Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - TWO RIVERS WATER & FARMING Co | Financial_Report.xls |

| EX-10.1 - LIMITED LIABILITY COMPANY AGREEMENT - TWO RIVERS WATER & FARMING Co | turv_ex101.htm |

| EX-10.3 - EXCHANGE AGREEMENT - TWO RIVERS WATER & FARMING Co | turv_ex103.htm |

| EX-31.2 - CERTIFICATION - TWO RIVERS WATER & FARMING Co | turv_ex312.htm |

| EX-32.2 - CERTIFICATION - TWO RIVERS WATER & FARMING Co | turv_ex322.htm |

| EX-32.1 - CERTIFICATION - TWO RIVERS WATER & FARMING Co | turv_ex321.htm |

| EX-31.1 - CERTIFICATION - TWO RIVERS WATER & FARMING Co | turv_ex311.htm |

| EX-10.2 - MEMBERSHIP INTEREST PURCHASE AGREEMENT - TWO RIVERS WATER & FARMING Co | turv_ex102.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

|

(Mark One)

|

|

|

þ

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended March 31, 2014

|

|

Or

|

|

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

|

|

|

EXCHANGE ACT OF 1934

|

|

|

For the transition period from _________ to _____________

|

Commission file number: 000-51139

Two Rivers Water & Farming Company

(Exact Name of Registrant as Specified in Its Charter)

|

Colorado

|

13-4228144

|

|

(State or Other Jurisdiction or

Incorporation or Organization)

|

(I.R.S. Employee

Identification No.)

|

|

2000 South Colorado Blvd.

Tower 1, Suite 3100

Denver, Colorado

|

80222

|

|

(Address of Principal Executive Offices)

|

(Zip Code)

|

Registrant’s telephone number, including area code: (303) 222-1000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One).

|

Large accelerated filer

|

o

|

Accelerated filer

|

o

|

|

|

Non-accelerated filer

(Do not check if a smaller reporting company)

|

o

|

Smaller reporting company

|

þ

|

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No þ

As of May 13, 2014 there were 24,879,549 shares outstanding of the registrant's Common Stock.

TABLE OF CONTENTS

|

Page

|

||

|

PART I – FINANCIAL INFORMATION

|

||

|

Item 1.

|

Financial Statements

|

3

|

|

Item 2.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

15

|

|

Item 3.

|

Quantitative and Qualitative Disclosures About Market Risk

|

18

|

|

Item 4.

|

Controls and Procedures

|

18

|

|

PART II – OTHER INFORMATION

|

||

|

Item 1A.

|

Risk Factors

|

19

|

|

Item 6.

|

Exhibits

|

19

|

|

SIGNATURES

|

20

|

|

2

PART I. OTHER INFORMATION

ITEM 1. FINANCIAL STATEMENTS

|

Page

|

|

|

Financial Statements (Unaudited):

|

|

|

Condensed Consolidated Balance Sheets – March 31, 2014 and December 31, 2013

|

4

|

|

Condensed Consolidated Statements of Operations – Three months ended March 31, 2014 and 2013

|

5

|

|

Condensed Consolidated Statements of Cash Flows – Three months ended March 31, 2014 and 2013

|

6

|

|

Notes to Condensed Consolidated Financial Statements

|

7

|

3

TWO RIVERS WATER & FARMING COMPANY AND SUBSIDIARIES

Condensed Consolidated Balance Sheets (In Thousands)

|

March 31, 2014

|

December 31, 2013

|

||||||||

|

ASSETS:

|

(Unaudited)

|

(Derived from Audit)

|

|||||||

|

Current Assets:

|

|||||||||

|

Cash and cash equivalents

|

$ | 2,184 | $ | 2,069 | |||||

|

Advances and accounts receivable, net

|

9 | 54 | |||||||

|

Farm product

|

321 | 29 | |||||||

|

Deposits and other current assets

|

121 | 108 | |||||||

|

Total Current Assets

|

2,635 | 2,260 | |||||||

|

Long Term Assets:

|

|||||||||

|

Property, equipment and software, net

|

1,959 | 1,892 | |||||||

|

Land and real estate, net

|

4,978 | 4,978 | |||||||

|

Water assets

|

31,449 | 31,507 | |||||||

|

Intangible assets, net

|

984 | 997 | |||||||

|

Other long term assets

|

71 | 68 | |||||||

|

Total Long Term Assets

|

39,441 | 39,442 | |||||||

|

TOTAL ASSETS

|

$ | 42,076 | $ | 41,702 | |||||

|

LIABILITIES & STOCKHOLDERS' EQUITY:

|

|||||||||

|

Current Liabilities:

|

|||||||||

|

Accounts payable

|

$ | 136 | $ | 47 | |||||

|

Accrued liabilities

|

347 | 317 | |||||||

|

Preferred shares and membership dividends payable

|

470 | - | |||||||

|

Current portion of long term debt (Note 4)

|

1,385 | 2,759 | |||||||

|

Total Current Liabilities

|

2,338 | 3,123 | |||||||

|

Long Term Debt (Note 4)

|

11,439 | 12,961 | |||||||

|

Total Liabilities

|

13,777 | 16,084 | |||||||

|

Commitments and contingencies (Note 4)

|

|||||||||

|

Stockholders' Equity:

|

|||||||||

|

Convertible preferred shares, $0.001 par value, 4,000,000 shares authorized, 3,494,000 shares outstanding at March 31, 2014 and 3,794,000 shares outstanding at December 31, 2013 (liquidation value of $3,494,000 and $3,794,000, respectively), net

|

2,627 | 2,851 | |||||||

|

Common stock, $0.001 par value, 100,000,000 shares authorized, 24,879,549 shares issued and outstanding at March 31, 2014 and December 31, 2013

|

25 | 25 | |||||||

|

Additional paid-in capital

|

61,114 | 60,220 | |||||||

|

Accumulated (deficit)

|

(49,509 | ) | (47,449 | ) | |||||

|

Total Two Rivers Water Company Shareholders' Equity

|

14,257 | 15,647 | |||||||

|

Noncontrolling interest in subsidiaries

|

14,042 | 9,971 | |||||||

|

Total Stockholders' Equity

|

28,299 | 25,618 | |||||||

|

TOTAL LIABILITIES & STOCKHOLDERS' EQUITY

|

$ | 42,076 | $ | 41,702 | |||||

The accompanying notes to condensed consolidated financial statements are an integral part of these statements.

