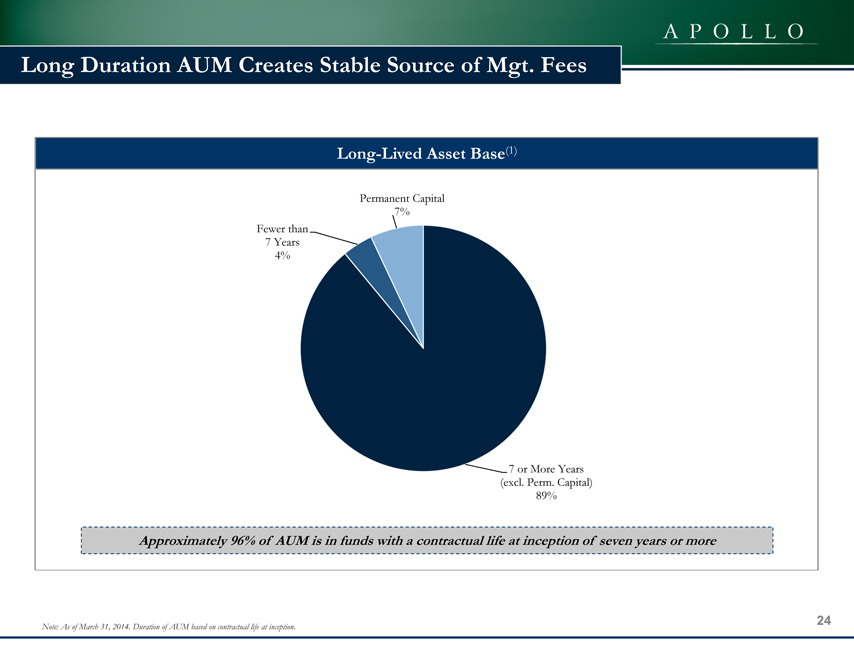

Long Duration AUM Creates Stable Source of Mgt. Fees

Long-Lived Asset Base(1)

Permanent Capital

7%

Fewer than

7 Years

4%

7 or More Years

(excl. Perm. Capital)

89%

Approximately 96% of AUM is in funds with a contractual life at inception of seven years or more

Note: As of March 31, 2014. Duration of AUM based on contractual life at inception.

24

Management Business Performance

25

($mm, except per share data)

2011

2012

2013

LTM Q1

2014

Management fees

$490

$623

$731

$791

Advisory & transaction fees

82

150

197

265

NII incentive fees -

AINV

45

38

37

36

Total management business revenues

617

811

964

1,092

Compensation expenses

319

344

361

409

Non-compensation expenses

224

257

302

295

Other income (loss) & minority interest

3

12

30

29

76

223

331

417

Mgt. business ENI per share (pre-tax)

$0.21

$0.58

$0.84

$1.05

Non-cash comp

68

69

66

107

Interest expense

41

37

29

25

Depreciation and amortization

11

10

11

11

Fee-related EBITDA

197

339

438

560

Operating

metrics

Mgt. business margin (%)

12%

27%

34%

38%

Mgt. comp % of mgt. revenues

52%

42%

37%

37%

Mgt. non-comp % mgt. revenues

36%

32%

31%

27%

Management business ENI – (pre-tax) |

Incentive Business Performance

26

1.

Using March 31, 2014, non-GAAP weighted average diluted shares

outstanding. 2.

Carried interest receivable less profit sharing payable on an unconsolidated

basis. ($mm, except per share data)

2011

2012

2013

LTM

Q1 2014

Economic ENI

ENI –

total carry:

Private equity

($449)

$1,668

$2,517

$1,630

Credit

7

481

337

270

Real estate

0

15

5

4

Total carry

($442)

$2,164

$2,859

$1,903

ENI –

total profit sharing expense:

Private equity

$727

$1,030

$709

Credit

36

138

143

146

Real estate

0

7

0

(1)

Total profit sharing expense

$872

$854

Equity method

investment gain / (loss)

5

120

111

138

$1,188

Incentive

business

ENI

(loss)

per

share

(pre-tax)

(1)

($1.01)

$3.65

$4.56

$3.01

Net realized

carry

Realized carry:

Private equity

$571

$813

$2,063

$2,166

Credit

74

180

393

408

Real estate

0

5

1

0

Total realized carry

$997

$2,456

$2,574

Realized profit sharing expense:

Private equity

$273

$383

$883

$933

Credit

37

63

95

97

Real estate

0

0

0

0

Total realized profit sharing expense

$978

$1,030

Net realized carry

$1,478

$1,544

$1,105

$1,173

$1,797

$1,295

$446

$551

$1,021

$516

$335

$645

($377)

($60)

($97)

Incentive business ENI (loss) (pre-tax)

