Attached files

| file | filename |

|---|---|

| EX-99.2 - PRINT VERSION OF QUARTERLY INVESTOR UPDATE - SPRINT Corp | a1q14sprintquarterlyinvestor.pdf |

| 8-K - FORM 8-K - SPRINT Corp | d8k.htm |

| EX-99.1 - PRESS RELEASE ANNOUNCING QUARTER ENDED MARCH 31, 2014 RESULTS - SPRINT Corp | dex991.htm |

SPRINT REPORTS RESULTS FOR QUARTER ENDED MARCH 31, 2014

● | Operating Income of $420 million is best in over seven years |  | |

● | Adjusted EBITDA* of more than $1.84 billion grew 22 percent year-over-year; third consecutive quarter of year-over-year growth | ||

● | Launched revolutionary Sprint FramilySM plans and new marketing campaigns | ||

○ | Nearly 3 million customers now on Sprint Framily plans | ||

● | Network deployments remain on track | ||

○ | 4G LTE coverage expected to reach 250 million people by mid-year | ||

○ | 3G and voice network rip and replace expected to be largely complete by mid-year | ||

○ | Sprint SparkTM now available in 24 markets with the launch of six more markets today including Orlando, Fla. and Oakland, Calif. | ||

Financial results in the enclosed tables include a predecessor period for the first quarter of 2013 related to the results of operations of Sprint Communications, Inc. (formerly Sprint Nextel) prior to the closing of the SoftBank transaction on July 10, 2013, and the applicable successor periods. In order to present financial results in a way that offers investors a more meaningful comparison of the year-over-year quarterly results, we have combined the first quarter 2013 results of operations for the predecessor and successor periods. The enclosed remarks relating to first quarter of 2013 are in reference to an unaudited combined period, unless otherwise noted. For additional information, please reference the section titled Financial Measures.

| TABLE OF CONTENTS | ||

Consolidated Results | 5 | ||

Wireless Results | 6 | ||

Wireline Results | 9 | ||

SPRINT'S EARNINGS CONFERENCE CALL - 8 A.M. ET TODAY | Forecast | 9 | |

U.S. or Canada: 800-938-1120 | Financial and Operational Results | 10 | |

Internationally: 706-634-7849 | Notes to Financial Information | 18 | |

Conference ID: 15177040 | Financial Measures | 18 | |

To listen via the Internet: sprint.com/investors | Safe Harbor | 20 | |

Sprint Corporation (NYSE: S) today reported operating results for the quarter ended March 31, 2014, including consolidated operating income of $420 million, the company’s best performance in over seven years. Adjusted EBITDA* of over $1.84 billion in the quarter grew 22 percent over the prior year period, and Adjusted EBITDA* margin of 23.4 percent was the highest in almost six years.

“In the quarter, operating revenue and Adjusted EBITDA* both grew year-over-year even as investments in our network improvements continued,” said Dan Hesse, Sprint CEO. “With the expected mid-year completion of the rip and replacement of our core 3G and voice network, the ongoing roll-out of Sprint SparkTM, and the evolution of Sprint FramilySM, we plan to build the best customer experience in the industry.”

Net Loss Narrows as Adjusted EBITDA* Grows |  |

Quarterly net loss was $151 million in the quarter, a 77 percent improvement from the first quarter of 2013, driven by growth in Adjusted EBITDA* of 22 percent compared to last year. Quarterly Adjusted EBITDA* of $1.84 billion improved by over $300 million compared to the first quarter of 2013, driven by growth in wireless Adjusted EBITDA*, partially offset by a decline in wireline. The growth in wireless Adjusted EBITDA* was primarily attributable to lower wireless expenses such as postpaid subsidy associated with impacts of the newly launched Sprint Easy Pay installment billing plan and device sales mix, lower customer care and cost of service expenses. | |

Subscriber Results | |

At the end of the quarter, the Sprint platform served nearly 54 million subscribers. During the quarter, Sprint platform postpaid gross additions grew by over 16 percent compared to the year-ago quarter, and retail smartphone sales were just under 5 million, representing 84 percent of total retail handset device sales in the quarter. Sprint reported a net loss of 231,000 Sprint platform postpaid customers during the quarter largely due to expected elevated churn levels related to service disruption associated with the company’s ongoing network overhaul. Sprint platform prepaid net loss of 364,000 customers was primarily caused by changes in the Lifeline program recertification process that impacted the Assurance Wireless® subscriber base. Sprint added 212,000 wholesale and affiliate customers during the quarter. | |

4G LTE, Sprint Spark and High-Definition Voice Deployment Continue to Expand | |

Sprint 4G LTE coverage is now available to more than 225 million people. The company continues to expect that by the middle of this year 4G LTE coverage will reach 250 million people. Additionally, Sprint’s replacement of its entire 3G and voice network and the nationwide roll-out of high-definition voice service are both expected to be largely complete by mid-year. | |

Deployment of Sprint Spark is also progressing with today’s launches in six more cities, including, Orlando, Fla. and Oakland, Calif. Sprint Spark is now available in 24 markets across the country and 14 Sprint Spark-capable devices are currently available, including the recently launched Samsung Galaxy S® 5 and HTC One (M8). | |

Sprint Spark is an innovative combination of advanced network and device technology with the potential to surpass wireless speeds of any U.S. network provider, capable of delivering 50-60 Megabits per second peak speeds today with potential speeds three times as fast by late 2015. Sprint Spark leverages the company’s 800MHz, 1.9GHz and 2.5GHz spectrum together with devices offering tri-band capability and high-definition voicei. | |

Sprint plans to deploy Sprint Spark in about 100 of America’s largest cities during the next three years. | |

THE SPRINT QUARTERLY INVESTOR UPDATE | 3 |

Join the Framily |

Early in the quarter, Sprint introduced Sprint Framily, a revolutionary new pricing program that lets customers build their own group plans bringing together their family and friends. This offering uniquely addresses the changing demographics of American society. |

Although Sprint Framily was only available in Sprint-branded stores during the quarter, it has grown faster than any new Sprint rate plan on record. Nearly 3 million customers are already enjoying the benefits of Sprint Framily and additional growth is anticipated as availability expands to other distribution channels. |

Sprint Leadership and Innovation Gains Third-Party Recognition |

For the fourth consecutive year, Sprint received a Best-In-Class Award from ATLANTIC-ACM, which named Sprint Wholesale Solutions as No. 1 for performance in the Voice Value category. In April, Sprint was the winner of the Informa Telecoms & Media MVNO’s Industry Awards 2013 Best Wholesale Operator for the second consecutive year. Sprint also received the 2014 Compass Intelligence A-List in M2M Award for its Sprint VelocitySM solution, winning in the Enabling Software or Technology for Automotive category. |

Boost Mobile received its third consecutive highest ranking for Non-Contract Providers from J.D. Power in the 2014 U.S. Wireless Purchase Experience Non-Contract StudySM, Volume 1. It was the seventh J.D. Power award since 2011 for Boost, which was also named as a J.D. Power 2014 Customer Champion - one of 50 companies across many industries to earn this distinction. Additionally, Sprint CEO Dan Hesse was named a Highest Rated CEO by Glassdoor, and was the only telecommunications executive to be named by employees in the CEO rankings. |

