Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - MERCURY PAYMENT SYSTEMS, INC. | d637391dex232.htm |

Table of Contents

As filed with the Securities and Exchange Commission on April 29, 2014

Registration No. 333-194879

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2 to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Mercury Payment Systems, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 7389 | 46-4255974 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Tech Center Plaza

10 Burnett Court, Suite 300

Durango, Colorado 81301

(970) 247-5557

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Matt Taylor

Chief Executive Officer

Mercury Payment Systems, Inc.

Tech Center Plaza

10 Burnett Court, Suite 300

Durango, Colorado 81301

(970) 247-5557

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| William H. Hinman, Jr. Daniel N. Webb Simpson Thacher & Bartlett LLP 2475 Hanover Street Palo Alto, California 94304 (650) 251-5000 |

Ross Agre Chief Legal Officer and Secretary Mercury Payment Systems, Inc. Tech Center Plaza 10 Burnett Court, Suite 300 Durango, Colorado 81301 (970) 247-5557 |

Julie H. Jones Thomas Holden Ropes & Gray LLP Prudential Tower 800 Boylston Street Boston, Massachusetts 02199 (617) 951-7000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated April 29, 2014.

Shares

Mercury Payment Systems, Inc.

Class A Common Stock

This is an initial public offering of shares of Class A common stock of Mercury Payment Systems, Inc. We are offering all of the shares in this offering. We intend to use the net proceeds from this offering to acquire interests in our business from our existing owners.

Prior to this offering, there has been no public market for our shares. We estimate the initial public offering price per share will be between $ and $ . We have applied to have our shares listed on the Nasdaq Global Select Market (the “Nasdaq”) under the symbol “MPS.”

After the completion of this offering, affiliates of Silver Lake Group, L.L.C. and affiliates of certain members of our board of directors will continue to beneficially own a majority of the voting power of all outstanding shares of our common stock. As a result, we will be a “controlled company” within the meaning of the corporate governance standards of the Nasdaq. See “Principal Stockholders.”

We are an “emerging growth company” as defined under the federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for future filings.

See “Risk Factors” beginning on page 23 to read about factors you should consider before buying shares of our Class A common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discount(1) |

$ | $ | ||||||

| Proceeds, before expenses, to Mercury Payment Systems, Inc. |

$ | $ | ||||||

| (1) | In addition, upon completion of this offering, we will pay a fee for certain financial consulting services to a broker-dealer that is not part of the underwriting syndicate. We have also agreed to reimburse the underwriters for certain expenses. See “Underwriting.” |

We have granted the underwriters an option for a period of 30 days to purchase up to additional shares of Class A common stock.

The underwriters expect to deliver the shares against payment in New York, New York on or about , 2014.

| J.P. Morgan | Barclays | Morgan Stanley |

, 2014

Table of Contents

See “Prospectus Summary—Key Operating Metrics” and “Industry Data and Operating Metrics” for definitions and additional information.

Table of Contents

Prospectus

| Page | ||||

| 1 | ||||

| 23 | ||||

| 54 | ||||

| 55 | ||||

| 56 | ||||

| 61 | ||||

| 62 | ||||

| 63 | ||||

| 65 | ||||

| 67 | ||||

| 71 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

72 | |||

| 95 | ||||

| 128 | ||||

| 137 | ||||

| 152 | ||||

| 160 | ||||

| 163 | ||||

| 172 | ||||

| Certain United States Federal Income and Estate Tax Consequences to Non-U.S. Holders |

174 | |||

| 178 | ||||

| 188 | ||||

| 188 | ||||

| 188 | ||||

| F-1 | ||||

Through and including , 2014 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

We and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

We and the underwriters have not done anything that would permit a public offering of the shares of our Class A common stock or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of Class A common stock and the distribution of this prospectus outside of the United States.

i

Table of Contents

This summary highlights information contained in greater detail elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our Class A common stock, you should carefully read this entire prospectus, including our financial statements and the related notes included in this prospectus and the information set forth under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Unless otherwise indicated in this prospectus, “Mercury,” “we,” “us” and “our” refer (1) prior to the reorganization transactions, as described under “Organizational Structure—Offering Transactions,” to Mercury Payment Systems, LLC and, where appropriate, its subsidiaries, and (2) after the reorganization transactions to Mercury Payment Systems, Inc. and, where appropriate, its subsidiaries.

Overview

Mercury was founded in 2001 with the vision that small- and medium-sized businesses (“SMBs”) would require seamless and adaptable payments services to accompany their increasing adoption of a new class of sophisticated point-of-sale (“POS”) technology solutions. We created our innovative Mercury Model that combines our payments technology with our robust partner distribution and support network to create a differentiated payments experience for our merchants. We believe this model has disrupted the merchant acquiring market, enabling our rise from the 45th largest merchant acquirer in the U.S. in 2004 to the 11th largest in 2013, measured by purchase transactions according to the Nilson Report. Based on this data, our purchase transactions grew at a 57% compound annual growth rate, ranking us as the fastest organically growing merchant acquirer in the U.S. during this period. In 2013, we had approximately 88,700 merchants, our systems processed over $34 billion in payments volume and we generated $237.3 million in net revenue, an increase in revenue of more than 16% year-over-year.

Mercury is a leading provider of payments technology and services in the U.S. and Canada and empowers merchants to accept a broad range of traditional and emerging electronic payments. We embed our payments technology into third-party software applications used by SMB merchants, enabling them to benefit from the combination of payments and business management functionality. We refer to this class of POS technology solutions as “Integrated Point-of-Sale” or “IPOS.” We utilize an efficient and scalable go-to-market strategy, which involves partnering with the many providers who develop and sell IPOS systems. This network of partners, which we call the Mercury Network, includes Developers, who create software for IPOS systems with functionality tailored for specific business requirements, and Dealers, who sell IPOS systems and provide technology, services and support to merchants.

A growing number of SMB merchants are adopting IPOS systems to take advantage of the declining cost of computers and the availability of new form factors such as tablets and high-quality, industry-specific software applications to better manage their businesses. In 2012, approximately 45% of point-of-sale devices were IPOS-capable, up from 39% in 2010 according to data on single-location SMBs (U.S. and Canada) from IHL, an industry research firm. Over time we expect IPOS adoption by SMBs to continue to grow and more closely reflect the adoption by the largest merchant category tracked by IHL (1,000+ store chains), where IPOS has already grown to represent over 90% of installed POS devices. We anticipate further growth in this category because IPOS solutions are becoming increasingly affordable and feature-rich, resulting in a more attractive value proposition for SMBs in comparison to stand-alone POS systems. Additionally, many SMB merchants will have an opportunity to upgrade their existing POS systems to IPOS as their legacy systems become obsolete or as they require more features and functionality.

1

Table of Contents

SMB merchants often have limited financial and operational resources due to their lower sales volume compared to larger merchants. As a result, SMB merchants typically lack the in-house technical capabilities and personnel to configure and support their IPOS systems and manage integrated payments. Thus, they often rely on a local Dealer to help them select an IPOS system and configure and support their retail technology environment. In the Mercury Model, we incentivize our Dealers to refer Mercury for payment processing services by offering recurring commissions and specialized IPOS customer support for them and their merchants. Since our Developers’ and Dealers’ primary focus is creating and selling IPOS systems, they are generally not well-positioned to handle the complexities of integrated payments functionality. Mercury serves as a single, value-added resource point for the entire ecosystem with respect to payments capabilities. We believe the Mercury Model benefits from powerful network effects, which drive significant benefits to all participants in our ecosystem, increase the value of our network and help sustain our growth.

