Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - Caesars Acquisition Co | d709426d8k.htm |

Exhibit 99.1

Offering Memorandum Excerpts

FORWARD LOOKING STATEMENTS

This offering memorandum contains “forward-looking statements” intended to qualify for the safe harbor from liability established by the Private Securities Litigation Reform Act of 1995. These statements can be identified by the fact that they do not relate strictly to historical or current facts. We have based these forward-looking statements on our current expectations about future events. Further, statements that include words such as “may,” “will,” “project,” “might,” “expect,” “believe,” “anticipate,” “intend,” “could,” “would,” “estimate,” “continue,” or “pursue,” or the negative of these words or other words or expressions of similar meaning may identify forward-looking statements. These forward-looking statements are found at various places throughout this offering memorandum. These forward-looking statements, including, without limitation, those relating to future actions, new projects, strategies, future performance, the outcome of contingencies such as legal proceedings, and future financial results, wherever they occur in this offering memorandum, are necessarily estimates reflecting the best judgment of our management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. These forward-looking statements should, therefore, be considered in light of various important factors set forth above and in this offering memorandum.

In addition to the risk factors set forth above, important factors that could cause actual results to differ materially from estimates or projections contained in the forward-looking statements include without limitation:

| • | our ability to satisfy the conditions to releasing the proceeds of this offering from escrow, if applicable; |

| • | the impact of our substantial indebtedness and the restrictions in our debt agreements upon the consummation of the Transactions; |

| • | our dependence on CEOC and its subsidiaries for services pursuant to the CGP Management Services Agreement (as defined below), services pursuant to the Property Management Agreements (as defined below), access to intellectual property rights, the Total Rewards® loyalty program, its customer database and other services, rights and information; |

| • | the effects of a default by Caesars Entertainment and its subsidiaries, including CEOC, on certain debt obligations; |

| • | our ability to use Caesars Entertainment’s customer-tracking, customer loyalty and yield-management programs to continue to increase customer loyalty and same-store or hotel sales; |

| • | our dependence on the management of Caesars Entertainment and Caesars Acquisition Company (“CAC”), the managers of our properties and, upon its implementation, Services, LLC (as defined below); |

| • | the adverse effects if Caesars Entertainment or any of its subsidiaries, including CEOC, were to file for bankruptcy; |

| • | the implementation of Services, LLC is subject to regulatory and other approvals, which may be delayed or which we may not receive; |

| • | the effects of competition, including locations of competitors, competition for new licenses and operating and market competition; |

| • | construction factors, including delays, increased costs of labor and materials, availability of labor and materials, zoning issues, environmental restrictions, soil and water conditions, weather and other hazards, site access matters, and building permit issues, including construction of The Cromwell (f/k/a Bill’s Gamblin’ Hall & Saloon) and the renovation of The Quad Resort & Casino (“The Quad”); |

| • | reductions in consumer discretionary spending due to economic downturns or other factors; |

| • | our ability to realize any or all of our adjustments to Adjusted EBITDAM—Pro Forma or our other projections included in this offering memorandum; |

| • | our ability to realize the benefits of development projects if not completed in the timeframes or in the manner contemplated herein; |

| • | our ability to retain our performers or other entertainment offerings on acceptable terms or at all; |

| • | litigation outcomes and judicial and governmental body actions, including gaming legislative action, referenda, regulatory disciplinary actions, fines and taxation and the threatened litigation described in “Summary—Recent Developments—Letter From CEOC Second Lien Noteholders” and “—Letter From Holders of CEOC First Lien Debt”; |

| • | the dependence of certain of the Properties (as defined below) on the success of third parties; |

| • | changes in the extensive governmental regulations to which we are subject, and changes in laws, including increased tax rates, smoking bans, gaming regulations or accounting standards, third-party relations and approvals, and decisions, disciplines and fines of courts, regulators and governmental bodies; |

| • | our or Growth Partners’ ability to access additional capital on acceptable terms or at all; |

| • | any impairments to goodwill, indefinite-lived intangible assets, or long-lived assets that we may incur; |

| • | acts of war or terrorist incidents, severe weather conditions, uprisings or natural disasters, including losses therefrom, including losses in revenues and damage to property, and the impact of severe weather conditions on our ability to attract customers to certain of our facilities; |

| • | fluctuations in energy prices; |

| • | work stoppages and other labor problems; |

| • | the impact, if any, of unfunded pension benefits under multi-employer pension plans; |

| • | our ability to recover on credit extended to our customers; |

| • | differences in our interests and those of our Sponsors (as defined below); |

| • | damage caused to our brands due to the unauthorized use of our brand names by third parties; |

| • | the failure of Caesars Entertainment to protect the trademarks that are licensed to us; |

| • | abnormal gaming holds (“gaming hold” is the amount of money that is retained by the casino from wagers by customers); |

| • | our exposure to environmental liability, including as a result of unknown environmental contamination; |

| • | our ability to recoup costs of capital investments through higher revenues; |

| • | access to insurance on reasonable terms for our assets; |

| • | the effects of compromises to our information systems or unauthorized access to confidential information or our customers’ personal information; and |

| • | the other factors set forth under “Risk Factors.” |

You are cautioned to not place undue reliance on these forward-looking statements, which speak only as of the date of this offering memorandum. We undertake no obligation to publicly update or release any revisions to these forward-looking statements to reflect events or circumstances after the date of this offering memorandum or to reflect the occurrence of unanticipated events, except as required by law.

SUMMARY

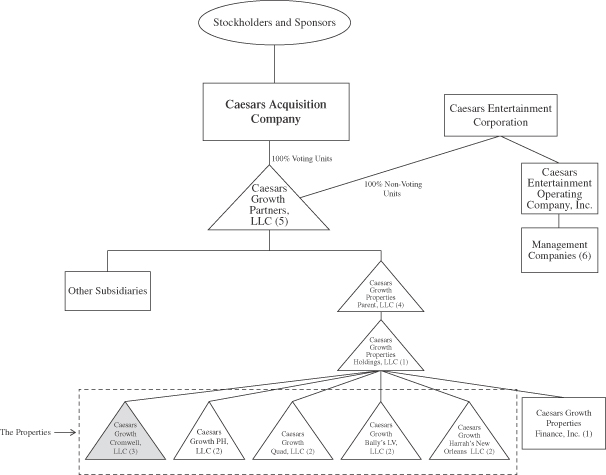

The following summary contains information about the Issuers, Growth Partners, Caesars Entertainment and its subsidiaries and the Notes. It does not contain all of the information that may be important to you in making a decision to participate in the offering. For a more complete understanding of the Issuers, Growth Partners and the Notes, we urge you to read this offering memorandum carefully, including the sections entitled “Risk Factors,” “Forward Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business” and the combined financial statements and related notes thereto included elsewhere in this offering memorandum. Unless otherwise noted or indicated by the context, the term “Growth Partners” refers to Caesars Growth Partners, LLC, and “we,” “us” and “our” refer to the Company and its consolidated subsidiaries, including the Properties (as defined below) on a combined basis after giving effect to the Transactions (as defined below under “—Recent Developments—The Transactions”).

In connection with this offering, the Company will acquire four casinos from CEOC (the “Purchased Properties”). Concurrently with the acquisition of the Purchased Properties, Growth Partners will contribute the entity that owns the assets comprising the Planet Hollywood Resort & Casino (together with the Purchased Properties, the “Properties”) to the Company. See “—Recent Developments—The Transactions.” Unless otherwise specified, all financial information provided in this offering memorandum gives pro forma effect to the closing of the Transactions.

Upon the consummation of the Acquisition (as defined below under “—Recent Developments—The Transactions”), the Company and its subsidiaries will collectively own the Properties. Caesars Entertainment manages the Properties as well as those properties held by Caesars Entertainment’s subsidiaries as one company, but the Company will not be entitled to receive any direct contribution or proceeds from the operations of Caesars Entertainment or its subsidiaries. None of Growth Partners, Growth Partners’ parent CAC, Caesars Entertainment or CEOC will guarantee the Notes.

Our Business

We are a newly created, wholly owned subsidiary of Growth Partners, a leading gaming and entertainment company focused on acquiring and developing a portfolio of high-growth operating assets in the gaming and interactive entertainment industries. Growth Partners’ current assets include its subsidiary Caesars Interactive Entertainment, Inc. (“Caesars Interactive”) (the businesses of which include social and mobile games, the World Series of Poker brand and regulated online real money gaming) and two casino properties: Planet Hollywood Resort & Casino (“Planet Hollywood”) and a 41% stake in the Horseshoe Baltimore Casino (currently under development). Concurrently with the acquisition of the Purchased Properties, Growth Partners will contribute to the Company the entity that owns the assets comprising Planet Hollywood. CEOC, a wholly owned subsidiary of Caesars Entertainment, manages the Properties through its subsidiaries. Accordingly, CEOC provides Growth Partners with access to Caesars Entertainment’s proven management expertise, brand equity, Total Rewards® loyalty program and structural synergies.