Sprint also received multiple awards for its corporate responsibility efforts. For the third straight year, Sprint was recognized as having the best phone buyback program among all major U.S. carriers by Compass Intelligence and, for the second consecutive year, Frost & Sullivan awarded Sprint its 2014 North American Award for Green Excellence. Sprint received the Supply Chain Leadership and Organizational Leadership awards from the U.S. Environmental Protection Agency for its supply chain engagement practices and the company’s continued focus to reduce greenhouse gas emissions. Finally, earlier this month PR News named Sprint as the 2014 best CSR corporation with more than 25,000 employees. |

THE SPRINT QUARTERLY INVESTOR UPDATE | 4 |

CONSOLIDATED RESULTS

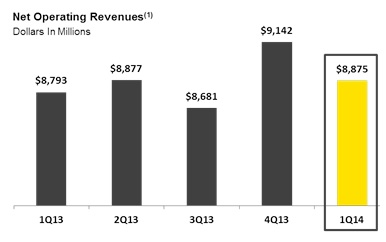

Net operating revenues of $8.9 billion for the quarter were up 1 percent when compared to the first quarter of 2013 and down 3 percent when compared to the fourth quarter of 2013. Equipment revenues were the primary driver for the sequential decline and the year-over-year increase.

Operating income was $420 million compared to operating income of $15 million for the first quarter of 2013 and an operating loss of $576 million for the fourth quarter of 2013. The year-over-year and sequential changes in operating income were primarily driven by items identified below in Adjusted EBITDA*. The year-over-year increase was also driven by lower depreciation, as the year-ago period included accelerated depreciation related to the Sprint and Nextel platforms.

Adjusted EBITDA* was $1.84 billion for the quarter, compared to $1.51 billion for the first quarter of 2013 and $1.15 billion in the fourth quarter of 2013. This represents a 22 percent year-over-year increase, primarily due to wireless expense reductions, including net subsidy with the introduction of installment billing for devices and a higher mix of tablet sales, customer care, and cost of service, partially offset by declines in the Wireline segment. Sequentially, Adjusted EBITDA* increased 60 percent primarily as a result of lower net subsidy and sales expenses related in part to seasonally lower sales volume.

Capital expenditures(2) were $1.1 billion in the quarter, compared to $1.8 billion in the first quarter of 2013 and $1.9 billion in the fourth quarter of 2013. Wireless capital expenditures were $930 million in the quarter, compared to $1.7 billion in both the first and fourth quarters of 2013. The sequential and year-over-year decline was primarily related to the legacy network upgrade approaching completion.

Net cash used in operating activities was $522 million for the quarter, compared to $938 million in the first quarter of 2013 and net cash used in operating activities was $761 million for the fourth quarter of 2013. The increase in cash provided by operating activities in the sequential period is primarily due to changes in working capital, a reduction in cash paid for interest related to the timing of interest payments, and call premiums paid on Clearwire debt redemptions in the fourth quarter 2013.

Free Cash Flow* was negative $1.1 billion for the quarter, compared to negative $495 million for the first quarter of 2013 and negative $2.8 billion for the fourth quarter of 2013.

The company’s total cash, cash equivalents, and short-term investments at the end of the quarter were $6.2 billion and its total liquidity position was $8.6 billion.

THE SPRINT QUARTERLY INVESTOR UPDATE | 5 |

WIRELESS RESULTS

• | The company served 54.9 million customers at the end of the quarter. Total customers include 30.5 million postpaid subscribers, 15.8 million prepaid subscribers and 8.6 million wholesale and affiliate subscribers. |

• | The Sprint platform lost 231,000 net postpaid customers during the quarter. Sprint platform postpaid net losses included 516,000 tablets offset by phone and other device net subscriber losses of 747,000. This compares to net additions of 12,000 in the first quarter of 2013, which included 264,000 subscribers recaptured from the Nextel platform, and subscriber additions of 58,000 in the fourth quarter of 2013, which included 466,000 tablets offset by 408,000 phone and other device net losses. |

• | The Sprint platform lost 364,000 net prepaid customers during the quarter primarily related to Assurance Wireless® customers who did not complete their annual certification. |

• | Wholesale and affiliate net subscriber additions on the Sprint platform were 212,000 in the quarter. Wholesale subscriber additions were primarily driven by an increase in connected device subscribers, largely related to connected vehicles. |

• | Sprint platform postpaid churn was 2.11 percent, compared to 1.84 percent for the year-ago period and 2.07 percent for the fourth quarter of 2013. Sprint platform quarterly postpaid churn increased year-over-year primarily due to network disruption issues. |

• | Approximately 7 percent of Sprint platform postpaid customers upgraded their devices during the quarter, compared to 7 percent for the year-ago period and 9 percent for the fourth quarter of 2013. Changes in upgrade eligibility with the introduction of our Framily and Easy Pay programs were offset by the elimination of Nextel platform subscribers migrating to the Sprint platform, keeping the upgrade rate flat year-over-year. The sequential decline in the upgrade rate was mostly driven by normal seasonality. |

• | Sprint platform prepaid churn for the quarter was 4.33 percent, compared to 3.05 percent for the year-ago period and 3.01 percent for the fourth quarter of 2013. Assurance churn related to annual certification was the primary driver of the sequential and year-over-year increase. |

• | Wireless retail service revenue of $7.1 billion for the quarter was down slightly both year-over-year and sequentially. Postpaid revenue was down year-over-year primarily due to the loss of Nextel platform subscribers, partially offset by additional revenue from the Clearwire acquisition, while prepaid revenue was up due to Clearwire-related revenue, in addition to growth in prepaid ARPU. |

THE SPRINT QUARTERLY INVESTOR UPDATE | 6 |

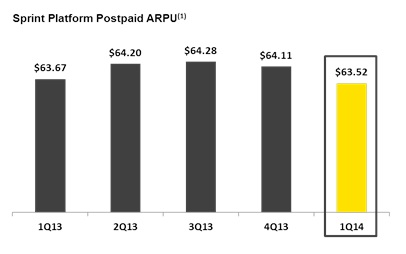

• | Sprint platform postpaid ARPU of $63.52 for the quarter declined by $.15 year-over-year and $.59 sequentially. The sequential decline was related to a higher mix of tablets, which generally have a lower ARPU than phones, and customer migration to Framily plans, partially offset by lower customer discounts and higher handset insurance revenue. While at different magnitudes, these factors all impacted the year-over-year changes in Sprint platform postpaid ARPU as well. |

• | Sprint platform prepaid ARPU of $26.45 increased from $25.95 in the first quarter of 2013 but declined from $26.78 in the fourth quarter of 2013. The year-over-year improvement was primarily driven by changes in the mix of our subscriber base among our prepaid brands. The sequential decline was primarily related to promotional activity within our Boost brand. |