We believe Mercury’s role has become increasingly important due to the continued adoption and innovation of IPOS technology over the last 10 years and lack of sufficient solutions from traditional merchant acquirers. These trends provide Mercury a large and growing addressable market. We have penetrated less than 10% of the over 1 million merchants in the installed base of our current Mercury Network partners, based on management estimates, and approximately 1% of the 7.2 million SMB merchants estimated to be in the U.S. by First Annapolis. We believe we are well-positioned to capitalize on this large market opportunity as merchants upgrade to IPOS systems.

We generate revenues primarily on a per transaction basis from fees paid by our merchants. For the year ended December 31, 2013, we reported net revenue of $237.3 million and GAAP net income of $42.7 million, an increase of 16.7% and a decrease of 8.4%, respectively, over the prior year. Also for the year ended December 31, 2013, we reported adjusted EBITDA of $92.9 million and adjusted net income of $57.1 million, increases of 22.9% and 14.9%, respectively, over the prior year. For a reconciliation of adjusted EBITDA and adjusted net income to GAAP net income, see “—Adjusted EBITDA and Adjusted Net Income.”

Industry Background

Overview of Electronic Payments

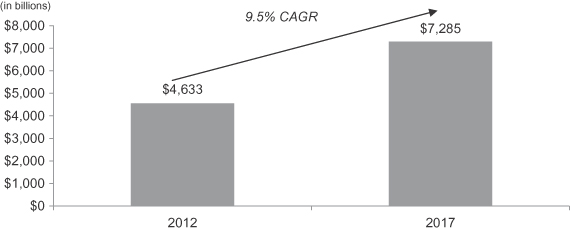

Electronic payments represent a large and growing market that is fueled by a powerful secular shift towards the use and acceptance of card-based payments, such as credit and debit cards, and away from paper-based payments like checks and cash. According to the Nilson Report, purchase volume on credit and debit cards in the U.S. was $4.6 trillion in 2012 and is projected to reach $7.3 trillion by 2017, a compound annual growth rate of 9.5%.

Overview of the Traditional Merchant Acquiring Industry

To facilitate the adoption and acceptance of card-based payments at the POS, banks began providing payments services to their local merchants in the 1950s. Providers of these services, both divisions of banks and independent companies, became known as merchant acquirers. Since that time, the merchant acquiring industry has grown and expanded significantly. The merchant acquiring industry now includes thousands of providers in the U.S., primarily comprised of banks, non-bank payment processors and third-party independent sales organizations (ISOs).

Traditional merchant acquirers sell their payment processing services to merchants of all sizes, but many focus on SMBs. SMBs are attractive customers because they tend to have higher growth rates and lower price sensitivity than larger merchants, given their smaller size and greater number of new business starts.

2

Table of Contents

Methods of Electronic Payments Acceptance

As electronic payments have gained widespread adoption, the technologies used to accept and process these payments (“POS technologies”) have evolved significantly. Historically, merchants chose stand-alone payments technologies to facilitate basic acceptance of electronic payments from their customers. Based on a number of trends in the industry, including advancements in electronic cash register and POS technologies, many merchants are choosing to integrate payment functionality with their other business management systems.

Stand-Alone POS Technologies

From the 1950s to the 1980s, merchants accepted card-based payments using a carbon paper-based imprinting method to capture customers’ card information. This method was replaced by the introduction of electronic card readers that captured the same information stored on a magnetic stripe on the payment cards. Stand-alone devices enable merchants to swipe a card or manually enter the account information on the card, but typically have limited functionality beyond accepting card payments.

Integrated POS Technologies

In the 1990s, advancements in electronic cash register and PC-based POS software technologies allowed for payments functionality to be embedded in these systems, creating an IPOS class of POS technologies. Larger merchants were early adopters of IPOS systems, and this technology is spreading into SMBs across many industry verticals. The technology is also evolving with mobile- and tablet-based software and hardware innovations.

Accelerating SMB Shift to IPOS Solutions

There is an accelerating shift among SMB merchants toward IPOS systems, displacing traditional stand-alone card technologies that lack the integrated, multi-purpose functionality that is available in IPOS systems. In 2012, approximately 45% of all POS devices were IPOS-capable, up from 39% in 2010 according to data on single-location SMBs (U.S. and Canada) from IHL, an industry research firm. In addition, this research indicates that in 2012, 69% of all new POS device shipments to SMB merchants were IPOS-capable, compared to 94% for the largest merchants. We believe this shift is due to a number of trends, including the decreasing costs of IPOS systems, demand for more payment options, vertical specialization of IPOS software, new security standards and the penetration of tablet and SaaS-based IPOS systems.

Increasing Adoption of New Payments Technologies and Services by SMBs

In addition to the significant advancement and adoption of IPOS, there has been substantial innovation and investment in the payments and POS industries over the last several years. As a result, numerous new payments products and services, such as rewards programs and mobile payments, are being promoted and increasingly adopted by SMB merchants. While these capabilities represent significant opportunities for SMB merchants to level the playing field with larger retailers, the wide spectrum of new choices, their technology requirements and their impact on other areas of merchants’ businesses can be overwhelming and risky. In addition, if these new payments technologies and services are not integrated with a SMB merchant’s POS technology, these emerging solutions can be nearly unusable by them. This presents an attractive opportunity for technology and service providers, including IPOS Developers and Dealers, to bundle, simplify and integrate these services into an IPOS solution.

3

Table of Contents

Traditional Merchant Acquirers’ Fragmented Approach to IPOS

When working with a traditional merchant acquirer, merchants using an IPOS system are typically required to use a number of different providers, each using separate, disjointed processes. The value chain can be complicated and expensive, involving the use of up to four different product and service providers, including a Developer, a Dealer, a payment gateway or middleware provider and a merchant acquirer. In this situation, merchants typically pay fees to both their merchant acquirer and the payment gateway or middleware provider due to the lack of a direct integration to their POS system. Furthermore, the complicated and fragmented nature of the value chain involved in setting up and utilizing IPOS solutions with traditional acquirers makes it difficult to diagnose the source of payments related support issues, which costs merchants both time and money to resolve.

Rapid Rate of Change and Complexity in the Payments and IPOS Sectors Creates New Opportunities

We believe many merchants are adopting sophisticated POS solutions to enhance the efficiency of their business and to help them attract customers and generate revenue. Payments integration is a critical and increasingly complex component of the overall solution, which is made more difficult by the numerous disparate technologies and specialized IPOS systems in the market. Based on our industry experience, we believe that neither the merchants, who frequently lack the IT expertise, nor the traditional merchant acquiring sales and support representatives, who typically are not familiar with the integrated payments landscape, are well-positioned to successfully navigate these solutions. As a result, we believe SMB merchants look for IPOS technology and payments providers who can help them navigate this complex market. Additionally, we believe IPOS Developers and Dealers may increasingly depend on, and are looking for, payments technology service partners who can (1) understand their unique needs and technologies, (2) help them embed payment processing solutions into their systems, (3) help them navigate the complexity and regulatory burdens of the payments industry and (4) provide high-quality support for these services.

The Mercury Model

The shift to IPOS requires a specialized approach to effectively and efficiently serve merchants and the technology and service providers upon which they rely. Mercury has built proprietary and differentiated payments technology and services to meet the specialized needs of Developers, Dealers and SMB merchants. For over 10 years, we have been successfully entering into partnerships and selling our services to meet these demands through a superior, disruptive business model that is gaining market share.