The Properties consist of four leading casino resort properties located in the heart of the attractive Las Vegas market and the only land-based casino in New Orleans, Louisiana. Initially, each of the Properties will be managed by subsidiaries of CEOC. See “Certain Relationships and Related Party Transactions.”

As part of the Transactions (as defined below), Growth Partners will contribute to us:

| • | Planet Hollywood Resort & Casino: a 2,496-room hotel and casino featuring 1,102 slot machines and 91 table games, 17 restaurants and bars, 86,833 square feet of meeting space and The AXIS, a 7,000-seat theater with high definition LED walls and a state-of-the-art sound system. |

Also as part of the Transactions, we will purchase from CEOC the Purchased Properties, which will strengthen our portfolio and expand our product offering and include:

| • | Bally’s Las Vegas Resort and Casino: a 2,814-room hotel and casino featuring 1,002 slot machines and 67 table games, 12 restaurants and bars, and 167,521 square feet of meeting space; |

| • | The Quad Resort and Casino: a 2,545-room hotel and casino featuring 772 slot machines and 68 table games, 13 restaurants and bars, and 49,647 square feet of meeting space (which includes O’Shea’s, leased by The Quad from an affiliate of Caesars Entertainment); |

| • | The Cromwell (formerly known as Bill’s Gamblin’ Hall & Saloon): currently undergoing renovations and when complete, which we expect will occur in the second quarter of 2014, will have 188 luxury hotel rooms and a new 65,000 square foot nightclub/poolclub operated by Victor Drai located on the roof of the property; and |

| • | Harrah’s New Orleans: a 450-room hotel and casino featuring 1,820 slot machines, 142 table games, 9 restaurants and bars, and 7,000 square feet of meeting space. |

As of December 31, 2013, the Properties had an aggregate of 340,423 square feet of gaming space, 8,493 hotel rooms, 5,120 slots, 423 gaming tables, 297,625 square feet of meeting space and 53 restaurants and bars. Corner Investment Company, LLC (“Corner Investment”), a wholly owned subsidiary of the Company that owns The Cromwell, will be a qualified non-recourse subsidiary of the Company. Accordingly, it will not guarantee the Notes, and its assets, including The Cromwell, will not be pledged as collateral for the Notes. Corner Investment will effectively be subject to limited covenants under the indenture governing the Notes and the Senior Secured Credit Facilities.

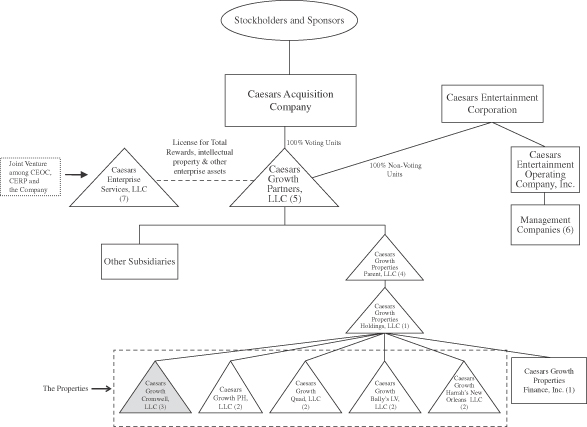

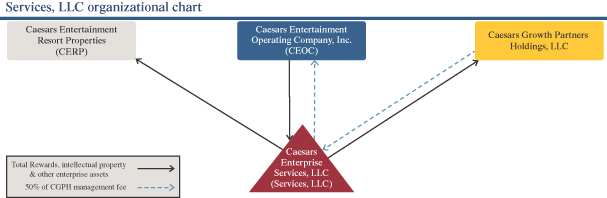

Subject to the receipt of required regulatory approvals, pursuant to the terms of the Transaction Agreement (as defined below), Caesars Entertainment Services, LLC (“Services, LLC”), a new services joint venture among CEOC, Caesars Entertainment Resort Properties LLC (“CERP”), a wholly owned subsidiary of Caesars Entertainment, and the Company, will manage both the intellectual property for the Caesars Entertainment enterprise (including for the Total Rewards system) and certain shared services operations across the portfolio of CEOC, CERP, Growth Partners and our properties. Following the implementation of Services, LLC, Services, LLC will license the intellectual property it manages to, among others, each of the owners of the Purchased Properties, and will also perform the obligations of the Property Managers (as defined herein) at each Property. The parties to the Transaction Agreement have agreed to use reasonable best efforts to establish Services, LLC, the implementation of which, including all the terms and conditions set forth herein, is subject to the review and approval of the special committees of CAC and Caesars Entertainment as well as regulatory approvals. We intend to file for all required regulatory approvals as soon as practicable. There can be no assurance, however, that the implementation of Services, LLC will be completed. See “Certain Relationships and Related Party Transactions—Services Joint Venture.”

We participate in Caesars Entertainment’s industry-leading customer loyalty program, Total Rewards®, which, as of December 31, 2013, had approximately 45 million members, including approximately 7.6 million active players. Caesars Entertainment is the world’s most diversified casino-entertainment provider and the most geographically diverse U.S. casino entertainment company. We use the Total Rewards® system to market promotions and to generate customer play within our properties. We additionally benefit from our access to Caesars Entertainment’s centralized reservation and convention booking systems, which allows us to leverage Caesars Entertainment’s marketing, brand and relationships. See “Certain Relationships and Related Party Transactions.”

For the year ended December 31, 2013, we derived approximately 55.3% of our gross revenues from gaming sources and approximately 44.7% from other sources, such as sales of lodging, food, beverages and entertainment. In future periods, we expect to derive additional revenue from non-gaming sources, such as new

restaurants and entertainment offerings we are currently developing at certain of the Properties. For the year ended December 31, 2013, we generated net revenues of $1,038.9 million and, pro forma for the Transactions, net loss of $26.2 million and Adjusted EBITDA of $237.7 million. See “—Summary Historical and Pro Forma Financial Information and Other Financial Data” for definitions of EBITDA and Adjusted EBITDA and reconciliations of these non-GAAP measures to net income.

Our Business and Properties

Set forth below is certain information as of December 31, 2013 concerning the Properties, each of which is more fully described following the table.

| Casino Floor Sq. Footage |

Hotel Rooms and Suites |

Slots | Gaming Tables | Meeting Space Sq. Footage |

Restaurant & Bars |

|||||||||||||||||||

| Planet Hollywood |

64,470 | 2,496 | 1,102 | 91 | 86,833 | 17 | ||||||||||||||||||

| Bally’s Las Vegas |

66,187 | 2,814 | 1,002 | 67 | 167,521 | 12 | ||||||||||||||||||

| The Quad(1) |

49,647 | 2,545 | 772 | 68 | 36,271 | 13 | ||||||||||||||||||

| The Cromwell(2) |

40,000 | 188 | 440 | 66 | — | 4 | ||||||||||||||||||

| Harrah’s New Orleans |

125,119 | 450 | 1,820 | 142 | 7,000 | 9 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

340,423 | 8,493 | 5,120 | 423 | 297,625 | 53 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (1) | Includes O’Shea’s, which is leased by an affiliate of Caesars Entertainment to The Quad. |

| (2) | Bill’s Gamblin’ Hall & Saloon is currently closed and undergoing renovations to become The Cromwell. The information provided reflects our current anticipated specifications for The Cromwell. Corner Investment, a wholly owned subsidiary of the Company that owns The Cromwell, will be a qualified non-recourse subsidiary of the Company. Accordingly, it will not guarantee the Notes and its assets, including The Cromwell, will not be pledged as collateral for the Notes. Corner Investment will effectively be subject to limited covenants under the indenture governing the Notes and the Senior Secured Credit Facilities. |

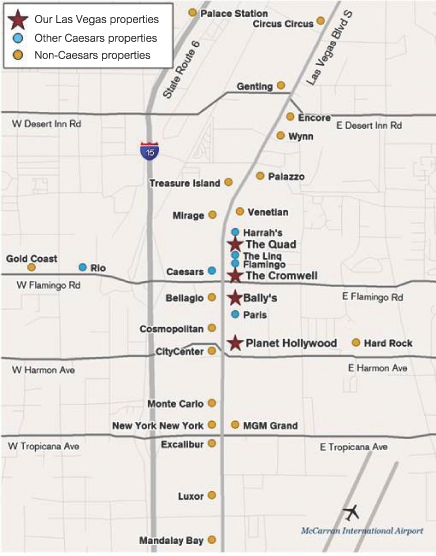

Las Vegas Properties

The Las Vegas market has shown signs of recovery since the visitation and spend declines in 2008 and 2009. Las Vegas visitation reached a near-record high of approximately 40 million people in 2013, and Las Vegas Strip gaming revenues for the year ended December 31, 2013 were approximately 17% higher than in 2009. Additionally, recent trends have reflected a growth in customer demand for non-gaming offerings. According to the Las Vegas Convention and Visitors Authority (“LVCVA”), approximately 47% of Las Vegas visitors in 2012 indicated that their primary reason to visit was for vacation or pleasure as opposed to solely for gambling as the main attraction, up from 39% of visitors in 2008.