• | Quarterly wholesale, affiliate and other revenues of $159 million increased by $26 million compared to the year-ago period and approximately $17 million sequentially. The year-over-year increase was a result of revenues from the Clearwire, U.S. Cellular, and Handmark acquisitions. The sequential growth was primarily due to higher wholesale revenue. |

• | Wireless equipment net subsidy in the quarter was $1 billion (equipment revenue of $1 billion, less cost of products of $2 billion). Equipment revenue was up $186 million year-over-year primarily due to the introduction of installment billing for devices while cost of products was down $255 million mostly due to a higher mix of tablet sales, resulting in a net subsidy decline of $441 million year-over-year. The sequential decline of $531 million in net subsidy expense was also driven by seasonally lower sales volumes. |

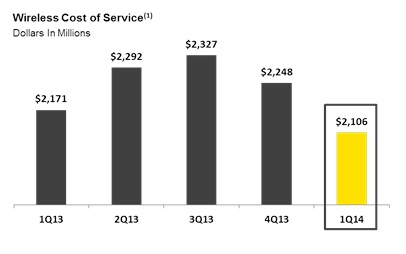

• | Wireless cost of service of $2.1 billion decreased $65 million year-over-year, primarily due to the elimination of network expenses related to the Nextel platform, lower 3G roaming expenses, and lower service and repair expenses, partially offset by the net impact of the Clearwire acquisition. Wireless cost of service improved $142 million sequentially, primarily as a result of lower Sprint network modernization spend and 3G roaming expenses. |

THE SPRINT QUARTERLY INVESTOR UPDATE | 7 |

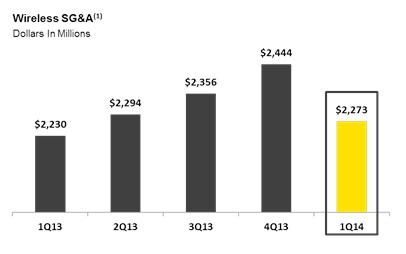

• | Wireless SG&A expenses of $2.3 billion increased $43 million year-over-year but were down $171 million sequentially. The year-over-year increase was primarily driven by higher bad debt and selling expenses, partially offset by lower care expenses. The sequential decline was driven by lower selling and care expenses, partially offset by higher marketing expenses to support the launch of Framily plans. |

• | Wireless depreciation and amortization expense of $1.2 billion decreased $169 million year-over-year and $246 million sequentially. The year-over-year decrease was related to a decline in depreciation as a result of the shutdown of the Sprint and Nextel platforms, partially offset by higher amortization of customer relationships resulting from the SoftBank transaction. The sequential decline was mostly due to the completion of accelerated depreciation on legacy CDMA assets in the fourth quarter of 2013. |

THE SPRINT QUARTERLY INVESTOR UPDATE | 8 |

WIRELINE RESULTS

• | Wireline revenue of $770 million for the quarter declined approximately 14 percent year-over-year and 10 percent sequentially. The sequential and year-over-year declines were primarily a result of the migration of wholesale cable VoIP customers off of Sprint’s IP platform and an intercompany rate reduction based on current market prices for voice and IP services sold to the wireless segment. |

• | Wireline net operating expenses were $832 million in the quarter. Net operating expenses declined 4 percent year-over-year and approximately 1 percent sequentially. The year-over-year decline was primarily due to lower depreciation. |

FORECAST

• | The company now expects calendar year 2014 Adjusted EBITDA* to be between $6.7 billion and $6.9 billion. |

The company expects calendar year 2014 capital expenditures of approximately $8 billion.

THE SPRINT QUARTERLY INVESTOR UPDATE | 9 |

Wireless Operating Statistics (Unaudited)

Quarter To Date | ||||||

3/31/14 | 12/31/13 | 3/31/13 | ||||

Net (Losses) Additions (in thousands) | ||||||

Sprint platform: | ||||||

Postpaid (3) | (231 | ) | 58 | 12 | ||

Prepaid (4) | (364 | ) | 322 | 568 | ||

Wholesale and affiliate | 212 | 302 | (224 | ) | ||

Total Sprint platform | (383 | ) | 682 | 356 | ||

Nextel platform: | ||||||

Postpaid (3) | — | — | (572 | ) | ||

Prepaid (4) | — | — | (199 | ) | ||

Total Nextel platform | — | — | (771 | ) | ||

Transactions: | ||||||

Postpaid (3) | (102 | ) | (127 | ) | — | |

Prepaid (4) | (51 | ) | (103 | ) | — | |

Wholesale | 69 | 25 | — | |||

Total transactions | (84 | ) | (205 | ) | — | |

Total retail postpaid net losses | (333 | ) | (69 | ) | (560 | ) |

Total retail prepaid net (losses) additions | (415 | ) | 219 | 369 | ||

Total wholesale and affiliate net additions (losses) | 281 | 327 | (224 | ) | ||

Total Wireless Net (Losses) Additions | (467 | ) | 477 | (415 | ) | |

End of Period Subscribers (in thousands) | ||||||

Sprint platform: | ||||||

Postpaid (3) | 29,918 | 30,149 | 30,257 | |||

Prepaid (4) | 15,257 | 15,621 | 15,701 | |||

Wholesale and affiliate | 8,376 | 8,164 | 7,938 | |||

Total Sprint platform | 53,551 | 53,934 | 53,896 | |||

Nextel platform: | ||||||

Postpaid (3) | — | — | 1,060 | |||

Prepaid (4) | — | — | 255 | |||

Total Nextel platform | — | — | 1,315 | |||

Transactions: (a) | ||||||

Postpaid (3) | 586 | 688 | — | |||

Prepaid (4) | 550 | 601 | — | |||

Wholesale | 200 | 131 | — | |||

Total transactions | 1,336 | 1,420 | — | |||

Total retail postpaid end of period subscribers | 30,504 | 30,837 | 31,317 | |||

Total retail prepaid end of period subscribers | 15,807 | 16,222 | 15,956 | |||

Total wholesale and affiliate end of period subscribers | 8,576 | 8,295 | 7,938 | |||

Total End of Period Subscribers | 54,887 | 55,354 | 55,211 | |||

Supplemental Data - Connected Devices | ||||||

End of Period Subscribers (in thousands) | ||||||

Retail postpaid | 968 | 922 | 824 | |||

Wholesale and affiliate | 3,882 | 3,578 | 2,803 | |||

Total | 4,850 | 4,500 | 3,627 | |||

Churn | ||||||

Sprint platform: | ||||||

Postpaid | 2.11 | % | 2.07 | % | 1.84 | % |

Prepaid | 4.33 | % | 3.01 | % | 3.05 | % |

Nextel platform: | ||||||

Postpaid | — | — | 7.57 | % | ||

Prepaid | — | — | 12.46 | % | ||

Transactions: (a) | ||||||

Postpaid | 5.48 | % | 5.48 | % | — | |

Prepaid | 5.11 | % | 8.18 | % | — | |

Total retail postpaid churn | 2.18 | % | 2.15 | % | 2.09 | % |

Total retail prepaid churn | 4.35 | % | 3.22 | % | 3.26 | % |

Nextel Platform Subscriber Recaptures | ||||||

Subscribers (in thousands) (5): | ||||||

Postpaid | — | — | 264 | |||

Prepaid | — | — | 67 | |||

Rate (6): | ||||||

Postpaid | — | — | 46 | % | ||

Prepaid | — | — | 34 | % | ||

(a) We acquired approximately 352,000 postpaid subscribers and 59,000 prepaid subscribers through the acquisition of assets from U.S. Cellular when the transaction closed on May 17, 2013. We acquired approximately 788,000 postpaid subscribers, 721,000 prepaid subscribers, 93,000 wholesale subscribers and transferred 29,000 Sprint wholesale subscribers that were originally recognized through our Clearwire MVNO arrangement to Transactions postpaid subscribers as a result of the Clearwire acquisition when the transaction closed on July 9, 2013.