4

TWO RIVERS WATER & FARMING COMANY AND SUBSIDIARIES

Condensed Consolidated Statements of Operations (In Thousands)

|

Three months ended March 31,

|

||||||||

|

2014

|

2013

|

|||||||

|

Revenue

|

||||||||

|

Other income

|

$ | 5 | $ | - | ||||

|

Total Revenue

|

5 | - | ||||||

|

Direct cost of revenue

|

- | - | ||||||

|

Gross Profit (Loss)

|

5 | - | ||||||

|

Operating Expenses:

|

||||||||

|

General and administrative

|

838 | 1,856 | ||||||

|

Depreciation

|

125 | 129 | ||||||

|

Total operating expenses

|

963 | 1,985 | ||||||

|

(Loss) from operations

|

(958 | ) | (1,985 | ) | ||||

|

Other income (expense):

|

||||||||

|

Interest expense

|

(335 | ) | (173 | ) | ||||

|

Warrant expense

|

- | (28 | ) | |||||

|

Other Income

|

11 | 5 | ||||||

|

Total other income (expense)

|

(324 | ) | (196 | ) | ||||

|

Net (Loss) before taxes

|

(1,282 | ) | (2,181 | ) | ||||

|

Income tax (provision) benefit

|

- | - | ||||||

|

Net (Loss) before preferred dividends and non-controlling interest

|

(1,282 | ) | (2,181 | ) | ||||

|

Preferred Dividends

|

(470 | ) | - | |||||

|

Net loss attributable to the noncontrolling interest

|

- | 1 | ||||||

|

Net (Loss) attributable to Two Rivers Water Company

|

$ | (1,752 | ) | $ | (2,180 | ) | ||

|

(Loss) Per Common Stock Share - Basic and Dilutive:

|

$ | (0.07 | ) | $ | (0.09 | ) | ||

|

Weighted Average Shares Outstanding:

|

||||||||

|

Basic and Dilutive

|

24,880 | 24,310 | ||||||

The accompanying notes to condensed consolidated financial statements are an integral part of these statements.

5

TWO RIVERS WATER & FARMING COMPANY AND SUBSIDIARIES

Condensed Consolidated Statements of Cash Flows (In Thousands)

|

For the three months ended March 31,

|

||||||||

|

2014

|

2013

|

|||||||

|

Cash Flows from Operating Activities:

|

||||||||

|

Net (Loss)

|

$ | (1,752 | ) | $ | (2,180 | ) | ||

|

Adjustments to reconcile net income or (loss) to net cash (used in) operating activities:

|

||||||||

|

Depreciation and amortization

|

125 | 129 | ||||||

|

Accretion of debt discount

|

47 | - | ||||||

|

Assumption of assessments due to purchase of HCIC shares

|

- | 80 | ||||||

|

Stock based compensation

|

- | 680 | ||||||

|

Stock and options for services

|

64 | 763 | ||||||

|

Gain on disposal of assets

|

(3 | ) | - | |||||

|

Impairment of asset

|

34 | - | ||||||

|

Net change in operating assets and liabilities:

|

||||||||

|

Decrease (increase) in advances & accounts receivable

|

44 | 82 | ||||||

|

(Increase) in farm product

|

(292 | ) | (112 | ) | ||||

|

(Increase) decrease in deposits, prepaid expenses and other assets

|

(16 | ) | (248 | ) | ||||

|

Increase (decrease) in accounts payable

|

50 | (30 | ) | |||||

|

Increase (decrease) in accrued liabilities and other

|

499 | (163 | ) | |||||

|

Net Cash (Used in) Operating Activities

|

(1,200 | ) | (999 | ) | ||||

|

Cash Flows from Investing Activities:

|

||||||||

|

Purchase of property, equipment and software

|

(42 | ) | (6 | ) | ||||

|

Purchase of land, water shares, infrastructure

|

- | (1,315 | ) | |||||

|

Net Cash (Used in) Investing Activities

|

(42 | ) | (1,321 | ) | ||||

|

Cash Flows from Financing Activities:

|

||||||||

|

Proceeds from Preferred Units

|

1,700 | - | ||||||

|

Proceeds from long-term debt

|

- | 1,050 | ||||||

|

Proceeds from sale of convertible preferred shares in DFP

|

- | 1,600 | ||||||

|

Payment of offering costs

|

- | (223 | ) | |||||

|

Payment on notes payable

|

(343 | ) | (133 | ) | ||||

|

Net Cash Provided by Financing Activities

|

1,357 | 2,294 | ||||||

|

Net (Decrease) Increase in Cash & Cash Equivalents

|

115 | (26 | ) | |||||

|

Beginning Cash & Cash Equivalents

|

2,069 | 1,340 | ||||||

|

Ending Cash & Cash Equivalents

|

$ | 2,184 | $ | 1,314 | ||||

|

Supplemental Disclosure of Cash Flow Information

Cash paid for interest

|

$ | 202 | $ | 148 | ||||

The accompanying notes to condensed consolidated financial statements are an integral part of these statements

6

TWO RIVERS WATER & FARMING COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

For the Three Months Ended March 31, 2014 and March 31, 2013

(Unaudited)

NOTE 1 – ORGANIZATION AND BUSINESS

Corporate Information

Two Rivers Water & Farming Company (the “Company”) is a Colorado corporation with principal executive offices at 2000 South Colorado Boulevard, Tower 1, Suite 3100, Denver, Colorado, and our telephone number at that address is (303) 222-1000.