We believe that our portfolio of assets is well positioned to capitalize on these trends. In 2013, approximately 68% of our gross revenues was derived from our properties located in Las Vegas and approximately 46% of our Las Vegas gross revenues was generated from non-gaming offerings. These amounts do not include expected revenues from The Cromwell, which is expected to open in the second quarter of 2014 or The Quad once its full renovation is complete during the first half of 2015. On a pro forma basis to include projected revenues from The Cromwell, which will not be pledged as collateral for the Notes and will be subject on a limited basis to the restrictive covenants in the indenture governing the Notes, and The Quad post-renovation, approximately 74% of our gross revenues in 2013 would have been derived from our Properties located in Las Vegas and approximately 57% of our gross revenues at our Las Vegas properties in 2013 would have been generated from our non-gaming offerings. See “—Recent Developments—Estimated Impact of Project Completions,” “—Summary Historical and Pro Forma Financial Information and Other Financial Data” and “Risk Factors—Risks Related to Our Business—We may not realize any or all of our projected increases to Adjusted EBITDA or other projections included in this offering memorandum.”

Our Las Vegas properties are all strategically located in the heart of Las Vegas right at the center of the Las Vegas Strip, near or adjacent to each other. In addition, Caesars Entertainment has invested to date approximately $533 million in the Linq, an open-air dining, entertainment and retail development on the east side of the Las Vegas Strip adjacent to The Quad and nearby to our other Las Vegas properties. The Linq will feature over 25 new retail, dining and entertainment offerings as well as the world’s tallest observation wheel, named the “High Roller,” which is 550 feet tall and opened March 31, 2014. The Linq recently opened the first phase of its development in December 2013 and is scheduled to be fully developed in the second quarter of 2014. Our nearby Las Vegas Strip properties should benefit from the investments in, and the visitation to, this new development. Further, all of our Las Vegas properties benefit from their prime location in the attractive Las Vegas market and from their close proximity to other casino properties owned by Caesars Entertainment, with which they share certain services and costs.

Map of Our Las Vegas Properties

Planet Hollywood Resort & Casino is a leading Hollywood-themed resort, casino and entertainment facility originally constructed in 2001, renovated in 2007 and acquired by Caesars Entertainment in 2010, then subsequently acquired by Growth Partners in 2013. Strategically located in the center of the Strip on Las Vegas Boulevard, the property features 17 bars and restaurants, a world-class entertainment facility, a salon and spa, and 86,833 square feet of conference and meeting space. In addition, the facility adjoins to a retail mall, the Miracle Mile Shops, with 170 retailers and 15 restaurants, and a 1,201 room timeshare tower operated by Hilton Grand Vacations, neither of which are owned by the Company or its subsidiaries. The adjoining mall and timeshare tower, as well as the amenities featured at Planet Hollywood, drive additional traffic through the Planet Hollywood complex. Additionally, Planet Hollywood receives a fee from Hilton Grand Vacations for timeshare units, approximately 33% of which had been sold as of December 31, 2013. The property has recently completed several renovations, including a remodel of Gordon Ramsay’s BURGR restaurant and a renovation of the PH Live theater into The AXIS, a 7,000-seat theater with high definition LED walls and a state-of-the-art sound system. Planet Hollywood is also home to Britney Spears’ new popular show, Britney: Piece of Me, which premiered in December 2013 and will feature 96 performances through 2015.

Planet Hollywood is one of our premium product offerings, benefitting from its prime location on a 35-acre site on the east side of the Las Vegas Strip as part of a contiguous strip of casinos owned and operated by Caesars Entertainment or its subsidiaries. Planet Hollywood targets a growing younger demographic that values the offerings of the non-gaming entertainment that complements the casino’s gaming activities. The property is able to elevate its guests’ experience by offering premium, Hollywood-themed entertainment and non-gaming options that remain fresh and relevant. This combination resulted in an all-time record high EBITDAM (which equals EBITDA plus management fees paid by the property) at the property since its 2010 acquisition by Caesars Entertainment of approximately $108 million in 2013, an increase of nearly four times compared to 2009 EBITDAM. We attribute this substantial growth to the introduction of the Total Rewards® loyalty program, management / operational expertise and structural synergies. For the year ended December 31, 2013, Planet Hollywood had approximately 79% cash room nights, 53% VIP rated play and 58% non-gaming revenue.

Bally’s Las Vegas Resort and Casino opened in 1973 and is located on the famous Four Corners of the Las Vegas Strip, adjacent to The Cromwell and nearby to the Linq. The property’s 43-acre site features 12 restaurants, including a new BLT Steak restaurant expected to open in May 2014, an Olympic-sized pool, a spa and salon, retail shopping and 167,521 square feet of conference and meeting space in a conference facility shared with Paris Las Vegas. In December 2013, the property completed the renovation to its 756-room south hotel tower, which has been rebranded as the Jubilee Tower. As a result of the renovation, the Average Daily Room Rate (“ADR”) per room for the renovated rooms has increased by approximately $40, and we expect revenue and EBITDA at the property will also increase as a result of anticipated increases in increased gaming play related to the increased ADR, particularly in the convention and meeting segment. See “Risk Factors—Risks Related to Our Business—We may not realize any or all of our projected increases to Adjusted EBITDA or other projections included in this offering memorandum.” The Grand Bazaar, which is not owned by the Company or its subsidiaries, is also expected to open in late 2014, and will make use of the currently under-utilized Strip-front space directly in front of Bally’s Las Vegas. The Grand Bazaar will consist of a new outdoor retail and dining complex, which we expect will drive additional visitation to the property. The Grand Bazaar is being developed by a third party, which will lease the space from Bally’s in exchange for an annual lease payment of $3 million for the first year of the lease, $4 million in for the second year and $5 million in years three to five. Bally’s Las Vegas is home to the popular show Jubilee!, which is the longest currently running show in the history of Las Vegas. Other entertainment offerings include: Tony N’ Tina’s Wedding, LA Comedy Club and The Rocky Horror Picture Show.

Bally’s Las Vegas benefits from its large convention business, which it shares with Paris Las Vegas, and strong customer loyalty cultivated over the past 30 years. Bally’s Las Vegas, having 167,521 square feet of conference and meeting space, combined with Paris Las Vegas, having approximately 140,000 square feet of

conference and meeting space, is the largest conference and meeting facility within Caesars Entertainment’s network of properties and, as a result, Bally’s Las Vegas has one of the highest percentage of convention room nights among the Caesars Entertainment network of properties, at approximately 13%. This large meeting space can accommodate conventions of up to 10,000 guests, driving increased visitation to the property. Additionally, Bally’s Las Vegas’s dedicated customer base drives a high mix of casino gaming customers to the property. For the year ended December 31, 2013, Bally’s Las Vegas had approximately 73% cash room nights, 29% VIP rated play and 56% non-gaming revenue.

The Quad Resort and Casino is ideally located on the Las Vegas Strip, adjacent to the Linq and nearby to The Cromwell. Formerly known as the Imperial Palace, The Quad was re-named in 2012 as part of an initial $90 million renovation to upgrade the complex concurrently with the development of the Linq. The Quad is currently undergoing a second renovation, which we expect will cost approximately $223 million and be finished during the first half of 2015. Once these renovations have been completed, the property will feature contemporary guest rooms, 12 bars and restaurants, including the popular Hash House A Go Go and Guy Fieri’s first Las Vegas restaurant, an upgraded pool, salon and spa, and 40,000 square feet of conference and meeting space. The Quad also features distinctive entertainment offerings including Divas Las Vegas, Recycled Percussion and the Jeff Civillico Comedy Show. Recent results of operations at The Quad have been hindered by its ongoing renovations and the construction disruption of the adjacent Linq.

