Attached files

| file | filename |

|---|---|

| EX-5.1 - EX-5.1 - First Foundation Inc. | d695234dex51.htm |

| EX-23.1 - EX-23.1 - First Foundation Inc. | d695234dex231.htm |

| EX-21.1 - EX-21.1 - First Foundation Inc. | d695234dex211.htm |

Table of Contents

As filed with the Securities and Exchange Commission on May 9, 2014

Registration No. 333-195392

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

PRE-EFFECTIVE AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

First Foundation Inc.

(Exact name of registrant as specified in its charter)

| California | 6022 | 20-8639702 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

18101 Von Karman Avenue, Suite 700

Irvine, California 92612

(949) 202-4160

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Scott F. Kavanaugh

Chief Executive Officer

18101 Von Karman Avenue, Suite 700

Irvine, California 92612

(949) 202-4160

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Ben A. Frydman, Esq. Ryan C. Wilkins, Esq. Stradling Yocca Carlson & Rauth, P.C. 660 Newport Center Drive, Suite 1600 Newport Beach, California 92660 (949) 725-4000 |

Craig D. Miller, Esq. Jordan E. Hamburger, Esq. Manatt, Phelps & Phillips, LLP One Embarcadero Center San Francisco, California 94111 (415) 291-7400 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee(2) | ||

| Common Stock, $0.001 par value per share |

$58,000,000 | 7,471.00 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended, and includes shares of our common stock that the underwriters have an option to purchase within 30 days of the date of this prospectus to cover overallotments. |

| (2) | Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated May 9, 2014

PRELIMINARY PROSPECTUS

2,222,222 Shares

Common Stock

This prospectus relates to the initial public offering of First Foundation Inc. We are offering 2,222,222 shares of our common stock.

Prior to this offering, there has been no established public market for our common stock. We currently estimate that the public offering price of our common stock will be between $21.00 and $24.00 per share. We have applied to list our common stock on The NASDAQ Global Market under the symbol “FFWM.”

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 and, as a result, are eligible for certain reduced public company reporting and disclosure requirements, the implications of which to purchasers of our common stock are set forth in “About This Prospectus” on page ii.

See “Risk Factors,” beginning on page 12 of this prospectus, for a discussion of certain risks that you should consider before making a decision to purchase our common stock.

| Per Share | Total |

|||||||

| Public offering price |

$ | [ ] | $ | [ ] | ||||

| Underwriting discount(1) |

$ | [ ] | $ | [ ] | ||||

| Proceeds, before expenses, to us |

$ | [ ] | $ | [ ] | ||||

| (1) | See “Underwriting” for additional information regarding the underwriting discount and certain expenses payable to the underwriters by us. |

We have granted the underwriters an option to purchase up to an additional 333,333 shares of our common stock, at the public offering price, less the underwriting discount, within 30 days after the date of this prospectus, to cover overallotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission nor any other regulatory authority has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The shares of our common stock that you purchase in this offering will not be deposits, savings accounts or other obligations of any bank or nonbank subsidiaries and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

The underwriters expect to deliver the shares of our common stock against payment in New York, New York on or about [ ], 2014.

| Sandler O’Neill + Partners, L.P. |

Keefe, Bruyette & Woods A Stifel Company | |||

| Sterne Agee | ||||

The date of this prospectus is [ ], 2014.

Table of Contents

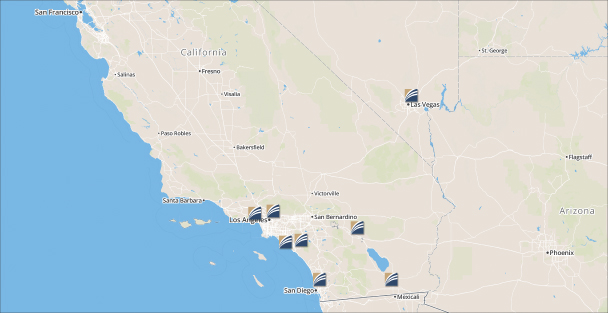

Corporate Organization Chart

| Asset Management Equities, Fixed Income, Hedge Funds, Private Equities, Real Estate, Commodities |

Banking Personal and Business Loans, Residential and Commercial Real Estate Loans, Deposit Accounts, Cash Management Services | |

| Wealth Planning Lifestyle/Retirement, Estate and Gift Planning, Philanthropic Giving, Generational Wealth Transfer, Tax Planning, Risk Management |

Trust Trustee Services, Estate Settlement Services, Guardianship Services, Family Business Services, Nevada Trust Powers | |

| Family and Philanthropic Consulting Consulting Services, Financial Competency Education, Life Skills Training, Foundation Services, Business Succession |

| |

Location of Wealth Management Offices

Table of Contents

| (ii) | ||||

| 1 | ||||

| 12 | ||||

| 28 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 34 | ||||

| 36 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

48 | |||

| 80 | ||||

| 89 | ||||

| 94 | ||||

| 96 | ||||

| 99 | ||||

| 101 | ||||

| 103 | ||||

| Certain Material U.S. Federal Income Tax Consequences for Non-U.S. Holders of Common Stock |

117 | |||

| 120 | ||||

| 124 | ||||

| 124 | ||||

| 124 | ||||

| F-1 |

(i)

Table of Contents

In considering whether to purchase shares of common stock in this offering, you should rely only on the information contained in this prospectus and any free writing prospectus we may file with the Securities and Exchange Commission, or SEC. We and the underwriters have not authorized anyone to provide any information different from that contained in this prospectus or in any free writing prospectuses we have prepared. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you.

This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of our common stock. Information contained on, or accessible through, our website is not part of this prospectus. Unless otherwise expressly stated or the context otherwise requires, all information in this prospectus assumes the underwriters have not exercised their overallotment option to purchase additional shares of our common stock.

Market Data

Market data used in this prospectus has been obtained from independent industry sources and publications as well as from research reports prepared for other purposes. Industry publications, surveys and reports generally state that the information contained therein has been obtained from sources believed to be reliable. However, we have not independently verified the data obtained from these sources. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties that apply to the other forward-looking statements that are described in this prospectus. In addition, while we are not aware of any misstatements regarding the market or industry data presented herein, such statements involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors” beginning on page 12 of this prospectus.

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart our Business Startups Act of 2012 (or the JOBS Act). An emerging growth company may take advantage of specified reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. As an emerging growth company:

| • | we are permitted to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations; |

| • | we are exempt from the requirement to obtain an attestation and report from our auditors on the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002; |

| • | we are permitted to provide less extensive disclosure about our executive compensation arrangements; |

| • | we are not required to give our shareholders non-binding advisory votes on executive compensation or golden parachute arrangements; and |

| • | we may elect to use an extended transition period for complying with new or revised accounting standards generally applicable to public companies. |

We may take advantage of these provisions for up to five years subsequent to the effective date of this prospectus or such earlier time that we are no longer an emerging growth company. We will cease to be an emerging growth company upon the earliest of (i) the last day of the first fiscal year in which our annual gross

(ii)

Table of Contents

revenues exceed $1 billion, (ii) December 31 of the fiscal year that we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, or the Exchange Act, which would occur if the market value of our common stock held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter and we have been publicly reporting for at least 12 months, or (iii) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period.

