Attached files

| file | filename |

|---|---|

| 8-K - 8-K - AMERIANA BANCORP | d724359d8k.htm |

AMERIANA BANCORP

ANNUAL MEETING

THURSDAY, MAY 15, 2014

|

CEO

PRESENTATION

: ASBI

Exhibit 99.1 |

FORWARD-LOOKING

STATEMENT

This presentation contains forward-looking statements, which

include statements about Ameriana’s future financial

performance, business plans and strategies. They often include

words like “believe,”

“expect,”

“anticipate,”

“estimate,”

and

“intend”

or future or conditional verbs such as “will,”

“would,”

“should,”

“could”

or “may.”

Forward-looking statements involve

future risks and uncertainties because of factors that could

cause actual results to differ materially from those expressed or

implied. Specific risk factors and other uncertainties that could

affect the accuracy of forward-looking statements are included in

Ameriana’s Form 10-K for the year ended December 31, 2013.

Ameriana does not undertake any obligation to update forward-

looking statements made in this document. |

AMERIANA BANCORP

ANNUAL FINANCIAL

PERFORMANCE

(IN THOUSANDS)

Year Ended

December 31,

2013

2012

Interest Income

$16,980

$18,032

Interest Expense

3,003

3,845

Net Interest Income

13,977

14,187

Provision for Loan Losses

755

1,145

Non-Interest Income

5,801

5,181

Non-Interest Expense

16,095

15,827

Income before Income Taxes

2,928

2,396

Income Tax Expense

741

556

Net Income

$ 2,187

$ 1,840 |

AMERIANA BANCORP

QUARTERLY FINANCIAL

PERFORMANCE

(IN THOUSANDS)

Three Months

Ended March 31,

2014

2013

$

4,474

$ 4,291

758

762

3,716

3,529

150

255

1,364

1,512

3,917

3,960

1,013

826

284

212

$ 729

$

614

Interest Income

Interest Expense

Net Interest Income

Provision for Loan Losses

Non-Interest Income

Non-Interest Expense

Income before Income Taxes

Income Tax Expense

Net Income |

AMERIANA BANK CAPITAL

(AS OF 3/31/14)

Bank

Peer*

Tier 1 Leverage Capital

9.38%

10.02%

Tier 1 RBC/Risk Wtd. Assets

14.13

14.75

Total RBC/Risk Wtd. Assets

15.38

15.94

Source: FDIC UBPR 3/31/2014

*Peer

group

defined

by

FDIC

for

Ameriana

is

“Peer

Group

3”

–

insured

commercial

banks having assets between $300 million and $1 billion

|

KEY

METRICS (AS OF 3/31/14)

Bank

Peer*

Non-accrual Loans/Total Loans

1.63%

1.27%

NCL+ OREO/Lns. + OREO

3.26

2.21

Net Loss/Avg. Loans

0.05

0.13

ALLL/Total Loans

1.29

1.58

Current Rest. Loans/Total Loans

2.86

0.68

Source: FDIC UBPR 3/31/2014

*Peer

group

defined

by

FDIC

for

Ameriana

is

“Peer

Group

3”

–

insured

commercial

banks having assets between $300 million and $1 billion

|

AMERIANA BANCORP

FINANCIAL PERFORMANCE

(FIRST QUARTER 2014)

Positive Factors:

*On a fully tax-equivalent basis

•

Net income of $729,000, or $0.24 per diluted share, for the

quarter was $115,000, or 18.7%, improvement over the first

quarter of 2013

•

Loan repurchase resulting in $173,000 of interest income

provided increase in net interest income

•

Net interest margin of 3.72%*, 1 bp lower than the same

quarter of 2013

•

Declared a quarterly dividend of $0.02 per share, which

represented a $0.01 per share increase |

Source: FDIC

UBPR 3/31/2014 Source: FDIC UBPR 3/31/2014

*Peer

group

defined

by

FDIC

for

Ameriana

is

“Peer

Group

3”

–

insured

commercial banks having assets between $300 million and $1 billion

AMERIANA BANCORP

FINANCIAL PERFORMANCE

(FIRST QUARTER 2014)