The large-scale renovation will transform The Quad to a product targeting younger guests, trend seekers and trend setters. The property, along with the adjacent Linq entertainment complex, is designed to appeal to the growing number of visitors to the Las Vegas region under the age of 40, which increased from approximately 28% in 2009 to 42% in 2013. Additionally, the property is ideally located off of the east side of the Strip. We expect that this prime location, combined with the large-scale renovation, will drive increased visitation to the property and attract more affluent casino gaming customers. The property is expected to further benefit from additional visitation once the adjacent Linq development is complete and fully developed in the second quarter of 2014. For the year ended December 31, 2013, The Quad had approximately 84% cash room nights, 19% VIP rated play and 58% non-gaming revenue.

The Cromwell (formerly known as Bill’s Gamblin’ Hall & Saloon) is currently closed and undergoing an estimated $235 million renovation to become a boutique “lifestyle” hotel and casino located in the heart of the Las Vegas Strip, offering a new, sophisticated Las Vegas experience that is intended to fill a gap in the market for an upscale, boutique “lifestyle” hotel. Scheduled to open in the second quarter of 2014, The Cromwell will feature 188 luxury hotel rooms, 4 restaurants and bars and a one-of-a-kind 65,000 square foot rooftop indoor / outdoor poolclub / nightclub with unparalleled views of the Las Vegas Strip and the Fountains, which is being developed with nightclub developer Victor Drai. The Cromwell is also working with Giada De Laurentiis to develop a 12,000 square foot restaurant with sweeping views of the Las Vegas Strip. Corner Investment, a wholly owned subsidiary of the Company that owns The Cromwell, will be a qualified non-recourse subsidiary of the Company. Accordingly, it will not guarantee the Notes and its assets, including The Cromwell, will not be pledged as collateral for the Notes. Corner Investment will effectively be subject to limited covenants under the indenture governing the Notes and the Senior Secured Credit Facilities.

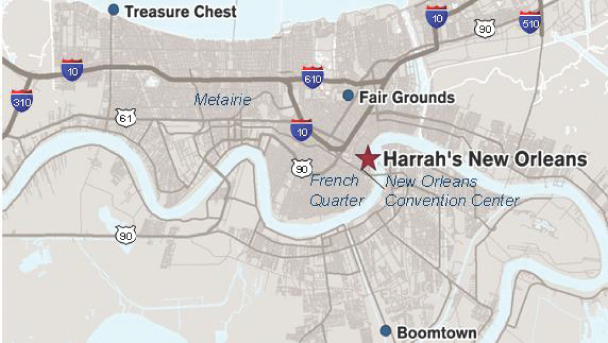

New Orleans Property

Map of Our New Orleans Property

Harrah’s New Orleans opened in 1999 and fully renovated in 2006, and is a French-themed resort and casino in the popular destination market of New Orleans, Louisiana. Located only blocks from the popular French Quarter, the Mississippi Riverfront and convention center in New Orleans, Harrah’s New Orleans is ideally situated to attract both hotel guests and casino gaming customers from the large visitation to the area. Additionally, Harrah’s New Orleans is the only land-based casino in the market and enjoys an approximately 55% share of the New Orleans gaming market based on 2013 gaming gross wins. The property features 450 rooms and suites and nine restaurants and bars (including the popular Ruth’s Chris Steakhouse, Besh Steak and Acme Oyster House), as well as the 5,100 square foot Masquerade nightclub. In addition, the Fulton Street Promenade, a pedestrian promenade featuring dining and outdoor concerts, lies just outside the Harrah’s New Orleans and is available for outdoor functions.

Harrah’s New Orleans benefits from its prime location in an increasingly popular destination market, as visitation to New Orleans reached a ten-year high of 9 million in 2012 (according to the New Orleans Convention and Visitors Bureau). Harrah’s New Orleans has capitalized on this trend, as the property generated over 50% of its gaming revenue in both 2012 and 2013 from visitors to the area compared to local residents. The property also has a distinct competitive advantage as the only land-based casino in the market. Harrah’s New Orleans also benefits from the current positive economic conditions in the area: since 2007, the population in New Orleans has grown approximately 28%, and the city was ranked fastest growing city by Forbes Magazine in June 2013. Additionally, there has been significant capital investment in the city, including the new GE Capital Technology Center, the new University Medical Center and the new VA Medical Center, which is expected to increase employment in New Orleans by providing higher paying jobs. For the year ended December 31, 2013, Harrah’s New Orleans had approximately 24% cash room nights, 57% VIP rated play and 22% non-gaming revenue.

Our Competitive Strengths

We attribute our operating success and the historical strong performance of our properties to the following key strengths that differentiate us from our competition:

Las Vegas concentration and irreplaceable center-Strip location. Our Las Vegas properties are located on the Las Vegas Strip in the heart of the attractive Las Vegas market, and our Las Vegas properties provided approximately 69% of our EBITDAM for 2013. The Las Vegas market is one of most visited casino resort destinations in the world and attracted a near-record level of approximately 40 million people in 2013. Additionally, Las Vegas Strip gaming revenue growth for 2013 outperformed several other U.S. major metro markets. We believe we are well positioned to continue to benefit from our significant exposure to the strong Las Vegas market.

Large, singular casino resort property in the attractive New Orleans market. Located in the center of the city, Harrah’s New Orleans is the only land-based casino in Louisiana, and New Orleans is a popular destination market that has shown increasing visitation trends and improving economic conditions. Visitation to the city grew to approximately 9 million in 2012, the highest in nearly ten years. Harrah’s New Orleans has capitalized on this trend, as the property generated over 50% of its gaming revenue in both 2012 and 2013 from visitors to the area compared to local residents. The property also benefits from the current positive economic conditions in New Orleans: since 2007, the population in New Orleans has grown approximately 28%, and the city is ranked fastest growing city by Forbes Magazine.

Well-known, large entertainment facilities generating significant revenue and free cash flow. We own large-scale casinos that bear some of the most highly recognized brand names in the gaming industry, including Harrah’s, Bally’s and Planet Hollywood. These brands have strong identities and enjoy widespread customer recognition. We believe the locations of our casino properties offer distinct advantages. Our Las Vegas properties are located on the Las Vegas Strip and several sit among a contiguous strip of casinos owned by Caesars Entertainment or its subsidiaries. In addition, Harrah’s New Orleans is located in the center of New Orleans, near the French Quarter and the Convention Center and only a few blocks from the Superdome. We believe our properties’ prime locations, adjoining facilities and accessibility enables them to attract a significant customer base and continue to capture growth in market share. All of our operating casinos have a successful track record of generating strong stable revenue and free cash flow.

Strong non-gaming presence to capitalize on trends in Las Vegas. LVCVA reports have shown that Las Vegas visitors have become more interested in the non-gaming offerings in Las Vegas, with 47% indicating that their primary purpose for visiting in 2012 was vacation or pleasure as opposed to for gambling, up from 39% in 2008. We currently have a strong presence in non-gaming offerings, with approximately 46% of our revenue from our Las Vegas properties in 2013 generated from non-gaming sources. Additionally, the newly renovated Quad and The Cromwell will feature a distinctive mix of lifestyle dining, retail and entertainment offerings to appeal to the region’s growing clientele under the age of 40, which increased from approximately 28% in 2009 to 42% in 2013.

Close proximity to new large developments in Las Vegas, driving increased visitation to our Las Vegas properties. Our Las Vegas properties are located near or adjacent to several new large developments in Las Vegas: The Quad renovation, The Cromwell, the Grand Bazaar and the Linq (which is owned by Caesars Entertainment), all of which we believe will drive increased visitation to our properties due to increased foot traffic and the presence of additional visitors in the vicinity of our properties. We anticipate that the extensive Quad renovation, expected to be complete during the first half of 2015, will drive increased visitation to The Quad, which currently has some of the lowest occupancy and ADR levels relative to other similarly located Las Vegas properties. In addition, our newly redeveloped luxury boutique hotel, The Cromwell, is currently

undergoing an estimated $235 million refurbishment at the famous Four Corners of the Las Vegas Strip and is expected to open in 2014. It will feature 188 luxury hotel rooms and a 65,000 square foot indoor/outdoor nightclub/poolclub. Caesars Entertainment has also invested over $533 million to date in the Linq, an open-air dining, entertainment and retail development that features the “High Roller” observation wheel. The Linq began opening in phases in December 2013, and is scheduled to be fully developed in the second quarter of 2014.