Organizational Restructuring

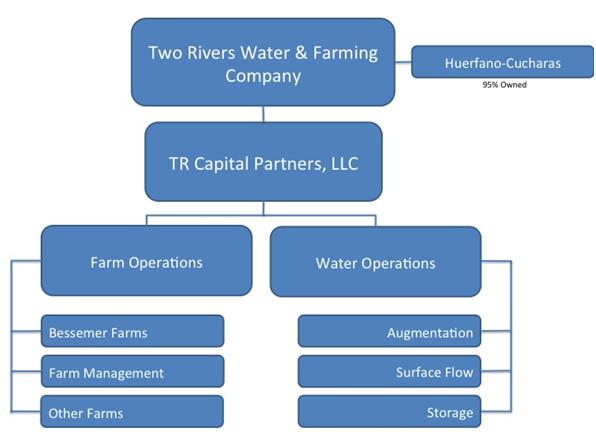

On January 29, 2014, the board of directors approved a plan to reorganize the Company’s subsidiaries in a more integrated manner based on functional operations. The Company formed a new company, TR Capital Partners, LLC (“TR Capital”), which issued all of its Common Units to the Company. TR Capital then initiated the transactions described below. Following the completion of those transactions in mid-2014, the Company expects that TR Capital and its other direct and indirect subsidiaries (excluding HCIC Holdings, LLC, or “HCIC,” and Huerfano-Cucharas Irrigation Company) (the “Transferring Subsidiaries”) will enter into a series of related transactions as the result of which assets and operations of the Transferring Subsidiaries will be transferred to TR Capital. As a result of those transactions, TR Capital would operate all of the operations formerly conducted by the Transferring Subsidiaries. The following chart shows the expected corporate organization following completion of the anticipated transactions among the Transferring Subsidiaries, as well as the principal operating areas to be managed by TR Capital:

The placement of Preferred Units is being effectuated by either (1) the holders of certain debt or equity securities of the Transferring Subsidiaries exchanging their ownership interest or debt holdings for Preferred Units or (2) the direct investment into TR Capital through the cash purchase of Preferred Units. These debt or equity securities or the cash consideration to purchase Preferred Units are collectively referred to as “Qualified Assets.”

7

The Qualified Assets are being exchanged into Preferred Units at a rate of $0.70 or $1.00. If new capital (cash) is invested in Preferred Units, for each new $1.00 of new capital, another $1.2988 of Qualified Assets can be converted into Preferred Units at a rate of $0.70. Additionally, the new capital (cash) purchases Preferred Units at a rate of $0.70. All other Qualified Assets are being exchanged into Preferred Units at a rate of $1.00.

The Preferred Units provide the member with the following:

|

●

|

The ability, upon exchange, to receive one share of the Company’s common stock and a warrant to purchase one-half of one share of the Company’s common stock for each Preferred Unit owned. The warrants expire five years after issuance and have a strike price of $2.10.

|

|

●

|

A quarterly dividend of 2% (8% annually) based on the consideration exchanged or paid for the Preferred Units.

|

|

●

|

An annual distribution based on the Adjusted Gross Profit (as defined) of the Company.

|

Basis of Presentation

The accompanying unaudited Consolidated Financial Statements do not include all of the disclosures required by accounting principles generally accepted in the U.S. (“GAAP”), pursuant to the rules and regulations of the SEC. The unaudited Consolidated Financial Statements reflect all adjustments, which, in the opinion of management, are necessary to present fairly the consolidated financial position of the Company as of March 31, 2014, and the consolidated results of operations and comprehensive income and cash flows of the Company for the three months ended March 31, 2014 and 2013. Operating results for the three months ended March 31, 2014 and due to the seasonality of the agriculture business are not necessarily indicative of the results that may be expected for the year ending December 31, 2014.

These unaudited Consolidated Financial Statements should be read in conjunction with the Company’s audited Consolidated Financial Statements and footnotes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013.

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of Two Rivers and its subsidiaries, TR Capital Partners, LLC and HCIC. All significant inter-company balances and transactions have been eliminated in consolidation.

Non-controlling Interest

Non-controlling interest is recorded for the ownership of HCIC not owned by the Company, for preferred shares not owned by the Company in the Company’s subsidiaries and for the TR Capital Preferred Units. Below is the detail of non-controlling interest shown on the balance sheet:

|

Entity

|

Mar 31, 2014

|

Dec 31, 2013

|

||||||

|

TR Capital

|

$ | 5,151,000 | $ | - | ||||

|

HCIC

|

1,363,000 | 1,363,000 | ||||||

|

Two Rivers Farms F-1, Inc.1

|

735,000 | 1,494,000 | ||||||

|

Two Rivers Farms F-2, Inc.1

|

3,806,000 | 3,933,000 | ||||||

|

Dionisio Farms & Produce, Inc. (“DFP”)1

|

2,987,000 | 3,181,000 | ||||||

|

Totals

|

$ | 14,042,000 | $ | 9,971,000 | ||||

1These entities will be owned by TR Capital after the organizational restructuring detailed in Note 1 is completed.

Based on ASC 815-40-25, the Company classified the TR Capital Preferred Units as permanent equity. Further, pursuant to the ASC 810-10, the Company determined that the TR Capital Preferred Units should be classified as a non-controlling interest in a subsidiary and shown separately within the Equity section of the Company’s Consolidated Balance Sheet.

Pursuant to ASC 470-20, the Company valued the Preferred Units by assessing the fair market value of the preferred units and the warrants and allocating those values to the face value of the Preferred Units.

8

The Preferred Units were valued based on the number of common shares into which the Preferred Units can be exchanged and the Company’s common share price on the date of the exchange. The Qualified Assets were exchange between February 1, 2014 and February 4, 2014. The common share price during those dates ranged from $0.85 to $0.90 per share. In total, the 8,924,286 Preferred Units have a fair market value of $7,799,000 based on these common share prices.

The fair market value of the warrants underlying the Preferred Units was determined using the Black Scholes model. Assumptions underlying the Black Scholes model were as follows:

|

Conversion Date

|

2/1/14 - 2/4/14

|

|||

|

Stock Price

|

$ | 0.85 - $0.90 | ||

|

Exercise Price

|

$ | 2.10 | ||

|

Term (in years)

|

5 | |||

|

Volatility

|

74.34 | % | ||

|

Annual Rate of Quarterly Dividends

|

0 | % | ||

|

Discount Rate - Bond Equivalent Yield

|

1.46% - 1.49 | % | ||

In total, the warrants underlying the Preferred Units have a fair market value of $1,659,000 based on these assumptions.

Reclassification

Certain amounts previously reported have been reclassified to conform to current presentation. Certain labels of accounts/classifications have been changed.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions. These estimates and assumptions affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported period. Actual results could differ materially from those estimates.

Cash and Cash Equivalents

For purposes of reporting cash flows, the Company considers cash and cash equivalents to include highly liquid investments with original maturities of 90 days or less. Those are readily convertible into cash and not subject to significant risk from fluctuations in interest rates. The recorded amounts for cash equivalents approximate fair value due to the short-term nature of these financial instruments.