We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different from the information you receive from our competitors that are public companies, or other public companies in which you hold stock.

Representations and Warranties

The representations, warranties and covenants made by us in any agreement that is filed as an exhibit to the registration statement of which this prospectus is a part were made solely for the benefit of the parties to such agreement, including, in some cases, for the purpose of allocating risk among the parties to such agreement, and should not be deemed to be a representation, warranty or covenant made to you or for your benefit. Moreover, such representations, warranties or covenants were accurate only as of the date they were made. Accordingly, such representations, warranties and covenants should not be relied on as accurately representing the current state of our affairs.

Trademarks

“First Foundation” and its logos are trademarks and/or service marks of First Foundation Inc. and its subsidiaries. All other trademarks, service marks and trade names referred to in this prospectus are the property of their respective owners.

(iii)

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before deciding whether to purchase shares of our common stock in this offering. You should read the entire prospectus carefully, including the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes thereto, before making an investment decision. Unless we state otherwise or the context otherwise requires, references in this prospectus to “we,” “our,” and “us” refer to First Foundation Inc., a California corporation, (or FFI or the Company) and its consolidated subsidiaries, First Foundation Advisors (or FFA) and First Foundation Bank (or FFB).

Overview

We are a California based financial services company that provides a comprehensive platform of personalized financial services to high net-worth individuals (that is, individuals with a net worth greater than $1.0 million, exclusive of their primary residence) and their families, family businesses and other affiliated organizations. Our integrated platform provides investment management, wealth planning, consulting, trust and banking products and services to effectively and efficiently meet the financial needs of our clients. We have also established a lending platform that offers loans to individuals and entities that own and operate multifamily residential and commercial real estate properties. In addition, we provide business banking products and services to small to moderate-sized businesses and professional firms, and consumer banking products and services to individuals and families who would not be considered high net-worth. As of March 31, 2014, we had $2.80 billion of assets under management (or AUM), $1.09 billion of total assets, $949 million of loans and $855 million of deposits. Our investment management, wealth planning, consulting, and trust services provide us with substantial, fee-based, recurring revenues, such that in 2013, our noninterest income was 36% of our total revenues.

Our strategy is focused on expanding our strong and stable client relationships by delivering high quality, coordinated investment management, wealth planning, consulting, trust and banking products and services. We are able to maintain a client-focused approach by recruiting and retaining experienced and qualified staff, including highly qualified relationship managers, private bankers and financial planners.

We intend to continue to grow our business by (i) cross-selling our services among our wealth management and banking clients; (ii) obtaining new client referrals from existing clients, attorney and accountant referral sources and through referral agreements with asset custodial firms; (iii) marketing our services directly to prospective new clients; (iv) adding experienced relationship managers and private bankers who may have established client relationships that we can serve; (v) establishing de novo wealth management offices in select markets, both within and outside our existing market areas; and (vi) making opportunistic acquisitions of complementary businesses.

Our History and Growth

We commenced our operations in 1990 as a fee-based investment advisory company, with the philosophy of providing personalized investment advisory services primarily to high net-worth individuals and their families to assist them in meeting their financial goals. From 1990 to 2007, we grew our client base and added relationship managers and supporting staff. We also entered into referral agreements with asset custodial firms from which we derived a significant portion of our new clients. As a result of this growth, our assets under management exceeded $1.2 billion and we had total staff of 23 as of June 30, 2007.

1

Table of Contents

In 2005 and 2006, we experienced increased competition from other companies offering a more comprehensive platform of services to their clients, including banking, investment advisory and wealth planning services. In response to this competition, we considered various strategic options, including selling our business to a larger financial institution, expanding our services or continuing on with our then-current limited offerings. In late 2006, we decided to establish a federally insured bank to expand the financial services we could provide to our clients to include trust and banking services, and to attract private banking clients to whom we could cross-sell our investment advisory and wealth planning services. As a result, we retained experienced banking executives to prepare and file an application to open a bank, and in September 2007, FFB was granted an insured federal savings bank charter and commenced its banking operations in the subsequent month. During the fourth quarter of 2007, we moved our corporate operations to our existing location and opened our first wealth management office in Irvine, California. We refer to each of our offices as a wealth management office since we offer a full suite of financial and investment advisory services at all locations.

In early 2008, we expanded our wealth planning and consulting offerings to include foundation administration and consulting services and family consulting services. While the trust and banking operations began to grow in 2008 and 2009, all of our operations were negatively impacted by the economic recession which began in 2008. As a result of the recession, FFB focused its lending efforts on lower risk and lower yielding products, such as multifamily lending. Our AUM at FFA decreased by over 20% between September 2007 and March 2009, resulting in decreased revenues. However, we believe that because of our strong capital position and our conservative approach to underwriting our loans, FFB did not experience the significant difficulties that most other banks faced, and we were allowed to continue to grow our business in line with our business plan. During this time, we took advantage of the opportunities to hire highly qualified relationship managers, private bankers and investment professionals that existed as a result of the turmoil being experienced by many of our competitors. As of December 31, 2009, we had $1.29 billion of AUM, $201 million of loans, $182 million of deposits, $239 million of total assets and our staff totaled 66.

From 2010 through 2012, we continued to focus on expanding our client base. Over this period, we opened new wealth management offices in Pasadena and San Diego and a small branch office in La Quinta, California. Effective June 28, 2012, we converted FFB from a federal savings bank to a California state chartered bank. On August 15, 2012 we acquired Desert Commercial Bank (or DCB), a California state-chartered commercial bank, based in Palm Desert, California, and merged DCB into FFB. As a result of that acquisition, we increased our total assets by $140 million, our loans by $90 million, and our deposits by $127 million, and we acquired our two wealth management offices in Palm Desert and in El Centro. Our small branch office in La Quinta was merged into the Palm Desert office. Subsequent to the acquisition of DCB in 2012, and during 2013, we opened new wealth management offices in West Los Angeles and in Las Vegas, Nevada, and completed the integration of DCB into our operations. Currently, we conduct our business from our corporate offices located in Irvine, California, and from seven wealth management offices, six of which are located in Southern California and one of which is located in Las Vegas, Nevada. As of March 31, 2014, we had $2.80 billion of AUM, $949 million of loans, $855 million of deposits and $1.09 billion of total assets and our staff totaled 194.