THE SPRINT QUARTERLY INVESTOR UPDATE | 10 |

Wireless Operating Statistics (Unaudited) (continued)

Successor | Predecessor | |||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | ||||||||||

3/31/14 | 12/31/13 | 3/31/13 | ||||||||||

ARPU (b) | ||||||||||||

Sprint platform: | ||||||||||||

Postpaid | $ | 63.52 | $ | 64.11 | $ | 63.67 | ||||||

Prepaid | $ | 26.45 | $ | 26.78 | $ | 25.95 | ||||||

Nextel platform: | ||||||||||||

Postpaid | $ | — | $ | — | $ | 35.43 | ||||||

Prepaid | $ | — | $ | — | $ | 31.75 | ||||||

Transactions: (a) | ||||||||||||

Postpaid | $ | 37.26 | $ | 36.30 | $ | — | ||||||

Prepaid | $ | 43.80 | $ | 40.80 | $ | — | ||||||

Total retail postpaid ARPU | $ | 62.98 | $ | 63.44 | $ | 62.47 | ||||||

Total retail prepaid ARPU | $ | 27.07 | $ | 27.34 | $ | 26.08 | ||||||

(a) We acquired approximately 352,000 postpaid subscribers and 59,000 prepaid subscribers through the acquisition of assets from U.S. Cellular when the transaction closed on May 17, 2013. We acquired approximately 788,000 postpaid subscribers, 721,000 prepaid subscribers, 93,000 wholesale subscribers and transferred 29,000 Sprint wholesale subscribers that were originally recognized through our Clearwire MVNO arrangement to Transactions postpaid subscribers as a result of the Clearwire acquisition when the transaction closed on July 9, 2013.

(b)ARPU is calculated by dividing service revenue by the sum of the average number of subscribers in the applicable service category. Changes in average monthly service revenue reflect subscribers for either the postpaid or prepaid service category who change rate plans, the level of voice and data usage, the amount of service credits which are offered to subscribers, plus the net effect of average monthly revenue generated by new subscribers and deactivating subscribers.

THE SPRINT QUARTERLY INVESTOR UPDATE | 11 |

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(Millions, except per Share Data)

Successor | Predecessor | Combined (1) | |||||||||||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | |||||||||||||||||

3/31/14 | 12/31/13 | 3/31/13 | 3/31/13 | 3/31/13 | |||||||||||||||||

Net Operating Revenues | $ | 8,875 | $ | 9,142 | $ | — | $ | 8,793 | $ | 8,793 | |||||||||||

Net Operating Expenses | |||||||||||||||||||||

Cost of services | 2,622 | 2,704 | — | 2,640 | 2,640 | ||||||||||||||||

Cost of products | 2,038 | 2,731 | — | 2,293 | 2,293 | ||||||||||||||||

Selling, general and administrative | 2,371 | 2,546 | 14 | 2,336 | 2,350 | ||||||||||||||||

Depreciation and amortization | 1,297 | 1,531 | — | 1,492 | 1,492 | ||||||||||||||||

Other, net | 127 | 206 | — | 3 | 3 | ||||||||||||||||

Total net operating expenses | 8,455 | 9,718 | 14 | 8,764 | 8,778 | ||||||||||||||||

Operating Income (Loss) | 420 | (576 | ) | (14 | ) | 29 | 15 | ||||||||||||||

Interest expense | (516 | ) | (502 | ) | — | (432 | ) | (432 | ) | ||||||||||||

Equity in earnings (losses) of unconsolidated investments and other, net | 1 | 55 | 6 | (202 | ) | (196 | ) | ||||||||||||||

Loss before Income Taxes | (95 | ) | (1,023 | ) | (8 | ) | (605 | ) | (613 | ) | |||||||||||

Income tax expense | (56 | ) | (15 | ) | (1 | ) | (38 | ) | (39 | ) | |||||||||||

Net Loss | $ | (151 | ) | $ | (1,038 | ) | $ | (9 | ) | $ | (643 | ) | $ | (652 | ) | ||||||

Basic Net Loss Per Common Share | $ | (0.04 | ) | $ | (0.26 | ) | NM | $ | (0.21 | ) | NM | ||||||||||

Diluted Net Loss Per Common Share | $ | (0.04 | ) | $ | (0.26 | ) | NM | $ | (0.21 | ) | NM | ||||||||||

Basic Weighted Average Common Shares outstanding | 3,949 | 3,944 | NM | 3,013 | NM | ||||||||||||||||

Diluted Weighted Average Common Shares outstanding | 3,949 | 3,944 | NM | 3,013 | NM | ||||||||||||||||

Effective Tax Rate | -58.9 | % | -1.5 | % | -12.5 | % | -6.3 | % | -6.4 | % | |||||||||||

NON-GAAP RECONCILIATION - NET LOSS TO ADJUSTED EBITDA* (Unaudited)

(Millions)

Successor | Predecessor | Combined (1) | |||||||||||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | |||||||||||||||||

3/31/14 | 12/31/13 | 3/31/13 | 3/31/13 | 3/31/13 | |||||||||||||||||

Net Loss | $ | (151 | ) | $ | (1,038 | ) | $ | (9 | ) | $ | (643 | ) | $ | (652 | ) | ||||||

Income tax expense | 56 | 15 | 1 | 38 | 39 | ||||||||||||||||

Loss before Income Taxes | (95 | ) | (1,023 | ) | (8 | ) | (605 | ) | (613 | ) | |||||||||||

Equity in earnings (losses) of unconsolidated investments and other, net | (1 | ) | (55 | ) | (6 | ) | 202 | 196 | |||||||||||||

Interest expense | 516 | 502 | — | 432 | 432 | ||||||||||||||||

Operating Income (Loss) | 420 | (576 | ) | (14 | ) | 29 | 15 | ||||||||||||||

Depreciation and amortization | 1,297 | 1,531 | — | 1,492 | 1,492 | ||||||||||||||||