Farm product

Farm product represents expenses directly attributed to the planting and cultivation of crop. Upon harvesting, the farm product is reduced in proportion of the revenue generated. The reduction of the farm product is recognized as direct cost of revenue.

Property and Equipment

Property and equipment are stated at cost less accumulated depreciation. Depreciation is computed principally on the straight-line method over the estimated useful life of each type of asset which ranges from three to twenty seven and a half years. Maintenance and repairs are charged to expense as incurred; improvements and betterments are capitalized. Upon retirement or disposition, the related costs and accumulated depreciation are removed from the accounts, and any resulting gains or losses are credited or charged to income.

9

Below is a summary of premises and equipment:

|

Asset Type

|

Life in Years

|

Mar 31, 2014

|

Dec 31, 2013

|

|||||||||

|

Office equipment, furniture, computers

|

5 – 7 | $ | 11,000 | $ | 11,000 | |||||||

|

Computers

|

3 | 40,000 | 40,000 | |||||||||

|

Vehicles

|

5 | 45,000 | 45,000 | |||||||||

|

Farm equipment

|

7 - 10 | 1,527,000 | 1,411,000 | |||||||||

|

Irrigation system

|

10 | 989,000 | 989,000 | |||||||||

|

Buildings

|

27.5 | 35,000 | 35,000 | |||||||||

|

Website

|

3 | 7,000 | 7,000 | |||||||||

|

Subtotal

|

2,654,000 | 2,538,000 | ||||||||||

|

Less Accumulated Depreciation

|

(695,000 | ) | (646,000 | ) | ||||||||

|

Net Book Value

|

$ | 1,959,000 | $ | 1,892,000 | ||||||||

Land

Land acquired for farming is recorded at cost. Some of the land acquired has not been farmed for many years, if not decades. Therefore, additional expenditures are required to make the land ready for efficient farming. Expenditures for leveling the land are added to the cost of the land. Irrigation is not capitalized in the cost of Land (Property and Equipment above). Land is not depreciated. However, once per year, management will assess the value of land held, and in their opinion, if the land has become impaired, management will establish an allowance against the land.

Water rights and infrastructure

Subsequent to purchase of water rights and water infrastructure, management periodically evaluates the carrying value of its assets, and if the carrying value is in excess of fair market value, the Company will establish an impairment allowance. Currently, there are no impairments on the Company’s land and water shares. No amortization or depreciation is taken on the water rights.

Intangibles

The Company recognizes the estimated fair value of water rights acquired by the Company’s purchase of equity interests in HCIC and Orlando Reservoir No. 2 Company, LLC (“Orlando”). These intangible assets will not be amortized because they have an indefinite remaining useful life based on many factors and considerations, including, the historical upward valuation of water rights within Colorado.

Revenue Recognition

Farm Revenues

Revenues from farming operations are recognized when sold into the market. All direct expenses related to farming operations are capitalized as farm inventory and recognized as a direct cost of sale upon the sale of the crops.

Water Revenues

Current water revenues are from the lease of water own by HCIC to farmers in the HCIC service area and through re-leasing of water from the Pueblo Board of Water lease. Water revenues are recognized when the water is consumed.

Member Assessments

Once per year the HCIC board estimates HCIC’s expenses, less anticipated water revenues, and establishes an annual assessment per ownership share. One-half of the member assessment is recorded in the first quarter of the calendar year and the other one-half of the member assessment is recorded in the third quarter of the calendar year. Assessments paid by the Company to HCIC are eliminated in consolidation of the financial statements.

HCIC does not reserve against any unpaid assessments. Assessments due, but unpaid, are secured by the member’s ownership of HCIC. The value of this ownership is significantly greater than the annual assessments.

10

Stock Based Compensation

Beginning January 1, 2006, the Company adopted the provisions of ASC 718 and accounts for stock-based compensation in accordance with ASC 718. Under the fair value recognition provisions of this standard, stock-based compensation cost is measured at the grant date based on the fair value of the award and is recognized as expense on a straight-line basis over the requisite service period, which generally is the vesting period. The Company elected the modified-prospective method, under which prior periods are not revised for comparative purposes. The valuation provisions of ASC 718 apply to new grants and to grants that were outstanding as of the effective date and are subsequently modified.

All options granted prior to the adoption of ASC 718 and outstanding during the periods presented were fully vested at the date of adoption.

In December 2007, the SEC issued Staff Accounting Bulletin (“SAB”) 110 which was issued to express the understanding that the use of a “simplified” method, as discussed in SAB 107 in developing an estimate of expected term of “plain vanilla” share options in accordance with ASC 718 would be acceptable beyond December 31, 2007. The Company adopted this standard beginning January 2008.

Net Income (Loss) per Share

Basic net income per share is computed by dividing net income (loss) attributed to the Company available to common shareholders for the period by the weighted average number of common shares outstanding for the period. Diluted net income (loss) per share is computed by dividing the net income for the period by the weighted average number of common and potential common shares outstanding during the period.

The dilutive effect of the outstanding 3,122,615 RSUs, 2,014,867 options and 9,890,209 warrants at March 31, 2014, has not been included in the determination of diluted earnings per share since, under ASC 260 they would anti-dilutive.

Recently issued Accounting Pronouncements

In July 2013, the FASB issued Accounting Standards Update No. 2013-11, “Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists” (“ASU No. 2013-11”). ASU No. 2013-11 requires an entity to present an unrecognized tax benefit, or a portion of an unrecognized tax benefit, in the financial statements as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss, or a tax credit carryforward, with limited exceptions. ASU No. 2013-11 is effective for interim and annual periods beginning after December 15, 2013 and may be applied retrospectively. The adoption of the provisions of ASU No. 2013-11 is not expected to have a material impact on the company’s financial position or results of operations.

Management does not believe that any other recently issued, but not effective, accounting standards if currently adopted would have a material effect on the accompanying consolidated financial statements.

11

NOTE 3 – INVESTMENTS AND LONG-LIVED ASSETS

Land

Upon purchasing land, the value is recorded at the purchase price or fair value, whichever is more accurate. Costs incurred to prepare the land for the intended purpose, which is efficient irrigated farming, is also capitalized in the recorded cost of the land. No amortization or depreciation is taken on land. However the land is reviewed by management at least once per year to ascertain if a further analysis is necessary for any potential impairments.