Overview of the Mercury Model

Mercury pioneered a new business and go-to-market model focused on IPOS Developers and Dealers. This model creates a differentiated merchant experience and a highly efficient distribution, customer acquisition and monetization engine. We developed the Mercury Model to meet the converging demands of Developers, Dealers and merchants. The four key elements of the Mercury Model are:

| (1) | The Use of IPOS Channel Distribution—We pioneered the distribution of payments technology and services through IPOS Developers and Dealers who embed, bundle and cross-sell our payments services in their own solutions, and in return, earn recurring commissions for each merchant they refer to Mercury. We are able to access SMB merchants through the Mercury Network of approximately 600 Developers and 2,430 Dealers (as of |

4

Table of Contents

| December 31, 2013), and, based on a Mercury-sponsored survey of a sample of Dealers, which included questions regarding the number of employees at each Dealer, and management’s evaluation of the responses provided in such survey and ongoing observations of staffing practices at our Dealers, we estimate there are over 13,000 employees at our Dealers who advise merchants on the selection and use of payments services. These employees provide key sales and marketing services for us in lieu of a direct sales force. |

| (2) | Differentiated Technology and Solutions—We built our proprietary technology to enable us to connect to and process transactions from IPOS systems more efficiently and cost effectively without the need for a third-party gateway or middleware, which many other merchant acquirers would require to offer integrated payments. We work with our Developers to embed our technology into their software so that it comes pre-integrated in the IPOS system. |

| (3) | Deep IPOS Domain Expertise—Over the past 10 years, we have developed deep domain expertise in serving the IPOS ecosystem of Developers, Dealers and merchants. We have used this experience to create proprietary technology solutions to meet their specific needs and build customized integrations into their varied and disparate technology systems. Our domain expertise has also enabled us to create a powerful culture of specialized customer service that other traditional merchant acquirers with less experience and dedication to serving the IPOS channel frequently lack. |

| (4) | Software-as-a-Service (SaaS) Delivery Model—We use a SaaS delivery model that enables us to provide our solutions with substantial scale and efficiency. This SaaS delivery combines our cloud-based technologies and Developer integration tools to provide automated updates through efficient methods of access to our proprietary technology platform. This model reduces cost for both Mercury and our partners because it allows us to provide new features and functionality to disparate systems without the need for on-premise updates to Mercury’s software. |

The Mercury Model’s Disruption of the Traditional Merchant Acquiring Industry

The applicability of the Mercury Model to today’s SMB payments landscape has enabled us to disrupt the traditional merchant acquiring approach. We believe the following attributes of the Mercury Model, in conjunction with increasing IPOS adoption, have enabled us to capture market share and grow faster than traditional merchant acquirers:

| • | Seamless technology integration—Our numerous payment integration options are designed to seamlessly embed our payments services within our Developers’ IPOS systems. This enables us to provide dedicated customer service that is able to understand and support our partners’ IPOS solutions and provide easier upgrades to and development of new functionality. |

| • | The strong relationships and economic alignment with our partners—We believe our Developers and Dealers are highly incentivized to promote our services due to the value we provide to their IPOS solutions, the strong customer support we provide both to them and to our shared merchants, as well as the valuable, recurring commissions that we provide as their merchants process more transactions. We believe our model is aligned with our distribution partners and is designed to avoid the channel conflicts created by many of our competitors, who use multiple, competing, direct and indirect sales channels. |

| • | Attractive economics—Our highly efficient distribution model is designed to provide attractive economics through high merchant retention and recurring revenue, low cost of merchant acquisitions, minimal up-front commission expenses and low price sensitivity due to the delivery of our services as a bundled offering with the IPOS system. |

5

Table of Contents

| • | The stickiness of our solutions—Our bundled technology offering is designed to be highly valuable to our distribution partners and to provide greater convenience and functionality to our merchants. We believe this creates a joint value proposition that is designed to be greater than the sum of its parts. As a result, our services can be harder to replace by a competing provider that lacks this connectivity and integration. Ultimately, we believe this results in high merchant and revenue retention. |

We believe the Mercury Model’s combination of economic efficiency, network effects and benefits to participants has disrupted the merchant acquiring industry and serves as a foundation for Mercury’s strategy. Furthermore, we believe that our momentum with emerging technologies, such as integrations with tablet IPOS Developers, will position us strongly as the landscape evolves.

Our Competitive Strengths

We believe we have attributes that differentiate us from our competitors and provide us with significant competitive advantages. The combination of these individual advantages produces a synergistic network effect that further differentiates the Mercury Model. We believe that the Mercury Model creates meaningful barriers to entry for other merchant acquirers attempting to reach the same scale with Developers and Dealers.

Market Leadership Established Through Early-Mover Advantage

We believe we have established ourselves as a leading provider of payments technology services to the IPOS ecosystem by pioneering the integration and distribution of our services through a network of over 3,000 IPOS Developers and Dealers, which management estimates is the largest network of IPOS Developers and Dealers among providers of payment processing services in the U.S. and Canada. We believe this enables us to build deep technology relationships and create strong economic bonds through our recurring commissions with our Developers and Dealers. We believe our leadership position attracts new business and reduces the likelihood of existing partners and merchants switching to other vendors.

Large, Integrated Network of IPOS Developers and Dealers

We have built a network of approximately 600 Developers and 2,430 Dealers as of December 31, 2013, which we believe is the largest ecosystem of IPOS partners in the U.S. and Canada. Based on a Mercury-sponsored survey of a sample of Dealers, which included questions regarding the number of employees at each Dealer, and management’s evaluation of the responses provided in such survey and ongoing observations of staffing practices at our Dealers, we estimate there are over 13,000 employees at our Dealers who advise merchants on the selection and use of payments services, which we believe is substantially larger than any direct sales force of payments related services in the U.S. and Canada. Furthermore, our partners provide broad merchant reach with minimal concentration.

Deep and Proprietary Expertise in Ecosystem Management

We have invested over 10 years exclusively focused on optimizing the methodologies, processes and systems required to manage our channel relationships. Leveraging these relationships with our partners and powered by our technology platform, we are able to obtain, store and utilize information within the ecosystem and have developed a differentiated domain expertise in serving the IPOS Developer, Dealer and merchant community. We believe these capabilities are difficult to replicate in part and as a whole system.

6

Table of Contents

IPOS Integration Technology and Support

We have developed proprietary technology, processes and tools for embedding payments in a variety of POS technology environments. Over the past 10 years, Developers have integrated our services into over 2,500 unique versions and sub-versions of IPOS software. This expertise enables us to address emerging technologies and form factors as they arise, as evidenced by our traction in establishing partnerships with approximately 30 tablet IPOS Developers, which we expect to grow.

