Attached files

| file | filename |

|---|---|

| EX-3.1 - EX-3.1 - Westlake Chemical Partners LP | d715499dex31.htm |

| EX-23.1 - EX-23.1 - Westlake Chemical Partners LP | d715499dex231.htm |

| EX-23.2 - EX-23.2 - Westlake Chemical Partners LP | d715499dex232.htm |

Table of Contents

Index to Financial Statements

As filed with the Securities and Exchange Commission on April 29, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Westlake Chemical Partners LP

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 2860 | 32-0436529 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification Number) |

2801 Post Oak Boulevard, Suite 600

Houston, Texas 77056

(713) 960-9111

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

L. Benjamin Ederington

Vice President, General Counsel and Secretary

2801 Post Oak Boulevard, Suite 600

Houston, Texas 77056

(713) 960-9111

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

| David P. Oelman E. Ramey Layne Vinson & Elkins L.L.P. 1001 Fannin Street, Suite 2500 Houston, Texas 77002 (713) 758-2222 |

William N. Finnegan IV Latham & Watkins LLP 811 Main Street, Suite 3700 Houston, Texas 77002 (713) 546-5400 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities To Be Registered |

Proposed Maximum Offering Price(1)(2) |

Amount of Registration Fee | ||

| Common units representing limited partner interests |

$271,687,000 | $34,993 | ||

|

| ||||

|

| ||||

| (1) | Includes common units issuable upon exercise of the underwriters’ option to purchase additional common units. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Index to Financial Statements

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated April 29, 2014

PROSPECTUS

Westlake Chemical Partners LP

Common Units

Representing Limited Partner Interests

This is the initial public offering of common units representing limited partner interests of Westlake Chemical Partners LP. We are offering common units. We were recently formed by Westlake Chemical Corporation (“Westlake”) and, prior to this offering, there has been no public market for our common units. We currently expect the initial public offering price to be between $ and $ per common unit. We intend to apply to list our common units on the New York Stock Exchange under the symbol “WLKP.”

Investing in our common units involves risks. Please read “Risk Factors” beginning on page 18.

These risks include the following:

| • | We are substantially dependent on Westlake for our cash flows. If Westlake does not pay us under the terms of the ethylene sales agreement (the “Ethylene Sales Agreement”) or if our assets fail to perform as intended, we may not have sufficient cash from operations following the establishment of cash reserves and payment of costs and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay the minimum quarterly distribution to our unitholders. |

| • | Westlake Chemical OpCo LP (“OpCo”), a partnership between Westlake and us, is a restricted subsidiary and guarantor under Westlake’s credit facility and the indentures governing its senior notes. Restrictions in the credit facility and indentures could limit OpCo’s ability to make distributions to us. |

| • | Our production facilities process volatile and hazardous materials that subject us to operating risks that could adversely affect our operating results. |

| • | Westlake owns and controls our general partner, which has sole responsibility for conducting our business and managing our operations. Our general partner and its affiliates, including Westlake, have conflicts of interest with us and limited duties, and they may favor their own interests to our detriment and that of our unitholders. |

| • | Holders of our common units have limited voting rights and are not entitled to elect our general partner or its directors, which could reduce the price at which our common units will trade. |

| • | Even if holders of our common units are dissatisfied, they cannot initially remove our general partner without its consent. |

| • | There is no existing market for our common units, and a trading market that will provide you with adequate liquidity may not develop. The price of our common units may fluctuate significantly, and unitholders could lose all or part of their investment. |

| • | Our tax treatment depends on our status as a partnership for federal income tax purposes, as well as us not being subject to a material amount of entity-level taxation by individual states. If the Internal Revenue Service were to treat us as a corporation for federal income tax purposes, or we become subject to entity-level taxation for state tax purposes, our distributable cash flow would be substantially reduced. |

| • | Even if you do not receive any cash distributions from us, you will be required to pay taxes on your share of our taxable income. |

| Per Common Unit | Total | |||||||

| Public Offering Price |

$ | $ | ||||||

| Underwriting Discount(1) |

$ | $ | ||||||

| Proceeds to Westlake Chemical Partners LP (before expenses) |

$ | $ | ||||||

| (1) | Excludes a structuring fee of % of the gross proceeds of this offering payable to Barclays Capital Inc. and UBS Securities LLC. Please read “Underwriting.” |

The underwriters may purchase up to an additional common units from us at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the common units to purchasers on or about , 2014 through the book-entry facilities of The Depository Trust Company.

| Barclays | UBS Investment Bank |

Prospectus dated , 2014

Table of Contents

Index to Financial Statements

[ARTWORK TO COME]

Table of Contents

Index to Financial Statements

i

Table of Contents

Index to Financial Statements

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

72 | |||

| 72 | ||||

| 72 | ||||

| 73 | ||||

| 73 | ||||

| Factors Affecting the Comparability of Our Financial Results |

75 | |||

| 75 | ||||

| 75 | ||||

| 76 | ||||

| 76 | ||||

| 79 | ||||

| 81 | ||||

| 81 | ||||

| 82 | ||||

| 83 | ||||

| 84 | ||||

| 84 | ||||

| 85 | ||||

| Locations of Ethylene Production Assets Utilizing Advantaged Ethane Feedstock in the U.S. |

87 | |||

| 88 | ||||

| 92 | ||||

| 92 | ||||

| 93 | ||||

| 93 | ||||

| 94 | ||||

| 95 | ||||

| 96 | ||||

| 97 | ||||

| 98 | ||||

| 98 | ||||

| 99 | ||||

| 100 | ||||

| 102 | ||||

| 102 | ||||

| 103 | ||||

| 104 | ||||

| 104 | ||||

| 104 | ||||

| 106 | ||||

| 107 | ||||

| 107 | ||||

| 108 | ||||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

112 | |||

| 114 | ||||

| 114 | ||||

| 114 | ||||

| Distributions and Payments to Our General Partner and Its Affiliates |

114 | |||

| 115 | ||||

| Procedures for Review, Approval and Ratification of Transactions with Related Persons |

122 | |||

ii

Table of Contents

Index to Financial Statements

| 123 | ||||

| 123 | ||||

| 123 | ||||

| 128 | ||||

| 131 | ||||

| 131 | ||||

| 131 | ||||

| 131 | ||||

| 133 | ||||

| 133 | ||||

| 133 | ||||

| 133 | ||||

| 133 | ||||

| 135 | ||||

| 135 | ||||

| 136 | ||||

| 136 | ||||

| Merger, Consolidation, Conversion, Sale or Other Disposition of Assets |

139 | |||

| 139 | ||||

| 140 | ||||

| 140 | ||||

| 141 | ||||

| 141 | ||||

| Transfer of Subordinated Units and Incentive Distribution Rights |

141 | |||

| 142 | ||||

| 142 | ||||

| 142 | ||||

| 143 | ||||

| 143 | ||||

| 144 | ||||

| 144 | ||||

| 144 | ||||

| 145 | ||||

| 145 | ||||

| 145 | ||||

| 146 | ||||

| 147 | ||||

| 149 | ||||

| 149 | ||||

| 151 | ||||

| 155 | ||||

| 156 | ||||

| 158 | ||||

| 159 | ||||

| 160 | ||||

| INVESTMENT IN WESTLAKE CHEMICAL PARTNERS LP BY EMPLOYEE BENEFIT PLANS |

162 | |||

| 163 | ||||

| 163 | ||||

| 164 | ||||

iii

Table of Contents

Index to Financial Statements

| 164 | ||||

| 165 | ||||

| 165 | ||||

| 165 | ||||

| 166 | ||||

| 166 | ||||

| 167 | ||||

| 167 | ||||

| 167 | ||||

| 167 | ||||

| 167 | ||||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| APPENDIX A—AMENDED AND RESTATED AGREEMENT OF LIMITED PARTNERSHIP OF WESTLAKE CHEMICAL PARTNERS LP |

A-1 | |||

| B-1 | ||||

You should rely only on the information contained in this prospectus, any free writing prospectus prepared by or on behalf of us or any other information to which we have referred you in connection with this offering. We have not, and the underwriters have not, authorized any other person to provide you with information different from that contained in this prospectus. Neither the delivery of this prospectus nor sale of our common units means that information contained in this prospectus is correct after the date of this prospectus. Our business, financial conditions, results of operations and prospects may have changed since that date. This prospectus is not an offer to sell or solicitation of an offer to buy our common units in any circumstances under which the offer or solicitation is unlawful.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Forward-Looking Statements.”