EBITDA* | 1,717 | 955 | (14 | ) | 1,521 | 1,507 | |||||||||||||||

Severance and exit costs (7) | 52 | 206 | — | 25 | 25 | ||||||||||||||||

Asset impairments (8) | 75 | — | — | — | — | ||||||||||||||||

Litigation (9) | — | — | — | (22 | ) | (22 | ) | ||||||||||||||

Hurricane Sandy (10) | — | (7 | ) | — | — | — | |||||||||||||||

Adjusted EBITDA* | $ | 1,844 | $ | 1,154 | $ | (14 | ) | $ | 1,524 | $ | 1,510 | ||||||||||

Capital expenditures (2) | 1,057 | 1,901 | — | 1,812 | 1,812 | ||||||||||||||||

Adjusted EBITDA* less Capex | $ | 787 | $ | (747 | ) | $ | (14 | ) | $ | (288 | ) | $ | (302 | ) | |||||||

Adjusted EBITDA Margin* | 23.4 | % | 14.5 | % | NM | 19.1 | % | 18.9 | % | ||||||||||||

Selected item: | |||||||||||||||||||||

Increase in deferred tax asset valuation allowance | $ | 82 | $ | 381 | $ | — | $ | 265 | $ | 265 | |||||||||||

THE SPRINT QUARTERLY INVESTOR UPDATE | 12 |

WIRELESS STATEMENTS OF OPERATIONS (Unaudited)

(Millions)

Successor | Predecessor | |||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | ||||||||||

3/31/14 | 12/31/13 | 3/31/13 | ||||||||||

Net Operating Revenues | ||||||||||||

Service revenue | ||||||||||||

Sprint platform: | ||||||||||||

Postpaid (3) | $ | 5,719 | $ | 5,782 | $ | 5,773 | ||||||

Prepaid (4) | 1,232 | 1,237 | 1,194 | |||||||||

Wholesale, affiliate and other | 145 | 132 | 133 | |||||||||

Total Sprint platform | 7,096 | 7,151 | 7,100 | |||||||||

Nextel platform: | ||||||||||||

Postpaid (3) | — | — | 143 | |||||||||

Prepaid (4) | — | — | 33 | |||||||||

Total Nextel platform | — | — | 176 | |||||||||

Transactions: | ||||||||||||

Postpaid (3) | 70 | 81 | — | |||||||||

Prepaid (4) | 75 | 80 | — | |||||||||

Wholesale | 14 | 10 | — | |||||||||

Total transactions | 159 | 171 | — | |||||||||

Equipment revenue | 999 | 1,161 | 813 | |||||||||

Total net operating revenues | 8,254 | 8,483 | 8,089 | |||||||||

Net Operating Expenses | ||||||||||||

Cost of services | 2,106 | 2,248 | 2,171 | |||||||||

Cost of products | 2,038 | 2,731 | 2,293 | |||||||||

Selling, general and administrative | 2,273 | 2,444 | 2,230 | |||||||||

Depreciation and amortization | 1,224 | 1,470 | 1,393 | |||||||||

Other, net | 123 | 187 | — | |||||||||

Total net operating expenses | 7,764 | 9,080 | 8,087 | |||||||||

Operating Income (Loss) | $ | 490 | $ | (597 | ) | $ | 2 | |||||

Supplemental Revenue Data | ||||||||||||

Total retail service revenue | $ | 7,096 | $ | 7,180 | $ | 7,143 | ||||||

Total service revenue | $ | 7,255 | $ | 7,322 | $ | 7,276 | ||||||

WIRELESS NON-GAAP RECONCILIATION (Unaudited)

(Millions)

Successor | Predecessor | |||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | ||||||||||

3/31/14 | 12/31/13 | 3/31/13 | ||||||||||

Operating Income (Loss) | $ | 490 | $ | (597 | ) | $ | 2 | |||||

Severance and exit costs (7) | 51 | 187 | 22 | |||||||||

Asset impairments (8) | 72 | — | — | |||||||||

Litigation (9) | — | — | (22 | ) | ||||||||

Hurricane Sandy (10) | — | (7 | ) | — | ||||||||

Depreciation and amortization | 1,224 | 1,470 | 1,393 | |||||||||

Adjusted EBITDA* | 1,837 | 1,053 | 1,395 | |||||||||

Capital expenditures (2) | 930 | 1,716 | 1,706 | |||||||||

Adjusted EBITDA* less Capex | $ | 907 | $ | (663 | ) | $ | (311 | ) | ||||

Adjusted EBITDA Margin* | 25.3 | % | 14.4 | % | 19.2 | % | ||||||

THE SPRINT QUARTERLY INVESTOR UPDATE | 13 |

WIRELINE STATEMENTS OF OPERATIONS (Unaudited)

(Millions)

Successor | Predecessor | |||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | ||||||||||

3/31/14 | 12/31/13 | 3/31/13 | ||||||||||

Net Operating Revenues | ||||||||||||

Voice | $ | 352 | $ | 386 | $ | 352 | ||||||

Data | 62 | 81 | 94 | |||||||||

Internet | 345 | 374 | 434 | |||||||||

Other | 11 | 18 | 13 | |||||||||

Total net operating revenues | 770 | 859 | 893 | |||||||||

Net Operating Expenses | ||||||||||||

Cost of services and products | 668 | 659 | 661 | |||||||||

Selling, general and administrative | 90 | 95 | 104 | |||||||||

Depreciation and amortization | 69 | 62 | 98 | |||||||||

Other, net | 5 | 20 | 3 | |||||||||

Total net operating expenses | 832 | 836 | 866 | |||||||||

Operating (Loss) Income | $ | (62 | ) | $ | 23 | $ | 27 | |||||

WIRELINE NON-GAAP RECONCILIATION (Unaudited)

(Millions)

Successor | Predecessor | |||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | ||||||||||

3/31/14 | 12/31/13 | 3/31/13 | ||||||||||

Operating (Loss) Income | $ | (62 | ) | $ | 23 | $ | 27 | |||||

Severance and exit costs (7) | 2 | 20 | 3 | |||||||||

Asset impairments (8) | 3 | — | — | |||||||||

Depreciation and amortization | 69 | 62 | 98 | |||||||||

Adjusted EBITDA* | 12 | 105 | 128 | |||||||||

Capital expenditures (2) | 72 | 82 | 61 | |||||||||

Adjusted EBITDA* less Capex | $ | (60 | ) | $ | 23 | $ | 67 | |||||

Adjusted EBITDA Margin* | 1.6 | % | 12.2 | % | 14.3 | % | ||||||

THE SPRINT QUARTERLY INVESTOR UPDATE | 14 |

CONDENSED CONSOLIDATED CASH FLOW INFORMATION (Unaudited)

(Millions)

Successor | Predecessor | Combined (1) | |||||||||||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | |||||||||||||||||

3/31/14 | 12/31/13 | 3/31/13 | 3/31/13 | 3/31/13 | |||||||||||||||||

Operating Activities | |||||||||||||||||||||

Net loss | $ | (151 | ) | $ | (1,038 | ) | $ | (9 | ) | $ | (643 | ) | $ | (652 | ) | ||||||