Well positioned for continued recovery in Las Vegas. Between 1970 and 2007, Las Vegas overall visitation grew at a 5% compound annual growth rate. Despite declines in 2008 and 2009 due to a broad macroeconomic slowdown, overall visitation continued to increase from 2009 through 2013. By 2013, total visitation to Las Vegas returned to all-time highs of approximately 40 million people. The average Las Vegas hotel ADR per room has also showed signs of improvement, but still remains significantly below its peak in 2007. Las Vegas Strip gaming revenues for the year ended December 31, 2013 were almost 5% higher than in 2012, but still remain approximately $324 million, or 4.8%, below peak levels in 2007. We believe we are well positioned to benefit if the recovery in Las Vegas continues, as our Las Vegas properties provided approximately 69% of our EBITDAM for 2013. See “—Summary Historical and Pro Forma Financial Information and Other Financial Data” for a definition of Adjusted EBITDAM—Pro Forma and a reconciliation to net income.

Access to leading casino brands, a global network of casinos, a leading innovator in the gaming industry and the Total Rewards® loyalty program. Caesars Entertainment is the world’s most diversified casino entertainment provider and the most geographically diverse U.S. casino entertainment company. As of December 31, 2013, Caesars Entertainment owned, operated or managed 52 casinos (including the Properties) that bear many of the most recognized brand names in the gaming industry. Pursuant to the Property Management Agreements (as defined herein), we have access to and utilize Caesars Entertainment’s scale and market leading position, in combination with its proprietary marketing technology and customer loyalty programs, to foster revenue growth and encourage repeat business. The close proximity of our properties in Las Vegas to other casino properties owned and operated by Caesars Entertainment and its subsidiaries allows us to leverage the Caesars brands to attract customers to our casinos and resorts. Caesars Entertainment, led by an experienced management team that includes Gary Loveman, also has a proven record of innovation, including revolutionizing our industry’s approach to marketing with the introduction of the Total Rewards® loyalty program in 1997, which is currently accepted at 38 casinos in North America.

We also have access to the Total Rewards® loyalty program, which is considered to be one of the leading loyalty rewards programs in the casino entertainment industry. For example, for the year ended December 31, 2013, Caesars Entertainment had an estimated 19% and 27% fair share premium in its destination and regional markets, respectively versus competitors. The Total Rewards® loyalty program rewards customers for their brand loyalty and incentivizes them to seek out Caesars Entertainment’s brands and is connected to the Total Rewards Marketplace, comprised of 38 casinos, 450 online retailers and over 2,000 stores as of December 31, 2013. Total Rewards® has also been successful in improving win per position. To support the Total Rewards® loyalty program, Caesars Entertainment created the Winner’s Information Network, or WINet, the industry’s first sophisticated nationwide customer database. In combination, these systems supported the first technology-based customer relationship management strategy implemented in the gaming industry and have enabled Caesars Entertainment’s management teams to enhance overall operating results at our properties. We also benefit from the Total Rewards® loyalty program through its marketing and technological capabilities in combination with Caesars Entertainment’s nationwide casino network. We believe that the Total Rewards® loyalty program, along with other marketing tools, provides us with a significant competitive advantage that enables us to efficiently market our products to a large and recurring customer base.

Access to a well-capitalized parent with access to liquidity. Our parent company, Growth Partners, had approximately $387 million of cash on hand as of December 31, 2013, on a pro forma basis after giving effect to the Transactions, and its parent, CAC, as of April 8, 2014, had a market capitalization of approximately

$1.8 billion, implying an equity value of Growth Partners of approximately $4.3 billion. We believe that Growth Partners’ capital structure will provide it with greater access to the equity and debt markets for additional liquidity, which could allow it to capitalize on new growth opportunities and quickly invest in new casino projects in new and expanding markets. In addition, Growth Partners currently owns a portfolio of debt investments, which could provide an additional source of future liquidity.

Our Business Strategy

Continue to invest in new non-gaming offerings in Las Vegas to drive visitation and profitability. Trends in Las Vegas have shown that non-gaming offerings are becoming increasingly important to visitors and that Las Vegas is attracting a younger demographic. We expect this trend to continue and have been investing in new food and beverage offerings as well as other non-gaming amenities to drive increased visitation and profitability. New restaurants being developed at the Properties include Giada de Laurentiis’ first restaurant at The Cromwell and BLT Steak at Bally’s Las Vegas. New entertainment offerings will include The Cromwell’s 65,000 square foot nightclub/poolclub located on the roof of the property and managed by Victor Drai, which we expect will open in the second quarter of 2014. We derived approximately 55.3% of our gross revenues from gaming sources and approximately 44.7% from non-gaming sources, such as sales of lodging, food, beverages and entertainment, for the year ended December 31, 2013.

Revitalize the east side of the Las Vegas Strip. We are focused on strategically investing in our casino properties located on the east side of the Las Vegas Strip. These projects include our renovations to The Quad in conjunction with the Linq development and our renovations to redevelop Bill’s as The Cromwell. These investments are focused on improving both gaming and non-gaming offerings, including upgrading our hotel rooms, casinos, public areas and general amenities. We plan to invest approximately $223 million to renovate The Quad in conjunction with the investment by Caesars Entertainment in the Linq, a new open-air dining, entertainment and retail development that will be located adjacent to The Quad. We expect that renovations of The Quad, which are scheduled to be completed during the first half of 2015, will enhance the resort and casino’s current offerings and capitalize on increased visitation at the Linq and the High Roller. Caesars Entertainment has also invested approximately $235 million to renovate Bill’s and transform it into The Cromwell, a luxury boutique hotel with new entertainment and dining options.

Capitalize on our prime location in New Orleans, a popular destination market. Harrah’s New Orleans is located in the heart of New Orleans, a popular tourist destination that hosts large-scale conventions and annual festivals. Our property is only blocks from large, popular tourist and entertainment venues, including the French Quarter, the Mississippi Riverfront, the Superdome and the New Orleans Convention Center. This ideal location allows us to capitalize on the increasing visitation to New Orleans, which reached a ten year high of approximately 9 million in 2012. We also plan to capitalize on the many large city-wide festivals and sporting events in New Orleans to drive additional customers to Harrah’s New Orleans. Festivals in New Orleans include the Jazz & Heritage Festival, the Voodoo Festival, The French Quarter Festival, The New Orleans Film Festival and Mardi Gras. Large sporting events have historically included the NCAA Final Four Championship, the Super Bowl and the Sugar Bowl.

Maximize our core business profitability in Las Vegas. While Las Vegas has shown signs of recovery, ADR at December 31, 2013 was 16.2%, or $21.37, below the peak in 2007 at Las Vegas Strip properties. This is in part due to an overall general decline in the gaming market and in part due to increased capacity from new casinos. The gaming business has inherently low variable costs such that positive change in revenues should drive relatively large improvements in EBITDA. An increase in ADR would drive nearly a dollar for dollar improvement in EBITDA. For example, based on two million cash room nights in our Las Vegas Strip properties in 2013, we estimate that a $20 increase in ADR on an annual basis would equate to an average improvement to annual EBITDA at our Las Vegas Strip properties of approximately $40 million. Additionally, resort fees were

introduced in March 2013 at Planet Hollywood, Bally’s Las Vegas and The Quad, and are already driving incremental EBITDA. Resort fees range from $18 to $20 per night and provide hotel customers with access to select property amenities, including fitness centers and internet access. Since the inception of the program, we believe that we have generated approximately $7.4 million in incremental EBITDA with little impact to occupancy at our Las Vegas Properties. We believe this favorable impact will increase as the program ramps to full effect and more hotel guests fall into the guidelines of the program.

Leverage Caesars Entertainment’s unique scale and proprietary loyalty programs to drive outperformance versus our competitors. We plan to continue to aggressively leverage Caesars Entertainment’s distribution platform and superior marketing and technological capabilities to generate same store gaming revenue growth and cross-market play. Our access to the industry-leading Total Rewards® loyalty program, which included over 45 million members as of December 31, 2013, improves the ability of our businesses to cross-market and cross-promote with Caesars Entertainment’s database and many of its casinos. Through this system, Caesars Entertainment promotes cross-market play and targets our efforts and marketing expenditures on areas and customer segments that generate the highest return. This relationship allows us to utilize Caesars Entertainment’s sophisticated customer database and technology systems to efficiently and effectively manage our existing customer relationships. As part of the Total Rewards®, we offer a unique value proposition to loyal players whereby they get the best service and product in their local market, and as a reward for their loyalty, they receive especially attentive and customized services when they visit our properties in Las Vegas and Louisiana. This distribution strategy is unique to Caesars Entertainment and an important source of our competitive advantage. Caesars Entertainment’s extensive historical knowledge and refined decision modeling procedures enable us to distribute best practices to ensure our marketing expenditures are being used to their utmost efficiency. Given Caesars Entertainment’s historical investments in information technology and broad geographic footprint, we believe we have a competitive advantage in stimulating customer demand.