INDUSTRY AND MARKET DATA

The data included in this prospectus regarding the olefins industry, including trends in the market and our position and the position of our competitors within the olefins industry, is based on a variety of sources, including independent industry publications, government publications and other published independent sources, information obtained from customers, distributors, suppliers, trade and business organizations and publicly available information (including the reports and other information other companies file with the SEC, which we did not participate in preparing and as to which we make no representation), as well as our good faith estimates, which have been derived from management’s knowledge and experience in the areas in which our business operates. Estimates of market size and relative positions in a market are difficult to develop and inherently uncertain. Accordingly, investors should not place undue weight on the industry and market data presented in this prospectus. The sources of the industry and market data used herein are the most recent data available to management and therefore management believes such data to be reliable.

We commissioned Wood Mackenzie Limited (“Wood Mackenzie”), an independent market consultant, to assist in the preparation of the “Industry” section of this prospectus, but we have not funded, nor are we otherwise affiliated with, any other third-party source cited herein. Any data sourced from Wood Mackenzie is used with the express written consent of Wood Mackenzie.

iv

Table of Contents

Index to Financial Statements

This summary highlights selected information appearing elsewhere in this prospectus. Because it is abbreviated, this summary does not contain all of the information that you should consider before investing in our common units. While this summary highlights what we consider to be the most important information about us, you should read the entire prospectus carefully, including the historical combined carve-out and unaudited pro forma combined carve-out financial statements and the notes to those financial statements. The information presented in this prospectus assumes (i) an initial public offering price of $ per common unit (the mid-point of the price range set forth on the cover page of this prospectus) and (ii) unless otherwise indicated, that the underwriters’ option to purchase additional common units is not exercised. You should read “Risk Factors” beginning on page 18 for more information about important risks that you should consider carefully before investing in our common units.

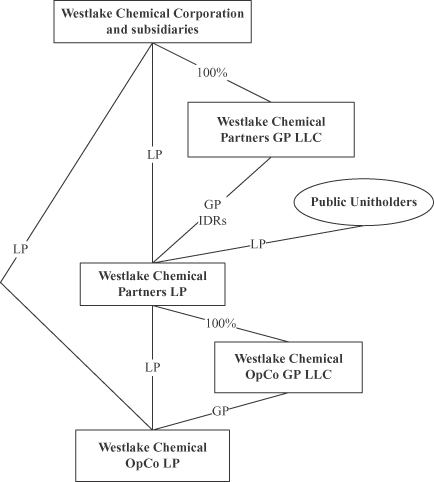

Unless the context otherwise requires, references in this prospectus to “our partnership,” “our,” “us,” “we” or like terms refer to “Westlake Chemical Partners LP” and, unless otherwise specified, Westlake Chemical OpCo LP and Westlake Chemical OpCo GP LLC. When used in a historical context, “our,” “us,” “we” or like terms refer to the ethylene business, including feedstock costs and revenue associated with the sale of ethylene and co-products, conducted by Westlake Chemical Corporation and its subsidiaries, a portion of which will be contributed to Westlake Chemical OpCo LP in connection with the closing of this offering. References in this prospectus to “our general partner” refer to Westlake Chemical Partners GP LLC. References to “OpCo” refer to Westlake Chemical OpCo LP, which is a newly created limited partnership owned by us and Westlake Chemical Corporation and its subsidiaries. References to “Westlake” refer collectively to Westlake Chemical Corporation and its subsidiaries, other than us, our general partner, OpCo and Westlake Chemical OpCo GP LLC, OpCo’s general partner. We will own a 10% limited partner interest and a general partner interest in OpCo. We will consolidate OpCo in our financial statements. We have provided definitions for some of the terms we use to describe our business and industry and other terms used in this prospectus in the “Glossary of Terms” attached as Appendix B to this prospectus.

Westlake Chemical Partners LP

We are a Delaware limited partnership recently formed by Westlake to operate, acquire and develop ethylene production facilities and related assets. Westlake is a vertically-integrated, international manufacturer and marketer of basic chemicals, polymers, and fabricated building products. Our business and operations are conducted through OpCo, a recently-formed partnership between Westlake and us. At the consummation of this offering, our assets will consist of a 10% limited partner interest in OpCo as well as the general partner interest in OpCo. Because we own OpCo’s general partner, we have control over all of OpCo’s assets and operations. Westlake has retained a 90% limited partner interest in OpCo and will retain a significant interest in us through its ownership of our general partner (which owns our incentive distribution rights) as well as % of our limited partner units (consisting of common units and all of the subordinated units).

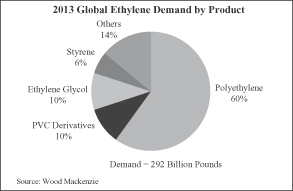

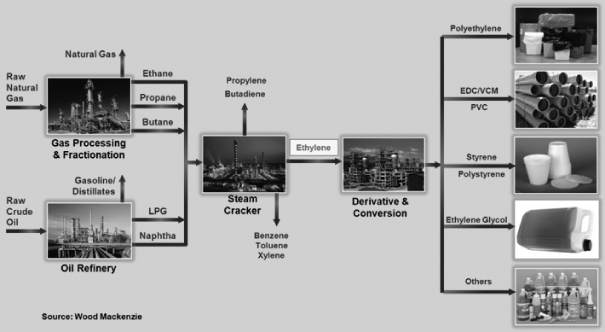

OpCo’s assets will be comprised of three ethylene production facilities, which convert primarily ethane into ethylene, with an aggregate annual capacity of approximately 3.4 billion pounds and a 200-mile ethylene pipeline. OpCo will derive substantially all of its revenue from its ethylene production facilities. Ethylene is the world’s most widely used petrochemical in terms of volume and is a key building block used to produce a number of key derivatives, such as polyethylene (“PE”) and polyvinyl chloride (“PVC”), which are used in a wide variety of end markets including packaging, construction and transportation. Westlake’s downstream PE and PVC production facilities will consume a substantial majority of the ethylene produced by OpCo. OpCo

1

Table of Contents

Index to Financial Statements

will generate revenue primarily by selling ethylene to Westlake and others, as well as through the sale of co-products of ethylene production, including propylene, crude butadiene, pyrolysis gasoline and hydrogen. Our sole revenue generating asset will be our 10% limited partner interest in OpCo.

In connection with this offering, OpCo will enter into a 12-year ethylene sales agreement with Westlake, under which Westlake will agree to purchase 95% of OpCo’s planned ethylene production each year on a cost-plus basis that is expected to generate a fixed margin per pound of $0.10 (the “Ethylene Sales Agreement”). We believe this agreement will promote more stable and predictable cash flows for OpCo. Any ethylene not sold to Westlake and all co-products that are produced by OpCo will be sold to third parties on either a spot or contract basis. OpCo will also enter into a feedstock supply agreement with Westlake that will supply OpCo with all of the ethane (and any other feedstocks) required for OpCo to produce ethylene under the Ethylene Sales Agreement (the “Feedstock Supply Agreement”).