Water rights and infrastructure

The Company has acquired both direct flow water rights and water storage rights. It has obtained water rights through the purchase of shares in a mutual ditch company, which it accomplished through its purchase of shares in HCIC, or through the purchase of an entity holding water rights, which it effected through its purchase of a membership interest of Orlando. The Company may also acquire water rights through outright purchase. In all cases, such rights are recognized under decrees of the Colorado water court and administered under the jurisdiction of the Office of the State Engineer.

Upon purchasing water rights, the value is recorded at our purchase price. If a majority interest is acquired in a company holding water assets (potentially with other assets including water delivery infrastructure, right of ways, and land), the Company determines the fair value of the assets. To assist with the valuation, the Company may consider reports from a third-party valuation firm. If the value of the water rights is greater than what the Company paid then a bargain purchase gain is recognized. If the value of the water assets are less than what the Company paid then goodwill is recognized.

Subsequent to purchase, management periodically evaluates the carrying value of its assets, and if the carrying value is in excess of fair market value, the Company will establish an impairment allowance. Currently, there are no impairments on the Company’s land and water shares. No amortization or depreciation is taken on the water rights.

Dam and water infrastructure construction in progress

The Company has commenced engineering for the reconstruction of the dam owned by the HCIC. In addition the Company is in the process of rehabilitating various outlet gates, pipes and water gates. These costs are capitalized, and not amortized or depreciated until the dam reconstruction is completed in accordance with ASC 360 and 835.

Reconstruction costs are as follows:

|

3 months ended

|

Year ended

|

|||||||

|

Mar 31, 2014

|

Dec 31, 2013

|

|||||||

|

Beginning balance

|

$ | 34,000 | $ | 34,000 | ||||

|

Additions

|

- | - | ||||||

|

Written off

|

34,000 | - | ||||||

|

Ending Balance

|

$ | - | $ | 34,000 | ||||

Intangible Assets

The Company acquired the Dionisio produce business and related equipment for $1,873,000 plus accrued interest of $30,000. The purchase price was allocated as follows:

|

Produce business

|

$ | 1,037,000 | ||

|

Equipment

|

836,000 | |||

|

Prepaid interest

|

30,000 | |||

|

Ending Balance

|

$ | 1,903,000 |

12

Based on the discounted cash flow analysis and assuming the average life of a customer is 20 years, the produce business has the following values:

|

Mar. 31, 2014

|

Dec. 31, 2013

|

|||||||

|

Customer list

|

$ | 580,000 | $ | 580,000 | ||||

|

Tradename

|

220,000 | 220,000 | ||||||

|

Residual goodwill

|

237,000 | 237,000 | ||||||

|

Purchase price

|

1,037,000 | 1,037,000 | ||||||

|

Less: Accumulated amortization

|

(53,000 | ) | (40,000 | ) | ||||

|

Intangible assets, net

|

$ | 984,000 | $ | 997,000 | ||||

The cost of the customer list and the tradename will be amortized on a straight-line basis over 20 years. The total amortization is $40,000 per year. The residual goodwill will be tested in December in each year for impairments, if any.

NOTE 4 – NOTES PAYABLE

Below is a summary of the Company’s long term debt:

|

Mar 31, 2014

|

|||||||||||||||||

|

Note

|

Dec 31, 2013 Principal Bal.

|

Principal balance

|

Accrued interest

|

Interest rate

|

Security

|

||||||||||||

|

HCIC seller carry back

|

$ | 7,896,000 | $ | 7,719,000 | $ | - | 6 | % |

Shares in the Mutual Ditch Company

|

||||||||

|

Orlando seller carry back

|

188,000 | 188,000 | 33,000 | 7 | % |

188 acres of land

|

|||||||||||

|

Series A convertible debt

|

110,000 | 85,000 | 6,000 | 6 | % |

F-1 assets

|

|||||||||||

|

Series B convertible debt

|

405,000 | 405,000 | 30,000 | 6 | % |

F-2 assets

|

|||||||||||

|

CWCB

|

1,151,000 | 1,104,000 | 3,000 | 2.5 | % |

Certain Orlando and Farmland assets

|

|||||||||||

|

FirstOak Bank - Dionisio Farm

|

826,000 | 826,000 | 12,000 | (1 | ) |

Dionisio farmland and 146.4 shares of Bessemer Irrigating Ditch Company Stock, well permits

|

|||||||||||

|

Seller Carry Back - Dionisio

|

590,000 | 590,000 | 9,000 | 6.0 | % |

Unsecured

|

|||||||||||

|

FirstOak Bank - Mater

|

166,000 | 166,000 | 3,000 | (1 | ) |

Secured by Mater assets purchased

|

|||||||||||

|

Seller Carry Back - Mater

|

25,000 | 25,000 | - | 6.0 | % |

Land from Mater purchase

|

|||||||||||

|

McFinney Agri-Finance

|

645,000 | 644,000 | - | 6.8 | % |

2,579 acres of pasture land in Ellicott Colorado

|

|||||||||||

|

Ellicott second mortgage

|

400,000 | 400,000 | - | 12.0 | % |

Second lien on above Ellicott land

|

|||||||||||

|

ASF Note holders

|

2,036,000 | 528,000 | - | 8.0 | % |

ASF assets

|

|||||||||||

|

Bridge Notes

|

1,300,000 | - | - | 12.0 | % |

Unsecured

|

|||||||||||

|

Kirby Group

|

45,000 | 105,000 | - | 6.0 | % | ||||||||||||

|

Equipment loans

|

485,000 | 540,000 | 8,000 | 5 - 8 | % |

Specific equipment

|

|||||||||||

|

Total

|

16,268,000 | 13,325,000 | $ | 104,000 | |||||||||||||

|

Less: HCIC Discount

|

(548,000 | ) | (501,000 | ) | |||||||||||||

|

Less: Current portion

|

(2,759,000 | ) | (1,385,000 | ) | |||||||||||||

|

Long Term portion

|

$ | 12,961,000 | $ | 11,439,000 | |||||||||||||

Note 1: Prime rate +1%, but not less than 6%

13

NOTE 5 – INFORMATION ON BUSINESS SEGMENTS

The Company organizes its business segments based on the nature of the products and services offered. It focuses on water and farming with Two Rivers Water & Farming Company as the parent company. Therefore, it reports its segments by these lines of businesses: Farms and Water. Farms contain all of farming activity. Water contains all of our water activity. Our parent category is not a separate reportable operating segment. Segment allocations may differ from those on the face of the income statement.