Assets per employee is improving ($ per million)

o

$3.33 compared to $3.10 in the same quarter in 2013,

($3.23 at 12/31/2013 and $2.89 at 12/31/2012)

Yield on loans compares favorably to peer group* results

o

5.19% compared to average yield of 5.14% for the first

quarter of 2014

Positive Factors:

•

• |

AMERIANA BANCORP

FINANCIAL PERFORMANCE

•

•

•

•

•

Funding costs are somewhat higher than peer

Assets per employee remains lower than peer (i.e. excess

capacity)

DDAs, although increasing, remain below high-performing

peer banks

Other non-personnel expenses are higher than peer

Personnel expense, due to number of offices, is higher than

peer

Negative Factors: |

FINANCIAL PERFORMANCE

(FIRST QUARTER 2014)

Profitability: (% of Avg. Assets)

Bank

Peer*

Interest Expense

0.62%

0.44%

Other Operating Expense

0.86

0.90

Occupancy Expense

0.53

0.37

Personnel Expense

1.83

1.59

Total Overhead Expense

3.21

2.87

Efficiency Ratio

72.19

67.83

Assets Per Employee ($ in millions)

$3.33

$4.78

Average Personnel Expense

60.29

71.75

Source: FDIC UBPR 3/31/2014

banks having assets between $300 million and $1 billion

*Peer

group

defined

by

FDIC

for

Ameriana

is

“Peer

Group

3”

–

insured

commercial

Per Employee ($ in thousands) |

FINANCIAL PERFORMANCE

(FIRST QUARTER 2014)

Profitability: (%)

Bank

Peer

Avg. Earning Assets/Avg. Assets

88.99%

93.97%

Avg. Int. Bearing Fds/Avg. Assets

83.53

76.92

Int. Income/Avg

. Earning Assets

4.37

4.19

NII/Average Earning Assets

3.68

3.71

Net Loans/Avg. Assets

66.89

63.22

Source: FDIC UBPR 3/31/2014

*Peer

group

defined

by

FDIC

for

Ameriana

is

“Peer

Group

3”

–

insured

commercial

banks having assets between $300 million and $1 billion

|

FINANCIAL PERFORMANCE

(FIRST QUARTER 2014)

Profitability: (%)

Bank

Peer

AFS Securities/Avg. Assets

8.95%

19.81%

DDA/Avg. Assets

5.85

10.93

Core Deposits/Avg. Assets

76.92

77.77

FHLB/Avg. Assets

7.16

2.43

Source: FDIC UBPR

3/31/2014

*Peer

group

defined

by

FDIC

for

Ameriana

is

“Peer

Group

3”

–

insured commercial

banks having assets between $300 million and $1 billion

|

TOTAL

LOANS (DOLLARS IN THOUSANDS)

$325,864

$326,573

$317,595

$317,087

$318,287

$316,959

$317,536

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

TOTAL

DEPOSITS (DOLLARS IN THOUSANDS)

$324,406

$338,381

$337,978

$337,250

$356,703

$362,701

$373,030

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

NET

INTEREST INCOME (DOLLARS IN THOUSANDS)

$11,793

$12,689

$13,411

$13,924

$14,187

$13,977

$3,716

2008

2009

2010

2011

2012

2013

1Q14 |

NET

INTEREST MARGIN (ON A FULLY TAX-EQUIVALENT BASIS)

3.08%

3.08%

3.63%

3.73%

3.71%

3.63%

3.72%

2008

2009

2010

2011

2012

2013

1Q14 |

NON-PERFORMING LOANS

(DOLLARS IN THOUSANDS)

$6,219

$9,053

$11,247

$8,828

$7,604

$5,058

$5,162

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

NON-ACCRUAL LOANS

(AS OF 3/31/2014)

($ in thousands)

Single-family residences –

Countrywide

originations (10 loans)

$ 2,078

Residential condominium development

1,515

Commercial

781

Commercial real estate

422

Sub-total

4,796

Single-family residences (6

loans)

331

Consumer (4 loans)

Total

$ 5,161

34 |

NON-PERFORMING LOANS/TOTAL

LOANS

1.91%

2.78%

3.54%

2.79%

2.39%

1.60%

1.62%

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

OREO

(DOLLARS IN THOUSANDS)