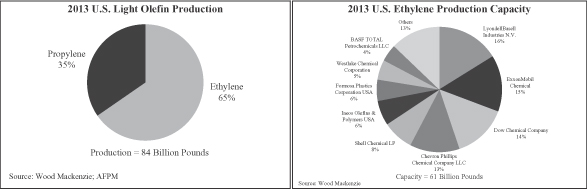

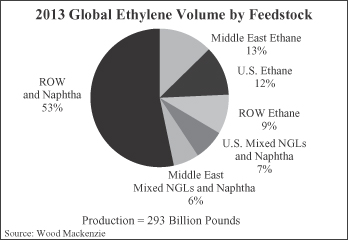

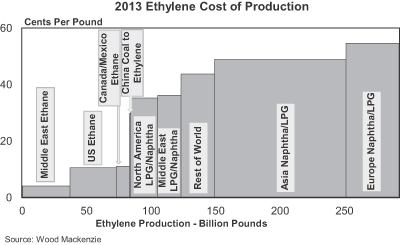

OpCo primarily uses ethane (a component of natural gas liquids, or NGLs) to produce ethylene. Approximately 66.5% of global ethylene production is based on higher priced feedstocks (primarily naphtha, as well as butane and propane) whose prices are linked to global oil prices. As a result, global ethylene and ethylene derivative prices have generally been linked to movements in global oil prices (principally Brent crude prices) for more than 20 years. In the U.S., technological advances in horizontal drilling and fracturing techniques in shale formations have dramatically increased the production of oil and gas and resulted in the oversupply of ethane. The spread between U.S. ethane and global oil prices has provided a margin advantage for U.S. ethane-based ethylene producers, such as OpCo. Throughout 2012 and 2013, production costs for U.S. ethane-based ethylene producers were significantly lower than global ethylene production facilities utilizing naphtha and other feedstocks. This feedstock cost advantage for U.S. ethane-based ethylene producers as compared to Asia naphtha-based ethylene producers has resulted in a positive cash cost differential that has ranged from $0.24 per pound to $0.49 per pound, and averaged $0.39 per pound, since 2012. Over the last decade, cash margins of U.S. ethane-based ethylene producers were above $0.10 per pound every year other than 2009, when cash margins were below $0.10 per pound due to the global economic recession.

Following the completion of this offering, Westlake will own a 90% limited partner interest in OpCo and will retain a significant interest in us through its ownership of our general partner (which owns our incentive distribution rights) as well as % of our limited partner units (consisting of common units and all of the subordinated units). Given Westlake’s significant ownership interest in us following this offering, we believe Westlake is incentivized to offer us the opportunity to purchase additional assets that it owns, including additional interests in OpCo, although it is under no obligation to do so. We may also pursue organic growth opportunities at OpCo as well as acquisitions from third parties, which could be effected jointly with Westlake. OpCo currently plans to expand the capacity of one of its ethylene production facilities by approximately 250 million pounds in late 2015 or early 2016.

For the year ended December 31, 2013, OpCo had pro forma revenues of approximately $1,202.8 million, pro forma EBITDA of approximately $367.1 million and pro forma net income of approximately $292.1 million. For the same time period, we had pro forma EBITDA (net of non-controlling interest) of approximately $36.7 million and pro forma net income (net of non-controlling interest) of approximately $29.2 million. On a pro forma basis, revenue from Westlake under the Ethylene Sales Agreement would have represented approximately 70% of OpCo’s pro forma revenues for the year ended December 31, 2013. The remaining 30% of OpCo’s pro forma revenues would have been comprised of third party ethylene and co-product sales. Please read “—Summary Historical and Pro Forma Combined Carve-out Financial and Operating Data—Non-GAAP Financial Measure” for the definition of EBITDA and a reconciliation of EBITDA to net income, on a historical basis and pro forma basis, and to cash flow from operating activities, on a historical basis, which reconciliation is presented in accordance with generally accepted accounting principles (“GAAP”).

2

Table of Contents

Index to Financial Statements

Our sole revenue generating asset will be our 10% limited partner interest in OpCo. We will also own the general partner interest of OpCo. OpCo, in turn, will own:

| • | two ethylene production facilities at Westlake’s Lake Charles, Louisiana complex (“Petro 1” and “Petro 2,” collectively referred to as “Lake Charles Olefins”), with a combined annual capacity of approximately 2.7 billion pounds; |

| • | one ethylene production facility at Westlake’s Calvert City, Kentucky complex (“Calvert City Olefins”), with an annual capacity of approximately 630 million pounds; and |

| • | a 200-mile common carrier ethylene pipeline that runs from Mont Belvieu, Texas to the Longview, Texas chemical complex, which includes Westlake’s Longview PE production facility (the “Longview Pipeline”). |

As the owner of the general partner interest of OpCo, we will control all aspects of the management of OpCo, including its cash distribution policy. See “Business—OpCo’s Assets.”

Ethylene Production Facilities. OpCo operates three ethylene production facilities. Ethylene can be produced from either NGL feedstocks, such as ethane, propane and butane, or from petroleum-derived feedstocks, such as naphtha. Lake Charles Olefins and Calvert City Olefins use ethane primarily as their feedstock. Calvert City Olefins can also use propane as a feedstock and Petro 2 can also use an ethane/propane mix, propane, butane or naphtha as a feedstock.

The following table provides information regarding OpCo’s ethylene production facilities as of , 2014:

| Plant Location (Description) |

Annual Production Capacity (millions of pounds) |

Feedstock |

Primary Uses of | |||||

| Lake Charles, LA (Petro 1) |

1,250 | ethane | PE and PVC | |||||

| Lake Charles, LA (Petro 2) |

1,490 | ethane, ethane/propane mix, propane, butane or naphtha | PE and PVC | |||||

| Calvert City, KY (Calvert City Olefins) |

630 | ethane or propane | PVC | |||||

|

|

|

|||||||

| Total |

3,370 | |||||||

|

|

|

|||||||

Longview Pipeline. OpCo owns the Longview Pipeline, which is a 200-mile common carrier ethylene pipeline, with a capacity of 3.5 million pounds per day that runs from Mont Belvieu, Texas to the Longview, Texas chemical complex, which includes Westlake’s Longview PE production facility.

Our Ethylene Sales Agreement with Westlake

In connection with this offering, OpCo will enter into the Ethylene Sales Agreement with Westlake. The Ethylene Sales Agreement will have an initial term through December 31, 2026 and will automatically renew thereafter for successive 12-month terms unless terminated by either party. The Ethylene Sales Agreement requires Westlake to purchase 95% of OpCo’s planned ethylene production each year, subject to certain exceptions and a maximum commitment of 3.8 billion pounds per year. If OpCo’s actual production is in excess of planned ethylene production, Westlake will have the option to purchase up to 95% of production in excess of planned production.

Westlake’s purchase price for the minimum commitment of ethylene under the Ethylene Sales Agreement will be calculated on a per pound basis and includes:

| • | the actual price paid by OpCo for the feedstock and natural gas to produce each pound of ethylene (subject to a cap and a floor on the amount of feedstock and natural gas used); plus |

3

Table of Contents

Index to Financial Statements

| • | the estimated per pound operating costs (including selling, general and administrative expenses) for the year and a five-year average of future expected maintenance capital expenditures and other turnaround expenditures; less |

| • | the proceeds received by OpCo from the sale of co-products associated with the ethylene purchased by Westlake; plus |

| • | a $0.10 per pound margin. |

Westlake’s purchase price for any ethylene produced in excess of the planned production amount will generally equal OpCo’s estimated variable costs of producing the incremental ethylene, plus a $0.10 per pound margin. The estimated operating costs and maintenance capital expenditures and other turnaround expenditures will be adjusted at the end of each year to reflect certain changes in forecasted costs. If OpCo’s actual operating costs and maintenance capital expenditures and other turnaround expenditures are higher than the estimate for any year, or OpCo’s actual production is below the planned production amount upon which the per pound operating costs and maintenance capital expenditures and other turnaround expenditures are based, OpCo will be entitled to include in the fee for the succeeding year a surcharge to recover the resulting shortfall. If these costs are lower than estimated, OpCo will retain the difference, but such difference may be reflected in periodic downward adjustments to the total estimated costs. The result of the fee structure is that OpCo should recover the portion of its total operating costs and maintenance capital expenditures and other turnaround expenditures attributable to Westlake’s ethylene purchases. Approximately 5% of OpCo’s ethylene production will be sold at market rates on either a spot or contract basis to third parties. Average U.S. industry margins for producing ethane-based ethylene are currently substantially in excess of $0.10 per pound, and averaged approximately $0.48 per pound in 2013.