In the following tables of financial data, the total of the operating results of these business segments is reconciled, as appropriate, to the corresponding consolidated amount. There are some corporate expenses that were not allocated to the business segments, and these expenses are contained in the “Total Operating Expenses” under Parent.

Operating results for each of the segments of the Company are as follows (in thousands):

|

For the three months ended March 31, 2014

|

For the three months ended March 31, 2013 | ||||||||||||||||||||||||||||||||

|

Parent

|

Farms

|

Water

|

Total

|

Parent

|

Farms

|

Water

|

Total

|

||||||||||||||||||||||||||

|

Revenue

|

|||||||||||||||||||||||||||||||||

|

Other & misc.

|

$ | - | $ | 2 | $ | 3 | $ | 5 | $ | - | $ | - | $ | - | $ | - | |||||||||||||||||

|

Less: direct cost of revenue

|

- | - | - | - | - | - | - | - | |||||||||||||||||||||||||

|

Gross Margin

|

- | 2 | 3 | 5 | - | - | - | - | |||||||||||||||||||||||||

|

Expenses

|

|||||||||||||||||||||||||||||||||

|

Total operating expenses

|

860 | 118 | 66 | 1,045 | 1,200 | 533 | 252 | 1,985 | |||||||||||||||||||||||||

|

Total other expense

|

300 | 8 | 14 | 322 | 39 | 25 | 132 | 196 | |||||||||||||||||||||||||

|

Income (Loss) from operations before taxes

|

(1,160 | ) | (124 | ) | (77 | ) | (1,362 | ) | (1,239 | ) | (558 | ) | (384 | ) | (2,181 | ) | |||||||||||||||||

|

Income Taxes (Expense)/Credit

|

- | - | - | - | - | - | - | - | |||||||||||||||||||||||||

|

Net (loss)

|

(1,160 | ) | (124 | ) | (77 | ) | (1,362 | ) | (1,239 | ) | (558 | ) | (384 | ) | (2,181 | ) | |||||||||||||||||

|

Non-controlling interest

|

- | - | - | - | - | - | 1 | 1 | |||||||||||||||||||||||||

|

Preferred Dividends

|

390 | - | - | 390 | - | - | - | - | |||||||||||||||||||||||||

|

Net (Loss) Income

|

$ | (1,551 | ) | $ | (124 | ) | $ | (77 | ) | $ | (1,752 | ) | $ | (1,239 | ) | $ | (558 | ) | $ | (383 | ) | $ | (2,180 | ) | |||||||||

|

Segment assets

|

$ | 1,763 | $ | 12,981 | $ | 27,332 | $ | 42,076 | $ | 304 | $ | 12,485 | $ | 33,029 | $ | 45,818 | |||||||||||||||||

NOTE 6 – EQUITY TRANSACTIONS

Common Stock

During the three months ended March 31, 2013, the Company had the following common stock transactions:

|

●

|

In February 2013 the Company issued 179,348 shares of our common stock to a consultant for work performed in 2012.

|

|

●

|

In February 2013 the Company issued 85,000 shares of our common stock to the independent members of the Board in exchange for Board of Director services rendered in 2012.

|

|

●

|

In March 2013 the Company issued 200,000 shares of our common stock to a consultant for investor relations work performed in first quarter, 2013.

|

|

●

|

In March 2013 the Company issued 100,000 shares of our common stock to an independent member of the DFP Board of Directors in exchange for services.

|

During the three months ended March 31, 2014, the Company had no common stock transactions.

NOTE 7 – SUBSEQUENT EVENTS

There were no material subsequent events through the date the financial statements were available to be issued.

14

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Unless the context requires otherwise, references in this Form 10-Q to “we,” “our,” “us” and similar terms refer to Two Rivers Water & Farming Company and its subsidiaries.

Note about Forward-Looking Statements

This Form 10-Q contains forward-looking statements, such as statements relating to our financial condition, results of operations, plans, objectives, future performance and business operations. These statements relate to expectations concerning matters that are not historical facts. These forward-looking statements reflect our current views and expectations based largely upon the information currently available to us and are subject to inherent risks and uncertainties. Although we believe our expectations are based on reasonable assumptions, they are not guarantees of future performance and there are a number of important factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements. By making these forward-looking statements, we do not undertake to update them in any manner except as may be required by our disclosure obligations in filings we make with the Securities and Exchange Commission under the Federal securities laws. Our actual results may differ materially from our forward-looking statements.

Overview

Currently, there is a significant arbitrage between the value of irrigation water and municipal water in the semi-arid regions of the southwestern United States. The arbitrage is amplified by a predicted water supply shortage for municipalities in the near future. The arbitrage results in a 5-10 fold increase in the price of municipal water over irrigation water. First generation western water business models attempted to capture the arbitrage by “buying and drying” irrigated farmland in order to sell the irrigation water to municipalities. The practice fallowed some of the most productive irrigated farmland and decimated entire agricultural communities. The buy and dry model failed to generate any significant revenues and earnings for investors as political and legal challenges developed. The buy and dry model became politically, economically and legally untenable. In the late 19th century, 85% of all water rights were granted to and are still primarily held by agriculture interests. Since then, populations have increased and people have moved from the farm to the city. This has resulted in a water shortage for municipalities, for which there must be a solution. Two Rivers has developed a more viable and sustainable solution than the buy and dry practices of the past.

Our business model reinvigorates, rather than decimates, agricultural communities and provides excess water to municipalities through market forces. Our core business converts irrigated farmland, which is marginally profitable growing low value feed crops, into highly profitable irrigated farmland growing high yield, high value, fruit and vegetable crops. Fruit & vegetable crops generate six times the revenue of feed crops with better margins. As a result of our higher revenue and better margins, we can afford to and are willing to pay a higher price for water. As the price of water increases, so does the supply. Farmers receive more for their crops and water. Municipal consumers pay more for excess water and make better water choices. The water arbitrage shrinks. Water supply and demand reaches equilibrium. Market action, between satisfied buyers and sellers from both the agricultural and municipal communities, rather than insurmountable political and legal processes, is the driving force of our business.