Depreciation and amortization | 1,297 | 1,531 | — | 1,492 | 1,492 | ||||||||||||||||

Provision for losses on accounts receivable | 153 | 142 | — | 83 | 83 | ||||||||||||||||

Share-based and long-term incentive compensation expense | 35 | 40 | — | 17 | 17 | ||||||||||||||||

Deferred income taxes | 46 | 10 | (1 | ) | 24 | 23 | |||||||||||||||

Equity in losses of unconsolidated investments, net | — | — | — | 202 | 202 | ||||||||||||||||

Contribution to pension plan | (10 | ) | (7 | ) | — | — | — | ||||||||||||||

Call premiums on debt redemptions | — | (180 | ) | — | — | — | |||||||||||||||

Amortization and accretion of long-term debt premiums and discounts | (74 | ) | (160 | ) | — | 14 | 14 | ||||||||||||||

Other working capital changes, net | (549 | ) | (954 | ) | (3 | ) | (276 | ) | (279 | ) | |||||||||||

Other, net | (225 | ) | (145 | ) | 11 | 27 | 38 | ||||||||||||||

Net cash provided by (used in) operating activities | 522 | (761 | ) | (2 | ) | 940 | 938 | ||||||||||||||

Investing Activities | |||||||||||||||||||||

Capital expenditures (2) | (1,488 | ) | (1,969 | ) | — | (1,381 | ) | (1,381 | ) | ||||||||||||

Expenditures relating to FCC licenses | (152 | ) | (115 | ) | — | (55 | ) | (55 | ) | ||||||||||||

Change in short-term investments, net | (115 | ) | 331 | — | 355 | 355 | |||||||||||||||

Decrease in restricted cash | — | 3,050 | — | — | — | ||||||||||||||||

Investment in Clearwire (including debt securities) | — | — | — | (80 | ) | (80 | ) | ||||||||||||||

Other, net | (1 | ) | 1 | — | 3 | 3 | |||||||||||||||

Net cash (used in) provided by investing activities | (1,756 | ) | 1,298 | — | (1,158 | ) | (1,158 | ) | |||||||||||||

Financing Activities | |||||||||||||||||||||

Proceeds from debt and financings | — | 2,674 | — | 204 | 204 | ||||||||||||||||

Debt financing costs | (1 | ) | (40 | ) | — | (10 | ) | (10 | ) | ||||||||||||

Repayments of debt and capital lease obligations | (159 | ) | (2,881 | ) | — | (59 | ) | (59 | ) | ||||||||||||

Proceeds from issuance of common stock and warrants, net | — | 15 | — | 7 | 7 | ||||||||||||||||

Other, net | — | 1 | — | — | — | ||||||||||||||||

Net cash (used in) provided by financing activities | (160 | ) | (231 | ) | — | 142 | 142 | ||||||||||||||

Net (Decrease) Increase in Cash and Cash Equivalents | (1,394 | ) | 306 | (2 | ) | (76 | ) | (78 | ) | ||||||||||||

Cash and Cash Equivalents, beginning of period | 6,364 | 6,058 | 5 | 6,351 | 6,356 | ||||||||||||||||

Cash and Cash Equivalents, end of period | $ | 4,970 | $ | 6,364 | $ | 3 | $ | 6,275 | $ | 6,278 | |||||||||||

RECONCILIATION TO CONSOLIDATED FREE CASH FLOW* (NON-GAAP) (Unaudited)

(Millions)

Successor | Predecessor | Combined (1) | |||||||||||||||||||

Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | Quarter to Date | |||||||||||||||||

3/31/14 | 12/31/13 | 3/31/13 | 3/31/13 | 3/31/13 | |||||||||||||||||

Net Cash Provided by (Used in) Operating Activities | $ | 522 | $ | (761 | ) | $ | (2 | ) | $ | 940 | $ | 938 | |||||||||

Capital expenditures (2) | (1,488 | ) | (1,969 | ) | — | (1,381 | ) | (1,381 | ) | ||||||||||||

Expenditures relating to FCC licenses, net | (152 | ) | (115 | ) | — | (55 | ) | (55 | ) | ||||||||||||

Other investing activities, net | (1 | ) | 1 | — | 3 | 3 | |||||||||||||||

Free Cash Flow* | (1,119 | ) | (2,844 | ) | (2 | ) | (493 | ) | (495 | ) | |||||||||||

Debt financing costs | (1 | ) | (40 | ) | — | (10 | ) | (10 | ) | ||||||||||||

(Decrease) increase in debt and other, net | (159 | ) | (207 | ) | — | 145 | 145 | ||||||||||||||

Proceeds from issuance of common stock and warrants, net | 15 | — | 7 | 7 | |||||||||||||||||

Decrease in restricted cash | 3,050 | — | — | — | |||||||||||||||||

Investment in Clearwire (including debt securities) | — | — | (80 | ) | (80 | ) | |||||||||||||||

Other financing activities, net | 1 | — | — | — | |||||||||||||||||

Net Decrease in Cash, Cash | |||||||||||||||||||||

Equivalents and Short-Term Investments | $ | (1,279 | ) | $ | (25 | ) | $ | (2 | ) | $ | (431 | ) | $ | (433 | ) | ||||||

THE SPRINT QUARTERLY INVESTOR UPDATE | 15 |

CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited)

(Millions)

Successor | ||||||

3/31/14 | 12/31/13 | |||||

Assets | ||||||

Current assets | ||||||

Cash and cash equivalents | $ | 4,970 | $ | 6,364 | ||

Short-term investments | 1,220 | 1,105 | ||||

Accounts and notes receivable, net | 3,607 | 3,570 | ||||

Device and accessory inventory | 982 | 1,205 | ||||

Deferred tax assets | 128 | 186 | ||||

Prepaid expenses and other current assets | 672 | 628 | ||||

Total current assets | 11,579 | 13,058 | ||||

Investments and other assets | 892 | 601 | ||||

Property, plant and equipment, net | 16,299 | 16,164 | ||||

Goodwill | 6,383 | 6,434 | ||||

FCC licenses and other | 41,978 | 41,824 | ||||

Definite-lived intangible assets, net | 7,558 | 8,014 | ||||

Total | $ | 84,689 | $ | 86,095 | ||

Liabilities and Shareholders' Equity | ||||||

Current liabilities | ||||||

Accounts payable | $ | 3,163 | $ | 3,312 | ||

Accrued expenses and other current liabilities | 5,544 | 6,363 | ||||

Current portion of long-term debt, financing and capital lease obligations | 991 | 994 | ||||

Total current liabilities | 9,698 | 10,669 | ||||

Long-term debt, financing and capital lease obligations | 31,787 | 32,017 | ||||

Deferred tax liabilities | 14,207 | 14,227 | ||||

Other liabilities | 3,685 | 3,598 | ||||

Total liabilities | 59,377 | 60,511 | ||||

Shareholders' equity | ||||||

Common shares | 39 | 39 | ||||

Paid-in capital | 27,364 | 27,330 | ||||

Accumulated deficit | (2,048 | ) | (1,887 | ) | ||

Accumulated other comprehensive loss | (43 | ) | 102 | |||

Total shareholders' equity | 25,312 | 25,584 | ||||

Total | $ | 84,689 | $ | 86,095 | ||

NET DEBT* (NON-GAAP) (Unaudited)