Our primary business objective is to operate efficiently and safely and to grow our business responsibly, enabling us to increase the amount of cash distributions we make to our unitholders over time while maintaining our financial stability. We intend to accomplish these objectives by executing the following strategies:

| • | Generate Stable, Fee-Based Cash Flows. We are focused on generating stable cash flows by selling 95% of our ethylene production to Westlake under a long-term, fee-based contract. Our contract with Westlake includes minimum volume commitments and a pricing provision designed to permit OpCo to generally recover its costs (including selling, general and administrative expenses), plus a fixed $0.10 margin per pound of ethylene sold. In addition, we plan to supplement these relatively stable cash flows with additional cash flows by maximizing the price of the 5% of our ethylene production and associated co-products sold to third parties. We intend to maintain our focus on fee-based cash flows as we grow. |

| • | Focus on Operational Excellence. We intend to maximize the throughput of our production facilities while providing safe, reliable and efficient operations. We believe that a key component in generating stable cash flows is to continuously maintain, monitor and improve the safety and reliability of our operations. |

| • | Pursue Organic Growth Opportunities. We intend to enhance the profitability of OpCo’s existing assets by pursuing opportunities such as capacity expansion projects. OpCo plans to expand Petro 1 to increase capacity by approximately 250 million pounds in late 2015 or early 2016 and expects to finance this expansion through borrowings from Westlake. We may also pursue additional organic development projects complementary to our existing businesses, either through OpCo or independently. |

| • | Increase our Ownership of OpCo. We intend to increase our ownership interest in OpCo over time either by purchasing newly issued interests from OpCo or by purchasing outstanding interests in OpCo from Westlake. |

4

Table of Contents

Index to Financial Statements

| • | Pursue Growth Opportunities Through Acquisitions. We intend to pursue acquisitions of complementary assets from third parties. Such acquisitions could be pursued independently by OpCo, independently by us or jointly with Westlake. |

We believe we are well positioned to execute our business strategies based on the following competitive strengths:

| • | Stable and Predictable Cash Flows from OpCo. The Ethylene Sales Agreement is designed to cover our costs and provide a $0.10 margin per pound on a substantial majority of the ethylene we produce, reducing our exposure to commodity price volatility and promoting more stable cash flow. Westlake is obligated to purchase 95% of our planned ethylene production. In addition, Westlake is expected to exercise its option to purchase 95% of our excess production. We believe each of those factors should result in more stable cash flows. |

Each of OpCo’s ethylene production facilities requires turnaround maintenance on average every five years. OpCo intends to reserve approximately $28.9 million per year to fund these turnaround expenditures. Reserving these amounts should enable OpCo to maintain steady cash flows for distributions while funding these significant non-annual expenditures. We intend to use $ million from the proceeds of this offering to fund OpCo’s initial balance for this turnaround reserve. Westlake’s purchase price for ethylene purchased under the Ethylene Sales Agreement will include a component (adjusted annually) designed to cover, over the long term, substantially all of OpCo’s turnaround expenditures.

| • | Strategic Relationship with Westlake. We have a strategic relationship with Westlake, which we believe will provide both us and OpCo with a stable base of cash flows as well as opportunities for growth. Westlake has an investment grade credit rating and is well-capitalized. Westlake will own % of our limited partner units (consisting of common units and all of the subordinated units) and our general partner (which will own our incentive distribution rights). OpCo’s ethylene production facilities are a critical supply source for Westlake’s production of diversified downstream products including PE and PVC and this vertical integration enables Westlake to capture the economic value of the entire ethylene value chain. In particular, we expect to benefit from the following aspects of our relationship with Westlake: |

| • | Attractive Downstream Polyethylene Product Mix. Westlake focuses on a low-density PE (“LDPE”) and linear low-density PE (“LLDPE”) product mix. LDPE has enjoyed higher margins than LLDPE and high-density PE (“HDPE”), the more commoditized PE grades. A majority of Westlake’s production is LDPE. Westlake is a leading producer of LDPE by capacity in North America and predominantly uses the autoclave technology (as opposed to tubular technology), which is capable of producing higher margin specialty PE products. Autoclave LDPE is a more specialized form of LDPE that feeds into a broad array of end products. In contrast, tubular LDPE is a more commoditized form of LDPE with a narrower range of applications. Approximately 80% of Westlake’s LDPE production is autoclave. Furthermore, most announced LDPE industry capacity additions in North American are projected to be tubular LDPE. |

| • | Highly Integrated Polymers and Vinyls Chain. Westlake is highly integrated along its PVC production chain. Most U.S.-based PVC producers including Westlake internally produce their chlorine requirements, but most rely on the merchant market for their ethylene requirements. Westlake, however, is substantially integrated into ethylene as well. As a result, Westlake enjoys operational and cost advantages relative to non-ethylene integrated PVC producers. Importantly, PVC producers that are integrated in ethylene have a cost advantage that supports higher operating |

5

Table of Contents

Index to Financial Statements

| rates, allowing such producers to be opportunistic in targeting both the domestic and export markets. Westlake’s vinyls, PVC and downstream PVC building products businesses are well positioned to capitalize on improvements in the construction market, which could drive additional usage of ethylene. |

| • | Acquisition and Growth Opportunities. Immediately after this offering we will own a 10% limited partner interest in OpCo. The opportunity to acquire additional ownership interests in OpCo is an important potential source of our future growth, although Westlake has no obligation to sell additional interests in OpCo to us. |

| • | Access to Operational and Industry Expertise. We expect to benefit from Westlake’s extensive operational, commercial and technical expertise, as well as its industry relationships, as we seek to optimize and expand OpCo’s existing asset base. |

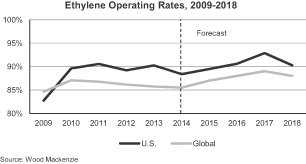

| • | Well Maintained Assets with Long History of Reliable Operations. OpCo continually invests in the maintenance and integrity of its assets. OpCo’s ethylene production facilities have operated above the industry average operating rate of 86.2% since 2005. OpCo conducts regularly scheduled turnarounds at each of its ethylene production facilities to perform planned major maintenance activities. OpCo is also continually focused on improving its asset portfolio and cost position. At Calvert City Olefins, OpCo recently completed an expansion and feedstock conversion project that resulted in a 180 million pound capacity expansion and also provided OpCo with 100% ethane feedstock capability. In addition, OpCo plans to expand Petro 1 by approximately 250 million pounds in late 2015 or early 2016. |

| • | Strategically Located Assets. OpCo benefits from the strategic location of its ethylene production facilities, which allows it to access low-cost ethane from the Gulf Coast and the Marcellus and Utica shale formations. Petro 1 and Petro 2 are both large-scale facilities with abundant feedstock sourcing capabilities given their proximity to Mont Belvieu, the largest NGLs hub on the Gulf Coast. Westlake currently supplies feedstock to Lake Charles Olefins through several pipelines from a variety of suppliers in Texas and Louisiana. Additionally, Calvert City Olefins is connected to the ATEX pipeline, allowing OpCo to use ethane feedstocks from the Marcellus and Utica shale formations. Westlake’s Calvert City complex is the only integrated U.S. vinyls complex located outside of the Gulf Coast, giving it a shipping advantage for certain key markets, such as the Midwest, the Northeast and Canada. OpCo recently completed an expansion and feedstock conversion project at this facility, which increased its ethylene production and enabled it to take advantage of low-cost ethane production from the Marcellus and Utica shale formations. |

| • | Conservative Financial Profile. OpCo has an intercompany credit agreement with Westlake that may be used to fund growth projects and working capital needs. We expect to have $ million of indebtedness at the closing of this offering and believe that our access to the debt and equity capital markets should provide us with the financial flexibility necessary to pursue organic expansion and acquisition opportunities. Westlake is a well-capitalized, credit worthy sponsor with an investment grade credit rating and a significant amount of liquidity. Westlake had cash, cash equivalents and current marketable securities of $700.7 million as of December 31, 2013. Westlake may also provide direct and indirect financing to us from time to time. |

| • | Experienced Management Team. Our management team consists of senior officers of Westlake, who average over 28 years of experience in the petrochemical industry. We believe the level of operational and financial expertise of our management team will prove critical in successfully executing our business strategies. |