Pursue opportunistic investment in high-return projects. We plan to pursue opportunistic investments to improve our portfolio of Properties. Utilizing our strategic and market expertise and our relationship with Caesars Entertainment, we will identify key projects that generate a high return and improve our offerings and competitive position as compared to our peers. A recent example of this includes our recently completed $90 million renovation of The Quad, as well as our plan to invest an additional $223 million in further renovations of The Quad. In addition, in December 2013, we completed the renovation to the Bally’s Las Vegas south hotel tower, known as the Jubilee Tower, which has increased the ADR per room at Bally’s Las Vegas by approximately $40. We also recently completed the renovation of the PH Live theater into The AXIS, a 7,000-seat theater at Planet Hollywood that is home to Britney Spears’ new show through 2015.

Continued focus on differentiated customer service as a competitive advantage. Caesars Entertainment concentrates intensely on measuring and continuously improving customer service. Customer service surveys are collected weekly from guests, allowing us to pinpoint customer feedback on over 35 attributes/functional areas. Each customer service department is required to develop and implement plans to improve its individual service scores. Management bonuses, as well as individual performance evaluations, are partially dependent on achieving measured improvement on year over year customer service scores.

Leverage Caesars Entertainment’s scale to optimize our cost structure. Caesars Entertainment’s global scale provides us with significant purchasing power and provides a larger fixed cost base with which to optimize our cost structure. Caesars Entertainment’s approximate $2.1 billion of annual enterprise-wide supplier spend provides us with unsurpassed scale and the associated negotiating power with our suppliers, allowing us to achieve optimal terms and providing us with significant cost savings. The use of Caesars Entertainment’s corporate services enables us to eliminate unnecessary expenses and improve efficiencies. Caesars Entertainment provides us with functional expertise in areas such as labor efficiency, food and beverage procurement and retailing to ensure that best practices are utilized throughout our business. We also benefit from shared work

groups in the areas of procurement, internal audit, planning and analysis, advertising and collections. Local competitors without Caesars Entertainment’s scale would require property-specific teams for these types of necessary functions. We also benefit from Caesars Entertainment’s national marketing initiatives for certain of our brand names. We believe that without the benefit of our affiliation with Caesars Entertainment’s brands, our marketing and branding costs would be substantially higher.

Our Relationships with Caesars Entertainment and CAC

We are a wholly owned subsidiary of Growth Partners, a joint venture between Caesars Entertainment and CAC. CAC serves as Growth Partners’ managing member and, as of December 31, 2013, owned all of Growth Partners’ outstanding voting units, while Caesars Entertainment owned all of Growth Partners’ outstanding non-voting units. Growth Partners benefits from a capital structure and governance that is separate from Caesars Entertainment. Growth Partners does not have a parent relationship with Caesars Entertainment, and Growth Partners and Caesars Entertainment have separate boards with different independent directors. In addition, neither our chief executive officer nor our chief financial officer are employed by Caesars Entertainment.

Caesars Entertainment

Caesars Entertainment is the world’s most diversified casino-entertainment provider and the most geographically diverse U.S. casino-entertainment company. Caesars Entertainment conducts business through its three distinct entities: CEOC, CERP and Growth Partners. As of December 31, 2013, Caesars Entertainment owned, operated, or managed, through various subsidiaries, 52 casinos in 13 U.S. states and five countries. Of the 52 casinos, 39 are in the United States and primarily consist of land-based and riverboat or dockside casinos. Caesars Entertainment’s 13 international casinos are land-based casino, most of which are located in England. As of December 31, 2013, Caesars Entertainment’s facilities had an aggregate of approximately three million square feet of gaming space and approximately 42,000 hotel rooms. As of December 31, 2013, Caesars Entertainment owned 100% of the outstanding non-voting units of Growth Partners, a joint venture between CAC and Caesars Entertainment and the parent of each Issuer, representing approximately 58% of the economic interests of Growth Partners.

Caesars Acquisition Company

CAC, a public company trading on NASDAQ under the symbol “CACQ,” was formed in 2013 to make an equity investment in Growth Partners. Growth Partners, a joint venture between CAC and Caesars Entertainment and the parent of each Issuer, is a casino asset and entertainment company focused on acquiring and developing a portfolio of high-growth operating assets and equity and debt investments in the gaming and interactive entertainment industries. CAC serves as Growth Partners’ managing member and, as of December 31, 2013, owned 100% of Growth Partners’ outstanding voting units, representing approximately 42% of the economic interests of Growth Partners.

Recent Developments

We expect to report that for the quarter ended March 31, 2014, revenues, net income and EBITDA will have increased compared to both the quarter ended December 31, 2013 and the quarter ended March 31, 2013. As of the date of this offering memorandum, our financial results for the quarter ended March 31, 2014 are not yet available. Our expectations on our revenues, net income and EBITDA for this period constitute forward-looking statements and are preliminary internal estimates, based on the information available to us as of the date of this offering memorandum. As we prepare our unaudited financial statements for the quarter ended March 31, 2014,

it is possible that additional work and procedures we perform to complete these quarterly financial statements could result in the actual results differing from our expectations. In addition, our financial results for the quarter ended March 31, 2014 will not necessarily be indicative of the financial results that may be expected for the year ended December 31, 2014. Accordingly, investors are cautioned not to place undue reliance on the foregoing guidance. See “Risk Factors” and “Forward Looking Statements.”

The Transactions

On March 1, 2014, CAC entered into a Transaction Agreement (the “Transaction Agreement”) with Caesars Entertainment, CEOC, Caesars License Company, LLC (f/k/a Harrah’s License Company, LLC) (“CLC”), Harrah’s New Orleans Management Company (“HNOMC”), Corner Investment, 3535 LV Corp., Parball Corporation, JCC Holding Company II, LLC and Growth Partners. The Transaction Agreement was fully negotiated by and between a Special Committee of Caesars Entertainment’s Board of Directors (the “CEC Special Committee”) and a Special Committee of CAC’s Board of Directors (the “CAC Special Committee”), each comprised solely of independent directors, and was recommended by both committees and approved by the Boards of Directors of Caesars Entertainment and CAC. The CEC Special Committee, the CAC Special Committee and the Boards of Directors of Caesars Entertainment and CAC each received fairness opinions from firms with experience in valuation matters, which stated that, based upon and subject to (and in reliance on) the assumptions made, matters considered and limits of such review, in each case as set forth in the opinions, the Purchase Price (as defined below) was fair from a financial point of view to Caesars Entertainment and Growth Partners, respectively.

Pursuant to the terms of the Transaction Agreement, Caesars Growth Properties, which was formed on February 21, 2014 as an indirect, wholly owned subsidiary of Growth Partners, will acquire from CEOC or one or more of its affiliates, (i) The Cromwell, The Quad, Bally’s Las Vegas and Harrah’s New Orleans, (ii) 50% of the ongoing management fees and any termination fees payable under the Property Management Agreements to be entered between a Property Manager (as defined below) and the owners of each of the Purchased Properties (the “Property Management Agreements”); and (iii) certain intellectual property that is specific to each of the Purchased Properties (together with the transactions described in (i) and (ii) above, the “Acquisition”) for an aggregate purchase price of approximately $2.0 billion (the “Purchase Price”), which includes $185 million of assumed debt related to The Cromwell, subject to various pre-closing and post-closing adjustments in accordance with the terms of the Transaction Agreement. Indemnification obligations of Caesars Entertainment and the sellers under the Transaction Agreement include amounts expended for new construction and renovation at The Quad in excess of the $223 million budgeted for renovation expenses (up to a maximum amount equal to 15% of such budgeted amount and subject to certain exceptions) and certain liabilities arising under employee benefit plans. In addition to the aforementioned indemnification obligations, the Transaction Agreement requires that CEOC ensure that the remaining amounts required to construct and open The Cromwell be fully-funded by CEOC, including providing a minimum amount of cash and cash equivalents located at The Cromwell in connection with the opening of The Cromwell. Caesars Entertainment and certain of its affiliates will indemnify CAC, Growth Partners and certain of their affiliates (including us) for a failure to open the hotel and casino at The Cromwell by a specified date and for failure to open the restaurant and nightclub at The Cromwell by a specified date. In addition, concurrently with the closing date of the Transactions (the “Closing”), Growth Partners will contribute to Caesars Growth Properties the entities that own the assets comprising Planet Hollywood, together with approximately $492 million in cash to fund a portion of the Acquisition consideration and to pay fees and expenses in connection with the Acquisition (the “Contribution”). The Acquisition and Contribution are subject to certain closing conditions, including the receipt of gaming and other required governmental approvals, accuracy of representations and warranties, compliance with covenants and receipt by Caesars Entertainment and the CEC Special Committee of certain opinions with respect to CEOC.