We believe that as a result of our client-focused approach, and our ability to offer a comprehensive platform of personalized financial services to our clients, we have been able to retain existing clients and attract new clients. This has resulted in significant growth during the four year period that ended December 31, 2013, which is demonstrated by the following financial metrics:

| • | AUM increased at a compound annual growth rate of 19.2%; |

| • | Loans increased at a compound annual growth rate of 45.6%; |

| • | Deposits increased at a compound annual growth rate of 44.9%; |

| • | Total assets increased at a compound annual growth rate of 44.4%; |

2

Table of Contents

| • | Trust AUM increased at a compound annual growth rate of 43.0%; and |

| • | Total revenues increased at a compound annual growth rate of 38.9%. |

To achieve this growth, we have raised additional capital to support the growth of FFB and made significant investments in our staff. The number of relationship managers and private bankers has increased from 18 at December 31, 2009 to 38 at March 31, 2014. As it typically takes two to three years to break even on the investment in a relationship manager or private banker, we are in a position to benefit from these investments in the coming years as the revenues generated from these relationship managers and private bankers begins to exceed the related costs. However, these investments in relationship managers and private bankers have, and over the next few years, will continue to result in higher costs in relation to our revenues.

Our Competitive Strengths

We believe that we are well-positioned to create additional value for our shareholders, particularly as a result of our competitive strengths, which include:

Breadth of our Services. As a result of our ability to provide investment management, wealth planning, and consulting services, in addition to traditional banking services, we believe that we offer a more comprehensive range of financial services than do most banks of comparable size in our market areas. Additionally, we believe that few banks of comparable size in our market currently provide trust services, which can provide us with a competitive advantage over those banks, as well as a source of additional fee income.

Executive Management Team with Demonstrated Ability to Grow. Our executive management team, which has been together since 2007, has proven its ability to effectively lead us and has demonstrated an ability to grow our operations, as evidenced by the over 40% compound annual growth rate in loans, deposits and total assets from December 31, 2009 to December 31, 2013, and the 19% compound annual growth rate in AUM from December 31, 2009 to December 31, 2013.

Experienced and Collaborative Wealth Management and Banking Professionals. We believe we have built a strong team of relationship managers and private bankers who have, on average, 24 years of industry experience. Moreover, our relationship managers and private bankers work collaboratively to coordinate the investment management, wealth planning, consulting, trust and banking services that we provide to our clients and have developed considerable experience in cross-selling our services.

Commitment to High Quality and Personalized Services. We believe that our growth is largely attributable to our commitment and success in providing high quality, coordinated and personalized financial services to our clients. Our client-focused culture has resulted in the majority of our new clients coming to us from referrals from existing clients, centers of influence, including attorneys and accountants, and from unaffiliated asset custodial firms with which we have entered into non-exclusive referral arrangements. Our team oriented approach provides our clients with multiple points of contact and resources to address their various financial needs. Our fee-based investment management services allow us to make unbiased decisions regarding our clients’ investments, as we are not motivated by higher fees in our selection of investment alternatives, and our fee structure does not reward us for making higher risk investments that may adversely impact our clients during a downturn in the markets.

Stable and Scalable Platform. We have built a scalable corporate and administrative infrastructure, and have made significant investments in technology for our banking and investment management processes. In addition to our relationship managers and private bankers, we have in place highly qualified executives, senior managers, and investment professionals who we believe are capable of supporting our continued growth. The

3

Table of Contents

nature of our business requires significant investments in operational and administrative functions. By growing our interest-earning assets and AUM, we are able to spread this fixed cost over a larger revenue base. To achieve increased profitability, we believe that it is essential for us to build our operations to a level that allows us to provide our investment management, wealth planning, consulting, trust and banking products and services in a cost effective manner.

Strong Credit Culture. We have implemented policies and procedures for credit underwriting and administration which have enabled us to maintain strong asset quality and at the same time grow our banking business, despite the continuing economic uncertainties and the sluggishness of the economic recovery in the United States. Our ratio of nonperforming assets (or NPAs) to total assets was 0.55% at March 31, 2014 and the ratio of net loan charge-offs-to average loans outstanding has averaged 0.07% for the three year period ended December 31, 2013.

Successful Multifamily and Commercial Real Estate Lending Platform. We have created a multifamily and commercial real estate lending platform that has resulted in the origination of over $700 million of loans since the beginning of 2009. We believe that this platform has enabled us to add interest-earning assets with minimal adverse credit results. Since FFB commenced its operations in 2007, we have not experienced any chargeoffs on loans that were originated through this platform and secured by multifamily and commercial real estate properties. As of March 31, 2014, multifamily and commercial real estate loans originated on this platform represented 56.9% of our total loans outstanding.

Located in Strategic Markets. Our wealth management offices are located in areas that either have a high concentration of high net-worth households or are in areas where we believe the competition from other companies that provide a comprehensive platform of financial services to high net-worth individuals is limited. In addition, our wealth management office in Las Vegas offers Nevada trust powers which can offer significant benefits to high net-worth individuals and their families.

Retention of Clients. We believe that because of our client-focused culture, we have experienced a high level of retention of our clients. As an example, during the five year period ending December 31, 2013, the weighted average amount of AUM withdrawn each year as a result of client terminations as a percentage of the beginning of that year’s AUM balance was less than 5%.

Diverse Revenue Base. We have a diverse revenue base as a result of our comprehensive platform of services. For 2013 our total revenue was comprised of net interest income (64%), investment management fees (28%), trust fees (3%), deposit and other banking fees (3%) and consulting fees (2%).

Strong Deposit Base. An important driver of our financial performance has been, and we believe will continue to be, the growth and stability of our deposit base, which we use to fund our loans and other interest-earning assets. In addition to the increase in the amount of our deposits, which have grown at a compound annual rate of 44.9% from December 31, 2009 to December 31, 2013, we have been able to increase the proportion of more stable demand deposits, which represented 53% of our total deposits at March 31, 2014 as compared to 12% at December 31, 2009.

Our Strategy

Grow Our Business Organically. In growing our business organically we intend to focus on adding experienced, high quality relationship managers and private bankers at both our existing wealth management offices and at new wealth management offices we may open in selected market areas, both within and outside of California, with demographics similar to those in our existing markets. Because a significant portion of our new business comes from referral sources, we plan to continue to work to obtain referrals from our clients, from

4

Table of Contents

centers of influence, including accountants and attorneys, and from loan brokers, and we will maintain referral agreements with unaffiliated asset custodial firms. We intend to continue our practice of establishing and maintaining advisory boards in each of our markets to provide client referrals.

Continue Cross-Selling our Services and Expand the Services We Offer Our Clients. We intend to continue to cross-sell our investment management, wealth planning, consulting, trust and banking products and services to our existing and future clients. Our compensation structures encourage a team approach to client service and reward relationship managers and private bankers for facilitating the cross selling of services to clients. We believe that our service-oriented culture and high quality client service will continue to enable us to strengthen and expand our client relationships and will foster continued growth in the services and products we offer them and, thereby, enabling us to increase and diversify our sources of revenues.

Grow our Business through Acquisitions. We intend to make opportunistic acquisitions that we believe will enable us to grow our franchise geographically. While we believe that banks provide the most likely opportunities for acquisition, we will also consider acquisitions of investment management firms and insurance brokerage firms. We believe that our experience with previous transactions makes us qualified to acquire other institutions and integrate their operations into our platform. In addition to providing us increased interest-earning assets and deposits, bank acquisitions would allow us to cross sell our investment management, wealth planning, consulting and trust services to clients acquired in the acquisition as well as new clients situated in the related geographic area. Although we do not have any immediate plans, arrangements or understandings related to any material acquisitions, we believe that the completion of this offering will further enhance our ability to compete for acquisition opportunities by providing available equity to invest and enabling us to offer publicly-traded shares of our common stock to the shareholders of prospective acquisition candidates.

