Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Stagwell Inc | v375810_8-k.htm |

| EX-99.1 - EXHIBIT 99.1 - Stagwell Inc | v375810_ex99-1.htm |

| EX-99.3 - EXHIBIT 99.3 - Stagwell Inc | v375810_ex99-3.htm |

April 24, 2014 Management Presentation First Quarter 2014 Results

2 FORWARD LOOKING STATEMENTS & OTHER INFORMATION This presentation, including our “ 2014 Financial Outlook”, contains forward - looking statements . The Company’s representatives may also make forward - looking statements orally from time to time . Statements in this presentation that are not historical facts, including statements about the Company’s beliefs and expectations, earnings guidance, recent business and economic trends, potential acquisitions, estimates of amounts for deferred acquisition consideration and “put” option rights, constitute forward - looking statements . These statements are based on current plans, estimates and projections, and are subject to change based on a number of factors, including those outlined in this section . Forward - looking statements speak only as of the date they are made, and the Company undertakes no obligation to update publicly any of them in light of new information or future events, if any . Forward - looking statements involve inherent risks and uncertainties . A number of important factors could cause actual results to differ materially from those contained in any forward - looking statements . Such risk factors include, but are not limited to, the following : • risks associated with severe effects of international, national and regional economic downturn ; • the Company’s ability to attract new clients and retain existing clients; • the spending patterns and financial success of the Company’s clients; • the Company’s ability to remain in compliance with its debt agreements and the Company’s ability to finance its contingent pa yme nt obligations when due and payable, including but not limited to those relating to “put” option rights and deferred acquisition co nsideration; • the successful completion and integration of acquisitions which compliment and expand the Company’s business capabilities; an d • foreign currency fluctuations. The Company’s business strategy includes ongoing efforts to engage in material acquisitions of ownership interests in entities in the marketing communications services industry . The Company intends to finance these acquisitions by using available cash from operations and through incurrence of bridge or other debt financing, either of which may increase the Company’s leverage ratios, or by issuing equity, which may have a dilutive impact on existing shareholders proportionate ownership . At any given time the Company may be engaged in a number of discussions that may result in one or more material acquisitions . These opportunities require confidentiality and may involve negotiations that require quick responses by the Company . Although there is uncertainty that any of these discussions will result in definitive agreements or the completion of any transactions, the announcement of any such transaction may lead to increased volatility in the trading price of the Company’s securities . Investors should carefully consider these risk factors and the additional risk factors outlined in more detail in the Annual Report on Form 10 - K under the caption “Risk Factors” and in the Company’s other SEC filings .

3 • Strong start to our fiscal 2014 • Results ahead of internal expectations across all key metrics • Industry - leading organic revenue growth • Strong EBITDA, operating leverage, and free cash flow growth • $24.4 million of net annualized new business revenue; robust pipeline • Significant advancements made across key strategic growth initiatives such as International, Media, and Analytics • Opportunistically accessed incremental growth capital and reduced borrowing costs • Increasing 2014 financial guidance SUMMARY

4 • Organic revenue growth of 8.3%, leading the industry • Revenue increased to $292.6 million from $265.6 million, up 10.1% • EBITDA increased to $36.4 million from $30.8 million, up 18.1% • EBITDA margin expanded to 12.5% from 11.6%, up 90 basis points • Net new business wins of $24.4 million • Free Cash Flow increased to $20.6 million from $15.4 million, up 34.0% FIRST QUARTER 2014 FINANCIAL HIGHLIGHTS

5 Note: Actuals may not foot due to rounding CONSOLIDATED REVENUE AND EARNINGS (US$ in millions, except percentages) 2014 2013 Revenue 292.6$ 265.6$ 10.1 % Operating Expenses Cost of services sold 191.7 177.9 7.8 % Office and general expenses 78.2 67.4 16.1 % Depreciation and amortization 11.3 9.5 19.2 % Operating Profit 11.4 10.9 Other, net (6.5) 2.7 Interest expense and finance charges (12.8) (12.4) Loss on redemption of notes 0.0 (55.6) Interest income 0.1 0.1 Income tax benefit (0.3) (14.3) Equity in earnings of non-consolidated affiliates 0.1 0.0 Loss from Continuing Operations (0.7) (40.0) Loss from discontinued operations, net of taxes (0.1) (2.2) Net Loss (7.5) (42.2) Net income attributable to non- controlling interests (1.4) (1.0) Net Loss Attributable to MDC Partners Inc. (8.8)$ (43.2)$ % Change Three Months Ended March 31,