(Millions)

Successor | ||||||

3/31/14 | 12/31/13 | |||||

Total Debt | $ | 32,778 | $ | 33,011 | ||

Less: Cash and cash equivalents | (4,970 | ) | (6,364 | ) | ||

Less: Short-term investments | (1,220 | ) | (1,105 | ) | ||

Net Debt* | $ | 26,588 | $ | 25,542 | ||

THE SPRINT QUARTERLY INVESTOR UPDATE | 16 |

SCHEDULE OF DEBT (Unaudited)

(Millions)

3/31/14 | |||||

ISSUER | COUPON | MATURITY | PRINCIPAL | ||

Sprint Corporation | |||||

7.25% Notes due 2021 | 7.250% | 09/15/2021 | $ | 2,250 | |

7.875% Notes due 2023 | 7.875% | 09/15/2023 | 4,250 | ||

7.125% Notes due 2024 | 7.125% | 06/15/2024 | 2,500 | ||

Sprint Corporation | 9,000 | ||||

Sprint Communications, Inc. | |||||

Export Development Canada Facility (Tranche 2) | 3.579% | 12/15/2015 | 500 | ||

6% Senior Notes due 2016 | 6.000% | 12/01/2016 | 2,000 | ||

9.125% Senior Notes due 2017 | 9.125% | 03/01/2017 | 1,000 | ||

8.375% Senior Notes due 2017 | 8.375% | 08/15/2017 | 1,300 | ||

9% Guaranteed Notes due 2018 | 9.000% | 11/15/2018 | 3,000 | ||

7% Guaranteed Notes due 2020 | 7.000% | 03/01/2020 | 1,000 | ||

7% Senior Notes due 2020 | 7.000% | 08/15/2020 | 1,500 | ||

11.5% Senior Notes due 2021 | 11.500% | 11/15/2021 | 1,000 | ||

9.25% Debentures due 2022 | 9.250% | 04/15/2022 | 200 | ||

6% Senior Notes due 2022 | 6.000% | 11/15/2022 | 2,280 | ||

Sprint Communications, Inc. | 13,780 | ||||

Sprint Capital Corporation | |||||

6.9% Senior Notes due 2019 | 6.900% | 05/01/2019 | 1,729 | ||

6.875% Senior Notes due 2028 | 6.875% | 11/15/2028 | 2,475 | ||

8.75% Senior Notes due 2032 | 8.750% | 03/15/2032 | 2,000 | ||

Sprint Capital Corporation | 6,204 | ||||

Clearwire Communications LLC | |||||

14.75% First-Priority Senior Secured Notes due 2016 | 14.750% | 12/01/2016 | 300 | ||

8.25% Exchangeable Notes due 2040 | 8.250% | 12/01/2040 | 629 | ||

Clearwire Communications LLC | 929 | ||||

iPCS Inc. | |||||

Second Lien Senior Secured Floating Rate Notes due 2014 | 3.488% | 05/01/2014 | 181 | ||

iPCS Inc. | 181 | ||||

EKN Secured Equipment Facility ($1 Billion) | 2.030% | 03/30/2017 | 762 | ||

Vendor financing notes - Clearwire Communications LLC | 2015 | 13 | |||

Tower financing obligation | 6.092% | 09/30/2021 | 327 | ||

Capital lease obligations and other | 2014 - 2023 | 174 | |||

TOTAL PRINCIPAL | 31,370 | ||||

Net premiums | 1,408 | ||||

TOTAL DEBT | $ | 32,778 | |||

Supplemental information:

The Company had $2.4 billion of borrowing capacity available under our unsecured revolving bank credit facility as of March 31, 2014. Our unsecured revolving bank credit facility expires in February 2018.

In May 2012, certain of our subsidiaries entered into a $1.0 billion secured equipment credit facility to finance equipment-related purchases for Network Vision. The facility is equally divided into two consecutive tranches of $500 million, with the drawdown availability contingent upon Sprint's acquisition of equipment-related purchases from Ericsson, up to the maximum of each tranche, ending on May 31, 2013 and May 31, 2014, for the first and second tranche, respectively. Interest and principal are payable semi-annually with a final maturity of March 2017 for both tranches.

*This table excludes (i) our unsecured revolving bank credit facility, which will expire in 2018 and has no outstanding balance, (ii) $914 million in letters of credit outstanding under the unsecured revolving bank credit facility, (iii) vendor financing notes assumed in the Clearwire Acquisition, and (iv) all capital leases and other financing obligations.

THE SPRINT QUARTERLY INVESTOR UPDATE | 17 |

SPRINT CORPORATION

NOTES TO THE FINANCIAL INFORMATION (Unaudited)

(1) Except for the quarter-to-date March 31, 2014 and December 31, 2013 periods, financial results include a Predecessor period from January 1, 2012, through the closing of the SoftBank transaction on July 10, 2013, and a Successor period from October 5, 2012 through December 31, 2013. In order to present financial results in a way that offers investors a more meaningful calendar period-to-period comparison, we have combined results of operations and cash flows for the Predecessor and Successor periods for the three-month period ended March 31, 2013. (See Financial Measures for further information)

(2) Capital expenditures is an accrual based amount that includes the changes in unpaid capital expenditures and excludes capitalized interest. Cash paid for capital expenditures includes total capitalized interest of $13 million for the successor quarter-to-date March 31, 2014 period and $15 million for the predecessor quarter-to-date March 31, 2013 period and can be found in the Condensed Consolidated Cash Flow Information and the Reconciliation to Free Cash Flow*.

(3) Postpaid subscribers on the Sprint platform are defined as retail postpaid devices with an active line of service on the CDMA network, including subscribers utilizing WiMax and LTE technology. Postpaid subscribers previously on the Nextel platform are defined as retail postpaid subscribers on the iDEN network, which was shut-down on June 30, 2013. Postpaid subscribers from transactions are defined as retail postpaid subscribers acquired from U.S. Cellular in May 2013 and Clearwire in July 2013 who had not deactivated or been recaptured on the Sprint platform. During the quarter-to-date March 31, 2014 period, the Sprint platform subscriber results included approximately 516,000 tablet net adds, which generally generate a significantly lower ARPU than other postpaid subscribers.

(4) Prepaid subscribers on the Sprint platform are defined as retail prepaid subscribers and session-based tablet users who utilize the CDMA network and WiMax and LTE technology via our multi-brand offerings. Prepaid subscribers previously on the Nextel platform are defined as retail prepaid subscribers who utilized the iDEN network, which was shut-down on June 30, 2013. Prepaid subscribers from transactions are defined as retail prepaid subscribers acquired from U.S. Cellular in May 2013 and Clearwire in July 2013 who had not deactivated or been recaptured on the Sprint platform.