Provide High Quality Client Services. We believe that stable long-term growth and profitability are the result of building strong client relationships, one at a time, and providing high quality, coordinated financial services. Our relationship managers and private bankers strive to build long-term relationships with our clients by understanding their financial needs and identifying and delivering appropriate and coordinated financial services to them. We believe that our service-oriented culture and high quality client service differentiates us from many of our competitors.

Attract and Retain High Quality Service Professionals. Having successful and high quality service professionals is critical to driving the development of our business and delivering high quality financial services. We have experienced low turnover in our client service personnel and intend to continue hiring and developing professionals who can establish and maintain long-term customer relationships which are the key to our culture, business and growth. We also believe that our business model, culture and scalable platform enable us to attract and retain high quality relationship managers and private bankers who share our work ethic and our commitment to providing personalized and client-focused financial services.

Our Management Team

We believe that our management team, led by Scott Kavanaugh, our Chief Executive Officer, Ulrich (“Rick”) Keller, Jr., our Executive Chairman of the Board, John Hakopian, President of FFA, Dave Rahn, President of FFB and John Michel, our Chief Financial Officer have the breadth of experience necessary to effectively execute our business strategy.

Our Market

Because our primary target market is high net-worth individuals and their families, family businesses and other affiliated organizations, we have located our offices in areas we believe offer us the best opportunity to

5

Table of Contents

locate and serve this client base. The Los Angeles-Long Beach Core-Based Statistical Area (CBSA), which includes Orange County, has over 250,000 high net-worth households (defined as those with $1.0 million or more of investable assets), making it the largest high net-worth market in the Western United States. As of December 31, 2013, 68% of our AUM was from clients located in the in Los Angeles-Long Beach CBSA. Our wealth management offices are located in or adjacent to four of the top 12 markets in the Western United States as ranked by estimated number of high net-worth households. Listed below are the largest core-based statistical areas by estimated number of high net worth households in the Western United States as of December 31, 2013, according to data obtained from Phoenix Marketing International’s “Global Wealth Monitor”:

| Rank | Statistical Areas in Western United States (1) |

Estimated Number of High Net Worth Households |

Wealth Management Office in Area | |||

| 1 | Los Angeles-Long Beach (CA) | 252,000 | Irvine, Pasadena, West Los Angeles | |||

| 2 | San Francisco-Oakland (CA) | 128,000 | ||||

| 3 | Seattle-Tacoma-Bellevue (WA) | 90,000 | ||||

| 4 | Phoenix-Mesa-Glendale (AZ) | 72,000 | ||||

| 5 | Riverside (CA) | 70,000 | Palm Desert | |||

| 6 | San Diego-Carlsbad (CA) | 69,000 | San Diego | |||

| 7 | Denver-Aurora-Broomfield (CO) | 63,000 | ||||

| 8 | San Jose-Sunnyvale (CA) | 52,000 | ||||

| 9 | Sacramento—Arden (CA) | 48,000 | ||||

| 10 | Portland-Vancouver (OR-WA) | 46,000 | ||||

| 11 | Las Vegas-Paradise (NV) | 31,000 | Las Vegas | |||

| 12 | Honolulu (HI) | 25,000 | ||||

| (1) | The Western United States is defined as Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, New Mexico, Nevada, Oregon, Utah, Washington and Wyoming. |

In addition to offering our comprehensive platform of personalized financial services primarily to high net-worth individuals and their families, family businesses and other affiliated organizations, we have established a lending platform that offers loans to individuals and entities that own and operate multifamily residential properties and commercial real estate properties. The underlying properties which secure these loans are primarily located in communities throughout California that have a significant population base and are already built out. The following is a breakdown of the location of our multifamily and commercial real estate loans by county as of December 31, 2013:

| (dollars in thousands) | Amount | % of Total | ||||||

| California Counties: |

||||||||

| Los Angeles |

$ | 325,738 | 58.0% | |||||

| Orange |

51,366 | 9.2% | ||||||

| Riverside |

48,460 | 8.6% | ||||||

| San Diego |

38,163 | 6.8% | ||||||

| San Francisco |

34,781 | 6.2% | ||||||

| Other counties—Northern California |

30,198 | 5.4% | ||||||

| Other counties—Southern California |

18,226 | 3.3% | ||||||

| Nevada—all counties |

2,305 | 0.4% | ||||||

| Other states |

11,935 | 2.1% | ||||||

|

|

|

|

|

|||||

| Total |

$ | 561,172 | 100.0% | |||||

|

|

|

|

|

|||||

6

Table of Contents

Our Challenges

As with all financial institutions, we face many challenges. There are a number of risks that you should consider before investing in our common stock. These risks are discussed more fully in the section entitled “Risk Factors,” beginning on page 12.

Additional Information

We were incorporated in California in 2006 to become the parent holding company of First Foundation Advisors and First Foundation Bank. We are registered as a bank holding company under the Bank Holding Company Act of 1956.

Our principal executive office is located at 18101 Von Karman Avenue, Suite 700, Irvine, California 92612, where our telephone number is (949) 202-4160. Our website address is www.ff-inc.com. The information contained on our website is not a part of, or incorporated by reference into, this prospectus.

7

Table of Contents

THE OFFERING

| Common stock offered by us |

2,222,222 shares |

| Underwriters’ overallotment option |

333,333 shares. |

| Shares of common stock offered as a percentage of our outstanding shares of common stock |

28.7%, assuming the underwriters do not exercise their overallotment option. |

| Shares of common stock outstanding after completion of this offering |

9,955,736 shares, assuming the underwriters do not exercise their overallotment option.(1) |

| Shares of common stock owned by our directors and executive officers |

Our directors and executive officers own, in the aggregate, a total of 2,620,099 shares of our common stock, which is not expected to materially change as a result of this offering. Each of our directors and executive officers has entered into a lock-up agreement agreeing not to sell any of their shares for 180 days after completion of this offering, subject to certain exceptions. For additional information, see “Underwriting”. |

| Use of proceeds |

The net proceeds from the sale of our common stock in this offering, after deducting estimated underwriting discounts and offering expenses, will be approximately $46.1 million (or $53.1 million if the underwriters exercise their overallotment option in full). We intend to use the net proceeds from this offering: |

| • | To repay a term loan obtained from an unaffiliated bank, the aggregate principal amount of which was $21.9 million at March 31, 2014. We used $17.5 million of the net proceeds of that loan for to make capital contributions to FFB to fund the continued growth of our banking business. |

| • | To support our organic growth, including the addition of new wealth management offices. |

| • | To fund possible acquisitions that we believe are complementary to our business and provide attractive risk-adjusted returns, although we do not have any immediate plans, arrangements or understandings relating to any material acquisition. |

| • | For other general corporate purposes, which may include the hiring of additional personnel and the payment of costs associated with operating as a public company. |

| For additional information, see “Use of Proceeds.” |

| Dividend policy |

We have not previously paid cash dividends on our common stock. It is our current intention to invest our cash flow and earnings in the |