$1,411

$310 |

|

|

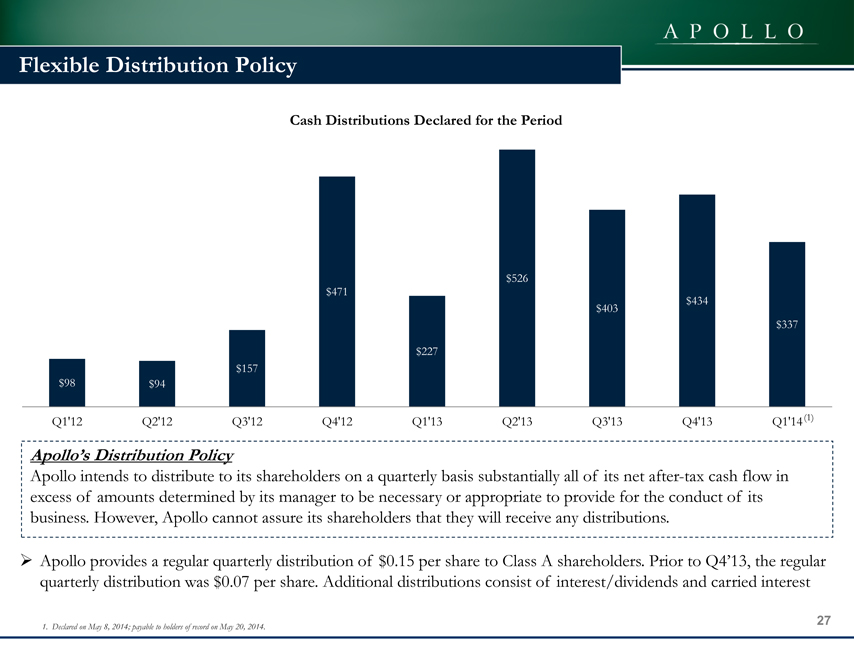

Flexible Distribution Policy

Cash Distributions Declared for the Period

$5

26

$471

$403 $434

$337

$227

$157

$98 $94

Q1’12 Q2’12 Q3’12 Q4’12 Q1’13 Q2’13 Q3’13 Q4’13 Q1’14 (1)

Apollo’s Distribution Policy

Apollo intends to distribute to its shareholders on a quarterly basis substantially all of its net after-tax cash flow in excess of amounts determined by its manager to be necessary or appropriate to provide for the conduct of its business. However, Apollo cannot assure its shareholders that they will receive any distributions.

Apollo provides a regular quarterly distribution of $0.15 per share to Class A shareholders. Prior to Q4’13, the regular quarterly distribution was $0.07 per share. Additional distributions consist of interest/dividends and carried interest

1. Declared on May 8, 2014; payable to holders of record on May 20, 2014.

27

Strong Financial Condition With Low Levels of Debt

28

1.

Financial condition amounts are shown without the impact of certain Apollo funds

that are required to be consolidated on its financial statements under U.S. GAAP.

2.

Net of profit sharing expense.

3.

Includes total General Partner investments using equity method, fair value

measurements of Apollo Senior Loan Fund, HFA and AAA (of which Apollo has a 2.6% ownership interest), and fair value measurement of Athene and AAA Services Derivatives.

4.

As of May 15, 2014. Based on a share price of $25.28 and 377.9mm shares

outstanding as of March 31, 2014, assuming full exchange of all outstanding Apollo Operating Group units as of such date into Class A shares.

|

Selected Financial Metrics and Leverage Analysis

29

($mm)

2011

2012

2013

LTM Q1

2014

Fee-related EBITDA

$197

$339

$438

$560

Fee-related EBITDA + 100% of net realized carry

531

890

1,915

2,103

Interest expense

41

37

29

25

Debt

738

738

750

750

Leverage ratios:

Fee-related EBITDA / interest expense

4.8x

9.1x

15.1x

22.5x

Fee-related EBITDA + 100% of net realized carry / interest expense

13.0x

24.0x

66.0x

84.1x

Debt / fee-related EBITDA

3.8x

2.2x

1.7x

1.3x

Debt / fee-related EBITDA + 100% of net realized carry

1.4x

0.8x

0.4x

0.4x |

Agenda

Topic

1)

Apollo Overview

2)

Segment update

3)

Financial Overview

4) Appendix

30 |

Bridge to GAAP Financials

31

($mm)

2011

2012

2013

LTM

Q1 2014

Fee-Related EBITDA + 100% net realized carry

$531

$890

$1,915

$2,103

Net unrealized carry

(716)

740

208

(493)

Net unrealized investment income

5

120

111

138

Net interest expense

(41)

(37)

(29)

(25)

Depreciation and amortization

(11)

(10)

(11)

(11)

Non-cash comp

(68)

(69)

(66)

(107)

ENI tax provision

(21)

(159)

(238)

(238)

Economic Net (Loss) Income (post-tax)

($322)

$1,476

$1,890

$1,368

ENI tax provision

21

159

238

238

Income tax provision

(12)

(65)

(108)

(122)

Net (loss) income attributable to non-controlling interests

in Apollo Operating Group

940

(685)

(1,258)

(928)

Non-cash charges related to equity-based compensation

(1,082)

(530)

(60)

(32)

Amortization of intangible assets

(15)

(43)

(43)

(41)

GAAP Net (Loss) Income

($469)

$311

$659

$483 |

Carried Interest Income Receivable

Note:

Figures

may

not

sum

due

to

rounding.