Our Relationship With Westlake

Our principal strength is our relationship with Westlake. Westlake is a vertically-integrated, international manufacturer and marketer of basic chemicals, polymers and fabricated building products. Westlake benefits from highly-integrated production facilities that allow it to process raw materials into higher value-added

6

Table of Contents

Index to Financial Statements

chemicals and building products. As of December 31, 2013, Westlake had 13.6 billion pounds per year of aggregate production capacity at 15 manufacturing sites in North America as well as a 59% interest in a joint venture that operates a vinyls facility in China. For the year ended December 31, 2013, Westlake had consolidated revenues of approximately $3.8 billion and net income of $610.4 million. Westlake’s common stock trades on the New York Stock Exchange (“NYSE”) under the symbol “WLK.”

Westlake will retain a significant interest in us through its ownership of % of our limited partner units (consisting of common units and all of the subordinated units) and our general partner (which will own all of our incentive distribution rights). We believe Westlake will promote and support the successful execution of our business strategies because of its significant ownership in us and our general partner and its intention to use us to grow its ethylene business. We believe Westlake will offer us the opportunity to purchase additional assets from it, including additional interests in OpCo, although it is under no obligation to do so. We also may have the opportunity to pursue acquisitions which could be effected jointly with Westlake.

We will enter into an omnibus agreement with Westlake in connection with this offering. Under the omnibus agreement, Westlake will agree to indemnify OpCo for certain environmental and other liabilities relating to OpCo’s ethylene production facilities and related assets and OpCo will indemnify Westlake for certain environmental liabilities for which Westlake is not otherwise obligated to indemnify OpCo and certain other losses and liabilities resulting from Westlake providing services to OpCo. We or OpCo will enter into a number of agreements with Westlake in connection with this offering, including the Ethylene Sales Agreement described under “—Our Ethylene Sales Agreement with Westlake” and the Feedstock Supply Agreement. Please read “Certain Relationships and Related Transactions.”

While our relationship with Westlake and its subsidiaries is a significant strength, it is also a source of potential conflicts. Please read “Conflicts of Interest and Fiduciary Duties.”

An investment in our common units involves risks. You should carefully consider the risks described in “Risk Factors” and the other information in this prospectus before deciding whether to invest in our common units.

We are managed and operated by the board of directors and executive officers of our general partner, Westlake Chemical Partners GP LLC, a wholly owned subsidiary of Westlake. As a result of owning our general partner, Westlake will have the right to appoint all members of the board of directors of our general partner, including at least three directors meeting the independence standards established by the NYSE, and the board of directors of our general partner will appoint its executive officers. At least one of our independent directors will be appointed prior to the date our common units are listed for trading on the NYSE. Our unitholders will not be entitled to elect our general partner or its directors or otherwise directly participate in our management or operations. For more information about the executive officers and directors of our general partner, please read “Management.”

Summary of Conflicts of Interest and Fiduciary Duties

Our general partner has a contractual duty to manage us in a manner that it believes is not adverse to our interests. However, the officers and directors of our general partner have fiduciary duties to manage our general partner in a manner beneficial to Westlake, the owner of our general partner. As a result, conflicts of interest may arise in the future between us or our unitholders, on the one hand, and Westlake and our general partner, on the other hand.

7

Table of Contents

Index to Financial Statements

Our partnership agreement limits the liability of and replaces the fiduciary duties owed by our general partner to our unitholders. Our partnership agreement also restricts the remedies available to our unitholders for actions that might otherwise constitute a breach of duties by our general partner or its directors or officers. Our partnership agreement permits the board of directors of our general partner to form a conflicts committee of independent directors and to submit to that committee matters that the board believes may involve conflicts of interest. Any matters approved by the conflicts committee will be conclusively deemed to be approved by us and all of our partners and not a breach by our general partner of any duties it may owe us or our unitholders. By purchasing a common unit, the purchaser agrees to be bound by the terms of our partnership agreement, and each unitholder is treated as having consented to various actions and potential conflicts of interest contemplated in the partnership agreement that might otherwise be considered a breach of fiduciary or other duties under Delaware law.

For a more detailed description of the conflicts of interest and duties of our general partner and its directors and officers, please read “Conflicts of Interest and Fiduciary Duties.” For a description of other relationships with our affiliates, please read “Certain Relationships and Related Transactions.”

Principal Executive Offices and Internet Address

Our principal executive offices are located at 2801 Post Oak Boulevard, Suite 600, Houston, Texas 77056, and our telephone number is (713) 960-9111. Our website address will be http://www. .com. We intend to make our periodic reports and other information filed with or furnished to the U.S. Securities and Exchange Commission, or SEC, available, free of charge, through our website, as soon as reasonably practicable after those reports and other information are electronically filed with or furnished to the SEC. Information on our website or any other website is not incorporated by reference into this prospectus and does not constitute a part of this prospectus.

Formation Transactions and Partnership Structure

We are a Delaware limited partnership formed in March 2014 by Westlake to own and operate certain of the businesses that have historically been conducted by Westlake.

At or prior to the closing of this offering:

| • | Westlake will cause to be transferred to OpCo Lake Charles Olefins, Calvert City Olefins and the Longview Pipeline; |

| • | OpCo will enter into the Ethylene Sales Agreement with Westlake pursuant to which Westlake will commit to purchase ethylene from OpCo; and |

| • | OpCo will enter into other agreements with Westlake relating to the purchase and supply of ethane and other feedstocks, the operation of OpCo’s ethylene production facilities, the sharing of various site services and other matters. |

For further details on our agreements with Westlake and its affiliates, please read “Business—Agreements with Affiliates” and “Certain Relationships and Related Transactions.”

In connection with the closing of this offering, the following will occur:

| • | Westlake will contribute a % limited partner interest in OpCo to us; |

| • | Westlake will contribute OpCo’s general partner to us; |

| • | in exchange for Westlake’s contribution, we will issue to Westlake common units and all subordinated units; |

8

Table of Contents

Index to Financial Statements

| • | we will issue to our general partner all of our incentive distribution rights; |

| • | we will issue common units to the public; |

| • | we will receive gross proceeds of $ million from the issuance and sale of common units at an assumed initial offering price of $ per unit; |

| • | we will use $ million of the proceeds from this offering to pay underwriting discounts, a structuring fee totaling $ million and estimated offering expenses of $ million; |

| • | we will use $ million of the proceeds from this offering to purchase an additional % limited partner interest in OpCo (resulting in us owning a 10% limited partner interest), which OpCo will use to repay intercompany debt to Westlake and will use $ million to establish an initial cash reserve for turnaround expenditures; |

| • | we and OpCo will enter into an omnibus agreement with Westlake, our general partner and other affiliates governing, among other things, indemnification obligations; and |

| • | OpCo will enter into a credit facility with Westlake. |

We have granted the underwriters a 30-day option to purchase up to an aggregate of additional common units. Any net proceeds received from the exercise of this option will be used to purchase an additional limited partner interest in OpCo. The amount of the additional interest purchased will depend on the amount of the option exercised, and will be calculated at approximately % purchased for each one million of additional common units purchased by the underwriters. If the underwriters exercise their option to purchase additional common units in full, we would purchase an additional % limited partner interest in OpCo.