8

Table of Contents

| growth of our businesses and, therefore, we have no plans to pay cash dividends for the foreseeable future. Investors should not purchase our common stock with the expectation of receiving cash dividends. |

| For additional information, see “Dividend Policy.” |

| Rank |

Our common stock may be subordinate to any new series of preferred stock that we may issue in the future. However, we have no current plans to issue any preferred stock. |

| Proposed Nasdaq Global Market Symbol |

We intend to apply to list our common stock on the Nasdaq Global Market under the trading symbol “FFWM.” |

| Risk factors |

Investing in our common stock involves risks. See “Risk Factors,” beginning on page 12, for a discussion of certain factors that you should carefully consider before making an investment decision. In addition, see “Cautionary Note Regarding Forward-Looking Statements.” |

| (1) | References in this section to the number of shares of our common stock outstanding after this offering are based on 7,733,514 shares of our common stock issued and outstanding as of March 31, 2014. Unless otherwise noted, these references exclude: |

| • | 1,497,092 shares of common stock are issuable upon exercise of outstanding options to purchase shares of common stock under the First Foundation Inc. 2007 Equity Incentive Plan and the First Foundation Inc. 2007 Management Stock Incentive Plan (or collectively, the Stock Incentive Plans) as of March 31, 2014, at a weighted average exercise price of $12.62 per share (of which options to acquire 1,263,789 shares of our common stock were vested as of March 31, 2014); |

| • | 296,345 shares of our common stock reserved for issuance under the Stock Incentive Plans; and |

| • | Up to an additional 270,000 shares of our common stock which may become issuable to the former shareholders of DCB. The number of these shares that will become issuable is dependent on the performance, over the two year period ending August 15, 2014, of certain assets we acquired as part of our acquisition of DCB in August 2012. Based on the performance of those assets through March 31, 2014, we believed, as of that date, that it was unlikely that any of these shares would become issuable. However, since the final determination will be based on the performance of those assets through August 15, 2014, some of these shares may ultimately become issuable to the former shareholders of DCB. |

9

Table of Contents

SELECTED HISTORICAL CONSOLIDATED FINANCIAL INFORMATION

With the exception of the certain items included in the selected performance and capital ratios, the following selected consolidated financial information as of and for the years ended December 31, 2013 and 2012 has been derived from our audited consolidated financial statements appearing elsewhere in this prospectus, and the selected consolidated financial information as of and for the year ended December 31, 2011 has been derived from our audited consolidated financial statements not appearing in this prospectus.

You should read the following selected financial and operating data in conjunction with other information contained in this prospectus, including the information set forth in the sections entitled “Capitalization” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, as well as our consolidated financial statements and the related notes included elsewhere in this prospectus. The average balances used in computing certain ratios, have been computed using daily averages, except for average equity, which is computed using the average of beginning and end of month balances. Our historical results as set forth below are not necessarily indicative of results to be expected in any future period. In addition, as described elsewhere in this prospectus, on August 15, 2012 we consummated the acquisition of DCB. The results of operations and other financial data of DCB for all periods prior to the date of its acquisition are not included in the table below and, therefore, our results and other financial data for these prior periods are not comparable in all respects to those for the periods subsequent to that acquisition. In addition, the income statement data set forth below may not be predictive of our future operating results.

| As of and for the Year Ended December 31, |

As of and for the Quarter Ended March 31 |

|||||||||||||||||||

| (In thousands, except share and per share |

2013 | 2012(1) | 2011 | 2014 | 2013 | |||||||||||||||

| Selected Income Statement Data: |

||||||||||||||||||||

| Net interest income |

$ | 35,674 | $ | 27,729 | $ | 20,141 | $ | 9,750 | $ | 8,192 | ||||||||||

| Provision for loan losses |

2,395 | 2,065 | 2,297 | $ | 235 | 622 | ||||||||||||||

| Noninterest Income: |

||||||||||||||||||||

| Asset management, consulting and other fees |

18,240 | 15,326 | 13,211 | 5,039 | 4,286 | |||||||||||||||

| Other(2) |

1,584 | 1,294 | 4,489 | 512 | 247 | |||||||||||||||

| Noninterest expense |

43,622 | 34,476 | 26,446 | 12,546 | 10,396 | |||||||||||||||

| Income before taxes |

9,481 | 7,808 | 9,098 | 2,520 | 1,707 | |||||||||||||||

| Net income |

7,851 | 5,801 | 9,098 | 1,462 | 1,058 | |||||||||||||||

| Share and Per Share Data: |

||||||||||||||||||||

| Net income per share: |

||||||||||||||||||||

| Basic |

$ | 1.06 | $ | 0.88 | $ | 1.48 | $ | 0.19 | $ | 0.14 | ||||||||||

| Diluted |

1.01 | 0.85 | 1.42 | 0.18 | 0.14 | |||||||||||||||

| Shares used in computation: |

||||||||||||||||||||

| Basic |

7,424,210 | 6,603,533 | 6,164,283 | 7,733,514 | 7,376,988 | |||||||||||||||

| Diluted |

7,742,215 | 6,831,955 | 6,393,713 | 8,093,777 | 7,613,234 | |||||||||||||||

| Tangible book value per share(3) |

$ | 11.18 | $ | 9.94 | $ | 7.98 | $ | 11.46 | $ | 10.15 | ||||||||||

| Shares outstanding at end of period(4) |

7,733,514 | 7,366,126 | 6,166,574 | 7,733,514 | 7,409,860 | |||||||||||||||

| Selected Balance Sheet Data: |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 56,954 | $ | 63,108 | $ | 10,098 | $ | 50,287 | $ | 42,443 | ||||||||||

| Loans, net of deferred fees |

903,645 | 743,627 | 524,103 | 948,844 | 785,760 | |||||||||||||||

| Allowance for loan and lease losses (“ALLL”) |

(9,915 | ) | (8,340 | ) | (6,550 | ) | (10,150 | ) | (8,210 | ) | ||||||||||

| Total assets |

1,037,360 | 830,509 | 551,584 | 1,090,348 | 869,830 | |||||||||||||||

| Noninterest-bearing deposits |

217,782 | 131,827 | 66,383 | 225,473 | 181,251 | |||||||||||||||

| Interest-bearing deposits |

584,255 | 517,914 | 340,443 | 629,211 | 523,577 | |||||||||||||||

| Borrowing - FHLB Advances |

134,000 | 100,000 | 91,000 | 119,000 | 85,000 | |||||||||||||||

| Borrowings – term note |

7,063 | - | - | 21,875 | - | |||||||||||||||

| Shareholders’ equity(4) |

86,762 | 73,580 | 49,197 | 88,841 | 75,499 | |||||||||||||||

10

Table of Contents

| As of and for the Year Ended December 31, | As of and for the Quarter Ended March 31 |