Our financial returns far outpace the revenues and margins generated by first generation western water business models. In the agricultural communities where we operate, we create new and better paying jobs for farming, marketing, handling and processing vegetables. In the municipal communities, we provide wholesale water not necessary for our core business, agriculture. We concentrate our acquisitions on water rights and infrastructure that are, in part, owned by municipalities, thereby letting the municipalities do the heavy legal and political lifting necessary to obtain excess water.

Results of Operations

For the Three Months Ended March 31, 2014, Compared to the Three Months Ended March 31, 2013

During the three months ended March 31, 2014 and March 31, 2013, we recognized no revenues from our farming operations and $5,000 versus $ -0- from other sources, respectively.

15

Operating expenses from continuing operations during the three months ended March 31, 2014 and 2013 were $963,000 and $1,985,000, respectively. The decrease of $1,022,000 was primarily due to the decrease of non-cash expense of granting of restrictive stock units (no expense for the three months ended March 31, 2014 compared to $680,000 for the three months ended March 31, 2013) and a reduction is stock and options issued for services ($64,000 for the three months ended March 31, 2014 compared to $763,000 for the three months ended March 31, 2013).

For operations, during the three months ended March 31, 2014 and 2013, we recognized a net loss of $958,000 and $1,985,000, respectively. The decreased loss of $1,027,000 is due primarily to the reasons stated above.

Net loss attributed to Two Rivers for the three months ended March 31, 2014 was $1,752,000, compared to a loss of $2,180,000 for the three months ended March 31, 2013. The decrease of $428,000 is due primarily to the reasons stated above, offset in part by declared dividends and distributions to Dionisio Farms & Produce, Inc. and TR Capital Partners, LLC, or TR Capital.

Liquidity and Capital Resources

From our inception through March 31, 2014, we have funded our operations primarily from the following sources:

|

-

|

Equity proceeds through private placements of Two Rivers Water & Farming Company and subsidiaries securities;

|

|

-

|

Revenue generated from operations;

|

|

-

|

Loans and lines of credit;

|

|

-

|

Sales of residential properties acquired through deed-in-lieu of foreclosure actions;

|

|

-

|

Sales of equity investments, and

|

|

-

|

Proceeds from the exercise of options.

|

As of March 31, 2014, we had no available line or letters of credit and do not intend to seek any such financing in the foreseeable future.

Cash flow from operations has not historically been sufficient to sustain our operations without the above additional sources of capital. As of March 31, 2014, we had cash and cash equivalents of $2,184,000. Cash flow consumed by our operating activities totaled $1,200,000 for the three months ended March 31, 2014, compared to operating activities consuming $999,000 for the three months ended March 31, 2013. The increase in the cash consumed by our operating activities is largely due to the expansion of our farming operations.

As of March 31, 2014, we had $2,635,000 in current assets and $2,338,000 in current liabilities. We expect TR Capital will receive an additional $3,000,000 through the sale of Preferred Units by June 30, 2014.

Cash used in investing activities was $42,000 for the three months ended March 31, 2014, compared to use of cash of $1,321,000 for the three months ended March 31, 2013. During the three months ended March 31, 2014, we purchased equipment compared to the three months ended March 31, 2013 we purchased land and invested in water infrastructure through the expenditure of $1,321,000.

Cash flows generated by our financing activities for the three months ended March 31, 2014, were $1,357,000 compared to $2,294,000 for the three months ended March 31, 2013. The decrease is primarily due to a reduction in borrowing. During the three months ended March 31, 2014, we initiated our TR Capital preferred membership unit offering and received gross proceeds of $1,700,000 and used $343,000 to pay down notes payable.

Critical Accounting Policies

We have identified the policies below as critical to our business operations and the understanding of our results from operations. The impact and any associated risks related to these policies on our business operations is discussed throughout Management’s Discussion and Analysis of Financial Conditions and Results of Operations where such policies affect our reported and expected financial results. For a detailed discussion on the application of these and other accounting policies, see Note 2 in the Notes to the Consolidated Financial Statements. Note that our preparation of this document requires management to make estimates and assumptions that affect the reported amount of assets and liabilities, disclosure of contingent assets and liabilities at the date of our financial statements, and the reported amounts of revenue and expenses during the reporting period. There can be no assurance that actual results will not differ from those estimates.

16

Revenue Recognition

We follow specific and detailed guidelines in measuring revenue; however, certain judgments may affect the application of our revenue policy. Revenue results are difficult to predict, and any shortfall in revenue or delay in recognizing revenue could cause our operating results to vary significantly from quarter to quarter and could result in future operating losses.

Goodwill and Intangible Assets

We have acquired water shares in HCIC, which is considered an intangible asset and shown on our balance sheet as part of “Water assets”. Currently, these shares are recorded at purchase price less our pro rata share of the negative net worth in HCIC. Management evaluates the carrying value, and if necessary, will establish an impairment of value to reflect current fair market value. Currently, there are no impairments on the water shares.

In 2012, we acquired a produce business, which is considered an intangible asset and shown on our balance sheet as “Intangible assets, net.” Management evaluated the purchase price of $1,037,000 and allocated this price to customer list, tradename and goodwill. See Note 3 to our Financial Statements for a detail allocation.

Seasonality of Farming Business

Our Farming Business is subject to seasonality. We begin planting early in the calendar year for harvesting that begins in early July and continues through November. Management believes that we have enough capital and outside capital resources to fund the farming inputs until revenue is generated.

Material Contractual Obligations

During the three months ended March 31, 2013, we purchased approximately an additional 4% of the shares of HCIC. For the purchase we assumed the sellers’ past due assessment to HCIC of $80,000, which was eliminated on consolidation. This transaction was recorded as a reclassification from HCIC non-controlling interest to additional paid in capital. Further, we committed to provide the sellers a 100-year water lease equal to 4% of the total water available through the HCIC system at no additional charge to the sellers.

Quantitative and Qualitative Disclosures About Market Risk

We are exposed to the impact of interest rate changes and change in the market values of our investments. Based on our market risk sensitive instruments outstanding as of March 31, 2014, as described below, management has determined that there was no material market risk exposure to our consolidated financial position, results of operations, or cash flows as of such date. We do not enter into derivatives or other financial instruments for trading or speculative purposes.