$3,881

$5,517

$9,067

$7,545

$6,326

$5,172

$5,262

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

OTHER

REAL ESTATE OWNED (AS OF 3/31/2014)

($ in thousands)

Retail strip center (partially occupied) and two outlots

$ 2,451

Single

family

residence

–

rented

783

Developed commercial land

820

Undeveloped land and developed residential building lots

750

Undeveloped land

214

Developed commercial lot

113

Four single-family residences (unrelated)

131

Sub-total

Total

5,040

$ 5,262 |

OREO/TOTAL LOANS

1.19%

1.69%

2.85%

2.38%

1.99%

1.63%

1.66%

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

NET

CHARGE-OFFS (DOLLARS IN THOUSANDS)

$936

$1,166

$1,726

$1,465

$1,038

$1,002

$42

2008

2009

2010

2011

2012

2013

1Q14

* |

NET

CHARGE-OFFS/AVG. LOANS 0.30%

0.35%

0.54%

0.47%

0.33%

0.31%

0.01%

2008

2009

2010

2011

2012

2013

1Q14 |

ALLOWANCE FOR LOAN LOSSES

(DOLLARS IN THOUSANDS)

$2,991

$4,005

$4,212

$4,132

$4,239

$3,993

$4,100

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

ALLOWANCE FOR LOAN

LOSSES/TOTAL LOANS

0.92%

1.23%

1.33%

1.30%

1.34%

1.26%

1.29%

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

TROUBLED DEBT

RESTRUCTURINGS (TDRS)

(DOLLARS IN THOUSANDS)

$0

$268

$8,393

$9,016

$12,171

$11,558

$11,998

12/31/2008

12/31/2009

12/31/2010

12/31/2011

12/31/2012

12/31/2013

3/31/2014 |

TROUBLED DEBT

RESTRUCTURINGS

(TDRS

-

AS

OF

3/31/2013)

($ in thousands)

Hotel loan

$ 3,752

Pass

Undeveloped commercial land

1,464

Substandard

Residential condominium development

1,515

Non-accrual

Undeveloped land –

two parcels –

same borrower

984

Substandard

Developed commercial land

1,013

Pass

Subtotal

8,728

Single-family residence (4 loans)

424

Substandard

Single-family residence (10 loans)

1,179

Non-accrual

Single-family residence (2 loans)

91

Single-family

residence

–

Countrywide

originations

(2

loans)

382

923

Commercial (3 loans)

253

Commercial real estate

15

$11,998

Pass

Single-family

residence

–

Countrywide

origination

(3

loans)

Pass

Non-accrual

Non-accrual

Pass

Total |

•

To be a relevant and robust

alternative to “banking as usual”

in central Indiana

•

To grow into new markets by

doing what it takes to become a

fully established, leading citizen

and business advocate in each

neighborhood we serve

•

To uphold and act on our core

values of being a true

community bank

OUR

VISION |

To

engage every customer in a meaningful dialogue regarding their financial

needs and provide advice and financial solutions that

assist them in achieving their goals

OUR MISSION |

Ethics:

Honesty, Integrity, Responsibility

Customers:

Service, Satisfaction, Relationships

Associates:

Talent, Teamwork, Personal Leadership

Community:

Service, Involvement, Leadership

Diversity:

Respect, Appreciation

OUR VALUES |

AMERIANA BUSINESS

STRATEGY

•

Customer needs client strategy focused on building long-

term relationships

•

Disciplined, relationship-building culture along all

business units

•

Business units

o

Commercial

o

Consumer

o

Mortgage

o

Insurance

o

Financial Management

•

Primary focus is value creation through growth in

Indianapolis and legacy markets |

AMERIANA COMMERCIAL

STRATEGY

•

C&I / Owner-Occupied CRE / Investment Real Estate

•

Focused on small business and middle market clients

•

Target loan size is $25,000 -

$5 million

•

Working capital lines, equipment financing, letters of credit,

term real estate and interest rate risk tools available

•

SBA Lending expertise

•

Experienced lending team, primarily focused on

Indianapolis market

•

Full suite of depository products, online money

management tools, merchant processing, insurance and

401(k) plan expertise |

AMERIANA CONSUMER

LENDING STRATEGY

•

Consumer lending focused on residential mortgage,

home equity, auto and other closed-end loans

Mortgage originators located in key markets within our

footprint

Fully-automated Loan Origination System in compliance

with all current regulations

Online consumer application system

•

•

• |

AMERIANA RETAIL CUSTOMER

STRATEGY

•

Relationship development focused on meeting financial

lifecycle needs and building products per household

•

On-The-Go Checking is key acquisition product

•

Focused on in-branch experience, as well as Electronic

Delivery Channels:

o

ATM access

o

Telephone Banking

o

Call Center

o

Online Banking

o

Mobile Banking –

check deposit, bill pay, alerts, etc.

o

e-Account Opening |

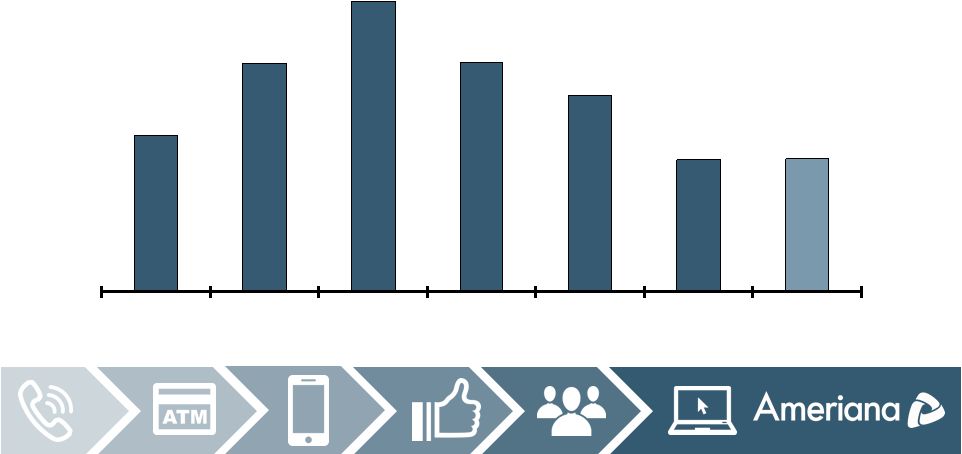

GROWTH IN CUSTOMER

RELATIONSHIPS BANK-WIDE |

GROWTH IN CROSS

SELL/MULTIPLE PRODUCTS

128% Increase |

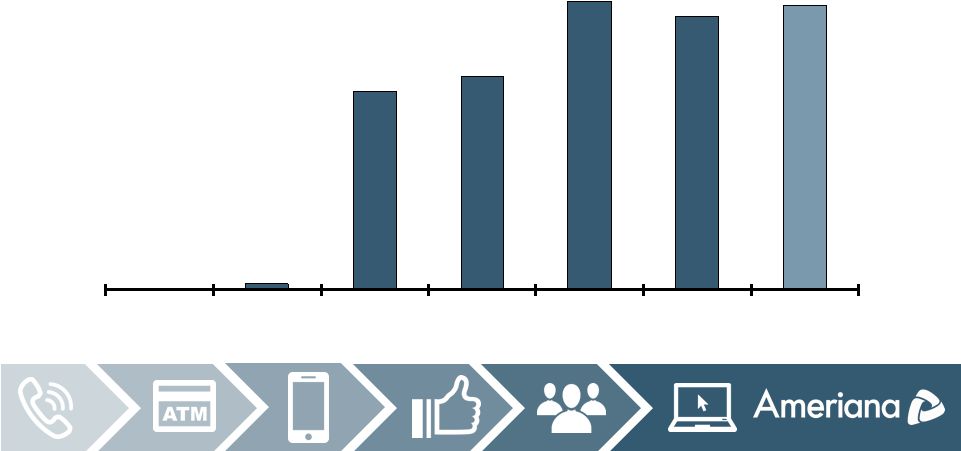

GROWTH IN DEPOSIT FEE

INCOME

(OTHER FEES AND SERVICE CHARGES)