|||||||||||||||||||

| (In thousands, except share and per |

2013 | 2012(1) | 2011 | 2014 | 2013 | |||||||||||||||

| Selected Performance and Capital Ratios: |

||||||||||||||||||||

| Return on average assets-annualized |

0.86% | 0.80% | 1.91% | 0.55% | 0.51% | |||||||||||||||

| Return on average equity-annualized |

10.2% | 9.9% | 20.7% | 6.6% | 5.7% | |||||||||||||||

| Net yield on interest-earning assets |

4.04% | 4.20% | 4.43% | 3.76% | 4.13% | |||||||||||||||

| Efficiency ratio(5) |

78.6% | 77.7% | 77.4% | 82.0% | 81.7% | |||||||||||||||

| Noninterest income as a % of total revenues |

35.7% | 37.5% | 46.8% | 36.3% | 35.6% | |||||||||||||||

| Tangible common equity to tangible assets(3) |

8.34% | 8.82% | 8.92% | 8.13% | 8.65% | |||||||||||||||

| Tier 1 leverage ratio |

8.67% | 9.19% | 8.92% | 8.22% | 9.19% | |||||||||||||||

| Tier 1 risk-based capital ratio |

13.04% | 13.60% | 13.54% | 12.40% | 13.12% | |||||||||||||||

| Total risk-based capital ratio |

14.30% | 14.85% | 14.80% | 13.65% | 14.37% | |||||||||||||||

| Other Information: |

||||||||||||||||||||

| Assets under management (end of period) |

$ | 2,594,961 | $ | 2,229,116 | $ | 1,827,436 | $ | 2,797,562 | 2,372,056 | |||||||||||

| NPAs to total assets |

0.32% | 0.17% | 0.00% | 0.55% | 0.41% | |||||||||||||||

| Charge-offs to average loans |

0.10% | 0.04% | 0.05% | 0.00% | 0.40% | |||||||||||||||

| Ratio of ALLL to loans(6) |

1.16% | 1.25% | 1.25% | 1.08% | 1.15% | |||||||||||||||

| Number of wealth management offices |

7 | 6 | 4 | 7 | 6 | |||||||||||||||

| (1) | Includes the results of operations of DCB for the period from the date of its acquisition on August 15, 2012 to December 31, 2012. |

| (2) | 2011 amount includes a $3.7 million gain on the sale of other real estate owned. |

| (3) | Tangible common equity, (also referred to as tangible book value) and tangible assets, are equal to common equity and assets, respectively, less $0.2 million of intangible assets as of March 31, 2014 or less $0.3 million of intangible assets as of December 31, 2013 and December 31, 2012. As of December 31, 2011, we did not have any intangible assets. |

| (4) | In December 2013, we sold and issued 318,987 shares of our common stock, at a price of $18 per share, in a private offering. We sold a total of 413,172 shares in a private offering, at a price of $15 per share, of which 374,438 were sold and issued in 2012 and 38,734 shares were sold and issued in 2013. Effective August 15, 2012, we issued a total of 815,447 shares of our common stock, valued at $15.00 per share, to the former DCB shareholders in our acquisition of DCB in exchange for all of the outstanding shares of DCB. |

| (5) | The efficiency ratio is the ratio of noninterest expense to the sum of net interest income and noninterest income. |

| (6) | This ratio excludes loans acquired in our acquisition of DCB, as generally accepted accounting principles in the United States, or GAAP, requires estimated credit losses for acquired loans to be recorded as discounts to those loans. |

11

Table of Contents

An investment in our common stock involves significant risks. You should consider carefully the risks described below, together with all of the other information included in this prospectus, before investing in our common stock. If any of the following risks actually occur, our business, financial condition, operating results and prospects could suffer. In that case, the trading price of our common stock may decline and you might lose all or part of your investment. Certain statements below are forward-looking statements. See the section entitled “Cautionary Note Regarding Forward-Looking Statements” beginning on page 28 of this prospectus.

Risks Affecting our Business

We could incur losses on the loans we make.

Loan defaults and the incurrence of losses on loans are inherent risks in our business. The incurrence of loan losses necessitate loan charge-offs and write-downs in the carrying values of a bank’s assets and, therefore, can adversely affect a bank’s results of operations and financial condition. As a result, our results of operations will be directly affected by the volume and timing of loan losses, which for a number of reasons can vary from period to period. The risks of loan losses are exacerbated by economic recessions and downturns, as evidenced by the substantial magnitude of the loan losses which many banks incurred as a result of the economic recession that commenced in 2008 and continued into 2010, or by other events that can lead to local or regional business downturns. Although an economic recovery in the U.S. has begun, unemployment remains high and there continues to be uncertainties about the strength and sustainability of the recovery. If the economic recovery were to remain weak or economic conditions were again to deteriorate, our borrowers may fail to perform in accordance with the terms of their loans and loan charge-offs and asset write-downs could increase, which could have a material adverse effect on our business, financial condition, results of operations and prospects.

If our allowance for loan and lease losses is not adequate to cover actual or estimated future loan losses, our earnings may decline.

On a quarterly basis we conduct various analyses to estimate the losses and risks inherent in our loan portfolio. However, this evaluation requires us to make a number of estimates and judgments regarding the financial condition of our borrowers, the fair value of the properties collateralizing the loans we have made to them and economic trends that could affect the ability of borrowers to meet their loan payment obligations to us and our ability to offset or mitigate loan losses by foreclosing and reselling the real properties collateralizing many of those loans. Based on those estimates and judgments, we make determinations, which are necessarily subjective, with respect to the adequacy of our allowance for loan and lease losses, or ALLL, and the extent to which it is necessary to increase our ALLL by making additional provisions for loan and lease losses through a charge to income. Inaccurate management assumptions, deterioration of economic conditions affecting borrowers, new information regarding existing loans, identification of additional problem loans and other factors, both within and outside of our control, may require us to increase our ALLL. In addition, our regulators, as an integral part of their examination process, periodically review our loan portfolio and the adequacy of our ALLL and may require adjustments based on judgments different than those of management. Further, if actual charge-offs in future periods exceed the amounts allocated to the ALLL, we may need additional provision for loan losses to restore the adequacy of our ALLL. If we are required to materially increase our level of ALLL for any reason, our business, financial condition, results of operations and prospects could be materially and adversely affected.

Adverse changes in economic conditions in Southern California could disproportionately harm us.

The substantial majority of our clients and the properties securing a large proportion of the loans we have made and will continue to make are located in Southern California, where foreclosure rates and unemployment

12

Table of Contents

have remained high relative to most other regions of the country. For example, the foreclosure rate in Los Angeles County as of March 2014 was 0.10% as compared to the national average of 0.08% and the unemployment rate in Los Angeles County as of February 2014 was 8.9% as compared to the national average of 6.7%. A downturn in economic conditions, or even the continued weakness of the economic recovery in California, or the occurrence of natural disasters, such as earthquakes or fires, which are more common in Southern California than in other parts of the country, could harm our business by:

| • | reducing loan demand which, in turn, would lead to reductions in our net interest margins and net interest income; |

| • | adversely affecting the financial capability of borrowers to meet their loan obligations to us, which could result in increases in loan losses and require us to make additional provisions for possible loan losses, thereby adversely affecting our operating results or causing us to incur losses in the future; and |

| • | causing reductions in real property values that, due to our reliance on real properties to collateralize many of our loans, could make it more difficult for us to prevent losses from being incurred on nonperforming loans through the foreclosure and sale of those real properties. |

Adverse changes in economic and market conditions, and changes in government regulations and government monetary policies could materially and negatively affect our business and results of operations.