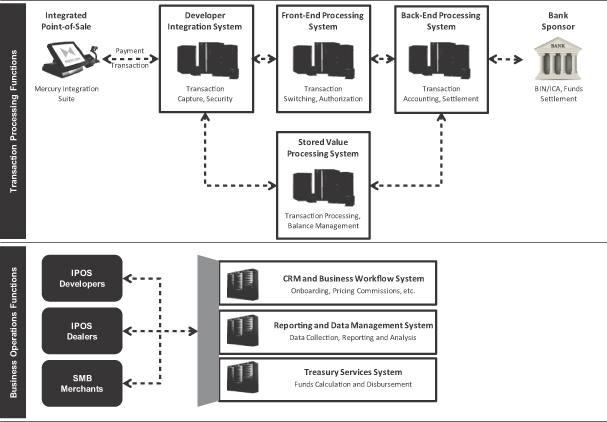

Proprietary Technology Platform and SaaS Delivery Model

We have a single, proprietary platform that enables us to integrate with over 2,500 IPOS software versions and sub-versions and provide a broad range of transaction processing services, including front- and back-end merchant processing systems, a stored value card processing system and CRM, reporting and other support systems. We use a SaaS delivery model that enables us to provide our solutions with substantial scale and efficiency.

Differentiated Suite of Products & Services

We believe the breadth and functionality of our products and services is a differentiator in the marketplace. We offer our distribution partners a comprehensive suite of technologies and services that enable the development, integration and utilization of our payments, stored value and security solutions across numerous IPOS systems and merchant industry verticals. We offer merchants a comprehensive suite of solutions for accepting both traditional and emerging payment types, managing stored value programs, reporting and providing omni-channel commerce services.

Deep-Rooted Culture Focused on Merchant and Partner Service

Our culture is deeply rooted in providing a differentiated merchant and partner service that leverages our IPOS domain expertise, technical knowledge and the enterprise-wide belief that we only succeed if our partners and merchants succeed.

Powerful Network Effects and Barriers to Entry

The large reach of the Mercury Network increases our merchant base, which helps us develop a broad set of products, services and support capabilities to meet this diverse community’s needs. These capabilities help us recruit additional Developers and Dealers to join the network, in order to offer a more competitive solution to their current and prospective merchants. This growing ecosystem then attracts other types of partners, like PayPal, who can provide additional functionality and services to SMB merchants at scale.

The powerful network effects combined with our other competitive strengths create barriers to entry that have impeded other merchant acquirers from reaching the same scale of channel distribution through Developers and Dealers that we have achieved.

Our Growth Strategies

Our large and scalable distribution capabilities, innovative technologies, and attractive products and services make us well positioned to pursue a variety of growth strategies. We plan to drive growth through the following strategies and expand the reach of the Mercury Network and the value we provide to our entire ecosystem.

7

Table of Contents

Continue to Penetrate the Mercury Network’s Installed Base of Merchants

We will continue to aggressively pursue the merchant installed base of our Developer and Dealer partners in the U.S and Canada. We believe many merchants who use one of our partners’ IPOS systems or POS terminals have not switched to using Mercury as their payments technology provider because they either have not been proactively approached or have not faced a catalyst that provides an opportunity to switch. Based on management estimates, less than 10% of our partners’ installed base of approximately 1 million merchants is currently served by Mercury. We believe selling to this installed base of merchants will be a significant driver of our growth in the near-term.

Expand the Mercury Network of Developers and Dealers

We plan to continue to expand the Mercury Network of Developers and Dealers to maximize our coverage of IPOS SMB merchants in the U.S. and Canada. We will strategically target Developers and Dealers that enable us to penetrate or consolidate our market leadership in specific industry verticals. We believe we have an addressable opportunity of over 3,000 Developers and over 5,000 Dealers in the markets we currently serve. Additionally, we expect the prevalence of new IPOS form factors, such as tablets, and the proliferation of consumer payment options to continue to support a large and diverse set of Developers and Dealers serving the SMB market.

Expand and Enhance Our Suite of Products & Services

We intend to maintain our leadership position in the industry by providing best-of-breed payments solutions to our Developers, Dealers and merchants. We will continue to leverage our single, proprietary platform and processing capabilities to promote innovation and expand our suite of products and services to meet the needs of our Developers, Dealers and merchants.

Expand and Promote Omni-Channel Commerce

SMB merchants are increasingly looking to sell through various channels, including brick-and-mortar stores and mobile and online channels, to increase sales and create a convenient customer experience. Today, approximately 8% of our merchants utilize our services for online or mobile commerce payments, and we expect this percentage to grow. We believe our disruptive business model is well suited to address the growing demands for omni-channel commerce, and we plan to pursue incremental growth opportunities.

Expand into New Verticals and Markets

In addition to the significant growth opportunities in our current markets, which today cover over 190 standard industrial classification (“SIC”) codes, we will continue to evaluate opportunities in new industry verticals and merchant categories as IPOS solutions gain adoption. Our business model and single, proprietary technology platform, further enhanced with new capabilities from our in-house processing investment, are highly flexible and can serve a variety of new merchant sizes, categories and locations.

Selectively Pursue Strategic Acquisitions

Given the large size and attractive growth trends of our current addressable market, we are primarily focused on growing our business organically. However, we may selectively pursue strategic acquisitions as opportunities arise.

8

Table of Contents

Our Solutions

We offer a comprehensive range of products and services to Developers, Dealers and merchants that enable the development, integration and utilization of our payment functionality within IPOS solutions, and provide opportunities for our Mercury Network partners to grow their portfolio of merchants with us. For merchants, these include solutions for accepting both traditional and emerging payment types, managing stored value programs, reporting and omni-channel commerce services. For distribution partners, these include methods for integrating payment acceptance capabilities into IPOS systems and a range of security, reporting and operational tools.

Summary of Risk Factors

Our business is subject to numerous risks, which are described under “Risk Factors” beginning on page 23. You should carefully consider these risks before making an investment. In particular, the following considerations, among others, may offset our competitive strengths or have a negative effect on our business strategy, which could cause a decline in the price of our Class A common stock and result in a loss of all or a portion of your investment:

| • | competition with larger firms that have greater financial resources; |

| • | dependence on non-exclusive Developers and Dealers to market our services; |

| • | liability resulting from unauthorized disclosure or impermissible use of data or disruptions to our services; |

| • | our need to keep pace with rapid developments in our industry and provide new products and services; |

| • | consolidation or restructuring of the IPOS software industry; |

| • | technical, operational and regulatory risks due to our new in-house processing initiative and with to respect our third-party providers’ systems and our other information technology systems; |

| • | reliance on third parties for significant services; |

| • | exposure to economic conditions affecting consumer and commercial spending; |

| • | degradation of the quality of our products, services and support; |

| • | our ability to increase our market share, expand into new markets and compete with new entrants; |

| • | compliance with and changes to government regulations and payment network rules and standards; |

| • | our ability to successfully manage our intellectual property; |

| • | our substantial level of indebtedness and increases in our indebtedness and operating and financial restrictions imposed by our senior secured credit facilities; and |

| • | the other factors set forth under “Risk Factors.” |

9

Table of Contents

Our History and Investment by Silver Lake

Mercury was founded by Jeff Katz and Marc Katz in Brewster, New York in 2001 to provide tech-enabled products and services that help small- and medium-sized merchants compete and thrive. The company moved to Durango, Colorado in 2002, where it is currently headquartered. Jeff and Marc developed the Mercury Model, and Larry Stone, an early investor and partner in the company, took an active role in helping the business grow. In 2013, Jeff and Marc were inducted into the Retail Solutions Providers Associations Hall of Fame, recognized as the “Pioneers of Integrated Point of Sale” as a result of their work with Mercury. Jeff Katz, Marc Katz and Larry Stone are sometimes referred to collectively in this prospectus as the “Founders.”