9

Table of Contents

Index to Financial Statements

The following is a simplified diagram of our ownership structure after giving effect to this offering and the related transactions.

| Public Common Units |

%(1) | |||

| Interests of Westlake: |

||||

| Common Units |

%(1) | |||

| Subordinated Units |

% | |||

| Non-Economic General Partner Interest |

0.0 | %(2) | ||

| Incentive Distribution Rights |

— | (3) | ||

|

|

|

|||

| 100.0 | % | |||

|

|

|

| (1) | Assumes no exercise of the underwriters’ option to purchase additional common units. |

| (2) | Our general partner owns a non-economic general partner interest in us. Please read “How We Make Distributions To Our Partners—General Partner Interest.” |

| (3) | Incentive distribution rights represent a variable interest in distributions and thus are not expressed as a fixed percentage. Please read “How We Make Distributions To Our Partners—Incentive Distribution Rights.” Distributions with respect to the incentive distribution rights will be classified as distributions with respect to equity interests. All of our incentive distribution rights will be issued to Westlake Chemical Partners GP LLC, our general partner, which is wholly owned by Westlake. |

10

Table of Contents

Index to Financial Statements

| Common units offered to the public |

common units. |

| common units if the underwriters exercise their option to purchase additional common units in full. |

| Units outstanding after this offering |

common units (or common units if the underwriters’ option to purchase additional common units is exercised in full) and subordinated units for a total of limited partner units (or limited partner units if the underwriters’ option to purchase additional common units is exercised in full). |

| Use of proceeds |

We intend to use the estimated net proceeds of approximately $ million from this offering (based on an assumed initial offering price of $ per common unit, the mid-point of the price range set forth on the cover page of this prospectus), after deducting the estimated underwriting discounts, structuring fee and offering expenses, to purchase a % limited partner interest in OpCo, and OpCo will use such net proceeds to repay $ million of intercompany debt to Westlake and establish a cash reserve of $ million for turnaround expenditures. The % interest in OpCo purchased with the proceeds from this offering, when combined with the % interest in OpCo contributed to us in connection with the formation transactions, will result in our ownership of a 10% limited partner interest in OpCo following the closing of this offering. |

| If the underwriters exercise their option to purchase additional common units in full, the additional net proceeds will be approximately $ million (based on an assumed initial offering price of $ per common unit, the mid-point of the price range set forth on the cover page of this prospectus). The net proceeds from any exercise of such option will be used to purchase an additional limited partner interest in OpCo, and OpCo will use such net proceeds to repay intercompany debt to Westlake. Please read “Use of Proceeds.” |

| Cash distributions |

Within 60 days after the end of each quarter, beginning with the quarter ending , 2014 we expect to make a minimum quarterly distribution of $ per common unit and subordinated unit ($ per common unit and subordinated unit on an annualized basis) to unitholders of record on the applicable record date. For the first quarter that we are publicly traded, we will pay a prorated distribution covering the period from the completion of this offering through , 2014, based on the actual length of that period. |

| The board of directors of our general partner will adopt a policy pursuant to which distributions for each quarter will be paid to the extent we have sufficient cash after establishment of cash reserves and payment of fees and expenses, including payments to our general partner and its affiliates. Our ability to pay the minimum quarterly |

11

Table of Contents

Index to Financial Statements

| distribution is subject to various restrictions and other factors described in more detail in “Cash Distribution Policy and Restrictions on Distributions.” |

| Our partnership agreement generally provides that we will distribute cash each quarter during the subordination period in the following manner: |

| • | first, to the holders of common units, until each common unit has received the minimum quarterly distribution of $ , plus any arrearages from prior quarters; |

| • | second, to the holders of subordinated units, until each subordinated unit has received the minimum quarterly distribution of $ ; and |

| • | third, to the holders of common and subordinated units, pro rata, until each unit has received a distribution of $ . |

| If cash distributions to our unitholders exceed $ per common unit and subordinated unit in any quarter, our unitholders and our general partner, as the holder of our incentive distribution rights (or IDRs), will receive distributions according to the following percentage allocations: |

| Marginal Percentage Interest in Distributions |

||||||||

| Total Quarterly Distribution Target Amount |

Unitholders | General Partner (as holder of IDRs) |

||||||

| above $ up to $ |

85.0 | % | 15.0 | % | ||||

| above $ up to $ |

75.0 | % | 25.0 | % | ||||

| above $ |

50.0 | % | 50.0 | % | ||||

| We refer to the additional increasing distributions to our general partner as “incentive distributions.” Please read “How We Make Distributions To Our Partners—Incentive Distribution Rights.” |

| The amount of distributable cash flow we generated during the year ended December 31, 2013 on a pro forma basis would have been approximately $26.3 million. This amount would have been sufficient to pay 100% of the aggregate minimum quarterly distribution on all common units for that period. However, this amount would only allow us to pay a cash distribution of $ per quarter ($ on an annualized basis), or approximately % of the minimum quarterly distribution, on all of our subordinated units. Please read “Cash Distribution Policy and Restrictions on Distributions.” |

| We believe, based on our financial forecast and related assumptions included in “Cash Distribution Policy and Restrictions on Distributions,” that we will have sufficient distributable cash flow to pay the minimum quarterly distribution of $ on all of our common units and subordinated units for the twelve months ending June 30, 2015. However, we do not have a legal or contractual obligation to pay quarterly distributions at the minimum quarterly distribution rate or at any other rate and there is no guarantee that we |

12

Table of Contents

Index to Financial Statements

| will pay distributions to our unitholders in any quarter. Please read “Cash Distribution Policy and Restrictions on Distributions.” |

| Subordinated Units |

Westlake will initially own all of our subordinated units. The principal difference between our common units and subordinated units is that for any quarter during the subordination period, holders of the subordinated units will not be entitled to receive any distribution from operating surplus until the common units have received the minimum quarterly distribution from operating surplus for such quarter plus any arrearages in the payment of the minimum quarterly distribution from prior quarters. Subordinated units will not accrue arrearages. |

| Conversion of subordinated units |

The subordination period will end on the first business day after we have earned and paid an aggregate amount of at least the minimum quarterly distribution multiplied by the total number of outstanding common and subordinated units for each of three consecutive, non-overlapping four-quarter periods ending on or after , 2017 and there are no outstanding arrearages on our common units. |

| Notwithstanding the foregoing, the subordination period will end on the first business day after we have paid an aggregate amount of at least 150.0% of the minimum quarterly distribution on an annualized basis multiplied by the total number of outstanding common and subordinated units and we have earned that amount plus the related distribution on the incentive distribution rights, for any four-quarter period ending on or after , 2015 and there are no outstanding arrearages on our common units. |

| When the subordination period ends, all subordinated units will convert into common units on a one-for-one basis, and all common units will thereafter no longer be entitled to arrearages. |

| Issuance of additional units |

Our partnership agreement authorizes us to issue an unlimited number of additional units without the approval of our unitholders. Please read “Units Eligible for Future Sale” and “The Partnership Agreement—Issuance of Additional Interests.” |

| Limited voting rights |

Our general partner will manage and operate us. Unlike the holders of common stock in a corporation, our unitholders will have only limited voting rights on matters affecting our business. Our unitholders will have no right to elect our general partner or its directors on an annual or other continuing basis. Our general partner may not be removed except by a vote of the holders of at least 66 2/3% of the outstanding units, including any units owned by our general partner and its affiliates, voting together as a single class. Upon consummation of this offering, Westlake will own an aggregate of % of our outstanding units (or % of our outstanding units, if the underwriters exercise their option to purchase additional common units in full). This will give Westlake the ability to prevent the removal of our general partner. In addition, any vote to remove our general partner during the subordination period must provide for the election of a successor general partner by the holders of a majority of |