Our business and results of operations are directly affected by factors such as political, economic and market conditions, broad trends in industry and finance, legislative and regulatory changes, changes in government monetary and fiscal policies and inflation, all of which are beyond our control. Deterioration in economic conditions, whether caused by global, national, regional or local concerns or problems, or a further downgrade in the United States debt rating, could result in the following consequences, any of which could have a material adverse effect on our business, financial condition, results of operations or prospects:

| • | a deterioration in the credit quality of our banking clients; |

| • | an increase in loan delinquencies and losses; |

| • | an increase in problem assets and foreclosures; |

| • | declines in the values of real properties collateralizing the loans we make; |

| • | the need to increase our ALLL; |

| • | fluctuations in the value of, or impairment losses which may be incurred with respect to, FFB’s investment securities; |

| • | decreases in the demand for our products and services; |

| • | increases in competition for low cost or non-interest bearing deposits; and |

| • | decreases in the investment management and advisory fees we generate. |

Changes in interest rates could reduce our net interest margin and net interest income.

Income and cash flows from our banking operations depend to a great extent on the difference or “spread” between the interest we earn on interest-earning assets, such as loans and investment securities, and the interest rates we pay on interest-bearing liabilities, such as deposits and borrowings. Interest rates are highly sensitive to many factors that are beyond our control, including general economic conditions, the monetary policies of the Federal Reserve Board, and competition from other banks and financial institutions. Changes in monetary policy, including changes in interest rates, will influence the origination and market value of and our yields on loans and investment securities and the interest we pay on deposits and on our borrowings. If we are unable to adjust our interest rates on loans and deposits on a timely basis in response to such changes in economic conditions or monetary policies, our earnings could be adversely affected. In addition, if the rates of interest we pay on deposits, borrowings and other interest-bearing liabilities increase faster than we are able to increase the rates of

13

Table of Contents

interest we charge on loans or the yields we realize on investments and other interest-earning assets, our net interest income and, therefore, our earnings will decrease. Rising interest rates also generally result in a reduction in loan originations, declines in loan repayment rates and reductions in the ability of borrowers to repay their current loan obligations, which could result in increased loan defaults and charge-offs and could require increases to our ALLL. Additionally, we could be prevented from increasing the interest rates we charge on loans or from reducing the interest rates we offer on deposits due to price competition from other banks and financial institutions with which we compete. Conversely, in a declining interest rate environment, our earnings could be adversely affected if the interest rates we are able to charge on loans or other investments decline more quickly than those we pay on deposits and borrowings.

Residential real estate loans represent a high percentage of the loans we make, making our results of operations vulnerable to downturns in the real estate market.

At March 31, 2014, loans secured by multifamily and single family residences represented 70% of FFB’s outstanding loans. The repayment of residential real estate loans is highly dependent on the market values of the real properties that collateralize these loans and on the ability of the borrowers to meet their loan repayment obligations to us, which can be adversely affected by economic downturns that lead to increases in unemployment, or by rising interest rates which can increase the amount of the interest borrowers are required to pay on their loans. As a result, our operating results are more vulnerable to adverse changes in the real estate market than other financial institutions with more diversified loan portfolios and we could incur losses in the event of changes in economic conditions that disproportionately affect the real estate markets.

Liquidity risk could adversely affect our ability to fund operations and hurt our financial condition.

Liquidity is essential to our banking business, as we use cash to make loans and purchase investment securities and other interest-earning assets and to fund deposit withdrawals that occur in the ordinary course of our business. Our principal sources of liquidity include earnings, deposits, Federal Home Loan Bank (or FHLB) borrowings, sales of loans or investment securities held for sale, and repayments by clients of loans we have made to them, and capital contributions that we may make to FFB with proceeds from sales of our common stock or from borrowings that we may incur. If the ability to obtain funds from these sources becomes limited or the costs of those funds increase, whether due to factors that affect us specifically, including our financial performance, or due to factors that affect the financial services industry in general, including weakening economic conditions or negative views and expectations about the prospects for the financial services industry as a whole, then our ability to grow our banking and investment advisory and wealth management businesses would be harmed, which could have a material adverse effect on our business, financial condition, results of operations and prospects.

Our 5 largest deposit clients account for 33% of our total deposits.

As of March 31, 2014, our 5 largest bank depositors accounted for, in the aggregate, 33% of our total deposits. As a result, a material decrease in the volume of those deposits by a relatively small number of our depositors could reduce our liquidity, in which event it could became necessary for us to replace those deposits with higher-cost deposits, lower-yielding securities or FHLB borrowings, which would adversely affect our net interest income and, therefore, our results of operations.

Although we plan to grow our business by acquiring other banks, there is no assurance that we will succeed in doing so.

One of the key elements of our business plan is to grow our banking franchise and increase our market share, and for that reason, we intend to take advantage of opportunities to acquire other banks. However, there is no assurance that we will succeed in doing so. Our ability to execute on our strategy to acquire other banks may require us to raise additional capital and to increase FFB’s capital position to support the growth of our banking

14

Table of Contents

franchise, and will also depend on market conditions, over which we have no control. Moreover, any bank acquisitions will require the approval of our bank regulators and there can be no assurance that we will be able to obtain such approvals on acceptable terms, if at all.

Expansion of our banking franchise may not increase our profitability and may adversely affect our future operating results.

Since we commenced our banking business in October 2007, we have grown our banking franchise by establishing three new wealth management offices in Southern California and one in Las Vegas, Nevada and acquiring two new offices in Palm Desert and El Centro, California as part of our acquisition of Desert Commercial Bank, or DCB. We plan to continue to grow our banking franchise both organically and through potential acquisitions of other banks. However, the implementation of our growth strategy will pose a number of risks, including:

| • | the risk that any newly established wealth management offices will not generate revenues in amounts sufficient to cover the start-up costs of those offices, which would reduce our income or possibly cause us to incur operating losses; |

| • | the risk that any bank acquisitions we might consummate in the future will prove not to be accretive to or may reduce our earnings if we do not realize anticipated cost savings or if we incur unanticipated costs in integrating the acquired banks into our operations or if a substantial number of the clients of the acquired banks move their banking business to our competitors; |

| • | the risk that such expansion efforts will divert management time and effort from our existing banking operations, which could adversely affect our future financial performance; and |

| • | the risk that the additional capital which we may need to support our growth or the issuance of shares in any bank acquisitions will be dilutive of the share ownership of our existing shareholders. |

We have borrowings of $21.9 million under a five year term loan that is secured by a pledge of all of FFB’s shares. As a result, a failure by us either to meet certain financial covenants applicable to that term loan or to repay that loan when due would have a material adverse effect on us.