Interest Rate Risk

At March 31, 2014,our exposure to market rate risk for changes in interest rates relates primarily to its borrowings and opportunities for retiring or rolling over our debt. We have not used derivative financial instruments in its credit facilities. A hypothetical 10% increase in the prime rate would not be significant to our financial position, results of operations, or cash flows.

Impairment Policy

At least once every year, management examines all of our assets for proper valuation and to determine if an allowance for impairment is necessary. In terms of real estate owned, this impairment examination also includes the accumulated depreciation. Management examines market valuations and if an additional impairment is necessary for lower of cost or market, then an impairment charge is recorded.

17

Inflation

We do not believe that inflation will have a material negative impact on our future operations.

We are exposed to the impact of interest rate changes and change in the market values of our real estate properties and water assets. Because we had no market risk sensitive instruments outstanding as of March 31, 2014, it was determined that there was no material market risk exposure to our consolidated financial position, results of operations, or cash flows as of such date. We do not enter into derivatives or other financial instruments for trading or speculative purposes.

ITEM 4. CONTROLS AND PROCEDURES

Disclosures Controls and Procedures

Our management, with the participation of our chief executive officer and chief financial officer, evaluated the effectiveness of our disclosure controls and procedures as of March 31, 2014. The term “disclosure controls and procedures,” as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act, means controls and other procedures of a company that are designed to ensure that information required to be disclosed by a company in the reports that it files or submits under the Securities Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the SEC’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed by a company in the reports that it files or submits under the Securities Exchange Act is accumulated and communicated to the company’s management, including its principal executive and principal financial officers, as appropriate to allow timely decisions regarding required disclosure. Management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving their objectives and management necessarily applies its judgment in evaluating the cost-benefit relationship of possible controls and procedures. Based on the evaluation of our disclosure controls and procedures as of March 31, 2014, and due to the material weakness in our internal control over financial reporting described in our Management's Annual Report on Internal Control over Financial Reporting accompanying our Annual Report on Form 10-K for the year ended December 31, 2013, our chief executive officer and chief financial officer concluded that, as of such date, our disclosure controls and procedures over financial reporting were not effective during reporting periods ended December 31, 2013 and March 31, 2014 as discussed below.

Changes in Internal Control over Financial Reporting

During the three months ended March 31, 2014, no changes other than those in conjunction with certain remediation efforts described below, were identified to our internal control over financial reporting that materially affected, or were reasonably likely to materially affect, our internal control over financial reporting.

Remediation Efforts

In the three months ended March 31, 2014, we continued to implement the following measures that we initiated in fiscal 2013 to improve our internal controls over the financial reporting process.

We increased our controls over financial reporting through the engagement in 2014 of an outside review team of our recording of transaction through the publishing of our financials.

We are seeking to hire a new senior level accountant with one of this person’s main responsibilities is the overseeing of our established internal controls.

We plan to do another formal assessment of our internal controls before the end of our quarter ending September 30, 2014; thereby allowing for internal corrective action before the end of our fiscal year ending December 31, 2014.

We will continue to monitor the effectiveness of our internal control over financial reporting in the areas affected by the facts described above and employ any additional tools and resources deemed necessary to ensure that our financial statements are fairly stated in all material respects.

18

PART II. OTHER INFORMATION

ITEM 1A. RISK FACTORS

The risks described in Item 1A. Risk Factors, in our Annual Report on Form 10-K for the year ended December 31, 2013, could materially and adversely affect our business, financial condition and results of operations. These risk factors do not identify all risks that we face—our operations could also be affected by factors that are not presently known to us or that we currently consider to be immaterial to our operations. The Risk Factors section of our 2013 Annual Report on Form 10-K remains current in material respects.

ITEM 6. EXHIBITS

The following is a complete list of exhibits filed as part of this Form 10Q/A. Exhibit number corresponds to the numbers in the Exhibit table of Item 601 of Regulation S-K.

|

Exhibit

Number

|

Description

|

|

|

10.1

|

Limited Liability Company Agreement dated as of January 31, 2014 among TR Capital Partners, LLC and the Members named therein

|

|

|

10.2

|

Membership Interest Purchase Agreement dated as of January 31, 2014 among TR Capital Partners, LLC and the Investors named therein

|

|

|

10.3

|

Exchange Agreement dated as of January 31, 2014 among TR Capital Partners, LLC, Two Rivers Water and Farming Company and the Holders named therein

|

|

|

31.1

|

Certification of Principal Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act

|

|

|

31.2

|

Certification of Principal Financial Officer pursuant to the Section 302 of the Sarbanes-Oxley Act

|

|

|

32.1

|

Certification of Principal Executive Officer pursuant to Section 906 of the Sarbanes-Oxley Act

|

|

|

32.2

|

Certification of Principal Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act

|

19

SIGNATURES

Pursuant to the requirements of Section 12 of the Securities and Exchange Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

TWO RIVERS WATER & FARMING COMPANY (Registrant)

|

|||

|

Date: May 13, 2014

|

By:

|

/s/ John McKowen | |

|

Chief Executive Officer & Chairman of the Board

|

|||

|

Date: May 13, 2014

|

By:

|

/s/ Wayne Harding | |

|

Chief Financial Officer & Principal Accounting Officer

|

|||

20

EXHIBIT INDEX

|

Exhibit

Number

|

Description

|

|

|

10.1

|

Limited Liability Company Agreement dated as of January 31, 2014 among TR Capital Partners, LLC and the Members named therein

|

|

|

10.2

|

Membership Interest Purchase Agreement dated as of January 31, 2014 among TR Capital Partners, LLC and the Investors named therein

|

|

|

10.3

|

Exchange Agreement dated as of January 31, 2014 among TR Capital Partners, LLC, Two Rivers Water and Farming Company and the Holders named therein

|

|

|

31.1

|

Certification of Principal Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act

|

|

|

31.2

|

Certification of Principal Financial Officer pursuant to the Section 302 of the Sarbanes-Oxley Act

|

|

|

32.1

|

Certification of Principal Executive Officer pursuant to Section 906 of the Sarbanes-Oxley Act

|

|

|

32.2

|

Certification of Principal Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act

|

21