13

Table of Contents

Index to Financial Statements

| the common units and a majority of the subordinated units, voting as separate classes. This will provide Westlake the ability to prevent the removal of our general partner. Please read “The Partnership Agreement—Voting Rights.” |

| Limited call right |

If at any time our general partner and its affiliates own more than 80% of the outstanding common units, our general partner has the right, but not the obligation, to purchase all of the remaining common units at a price equal to the greater of (i) the average of the daily closing price of the common units over the 20 trading days preceding the date three days before notice of exercise of the call right is first mailed and (ii) the highest per-unit price paid by our general partner or any of its affiliates for common units during the 90-day period preceding the date such notice is first mailed. Please read “The Partnership Agreement—Limited Call Right.” |

| Directed Unit Program |

At our request, the underwriters have reserved up to % of the common units being offered by this prospectus for sale at the initial public offering price to the officers, directors and employees of our general partner and its affiliates and certain other persons associated with us, as designated by us. For further information regarding our directed unit program, please read “Underwriting.” |

| Members of the Chao family or entities affiliated with such members, who in the aggregate beneficially own approximately 69% of Westlake’s common stock, have indicated an interest in purchasing a portion of the common units being offered in this offering through our directed unit program. |

| Estimated ratio of taxable income to distributions |

We estimate that if you own the common units you purchase in this offering through the record date for distributions for the period ending December 31, 2016, you will be allocated, on a cumulative basis, an amount of federal taxable income for that period that will be less than 20% of the cash distributed to you with respect to that period. For example, if you receive an annual distribution of $ per unit, we estimate that your average allocable federal taxable income per year will be no more than approximately $ per unit. Thereafter, the ratio of allocable taxable income to cash distributions to you could substantially increase. Please read “Material U.S. Federal Income Tax Consequences—Tax Consequences of Unit Ownership” for the basis of this estimate. |

| Material federal income tax consequences |

For a discussion of the material federal income tax consequences that may be relevant to unitholders who are individual citizens or residents of the United States, please read “Material U.S. Federal Income Tax Consequences.” |

| Exchange listing |

We intend to apply to list our common units on the New York Stock Exchange (the “NYSE”) under the symbol “WLKP.” |

14

Table of Contents

Index to Financial Statements

Summary Historical and Pro Forma Combined Carve-out Financial and Operating Data

We were formed on March 14, 2014 and have had no operations since formation. Therefore, our historical financial data is not included in the following table. The following table shows summary historical combined carve-out financial data of the predecessor of Westlake Chemical Partners LP (the “Predecessor”). The following table also shows our summary unaudited pro forma combined carve-out financial data for the period and as of the date indicated. The summary historical combined carve-out balance sheet data presented as of December 31, 2013 and 2012 and the statement of operations data for the years ended December 31, 2013, 2012, and 2011 are derived from the audited historical combined carve-out financial statements of our Predecessor, which are included elsewhere in this prospectus. The summary historical combined carve-out balance sheet data presented as of December 31, 2011 is derived from the unaudited historical combined carve-out financial statements of our Predecessor, which are not included in this prospectus.

The summary historical combined carve-out financial statements of our Predecessor reflect Westlake’s entire ethylene business, including, but not limited to, procuring feedstock, managing inventory and commodity risk and transporting ethylene from manufacturing facilities. Our assets on the closing date of the offering will consist only of our 10% limited partner interest in OpCo. OpCo’s assets will consist of Lake Charles Olefins, Calvert City Olefins and the Longview Pipeline. OpCo’s financial results will be consolidated into ours for financial reporting purposes. The following table should be read together with, and is qualified in its entirety by reference to, the historical audited combined carve-out financial statements of the Predecessor and the accompanying notes included elsewhere in this prospectus. The following table should also be read together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The summary unaudited pro forma combined carve-out financial data presented in the following table as of, and for the year ended, December 31, 2013, are derived from the unaudited pro forma combined carve-out financial statements included elsewhere in this prospectus. The unaudited pro forma combined carve-out balance sheet assumes the offering and the related transactions occurred as of December 31, 2013, and the unaudited pro forma combined carve-out statement of operations for the year ended December 31, 2013, assumes the offering and the related transactions occurred as of January 1, 2013. These transactions include, and the unaudited pro forma combined carve-out financial statements give effect to, the following:

| • | Westlake’s contribution to OpCo of Lake Charles Olefins, Calvert City Olefins and the Longview Pipeline; |

| • | the transfer by Westlake to us of a limited partner interest in OpCo, and a 100% interest in Westlake Chemical OpCo GP LLC, which holds the general partner interest in OpCo, in exchange for the issuance by us to subsidiaries of Westlake of common units, subordinated units and all of the incentive distribution rights; |

| • | the consummation of this offering and our issuance of common units to the public at an assumed initial offering price of $ per unit and the use of proceeds therefrom as described under “Use of Proceeds”; and |

| • | OpCo’s execution of the Ethylene Sales Agreement, omnibus agreement and services agreement with Westlake. |

The unaudited pro forma combined carve-out financial statements do not give effect to an estimated $3.0 million in incremental general and administrative expenses that we expect to incur annually as a result of being a separate, publicly traded partnership, including costs associated with preparing and filing annual and quarterly reports to unit holders, financial statement audits, tax return and Schedule K-1 preparation and distribution, investor relations activities, registrar and transfer agent fees and independent director compensation.

15

Table of Contents

Index to Financial Statements

The following table presents the non-GAAP financial measure of EBITDA, which we use in our business. For a definition of EBITDA and a reconciliation to our most directly comparable financial measures calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measure.”

| Westlake Chemical Partners

LP Predecessor Historical |

Westlake Chemical Partners LP Pro Forma |

|||||||||||||||

| Year Ended December 31, | ||||||||||||||||

| 2013 | 2012 | 2011 | 2013 | |||||||||||||

| (dollars in thousands, except per unit data) |

(unaudited) | |||||||||||||||

| Combined Carve-out Statement of Operations Data: |

||||||||||||||||

| Total net sales |

$ | 2,127,747 | $ | 2,249,098 | $ | 2,251,043 | $ | 1,202,791 | ||||||||

| Gross profit |

872,607 | 635,652 | 409,098 | 322,450 | ||||||||||||

| Selling, general and administrative expenses |

25,451 | 24,103 | 24,312 | 25,451 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income from operations |

847,156 | 611,549 | 384,786 | 296,999 | ||||||||||||

| Interest expense—Westlake |

(8,032 | ) | (8,937 | ) | (8,947 | ) | (3,460 | ) | ||||||||

| Other income (expense), net |

7,701 | 4,186 | 2,804 | (168 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before income taxes |

846,825 | 606,798 | 378,643 | 293,371 | ||||||||||||

| Provision for income taxes |

300,279 | 210,878 | 131,670 | 1,316 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

$ | 546,546 | $ | 395,920 | $ | 246,973 | $ | 292,055 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income attributable to Westlake Chemical Partners LP |