Mercury Payment Systems, LLC was formed in 2010, in connection with an investment by Silver Lake, to hold the assets relating to our business. In April 2010, SL Quicksilver LLC (“SL Quicksilver”), an affiliate of Silver Lake, acquired Class A units representing a majority interest in Mercury Payment Systems, LLC from Mercury Payment Systems, LLC and from certain existing holders for an aggregate of approximately $450.6 million. As of December 31, 2013, SL Quicksilver held approximately 62% of the outstanding membership interests of Mercury Payment Systems, LLC.

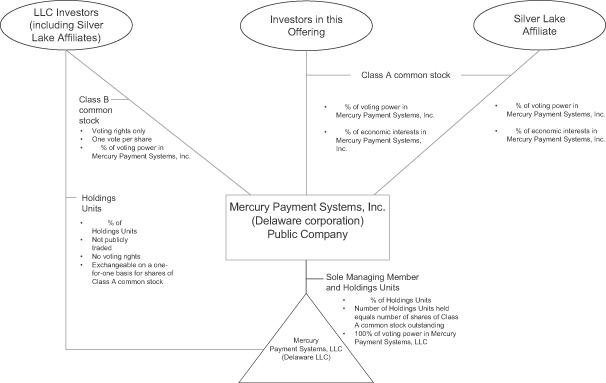

Our Structure

Immediately following this offering, Mercury Payment Systems, Inc. will be a holding company, and its sole material asset will be a controlling equity interest in Mercury Payment Systems, LLC. As the sole managing member of Mercury Payment Systems, LLC, Mercury Payment Systems, Inc. will operate and control all of the business and affairs of Mercury Payment Systems, LLC and, through Mercury Payment Systems, LLC and its subsidiaries, conduct our business. Mercury Payment Systems, Inc. will consolidate Mercury Payment Systems, LLC in its consolidated financial statements and will report a noncontrolling interest related to the Holdings Units held by certain of our existing owners on its consolidated financial statements.

Before the completion of this offering, the limited liability company agreement of Mercury Payment Systems, LLC will be amended and restated to, among other things, modify its capital structure to create a single new class of units that we refer to as “Holdings Units.” We and certain of our existing owners will also enter into an exchange agreement under which they will have the right, subject to the terms of the exchange agreement, to exchange their Holdings Units for shares of our Class A common stock on a one-for-one basis, subject to customary conversion rate adjustments for stock splits, stock dividends, reclassifications and other similar transactions. See “Organizational Structure” and “Certain Relationships and Related Party Transactions—Exchange Agreement.”

Following the reorganization transactions described in “Organizational Structure,” each of our existing owners that continues to hold Holdings Units and that held voting units prior to the reorganization transactions will also hold shares of Class B common stock of Mercury Payment Systems, Inc. The shares of Class B common stock have no economic rights but entitle the holder to one vote per share on matters presented to stockholders of Mercury Payment Systems, Inc.

10

Table of Contents

The diagram below depicts our organizational structure immediately following this offering assuming no exercise by the underwriters of their option to purchase additional shares of Class A common stock.

11

Table of Contents

Our Sponsor

Silver Lake is a global investment firm focused on the technology, technology-enabled and related growth industries with offices in Silicon Valley, New York, London, Hong Kong, Shanghai and Tokyo. Silver Lake was founded in 1999 and has over $20 billion in combined assets under management and committed capital across its large-cap private equity, middle-market private equity, growth equity and credit investment strategies.

After the completion of this offering, Silver Lake and affiliates of the Founders will continue to control a majority of the voting power of all outstanding shares of our voting stock. For a discussion of certain risks, potential conflicts and other matters associated with control by Silver Lake and the Founders, see “Risk Factors—Risks Related to Our Company and Our Organizational Structure—We are controlled by affiliates of Silver Lake and the Founders, whose interests may be different than the interests of other holders of our securities” and “Description of Capital Stock.”

Corporate Information

Mercury Payment Systems, Inc. was incorporated in Delaware in December 2013 under the name Mercury Payment Systems Holdings, Inc. In March 2014, we changed our name to “Mercury Payment Systems, Inc.” Our principal executive offices are located at Tech Center Plaza, 10 Burnett Court, Suite 300, Durango, Colorado 81301. Our telephone number is (970) 247-5557. Our website address is www.mercurypay.com. Information contained on, or that can be accessed through, our website does not constitute part of this prospectus, and inclusions of our website address in this prospectus are inactive textual references only.

Trademarks and Trade Names

We own or have rights to trademarks or trade names that we use in conjunction with the operation of our business. In addition, our name, logo and website name and address are our service marks or trademarks. Some of the more important trademarks that we use include Mercury®, Mercury Payment Systems®, MercuryPay®, MercuryGift®, MercuryAnyware®, MercuryMailTM, MercuryLoyaltyTM and MercuryActivateTM. This prospectus contains additional trade names, trademarks and service marks of other companies. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply relationships with, or endorsement or sponsorship of us by, these other companies.

12

Table of Contents

The Offering

| Class A common stock offered by us |

shares |

| Class A common stock outstanding after giving effect to this offering |

shares (or shares if all then outstanding exchangeable Holdings Units were exchanged for newly-issued shares of Class A common stock on a one-for-one basis). |

| Class B common stock outstanding after giving effect to this offering |

shares |

| Option to purchase additional shares of Class A common stock from us |

The underwriters have been granted an option to purchase up to additional shares of Class A common stock from us at any time within 30 days from the date of this prospectus. |

| Voting power held by holders of Class A common stock after giving effect to this offering |

% (or 100% if all then outstanding exchangeable Holdings Units were exchanged for newly-issued shares of Class A common stock on a one-for-one basis). |

| Voting power held by holders of Class B common stock after giving effect to this offering |

% (or 0% if all then outstanding exchangeable Holdings Units were exchanged for newly-issued shares of Class A common stock on a one-for-one basis). |

| Use of proceeds |

We estimate that the proceeds to us from this offering, after deducting underwriting discounts and commissions and estimated offering expenses payable by us, will be approximately $ million, based on the assumed initial public offering price of $ per share, which is the midpoint of the price range set forth on the front cover of this prospectus. Mercury Payment Systems, LLC will bear or reimburse Mercury Payment Systems, Inc. for all of the expenses of this offering, which we estimate will be approximately $ million. |

| We intend to use the net proceeds from this offering, or $ million, to purchase Holdings Units and shares of Class A common stock from our existing owners, as described under “Organizational Structure—Offering Transactions.” Accordingly, we will not retain any of these proceeds. See “Principal Stockholders” for information regarding the economic interest of certain of our related parties in MPS 1, Inc., and Mercury Payment Systems II, LLC, two of the existing owners from which we intend to purchase Holdings Units with proceeds from this offering. See also “Use of Proceeds.” |