The Transaction Agreement provides that, at the Closing, the owner of each Property, except Planet Hollywood, will enter into a Property Management Agreement with the applicable Property Manager, pursuant to

which, among other things, the Property Managers will provide management services to the applicable Property and CLC will license enterprise-wide intellectual property used in the operation of the Purchased Properties. See “Certain Relationships and Related Party Transactions— Property Management Agreements.” Pursuant to the terms of the Transaction Agreement, the parties have also agreed to use reasonable best efforts to establish Services, LLC. Upon its implementation, Services, LLC will manage the intellectual property for the Caesars Entertainment enterprise (including for the Total Rewards system), which Services, LLC will license to, among other parties, each of the owners of the Purchased Properties pursuant to the Cross-License Agreement (as defined herein). Services, LLC will also manage certain shared services operations across the portfolio of CEOC, CERP, Growth Partners and our properties and perform the obligations of the Property Managers (as defined herein) at each Property. We have begun to seek the approvals necessary for the implementation of Services, LLC and intend to file for all such regulatory approvals as soon as possible. See “Certain Relationships and Related Party Transactions—Services Joint Venture.”

In connection with the Acquisition and the Contribution, we intend to repay the approximately $463.0 million outstanding under the senior secured term loan of PHWLV, LLC (the “PHW Credit Facility”), one of the subsidiaries contributed to us in the Contribution and the holder of the Planet Hollywood assets, and such facility will be cancelled (the “Refinancing”).

We will use the proceeds from the borrowing under the Term Loan Facility and the issuance of the Notes, together with the cash contributed to us in the Contribution, to fund a portion of the Acquisition, to complete the Refinancing and to pay fees and expenses in connection with the Transactions (as defined below). See “Use of Proceeds.” We do not expect to draw any borrowings under the Revolving Credit Facility in connection with the Acquisition.

If the Escrow Conditions are not satisfied prior to the consummation of this offering, we will deposit the gross proceeds of this offering into a segregated escrow account (pledged for the benefit of the noteholders), together with additional amounts necessary to redeem the Notes at a price equal to 100% of the gross proceeds of this offering, plus accrued and unpaid interest to (but not including) the last possible date of redemption. Concurrently with the closing of the Transactions, we will enter into our new $1,325.0 million Senior Secured Credit Facilities, which include a five-year $150.0 million senior secured revolving credit facility (the “Revolving Credit Facility”) and a seven-year $1,175.0 million senior secured term loan credit facility (the “Term Loan Facility”). Upon delivery to the escrow agent of an officer’s certificate instructing the escrow agent to release the escrowed funds and certifying, among other things, that prior to or concurrently with the release of funds from escrow to us (i) the Acquisition shall have been consummated in accordance with the terms described under “—The Transactions,” (ii) borrowings (or release of escrow) under our new Term Loan Facility will have been made, (iii) the Contribution will have been consummated in accordance with the terms described under “—The Transactions” and (iv) all approvals required for the consummation of the Transactions (other than in respect of Services, LLC) will have been obtained (collectively, the “Escrow Conditions”), the escrowed funds will be released to us.

If the Escrow Conditions are not satisfied on or prior to August 31, 2014, or such earlier date as we determine in our sole discretion that the Escrow Conditions cannot be satisfied, we will be required to redeem the Notes no later than five business days thereafter at a price equal to 100% of the gross proceeds of the Notes, together with interest accrued and unpaid on the Notes from the issue date to, but not including, the date of redemption. Escrowed funds would be released and applied to pay for any such redemption.

Throughout this offering memorandum, we collectively refer to the Acquisition, the Contribution, the entry into the Senior Secured Credit Facilities, the consummation of this offering and the Refinancing as the “Transactions.” This offering (or the escrow release, as applicable) is conditioned on the substantially concurrent closing of the other Transactions.

Letter From CEOC Second Lien Noteholders

On March 21, 2014, CAC, Growth Partners, Caesars Entertainment, CEOC and CERP received a letter (the “Second Lien Holders’ Letter”) from a law firm acting on behalf of unnamed clients who claim to hold Second-Priority Secured Notes of CEOC, alleging, among other things, that CEOC is insolvent and that CEOC’s owners improperly transferred or seek to transfer valuable assets of CEOC to affiliated entities in connection with: (a) the transaction agreement dated October 21, 2013 by and among Caesars Entertainment, certain subsidiaries of Caesars Entertainment and CEOC, CAC and Growth Partners, which, among other things, provide for the asset transfers from subsidiaries of CEOC to Growth Partners of the Planet Hollywood casino and interests in Horseshoe Baltimore that was consummated in 2013 (the “2013 CGP Transaction”); (b) the transfer by CEOC to CERP of Octavius Tower and the Linq that was consummated in 2013; and (c) the contemplated transfers by CEOC to Growth Partners of the Properties (the “Contemplated Transaction”). The Second Lien Holders’ Letter does not identify the holders or specify the amount of Second-Priority Secured Notes or other securities that they may hold. The Second Lien Holders’ Letter includes allegations that these transactions constitute or will constitute voidable fraudulent transfers and represent breaches of alleged fiduciary duties owed to CEOC creditors and that certain disclosures concerning the transactions were inadequate. The Second Lien Holders’ Letter demands, among other things, that the transactions be rescinded or terminated, as would be applicable.

Growth Partners strongly believes there is no merit to the Second Lien Holders’ Letter’s allegations and will defend itself vigorously and seek appropriate relief should any action be brought. If a court were to order rescission of the 2013 CGP Transaction or enjoin consummation of the Contemplated Transaction, Growth Partners and the Company may have to return the Properties and/or the assets transferred to Growth Partners in the 2013 CGP Transaction or their value to Caesars Entertainment or CEOC, be forced to pay additional amounts therefor, or to take other actions ordered by the court. In addition, if the Contemplated Transaction were consummated and a court were to find that those transfers were improper, that could trigger a default under the Company’s Senior Secured Credit Facilities and the Notes and a court could fashion a number of remedies, including declaring that the liens on the returned assets securing the Company’s Senior Secured Credit Facilities and the Notes are not valid or enforceable, or that they may be equitably subordinated or otherwise impaired. These consequences could have a material adverse effect on Growth Partners’ and the Company’s business, financial condition, results of operations and prospects and on the ability of lenders and noteholders to recover on claims under the Senior Secured Credit Facilities and the Notes. See “Risk Factors—Risks Related to Our Business—We are or may become involved in legal proceedings that, if adversely adjudicated or settled, could impact our financial condition.”

Letter From Holders of CEOC First Lien Debt

On April 3, 2014, a letter was sent to the boards of directors of Caesars Entertainment and CEOC (the “First Lien Holders’ Letter”) by a law firm claiming to act on behalf of unnamed parties who assert that they are lenders under CEOC’s credit agreement and/or holders of CEOC’s first-priority senior secured notes (collectively, the “First Lien Group”), alleging, among other things, that Caesars Entertainment and CEOC improperly transferred or seek to transfer assets of Caesars Entertainment and CEOC to affiliated entities in connection with: (a) the transaction agreement dated October 21, 2013 by and among Caesars Entertainment, certain subsidiaries of Caesars Entertainment and CEOC, CAC and Growth Partners, which, among other things, provides for the contributions by Caesars Entertainment and its subsidiaries to Growth Partners of Caesars Interactive and $1.1 billion face amount of CEOC’s unsecured notes in exchange for non-voting interests of Growth Partners, and the asset transfers from subsidiaries of CEOC to Growth Partners of the Planet Hollywood casino and interests in Horseshoe Baltimore that was consummated in 2013; (b) the transfer by CEOC to CERP of Octavius Tower and Project Linq that was consummated in 2013; and (c) the contemplated transfers by CEOC to Growth Partners of The Cromwell, The Quad, Bally’s Las Vegas and Harrah’s New Orleans and formation of Services, LLC among CEOC, CERP and the Company to provide certain centralized services, including but not

limited to common management of enterprise-wide intellectual property (the “Contested Transactions”). The First Lien Holders’ Letter asserts that the consideration received by Caesars Entertainment and CEOC in the Contested Transactions is inadequate, that Caesars Entertainment and CEOC were insolvent when the transactions were approved, that the Contested Transactions represented breaches of alleged fiduciary duties, that certain disclosures concerning the Contested Transactions were inadequate and concerns about governance of CEOC. The First Lien Holders’ Letter claims that the First Lien Group consists of holders of a total of more than $1.85 billion of CEOC’s first lien debt and that holders of an additional $880 million of CEOC’s first lien debt endorse and support the First Lien Holders’ Letter but are not part of the group. The First Lien Holders’ Letter demands, among other things, rescission or termination of the Contested Transactions and requests a meeting with representatives of Caesars Entertainment and other parties to discuss these matters.