Amounts

presented

are

on

an

unconsolidated

basis.

32

($mm)

2012

2013

Q1 2014

Private equity funds:

Fund VII

$904

$891

$774

Fund VI

270

698

522

Fund V

134

43

54

Fund IV

11

8

5

Other (AAA, Stanhope)

94

229

219

Total private equity funds

$1,413

$1,868

$1,574

Credit funds:

U.S. performing credit

$402

$180

$163

Opportunistic credit

37

60

49

Structured credit

21

54

61

European credit

18

36

18

Non-performing loans

102

154

120

Total credit funds

$580

$484

$410

Real estate funds

CPI other

$11

$5

$4

AGRE US real estate

-

6

7

Other

-

4

4

Total real estate funds

$11

$15

$15

Total

$2,004

$2,367

$1,999 |

Structure Chart as of May 9, 2014

33

100%

39.44% of the LP units of certain

Apollo Operating Group Entities

11.82% of

LP

units

31.26% of total voting power

Managing Partners

APO (FC), LLC

Apollo Asset Co., LLC

APO Corp.

Apollo Operating Group

39.44% of the LP units of certain

Apollo Operating Group Entities

39.44% of the LP units of certain

Apollo Operating Group Entities

100%

100%

Intermediate Holding

Companies

Class A Shareholders

(Class A Shares)

AGM

Management, LLC

(Our Manager)

BRH Holdings

GP, Ltd.

(Class B Shares)

BRH

Holdings, L.P.

AP Professional

Holdings, L.P.

(60.56% of Apollo

Operating

Group Units)

Contributing Partners

60.56% of the LP units of each

Apollo Operating Group Entity

88.18% of

LP units

68.74% of total

voting power

100% of LP

units

GP

GP

Note: The organizational structure chart above depicts a simplified version of

the Apollo structure. It does not include all legal entities in the structure. APOLLO GLOBAL MANAGEMENT, LLC

(39.44% of Apollo Operating Group Units) |

Appendix: Credit Fund Summary

Apollo Fund

Year of Inception

Apollo Fund

Year of Inception

Apollo / Artus Investors 2007 –

1

2007

ALM VII (R) Ltd.

2013

Apollo Credit Liquidity Fund

2007

ALM VII (R)-2 Ltd.

2013

Apollo Credit Opportunity Fund I

2008

ALM VIII

2013

Apollo Credit Opportunity Fund II

2008

ALM X

2014

Apollo Credit Opportunity Fund III

2013

ALME

2013

Apollo Senior Loan Fund

2010

Compass 2005-II

2006

Apollo European Principal Finance

2007

Compass 2007

2007

Apollo European Principal Finance II

2012

Cornerstone CLO

2007

Apollo Investment Corporation (NASDAQ: AINV)

2004

Rampart CLO 2006-I

2006

AP

Investment

Europe

Limited

(1)

2006

Rampart CLO 2007-I

2007

Apollo Investment Europe II

2008

Rashinban

2006

Apollo European Credit Fund

2011

Sextant 2006

2006

Apollo Senior Floating Rate Fund Inc (NYSE: AFT)

2011

Sextant 2007

2007

Apollo Strategic Value Fund

2006

Stone Tower CLO V

2006

Apollo Value Investment Fund

2003

Stone Tower CLO VI

2007

Apollo

Credit

Fund

(2)

2005

Stone Tower CLO VII

2007

Apollo

Credit

Strategies

Fund

(2)

2011

Apollo Financial Credit Investment I

2011

Apollo Structured Credit Recovery Fund II

2012

Apollo Financial Credit Investment II

2013

ALM IV

2011

Apollo Total Return Fund

2014

ALM V

2012

Apollo Structured Credit Recovery Fund III

2014

ALM VI

2012

Apollo Credit Short Opportunities Fund

2014

ALM VII

2012

34

It should not be assumed that future Credit funds or CLOs will equal the

performance of the funds and CLOs on this list, nor should it be assumed that the past performance of the funds and CLOs on this list are indicative or a guarantee of future performance of such funds and CLOs.

(1) Fund is currently winding down. (2) Track record was accumulated by the

investment committee, of which two members are no longer at the firm as of June 30, 2012. Note: As of April 2014, the following CLOs have been called: ALM I and III, Compass 2002-1, 2003-1,

2004-1 and 2005-I, Neptune, Granite Ventures I, II, and III, Stone Tower

CLOs I, II, III, IV. This list excludes CDOs, SIVs, managed accounts and strategic partnerships. The above list is reflective of funds currently in existence as of April 2014 and excludes funds and

investment vehicles that have since been dissolved but previously managed by

Apollo. Additional information on such funds is available upon request.

|