6 • Q1 2014 revenue of $292.6 million represents 10.1% YoY growth • Growth driven by strength broadly across disciplines including Advertising, Media, Strategic Communications & PR, Insights, Design, and International SUMMARY OF SEGMENT RESULTS - REVENUE Note: Actuals may not foot due to rounding (US$ in millions, except percentages) 2014 2013 Revenue Strategic Marketing Services 205.9$ 183.4$ 12.3 % Performance Marketing Services 86.6 82.2 5.4 % Total Revenue 292.6$ 265.6$ 10.1 % % Change Three Months Ended March 31,

7 Note: Actuals may not foot due to rounding ORGANIC REVENUE GROWTH BY SEGMENT Note: Actuals may not foot due to rounding • Strategic Marketing Services continues to deliver exceptional organic growth, increasing 12.8% in the quarter, on top of double - digit growth last year • Performance Marketing Services benefitted from strong growth amongst its highest margin businesses • Acquisitions of Luntz , Kingsdale and LBN contributed 2.8% to reported growth • FX headwinds (largely CAD weakness) negatively impacted revenue by 100bp Strategic Performance Weighted Marketing Marketing Average Services Services Total Organic Growth 12.8% -1.7% 8.3% Acquisition Growth 0.0% 9.1% 2.8% Foreign Exchange Impact -0.5% -2.0% -1.0% Total 12.3% 5.4% 10.1% Three Months Ended March 31,

8 Q1 2014 Mix Year - over - Year Growth by Category • Financials, Healthcare, Retail, and Technology are our fastest growing sectors • Our top 10 clients declined to 25.5% of revenue in Q1 2014 from 28.3% a year ago, demonstrating the ongoing diversification of the business (largest <5%) FIRST QUARTER REVENUE BY CLIENT INDUSTRY Note: Actuals may not foot due to rounding Q1 2014 Above 10% Financials, Healthcare, Retail 0% to 10% Technology, Auto, Consumer Products Below 0% Communications, Other

9 ORGANIC GROWTH HIGHLIGHTS SUSTAINED MARKET SHARE GAINS Note: Peers include Omnicom, IPG, WPP, Havas and Publicis . WPP and Havas have not yet reported 1Q 2014 results and therefore are not included in the peer aggregate for the most recent quarter.

10 Note: Actuals may not foot due to rounding • We remain focused on optimizing profitability in addition to benefitting from our highest margin businesses delivering above average growth SUMMARY OF SEGMENT RESULTS - EBITDA (US$ in millions, except percentages) 2014 2013 EBITDA Strategic Marketing Services 35.4$ 30.2$ 17.1 % margin 17.2% 16.5% Performance Marketing Services 9.7 4.9 100.2 % margin 11.2% 5.9% Marketing Communications 45.1 35.1 28.7 % margin 15.4% 13.2% Corporate Expenses (8.7) (7.3) 19.1 % Profit Distributions from Affiliates 0.0 3.1 Total EBITDA 36.4$ 30.8$ 18.1 % margin 12.5% 11.6% % Change Three Months Ended March 31,

11 Note: Actuals may not foot due to rounding FREE CASH FLOW (1) Capital Expenditures, net represents capital expenditures net of landlord reimbursements . (2) Cash Interest, net & Other represents the quarterly accrual of cash interest under our Senior Notes . (3) Free Cash Flow is a non - GAAP measure. As shown above, Free Cash Flow represents EBITDA less net income attributable to non - controlling interests, less capital expenditures, less cash taxes, less net cash interest (including interest paid and other). (US$ in millions) 2014 2013 Cash Flow Used in Continuing Operating Activities ($39.2) ($31.5) Distributions 0.3 3.1 Interest Expense, net 12.6 12.3 Changes in Working Capital 48.8 47.8 Changes in Non-Current Assets & Liabilities 12.2 (1.2) Other 1.7 0.3 EBITDA $36.4 $30.8 Net Income Attibutable to Noncontrolling Interests (1.4) (1.0) Capital Expenditures, net (1) (3.0) (2.6) Cash Taxes (0.1) (0.1) Cash Interest, net & Other (2) (11.4) (11.8) Free Cash Flow (3) $20.6 $15.4 Three Months Ended March 31,