$ | 29,205 | ||||||||||||||

| Limited partners’ interest in net income attributable to Westlake Chemical Partners LP |

||||||||||||||||

| Common units |

$ | |||||||||||||||

| Subordinated units |

$ | |||||||||||||||

| Net income per limited partner unit (basic and diluted): |

||||||||||||||||

| Common units |

$ | |||||||||||||||

| Subordinated units |

$ | |||||||||||||||

| Combined Carve-out Balance Sheet Data (end of period): |

||||||||||||||||

| Working capital |

$ | 43,642 | $ | 40,336 | $ | 90,420 | ||||||||||

| Total assets |

1,041,474 | 834,843 | 800,376 | |||||||||||||

| Total debt |

252,973 | 253,000 | 253,000 | |||||||||||||

| Net investment |

455,432 | 273,812 | 216,705 | |||||||||||||

| Combined Carve-out Cash Flow Data: |

||||||||||||||||

| Cash flow from: |

||||||||||||||||

| Operating activities |

$ | 602,509 | $ | 496,821 | $ | 268,716 | ||||||||||

| Investing activities |

(230,050 | ) | (158,008 | ) | (71,637 | ) | ||||||||||

| Financing activities |

(372,459 | ) | (338,813 | ) | (197,079 | ) | ||||||||||

| Other Data: |

||||||||||||||||

| Depreciation and amortization |

$ | 73,463 | $ | 64,257 | $ | 57,193 | ||||||||||

| Capital expenditures |

223,130 | 158,440 | 73,681 | |||||||||||||

| EBITDA(1) |

928,320 | 679,992 | 444,783 | $ | 367,086 | |||||||||||

| EBITDA attributable to Westlake Chemical Partners LP |

$ | 36,709 | ||||||||||||||

| (1) | For a definition of EBITDA and a reconciliation of EBITDA to our most directly comparable financial measures calculated and presented in accordance with GAAP, please read “—Non-GAAP Financial Measure.” |

16

Table of Contents

Index to Financial Statements

We define EBITDA as net income before interest expense, income taxes, depreciation and amortization. EBITDA is not a measure made in accordance with GAAP. EBITDA is used as a supplemental financial measure by management and by external users of our financial statements, such as investors, lenders and rating agencies, to assess:

| • | our operating performance as compared to that of other publicly traded partnerships, without regard to historical cost basis or capital structure; |

| • | our ability to incur and service debt and fund capital expenditures; and |

| • | the viability of acquisitions and other capital expenditure projects and the returns on investment of various investment opportunities. |

We believe that the presentation of EBITDA in this prospectus provides useful information to investors in assessing our financial condition and results of operations. The GAAP measures most directly comparable to EBITDA are net income and cash flow from operating activities. EBITDA should not be considered as an alternative to GAAP net income or cash flow from operating activities. EBITDA has important limitations as an analytical tool because it excludes some but not all items that affect net income and cash flow from operating activities. You should not consider EBITDA in isolation or as a substitute for analysis of our results as reported under GAAP. Additionally, because EBITDA may be defined differently by other companies in our industry, our definition of EBITDA may not be comparable to similarly titled measures of other companies, thereby diminishing its utility.

The following table presents a reconciliation of EBITDA to net income, on a historical basis and pro forma basis, and cash flow from operating activities, on a historical basis.

| Westlake Chemical Partners LP Predecessor Historical |

Westlake Chemical Partners LP Pro Forma |

|||||||||||||||

| Year Ended December 31, | ||||||||||||||||

| 2013 | 2012 | 2011 | 2013 | |||||||||||||

| (dollars in thousands) | (unaudited) | |||||||||||||||

| Reconciliation of EBITDA and Pro Forma EBITDA to net income and cash flow from operating activities |

||||||||||||||||

| EBITDA attributable to Westlake Chemical Partners LP |

$ | 36,709 | ||||||||||||||

| Add: EBITDA attributable to noncontrolling interest in OpCo |

330,377 | |||||||||||||||

| EBITDA |

$ | 928,320 | $ | 679,992 | $ | 444,783 | 367,086 | |||||||||

| Less: |

||||||||||||||||

| Provision for income taxes |

(300,279 | ) | (210,878 | ) | (131,670 | ) | (1,316 | ) | ||||||||

| Interest expense |

(8,032 | ) | (8,937 | ) | (8,947 | ) | (3,460 | ) | ||||||||

| Depreciation and amortization |

(73,463 | ) | (64,257 | ) | (57,193 | ) | (70,255 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

$ | 546,546 | $ | 395,920 | $ | 246,973 | $ | 292,055 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Changes in operating assets and liabilities, and other |

16,562 | 105,804 | 22,907 | |||||||||||||

| Equity in loss (income) of joint venture, net of dividends |

402 | 277 | (364 | ) | ||||||||||||

| Deferred income taxes |

37,054 | (8,096 | ) | (1,859 | ) | |||||||||||

| Loss from disposition of fixed assets |

1,905 | 2,834 | 30 | |||||||||||||

| Provision for doubtful accounts |

40 | 82 | 1,029 | |||||||||||||

|

|

|

|

|

|

|

|||||||||||

| Cash flow from operating activities |

$ | 602,509 | $ | 496,821 | $ | 268,716 | ||||||||||

|

|

|

|

|

|

|

|||||||||||

17

Table of Contents

Index to Financial Statements

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors together with all of the other information included in this prospectus in evaluating an investment in our common units.

If any of the following risks were to occur, our business, financial condition, results of operations and distributable cash flow could be materially adversely affected. In that case, we might not be able to make distributions on our common units, the trading price of our common units could decline and you could lose all or part of your investment.

Risks Inherent in Our Business

We are substantially dependent on Westlake for our cash flows. If Westlake does not pay us under the terms of the Ethylene Sales Agreement or if our assets fail to perform as intended, we may not have sufficient cash from operations following the establishment of cash reserves and payment of costs and expenses, including cost reimbursements to our general partner and its affiliates, to enable us to pay the minimum quarterly distribution to our unitholders.

We may not have sufficient cash each quarter to pay the full amount of our minimum quarterly distribution of $ per unit, or $ per unit per year, which will require us to have distributable cash flow of approximately $ million per quarter, or $ million per year, based on the number of common and subordinated units that will be outstanding after the completion of this offering.

Initially, all of our cash flow will be generated from cash distributions from OpCo, a partnership between us and Westlake, and a substantial majority of OpCo’s cash flow will be generated from payments by Westlake under the Ethylene Sales Agreement. Westlake’s obligations to purchase ethylene under the Ethylene Sales Agreement may be temporarily suspended to the extent OpCo is unable to perform its obligations caused by any of certain events outside the reasonable control of OpCo. Such events include, for example, acts of God or calamities which affect the operation of OpCo’s facilities; certain labor difficulties (whether or not the demands of the employees are within the power of OpCo to concede); and governmental orders or laws. In addition, Westlake is not obligated to purchase ethylene with respect to any period during which OpCo’s facilities are not operating due to scheduled or unscheduled maintenance or turnarounds other than under certain circumstances relating to the occurrence of force majeure. A suspension of Westlake’s obligations under the Ethylene Sales Agreement would reduce OpCo’s revenues and cash flows, and could materially adversely affect our ability to make distributions to our unitholders.

Westlake may be unable to generate enough cash flow from operations to meet its minimum obligations under the Ethylene Sales Agreement if its business is adversely impacted by competition, operational problems, general adverse economic conditions or inability to obtain feedstock. If Westlake were unable to meet its minimum payment obligations to OpCo as a result of any one or more of these factors, our ability to make distributions to our unitholders would be reduced or eliminated. The level of payments made by Westlake will depend upon its ability to pay its minimum obligations under the Ethylene Sales Agreement and its ability and election to increase volumes above the minimums specified in the Ethylene Sales Agreement, which in turn are dependent upon, among other things, the level of production at Westlake’s other facilities. If Westlake is unable to generate sufficient cash flow from its operations to meet its obligations under the Ethylene Sales Agreement, OpCo will not have sufficient available cash to distribute to us to enable us to pay the minimum quarterly distribution, which will fluctuate from quarter to quarter based on the following factors, some of which are beyond our control:

| • | severe financial hardship or bankruptcy of Westlake or one of our other customers, or the occurrence of other events affecting our ability to collect payments from Westlake or our other customers, including any of our customers’ default; |

18

Table of Contents

Index to Financial Statements

| • | volatility and cyclical downturns in the chemicals industry and other industries which materially and adversely impact Westlake and our other customers; |

| • | Westlake’s inability to perform under the Ethylene Sales Agreement; |