13

Table of Contents

| Voting rights |

Each share of our Class A common stock entitles its holder to one vote on all matters to be voted on by stockholders generally. |

| Following the reorganization transactions, each of our existing owners that continues to hold Holdings Units and that held voting units prior to the reorganization transactions will hold a number of shares of Class B common stock equal to the number of Holdings Units held by such person. The shares of Class B common stock have no economic rights but entitle the holder to one vote per share on matters presented to stockholders of Mercury Payment Systems, Inc. See “Description of Capital Stock—Capital Stock—Common Stock—Class B Common Stock.” |

| Holders of our Class A common stock and Class B common stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law. |

| Dividend policy |

We do not intend to pay dividends on our Class A common stock in the foreseeable future. |

| Immediately following this offering, Mercury Payment Systems, Inc. will be a holding company, and its sole material asset will be a controlling equity interest in Mercury Payment Systems, LLC. We intend to cause Mercury Payment Systems, LLC to make distributions to Mercury Payment Systems, Inc. in an amount sufficient to cover cash dividends, if any, declared by us. If Mercury Payment Systems, LLC makes such distributions to Mercury Payment Systems, Inc., the other holders of Holdings Units will be entitled to receive pro rata distributions. |

| Our ability to pay dividends on our Class A common stock is effectively limited by the covenants of the senior secured credit facilities of Mercury Payment Systems, LLC (the “Credit Facilities”) and may be further restricted by the terms of any future debt or preferred securities incurred or issued by us or our subsidiaries. See “Dividend Policy” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Senior Secured Credit Facilities.” |

| Exchange agreement |

Prior to this offering, we will enter into an exchange agreement with our existing owners that will continue to hold Holdings Units following the reorganization transactions so that they may, subject to the terms of the exchange agreement, exchange their Holdings Units for shares of Class A common stock on a one-for-one basis, subject to customary conversion rate adjustments for |

14

Table of Contents

| stock splits, stock dividends, reclassifications and other similar transactions. When a Holdings Unit is exchanged by an existing owner who held shares of Class B common stock, a corresponding share of Class B common stock will be cancelled. |

| Tax receivable agreements |

Our purchase of Holdings Units in connection with this offering and future offerings and future exchanges of Holdings Units for shares of our Class A common stock are expected to produce favorable tax attributes for us, as is the SLP Corp Merger described under “Organizational Structure.” These tax attributes would not be available to us in the absence of those transactions. Upon the closing of this offering, we will be a party to two tax receivable agreements. Under the first of those agreements, we generally will be required to pay to our existing owners that will continue to hold Holdings Units following the reorganization transactions 85% of the applicable cash savings, if any, in U.S. federal and state income tax that we actually realize (or are deemed to realize in certain circumstances) as a result of (1) certain tax attributes of their Holdings Units sold to us or exchanged and that are created as a result of the sales or exchanges of their Holdings Units for shares of our Class A common stock, (2) tax benefits related to imputed interest and (3) payments under such tax receivable agreement. Under the second tax receivable agreement, we generally will be required to pay to the sole stockholder of SLP III Quicksilver Feeder Corp. (“SLP Corp”), an affiliate of Silver Lake, 85% of the amount of cash savings, if any, in U.S. federal and state income tax that we actually realize (or are deemed to realize in certain circumstances) as a result of (1) the tax attributes of the Holdings Units we acquire in the SLP Corp Merger, (2) net operating losses available as a result of the SLP Corp Merger and (3) tax benefits related to imputed interest. Under both agreements, we generally will retain the benefit of the remaining 15% of the applicable tax savings. However, the sole stockholder of SLP Corp, the other affiliates of Silver Lake and affiliates of the Founders will be entitled to elect, starting in 2020, to accelerate our obligations under their respective tax receivable agreements and receive a lump sum payment equal to the present value of 100% of the anticipated future cash savings in respect of the applicable tax benefits, determined based on certain assumptions. See “Certain Relationships and Related Party Transactions—Tax Receivable Agreements” and “Organizational Structure.” |

| Controlled company |

Upon the completion of this offering, affiliates of Silver Lake and affiliates of the Founders will control approximately % of the voting power of our outstanding common stock (or approximately % if the underwriters exercise in full their option to purchase additional shares). As a result, we will be a “controlled company” under the Nasdaq corporate governance |

15

Table of Contents

| standards. Under these standards, a company of which more than 50% of the voting power is held by an individual, group or another company is a “controlled company” and may elect not to comply with certain corporate governance standards. See “Management—Controlled Company Exemption.” |

| Directed Share Program |

At our request, the underwriters have reserved up to shares, or five percent, of the Class A common stock offered by this prospectus for sale, at the initial public offering price, to certain persons identified by our directors and executive officers. The number of shares of our Class A common stock available for sale to the general public will be reduced to the extent these persons purchase such reserved shares. Any reserved shares of our Class A common stock that are not so purchased will be offered by the underwriters to the general public on the same terms as the other shares of our Class A common stock offered by this prospectus. |

| Proposed Nasdaq symbol |

“MPS” |

In this prospectus, unless otherwise indicated, the number of shares of our Class A common stock outstanding and the other information based thereon does not reflect:

| • | shares of Class A common stock issuable upon exchange of Holdings Units (or, if the underwriters exercise in full their option to purchase additional shares of Class A common stock, shares of Class A common stock issuable upon exchange of Holdings Units) that will be held by certain of our existing owners immediately following this offering; |

| • | shares of Class A common stock issuable upon exercise of options outstanding on the date of this prospectus at a weighted average exercise price of $ per share under our 2010 Incentive Plan (which will become subject to our 2014 Stock Award Plan in connection with this offering); and |

| • | additional shares of Class A common stock reserved for future issuance under the Mercury Payment Systems, Inc. 2014 Stock Award Plan, including shares of Class A common stock issuable upon the exercise of options expected to be granted in connection with this offering with an exercise price equal to the initial public offering price. |

Except as otherwise indicated, all information in this prospectus assumes:

| • | no exercise of options subsequent to December 31, 2013; |

| • | no exercise by the underwriters of their option to purchase up to additional shares of Class A common stock from us; and |

| • | the filing and effectiveness of our amended and restated certificate of incorporation and the effectiveness of our amended and restated bylaws in connection with the closing of this offering. |

16

Table of Contents

Summary Consolidated Financial Data

The following summary consolidated financial and other data of Mercury Payment Systems, LLC should be read in conjunction with “Organizational Structure,” “Use of Proceeds,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our audited consolidated financial statements and unaudited consolidated financial statements and the related notes included elsewhere in this prospectus. Mercury Payment Systems, LLC will be considered our predecessor for accounting purposes, and its consolidated financial statements will be our historical financial statements following this offering.

The income statement data set forth below for the years ended December 31, 2011, 2012 and 2013 are derived from the audited consolidated financial statements of Mercury Payment Systems, LLC that are included elsewhere in this prospectus. The historical results presented below are not necessarily indicative of financial results to be achieved in future periods.

The unaudited pro forma income statement data set forth below for the year ended December 31, 2013 present our consolidated results of operations giving pro forma effect to the reorganization transactions and the use of the estimated net proceeds from this offering, as if such transactions had occurred on January 1, 2013. The unaudited pro forma balance sheet data set forth below as of December 31, 2013 presents our consolidated financial position giving pro forma effect to the reorganization transactions and the use of the estimated net proceeds from this offering, as if such transactions had occurred on December 31, 2013. The pro forma adjustments are based on available information and upon assumptions that our management believes are reasonable in order to reflect, on a pro forma basis, the impact of these transactions on the historical financial information of Mercury Payment Systems, LLC. The unaudited pro forma consolidated financial data is included for informational purposes only and does not purport to reflect the results of operations or financial position of Mercury Payment Systems, Inc. that would have occurred had we operated as a public company during the periods presented. The unaudited pro forma financial data presented below are not necessarily indicative of financial results to be achieved in future periods.