Caesars Entertainment and CEOC strongly believe there is no merit to the First Lien Holders’ Letter’s allegations and will defend themselves vigorously and seek appropriate relief should any action be brought. If a court were to order rescission or termination of the Contested Transactions, Growth Partners and its subsidiaries may have to return the assets transferred to Growth Partners in the Contested Transactions or their value to Caesars Entertainment or CEOC, be forced to pay additional amounts therefor, or to take other actions ordered by the court. In addition, if the contemplated transfers were consummated and a court were to find that those transfers were improper, that could trigger a default under the debt that Growth Partners is raising to finance such transfers and a court could fashion a number of remedies, including declaring that the liens on the returned assets securing such financing are not valid or enforceable, or that they may be equitably subordinated or otherwise impaired. Furthermore, a court could enjoin the consummation or order rescission of the Services, LLC transaction. These consequences could have a material adverse effect on Growth Partners’ business, financial condition, results of operations and prospects. See “Risk Factors—Risks Related to Our Business—We are or may become involved in legal proceedings that, if adversely adjudicated or settled, could impact our financial condition.”

Estimated Impact of Project Completions

We expect that the renovation at The Quad, the end of construction disruption at the Linq and The Quad and the completion of The Cromwell will have a significant positive impact on our results of operations. The following discusses the estimated impact of the completion of these projects. These estimates assume the projects are open or fully implemented and operated at a steady state, which may not occur until 12 to 24 months after the date of this offering memorandum.

This “Estimated Impact of Project Completions” section and other parts of this offering memorandum contain forward-looking statements, including, without limitation, statements relating to our future actions, new projects, strategies, future performance and future financial results, and are necessarily estimates reflecting the best judgment of our management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by such forward-looking statements. Investors should also recognize that the reliability of any forecasted financial data diminishes the farther in the future that the data is forecast. In light of the foregoing, investors are urged to put the information in context and not to place undue reliance on it. See “Forward Looking Statements” and “Risk Factors,” including “Risk Factors—Risks Related to Our Business—We may not realize any or all of our projected increases to Adjusted EBITDA or other projections included in this offering memorandum.” You are cautioned to not place undue reliance on these forward-looking statements, which represent our estimates and speak only as of the date of this offering memorandum. Prospective financial information is necessarily speculative in nature and it can be expected that some or all of the assumptions of the information described above may not materialize or will vary significantly from actual results. We undertake no obligation to update publicly any forward-looking statement for any reason after the date of this document to conform these statements to actual results or to change to our expectations.

Estimated Additional Revenues from The Quad

We plan to invest an additional $223 million towards the renovation of The Quad, which is scheduled to be completed during the first half of 2015. We estimate that additional gaming and lodging revenues at The Quad subsequent to the completion of the renovation will result in approximately $31 million to $47 million of incremental Adjusted EBITDAM annually. Based on the average performance of Caesars Entertainment Corporation’s properties in Las Vegas, we estimate that The Quad’s cash ADR will increase between $70 and $110, and wins per day (“WPD”) will increase to between $240 and $320. As of December 31, 2013, the Quad had the lowest WPD of Caesars Entertainment Corporation’s eight Las Vegas gaming properties. We estimate the renovation of The Quad would improve the property to the fourth highest WPD among Caesars Entertainment Corporation’s eight Las Vegas gaming properties.

End of Construction Disruption

Based upon our review of the trends and results of operations at properties in Las Vegas owned by Caesars Entertainment comparable to The Quad, we believe that construction related to the Linq and the $90 million renovation at The Quad (which together affected the gaming floor at The Quad as well as areas directly adjacent to The Quad) has negatively impacted performance at The Quad since construction began in 2011. From 2011 to 2013, The Quad experienced a 27% decline in net revenue. During the same timeframe, comparable Las Vegas Caesars’ properties experienced a 5.5% decrease in net revenue. We estimate the negative revenue impact of the Linq construction and The Quad renovation disruption was $26 million to $33 million in fiscal year 2013. Assuming 55% to 75% of net revenue flow through to Adjusted EBITDAM, we estimate the Adjusted EBITDAM impact of this disruption for the year ended December 31, 2013 was between $14 million and $25 million.

Estimated Additional Revenues from The Cromwell

We estimate that The Cromwell, which is owned by Corner Investment, a qualified non-recourse subsidiary of the Company, will generate an annual rate of Adjusted EBITDAM of $40 to $50 million. Any revenue (or EBITDA) derived for The Cromwell or Corner Investment will not count towards any financial calculation under the indenture governing the Notes or the Senior Secured Credit Facilities, and noteholders will not have any direct benefit from such revenue. Estimates for the property are based on Caesars Entertainment’s experience in developing and operating casino resorts in Las Vegas, management research on other Las Vegas casino resorts that feature popular nightclubs/poolclubs similar to the club we are developing at The Cromwell and research and information obtained from the developer of the nightclub/poolclub at The Cromwell, Victor Drai, which we expect will drive visitation and spend in gaming, lodging, food and beverage and entertainment at the complex. See “Risk Factors—Risks Related to Our Business—We may not realize any or all of our projected increases to Adjusted EBITDA or other projections included in this offering memorandum.”

These projections reflect the annual run-rate Adjusted EBITDAM estimated from the property once open or fully implemented and operated at a steady state, which may not occur until 12 to 24 months after the property commences operations. These projections are based on the current estimates of the Company, and they involve risks, uncertainties, assumptions and other factors that may cause actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by projections. As to The Cromwell, our estimates are largely based on the anticipated performance of the nightclub/poolclub at the property. We have never built a boutique hotel with a nightclub/poolclub like The Cromwell, and our estimated annual rate of Adjusted EBITDAM from the property may materially differ from the actual results at the property if the performance or results of the nightclub/poolclub or the complex in general do not meet our expectations. We undertake no obligation to update publicly any forward-looking statement for any reason after the date of this document to conform these statements to actual results or to changes to our expectations.

As a qualified non-recourse subsidiary, The Cromwell (i) will not guarantee the Senior Secured Credit Facilities or the Notes and will not provide any portion of the collateral securing the Senior Secured Credit Facilities or the Notes, (ii) has no obligation to pay any amounts due pursuant to the Senior Secured Credit Facilities or the Notes and (iii) will be subject on a limited basis to the restrictive covenants in the credit agreement governing the Senior Secured Credit Facilities and the indenture governing the Notes. In addition, as of December 31, 2013, The Cromwell had approximately $185.0 million face value of outstanding secured indebtedness under the Cromwell Credit Facility (as defined below), dated as of November 2, 2012, among The Cromwell and certain other parties thereto, all of which ranks senior to the Senior Secured Credit Facilities and the Notes. See “Risk Factors—Risks Related to the Notes and this Offering—The Notes will be structurally subordinated to all liabilities of the Issuers’ subsidiaries that are not Subsidiary Guarantors.”

Sources and Uses of Funds

The following table sets forth the estimated sources and uses of funds in connection with the Transactions, assuming they occurred on December 31, 2013.

| Sources of funds |

Uses of funds |

|||||||||

| (in millions) |

||||||||||

| Senior Secured Credit Facilities(1) | $ | 1,175 | Purchase price for the Purchased Properties | $ | 1,815 | |||||

| Notes offered hereby | 675 | Repayment of PHW Credit Facility(4) | 495 | |||||||

| Rollover of existing debt(2) | 185 | Pre-funded capital expenditures at The Quad(5) | 100 | |||||||