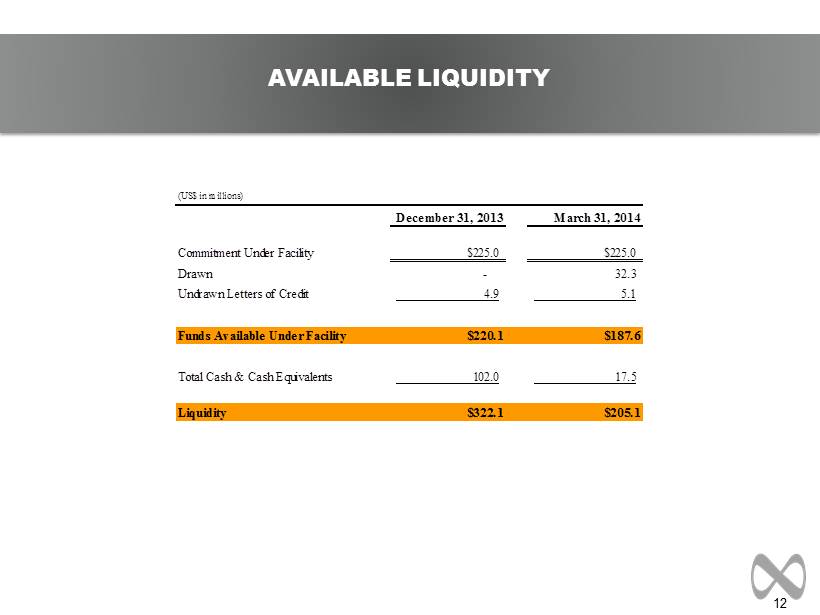

12 AVAILABLE LIQUIDITY (US$ in millions) December 31, 2013 March 31, 2014 Commitment Under Facility $225.0 $225.0 Drawn - 32.3 Undrawn Letters of Credit 4.9 5.1 Funds Available Under Facility $220.1 $187.6 Total Cash & Cash Equivalents 102.0 17.5 Liquidity $322.1 $205.1

13 • We are raising our full year outlook based on the strong start to the year and the solid momentum broadly across the portfolio by our partner firms 2014 FINANCIAL OUTLOOK Note: See appendix for definitions of non - GAAP measures Initial Revised Implied 2013 2014 2014 Year over Year Actuals Guidance Guidance Change Revenue $1.15 billion $1.230 - $1.255 billion $1.245 - $1.270 billion +8.4% to +10.5% EBITDA $159.4 million $177 - $181 million $181 - $185 million +13.5% to +16.1% Free Cash Flow $91.6 million $104 - $108 million $106 - $110 million +15.8% to +20.2% Implied EBITDA Margin 13.9% 14.4% 14.5% to 14.6% +60 to 70 basis points

14 APPENDIX

15 TEMPORAL PUT OBLIGATIONS AND IMPACT ON EBITDA Incremental (US$ in millions) Cash Stock Total EBITDA in Period 2014 1.8 0.3 2.1 1.7 2015 3.7 0.3 4.0 1.9 2016 3.7 0.4 4.1 0.1 2017 4.1 0.0 4.1 0.9 Thereafter 2.1 0.0 2.1 0.0 Total $15.4 $1.0 $16.4 $4.6 Effective Multiple 3.6x Estimated Put Impact at March 31, 2014 Payment Consideration

16 Note: Actuals may not foot due to rounding SUMMARY OF CASH FLOW Note: Actuals may not foot due to rounding (US$ in millions) 2014 2013 Cash flows used in continuing operating activities ($39.2) ($31.5) Discontinued operations (0.1) (1.5) Net cash used in operating activities ($39.3) ($33.0) Cash flows used in continuing investing activities ($44.7) ($1.0) Discontinued operations 0.0 (0.0) Net cash used in investing activities ($44.7) ($1.0) Net cash provided by (used in) continuing financing activities ($0.5) $45.1 Effect of exchange rate changes on cash and cash equivalents $0.0 ($0.1) Net increase (decrease) in cash and cash equivalents ($84.5) $11.0 Three Months Ended March 31,

17 Note: Actuals may not foot due to rounding DEFINITION OF NON - GAAP MEASURES EBITDA: EBITDA is a non - GAAP measure, that represents operating profit plus depreciation and amortization, stock - based compensation, acquisition deal costs, deferred acquisition consideration adjustments, and profit distributions from affiliates. Organic Growth: Organic revenue growth is a non - GAAP measure that refers to growth in revenues from sources other than acquisitions or foreign exchange impacts. Free Cash Flow: Free cash flow is a non - GAAP measure that represents EBITDA less net income attributable to non - controlling interests, less capital expenditures net of landlord reimbursements, less net cash interest (including interest paid and to be paid on the Senior Notes), less cash taxes plus realized cash foreign exchange gains. Net Bank Debt or Net Debt: Debt due pertaining to the revolving credit facility plus debt pertaining to the Senior Notes less total cash and cash equivalents. Note: A reconciliation of Non - GAAP to US GAAP reported results has been provided by the Company in the tables included in the earnings release issued on April 24, 2014.

MDC Partners Innovation Centre 745 Fifth Avenue, Floor 19 New York, NY 10151 646 - 429 - 1800 www.mdc - partners.com