17

Table of Contents

| Year Ended | Pro Forma | |||||||||||||||

| December 31, 2011 |

December 31, 2012 |

December 31, 2013 |

Year Ended December 31, 2013 |

|||||||||||||

| Income Statement Data (in thousands): |

||||||||||||||||

| Net Revenue |

$ | 154,703 | $ | 203,277 | $ | 237,259 | $ | |||||||||

| Cost of services and sales |

48,336 | 62,536 | 74,088 | |||||||||||||

| Operating expenses |

55,428 | 78,951 | 100,796 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

50,939 | 61,790 | 62,375 | |||||||||||||

| Total other income (expense) |

(7,946 | ) | (15,249 | ) | (19,722 | ) | ||||||||||

| Income taxes |

— | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net Income (loss) |

42,993 | 46,541 | 42,653 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Other Financial Data (in thousands)(1): |

||||||||||||||||

| Adjusted EBITDA |

$ | 61,169 | $ | 75,569 | $ | 92,894 | $ | |||||||||

| Adjusted net income |

45,348 | 49,647 | 57,066 | |||||||||||||

| Selected Operational Data(2): |

||||||||||||||||

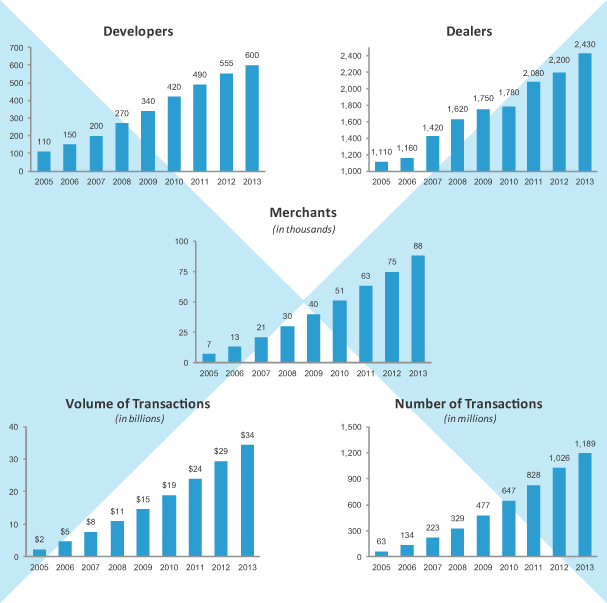

| Developers |

490 | 555 | 600 | |||||||||||||

| Dealers |

2,080 | 2,200 | 2,430 | |||||||||||||

| Merchants |

63,300 | 75,800 | 88,700 | |||||||||||||

| Volume of Transactions (in millions) |

$ | 23,961 | $ | 29,370 | $ | 34,307 | ||||||||||

| Number of Transactions (in millions) |

828 | 1,026 | 1,189 | |||||||||||||

| (1) | See “—Adjusted EBITDA and Adjusted Net Income.” |

| (2) | Approximation. See “—Key Operating Metrics” and “Industry Data and Operating Metrics.” |

| As of December 31, 2013 | ||||||||

| Actual | Pro Forma(1) | |||||||

| (in thousands) | ||||||||

| Balance Sheet Data (at end of period): |

||||||||

| Cash and cash equivalents |

$ | 20,905 | $ | |||||

| Total assets |

130,512 | |||||||

| Total liabilities |

319,744 | |||||||

| Long-term debt, including current portion, net of discount |

290,770 | |||||||

| Total equity (deficit) |

(189,232 | ) | ||||||

| (1) | Pro forma balance sheet data presents balance sheet data on a pro forma basis for Mercury Payment Systems, Inc. after giving effect to the reorganization transactions as described in “Organizational Structure” and after giving effect to this offering and the application of the proceeds from this offering as described in “Use of Proceeds,” assuming an initial public offering price of $ per share, which is the midpoint of the price range set forth on the front cover of this prospectus. A $1.00 increase or decrease in the assumed initial public offering price would increase or decrease, as applicable, cash and cash equivalents, total assets and total equity by $ , assuming the number of shares offered by us, as set forth on the front cover of this prospectus, remains the same and after deducting assumed underwriting discounts and commissions and the estimated offering expenses payable by us. An increase or decrease of 100,000 shares in the number of shares sold in this offering by us would increase or decrease, as applicable, cash and cash equivalents, total assets and total equity by $ , assuming an initial public offering price of $ per share, which is the midpoint of the price range set forth on the front cover of this prospectus, and after deducting assumed underwriting discounts and commissions and the estimated offering expenses payable by us. |

18

Table of Contents

Adjusted EBITDA and Adjusted Net Income

Adjusted net income is calculated as net income plus costs related to the restructuring in connection with this offering, share-based compensation expense, non-cash write-offs, organizational restructuring-related severance and compensation and headquarters construction expense. Adjusted EBITDA is equal to adjusted net income plus gross interest expense, income taxes and depreciation and amortization.

Adjusted EBITDA and adjusted net income eliminate the effects of items that we do not consider indicative of our core operating performance. As a result, we consider adjusted EBITDA and adjusted net income to be important indicators of our operational strength and the performance of our business. Management believes the use of adjusted EBITDA and adjusted net income are appropriate to provide additional information to investors about certain material non-cash items and about unusual items that we do not expect to continue at the same level in the future. By providing these non-GAAP financial measures, together with a reconciliation to GAAP results, we believe we are enhancing investors’ understanding of our business and our results of operations, as well as assisting investors in evaluating how well we are executing strategic initiatives. We believe adjusted EBITDA and adjusted net income are used by investors as a supplemental measure to evaluate the overall operating performance of companies in our industry.

Adjusted EBITDA and adjusted net income are not measures determined in accordance with GAAP and should not be considered as an alternative to, or more meaningful than, net income (as determined in accordance with GAAP) as a measure of our operating results or net cash provided by operating activities (as determined in accordance with GAAP) as a measure of our liquidity. Adjusted EBITDA and adjusted net income as presented by us may not be comparable to similarly titled measures reported by other companies. In particular, adjusted EBITDA has significant limitations as an analytical tool because it excludes certain material costs. For example, it does not include interest expense, which has been a necessary element of our costs. Because of our use of certain property, equipment and software, depreciation expense is a necessary element of our costs and ability to generate revenue. In addition, the omission of amortization expense associated with our intangible assets further limits the usefulness of this measure. Because adjusted EBITDA does not account for these expenses, its utility as a measure of our operating performance has material limitations. Because of these limitations, management does not view adjusted EBITDA in isolation and also uses other measures, such as net revenue, gross margin, cost of services and sales and net income to measure operating performance.

19

Table of Contents

The reconciliation of our adjusted EBITDA and adjusted net income to net income is as follows:

| Year Ended | Pro Forma | |||||||||||||||

| December 31, 2011 |

December 31, 2012 |

December 31, 2013 |

Year Ended December 31, 2013 |

|||||||||||||

| (in thousands) | ||||||||||||||||

| Net income |

$ | 42,993 | $ | 46,541 | $ | 42,653 | $ | |||||||||

| Percentage of net revenue |

28 | % | 23 | % | 18 | % | % | |||||||||

| Plus: |

||||||||||||||||

| Formation and reorganization expenses(a) |

— | — | 838 | |||||||||||||

| Share-based compensation (non-cash) |

1,456 | 1,858 | 1,959 | |||||||||||||

| Share-based compensation due to options modifications (cash) |

899 | 790 | — | |||||||||||||

| Non-cash technology and other write-off(b) |

— | — | 7,817 | |||||||||||||

| Organizational restructuring expense(c) |

— | — | 3,008 | |||||||||||||

| Headquarters construction expense(d) |

— | 458 | 791 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted net income |