(5) Nextel Subscriber Recaptures are defined as the number of subscribers that deactivated service from the postpaid or prepaid Nextel platform, as applicable, during each period but remained with the Company as subscribers on the postpaid or prepaid Sprint platform, respectively. Subscribers that deactivated service from the Nextel platform and activated service on the Sprint platform are included in the Sprint platform net additions for the applicable period.

(6) The Postpaid and Prepaid Nextel Recapture Rates are defined as the portion of total subscribers that left the postpaid or prepaid Nextel platform, as applicable, during the period and were retained on the postpaid or prepaid Sprint platform, respectively.

(7) Severance and lease exit costs are primarily associated with workforce reductions and exit costs associated with the Nextel platform and those related to exiting certain operations of Clearwire.

(8) For the quarter-to-date March 31, 2014 period, asset impairment activity is primarily due to network equipment assets that are no longer necessary for management's strategic plans.

(9) For the quarter-to-date March 31, 2013 period, litigation activity is primarily a result of favorable developments in connection with a tax (non-income) related contingency.

(10) Hurricane Sandy amounts for the quarter-to-date December 31, 2013 period represent insurance recoveries.

*FINANCIAL MEASURES

On July 9, 2013, Sprint Communications, Inc. (formerly Sprint Nextel Corporation) completed its acquisition of Clearwire. On July 10, 2013 we consummated the SoftBank Merger with Starburst II, which immediately changed its name to Sprint Corporation (now referred to as the Company or Sprint). As a result of these transactions, the assets and liabilities of Sprint Communications, Inc. and Clearwire were adjusted to fair value on the respective closing dates. The Company's financial statement presentations herein distinguish between a predecessor period relating to Sprint Communications, Inc. for periods prior to the SoftBank Merger (Predecessor) and a successor period (Successor). The Successor information represents Sprint Corporation, which includes the activity and accounts of Sprint Communications as of and for the three-month periods ended March 31, 2014 and December 31, 2013. The accounts and activity for the successor periods from October 5, 2012 (date of inception) to December 31, 2012 and from January 1, 2103 to July 10, 2013 consist of the activity of Starburst II prior to the close of the SoftBank Merger. The Predecessor information contained herein represents the historical basis of presentation for Sprint Communications, Inc. for all periods prior to the SoftBank Merger date on July 10, 2013. As a result of the valuation of assets acquired and liabilities assumed at fair value at the time of the SoftBank Merger and Clearwire Acquisition, the financial statements for the successor period are presented on a measurement basis different than the predecessor period, which was Sprint Communication’s historical cost, and are, therefore, not comparable.

THE SPRINT QUARTERLY INVESTOR UPDATE | 18 |

In order to present financial results in a way that offers investors a more meaningful calendar period-to-period comparison, we have combined the current and prior year results of operations for the predecessor with successor results of operations on an unaudited combined basis. The combined information for the three-month period ended March 31, 2013 does not purport to represent what our consolidated results of operations would have been if the acquisition had occurred as of the beginning of 2013.

Sprint provides financial measures determined in accordance with GAAP and adjusted GAAP (non-GAAP). The non-GAAP financial measures reflect industry conventions, or standard measures of liquidity, profitability or performance commonly used by the investment community for comparability purposes. These measurements should be considered in addition to, but not as a substitute for, financial information prepared in accordance with GAAP. Other than the use of non-GAAP combined results as described above, we have defined below each of the non-GAAP measures we use, but these measures may not be synonymous to similar measurement terms used by other companies.

Sprint provides reconciliations of these non-GAAP measures in its financial reporting. Because Sprint does not predict special items that might occur in the future, and our forecasts are developed at a level of detail different than that used to prepare GAAP-based financial measures, Sprint does not provide reconciliations to GAAP of its forward-looking financial measures.

The measures used in this release include the following:

EBITDA is operating income/(loss) before depreciation and amortization. Adjusted EBITDA is EBITDA excluding severance, exit costs, and other special items. Adjusted EBITDA Margin represents Adjusted EBITDA divided by non-equipment net operating revenues for Wireless and Adjusted EBITDA divided by net operating revenues for Wireline. We believe that Adjusted EBITDA and Adjusted EBITDA Margin provide useful information to investors because they are an indicator of the strength and performance of our ongoing business operations, including our ability to fund discretionary spending such as capital expenditures, spectrum acquisitions and other investments and our ability to incur and service debt. While depreciation and amortization are considered operating costs under GAAP, these expenses primarily represent non-cash current period costs associated with the use of long-lived tangible and definite-lived intangible assets. Adjusted EBITDA and Adjusted EBITDA Margin are calculations commonly used as a basis for investors, analysts and credit rating agencies to evaluate and compare the periodic and future operating performance and value of companies within the telecommunications industry.

Free Cash Flow is the cash provided by operating activities less the cash used in investing activities other than short-term investments, including changes in restricted cash, and amounts included as investments in Clearwire and Sprint Communications, Inc. during the period. We believe that Free Cash Flow provides useful information to investors, analysts and our management about the cash generated by our core operations after interest and dividends, if any, and our ability to fund scheduled debt maturities and other financing activities, including discretionary refinancing and retirement of debt and purchase or sale of investments.

Net Debt is consolidated debt, including current maturities, less cash and cash equivalents, short-term investments and if any, restricted cash. We believe that Net Debt provides useful information to investors, analysts and credit rating agencies about the capacity of the company to reduce the debt load and improve its capital structure.

THE SPRINT QUARTERLY INVESTOR UPDATE | 19 |

SAFE HARBOR

This release includes “forward-looking statements” within the meaning of the securities laws. The words “may,” “could,” “should,” “estimate,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “target,” “plan,” “providing guidance,” and similar expressions are intended to identify information that is not historical in nature. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future - including statements relating to our network, subscriber growth, and liquidity, and statements expressing general views about future operating results - are forward-looking statements. Forward-looking statements are estimates and projections reflecting management’s judgment based on currently available information and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. With respect to these forward-looking statements, management has made assumptions regarding, among other things, the ability to operationalize the anticipated benefits from the SoftBank, Clearwire and U.S. Cellular transactions, the development and deployment of new technologies; efficiencies and cost savings of new technologies and services; customer and network usage; customer growth and retention; service, speed, coverage and quality; availability of devices; the timing of various events and the economic environment. Sprint believes these forward-looking statements are reasonable; however, you should not place undue reliance on forward-looking statements, which are based on current expectations and speak only as of the date when made. Sprint undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our company's historical experience and our present expectations or projections. Factors that might cause such differences include, but are not limited to, those discussed in Sprint Corporation’s Annual Report on Form 10-K for the year ended December 31, 2013, and when filed our Transition Report on Form 10-K for the period ended March 31, 2014. You should understand that it is not possible to predict or identify all such factors. Consequently, you should not consider any such list to be a complete set of all potential risks or uncertainties.

i Sprint Spark actual deployment plans and speeds will be determined over time based on many factors, including build economics and the availability of equipment, devices and applications.

THE SPRINT QUARTERLY INVESTOR UPDATE | 20 |