44% Increase

$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

2007

2008

2009

2010

2011

2012

2013

Fee Income Trend 2007 -

2013

Fee Income |

SHIFT

IN DEPOSIT MIX CDs

61%

Non-

Maturity

Deposits

39%

CDs

40%

Non-

Maturity

Deposits

60%

12/31/13

12/31/08 |

OMNI-CHANNEL INTEGRATION

•

The Connected Consumer

•

Simultaneous Channel

Usage

•

Experiential Brand

•

Knowledge-based Delivery |

SURROUND THE CUSTOMER

Employees

Online &

Mobile Banking

Customer Care

Facility

Environment

Word of Mouth

Advertising

Direct Mail /

Newsletters

Media

Policies

Community

Outreach

Investor

Relations

Monthly

Statement

Customer

Communication

Social Media

Sponsorships

& Events

Debit Card

Customer Brand Experience

Customer Brand Experience |

NEW

PRODUCTS AND SERVICES

Mobile Banking App (iPhone, iPad, Android

smartphones)

o

Business Mobile App

Instant Issue Check Card

e-Account Opening

Online Loan Application

Health Savings Accounts (HSAs)

Check Deposit, Bill Pay, Alerts

•

•

•

•

•

• |

CUSTOMER PREFERENCES

55% will buy

a service

that helps

them use

data to

improve their

lives

76% prefer

virtual

channels for

basic

banking

transactions

2.5 monthly

visits by

mobile

bankers

users

1/3 of mobile

users will

bank via

phone

65% prefer

branch for

advice and

personalized

attention

83% open to

new advisory

services,

including

financial

education.

Customer |

HAMILTON COUNTY STORES |

BROAD

RIPPLE DEVELOPMENT 59

& COLLEGE AVENUE

TH |

BROAD

RIPPLE DEVELOPMENT 59

TH

&

COLLEGE

AVENUE |

Other sites will be

evaluated in Marion County, such as Downtown, Mass Ave., etc.

BRANCH OPENING TIMELINE

2014

2015

2016

Noblesville

(Summer)

Allisonville

(Summer)

•

•

Broad

•

Plainfield

•

Ripple

(2Q) |

REGULATORY AND

ENTERPRISE RISK

MANAGEMENT

•

Experienced ERM Team

o

Janelle

Gamble,

SVP

–

Chief

Risk

Officer

+

Compliance

and

CRA Officer

Gloria Corbin, BSA

Stephanie Cunningham, Compliance

Ron Holloway, Loan Review

Joan Kerulis and Debra Hay, Audit |

COMMUNITY OUTREACH

Corporate Sponsorship of the Humane Society for Hamilton

County –

Ameriana Bank Foster Program

o

2013 Corporate Sponsor of the Year

Checking It Forward

o

$43,400 donated to 34 non-profit organizations in 2013

o

Approximately 868 accounts opened through the program

Help Our Heroes –

to benefit the USO of Indiana

o

Nearly $600 in monetary donations, more than 60 boxes of items

Marketplace at Westfield

230.5 hours of volunteering by non-exempt associates

Numerous other community-focused events and countless

volunteer hours from exempt associates

•

•

•

•

•

• |

2014

EARNINGS TARGETS BANK

$2,850,000

BANCORP

$2,286,000 |

STOCK

PERFORMANCE Source: SNL Financial

Change %

As of 5/7/2014

YTD

1 Year

3 Years

SNL Bank & Thrift

(3.46)

16.50

34.26

SNL Bank < $500mm

7.29

21.65

43.87

KBW Bank

(3.08)

16.38

32.33

NASDAQ Bank

(5.68)

18.32

36.84

SNL Micro Cap

2.99

16.91

49.76

ASBI

5.66

50.54

181.63 |

AMERIANA FRANCHISE

HIGHLIGHTS

Focused on maintaining and improving shareholder

value

Improved operating fundamentals

o

Growth strategies focused on building relationships,

growing deposits and fee revenue

Investments in Indianapolis area are producing results

Well-capitalized with ability to support further organic

growth

Able to effectively manage to increased regulatory

requirements

19 quarters of profitability through first quarter of 2014

•

•

•

•

•

• |

QUESTIONS? |