$ | 45,348 | $ | 49,647 | $ | 57,066 | $ | |||||||||

| Percentage of net revenue |

29 | % | 24 | % | 24 | % | % | |||||||||

| Plus: |

||||||||||||||||

| Interest expense, gross |

8,019 | 15,314 | 19,279 | |||||||||||||

| Income taxes |

— | — | — | |||||||||||||

| Depreciation and amortization, net of debt discount and fee amortization |

7,802 | 10,608 | 16,549 | |||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Adjusted EBITDA |

$ | 61,169 | $ | 75,569 | $ | 92,894 | $ | |||||||||

| Percentage of net revenue |

40 | % | 37 | % | 39 | % | % | |||||||||

| (a) | Includes costs associated with forming Mercury Payment Systems, Inc. and other expenses directly related to the reorganization transactions and this offering. |

| (b) | Non-cash technology write-offs of $7,162 are defined as the disposal of systems which we had anticipated we would use to process transactions for our merchants, but which we later elected to source from a supplier under a long-term agreement. Another write-off is related to land that is held for sale in the amount of $655. |

| (c) | Organizational restructuring expense is made up of the one-time severance expense and outplacement expenses we incurred when we re-organized and decreased our workforce in 2013, plus the compensation associated with those employees affected who we do not anticipate replacing. |

| (d) | Headquarters construction expense is the one-time expense associated with building our headquarters, which was incurred between construction inception in 2012 and will continue through construction completion in the third quarter of 2014. |

20

Table of Contents

Key Operating Metrics

Below are charts that show growth over time in:

| • | the number of Developers in our ecosystem, |

| • | the number of Dealers in our ecosystem, |

| • | the number of merchants processing with us, |

| • | the dollar volume of payments our merchants process through us, and |

| • | the number of transactions our merchants process with us. |

We use these metrics to evaluate our performance, as described below under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Operating Metrics.” However, investors should not rely on historical growth rates in our operating metrics as an indication of future growth rates, as we do not expect to sustain the rates of growth we experienced in growing from a small enterprise to our current scale. See “Industry Data and Operating Metrics.”

21

Table of Contents

Developers—Developers are also known as independent software vendors in our industry. We define a Developer as a software and/or hardware vendor that has successfully integrated its products with our payment processing technology for at least one of our merchants. However, prior to 2012, we did not track specifically when a Developer first integrated its products with our payment technology. Accordingly, Developer numbers for periods before 2012 reflect our estimate based on company information with respect to Developer relationships recorded during the relevant period. See “Industry Data and Operating Metrics” for further detail. We focus on Developers of IPOS software and hardware because having our payment processing functionality embedded in Developers’ products allows us to provide our services to their merchant customers.

Dealers—We define a Dealer as an entity that referred a merchant to us within the past twelve months. Dealers are also known as value-added resellers in our industry. Developers who directly sell to merchants are also counted as Dealers if they have referred a merchant to us within the last 12 months. We focus on Dealers of IPOS software and systems because they source potential merchant customers for us.

Merchants—We define a merchant as a merchant location that is actively paying us fees. Our merchant count also includes a small number of merchants that pay us fees intermittently or are otherwise considered active from a customer relations perspective. See “Industry Data and Operating Metrics” for more detail. We focus on merchants because they are our principal source of revenue.

Volume—We define volume as the dollar value of Visa, MasterCard, Discover and other nominal non-American Express transactions processed by our merchants. We also allow our merchants to process American Express transactions, but due to the nature of our relationship with American Express, we do not include these transactions in volume metrics. We focus on volume, because it is a reflection of the scale and economic activity of our merchant base and because a significant part of our revenue is derived as a percentage of our merchants’ dollar volume receipts.

Transactions—We define a transaction as a Visa, MasterCard, Discover or other nominal non-American Express transactions processed by our merchants. For the reasons discussed above, we do not include American Express transactions. We focus on transactions, because it is a reflection of the scale and economic activity of our merchant base and because a significant part of our revenue is derived on a per transaction basis.

22

Table of Contents

Investing in our Class A common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as the other information in this prospectus, before deciding whether to invest in shares of our Class A common stock. The occurrence of any of the events described below could materially adversely affect our business, financial condition and results of operations. In such an event, the trading price of our Class A common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business

The payment processing industry is highly competitive, and we compete with certain firms that are larger and that have greater financial resources. Such competition could adversely affect the fees we receive from merchants and the compensation we pay to Developers and Dealers, and as a result, our margins, business, financial condition and results of operations.

The market for payment processing services is highly competitive. Other providers of payment processing services have established a sizable market share in the merchant acquiring sector and service more small- and medium-sized merchants than we do. Our growth will depend on a combination of the continued growth of electronic payments and our ability to increase our market share.

Our competitors include traditional merchant acquirers such as financial institutions, affiliates of financial institutions and well-established payment processing companies that target SMB merchants directly, including Bank of America Merchant Services, Chase Paymentech, Elavon, Inc. (a subsidiary of U.S. Bancorp), First Data Corporation, Heartland Payment Systems, Inc., Vantiv, Inc. and WorldPay US, Inc. In addition, we compete with vendors that are specifically targeting independent software vendors and value-added resellers as distribution partners for their merchant acquiring services, such as Accelerated Payments (owned by Global Payments Inc. (“Global Payments”)), PayPros (owned by Global Payments) and Merchant Warehouse.

Many of our competitors have substantially greater financial, technological and marketing resources than we have. Accordingly, if these competitors specifically target our business model, they may be able to offer more attractive fees or payment terms and advances to our current and prospective merchants and more attractive compensation to our Developer and Dealer partners. They also may be able to offer and provide services that we do not offer. Competition may influence the fees we receive from merchants and the compensation that we pay to our partners. If competition causes us to reduce the fees we charge or the compensation we pay to our partners, we will need to aggressively control our costs to maintain our profit margins. Competition could also result in a loss of existing Developers, Dealers and merchants and greater difficulty attracting new Developers, Dealers and merchants, which we may not be able to do. One or more of these factors could have a material adverse effect on our business, financial condition and results of operations.

To acquire and retain merchant accounts, we depend on Developers and Dealers that do not serve us exclusively and whose role in the payments industry could be diminished by changes in how IPOS software or payment services are provided to merchants.

We rely primarily on the efforts of Developers and Dealers to market our services to merchants seeking to establish an account with a payment processor. As a component of their businesses, Developers and Dealers seek to introduce both newly-established and existing SMB merchants, including retailers, restaurants and service providers, such as physicians, to providers of transaction payment processing services like us. Generally, our agreements with Developers and Dealers that refer merchants to us are non-exclusive in that they have the right to refer merchants to other service providers. If a Developer or Dealer switches some or all of their referrals to another payment

23

Table of Contents

processor, ceases operations or enters the processing business themselves, we may no longer receive new merchant referrals from them, and we risk losing existing merchants that were originally enrolled by them. If we fail to maintain our relationships with dealers in our network, or to recruit and establish relationships with new Developers and Dealers, we may experience increased merchant attrition and find it more difficult to attract new merchants, which could adversely affect our revenues.

The role of the IPOS distribution channels on which we rely to gain access to merchants could be negatively impacted by competition with other participants in the payments marketplace or by structural changes in the methods by which IPOS software or payments services are sold or made available to end users. The resulting impact on our channel partners could directly impact our ability to retain existing merchants and attract new merchants.

Unauthorized disclosure, destruction or modification of data, through cybersecurity breaches, computer viruses or otherwise or disruption of our services could expose us to liability, protracted and costly litigation and damage our reputation.