In April 2013, we obtained a five year term loan in the amount of $7.5 million from an unaffiliated bank. In March 2014, we obtained a $15 million increase in that loan, bringing the total principal amount to approximately $21.9 million. We used $17.5 million of the proceeds of the loan to make capital contributions to FFB to fund the growth of our banking business. In order to obtain that loan, however, we were required to pledge all of the shares of FFB stock to the bank lender as security for our payment and other obligations under that loan agreement. Additionally, the loan agreement contains a number of financial and other covenants which we are required to meet over the five year term of the loan. As a result, such borrowings may make us more vulnerable to general economic downturns and competitive pressures, which could cause us to fail to meet one or more of those financial covenants. If we were unable to meet any of those covenants, we could be required to repay the loan sooner than its maturity date in May 2018. If we are unable to repay the loan when due, whether at maturity or earlier, the lender would have the right to sell our FFB shares to recover the amounts that are due it by us under the loan agreement. Since the stock of FFB comprises one of our most important assets on which our success is dependent, an inability on our part to repay the loan would have a material adverse effect on our business, financial condition, results of operations and prospects and cause us to incur significant losses. See the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Financial Condition—Term Loan” for additional information about this loan.

We face intense competition from other banks and financial institutions and other wealth and investment management firms that could hurt our business.

We conduct our business operations primarily in Southern California, where the banking business is highly competitive and is dominated by large multi-state and in-state banks with operations and offices covering

15

Table of Contents

wide geographic areas. We also compete with other financial service businesses, including investment advisory and wealth management firms, mutual fund companies, and securities brokerage and investment banking firms that offer competitive banking and financial products and services as well as products and services that we do not offer. Larger banks and many of those other financial service organizations have greater financial and marketing resources that enable them to conduct extensive advertising campaigns and to shift resources to regions or activities of greater potential profitability. They also have substantially more capital and higher lending limits, which enable them to attract larger clients and offer financial products and services that we are unable to offer, putting us at a disadvantage in competing with them for loans and deposits and investment management clients. If we are unable to compete effectively with those banking or other financial services businesses, we could find it more difficult to attract new and retain existing clients and our net interest margins, net interest income and investment management advisory fees could decline, which would adversely affect our results of operations and could cause us to incur losses in the future.

In addition, our ability to successfully attract and retain investment advisory and wealth management clients is dependent on our ability to compete with competitors’ investment products, level of investment performance, client services and marketing and distribution capabilities. If we are not successful in attracting new and retaining existing clients, our business, financial condition, results of operations and prospects may be materially and adversely affected.

The loss of key personnel or inability to attract additional personnel could hurt our future financial performance.

We currently depend heavily on the contributions and services provided by Rick Keller, our Executive Chairman, Scott Kavanaugh, Chief Executive Officer of FFI and FFB, John Hakopian, President of FFA, Dave Rahn, President of FFB and John Michel, Chief Financial Officer of FFI, FFB and FFA, as well as a number of other key management personnel. Our future success also will depend, in part, on our ability to attract and retain additional qualified relationship managers, private banking officers and investment managers. Competition for such personnel is intense and we may not succeed in retaining our existing personnel or attracting additional personnel we will need to continue to grow our business. If we are unable to continue to retain the services of any of our existing executive management personnel, or attract and retain qualified relationship managers, private banking officers and investment managers, our ability to retain existing clients or attract new clients could be adversely affected and our business, financial condition, results of operations or prospects could be significantly harmed.

Banking laws and government regulations may adversely affect our operations, restrict our growth or increase our operating costs.

We are also subject to extensive supervision and regulation by federal and California state bank regulatory agencies. The primary objective of these agencies is to protect bank depositors and not shareholders, whose respective interests often differ. These regulatory agencies have the legal authority to impose restrictions which they believe are needed to protect depositors, even if those restrictions would adversely affect the ability of a banking institution to expand its business, restrict its ability to pay cash dividends, cause its costs of doing business to increase, or hinder its ability to compete with less regulated financial services companies.

We are also subject to numerous laws and government regulations that are applicable to banks and other financial institutions, including:

Consumer Protection Laws and Regulations. We are required to comply with various consumer protection laws, including the Community Reinvestment Act, the Equal Credit Opportunity Act, the Fair Housing Act and other fair lending laws and regulations impose nondiscriminatory lending requirements on financial institutions.

16

Table of Contents

Bank Secrecy Act and other Anti-Money Laundering Laws and Regulations. As a financial institution, we are required by the Bank Secrecy Act, the USA PATRIOT Act of 2001 and other anti-money laundering laws and regulations, to institute and maintain an effective anti-money laundering program and file suspicious activity and currency transaction reports as appropriate. We are also subject to increased scrutiny of compliance with the rules enforced by the Office of Foreign Assets Control.

If the policies, procedures or systems which we have adopted to comply with these laws and regulations are found by any regulatory or other government agencies to be deficient or we fail to comply with any of these banking laws or regulations, we would be subject to liability, including fines and regulatory actions, which may lead to the imposition of restrictions on our ability to pay dividends or to proceed with certain aspects of our business plan, including our acquisition plans. Additionally, a failure to maintain and implement adequate programs to combat money laundering and terrorist financing could also have serious reputational consequences for us. Due, moreover, to the complex and technical nature of many of these laws and government regulations, inadvertent violations may and sometimes do occur. In such an event, we would be required to correct or implement measures to prevent a recurrence of such violations, which could increase our operating costs. If more serious violations were to occur, the regulatory agencies could limit our activities or growth, fine us, or ultimately put FFB out of business if it was to encounter severe liquidity problems or a significant erosion of capital below the minimum amounts required under applicable bank regulations. Any of these occurrences could have a material adverse effect on our business, financial condition, results of operations or prospects.

The enactment of the Dodd-Frank Act and the new Basel III capital rules pose uncertainties for our business and are likely to increase our costs of doing business in the future.

On July 21, 2010, the President signed the Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, into law. Changes made by the Dodd-Frank Act include, among others: (i) the establishment of new requirements on banking, derivative and investment activities, including modified capital requirements, (ii) the repeal of the prohibition on the payment of interest on business demand deposit accounts, (iii) the imposition of limitations on debit card interchange fees, (iv) the promulgation of enhanced financial institution safety and soundness regulations, (v) increases in assessment fees and deposit insurance coverage, and (vi) the establishment of new regulatory bodies, such as the Bureau of Consumer Financial Protection, or the BCFP. The BCFP has been granted rulemaking authority over several federal consumer financial protection laws and, in some instances, has the authority to examine and supervise and enforce compliance by banks and other financial service organizations with these laws and regulations. We expect that the Dodd-Frank Act and its implementing regulations will increase the costs of doing business for us, as well as for other banking institutions. We also expect that the repeal of the prohibition on the payment by banks of interest on business demand deposits will result in increased “price” competition among banks for such deposits, which could increase the costs of funds to us (as well as to other banks) and result in a reduction in our net interest margins and income in the future.